Embed Size (px)

Citation preview

Prevailing Wage Rates in Minnesota

An Examination of Alternative Calculation Methods and Their Effects on Public Construction Wages

Minnesota Taxpayers Association

February 2005

Acknowledgements

We wish to thank the Minnesota Departments of Labor and Industry and Employment and Economic Development for information provided on prevailing wage rates and median wage rates that were used in the preparation of this report. Aaron Twait, MTA Research Associate, did most of the research, calculations, and initial drafting of the report. Lynn Reed, MTA Executive Director, did the final editing for publication. The research for this report was funded entirely by the Associated Builders and Contractors of Minnesota. MTA is solely responsible for the research, analysis, conclusions, and recommendations contained in this report.

About the Minnesota Taxpayers Association

The Minnesota Taxpayers Association did most of the research and analysis for this study in cooperation with other members of the NTC (see below). MTA was founded in 1926 for the purpose of disseminating factual information that will educate and inform all Minnesotans about Minnesota tax and spending policies. For over seventy-five years, the Association has advocated for the adoption of sound fiscal policies through its research efforts, publications, and meetings. The Association is a non-profit, non-partisan group supported by membership dues. For information about membership, call (651) 224-7477, or visit our web site at www.mntax.org.

Table of Contents

I. EXECUTIVE SUMMARY............................................................................................................. I Purpose and Objectives of the Study ................................................................................................ i Methodology of the Study................................................................................................................. i Analysis............................................................................................................................................ ii

Comparison of Minnesota Law to other State and Federal Prevailing Wage Statutes ..... ii Labor Cost Comparison Between Current Law and Alternatives ..................................... ii

Recommendations ........................................................................................................................... iii II. BACKGROUND AND POLICY PROBLEM ............................................................................. 1

Policy Problem—Why This Study? ................................................................................................. 4 III. METHODOLOGY......................................................................................................................... 5

Public Construction Projects ............................................................................................................ 5 Estimates of Public Construction Project Wage Costs..................................................................... 5 Sources for Prevailing Wage Data ................................................................................................... 6 Estimates of Labor Inputs ................................................................................................................ 7 Matching Job Classification Categories ........................................................................................... 7 Comparison Between State Prevailing Wage, Federal Prevailing Wage and Median Wage........... 8 Data Limitations............................................................................................................................... 8

IV. ANALYSIS AND INTERPRETATION ...................................................................................... 9 Comparison Between Current Law and Federal Prevailing Wage Determinations ......................... 9 Comparison Between Current Law and Median Wage Determinations ........................................ 13 Corroboration by Other Studies ..................................................................................................... 15

V. RECOMMENDATIONS............................................................................................................. 17

VI. APPENDIX A: PROJECTS ANALYZED IN COURSE OF STUDY.................................... 19

VII. APPENDIX B: DEED PLANNING AREAS AND MINNESOTA HIGHWAY/HEAVY PREVAILING WAGE REGIONS, BY COUNTY ................................................................... 30

VIII. APPENDIX C: BRIEF SURVEY OF OTHER STATES' PREVAILING WAGE LAWS ........................................................................................................................................................ 31

IX. APPENDIX D: EXAMPLES OF INDIVIDUAL PROJECT SAVINGS OR COST ............. 33

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

i

I. Executive Summary

Purpose and Objectives of the Study Prevailing wage laws govern much of the public construction in the United States. They require contractors constructing buildings involving the federal or Minnesota state governments to pay government-designated wage and benefit rates that are “prevailing” in the area in which the construction is occurring. The wage and benefit rates for each job classification (electrician, carpenter, roofer, et cetera) are determined independent of each other. Such laws have been in force at the federal level since 1931, and in Minnesota since 1973. Although citizens may equate “prevailing wage” with “average wage”, this is not always the case. In many cases, the government-determined prevailing wage is 30 to 40 percent higher than the wages paid to an average laborer undertaking the same work on a job which is not subject to the prevailing wage requirements. The federal law was instituted during the nation’s Great Depression primarily as a method of protecting local laborers from cheaper imported labor. Proponents of prevailing wage laws also believe it improves the quality of construction, but evaluating that claim is not the purpose of this study. This study focuses on the more narrow question of the direct fiscal impact of such laws on public construction expenditures. This study was funded by the Associated Builders and Contractors, Inc. of Minnesota, an association of mostly non-union builders and contractors and has two main parts: 1. History and overview: a synopsis of the history of prevailing wage laws, both federally

and in Minnesota, to present the arguments made for and against prevailing wage legislation, and to describe the unique features of Minnesota’s prevailing wage statutes as compared with similar state and federal legislation.

2. Analysis of labor costs under different prevailing wage scenarios: compiles a list of

state public construction projects in Minnesota subject to prevailing wage legislation, and evaluates changes in labor costs for those projects when substituting federal prevailing wage rates and government-determined median wage rates for Minnesota’s current prevailing wage rates.

Methodology of the Study A list of school, state, and state transportation construction projects approved in calendar year 2002 was compiled from the Minnesota Department of Education, the 2002 Capital Investment Bill, and the Minnesota Department of Transportation. Using data from the Minnesota Department of Labor and Industry, the federal Department of Labor and the Minnesota Department of Employment and Economic Development (DEED), we estimated each job classification’s share of the labor undertaken on projects on a county-by-county basis. MTA staff then compared labor costs given current prevailing wage rates to estimated labor costs if federal prevailing wage rates or DEED-determined median wages were substituted.

Executive Summary

ii

Analysis Comparison of Minnesota Law to other State and Federal Prevailing Wage Statutes As part of the study, Minnesota Associated Builders and Contractors surveyed states to update the national Associated Builders and Contractors’ 1995 prevailing wage study. This information indicated that 32 states and the federal government currently have prevailing wage laws, although nine other states have had prevailing wage laws in the past which have been repealed. Prevailing wage determinations in the 32 states are made in one of four ways:

1. by adopting the federal prevailing wage determinations, 2. by empowering a state official or officials to determine the rates, 3. by adopting collectively bargained rates, 4. by surveying to set prevailing wage rates (the method used by the federal

government). Minnesota employs the fourth option using survey information to derive the prevailing wage. However, Minnesota (and California) law does differ from the Davis-Bacon Act, and from most other state prevailing wage laws which average survey data, in one major respect. Most states and the federal government use two approaches to calculate the prevailing wage. If more than half of the workers in a survey are paid the same wage, then that wage is used. If no majority emerges, then an average is used. Minnesota and California, however, are unique in using a modal calculation: whatever rate is most frequently reported in a survey is the rate designated as “prevailing”. Given a class of workers with five survey responses of hourly wages of $7.00, $9.00, $12.00, $12.00 and $13.00, Minnesota would set the prevailing wage at $12.00 (the mode—that most frequently reported); while many other states and the federal government would set the prevailing wage at $10.60 (the average of the five salaries, since a majority did not emerge). The use of the modal method for determining prevailing wage increases the likelihood that large-scale collectively-bargained wage rates become the prevailing wage, since these rates tend to be uniform within a specific job class.

Labor Cost Comparison Between Current Law and Alternatives This study incorporated 34 school district construction projects (excluding land purchases), 57 state building projects and 247 state transportation projects, with total project costs of over $1.7 billion. From an analysis of the labor costs associated with the different alternatives, we found that:

o In 26 of the 32 counties which state building projects were located, federal prevailing wage rates were set entirely from union rates

o In 17 of the 82 counties in which state transportation projects were located, federal prevailing wage rates were set entirely from union rates

o Minnesota would have experienced estimated additional costs of $3.1 to $8.7 million, or 0.2% to 0.5% of total project cost, if the state substituted the federal rates for current state prevailing wage rates

o In 64 of the 82 counties in which state transportation projects were located, federal prevailing wage rates were 5 years old or older, likely depressing the estimated costs of substituting the federal prevailing wage rates

o Minnesota would have experienced estimated savings of $126 to $171 million, or 7.4% to 10.0% of total project costs in 2002 if the state had

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

iii

substituted the Department of Employment and Economic Development median wage rates for current state prevailing wage rates (assuming benefits at 22% of the reported median wages)

Recommendations Minnesota’s modal method of determining prevailing wages for public construction projects is used only in one other state, California. It results in wage rates significantly higher than those reported by DEED in its median wage survey. Using the federal method for calculating prevailing wage rates would add even more cost to public construction projects, apparently because of the limited number of federal projects and limited federal survey data in Minnesota. The term “prevailing wage” itself connotes a wage that is typical of an area, and is most likely commonly understood as an average wage by the general public. However, its application in Minnesota results in prevailing wage rates that are not reflective of typical wage rates. The primary purpose of “Little Davis-Bacon” laws is to protect local workers from cheap, imported labor, and as long as the wage rates that are used are truly “prevailing” (that is, typical of an area), that purpose does not seem to be threatened regardless of the methodology used to calculate those rates. The claim by proponents of the current method of calculating Minnesota’s prevailing wage rates that buildings are constructed more quickly and with better quality cannot be evaluated in a study like this of such limited scope. However, our underlying assumption is that contract specifications, penalty provisions for delays, and aggressive construction management can provide at the very least an equally effective alternative method for addressing timing and quality issues for public construction projects. In view of these observations, MTA recommends: • that the widely used DEED survey for median wages be used as an alternative definition

of prevailing wage for public construction projects in Minnesota; • that DEED develop a survey comparable to the median wage survey for employee

benefits to be used for the benefits portion of the prevailing wage rates as an alternative to the currently determined prevailing benefit rates;

• this alternate method of determining prevailing wage rates be tested in specific locations and compared to comparable public construction projects in the state in order to compare the costs of such projects directly with one another, at the earliest possible time.

