Embed Size (px)

Citation preview

www.mergermarket.com

press releasemergermarket M&A Round-up for Year End 2011

January 3 2012, for immediate release

PRESS CONTACTS

EMEA: Flora Wilke Americas: Dara Silverstein Asia-Pacific: Michel [email protected] [email protected] [email protected]: +44 207 059 6348 Tel: +1 646 3783118 Tel: +852 2158 9706

Press Release: www.mergermarket.com 2mergermarket M&A Round-up for Year End 2011

Global M&A up 2.5% in 2011Global M&A in 2011 totalled US$ 2,178.4bn, up 2.5% from the same period in 2010 (US$ 2,125.9bn), in the busiest year since 2008 which saw US$ 2,405.8bn-worth of deals. Activity was, however, down for four successive quarters, with US$ 432bn-worth of deals announced globally in the fourth quarter of 2011, down 22.5% from Q3 2011.

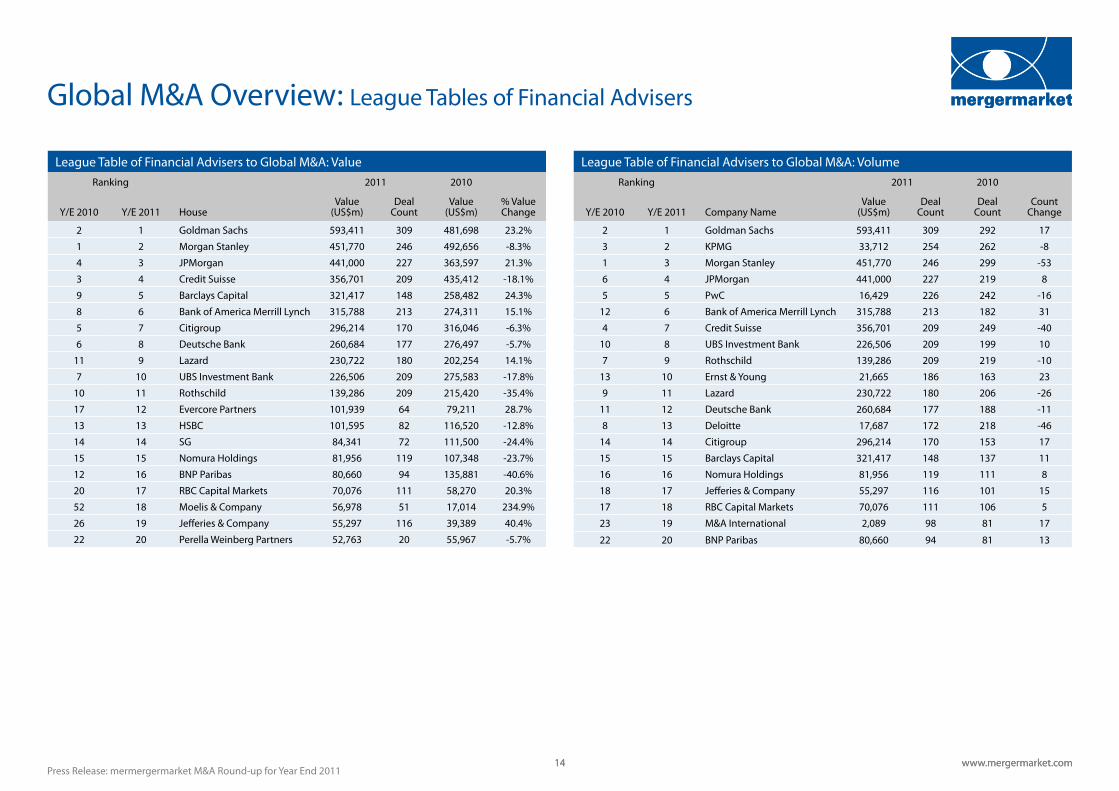

Goldman Sachs remains on topGoldman Sachs topped the global M&A financial advisory tables by total deal value for 2011, having advised on 309 deals worth US$ 593.4bn. Goldman worked on five of the ten largest deals announced last year.

US M&A strong in 2011 though dipping at end of yearThe US saw the announcement of US$ 820.6bn-worth of deals in 2011, the highest annual total deal value since 2007 (US$ 1,328.1bn), and 14.4% higher than 2010 (US$ 717.2bn). Activity, however, waned in Q4 with a decrease of 9.3% compared to Q3.

Emerging Market M&A down in spite of strong cross border deal flowEmerging market deal activity in 2011 decreased 11.7% from the same period in 2010. However, inbound cross-border activity into emerging market countries in 2011 added up to US$ 200.3bn, up 19.1% compared to 2010 (US$ 168.2bn) and was the highest annual total on mergermar-ket record.

Private Equity Buyouts strongest since 20082011 was the strongest year for buyout activity since 2008, with deals announced with a total value of US$ 277.7bn, a 15.3% increase from the same period in 2010. The proportion of global M&A activity in 2011 accounted for by buyouts was 12.9%, up from 11.3% in 2010 and the highest proportion since 2007.

Highest exit premiums in US and Europe since 2008Last year was the first to see an upward trend in exit premiums in the US and Europe since 2008. European average premiums on private equity exits in 2011 were at their highest levels on mergermarket record (since 2001).

Energy, Mining & Utilities top sector in 2011 The Energy, Mining & Utilities sector saw the highest total value of M&A deals in 2011, accounting for 25.6% of global M&A deals announced, with deals totalling US$ 557.7bn. Industrials & Chemicals followed with US$ 365bn-worth of deals.

Busy year for Cross-border M&A2011 was the busiest year for cross-border M&A since 2008. Cross-border deals between individual countries accounted for 41.5% of global M&A activity, the second highest proportion since 2007.

European M&A for the year valued US$ 697.9bn, up 4.8% from 2010 (US$ 665.9bn)Q4 2011 saw US$ 116.3bn-worth of deals, a 28.7% drop from the previous quarter (US$ 163.1bn in Q3).

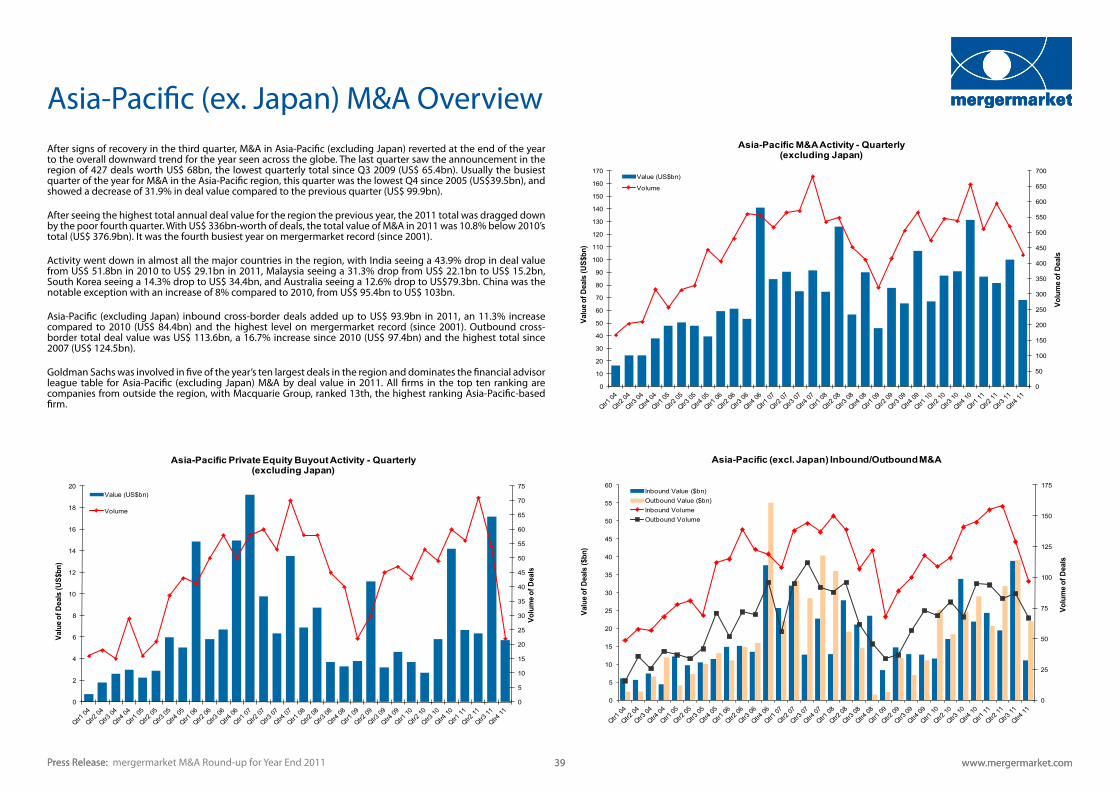

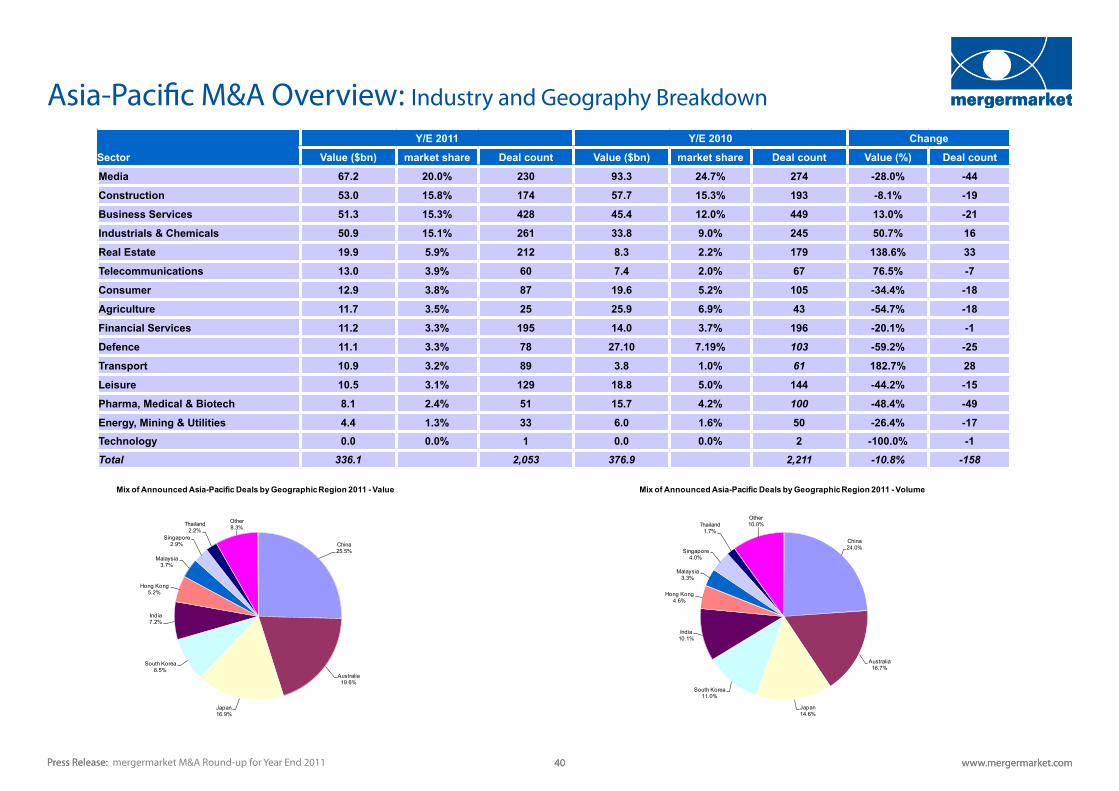

Asia-Pacific M&A valued US$ 336.1bn, down 10.8% from 2010 (US$ 376.9bn)Q4 activity was down 31.9%, from US$ 100bn in Q3 to US$ 68bn.

mergermarket M&A Round-up for Year End 2011 CONTENTS:2 mergermarket M&A Round-up3 Global M&A Overview 6 - Mid-Market 7 - Private Equity9 - Emerging Markets10 - Premia and Multiples Analysis 11 - Deal Type/Deal Value Breakdown 12 - Consideration Structure/

Insolvency 13 - Demerger 14 - Global M&A Overview 16 - European M&A Overview 29 - US M&A Overview 39 - Asia -Pacific (ex.Japan) M&A

Overview 49 - Africa & Middle East M&A

Overview 52 - Criteria/About mergermarket

PRESS CONTACTS:EMEA: Flora Wilke

Tel: +44 207 059 6348

Americas: Dara Silverstein

[email protected]: +1 646 378 3118

Asia-Pacific: Michel Chau

[email protected]: +852 2158 9706

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500

2,750

3,000

3,250

3,500

3,750

4,000

4,250

4,500

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

Volu

me o

f Dea

ls

Valu

e of D

eals

(US$

bn)

Global M&A Activity - Quarterly

RoW M&A

Asia-Pacif ic ex Jp M&A

US M&A

European M&A

Volume

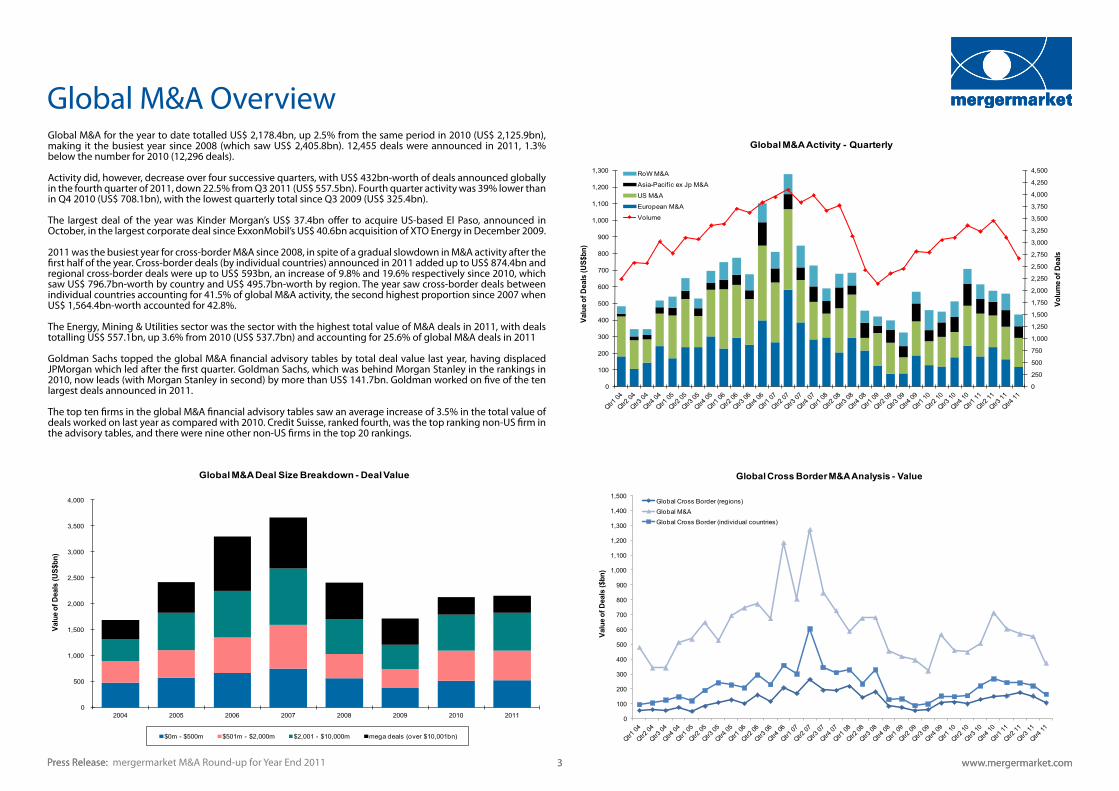

Global M&A for the year to date totalled US$ 2,178.4bn, up 2.5% from the same period in 2010 (US$ 2,125.9bn), making it the busiest year since 2008 (which saw US$ 2,405.8bn). 12,455 deals were announced in 2011, 1.3% below the number for 2010 (12,296 deals).

Activity did, however, decrease over four successive quarters, with US$ 432bn-worth of deals announced globally in the fourth quarter of 2011, down 22.5% from Q3 2011 (US$ 557.5bn). Fourth quarter activity was 39% lower than in Q4 2010 (US$ 708.1bn), with the lowest quarterly total since Q3 2009 (US$ 325.4bn).

The largest deal of the year was Kinder Morgan’s US$ 37.4bn offer to acquire US-based El Paso, announced in October, in the largest corporate deal since ExxonMobil’s US$ 40.6bn acquisition of XTO Energy in December 2009.

2011 was the busiest year for cross-border M&A since 2008, in spite of a gradual slowdown in M&A activity after the first half of the year. Cross-border deals (by individual countries) announced in 2011 added up to US$ 874.4bn and regional cross-border deals were up to US$ 593bn, an increase of 9.8% and 19.6% respectively since 2010, which saw US$ 796.7bn-worth by country and US$ 495.7bn-worth by region. The year saw cross-border deals between individual countries accounting for 41.5% of global M&A activity, the second highest proportion since 2007 when US$ 1,564.4bn-worth accounted for 42.8%.

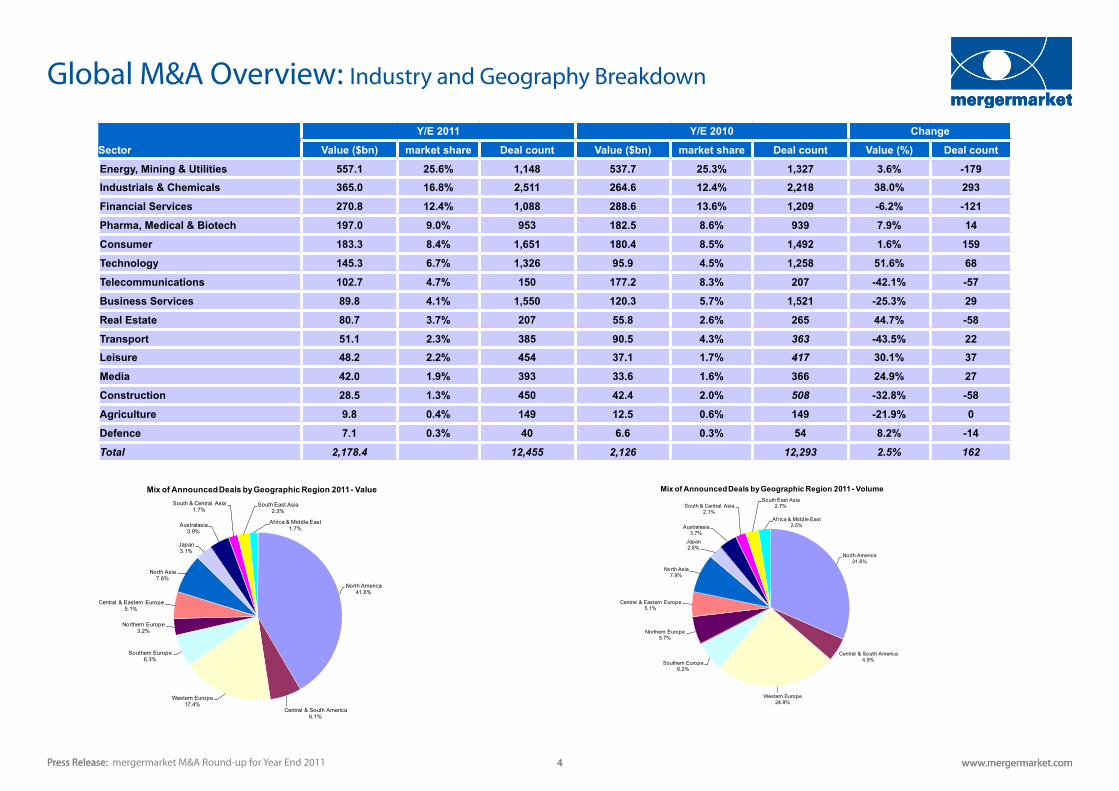

The Energy, Mining & Utilities sector was the sector with the highest total value of M&A deals in 2011, with deals totalling US$ 557.1bn, up 3.6% from 2010 (US$ 537.7bn) and accounting for 25.6% of global M&A deals in 2011

Goldman Sachs topped the global M&A financial advisory tables by total deal value last year, having displaced JPMorgan which led after the first quarter. Goldman Sachs, which was behind Morgan Stanley in the rankings in 2010, now leads (with Morgan Stanley in second) by more than US$ 141.7bn. Goldman worked on five of the ten largest deals announced in 2011.

