Embed Size (px)

Citation preview

Presentation of Q1 2017 Results Bucharest, 15 May 2017

Highlights

Highlights

Executive Summary

Distribution Overview

Supply Overview

Corporate Governance

2

Main corporate events in Q1 2017 and up to date

3

Main resolutions of the April 27th, 2017 General Meetings of Shareholders:

Approval of the 2017 budgets of Electrica, at standalone and consolidated levels;

Approval of the 2016 financials statements of Electrica at standalone and consolidated levels;

Approval of the 2016 profit distribution; gross dividend – RON 0.7415 per share; payment date – 22 June 2017;

Approval of the proposal for amendment of the Articles of Association of Societatea Energetica Electrica SA by

eliminating two provisions so that the decisions for subsidiaries’ mergers, spin offs and global strategy,

including but not limited to development and restructuring to be transferred to BoD;

Rejection of the empowerment of Electrica BoD to approve changes in the structure of the income and expenses

budget of Electrica for financial year 2017, at standalone and consolidated levels up to a total variation of 10% in

the line of total income and total expenses.

Main corporate governance events in Q1 2017 up to date:

The Board of Directors decided to:

Reappoint Mr. Cristian Busu as BoD chair for a mandate of one year and the BoD’s committees to remain

unchanged and re-elected their chairs for a one-year mandate, starting January 27th;

Revoke Mr. Ramiro Angelescu from the position of Executive Manager of the Sales Coordination Division of

Electrica SA, as of January 27th;

Appoint Ms. Livioara Sujdea, as Chief Distribution Officer, starting with February 1st;

Appoint Mr. Dan Crisfalusi as IT & Telecom Officer, starting with March 6th, for a four-year period;

Approve the Remuneration policy of Electrica’s directors and executive managers drafted based on OGMS

resolutions no.2/09.07.2015 and 01/31.03.2016

Appoint Ms. Anamaria Acristini as Chief Strategy Officer, starting with May 1st, for a four-year period.

Mrs. Corina Georgeta Popescu resigned, on the 31st of March 2017, from her position as member of the Board of

Directors of Electrica SA; following this decision, the BoD appointed Mr. Gicu Iorga as interim member of the

Board of Directors, starting with May 1st 2017, and until April 30th 2018, or until the next Ordinary General Meeting

of Shareholders of the Company, which of the dates comes first.

Relevant

developments in

Corporate

Governance

in Q1 2017 and up

to date

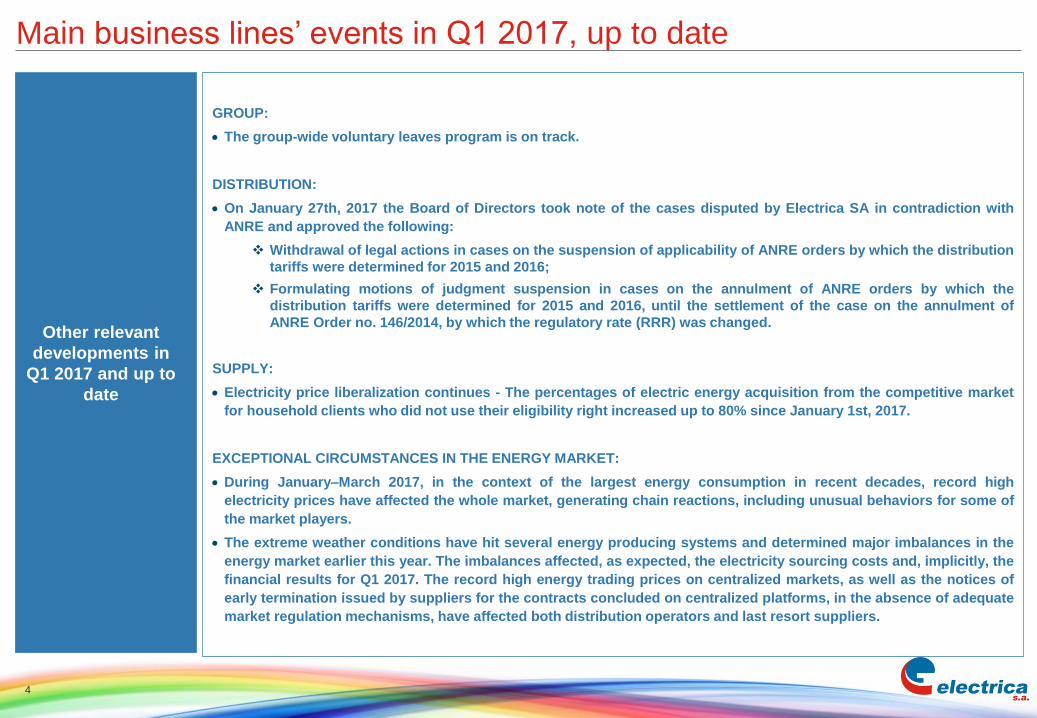

Main business lines’ events in Q1 2017, up to date

GROUP:

The group-wide voluntary leaves program is on track.

DISTRIBUTION:

On January 27th, 2017 the Board of Directors took note of the cases disputed by Electrica SA in contradiction with

ANRE and approved the following:

Withdrawal of legal actions in cases on the suspension of applicability of ANRE orders by which the distribution

tariffs were determined for 2015 and 2016;

Formulating motions of judgment suspension in cases on the annulment of ANRE orders by which the

distribution tariffs were determined for 2015 and 2016, until the settlement of the case on the annulment of

ANRE Order no. 146/2014, by which the regulatory rate (RRR) was changed.

SUPPLY:

Electricity price liberalization continues - The percentages of electric energy acquisition from the competitive market

for household clients who did not use their eligibility right increased up to 80% since January 1st, 2017.

EXCEPTIONAL CIRCUMSTANCES IN THE ENERGY MARKET:

During January–March 2017, in the context of the largest energy consumption in recent decades, record high

electricity prices have affected the whole market, generating chain reactions, including unusual behaviors for some of

the market players.

The extreme weather conditions have hit several energy producing systems and determined major imbalances in the

energy market earlier this year. The imbalances affected, as expected, the electricity sourcing costs and, implicitly, the

financial results for Q1 2017. The record high energy trading prices on centralized markets, as well as the notices of

early termination issued by suppliers for the contracts concluded on centralized platforms, in the absence of adequate

market regulation mechanisms, have affected both distribution operators and last resort suppliers.

Other relevant

developments in

Q1 2017 and up to

date

4

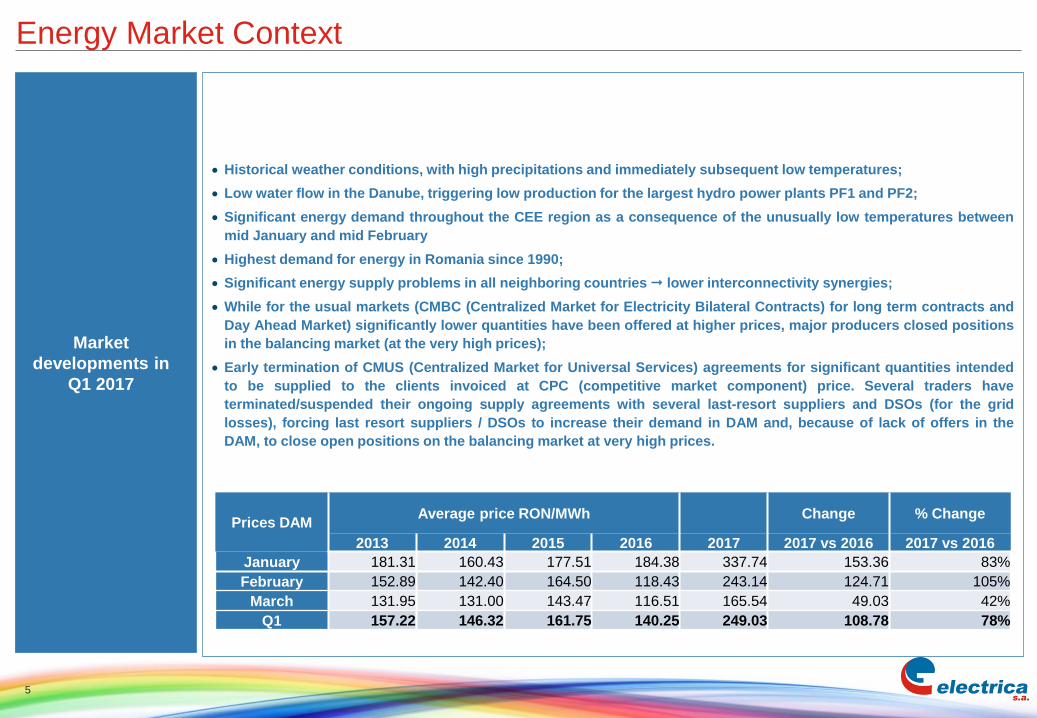

Energy Market Context

Historical weather conditions, with high precipitations and immediately subsequent low temperatures;

Low water flow in the Danube, triggering low production for the largest hydro power plants PF1 and PF2;

Significant energy demand throughout the CEE region as a consequence of the unusually low temperatures between

mid January and mid February

Highest demand for energy in Romania since 1990;

Significant energy supply problems in all neighboring countries lower interconnectivity synergies;

While for the usual markets (CMBC (Centralized Market for Electricity Bilateral Contracts) for long term contracts and

Day Ahead Market) significantly lower quantities have been offered at higher prices, major producers closed positions

in the balancing market (at the very high prices);

Early termination of CMUS (Centralized Market for Universal Services) agreements for significant quantities intended

to be supplied to the clients invoiced at CPC (competitive market component) price. Several traders have

terminated/suspended their ongoing supply agreements with several last-resort suppliers and DSOs (for the grid

losses), forcing last resort suppliers / DSOs to increase their demand in DAM and, because of lack of offers in the

DAM, to close open positions on the balancing market at very high prices.

