Embed Size (px)

Citation preview

h d d d lPresenting a live 110‐minute teleconference with interactive Q&A

The ASB's Audit Standards Clarity Project: Prepare Now to ComplyM ti th Ch ll f I t ti l C N Obj tiMeeting the Challenges of International Convergence, New Objectivesand Special Considerations in the Revised Standards

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, JUNE 29, 2011

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Andy Mintzer Director Hemming Morse Inc. Los AngelesAndy Mintzer, Director, Hemming Morse Inc., Los Angeles

Ahava Goldman, Senior Technical Manager, AICPA, New York

For this program, attendees must listen to the audio over the telephone.

Please refer to the instructions emailed to the registrant for the dial-in information.Attendees can still view the presentation slides online. If you have any questions, pleasecontact Customer Service at1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

Attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online but there is no online audio for this program.

Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.at 1 800 926 7926 ext. 10.

Tips for Optimal Quality

S d Q litSound Quality

For this program, you must listen via the telephone by dialing 1-866-873-1442 and entering your PIN when prompted. There will be no sound over the web connection.co ect o .

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

The ASB Audit Standards Clarity P j t P N T C l Project: Prepare Now To Comply Seminar

June 29, 2011

Ahava Goldman, [email protected]

Andy Mintzer, Hemming Morse [email protected]

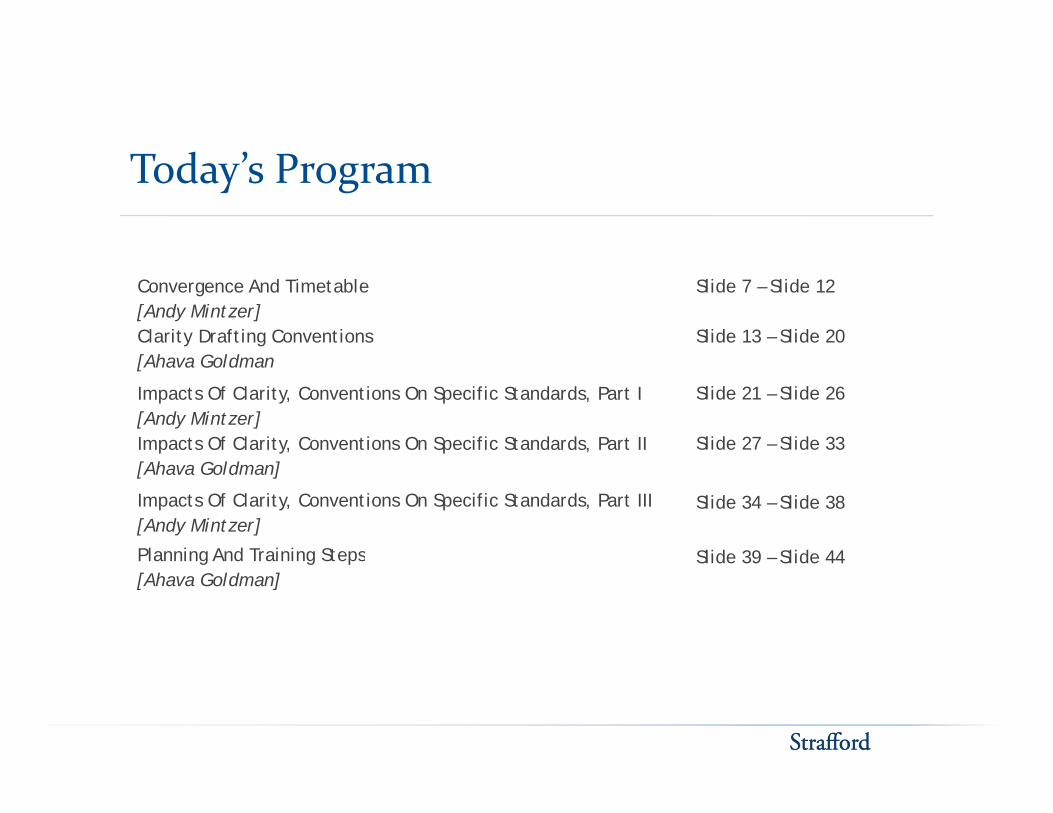

Today’s Program

Convergence And Timetable[Andy Mintzer]Clarity Drafting Conventions[Ah G ld

Slide 7 – Slide 12

Slide 13 – Slide 20[Ahava Goldman

Impacts Of Clarity, Conventions On Specific Standards, Part I[Andy Mintzer]Impacts Of Clarity, Conventions On Specific Standards, Part II

Slide 21 – Slide 26

Slide 27 – Slide 33[Ahava Goldman]

Impacts Of Clarity, Conventions On Specific Standards, Part III[Andy Mintzer]

Planning And Training Steps Slide 39 – Slide 44

Slide 34 – Slide 38

Planning And Training Steps[Ahava Goldman]

Slide 39 Slide 44

CONVERGENCE AND Andy Mintzer, Hemming Morse Inc.

CONVERGENCE AND TIMETABLE

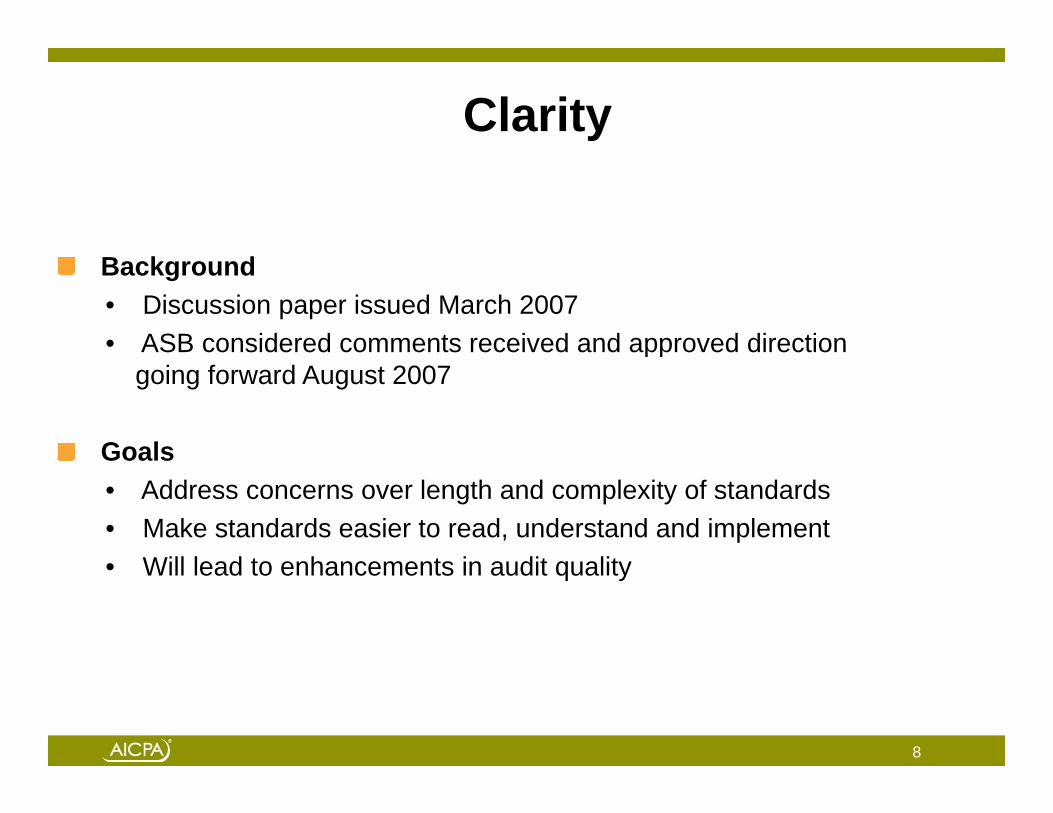

Clarity

Background• Discussion paper issued March 2007• ASB considered comments received and approved direction pp

going forward August 2007

GoalsGoals• Address concerns over length and complexity of standards• Make standards easier to read, understand and implement

Will l d t h t i dit lit• Will lead to enhancements in audit quality

8

Clarity And ConvergenceC a ty d Co e ge ce

Convergence?S S G O C O• IAASB, ASB, GAO, PCAOB

Convergence with ISAs• Harmonize, not adopt• Most audits performed internationally are of non-public

entities; therefore, ASB and IAASB have a similar focus.• Avoid unnecessary differences with PCAOBy• ASB standards: More “shoulds” than ISAs, but less than

existing SASs

9American Institute of CPAs

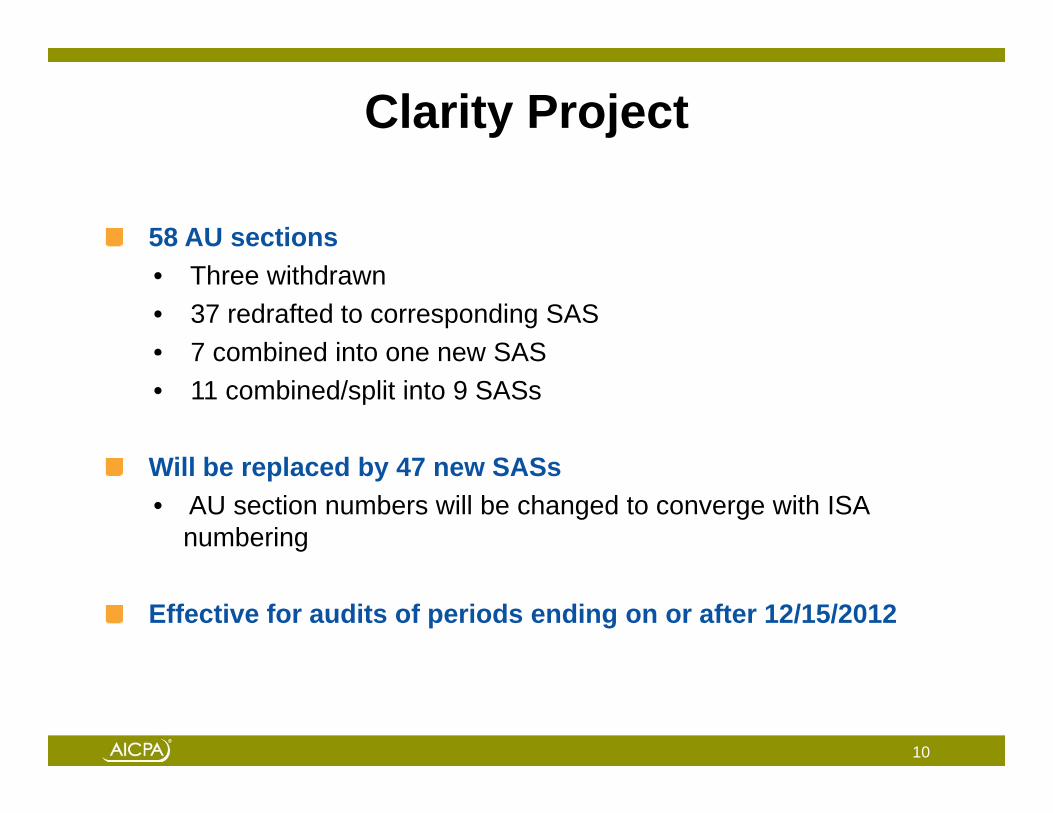

Clarity Project

58 AU sections• Three withdrawn• 37 redrafted to corresponding SAS• 7 combined into one new SAS7 combined into one new SAS• 11 combined/split into 9 SASs