Such a comparison would allow there to be an empirical test of the claims of both proponents and opponents of Minnesota’s current prevailing wage law. Should the test demonstrate that using the median wage rates calculated by Minnesota’s DEED results in lowered costs for public construction projects, those median wage rates (along with DEED’s surveyed benefits rates) should replace Minnesota’s current method of determining prevailing wage rates.

Executive Summary

iv

This Page Intentionally Blank

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

1

II. Background and Policy Problem

History of Prevailing Wage Laws The first law in the United States regulating minimum pay standards for construction workers was passed by the Kansas legislature in 1891. The debate began at the federal level after that, and successful action was instigated after an Alabama construction firm brought construction laborers from that state to work on a Long Island hospital building project in 1927. The wages paid to these workers were those prevalent in their home state of Alabama, rather than the higher wages typically paid to New York construction workers. Fearful that they would continue to be undercut, New York businessmen complained about the practice to Congress. By 1931, Congress has passed the Davis-Bacon bill (so-named for its sponsors, Republican Representative Robert Bacon of New York and Republican Senator James Davis of Pennsylvania), which prohibited contractors engaged on federal construction projects from importing “cheap labor” to cut costs. The bill was later modified in 1935 to “require the payment of not less than the wages found by the Secretary of Labor to be ‘prevailing for the corresponding classes of laborers and mechanics employed on projects of a character similar to the contract work in the city, town, village or other civil subdivision of the state in which the work is be to performed.”1 A similar scenario took place on a University of Minnesota farm project in the early 1970s, when out-of-state workers were hired for less than local workers. In 1973, Minnesota’s legislature enacted a state prevailing wage law (often referred to, along with other state prevailing wage laws, as the “little Bacon-Davis law), which Governor Wendell Anderson signed. Like its federal counterpart, the Minnesota law requires persons employed on construction projects which are entirely or partially funded with state monies to be paid the “prevailing wage”. Currently, 32 states have prevailing wage statutes. Of the other 18, 9 have never had prevailing wage laws, while the other 9 have repealed earlier “little Davis-Bacon” laws.

Literature Review A significant amount of literature has been published on the effects of the prevailing wage laws. Unions, their members, union contractors, liberal academics and liberal policy groups tend to support prevailing wage. Non-union contractors, public executive officials, conservative academics and conservative policy groups tend to oppose prevailing wage. Although many studies have been published on the effects of prevailing wage laws, most of them have been conducted and/or funded by these groups. Few of them have been conducted by government entities. Notable exceptions are the Kentucky Legislative Research Commission’s (LRC) Analysis of Kentucky’s Prevailing Wage Laws and Procedures, the Ohio Legislative Service Commission’s (LSC) Effects of the Exemption of School Construction Projects from Ohio’s Prevailing Wage Law, and various reports published by the federal Government Accounting Office (GAO). Not surprisingly, there is a wide disparity of findings. Proponents of prevailing wage make the following arguments:

• Prevailing wage laws prevent contractors from hiring non-local workers at lower wages, thus preserving the jobs and wages of local construction workers.

1 A Guide to Minnesota’s Prevailing Wage. Minnesota Department of Labor and Industry

Background and Policy Problem

2

As noted earlier, this was the original justification used for passage of the Davis-Bacon Act in 1931.

• Prevailing wage laws reduce, rather than increase, building costs over the life of the building. Supporters assert that wages correlate with skill level, and so paying the higher prevailing wage draws more highly skilled workers to a construction project than would work there with a lower wage. Prevailing wage proponents cite three separate savings associated with skilled workers:

1. They argue that skilled workers provide increased job productivity. With greater skills, construction workers can work more quickly. Contractors also have an incentive to substitute mechanical labor for human laborers in an effort to cut costs. Although the per hour construction wage rates may be greater with prevailing wage, the total cost is lower because laborers work significantly less hours, resulting in savings to the taxpayer.

2. Proponents contend that more highly skilled workers are less likely to cause accidents. Accidents are costly because they extend the time needed to complete a project, adding extra wage hours to the project’s overall cost. Moreover, in the case of serious accidents, employers must contribute to the injured laborer’s health care costs, are liable for sick pay, and must compensate for the loss of the laborer on the project either by increasing existing worker productivity or by hiring a replacement. Since skilled workers are already assumed to be working at a high level of productivity, there will be few gains to be made and the contractor must either hire a replacement or extend the life of the project.

3. Proponents maintain that more highly skilled workers produce a higher-quality product. Fewer materials and man-hours are wasted with higher quality work, reducing construction costs. In addition, proponents assert that, with higher quality buildings, there will be fewer maintenance and repair costs associated with the building over its useful life. Hence, although construction costs are higher, savings are reaped over the life of the building.

• Prevailing wage laws support training and education of construction workers. Certain studies indicate that “where prevailing wages are paid, training programs are more prevalent, including higher participation by minorities and disadvantaged workers”.2 Proponents argue that these programs not only enable minorities and the disadvantaged to become construction workers, but that they also increase the skill level of all workers that take part in the programs, leading to a higher overall skill level.

• Prevailing wage laws increase local tax bases. Proponents contend that, by enforcing the prevailing wage, lower-skilled workers with lower wages do not drive out more highly-skilled workers with their higher wages. If lower-skilled workers did drive higher-skilled workers out of the locality, the income base would be eroded, leading to lower income tax collections.

Opponents of the current prevailing wage laws make their own, sometimes competing claims: • Prevailing wage laws add unnecessary expenses to construction projects.

Various studies indicate that the prevailing wage is higher that that necessary to complete the project.

• Prevailing wage laws make unions too powerful in setting prevailing wage rates. As Kentucky’s Legislative Research Commission (LRC) study notes: “the

2 State Building and Construction Trades Council of California, http://sbctc.org/?id=895&pagetype=sitemap

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

3

determination process used…is more likely to yield prevailing wages that are representative of union wages than wages for all construction workers in the locality. While union workers account for approximately 21% of non-residential construction workers, 81% of the workers for which wages were submitted at prevailing wage hearings were union members. Sixty-four percent of the determinations made resulted in the prevailing wage being set equal to the union wage.”

The Kentucky LRC’s study provides a good summary for the reasons behind the wide divergence of study results:

Empirical estimates of the effects vary greatly, due largely to the difficulty in separating the effects of prevailing wage laws from other factors that affect construction costs. Ideally, to measure any cost effect from prevailing wage laws, it is necessary to compare the costs of projects under the prevailing wage to the costs of the same exact projects in the absence of a prevailing wage law. Unfortunately, it is not possible to see what construction costs would be in the total absence of a prevailing wage law. Therefore, several alternative methods have been developed over the years in an attempt to estimate the effects. Some studies compare construction costs in prevailing wage states to construction costs in non-prevailing wage states. Other compare the Davis-Bacon wages to other, more representative measures of wages. These methods are discussed in a number of studies. There is little agreement between the studies as to whether prevailing wage laws increase costs, because a commonality in all of them is that there is always some technical issue that could substantially affect the results.3

Prevailing Wage Determination Methods Minnesota’s prevailing wage law is, in most respects, similar to the federal Davis-Bacon legislation and many other state prevailing wage laws. The Department of Labor and Industry defines classes of labor and determines prevailing wage rates for two different types of construction: highway/heavy and commercial. Labor and Industry sets these rates through an annual survey of entities involved in the construction industry, mainly businesses and unions. Labor and Industry defines highway/heavy construction as “construction and maintenance of highways, streets, airport runways, bridges, power plants, dams, wastewater treatment plants, water towers, high-voltage power lines and utilities”.4 While it does not determine prevailing wage rates, Minnesota’s Department of Transportation is responsible for enforcing wage rates on highway construction projects. State highway/heavy prevailing wage rates are determined for ten regions, into which each of Minnesota’s counties then fall. Labor and Industry defines commercial construction as “building projects exclusive of residential [single- or two-family home] construction”.5 State commercial construction prevailing wage rates are set on a county-by-county basis.

Prevailing wage determinations in the 32 states are made in one of four ways:

1. by adopting the federal prevailing wage determinations, 2. by empowering a state official or officials to determine the rates, 3. by adopting collectively bargained rates,

3 Kentucky LRC Report, pp. 45-46. 4 Minnesota Department of Labor and Industry website: http://www.doli.state.mn.us/laborlaw 5 Ibid.

Background and Policy Problem

4

4. by surveying to set prevailing wage rates (the method used by the federal government).6

Minnesota employs the fourth option using survey information to derive the prevailing wage. However, Minnesota law does differ from the Davis-Bacon Act, and from most other state prevailing wage laws which average survey data, in one major respect. Most states and the federal government use two approaches to calculate the prevailing wage. If more than half of the workers in a survey are paid the same wage, then that wage is used. If no majority emerges, then an average is used. Minnesota calculates the prevailing wage differently. An administrative law judge has concluded that the Minnesota law requires the mode, or most-often-cited wage, to become the prevailing wage, regardless of whether or not that wage is paid to a majority of workers in the survey. For example, if a class of workers had five survey responses, with those persons being paid wages of $9.17, $10.40, $13.55, $13.55 and $14.06, then the state of Minnesota would set the prevailing wage at $13.55 (the mode); while the federal government would set the prevailing wage at $12.15 (the average of the five salaries, since a majority did not emerge).7 The State of California effectively uses the same prevailing wage determination method as Minnesota.8

Policy Problem—Why This Study? This study is primarily a comparison of the wage costs of public construction projects subject to prevailing wage laws under current Minnesota law, and our estimates of what those costs would be if either federal prevailing wage law were in effect, or if the prevailing wage statutes set wages equal to the median wages as determined by the Minnesota Department of Employment and Economic Development (DEED). The Associated Builders and Contractors, Inc. (ABC) of Minnesota requested that MTA do the research for this study. We agreed to estimate the narrow question of what differences in cost arise by using Minnesota’s method of calculating prevailing wage rates rather than using the federal method, or using DEED’s median wage rates.

