Embed Size (px)

Citation preview

Presenting a live 110‐minute teleconference with interactive Q&A

Recourse and Non‐Recourse Liability in Partnership Agreements Leveraging Section 752 to Minimize Tax Impact of Partnership Liability and Debt Allocations

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, SEPTEMBER 15, 2011

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Walter McGrail Senior Manager Cendrowski Selecky Bloomfield Hills MichWalter McGrail, Senior Manager, Cendrowski Selecky, Bloomfield Hills, Mich.

Andrew W. Ratts, Partner, Winston & Strawn, Chicago

Attendees seeking CPE credit must listen to the audio over the telephone.

Please refer to the instructions emailed to registrants for dial-in information. Attendees can still view the presentation slides online. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

For CLE credits, please let us know how many people are listening online by completing each of the following steps:

• Close the notification box

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the SEND button beside the box

For CPE credits, attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online.

Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Tips for Optimal Quality

S d Q litSound QualityFor this program, you must listen via the telephone by dialing 1-866-869-6667and entering your PIN when prompted. There will be no sound over the web connection.

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problemwe can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

Overview of Section 752 LiabilitiesOverview of Section 752 Liabilities and Interplay with IRC Section 704

AllocationsAllocations

Andrew W. RattsWinston Strawn

[email protected] 558 5991312.558.5991

September 15, 2011 5

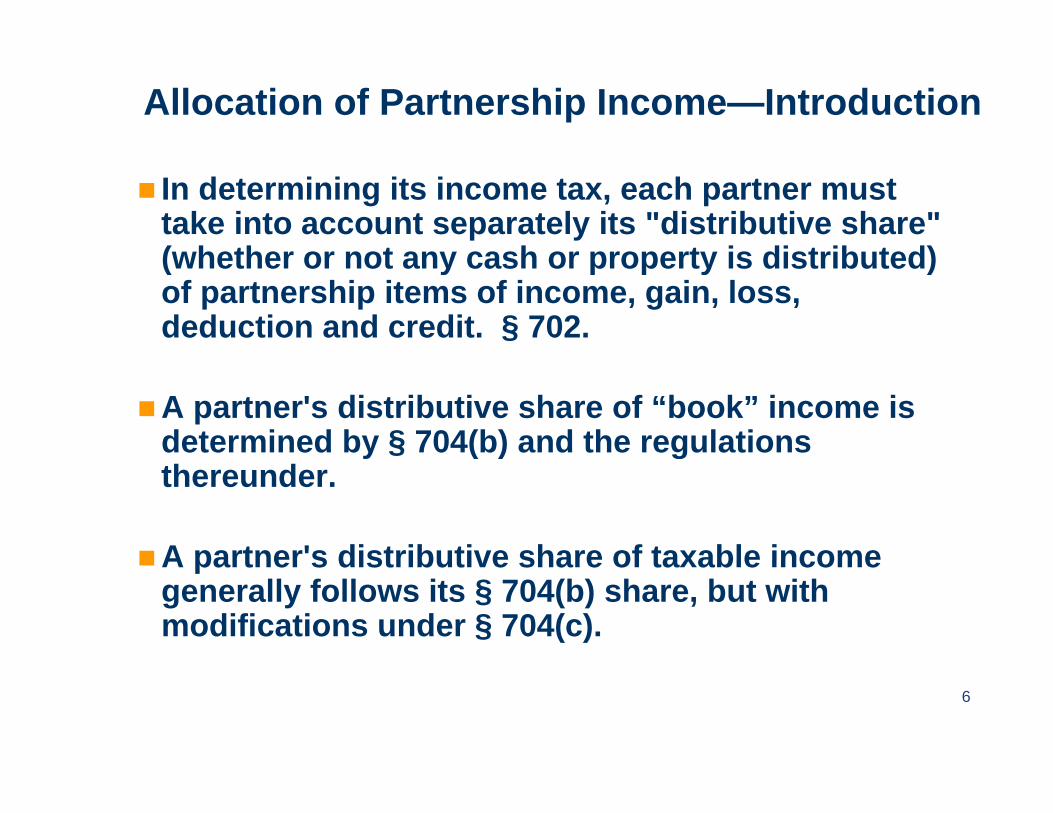

Allocation of Partnership Income—Introduction

In determining its income tax, each partner must take into account separately its "distributive share" (whether or not any cash or property is distributed)(whether or not any cash or property is distributed) of partnership items of income, gain, loss, deduction and credit. § 702.

A partner's distributive share of “book” income is determined by § 704(b) and the regulations y § ( ) gthereunder.

A partner's distributive share of taxable incomeA partner s distributive share of taxable income generally follows its § 704(b) share, but with modifications under § 704(c).

66

Allocation of Income—sec. 704(b)

Treas. Reg. § 1.704-1(b) provides the rules to determine whether an allocation provided y the partnership agreement will be respected for tax purposes as either

(i) having substantial economic effect or

(ii) being in accordance with the partners' interest in the partnership.

7

Allocation of Taxable Income—sec. 704(c)

Income, gain, loss and deduction with respect to property contributed by a partner to a partnership shall, under regulations, be shared among the partners so as to take account the variationbe shared among the partners so as to take account the variation between the basis of the property to the partnership and its FMV at the time of contribution. (§704(c)(1)(A))

Treas. Reg. § 1.704-3 provides three methods for eliminating book/tax disparities: the traditional method, the traditional method with curative allocations and the remedial methodwith curative allocations and the remedial method.

The partnership is also permitted to use any reasonable method of making the allocations. The partnership is not limited to the three methods described in the regulationslimited to the three methods described in the regulations.

The choice of method may be made on a property-by-property basis.

8

Allocation of Taxable Income - IRC §704(c)

Traditional Method Tax allocations to the noncontributing partnerTax allocations to the noncontributing partner

of cost recovery deductions with respect to the 704(c) property must equal book allocations of those deductions to the extentallocations of those deductions to the extent possible.

The “ceiling rule” provides that total income, gain, loss, or deduction may not exceed the partnership’s total income gain loss orpartnership’s total income, gain, loss, or deduction recognized for tax purposes.

9

Allocation of Taxable Income - IRC §704(c)

ExampleTraditional Method

10

Allocation of Taxable Income - IRC §704(c)

Traditional Method With Curative Allocations If the ceiling rule applies, the partnership looks for another g pp p p

tax item of the same amount an character as the item limited by the ceiling rule.

Remedial Allocation MethodRemedial Allocation Method Two elements.

The partnership steps into the shoes of the contributing partner for the portion of the book value equal to the adjustedpartner for the portion of the book value equal to the adjusted tax basis.

The remainder of the book value (book value less tax basis) is recovered as if it were a newly purchased asset placed in y p pservice at the time of the contribution.

11

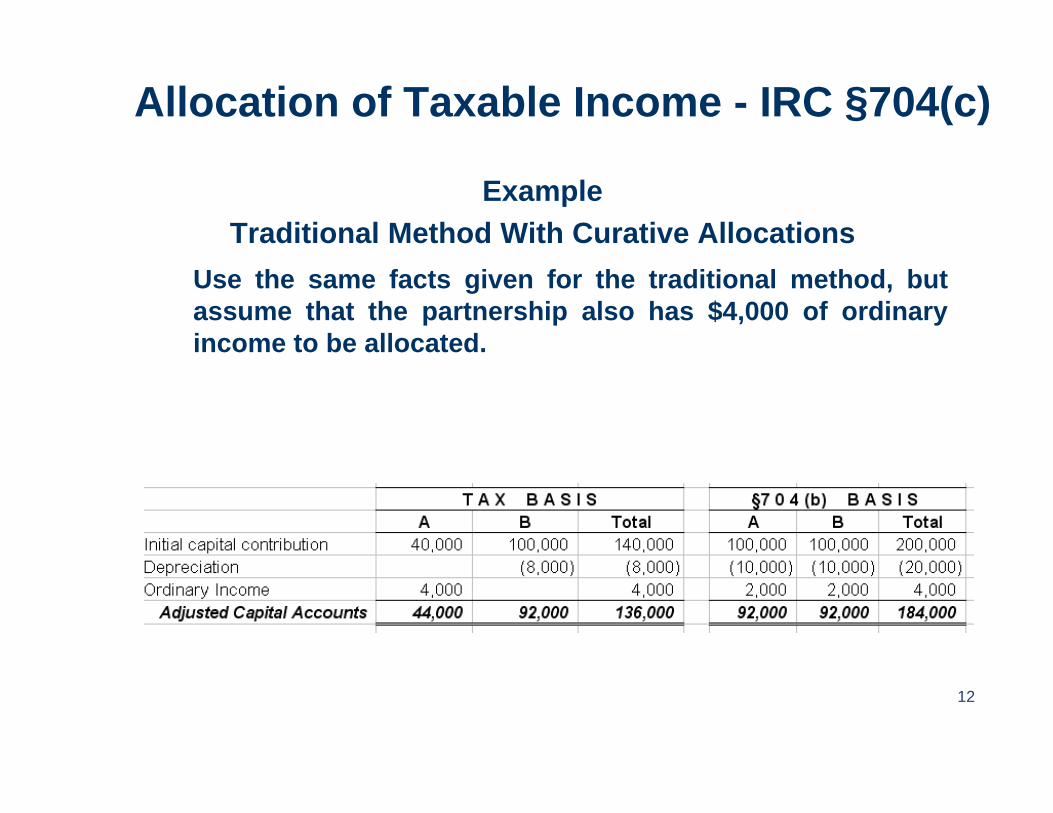

Allocation of Taxable Income - IRC §704(c)

ExampleTraditional Method With Curative Allocations

Use the same facts given for the traditional method, butassume that the partnership also has $4,000 of ordinaryincome to be allocated.

12

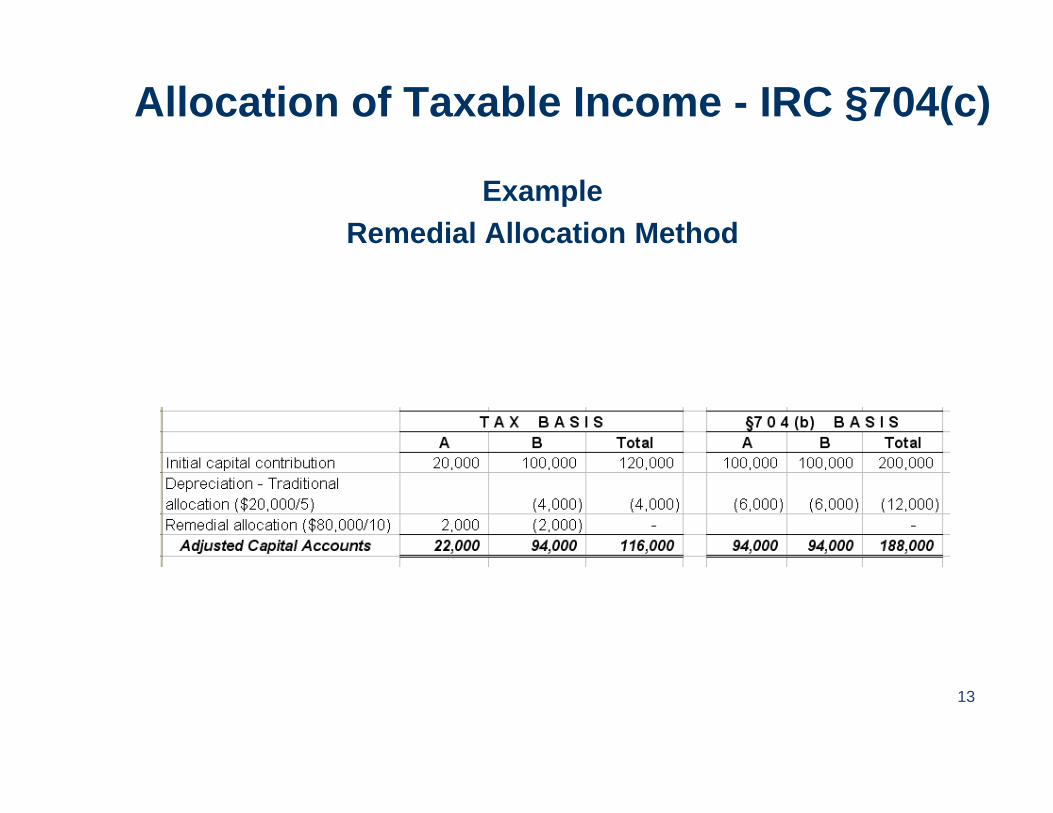

Allocation of Taxable Income - IRC §704(c)