Will b l d b 47 SASWill be replaced by 47 new SASs • AU section numbers will be changed to converge with ISA

numbering

Effective for audits of periods ending on or after 12/15/2012

10

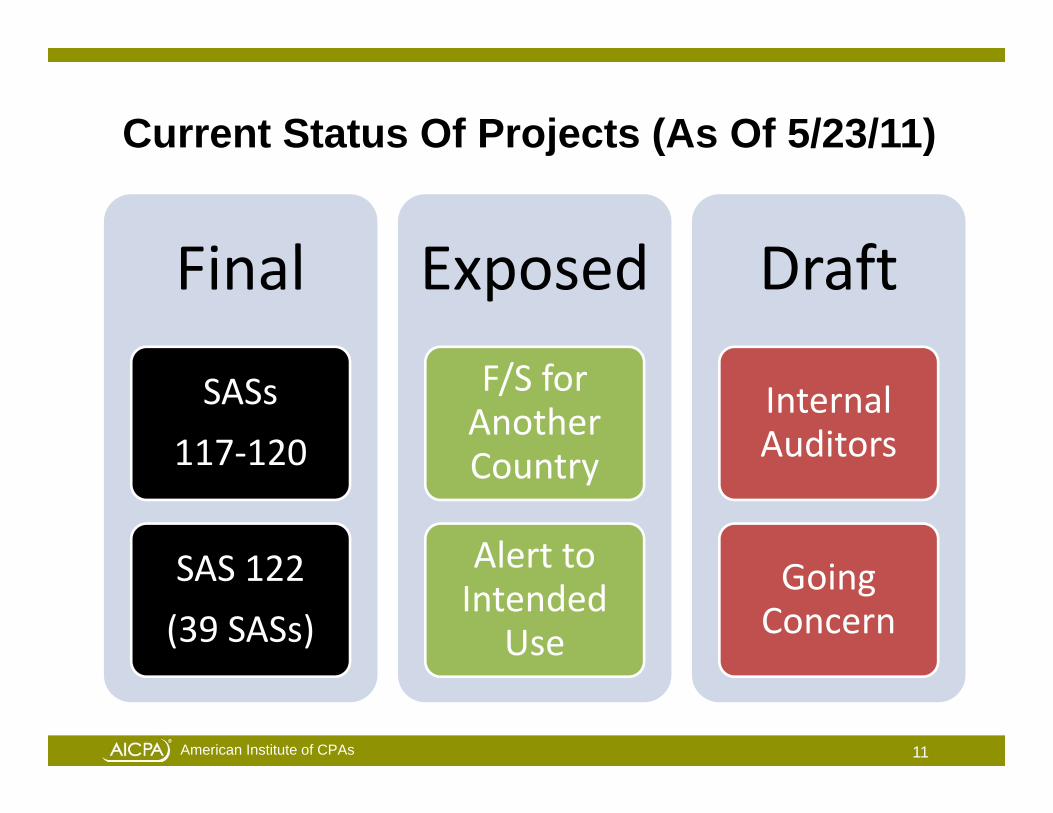

Current Status Of Projects (As Of 5/23/11)j ( )

Fi l E d D ftFinal Exposed Draft

SASs

117‐120

F/S for Another C t

Internal Auditors117 120

SAS 122

Country

Alert toSAS 122

(39 SASs)

Alert to Intended

Use

Going Concern

11American Institute of CPAs

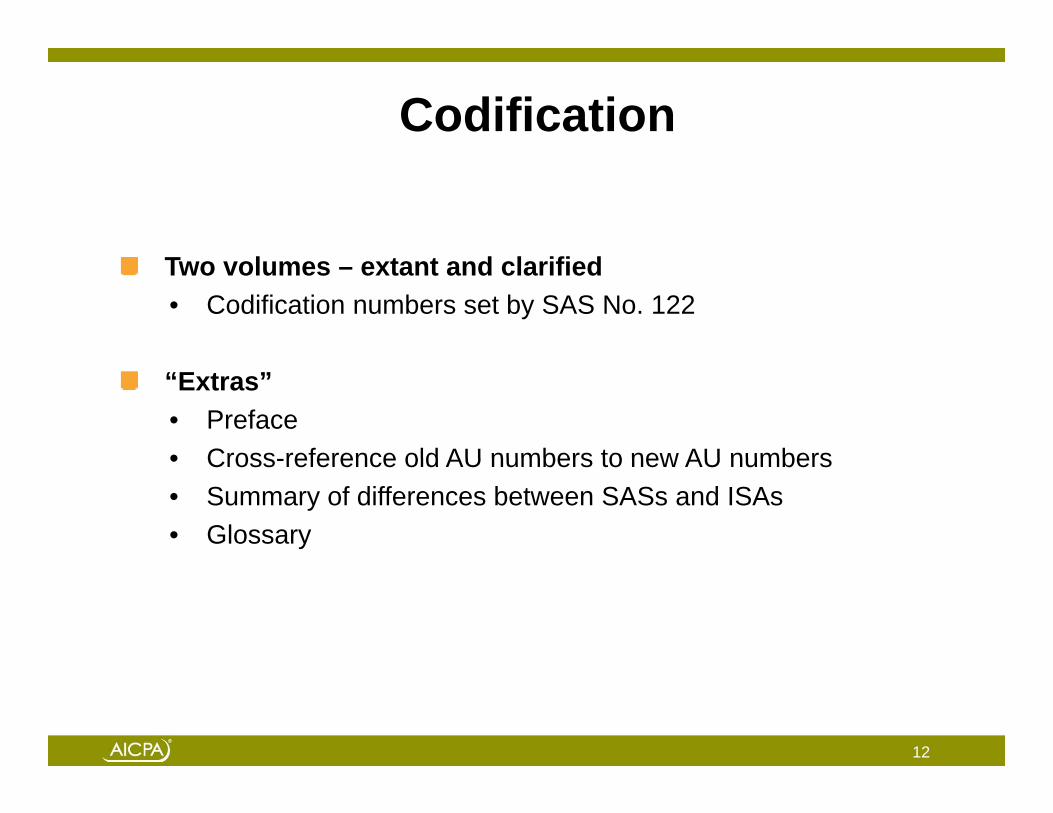

Codification

Two volumes – extant and clarified• Codification numbers set by SAS No. 122

“Extras”• Preface• Cross reference old AU numbers to new AU numbers• Cross-reference old AU numbers to new AU numbers• Summary of differences between SASs and ISAs• Glossary