The top ten firms in the global M&A financial advisory tables saw an average increase of 3.5% in the total value of deals worked on last year as compared with 2010. Credit Suisse, ranked fourth, was the top ranking non-US firm in the advisory tables, and there were nine other non-US firms in the top 20 rankings.

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

Valu

e of

Dea

ls ($

bn)

Global Cross Border M&A Analysis - Value

GlobalCrossBorder(regions)Global M&AGlobalCrossBorder(individualcountries)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2004 2005 2006 2007 2008 2009 2010 2011

Valu

e of D

eals

(US$

bn)

Global M&A Deal Size Breakdown - Deal Value

$0m- $500m $501m- $2,000m $2,001 - $10,000m megadeals(over$10,001bn)

Press Release: www.mergermarket.com 3Press Release: www.mergermarket.com 3

Global M&A Overview

mergermarket M&A Round-up for Year End 2011

NorthAmerica41.6%

Central&SouthAmerica6.1%

Western Europe17.4%

Southern Europe6.3%

Northern Europe3.2%

Central & Eastern Europe5.1%

North Asia7.6%

Japan3.1%

Australasia3.9%

South & Central Asia1.7%

South East Asia2.3%

Africa&MiddleEast1.7%

Mix of Announced Deals by Geographic Region 2011 - Value

NorthAmerica31.6%

Central&SouthAmerica4.9%

Western Europe24.8%

Southern Europe6.2%

Northern Europe5.7%

Central & Eastern Europe5.1%

North Asia7.9%

Japan2.8%

Australasia3.7%

South & Central Asia2.1%

South East Asia2.7%

Africa&MiddleEast2.5%

Mix of Announced Deals by Geographic Region 2011 - Volume

Press Release: www.mergermarket.com 4Press Release: www.mergermarket.com 4

Global M&A Overview: Industry and Geography Breakdown

Y/E 2011 Y/E 2010 Change

Sector Value ($bn) market share Deal count Value ($bn) market share Deal count Value (%) Deal count

Energy, Mining & Utilities 557.1 25.6% 1,148 537.7 25.3% 1,327 3.6% -179Industrials & Chemicals 365.0 16.8% 2,511 264.6 12.4% 2,218 38.0% 293

Financial Services 270.8 12.4% 1,088 288.6 13.6% 1,209 -6.2% -121

Pharma, Medical & Biotech 197.0 9.0% 953 182.5 8.6% 939 7.9% 14

Consumer 183.3 8.4% 1,651 180.4 8.5% 1,492 1.6% 159

Technology 145.3 6.7% 1,326 95.9 4.5% 1,258 51.6% 68

Telecommunications 102.7 4.7% 150 177.2 8.3% 207 -42.1% -57

Business Services 89.8 4.1% 1,550 120.3 5.7% 1,521 -25.3% 29

Real Estate 80.7 3.7% 207 55.8 2.6% 265 44.7% -58

Transport 51.1 2.3% 385 90.5 4.3% 363 -43.5% 22Leisure 48.2 2.2% 454 37.1 1.7% 417 30.1% 37

Media 42.0 1.9% 393 33.6 1.6% 366 24.9% 27

Construction 28.5 1.3% 450 42.4 2.0% 508 -32.8% -58

Agriculture 9.8 0.4% 149 12.5 0.6% 149 -21.9% 0

Defence 7.1 0.3% 40 6.6 0.3% 54 8.2% -14

Total 2,178.4 12,455 2,126 12,293 2.5% 162

mergermarket M&A Round-up for Year End 2011

Press Release: www.mergermarket.com 5Press Release: www.mergermarket.com 5mergermarket M&A Round-up for Year End 2011

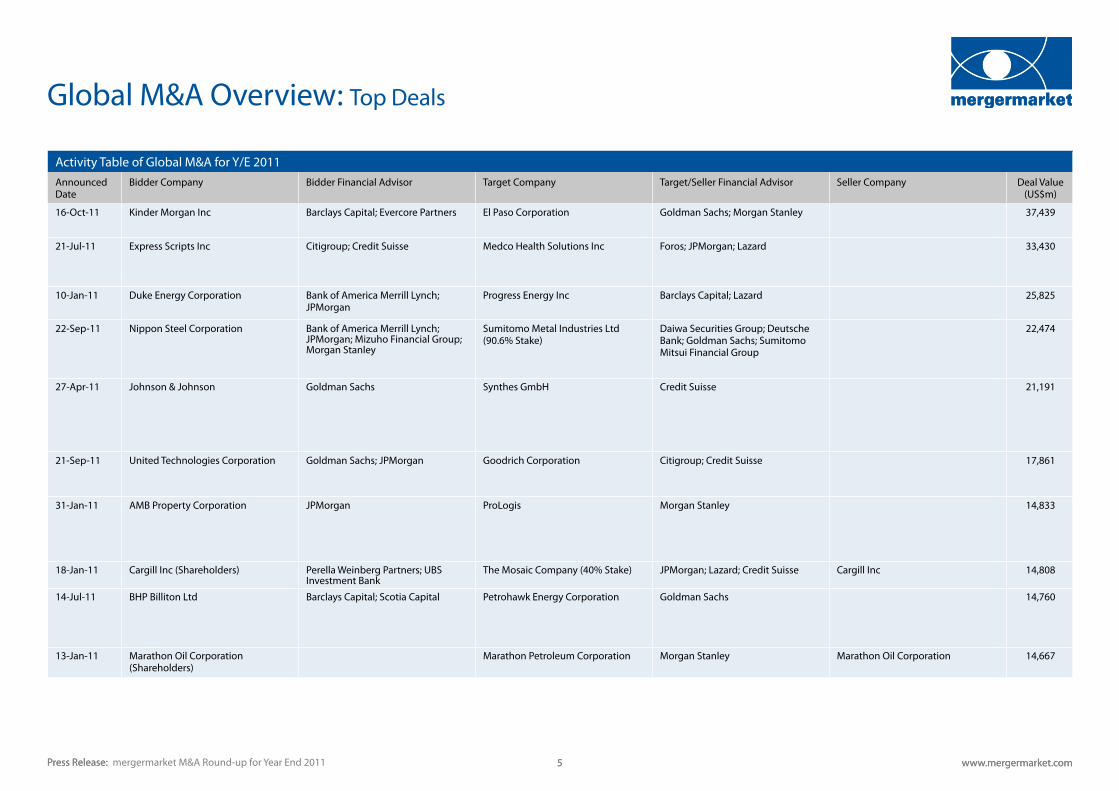

Global M&A Overview: Top Deals

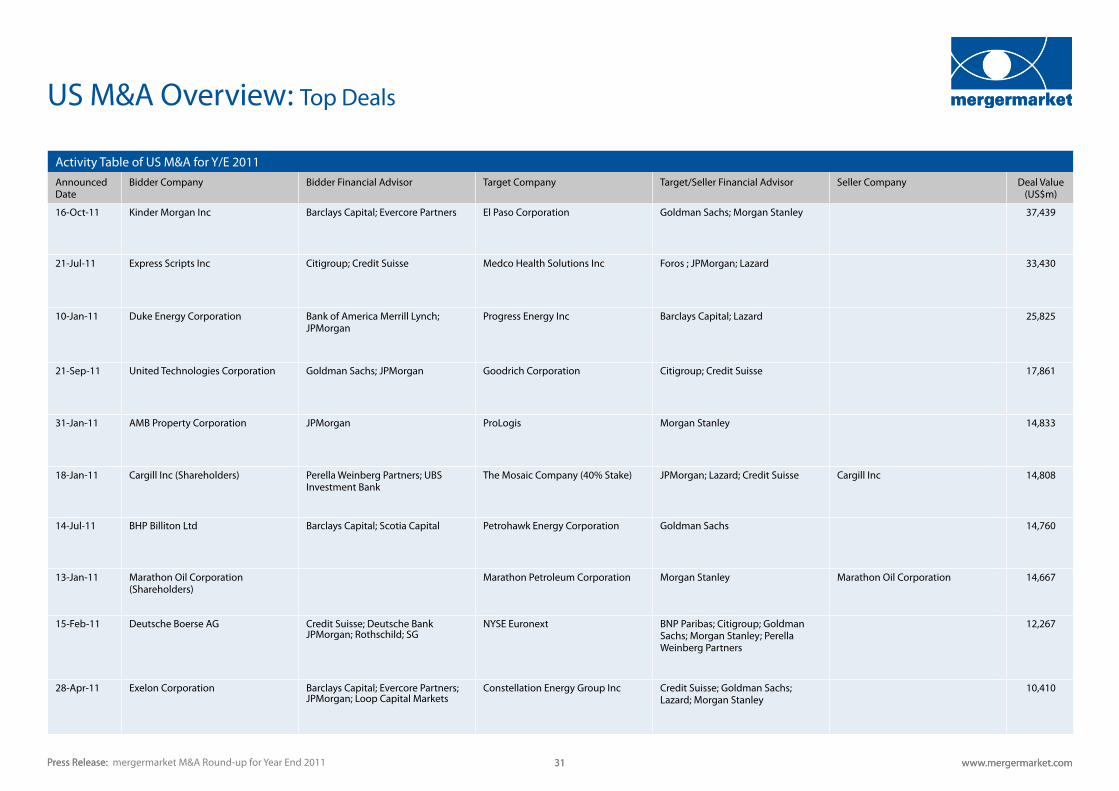

Activity Table of Global M&A for Y/E 2011 Announced Date

Bidder Company Bidder Financial Advisor Target Company Target/Seller Financial Advisor Seller Company Deal Value (US$m)

16-Oct-11 Kinder Morgan Inc Barclays Capital; Evercore Partners El Paso Corporation Goldman Sachs; Morgan Stanley 37,439

21-Jul-11 Express Scripts Inc Citigroup; Credit Suisse Medco Health Solutions Inc Foros; JPMorgan; Lazard 33,430

10-Jan-11 Duke Energy Corporation Bank of America Merrill Lynch; JPMorgan

Progress Energy Inc Barclays Capital; Lazard 25,825

22-Sep-11 Nippon Steel Corporation Bank of America Merrill Lynch; JPMorgan; Mizuho Financial Group; Morgan Stanley

Sumitomo Metal Industries Ltd (90.6% Stake)

Daiwa Securities Group; Deutsche Bank; Goldman Sachs; Sumitomo Mitsui Financial Group

22,474

27-Apr-11 Johnson & Johnson Goldman Sachs Synthes GmbH Credit Suisse 21,191

21-Sep-11 United Technologies Corporation Goldman Sachs; JPMorgan Goodrich Corporation Citigroup; Credit Suisse 17,861

31-Jan-11 AMB Property Corporation JPMorgan ProLogis Morgan Stanley 14,833

18-Jan-11 Cargill Inc (Shareholders) Perella Weinberg Partners; UBS Investment Bank

The Mosaic Company (40% Stake) JPMorgan; Lazard; Credit Suisse Cargill Inc 14,808

14-Jul-11 BHP Billiton Ltd Barclays Capital; Scotia Capital Petrohawk Energy Corporation Goldman Sachs 14,760

13-Jan-11 Marathon Oil Corporation (Shareholders)

Marathon Petroleum Corporation Morgan Stanley Marathon Oil Corporation 14,667

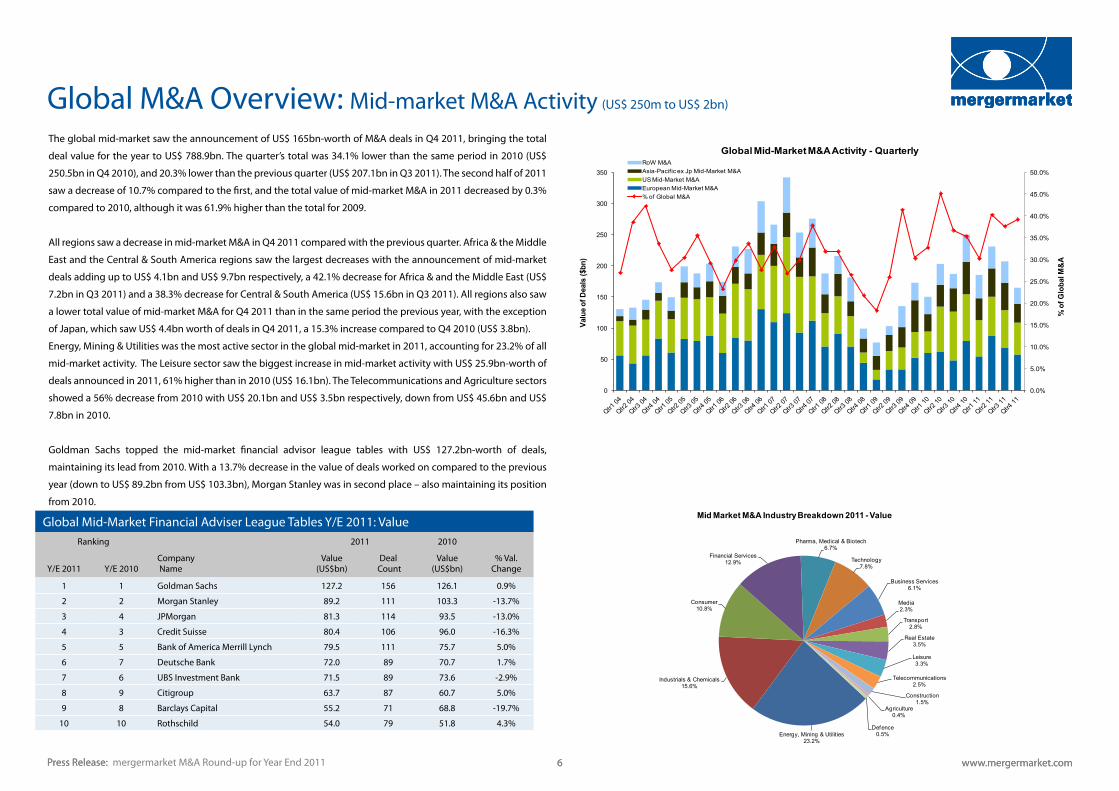

The global mid-market saw the announcement of US$ 165bn-worth of M&A deals in Q4 2011, bringing the total

deal value for the year to US$ 788.9bn. The quarter’s total was 34.1% lower than the same period in 2010 (US$

250.5bn in Q4 2010), and 20.3% lower than the previous quarter (US$ 207.1bn in Q3 2011). The second half of 2011

saw a decrease of 10.7% compared to the first, and the total value of mid-market M&A in 2011 decreased by 0.3%

compared to 2010, although it was 61.9% higher than the total for 2009.

All regions saw a decrease in mid-market M&A in Q4 2011 compared with the previous quarter. Africa & the Middle

East and the Central & South America regions saw the largest decreases with the announcement of mid-market

deals adding up to US$ 4.1bn and US$ 9.7bn respectively, a 42.1% decrease for Africa & and the Middle East (US$

7.2bn in Q3 2011) and a 38.3% decrease for Central & South America (US$ 15.6bn in Q3 2011). All regions also saw

a lower total value of mid-market M&A for Q4 2011 than in the same period the previous year, with the exception

of Japan, which saw US$ 4.4bn worth of deals in Q4 2011, a 15.3% increase compared to Q4 2010 (US$ 3.8bn).

Energy, Mining & Utilities was the most active sector in the global mid-market in 2011, accounting for 23.2% of all

mid-market activity. The Leisure sector saw the biggest increase in mid-market activity with US$ 25.9bn-worth of

deals announced in 2011, 61% higher than in 2010 (US$ 16.1bn). The Telecommunications and Agriculture sectors

showed a 56% decrease from 2010 with US$ 20.1bn and US$ 3.5bn respectively, down from US$ 45.6bn and US$

7.8bn in 2010.

Goldman Sachs topped the mid-market financial advisor league tables with US$ 127.2bn-worth of deals,

maintaining its lead from 2010. With a 13.7% decrease in the value of deals worked on compared to the previous

year (down to US$ 89.2bn from US$ 103.3bn), Morgan Stanley was in second place – also maintaining its position

from 2010.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

0

50

100

150

200

250

300

350

Valu

e of

Dea

ls ($

bn)

Global Mid-Market M&A Activity - QuarterlyRoW M&AAsia-PacificexJpMid-Market M&AUSMid-Market M&AEuropeanMid-Market M&A%ofGlobalM&A

% o

fGlo

bal M

&A

Global Mid-Market Financial Adviser League Tables Y/E 2011: ValueRanking 2011 2010

Y/E 2011 Y/E 2010Company Name

Value (US$bn)

Deal Count

Value (US$bn)

% Val. Change

1 1 Goldman Sachs 127.2 156 126.1 0.9%

2 2 Morgan Stanley 89.2 111 103.3 -13.7%

3 4 JPMorgan 81.3 114 93.5 -13.0%

4 3 Credit Suisse 80.4 106 96.0 -16.3%

5 5 Bank of America Merrill Lynch 79.5 111 75.7 5.0%

6 7 Deutsche Bank 72.0 89 70.7 1.7%

7 6 UBS Investment Bank 71.5 89 73.6 -2.9%

8 9 Citigroup 63.7 87 60.7 5.0%

9 8 Barclays Capital 55.2 71 68.8 -19.7%

10 10 Rothschild 54.0 79 51.8 4.3%

Press Release: www.mergermarket.com 6Press Release: www.mergermarket.com 6

Global M&A Overview: Mid-market M&A Activity (US$ 250m to US$ 2bn)

mergermarket M&A Round-up for Year End 2011

Energy,Mining&Utilities23.2%

Industrials&Chemicals15.6%

Consumer10.8%

Financial Services12.9%

Pharma,Medical&Biotech6.7%

Technology7.8%

Business Services6.1%

Media2.3%

Transport2.8%

Real Estate3.5%

Leisure3.3%

Telecommunications2.5%

Construction1.5%

Agriculture0.4%

Defence0.5%

Mid Market M&A Industry Breakdown 2011 -Value

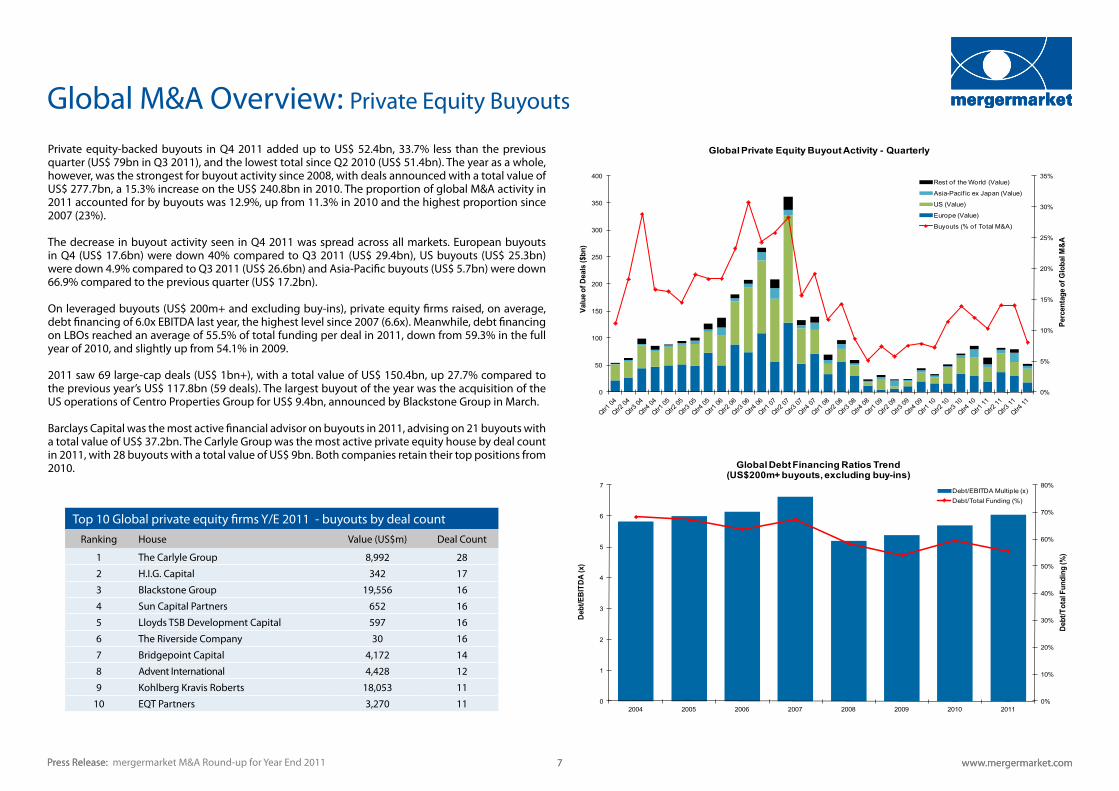

Private equity-backed buyouts in Q4 2011 added up to US$ 52.4bn, 33.7% less than the previous quarter (US$ 79bn in Q3 2011), and the lowest total since Q2 2010 (US$ 51.4bn). The year as a whole, however, was the strongest for buyout activity since 2008, with deals announced with a total value of US$ 277.7bn, a 15.3% increase on the US$ 240.8bn in 2010. The proportion of global M&A activity in 2011 accounted for by buyouts was 12.9%, up from 11.3% in 2010 and the highest proportion since 2007 (23%).