ExampleRemedial Allocation Method

13

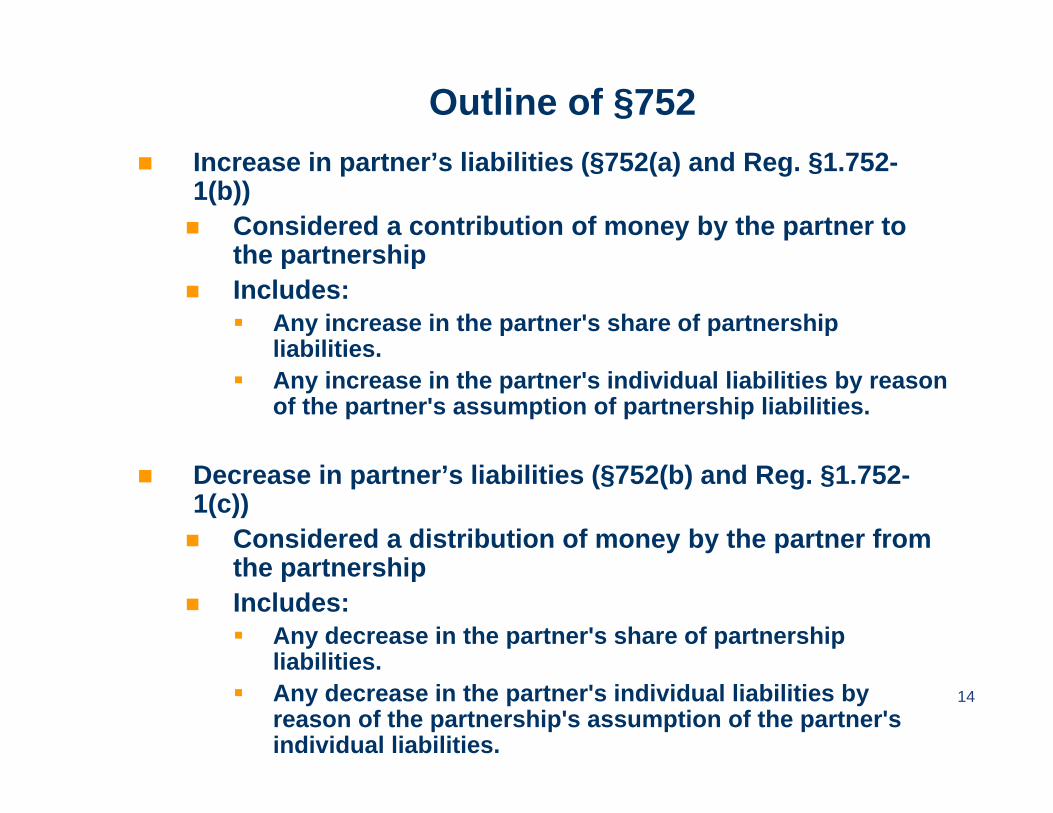

Outline of §752 Increase in partner’s liabilities (§752(a) and Reg. §1.752-

1(b)) Considered a contribution of money by the partner to

the partnershipthe partnership Includes:

Any increase in the partner's share of partnership liabilities.liabilities.

Any increase in the partner's individual liabilities by reason of the partner's assumption of partnership liabilities.

Decrease in partner’s liabilities (§752(b) and Reg. §1.752-1(c)) Considered a distribution of money by the partner from

th t hithe partnership Includes:

Any decrease in the partner's share of partnership liabilitiesliabilities.

Any decrease in the partner's individual liabilities by reason of the partnership's assumption of the partner's individual liabilities.

14

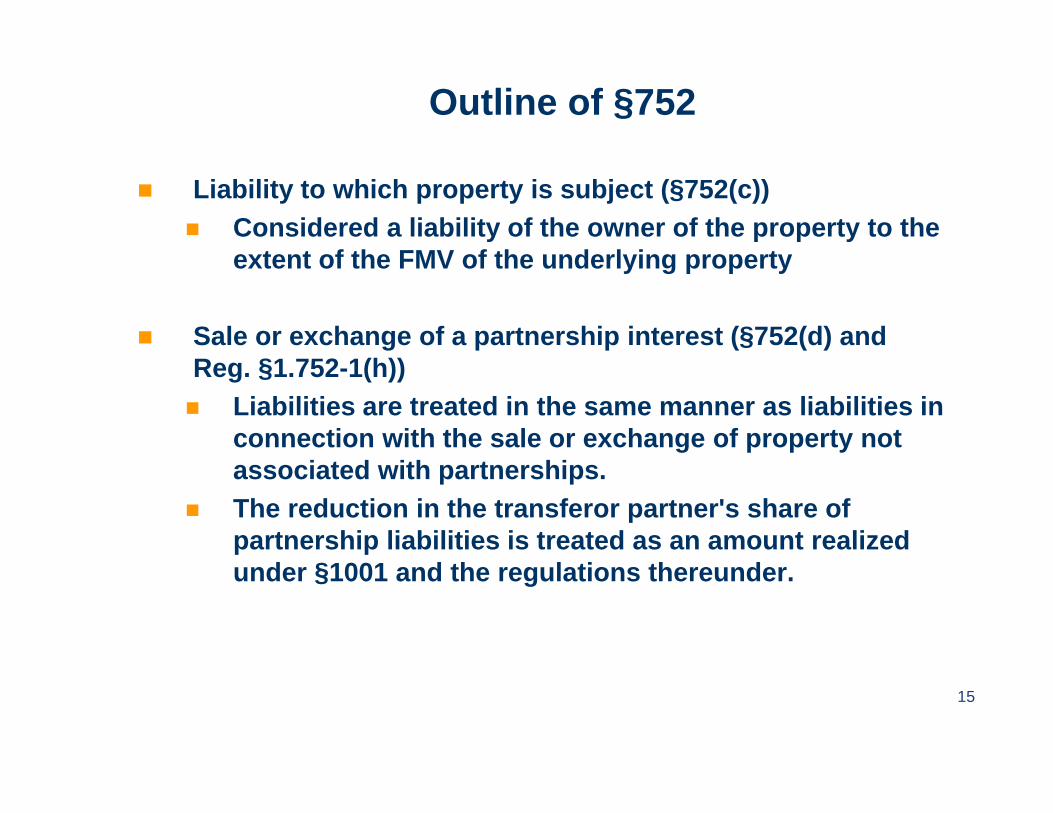

Outline of §752

Liability to which property is subject (§752(c)) Considered a liability of the owner of the property to the

t t f th FMV f th d l i textent of the FMV of the underlying property

Sale or exchange of a partnership interest (§752(d) and Reg. §1.752-1(h)) Liabilities are treated in the same manner as liabilities in

connection with the sale or exchange of property not associated with partnerships.

The reduction in the transferor partner's share of partnership liabilities is treated as an amount realized under §1001 and the regulations thereunder.

15

Liability Defined

An obligation is a liability only if, when, and to the extent that incurring the obligation: Creates or increases the basis of any obligor’s assets

(including cash); Gives rise to an immediate deduction of the obligor; or g ; Gives rise to an expense that is not deductible in

computing the obligor’s taxable income and is not properly chargeable to capital.properly chargeable to capital. An obligation is fixed or contingent obligation to

make payment without regard to whether the obligation is otherwise taken into account forobligation is otherwise taken into account for purposes of the Code.

16

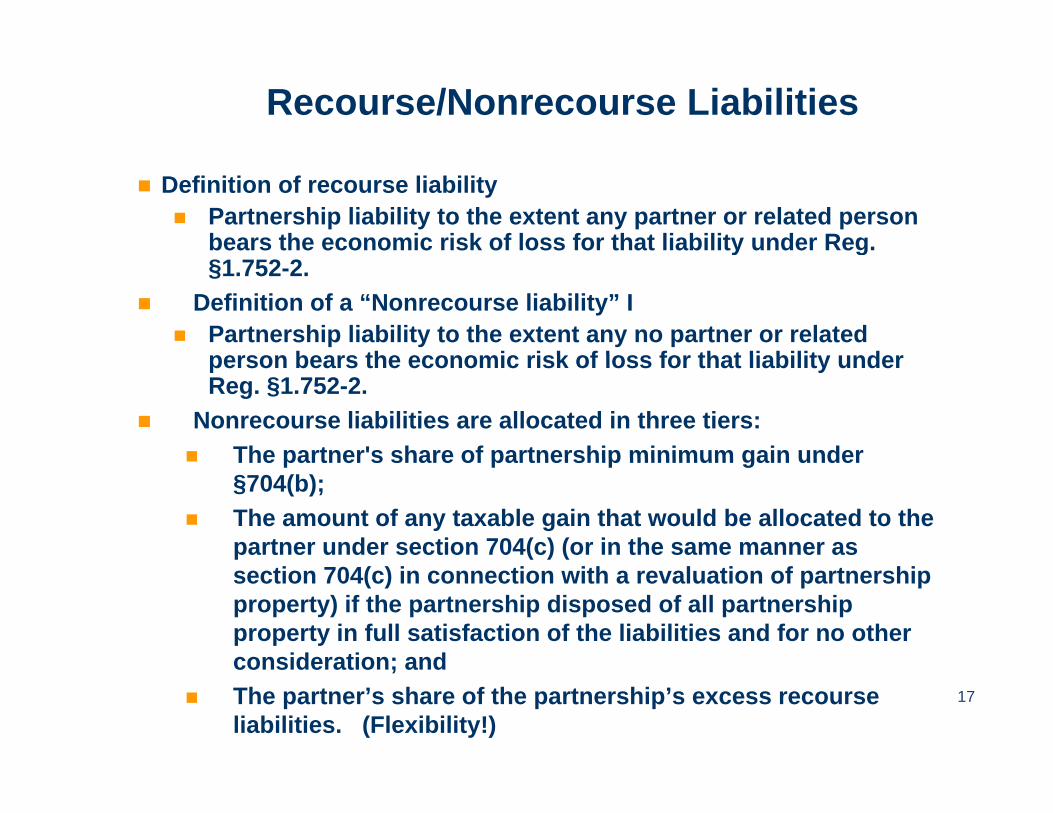

Recourse/Nonrecourse Liabilities

Definition of recourse liability Partnership liability to the extent any partner or related person

bears the economic risk of loss for that liability under Reg. y g§1.752-2.

Definition of a “Nonrecourse liability” I Partnership liability to the extent any no partner or related

person bears the economic risk of loss for that liabilit nderperson bears the economic risk of loss for that liability under Reg. §1.752-2.

