Embed Size (px)

Citation preview

Presentation to the House Appropriations Subcommittee on Article II:

Overview of Texas Medicaid Hospital Finance and the Section 1115 Demonstration Waiver

Health and Human Services Commission

Charles Smith, Executive Commissioner Pam McDonald, Director of Rate Analysis

Ardas Khalsa, Deputy Medicaid/CHIP Director, Healthcare Transformation Waiver

July 13, 2016

2

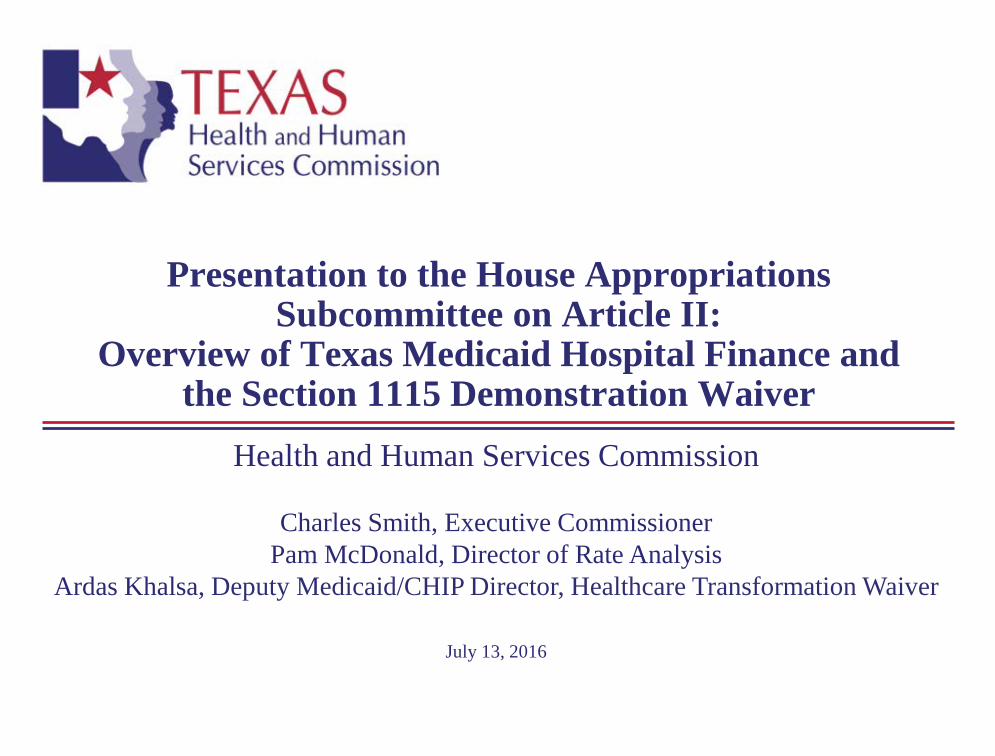

Overview of Hospital Finance Texas Medicaid Hospital Payment Overview

• Historically hospital payments have been made using four mechanisms: Inpatient payments Outpatient payments Disproportionate Share Hospital (DSH) payments Upper Payment Limit (UPL) payments

UPL payments transitioned to Medicaid 1115 Transformation Waiver Uncompensated Care (UC) Pool payments in FFY 2012.

• A fifth mechanism, Delivery System Reform Incentive Payments (DSRIP) under the waiver, began in early FFY 2013.

• An additional mechanism, the Network Adequacy Improvement Program (NAIP), began in March 2015.

3

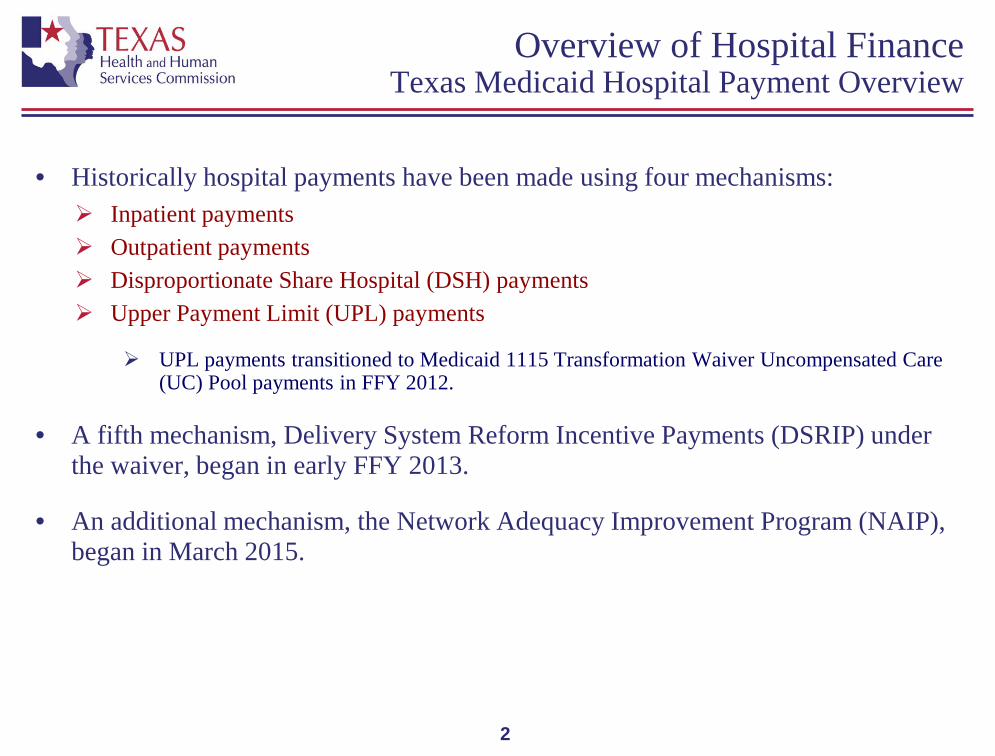

Overview of Hospital Finance Inpatient Rates

• Inpatient Methodology

Standard Dollar Amounts (SDAs): Represent a percentage of the average cost of an inpatient admission General; Children’s; Rural (facility-specific) SDAs only change through Legislative action

All Patient Refined Diagnosis-Related Group (APR – DRGs) weights Outlier Payments for cost and length of stay outliers (children only) Add-ons: geographic wage; teaching; safety net, trauma (not available for Children’s

since all Children’s are trauma-certified and trauma costs are included in base). No add-ons for Rural since they are paid using facility-specific SDAs.

State-owned hospitals reimbursed through the Tax Equity and Fiscal Responsibility Act of 1982 (TEFRA) (cost-based)

SDA Add-ons

DRG Relative Weight

Inpatient Reimbursement

4

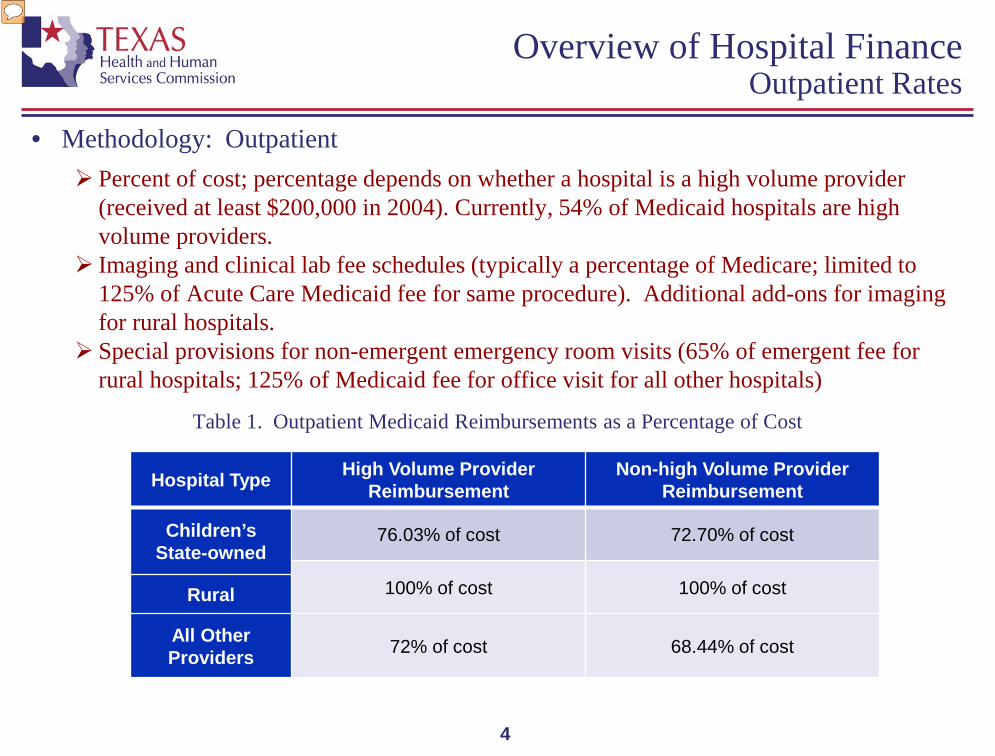

Overview of Hospital Finance Outpatient Rates

• Methodology: Outpatient Percent of cost; percentage depends on whether a hospital is a high volume provider

(received at least $200,000 in 2004). Currently, 54% of Medicaid hospitals are high volume providers.

Imaging and clinical lab fee schedules (typically a percentage of Medicare; limited to 125% of Acute Care Medicaid fee for same procedure). Additional add-ons for imaging for rural hospitals.

Special provisions for non-emergent emergency room visits (65% of emergent fee for rural hospitals; 125% of Medicaid fee for office visit for all other hospitals)

Table 1. Outpatient Medicaid Reimbursements as a Percentage of Cost

Hospital Type High Volume Provider Reimbursement

Non-high Volume Provider Reimbursement

Children’s State-owned

76.03% of cost 72.70% of cost

100% of cost 100% of cost Rural

All Other Providers 72% of cost 68.44% of cost

5

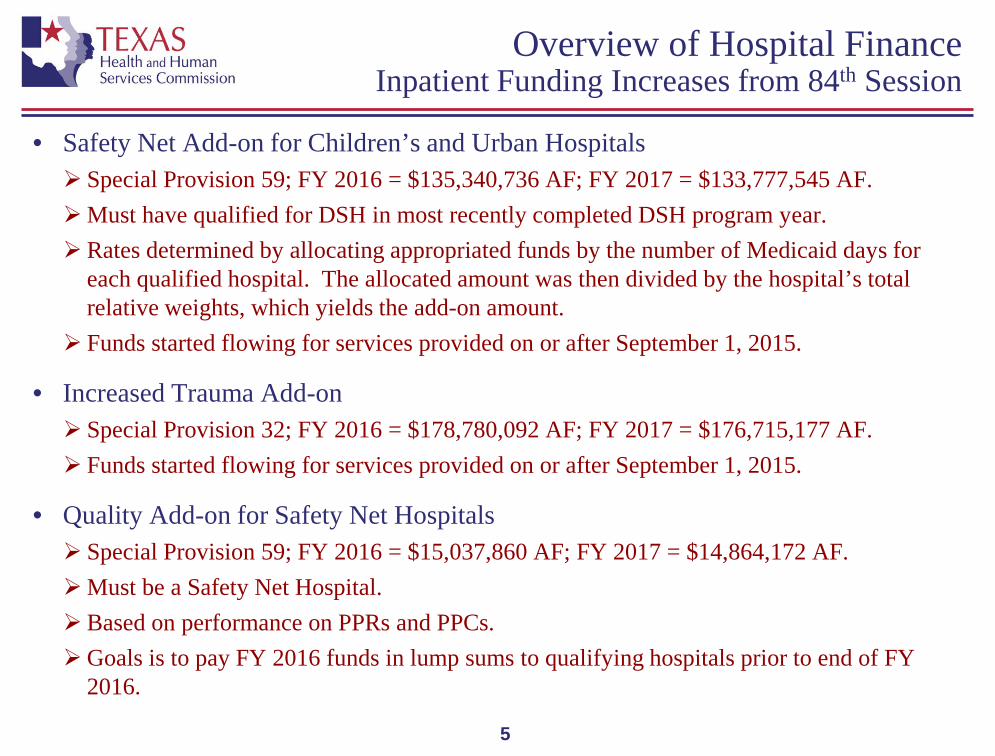

Overview of Hospital Finance Inpatient Funding Increases from 84th Session

• Safety Net Add-on for Children’s and Urban Hospitals

Special Provision 59; FY 2016 = $135,340,736 AF; FY 2017 = $133,777,545 AF. Must have qualified for DSH in most recently completed DSH program year. Rates determined by allocating appropriated funds by the number of Medicaid days for

each qualified hospital. The allocated amount was then divided by the hospital’s total relative weights, which yields the add-on amount.

Funds started flowing for services provided on or after September 1, 2015.

• Increased Trauma Add-on

Special Provision 32; FY 2016 = $178,780,092 AF; FY 2017 = $176,715,177 AF. Funds started flowing for services provided on or after September 1, 2015.

• Quality Add-on for Safety Net Hospitals

Special Provision 59; FY 2016 = $15,037,860 AF; FY 2017 = $14,864,172 AF. Must be a Safety Net Hospital. Based on performance on PPRs and PPCs. Goals is to pay FY 2016 funds in lump sums to qualifying hospitals prior to end of FY

2016.

6

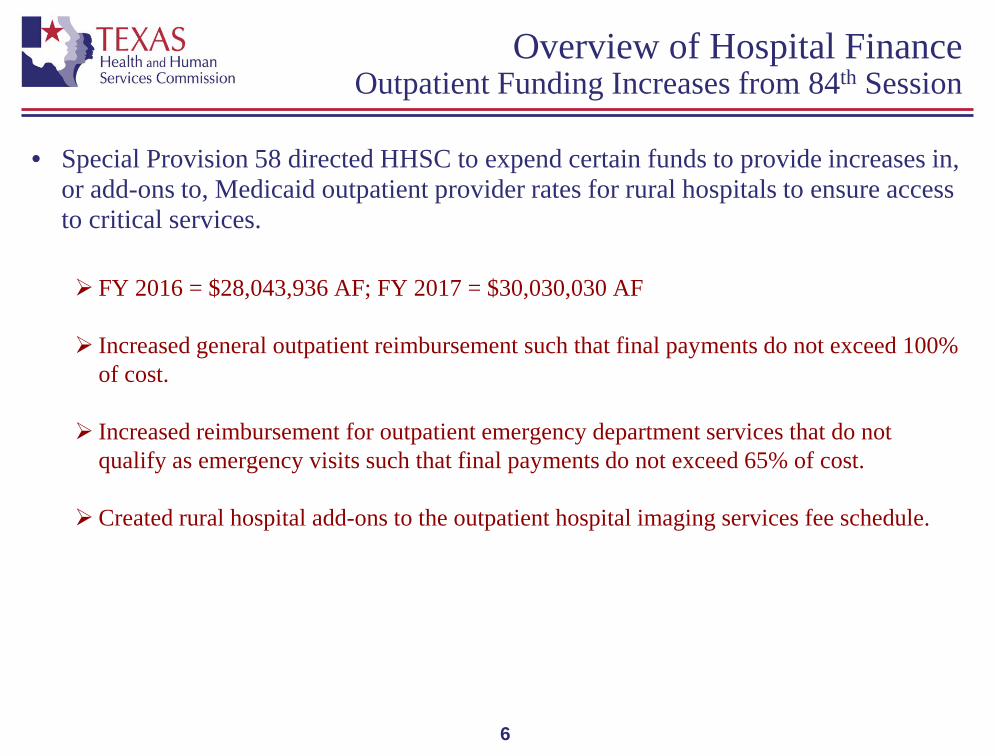

Overview of Hospital Finance Outpatient Funding Increases from 84th Session

• Special Provision 58 directed HHSC to expend certain funds to provide increases in, or add-ons to, Medicaid outpatient provider rates for rural hospitals to ensure access to critical services.

FY 2016 = $28,043,936 AF; FY 2017 = $30,030,030 AF

Increased general outpatient reimbursement such that final payments do not exceed 100%

of cost.

Increased reimbursement for outpatient emergency department services that do not qualify as emergency visits such that final payments do not exceed 65% of cost.

Created rural hospital add-ons to the outpatient hospital imaging services fee schedule.

7

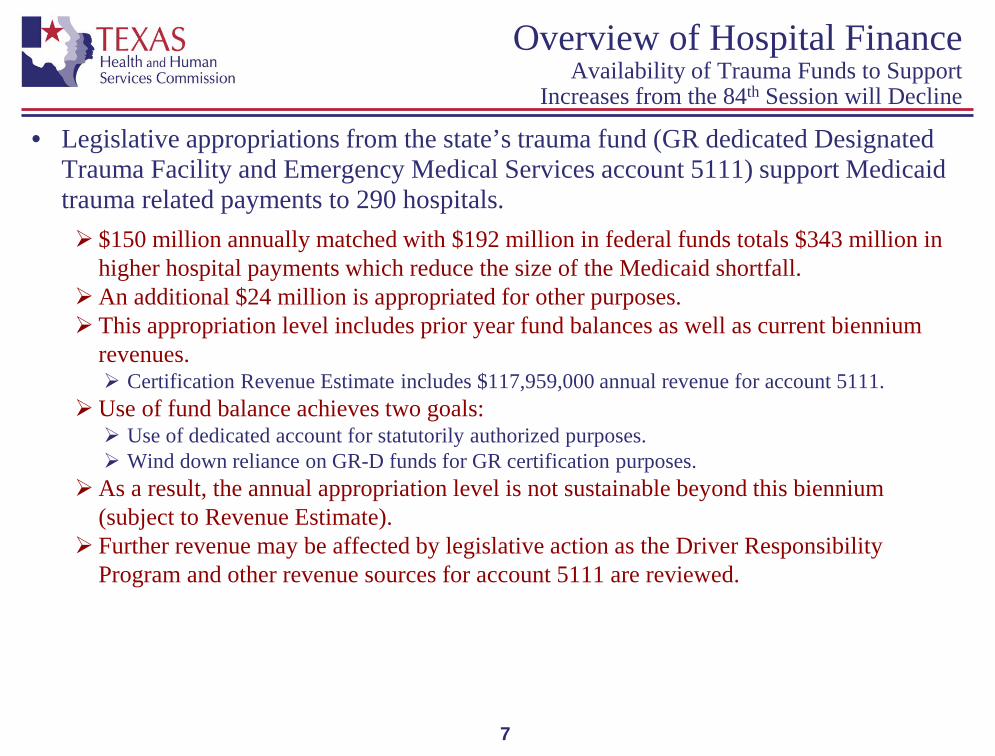

Overview of Hospital Finance Availability of Trauma Funds to Support

Increases from the 84th Session will Decline

• Legislative appropriations from the state’s trauma fund (GR dedicated Designated Trauma Facility and Emergency Medical Services account 5111) support Medicaid trauma related payments to 290 hospitals. $150 million annually matched with $192 million in federal funds totals $343 million in

higher hospital payments which reduce the size of the Medicaid shortfall. An additional $24 million is appropriated for other purposes. This appropriation level includes prior year fund balances as well as current biennium

revenues. Certification Revenue Estimate includes $117,959,000 annual revenue for account 5111.

Use of fund balance achieves two goals: Use of dedicated account for statutorily authorized purposes. Wind down reliance on GR-D funds for GR certification purposes.

As a result, the annual appropriation level is not sustainable beyond this biennium (subject to Revenue Estimate).

Further revenue may be affected by legislative action as the Driver Responsibility Program and other revenue sources for account 5111 are reviewed.

8

Overview of Hospital Finance Children’s and Rural Hospitals

• Prior to September 1, 2013, children’s and rural hospitals’ inpatient costs were reimbursed using a cost-based methodology that followed principles laid out in the federal Tax Equity and Fiscal Responsibility Act of 1982 (TEFRA).

• The 2014-2015 General Appropriations Act, Article II, Rider 38 directed HHSC to rebase rural hospital rates by implementing a facility-specific prospective full cost standard dollar amount (SDA) based on historical costs, trended forward for inflation and limited by a floor and a ceiling.

• Rider 51.b.(17) and (19) directed HHSC to pay more appropriate outlier payments and to adjust inpatient hospital reimbursement for labor and delivery services provided to adults at a children’s hospital.

• Rider 71 directed HHSC to implement an All Patient Refined Diagnostic Related Group (APR-DRG) prospective payment system for inpatient services provided by a children’s hospital, trended forward for inflation.

9

Overview of Hospital Finance Children’s and Rural Hospitals (cont.)

• Currently, Children’s Hospitals: Are reimbursed for inpatient services using a single, children’s statewide base SDA with

add-ons for geographic wage differences and for teaching medical education. The children’s hospital single base SDA is currently $9,506 (by way of comparison, the

urban base SDA is $2,994) The average children’s hospital inpatient SDA with add-ons is $12,040. Average adult delivery rate in a children’s hospital is $3,305. Outpatient reimbursement as percentage of cost is approximately 4 percent greater than

for urban hospitals.

• Currently, Rural Hospitals: Are reimbursed for inpatient services using facility-specific SDA’s with a floor of $4,533

and a ceiling of $12,968. Because SDAs are facility-specific based on each hospitals’ costs, there are no add-ons. General outpatient services are reimbursed at 100% of cost. Non-emergent, emergency room services are reimbursed at 65% of cost. Imaging and clinical laboratory services are reimbursed via a fee schedule with special

rural hospital add-ons for imaging.

10

Overview of Hospital Finance “Medicaid Shortfall” and Hospital-specific Limit

• “Medicaid Shortfall” Definition: Medicaid costs not covered by Medicaid rates result in the Medicaid shortfall. Inpatient: In 2014, Medicaid rates covered approximately 57% of Medicaid costs, on

average, for general Medicaid hospitals (excluding children’s, rural and state-owned) and 67% of Medicaid costs, on average, for all Medicaid hospitals.

Outpatient rules for general hospitals limit payments to 72% of cost for high volume providers and 68.44% of cost for all other hospitals. For children’s and state-owned hospitals, outpatient rules limit payments to 76.03% for high volume providers and 72.70% for all others. Rural hospitals are reimbursed 100% of cost for general outpatient services.

• For each hospital, a hospital-specific limit (HSL) is calculated as the sum of: The hospital’s Medicaid shortfall (difference between hospital costs for Medicaid patients

and Medicaid claims payments); and The hospital’s unreimbursed costs of caring for low-income uninsured individuals.

