Embed Size (px)

Citation preview

KeyCorp Inves tor Pres entation 2003October

PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995FORWARD-LOOKING STATEMENT DISCLOSURE

1

The presentation and discussion, including related questions and answers, and presentation materials, contain forward-looking statements about issues like anticipated fourth quarter and full-year 2003 earnings, anticipated level of net loan charge-offs and nonperforming assets and anticipated improvement in profitability and competitiveness. Forward-looking statements by their nature are subject to assumptions, risks and uncertainties. Actual results could differ materially from those contained in or implied by such forward-looking statements for a variety of factors including: changes in interest rates; continued weakness in the economy, which could materially impact credit quality trends and the ability to generate loans; failure of the capital markets to function consistent with customary levels; delay in or inability to execute strategic initiatives designed to grow revenues and/or manage expenses; consummation of significant business combinations or divestitures; new legal obligations or restrictions or unfavorable resolution of litigation; further disruption in the economy or the general business climate as a result of terrorist activities or military actions; and changes in accounting, tax or regulatory practices or requirements.

Reshaping Key: A Different Company

Exit Auto LeaseEst. Runoff Portfolio

2001 2002 2003

Henry Meyer Elected Chairman

Built Loan Loss

Reserve

HiredTom Bunn

Corporate Banking

CompletedPEG

$250 mill.savings

Hired New CFO

Jeff Weeden

Union Bankshares Acquisition

Integrated Investment & Commercial

Banking

T.D. Leasing Portfolio

Acquisition

Focused on product

Higher credit risk tolerance

Unfocused expense culture

Inconsistent financial measures

Focused on deepening relationships

Re-established conservative credit culture

PEG expense culture

Economic Profit Added (EPA)

NewBridge Acquisition

ConningAcquisition

2

Strategic Priorities

Profitably grow revenue• Focus on relationship businesses• Increase deposits• Improve cross-sell

Improve credit quality

Maintain expens e dis c ipline

( )Improve s hareholder value EPA

3

Net Income by Line of Business

Corporate & Inves tment Banking

40%Cons umerBanking

50%

Inves tment Management

Services

- 3 03Net Income Q

•Retail Banking•Small Business•Consumer Finance

•Corporate Banking•KeyBank Real Estate Capital•Key Equipment Finance

10%

4

Depos it growth -Increas e cros s s e ll New client acquis ition

• Adding new KeyCenters and RMs : -Cons umer Finance repos ition and improve cros s s e ll : Bus ines s Banking focus on bus ines s deve lopment

Bus ines s Initiatives

Consumer Banking

Bus ines s Scale 900 - 2,200 KeyCenters ATMs - : 722,000 (37% )On line Clients Penetration : 10 Small Bus ines s th larges t in loan balances

•Retail Banking•Small Business•Consumer Finance

5

Revenue Growth• Align commercial & investment banking• “Lead with Leasing”

Depos it Growth• Cross-sell loans and deposits• Focus on client specific segments

Improve as s et quality

- Maximize Key led trans actions

#5 Equipment Leas ing #5 Commercial Real Es tate Lender

Corporate & Inves tment Banking

Bus ines s Initiatives

Bus ines s Scale •Corporate Banking•KeyBank R/E Capital•Key Equipment Finance

6

Inves tment Management Services

Bus ines s Scale

- : 128 .Managed & Non Managed As s e ts $ Bill

Bus ines s Initiatives Victory Capital

• Leverage external distribution• Continue to penetrate the franchise• Fill out product menu - NewBridge

MFG• Rationalize cost structure• Align teams around high net worth clients

•Victory Capital Mgmt•McDonald Financial Group (MFG)

