Embed Size (px)

Citation preview

20 Novembre, 2010

Investor Meetings in Europe

Fiat post-demerger

Nov 29-Dec 2, 2010 Investor Meetings in Europe 2

Certain information included in this document is forwardlooking and is subject to important risks and uncertaintiesthat could cause actual results to differ materially. TheCompany's businesses include its automotive,automotive-related and other sectors, and its outlook ispredominantly based on its interpretation of what itconsiders to be the key economic factors affecting thesebusinesses. Forward-looking statements with regard tothe Group's businesses involve a number of importantfactors that are subject to change, including: the manyinterrelated factors that affect consumer confidence andworldwide demand for automotive and automotive-relatedproducts; factors affecting the agricultural businessincluding commodities prices, weather, and governmentalfarm programs; general economic conditions in each ofthe Group's markets; legislation, particularly that relatingto automotive-related issues, agriculture, theenvironment, trade and commerce and infrastructuredevelopment; actions of competitors in the variousindustries in which the Group competes; productiondifficulties, including capacity and supply constraints andexcess inventory levels; labor relations; interest rates andcurrency exchange rates; political and civil unrest; and

other risks and uncertainties. Any forward-lookingstatements contained in this document are referred to thecurrent date and, therefore, any of the assumptionsunderlying this document or any of the circumstances ordata mentioned in this document may change. Fiat S.p.A.expressly disclaims and does not assume any liability inconnection with any inaccuracies in any of theseforward-looking statements or in connection with any useby any third party of such forward-looking statements.This document does not represent investment advice or arecommendation for the purchase or sale of financialproducts and/or of any kind of financial services. Finally,this document does not represent an investmentsolicitation in Italy, pursuant to Section 1, letter (t) ofLegislative Decree no. 58 of February 24, 1998, or in anyother country or state. The data related to Chrysler GroupLLC were independently prepared by Chrysler Group LLCand, to the extent they are related to the data publiclydisclosed on November 4, 2009 and to other ChryslerGroup LLC documents, are subject to the disclaimers ofthe presentation held on November 2009 and the forwardlooking statements set forth therein areherein incorporated by reference.

Safe Harbor Statement

Nov 29-Dec 2, 2010 Investor Meetings in Europe 3

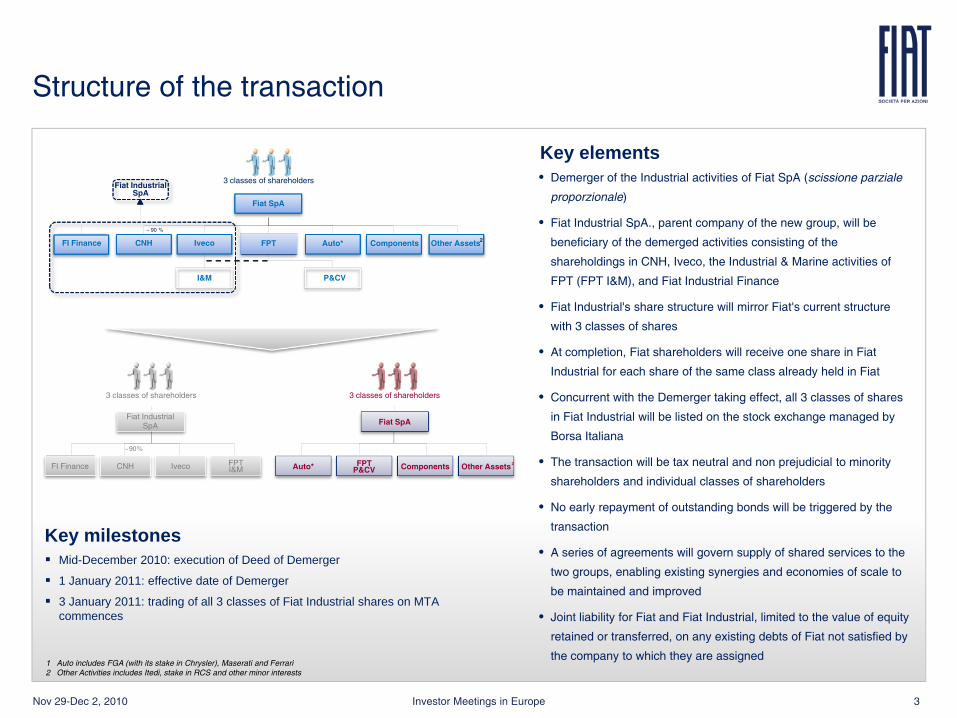

Structure of the transaction

• Demerger of the Industrial activities of Fiat SpA (scissione parziale

proporzionale)

• Fiat Industrial SpA., parent company of the new group, will be

beneficiary of the demerged activities consisting of the

shareholdings in CNH, Iveco, the Industrial & Marine activities of

FPT (FPT I&M), and Fiat Industrial Finance

• Fiat Industrial's share structure will mirror Fiat's current structure

with 3 classes of shares

• At completion, Fiat shareholders will receive one share in Fiat

Industrial for each share of the same class already held in Fiat

• Concurrent with the Demerger taking effect, all 3 classes of shares

in Fiat Industrial will be listed on the stock exchange managed by

Borsa Italiana

• The transaction will be tax neutral and non prejudicial to minority

shareholders and individual classes of shareholders

• No early repayment of outstanding bonds will be triggered by the

transaction

• A series of agreements will govern supply of shared services to the

two groups, enabling existing synergies and economies of scale to

be maintained and improved

• Joint liability for Fiat and Fiat Industrial, limited to the value of equity

retained or transferred, on any existing debts of Fiat not satisfied by

the company to which they are assigned1 Auto includes FGA (with its stake in Chrysler), Maserati and Ferrari2 Other Activities includes Itedi, stake in RCS and other minor interests