12

CLARITY DRAFTING Ahava Goldman, AICPA

CLARITY DRAFTING CONVENTIONS

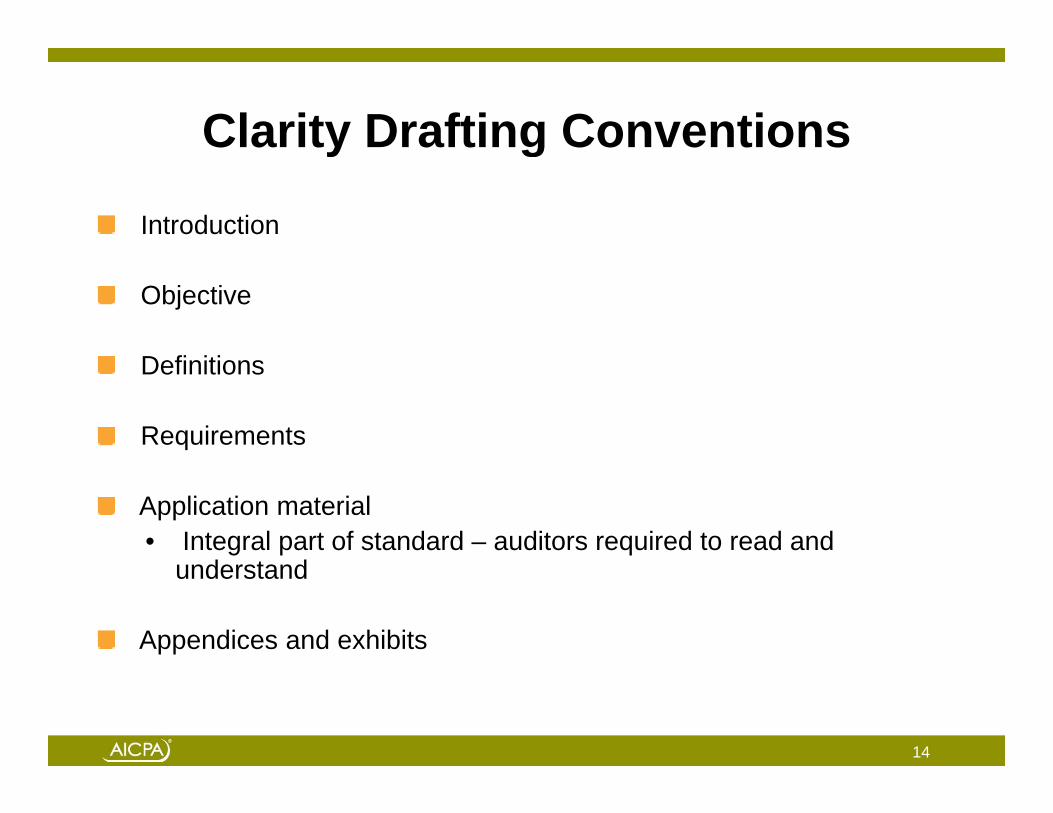

Clarity Drafting Conventionsy g

Introduction

Objective

D fi i iDefinitions

Requirements

Application material• Integral part of standard – auditors required to read and

d t dunderstand

Appendices and exhibits

14

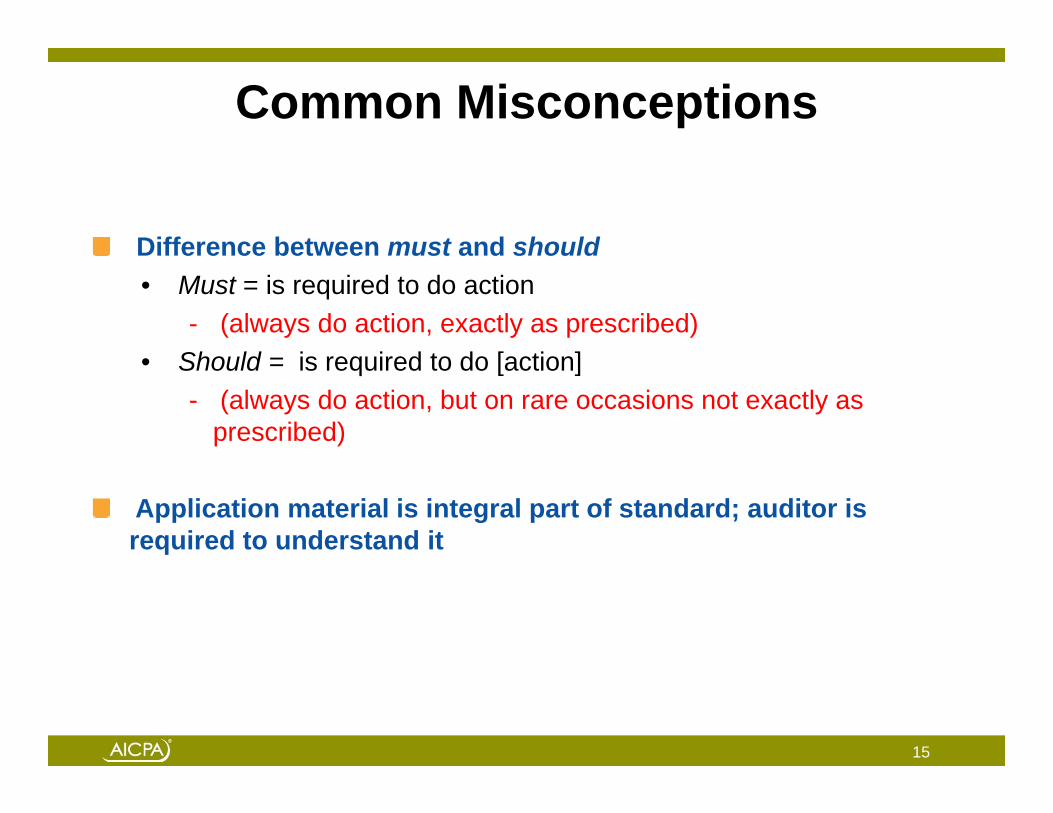

Common Misconceptions

Difference between must and shouldDifference between must and should• Must = is required to do action

- (always do action, exactly as prescribed)Sh ld i i d t d [ ti ]• Should = is required to do [action]- (always do action, but on rare occasions not exactly as

prescribed)

Application material is integral part of standard; auditor is required to understand it

15

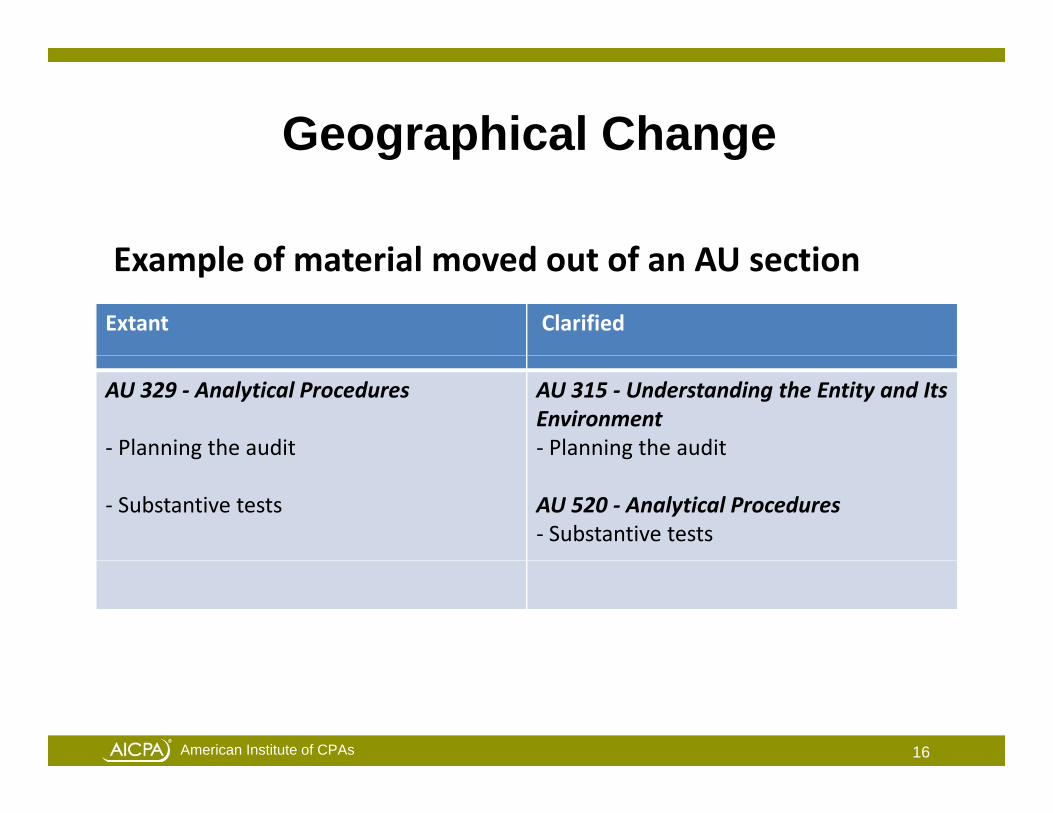

Geographical ChangeGeog ap ca C a ge

E l f t i l d t f AU ti

Extant Clarified

Example of material moved out of an AU section

AU 329 ‐ Analytical Procedures

‐ Planning the audit

AU 315 ‐ Understanding the Entity and Its Environment‐ Planning the auditg

‐ Substantive tests

g

AU 520 ‐ Analytical Procedures‐ Substantive tests

16American Institute of CPAs

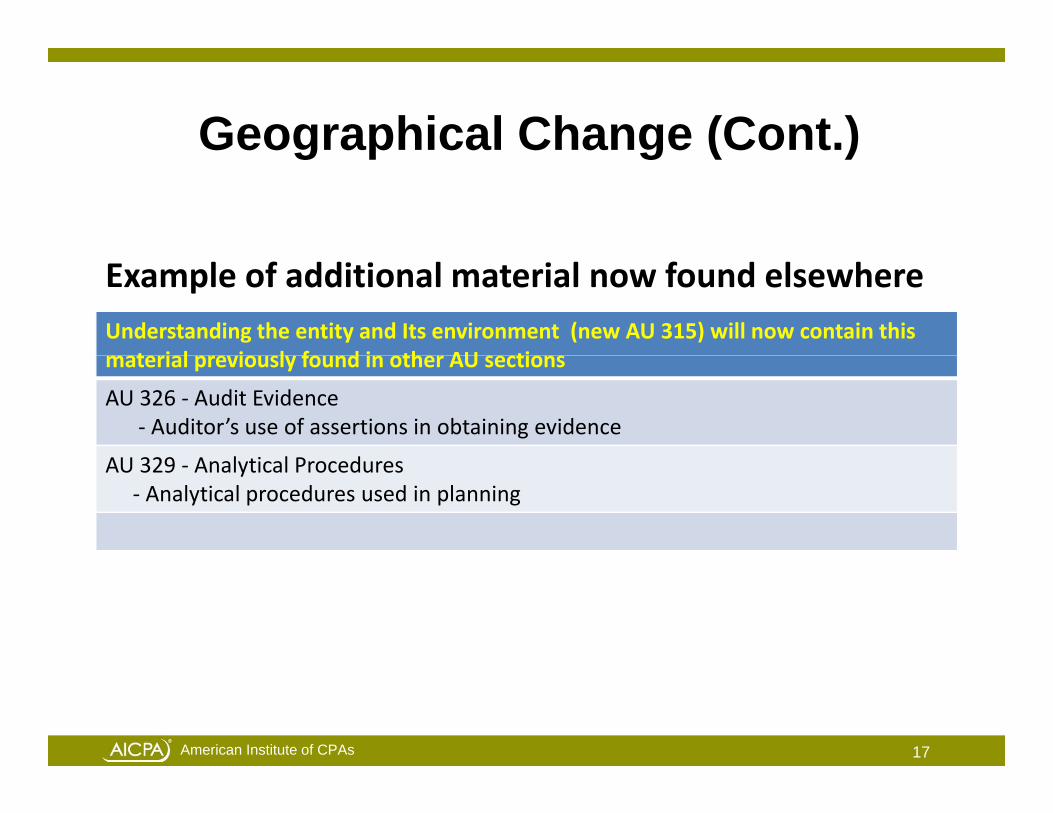

Geographical Change (Cont.)Geog ap ca C a ge (Co t )

Understanding the entity and Its environment (new AU 315) will now contain this t i l i l f d i th AU ti

Example of additional material now found elsewhere

material previously found in other AU sections

AU 326 ‐ Audit Evidence‐ Auditor’s use of assertions in obtaining evidence

AU 329 A l i l P dAU 329 ‐ Analytical Procedures‐ Analytical procedures used in planning