Market

developments in

Q1 2017

5

Prices DAMAverage price RON/MWh Change % Change

2013 2014 2015 2016 2017 2017 vs 2016 2017 vs 2016

January 181.31 160.43 177.51 184.38 337.74 153.36 83%

February 152.89 142.40 164.50 118.43 243.14 124.71 105%

March 131.95 131.00 143.47 116.51 165.54 49.03 42%

Q1 157.22 146.32 161.75 140.25 249.03 108.78 78%

Energy Market Context

Aiming to keep the financial performance of 2017 as much as possible on track and meet investors' expectations, the

management continues to implement the optimization program in all Electrica Group entities, while aligning the

measures to the current market conditions. This includes measures aimed mainly at EFSA's portfolio optimization (both

for eligible and captive customers), as well as cost reduction measures for EFSA and DSOs (with effect already in 2017).

While the management is committed to take all the measures, considering the Q1 market challenges and taking into

account the current average energy prices in the centralized markets (higher that last year's), as well as the weather

forecast indicating a dry hot summer, a certain risk remains for the rest of the year in relation to the cost of the

electricity on the wholesale market.

In such case, should the optimization measures already started prove insufficient to ensure achievement of 2017 result,

other measures (including distribution of reserves) might be considered, in order to preserve the dividend distribution

level.

Measures to

overcome the Q1

2017 results

6

Executive Summary

Highlights

Executive Summary

Distribution Overview

Supply Overview

Corporate Governance

7

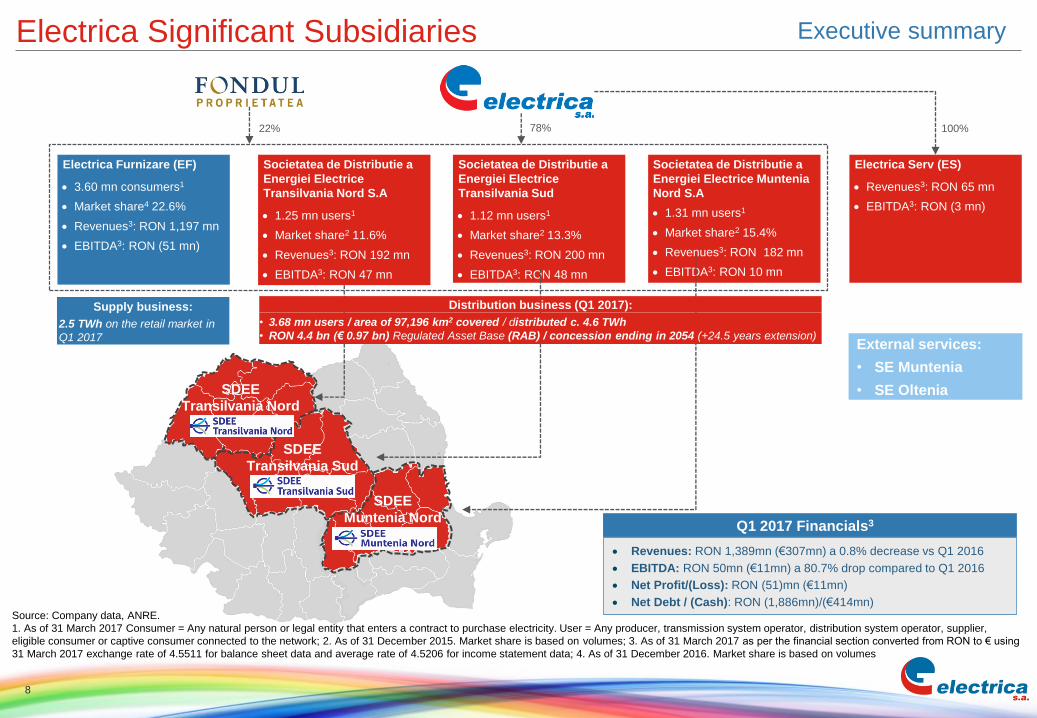

Electrica Significant Subsidiaries Executive summary

8

Source: Company data, ANRE.

1. As of 31 March 2017 Consumer = Any natural person or legal entity that enters a contract to purchase electricity. User = Any producer, transmission system operator, distribution system operator, supplier,

eligible consumer or captive consumer connected to the network; 2. As of 31 December 2015. Market share is based on volumes; 3. As of 31 March 2017 as per the financial section converted from RON to € using

31 March 2017 exchange rate of 4.5511 for balance sheet data and average rate of 4.5206 for income statement data; 4. As of 31 December 2016. Market share is based on volumes

Societatea de Distributie a

Energiei Electrice

Transilvania Nord S.A

1.25 mn users1

Market share2 11.6%

Revenues3: RON 192 mn

EBITDA3: RON 47 mn

Societatea de Distributie a

Energiei Electrice

Transilvania Sud

1.12 mn users1

Market share2 13.3%

Revenues3: RON 200 mn

EBITDA3: RON 48 mn

Electrica Furnizare (EF)

3.60 mn consumers1

Market share4 22.6%

Revenues3: RON 1,197 mn

EBITDA3: RON (51 mn)

Electrica Serv (ES)

Revenues3: RON 65 mn

EBITDA3: RON (3 mn)

78% 100%22%

External services:

• SE Muntenia

• SE Oltenia

Supply business:

2.5 TWh on the retail market in

Q1 2017

Societatea de Distributie a

Energiei Electrice Muntenia

Nord S.A

1.31 mn users1

Market share2 15.4%

Revenues3: RON 182 mn

EBITDA3: RON 10 mn

Q1 2017 Financials3

Revenues: RON 1,389mn (€307mn) a 0.8% decrease vs Q1 2016

EBITDA: RON 50mn (€11mn) a 80.7% drop compared to Q1 2016

Net Profit/(Loss): RON (51)mn (€11mn)

Net Debt / (Cash): RON (1,886mn)/(€414mn)

Distribution business (Q1 2017):

• 3.68 mn users / area of 97,196 km2 covered / distributed c. 4.6 TWh

• RON 4.4 bn (€ 0.97 bn) Regulated Asset Base (RAB) / concession ending in 2054 (+24.5 years extension)