Fiat SpA

CNH Iveco FPT Auto* Components

~ 90 %

Fiat IndustrialSpA

Fiat Industrial SpA Fiat SpA

~90%

FI Finance Other Assets

I&M P&CV

3 classes of shareholders

3 classes of shareholders 3 classes of shareholders

2

CNH Iveco FPTI&M Auto*FI Finance Other Assets2FPT

P&CV Components

Key elements

Key milestonesMid-December 2010: execution of Deed of Demerger

1 January 2011: effective date of Demerger

3 January 2011: trading of all 3 classes of Fiat Industrial shares on MTA commences

Nov 29-Dec 2, 2010 Investor Meetings in Europe 4

Strong track record at FGA• Focus on profitable growth while improving market share• Remained profitable during downturn and addressed structural cost inefficiencies in Europe• Strengthened presence in European passenger cars, leader in European LCV• Dominant player in Brazil and well-positioned in fast growing LatAm market

New global paradigm with Chrysler: a game changing strategic transformation• Complementary products and technologies allowing for development of compelling full product lineup• Complementary geographies allowing for joint distribution • Providing scale to compete. Significant synergies from joint purchasing, joint product development, optimized shared production

capacity

Significant opportunities for growth and enhanced profitability at FGA• Poised for market share gains in recovering European market, backed by strong pipeline of new products starting from 2011• Well positioned to benefit from expanding emerging market presence in LatAm and other BRIC countries through JVs• Significant synergies from Chrysler integration and optimized production capacity to drive profitability

Ferrari and Maserati unique iconic assets• Widening margins and accelerating growth on the back of strong secular trends for the luxury sector

Profitable and growing powertrain and components businesses• Excellence in eco-friendly powertrain technologies: non-captive sales increasing from 9% to 24% in the 2009-14 period, leveraging

on technology leadership and extended products line-up• Industry leading capabilities in powertrain, lighting and electronics• Significant growth prospects from third party business and Chrysler integration

World class industrial base• Improved cost structure thanks to greater capacity utilization and World Class Manufacturing• Sharing of R&D between FGA, Chrysler and Fiat Industrial• Sustainability as a way of doing business

Investment highlightsDisciplined and focused global automotive player generating consistent profitability

1

2

3

4

5

6

Nov 29-Dec 2, 2010 Investor Meetings in Europe 5

Revenues and trading margin evolution

Track record of success at FGA

Industrial trading profit margin*

Source: companies annual reports* excluding non-recurring

2004

2009

19.7 19.5

23.7

26.8 26.9 26.3

0

5

10

15

20

25

30

-822

-281

291

803691

470

-1,000

-500

0

500

1,000

1,500

Net

rev

enue

s (€

bn)

Tra

ding

pro

fit (

€mn)

Trading margin (4.2)% (1.4)% 1.2% 3.0% 2.6% 1.8%

‘07 ’09‘08‘04 ‘06‘05

VW D

AI

PS

A RN

O

BM

W

NIS

TO

Y

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

(4.4)%

FGA, Ferrari & Maserati

TO

Y

PS

A

RN

O

DA

I

NIS

BM

W

VW

-6%

-4%

-2%

0%

2%

4%

2.4%FGA, Ferrari & Maserati

1

Nov 29-Dec 2, 2010 Investor Meetings in Europe 6

Significantly strengthened position in Europe

Market share trendFGA passenger cars

Sequential year-over-year market share gains in Europe (EU27+EFTA) until 2009

All brands repositioned in most EU countries (Fiat brand the most solid and Alfa Romeo requiring significant additional work)

2010 YTD market share performance negatively impacted by the disproportionate reduction for both smaller and LPG/CNG vehicles, where FGA is market leader, following the phase-out of eco-incentives

TerminatedNew

appointments

~1,550

Dec-04 Dec-09

~5,350

~2,100

~5,900

European dealer networkBackbone of retail channel now built

European network reshaped, enhanced and right-sized to support sales over 2006-09

Network financially healthier

Centralized Customer Care service implemented

Sound volume growth

1

28.1% 28.0%30.8% 31.4% 31.9% 32.8%

3.8%

2.8%3.4% 3.5%

3.9%4.3%

0%

2%

4%

6%

8%

10%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2004 2005 2006 2007 2008 2009