17American Institute of CPAs

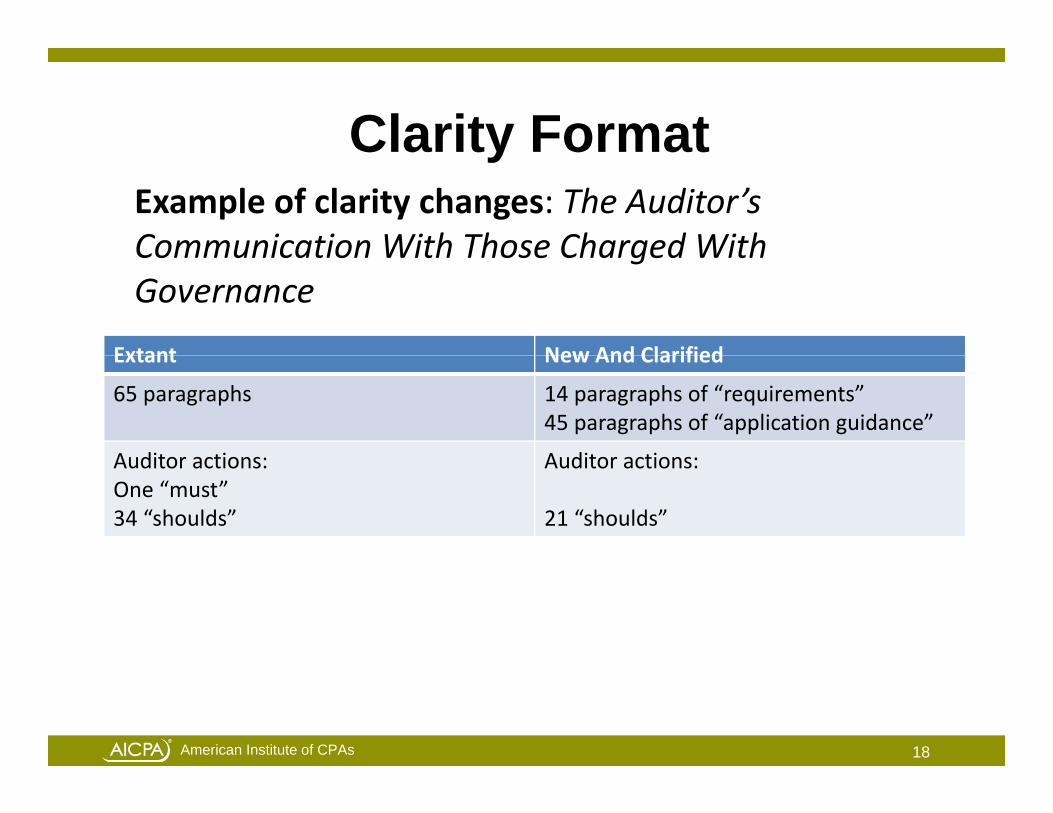

Clarity FormatClarity FormatExample of clarity changes: The Auditor’s Communication With Those Charged With

Extant New And Clarified

Communication With Those Charged With Governance

Extant New And Clarified

65 paragraphs 14 paragraphs of “requirements”45 paragraphs of “application guidance”

Auditor actions: Auditor actions:Auditor actions:One “must”34 “shoulds”

Auditor actions:

21 “shoulds”

18American Institute of CPAs

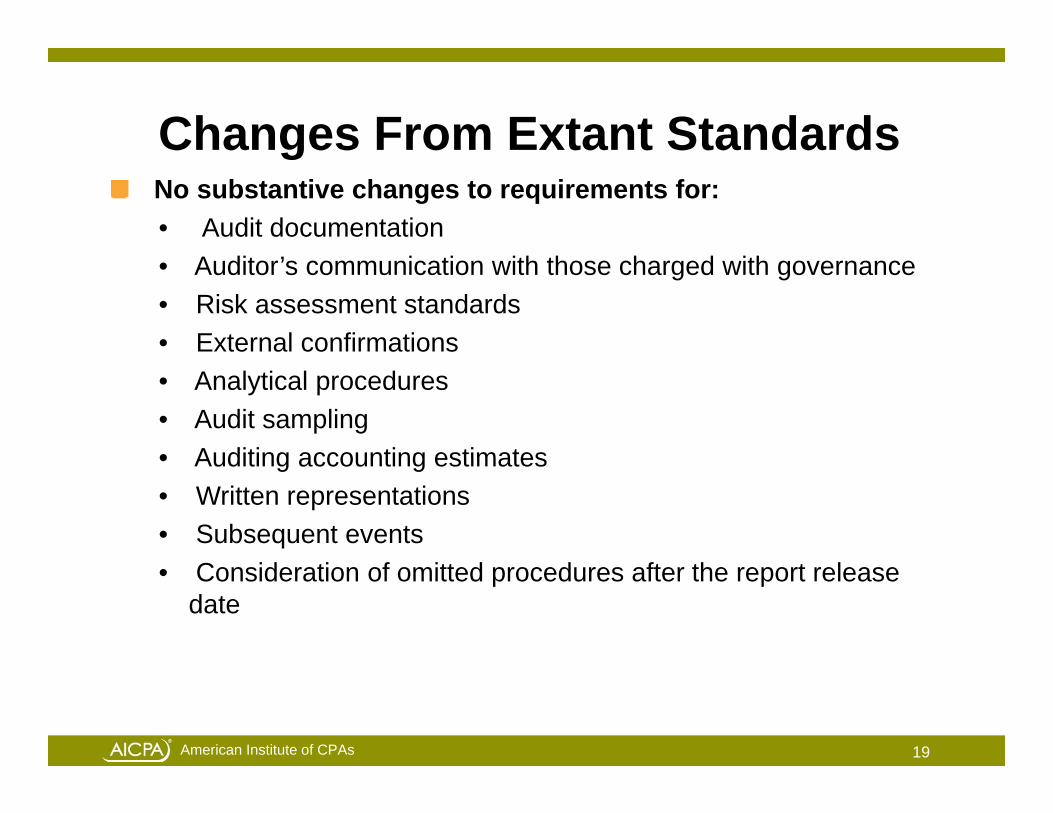

Changes From Extant StandardsC a ges o ta t Sta da dsNo substantive changes to requirements for:• Audit documentation• Auditor’s communication with those charged with governance• Risk assessment standards• External confirmations• Analytical procedures• Audit sampling• Auditing accounting estimates• Auditing accounting estimates• Written representations• Subsequent events• Consideration of omitted procedures after the report release

date

19American Institute of CPAs

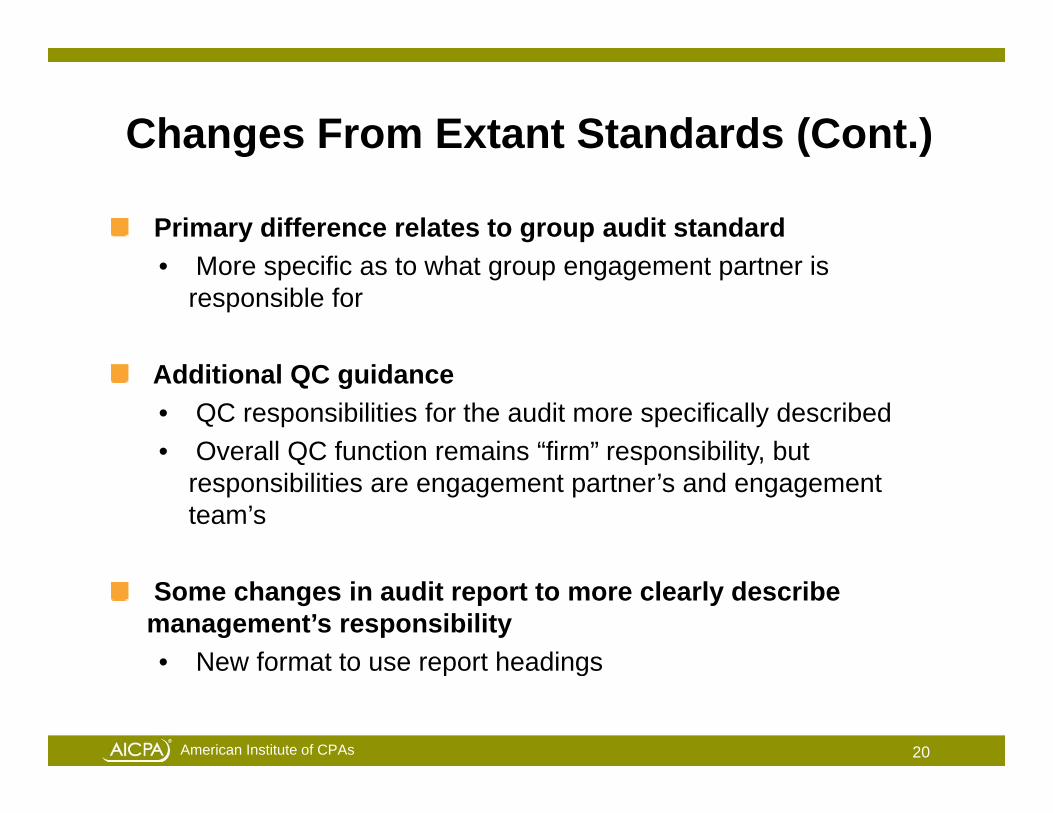

Changes From Extant Standards (Cont.)g ( )

Primary difference relates to group audit standard• More specific as to what group engagement partner is

responsible for

Additional QC guidance• QC responsibilities for the audit more specifically described• Overall QC function remains “firm” responsibility, butOverall QC function remains firm responsibility, but

responsibilities are engagement partner’s and engagement team’s

Some changes in audit report to more clearly describe management’s responsibility• New format to use report headings

20American Institute of CPAs

• New format to use report headings

IMPACTS OF CLARITY, Andy Mintzer, Hemming Morse Inc.