6 This information was provided by Minnesota Associated Builders and Contractors, who provided us with their national association’s 1995 prevailing wage study. They also surveyed states to determine what changes had taken place since then. The relevant information which they provided is attached at the end of this report as Appendix C. 7 House Research, Minnesota House of Representatives, http://www.house.leg.state.mn.us/hrd/issinfo/prevwage.htm. 8 California Department of Industrial Relations, http://workitout.ca.gov/viewfaq.asp?id=143&fid=216.

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

5

III. Methodology

Public Construction Projects A list of public construction projects subject to prevailing wage rates was obtained from several state agencies. The Department of Education collects data from all school districts regarding building projects. Education posts this data on its website as part of the Review and Comment process, and we collected our school construction data from that website. Unfortunately, this data only includes the aggregate amount bonded for each project. State highway construction projects are let at auction, and the bidding results are posted on the Department of Transportation’s website. State building projects are not processed or compiled centrally, and so to facilitate the study, we used those projects funded through capital investment (“bonding”) bills as our list of state-funded building projects. Given that the legislature failed to enact a bonding bill during the 2004 session, we used the 2002 bonding bill to determine state-funded building projects, as well as 2002 school and transportation projects. Based on discussions with experts in local finance, we excluded any potential city, county and township projects as inordinately difficult to compile. Our complete list of projects follows this report as Appendix A. Importantly, only Minnesota counties with public construction projects have been included in this analysis. Five counties; Brown, Jackson, McLeod, Murray and Watonwan, had no public building or transportation projects included in our list of 2002 list, projects so have been excluded entirely from this analysis. Another 50 counties had transportation, but no building projects. Those counties are included in our analysis of transportation prevailing wage, but not building prevailing wage.

Estimates of Public Construction Project Wage Costs The available public construction data available presented aggregate building project costs. Since only wage payments are subject to prevailing wage statutes, we set about to determine what portion of total public construction costs are wage costs. In order to do this, we used the following formulas Prevailing wage (PW) costs = raw construction costs (RCC) X percent of RCC subject to PW RCC = bond costs – non-construction costs – profit fees not subject to prevailing wage Determining raw construction costs (RCC) was not difficult for transportation projects, since those bidding results were actual project, rather than bonding costs. To determine raw construction costs for state-funded building projects, we compared construction costs versus total costs for all proposed 2002 state building projects, which were available through each agency’s capital budget request through the Department of Finance. Our analysis indicated that the raw construction costs ranged from 71 to 77 percent of total costs. Since this data was not readily available to us for bonding projects, we consulted construction and architectural professionals, who indicated that on a typical bond issue, 65 to 70 percent of the bond pertains to construction costs. Of that, 10 to 12 percent is profit, project management fees that are not subject to prevailing wage. That leaves 53 to 60 percent of “raw construction costs”.

Methodology

6

Since this data was not readily available to us for state transportation and school building projects, we again consulted construction and architectural professionals. They indicated that 40 to 55 percent is typically construction labor costs subject to prevailing wage. From this data, we estimated that the total public construction project costs subject to prevailing wage fall into the following ranges:

Table 1: Percentage of Total Public Construction Project Costs Subject to Prevailing Wage Schools State – Building State - Transportation

Cost Category Low Wage High Wage Low Wage High Wage Low Wage High Wage

Construction-related bonding costs: 65% 70% N.A. N.A. 100% 100%

Minus project management bonding costs - 12% - 10% N.A. N.A. - 12% - 10%

= Raw construction bonding costs 53% 60% 71% 77% 88% 90%Times percent of raw construction costs subject to prevailing wage x 40% x 50% x 40% x 50% x 40% x 50%

= Estimated Cost Subject to Prevailing Wage 21.2% 33.3% 28.4% 38.5% 35.2% 45.0%Sources: Department of Finance agency capital budget requests, informal MTA surveys of architectural and construction professionals. N.A. indicates percentages are not available.

Finally, we assigned each project into the county in which it was located. Certain transportation projects were assigned to multiple counties throughout a region. In those cases, the project was divided equally among relevant counties. Certain state building projects were also designated “systemwide” or “statewide”. University of Minnesota statewide projects were divided by enrollment at each of the four campuses (Twin Cities, Duluth, Crookston and Morris). The portion of projects assigned to the Twin Cities Campus were then equally divided between Hennepin County (Minneapolis Campus), and Ramsey County (St. Paul Campus). Other “systemwide” or “statewide” building projects were not assigned to a particular county, but instead were analyzed in a separate “statewide” category.

Sources for Prevailing Wage Data We also determined median wage rates, state prevailing wage rates and federal prevailing wage rates for each county in Minnesota. Minnesota’s Department of Employment and Economic Development (DEED) surveys Minnesota businesses quarterly to provide Occupational Employment Statistics (OES) wage data. We used third quarter 2004 data for “Construction and Extraction Occupations” as the median wage9. State prevailing wage rates are provided by the Minnesota Department of Labor and Industry (DOLI), and were current as of November, 2004.10 The Wage and Hour Division of the U.S. Department of Labor determines prevailing wage rates to be paid on federally funded or assisted construction projects, and that data was also current as of November, 2004.11 None of these agencies provides archived data through their websites. Separate surveys are conducted for construction projects (buildings) and for transportation projects (roads). One major difference between the prevailing wage data and median wage data is that prevailing wage data includes hourly benefit rates, while median wage data does not. We undertook a cursory survey of benefit packages in the construction industry, and concluded

9 DEED provides this information at http://www.deed.state.mn.us/lmi/tools/oes.htm. 10 DOLI provides this information at http://www.doli.state.mn.us/pw_rates.html. 11 The U.S. Department of Labor provides this information at http://www.access.gpo.gov/davisbacon/.

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

7

that industry-wide, companies provide benefits 22% beyond salary. We adjusted our median wage data to reflect this finding.

Estimates of Labor Inputs Wage differentials between median wage, state prevailing wage and federal prevailing wage vary according to job classification (carpenter, electrician, et cetera). In order to adequately assess the costs associated with each wage determination method, we next estimated the portion of total work completed on a public construction project by each job classification. This allows us to correctly weight the wage differentials. Since the project data did not readily indicate how much of the work on each project, we used the share of total state employment in the construction industry as reported in the OES wage data as a proxy. DEED personnel confirmed our assumption as reasonable. We excluded “first-line supervisors/managers of construction trades and extraction workers (47-1011) and “construction and building inspectors” (47-4011) after determining that the prevailing wage statutes do not apply to persons employed in those categories. We also excluded any classification number 47-5000 and above, since those categories apply to extraction, rather than construction workers. We collected OES wage and employment data by planning area, and applied the data to each county within the planning area. A list of planning areas and their constituent counties follows this report as Appendix B.

Matching Job Classification Categories Using OES employment data as the basis for classification, we then matched the state and federal prevailing wage classes to it. While these three measurement methods share many job classifications, others differed from method to method. In particular, three assumptions deserve to be highlighted. First, the median wage job classifications “paving, surfacing, and tamping equipment operators” (47-2071) and “operating engineers and other construction equipment operators” (47-2073) do not have equivalent prevailing wage counterparts. Both state and federal prevailing wage statements list “power equipment operators” and “truck drivers”, both of which are usually divided into multiple groups. At both the state and federal levels, we averaged wage listings for all groups within “power equipment operators” and “truck drivers” and matched the result to the two above-mentioned median wage job classifications. Second, median wage calculations include various “helper” categories. Private industry classifies such “helpers” as apprentices or juniors in their particular fields, and as such, pays a significantly smaller wage. However, these “helper” classifications are generally not recognized by prevailing wage as apprentices, and so the statutes require that they be paid at the full journeyman rate. Therefore, although we have carried the “helper” job classifications into prevailing wage (where they do not exist), we have applied the journeyman wage rate to them. This allows us to measure costs associated with prevailing wage’s apprentice requirements. Lastly, certain job classifications were not represented in every wage determination method. When comparing two methods of wage determination, we applied the total differential between job classifications that did match to those that did not. For example, if the federal prevailing wage costs exceeded the state prevailing wage costs by two percent for all job

Methodology

8

classifications that did match, then we applied that two percent increase to all remaining job classifications.

Comparison Between State Prevailing Wage, Federal Prevailing Wage and Median Wage Once these methodological hurdles were overcome, we began converting between wage determination methods. The wage cost for each project was divided into the wages paid to each job classification. We then divided total job classification wages by the state prevailing wage rate to estimate the total number of hours worked by persons employed in each job classification on the project. To determine the project wage costs under federal prevailing wage and median wage, we then multiplied hours worked in each job classification by the appropriate federal prevailing wage rate or median wage rate. By using a low and high wage estimates, we arrived at a range within which total wages paid will fall.

Data Limitations Our data on public construction projects is limited substantially in three respects:

• We were unable to obtain a comprehensive list of public construction projects for political subdivisions in the state, excepting school districts. No centralized database of such projects is known to exist.

• We were able to determine labor costs only for state building projects. No such detail was available for school district or highway construction projects.

• None of the public construction project information available contained detailed information on either the amount of work performed by laborers in each job classification, or the amount of wages paid to laborers in each job classification. Although our assumptions regarding the labor mix were confirmed by DEED personnel as reasonable, further information could alter our labor mix assumptions substantially. Given the number of variables involved, a sensitivity analysis is not feasible.