7

Financial Review

Financial Objectives

Achieve long term targets •ROE: 16 - 18%•EPS Growth: 7 – 8%

Continue expens e dis c ipline

Improve as s et quality

Manage s trong capital pos ition•New authorization to repurchase 25 million

shares

9

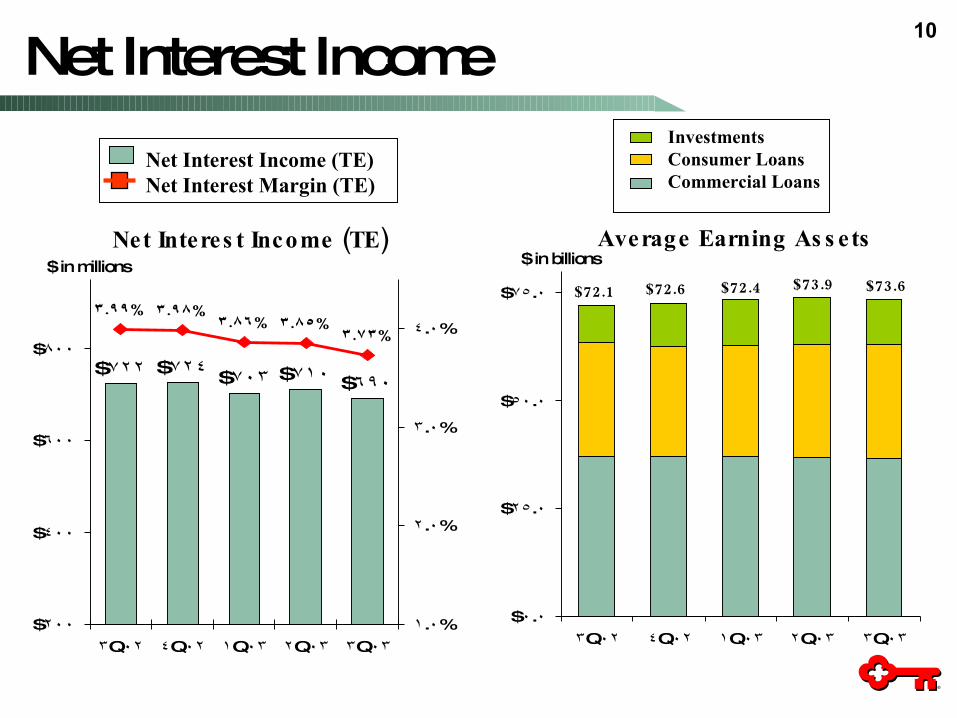

Net Interest Income

$722 $724 $703 $710 $690

. %3 99 . %3 98. %3 86 . %3 85

. %3 73

$200

$400

$600

$800

Q3 02 Q4 02 Q1 03 Q2 03 Q3 03

. %1 0

. %2 0

. %3 0

. %4 0

$ .0 0

$ .25 0

$ .50 0

$ .75 0

Q3 02 Q4 02 Q1 03 Q2 03 Q3 03

Net Interest Income (TE)Net Interest Margin (TE)

( )Net Interes t Income TE Average Earning As s ets

InvestmentsConsumer LoansCommercial Loans

$ in millions

72.1$ 72.6$ 72.4$ 73.9$ 73.6$

10

$ in billions

38.1 37.7 37.1 $ $ $ 37.1 36.5 36.4 36.5 36.5 36.4 $ $ $ $ $ $ (1)%

23.3 22.0 22.9 24.0 24.6 24.3 24.7 25.2 25.7 6

3.5 3.0 2.5 2.0 1.7 1.4 1.1 0.9 0.8 (61) 1.3 1.1 1.0 0.8 0.7 0.6 0.5 0.4 0.2 (166)

.$66 2 .$63 8 .$63 1.$63 0.$62 8.$62 7.$63 5.$63 9.$63 5

3Q01 4Q01 1Q02 2Q02 3Q02 4Q02 1Q03 2Q03 3Q03

in billions

% change *3 03 . 2 03Q vs Q

* Annualized

Commerc ialCons umer

AutoCommerc ial

Exit Portfo lios

Average Loans11

in billions

Average Core Depos its

* Annualized

.$37 3 .$37 0 .$37 2.$39 2 .$40 4 .$41 3 .$42 2

.$37 0 .$37 4

3Q01 4Q01 1Q02 2Q02 3Q02 4Q02 1Q03 2Q03 3Q03 /Now MMDA 13.1$ 13.0$ 13.4$ 13.2$ 13.3$ 15.1$ 16.8$ 17.7$ 18.4 14% Savings 1.9 1.9 1.9 2.0 2.0 2.0 2.0 2.1 2.1 2 ’CD s 13.7 13.7 13.4 13.1 12.7 12.2 11.8 11.4 11.1 (13) DDA 8.3 8.8 8.6 8.7 9.2 9.9 9.8 10.1 10.6 23