,CONVENTIONS ON SPECIFIC STANDARDS PART ISTANDARDS, PART I

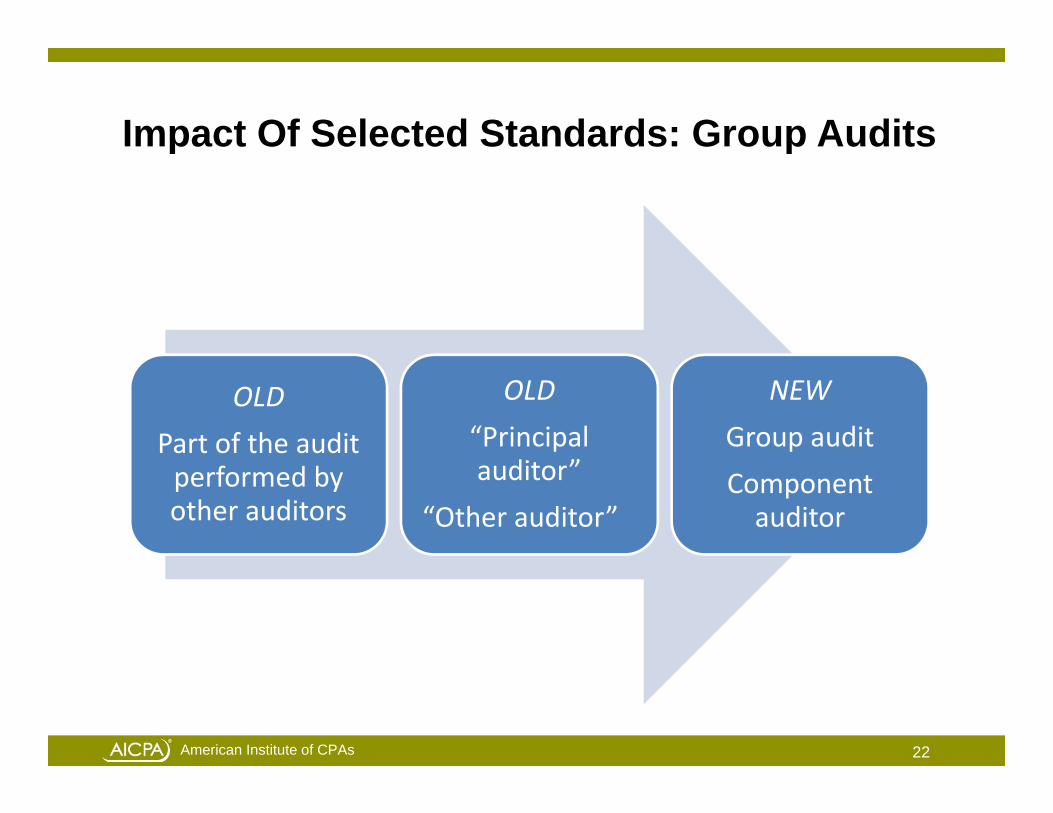

Impact Of Selected Standards: Group Auditsp p

OLD

Part of the audit

OLD

“Principal

NEW

Group auditperformed by other auditors

auditor”

“Other auditor”Component auditor

22American Institute of CPAs

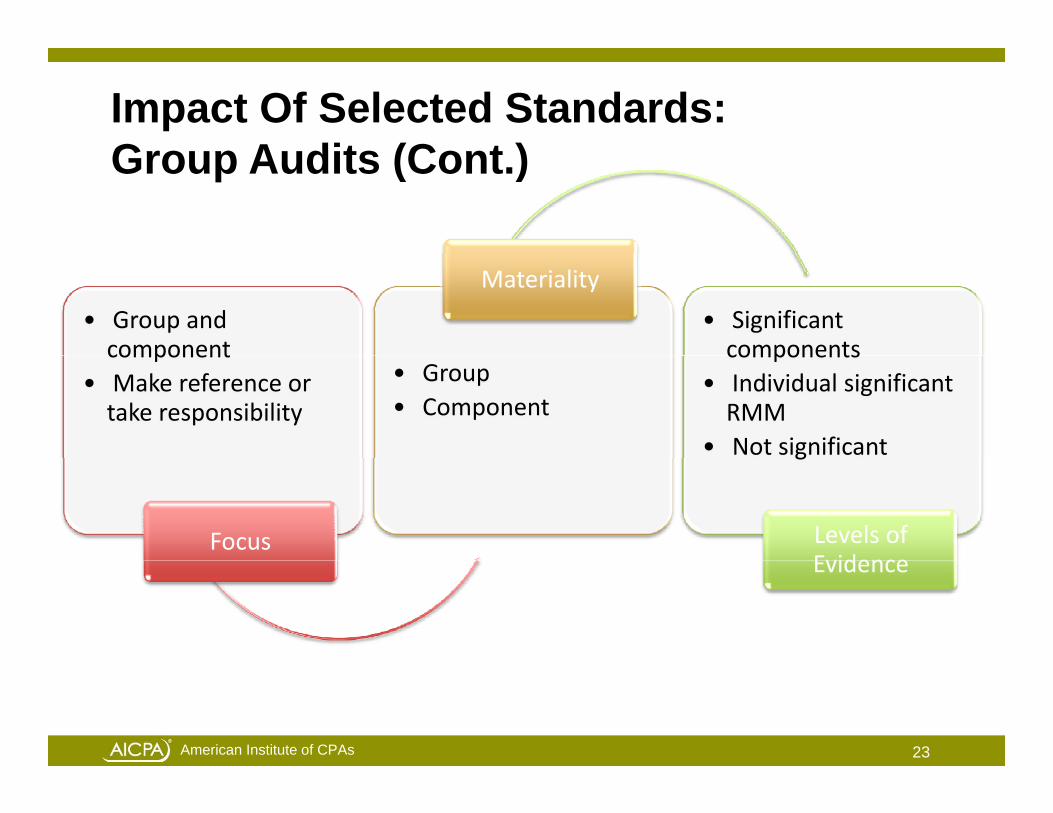

Impact Of Selected Standards:G A dit (C t )Group Audits (Cont.)

• Group and component

Materiality

• Significant componentscomponent

• Make reference or take responsibility

• Group• Component

components• Individual significant RMM

• Not significant

Focus

g

Levels of EvidenceEvidence

23American Institute of CPAs

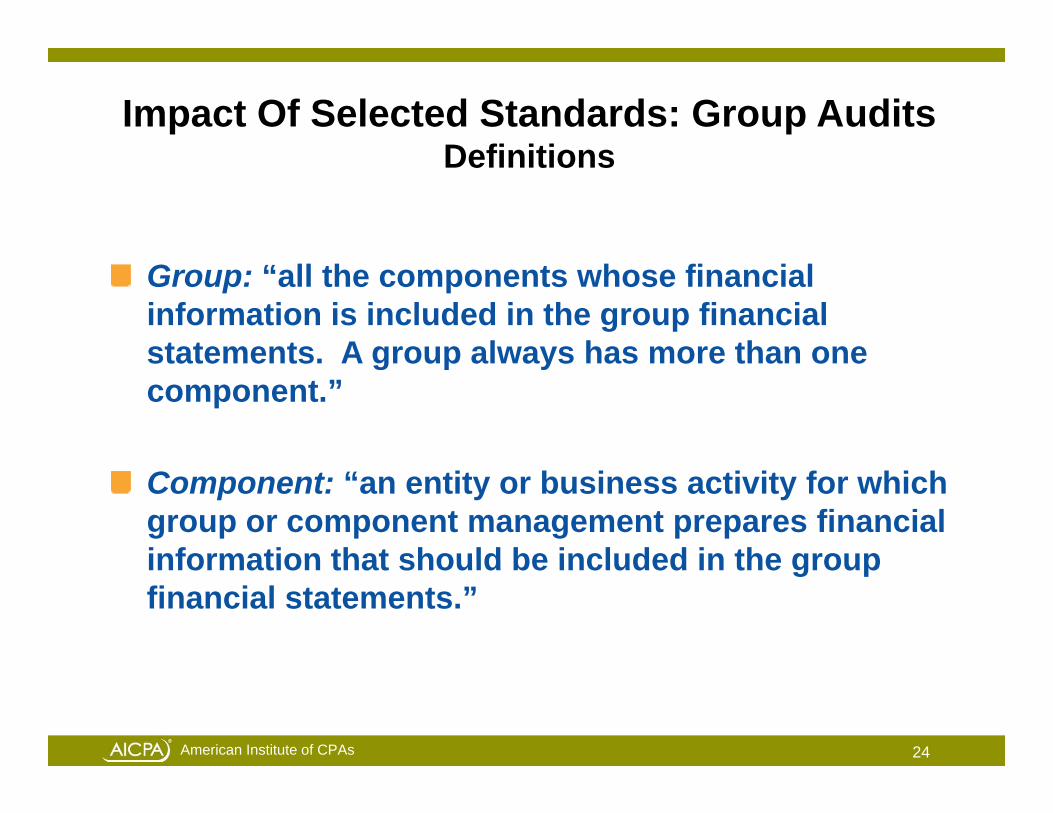

Impact Of Selected Standards: Group AuditsDefinitionsDefinitions

Group: “all the components whose financial information is included in the group financial statements A group always has more than onestatements. A group always has more than one component.”

Component: “an entity or business activity for which group or component management prepares financial information that should be included in the groupinformation that should be included in the group financial statements.”

24American Institute of CPAs

Impact Of Selected Standards: Group AuditsDefinitions (Cont )Definitions (Cont.)