Nonrecourse liabilities are allocated in three tiers: The partner's share of partnership minimum gain under The partner s share of partnership minimum gain under

§704(b); The amount of any taxable gain that would be allocated to the

partner under section 704(c) (or in the same manner as section 704(c) in connection with a revaluation of partnership property) if the partnership disposed of all partnership property in full satisfaction of the liabilities and for no other consideration; andconsideration; and

The partner’s share of the partnership’s excess recourse liabilities. (Flexibility!)

17

Allocations Attributable to Nonrecourse Liabilities (Reg. §1.704-2)

Deductions attributable to partnership nonrecourse liabilities (“nonrecourse deductions”) cannot have economic effecteconomic effect.

Nonrecourse deductions must be allocated in manner deemed to be in accordance with the partners’ interests in the partnership is provided in Reg §1 704-2(e)the partnership is provided in Reg. §1.704-2(e). Partnership agreement must complies with capital

account maintenance rules.P t hi t ll t Partnership agreement allocates nonrecourse deductions “in a manner that is reasonably consistent” with allocations that have substantial economic effect of some other significant item attributable to the propertysome other significant item attributable to the property securing the nonrecourse liabilities.

Partnership agreement must contain a “minimum gain chargeback” provisionchargeback provision.

18

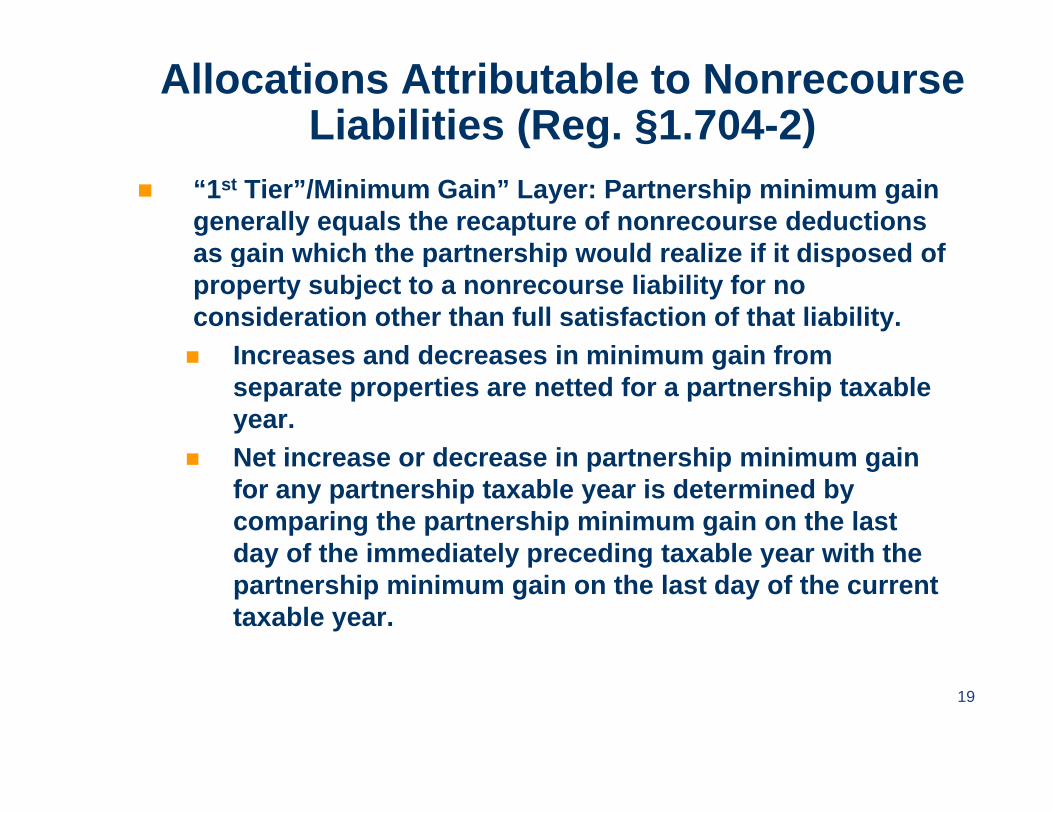

Allocations Attributable to Nonrecourse Liabilities (Reg. §1.704-2)

“1st Tier”/Minimum Gain” Layer: Partnership minimum gain generally equals the recapture of nonrecourse deductions as gain which the partnership would realize if it disposed ofas gain which the partnership would realize if it disposed of property subject to a nonrecourse liability for no consideration other than full satisfaction of that liability. Increases and decreases in minimum gain from Increases and decreases in minimum gain from

separate properties are netted for a partnership taxable year.

Net increase or decrease in partnership minimum gain Net increase or decrease in partnership minimum gain for any partnership taxable year is determined by comparing the partnership minimum gain on the last day of the immediately preceding taxable year with theday of the immediately preceding taxable year with the partnership minimum gain on the last day of the current taxable year.

19

Allocations Attributable to Nonrecourse Liabilities (Reg. §1.704-2)

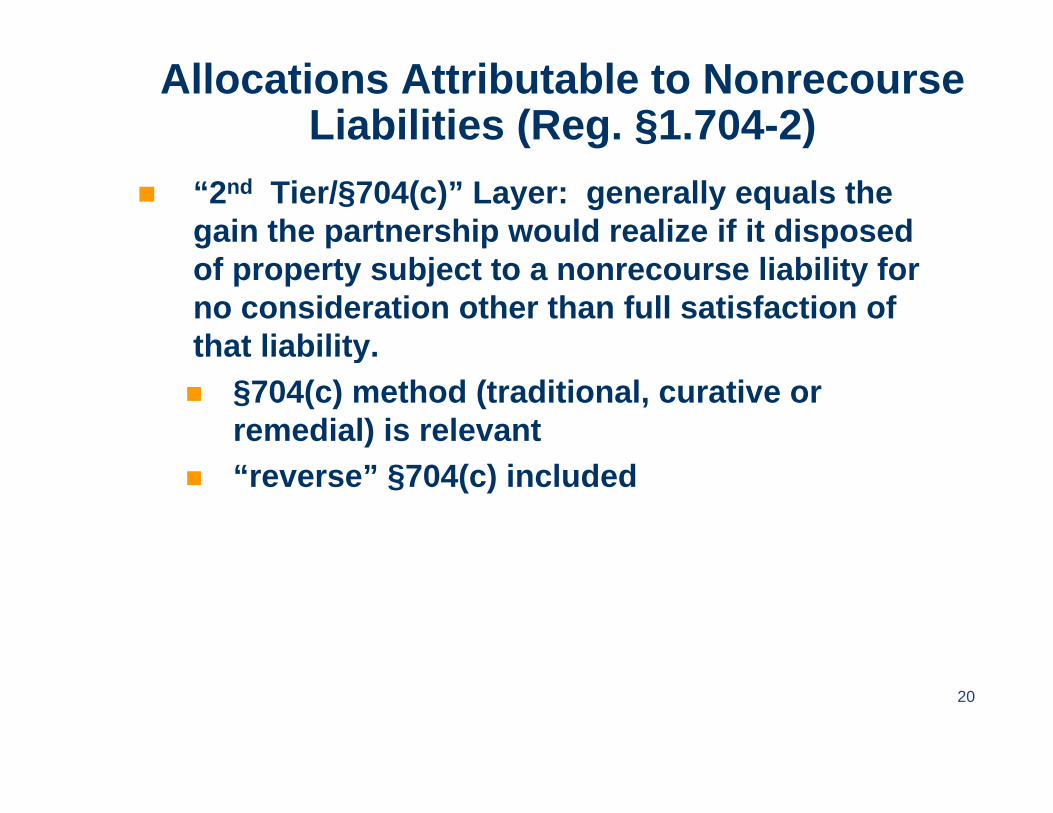

“2nd Tier/§704(c)” Layer: generally equals the gain the partnership would realize if it disposed of property subject to a nonrecourse liability for no consideration other than full satisfaction of that liability.that liability. §704(c) method (traditional, curative or

remedial) is relevant “reverse” §704(c) included

20

Allocations Attributable to Nonrecourse Liabilities (Reg. §1.704-2)

“3rd Tier/Excess” Layer: (very) generally “ in accordance with “partnership profits” in accordance with facts and circumstancescircumstances. Option 1: As such profits interests are specified , provided

that the specified profits interests “are reasonably consistent” with the allocations of some other significant item of gpartnership income or gain.

Option 2: In the manner in which it is reasonably expected that the deductions attributable to such nonrecourse liability

( § ( ))will be allocated (taking into account §704(c)). Option 3: Up to the amount of the remaining §704(c) gain

(including reverse §704(c) gain) not taking into account under the 2nd tier with any remaining amount under another methodthe 2 tier, with any remaining amount under another method.

A different method may be applied each year.

21

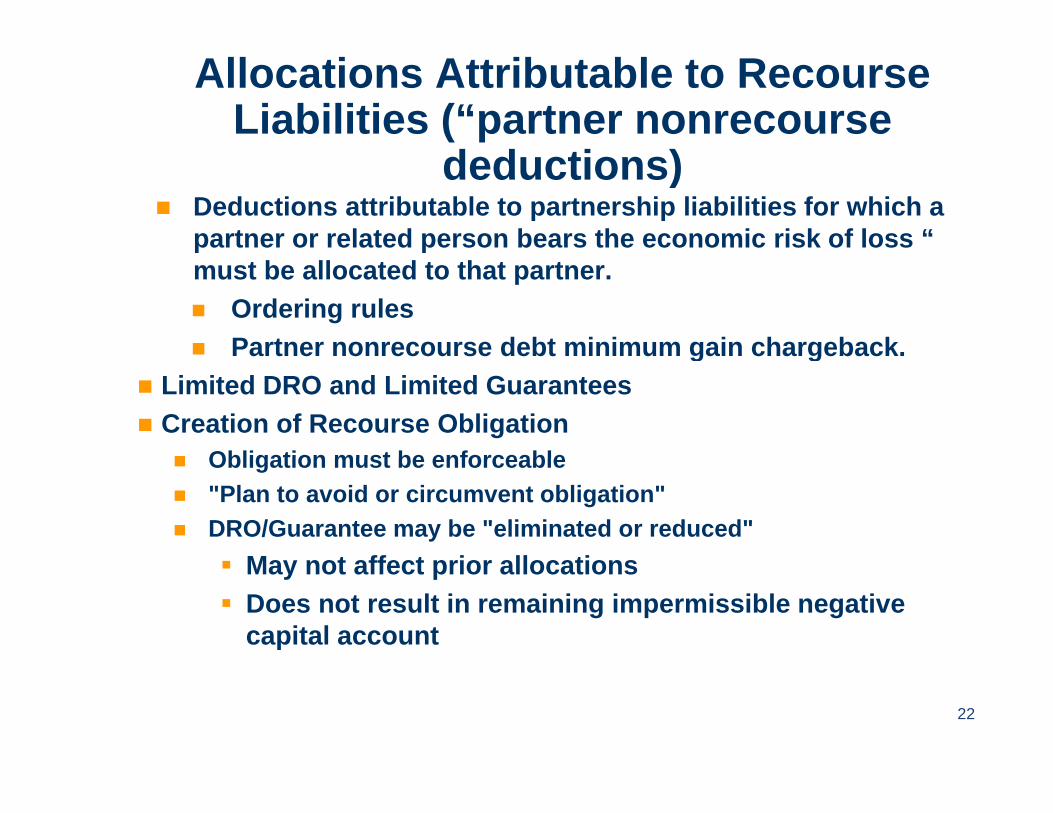

Allocations Attributable to Recourse Liabilities (“partner nonrecourse

d d ti )deductions) Deductions attributable to partnership liabilities for which a

partner or related person bears the economic risk of loss “ must be allocated to that partner. Ordering rules Partner nonrecourse debt minimum gain chargeback.Partner nonrecourse debt minimum gain chargeback.