TOTAL 37.0 37.4$ $ 37.3$ 37.0$ 37.2$ 39.2$ 40.4$ 41.3$ 42.2$8%

% change *3 03 . 2 03Q vs Q

12

As s et Quality Indicators

$ in millions 3 02Q 4 02Q 1 03Q 2 03Q 3 03Q

Nonperforming Loans $987 $943 $904 $837 $795to EOP Loans 1.57% 1.51% 1.44% 1.32% 1.27%

Nonperforming Assets $1,017 $993 $968 $897 $862to EOP Loans + OREO 1.61% 1.59% 1.54% 1.42% 1.37%

Net C/O $185 $186 $161 $141 $123to Average Loans 1.16% 1.18% 1.04% .90% .77%

Allowance $1,489 $1,452 $1,421 $1,405 $1,405to Total Loans 2.37% 2.32% 2.27% 2.22% 2.24%to Nonperforming Loans 151% 154% 157% 168% 177%

13

Tangible Equity to Tangible As s ets

. %6 94

. %6 16 . %6 12. %6 29

. %6 51

. %6 29

. %6 57. %6 73

. %6 10

. %6 69 . %6 71. %6 71

. %6 25. %6 12

. %6 90

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

1Q00 2Q00 3Q00 4Q00 1Q01 2Q01 3Q01 4Q01 1Q02 2Q02 3Q02 4Q02 1Q03 2Q03 3Q03

KEY Pe er Median S&P Regional & Diversified Bank Indice s

3 03: 20 24 Q of banks reporting

6.78%

14

Dividend Record

.56.56.64.64

.72.72.76.76

.84.84.94.94

1.041.041.121.12

1.201.201.181.18

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003T

1.221.22

15

Thinking Like An Owner

: 7%Total ins ider owners hip• 77% of employees own Key shares• 69% of employees have stock options

Stock owners hip guide lines• CEO: 6 x salary• CEO direct reports: 4 x salary• Executive Council: 2 x salary

16

Summary

New management team focus ed on :improving performance

• Profitably grow revenue• Focus on relationship businesses• Increase deposits• Improve asset quality• Manage expenses

Alignment of management and s hareholder interes ts

Strong dividend record

17

Appendix

Retail Banking Markets

900 KeyCenters2,200 ATMs1-800-KEY-2-YOUKey.com

12 State Footprint2.2 Million Clients6,100+ Employees$1.3+ Billion Revenues

A-1

Market Share by District

District

* Deposit Market Position

* KeyBank Deposits

(in billions)

* KeyBank Deposit

Market Share# of

KeyCentersCLEVELAND OH 1 $16.2 36% 68CENTRAL NEW YORK 1 $1.8 12% 59MAINE 2 $1.9 13% 62TOLEDO OH 2 $1.4 10% 38WESTERN NEW YORK 3 $2.3 9% 42SOUTH PUGET SOUND WA 3 $2.0 12% 62ALBANY NY 3 $1.8 12% 46HUDSON VALLEY NY 3 $1.6 7% 36NORTHERN INDIANA 3 $0.9 12% 33IDAHO 3 $0.6 7% 30SEATTLE WA 4 $1.6 6% 42DAYTON OH 4 $0.8 8% 24VERMONT 4 $0.4 8% 12TOTAL (KEY POSITION 1-4) $33.3 15% 554% OF KEYBANK'S TOTAL 78% 62%

OREGON 5 $2.0 7% 66TRANS MOUNTAIN WA 5 $0.8 5% 32ALASKA 5 $0.4 6% 17AKRON/CANTON OH 6 $1.2 7% 38CENTRAL INDIANA 6 $0.8 5% 32COLUMBUS OH 6 $0.8 6% 25CINCINNATI OH 6 $0.6 2% 23ROCHESTER NY 8 $0.3 3% 14COLORADO 9 $1.0 2% 41MICHIGAN 9 $0.5 4% 21UTAH 10 $0.6 1% 37TOTAL (KEY POSITION 5-10) $9.3 3% 346% OF KEYBANK'S TOTAL 22% 38%KEYBANK TOTALS $42.5 900