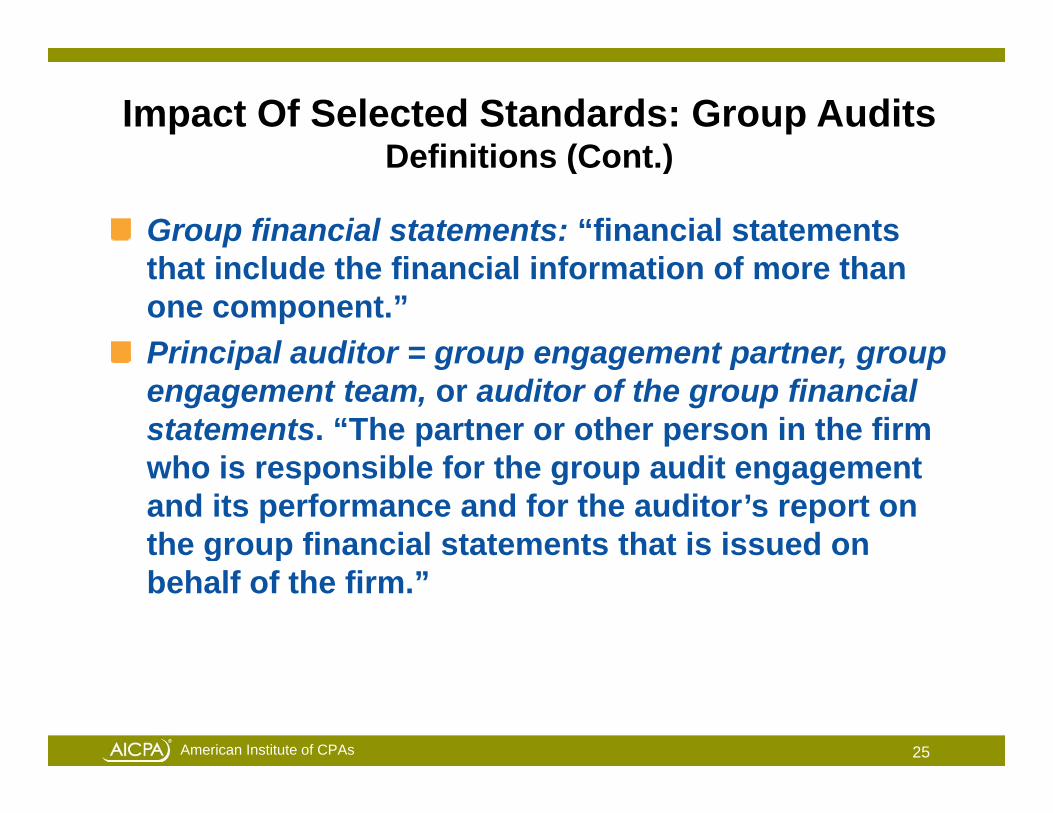

Group financial statements: “financial statements that include the financial information of more than one component.”Principal auditor = group engagement partner groupPrincipal auditor = group engagement partner, group engagement team, or auditor of the group financial statements. “The partner or other person in the firm

h i ibl f th dit twho is responsible for the group audit engagement and its performance and for the auditor’s report on the group financial statements that is issued on g pbehalf of the firm.”

25American Institute of CPAs

Impact Of Selected Standards: Group Audits (Cont.)p p ( )

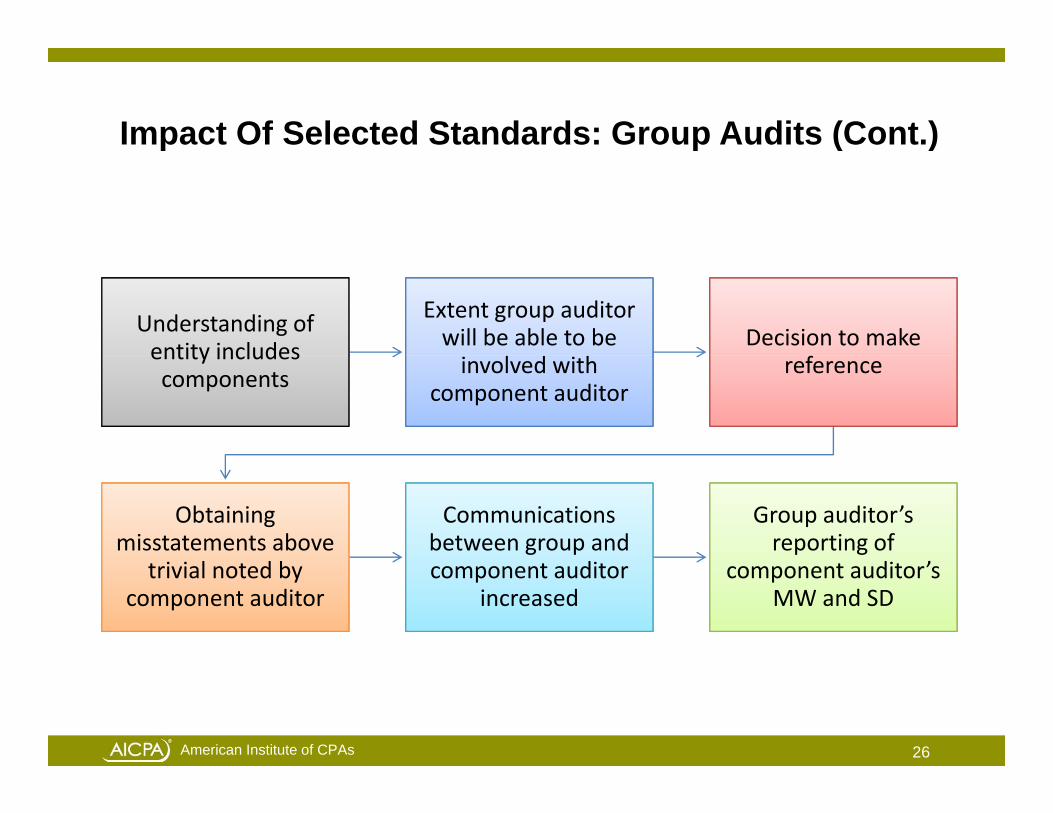

Understanding of entity includes

Extent group auditor will be able to be Decision to make entity includes

components involved with component auditor

reference

Obtaining misstatements above

Communications between group and

Group auditor’s reporting of

trivial noted by component auditor

component auditor increased

component auditor’s MW and SD

26American Institute of CPAs

IMPACTS OF CLARITY, Ahava Goldman, AICPA

,CONVENTIONS ON SPECIFIC STANDARDS PART IISTANDARDS, PART II

Impact Of Selected Standards: OverallObjectives SASObjectives SAS

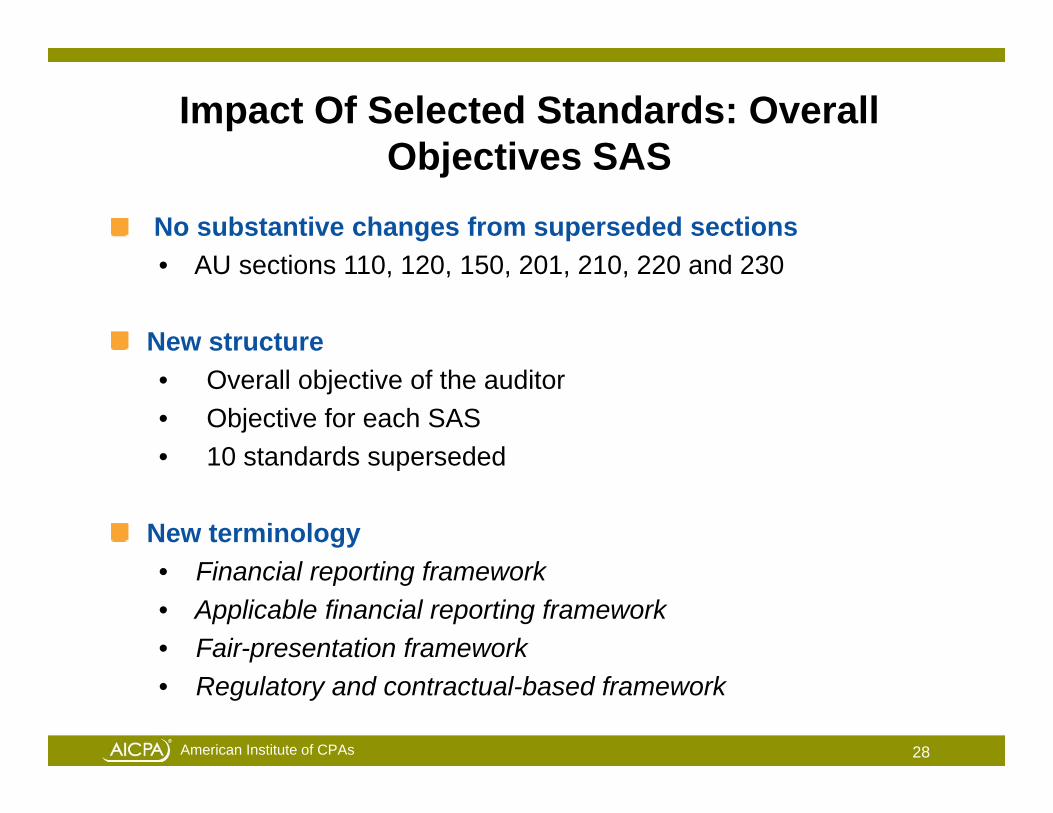

No substantive changes from superseded sections• AU sections 110, 120, 150, 201, 210, 220 and 230

New structure• Overall objective of the auditor• Objective for each SAS• 10 standards superseded• 10 standards superseded

New terminology • Financial reporting framework • Applicable financial reporting framework • Fair-presentation framework

28American Institute of CPAs

• Regulatory and contractual-based framework

Overall Objective Of An Auditor

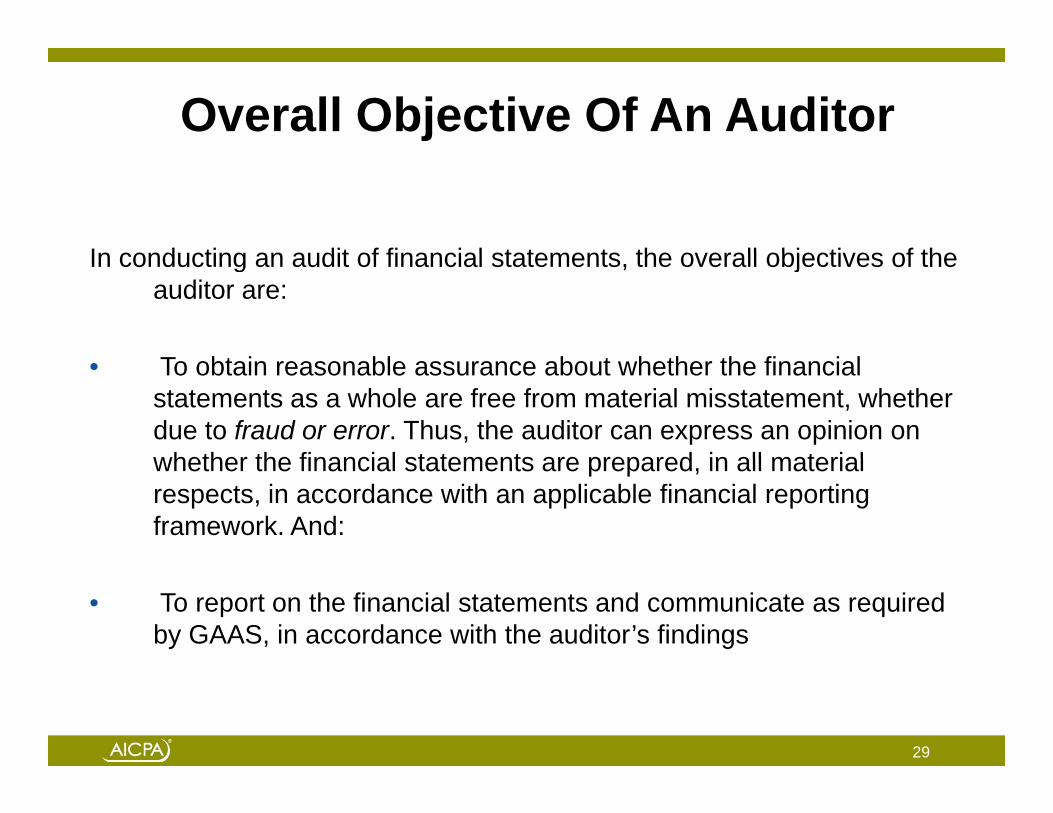

In cond cting an a dit of financial statements the o erall objecti es of theIn conducting an audit of financial statements, the overall objectives of the auditor are:

• To obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error. Thus, the auditor can express an opinion on whether the financial statements are prepared in all materialwhether the financial statements are prepared, in all material respects, in accordance with an applicable financial reporting framework. And:

• To report on the financial statements and communicate as required by GAAS, in accordance with the auditor’s findings

29

Overall Objective Of An Auditor (Cont.)