Limited DRO and Limited Guarantees Creation of Recourse Obligation

Obligation must be enforceable Obligation must be enforceable "Plan to avoid or circumvent obligation" DRO/Guarantee may be "eliminated or reduced"

May not affect prior allocations May not affect prior allocations Does not result in remaining impermissible negative

capital account

22

Distinguishing Recourse v Non-Distinguishing Recourse v. Nonrecourse Liabilities and Debt

Walter [email protected]

248.540.5760

23

Basic Distinction Between Recourse and Nonrecourse Debt

• Basic Distinction between Recourse andBasic Distinction between Recourse and Nonrecourse Indebtedness (Generic)

Nonrecourse Loan a loan secured by– Nonrecourse Loan – a loan secured by property that limits the creditor to satisfying their claim with the secured property.p p y

– Recourse Loan – a loan which permits the creditor to satisfy their claim with other assets yof the debtor

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

24

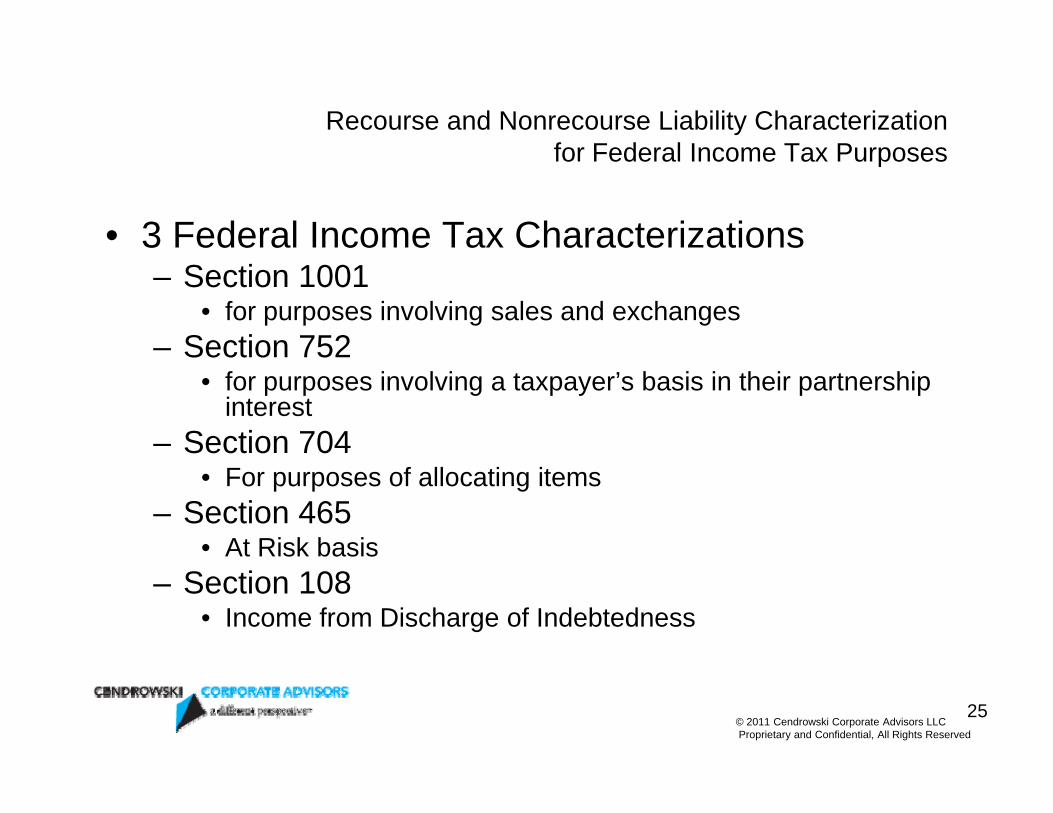

Recourse and Nonrecourse Liability Characterizationfor Federal Income Tax Purposesfor Federal Income Tax Purposes

• 3 Federal Income Tax Characterizations– Section 1001

• for purposes involving sales and exchanges– Section 752Section 752

• for purposes involving a taxpayer’s basis in their partnership interest

– Section 704 • For purposes of allocating items

– Section 465• At Risk basis

– Section 108• Income from Discharge of Indebtedness

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

25

Definitions of Recourse and Nonrecourse Under Section 1001

• No Statutory Definition under Section 1001y• No regulatory definitions• No developed case law definitions

M t t t t th t t t l d fi iti• Most commentators suggest that state law definitions likely apply (see the generic definition supra)

• Characterization as recourse or nonrecourse under Section 1001 have consequences– For the disposition of property subject to that liability.

Foreclosure and Com’r v.Tufts,– change to the terms of a liability that constitutes a significant

modification

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

26

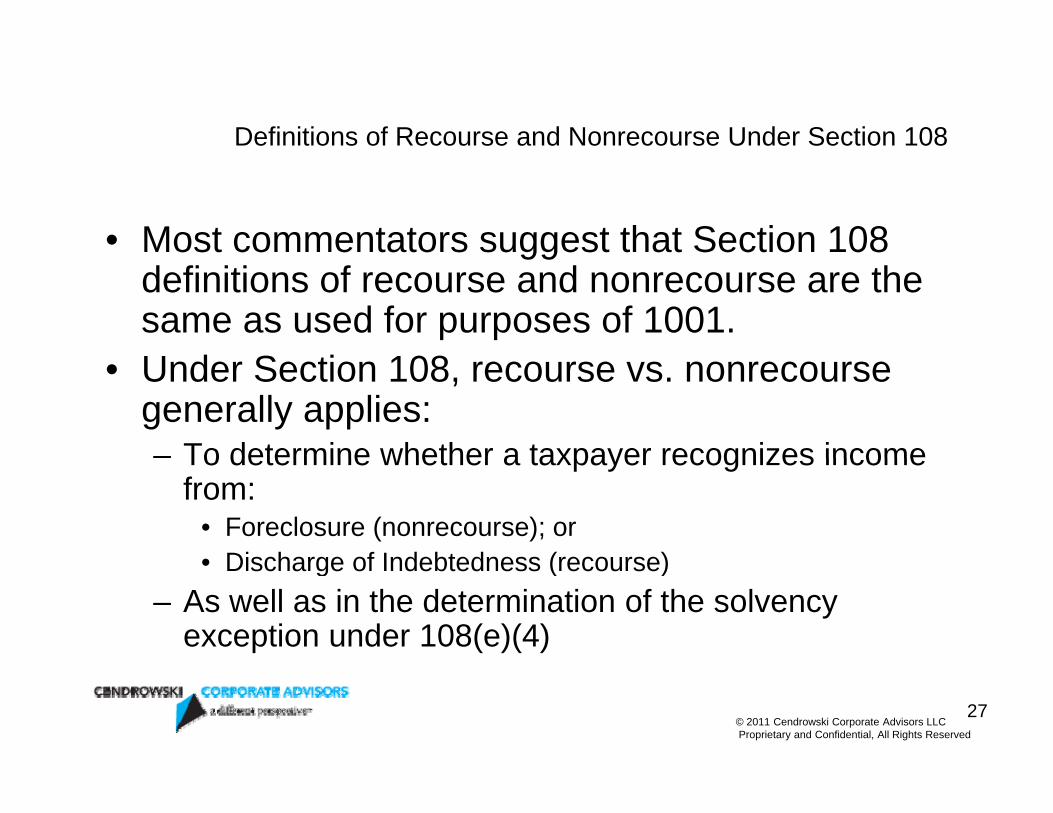

Definitions of Recourse and Nonrecourse Under Section 108

• Most commentators suggest that Section 108 ggdefinitions of recourse and nonrecourse are the same as used for purposes of 1001.U d S i 108• Under Section 108, recourse vs. nonrecourse generally applies:– To determine whether a taxpayer recognizes incomeTo determine whether a taxpayer recognizes income

from:• Foreclosure (nonrecourse); or• Discharge of Indebtedness (recourse)• Discharge of Indebtedness (recourse)

– As well as in the determination of the solvency exception under 108(e)(4)

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

27

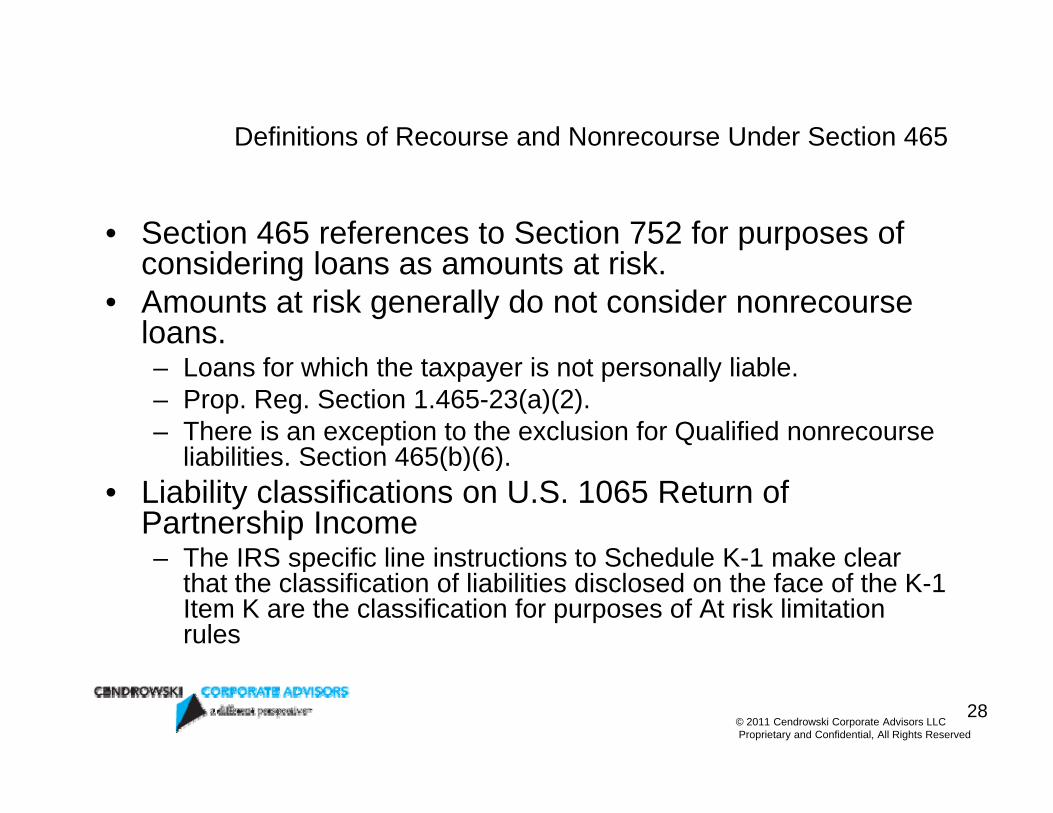

Definitions of Recourse and Nonrecourse Under Section 465

• Section 465 references to Section 752 for purposes of id i l t t i kconsidering loans as amounts at risk.