The decrease in buyout activity seen in Q4 2011 was spread across all markets. European buyouts in Q4 (US$ 17.6bn) were down 40% compared to Q3 2011 (US$ 29.4bn), US buyouts (US$ 25.3bn) were down 4.9% compared to Q3 2011 (US$ 26.6bn) and Asia-Pacific buyouts (US$ 5.7bn) were down 66.9% compared to the previous quarter (US$ 17.2bn).

On leveraged buyouts (US$ 200m+ and excluding buy-ins), private equity firms raised, on average, debt financing of 6.0x EBITDA last year, the highest level since 2007 (6.6x). Meanwhile, debt financing on LBOs reached an average of 55.5% of total funding per deal in 2011, down from 59.3% in the full year of 2010, and slightly up from 54.1% in 2009.

2011 saw 69 large-cap deals (US$ 1bn+), with a total value of US$ 150.4bn, up 27.7% compared to the previous year’s US$ 117.8bn (59 deals). The largest buyout of the year was the acquisition of the US operations of Centro Properties Group for US$ 9.4bn, announced by Blackstone Group in March.

Barclays Capital was the most active financial advisor on buyouts in 2011, advising on 21 buyouts with a total value of US$ 37.2bn. The Carlyle Group was the most active private equity house by deal count in 2011, with 28 buyouts with a total value of US$ 9bn. Both companies retain their top positions from 2010.

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

1

2

3

4

5

6

7

2004 2005 2006 2007 2008 2009 2010 2011

Debt

/Tot

al F

undi

ng (%

)

Debt

/EBI

TDA

(x)

Global Debt Financing Ratios Trend(US$200m+ buyouts, excluding buy-ins)

Debt/EBITDAMultiple(x)Debt/TotalFunding(%)

0%

5%

10%

15%

20%

25%

30%

35%

0

50

100

150

200

250

300

350

400

Perc

enta

ge o

f Glo

bal M

&A

Valu

e of D

eals

($bn

)

Global Private Equity Buyout Activity - Quarterly

Restof theWorld(Value)

Asia-Pacif icexJapan(Value)

US(Value)

Europe(Value)

Buyouts(%of TotalM&A)

Top 10 Global private equity firms Y/E 2011 - buyouts by deal countRanking House Value (US$m) Deal Count

1 The Carlyle Group 8,992 28

2 H.I.G. Capital 342 17

3 Blackstone Group 19,556 16

4 Sun Capital Partners 652 16

5 Lloyds TSB Development Capital 597 16

6 The Riverside Company 30 16

7 Bridgepoint Capital 4,172 14

8 Advent International 4,428 12

9 Kohlberg Kravis Roberts 18,053 11

10 EQT Partners 3,270 11

Press Release: www.mergermarket.com 7Press Release: www.mergermarket.com 7

Global M&A Overview: Private Equity Buyouts

mergermarket M&A Round-up for Year End 2011

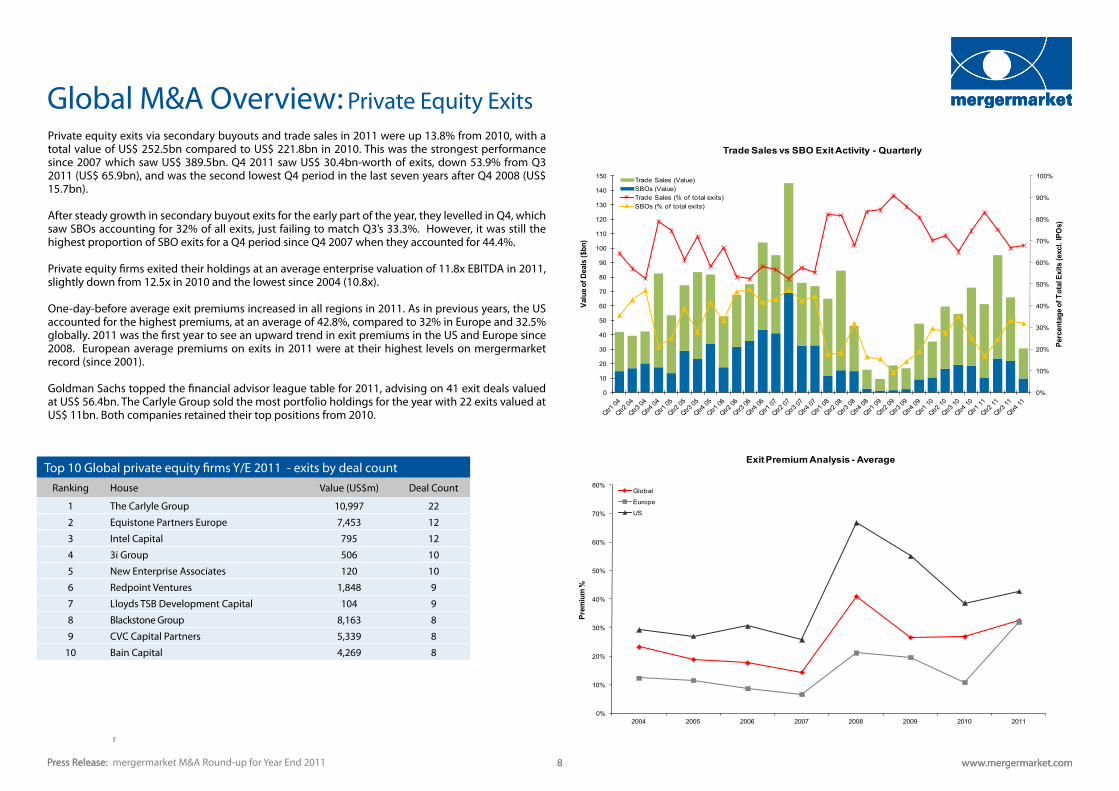

Private equity exits via secondary buyouts and trade sales in 2011 were up 13.8% from 2010, with a total value of US$ 252.5bn compared to US$ 221.8bn in 2010. This was the strongest performance since 2007 which saw US$ 389.5bn. Q4 2011 saw US$ 30.4bn-worth of exits, down 53.9% from Q3 2011 (US$ 65.9bn), and was the second lowest Q4 period in the last seven years after Q4 2008 (US$ 15.7bn).

After steady growth in secondary buyout exits for the early part of the year, they levelled in Q4, which saw SBOs accounting for 32% of all exits, just failing to match Q3’s 33.3%. However, it was still the highest proportion of SBO exits for a Q4 period since Q4 2007 when they accounted for 44.4%.

Private equity firms exited their holdings at an average enterprise valuation of 11.8x EBITDA in 2011, slightly down from 12.5x in 2010 and the lowest since 2004 (10.8x).

One-day-before average exit premiums increased in all regions in 2011. As in previous years, the US accounted for the highest premiums, at an average of 42.8%, compared to 32% in Europe and 32.5% globally. 2011 was the first year to see an upward trend in exit premiums in the US and Europe since 2008. European average premiums on exits in 2011 were at their highest levels on mergermarket record (since 2001).

Goldman Sachs topped the financial advisor league table for 2011, advising on 41 exit deals valued at US$ 56.4bn. The Carlyle Group sold the most portfolio holdings for the year with 22 exits valued at US$ 11bn. Both companies retained their top positions from 2010.

0%

10%

20%

30%

40%

50%

60%

70%

80%

2004 2005 2006 2007 2008 2009 2010 2011

Prem

ium

%

Exit Premium Analysis - Average

Global

Europe

US

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

Perc

enta

ge o

f Tot

al E

xits

(exc

l. IP

Os)

Valu

e of D

eals

($bn

)

Trade Sales vs SBO Exit Activity - Quarterly

TradeSales(Value)SBOs(Value)TradeSales(%of totalexits)SBOs(%of totalexits)

Top 10 Global private equity firms Y/E 2011 - exits by deal countRanking House Value (US$m) Deal Count

1 The Carlyle Group 10,997 22

2 Equistone Partners Europe 7,453 12

3 Intel Capital 795 12

4 3i Group 506 10

5 New Enterprise Associates 120 10

6 Redpoint Ventures 1,848 9

7 Lloyds TSB Development Capital 104 9

8 Blackstone Group 8,163 8

9 CVC Capital Partners 5,339 8

10 Bain Capital 4,269 8

Press Release: www.mergermarket.com 8Press Release: www.mergermarket.com 8

Global M&A Overview: Private Equity Exits

mergermarket M&A Round-up for Year End 2011

r

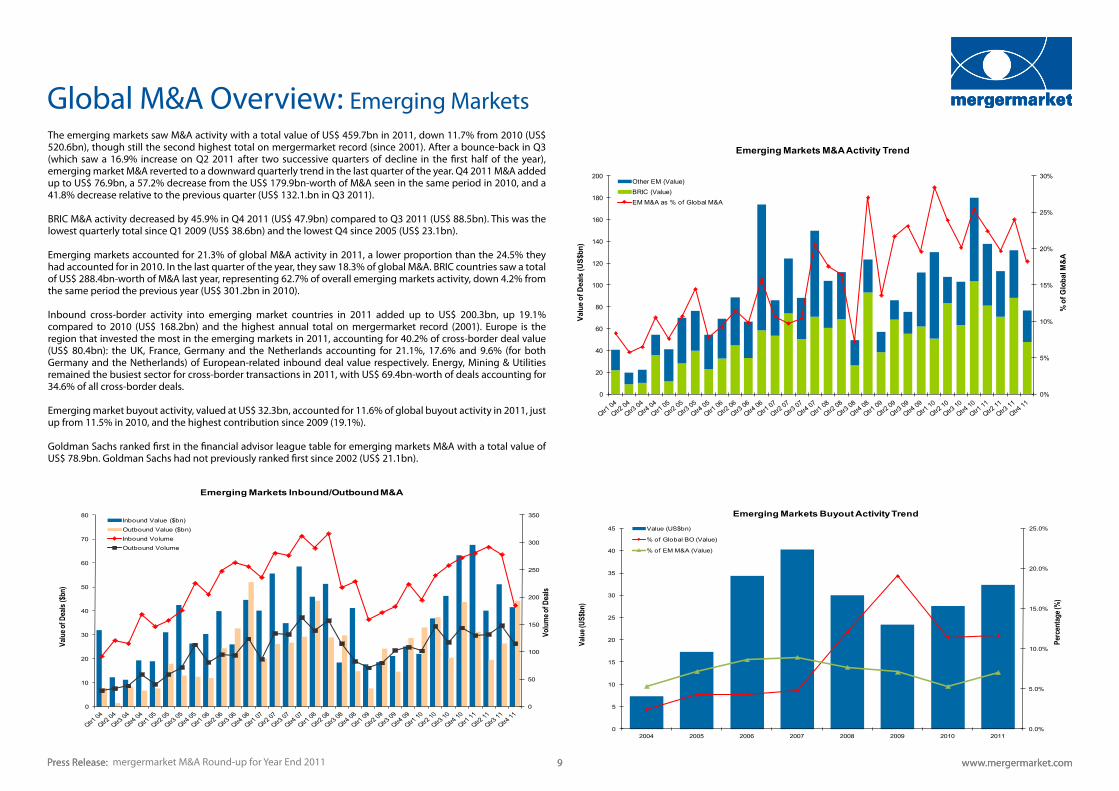

The emerging markets saw M&A activity with a total value of US$ 459.7bn in 2011, down 11.7% from 2010 (US$ 520.6bn), though still the second highest total on mergermarket record (since 2001). After a bounce-back in Q3 (which saw a 16.9% increase on Q2 2011 after two successive quarters of decline in the first half of the year), emerging market M&A reverted to a downward quarterly trend in the last quarter of the year. Q4 2011 M&A added up to US$ 76.9bn, a 57.2% decrease from the US$ 179.9bn-worth of M&A seen in the same period in 2010, and a 41.8% decrease relative to the previous quarter (US$ 132.1.bn in Q3 2011).

BRIC M&A activity decreased by 45.9% in Q4 2011 (US$ 47.9bn) compared to Q3 2011 (US$ 88.5bn). This was the lowest quarterly total since Q1 2009 (US$ 38.6bn) and the lowest Q4 since 2005 (US$ 23.1bn).

Emerging markets accounted for 21.3% of global M&A activity in 2011, a lower proportion than the 24.5% they had accounted for in 2010. In the last quarter of the year, they saw 18.3% of global M&A. BRIC countries saw a total of US$ 288.4bn-worth of M&A last year, representing 62.7% of overall emerging markets activity, down 4.2% from the same period the previous year (US$ 301.2bn in 2010).

Inbound cross-border activity into emerging market countries in 2011 added up to US$ 200.3bn, up 19.1% compared to 2010 (US$ 168.2bn) and the highest annual total on mergermarket record (2001). Europe is the region that invested the most in the emerging markets in 2011, accounting for 40.2% of cross-border deal value (US$ 80.4bn): the UK, France, Germany and the Netherlands accounting for 21.1%, 17.6% and 9.6% (for both Germany and the Netherlands) of European-related inbound deal value respectively. Energy, Mining & Utilities remained the busiest sector for cross-border transactions in 2011, with US$ 69.4bn-worth of deals accounting for 34.6% of all cross-border deals.

Emerging market buyout activity, valued at US$ 32.3bn, accounted for 11.6% of global buyout activity in 2011, just up from 11.5% in 2010, and the highest contribution since 2009 (19.1%).

Goldman Sachs ranked first in the financial advisor league table for emerging markets M&A with a total value of US$ 78.9bn. Goldman Sachs had not previously ranked first since 2002 (US$ 21.1bn).

0%

5%

10%

15%

20%

25%

30%

0

20

40

60

80

100

120

140

160

180

200

% o

f Glo

bal M

&A

Valu

e of D

eals

(US$

bn)

Emerging Markets M&A Activity Trend

OtherEM(Value)BRIC(Value)EMM&Aas%of GlobalM&A

0

50

100

150

200

250

300

350

0

10

20

30

40

50

60

70

80

Volu

me o

f Dea

ls

Valu

e of D

eals

($bn

)

Emerging Markets Inbound/Outbound M&A

InboundValue($bn)OutboundValue($bn)InboundVolumeOutboundVolume

Press Release: www.mergermarket.com 9Press Release: www.mergermarket.com 9

Global M&A Overview: Emerging Markets

mergermarket M&A Round-up for Year End 2011

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

0

5

10

15

20

25

30

35

40

45

2004 2005 2006 2007 2008 2009 2010 2011

Perc

enta

ge (%

)

Valu

e (US

$bn)

Emerging Markets Buyout Activity TrendValue(US$bn)

%of GlobalBO(Value)

%of EMM&A(Value)

0

5

10

15

20

25

30

2004 2005 2006 2007 2008 2009 2010 2011

EBIT

DA M

ultip

le (x

) -Av

erag

e

EBITDA Multiple Analysis - Average

Global

Europe

NorthAmerica

Asia-Pacif ic(excl.Japan)

Japan

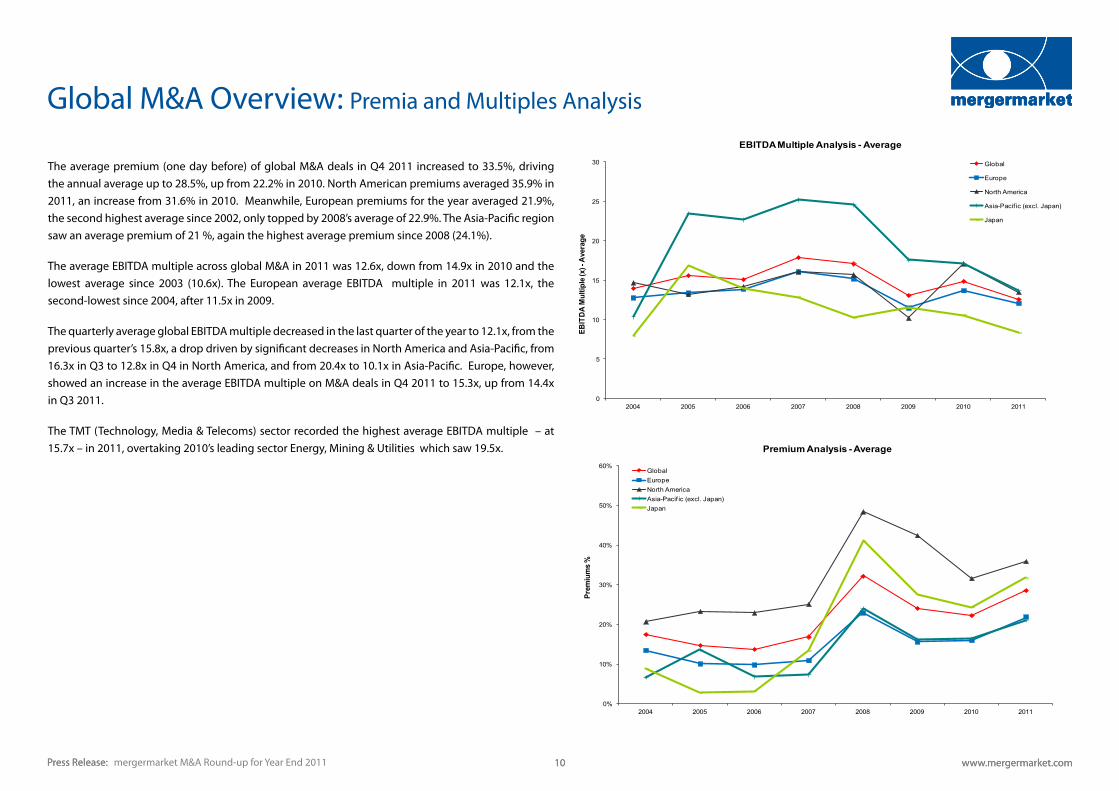

The average premium (one day before) of global M&A deals in Q4 2011 increased to 33.5%, driving the annual average up to 28.5%, up from 22.2% in 2010. North American premiums averaged 35.9% in 2011, an increase from 31.6% in 2010. Meanwhile, European premiums for the year averaged 21.9%, the second highest average since 2002, only topped by 2008’s average of 22.9%. The Asia-Pacific region saw an average premium of 21 %, again the highest average premium since 2008 (24.1%).

The average EBITDA multiple across global M&A in 2011 was 12.6x, down from 14.9x in 2010 and the lowest average since 2003 (10.6x). The European average EBITDA multiple in 2011 was 12.1x, the second-lowest since 2004, after 11.5x in 2009.

The quarterly average global EBITDA multiple decreased in the last quarter of the year to 12.1x, from the previous quarter’s 15.8x, a drop driven by significant decreases in North America and Asia-Pacific, from 16.3x in Q3 to 12.8x in Q4 in North America, and from 20.4x to 10.1x in Asia-Pacific. Europe, however, showed an increase in the average EBITDA multiple on M&A deals in Q4 2011 to 15.3x, up from 14.4x in Q3 2011.

The TMT (Technology, Media & Telecoms) sector recorded the highest average EBITDA multiple – at 15.7x – in 2011, overtaking 2010’s leading sector Energy, Mining & Utilities which saw 19.5x.