• Each hospital that is eligible may receive combined DSH and UC payments up to its HSL, if there are sufficient non-federal funds to support these payments. Under the Transformation Waiver, hospitals may also receive payments for uncompensated physician, clinic and pharmacy costs.

11

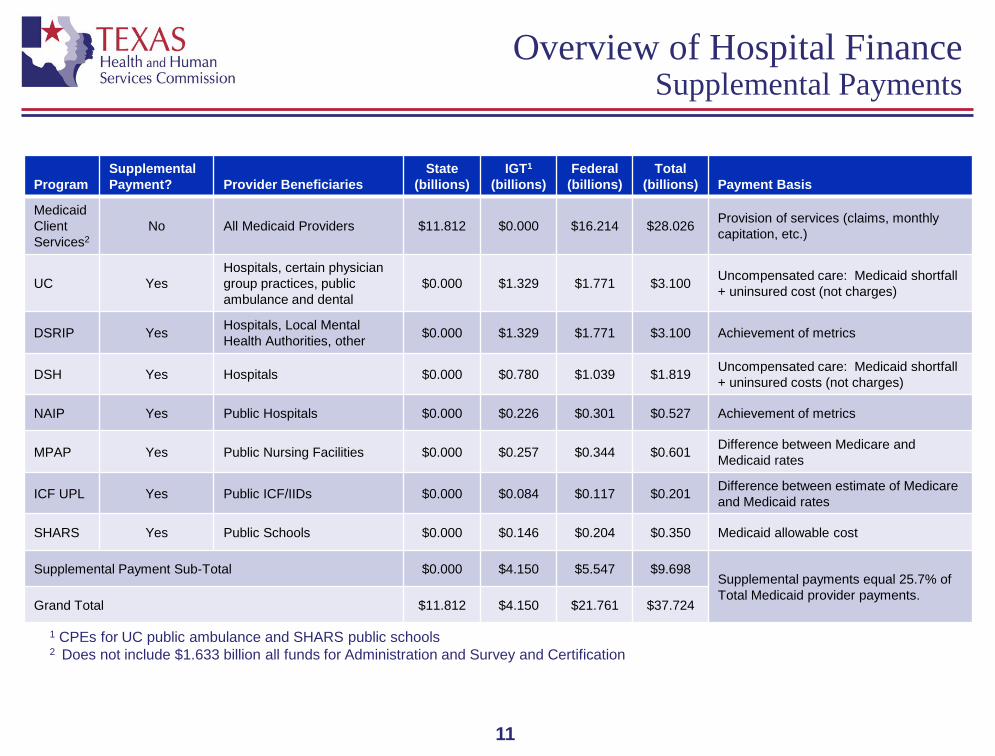

Overview of Hospital Finance Supplemental Payments

Program

Supplemental Payment?

Provider Beneficiaries

State (billions)

IGT1 (billions)

Federal (billions)

Total (billions)

Payment Basis

Medicaid Client Services2

No All Medicaid Providers $11.812 $0.000 $16.214 $28.026 Provision of services (claims, monthly capitation, etc.)

UC Yes Hospitals, certain physician group practices, public ambulance and dental

$0.000 $1.329 $1.771 $3.100 Uncompensated care: Medicaid shortfall + uninsured cost (not charges)

DSRIP Yes Hospitals, Local Mental Health Authorities, other $0.000 $1.329 $1.771 $3.100 Achievement of metrics

DSH Yes Hospitals $0.000 $0.780 $1.039 $1.819 Uncompensated care: Medicaid shortfall + uninsured costs (not charges)

NAIP Yes Public Hospitals $0.000 $0.226 $0.301 $0.527 Achievement of metrics

MPAP Yes Public Nursing Facilities $0.000 $0.257 $0.344 $0.601 Difference between Medicare and Medicaid rates

ICF UPL Yes Public ICF/IIDs $0.000 $0.084 $0.117 $0.201 Difference between estimate of Medicare and Medicaid rates

SHARS Yes Public Schools $0.000 $0.146 $0.204 $0.350 Medicaid allowable cost

Supplemental Payment Sub-Total $0.000 $4.150 $5.547 $9.698 Supplemental payments equal 25.7% of Total Medicaid provider payments.

Grand Total $11.812 $4.150 $21.761 $37.724

1 CPEs for UC public ambulance and SHARS public schools 2 Does not include $1.633 billion all funds for Administration and Survey and Certification

12

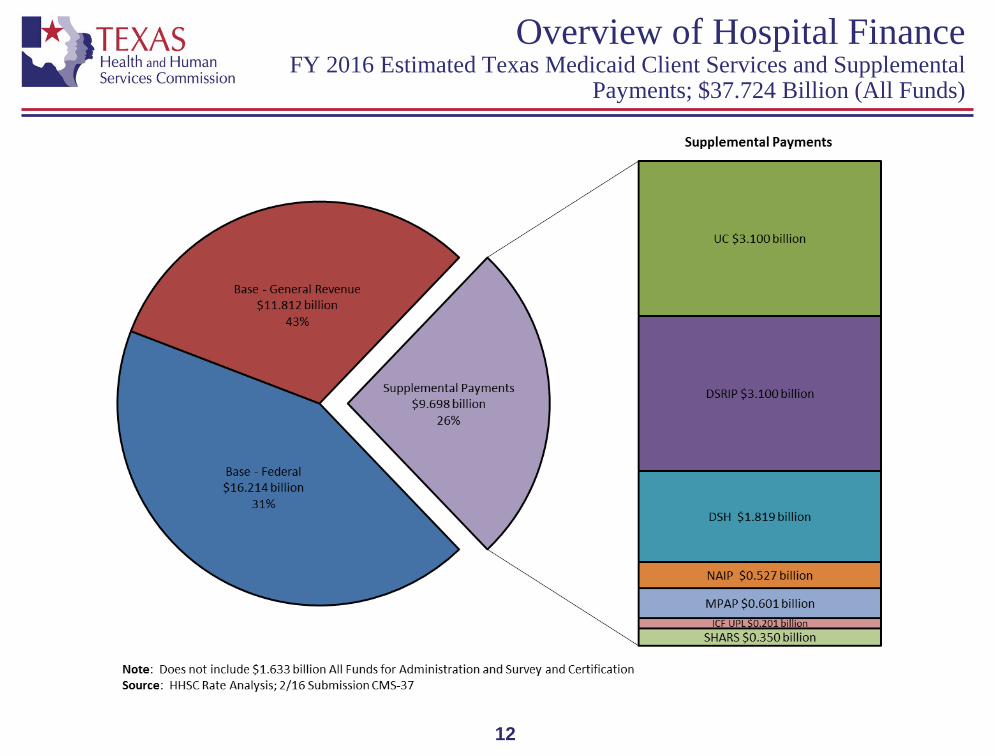

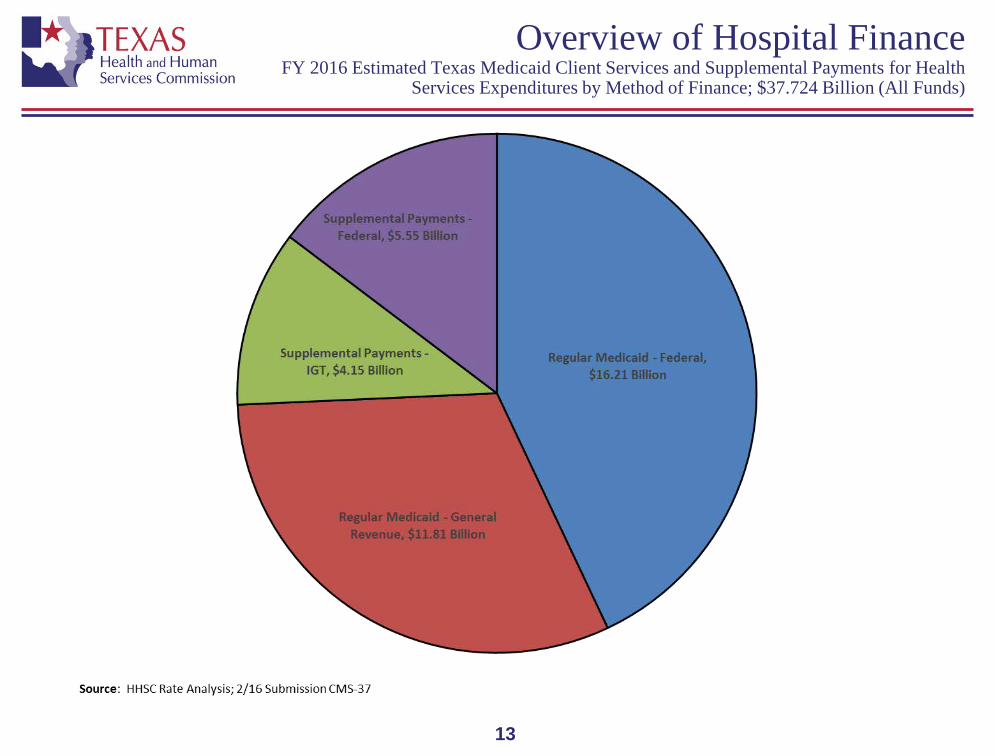

Overview of Hospital Finance FY 2016 Estimated Texas Medicaid Client Services and Supplemental

Payments; $37.724 Billion (All Funds)

13

Overview of Hospital Finance FY 2016 Estimated Texas Medicaid Client Services and Supplemental Payments for Health

Services Expenditures by Method of Finance; $37.724 Billion (All Funds)

14

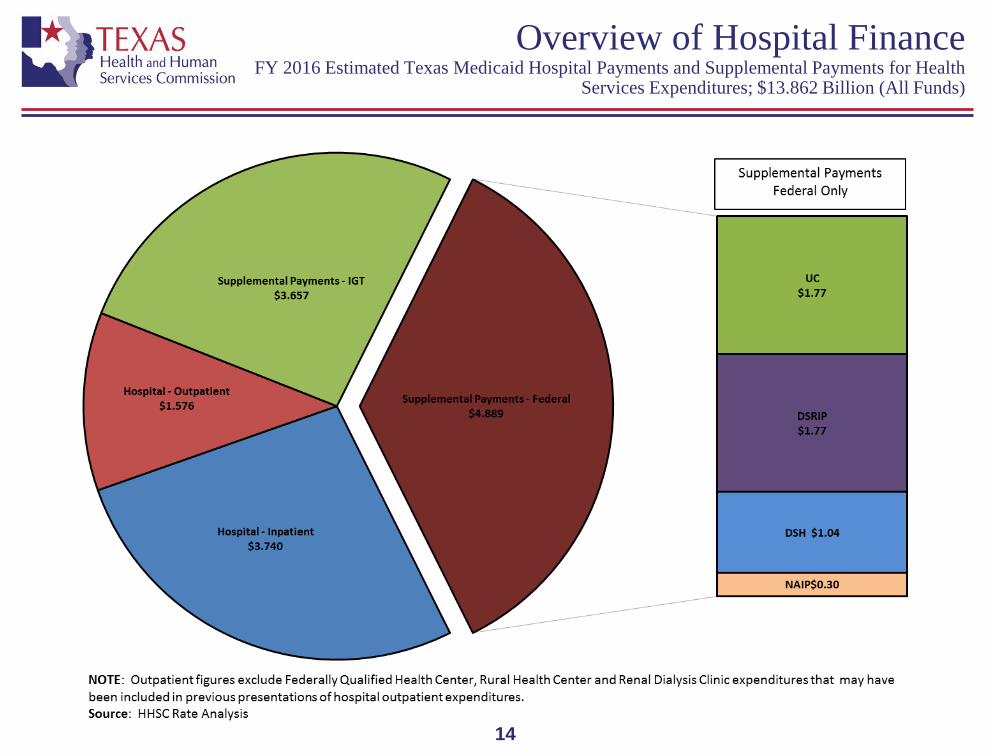

Overview of Hospital Finance FY 2016 Estimated Texas Medicaid Hospital Payments and Supplemental Payments for Health

Services Expenditures; $13.862 Billion (All Funds)

15

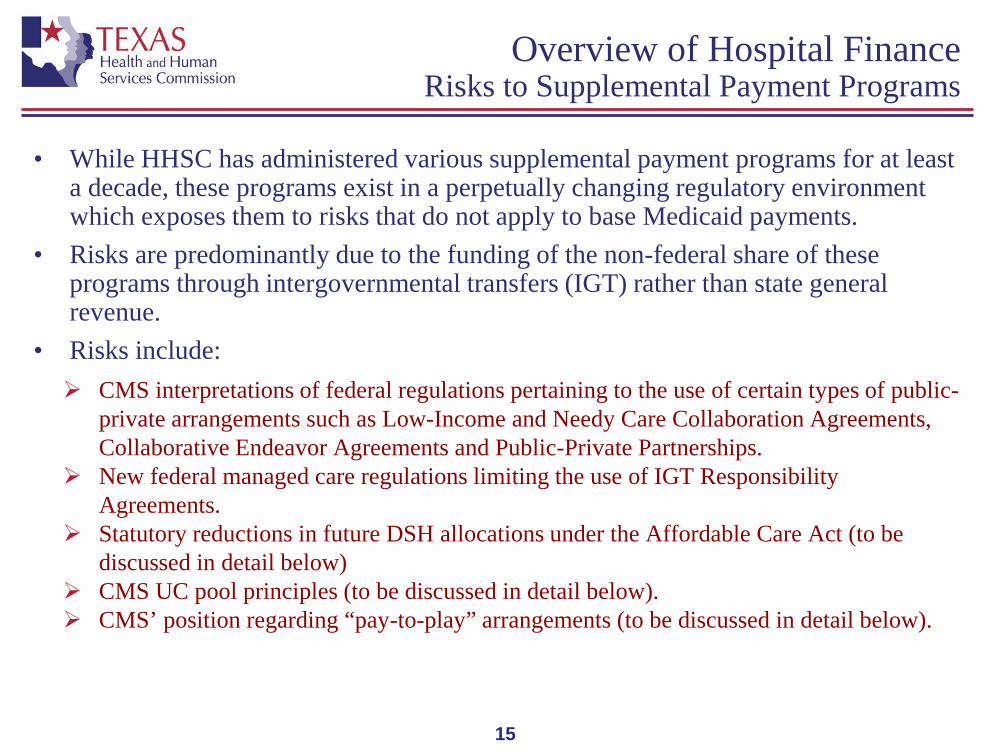

Overview of Hospital Finance Risks to Supplemental Payment Programs

• While HHSC has administered various supplemental payment programs for at least a decade, these programs exist in a perpetually changing regulatory environment which exposes them to risks that do not apply to base Medicaid payments.

• Risks are predominantly due to the funding of the non-federal share of these programs through intergovernmental transfers (IGT) rather than state general revenue.

• Risks include: CMS interpretations of federal regulations pertaining to the use of certain types of public-

private arrangements such as Low-Income and Needy Care Collaboration Agreements, Collaborative Endeavor Agreements and Public-Private Partnerships.

New federal managed care regulations limiting the use of IGT Responsibility Agreements.

Statutory reductions in future DSH allocations under the Affordable Care Act (to be discussed in detail below)

CMS UC pool principles (to be discussed in detail below). CMS’ position regarding “pay-to-play” arrangements (to be discussed in detail below).

16

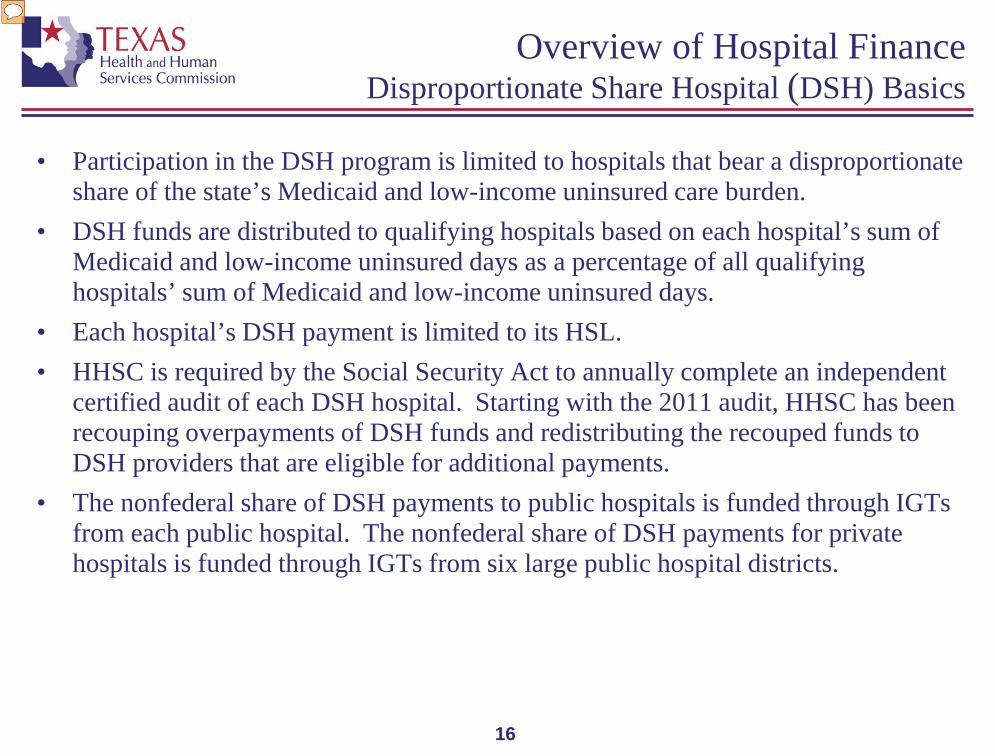

Overview of Hospital Finance Disproportionate Share Hospital (DSH) Basics

• Participation in the DSH program is limited to hospitals that bear a disproportionate share of the state’s Medicaid and low-income uninsured care burden.

• DSH funds are distributed to qualifying hospitals based on each hospital’s sum of Medicaid and low-income uninsured days as a percentage of all qualifying hospitals’ sum of Medicaid and low-income uninsured days.

• Each hospital’s DSH payment is limited to its HSL. • HHSC is required by the Social Security Act to annually complete an independent

certified audit of each DSH hospital. Starting with the 2011 audit, HHSC has been recouping overpayments of DSH funds and redistributing the recouped funds to DSH providers that are eligible for additional payments.

• The nonfederal share of DSH payments to public hospitals is funded through IGTs from each public hospital. The nonfederal share of DSH payments for private hospitals is funded through IGTs from six large public hospital districts.

17

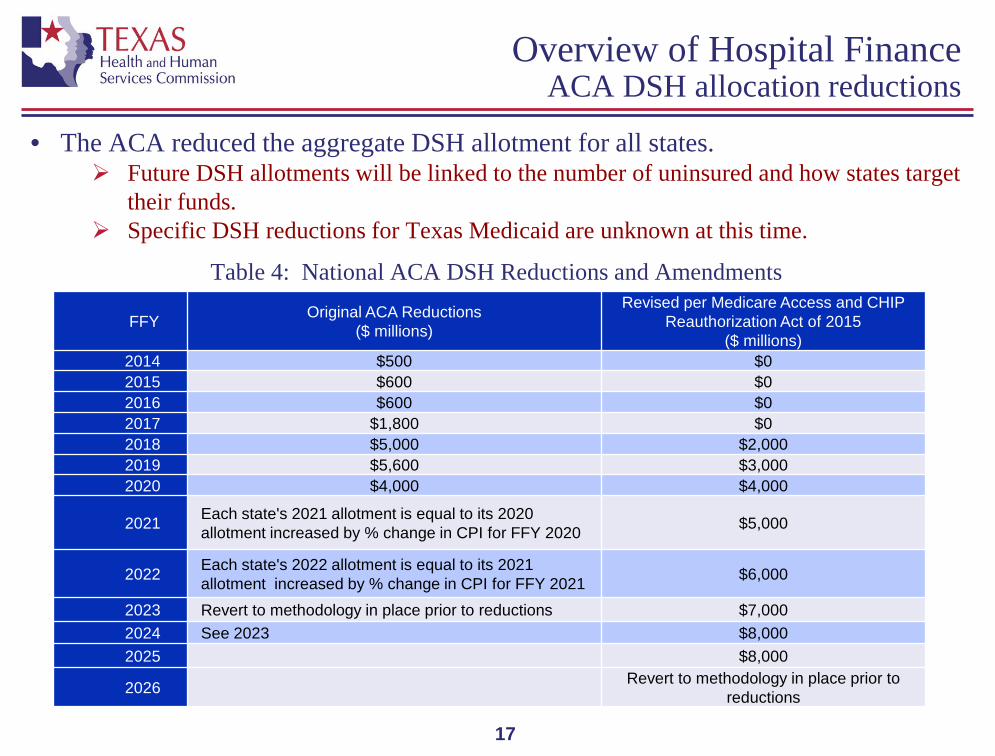

Overview of Hospital Finance ACA DSH allocation reductions

• The ACA reduced the aggregate DSH allotment for all states.

Future DSH allotments will be linked to the number of uninsured and how states target their funds.

Specific DSH reductions for Texas Medicaid are unknown at this time.