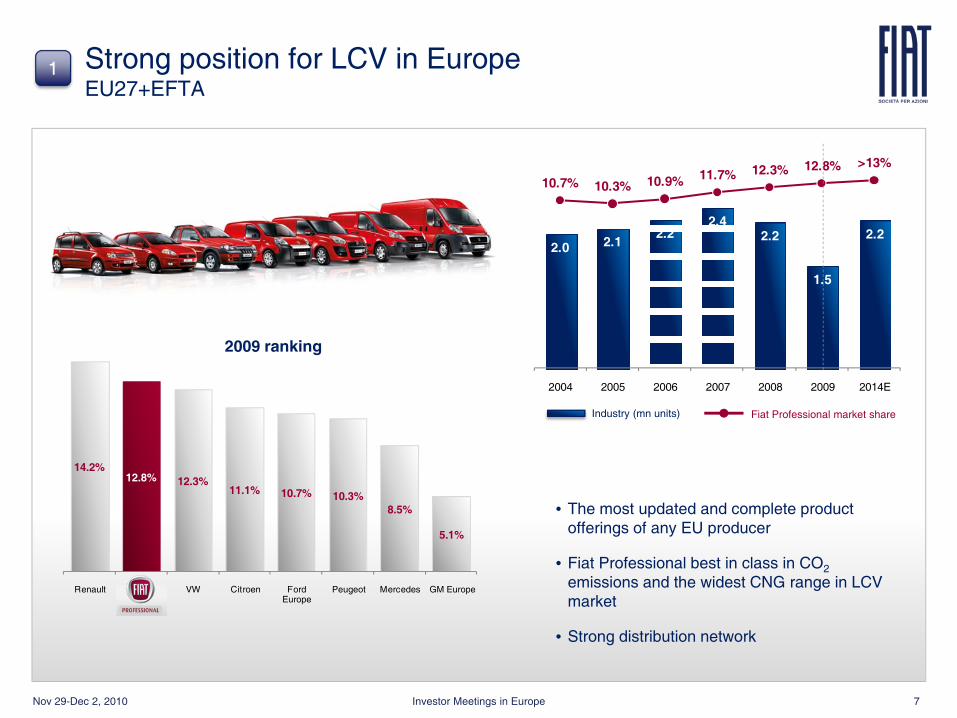

Nov 29-Dec 2, 2010 Investor Meetings in Europe 7

14.2%12.8% 12.3%

11.1% 10.7% 10.3%8.5%

5.1%

Renault Fiat Professional

VW Citroen Ford Europe

Peugeot Mercedes GM Europe

• The most updated and complete product offerings of any EU producer

• Fiat Professional best in class in CO2emissions and the widest CNG range in LCV market

• Strong distribution network

2.0 2.12.2

2.42.2

1.5

2.2

10.7% 10.3% 10.9% 11.7% 12.3% 12.8% >13%

2004 2005 2006 2007 2008 2009 2014E

Industry (mn units) Fiat Professional market share

2009 ranking

Strong position for LCV in EuropeEU27+EFTA

1

Nov 29-Dec 2, 2010 Investor Meetings in Europe 8

Long-standing leadership in Brazil and well-positioned for continued success

• Market leader in Brazil for 8 years

• Fiat perceived as a domestic player

• Expansive dealer network

• Highly versatile and flexible manufacturing footprint

• Significant barriers to replicate Fiat’s market position

Market Fiat

Brazil

Rest of LatAm

Fiat Market Share

3,010

4,300

7371,025

2009 2014E CAGR 2010-2014

6.5%7.4%

24.5% 23.8%

1,995

2,790

62 100

10.0%

6.9%

2009 2014E CAGR 2010-2014

3.1%3.6%

Units ‘000

Units ‘000

1

15.2%

24.5%

10%

15%

20%

25%

30%

90 92 94 96 98 00 02 04 06 08 09

Brazil market share

Nov 29-Dec 2, 2010 Investor Meetings in Europe 9

• Optimal capital allocation and improved capacity utilization through product portfolio integration

• Greater geographic penetration: North America for Fiat and Europe / Latin America for Chrysler

• Significant cost synergies particularly in purchasing and engineering, targeting ~€1.5 billion of cumulative savings for FGA through 2014

• Sharing of best practices in the area of WCM, engineering & design, quality and management

Scale advantages of a new global player without merger integration risks

The Chrysler integration - A game changing strategic transformation

2

Nov 29-Dec 2, 2010 Investor Meetings in Europe 10

2009A 2014E

2009A 2014E

Complementary global presenceCritical mass

China

50/50 FGA / GAC

India

50/50 Fiat India JV Automobiles Private Limited

Russia

Fiat / SOLLERS

13.7%11.0%

Fiat / Chrysler

09-14 CAGR: 12.3%

3.5

>6*

2009 2014E

1.3

2.3

2.8

4.3

FGA and Chrysler will achieve the necessary critical mass for continued success and profitability on a global scale

14.0%

8.8%

Units millions

FGA & Chrysler - A leading global auto player

* Including eliminations

2

Europe

9.0%12.1%

2009A 2014E

Canada

USA

2009A 2014EMexico

12.1%10.7%

2009A 2014EBrazil

24.6% 23.8%

Fiat Group Automobiles (including JVs)

Chrysler Group

Nov 29-Dec 2, 2010 Investor Meetings in Europe 11

Mini

Small

Compact

SUV

MPV

Pick-up

Large

Segment architecture

Fiat Group

Chrysler Group

Architecture origin

LCVs

Complementary integrated architecture and product strategy

Fiat and Chrysler each to focus on their core strengths

Maximize architecture convergence and components standardization

Fiat to move from 11 to 5 architectures by 2014

The 3 main architectures expected to exceed 1mn units each by 2014

2

Nov 29-Dec 2, 2010 Investor Meetings in Europe 12

Fiat & Chrysler technology and know-how sharingA win-win combination

Planetary automatic transmission with wide gear spread

Pentastar V6 Engine3.0L - 3.6L V6 24v

World Gas Engine 2.0-2.4L 16v

Cost Effective and Fuel EfficientL4 and V6 gasoline engines

MultiAir technology application to WGE & V6 Pentastar engines

(~1mn systems/year expected by 2014)

Off-road capability, Driveline disconnect

Electrification/hybridization

Significant synergies in hybrid and in electric propulsion for specific niche markets

Dual dry clutch transmission application to Chrysler C & D vehicle segments

CNG Fiat’s technological leadership in Europe, a key asset for US natural gas vehicle market