SDEE

Transilvania Nord

SDEE

Transilvania Sud

SDEE

Muntenia Nord

15%

13%

12%

60%

SDMN

SDTS

SDTN

Others

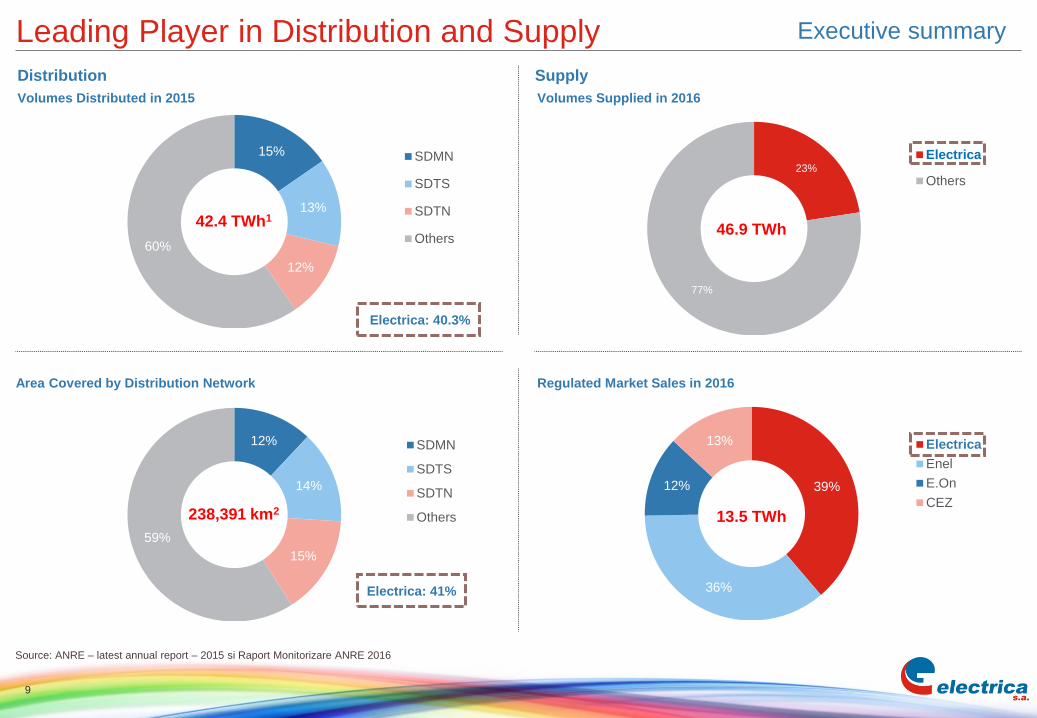

Volumes Distributed in 2015 Volumes Supplied in 2016

Regulated Market Sales in 2016Area Covered by Distribution Network

Distribution Supply

Leading Player in Distribution and Supply

Electrica: 40.3%

42.4 TWh1

Source: ANRE – latest annual report – 2015 si Raport Monitorizare ANRE 2016

23%

77%

Electrica

Others

46.9 TWh

12%

14%

15%

59%

SDMN

SDTS

SDTN

Others238,391 km2

39%

36%

12%

13% Electrica

Enel

E.On

CEZ13.5 TWh

Electrica: 41%

Executive summary

9

Background and Basis of Preparation for the Financials

10

Background

Group structure and

segment reporting

Historical consolidated financial statements prepared in accordance with International Financial

Reporting Standards as endorsed by the European Union (IFRS-EU)

The presentation currency is Romanian New Leu (RON)

Since January 2016, the Electrica Group includes 8 companies, following the deconsolidation of SE

Moldova after its bankruptcy.

The Group is divided into two main segments for the purpose of segmental reporting: distribution (further

split into three DSO’s and the energy services company) and supply

Until April 10th, 2014 Electrica held minority holdings in various entities which were subject to a spin-off in

2014 before the IPO; Electrica produced pro-forma financial statements for the period 2011-2013 which

carved-out the impact of spun-off items

The management reassessed the accounting treatment used for its distribution subsidiaries concession

agreements following the IPO and as a result adopted IFRIC 12 at the end of 2014. The Group has

applied the change in accounting policy retrospectively and restated the comparative periods

Source: Company data.

Executive summary

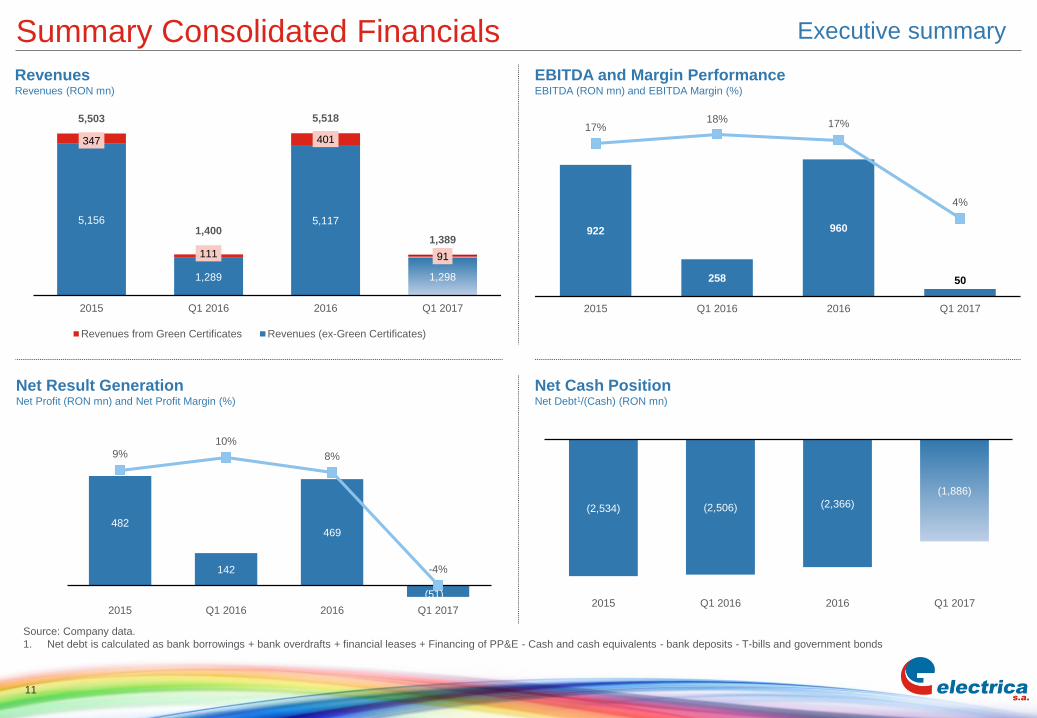

922

258

960

50

17%18% 17%

4%

2015 Q1 2016 2016 Q1 2017

Summary Consolidated Financials

Net Cash PositionNet Debt1/(Cash) (RON mn)

Net Result GenerationNet Profit (RON mn) and Net Profit Margin (%)

RevenuesRevenues (RON mn)

EBITDA and Margin PerformanceEBITDA (RON mn) and EBITDA Margin (%)

Source: Company data.

1. Net debt is calculated as bank borrowings + bank overdrafts + financial leases + Financing of PP&E - Cash and cash equivalents - bank deposits - T-bills and government bonds

5,156

1,289

5,117

1,298

347

111

401

91

5,503

1,400

5,518

1,389

2015 Q1 2016 2016 Q1 2017

Revenues from Green Certificates Revenues (ex-Green Certificates)

Executive summary

11

482

142

469

(51)

9%

10%

8%

-4%

2015 Q1 2016 2016 Q1 2017

(2,534) (2,506) (2,366)

(1,886)

2015 Q1 2016 2016 Q1 2017

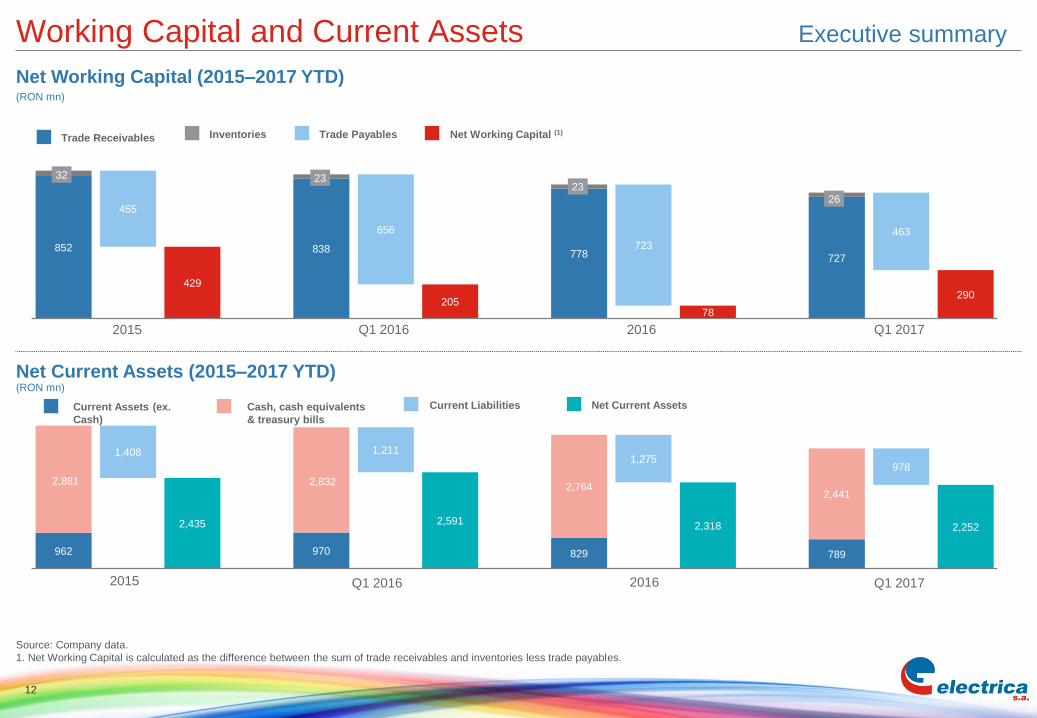

962

2,435

970

2,591

829

2,318

789

2,252

2,881

1,408

2,832

1,211

2,764

1,275

2,441

978

2016

Working Capital and Current Assets

Source: Company data.