Table 4: National ACA DSH Reductions and Amendments

FFY Original ACA Reductions ($ millions)

Revised per Medicare Access and CHIP Reauthorization Act of 2015

($ millions) 2014 $500 $0 2015 $600 $0 2016 $600 $0 2017 $1,800 $0 2018 $5,000 $2,000 2019 $5,600 $3,000 2020 $4,000 $4,000

2021 Each state's 2021 allotment is equal to its 2020 allotment increased by % change in CPI for FFY 2020 $5,000

2022 Each state's 2022 allotment is equal to its 2021 allotment increased by % change in CPI for FFY 2021 $6,000

2023 Revert to methodology in place prior to reductions $7,000 2024 See 2023 $8,000 2025 $8,000

2026 Revert to methodology in place prior to reductions

18

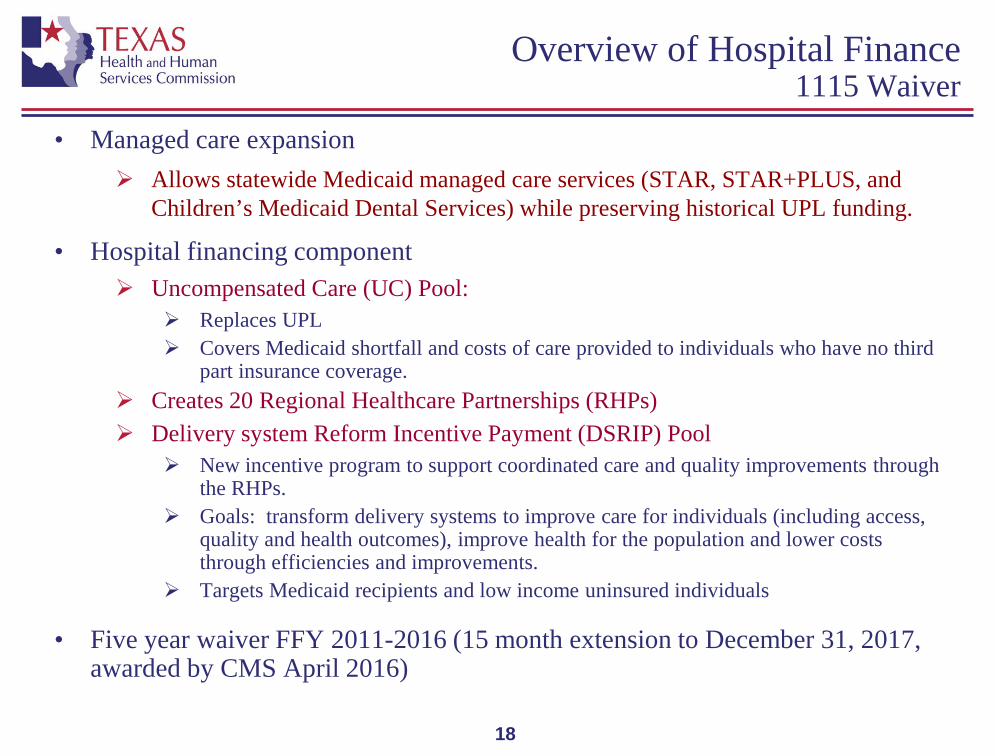

Overview of Hospital Finance 1115 Waiver

• Managed care expansion Allows statewide Medicaid managed care services (STAR, STAR+PLUS, and

Children’s Medicaid Dental Services) while preserving historical UPL funding.

• Hospital financing component Uncompensated Care (UC) Pool:

Replaces UPL Covers Medicaid shortfall and costs of care provided to individuals who have no third

part insurance coverage. Creates 20 Regional Healthcare Partnerships (RHPs) Delivery system Reform Incentive Payment (DSRIP) Pool

New incentive program to support coordinated care and quality improvements through the RHPs.

Goals: transform delivery systems to improve care for individuals (including access, quality and health outcomes), improve health for the population and lower costs through efficiencies and improvements.

Targets Medicaid recipients and low income uninsured individuals

• Five year waiver FFY 2011-2016 (15 month extension to December 31, 2017, awarded by CMS April 2016)

19

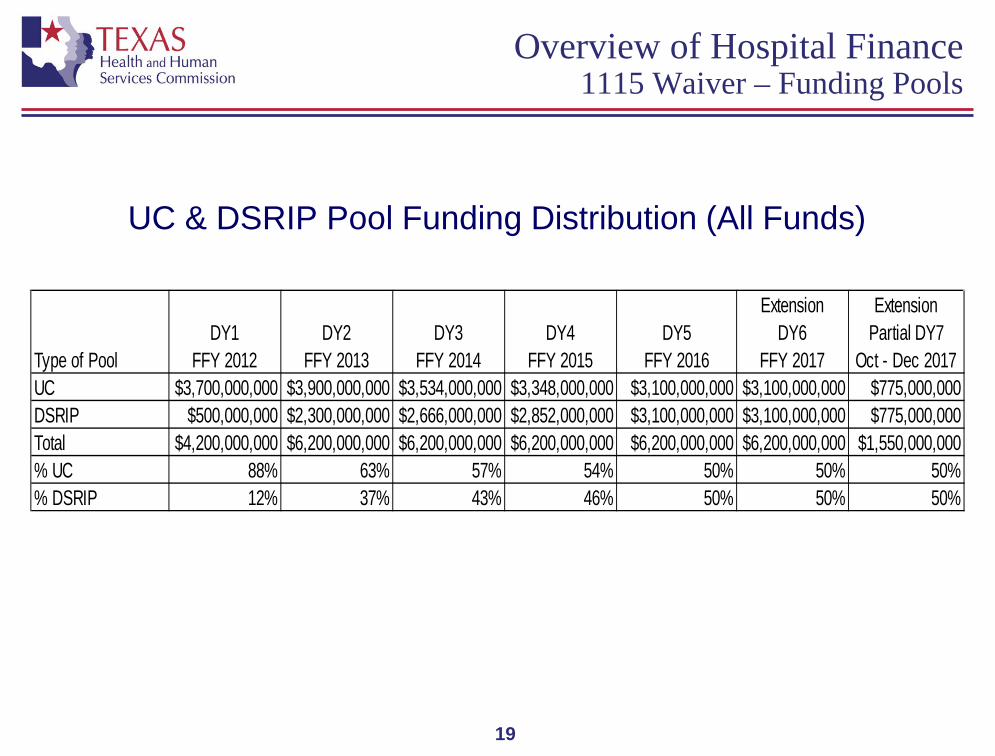

Overview of Hospital Finance 1115 Waiver – Funding Pools

UC & DSRIP Pool Funding Distribution (All Funds)

Type of PoolDY1

FFY 2012DY2

FFY 2013DY3

FFY 2014DY4

FFY 2015DY5

FFY 2016

ExtensionDY6

FFY 2017

ExtensionPartial DY7

Oct - Dec 2017UC $3,700,000,000 $3,900,000,000 $3,534,000,000 $3,348,000,000 $3,100,000,000 $3,100,000,000 $775,000,000DSRIP $500,000,000 $2,300,000,000 $2,666,000,000 $2,852,000,000 $3,100,000,000 $3,100,000,000 $775,000,000Total $4,200,000,000 $6,200,000,000 $6,200,000,000 $6,200,000,000 $6,200,000,000 $6,200,000,000 $1,550,000,000% UC 88% 63% 57% 54% 50% 50% 50%% DSRIP 12% 37% 43% 46% 50% 50% 50%

20

Overview of Hospital Finance 1115 Waiver - UC Basics

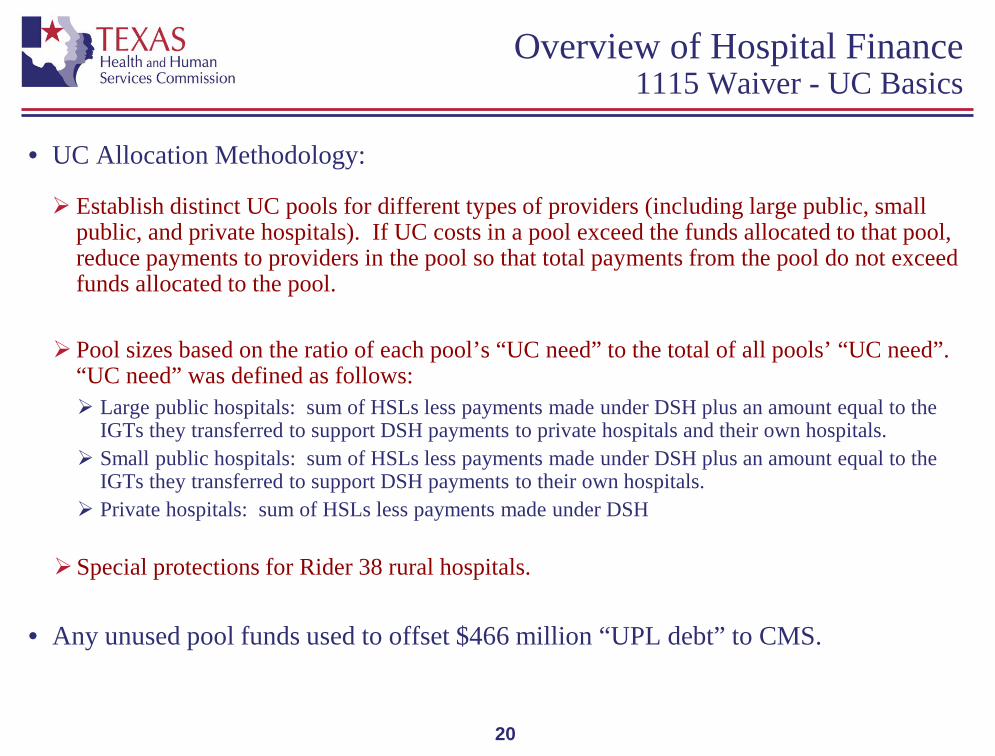

• UC Allocation Methodology:

Establish distinct UC pools for different types of providers (including large public, small public, and private hospitals). If UC costs in a pool exceed the funds allocated to that pool, reduce payments to providers in the pool so that total payments from the pool do not exceed funds allocated to the pool.

Pool sizes based on the ratio of each pool’s “UC need” to the total of all pools’ “UC need”.

“UC need” was defined as follows: Large public hospitals: sum of HSLs less payments made under DSH plus an amount equal to the

IGTs they transferred to support DSH payments to private hospitals and their own hospitals. Small public hospitals: sum of HSLs less payments made under DSH plus an amount equal to the

IGTs they transferred to support DSH payments to their own hospitals. Private hospitals: sum of HSLs less payments made under DSH

Special protections for Rider 38 rural hospitals.

• Any unused pool funds used to offset $466 million “UPL debt” to CMS.

21

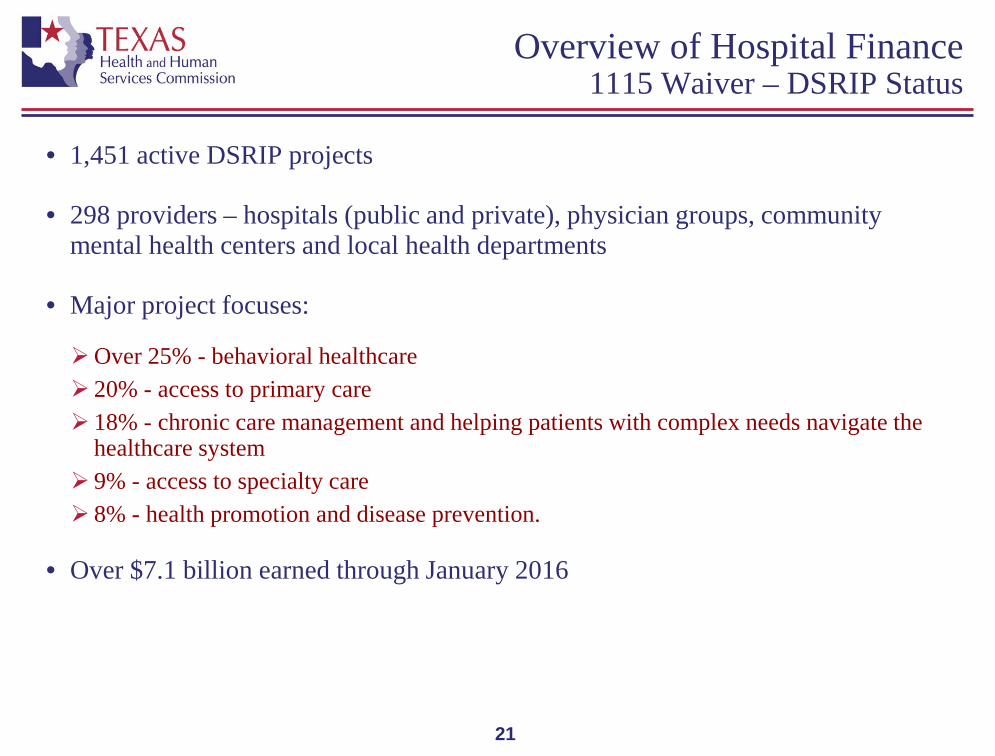

Overview of Hospital Finance 1115 Waiver – DSRIP Status

• 1,451 active DSRIP projects

• 298 providers – hospitals (public and private), physician groups, community mental health centers and local health departments

• Major project focuses:

Over 25% - behavioral healthcare 20% - access to primary care 18% - chronic care management and helping patients with complex needs navigate the

healthcare system 9% - access to specialty care 8% - health promotion and disease prevention.

• Over $7.1 billion earned through January 2016

22

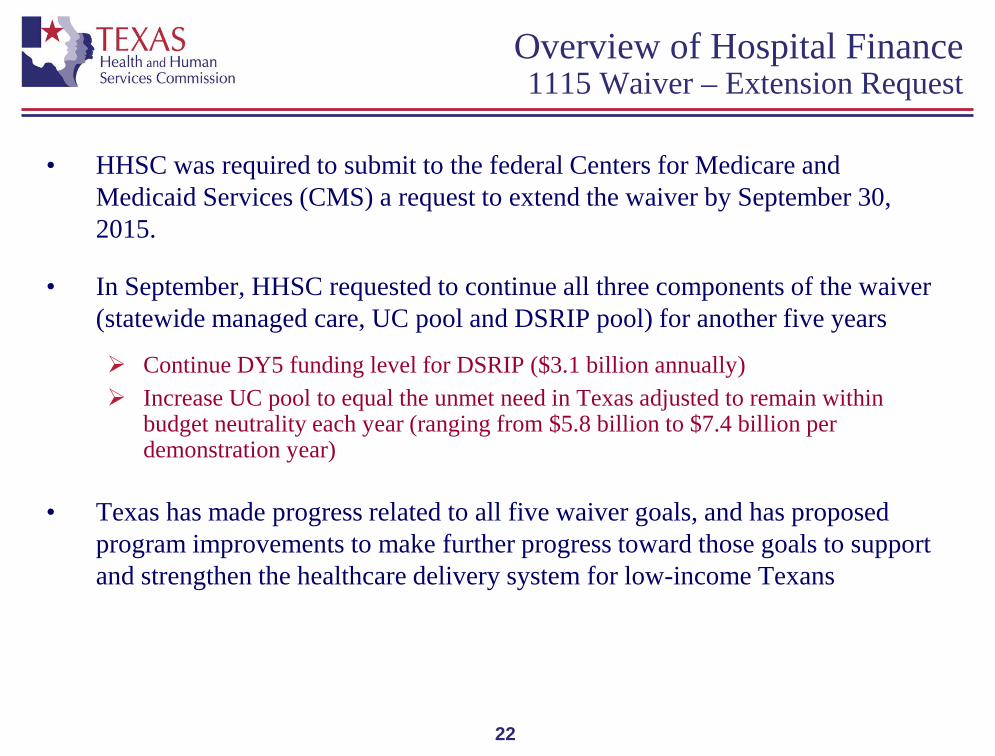

Overview of Hospital Finance 1115 Waiver – Extension Request

• HHSC was required to submit to the federal Centers for Medicare and Medicaid Services (CMS) a request to extend the waiver by September 30, 2015.

• In September, HHSC requested to continue all three components of the waiver (statewide managed care, UC pool and DSRIP pool) for another five years

Continue DY5 funding level for DSRIP ($3.1 billion annually) Increase UC pool to equal the unmet need in Texas adjusted to remain within

budget neutrality each year (ranging from $5.8 billion to $7.4 billion per demonstration year)

• Texas has made progress related to all five waiver goals, and has proposed program improvements to make further progress toward those goals to support and strengthen the healthcare delivery system for low-income Texans

23

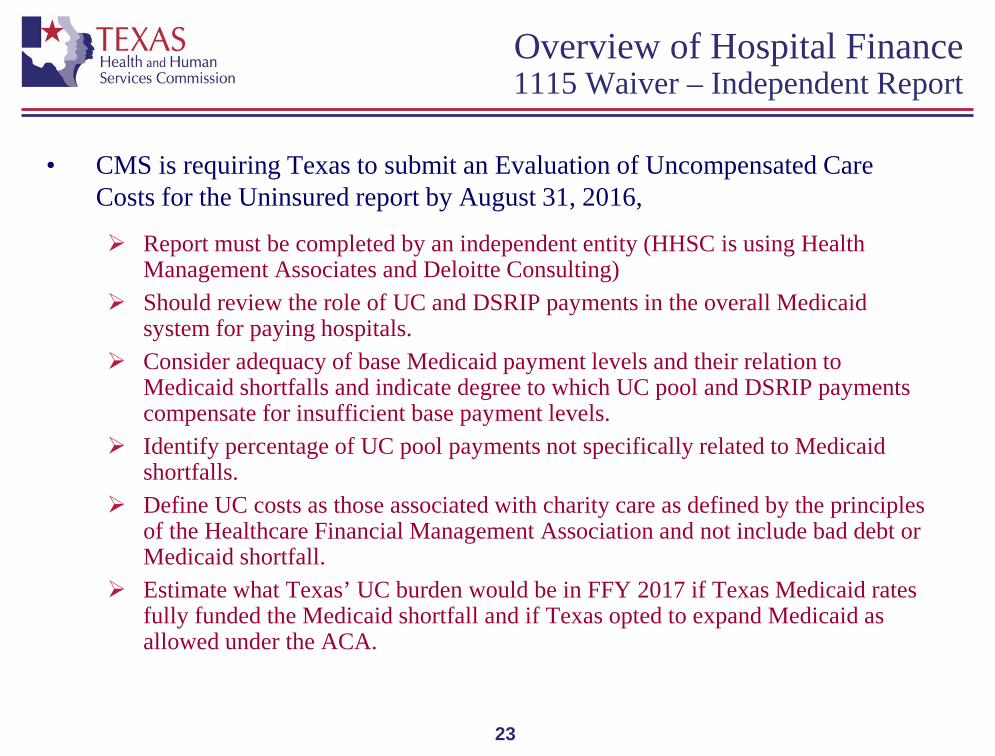

Overview of Hospital Finance 1115 Waiver – Independent Report

• CMS is requiring Texas to submit an Evaluation of Uncompensated Care Costs for the Uninsured report by August 31, 2016,

Report must be completed by an independent entity (HHSC is using Health Management Associates and Deloitte Consulting)

Should review the role of UC and DSRIP payments in the overall Medicaid system for paying hospitals.

Consider adequacy of base Medicaid payment levels and their relation to Medicaid shortfalls and indicate degree to which UC pool and DSRIP payments compensate for insufficient base payment levels.

Identify percentage of UC pool payments not specifically related to Medicaid shortfalls.

Define UC costs as those associated with charity care as defined by the principles of the Healthcare Financial Management Association and not include bad debt or Medicaid shortfall.

Estimate what Texas’ UC burden would be in FFY 2017 if Texas Medicaid rates fully funded the Medicaid shortfall and if Texas opted to expand Medicaid as allowed under the ACA.

24

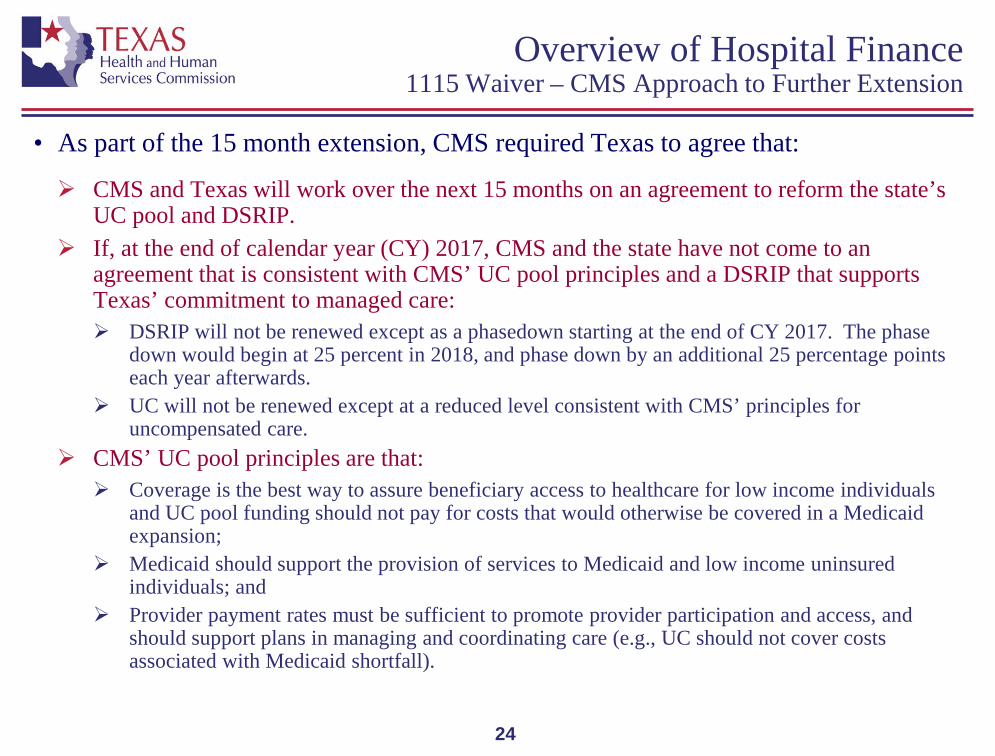

Overview of Hospital Finance 1115 Waiver – CMS Approach to Further Extension

• As part of the 15 month extension, CMS required Texas to agree that:

CMS and Texas will work over the next 15 months on an agreement to reform the state’s UC pool and DSRIP.

If, at the end of calendar year (CY) 2017, CMS and the state have not come to an agreement that is consistent with CMS’ UC pool principles and a DSRIP that supports Texas’ commitment to managed care: DSRIP will not be renewed except as a phasedown starting at the end of CY 2017. The phase

down would begin at 25 percent in 2018, and phase down by an additional 25 percentage points each year afterwards.

UC will not be renewed except at a reduced level consistent with CMS’ principles for uncompensated care.

CMS’ UC pool principles are that: Coverage is the best way to assure beneficiary access to healthcare for low income individuals

and UC pool funding should not pay for costs that would otherwise be covered in a Medicaid expansion;

Medicaid should support the provision of services to Medicaid and low income uninsured individuals; and

Provider payment rates must be sufficient to promote provider participation and access, and should support plans in managing and coordinating care (e.g., UC should not cover costs associated with Medicaid shortfall).