• Amounts at risk generally do not consider nonrecourse loans.– Loans for which the taxpayer is not personally liable.– Prop. Reg. Section 1.465-23(a)(2).– There is an exception to the exclusion for Qualified nonrecourse

liabilities Section 465(b)(6)liabilities. Section 465(b)(6).• Liability classifications on U.S. 1065 Return of

Partnership Income– The IRS specific line instructions to Schedule K-1 make clear– The IRS specific line instructions to Schedule K-1 make clear

that the classification of liabilities disclosed on the face of the K-1 Item K are the classification for purposes of At risk limitation rules

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

28

Definitions of Recourse and Nonrecourse Under Section 752

• Recourse liability: a liability for which anyRecourse liability: a liability for which any partner (or member of an LLC taxable as a partnership) or related person bears the p p) peconomic risk of loss for that liability.– Treas. Reg. Section 1.752-1(a)(1).

• Nonrecourse liability to the extent that no partner or related person bears the economic risk of loss for that liability.– Treas. Reg. Section 1.752-1(a)(2).

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

29

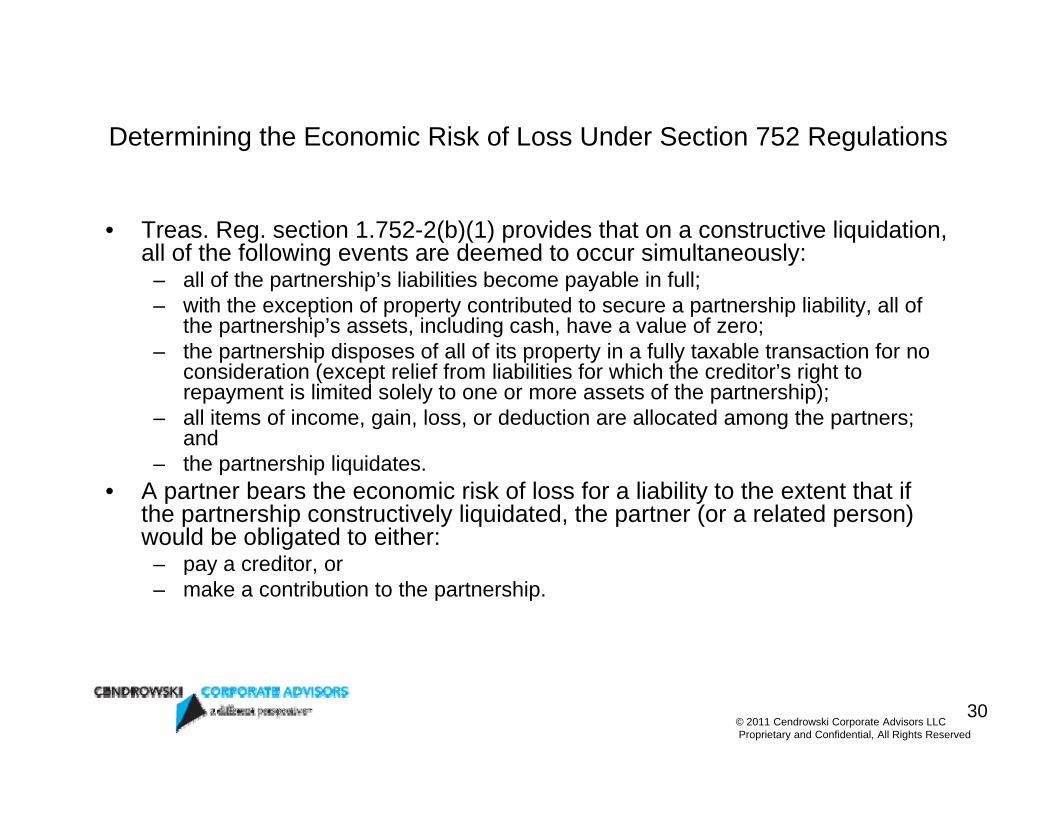

Determining the Economic Risk of Loss Under Section 752 Regulationsg g

• Treas. Reg. section 1.752-2(b)(1) provides that on a constructive liquidation, all of the following events are deemed to occur simultaneously:all of the following events are deemed to occur simultaneously:

– all of the partnership’s liabilities become payable in full;– with the exception of property contributed to secure a partnership liability, all of

the partnership’s assets, including cash, have a value of zero;– the partnership disposes of all of its property in a fully taxable transaction for nothe partnership disposes of all of its property in a fully taxable transaction for no

consideration (except relief from liabilities for which the creditor’s right to repayment is limited solely to one or more assets of the partnership);

– all items of income, gain, loss, or deduction are allocated among the partners; andth t hi li id t– the partnership liquidates.

• A partner bears the economic risk of loss for a liability to the extent that if the partnership constructively liquidated, the partner (or a related person) would be obligated to either:

pay a creditor or– pay a creditor, or– make a contribution to the partnership.

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

30

Agreements Affecting the Economic Risk of Loss under Section 752g g

• Reg. section 1.752-2(b)(3) provides that all statutory and contractual obligations relating to the partnership liability are taken into accountobligations relating to the partnership liability are taken into account for purposes of determining which partner bears the economic risk of loss, including: contractual obligations outside the partnership– Guarantees,– Indemnifications,– Reimbursement agreements,– Obligations to make a capital contribution or restore a deficit capital

account; and;– The operation of:

• State law provisions for contribution; • Agreements, including partnership and LLC operating agreements.

• A partner is also considered to bear the economic risk of loss for aA partner is also considered to bear the economic risk of loss for a partnership liability to the extent that the partner or a related person makes (or acquires an interest in) a nonrecourse loan to the partnership.

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

31

Specific Consideration and their Impact on Recourse and Nonrecourse Liabilities and Economic Risk of LossNonrecourse Liabilities and Economic Risk of Loss

• GPs vs. LPs. vs. LLCs– Wholly owned LLCs

• Guarantees vs. IndemnitiesE c lpation cla ses• Exculpation clauses– Spring recourse obligations

• ContingenciesContingencies• Interplay of the various code sections.

– Great Plains Gasification Associates v. Commissioner T C M 534 (2006)Commissioner, T.C.M. 534 (2006).

• Effects of classification as recourse or nonrecourse.

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

32

Recent Transactions and Cases Interpreting Section 752 Allocationsp g

Andrew W. Ratts

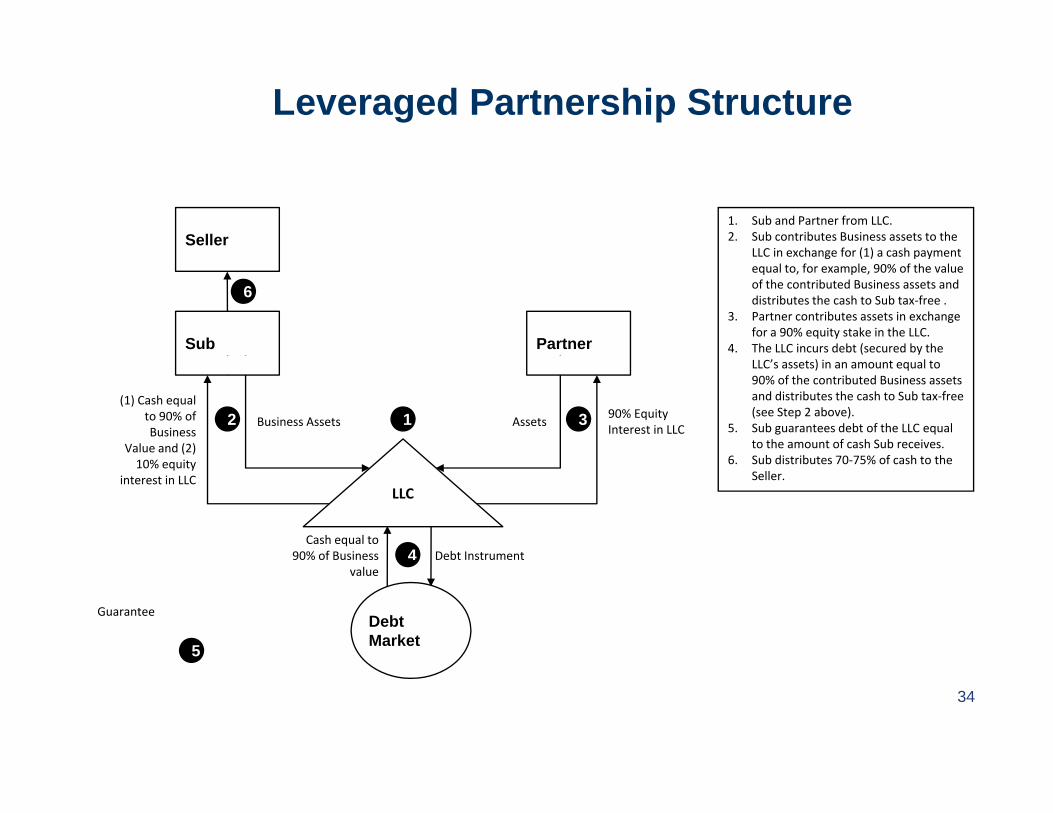

Leveraged Partnership Structure

Seller1. Sub and Partner from LLC.2. Sub contributes Business assets to the

LLC in exchange for (1) a cash payment

Sub Partner

LLC in exchange for (1) a cash payment equal to, for example, 90% of the value of the contributed Business assets and distributes the cash to Sub tax‐free .

3. Partner contributes assets in exchange for a 90% equity stake in the LLC.

4. The LLC incurs debt (secured by the

6

AssetsBusiness Assets90% EquityInterest in LLC

(1) Cash equal to 90% of Business

Value and (2)

LLC’s assets) in an amount equal to 90% of the contributed Business assets and distributes the cash to Sub tax‐free (see Step 2 above).

5. Sub guarantees debt of the LLC equal to the amount of cash Sub receives.

6 Sub distributes 70 75% of cash to the

12 3

LLC

Cash equal to 90% of Business Debt Instrument

10% equity interest in LLC

6. Sub distributes 70‐75% of cash to the Seller.

4

DebtMarket

value

Guarantee

5

34

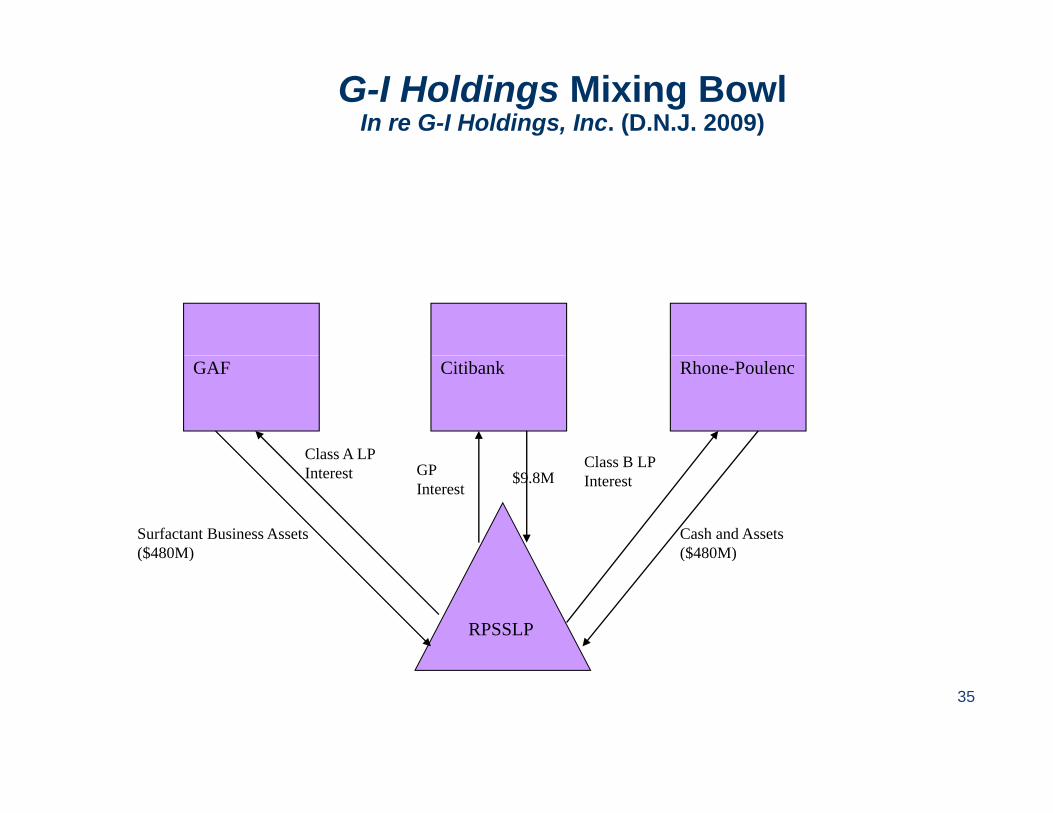

G-I Holdings Mixing Bowl In re G-I Holdings, Inc. (D.N.J. 2009)