Diesel MultiJet II engines with High Pressure Common Rail technology

SDE & Fam.B 1.3L – 2.0L

Dual Dry Clutch Transmission 6/7-speed

Alternative Fuels CNG, LPG…

Fam.B1.8L 16v

Turbocharged engines with MultiAir and DI technologies

TwinAir & Fire0.9L – 1.4L 16v

2

Broader technology and products portfolio on diesel, AWD and transmissions

Nov 29-Dec 2, 2010 Investor Meetings in Europe 13

Extensive product launches support forecast volume gains in Europe

34 new models (of which 13 produced in NAFTA)17 major product interventions

Chrysler Group

Fiat Group

PRODUCT ACTIONS

Major modification

NEW MODEL PRODUCED BY

2010 2011 2012 2013 2014Strategy

Major focus on core A,B,C segments

Full integration with Chrysler

Comprehensive product line leveraging on Chrysler nameplates

Re-launch of Alfa Romeo brand, including strong European push

Return to North American market through Chrysler network

Continue building on sporty image

Positioning as a global brand

Enhance European and LatAm leadership

Brand

3

Nov 29-Dec 2, 2010 Investor Meetings in Europe 14

Volumes growth driven by market recovery and new products momentum

Source: IHS Global Insight and FGA estimatesNotes: (1) Include c.20k units in NAFTA and c.110k units in RoW. (2) Include c.85k units in NAFTA and c.10k units in RoW

Total growth

1.6Contract manufacturing

2.2

3.8

2009 2014EContract manufac.

Market driven growth

Market share growth

RoW / New markets

Reported sales by brand (Passenger Cars & LCVs)

Units millions

Market drivengrowth

(EU+LatAm)

0.6

0.2

0.2

0.3

Jeep(EU)

Market drivengrowth

(EU+LatAm)

Market drivengrowth(EU)

Market drivengrowth(EU)

Market sharegrowth

(EU+LatAm)

Market sharegrowth

(EU+LatAm)

Market sharegrowth(EU)

Market sharegrowth(EU)

RoW /New markets

RoW /New markets

0.3

1

2

3

Nov 29-Dec 2, 2010 Investor Meetings in Europe 15

Enablers in place to further expand emerging markets footprint

8,428

14,000

All models share single architecture

Targeting ~300k units by 2014 and 2% market

share

1,958

3,100

Sales target of ~280k units by 2014

Passenger cars: ~230k, 7% market shareLCVs: ~50k units

1,772

2,900

Sales target of ~130k units by 2014 or 5%

market share

50-50 JV with 50-50 JV with 50-50 JV with

Industry Volume Units ‘000Local market segment classification

€3.3bn investment in R&D and Capex jointly funded with partners through 2014 (90+% without requiring financial support from Fiat)

Focus on C, D and SUV segments, leveraging on the Jeep brand

Focus on B, C, D and SUV segments, leveraging on the Jeep brand

Focus on B and C segments

Strengthening dealer network

Industry Volume Units ‘000Local market segment classification

Industry Volume Units ‘000Local market segment classification

3

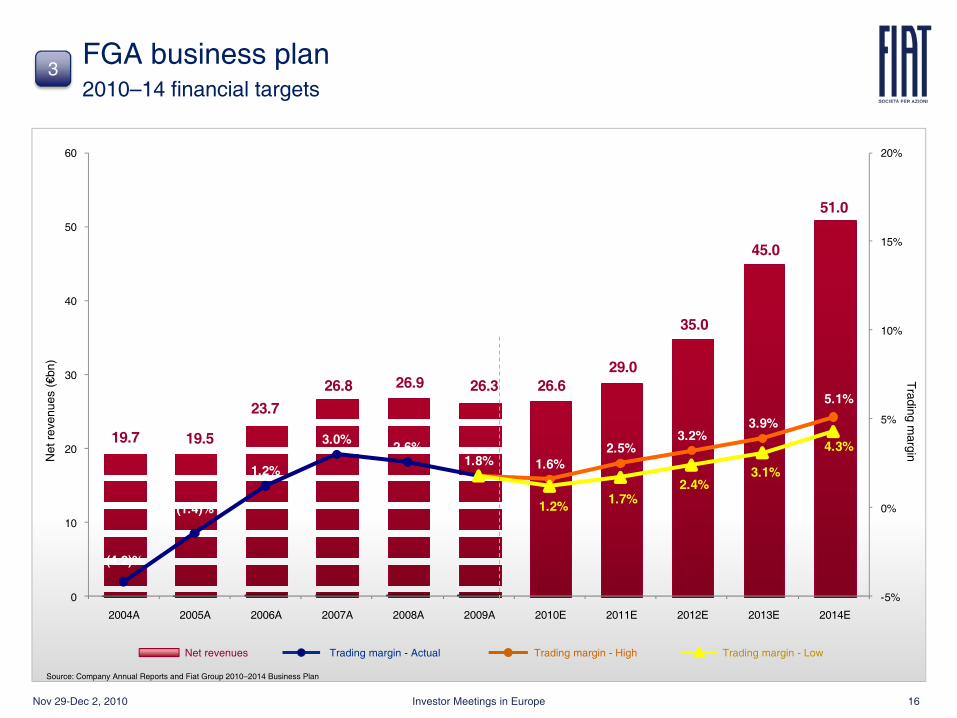

Nov 29-Dec 2, 2010 Investor Meetings in Europe 16

19.7 19.5

23.7

26.8 26.9 26.3 26.629.0

35.0

45.0

51.0

(4.2)%

(1.4)%

1.2%

3.0% 2.6%1.8% 1.6%

2.5%3.2%

3.9%

5.1%

1.2% 1.7%2.4%

3.1%

4.3%

0

10

20

30

40

50

60

-5%

0%

5%

10%

15%

20%

2004A 2005A 2006A 2007A 2008A 2009A 2010E 2011E 2012E 2013E 2014E

Net

rev

enue

s (€

bn)