25

Overview of Hospital Finance 1115 Waiver – Lessons from Florida Renewal

• Florida has a Low Income Pool (LIP) that serves a similar purpose to Texas’ UC pool.

• CMS granted Florida a one year extension of its pool when it initially expired but required Florida to commission a UC study similar to the study now required of Texas and indicated that it would apply the same principles to Florida’s UC pool renewal as detailed on the previous slide.

• In June 2015, CMS and Florida agreed to extend the LIP for two years with pool size limited to projected costs of care for those uninsured individuals who would not be eligible for Medicaid coverage if Florida had expanded Medicaid, whether or not Florida actual expands Medicaid.

• Final LIP pool size is $1 billion for July 2015 – June 2016 and $608 million for July 2016 – June 2017.

26

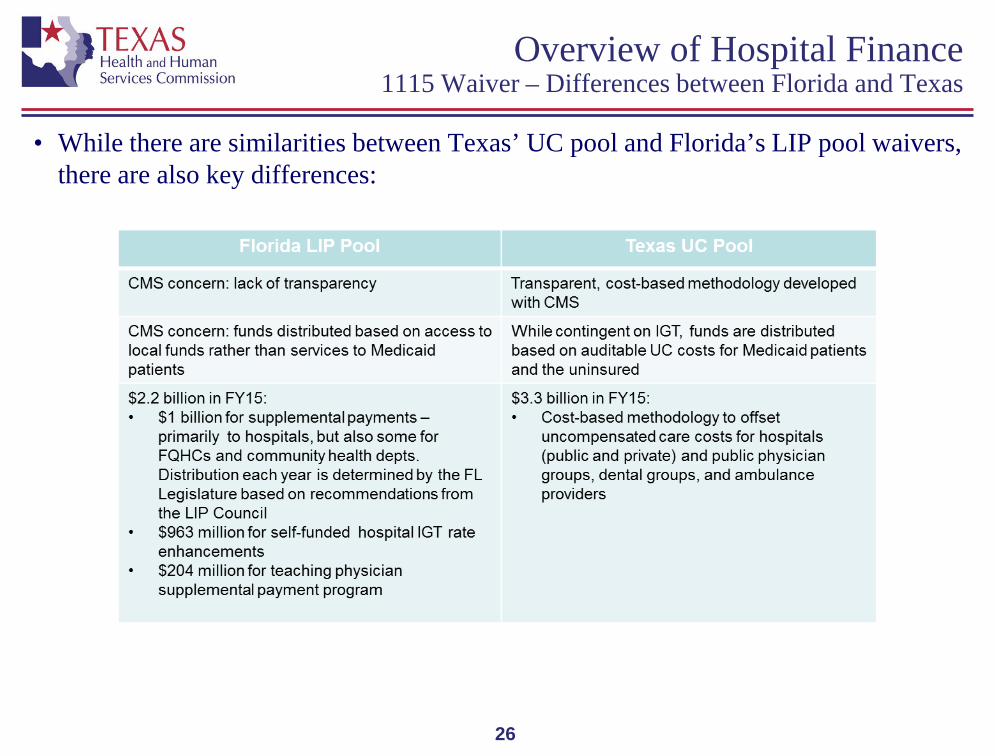

Overview of Hospital Finance 1115 Waiver – Differences between Florida and Texas

• While there are similarities between Texas’ UC pool and Florida’s LIP pool waivers, there are also key differences:

27

Overview of Hospital Finance Nursing Facility Minimum Payment Amounts Program (MPAP)

• While not specifically a hospital program, public hospital districts and authorities that own nursing facilities (NFs) benefit from MPAP.

MPAP has existed since NFs were carved in to managed care on March 1, 2015. 279 publically owned NFs will receive $601 million in MPAP for FY 2016 Since the implementation of the precursor program NF UPL in October, 2013, the number

of publically owned NFs has grown from about 20 to 279. Most MPAP NFs are owned by small public hospital districts but Dallas County Hospital

District and Bexar County Hospital District also participate. In an April 2016, letter to HHSC, CMS indicated that it would not approve the

continuation of the MPAP beyond August 31, 2016 because: HHSC requires MPAP NFs to enter into an agreement to provide an IGT to fund the non-federal

share of the MPAP. MPAP payments are only made to NFs that have entered into such an agreement, making the

funding contingent upon the IGTs. This funding arrangement represents a stipulation on provider payments which violates section

1902(a)(2) of the Social Security Act and 42 Code of Regulations 433.53(c)(2). HHSC requested an extension of MPAP through August 2017 (at which time HHSC

expects to implement a compliant replacement program), CMS denied this request.

Hospital Financing Overview

45.6%Salaries and

benefits29.2%

Other

18.1%Supplies

5.6%Depreciation

1.5%Interest

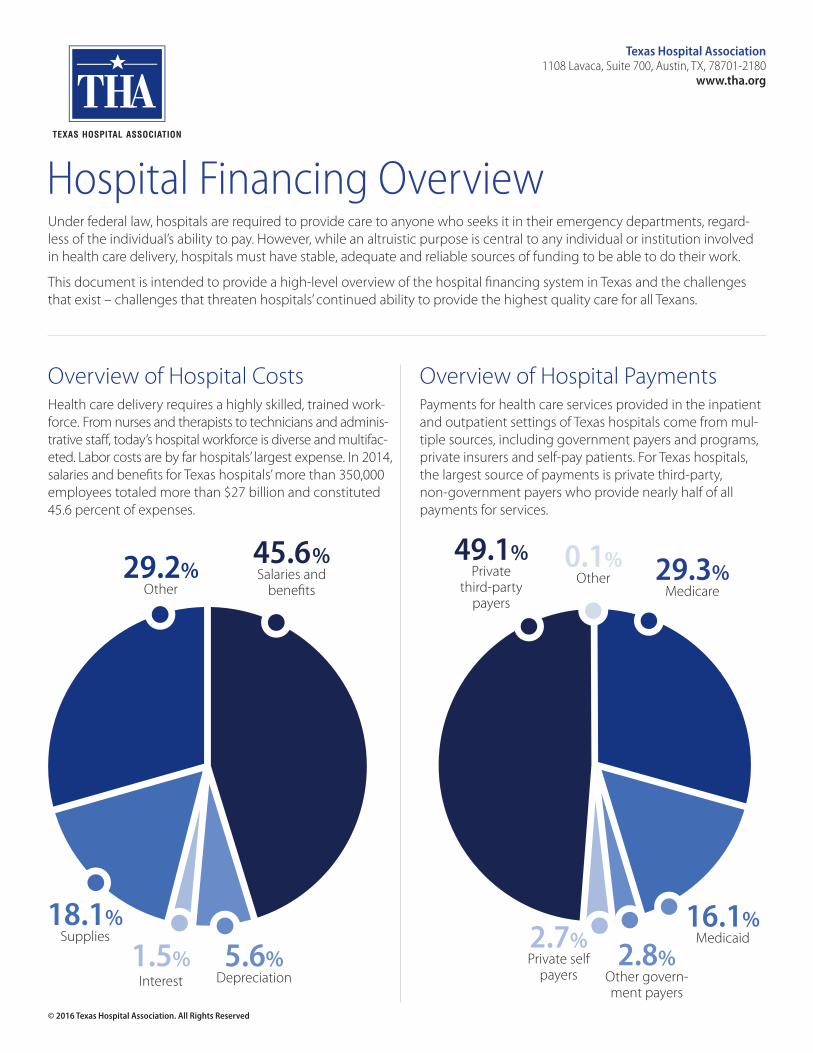

Under federal law, hospitals are required to provide care to anyone who seeks it in their emergency departments, regard-less of the individual’s ability to pay. However, while an altruistic purpose is central to any individual or institution involved in health care delivery, hospitals must have stable, adequate and reliable sources of funding to be able to do their work.

This document is intended to provide a high-level overview of the hospital financing system in Texas and the challenges that exist – challenges that threaten hospitals’ continued ability to provide the highest quality care for all Texans.

Overview of Hospital CostsHealth care delivery requires a highly skilled, trained work-force. From nurses and therapists to technicians and adminis-trative staff, today’s hospital workforce is diverse and multifac-eted. Labor costs are by far hospitals’ largest expense. In 2014, salaries and benefits for Texas hospitals’ more than 350,000 employees totaled more than $27 billion and constituted 45.6 percent of expenses.

Overview of Hospital PaymentsPayments for health care services provided in the inpatient and outpatient settings of Texas hospitals come from mul-tiple sources, including government payers and programs, private insurers and self-pay patients. For Texas hospitals, the largest source of payments is private third-party, non-government payers who provide nearly half of all payments for services.

49.1%Private

third-party payers

29.3%Medicare

16.1%Medicaid

2.8%Other govern-ment payers

2.7%Private self

payers

0.1%Other

Texas Hospital Association1108 Lavaca, Suite 700, Austin, TX, 78701-2180

www.tha.org

© 2016 Texas Hospital Association. All Rights Reserved

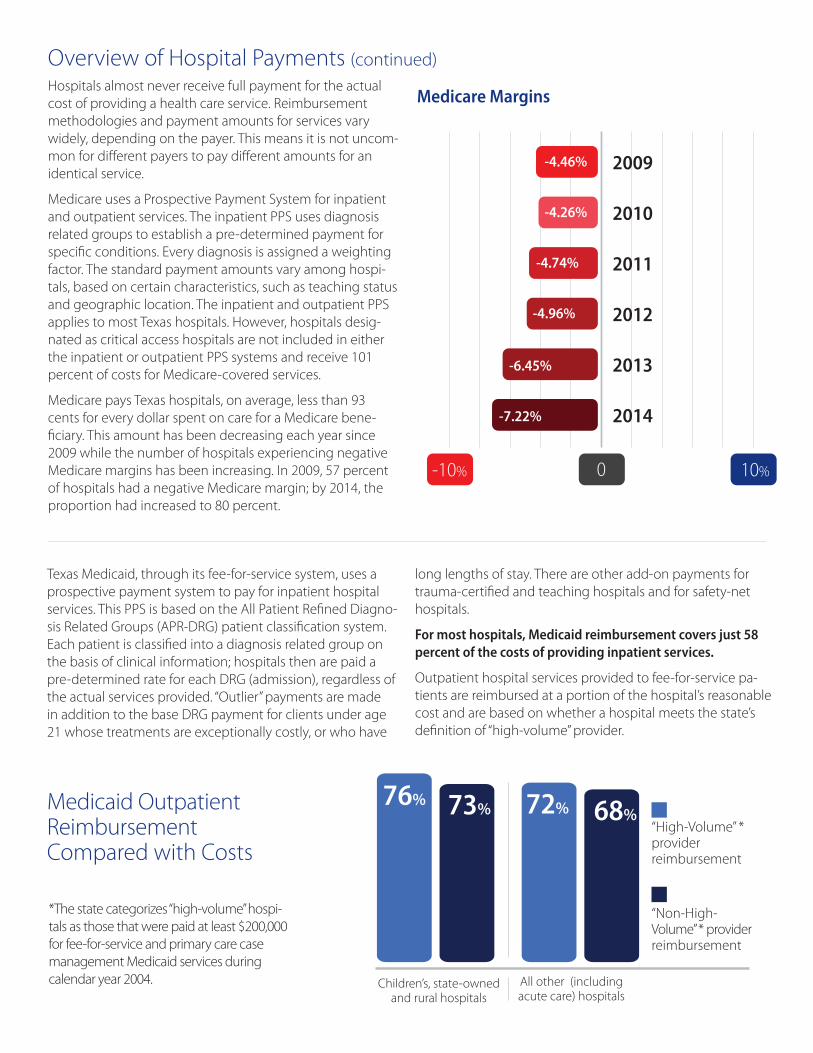

Hospitals almost never receive full payment for the actual cost of providing a health care service. Reimbursement methodologies and payment amounts for services vary widely, depending on the payer. This means it is not uncom-mon for different payers to pay different amounts for an identical service.

Medicare uses a Prospective Payment System for inpatient and outpatient services. The inpatient PPS uses diagnosis related groups to establish a pre-determined payment for specific conditions. Every diagnosis is assigned a weighting factor. The standard payment amounts vary among hospi-tals, based on certain characteristics, such as teaching status and geographic location. The inpatient and outpatient PPS applies to most Texas hospitals. However, hospitals desig-nated as critical access hospitals are not included in either the inpatient or outpatient PPS systems and receive 101 percent of costs for Medicare-covered services.

Medicare pays Texas hospitals, on average, less than 93 cents for every dollar spent on care for a Medicare bene-ficiary. This amount has been decreasing each year since 2009 while the number of hospitals experiencing negative Medicare margins has been increasing. In 2009, 57 percent of hospitals had a negative Medicare margin; by 2014, the proportion had increased to 80 percent.

0 10%-10%

-7.22%

-6.45%

-4.96%

-4.74%

-4.26%

-4.46% 2009

2010

2011

2012

2013

2014

Overview of Hospital Payments (continued)

Medicare Margins

Texas Medicaid, through its fee-for-service system, uses a prospective payment system to pay for inpatient hospital services. This PPS is based on the All Patient Refined Diagno-sis Related Groups (APR-DRG) patient classification system. Each patient is classified into a diagnosis related group on the basis of clinical information; hospitals then are paid a pre-determined rate for each DRG (admission), regardless of the actual services provided. “Outlier” payments are made in addition to the base DRG payment for clients under age 21 whose treatments are exceptionally costly, or who have

“High-Volume” * provider reimbursement

76% 73% 72% 68%

Children’s, state-owned and rural hospitals

All other (including acute care) hospitals

Medicaid Outpatient Reimbursement Compared with Costs

*The state categorizes “high-volume” hospi-tals as those that were paid at least $200,000 for fee-for-service and primary care case management Medicaid services during calendar year 2004.

“Non-High- Volume” * provider reimbursement

long lengths of stay. There are other add-on payments for trauma-certified and teaching hospitals and for safety-net hospitals.

For most hospitals, Medicaid reimbursement covers just 58 percent of the costs of providing inpatient services.

Outpatient hospital services provided to fee-for-service pa-tients are reimbursed at a portion of the hospital’s reasonable cost and are based on whether a hospital meets the state’s definition of “high-volume” provider.

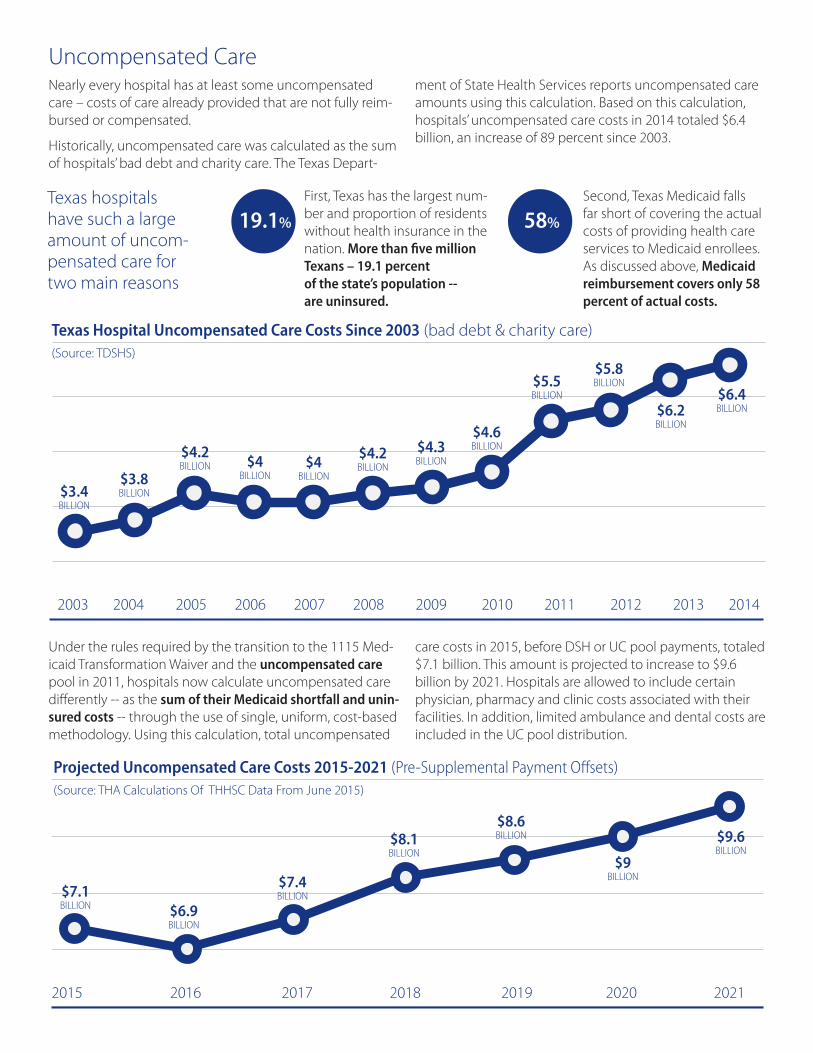

Uncompensated CareNearly every hospital has at least some uncompensated care – costs of care already provided that are not fully reim-bursed or compensated.

Historically, uncompensated care was calculated as the sum of hospitals’ bad debt and charity care. The Texas Depart-

Under the rules required by the transition to the 1115 Med-icaid Transformation Waiver and the uncompensated care pool in 2011, hospitals now calculate uncompensated care differently -- as the sum of their Medicaid shortfall and unin-sured costs -- through the use of single, uniform, cost-based methodology. Using this calculation, total uncompensated

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

$3.4 BILLION

$3.8 BILLION

$4.2 BILLION $4

BILLION$4

BILLION

$4.2 BILLION

$4.3 BILLION

$4.6 BILLION

$5.5 BILLION

$5.8 BILLION

$6.2 BILLION

$6.4 BILLION

Texas Hospital Uncompensated Care Costs Since 2003 (bad debt & charity care)(Source: TDSHS)

Texas hospitals have such a large amount of uncom-pensated care for two main reasons

First, Texas has the largest num-ber and proportion of residents without health insurance in the nation. More than five million Texans – 19.1 percent of the state’s population -- are uninsured.

Second, Texas Medicaid falls far short of covering the actual costs of providing health care services to Medicaid enrollees. As discussed above, Medicaid reimbursement covers only 58 percent of actual costs.

ment of State Health Services reports uncompensated care amounts using this calculation. Based on this calculation, hospitals’ uncompensated care costs in 2014 totaled $6.4 billion, an increase of 89 percent since 2003.

care costs in 2015, before DSH or UC pool payments, totaled $7.1 billion. This amount is projected to increase to $9.6 billion by 2021. Hospitals are allowed to include certain physician, pharmacy and clinic costs associated with their facilities. In addition, limited ambulance and dental costs are included in the UC pool distribution.

2015 2016 2017 2018 2019 2020 2021

$7.1 BILLION $6.9

BILLION

$7.4 BILLION

$8.1 BILLION

$8.6 BILLION

$9 BILLION

$9.6 BILLION

Projected Uncompensated Care Costs 2015-2021 (Pre-Supplemental Payment Offsets)(Source: THA Calculations Of THHSC Data From June 2015)

19.1% 58%

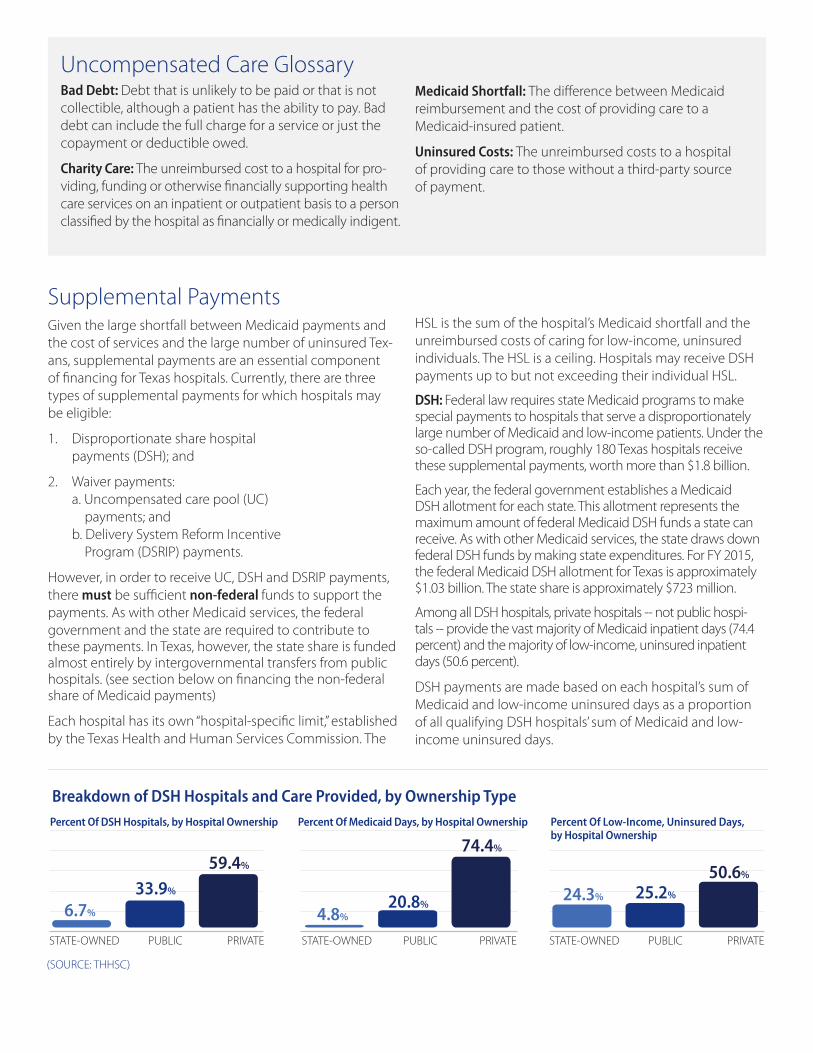

Supplemental PaymentsGiven the large shortfall between Medicaid payments and the cost of services and the large number of uninsured Tex-ans, supplemental payments are an essential component of financing for Texas hospitals. Currently, there are three types of supplemental payments for which hospitals may be eligible:

1. Disproportionate share hospital payments (DSH); and

2. Waiver payments: a. Uncompensated care pool (UC) payments; and b. Delivery System Reform Incentive Program (DSRIP) payments.