Our prevailing wage data also suffers from the following limitations: • Job classification categories differ slightly in some regards between the different wage

determination methodologies. Importantly, our method of averaging the reported wages for all subcategories within the prevailing wage job categories of “power equipment operator” and “truck driver” creates some concern. Again, our lack of knowledge concerning the actual labor mix is the key factor here: if we knew how to accurately weight each of the subcategories within these groups, our prevailing wage estimates for them would almost certainly change. Since, however, the wages for most of these subcategories are within a fairly narrow range, it is unlikely that any changes would significantly impact our findings.

• We have not been able to examine the actual surveys upon which the state and federal prevailing wage determinations are based. This leads to a number of limitations:

o We must use the time frames provided by these agencies. This is problematic since much of the federal highway construction prevailing wage data is generally two to four years older than comparable state data. More current data would almost certainly raise the costs of transportation projects under the federal prevailing wage model.

o We do not know how many surveys were submitted to the relevant authority for any of the prevailing wage determinations. Hence, we do not have the ability to accurately ascertain the veracity of the prevailing wage determinations provided by either the state or federal government.

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

9

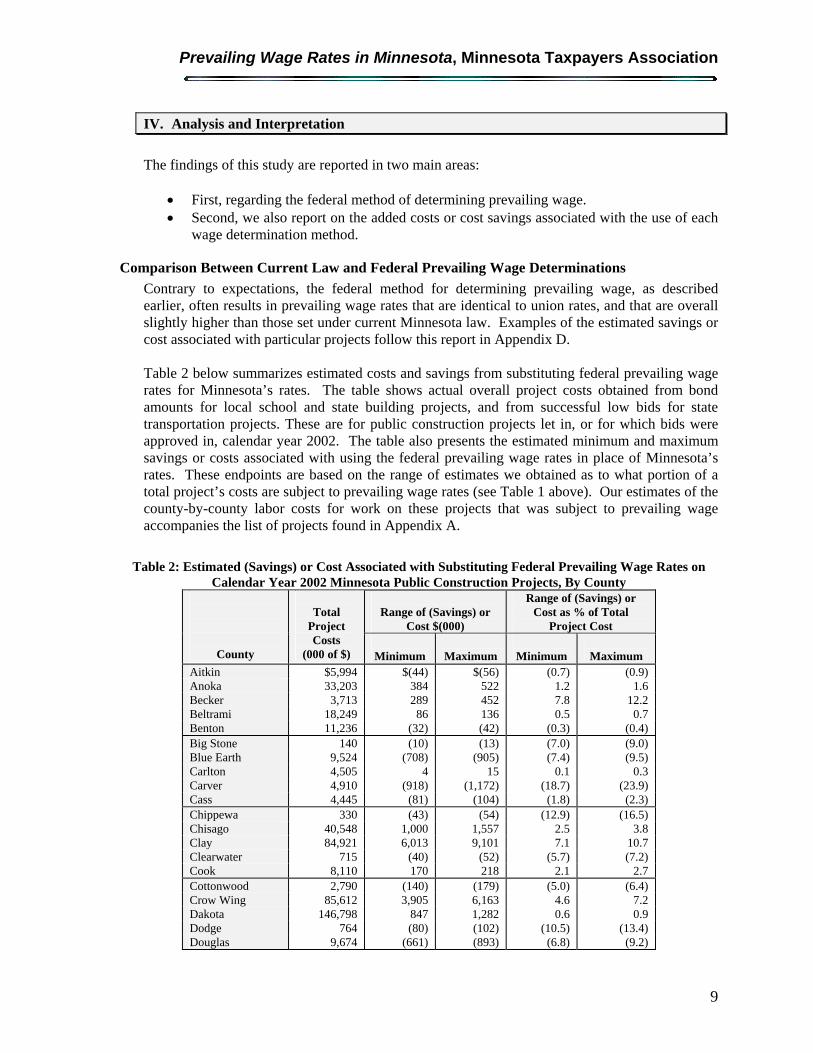

IV. Analysis and Interpretation

The findings of this study are reported in two main areas:

• First, regarding the federal method of determining prevailing wage. • Second, we also report on the added costs or cost savings associated with the use of each

wage determination method.

Comparison Between Current Law and Federal Prevailing Wage Determinations Contrary to expectations, the federal method for determining prevailing wage, as described earlier, often results in prevailing wage rates that are identical to union rates, and that are overall slightly higher than those set under current Minnesota law. Examples of the estimated savings or cost associated with particular projects follow this report in Appendix D. Table 2 below summarizes estimated costs and savings from substituting federal prevailing wage rates for Minnesota’s rates. The table shows actual overall project costs obtained from bond amounts for local school and state building projects, and from successful low bids for state transportation projects. These are for public construction projects let in, or for which bids were approved in, calendar year 2002. The table also presents the estimated minimum and maximum savings or costs associated with using the federal prevailing wage rates in place of Minnesota’s rates. These endpoints are based on the range of estimates we obtained as to what portion of a total project’s costs are subject to prevailing wage rates (see Table 1 above). Our estimates of the county-by-county labor costs for work on these projects that was subject to prevailing wage accompanies the list of projects found in Appendix A.

Table 2: Estimated (Savings) or Cost Associated with Substituting Federal Prevailing Wage Rates on Calendar Year 2002 Minnesota Public Construction Projects, By County

Range of (Savings) or

Cost $(000)

Range of (Savings) or Cost as % of Total

Project Cost

County

Total

Project Costs

(000 of $)

Minimum

Maximum

Minimum

Maximum Aitkin $5,994 $(44) $(56) (0.7) (0.9) Anoka 33,203 384 522 1.2 1.6 Becker 3,713 289 452 7.8 12.2 Beltrami 18,249 86 136 0.5 0.7 Benton 11,236 (32) (42) (0.3) (0.4) Big Stone 140 (10) (13) (7.0) (9.0) Blue Earth 9,524 (708) (905) (7.4) (9.5) Carlton 4,505 4 15 0.1 0.3 Carver 4,910 (918) (1,172) (18.7) (23.9) Cass 4,445 (81) (104) (1.8) (2.3) Chippewa 330 (43) (54) (12.9) (16.5) Chisago 40,548 1,000 1,557 2.5 3.8 Clay 84,921 6,013 9,101 7.1 10.7 Clearwater 715 (40) (52) (5.7) (7.2) Cook 8,110 170 218 2.1 2.7 Cottonwood 2,790 (140) (179) (5.0) (6.4) Crow Wing 85,612 3,905 6,163 4.6 7.2 Dakota 146,798 847 1,282 0.6 0.9 Dodge 764 (80) (102) (10.5) (13.4) Douglas 9,674 (661) (893) (6.8) (9.2)

Analysis and Interpretation

10

Range of (Savings) or

Cost $(000)

Range of (Savings) or Cost as % of Total

Project Cost

County

Total

Project Costs

(000 of $)

Minimum

Maximum

Minimum

Maximum Faribault 449 (33) (43) (7.4) (9.5) Fillmore 2,686 (281) (359) (10.5) (13.4) Freeborn $15,577 $(3,046) $(3,894) (0.2) (25.0) Goodhue 4,842 (243) (310) (5.0) (6.4) Grant 7,122 (480) (613) (6.7) (8.6) Hennepin 251,476 1,755 2,511 0.7 1.0 Houston 12,464 (87) (111) (0.7) (0.9) Hubbard 387 (15) (20) (4.0) (5.1) Isanti 3,777 (680) (869) (18.0) (23.0) Itasca 16,918 (117) (134) (0.7) (0.8) Kanabec 36 (1) (2) (4.1) (5.3) Kandiyohi 40,827 (5,251) (6,714) (12.9) (16.4) Kittson 390 (135) (173) (34.6) (44.2) Koochiching 2,559 (339) (434) (13.3) (16.9) Lac Qui Parle 1,628 (210) (268) (12.9) (16.5) Lake 39,885 513 789 1.3 2.0 Lake of the Woods 1,683 (95) (121) (5.7) (7.2) Le Sueur 6,383 (467) (598) (7.3) (9.4) Lincoln 1,114 (144) (183) (12.9) (16.5) Lyon 8,427 (746) (955) (8.9) (11.3) Mahnomen 7,286 308 482 4.2 6.6 Marshall 4,239 (257) (328) (6.1) (7.7) Martin 111 (6) (7) (5.0) (6.4) Meeker 156 (14) (17) (8.7) (11.2) Mille Lacs 36 (1) (2) (4.1) (5.3) Morrison 14,052 368 635 2.6 4.5 Mower 59 (6) (8) (10.5) (13.4) Nicollet 4,351 (5) (3) (0.1) (0.1) Nobles 1,445 (73) (94) (5.1) (6.5) Norman 306 (19) (24) (6.1) (7.7) Olmsted 779 (5) (7) (0.7) (0.9) Otter Tail 7,772 (433) (587) (5.6) (7.6) Pennington 3,153 (34) (39) (1.1) (1.2) Pine 592 (25) (32) (4.2) (5.4) Pipestone 5,396 (695) (888) (12.9) (16.5) Polk 10,338 187 253 1.8 2.5 Pope 182 (13) (17) (7.2) (9.1) Ramsey 176,160 1,071 1,455 0.6 0.8 Red Lake 306 (19) (24) (6.1) (7.7) Redwood 1,745 (174) (223) (10.0) (12.8) Renville 5,784 (744) (951) (12.9) (16.4) Rice 1,528 (2) (2) (0.1) (0.1) Rock 1,864 (95) (121) (5.1) (6.5) Roseau 4,545 (59) (59) (1.3) (1.3) Saint Louis 86,230 1,002 1,401 1.2 1.6 Scott 9,874 92 134 0.9 1.4 Sherburne 12,358 453 580 3.7 4.7 Sibley 1,976 (143) (183) (7.2) (9.3) Stearns 2,824 28 43 1.0 1.5 Steele 3,087 (350) (447) (11.3) (14.5) Stevens 28,045 (10) (12) (0.0) (0.0) Swift 140 (19) (25) (13.9) (17.8) Todd 6,859 (956) (1,222) (13.9) (17.8) Traverse 645 (44) (56) (6.9) (8.8) Wabasha 809 (68) (87) (8.4) (10.7)