Citibank Rhone-PoulencGAF

Class A LP Cl B LP

Surfactant Business Assets ($480M)

Class A LP Interest GP

Interest$9.8M

Class B LP Interest

Cash and Assets ($480M)

RPSSLP

( ) ( )

35

G-I Holdings Mixing Bowl

Rh P l

$460M

GAFCredit Suisse Rhone-Poulenc

Pledge of Class A LP Interest

Class A PriorityClass A Priority Return (Equal to Interest on Loan) Guarantee of Class

A Priority Return and additional financial obligations

RPSSLP

financial obligations under the Partnership Agreement

36

Partnership Anti-Abuse

Subchapter K is intended to permit taxpayers to conduct jointbusiness activity through a flexible economic arrangementwithout incurring an entity level taxwithout incurring an entity-level tax

Implicit in this intent are three requirements: The partnership must be bona fide and used for a

b t ti l b isubstantial business purpose; The transaction must be respected under a substance

over form analysis; and The resulting tax consequences must clearly reflect

income (or else the distortion must be clearlycontemplated by the applicable provision). Treas. Reg. §1 701 2(b)1.701-2(b)

Does compliance with regulatory provisions of Sections 707and 752 mean partnership anti-abuse rule does not apply?

37

IRS Response to Levpar Transactions

CCA 2002-46-014 (Aug. 8, 2002)Facts:Facts: Taxpayer's subsidiary Y, contributed assets to a

partnership, ZZ b d f di f b k d Z borrowed money from a syndicate of banks, andmade a special distribution to Y. Y then distributedthis amount as a dividend to Taxpayer

Y guaranteed Z's liability, increasing its basis in itsinterest in Z (which allowed Y to avoid recognizingincome on the distribution from Z))

38

C.C.A. 2002-46-014, cont.

IRS disregarded Y's guarantee, finding that Y's lackof capital and the restrictive prerequisites for Y'sperformance under the guarantee suggested theexistence of a plan to avoid any performanceobligation from Y on the guaranteeobligation from Y on the guarantee

Without the guarantee, the liability of thepartnership was treated as nonrecourse, which

ll d th t ti t b t t dgenerally caused the transaction to be treated as adisguised sale

39

C.C.A. 2002-46-014, cont.

The IRS also sought to disregard the transaction on thefollowing grounds: Partnership Anti Abuse Rule: transaction was entered Partnership Anti-Abuse Rule: transaction was entered

into with a principal purpose of reducing the partners'federal tax liability

Substance-Over-Form: taxpayer effectively parted with Substance Over Form: taxpayer effectively parted withthe benefits and burdens of the assets while receivingcash equal to the value of the assets, thus taxpayershould be taxed in accordance with the substance of thetransaction (a sale) and not its form (contrib tion andtransaction (a sale) and not its form (contribution anddistribution)

Sham Partnership: facts did not show that taxpayer andother nominal partner in good faith and acting with aother nominal partner in good faith and acting with abusiness purpose intended to join together in the conductof a business

40

Canal Corp. vs. Commissioner, 135 T.C. No. 9 (2010)

The court held that the formation of a joint venturebetween a subsidiary of Chesapeake Corp. (now known

C l C ) d G i P ifi ("GP")as Canal Corp.), and Georgia Pacific ("GP"), wasactually a disguised sale under Section 707(a)(2)(B).

As a result, Chesapeake had to include an additional$524 million of income on its consolidated return.

41

Canal Corp. vs. Commissioner

Wisconsin Tissue Mills Inc. ("WISCO"), a wholly-ownedsubsidiary of Chesapeake, owned and operated a

i l ti b i th t Ch k t d tcommercial tissue business that Chesapeake wanted toget rid of.

42

Canal Corporation Structure

WISCO and GP formed Georgia Pacific Tissue LLC. GP contributed its tissue business assets with an agreed

l f $376 4 illi i h f 95% i t tvalue of $376.4 million in exchange for a 95% interest. WISCO contributed its tissue business assets with an agreed

value of $775 million in exchange for a 5% interest. On the contribution date, the LLC borrowed $755.2 million

from BoA and immediately distributed the borrowed funds to WISCO as a special distribution.

WISCO received a "should" opinion from PwC regarding the tax-free nature of the transaction.

43

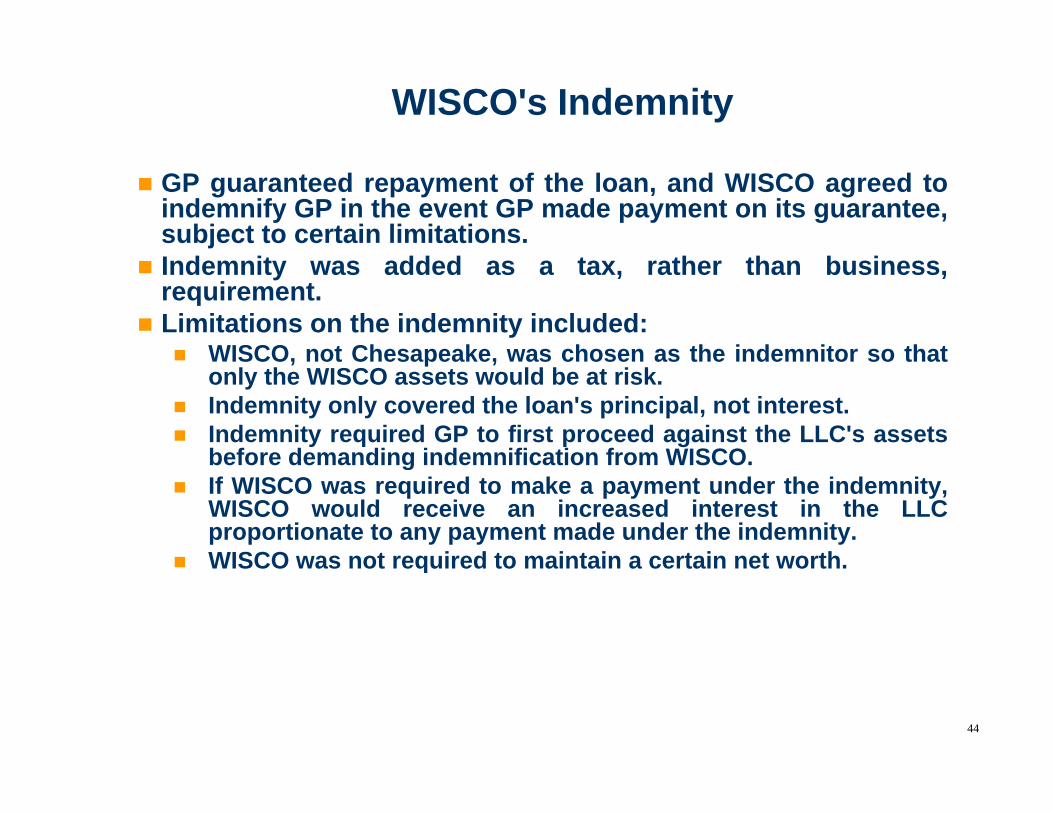

WISCO's Indemnity

GP guaranteed repayment of the loan, and WISCO agreed toindemnify GP in the event GP made payment on its guarantee,subject to certain limitations.

Indemnity was added as a tax, rather than business,requirement.

Limitations on the indemnity included: WISCO not Chesapeake was chosen as the indemnitor so that WISCO, not Chesapeake, was chosen as the indemnitor so that

only the WISCO assets would be at risk. Indemnity only covered the loan's principal, not interest. Indemnity required GP to first proceed against the LLC's assets

before demanding indemnification from WISCObefore demanding indemnification from WISCO. If WISCO was required to make a payment under the indemnity,

WISCO would receive an increased interest in the LLCproportionate to any payment made under the indemnity.

WISCO was not required to maintain a certain net worth WISCO was not required to maintain a certain net worth.

44

WISCO's Assets & Liabilities

WISCO used the distributed funds to repay certain intercompany debt and to pay a dividend.WISCO l l d $151 illi t Ch k i h WISCO also loaned $151 million to Chesapeake in exchange for a promissory note.

Following the transaction, WISCO's assets consisted of the $151 illi i t t d t j t th $6$151 million intercompany note and a corporate jet worth $6 million (or approximately 21% of the maximum exposure under the indemnity).

In addition WISCO was still subject to certain environmental In addition, WISCO was still subject to certain environmental liabilities and was a guarantor on a Chesapeake line of credit.

45

Tax Court Analysis

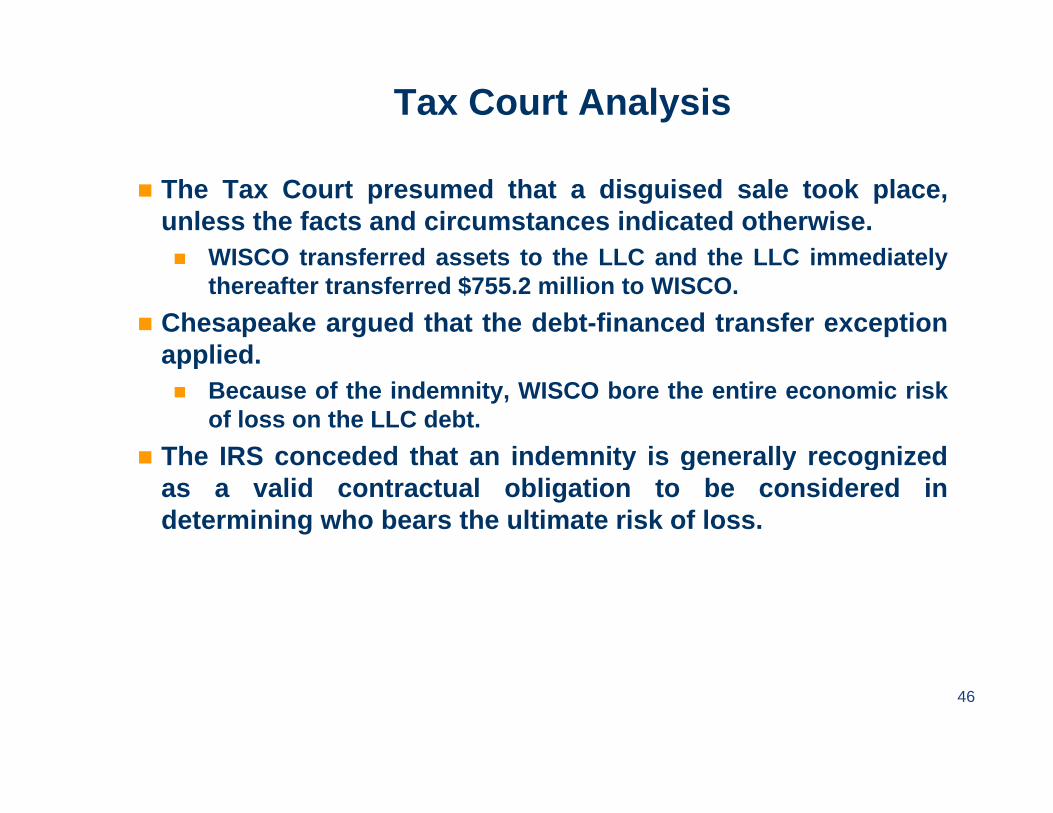

The Tax Court presumed that a disguised sale took place,unless the facts and circumstances indicated otherwise.