Trading m

argin

Source: Company Annual Reports and Fiat Group 2010–2014 Business Plan

Net revenues Trading margin - High Trading margin - LowTrading margin - Actual

FGA business plan 2010–14 financial targets

3

Nov 29-Dec 2, 2010 Investor Meetings in Europe 17

Ferrari - Exclusive cars without compare

• Increase product differentiation to target new customers in the high end sport cars segment

• Keep innovating with a new model every year to sustain turnover and reinforce brand

• Selectively exploit Special Series to target high end customers and collectors

• Continuing search for opportunities in emerging markets, maintaining exclusivity in mature ones

• Personalization, one-off program, spare parts and after sales services improvement

• Production efficiencies and fixed cost optimization

• Further growth of Licensing, Retail & E-commerce and Ferrari Financial Services

StrategyInvestment highlights

• Ferrari: a legendary brand since 1947 with a strong relationship between road & racing cars

The only car manufacturer racing in Formula 1 since the beginning (1950)

The most successful Formula 1 constructor with, with its 15 world titles

• Exploiting significant growth from emerging markets

• Double digit profitability

Tra

ding

Mar

gin

4

12.2% 12.6%

15.9%17.6%

13.4%

0%

10%

20%

2005 2006 2007 2008 2009

Nov 29-Dec 2, 2010 Investor Meetings in Europe 18

• New generation of Quattroporte

• Extend luxury market coverage by entering high-end E and I segments

• Maintain and sustain GranTurismo and GranCabrio products in H segment

• Increase global market shares in all segments

• G segment: from 3% to 8%

• E segment: > 10%, in high-end

• I segment: > 4%

• H segment: > 10%, maintaining current top 3 ranking position

• Dealer network improvement to support volume growth

• Production efficiencies and fixed cost optimization

StrategyInvestment highlights

• Relevant PlayerMaserati is a relevant Player in the G and H Segment ranking within the Top 5 Premium Manufacturers

Tra

ding

Mar

gin

4

-15.9%

-6.4%

3.5%

8.7%

2.5%

-20%

-10%

0%

10%

2005 2006 2007 2008 2009

Maserati - Long and glorious heritage

• Unique positioning in sports and luxury segment

Launch of GranCabrio and GranTurismo MC Stradaleenlarged Maserati’s product offering

• Restructuring successfully completedTurn to profitability in 2007 (first year since 1993)

Targeting double digit profitability by end of plan period

Nov 29-Dec 2, 2010 Investor Meetings in Europe 19

1.51.7

1.9

2.3

2.6

2.22.1

2.2

2.8

3.73.9

-2.0%

4.1%

7.9%

12.8%

15.7%

11.5%10.2%

11.7%

16.1%14.2% 15.0%

9.8%10.9%

15.3%13.4%

14.2%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

2004A 2005A 2006A 2007A 2008A 2009A 2010E 2011E 2012E 2013E 2014E

Net

rev

enue

s (€

bn)

Trading m

argin

Source: Company Annual Reports and Fiat Group 2010–2014 Business Plan

Net revenues Trading margin - High Trading margin - LowTrading margin - Actual

Ferrari & Maserati2010-14 financial targets

4

Nov 29-Dec 2, 2010 Investor Meetings in Europe 20

• New breed of technologies to achieve CO2 reduction in combustion engines

2nd generation MultiAir technology

In-house development of advanced turbo charging Systems

MultiAir coupled with GDI technology

• Extension of MultiAir technology to diesel engines combined with new IP in EGR control functionality

• New high-efficiency downsized enginesFirst application of the 0.9L TwinAir Turbo in the Fiat 500 (Q3 2010)

Gasoline engines:Leveraging on MultiAir

Diesel engines:MultiJet II technology

Transmissions:New small DDCT

FPT P&CVExcellence in powertrain

• To extend dual-clutch transmission technology to A-B segments

• To be the basis for a compact, low-weight and low-cost Hybrid Powertrain

• Add-on option of baseline powertrain minimizing specific investments and R&D costs Base

Add-on electric motor

1.3L MultiJet II

Base Version

Hybrid Small

1.4L Fire MultiAir Turbo 1.8L GDI Turbo

Main benefits:Up to 25% CO2 emissions and fuel consumption reduction over a

higher displacement naturally aspirated engine

• Digital injection rate shaping

• Greater accuracy in fuel injection quantity control

Noise and driveability improvement

• Able to meet Euro 5 pollution standards

First application on Fiat Punto Evo (Q4 2009)

Main benefits:CO2 emissions up to 3% lower and

NOx emissions up to 20% lower

5

Nov 29-Dec 2, 2010 Investor Meetings in Europe 21

Fiat Group

German OEMs

French OEMs

US OEMs

Others

Lighting

Electronics

Powertrain

Revenues breakdown by product

2009A Revenues:

€4.5bn

Revenues by customer group (OE + AM)

Magneti Marelli - High value added components business

• Leadership in Lighting, Electronics and Powertrain

• Diverse automotive customer base

• Strong backlog

• Track record of growth and profitability

26%

11%

18%

45%

Exhaust SystemsSuspension SystemsPlastic Components and Modules Shock AbsorbersAfter Market