However, in order to receive UC, DSH and DSRIP payments, there must be sufficient non-federal funds to support the payments. As with other Medicaid services, the federal government and the state are required to contribute to these payments. In Texas, however, the state share is funded almost entirely by intergovernmental transfers from public hospitals. (see section below on financing the non-federal share of Medicaid payments)

Each hospital has its own “hospital-specific limit,” established by the Texas Health and Human Services Commission. The

Percent Of DSH Hospitals, by Hospital Ownership

STATE-OWNED PUBLIC PRIVATE

Percent Of Medicaid Days, by Hospital Ownership

STATE-OWNED PUBLIC PRIVATE

Percent Of Low-Income, Uninsured Days, by Hospital Ownership

STATE-OWNED PUBLIC PRIVATE

24.3% 25.2%

50.6%

6.7%

33.9%

59.4%

4.8%20.8%

74.4%

Uncompensated Care GlossaryBad Debt: Debt that is unlikely to be paid or that is not collectible, although a patient has the ability to pay. Bad debt can include the full charge for a service or just the copayment or deductible owed.

Charity Care: The unreimbursed cost to a hospital for pro-viding, funding or otherwise financially supporting health care services on an inpatient or outpatient basis to a person classified by the hospital as financially or medically indigent.

Medicaid Shortfall: The difference between Medicaid reimbursement and the cost of providing care to a Medicaid-insured patient.

Uninsured Costs: The unreimbursed costs to a hospital of providing care to those without a third-party source of payment.

HSL is the sum of the hospital’s Medicaid shortfall and the unreimbursed costs of caring for low-income, uninsured individuals. The HSL is a ceiling. Hospitals may receive DSH payments up to but not exceeding their individual HSL.

DSH: Federal law requires state Medicaid programs to make special payments to hospitals that serve a disproportionately large number of Medicaid and low-income patients. Under the so-called DSH program, roughly 180 Texas hospitals receive these supplemental payments, worth more than $1.8 billion.

Each year, the federal government establishes a Medicaid DSH allotment for each state. This allotment represents the maximum amount of federal Medicaid DSH funds a state can receive. As with other Medicaid services, the state draws down federal DSH funds by making state expenditures. For FY 2015, the federal Medicaid DSH allotment for Texas is approximately $1.03 billion. The state share is approximately $723 million.

Among all DSH hospitals, private hospitals -- not public hospi-tals -- provide the vast majority of Medicaid inpatient days (74.4 percent) and the majority of low-income, uninsured inpatient days (50.6 percent).

DSH payments are made based on each hospital’s sum of Medicaid and low-income uninsured days as a proportion of all qualifying DSH hospitals’ sum of Medicaid and low- income uninsured days.

(SOURCE: THHSC)

Breakdown of DSH Hospitals and Care Provided, by Ownership Type

2014 2015 2016 2017 2018 2019 2020 2021

Uncompensated Care Costs vs. Available Supplemental Payments*

(Source: THA Calculations Of THHSC Data from June 2015)

*assumes no UC payments through the waiver after 2017UC costs Supplemental Payments (DSH and UC) Difference between cost and payments

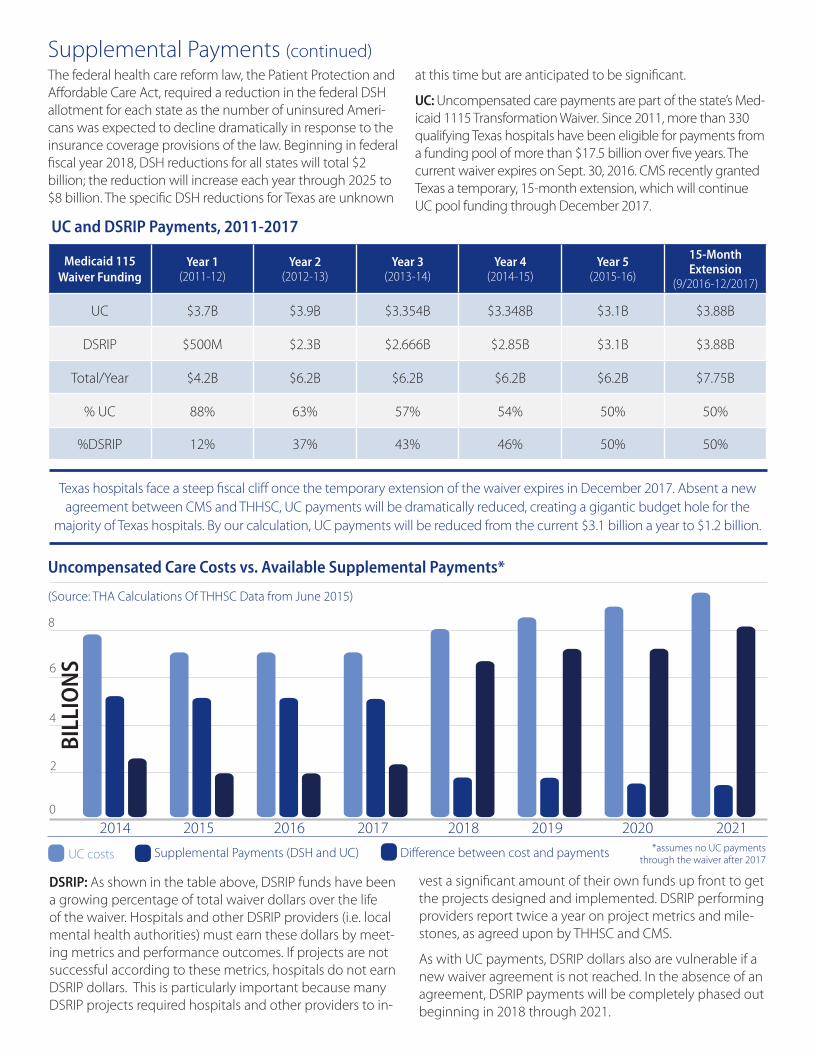

The federal health care reform law, the Patient Protection and Affordable Care Act, required a reduction in the federal DSH allotment for each state as the number of uninsured Ameri-cans was expected to decline dramatically in response to the insurance coverage provisions of the law. Beginning in federal fiscal year 2018, DSH reductions for all states will total $2 billion; the reduction will increase each year through 2025 to $8 billion. The specific DSH reductions for Texas are unknown

Supplemental Payments (continued)at this time but are anticipated to be significant.

UC: Uncompensated care payments are part of the state’s Med-icaid 1115 Transformation Waiver. Since 2011, more than 330 qualifying Texas hospitals have been eligible for payments from a funding pool of more than $17.5 billion over five years. The current waiver expires on Sept. 30, 2016. CMS recently granted Texas a temporary, 15-month extension, which will continue UC pool funding through December 2017.

Medicaid 115Waiver Funding

Year 1 (2011-12)

Year 2 (2012-13)

Year 3 (2013-14)

Year 4 (2014-15)

Year 5 (2015-16)

15-Month Extension

(9/2016-12/2017)

UC $3.7B $3.9B $3.354B $3.348B $3.1B $3.88B

DSRIP $500M $2.3B $2.666B $2.85B $3.1B $3.88B

Total/Year $4.2B $6.2B $6.2B $6.2B $6.2B $7.75B

% UC 88% 63% 57% 54% 50% 50%

%DSRIP 12% 37% 43% 46% 50% 50%

Texas hospitals face a steep fiscal cliff once the temporary extension of the waiver expires in December 2017. Absent a new agreement between CMS and THHSC, UC payments will be dramatically reduced, creating a gigantic budget hole for the

majority of Texas hospitals. By our calculation, UC payments will be reduced from the current $3.1 billion a year to $1.2 billion.

DSRIP: As shown in the table above, DSRIP funds have been a growing percentage of total waiver dollars over the life of the waiver. Hospitals and other DSRIP providers (i.e. local mental health authorities) must earn these dollars by meet-ing metrics and performance outcomes. If projects are not successful according to these metrics, hospitals do not earn DSRIP dollars. This is particularly important because many DSRIP projects required hospitals and other providers to in-

vest a significant amount of their own funds up front to get the projects designed and implemented. DSRIP performing providers report twice a year on project metrics and mile-stones, as agreed upon by THHSC and CMS.

As with UC payments, DSRIP dollars also are vulnerable if a new waiver agreement is not reached. In the absence of an agreement, DSRIP payments will be completely phased out beginning in 2018 through 2021.

0

8

6

4

2

UC and DSRIP Payments, 2011-2017

BILL

ION

S

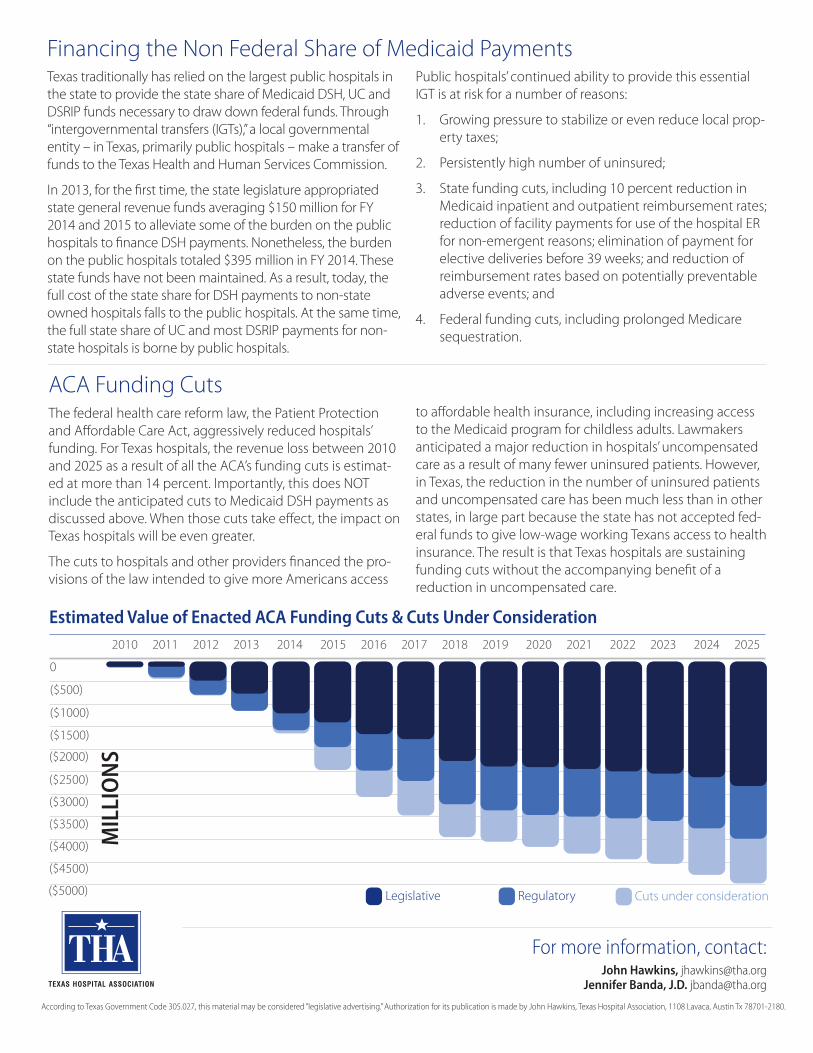

Texas traditionally has relied on the largest public hospitals in the state to provide the state share of Medicaid DSH, UC and DSRIP funds necessary to draw down federal funds. Through “intergovernmental transfers (IGTs),” a local governmental entity – in Texas, primarily public hospitals – make a transfer of funds to the Texas Health and Human Services Commission.

In 2013, for the first time, the state legislature appropriated state general revenue funds averaging $150 million for FY 2014 and 2015 to alleviate some of the burden on the public hospitals to finance DSH payments. Nonetheless, the burden on the public hospitals totaled $395 million in FY 2014. These state funds have not been maintained. As a result, today, the full cost of the state share for DSH payments to non-state owned hospitals falls to the public hospitals. At the same time, the full state share of UC and most DSRIP payments for non-state hospitals is borne by public hospitals.

Public hospitals’ continued ability to provide this essential IGT is at risk for a number of reasons:

1. Growing pressure to stabilize or even reduce local prop-erty taxes;

2. Persistently high number of uninsured;

3. State funding cuts, including 10 percent reduction in Medicaid inpatient and outpatient reimbursement rates; reduction of facility payments for use of the hospital ER for non-emergent reasons; elimination of payment for elective deliveries before 39 weeks; and reduction of reimbursement rates based on potentially preventable adverse events; and

4. Federal funding cuts, including prolonged Medicare sequestration.

ACA Funding CutsThe federal health care reform law, the Patient Protection and Affordable Care Act, aggressively reduced hospitals’ funding. For Texas hospitals, the revenue loss between 2010 and 2025 as a result of all the ACA’s funding cuts is estimat-ed at more than 14 percent. Importantly, this does NOT include the anticipated cuts to Medicaid DSH payments as discussed above. When those cuts take effect, the impact on Texas hospitals will be even greater.

The cuts to hospitals and other providers financed the pro-visions of the law intended to give more Americans access

Financing the Non Federal Share of Medicaid Payments

Estimated Value of Enacted ACA Funding Cuts & Cuts Under Consideration

0

($500)

($1000)

($1500)

($2000)

($2500)

($3000)

($3500)

($4000)

($4500)

($5000)

MIL

LIO

NS

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Cuts under considerationRegulatoryLegislative

to affordable health insurance, including increasing access to the Medicaid program for childless adults. Lawmakers anticipated a major reduction in hospitals’ uncompensated care as a result of many fewer uninsured patients. However, in Texas, the reduction in the number of uninsured patients and uncompensated care has been much less than in other states, in large part because the state has not accepted fed-eral funds to give low-wage working Texans access to health insurance. The result is that Texas hospitals are sustaining funding cuts without the accompanying benefit of a reduction in uncompensated care.

For more information, contact:John Hawkins, [email protected]

Jennifer Banda, J.D. [email protected]

According to Texas Government Code 305.027, this material may be considered “legislative advertising.” Authorization for its publication is made by John Hawkins, Texas Hospital Association, 1108 Lavaca, Austin Tx 78701-2180.

1

Testimony for House Appropriations Art. II Sub-Committee Hearing

Charge: Texas Healthcare Transformation and Quality Improvement Program 1115 Waiver (Invited Testimony July 13th, 2016. Dr. Fred Cerise, THOT Chair, President & CEO of

Parkland Health and Hospital System). Who we are

• While only representing about five percent of Texas’ hospitals and 16% of patient days, THOT members provide 23% of Medicaid care; 36% of the hospital care provided to uninsured Texans; almost two-thirds of Level 1 Trauma care; and about two-thirds of hospital based Graduate Medical Education residencies. THOT members comprise 11 of the 20 waiver anchors; provide significant outpatient care; and provide the bulk of the state match for the waivers’ billions in healthcare investments for Texas providers (See Appendix Chart 1).

Thank you - Increased funding in 16-17

• Thank you for Trauma SDA Add On funding increase from payments of about $87M of $300 trauma UC to about $180M (See Appendix Chart 2). We are particularly grateful since THOT’s members provide nearly half of Texas’ uncompensated trauma care.

• Thank you also for the Safety Net Add On which brought safety net funding for hospitals

and systems that provide care to low income Texans to $135M all funds per year for the biennium. While the prior session’s $300 million General Revenue support for DSH was not continued, the trauma and safety net add on payments helped to offset part of that discontinuation.

• To better target scarce state funds consistent with legislative language, we recommend that

moving forward, safety net funding be distributed based on providers’ share of both Medicaid and uninsured care provided. Under the current distribution methodology, providers serving a significant share of uninsured Texans are disadvantaged. For providers with thin margins, these funds make a difference in providing care or cutting services. (Page 2 of the detailed testimony provides an illustration.)

Emerging Financial Challenges Texas’ 1115 Waiver Renewal • We are thankful and appreciative of HHSC’s successful 15-month waiver extension at

current funding levels. The extension provides short term stability and certainty.

THOT members shared commitments include: Supporting access to care for all in our communities, with a special focus on

vulnerable populations; Providing and coordinating essential community health services, such as

trauma and disaster management; and Preparing for the future by training tomorrow’s healthcare providers and

supporting clinical and health delivery system research and transformation.

2

• Waiver funding of $6 billion per year represents an important and significant share of all Texas Medicaid hospital payments: about 40% in 2013. With a matching rate of 44% county funds (transferred to the state) and 56% federal funds that’s about 3.5 billion a year in federal funds and 2.7 billion in local funding. (As you know, state match for the bulk of the 1115 Waiver is funded with local property taxes and IGT funding from health related institutions, local mental health authorities, and public hospitals.)

• CMS indicates that without rate increases and coverage improvements, uncompensated care funds will be cut and DSRIP investments will be eliminated (See Appendix Chart 3).

• If Texas fails to renew the waiver at close to current levels, or to develop an alternate funding strategy, we will face dramatic effects on our state’s social and safety net systems and our ability to provide care; in particular, for providers that today have slim positive operating margins.

• Waiver funds today make the difference between some hospitals’ ability to continue

providing services. For example: o With waiver funding, Harris Health system has a $1.2 million or 0.09 percent margin

off a $1.3 billion budget. o Without waiver funding:

Harris would face a negative margin of $209 million or negative 16 percent. Loss of waiver funds in Harris also would lead to closing 6 same day clinics

and elimination of 150,000 same day appointments. o Parkland Health will face similar challenges without waiver funding. o Across our membership, funding reductions will lead to increased avoidable

emergency department use; more avoidable inpatient days; poorer health; job loss; loss of GME positions and Texas’ medical school investments as residents go to other states; loss of critical behavioral health investments and care; increased county court and incarceration costs and increased pressure on local property taxes.

• The waiver also created an unparalleled level of provider coordination that has achieved

significant results. Loss of the waiver or waiver funding will set back coordination, could unravel the coordinating infrastructure of the Regional Healthcare Partnerships, and would terminate some projects before the full return on investment can be achieved.

Challenges from CMS’ New Managed Care Rules • CMS recently finalized Medicaid managed care rules that threaten Texas’ current

Medicaid hospital Financing System; in particular use of IGT that now supports almost half of all hospitals’ Medicaid payments.

o The rules limit and regulate the ability of the state to make direct supplemental payments to providers or to direct HMOs to make targeted provider payments.

o Because of their uninsured care and low Medicaid rates, teaching hospitals have increasingly become reliant on supplemental Medicaid programs to continue providing services. These programs use local funds (rather than general revenue) as the state’s match.

o CMS’ managed care rules already have resulted in the state making or considering changes to current hospital financing programs that compound our current waiver financing challenges. While so far, Texas can continue value-based supplemental programs such as the Network Access Improvement Program (for health research

3

institutions and public hospitals), CMS is looking more closely and critically at the use of local funding and how these programs are set up.

Opportunities • The waiver renewal process provides Texas with risks and with two important opportunities. • Two key opportunities:

o Develop a sustainable financing strategy; o Create integrated provider based systems of care that leverage local innovation and

investments to improve quality, and cost-effectiveness using value-based incentives. Conclusions & Recommendations: • Emerging CMS policy and regulations in the waiver and in managed care rules are intended to

encourage states to increase Medicaid rates, provide broad health coverage, and develop equitable, sustainable, and transparent Medicaid financing.

• If we are not successful in retaining waiver funding, and if we do not develop a sustainable, transparent, and equitable approach for Medicaid funding in Texas, we face a significant reduction in services and health capacity. Significant loss of funds is a particular risk for providers with already narrow margins.

• Texas and hospital providers need to identify and agree to a methodology for supporting increased provider rates and a strategy to negotiate coverage improvements.

• At the same time, we envision an opportunity and much to gain if we are successful in first, creating a convincing vision and second a realistic path to address our Medicaid hospital funding challenges.

• We believe that leveraging the waiver to invest in transformation and creation of integrated,

value-based public and private health systems is part of a winning negotiation and transformation strategy for improving care and maximizing waiver funds.

• Texas can and should leverage local innovation and waiver financing to create coordinated

healthcare systems with integrated outpatient, primary, specialty care, and inpatient care. With significant community partner engagement and value-based financing, we can double down on our Texas waiver successes, creating quality and cost-effective care systems using value-based infrastructure and incentives.

4

Appendix:

Chart 1: THOT’s Key Hospital Activity

Chart 2: SDA Trauma Care Add-on 2016-2017

0

20

40

60

80

100

120

140

160

180

Est. Trauma Approps2015

Est. Trauma Approps2016

Est. Trauma Approps2017

2016-2017 Trauma SDA Add-On Thank you!

Federal $

Trauma GR

Millions

5

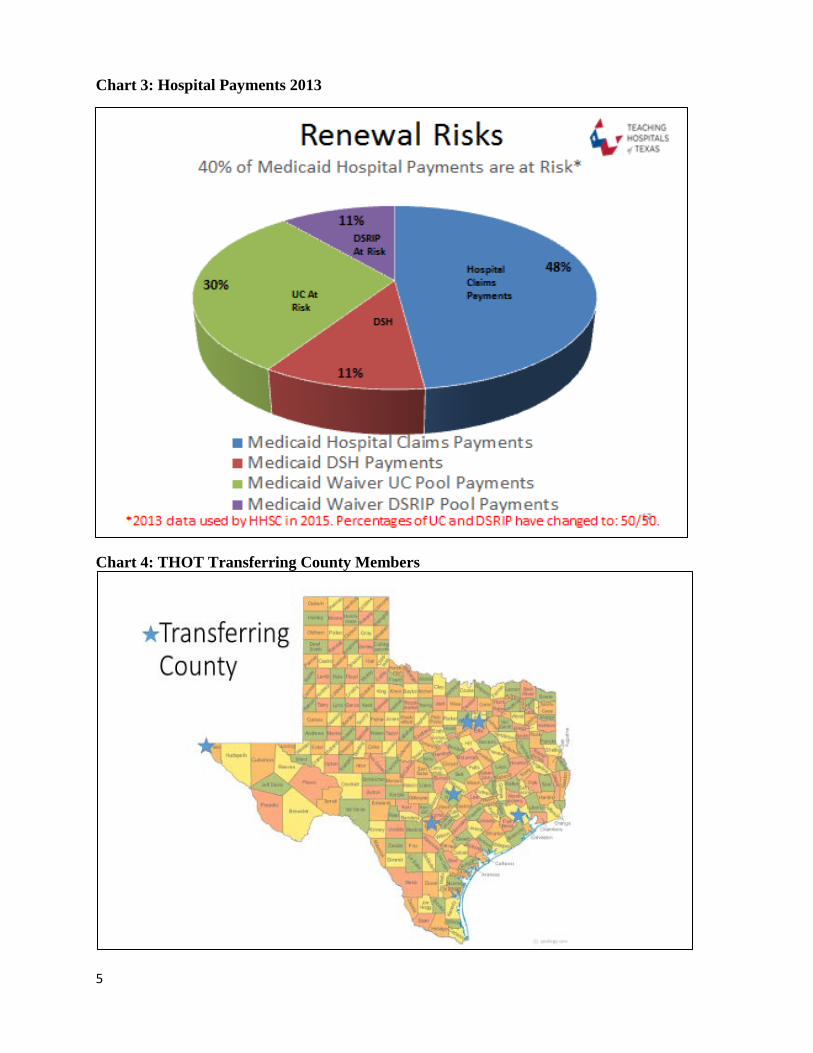

Chart 3: Hospital Payments 2013

Chart 4: THOT Transferring County Members

1

Contact:

Maureen Milligan, President and CEO Teaching Hospitals of Texas 1005 Congress Avenue; Suite 830 Austin, TX 78701 Phone: 512.476.1497 Email: [email protected]

THOT Document for House Appropriations Article II Sub-Committee

Charge: Texas Healthcare Transformation and Quality Improvement Program 1115 Waiver (Invited Testimony) Who we are • The Teaching Hospitals of Texas have commitments to provide quality care to all, in

particular vulnerable Texans; to be prepared for and provide trauma and disaster services and care; and to plan for tomorrow by supporting the Texas healthcare workforce and graduate medical education as well as clinical and delivery system research and transformation.