WISCO transferred assets to the LLC and the LLC immediately WISCO transferred assets to the LLC and the LLC immediatelythereafter transferred $755.2 million to WISCO.

Chesapeake argued that the debt-financed transfer exceptionappliedapplied. Because of the indemnity, WISCO bore the entire economic risk

of loss on the LLC debt. The IRS conceded that an indemnity is generally recognized The IRS conceded that an indemnity is generally recognized

as a valid contractual obligation to be considered indetermining who bears the ultimate risk of loss.

46

Tax Court Analysis

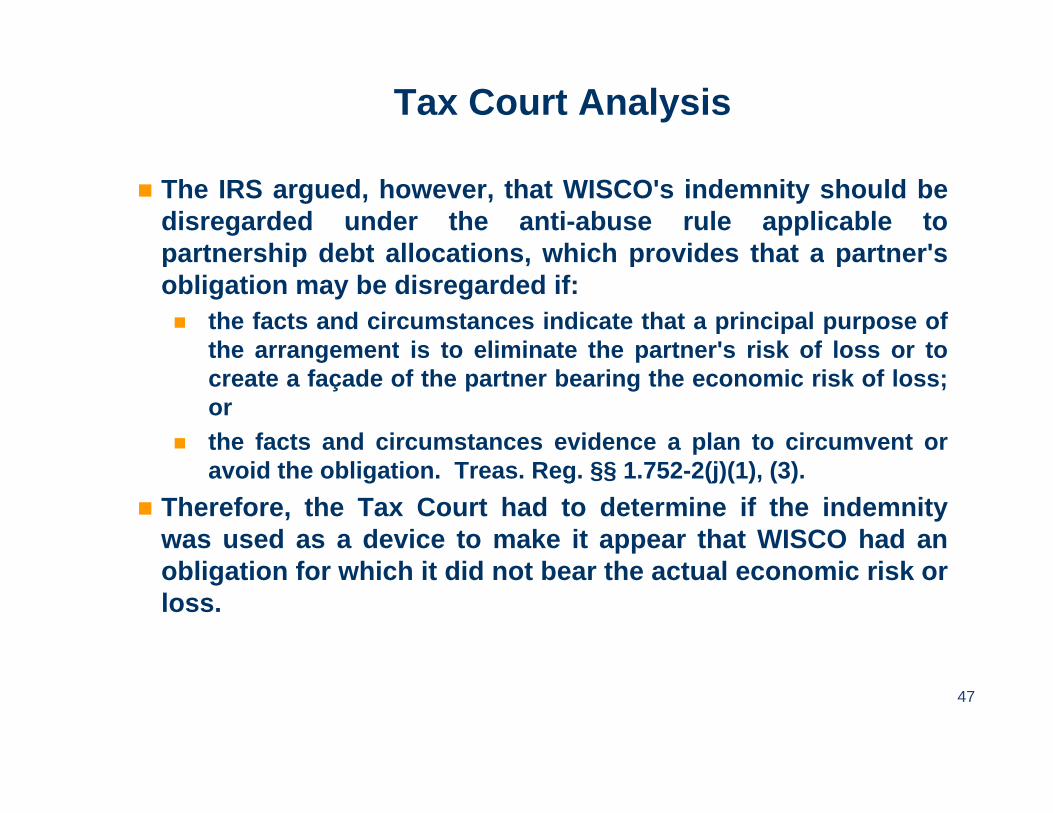

The IRS argued, however, that WISCO's indemnity should bedisregarded under the anti-abuse rule applicable topartnership debt allocations which provides that a partner'spartnership debt allocations, which provides that a partner sobligation may be disregarded if: the facts and circumstances indicate that a principal purpose of

the arrangement is to eliminate the partner's risk of loss or tothe arrangement is to eliminate the partner s risk of loss or tocreate a façade of the partner bearing the economic risk of loss;or

the facts and circumstances evidence a plan to circumvent oravoid the obligation. Treas. Reg. §§ 1.752-2(j)(1), (3).

Therefore, the Tax Court had to determine if the indemnitywas used as a device to make it appear that WISCO had anobligation for which it did not bear the actual economic risk orloss.

47

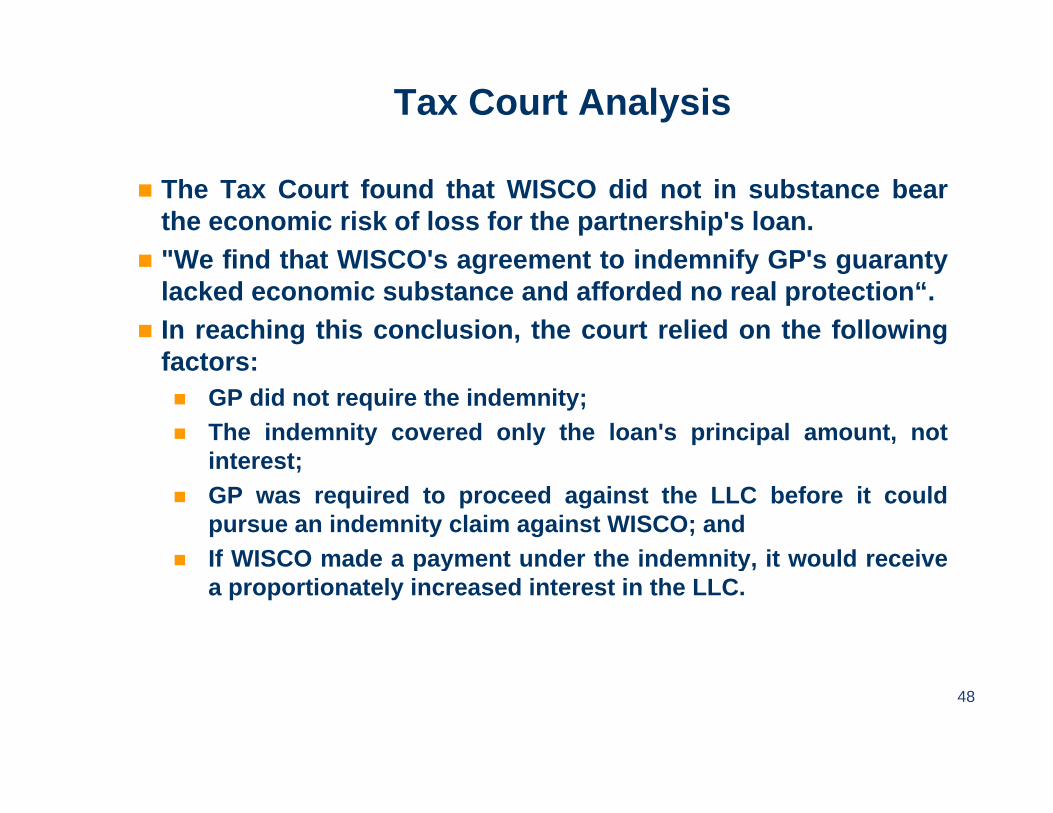

Tax Court Analysis

The Tax Court found that WISCO did not in substance bearthe economic risk of loss for the partnership's loan."W fi d th t WISCO' t t i d if GP' t "We find that WISCO's agreement to indemnify GP's guarantylacked economic substance and afforded no real protection“.

In reaching this conclusion, the court relied on the followingf tfactors: GP did not require the indemnity; The indemnity covered only the loan's principal amount, not

interest;interest; GP was required to proceed against the LLC before it could

pursue an indemnity claim against WISCO; and If WISCO made a payment under the indemnity it would receive If WISCO made a payment under the indemnity, it would receive

a proportionately increased interest in the LLC.

48

Tribune Newsday Transaction– Step 1

Tribune Co. CSC Holdings, Inc.(“Cablevision”)( Cablevision”)

100% 100%

Newsday, Inc. NMG Holdings, Inc.

NewsdayHoldings,

LLC

Membership Interest Membership Interest

Specified Amount and$650 Million of 8% Notes

Newsday,Newsday Assets & Liabilities

49

Newsday, LLC

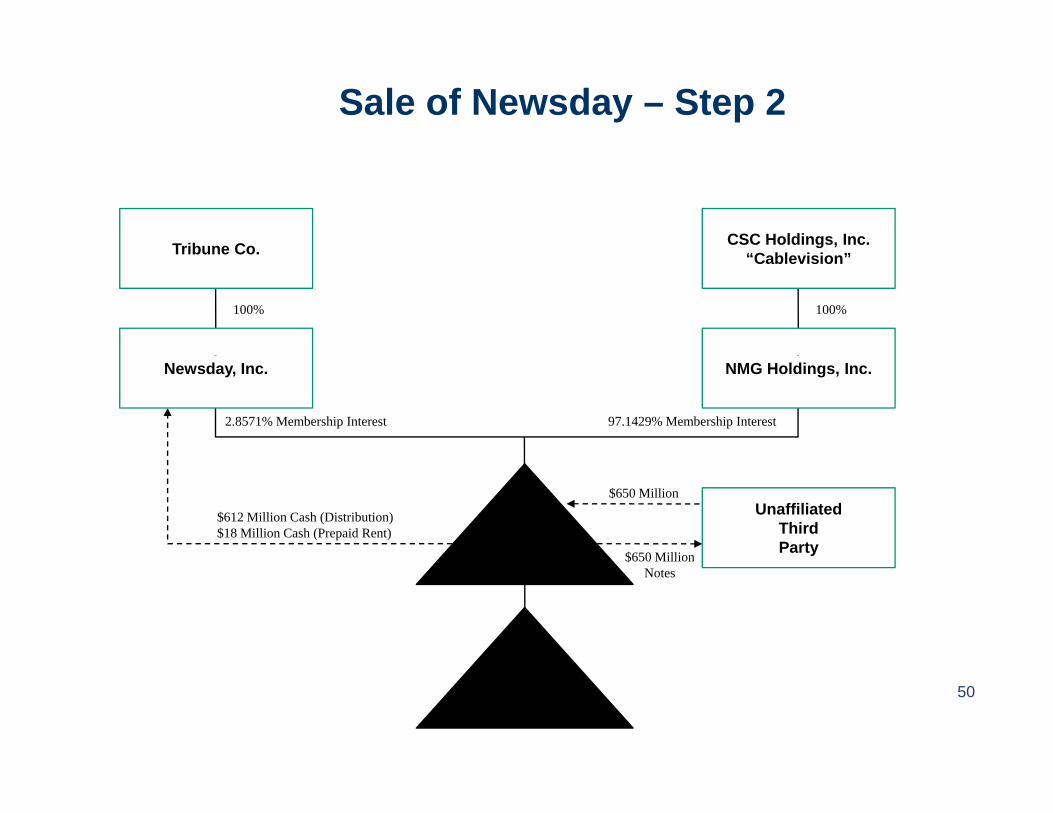

Sale of Newsday – Step 2

Tribune Co. CSC Holdings, Inc.“C bl i i ”Tribune Co. “Cablevision”

100% 100%

Newsday, Inc. NMG Holdings, Inc.