Revenues breakdown by customer

Fiat Group

German OEMs

French OEMs

US OEMs

Others

2010E Revenues:

€4.9bn

8%44%

8%

20%

20%

2014E Revenues:

€7.7bn13%

40%

10%

19%

18%

NonCaptiveNon

Captive

2010E 2014E

€7.7bn

€4.9bn

56%

44%

60%

40%

5

Nov 29-Dec 2, 2010 Investor Meetings in Europe 22

3.8 4.04.5

5.05.4

4.54.9

5.7

6.4

7.27.7

3.1%

4.0% 4.3% 4.3%

3.2%

0.6%

2.1%

3.7%

4.9%

5.9%

6.5%

1.7%

2.9%

4.1%

5.1%5.7%

0

1

2

3

4

5

6

7

8

0%

2%

4%

6%

8%

10%

2004A 2005A 2006A 2007A 2008A 2009A 2010E 2011E 2012E 2013E 2014E

Magneti Marelli - Roadmap to growth and enhanced profitability

Retain key role as technology supplier to Fiat Group

Leverage Fiat – Chrysler platform integration

Growth from emerging market and non-captive customers

Optimisation of global footprint and capacity utilisation

Historical financials and business plan targets

Net

rev

enue

s (€

bn)

Trading m

argin

5

Source: Company Annual Reports and Fiat Group 2010–2014 Business Plan

Net revenues Trading margin - High Trading margin - LowTrading margin - Actual

Nov 29-Dec 2, 2010 Investor Meetings in Europe 23

759

600199 13

Purchasing Engineering Sales of Powertrains

Royalties Total Cumulative Synergies

81%

40%

129%

60%

Rest of Europe

Italy

World class industrial base

• Maximize standardization of components

• Sub-system standardization

• Wide spread adoption of modern standard and modular architectures

Capacity utilization at FGA

• One standard

• Shared best practices throughout the enlarged Fiat Group

• Extension of World Class Manufacturing program to supplier plants

• ~190k new projects being implemented (230k cumulative projects since 2006)

• €1.9bn expected savings from WCM from 2010 to 2014 (€2.6bn cumulative savings since 2006)

FGA synergies thanks to Chrysler2010-2014 cumulative synergies

(€ in millions)

Sharing R&D

World Class Manufacturing

Capacity:Harbour definition: 235 days per annum/16 hours per dayTechnical definition: 280 days per annum/3 shifts per day

Harbour definition Technical definition

77%

89%

123%

133%

Rest of Europe

Italy

~1,5002009A 2014E

6

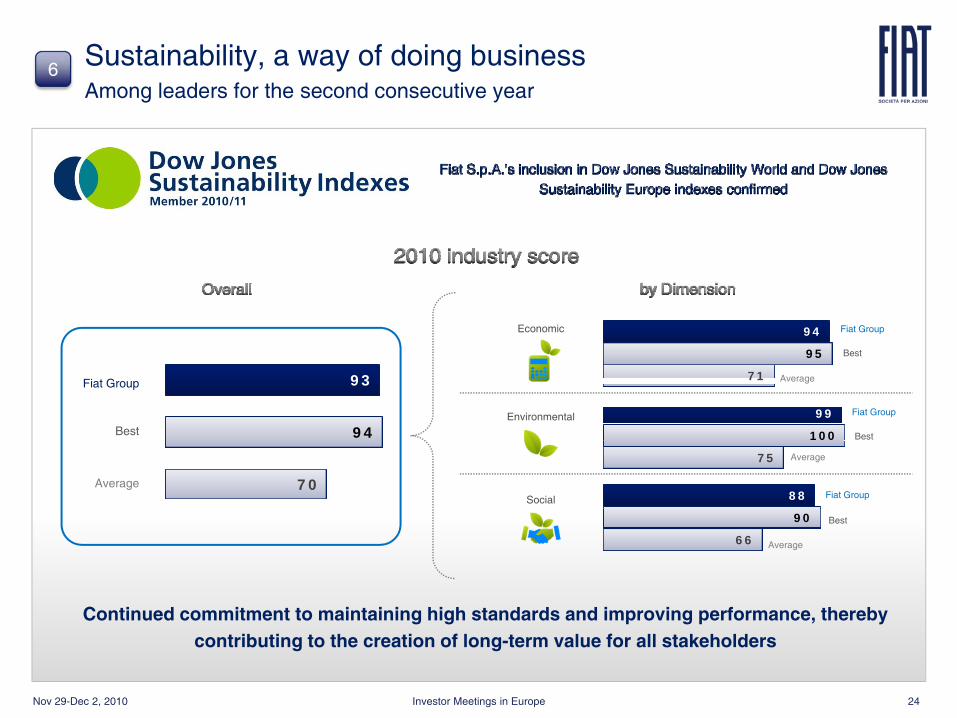

Nov 29-Dec 2, 2010 Investor Meetings in Europe 24

70

94

93

66

75

71

90

100

95

88

99

94

Fiat S.p.A.’s inclusion in Dow Jones Sustainability World and Dow Jones Sustainability Europe indexes confirmed

Best

Fiat Group

Average

Economic

Environmental

Social

Best

Fiat Group

Average

Best

Fiat Group

Average

Best

Fiat Group

Average

Sustainability, a way of doing businessAmong leaders for the second consecutive year

Continued commitment to maintaining high standards and improving performance, thereby contributing to the creation of long-term value for all stakeholders

