Embed Size (px)

Citation preview

Presented by:Planning & Analysis

1

Budget Revision Training - Background

Planning & Analysis Website: www.utrgv.edu/en-us/About/Administration/Finance-

and-Administration/Planning-and-Analysis

2

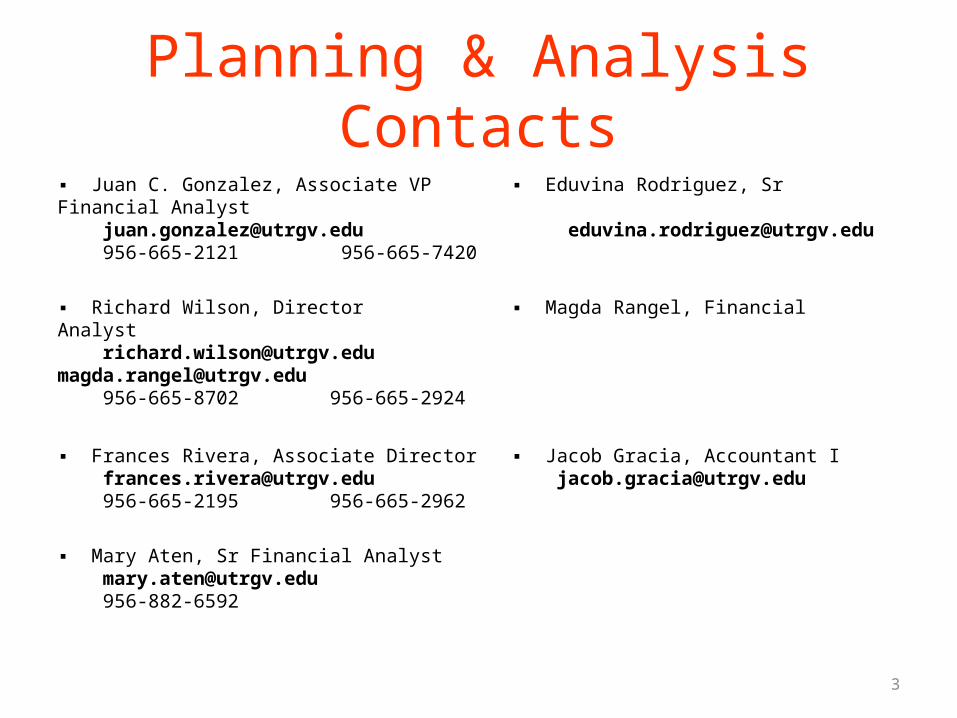

Planning & Analysis Contacts

3

▪ Juan C. Gonzalez, Associate VP ▪ Eduvina Rodriguez, Sr Financial Analyst [email protected] [email protected] 956-665-2121 956-665-7420

▪ Richard Wilson, Director ▪ Magda Rangel, Financial Analyst [email protected] [email protected] 956-665-8702 956-665-2924

▪ Frances Rivera, Associate Director ▪ Jacob Gracia, Accountant I [email protected] [email protected] 956-665-2195 956-665-2962

▪ Mary Aten, Sr Financial Analyst [email protected] 956-882-6592

Topics to be coveredBackground Information• GL Accounting String• Funds Checking• GL Funds Inquiry• Fiscal vs. Rollover Accounts• Budget Revisions Needed• Budget Revisions Not Allowed• Drill Down Procedure*

4

* Please note that Oracle is still being updated with UTRGV information therefore the screen shots will not fully reflect a UTRGV environment.

GL Accounting String

11.G0000.73160.110000042.53001.000060

Example: Planning & Analysis operating expense line

5

Fund

First Two Digits

11.G0000.73160.110000042.53001.000060

Ranges:11 – Educational & General (E&G)21 – Designated (DES)31 – Auxiliary (AUX)41 – Restricted (RES)51 – Loans 61 – Endowment71 – Plant81 – Agency

6

Funding SourceFive Characters – A letter and 4 numbers

11.G0000.73160.110000042.53001.000060

Examples:G0000 – E&G Unspecified (G1xxx is “Fund 1”; G2xxx is “Fund 2”)*(For E&G always use G0000 for budget revisions regardless of actual funding Source)D1000 – DesignatedD2000 – Service DepartmentsD4000 – Indirect Cost RecoveryA1000 – AES Student ServicesP0100 – Investment in PlantR1000 – Federal GrantR5000 – Private GrantZ2000 – Agency Scholarship(This list is NOT all inclusive)

7

Organization

Five digits

11.G0000.73160.110000042.53001.000060

Ranges:

72xxx – President73xxx – Finance & Administration74xxx - Research75xxx & 76xxx – Academic Affairs/Colleges/School of Medicine77xxx – Operations & Chief of Staff78xxx – Institutional Advancement79xxx – Govt & Community Relations

8

Project Value

Nine digits

11.G0000.73160.110000042.53001.000060

9

First digit of project will correspond to the fund it

belongs to.