2.8571% Membership Interest 97.1429% Membership Interest

NewsdayHoldings,

LLC

$612 Million Cash (Distribution)$18 Million Cash (Prepaid Rent)

$650 Million

UnaffiliatedThird Party

$650 Million

LLC $650 MillionNotes

50Newsday,

LLC

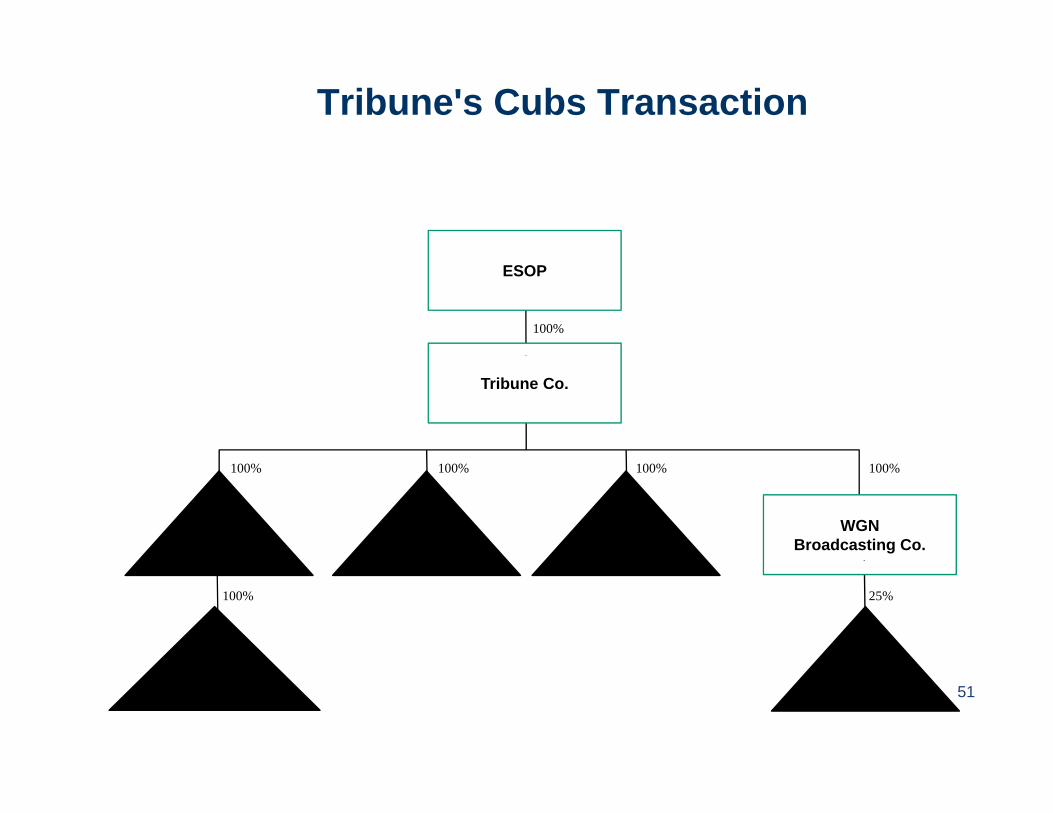

Tribune's Cubs Transaction

ESOP

100%

Tribune Co.

Cubs LLC

PremiumTickets

DQLLC

WGNBroadcasting Co.

100% 100% 100% 100%

LLC25%100%

51Dominican

LLCCSN

Chicago

Sale of Cubs – Step 1

T ib CJoe and Marlene

Ri k ttTribune Co. RickettsGrandchildren’s Trust

Membership Interest

100%100%

CubsEntities Ricketts

Acquisition LLC

MembershipInterest

CubsContributed

Assets

NewcoLLC

$100 Million Cash

Direct CubsContributed Assets

LLC

Newco

52

NewcoSubs

Sale of Cubs – Step 2

Tribune Co. RickettsAcquisition

LLC

5% Membership Interest 95% Membership Interest

NewcoUnaffiliated

Third Parties$740 Million Cash

$698.75MillionCash

$698.75MillionNotes

LLC

53

Relied Upon Exception to Disguised Sale Rules

If, as here, a partner transfers property to apartnership and the partnership incurs a liability,and all or a portion of the proceeds of that liabilityare allocable to a transfer of money to the partnermade within 90 days of incurring the liability…made within 90 days of incurring the liability…

Then, the transfer of money to the partner is takeninto account (as proceeds of a disguised sale) onlyt th t t th t th t f t f dto the extent that the amount of money transferredexceeds the partner's allocable share of thepartnership liabilityp p y See Treas. Reg. § 1.707-5(b)(1).

54

Guarantee in Bankruptcy?

Newsday and Tribune have only 2.8571% and 5% membershipinterests in the new partnerships, but are allocatedsubstantially greater amounts of the debt pursuant tosubstantially greater amounts of the debt pursuant toguarantees.

In the Newsday deal, Tribune indemnified Cablevision for anypayments made under Cablevision's guarantee of thepayments made under Cablevision s guarantee of theNewsday, LLC credit facility

However, should Tribune's obligation be disregardedpursuant to Treas Reg § 1 752-2(j)?pursuant to Treas. Reg. § 1.752-2(j)? Tribune filed for bankruptcy on December 8, 2008 Generally, Tribune's obligation should be respected so long as

Tribune did not know its bankruptcy was imminent at the time itTribune did not know its bankruptcy was imminent at the time itentered into the indemnification agreement

55

Guarantee in Bankruptcy, cont.

At the time of the Cubs sale, Tribune was in bankruptcy Tribune guaranteed repayment of debt of Newco, LLC

Only provided a guarantee of collection, which requiresexhaustion of all lender remedies against Newco, all otherguarantors, and all collateral before Tribune is required toperform on its guarantee

Should Tribune's guarantee be disregarded? See CCA 2002-46-014 (Aug. 8, 2002) (discussed below)See CC 00 6 0 ( ug 8, 00 ) (d scussed be o )

56

Recourse and Nonrecourse Liability in Partnership Agreements

Circular 230 Disclosure

These materials are intended for internal discussion purposesThese materials are intended for internal discussion purposes only. To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. tax advice contained in this communication is not intended or written to be used, and ,cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or any other state or local law, or (ii) promoting, marketing or recommending to another party any transaction or matter addressed hereinparty any transaction or matter addressed herein.

57

Planning Strategies and Techniques

Walter McGrailWalter McGrail

58

Internal Revenue Service Partnership - Audit Technique Guide p q

• The IRS publishes general considerationsThe IRS publishes general considerations to be employed by their agents in the conduct of a taxpayer examination andconduct of a taxpayer examination and partnerships are no different.

Web citation:– Web citation: http://www.irs.gov/businesses/partnerships/article/0,,id=134697,00.html#5,, ,

– Last updated March 2011

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

59

IRS Partnership - Audit Technique Guide “Zombie Partnerships”p q p

• Partnerships whichPartnerships which are no longer actively engaged in businessengaged in business but which still wander aimlessly aboutaimlessly about shedding tax benefits or postponing gainor postponing gain.

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

60

IRS Partnership - Audit Technique Guide Identifying “Zombie Partnerships”Identifying Zombie Partnerships

• According to the IRS, a Zombie partnership has:g p p– debt,– a large negative capital account, and– very little in the way of assets or economic activity.y y y

• A Zombie U. S. Form 1065 Schedule L Balance Sheet may report:– Negative assets and no liabilities– Negative assets and no liabilities

• A more unusual type of Zombie partnership continues to report:

Si ifi t t l ti it d t hi b t th t l– Significant rental activity and property ownership, but the rental loss is covered by depreciation and interest accruals.

• What is the IRS really after?

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

61

IRS Partnership - Audit Technique Guide Agent Examination Techniques Involving “Zombie Partnerships”Examination Techniques Involving Zombie Partnerships

• Documents to RequestPartnership Agreement and all amendments– Partnership Agreement and all amendments.

– Copies of all loan documents including, but not limited to promissory notes, deeds of trust, mortgages, loan payment histories, loan guarantees and/or loan indemnification agreements.

– If the partnership is tiered, copies of that partnership agreement and allIf the partnership is tiered, copies of that partnership agreement and all amendments, together with all Schedules K-1 ever received.

– Copies of all purchase and sales documents and settlement sheets.– Real Estate Tax statements (to show ownership and value).– Verification, as of year end, of the amount and type of liability supporting the

i i lnegative capital account.• Interview Questions

– What happened to partnership assets and when did it occur?– What is the basis for your claim that the partnership was still liable for the debt

h th b l h t/S h d l K 1?shown on the balance sheet/Schedule K-1?– To what extent do these liabilities include accruals for interest and taxes?

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

62

IRS Partnership - Audit Technique Guide Agent Foreclosures vs Discharge of IndebtednessForeclosures vs. Discharge of Indebtedness

• The IRS has an interest in scrutinizing taxpayer g p yreporting of:– Cancellation of debt income (COD) versus

I f f l– Income from foreclosure• COD

Taxable ordinary Income– Taxable ordinary Income– May qualify for exclusion

• Foreclosure– Taxable at capital gains rates– Not subject to exclusions

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

63

IRS Partnership - Audit Technique Guide Agent Foreclosures vs. Discharge of Indebtedness IRS Examination ConsiderationsDischarge of Indebtedness IRS Examination Considerations

• COD versus Sale:If th t hi t l f t d COD i l– If the partnership reports a sale of property and COD income, analyze all loan documents to determine whether loan was non-recourse or recourse.

• If non-recourse, determine whether there were two transactions or one.If i ti f th t hi t i di t th t COD i– If inspection of the partnership return indicates that COD income was reported, property decreased on the balance sheet, and a loss/very small gain/ or no gain on sale of partnership property was reported, determine whether partnership properly reported transaction.Analyze documents– Analyze documents.

• If a guarantee of non-recourse debt was made at the eleventh hour, it may not change the status of the loan from non-recourse to recourse.

• If the guarantee provides that a partner must repay the loan only if he fights the foreclosure sale, this would be considered a contingent guarantee and , g gwould not change the loan from non-recourse to recourse.

• If there is an 11th hour guarantee issue, call a Technical Advisor.

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

64

Springing Recourse Obligationsp g g g

• History of Springing Recourse Obligationsy p g g g– Borrower and / or its investors are exculpated unless:

• Fraud,• Misrepresentation,p ,• Conversion, or• Other so-called Bad Boy Acts

– Current State of Play – Expansion of the Springing y p p g gprovisions

• Filing for protection from creditors;• Placing additional “junior” liens on the secured assets;• Solvency of the borrower

– Consider not only the “Kobayashi Maru” economic trap for the unwary borrower, but the possible federal income tax ramifications as well.

© 2011 Cendrowski Corporate Advisors LLCProprietary and Confidential, All Rights Reserved

65