6

Nov 29-Dec 2, 2010 Investor Meetings in Europe 25

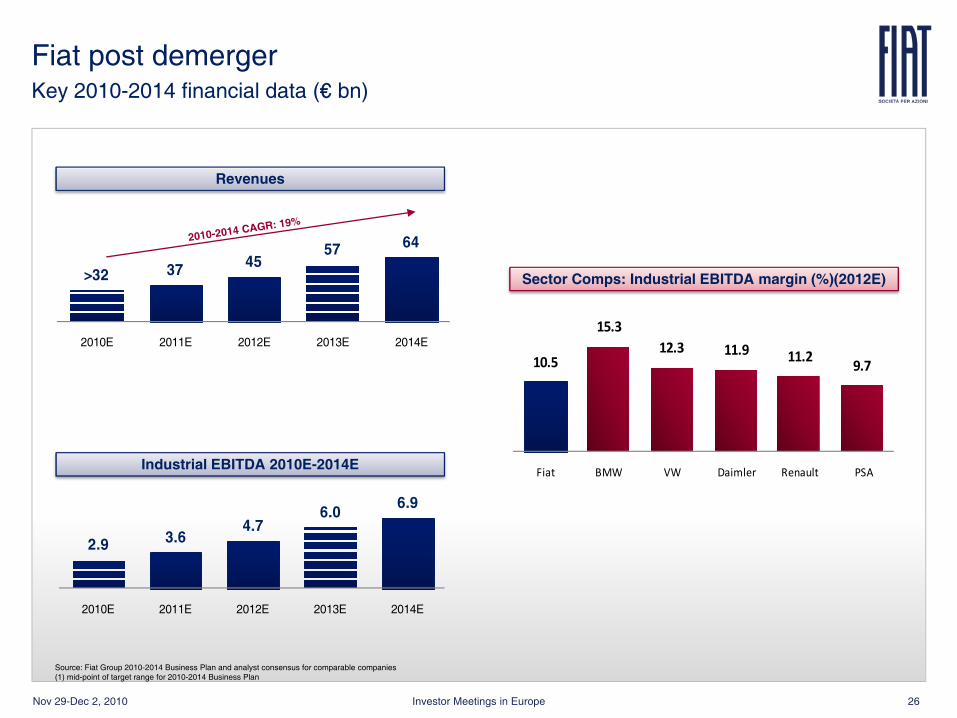

Fiat post demerger2010-14 financial targets

(€ bn) Sep YTD 2010 2010E 2011E 2012E 2013E 2014E

Revenues 26.4 >32 37 45 57 64

% growth rate n.a. n.a. <15.6% 21.6% 26.7% 12.3%

Trading profit 0.8 ~0.6 1.1 1.8 2.7 3.5

% margin 3.0% ~1.7% 2.8% 4.0% 4.7% 5.5%

Industrial EBITDA 2.4 2.9 3.6 4.7 6.0 6.9

% margin 9.0% ~9.1% 9.7% 10.4% 10.5% 10.8%

Capex 1.8 3.7 4.5 4.2 3.6 3.7

% of sales 6.9% ~11.6% 12.2% 9.3% 6.3% 5.8%Source: Fiat Group 2010–2014 Business Plan (mid-point of target range)

Profitability targets are realistic and can be achieved even with slower than expected top line growth

Expected financial and liquidity position (1 January 2011)

Industrial Activities

Liquidity

Bonds

Financial Services

Receivables from financing activities

Net Industrial Debt (consolidated)

Net Debt of Financial Services (consolidated)

Nov 29-Dec 2, 2010 Investor Meetings in Europe 26

Fiat post demergerKey 2010-2014 financial data (€ bn)

Revenues

>32 37 4557 64

2010E 2011E 2012E 2013E 2014E

2.9 3.64.7

6.06.9

2010E 2011E 2012E 2013E 2014E

Sector Comps: Industrial EBITDA margin (%)(2012E)

10.5

15.312.3 11.9 11.2

9.7

Fiat BMW VW Daimler Renault PSA

Source: Fiat Group 2010-2014 Business Plan and analyst consensus for comparable companies(1) mid-point of target range for 2010-2014 Business Plan