A-2

Commercial Portfolio - Geography

Northeas t23%

Rocky Mountain

9%

Northwes t22%

Great Lakes

46%

A-3

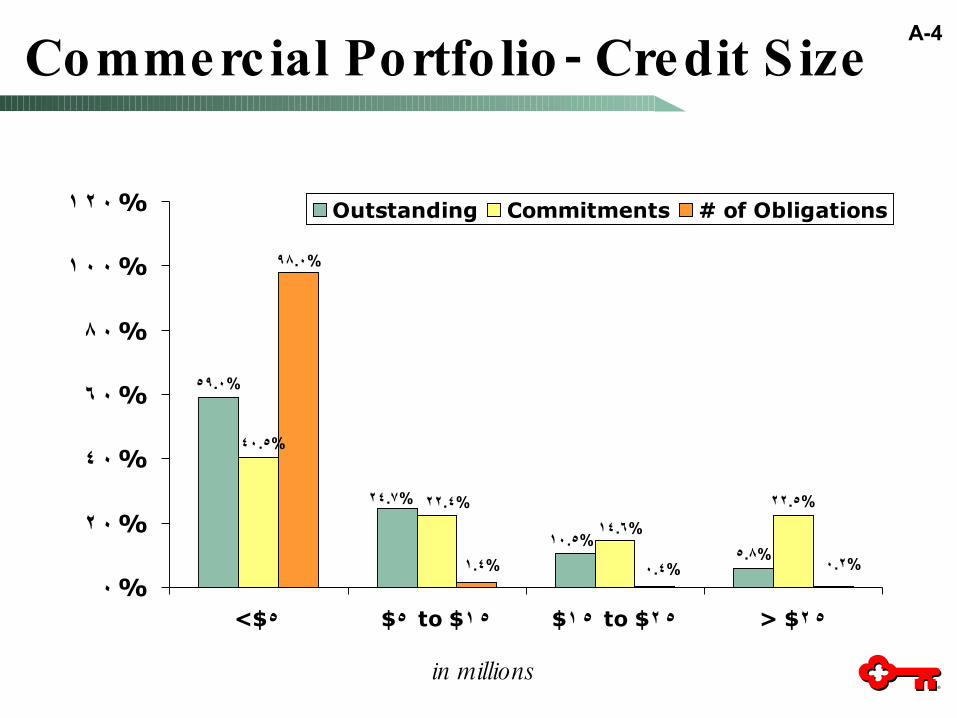

- Commercial Portfo lio Credit S ize

59.0%

24.7%

10.5%5.8%

14.6%

22.5%

40.5%

22.4%

98.0%

1.4% 0.4% 0.2%

%0

%2 0

%4 0

%6 0

%8 0

%1 0 0

%1 2 0

<$5 $ to $5 1 5 $ to $1 5 2 5 > $2 5

Outstanding Commitments # of Obligations

in millions

A-4

- Commercial Portfo lio Utilization Rate

* Excludes Real Estate, Leasing and Commercial Run-off portfolios

. %40 2 . %39 7. %38 8

. %41 1

. %44 0

. %45 2

. %42 5. %42 0

. %44 0. %44 3

. %45 9

. %47 3

. %45 9. %46 5 . %46 1

%30

%35

%40

%45

%50

1Q00 2Q00 3Q00 4Q00 1Q01 2Q01 3Q01 4Q01 1Q02 2Q02 3Q02 4Q02 1Q03 2Q03 3Q03

A-5

Net Charge-Offs to Average Loans

. %0 84

. %0 42

. %0 63 . %0 64 . %0 66

. %1 02 . %1 04

. %1 37. %1 32

. %1 27

. %1 16 . %1 18

. %1 04

. %0 90

. %0 77

. %0 44

0.00%

0.30%

0.60%

0.90%

1.20%

1.50%

1Q00 2Q00 3Q00 4Q00 1Q01 2Q01 3Q01 4Q01 1Q02 2Q02 3Q02 4Q02 1Q03 2Q03 3Q03

KEY Pe e r Me dian S&P Re gional & Dive rsifie d Bank Indice s3 03: 20 24 Q of banks reporting