• While representing only about 5% of Texas’ hospitals and 16% of patient days, THOT members provide about 23% of Medicaid care; 36% of the hospital care provided to uninsured Texans; almost two-thirds of Level 1 Trauma care; and about two-thirds of hospital based Graduate Medical Education residencies. Related to waivers, THOT members represent 11 of the 20 waiver anchors or regional coordinators, provide significant uninsured inpatient and outpatient care, and provide the bulk of funding that makes possible the access to the waivers’ billions in healthcare investments.

Thank you -- Increased funding in 16-17

• With our focus and share of trauma services, and our mission to provide care for vulnerable and low-income

Texans, THOT members are particularly grateful for the increases in Safety Net funding and Trauma funding. Trauma SDA Add On funding increased from about $87 million to about $180 million. These additional funds increased the percent of uncompensated trauma care funding from

2

one-third (as in the 2014 chart above) to about two-thirds; leaving only one-third of uncompensated trauma costs without trauma funding in 2016-2017. While the prior session’s $300 million General Revenue support for DSH was not continued, the trauma and safety net add on payments helped to offset part of that discontinuation.

• Thank you also for the safety net add on which brought safety net funding for hospitals and

systems that provide care to low income Texans to $135M all funds per year for the biennium. For providers with thin margins, these funds make a difference in providing care or cutting services. To better target scarce state funds consistent with legislative language, we ask your consideration that moving forward, these funds be distributed based on providers’ share of both Medicaid and uninsured care provided. By only addressing the Medicaid half of the

equation as under the current distribution, hospitals that see more uninsured receive less of the available targeted funding than if uninsured were included.

Emergent Financing Challenges Texas is faced with several converging financial challenges including waiver renewal and new managed care rules. Texas’ 1115 Waiver Challenges • We are also thankful and appreciative

of the Health and Human Services Commission and your support for negotiating a 15-month waiver extension at current funding levels. This extension provides a very important measure of stability and certainty as the state negotiates for

Hospital A Illustration

• Serves 5% of the state’s Medicaid days • Serves 10% of the state’s uninsured

• Has 13% of the state’s unreimbursed

costs. (3% from Medicaid where 60% of costs are paid and 10% from uninsured)

HHSC RULE

Receives 5% of available targeted funds

PROPOSED CHANGE

Receives 13% of available targeted funds

Hospital B Illustration

• Serves 5% of the state’s Medicaid days • Serves 1% of the state’s uninsured

• Has 4% of the state’s unreimbursed

costs. (3% from Medicaid where 60% of costs are paid and 1% from uninsured)

HHSC RULE

Receives 5% of available targeted funds

PROPOSED CHANGE

Receives 4% of available targeted funds

3

the full waiver renewal. THOT members include the entities providing the majority of state match for the waiver’s $6 billion in funding; and represent 11 of the 20 waiver “anchors” or administrative coordinators throughout Texas. Waiver funding is particularly crucial for our members since it makes the difference between slim positive and significant negative margins and their ability to maintain services.

• The 1115 Waiver is funded on the local level through Intergovernmental Transfers from health related institutions, local mental health authorities, and public hospitals.

• Waiver funding of $6 billion per year represented a significant share of all Texas Medicaid

hospital related payments: about 40% in 2013. (The green section in the “Renewal Risks” chart represents UC payments and the DSRIP is in purple. Both are at risk.)

• Yet CMS has indicated that unless Texas increases rates and proposes a coverage option, waiver funding for uncompensated care will be significantly reduced, and funding for innovation-based DSRIP funds will evaporate. Even at current waiver funding levels, Texas hospitals still have over $2 billion in costs of care that are unfunded. These reductions will have dramatic consequences on Texas’ social and safety net systems and on our ability to continue providing care.

• Waiver funds today make the difference between some hospitals’ ability to continue providing

services. For example: o With waiver funding, Harris Health system has a $1.2 million or 0.09 percent margin

off a $1.3 billion budget. o Without waiver funding:

Harris would face a negative margin of $209 million or negative 16 percent. Loss of waiver funds in Harris also would lead to closing 6 same day clinics

and elimination of 150,000 same day appointments.

• Funding reductions will lead to:

Increased avoidable emergency department use; more avoidable inpatient days; poorer health; job loss; loss of GME positions and of Texas’ medical school investments as residents go to other states; loss of critical behavioral health investments and care; increased county court and incarceration costs; and increased pressure on local property taxes.

• The waiver has also created an unparalleled level of provider coordination that has achieved significant results. Through their innovation in

Waiver innovation includes using paramedics on down time to check on patients recently discharged from hospitals or needing assurance; bringing providers to homeless shelters to provide care; creating and using sophisticated predictive analytics to identify and provide care management to those most likely to need it; creating at home IV antibiotic protocols and training that have saved nearly 28,000 patient days and achieved a 47% reduction in preventable hospital readmissions; and using telemedicine to make behavioral health providers more available. These innovations have reduced ED visits, inpatient days and created improvements beyond health care, for example it can reduce community court and incarceration costs.

4

the current waiver, providers including hospitals, behavioral health providers, participating physicians, and other integrated partners have reduced avoidable Emergency Department visits, inpatient stays and provided better care often with less cost that focuses on the needs of patients.

Loss of the waiver or waiver funding will set back coordination, could unravel the coordinating infrastructure of the Regional Healthcare Partnerships, and would terminate some projects before the full return on investment can be achieved.

Challenges from CMS’ New Managed Care Rules • Teaching hospitals have

increasingly become reliant on supplemental Medicaid programs in order to meet the needs of their communities. The state’s share of match for these programs is funded at the local level rather than state general revenue.

• New CMS Medicaid managed care limit and regulate the ability of the state to make direct payments to providers or to direct HMOs to make targeted provider payments.

• The regulations threaten Texas’ current Intergovernmental Transfer 0 F

1(IGT)-based approach used in many Medicaid hospital programs. With more than half of the state match for Medicaid hospital payments coming from IGT, Texas must create an equitable, sustainable financing strategy that complies with CMS’ new requirements using general revenue or alternative sources of funding. The limited number of large IGTing counties will be unable to fund a larger share of the state’s Medicaid hospital program.

• CMS’ managed care rules already have resulted in the state making or considering changes to current hospital financing programs that compound our current waiver financing challenges.

• Under the new managed care rules, Texas can continue value-based supplemental programs such as the Network Access Improvement Program for certain classes of hospitals such health research institutions and public hospitals but we will be under increased scrutiny from CMS on how these programs are set up.

1 Medicaid is funded with both federal and state funding. In the supplemental programs, funds from local government entities, rather than from general revenue, primarily are used as the state match. These local funds when used for state match in Medicaid are called Intergovernmental Transfers or IGT.

5

Opportunities • Waiver renewal negotiations provide Texas with risks but also with two important

opportunities:

o First, the renewal process provides an impetus to address our need for a long term sustainable approach to equitably fund Medicaid payments for hospitals.

o Second, it provides Texas and Texas providers the opportunity to use the lessons and successes of the current waiver to create public and private provider based integrated systems of care. What does that mean?

• First with Medicaid rates paying most hospitals significantly less than the costs of services

provided, myriad complex payment programs, largely funded by a diminishing number of counties’ property taxes, have evolved into a very complicated, unstable and unsustainable patchwork of Medicaid hospital financing. In addition to DSH, Texas used UPL, and now has DSRIP, UC, NAIP and MPAP1F

i programs– mostly funded with county property tax and complex financing relationships. The waiver renewal process will give Texas the opportunity to create a more streamlined efficient and equitable payment system that addresses the fundamental problems of low hospital rates, and increasing dependence on a diminishing number of local county property taxes.

• Second, the waiver renewal offers Texas providers the opportunity to create provider based, integrated healthcare systems that improve care and bend the cost curve by tapping into the deep roots and strong community relationships that our public and private hospitals have. It provides the opportunity to continue providing innovative care for all Texans, including uninsured Texans through “DSRIP” innovation in provider based systems. CMS has supported and encouraged similar integrated provider based systems that include approaches like these (for example in New York and California), that preference value of care over simple volume of care. Through the 1115 waiver, Texas has been leading the way with an unprecedented scale of innovation and local engagement.

Conclusions and recommendations: • Emerging CMS policy and regulations in the waiver and in managed care rules are intended to

encourage states to increase Medicaid rates, provide health coverage, and develop equitable, sustainable, and transparent Medicaid financing.

• If we aren’t successful in negotiating the waiver renewal and funding, and if we do not develop a sustainable, transparent, and equitable approach for Medicaid funding in Texas, we’ll face significant care reductions.

Two key opportunities: 1) Develop sustainable financing; 2) Create integrated provider based

systems of care that leverage local innovation and investments improving quality, and cost-effectiveness using value-based incentives.

6

• Texas and hospital providers need to identify and agree to a methodology for supporting increased provider rates and a strategy to negotiate coverage improvements in order to limit CMS’ funding cuts.

• At the same time, we envision an opportunity and much to gain if we are successful in first, creating a convincing vision and second a realistic path to address our Medicaid hospital funding challenges.

• We believe that leveraging the waiver to invest in transformation and creation of integrated, value-based public and private health systems is part of a winning negotiation and transformation strategy for improving care and maximizing waiver funds.

• Texas can and should leverage local innovation and waiver financing to continue waiver funding for investments in coordinated provider-based healthcare systems with integrated outpatient, primary, specialty care, and inpatient care for uninsured Texans losing services now available through DSRIP. With significant community partner engagement and value-based financing, we can double down on our Texas waiver successes, creating quality and cost-effective care systems using value-based infrastructure and incentives.

7

Appendix I. THOT Membership and Mission:

THOT represents 17 health systems and hospital districts providing essential health services to their communities sharing the following core commitments:

• Supporting access to care for all in our communities with a special focus on vulnerable populations;

• Providing and coordinating essential community health services, such as trauma and disaster management; and

• Preparing for the future by training tomorrow’s healthcare providers and supporting health research and healthcare transformation.

Texas’ 1115 Waiver Regions:

In 11 of the 20 Regions THOT members serve as Waiver Anchors/Coordinators. (THOT members identified below. Those outlined in red are THOT Anchors)

Chart 1

8

i Disproportionate Share Hospital or DSH funding; Upper Payment Limit or UPL funding; Delivery System Reform Incentive Payment or DSRIP funding; Uncompensated Care or UC funding; Network Access Improvement Program or NAIP, and Minimum Payments Amounts Program or MPAP.

Testimony of the Children’s Hospital Association of Texas

House Appropriations Committee July 13, 2016

Stacy E. Wilson, J.D. President 823 Congress Ave., Suite 1500 Austin, TX 78701 (512) 320-0910

Children’s Hospital Association of Texas

2

• Non-profit association representing seven non-profit, freestanding Texas children’s hospitals

• Members: – Children’s Health, Dallas – The Children’s Hospital of San Antonio – Cook Children’s Health Care System, Fort Worth – Covenant Children’s Hospital, Lubbock – Dell Children’s Medical Center, Austin – Driscoll Children’s Hospital, Corpus Christi – Texas Children’s Hospital, Houston

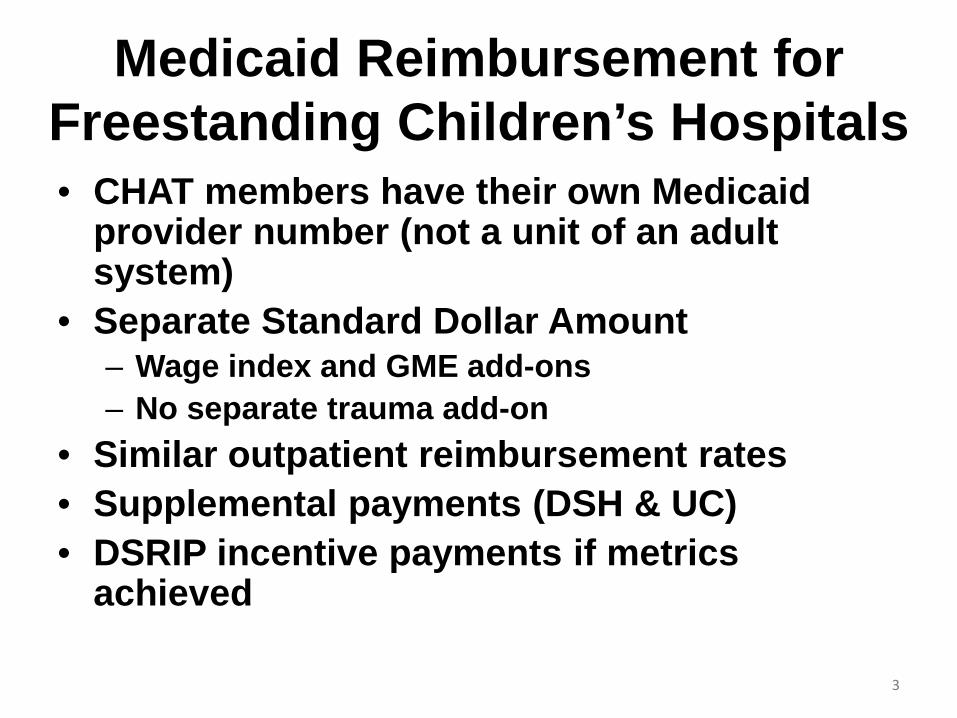

Medicaid Reimbursement for Freestanding Children’s Hospitals • CHAT members have their own Medicaid

provider number (not a unit of an adult system)

• Separate Standard Dollar Amount – Wage index and GME add-ons – No separate trauma add-on

• Similar outpatient reimbursement rates • Supplemental payments (DSH & UC) • DSRIP incentive payments if metrics

achieved

3

Key Facts About Freestanding Children’s Hospitals

• Have high Medicaid payor mix (50% - 70%) • Use higher staffing ratios • Treat medically complex children • Provide intense services • Serve children from across the nation and state • Providing more outpatient services when appropriate • Children as patients

– Different needs (not just small adults) – Schooling – Child life services – Family supports

4

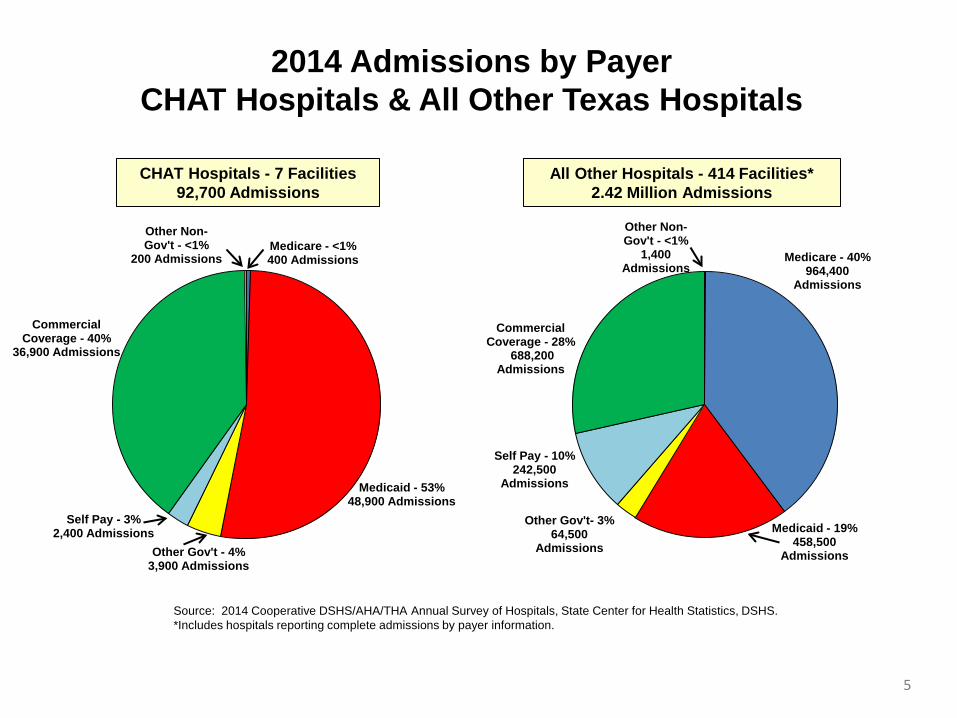

Medicare - <1% 400 Admissions

Medicaid - 53% 48,900 Admissions

Other Gov't - 4% 3,900 Admissions

Self Pay - 3% 2,400 Admissions

Commercial Coverage - 40%

36,900 Admissions

Other Non- Gov't - <1%

200 Admissions

CHAT Hospitals - 7 Facilities 92,700 Admissions

All Other Hospitals - 414 Facilities* 2.42 Million Admissions

Source: 2014 Cooperative DSHS/AHA/THA Annual Survey of Hospitals, State Center for Health Statistics, DSHS. *Includes hospitals reporting complete admissions by payer information.

Medicare - 40% 964,400

Admissions

Medicaid - 19% 458,500

Admissions

Other Gov't- 3% 64,500

Admissions

Self Pay - 10% 242,500

Admissions

Commercial Coverage - 28%

688,200 Admissions

Other Non-Gov't - <1%

1,400 Admissions

2014 Admissions by Payer CHAT Hospitals & All Other Texas Hospitals

5

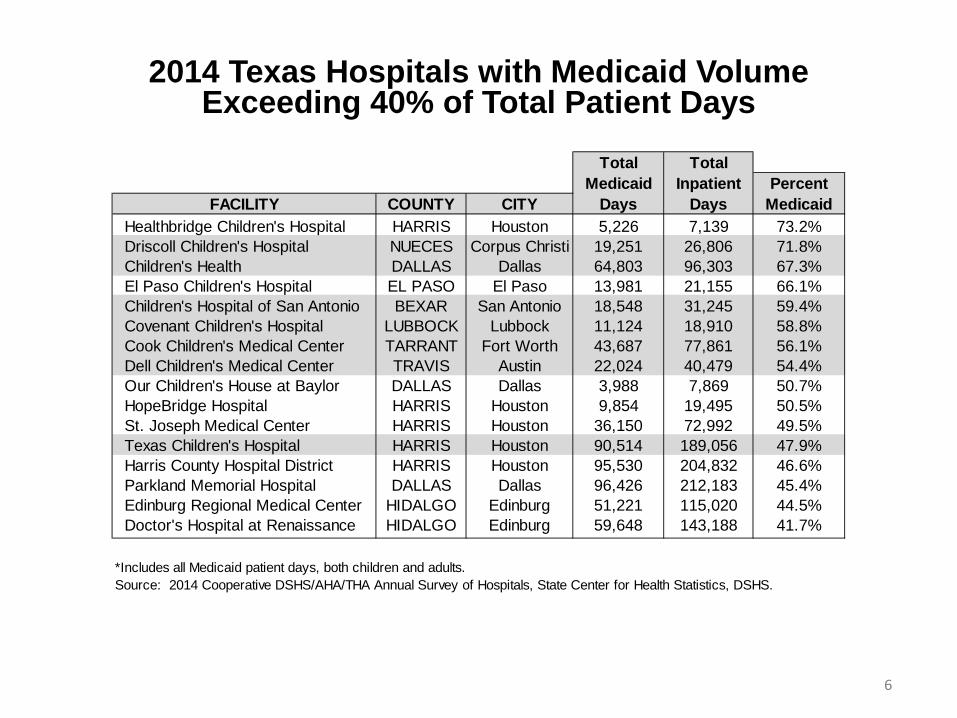

Total TotalMedicaid Inpatient Percent

FACILITY COUNTY CITY Days Days MedicaidHealthbridge Children's Hospital HARRIS Houston 5,226 7,139 73.2%Driscoll Children's Hospital NUECES Corpus Christi 19,251 26,806 71.8%Children's Health DALLAS Dallas 64,803 96,303 67.3%El Paso Children's Hospital EL PASO El Paso 13,981 21,155 66.1%Children's Hospital of San Antonio BEXAR San Antonio 18,548 31,245 59.4%Covenant Children's Hospital LUBBOCK Lubbock 11,124 18,910 58.8%Cook Children's Medical Center TARRANT Fort Worth 43,687 77,861 56.1%Dell Children's Medical Center TRAVIS Austin 22,024 40,479 54.4%Our Children's House at Baylor DALLAS Dallas 3,988 7,869 50.7%HopeBridge Hospital HARRIS Houston 9,854 19,495 50.5%St. Joseph Medical Center HARRIS Houston 36,150 72,992 49.5%Texas Children's Hospital HARRIS Houston 90,514 189,056 47.9%Harris County Hospital District HARRIS Houston 95,530 204,832 46.6%Parkland Memorial Hospital DALLAS Dallas 96,426 212,183 45.4%Edinburg Regional Medical Center HIDALGO Edinburg 51,221 115,020 44.5%Doctor's Hospital at Renaissance HIDALGO Edinburg 59,648 143,188 41.7%

*Includes all Medicaid patient days, both children and adults.Source: 2014 Cooperative DSHS/AHA/THA Annual Survey of Hospitals, State Center for Health Statistics, DSHS.