0%

10%

20%

30%

40%

50%

60%

2004 2005 2006 2007 2008 2009 2010 2011

Prem

ium

s %

Premium Analysis - Average

GlobalEuropeNorthAmericaAsia-Pacif ic(excl.Japan)Japan

Press Release: www.mergermarket.com 10Press Release: www.mergermarket.com 10 mergermarket M&A Round-up for Year End 2011

Global M&A Overview: Premia and Multiples Analysis

37.7% 41.2% 37.7%46.2%

31.7% 33.2%27.5%

36.2%

6.0%4.1% 10.1%

2.7%

10.9% 5.0%

4.1%

2.7%

1.7%6.6%

8.6%1.4%

2.4%

0.5%1.2%

0.7%

54.5%48.1%

43.6%49.7%

54.9%61.3%

67.1%60.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005 2006 2007 2008 2009 2010 2011

Shar

e of t

otal

Glo

bal M

&A -D

eal V

alue

s

M&A Deal Type - Deal Value

Recommended Hostile Contested Non-public M&A

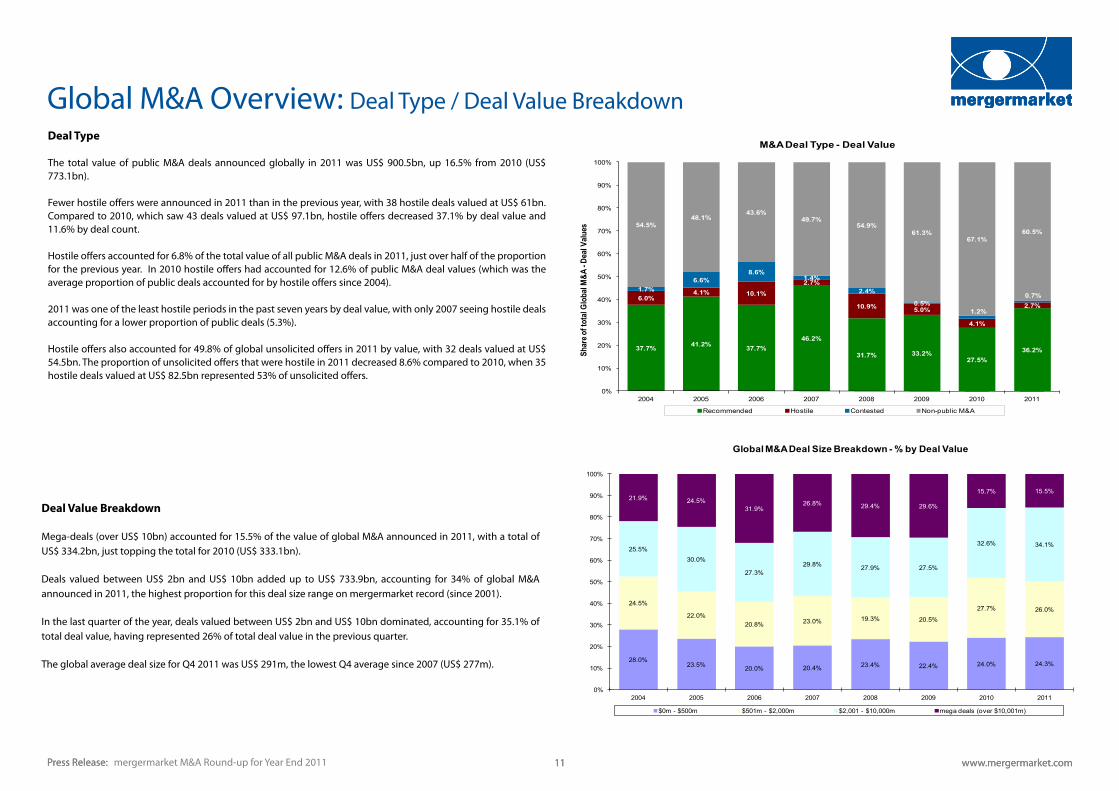

Deal Type

The total value of public M&A deals announced globally in 2011 was US$ 900.5bn, up 16.5% from 2010 (US$ 773.1bn).

Fewer hostile offers were announced in 2011 than in the previous year, with 38 hostile deals valued at US$ 61bn. Compared to 2010, which saw 43 deals valued at US$ 97.1bn, hostile offers decreased 37.1% by deal value and 11.6% by deal count.

Hostile offers accounted for 6.8% of the total value of all public M&A deals in 2011, just over half of the proportion for the previous year. In 2010 hostile offers had accounted for 12.6% of public M&A deal values (which was the average proportion of public deals accounted for by hostile offers since 2004).

2011 was one of the least hostile periods in the past seven years by deal value, with only 2007 seeing hostile deals accounting for a lower proportion of public deals (5.3%).

Hostile offers also accounted for 49.8% of global unsolicited offers in 2011 by value, with 32 deals valued at US$ 54.5bn. The proportion of unsolicited offers that were hostile in 2011 decreased 8.6% compared to 2010, when 35 hostile deals valued at US$ 82.5bn represented 53% of unsolicited offers.

28.0%23.5% 20.0% 20.4% 23.4% 22.4% 24.0% 24.3%

24.5%

22.0%20.8% 23.0% 19.3% 20.5%

27.7% 26.0%

25.5%30.0%

27.3%29.8% 27.9% 27.5%

32.6% 34.1%

21.9% 24.5%31.9%

26.8% 29.4% 29.6%

15.7% 15.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005 2006 2007 2008 2009 2010 2011

Global M&A Deal Size Breakdown - % by Deal Value

$0m- $500m $501m- $2,000m $2,001 - $10,000m megadeals(over$10,001m)

Deal Value Breakdown

Mega-deals (over US$ 10bn) accounted for 15.5% of the value of global M&A announced in 2011, with a total of US$ 334.2bn, just topping the total for 2010 (US$ 333.1bn).

Deals valued between US$ 2bn and US$ 10bn added up to US$ 733.9bn, accounting for 34% of global M&A announced in 2011, the highest proportion for this deal size range on mergermarket record (since 2001).

In the last quarter of the year, deals valued between US$ 2bn and US$ 10bn dominated, accounting for 35.1% of total deal value, having represented 26% of total deal value in the previous quarter.

The global average deal size for Q4 2011 was US$ 291m, the lowest Q4 average since 2007 (US$ 277m).

Press Release: www.mergermarket.com 11Press Release: www.mergermarket.com 11 mergermarket M&A Round-up for Year End 2011

Global M&A Overview: Deal Type / Deal Value Breakdown

57.0% 58.2% 59.1%66.8% 69.8%

55.3%64.2% 65.5%

18.6% 19.2%26.3%

17.8%

23.5%

23.5%

22.5% 20.1%

24.4% 22.7%14.6% 15.4%

6.7%

21.1%13.3% 14.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005 2006 2007 2008 2009 2010 2011

% o

f Glo

bal M

&A

Global Consideration Breakdown - Value %cashonlydeals%equityonlydeals%cash&equitydeals

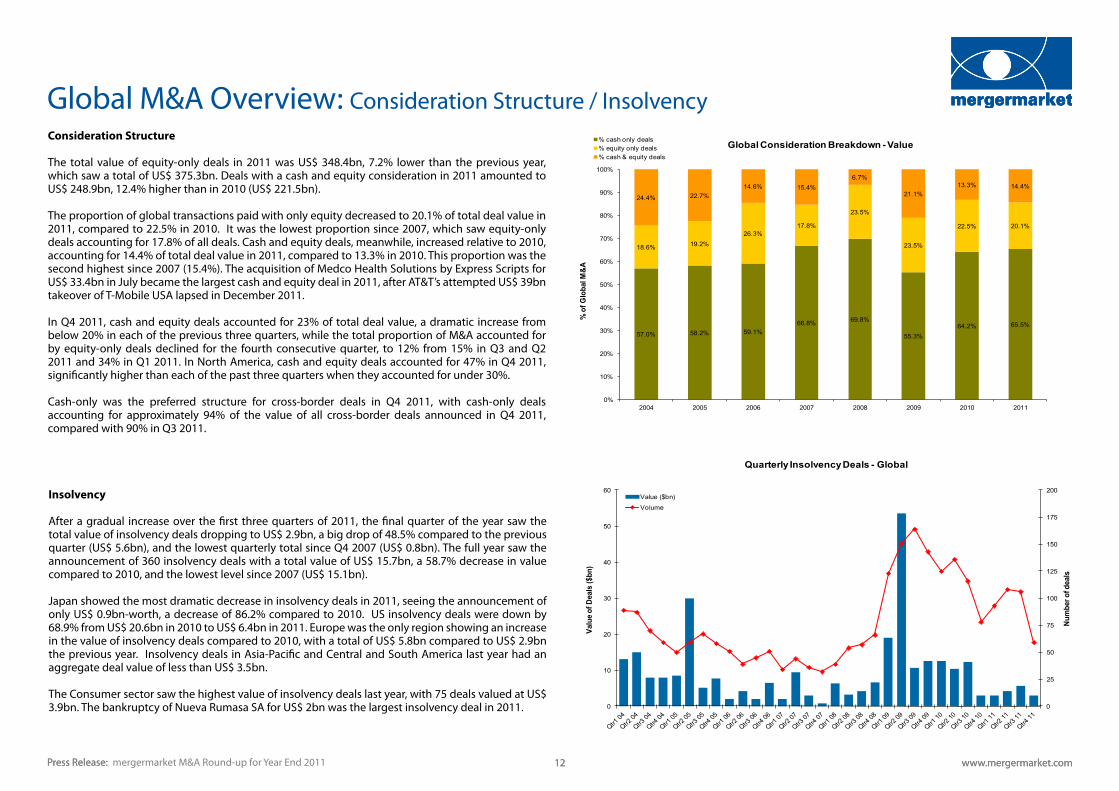

Consideration Structure

The total value of equity-only deals in 2011 was US$ 348.4bn, 7.2% lower than the previous year, which saw a total of US$ 375.3bn. Deals with a cash and equity consideration in 2011 amounted to US$ 248.9bn, 12.4% higher than in 2010 (US$ 221.5bn).

The proportion of global transactions paid with only equity decreased to 20.1% of total deal value in 2011, compared to 22.5% in 2010. It was the lowest proportion since 2007, which saw equity-only deals accounting for 17.8% of all deals. Cash and equity deals, meanwhile, increased relative to 2010, accounting for 14.4% of total deal value in 2011, compared to 13.3% in 2010. This proportion was the second highest since 2007 (15.4%). The acquisition of Medco Health Solutions by Express Scripts for US$ 33.4bn in July became the largest cash and equity deal in 2011, after AT&T’s attempted US$ 39bn takeover of T-Mobile USA lapsed in December 2011.

In Q4 2011, cash and equity deals accounted for 23% of total deal value, a dramatic increase from below 20% in each of the previous three quarters, while the total proportion of M&A accounted for by equity-only deals declined for the fourth consecutive quarter, to 12% from 15% in Q3 and Q2 2011 and 34% in Q1 2011. In North America, cash and equity deals accounted for 47% in Q4 2011, significantly higher than each of the past three quarters when they accounted for under 30%.

Cash-only was the preferred structure for cross-border deals in Q4 2011, with cash-only deals accounting for approximately 94% of the value of all cross-border deals announced in Q4 2011, compared with 90% in Q3 2011.

0

25

50

75

100

125

150

175

200

0

10

20

30

40

50

60

Num

ber o

f dea

ls

Valu

e of D

eals

($bn

)

Quarterly Insolvency Deals - Global

Value($bn)

Volume

Insolvency

After a gradual increase over the first three quarters of 2011, the final quarter of the year saw the total value of insolvency deals dropping to US$ 2.9bn, a big drop of 48.5% compared to the previous quarter (US$ 5.6bn), and the lowest quarterly total since Q4 2007 (US$ 0.8bn). The full year saw the announcement of 360 insolvency deals with a total value of US$ 15.7bn, a 58.7% decrease in value compared to 2010, and the lowest level since 2007 (US$ 15.1bn).

Japan showed the most dramatic decrease in insolvency deals in 2011, seeing the announcement of only US$ 0.9bn-worth, a decrease of 86.2% compared to 2010. US insolvency deals were down by 68.9% from US$ 20.6bn in 2010 to US$ 6.4bn in 2011. Europe was the only region showing an increase in the value of insolvency deals compared to 2010, with a total of US$ 5.8bn compared to US$ 2.9bn the previous year. Insolvency deals in Asia-Pacific and Central and South America last year had an aggregate deal value of less than US$ 3.5bn.

The Consumer sector saw the highest value of insolvency deals last year, with 75 deals valued at US$ 3.9bn. The bankruptcy of Nueva Rumasa SA for US$ 2bn was the largest insolvency deal in 2011.

Press Release: www.mergermarket.com 12Press Release: www.mergermarket.com 12

Global M&A Overview: Consideration Structure / Insolvency

mergermarket M&A Round-up for Year End 2011

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

0

50

100

150

200

250

2004 2005 2006 2007 2008 2009 2010 2011

% o

f Glo

bal M

&A

Valu

e of D

eals

(US$

bn)

Global Demerger Activity Trend

RoWValue(US$bn)

Asia-Pacif icValue(US$bn)

EuropeValue(US$bn)

N.AmericaValue(US$bn)

%of GlobalM&Ainvalue

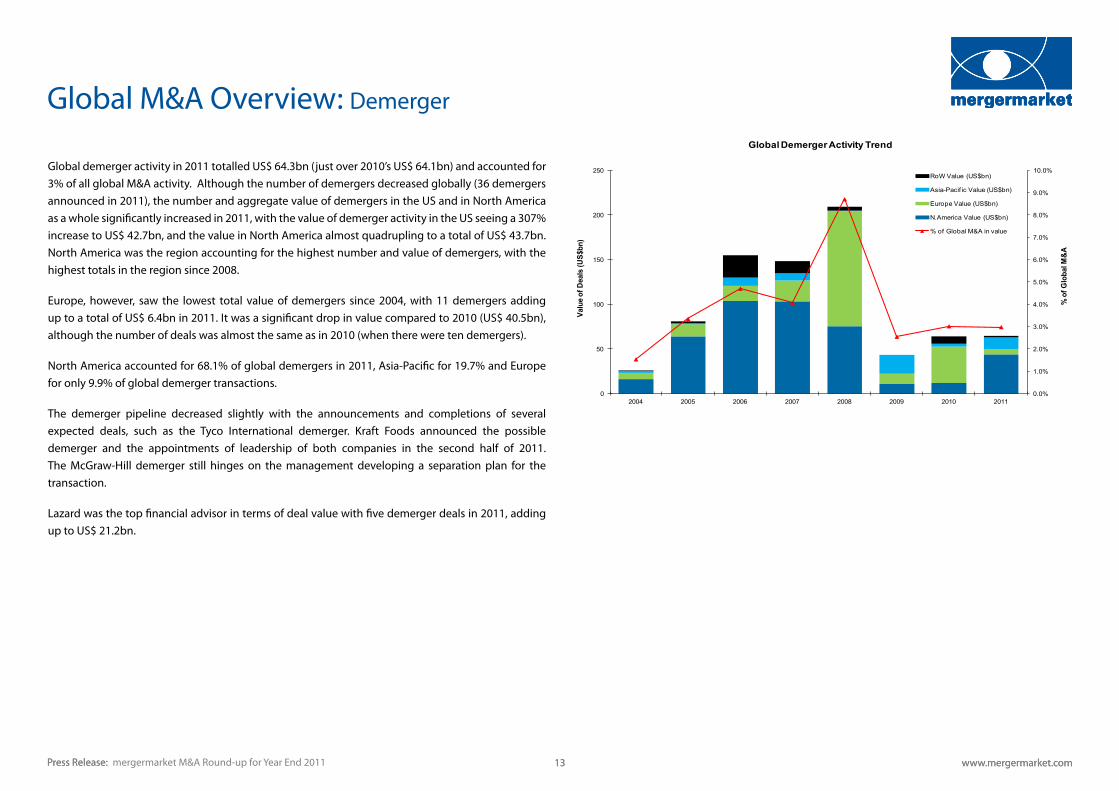

Global demerger activity in 2011 totalled US$ 64.3bn (just over 2010’s US$ 64.1bn) and accounted for 3% of all global M&A activity. Although the number of demergers decreased globally (36 demergers announced in 2011), the number and aggregate value of demergers in the US and in North America as a whole significantly increased in 2011, with the value of demerger activity in the US seeing a 307% increase to US$ 42.7bn, and the value in North America almost quadrupling to a total of US$ 43.7bn. North America was the region accounting for the highest number and value of demergers, with the highest totals in the region since 2008.

Europe, however, saw the lowest total value of demergers since 2004, with 11 demergers adding up to a total of US$ 6.4bn in 2011. It was a significant drop in value compared to 2010 (US$ 40.5bn), although the number of deals was almost the same as in 2010 (when there were ten demergers).

North America accounted for 68.1% of global demergers in 2011, Asia-Pacific for 19.7% and Europe for only 9.9% of global demerger transactions.

The demerger pipeline decreased slightly with the announcements and completions of several expected deals, such as the Tyco International demerger. Kraft Foods announced the possible demerger and the appointments of leadership of both companies in the second half of 2011. The McGraw-Hill demerger still hinges on the management developing a separation plan for the transaction.

Lazard was the top financial advisor in terms of deal value with five demerger deals in 2011, adding up to US$ 21.2bn.

Press Release: www.mergermarket.com 13Press Release: www.mergermarket.com 13

Global M&A Overview: Demerger

mergermarket M&A Round-up for Year End 2011

Press Release: mermergermarket M&A Round-up for Year End 2011www.mergermarket.com 14 www.mergermarket.com 14

Global M&A Overview: League Tables of Financial Advisers

League Table of Financial Advisers to Global M&A: ValueRanking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

2 1 Goldman Sachs 593,411 309 481,698 23.2%

1 2 Morgan Stanley 451,770 246 492,656 -8.3%

4 3 JPMorgan 441,000 227 363,597 21.3%

3 4 Credit Suisse 356,701 209 435,412 -18.1%

9 5 Barclays Capital 321,417 148 258,482 24.3%

8 6 Bank of America Merrill Lynch 315,788 213 274,311 15.1%

5 7 Citigroup 296,214 170 316,046 -6.3%

6 8 Deutsche Bank 260,684 177 276,497 -5.7%

11 9 Lazard 230,722 180 202,254 14.1%

7 10 UBS Investment Bank 226,506 209 275,583 -17.8%

10 11 Rothschild 139,286 209 215,420 -35.4%

17 12 Evercore Partners 101,939 64 79,211 28.7%

13 13 HSBC 101,595 82 116,520 -12.8%

14 14 SG 84,341 72 111,500 -24.4%

15 15 Nomura Holdings 81,956 119 107,348 -23.7%

12 16 BNP Paribas 80,660 94 135,881 -40.6%

20 17 RBC Capital Markets 70,076 111 58,270 20.3%

52 18 Moelis & Company 56,978 51 17,014 234.9%

26 19 Jefferies & Company 55,297 116 39,389 40.4%

22 20 Perella Weinberg Partners 52,763 20 55,967 -5.7%

League Table of Financial Advisers to Global M&A: VolumeRanking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

2 1 Goldman Sachs 593,411 309 292 17

3 2 KPMG 33,712 254 262 -8

1 3 Morgan Stanley 451,770 246 299 -53

6 4 JPMorgan 441,000 227 219 8

5 5 PwC 16,429 226 242 -16

12 6 Bank of America Merrill Lynch 315,788 213 182 31

4 7 Credit Suisse 356,701 209 249 -40

10 8 UBS Investment Bank 226,506 209 199 10

7 9 Rothschild 139,286 209 219 -10

13 10 Ernst & Young 21,665 186 163 23

9 11 Lazard 230,722 180 206 -26

11 12 Deutsche Bank 260,684 177 188 -11

8 13 Deloitte 17,687 172 218 -46

14 14 Citigroup 296,214 170 153 17

15 15 Barclays Capital 321,417 148 137 11

16 16 Nomura Holdings 81,956 119 111 8

18 17 Jefferies & Company 55,297 116 101 15

17 18 RBC Capital Markets 70,076 111 106 5

23 19 M&A International 2,089 98 81 17

22 20 BNP Paribas 80,660 94 81 13

Press Release: www.mergermarket.com 15Press Release: www.mergermarket.com 15mergermarket M&A Round-up for Year End 2011

Global M&A Overview: League Tables of Financial Advisers

League Table of Financial Advisers to Global Buyouts*: ValueRanking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

1 1 Barclays Capital 37,164 21 37,572 -1.1%

6 2 Citigroup 33,567 19 19,222 74.6%

3 3 Bank of America Merrill Lynch 29,441 17 29,375 0.2%

7 4 Deutsche Bank 27,736 13 15,569 78.1%

9 5 Goldman Sachs 25,207 27 10,403 142.3%

4 6 Morgan Stanley 24,110 19 23,522 2.5%

14 7 RBC Capital Markets 23,343 23 6,788 243.9%

2 8 Credit Suisse 20,747 20 31,051 -33.2%

73 9 Wells Fargo Securities 18,602 4 410 4,437.1%

8 10 UBS Investment Bank 18,597 14 14,834 25.4%

15 11 Nomura Holdings 16,242 16 6,711 142.0%

17 12 HSBC 11,528 13 5,933 94.3%

187 13 BMO Capital Markets 7,687 5 - -

38 14 Jefferies & Company 7,344 11 1,412 420.1%

19 15 Rothschild 6,926 13 4,593 50.8%

13 16 Lazard 6,341 15 7,384 -14.1%

5 17 JPMorgan 6,203 7 20,967 -70.4%

20 18 Evercore Partners 5,950 3 3,976 49.6%

58 19 Tudor, Pickering, Holt & Co 5,400 1 725 644.8%

37 20 Banca IMI/Intesa Sanpaolo 4,715 7 1,419 232.3%

*Based on the target geography only and the advisor advising the buy-side only.