1. Net Working Capital is calculated as the difference between the sum of trade receivables and inventories less trade payables.

Trade Receivables Trade PayablesInventories Net Working Capital (1)

2015 Q1 2016 2016

Net Working Capital (2015–2017 YTD)

Net Current Assets (2015–2017 YTD)

Current Assets (ex.

Cash)

Cash, cash equivalents

& treasury bills

Current Liabilities Net Current Assets

2015 Q1 2016 Q1 2017

(RON mn)

(RON mn)

Executive summary

12

852

429

838

205

778

78

727

290

32

455

23

656

23

723

26

463

Q1 2017

Distribution Overview

Highlights

Executive Summary

Distribution Overview

Supply Overview

Corporate Governance

13

Number of Users(‘000’s)

39% 40% 40%

Distribution Market Overview

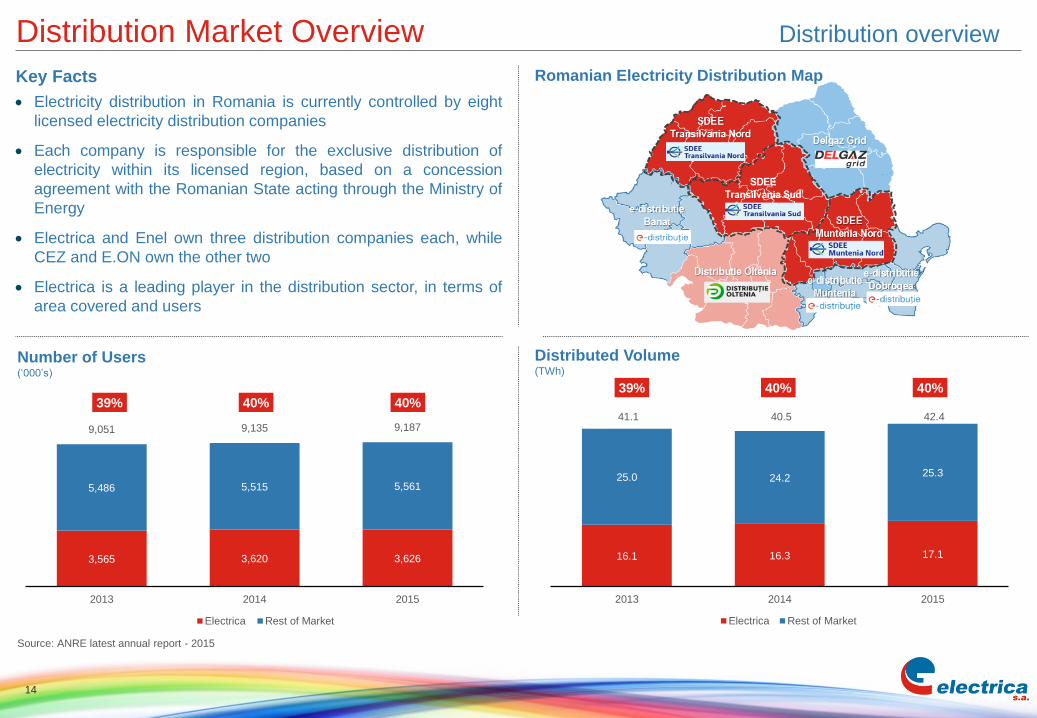

Key Facts

Electricity distribution in Romania is currently controlled by eight

licensed electricity distribution companies

Each company is responsible for the exclusive distribution of

electricity within its licensed region, based on a concession

agreement with the Romanian State acting through the Ministry of

Energy

Electrica and Enel own three distribution companies each, while

CEZ and E.ON own the other two

Electrica is a leading player in the distribution sector, in terms of

area covered and users

Romanian Electricity Distribution Map

Distributed Volume(TWh)

Source: ANRE latest annual report - 2015

3,565 3,620 3,626

5,486 5,515 5,561

9,051 9,135 9,187

2013 2014 2015

Electrica Rest of Market

16.1 16.3 17.1

25.0 24.225.3

41.1 40.5 42.4

2013 2014 2015

Electrica Rest of Market

Distribution overview

14

39% 40% 40%

Q1 2017 Regulated Asset Base (RAB) of RON 4.436 bn

195,923 km of voltage lines (7,574 km HV; 45,080 km MV; 143,270 km LV) (Q1 2017)

Area of operation: 97,196 km2, 40.7% of Romania’s territory

3.68 mn users (Q1 2017)

4.6 TWh of electricity distributed in Q1 2017, 4% increase compared to Q1 2016

40.3% market share for electricity distribution to end users in 2015

Financials variances

o 34% lower EBITDA mainly due to significantly network losses higher sourcing cost (price

effect due to the historical highest energy acquisition prices)

o Significant decrease in net profit mainly due to EBITDA impact and higher depreciation

costs

Key Financial Metrics

EBITDA(RON mn)

Net Profit(RON mn)

Net Debt/(Net Cash)1

(RON mn)

Revenues(RON mn)

Source: Company data.

1. Net debt is calculated as bank borrowings + bank overdrafts + Financing for PP&E and financial leases - Cash and cash equivalents - bank deposits - T-bills and government bonds

Distribution Highlights

809

154

760

101

2015 Q1 2016 2016 Q1 2017

377

51

312

(3)

2015 Q1 2016 2016 Q1 2017

(8)(5)

175

335

2015 Q1 2016 2016 Q1 2017

Distribution segment overview

15

2,613

546

2,498

583

2015 Q1 2016 2016 Q1 2017

5045

83

108

2015 Q1 2016 2016 Q1 2017

132

32

108

9

2015 Q1 2016 2016 Q1 2017

276

70

256

48

2015 Q1 2016 2016 Q1 2017

840

186

790

200

2015 Q1 2016 2016 Q1 2017

SDTS Overview

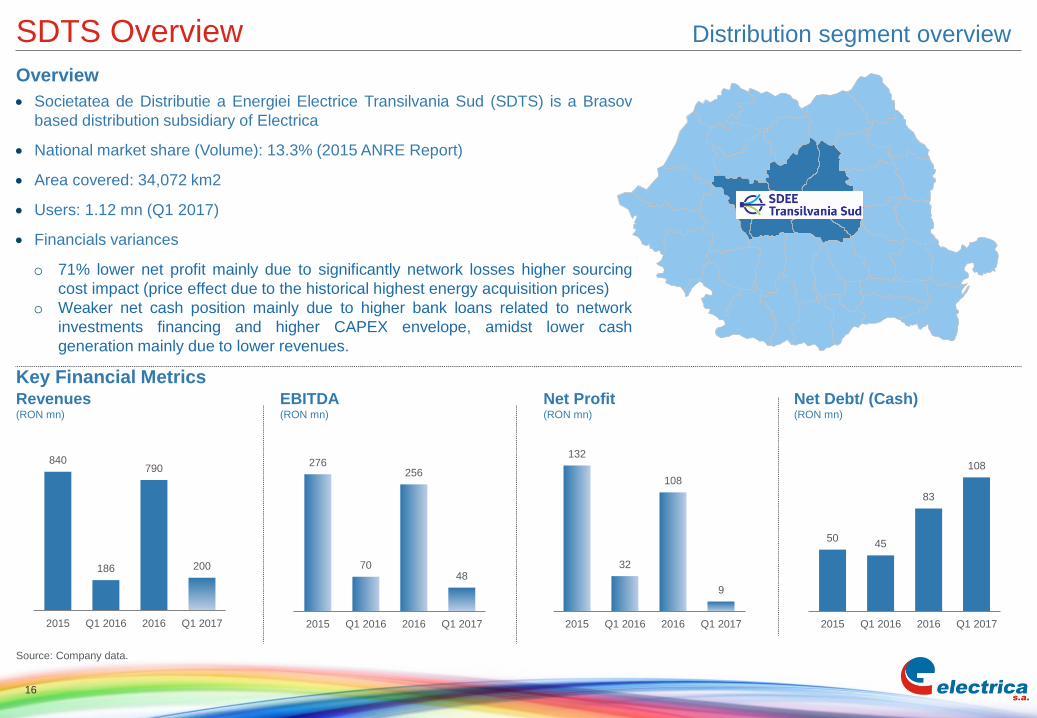

Overview

Societatea de Distributie a Energiei Electrice Transilvania Sud (SDTS) is a Brasov

based distribution subsidiary of Electrica

National market share (Volume): 13.3% (2015 ANRE Report)

Area covered: 34,072 km2

Users: 1.12 mn (Q1 2017)

Financials variances

o 71% lower net profit mainly due to significantly network losses higher sourcing

cost impact (price effect due to the historical highest energy acquisition prices)

o Weaker net cash position mainly due to higher bank loans related to network

investments financing and higher CAPEX envelope, amidst lower cash

generation mainly due to lower revenues.