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

11

Range of (Savings) or

Cost $(000)

Range of (Savings) or Cost as % of Total

Project Cost

County

Total

Project Costs

(000 of $)

Minimum

Maximum

Minimum

Maximum Wadena 199 (27) (35) (13.7) (17.5) Waseca 7,157 (532) (680) (7.4) (9.5) Washington 132,426 140 185 0.1 0.1 Wilkin 3,638 (234) (305) (6.4) (8.4) Winona 31,873 782 1,062 2.5 3.3 Wright 15,465 338 495 2.2 3.2 Yellow Medicine 212 (27) (35) (12.9) (16.5) Unassigned 216,459 3,573 4,845 1.7 0.0 Totals $1,707,269 $3,091 $8,427 0.2% 0.5%

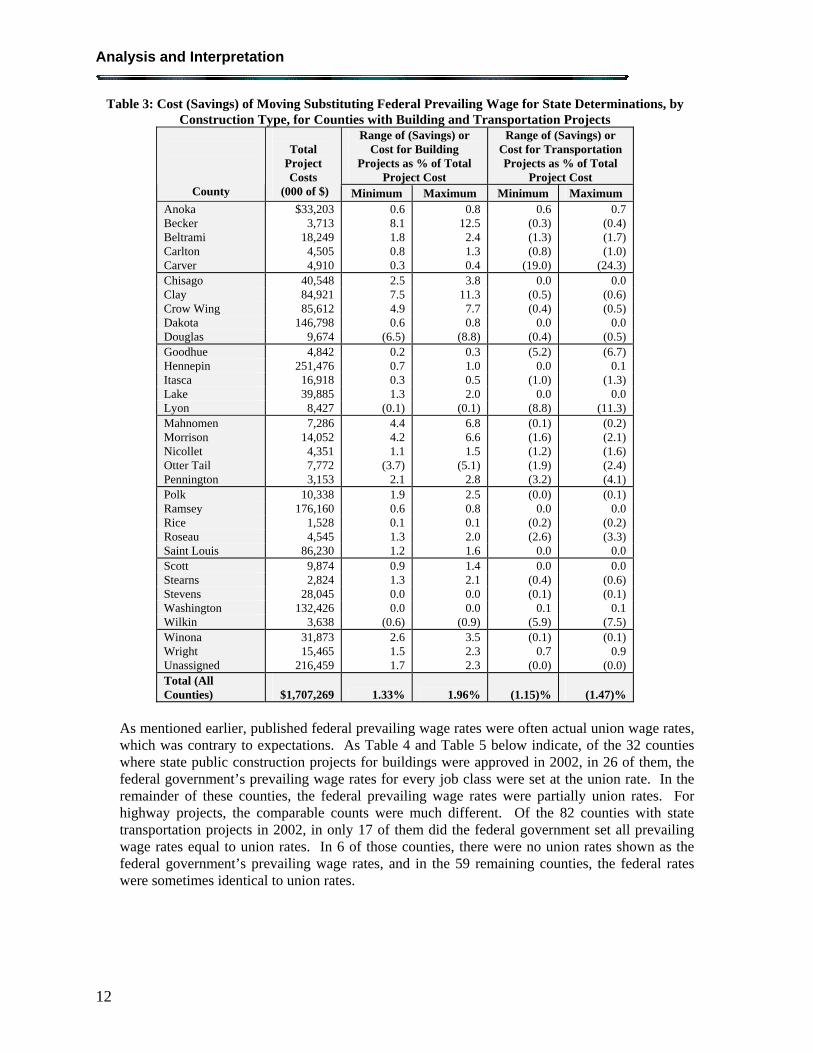

As Table 2 indicates, public construction costs would rise slightly if the state used the federal method of determining prevailing wage, but there would likely be additional costs associated with moving to the federal method of determining prevailing wages. While the federal prevailing wage rates reported for building projects generally date from between 2002 and 2004, the rates reported for building projects were much older. In 61 counties, the rates dated from 1999. In one county (Polk), the non-union rates date from 1992. In three other counties, Carver, Clay and Isanti, the non-union rates date from 1990. The time period disparity is evident when comparing estimated costs or savings of substituting the federal prevailing wages by construction type. As Table 3 below reveals, wage costs increase significantly more for building (non-highway) projects under such a substitution, both overall and at the county-by-county level. In only four counties (Douglas, Lake, Otter Tail and Wright) do transportation wage costs increase more than building wage costs under a move from state to federal prevailing wages. Our analysis indicates that, while the state would save 1.2% to 1.5% on transportation projects by making this switch, Minnesota would assume 1.3% to 2.0% higher costs for building projects. Not surprisingly, because of the datedness of the rates, Carver, Clay and Isanti counties had, respectively the largest, second-largest and fourth-largest reductions in costs when federal prevailing wage rates were substituted for state rates for transportation projects. With a more timely determination of rates, such savings on transportation projects by using federal prevailing wage rates would disappear, further increasing the statewide costs of such a substitution.

Analysis and Interpretation

12

Table 3: Cost (Savings) of Moving Substituting Federal Prevailing Wage for State Determinations, by Construction Type, for Counties with Building and Transportation Projects

Range of (Savings) or Cost for Building

Projects as % of Total Project Cost

Range of (Savings) or Cost for Transportation Projects as % of Total

Project Cost

County

Total

Project Costs

(000 of $) Minimum Maximum Minimum Maximum Anoka $33,203 0.6 0.8 0.6 0.7 Becker 3,713 8.1 12.5 (0.3) (0.4) Beltrami 18,249 1.8 2.4 (1.3) (1.7) Carlton 4,505 0.8 1.3 (0.8) (1.0) Carver 4,910 0.3 0.4 (19.0) (24.3) Chisago 40,548 2.5 3.8 0.0 0.0 Clay 84,921 7.5 11.3 (0.5) (0.6) Crow Wing 85,612 4.9 7.7 (0.4) (0.5) Dakota 146,798 0.6 0.8 0.0 0.0 Douglas 9,674 (6.5) (8.8) (0.4) (0.5) Goodhue 4,842 0.2 0.3 (5.2) (6.7) Hennepin 251,476 0.7 1.0 0.0 0.1 Itasca 16,918 0.3 0.5 (1.0) (1.3) Lake 39,885 1.3 2.0 0.0 0.0 Lyon 8,427 (0.1) (0.1) (8.8) (11.3) Mahnomen 7,286 4.4 6.8 (0.1) (0.2) Morrison 14,052 4.2 6.6 (1.6) (2.1) Nicollet 4,351 1.1 1.5 (1.2) (1.6) Otter Tail 7,772 (3.7) (5.1) (1.9) (2.4) Pennington 3,153 2.1 2.8 (3.2) (4.1) Polk 10,338 1.9 2.5 (0.0) (0.1) Ramsey 176,160 0.6 0.8 0.0 0.0 Rice 1,528 0.1 0.1 (0.2) (0.2) Roseau 4,545 1.3 2.0 (2.6) (3.3) Saint Louis 86,230 1.2 1.6 0.0 0.0 Scott 9,874 0.9 1.4 0.0 0.0 Stearns 2,824 1.3 2.1 (0.4) (0.6) Stevens 28,045 0.0 0.0 (0.1) (0.1) Washington 132,426 0.0 0.0 0.1 0.1 Wilkin 3,638 (0.6) (0.9) (5.9) (7.5) Winona 31,873 2.6 3.5 (0.1) (0.1) Wright 15,465 1.5 2.3 0.7 0.9 Unassigned 216,459 1.7 2.3 (0.0) (0.0) Total (All Counties)

$1,707,269 1.33% 1.96%

(1.15)%

(1.47)%

As mentioned earlier, published federal prevailing wage rates were often actual union wage rates, which was contrary to expectations. As Table 4 and Table 5 below indicate, of the 32 counties where state public construction projects for buildings were approved in 2002, in 26 of them, the federal government’s prevailing wage rates for every job class were set at the union rate. In the remainder of these counties, the federal prevailing wage rates were partially union rates. For highway projects, the comparable counts were much different. Of the 82 counties with state transportation projects in 2002, in only 17 of them did the federal government set all prevailing wage rates equal to union rates. In 6 of those counties, there were no union rates shown as the federal government’s prevailing wage rates, and in the 59 remaining counties, the federal rates were sometimes identical to union rates.

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

13

Table 4: Counties Whose Federal Prevailing Wage Rates are Entirely Union Wage Rates, by Construction Type

Building Highway Anoka Mahnomen Anoka Sherburne Becker Morrison Benton Stearns Beltrami Nicollet Carlton Washington Carlton Pennington Chisago Wright Carver Polk Cook Chisago Ramsey Dakota Clay Rice Hennepin Crow Wing Roseau Houston Dakota Saint Louis Lake Goodhue Scott Olmsted Hennepin Washington Ramsey Itasca Winona Saint Louis Lake Wright Scott

Table 5: Counties Whose Federal Prevailing Wage Rates Include No Union Wage Rates, by Construction Type

Building (no counties) Highway Carver Steele Clay Todd Isanti Wadena

Because the methodology requires the Department of Labor to use the average, rather than the modal wage, the expectation was that the federal prevailing wage rates would not typically use union rates and would be lower than Minnesota’s rates. Since data submitted through this survey program is confidential, we can only speculate as to why higher union rates are so often used as the federal prevailing rate. Anecdotal evidence indicates that while non-union contractors are aware of this survey, few know how even to obtain the requisite forms from the Department of Labor, and are thus likely under-represented in the survey data.