To achieve the overall objectives of the auditor the auditor uses theTo achieve the overall objectives of the auditor, the auditor uses the objectives stated in individual AU sections in planning and performing the audit considering the interrelationships within GAAS, to:• Determine whether any audit procedures in addition to those• Determine whether any audit procedures in addition to those

required by individual AU sections are necessary in pursuance of the objectives stated in each AU section; and

• Evaluate whether sufficient appropriate audit evidence has been• Evaluate whether sufficient appropriate audit evidence has been obtained.

30

Principles Governing An Audit

Preserves function of the 10 standardsPreserves function of the 10 standards

• Describing what an audit is

• Setting the structure for the codification of the SASs

• Used in the classroom and the courtroom• Used in the classroom and the courtroom

31American Institute of CPAs

Impact Of Selected Standards:T Of E tTerms Of Engagement

Terms SAS supersedes AU 311.05–.10. and AU 315.03, .05–.10, d 14and .14

C ’t t dit lCan’t accept audit unless:• Management acknowledges its responsibilities• Applicable financial reporting framework is acceptableg• No scope limitation at outset that will result in disclaimer

32American Institute of CPAs

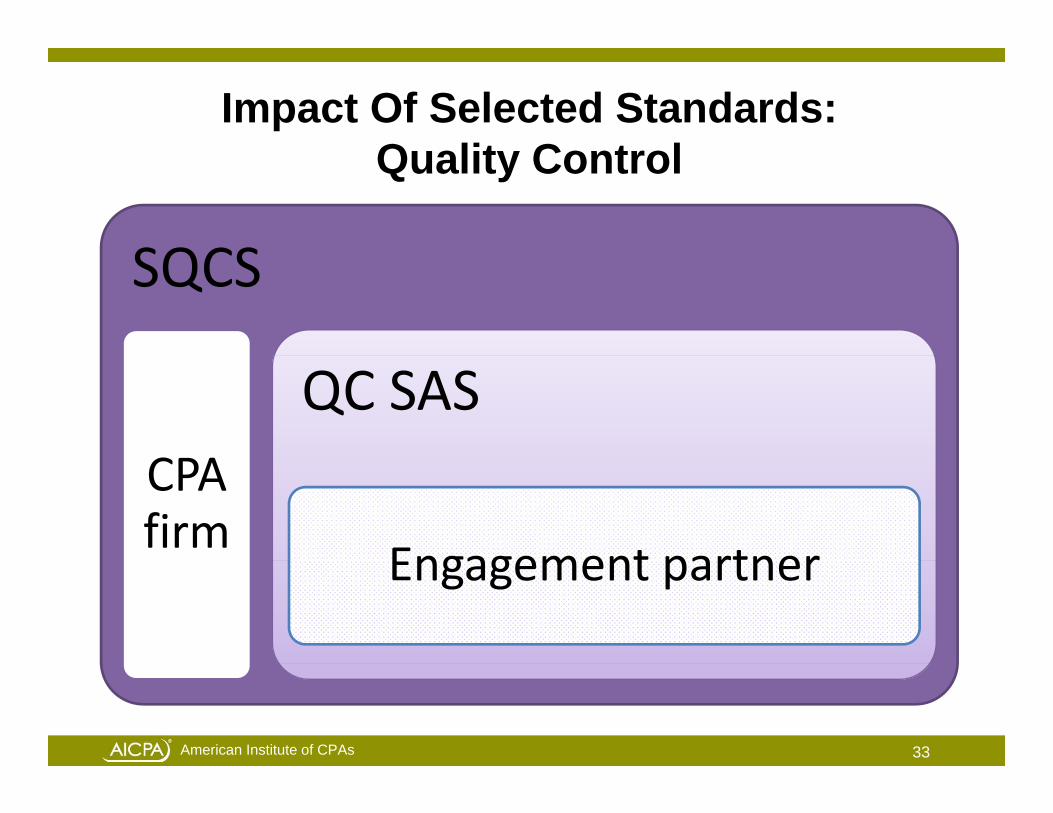

Impact Of Selected Standards:Q lit C t lQuality Control

SQCSSQCS

CPA

QC SASCPA firm

Engagement partnerEngagement partner

33American Institute of CPAs

IMPACTS OF CLARITY, Andy Mintzer, Hemming Morse Inc.

,CONVENTIONS ON SPECIFIC STANDARDS PART IIISTANDARDS, PART III

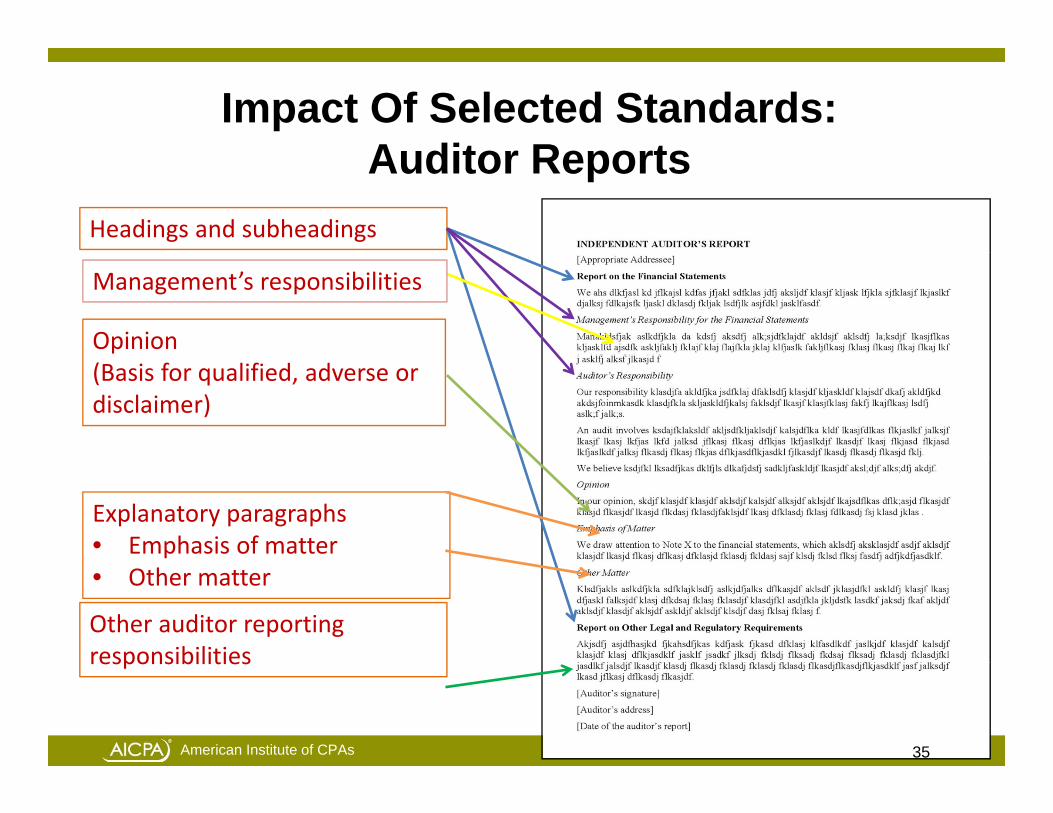

Impact Of Selected Standards:A dit R tAuditor Reports

Headings and subheadings

Opinion

Management’s responsibilities

(Basis for qualified, adverse or disclaimer)

Explanatory paragraphs• Emphasis of matter• Other matter

Other auditor reporting responsibilities

35American Institute of CPAs

responsibilities

35

Impact Of Selected Standards:A dit R t (C t )Auditor Reports (Cont.)