Source: Company data.

Key Financial MetricsEBITDA(RON mn)

Net Profit(RON mn)

Net Debt/ (Cash)(RON mn)

Revenues(RON mn)

Distribution segment overview

16

SDTS Overview (Cont’d)

Network Losses(GWh)

Costs due to Network Losses(RON mn)

Network Losses(%)

Source: Company data.

163

50

163

69

2015 Q1 2016 2016 Q1 2017

785

230

775

252

2015 Q1 2016 2016 Q1 2017

11.40% 11.15% 10.97%

13.45%

10.97% 10.74% 10.55%

12.65%

Reg. Realised Reg. Realised Reg. Realised Reg. Realised

2015 Q1 2016 2016 Q1 2017

Distribution segment overview

17

Capex(RON mn)

2.44

0.68

2.51

0.71

2.31

0.59

2.35

0.62

0.88

0.22

0.96

0.23

5.63

1.49

5.82

1.56

2015 Q1 2016 2016 Q1 2017

Low Voltage Medium Voltage High Voltage

Distributed Volumes (TWh)

157

15

148

32

2015 Q1 2016 2016 Q1 2017

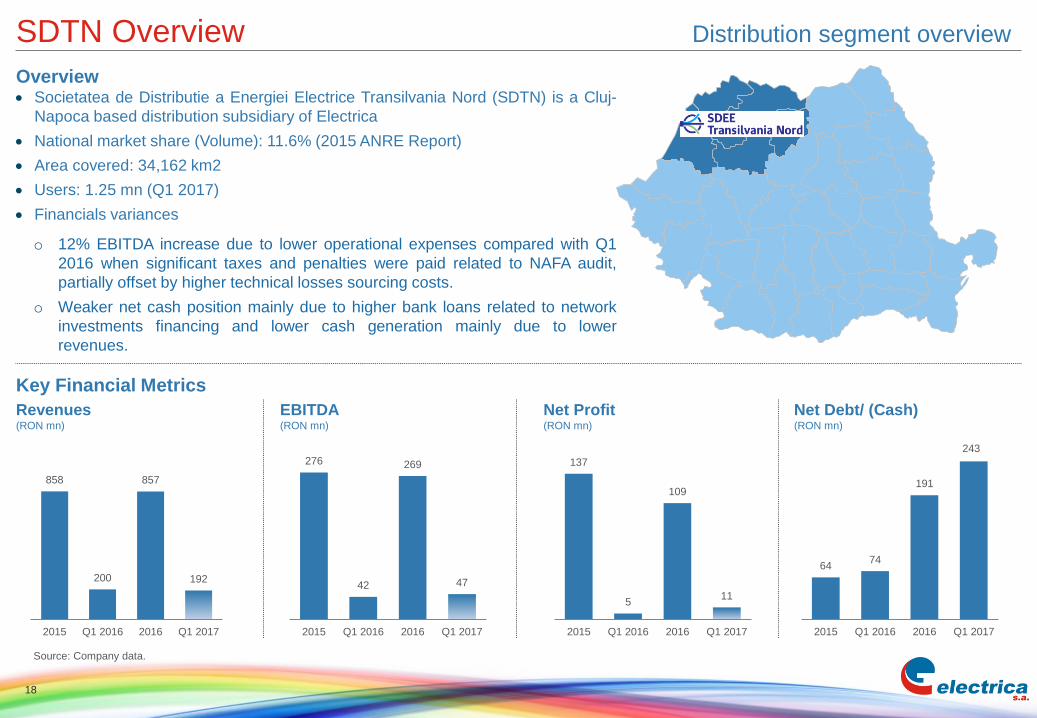

137

5

109

11

2015 Q1 2016 2016 Q1 2017

276

42

269

47

2015 Q1 2016 2016 Q1 2017

858

200

857

192

2015 Q1 2016 2016 Q1 2017

SDTN Overview

Key Financial Metrics

Overview Societatea de Distributie a Energiei Electrice Transilvania Nord (SDTN) is a Cluj-

Napoca based distribution subsidiary of Electrica

National market share (Volume): 11.6% (2015 ANRE Report)

Area covered: 34,162 km2

Users: 1.25 mn (Q1 2017)

Financials variances

o 12% EBITDA increase due to lower operational expenses compared with Q1

2016 when significant taxes and penalties were paid related to NAFA audit,

partially offset by higher technical losses sourcing costs.

o Weaker net cash position mainly due to higher bank loans related to network

investments financing and lower cash generation mainly due to lower

revenues.

Source: Company data.

EBITDA(RON mn)

Net Profit(RON mn)

Net Debt/ (Cash)(RON mn)

Revenues(RON mn)

6474

191

243

2015 Q1 2016 2016 Q1 2017

Distribution segment overview

18

SDTN Overview (Cont’d)

Network Losses(GWh)

Costs due to Network Losses(RON mn)

Network Losses(%)

134

41

136

60

2015 Q1 2016 2016 Q1 2017

632

192

640

200

2015 Q1 2016 2016 Q1 2017

11.48% 11.08% 10.96%

12.34%

10.96% 10.75% 10.43%

12.33%

Reg. Realised Reg. Realised Reg. Realised Reg. Realised

2015 Q1 2016 2016 Q1 2017

Distribution segment overview

19

Source: Company data.

Capex(RON mn)

2.59

0.71

2.67

0.74

1.79

0.48

1.91

0.50

0.55

0.13

0.55

0.13

4.93

1.32

5.13

1.37

2015 Q1 2016 2016 Q1 2017

Low Voltage Medium Voltage High Voltage

Distributed Volumes (TWh)

223

37

234

35

2015 Q1 2016 2016 Q1 2017

135

16

98

-19

2015 Q1 2016 2016 Q1 2017

263

40

227

10

2015 Q1 2016 2016 Q1 2017

Societatea de Distributie a Energiei Electrice Muntenia Nord (SDMN) is a Ploiesti

based distribution subsidiary of Electrica

National market share (Volume): 15.4% (2015 ANRE Report)

Area covered: 28,962 km2

Users: 1.31 mn (Q1 2017)

Financials variances

o 76% lower EBITDA mainly due to significantly network losses higher sourcing cost

(price effect due to the historical highest energy acquisition prices)

o Significant decrease in net profit mainly due to EBITDA impact and higher

depreciation costs

o Weaker net cash position mainly due to higher bank loans related to network

investments financing and lower cash generation mainly due to lower revenues.

Overview

Key Financial Metrics

EBITDA(RON mn)

Net Profit(RON mn)

Net Debt/ (Cash)(RON mn)

Revenues(RON mn)

Source: Company data.

872

189

801

182

2015 Q1 2016 2016 Q1 2017

(121)(128)

(85)

(19)

2015 Q1 2016 2016 Q1 2017

Distribution segment overview

20

SDMN Overview

SDMN Overview (Cont’d)

Network Losses(GWh)

Costs due to Network Losses(RON mn)

Network Losses(%)

194

66

201

88

2015 Q1 2016 2016 Q1 2017

925

304

932

298

2015 Q1 2016 2016 Q1 2017

10.44%11.40%

10.03%

14.34%

10.03%

11.42%

10.05%

13.32%

Reg. Realised Reg. Realised Reg. Realised Reg. Realised

2015 Q1 2016 2016 Q1 2017

Distribution segment overview

21

Source: Company data

Capex(RON mn)

2.63

0.69

2.66

0.74

2.07

0.49

2.09

0.52

1.82

0.47

1.82

0.45

6.51

1.65

6.57

1.71

2015 Q1 2016 2016 Q1 2017

Low Voltage Medium Voltage High Voltage

Distributed Volumes(TWh)