2014 Texas Hospitals with Medicaid Volume Exceeding 40% of Total Patient Days

6

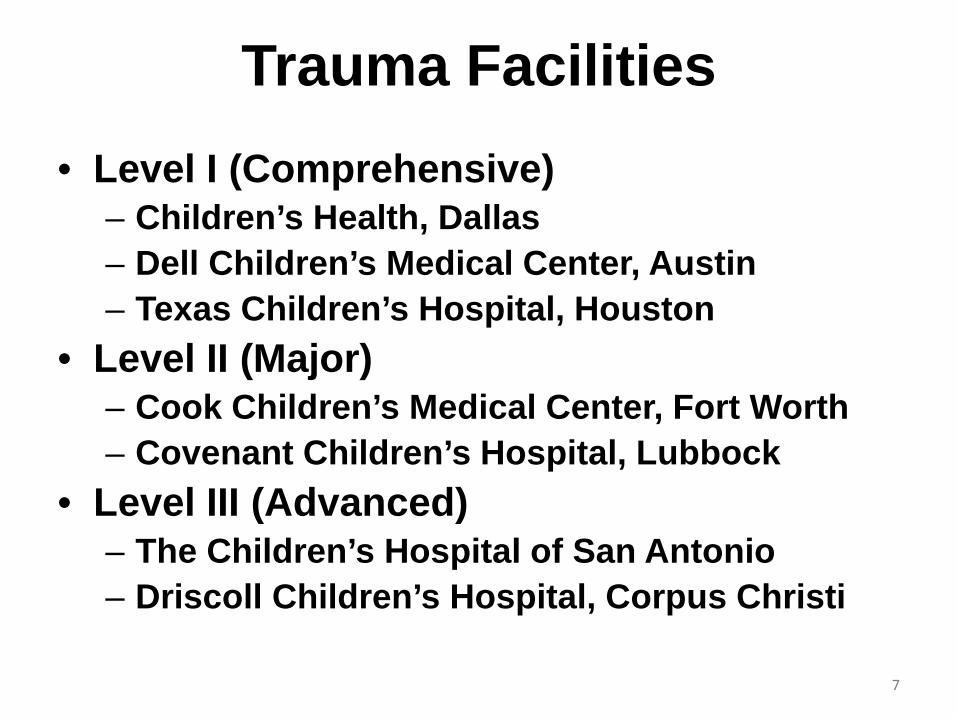

Trauma Facilities • Level I (Comprehensive)

– Children’s Health, Dallas – Dell Children’s Medical Center, Austin – Texas Children’s Hospital, Houston

• Level II (Major) – Cook Children’s Medical Center, Fort Worth – Covenant Children’s Hospital, Lubbock

• Level III (Advanced) – The Children’s Hospital of San Antonio – Driscoll Children’s Hospital, Corpus Christi

7

2.3

1.3

3.1

1.7

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

CHAT Hospitals All Other Hospitals

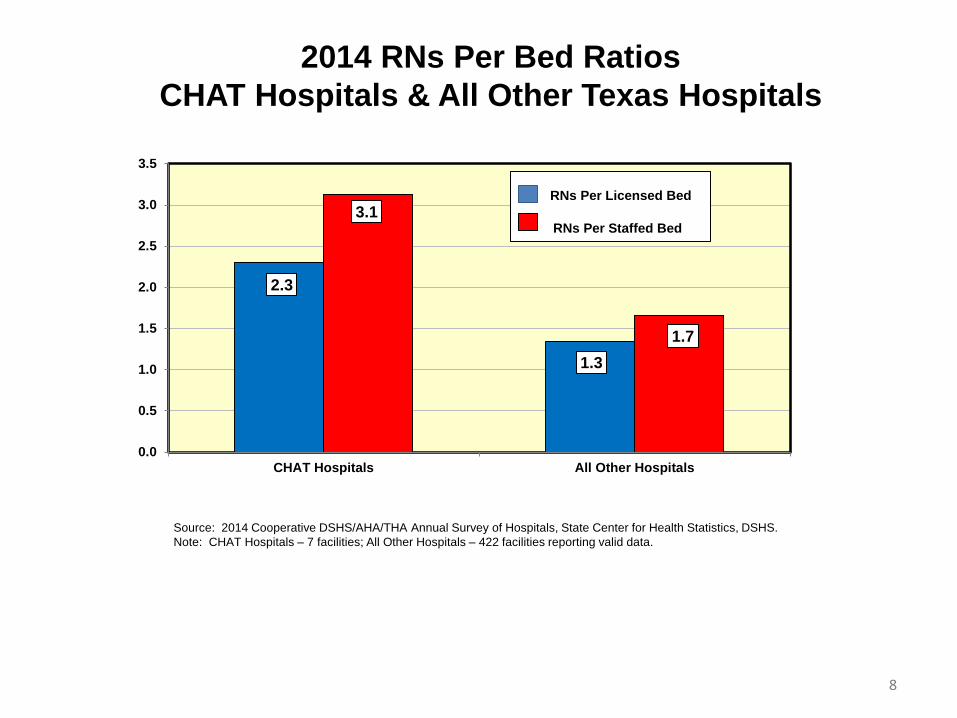

2014 RNs Per Bed Ratios CHAT Hospitals & All Other Texas Hospitals

RNs Per Licensed Bed RNs Per Staffed Bed

Source: 2014 Cooperative DSHS/AHA/THA Annual Survey of Hospitals, State Center for Health Statistics, DSHS. Note: CHAT Hospitals – 7 facilities; All Other Hospitals – 422 facilities reporting valid data.

8

84%

73% 71%

65%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Organ Transplants Cardiac Surgery Neurosurgery Spinal Surgery

Perc

ent o

f Pat

ient

Day

s

9

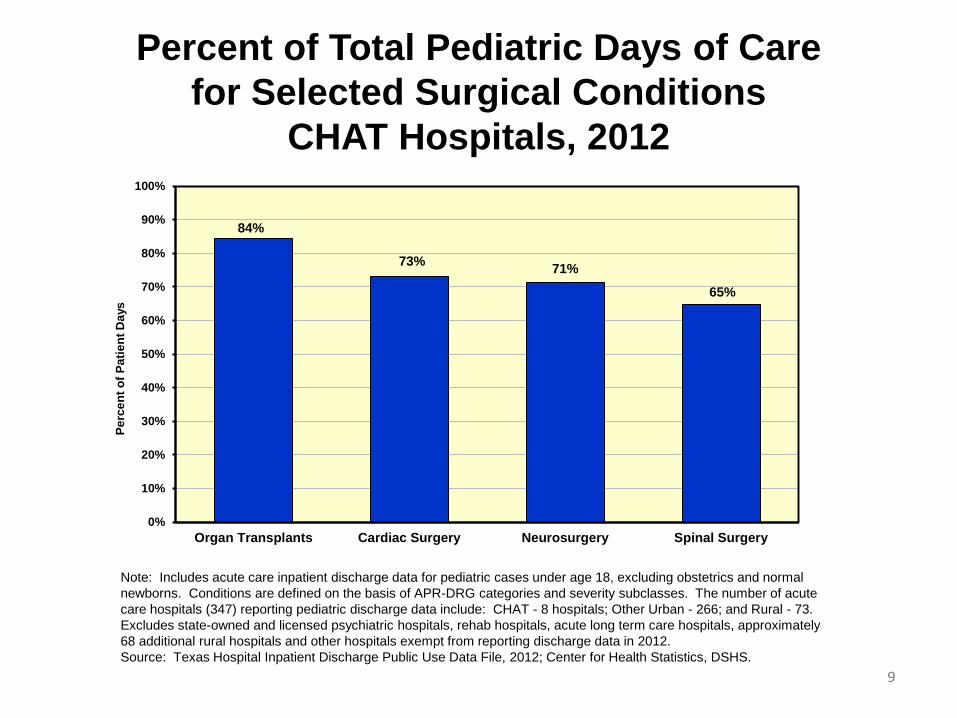

Percent of Total Pediatric Days of Care for Selected Surgical Conditions

CHAT Hospitals, 2012

Note: Includes acute care inpatient discharge data for pediatric cases under age 18, excluding obstetrics and normal newborns. Conditions are defined on the basis of APR-DRG categories and severity subclasses. The number of acute care hospitals (347) reporting pediatric discharge data include: CHAT - 8 hospitals; Other Urban - 266; and Rural - 73. Excludes state-owned and licensed psychiatric hospitals, rehab hospitals, acute long term care hospitals, approximately 68 additional rural hospitals and other hospitals exempt from reporting discharge data in 2012. Source: Texas Hospital Inpatient Discharge Public Use Data File, 2012; Center for Health Statistics, DSHS.

88% 83%

69% 67% 61%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cystic Fibrosis Sickle Cell AnemiaCrisis

Cerebral Palsy Cancer Spina Bifida

Perc

ent o

f Pat

ient

Day

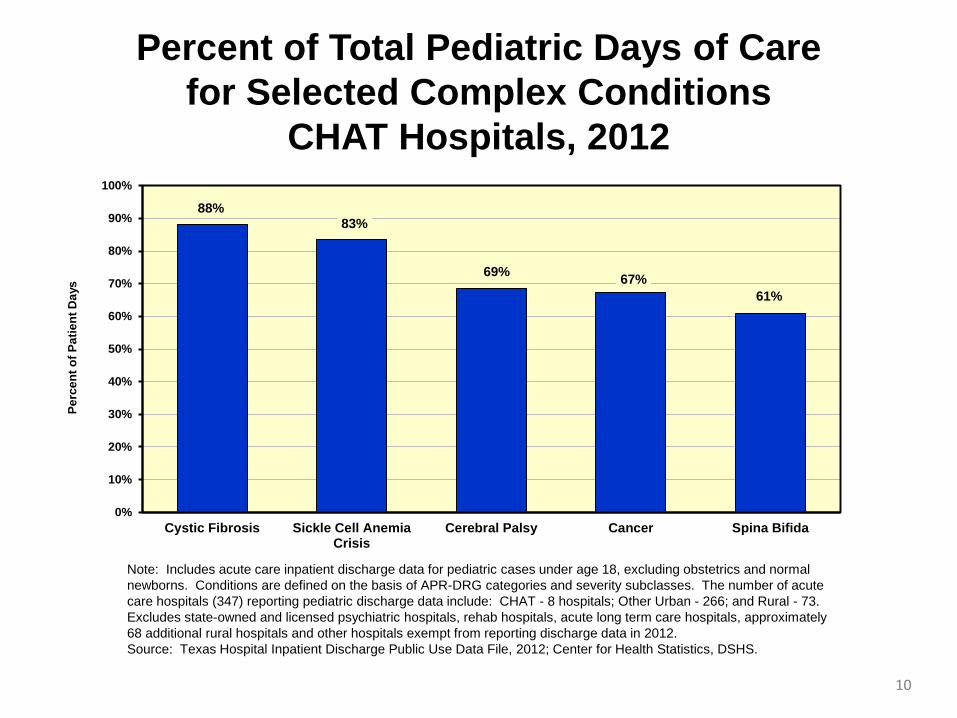

s Percent of Total Pediatric Days of Care

for Selected Complex Conditions CHAT Hospitals, 2012

Note: Includes acute care inpatient discharge data for pediatric cases under age 18, excluding obstetrics and normal newborns. Conditions are defined on the basis of APR-DRG categories and severity subclasses. The number of acute care hospitals (347) reporting pediatric discharge data include: CHAT - 8 hospitals; Other Urban - 266; and Rural - 73. Excludes state-owned and licensed psychiatric hospitals, rehab hospitals, acute long term care hospitals, approximately 68 additional rural hospitals and other hospitals exempt from reporting discharge data in 2012. Source: Texas Hospital Inpatient Discharge Public Use Data File, 2012; Center for Health Statistics, DSHS.

10

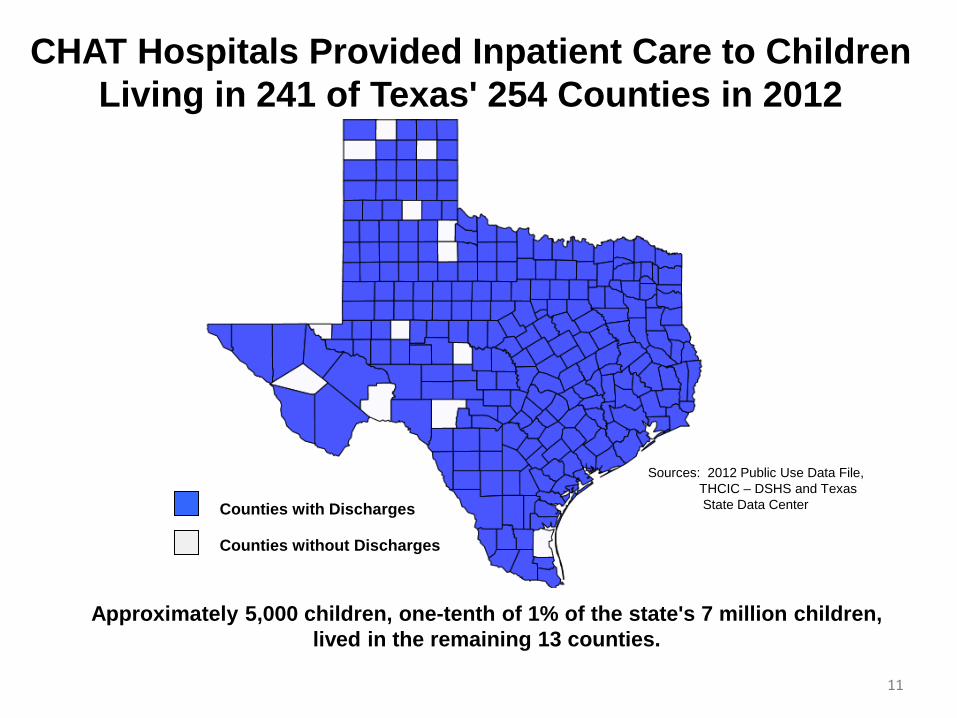

CHAT Hospitals Provided Inpatient Care to Children Living in 241 of Texas' 254 Counties in 2012

Counties with Discharges

Counties without Discharges

Sources: 2012 Public Use Data File, THCIC – DSHS and Texas State Data Center

Approximately 5,000 children, one-tenth of 1% of the state's 7 million children, lived in the remaining 13 counties.

11

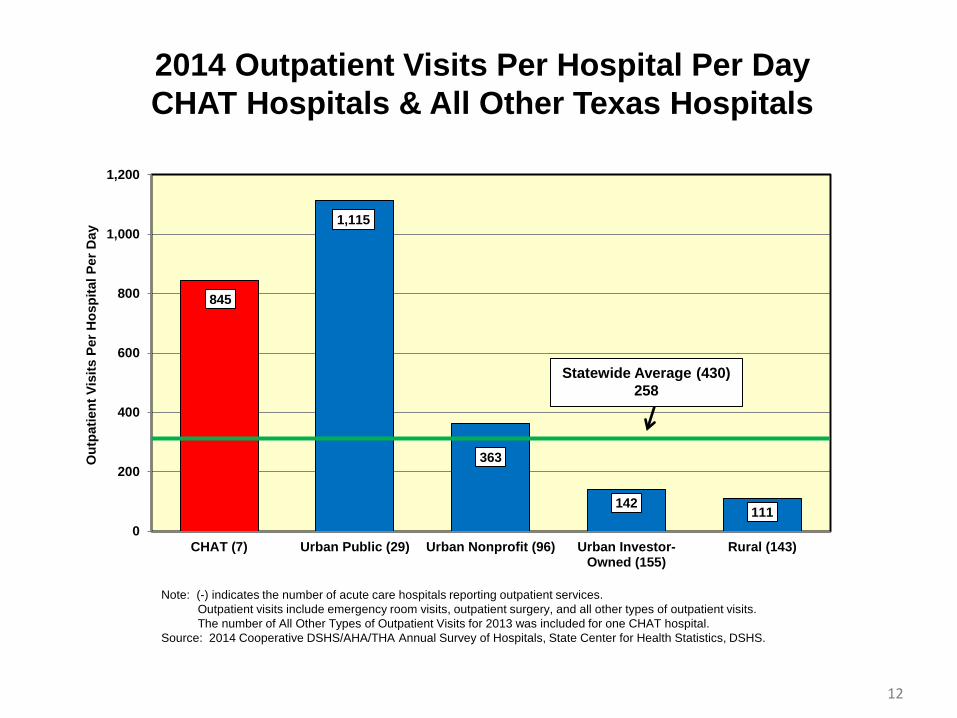

845

1,115

363

142 111 0

200

400

600

800

1,000

1,200

CHAT (7) Urban Public (29) Urban Nonprofit (96) Urban Investor-Owned (155)

Rural (143)

Out

patie

nt V

isits

Per

Hos

pita

l Per

Day

2014 Outpatient Visits Per Hospital Per Day CHAT Hospitals & All Other Texas Hospitals

Statewide Average (430) 258

Note: (-) indicates the number of acute care hospitals reporting outpatient services. Outpatient visits include emergency room visits, outpatient surgery, and all other types of outpatient visits. The number of All Other Types of Outpatient Visits for 2013 was included for one CHAT hospital. Source: 2014 Cooperative DSHS/AHA/THA Annual Survey of Hospitals, State Center for Health Statistics, DSHS.

12

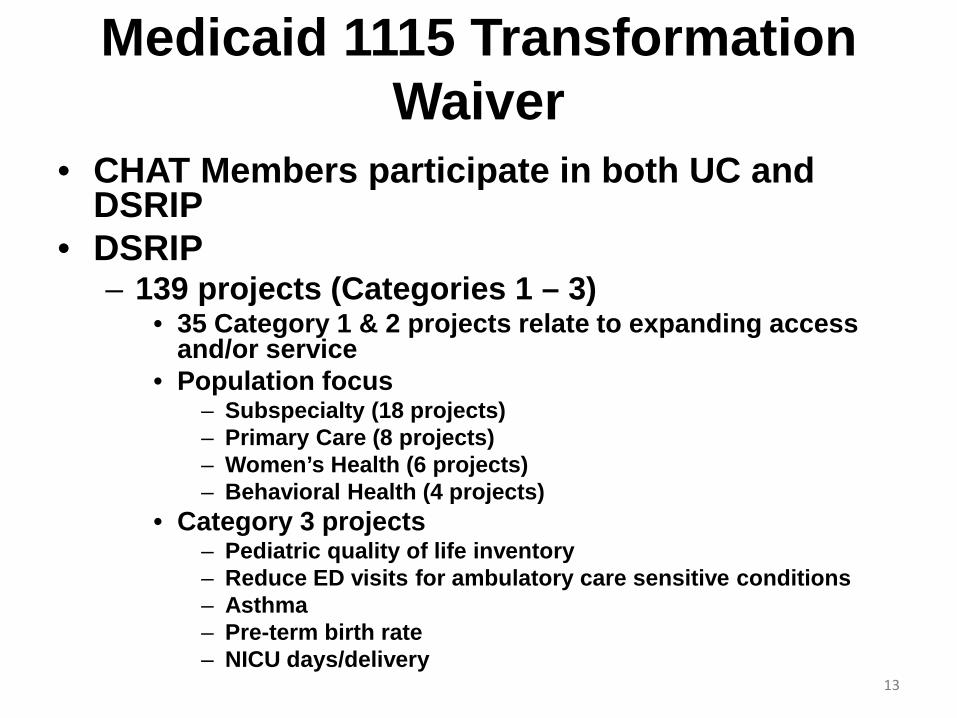

Medicaid 1115 Transformation Waiver

• CHAT Members participate in both UC and DSRIP

• DSRIP – 139 projects (Categories 1 – 3)

• 35 Category 1 & 2 projects relate to expanding access and/or service

• Population focus – Subspecialty (18 projects) – Primary Care (8 projects) – Women’s Health (6 projects) – Behavioral Health (4 projects)

• Category 3 projects – Pediatric quality of life inventory – Reduce ED visits for ambulatory care sensitive conditions – Asthma – Pre-term birth rate – NICU days/delivery

13

Moving to Value-Based Care Patient Safety & Quality Collaboratives

• Solutions for Patient Safety – Reducing patient harm in children’s

hospitals • Three quality collaboratives

– Asthma – Sepsis – Bronchiolitis – Improving quality of care, patient

experience, and lowering cost of care

14

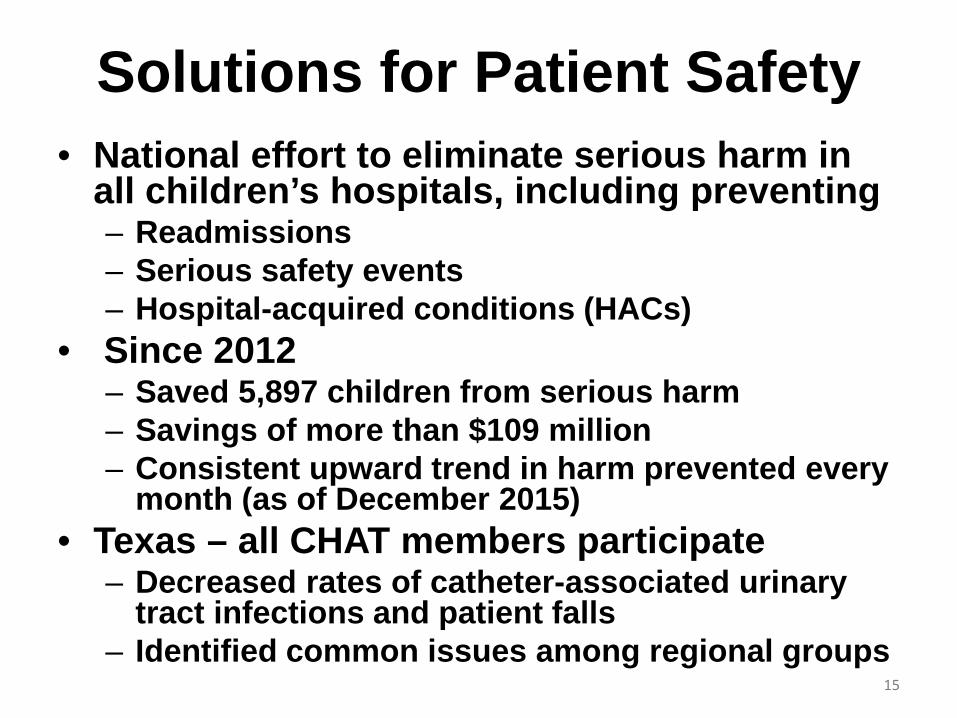

Solutions for Patient Safety • National effort to eliminate serious harm in

all children’s hospitals, including preventing – Readmissions – Serious safety events – Hospital-acquired conditions (HACs)