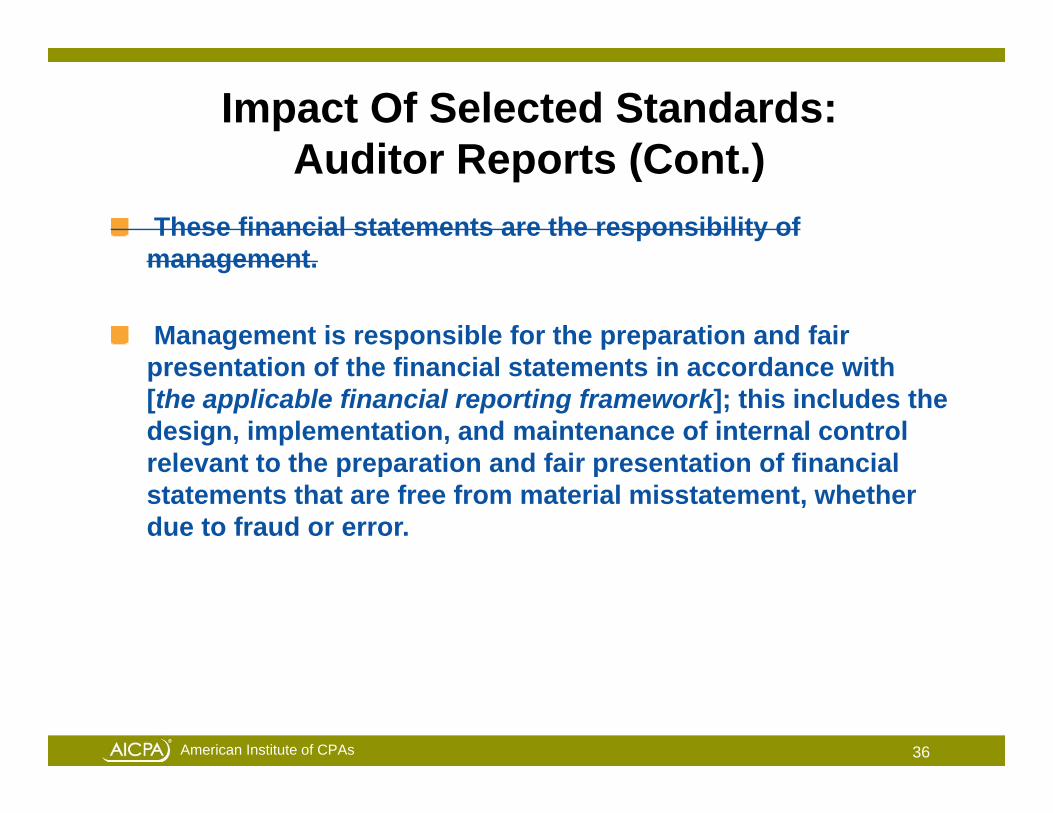

These financial statements are the responsibility of tmanagement.

Management is responsible for the preparation and fair presentation of the financial statements in accordance with [the applicable financial reporting framework]; this includes the design, implementation, and maintenance of internal control rele ant to the preparation and fair presentation of financialrelevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

36American Institute of CPAs

Impact Of Selected Standards:A dit R t (C t )Auditor Reports (Cont.)

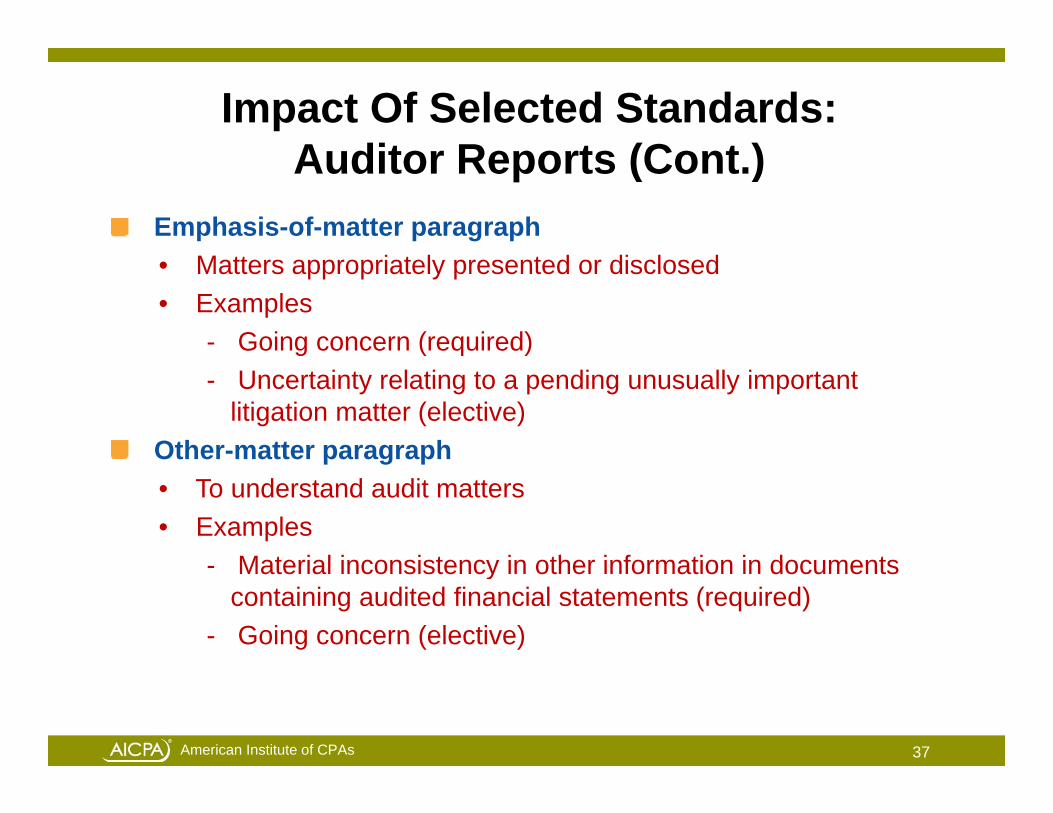

Emphasis-of-matter paragraph• Matters appropriately presented or disclosed• Examples

- Going concern (required)g ( q )- Uncertainty relating to a pending unusually important

litigation matter (elective)Other-matter paragraphOther matter paragraph• To understand audit matters• Examples

Material inconsistency in other information in documents- Material inconsistency in other information in documents containing audited financial statements (required)

- Going concern (elective)

37American Institute of CPAs

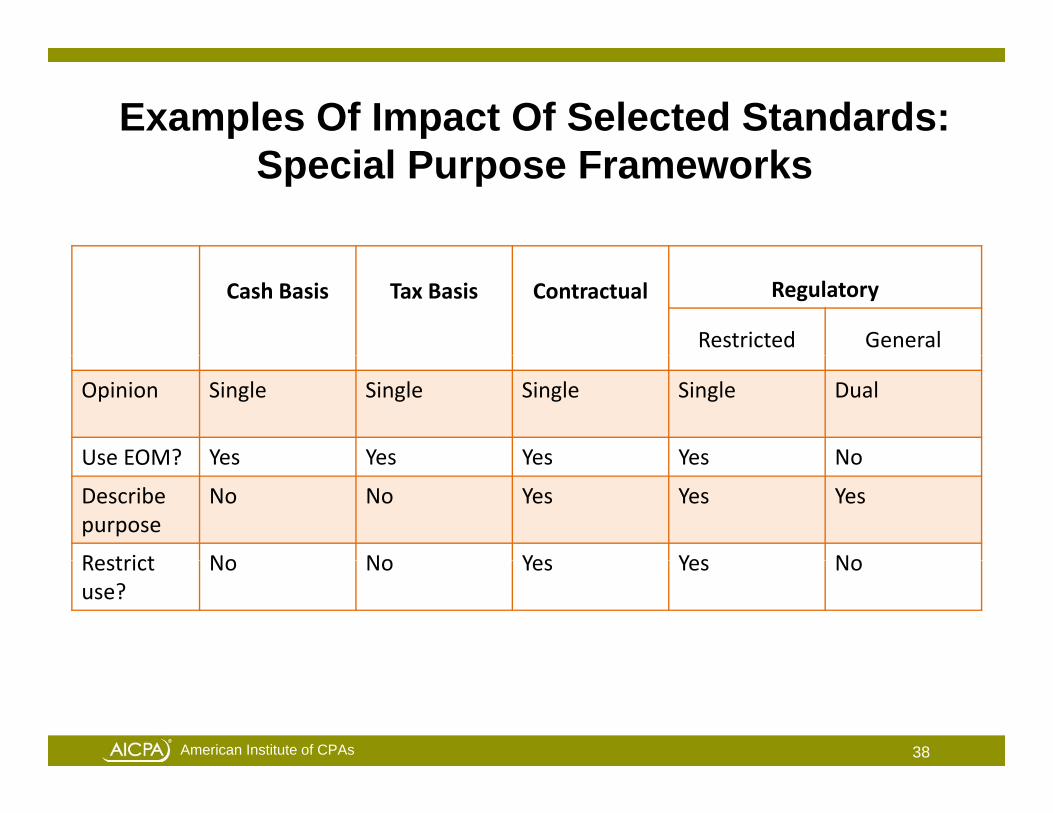

Examples Of Impact Of Selected Standards:S i l P F kSpecial Purpose Frameworks

Cash Basis Tax Basis Contractual Regulatory

Restricted General

Opinion Single Single Single Single Dual

Use EOM? Yes Yes Yes Yes NoUse EOM? Yes Yes Yes Yes No

Describepurpose

No No Yes Yes Yes

Restrict No No Yes Yes NoRestrict use?

No No Yes Yes No

38American Institute of CPAs

PLANNING AND TRAINING Ahava Goldman, AICPA

STEPS

Implementation Strategiesp e e tat o St ateg es

Wait, hope and pray?, p p y

Hitch a ride with someone else?Hitch a ride with someone else?• Still need to learn the content

Get on your own horse and hit the trail!

40American Institute of CPAs

Implementation Strategies (Cont.)p e e tat o St ateg es (Co t )

Gotta know the stuff• Read, read, read

- Application guidance, appendices and exhibitspp g pp- Updated AICPA audit guides

- Risk assessment standards- State and local governments- State and local governments- Not-for-profit entities

• Watch for AICPA clarity educational efforts• Attend this and other educational events• Talk with others!!!

41American Institute of CPAs

Implementation Strategies (Cont.)p e e tat o St ateg es (Co t )

A proactive approach• Begin updating for CY 2012/FY 2013 financial statement audits

- Your policies and procedures manuals, forms, checklists p pand audit processes

• Arizona OAG example- Began with exposure drafts (i.e., small task forces)Began with exposure drafts (i.e., small task forces)- Cataloguing changes (e.g., significant changes, things to

watch for, government-specific)- Some centralized effort but use/reinstate task forces for- Some centralized effort, but use/reinstate task forces for

implementation analysis

42American Institute of CPAs

Clarity Project Web Site Resourcesy j

Guide to Clarified and Converged Standards for Auditing and Q lit C t lQuality Control

All finalized SASs

Mapping of existing AU sections to clarified SASs

Summary of differences between existing SASs and clarified SASs

Clarity project FAQs

43American Institute of CPAs

Matrices of detailed differences from ISAs

Clarity Project Web SiteC a ty oject eb S te

http://www.aicpa.org/InterestAreas/AccountingAndAuditing/Resources/g gAudAttest/AudAttestStndrds/ASBClarity/Pages/ImprovingClarityASBStandards aspxStandards.aspx

44American Institute of CPAs