League Table of Financial Advisers to Global Buyouts*: VolumeRanking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

10 1 Goldman Sachs 25,207 27 17 10

3 2 PwC 1,862 25 31 -6

29 3 RBC Capital Markets 23,343 23 5 18

5 4 Barclays Capital 37,164 21 27 -6

2 5 Credit Suisse 20,747 20 32 -12

4 6 Deloitte 1,572 20 28 -8

9 7 Citigroup 33,567 19 17 2

8 8 Morgan Stanley 24,110 19 23 -4

6 9 Ernst & Young 1,601 19 24 -5

1 10 KPMG 2,073 18 41 -23

7 11 Bank of America Merrill Lynch 29,441 17 23 -6

23 12 Grant Thornton Corporate Finance 224 17 9 8

12 13 Nomura Holdings 16,242 16 15 1

19 14 Lazard 6,341 15 10 5

20 15 UBS Investment Bank 18,597 14 9 5

13 16 Deutsche Bank 27,736 13 14 -1

16 17 HSBC 11,528 13 11 2

11 18 Rothschild 6,926 13 16 -3

17 19 DC Advisory Partners 2,326 12 11 1

35 20 Jefferies & Company 7,344 11 4 7

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

0

50

100

150

200

250

300

350

400

450

500

550

600

Volu

me o

f Dea

ls

Valu

e of D

eals

(US$

bn)

European M&A Activity - Quarterly

Value(US$bn)

Volume

0

25

50

75

100

125

150

175

200

225

250

275

300

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

Volu

me o

f Dea

ls

Valu

e of D

eals

($bn

)

European Inbound/Outbound M&A

InboundValue($bn)OutboundValue($bn)InboundVolumeOutboundVolume

In line with the global trend, European M&A decreased - in terms of both deal value and number of deals - over the second half of 2011, and the decline in Europe was more pronounced than in other major regions. Q4 2011 saw US$ 116.3bn-worth of deals, a 28.7% decrease from the previous quarter (US$ 163.1bn in Q3), and a 52.4% decrease from the same period the previous year (US$ 244.3bn). The second half of 2011 saw US$ 279.4bn-worth of deals, a total M&A value 33.2% lower than the first half (which saw US$ 418.5bn-worth).

The majority of the larger European countries showed a decline of 50% or more in M&A activity by value in Q4 2011 compared to the previous quarter. Whilst this was not unexpected in some of these countries (such as Ireland down 95% to US$ 820m, Spain down 61.6% to US$ 8.6bn and UK down 44.6% to US$ 21.4bn) due to the current market conditions, some other decreases were more surprising with Russia down by 31.3% (to US$ 13.7bn), Germany by 48.5% (to US$ 4.5bn), Turkey by 13.3% (to US$ 2.6bn) and Poland by 26.3% (to US$ 2.9bn).

Europe finished the year with a higher total M&A value than 2010, a total of US$ 697.9bn for the year compared to US$ 665.9bn for 2010.

Northern Europe, and a few of the Western European countries, had a better year for M&A in 2011 than in 2010, during which the Nordic countries saw a 70.8% increase to US$ 69bn-worth of deals. France, Ireland, Spain and Poland saw similar jumps of 47.9% (to US$ 71.7bn), 57.4% (to US$ 20.5bn), 169.3% (to US$ 81.2bn) and 88.1% (to US$ 22.7bn) respectively. The poor M&A totals in H2 2011, however, affected many other European countries with Portugal down 16.3% (to US$ 3.8bn), Austria 69.6% (to US$ 3.9bn), Italy 54.3% (to US$ 36bn), Turkey 43.6% (to US$ 12.6bn), the Netherlands and Belgium both down around 40% (to US$ 18.9bn and US$ 19.5bn respectively) and Greece down 30.5% (to US$ 3.4bn).

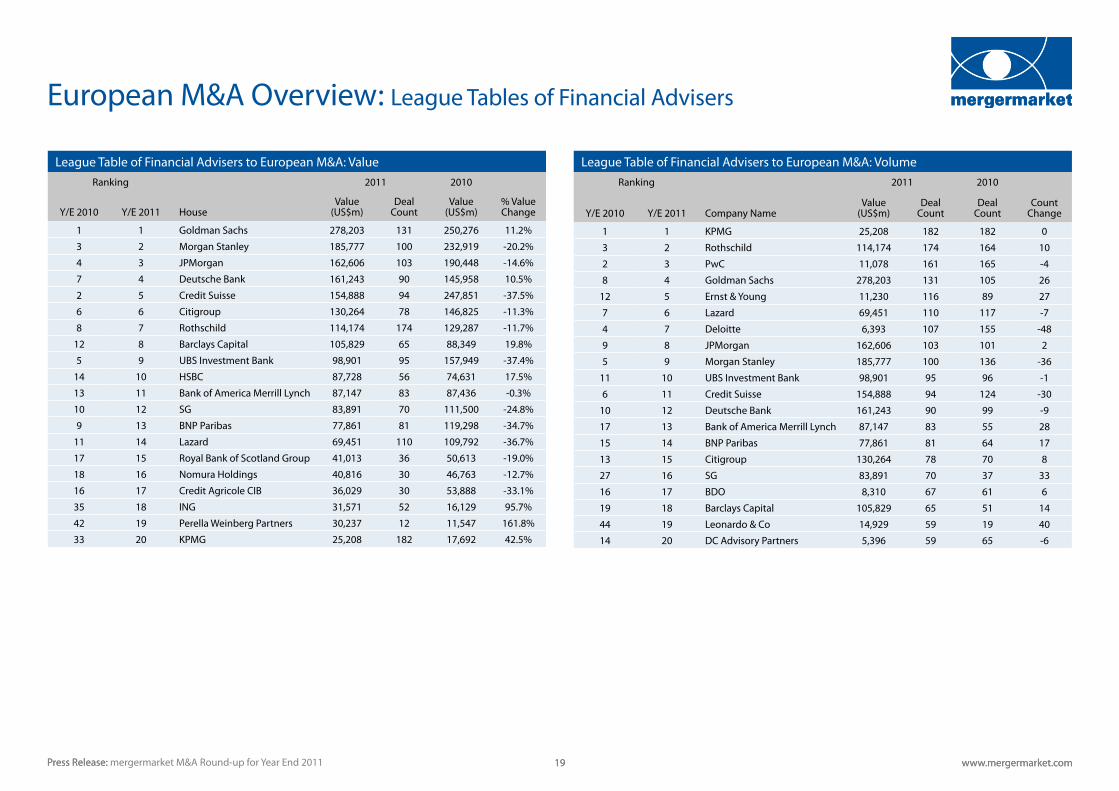

Goldman Sachs and Morgan Stanley held onto their top rankings in the European M&A financial advisory tables by total deal value. Goldman Sachs worked on seven of the ten largest deals in Europe for 2011.

0

25

50

75

100

125

150

175

200

225

250

275

300

325

350

375

400

0

10

20

30

40

50

60

70

80

90

100

110

120

130

Volu

me o

f Dea

ls

Valu

e of D

eals

(US$

bn)

European Private Equity Buyout Activity - Quarterly

Value(US$bn)

Volume

Press Release: www.mergermarket.com 16Press Release: www.mergermarket.com 16

European M&A Overview

mergermarket M&A Round-up for Year End 2011

Press Release: www.mergermarket.com 17Press Release: www.mergermarket.com 17mergermarket M&A Round-up for Year End 2011

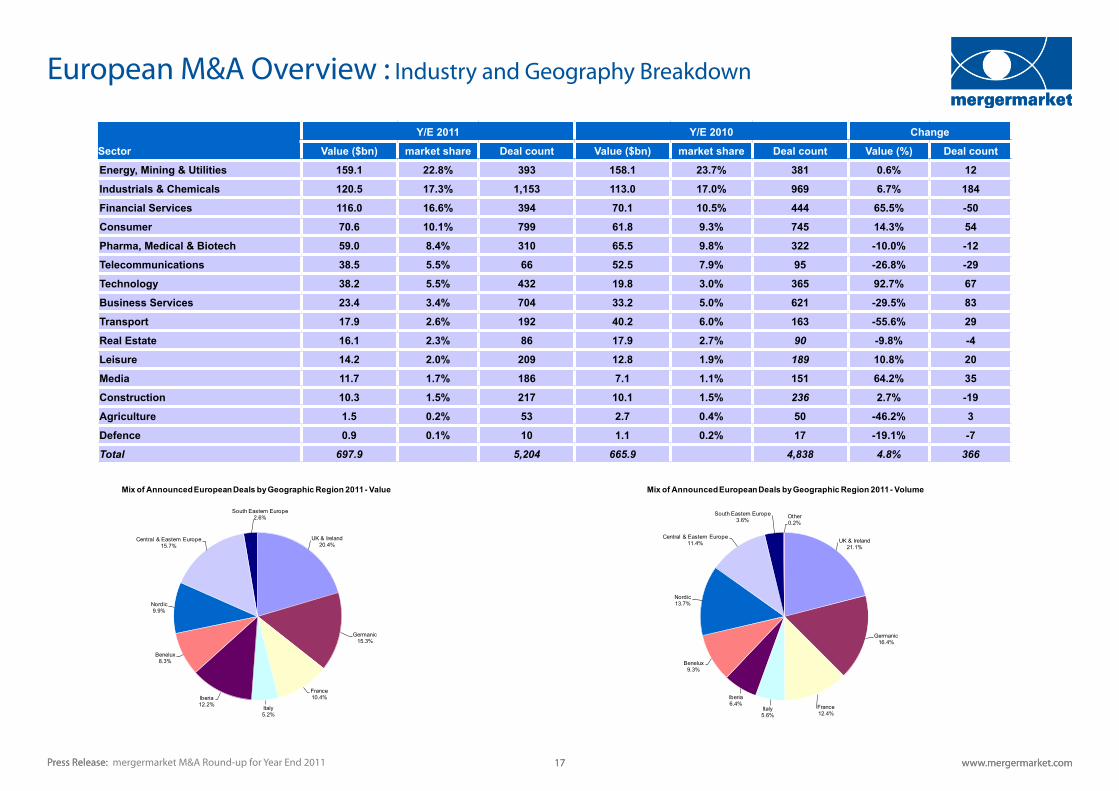

European M&A Overview : Industry and Geography Breakdown

UK&Ireland20.4%

Germanic15.3%

France10.4%

Italy5.2%

Iberia12.2%

Benelux8.3%

Nordic9.9%

Central & Eastern Europe15.7%

South Eastern Europe2.6%

Mix of Announced European Deals by Geographic Region 2011 - Value

UK&Ireland21.1%

Germanic16.4%

France12.4%

Italy5.6%

Iberia6.4%

Benelux9.3%

Nordic13.7%

Central & Eastern Europe11.4%

South Eastern Europe3.6%

Other0.2%

Mix of Announced European Deals by Geographic Region 2011 - Volume

Y/E 2011 Y/E 2010 Change

Sector Value ($bn) market share Deal count Value ($bn) market share Deal count Value (%) Deal count

Energy, Mining & Utilities 159.1 22.8% 393 158.1 23.7% 381 0.6% 12

Industrials & Chemicals 120.5 17.3% 1,153 113.0 17.0% 969 6.7% 184

Financial Services 116.0 16.6% 394 70.1 10.5% 444 65.5% -50

Consumer 70.6 10.1% 799 61.8 9.3% 745 14.3% 54

Pharma, Medical & Biotech 59.0 8.4% 310 65.5 9.8% 322 -10.0% -12

Telecommunications 38.5 5.5% 66 52.5 7.9% 95 -26.8% -29

Technology 38.2 5.5% 432 19.8 3.0% 365 92.7% 67

Business Services 23.4 3.4% 704 33.2 5.0% 621 -29.5% 83

Transport 17.9 2.6% 192 40.2 6.0% 163 -55.6% 29

Real Estate 16.1 2.3% 86 17.9 2.7% 90 -9.8% -4

Leisure 14.2 2.0% 209 12.8 1.9% 189 10.8% 20

Media 11.7 1.7% 186 7.1 1.1% 151 64.2% 35

Construction 10.3 1.5% 217 10.1 1.5% 236 2.7% -19

Agriculture 1.5 0.2% 53 2.7 0.4% 50 -46.2% 3

Defence 0.9 0.1% 10 1.1 0.2% 17 -19.1% -7

Total 697.9 5,204 665.9 4,838 4.8% 366

Press Release: www.mergermarket.com 18Press Release: www.mergermarket.com 18mergermarket M&A Round-up for Year End 2011

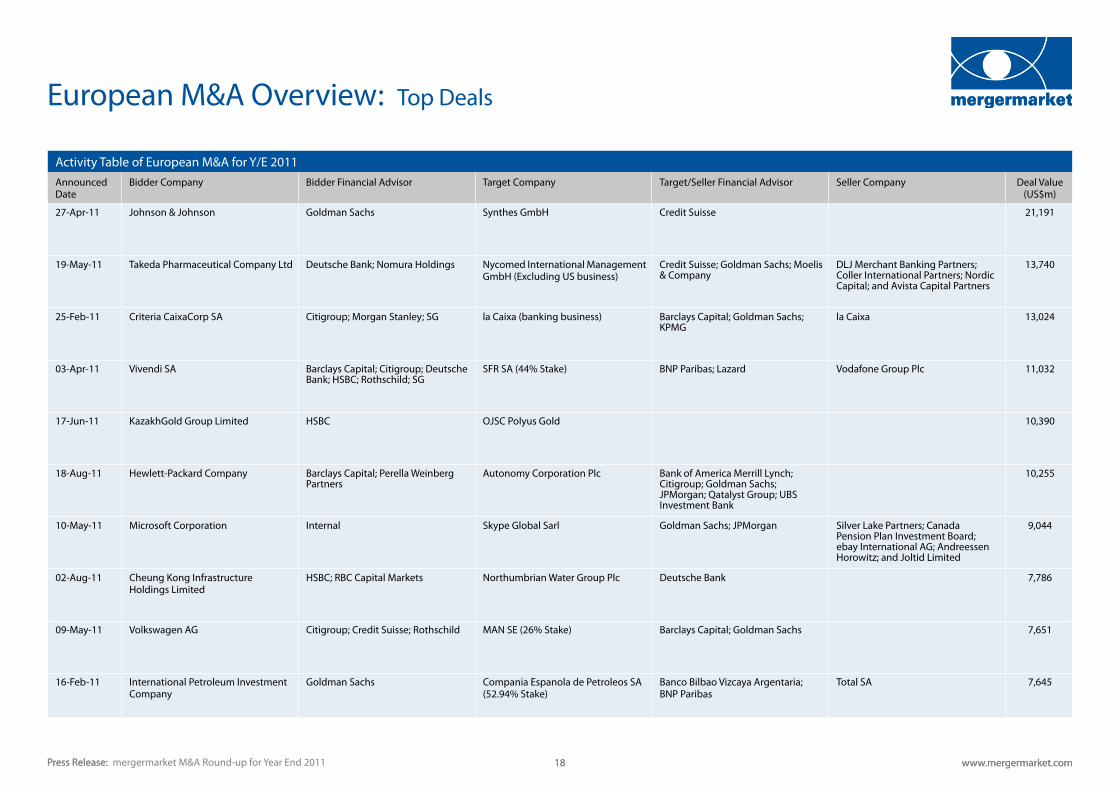

European M&A Overview: Top Deals

Activity Table of European M&A for Y/E 2011Announced Date

Bidder Company Bidder Financial Advisor Target Company Target/Seller Financial Advisor Seller Company Deal Value (US$m)

27-Apr-11 Johnson & Johnson Goldman Sachs Synthes GmbH Credit Suisse 21,191

19-May-11 Takeda Pharmaceutical Company Ltd Deutsche Bank; Nomura Holdings Nycomed International Management GmbH (Excluding US business)

Credit Suisse; Goldman Sachs; Moelis & Company

DLJ Merchant Banking Partners; Coller International Partners; Nordic Capital; and Avista Capital Partners

13,740

25-Feb-11 Criteria CaixaCorp SA Citigroup; Morgan Stanley; SG la Caixa (banking business) Barclays Capital; Goldman Sachs; KPMG

la Caixa 13,024

03-Apr-11 Vivendi SA Barclays Capital; Citigroup; Deutsche Bank; HSBC; Rothschild; SG

SFR SA (44% Stake) BNP Paribas; Lazard Vodafone Group Plc 11,032

17-Jun-11 KazakhGold Group Limited HSBC OJSC Polyus Gold 10,390

18-Aug-11 Hewlett-Packard Company Barclays Capital; Perella Weinberg Partners

Autonomy Corporation Plc Bank of America Merrill Lynch; Citigroup; Goldman Sachs; JPMorgan; Qatalyst Group; UBS Investment Bank

10,255

10-May-11 Microsoft Corporation Internal Skype Global Sarl Goldman Sachs; JPMorgan Silver Lake Partners; Canada Pension Plan Investment Board; ebay International AG; Andreessen Horowitz; and Joltid Limited

9,044

02-Aug-11 Cheung Kong Infrastructure Holdings Limited

HSBC; RBC Capital Markets Northumbrian Water Group Plc Deutsche Bank 7,786

09-May-11 Volkswagen AG Citigroup; Credit Suisse; Rothschild MAN SE (26% Stake) Barclays Capital; Goldman Sachs 7,651

16-Feb-11 International Petroleum Investment Company

Goldman Sachs Compania Espanola de Petroleos SA (52.94% Stake)

Banco Bilbao Vizcaya Argentaria; BNP Paribas

Total SA 7,645

Press Release: www.mergermarket.com 19Press Release: mergermarket M&A Round-up for Year End 2011 www.mergermarket.com 19

European M&A Overview: League Tables of Financial Advisers

League Table of Financial Advisers to European M&A: ValueRanking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

1 1 Goldman Sachs 278,203 131 250,276 11.2%

3 2 Morgan Stanley 185,777 100 232,919 -20.2%

4 3 JPMorgan 162,606 103 190,448 -14.6%

7 4 Deutsche Bank 161,243 90 145,958 10.5%

2 5 Credit Suisse 154,888 94 247,851 -37.5%

6 6 Citigroup 130,264 78 146,825 -11.3%

8 7 Rothschild 114,174 174 129,287 -11.7%

12 8 Barclays Capital 105,829 65 88,349 19.8%

5 9 UBS Investment Bank 98,901 95 157,949 -37.4%

14 10 HSBC 87,728 56 74,631 17.5%

13 11 Bank of America Merrill Lynch 87,147 83 87,436 -0.3%

10 12 SG 83,891 70 111,500 -24.8%

9 13 BNP Paribas 77,861 81 119,298 -34.7%

11 14 Lazard 69,451 110 109,792 -36.7%

17 15 Royal Bank of Scotland Group 41,013 36 50,613 -19.0%

18 16 Nomura Holdings 40,816 30 46,763 -12.7%

16 17 Credit Agricole CIB 36,029 30 53,888 -33.1%

35 18 ING 31,571 52 16,129 95.7%

42 19 Perella Weinberg Partners 30,237 12 11,547 161.8%

33 20 KPMG 25,208 182 17,692 42.5%

League Table of Financial Advisers to European M&A: VolumeRanking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