152

28

162

23

2015 Q1 2016 2016 Q1 2017

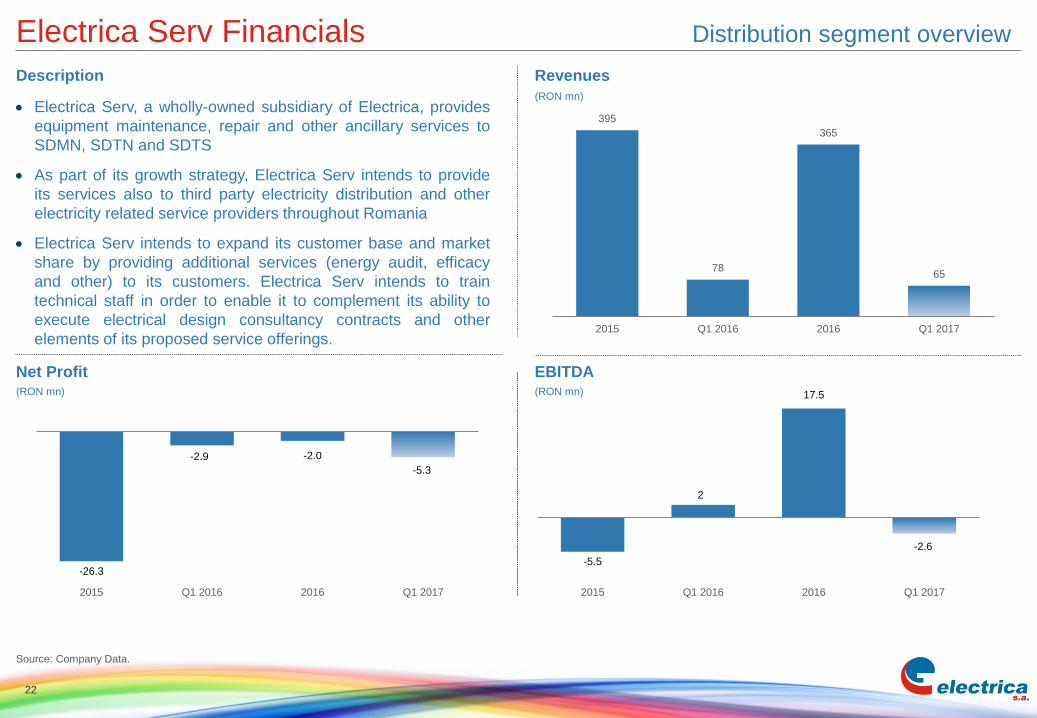

Electrica Serv, a wholly-owned subsidiary of Electrica, provides

equipment maintenance, repair and other ancillary services to

SDMN, SDTN and SDTS

As part of its growth strategy, Electrica Serv intends to provide

its services also to third party electricity distribution and other

electricity related service providers throughout Romania

Electrica Serv intends to expand its customer base and market

share by providing additional services (energy audit, efficacy

and other) to its customers. Electrica Serv intends to train

technical staff in order to enable it to complement its ability to

execute electrical design consultancy contracts and other

elements of its proposed service offerings.

Electrica Serv Financials

Net Profit

Revenues

(RON mn)

(RON mn)

Source: Company Data.

Description

395

78

365

65

2015 Q1 2016 2016 Q1 2017

Distribution segment overview

22

EBITDA(RON mn)

-5.5

2

17.5

-2.6

2015 Q1 2016 2016 Q1 2017

-26.3

-2.9 -2.0

-5.3

2015 Q1 2016 2016 Q1 2017

Supply Overview

Highlights

Executive Summary

Distribution Overview

Supply Overview

Corporate Governance

23

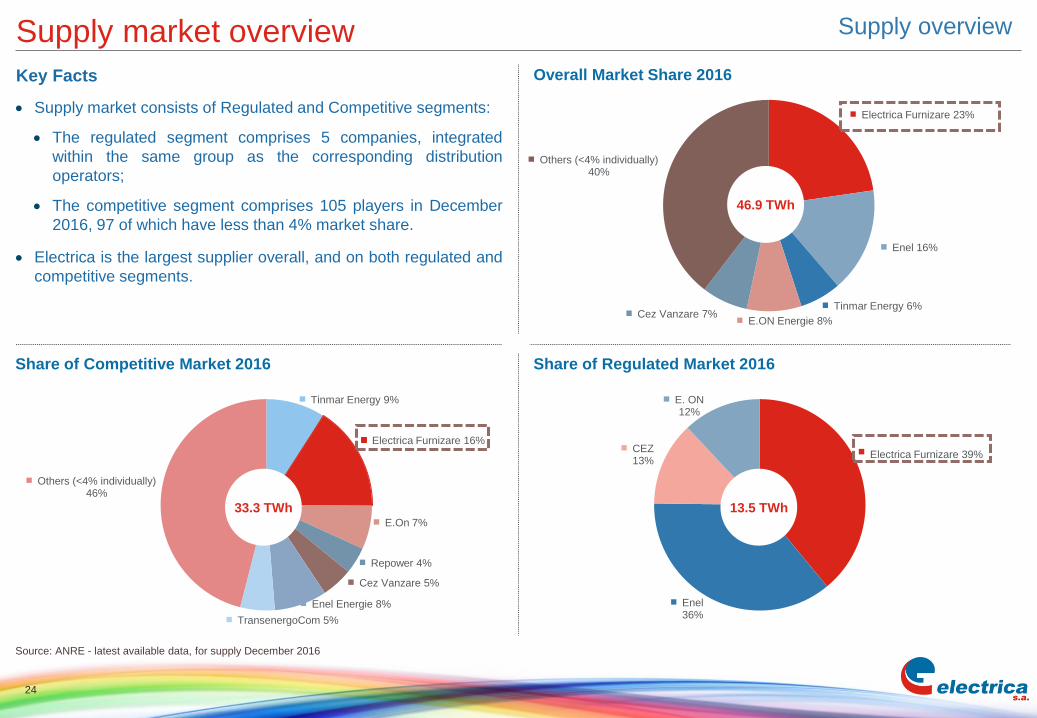

Electrica Furnizare 23%

Enel 16%

Tinmar Energy 6%

E.ON Energie 8%Cez Vanzare 7%

Others (<4% individually)40%

Supply market overview

Key Facts

Supply market consists of Regulated and Competitive segments:

The regulated segment comprises 5 companies, integrated

within the same group as the corresponding distribution

operators;

The competitive segment comprises 105 players in December

2016, 97 of which have less than 4% market share.

Electrica is the largest supplier overall, and on both regulated and

competitive segments.

Overall Market Share 2016

Share of Competitive Market 2016 Share of Regulated Market 2016

Source: ANRE - latest available data, for supply December 2016

46.9 TWh

Electrica Furnizare 39%

Enel36%

CEZ13%

E. ON12%

13.5 TWh

Supply overview

24

Tinmar Energy 9%

Electrica Furnizare 16%

E.On 7%

Repower 4%

Cez Vanzare 5%

Enel Energie 8%

TransenergoCom 5%

Others (<4% individually)46%

33.3 TWh

Regulated, 55%

Competitive, 45%

5.38

1.43

5.30

1.40

4.72

1.36

5.30

1.14

10.10

2.78

10.60

2.54

2015 Q1 2016 2016 Q1 2017

Regulated Competitive

Source: Company data.

Volume of Electricity Supplied on Retail Market(TWh)

Number of ConsumersConsumers (‘000’s)

3,520 3,518 3,469 3,436

90 91 131 162

3,610 3,609 3,600 3,598

2015 Q1 2016 2016 Q1 2017

Competitive Regulated

25

Supply business overview Supply overview

Average energy acquisition priceConsumers by Revenues (Q1 2017)

Regulated, 64%

Competitive, 36%

Consumers by Volume (Q1 2017)

160 160 154

200

2015 Q1 2016 2016 Q1 2017

4,142

1,081

4,031

1,106

347

111

401

91

4,488

1,192

4,432

1,197

2015 Q1 2016 2016 Q1 2017

Net Revenues Green Certificates

Key Financials

EBITDA(RON mn)

Net Profit(RON mn)

Net Debt / (Cash)(RON mn)

Revenues(RON mn)

Supply Segment Overview

Overview

Electrica Furnizare is the supply company of Electrica

Market share: 22.6% (December 2016 ANRE Report)

Consumers: 3.60 mn (Q1 2017)

Financials variances

o Significantly lower EBITDA and net profit mainly due to

significantly higher sourcing costs caused by the energy

market turmoil

o Strong net cash position in line with Q1 2016

Source: Company data.