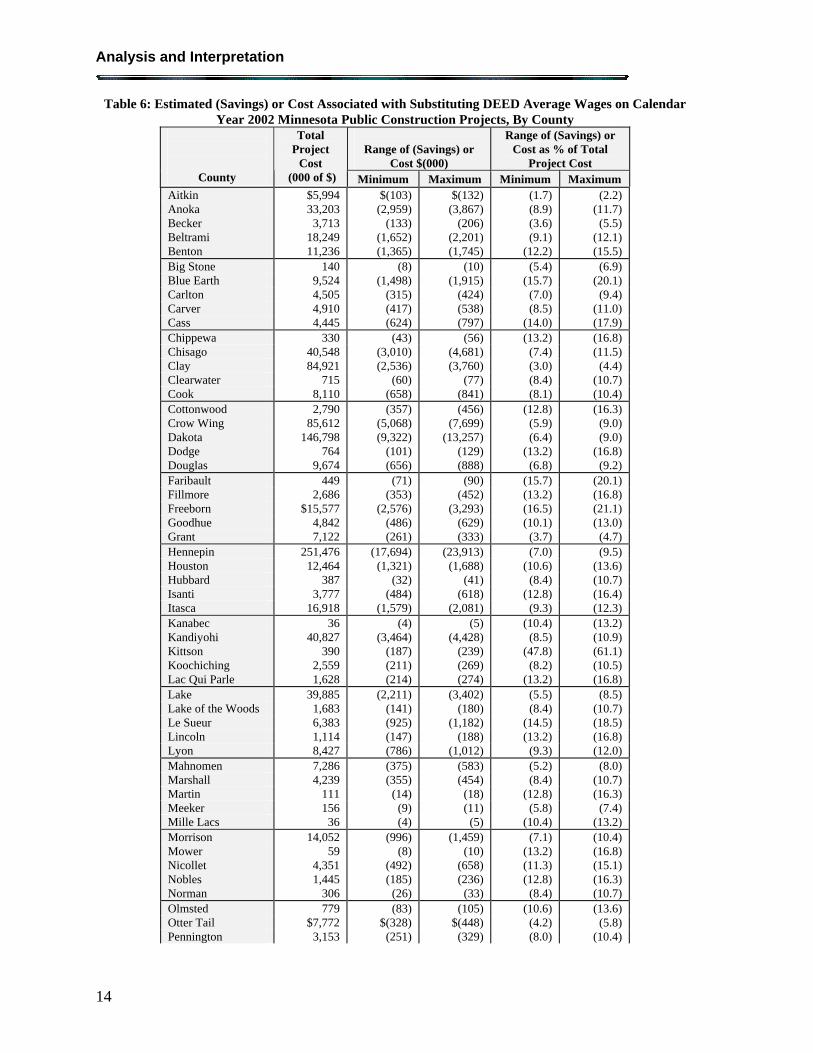

Comparison Between Current Law and Median Wage Determinations Because the general public most likely intuitively expects a term like “prevailing wage” to be similar to an average wage, we examined the effect on public construction costs of using wage rates that are closer to that intuitive understanding. The Minnesota Department of Employment and Economic Development (DEED) surveys Minnesota businesses regarding wages on a quarterly basis. The survey has a much wider distribution than current prevailing wage rate surveys, since employers are required to participate in the survey in order to qualify for certain discounts associated with the state’s insurance policies. We estimate that state and local governments would experience significant savings in wage costs if DEED average wages were substituted for the current prevailing wage system. After factoring in fringe benefits of 22% plus wages, based on informal surveys from non-union construction contractors, we estimate that between $126 million and $171 million could have been cut from the project costs examined for this study. Put another way, the same projects could have been constructed for 7.4% to 10.0% less than actual or proposed costs, under the assumptions used in this study. Table 6 provides a county-by-county summary of our findings.

Analysis and Interpretation

14

Table 6: Estimated (Savings) or Cost Associated with Substituting DEED Average Wages on Calendar Year 2002 Minnesota Public Construction Projects, By County

Range of (Savings) or

Cost $(000)

Range of (Savings) or Cost as % of Total

Project Cost

County

Total Project

Cost (000 of $) Minimum Maximum Minimum Maximum

Aitkin $5,994 $(103) $(132) (1.7) (2.2) Anoka 33,203 (2,959) (3,867) (8.9) (11.7) Becker 3,713 (133) (206) (3.6) (5.5) Beltrami 18,249 (1,652) (2,201) (9.1) (12.1) Benton 11,236 (1,365) (1,745) (12.2) (15.5) Big Stone 140 (8) (10) (5.4) (6.9) Blue Earth 9,524 (1,498) (1,915) (15.7) (20.1) Carlton 4,505 (315) (424) (7.0) (9.4) Carver 4,910 (417) (538) (8.5) (11.0) Cass 4,445 (624) (797) (14.0) (17.9) Chippewa 330 (43) (56) (13.2) (16.8) Chisago 40,548 (3,010) (4,681) (7.4) (11.5) Clay 84,921 (2,536) (3,760) (3.0) (4.4) Clearwater 715 (60) (77) (8.4) (10.7) Cook 8,110 (658) (841) (8.1) (10.4) Cottonwood 2,790 (357) (456) (12.8) (16.3) Crow Wing 85,612 (5,068) (7,699) (5.9) (9.0) Dakota 146,798 (9,322) (13,257) (6.4) (9.0) Dodge 764 (101) (129) (13.2) (16.8) Douglas 9,674 (656) (888) (6.8) (9.2) Faribault 449 (71) (90) (15.7) (20.1) Fillmore 2,686 (353) (452) (13.2) (16.8) Freeborn $15,577 (2,576) (3,293) (16.5) (21.1) Goodhue 4,842 (486) (629) (10.1) (13.0) Grant 7,122 (261) (333) (3.7) (4.7) Hennepin 251,476 (17,694) (23,913) (7.0) (9.5) Houston 12,464 (1,321) (1,688) (10.6) (13.6) Hubbard 387 (32) (41) (8.4) (10.7) Isanti 3,777 (484) (618) (12.8) (16.4) Itasca 16,918 (1,579) (2,081) (9.3) (12.3) Kanabec 36 (4) (5) (10.4) (13.2) Kandiyohi 40,827 (3,464) (4,428) (8.5) (10.9) Kittson 390 (187) (239) (47.8) (61.1) Koochiching 2,559 (211) (269) (8.2) (10.5) Lac Qui Parle 1,628 (214) (274) (13.2) (16.8) Lake 39,885 (2,211) (3,402) (5.5) (8.5) Lake of the Woods 1,683 (141) (180) (8.4) (10.7) Le Sueur 6,383 (925) (1,182) (14.5) (18.5) Lincoln 1,114 (147) (188) (13.2) (16.8) Lyon 8,427 (786) (1,012) (9.3) (12.0) Mahnomen 7,286 (375) (583) (5.2) (8.0) Marshall 4,239 (355) (454) (8.4) (10.7) Martin 111 (14) (18) (12.8) (16.3) Meeker 156 (9) (11) (5.8) (7.4) Mille Lacs 36 (4) (5) (10.4) (13.2) Morrison 14,052 (996) (1,459) (7.1) (10.4) Mower 59 (8) (10) (13.2) (16.8) Nicollet 4,351 (492) (658) (11.3) (15.1) Nobles 1,445 (185) (236) (12.8) (16.3) Norman 306 (26) (33) (8.4) (10.7) Olmsted 779 (83) (105) (10.6) (13.6) Otter Tail $7,772 $(328) $(448) (4.2) (5.8) Pennington 3,153 (251) (329) (8.0) (10.4)

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

15

Range of (Savings) or

Cost $(000)

Range of (Savings) or Cost as % of Total

Project Cost

County

Total Project

Cost (000 of $) Minimum Maximum Minimum Maximum

Pine 592 (83) (106) (14.1) (18.0) Pipestone 5,396 (711) (909) (13.2) (16.8) Polk 10,338 (793) (1,056) (7.7) (10.2) Pope 182 (7) (9) (3.9) (5.0) Ramsey 176,160 (13,125) (17,483) (7.5) (9.9) Red Lake 306 (26) (33) (8.4) (10.7) Redwood 1,745 (230) (294) (13.2) (16.9) Renville 5,784 (491) (627) (8.5) (10.9) Rice 1,528 (153) (208) (10.0) (13.6) Rock 1,864 (238) (304) (12.8) (16.3) Roseau 4,545 (325) (461) (7.2) (10.2) Saint Louis 86,230 (7,639) (10,057) (8.9) (11.7) Scott 9,874 (579) (839) (5.9) (8.5) Sherburne 12,358 (1,501) (1,919) (12.2) (15.5) Sibley 1,976 (314) (402) (15.9) (20.3) Stearns 2,824 (222) (345) (7.9) (12.2) Steele 3,087 (354) (452) (11.5) (14.7) Stevens 28,045 (47) (70) (0.2) (0.3) Swift 140 (16) (21) (11.7) (14.9) Todd 6,859 (931) (1,191) (13.6) (17.4) Traverse 645 (24) (31) (3.7) (4.8) Wabasha 809 (93) (119) (11.5) (14.7) Wadena 199 (27) (34) (13.4) (17.1) Waseca 7,157 (1,126) (1,439) (15.7) (20.1) Washington 132,426 (11,321) (14,505) (8.6) (11.0) Wilkin 3,638 (134) (177) (3.7) (4.9) Winona 31,873 (2,591) (3,504) (8.1) (11.0) Wright 15,465 (1,327) (1,968) (8.6) (12.7) Yellow Medicine 212 (28) (36) (13.2) (16.8) Unassigned 216,459 (14,887) (20,177) (6.9) (9.3) Totals $1,707,269 $(126,495) $(171,120) (7.4)% (10.0)%

Corroboration by Other Studies Other studies of prevailing wage legislation have come to similar conclusions regarding wage rate differentials between a state’s prevailing wage rate determination and average or median rates.