1 1 KPMG 25,208 182 182 0

3 2 Rothschild 114,174 174 164 10

2 3 PwC 11,078 161 165 -4

8 4 Goldman Sachs 278,203 131 105 26

12 5 Ernst & Young 11,230 116 89 27

7 6 Lazard 69,451 110 117 -7

4 7 Deloitte 6,393 107 155 -48

9 8 JPMorgan 162,606 103 101 2

5 9 Morgan Stanley 185,777 100 136 -36

11 10 UBS Investment Bank 98,901 95 96 -1

6 11 Credit Suisse 154,888 94 124 -30

10 12 Deutsche Bank 161,243 90 99 -9

17 13 Bank of America Merrill Lynch 87,147 83 55 28

15 14 BNP Paribas 77,861 81 64 17

13 15 Citigroup 130,264 78 70 8

27 16 SG 83,891 70 37 33

16 17 BDO 8,310 67 61 6

19 18 Barclays Capital 105,829 65 51 14

44 19 Leonardo & Co 14,929 59 19 40

14 20 DC Advisory Partners 5,396 59 65 -6

Press Release: www.mergermarket.com 20Press Release: mergermarket M&A Round-up for Year End 2011 www.mergermarket.com 20

European M&A Overview: League Tables of Financial Advisers

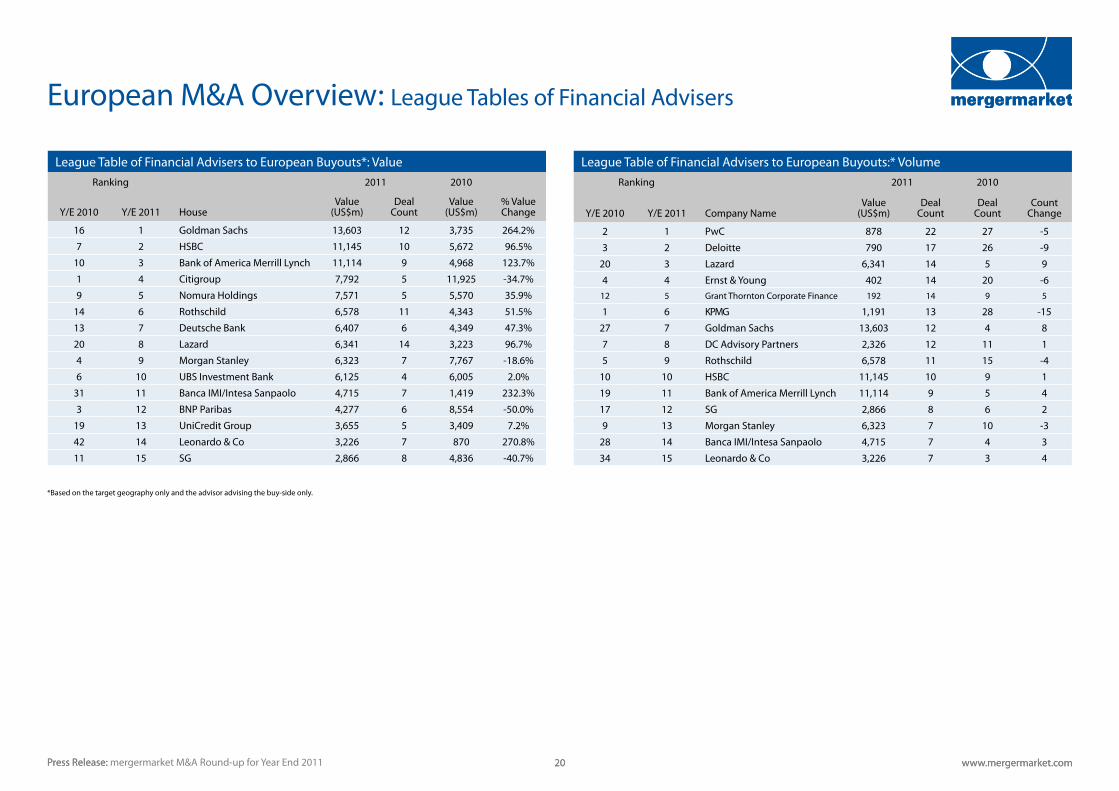

League Table of Financial Advisers to European Buyouts*: ValueRanking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

16 1 Goldman Sachs 13,603 12 3,735 264.2%

7 2 HSBC 11,145 10 5,672 96.5%

10 3 Bank of America Merrill Lynch 11,114 9 4,968 123.7%

1 4 Citigroup 7,792 5 11,925 -34.7%

9 5 Nomura Holdings 7,571 5 5,570 35.9%

14 6 Rothschild 6,578 11 4,343 51.5%

13 7 Deutsche Bank 6,407 6 4,349 47.3%

20 8 Lazard 6,341 14 3,223 96.7%

4 9 Morgan Stanley 6,323 7 7,767 -18.6%

6 10 UBS Investment Bank 6,125 4 6,005 2.0%

31 11 Banca IMI/Intesa Sanpaolo 4,715 7 1,419 232.3%

3 12 BNP Paribas 4,277 6 8,554 -50.0%

19 13 UniCredit Group 3,655 5 3,409 7.2%

42 14 Leonardo & Co 3,226 7 870 270.8%

11 15 SG 2,866 8 4,836 -40.7%

*Based on the target geography only and the advisor advising the buy-side only.

League Table of Financial Advisers to European Buyouts:* VolumeRanking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

2 1 PwC 878 22 27 -5

3 2 Deloitte 790 17 26 -9

20 3 Lazard 6,341 14 5 9

4 4 Ernst & Young 402 14 20 -612 5 Grant Thornton Corporate Finance 192 14 9 5

1 6 KPMG 1,191 13 28 -15

27 7 Goldman Sachs 13,603 12 4 8

7 8 DC Advisory Partners 2,326 12 11 1

5 9 Rothschild 6,578 11 15 -4

10 10 HSBC 11,145 10 9 1

19 11 Bank of America Merrill Lynch 11,114 9 5 4

17 12 SG 2,866 8 6 2

9 13 Morgan Stanley 6,323 7 10 -3

28 14 Banca IMI/Intesa Sanpaolo 4,715 7 4 3

34 15 Leonardo & Co 3,226 7 3 4

Press Release: www.mergermarket.com 21Press Release: www.mergermarket.com 21mergermarket M&A Round-up for Year End 2011

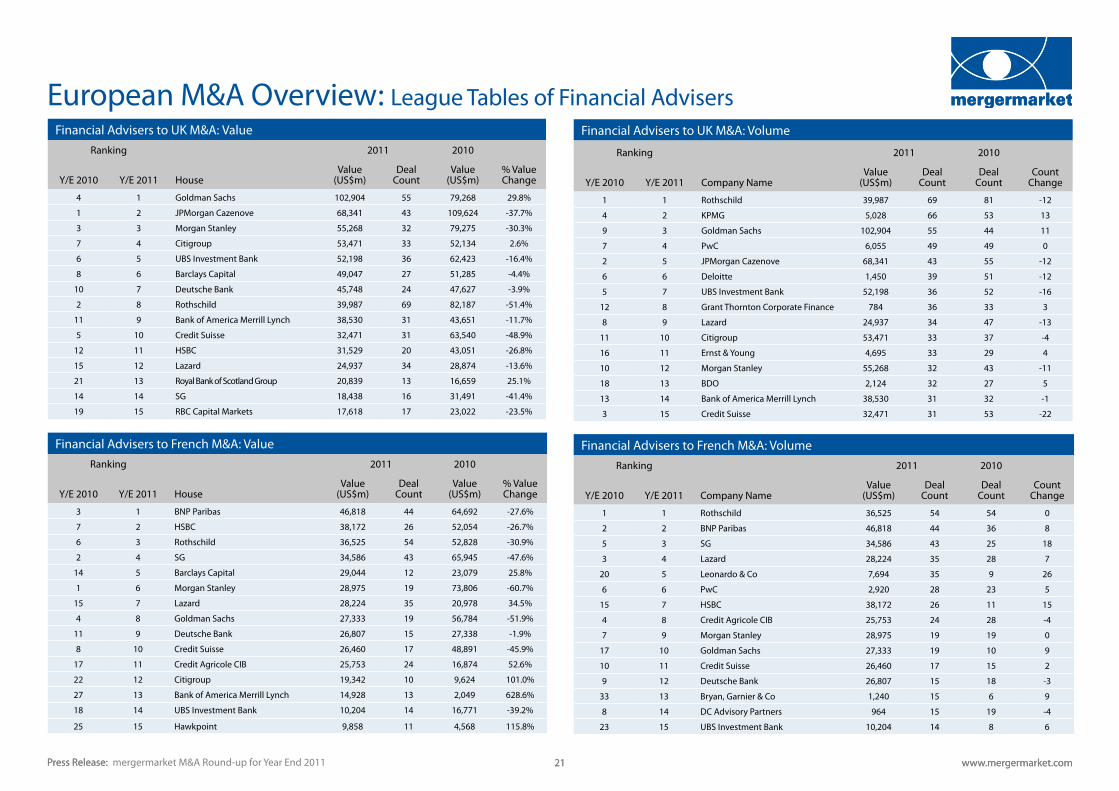

European M&A Overview: League Tables of Financial AdvisersFinancial Advisers to UK M&A: Value

Ranking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

4 1 Goldman Sachs 102,904 55 79,268 29.8%

1 2 JPMorgan Cazenove 68,341 43 109,624 -37.7%

3 3 Morgan Stanley 55,268 32 79,275 -30.3%

7 4 Citigroup 53,471 33 52,134 2.6%

6 5 UBS Investment Bank 52,198 36 62,423 -16.4%

8 6 Barclays Capital 49,047 27 51,285 -4.4%

10 7 Deutsche Bank 45,748 24 47,627 -3.9%

2 8 Rothschild 39,987 69 82,187 -51.4%

11 9 Bank of America Merrill Lynch 38,530 31 43,651 -11.7%

5 10 Credit Suisse 32,471 31 63,540 -48.9%

12 11 HSBC 31,529 20 43,051 -26.8%

15 12 Lazard 24,937 34 28,874 -13.6%

21 13 Royal Bank of Scotland Group 20,839 13 16,659 25.1%

14 14 SG 18,438 16 31,491 -41.4%

19 15 RBC Capital Markets 17,618 17 23,022 -23.5%

Financial Advisers to French M&A: ValueRanking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

3 1 BNP Paribas 46,818 44 64,692 -27.6%

7 2 HSBC 38,172 26 52,054 -26.7%

6 3 Rothschild 36,525 54 52,828 -30.9%

2 4 SG 34,586 43 65,945 -47.6%

14 5 Barclays Capital 29,044 12 23,079 25.8%

1 6 Morgan Stanley 28,975 19 73,806 -60.7%

15 7 Lazard 28,224 35 20,978 34.5%

4 8 Goldman Sachs 27,333 19 56,784 -51.9%

11 9 Deutsche Bank 26,807 15 27,338 -1.9%

8 10 Credit Suisse 26,460 17 48,891 -45.9%

17 11 Credit Agricole CIB 25,753 24 16,874 52.6%

22 12 Citigroup 19,342 10 9,624 101.0%

27 13 Bank of America Merrill Lynch 14,928 13 2,049 628.6%

18 14 UBS Investment Bank 10,204 14 16,771 -39.2%

25 15 Hawkpoint 9,858 11 4,568 115.8%

Financial Advisers to UK M&A: Volume

Ranking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

1 1 Rothschild 39,987 69 81 -12

4 2 KPMG 5,028 66 53 13

9 3 Goldman Sachs 102,904 55 44 11

7 4 PwC 6,055 49 49 0

2 5 JPMorgan Cazenove 68,341 43 55 -12

6 6 Deloitte 1,450 39 51 -12

5 7 UBS Investment Bank 52,198 36 52 -16

12 8 Grant Thornton Corporate Finance 784 36 33 3

8 9 Lazard 24,937 34 47 -13

11 10 Citigroup 53,471 33 37 -4

16 11 Ernst & Young 4,695 33 29 4

10 12 Morgan Stanley 55,268 32 43 -11

18 13 BDO 2,124 32 27 5

13 14 Bank of America Merrill Lynch 38,530 31 32 -1

3 15 Credit Suisse 32,471 31 53 -22

Financial Advisers to French M&A: VolumeRanking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

1 1 Rothschild 36,525 54 54 0

2 2 BNP Paribas 46,818 44 36 8

5 3 SG 34,586 43 25 18

3 4 Lazard 28,224 35 28 7

20 5 Leonardo & Co 7,694 35 9 26

6 6 PwC 2,920 28 23 5

15 7 HSBC 38,172 26 11 15

4 8 Credit Agricole CIB 25,753 24 28 -4

7 9 Morgan Stanley 28,975 19 19 0

17 10 Goldman Sachs 27,333 19 10 9

10 11 Credit Suisse 26,460 17 15 2

9 12 Deutsche Bank 26,807 15 18 -3

33 13 Bryan, Garnier & Co 1,240 15 6 9

8 14 DC Advisory Partners 964 15 19 -4

23 15 UBS Investment Bank 10,204 14 8 6

Press Release: www.mergermarket.com 22Press Release: www.mergermarket.com 22mergermarket M&A Round-up for Year End 2011

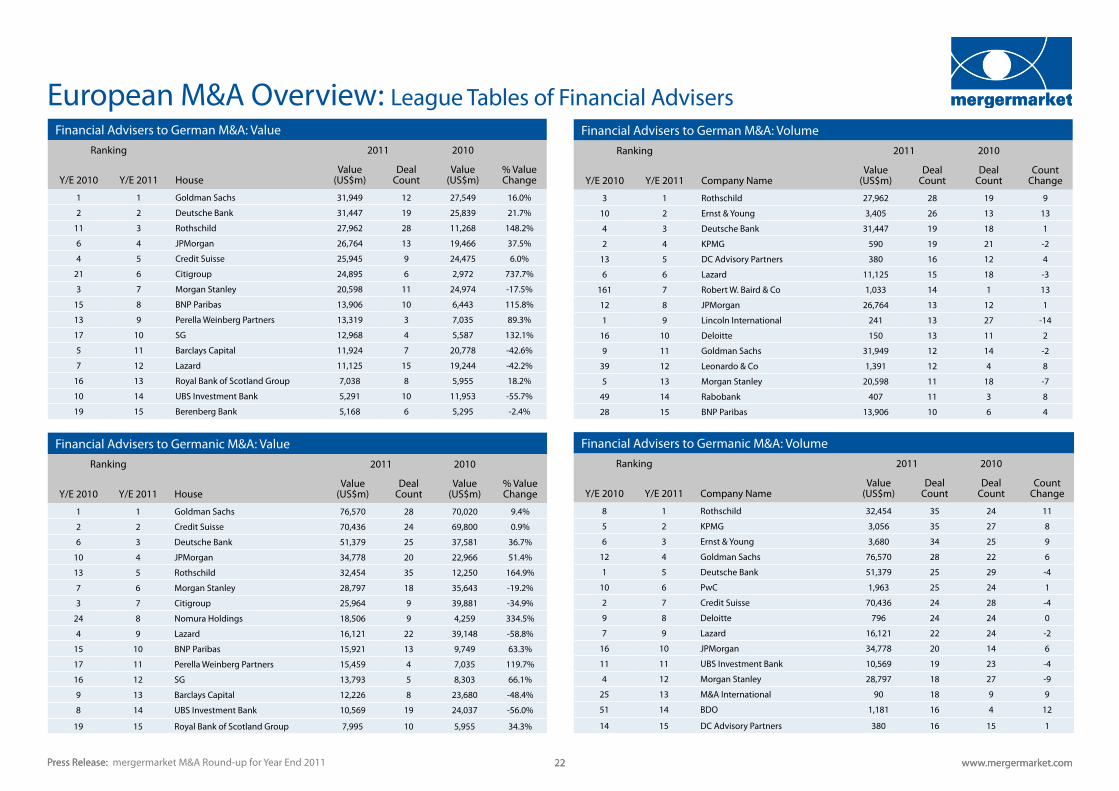

European M&A Overview: League Tables of Financial AdvisersFinancial Advisers to German M&A: Value

Ranking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

1 1 Goldman Sachs 31,949 12 27,549 16.0%

2 2 Deutsche Bank 31,447 19 25,839 21.7%

11 3 Rothschild 27,962 28 11,268 148.2%

6 4 JPMorgan 26,764 13 19,466 37.5%

4 5 Credit Suisse 25,945 9 24,475 6.0%

21 6 Citigroup 24,895 6 2,972 737.7%

3 7 Morgan Stanley 20,598 11 24,974 -17.5%

15 8 BNP Paribas 13,906 10 6,443 115.8%

13 9 Perella Weinberg Partners 13,319 3 7,035 89.3%

17 10 SG 12,968 4 5,587 132.1%

5 11 Barclays Capital 11,924 7 20,778 -42.6%

7 12 Lazard 11,125 15 19,244 -42.2%

16 13 Royal Bank of Scotland Group 7,038 8 5,955 18.2%

10 14 UBS Investment Bank 5,291 10 11,953 -55.7%

19 15 Berenberg Bank 5,168 6 5,295 -2.4%

Financial Advisers to Germanic M&A: ValueRanking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

1 1 Goldman Sachs 76,570 28 70,020 9.4%

2 2 Credit Suisse 70,436 24 69,800 0.9%

6 3 Deutsche Bank 51,379 25 37,581 36.7%

10 4 JPMorgan 34,778 20 22,966 51.4%

13 5 Rothschild 32,454 35 12,250 164.9%

7 6 Morgan Stanley 28,797 18 35,643 -19.2%

3 7 Citigroup 25,964 9 39,881 -34.9%

24 8 Nomura Holdings 18,506 9 4,259 334.5%

4 9 Lazard 16,121 22 39,148 -58.8%

15 10 BNP Paribas 15,921 13 9,749 63.3%

17 11 Perella Weinberg Partners 15,459 4 7,035 119.7%

16 12 SG 13,793 5 8,303 66.1%

9 13 Barclays Capital 12,226 8 23,680 -48.4%

8 14 UBS Investment Bank 10,569 19 24,037 -56.0%

19 15 Royal Bank of Scotland Group 7,995 10 5,955 34.3%

Financial Advisers to German M&A: VolumeRanking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

3 1 Rothschild 27,962 28 19 9

10 2 Ernst & Young 3,405 26 13 13

4 3 Deutsche Bank 31,447 19 18 1

2 4 KPMG 590 19 21 -2

13 5 DC Advisory Partners 380 16 12 4

6 6 Lazard 11,125 15 18 -3

161 7 Robert W. Baird & Co 1,033 14 1 13

12 8 JPMorgan 26,764 13 12 1

1 9 Lincoln International 241 13 27 -14

16 10 Deloitte 150 13 11 2

9 11 Goldman Sachs 31,949 12 14 -2

39 12 Leonardo & Co 1,391 12 4 8

5 13 Morgan Stanley 20,598 11 18 -7

49 14 Rabobank 407 11 3 8

28 15 BNP Paribas 13,906 10 6 4

Financial Advisers to Germanic M&A: VolumeRanking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

8 1 Rothschild 32,454 35 24 11

5 2 KPMG 3,056 35 27 8

6 3 Ernst & Young 3,680 34 25 9

12 4 Goldman Sachs 76,570 28 22 6

1 5 Deutsche Bank 51,379 25 29 -4

10 6 PwC 1,963 25 24 1

2 7 Credit Suisse 70,436 24 28 -4

9 8 Deloitte 796 24 24 0

7 9 Lazard 16,121 22 24 -2

16 10 JPMorgan 34,778 20 14 6

11 11 UBS Investment Bank 10,569 19 23 -4

4 12 Morgan Stanley 28,797 18 27 -9

25 13 M&A International 90 18 9 9

51 14 BDO 1,181 16 4 12

14 15 DC Advisory Partners 380 16 15 1

Press Release: www.mergermarket.com 23Press Release: mergermarket M&A Round-up for Year End 2011 www.mergermarket.com 23