• Since 2012 – Saved 5,897 children from serious harm – Savings of more than $109 million – Consistent upward trend in harm prevented every

month (as of December 2015) • Texas – all CHAT members participate

– Decreased rates of catheter-associated urinary tract infections and patient falls

– Identified common issues among regional groups 15

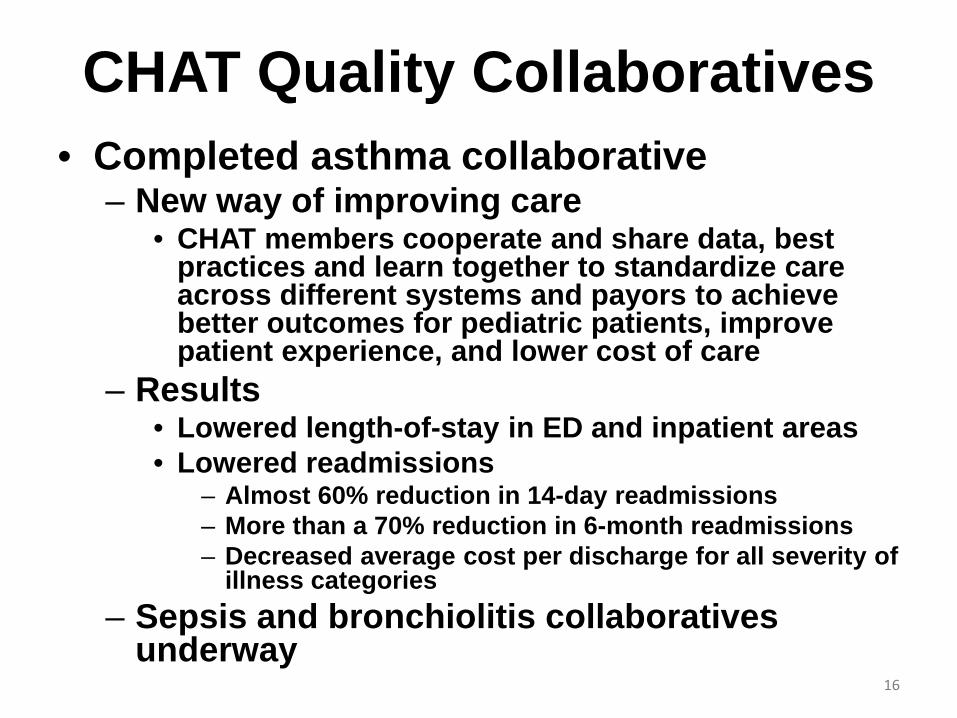

CHAT Quality Collaboratives • Completed asthma collaborative

– New way of improving care • CHAT members cooperate and share data, best

practices and learn together to standardize care across different systems and payors to achieve better outcomes for pediatric patients, improve patient experience, and lower cost of care

– Results • Lowered length-of-stay in ED and inpatient areas • Lowered readmissions

– Almost 60% reduction in 14-day readmissions – More than a 70% reduction in 6-month readmissions – Decreased average cost per discharge for all severity of

illness categories – Sepsis and bronchiolitis collaboratives

underway 16

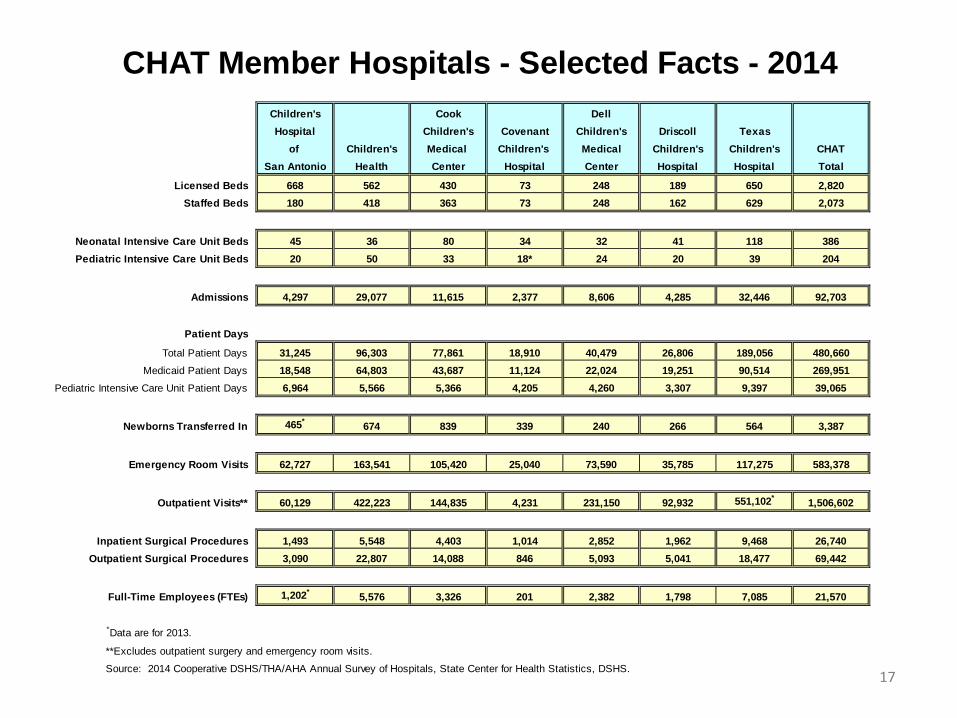

Children's Cook DellHospital Children's Covenant Children's Driscoll Texas

of Children's Medical Children's Medical Children's Children's CHATSan Antonio Health Center Hospital Center Hospital Hospital Total

Licensed Beds 668 562 430 73 248 189 650 2,820Staffed Beds 180 418 363 73 248 162 629 2,073

Neonatal Intensive Care Unit Beds 45 36 80 34 32 41 118 386Pediatric Intensive Care Unit Beds 20 50 33 18* 24 20 39 204

Admissions 4,297 29,077 11,615 2,377 8,606 4,285 32,446 92,703

Patient Days

Total Patient Days 31,245 96,303 77,861 18,910 40,479 26,806 189,056 480,660 Medicaid Patient Days 18,548 64,803 43,687 11,124 22,024 19,251 90,514 269,951

Pediatric Intensive Care Unit Patient Days 6,964 5,566 5,366 4,205 4,260 3,307 9,397 39,065

Newborns Transferred In 465* 674 839 339 240 266 564 3,387

Emergency Room Visits 62,727 163,541 105,420 25,040 73,590 35,785 117,275 583,378

Outpatient Visits** 60,129 422,223 144,835 4,231 231,150 92,932 551,102* 1,506,602

Inpatient Surgical Procedures 1,493 5,548 4,403 1,014 2,852 1,962 9,468 26,740 Outpatient Surgical Procedures 3,090 22,807 14,088 846 5,093 5,041 18,477 69,442

Full-Time Employees (FTEs) 1,202* 5,576 3,326 201 2,382 1,798 7,085 21,570

*Data are for 2013.

**Excludes outpatient surgery and emergency room visits.

Source: 2014 Cooperative DSHS/THA/AHA Annual Survey of Hospitals, State Center for Health Statistics, DSHS.

CHAT Member Hospitals - Selected Facts - 2014

17

Children’s Hospital Association of Texas

Stacy E. Wilson, J.D. President 823 Congress Ave., Suite 1500 Austin, TX 78701 (512) 320-0910 [email protected]

1 | P a g e

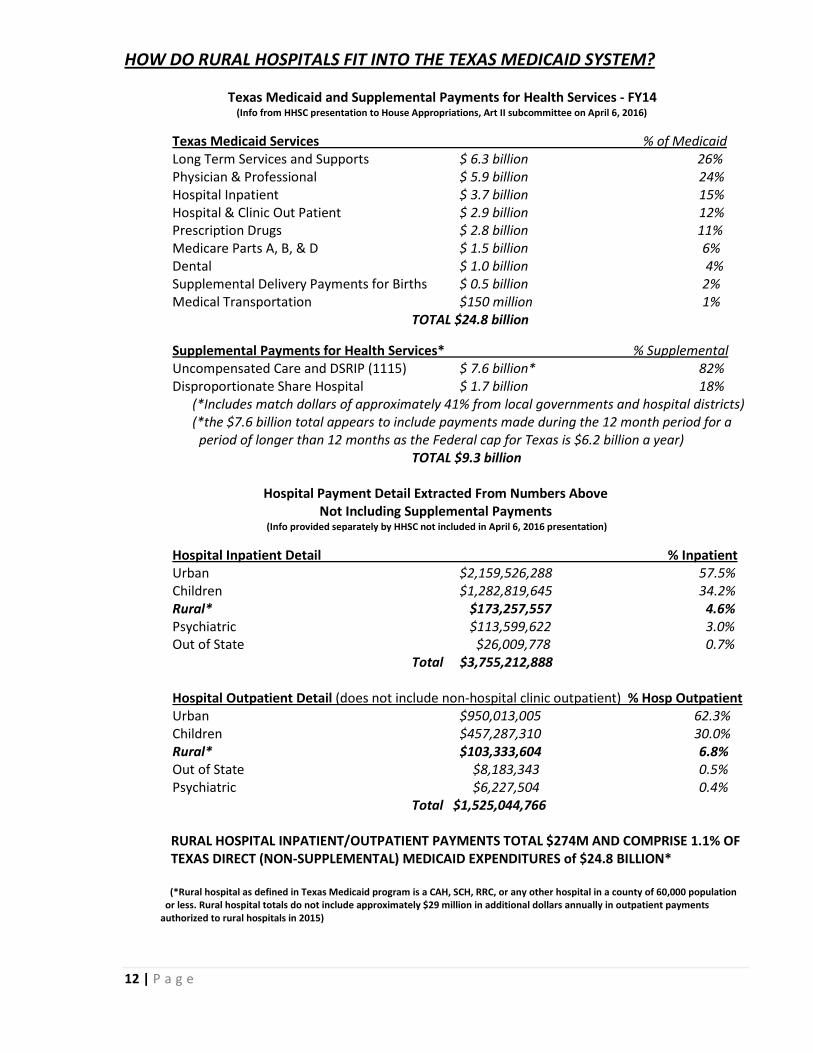

TEXAS RURAL HOSPITAL MEDICAID PAYMENTS

Presented to the Texas House

Appropriations Subcommittee on Article II

By Don McBeath

Director of Government Relations Texas Organization of Rural & Community Hospitals

(TORCH)

July 13, 2016

2 | P a g e

TEXAS RURAL HOSPITAL MEDICAID PAYMENTS

PAGE 3 WHAT IS A RURAL HOSPITAL?

PAGE 4 MAP OF TEXAS RURAL HOSPITALS PAGE 5 RURAL HOSPITAL CRISIS

PAGE 6 CRITICAL OPERATING DYNAMICS FOR TEXAS RURAL HOSPITALS

PAGE 7 FEDERAL HISTORY ON RURAL HOSPITAL REIMBURSEMENT

TEXAS HISTORY ON RURAL HOSPITAL REIMBURSEMENT

PAGE 8 POLICY CONSIDERATIONS WITH THE RURAL HOSPITAL BUDGET RIDER 84TH SESSION CHANGES TO RURAL HOSPITAL RIDER

PAGE 9 WHAT DOES THE CURRENT RIDER STATE?

PAGE 10 HOW DID HHSC IMPLEMENT THE NEW OUTPATIENT RIDER AND

CONTINUE THE INPATIENT POLICY

PAGE 11 KEY FACTS ABOUT RURAL HOSPITAL MEDICAID PAYMENTS

PAGE 12 HOW DO RURAL HOSPITALS FIT INTO THE TEXAS MEDICAID SYSTEM?

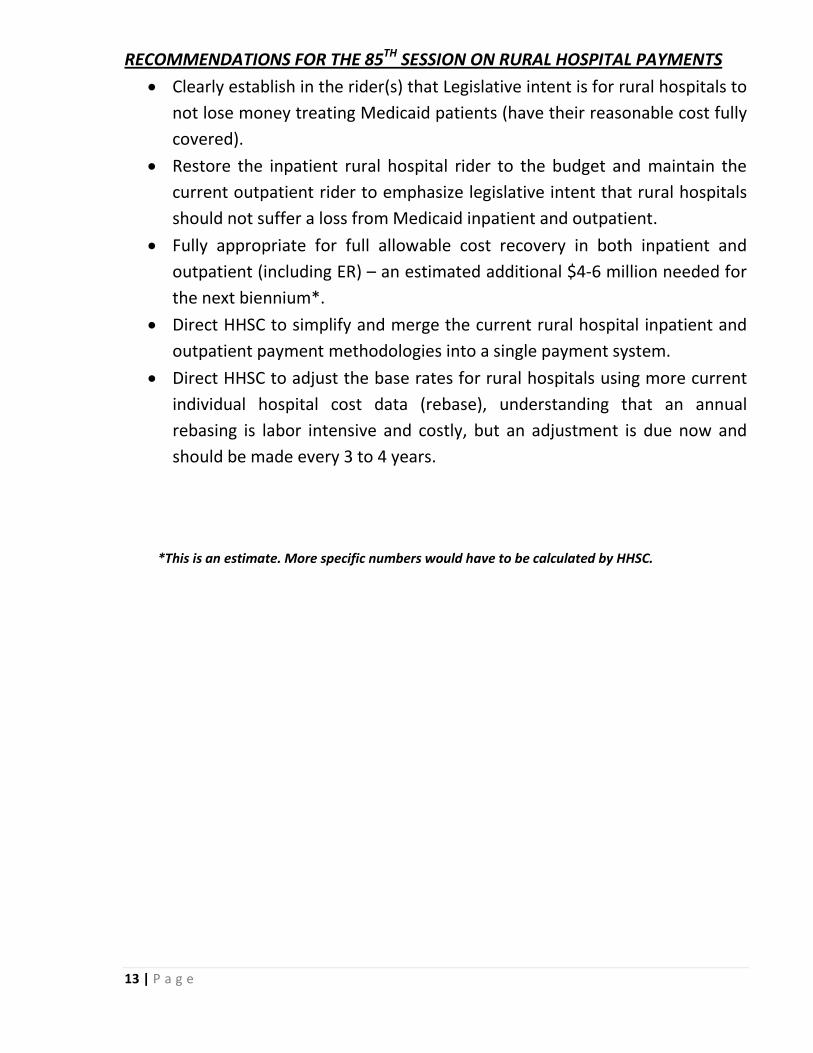

PAGE 13 RECOMMENDATIONS FOR THE 85TH SESSION ON RURAL HOSPITAL PAYMENTS

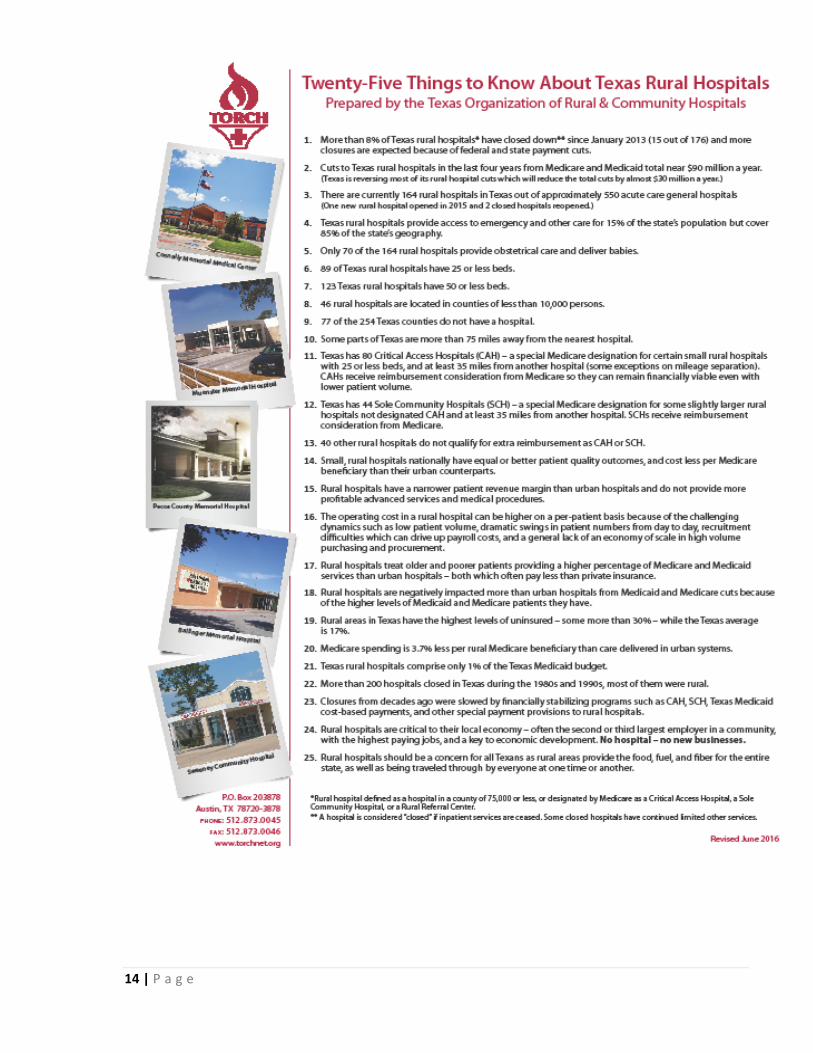

PAGE 14 (ATTACHMENT) RURAL HOSPITAL FACTSHEET

PAGE 15-17 (ATTACHMENT) HISTORY OF RURAL HOSPITAL RIDER LANGUAGE

3 | P a g e

WHAT IS A RURAL HOSPITAL?

• It depends on whose definition of rural you use! • Generally considered to be a hospital located in a rural area or one that

serves a high percentage of rural residents. • The federal government and Texas have dozens of definitions of rural

depending on which program, agency, etc. • The Texas Legislative Council in 2014 identified 48 definitions of rural in

Texas laws and codes. • Medicaid (Texas) definition of a rural hospital – Hospital with a Critical

Access Hospital (CAH), Sole Community Hospital (SCH), Rural Referral Center (RRC) designation from Medicare, or any other hospital in a county of 60,000 and less (according to the 2010 census) – (this definition has changed over the years).

• Medicare definition of a rural hospital – Hospital in a non-Metropolitan Statistical Area or in a rural census tract of a MSA, a hospital designated by state law or regulation as rural, or an urban hospital that would meet all requirements of a RRC or a SCH if it was located in a rural area.

• TORCH association definition - Hospital with a CAH, SCH, RRC designation from Medicare or any other hospital in a county of 75,000 and less.

• Under the Medicaid definition, Texas has 159 rural hospitals. • Under TORCH definition, Texas has 164 rural hospitals.

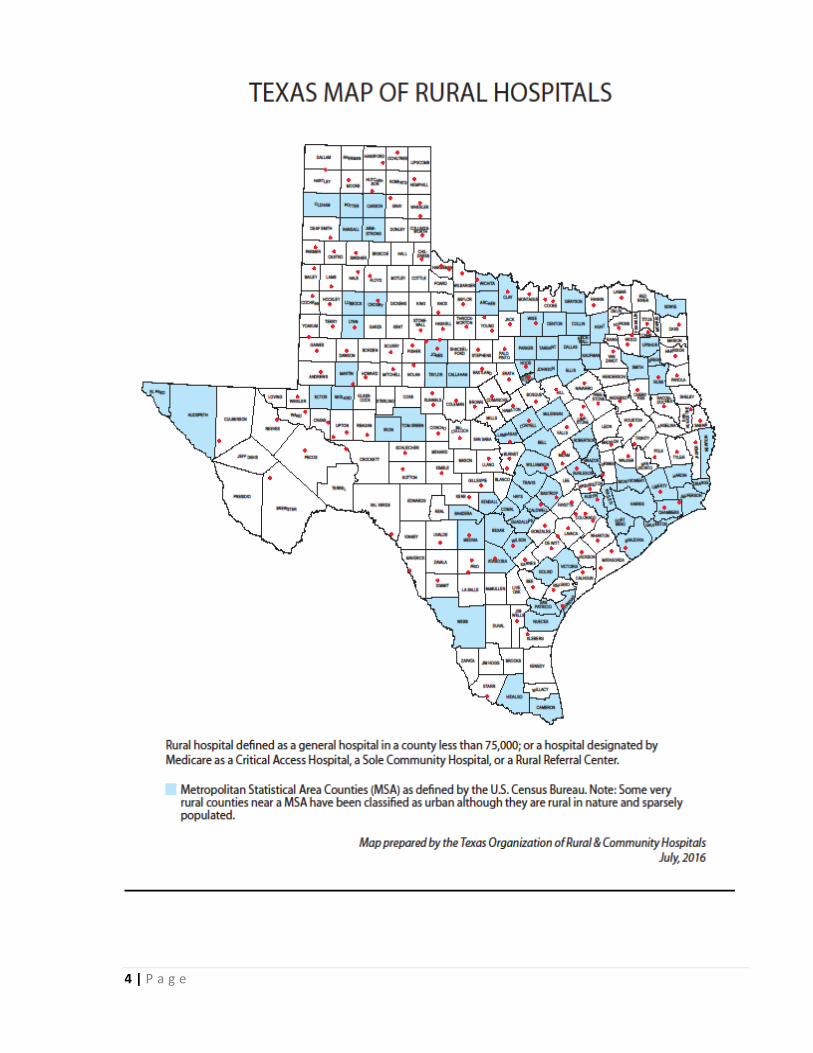

4 | P a g e

5 | P a g e