165

57

185

(51)

2.4%

4.8%4.2%

(4.3)%

2015 Q1 2016 2016 Q1 2017

EBITDA EBITDA Margin

136

44

139

(54)

3.0%

3.7%3.1%

(4.5)%

2015 Q1 2016 2016 Q1 2017

Net Income Net Income Margin

(338)(302)

(465)

(312)

2015 Q1 2016 2016 Q1 2017

Supply overview

26

Regulated Market

Competitive Market

Electrica Furnizare

Coverage

Corporate Governance

Highlights

Executive Summary

Distribution Overview

Supply Overview

Corporate Governance

27

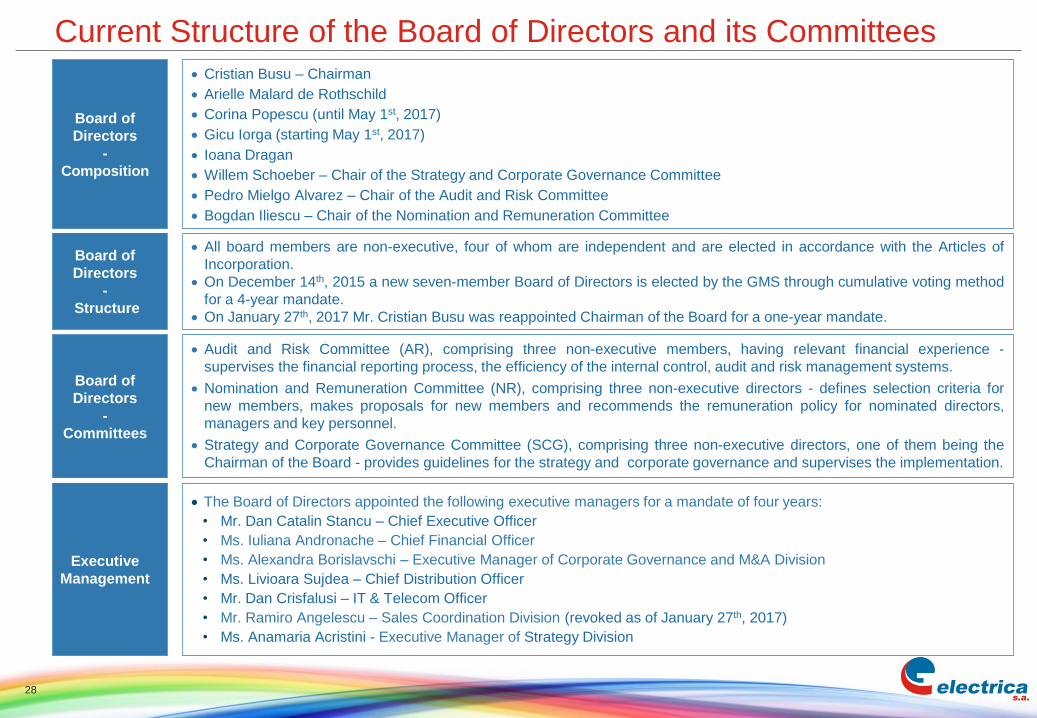

Current Structure of the Board of Directors and its Committees

28

Board of

Directors

-

Structure

Board of

Directors

-

Committees

All board members are non-executive, four of whom are independent and are elected in accordance with the Articles of

Incorporation.

On December 14th, 2015 a new seven-member Board of Directors is elected by the GMS through cumulative voting method

for a 4-year mandate.

On January 27th, 2017 Mr. Cristian Busu was reappointed Chairman of the Board for a one-year mandate.

Audit and Risk Committee (AR), comprising three non-executive members, having relevant financial experience -

supervises the financial reporting process, the efficiency of the internal control, audit and risk management systems.

Nomination and Remuneration Committee (NR), comprising three non-executive directors - defines selection criteria for

new members, makes proposals for new members and recommends the remuneration policy for nominated directors,

managers and key personnel.

Strategy and Corporate Governance Committee (SCG), comprising three non-executive directors, one of them being the

Chairman of the Board - provides guidelines for the strategy and corporate governance and supervises the implementation.

Board of

Directors

-

Composition

Cristian Busu – Chairman

Arielle Malard de Rothschild

Corina Popescu (until May 1st, 2017)

Gicu Iorga (starting May 1st, 2017)

Ioana Dragan

Willem Schoeber – Chair of the Strategy and Corporate Governance Committee

Pedro Mielgo Alvarez – Chair of the Audit and Risk Committee

Bogdan Iliescu – Chair of the Nomination and Remuneration Committee

The Board of Directors appointed the following executive managers for a mandate of four years:

• Mr. Dan Catalin Stancu – Chief Executive Officer

• Ms. Iuliana Andronache – Chief Financial Officer

• Ms. Alexandra Borislavschi – Executive Manager of Corporate Governance and M&A Division

• Ms. Livioara Sujdea – Chief Distribution Officer

• Mr. Dan Crisfalusi – IT & Telecom Officer

• Mr. Ramiro Angelescu – Sales Coordination Division (revoked as of January 27th, 2017)

• Ms. Anamaria Acristini - Executive Manager of Strategy Division

Executive

Management

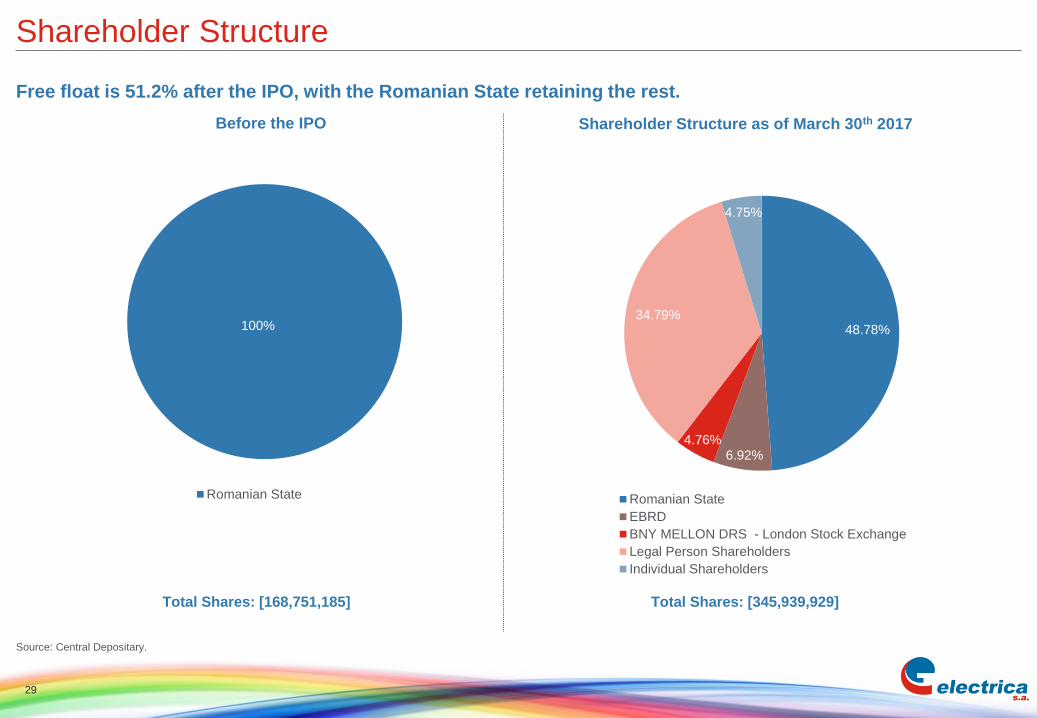

Shareholder Structure

29

Shareholder Structure as of March 30th 2017

100%

Romanian State

Before the IPO

Source: Central Depositary.

Total Shares: [168,751,185] Total Shares: [345,939,929]

Free float is 51.2% after the IPO, with the Romanian State retaining the rest.