A-6

- Net Charge Offs to Average Loans by Loan Type

. %0 73

. %0 84

. %1 51

. %0 93

. %0 77

. %1 43

. %1 32

. %0 97

. %1 08

. %0 97. %1 00

. %0 75

2 02 3 02 4 02 1 03 2 03 3 03Q Q Q Q Q Q

Cons umerCommercial

2 02 3 02 4 02 1 03 2 03 3 03Q Q Q Q Q Q

A-7

NPAs to Loans and OREO

1.41%

1.56%

1.42%1.37%

1.10%

1.61%1.59%

1.54%

1.58%

1.49%

0.88%0.93%

1.00%

0.78%

1.23%

0.00%

0.40%

0.80%

1.20%

1.60%

2.00%

1Q00 2Q00 3Q00 4Q00 1Q01 2Q01 3Q01 4Q01 1Q02 2Q02 3Q02 4Q02 1Q03 2Q03 3Q03

KEY Pe e r Me dian S&P Re gional & Dive rsifie d Bank Indice s3 03: 20 24 Q of banks reporting

0.74%

A-8

Allowance to Total Loans

1.49%

2.22% 2.24%

1.82%

2.27%2.32%2.37%

1.53% 1.51% 1.50% 1.49%

1.85%

2.41%2.51%

2.65%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

1Q00 2Q00 3Q00 4Q00 1Q01 2Q01 3Q01 4Q01 1Q02 2Q02 3Q02 4Q02 1Q03 2Q03 3Q03

KEY Pe er Median S&P Regional & Dive rsifie d Bank Indice s3 03: 20 24 Q of banks reporting

1.45%

A-9

( )Net Interes t Margin TE

3.73%

3.85%3.85%

3.68%

3.86%

3.98%3.99%

3.68% 3.68%3.71%

3.63%

3.77%

3.98%3.93%

3.98%

3.00%

3.25%

3.50%

3.75%

4.00%

4.25%

4.50%

1Q00 2Q00 3Q00 4Q00 1Q01 2Q01 3Q01 4Q01 1Q02 2Q02 3Q02 4Q02 1Q03 2Q03 3Q03

KEY Pe er Median S&P Regional & Dive rsified Bank Indice s

3.73%

3.85%3.85%

3.68%

3.86%

3.98%3.99%

3.68% 3.68%3.71%

3.63%

3.77%

3.98%3.93%

3.98%

3.00%

3.25%

3.50%

3.75%

4.00%

4.25%

4.50%

1Q00 2Q00 3Q00 4Q00 1Q01 2Q01 3Q01 4Q01 1Q02 2Q02 3Q02 4Q02 1Q03 2Q03 3Q03

KEY Pe er Median S&P Regional & Dive rsified Bank Indice s

3.57%

3 03: 20 24 Q of banks reporting

A-10

. 18.3M Mkt 19.7 21.8 22.2 23.3 21.3 20.0 19.5 20.7 19.3 18.3 19.1 19.3 18.9 .Fixed Inc 14.3 13.1 13.2 13.0 13.7 15.3 15.7 17.3 17.5 16.3 16.1 16.3 17.1 17.3 37.9 39.6Equity 37.7 35.5 36.6 32.8 35.6 36.1 32.4 26.8 27.2 25.4 26.9 28.8

As s ets Under Management$ in billions

.$65 0.$63 3

.$72 8 .$70 7 .$73 6.$69 4

.$71 2 .$72 9 .$70 7

.$62 5 .$61 7 .$60 8

.$70 5.$72 4

-Dec98

-Dec99

-Dec00

1Q01 2Q01 3Q01 4Q01 1Q02 2Q02 3Q02 4Q02 1Q03 2Q03 3Q03

A-11

Relative ly s table net interes t margin

Stable to modes t loan growth

- Improving c limate for fee bas edbus ines s es

Continued focus on expens es

– As s et Quality s table to improving

4 03 : 0.52 0.55Q EPS $ to $

2003 Fourth Quarter OutlookA-12