• MTA’s 1997 limited examination of the fiscal implications of the prevailing wage law on Minnesota school districts showed that the prevailing wage requirement added 4-10% to the cost of the selected school building projects already in progress.

• The estimates in this study also resemble the findings from a study authorized by the State of Ohio from 1997 to 2001. During that period, the state exempted construction undertaken by school districts from the state’s prevailing wage requirements. The Ohio Legislative Service Commission, found “indications of a savings of $487.9 million in aggregate school construction savings during the post exemption period, an overall savings of 10.7 percent.”12 Given that inflation factors would likely decrease the number

12 S.B. 102 Report: The Effects of the Exemption of School Construction Projects from Ohio’s Prevailing Wage Law, Ohio Legislative Service Commission, May 20, 2002.

Analysis and Interpretation

16

somewhat, the savings from this study would almost certainly fall within the range indicated above.

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

17

V. Recommendations

This report has examined the issue of prevailing wages in the state of Minnesota, and has tried to provide reasonable estimates of the fiscal impact on taxpayers of the changes to current statute; both by moving to the federal wage determinations, and from moving to DEED’s published median wage. Minnesota’s modal method of determining prevailing wages for public construction projects is used only in one other state, California. It results in wage rates significantly higher than those reported by DEED in its median wage survey. Using the federal method for calculating prevailing wage rates would add even more cost to public construction projects, apparently because of the limited number of federal projects and limited federal survey data in Minnesota. The term “prevailing wage” itself connotes a wage that is typical of an area, and is most likely commonly understood as an average wage by the general public. However, its application in Minnesota results in prevailing wage rates that are not reflective of typical wage rates. The primary purpose of “Little Davis-Bacon” laws is to protect local workers from cheap, imported labor, and as long as the wage rates that are used are truly “prevailing” (that is, typical of an area), that purpose does not seem to be threatened regardless of the methodology used to calculate those rates. The claim by proponents of the current method of calculating Minnesota’s prevailing wage rates that buildings are constructed more quickly and with better quality cannot be evaluated in a study like this of such limited scope. However, our underlying assumption is that contract specifications, penalty provisions for delays, and aggressive construction management can provide at the very least an equally effective alternative method for addressing timing and quality issues for public construction projects. In view of these observations, MTA recommends: • That the widely used DEED survey for median wages be used as an alternative definition

of prevailing wage for public construction projects in Minnesota; o The methodology underlying the current system is, at best, not indicative of wage

rates that actually prevail in a given area. The modal, rather than median or average, calculation of prevailing wage provides a built-in incentive to unions to report their wage rates, which are standardized to the penny. The voluntary reporting system further ensures that those who benefit least from the current wage determination system have little, if any reason to report wage data.

• that DEED develop a survey comparable to the median wage survey for employee benefits to be used for the benefits portion of the prevailing wage rates as an alternative to the currently determined prevailing benefit rates;

o The Department of Employment and Economic Development’s quarterly survey is the most comprehensive in the state.

• that this alternate method of determining prevailing wage rates be tested in specific locations and compared to comparable public construction projects in the state in order to compare the costs of such projects directly with one another, at the earliest possible time.

Such a comparison would allow there to be an empirical test of the claims of both proponents and opponents of Minnesota’s current prevailing wage law. Should the test demonstrate that

Recommendations

18

using the median wage rates calculated by Minnesota’s DEED results in lowered costs for public construction projects, those median wage rates (along with DEED’s surveyed benefits rates) should then replace Minnesota’s current method of determining prevailing wage rates.