Object Code

Five digits

11.G0000.73160.110000042.53001.000060

Examples:40001 – Revenue Budget 52001 – Employee Benefits44600 – Transfer In Intrafund 53001 – Operating Budget51001 – Single Incumbent Salaries 53425 – Transfer Out Intrafund51002 – Faculty Salaries 54001 – Books51003 – Longevity 55001 – Scholarships51010 – Pooled Salaries 57001 – Travel51101 – Wages 58001 – Capital Outlay

10

NACUBO Function

Six digit code used to classify expenses by function11.G0000.73160.110000042.53001.000060

NACUBO codes to be used by UTRGV000010 – Instruction000020 – Research000030 – Public Service000035 – Hospitals and Clinics000040 – Academic Support000050 – Student Services

000060 – Institutional Support000070 – Operation & Maintenance of Plant000080 – Scholarship000090 – Auxiliary 000100 – Depreciation & Amortization000110 – Agency

11

000000 – Unassigned (Used only for Revenue & Transfers)

(What it stands for: National Association of College and University Business Officers)

GL Funds CheckBudgeted Object Codes Summary Objects

▼ ▼ ▼ ▼ ▼ ▼40001 Revenue

40000 49999

99999

44600 Transfer In (Intrafund) 446xx Transfer In (Interfund) 51001 Single Incumbent Salaries

5000051000

52999

90000

51002 Faculty Salaries51003 Longevity Pay51010 Pooled Salaries 5000151101 Wages 5110052001 Benefits 5200053001 Operating Expense

53999

60000

53425 Transfer Out (Intrafund)534xx Transfer Out (Interfund)54001 Books 5499955001 Scholarship 5599957001 Travel 5799958001 Capital Outlay 5899959001 Merchandise for Resale 59999

12

The Project should not go into a deficit (negative amount) at the overall 99999 level

Oracle checks funds at the non-labor expense subtotal

60000 object code.

To pass funds check, budget changes between non-labor expense object codes are not required.

GL Funds Inquiry Screen

13

Budget – Encumbrance – Actual = Funds Available

Account Balance is the 99999 Total.

A negative amount is a deficit.

Selection Criteria:Budget should be REVISED.

To choose period type in first 3 letters and hit tab for list.

Hint: Start with summary level and then drill

down to detail.

Two Types of Accounts

Fiscal

• Funds lapse• Ending balances DO NOT

carryforward to the following year

Rollover

• Funds do not lapse• Ending balances DO

carryforward to the following year

14

Fiscal Accounts• E&G (11) & Auxiliary (31)• Funded by Expense Budget• Unencumbered balance lapses at fiscal yearend• Simply move budget to transfer funds between accounts within same fund• Budget revision transfer only requires a minimum of two lines

15

Rollover Accounts• Designated (21), Restricted (41), Plant (71), and Agency (81)• Funded by revenues (self-funded), transfers-in, and/or carryover balances• Balance before encumbrances carries forward to next year (non-lapsing)• Account is fully funded when revenue summary (49999) is non-negative• Transfer between accounts by actual funds transfer, not by simply moving

budget• Budget revision transfer requires a minimum of four lines

16

Rollover Accounts (continued)

17

◄ $200 revenue shortage

(after $800 received)

$200 ►revenue surplus

(after $1,200 received)

Budget column total always equals cumulative carryover from prior years.

When is a budget revision needed?

• To set up the initial budget for a project • To align expenditures with actual or anticipated revenues• To fully fund labor costs

– Position Changes– Benefits and Longevity (non-E&G accounts)

• To address or avoid funds checking failures in non-labor expenses

• To transfer funds between two or more accounts

18

Which types of transfers are not allowed?

• You should NOT do a transfer across funds (there are very few exceptions but please contact budget office for assistance)

19

E&G Fund

11

Designated Fund

21

Transfers not allowed (continued)

• DO NOT transfer funds in or out of the following subgroups:

• DO NOT transfer funds to be used for something that would violate the purpose of the funds.

Examples:▪ Endowment income restricted to payment of scholarships may not pay travel.▪ Fee revenue may not be used for purposes outside of the fee justification.

20

Prefix SUBGROUP Prefix SUBGROUP

120 Lab Fees 140 Transfers from other agencies

130 Special Lines/state transfers

24 Indirect Cost Recoveries

Drill Down Procedure

21

#1 Go into account at the Summary level

#3 Click on Period

Balances button

#2 click on

square

Drill Down Procedure (continued)

22

#6 You can choose between seeing the Budget lines, Actual

lines or Encumbrance lines.

#4 Place cursor on month you want to drill down into.

#5 Click on Tools to get drop down menu

Drill Down Procedure (continued)

23

#8 Click on Journal

button

#9 The journal is displayed#7

The list of journals which make up the amount will be listed.

Alternate Drill Down Procedure

1. Go into account at the summary level.2. Place cursor on line you wish to drill down into.3. Go to Tools on menu bar and select Detail Accounts from drop down menu.

4. Place cursor on the detail account line you wish to drill down into.

5. Go to Tools and select Period Balances

6. Place cursor on month you want to drill down into.

7. Go to Tools and select either Budget Lines, Actual Lines, or Encumbrance Lines based on type of inquiry.

24

25

Question Time

UTRGV