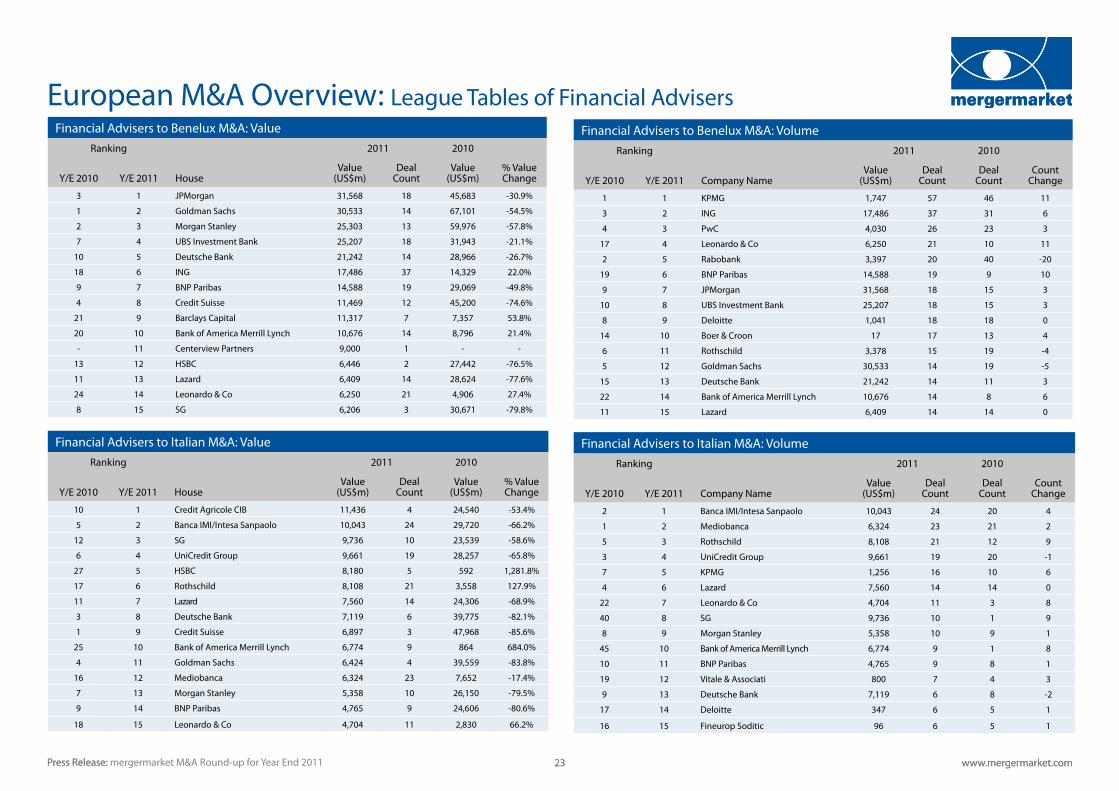

European M&A Overview: League Tables of Financial AdvisersFinancial Advisers to Benelux M&A: Value

Ranking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

3 1 JPMorgan 31,568 18 45,683 -30.9%

1 2 Goldman Sachs 30,533 14 67,101 -54.5%

2 3 Morgan Stanley 25,303 13 59,976 -57.8%

7 4 UBS Investment Bank 25,207 18 31,943 -21.1%

10 5 Deutsche Bank 21,242 14 28,966 -26.7%

18 6 ING 17,486 37 14,329 22.0%

9 7 BNP Paribas 14,588 19 29,069 -49.8%

4 8 Credit Suisse 11,469 12 45,200 -74.6%

21 9 Barclays Capital 11,317 7 7,357 53.8%

20 10 Bank of America Merrill Lynch 10,676 14 8,796 21.4%

- 11 Centerview Partners 9,000 1 - -

13 12 HSBC 6,446 2 27,442 -76.5%

11 13 Lazard 6,409 14 28,624 -77.6%

24 14 Leonardo & Co 6,250 21 4,906 27.4%

8 15 SG 6,206 3 30,671 -79.8%

Financial Advisers to Italian M&A: ValueRanking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

10 1 Credit Agricole CIB 11,436 4 24,540 -53.4%

5 2 Banca IMI/Intesa Sanpaolo 10,043 24 29,720 -66.2%

12 3 SG 9,736 10 23,539 -58.6%

6 4 UniCredit Group 9,661 19 28,257 -65.8%

27 5 HSBC 8,180 5 592 1,281.8%

17 6 Rothschild 8,108 21 3,558 127.9%

11 7 Lazard 7,560 14 24,306 -68.9%

3 8 Deutsche Bank 7,119 6 39,775 -82.1%

1 9 Credit Suisse 6,897 3 47,968 -85.6%

25 10 Bank of America Merrill Lynch 6,774 9 864 684.0%

4 11 Goldman Sachs 6,424 4 39,559 -83.8%

16 12 Mediobanca 6,324 23 7,652 -17.4%

7 13 Morgan Stanley 5,358 10 26,150 -79.5%

9 14 BNP Paribas 4,765 9 24,606 -80.6%

18 15 Leonardo & Co 4,704 11 2,830 66.2%

Financial Advisers to Benelux M&A: VolumeRanking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

1 1 KPMG 1,747 57 46 11

3 2 ING 17,486 37 31 6

4 3 PwC 4,030 26 23 3

17 4 Leonardo & Co 6,250 21 10 11

2 5 Rabobank 3,397 20 40 -20

19 6 BNP Paribas 14,588 19 9 10

9 7 JPMorgan 31,568 18 15 3

10 8 UBS Investment Bank 25,207 18 15 3

8 9 Deloitte 1,041 18 18 0

14 10 Boer & Croon 17 17 13 4

6 11 Rothschild 3,378 15 19 -4

5 12 Goldman Sachs 30,533 14 19 -5

15 13 Deutsche Bank 21,242 14 11 3

22 14 Bank of America Merrill Lynch 10,676 14 8 6

11 15 Lazard 6,409 14 14 0

Financial Advisers to Italian M&A: VolumeRanking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

2 1 Banca IMI/Intesa Sanpaolo 10,043 24 20 4

1 2 Mediobanca 6,324 23 21 2

5 3 Rothschild 8,108 21 12 9

3 4 UniCredit Group 9,661 19 20 -1

7 5 KPMG 1,256 16 10 6

4 6 Lazard 7,560 14 14 0

22 7 Leonardo & Co 4,704 11 3 8

40 8 SG 9,736 10 1 9

8 9 Morgan Stanley 5,358 10 9 1

45 10 Bank of America Merrill Lynch 6,774 9 1 8

10 11 BNP Paribas 4,765 9 8 1

19 12 Vitale & Associati 800 7 4 3

9 13 Deutsche Bank 7,119 6 8 -2

17 14 Deloitte 347 6 5 1

16 15 Fineurop Soditic 96 6 5 1

Press Release: www.mergermarket.com 24Pre: www.mergermarket.com 24mergermarket M&A Round-up for Year End 2011

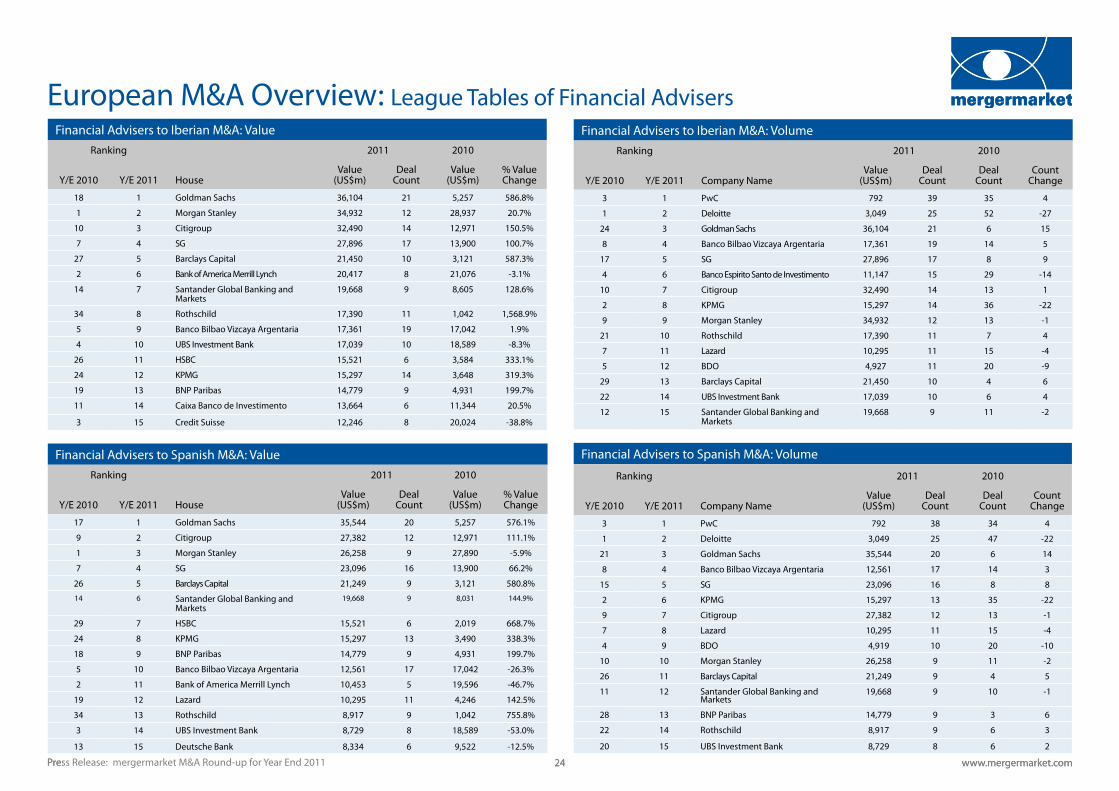

European M&A Overview: League Tables of Financial AdvisersFinancial Advisers to Iberian M&A: Value

Ranking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

18 1 Goldman Sachs 36,104 21 5,257 586.8%

1 2 Morgan Stanley 34,932 12 28,937 20.7%

10 3 Citigroup 32,490 14 12,971 150.5%

7 4 SG 27,896 17 13,900 100.7%

27 5 Barclays Capital 21,450 10 3,121 587.3%

2 6 Bank of America Merrill Lynch 20,417 8 21,076 -3.1%

14 7 Santander Global Banking and Markets

19,668 9 8,605 128.6%

34 8 Rothschild 17,390 11 1,042 1,568.9%

5 9 Banco Bilbao Vizcaya Argentaria 17,361 19 17,042 1.9%

4 10 UBS Investment Bank 17,039 10 18,589 -8.3%

26 11 HSBC 15,521 6 3,584 333.1%

24 12 KPMG 15,297 14 3,648 319.3%

19 13 BNP Paribas 14,779 9 4,931 199.7%

11 14 Caixa Banco de Investimento 13,664 6 11,344 20.5%

3 15 Credit Suisse 12,246 8 20,024 -38.8%

Financial Advisers to Spanish M&A: ValueRanking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

17 1 Goldman Sachs 35,544 20 5,257 576.1%

9 2 Citigroup 27,382 12 12,971 111.1%

1 3 Morgan Stanley 26,258 9 27,890 -5.9%

7 4 SG 23,096 16 13,900 66.2%

26 5 Barclays Capital 21,249 9 3,121 580.8%

14 6 Santander Global Banking and Markets

19,668 9 8,031 144.9%

29 7 HSBC 15,521 6 2,019 668.7%

24 8 KPMG 15,297 13 3,490 338.3%

18 9 BNP Paribas 14,779 9 4,931 199.7%

5 10 Banco Bilbao Vizcaya Argentaria 12,561 17 17,042 -26.3%

2 11 Bank of America Merrill Lynch 10,453 5 19,596 -46.7%

19 12 Lazard 10,295 11 4,246 142.5%

34 13 Rothschild 8,917 9 1,042 755.8%

3 14 UBS Investment Bank 8,729 8 18,589 -53.0%

13 15 Deutsche Bank 8,334 6 9,522 -12.5%

Financial Advisers to Iberian M&A: VolumeRanking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

3 1 PwC 792 39 35 4

1 2 Deloitte 3,049 25 52 -27

24 3 Goldman Sachs 36,104 21 6 15

8 4 Banco Bilbao Vizcaya Argentaria 17,361 19 14 5

17 5 SG 27,896 17 8 9

4 6 Banco Espirito Santo de Investimento 11,147 15 29 -14

10 7 Citigroup 32,490 14 13 1

2 8 KPMG 15,297 14 36 -22

9 9 Morgan Stanley 34,932 12 13 -1

21 10 Rothschild 17,390 11 7 4

7 11 Lazard 10,295 11 15 -4

5 12 BDO 4,927 11 20 -9

29 13 Barclays Capital 21,450 10 4 6

22 14 UBS Investment Bank 17,039 10 6 4

12 15 Santander Global Banking and Markets

19,668 9 11 -2

Financial Advisers to Spanish M&A: Volume

Ranking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

3 1 PwC 792 38 34 4

1 2 Deloitte 3,049 25 47 -22

21 3 Goldman Sachs 35,544 20 6 14

8 4 Banco Bilbao Vizcaya Argentaria 12,561 17 14 3

15 5 SG 23,096 16 8 8

2 6 KPMG 15,297 13 35 -22

9 7 Citigroup 27,382 12 13 -1

7 8 Lazard 10,295 11 15 -4

4 9 BDO 4,919 10 20 -10

10 10 Morgan Stanley 26,258 9 11 -2

26 11 Barclays Capital 21,249 9 4 5

11 12 Santander Global Banking and Markets

19,668 9 10 -1

28 13 BNP Paribas 14,779 9 3 6

22 14 Rothschild 8,917 9 6 3

20 15 UBS Investment Bank 8,729 8 6 2

Press Release: www.mergermarket.com 25Press Release: www.mergermarket.com 25mergermarket M&A Round-up for Year End 2011

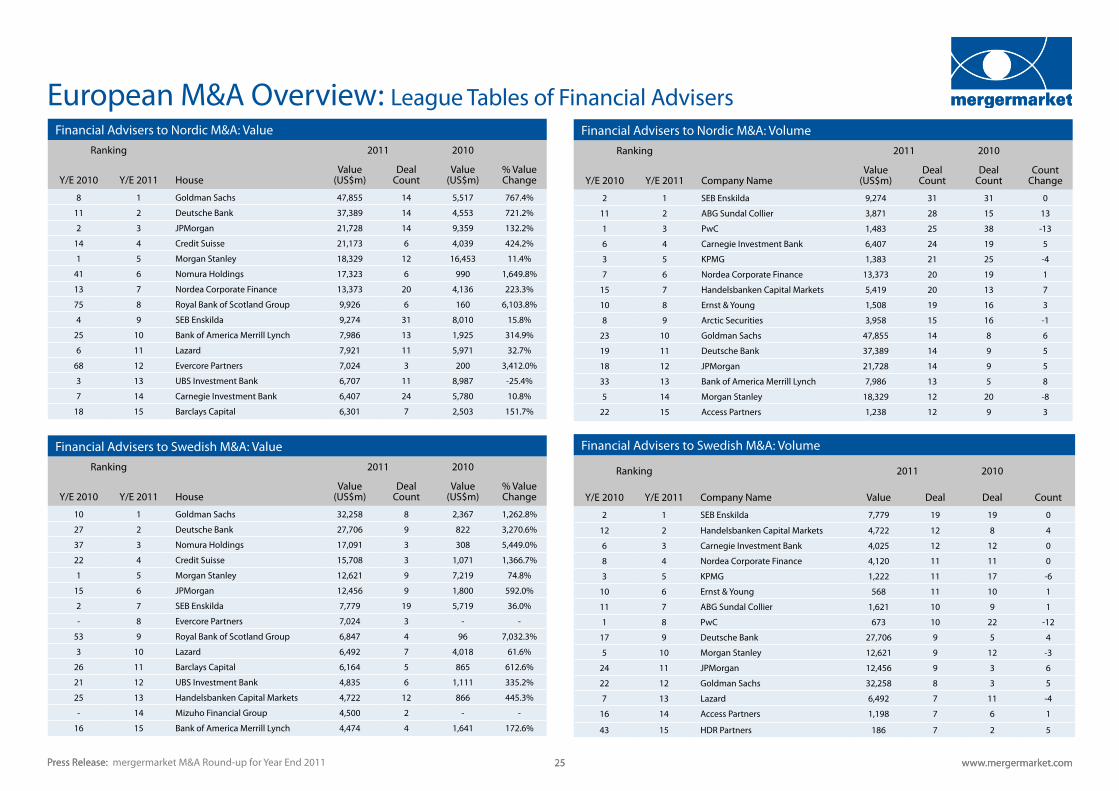

European M&A Overview: League Tables of Financial AdvisersFinancial Advisers to Nordic M&A: Value

Ranking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

8 1 Goldman Sachs 47,855 14 5,517 767.4%

11 2 Deutsche Bank 37,389 14 4,553 721.2%

2 3 JPMorgan 21,728 14 9,359 132.2%

14 4 Credit Suisse 21,173 6 4,039 424.2%

1 5 Morgan Stanley 18,329 12 16,453 11.4%

41 6 Nomura Holdings 17,323 6 990 1,649.8%

13 7 Nordea Corporate Finance 13,373 20 4,136 223.3%

75 8 Royal Bank of Scotland Group 9,926 6 160 6,103.8%

4 9 SEB Enskilda 9,274 31 8,010 15.8%

25 10 Bank of America Merrill Lynch 7,986 13 1,925 314.9%

6 11 Lazard 7,921 11 5,971 32.7%

68 12 Evercore Partners 7,024 3 200 3,412.0%

3 13 UBS Investment Bank 6,707 11 8,987 -25.4%

7 14 Carnegie Investment Bank 6,407 24 5,780 10.8%

18 15 Barclays Capital 6,301 7 2,503 151.7%

Financial Advisers to Nordic M&A: VolumeRanking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

2 1 SEB Enskilda 9,274 31 31 0

11 2 ABG Sundal Collier 3,871 28 15 13

1 3 PwC 1,483 25 38 -13

6 4 Carnegie Investment Bank 6,407 24 19 5

3 5 KPMG 1,383 21 25 -4

7 6 Nordea Corporate Finance 13,373 20 19 1

15 7 Handelsbanken Capital Markets 5,419 20 13 7

10 8 Ernst & Young 1,508 19 16 3

8 9 Arctic Securities 3,958 15 16 -1

23 10 Goldman Sachs 47,855 14 8 6

19 11 Deutsche Bank 37,389 14 9 5

18 12 JPMorgan 21,728 14 9 5

33 13 Bank of America Merrill Lynch 7,986 13 5 8

5 14 Morgan Stanley 18,329 12 20 -8

22 15 Access Partners 1,238 12 9 3

Financial Advisers to Swedish M&A: Volume

Ranking 2011 2010

Y/E 2010 Y/E 2011 Company Name Value Deal Deal Count

2 1 SEB Enskilda 7,779 19 19 0

12 2 Handelsbanken Capital Markets 4,722 12 8 4

6 3 Carnegie Investment Bank 4,025 12 12 0

8 4 Nordea Corporate Finance 4,120 11 11 0

3 5 KPMG 1,222 11 17 -6

10 6 Ernst & Young 568 11 10 1

11 7 ABG Sundal Collier 1,621 10 9 1

1 8 PwC 673 10 22 -12

17 9 Deutsche Bank 27,706 9 5 4

5 10 Morgan Stanley 12,621 9 12 -3

24 11 JPMorgan 12,456 9 3 6

22 12 Goldman Sachs 32,258 8 3 5

7 13 Lazard 6,492 7 11 -4

16 14 Access Partners 1,198 7 6 1

43 15 HDR Partners 186 7 2 5

Financial Advisers to Swedish M&A: ValueRanking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

10 1 Goldman Sachs 32,258 8 2,367 1,262.8%

27 2 Deutsche Bank 27,706 9 822 3,270.6%

37 3 Nomura Holdings 17,091 3 308 5,449.0%

22 4 Credit Suisse 15,708 3 1,071 1,366.7%

1 5 Morgan Stanley 12,621 9 7,219 74.8%

15 6 JPMorgan 12,456 9 1,800 592.0%

2 7 SEB Enskilda 7,779 19 5,719 36.0%

- 8 Evercore Partners 7,024 3 - -

53 9 Royal Bank of Scotland Group 6,847 4 96 7,032.3%

3 10 Lazard 6,492 7 4,018 61.6%

26 11 Barclays Capital 6,164 5 865 612.6%

21 12 UBS Investment Bank 4,835 6 1,111 335.2%

25 13 Handelsbanken Capital Markets 4,722 12 866 445.3%

- 14 Mizuho Financial Group 4,500 2 - -

16 15 Bank of America Merrill Lynch 4,474 4 1,641 172.6%

Press Release: mergermarket M&A Round-up for Year End 2011 www.mergermarket.com 26 www.mergermarket.com 26