48.78%

6.92%4.76%

34.79%

4.75%

Romanian State

EBRD

BNY MELLON DRS - London Stock Exchange

Legal Person Shareholders

Individual Shareholders

Source: BSE, LSE

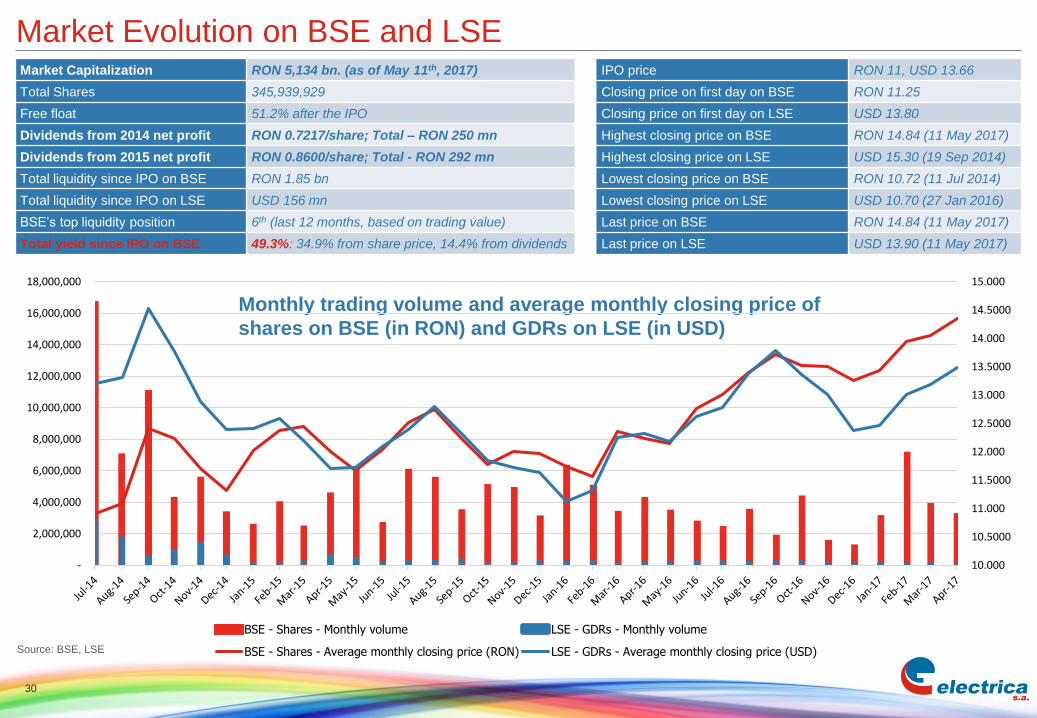

Market Evolution on BSE and LSE

30

Monthly trading volume and average monthly closing price of

shares on BSE (in RON) and GDRs on LSE (in USD)

Market Capitalization RON 5,134 bn. (as of May 11th, 2017) IPO price RON 11, USD 13.66

Total Shares 345,939,929 Closing price on first day on BSE RON 11.25

Free float 51.2% after the IPO Closing price on first day on LSE USD 13.80

Dividends from 2014 net profit RON 0.7217/share; Total – RON 250 mn Highest closing price on BSE RON 14.84 (11 May 2017)

Dividends from 2015 net profit RON 0.8600/share; Total - RON 292 mn Highest closing price on LSE USD 15.30 (19 Sep 2014)

Total liquidity since IPO on BSE RON 1.85 bn Lowest closing price on BSE RON 10.72 (11 Jul 2014)

Total liquidity since IPO on LSE USD 156 mn Lowest closing price on LSE USD 10.70 (27 Jan 2016)

BSE’s top liquidity position 6th (last 12 months, based on trading value) Last price on BSE RON 14.84 (11 May 2017)

Total yield since IPO on BSE 49.3%: 34.9% from share price, 14.4% from dividends Last price on LSE USD 13.90 (11 May 2017)

10.000

10.5000

11.000

11.5000

12.000

12.5000

13.000

13.5000

14.000

14.5000

15.000

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

BSE - Shares - Monthly volume LSE - GDRs - Monthly volume

BSE - Shares - Average monthly closing price (RON) LSE - GDRs - Average monthly closing price (USD)

Source: Company data; BSE

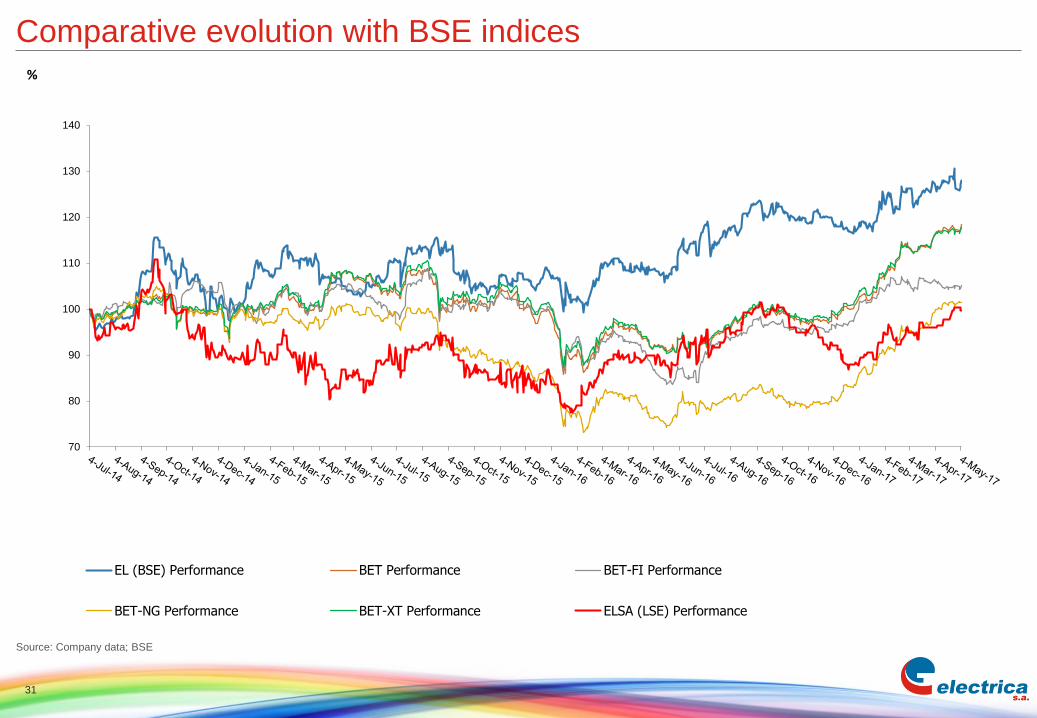

Comparative evolution with BSE indices

31

70

80

90

100

110

120

130

140

EL (BSE) Performance BET Performance BET-FI Performance

BET-NG Performance BET-XT Performance ELSA (LSE) Performance

%

2017 Financial Calendar

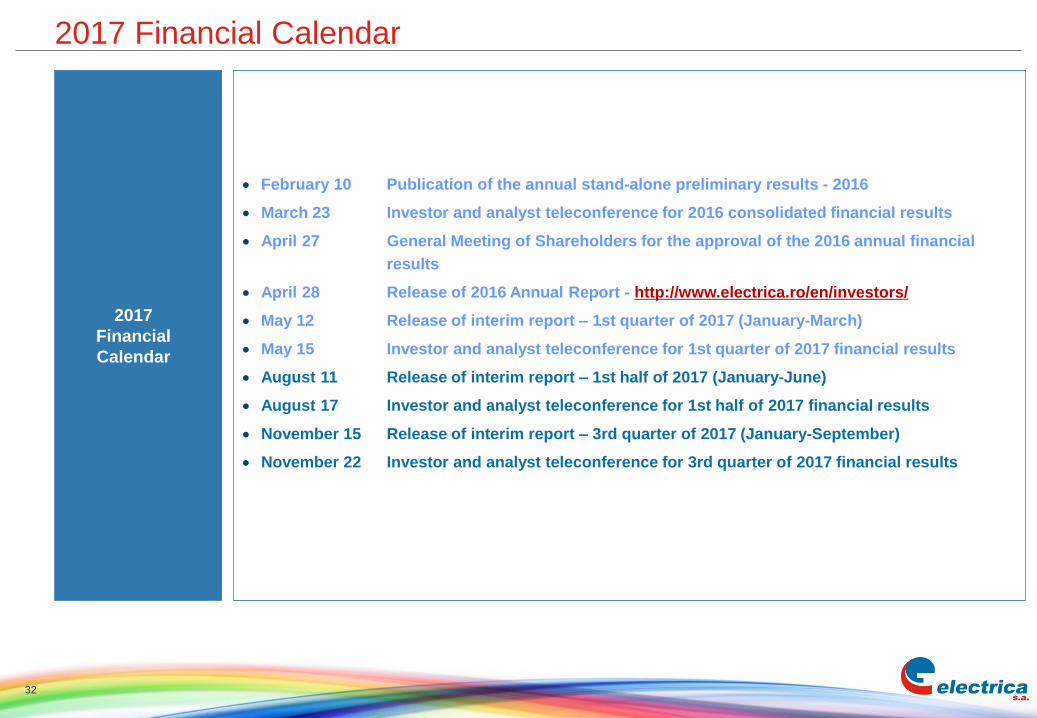

February 10 Publication of the annual stand-alone preliminary results - 2016

March 23 Investor and analyst teleconference for 2016 consolidated financial results

April 27 General Meeting of Shareholders for the approval of the 2016 annual financial

results

April 28 Release of 2016 Annual Report - http://www.electrica.ro/en/investors/

May 12 Release of interim report – 1st quarter of 2017 (January-March)

May 15 Investor and analyst teleconference for 1st quarter of 2017 financial results

August 11 Release of interim report – 1st half of 2017 (January-June)

August 17 Investor and analyst teleconference for 1st half of 2017 financial results

November 15 Release of interim report – 3rd quarter of 2017 (January-September)

November 22 Investor and analyst teleconference for 3rd quarter of 2017 financial results

2017

Financial

Calendar

32