Industrial EBITDA 2010E-2014E

27Nov 29‐Dec 2, 2010 Investor Meetings in Europe

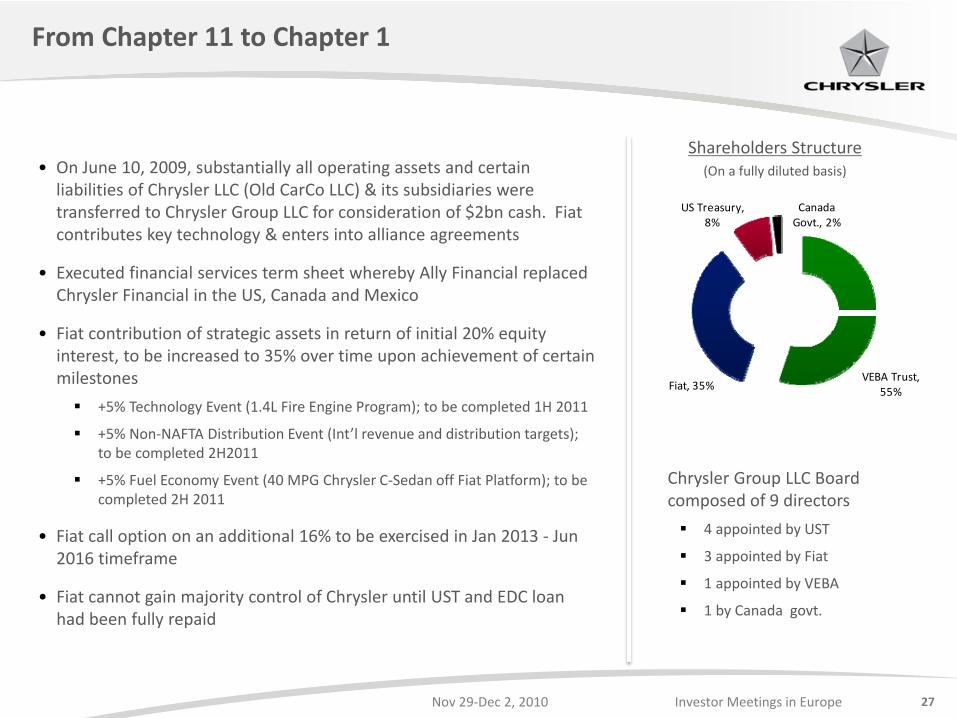

From Chapter 11 to Chapter 1

VEBA Trust, 55%Fiat, 35%

US Treasury, 8%

Canada Govt., 2%

Shareholders Structure(On a fully diluted basis)• On June 10, 2009, substantially all operating assets and certain

liabilities of Chrysler LLC (Old CarCo LLC) & its subsidiaries were transferred to Chrysler Group LLC for consideration of $2bn cash. Fiat contributes key technology & enters into alliance agreements

• Executed financial services term sheet whereby Ally Financial replaced Chrysler Financial in the US, Canada and Mexico

• Fiat contribution of strategic assets in return of initial 20% equity interest, to be increased to 35% over time upon achievement of certain milestones

+5% Technology Event (1.4L Fire Engine Program); to be completed 1H 2011

+5% Non‐NAFTA Distribution Event (Int’l revenue and distribution targets); to be completed 2H2011

+5% Fuel Economy Event (40 MPG Chrysler C‐Sedan off Fiat Platform); to be completed 2H 2011

• Fiat call option on an additional 16% to be exercised in Jan 2013 ‐ Jun 2016 timeframe

• Fiat cannot gain majority control of Chrysler until UST and EDC loan had been fully repaid

Chrysler Group LLC Board composed of 9 directors

4 appointed by UST

3 appointed by Fiat

1 appointed by VEBA

1 by Canada govt.

28Nov 29‐Dec 2, 2010 Investor Meetings in Europe

$ Billions

US GAAP

Chrysler 2010-2014 Business Plan targets announced November 4, 2009/1 Using Mid-Point Convention/2 Free cash flow after pension contributions and before debt changes/3 Change in net debt includes PIK interest accrued and paid as principal for ~$0.4B and accrued interest for VEBA /

HCT trust and other for ~0.6B. DoE loan application pending

Chrysler on track to meet 2010‐2014 business plan targets

• Integration with Fiat underway and ahead of plan

• Chrysler profitable and cash generative in 2010 YTD

Three consecutive quarters of improved performance

US market share recovery to 9.6% in 3Q 2010 from 8.0% in the same period of 2009

• Guidance upgraded for 2010

• Total volumes to increase to 2.8mn in 2014 driven by 13% share of 14.5mn U.S. market plus International volumes of ~500k

• Net income break‐even in 2011, increasing to ~$3bnby 2014

• Product spending (R&D and Capex) averaging $4.5bn per year

• Net debt to be reduced to $4bn by 2014/3

• TARP and EDC borrowing fully paid back by 2014

29Nov 29‐Dec 2, 2010 Investor Meetings in Europe

Chrysler is committed to significant investment in enhancing its product portfolio

Chrysler Group

Fiat Group

PLATFORM ORIGIN

27 new models

14 major product

interventions

PRODUCT ACTIONS

Major modification Refresh

IMPORTED VEHICLE

Fiat Group produced

• 16 new products or 75% of vehicle line renewed and refreshed by 2010

• 100% by 2012

2010 2011 2012 2013 2014

Nov 29-Dec 2, 2010 Investor Meetings in Europe 30

2010-14 financial targetsFiat post-demerger and Chrysler Group pro-forma

Fiat post-demerger

Trading margin range - Low Trading margin range - High

Chrysler Group Eliminations

Source: Fiat Group 2010–2014 Business Plan

Nov 29-Dec 2, 2010 Investor Meetings in Europe 31

FGA & Chrysler - a global player in the making

Builds on FGA’s strong track record and solid position in selected markets

Integration with Chrysler provides scale, global reach and complementary products and technologies

Significant scope for growth and enhanced profitability within the 2010 – 2014 business plan

Ferrari and Maserati unique iconic assets

Profitable and growing components businesses

Fiat Group: world class industrial base

Conclusions

Disciplined and focused automotive global player generating consistent profitability

1

2

3

4

5

6

7

Nov 29-Dec 2, 2010 Investor Meetings in Europe 32

Fiat Group Investor Relations team

Marco Auriemma phone: +39-011-006-3290 Vice President

Federico Donati phone: +39-011-006-2756

Alexandra Deschner phone: +39-011-006-2308

Maristella Borotto phone: +39-011-006-2709

fax: +39-011-006-3796

email: [email protected]

website: www.fiatgroup.com

Contacts

![La Scissione - Università... · della scissione, ma azioni o quote della società scissa [c.d. scissione asimmetrica] (comma 2). ... Aspetti Fiscali. PwC Imposte dirette Normativa](https://img.pdfslide.net/doc/110x75/5c6a27cd09d3f20c178c389d/la-scissione-universita-della-scissione-ma-azioni-o-quote-della-societa.jpg)