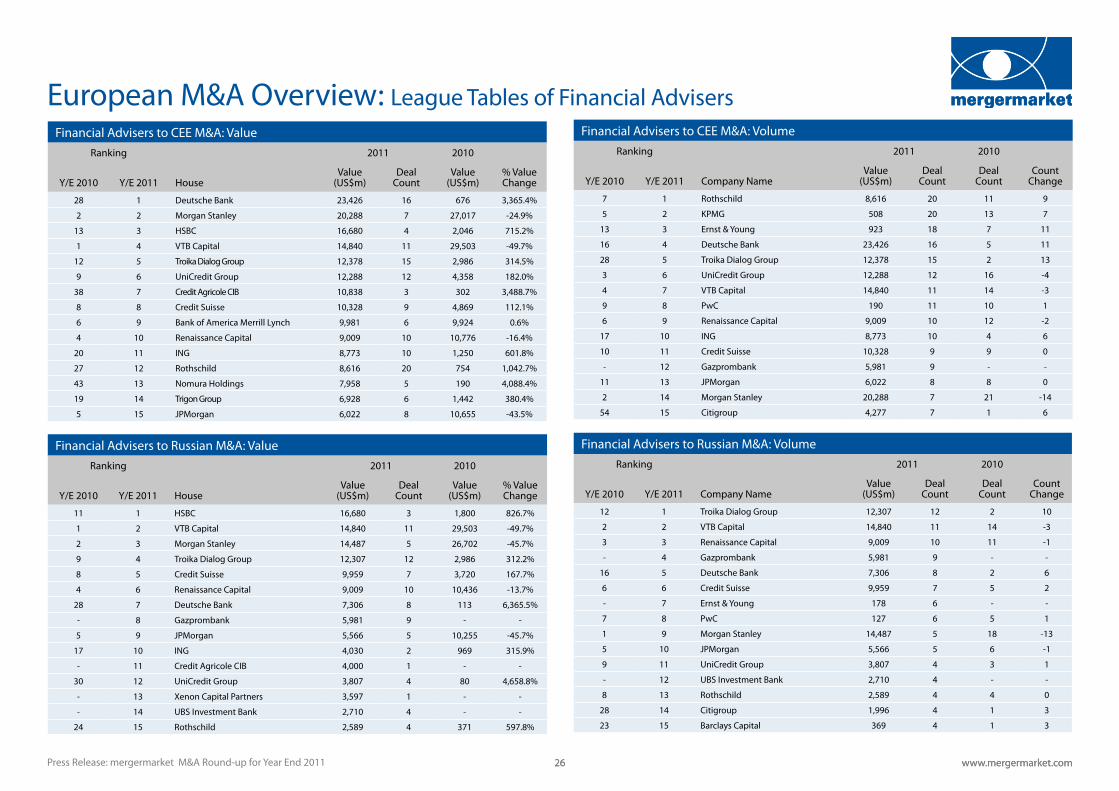

European M&A Overview: League Tables of Financial AdvisersFinancial Advisers to CEE M&A: Volume

Ranking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

7 1 Rothschild 8,616 20 11 9

5 2 KPMG 508 20 13 7

13 3 Ernst & Young 923 18 7 11

16 4 Deutsche Bank 23,426 16 5 11

28 5 Troika Dialog Group 12,378 15 2 13

3 6 UniCredit Group 12,288 12 16 -4

4 7 VTB Capital 14,840 11 14 -3

9 8 PwC 190 11 10 1

6 9 Renaissance Capital 9,009 10 12 -2

17 10 ING 8,773 10 4 6

10 11 Credit Suisse 10,328 9 9 0

- 12 Gazprombank 5,981 9 - -

11 13 JPMorgan 6,022 8 8 0

2 14 Morgan Stanley 20,288 7 21 -14

54 15 Citigroup 4,277 7 1 6

Financial Advisers to Russian M&A: VolumeRanking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

12 1 Troika Dialog Group 12,307 12 2 10

2 2 VTB Capital 14,840 11 14 -3

3 3 Renaissance Capital 9,009 10 11 -1

- 4 Gazprombank 5,981 9 - -

16 5 Deutsche Bank 7,306 8 2 6

6 6 Credit Suisse 9,959 7 5 2

- 7 Ernst & Young 178 6 - -

7 8 PwC 127 6 5 1

1 9 Morgan Stanley 14,487 5 18 -13

5 10 JPMorgan 5,566 5 6 -1

9 11 UniCredit Group 3,807 4 3 1

- 12 UBS Investment Bank 2,710 4 - -

8 13 Rothschild 2,589 4 4 0

28 14 Citigroup 1,996 4 1 3

23 15 Barclays Capital 369 4 1 3

Financial Advisers to CEE M&A: ValueRanking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

28 1 Deutsche Bank 23,426 16 676 3,365.4%

2 2 Morgan Stanley 20,288 7 27,017 -24.9%

13 3 HSBC 16,680 4 2,046 715.2%

1 4 VTB Capital 14,840 11 29,503 -49.7%

12 5 Troika Dialog Group 12,378 15 2,986 314.5%

9 6 UniCredit Group 12,288 12 4,358 182.0%

38 7 Credit Agricole CIB 10,838 3 302 3,488.7%

8 8 Credit Suisse 10,328 9 4,869 112.1%

6 9 Bank of America Merrill Lynch 9,981 6 9,924 0.6%

4 10 Renaissance Capital 9,009 10 10,776 -16.4%

20 11 ING 8,773 10 1,250 601.8%

27 12 Rothschild 8,616 20 754 1,042.7%

43 13 Nomura Holdings 7,958 5 190 4,088.4%

19 14 Trigon Group 6,928 6 1,442 380.4%

5 15 JPMorgan 6,022 8 10,655 -43.5%

Financial Advisers to Russian M&A: ValueRanking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

11 1 HSBC 16,680 3 1,800 826.7%

1 2 VTB Capital 14,840 11 29,503 -49.7%

2 3 Morgan Stanley 14,487 5 26,702 -45.7%

9 4 Troika Dialog Group 12,307 12 2,986 312.2%

8 5 Credit Suisse 9,959 7 3,720 167.7%

4 6 Renaissance Capital 9,009 10 10,436 -13.7%

28 7 Deutsche Bank 7,306 8 113 6,365.5%

- 8 Gazprombank 5,981 9 - -

5 9 JPMorgan 5,566 5 10,255 -45.7%

17 10 ING 4,030 2 969 315.9%

- 11 Credit Agricole CIB 4,000 1 - -

30 12 UniCredit Group 3,807 4 80 4,658.8%

- 13 Xenon Capital Partners 3,597 1 - -

- 14 UBS Investment Bank 2,710 4 - -

24 15 Rothschild 2,589 4 371 597.8%

Press Release: www.mergermarket.com 27Press Release: www.mergermarket.com 27mergermarket M&A Round-up for Year End 2011

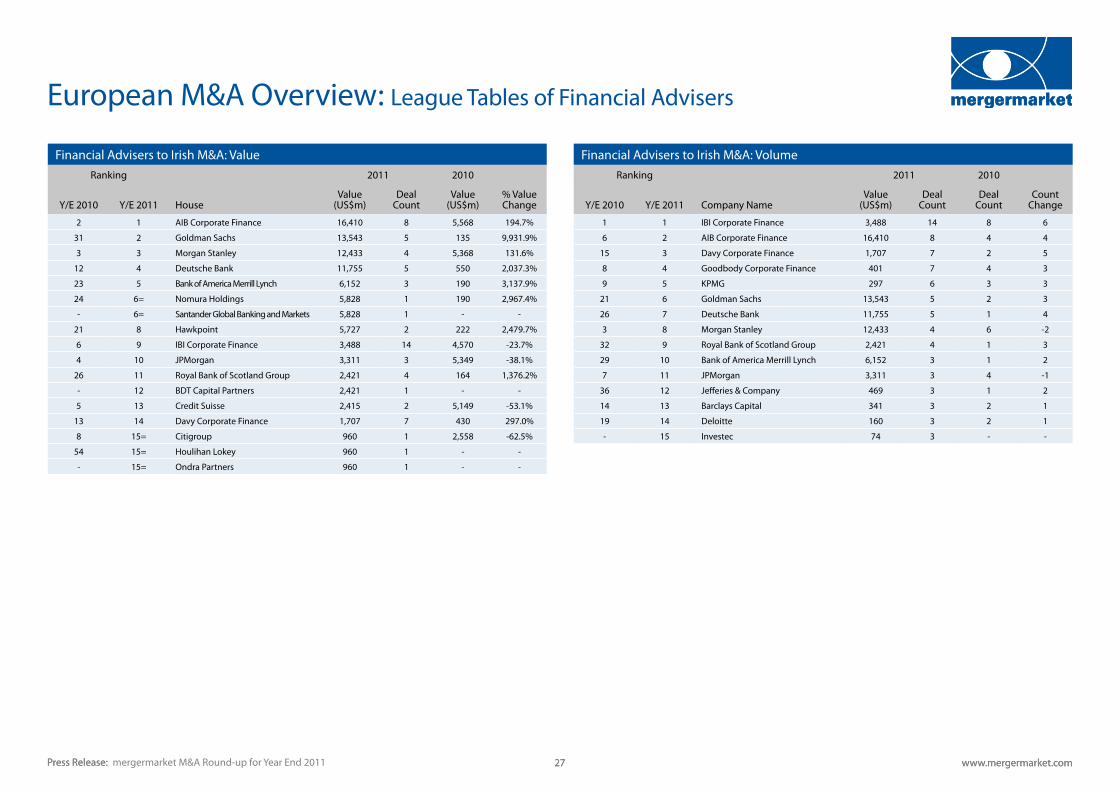

European M&A Overview: League Tables of Financial Advisers

Financial Advisers to Irish M&A: ValueRanking 2011 2010

Y/E 2010 Y/E 2011 HouseValue

(US$m)Deal

CountValue

(US$m)% Value Change

2 1 AIB Corporate Finance 16,410 8 5,568 194.7%

31 2 Goldman Sachs 13,543 5 135 9,931.9%

3 3 Morgan Stanley 12,433 4 5,368 131.6%

12 4 Deutsche Bank 11,755 5 550 2,037.3%

23 5 Bank of America Merrill Lynch 6,152 3 190 3,137.9%

24 6= Nomura Holdings 5,828 1 190 2,967.4%

- 6= Santander Global Banking and Markets 5,828 1 - -

21 8 Hawkpoint 5,727 2 222 2,479.7%

6 9 IBI Corporate Finance 3,488 14 4,570 -23.7%

4 10 JPMorgan 3,311 3 5,349 -38.1%

26 11 Royal Bank of Scotland Group 2,421 4 164 1,376.2%

- 12 BDT Capital Partners 2,421 1 - -

5 13 Credit Suisse 2,415 2 5,149 -53.1%

13 14 Davy Corporate Finance 1,707 7 430 297.0%

8 15= Citigroup 960 1 2,558 -62.5%

54 15= Houlihan Lokey 960 1 - -

- 15= Ondra Partners 960 1 - -

Financial Advisers to Irish M&A: VolumeRanking 2011 2010

Y/E 2010 Y/E 2011 Company NameValue

(US$m)Deal

CountDeal

Count Count

Change

1 1 IBI Corporate Finance 3,488 14 8 6

6 2 AIB Corporate Finance 16,410 8 4 4

15 3 Davy Corporate Finance 1,707 7 2 5

8 4 Goodbody Corporate Finance 401 7 4 3

9 5 KPMG 297 6 3 3

21 6 Goldman Sachs 13,543 5 2 3

26 7 Deutsche Bank 11,755 5 1 4

3 8 Morgan Stanley 12,433 4 6 -2

32 9 Royal Bank of Scotland Group 2,421 4 1 3

29 10 Bank of America Merrill Lynch 6,152 3 1 2

7 11 JPMorgan 3,311 3 4 -1

36 12 Jefferies & Company 469 3 1 2

14 13 Barclays Capital 341 3 2 1

19 14 Deloitte 160 3 2 1

- 15 Investec 74 3 - -

Press Release: www.mergermarket.com 28Press Release: www.mergermarket.com 28mergermarket M&A Round-up for Year End 2011

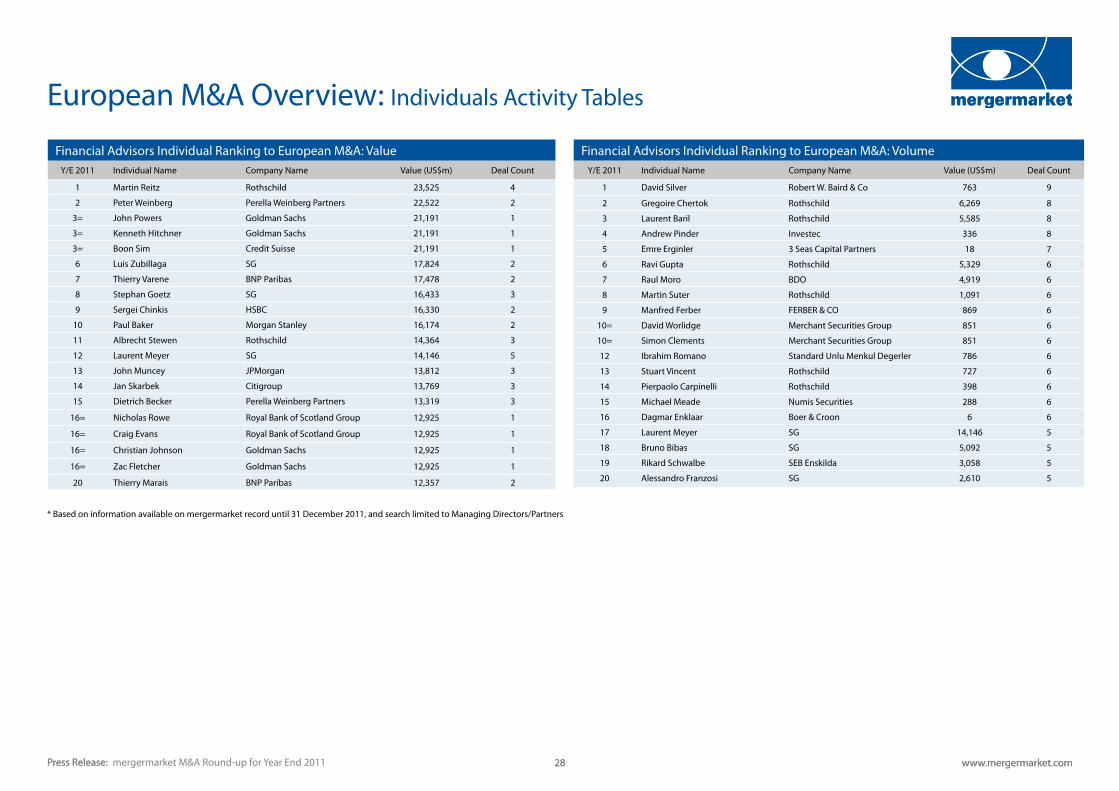

European M&A Overview: Individuals Activity Tables

Financial Advisors Individual Ranking to European M&A: ValueY/E 2011 Individual Name Company Name Value (US$m) Deal Count

1 Martin Reitz Rothschild 23,525 4

2 Peter Weinberg Perella Weinberg Partners 22,522 2

3= John Powers Goldman Sachs 21,191 1

3= Kenneth Hitchner Goldman Sachs 21,191 1

3= Boon Sim Credit Suisse 21,191 1

6 Luis Zubillaga SG 17,824 2

7 Thierry Varene BNP Paribas 17,478 2

8 Stephan Goetz SG 16,433 3

9 Sergei Chinkis HSBC 16,330 2

10 Paul Baker Morgan Stanley 16,174 2

11 Albrecht Stewen Rothschild 14,364 3

12 Laurent Meyer SG 14,146 5

13 John Muncey JPMorgan 13,812 3

14 Jan Skarbek Citigroup 13,769 3

15 Dietrich Becker Perella Weinberg Partners 13,319 3

16= Nicholas Rowe Royal Bank of Scotland Group 12,925 1

16= Craig Evans Royal Bank of Scotland Group 12,925 1

16= Christian Johnson Goldman Sachs 12,925 1

16= Zac Fletcher Goldman Sachs 12,925 1

20 Thierry Marais BNP Paribas 12,357 2

Financial Advisors Individual Ranking to European M&A: VolumeY/E 2011 Individual Name Company Name Value (US$m) Deal Count

1 David Silver Robert W. Baird & Co 763 9

2 Gregoire Chertok Rothschild 6,269 8

3 Laurent Baril Rothschild 5,585 8

4 Andrew Pinder Investec 336 8

5 Emre Erginler 3 Seas Capital Partners 18 7

6 Ravi Gupta Rothschild 5,329 6

7 Raul Moro BDO 4,919 6

8 Martin Suter Rothschild 1,091 6

9 Manfred Ferber FERBER & CO 869 6

10= David Worlidge Merchant Securities Group 851 6

10= Simon Clements Merchant Securities Group 851 6

12 Ibrahim Romano Standard Unlu Menkul Degerler 786 6

13 Stuart Vincent Rothschild 727 6

14 Pierpaolo Carpinelli Rothschild 398 6

15 Michael Meade Numis Securities 288 6

16 Dagmar Enklaar Boer & Croon 6 6

17 Laurent Meyer SG 14,146 5

18 Bruno Bibas SG 5,092 5

19 Rikard Schwalbe SEB Enskilda 3,058 5

20 Alessandro Franzosi SG 2,610 5

* Based on information available on mergermarket record until 31 December 2011, and search limited to Managing Directors/Partners

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

0

50

100

150

200

250

300

350

400

450

500

Volu

me o

f Dea

ls

Valu

e of D

eals

(US$

bn)

US M&A Activity - Quarterly

Value(US$bn)

Volume

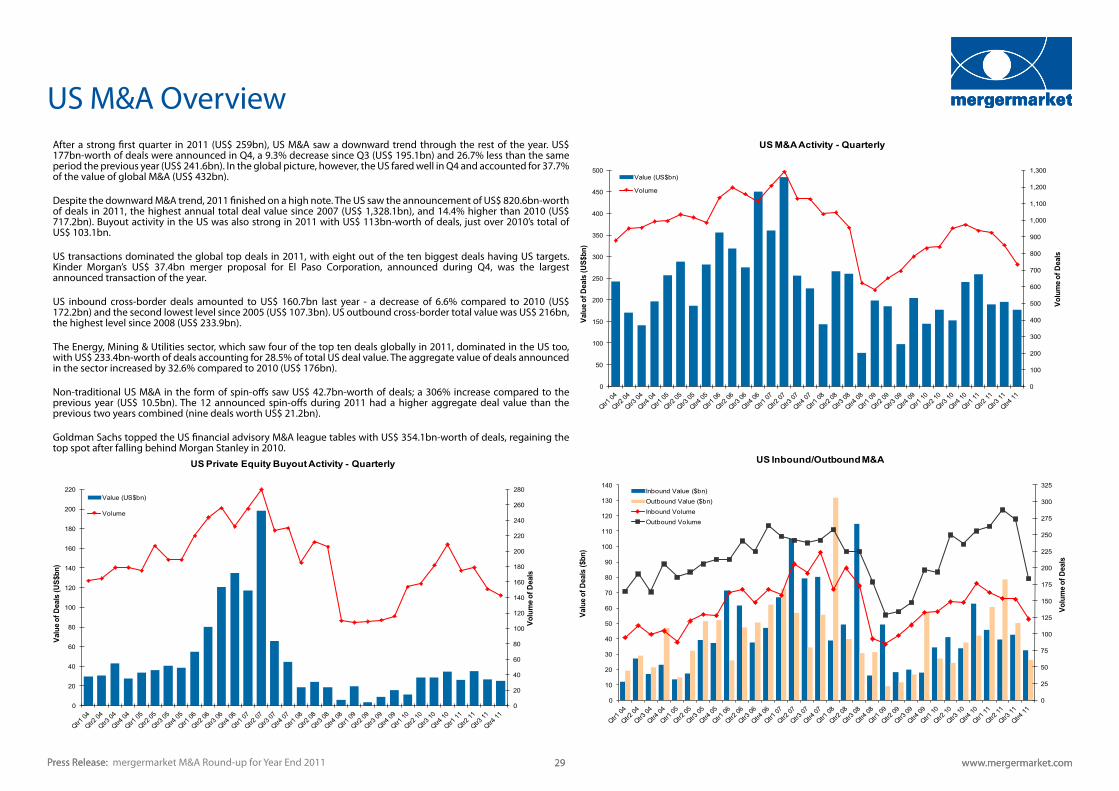

After a strong first quarter in 2011 (US$ 259bn), US M&A saw a downward trend through the rest of the year. US$ 177bn-worth of deals were announced in Q4, a 9.3% decrease since Q3 (US$ 195.1bn) and 26.7% less than the same period the previous year (US$ 241.6bn). In the global picture, however, the US fared well in Q4 and accounted for 37.7% of the value of global M&A (US$ 432bn).