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

19

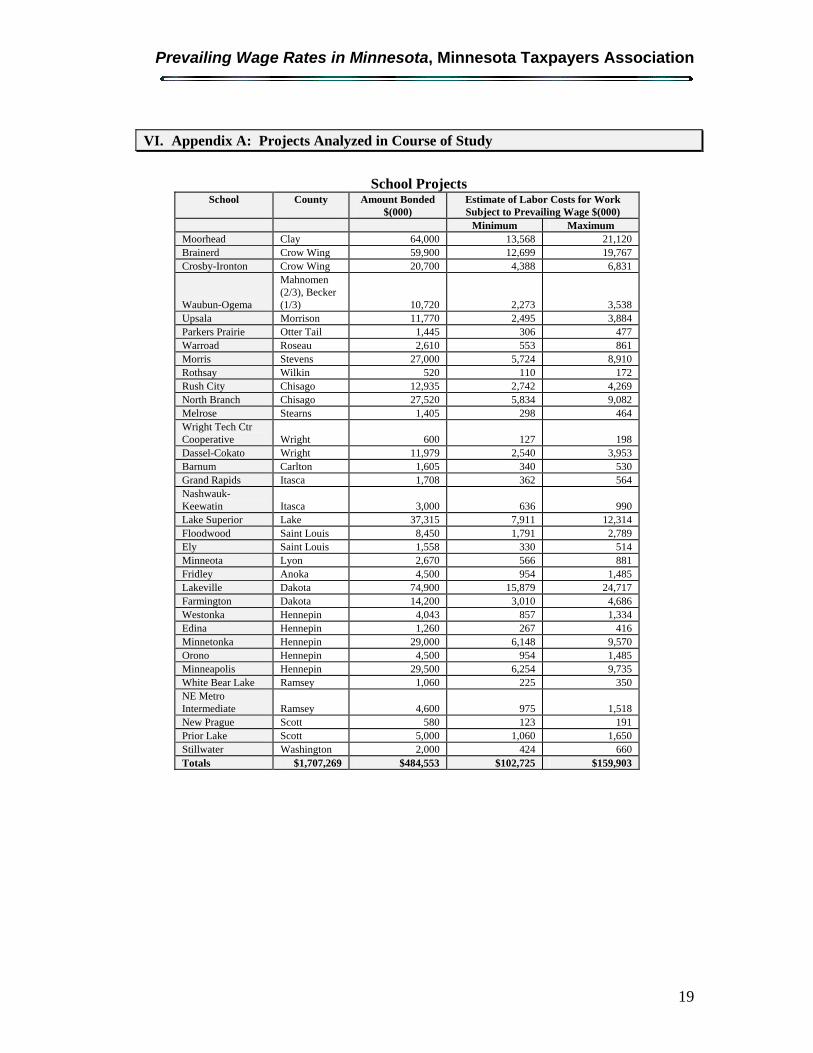

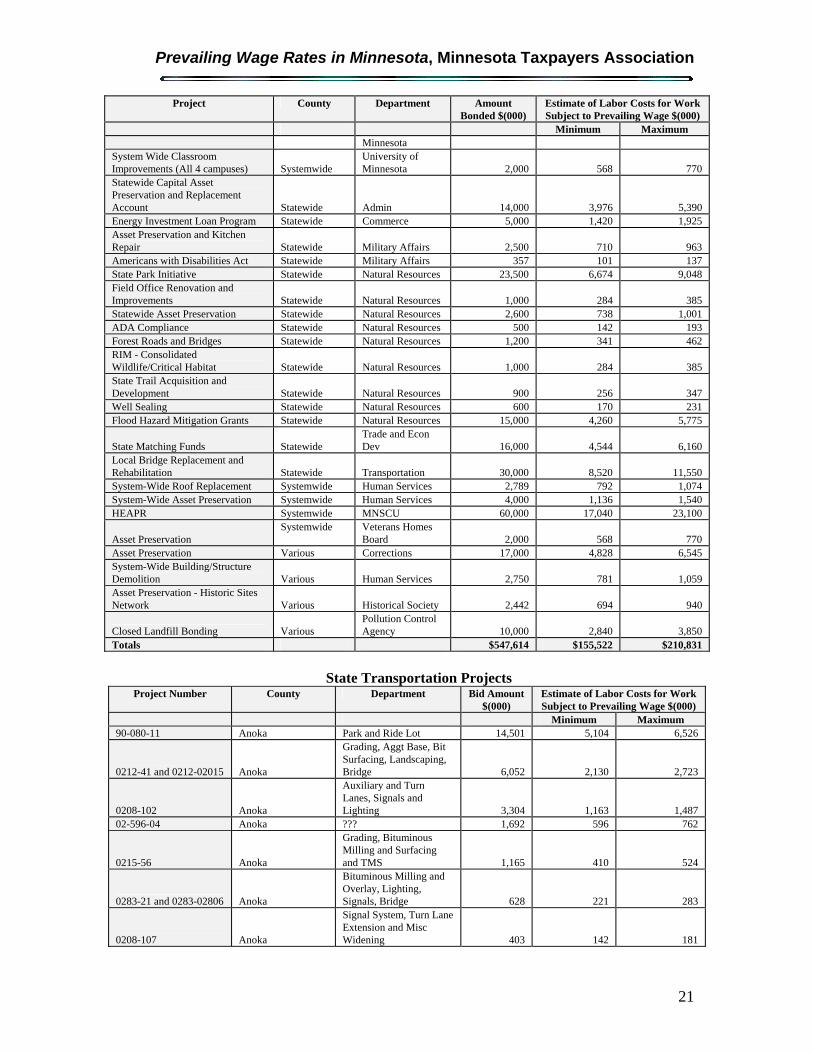

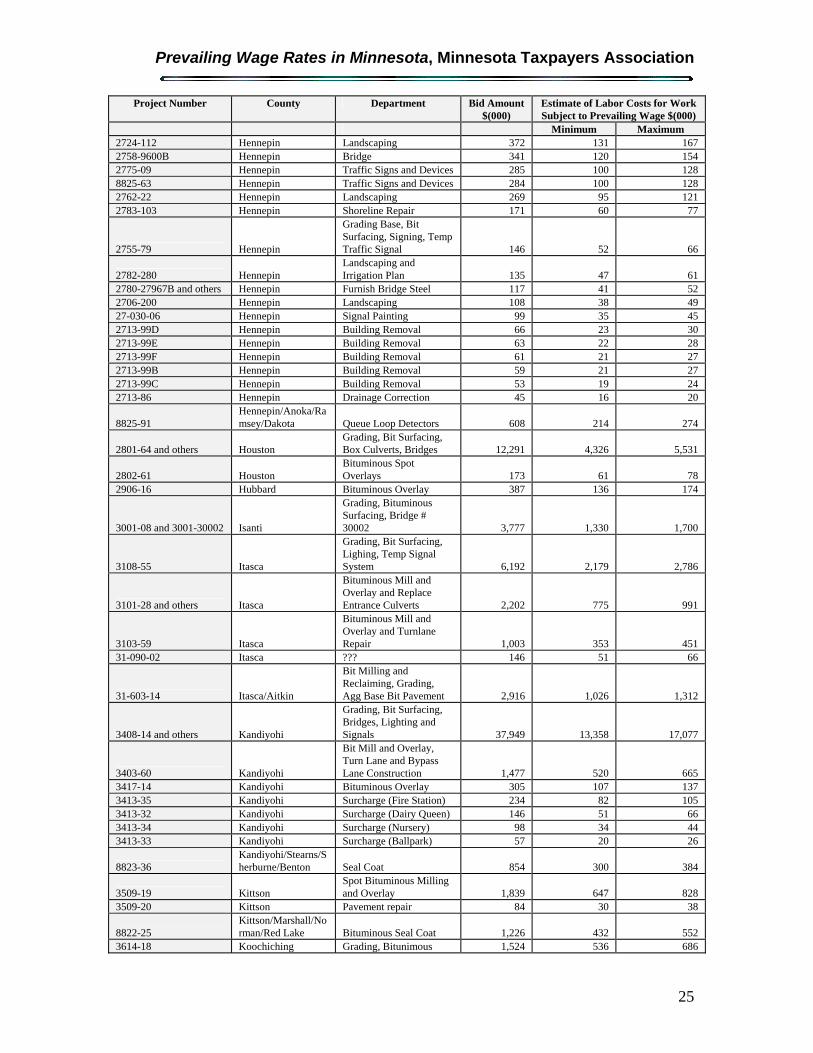

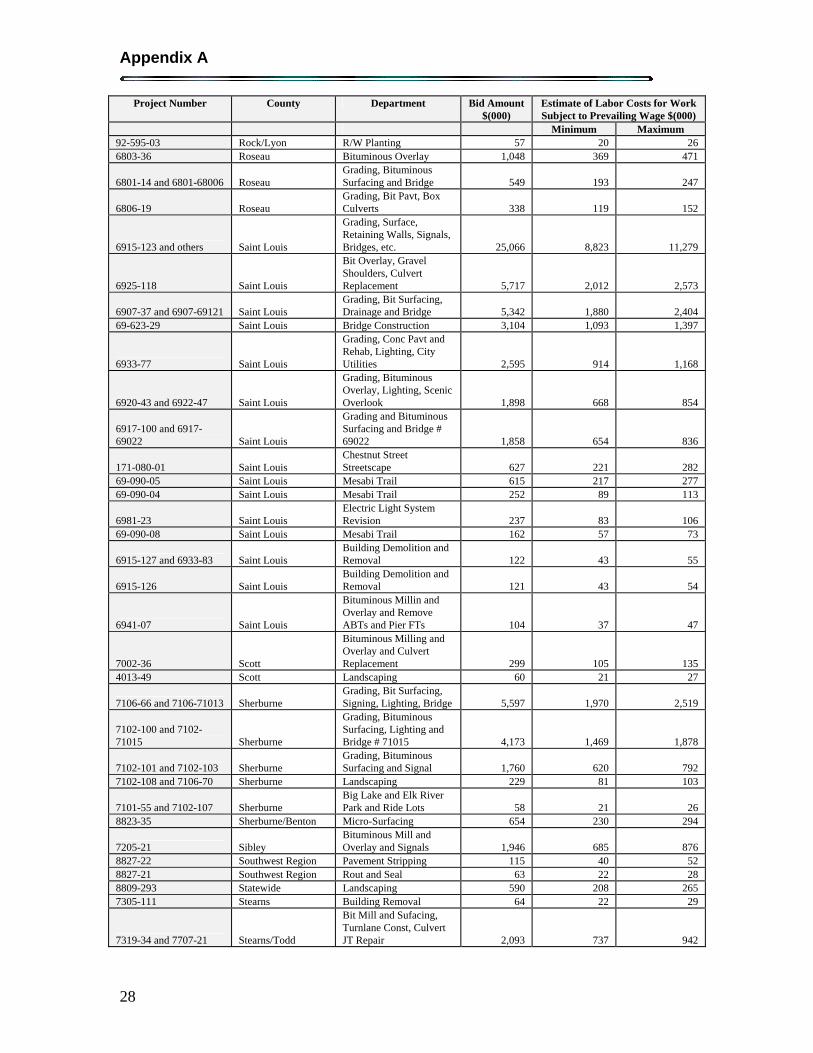

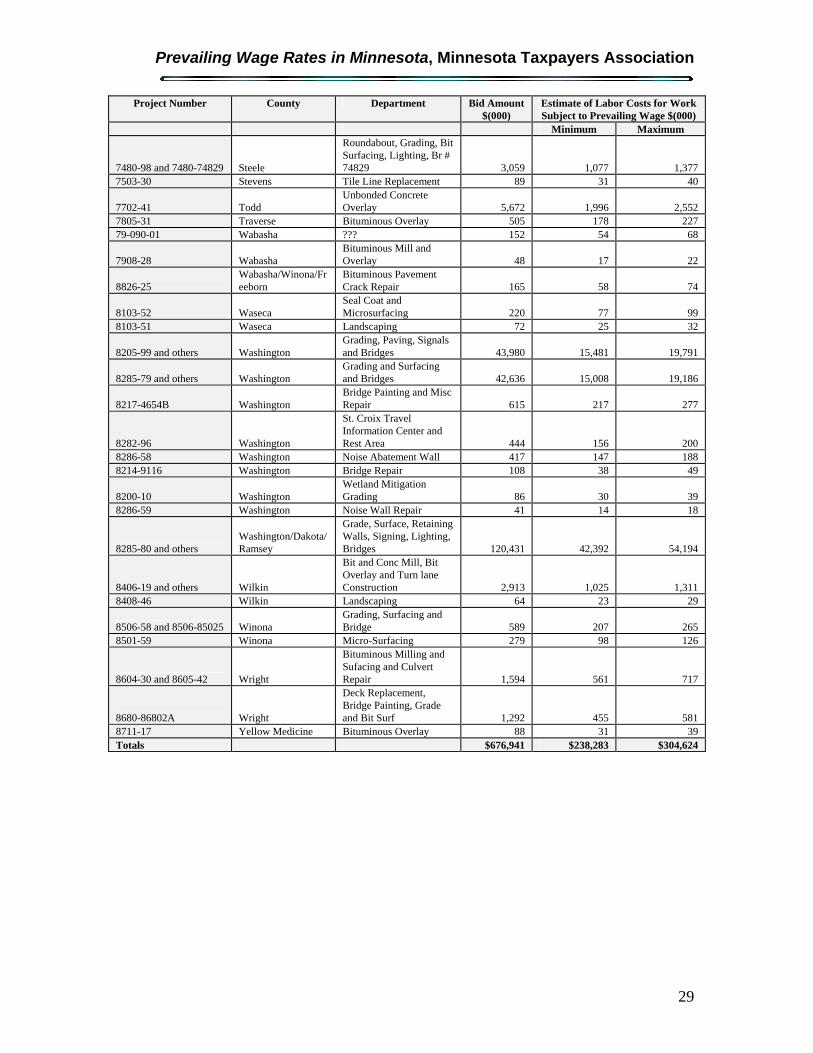

VI. Appendix A: Projects Analyzed in Course of Study

School Projects

School County Amount Bonded $(000)

Estimate of Labor Costs for Work Subject to Prevailing Wage $(000)

Minimum Maximum Moorhead Clay 64,000 13,568 21,120 Brainerd Crow Wing 59,900 12,699 19,767 Crosby-Ironton Crow Wing 20,700 4,388 6,831

Waubun-Ogema

Mahnomen (2/3), Becker (1/3) 10,720 2,273 3,538

Upsala Morrison 11,770 2,495 3,884 Parkers Prairie Otter Tail 1,445 306 477 Warroad Roseau 2,610 553 861 Morris Stevens 27,000 5,724 8,910 Rothsay Wilkin 520 110 172 Rush City Chisago 12,935 2,742 4,269 North Branch Chisago 27,520 5,834 9,082 Melrose Stearns 1,405 298 464 Wright Tech Ctr Cooperative Wright 600 127 198 Dassel-Cokato Wright 11,979 2,540 3,953 Barnum Carlton 1,605 340 530 Grand Rapids Itasca 1,708 362 564 Nashwauk-Keewatin Itasca 3,000 636 990 Lake Superior Lake 37,315 7,911 12,314 Floodwood Saint Louis 8,450 1,791 2,789 Ely Saint Louis 1,558 330 514 Minneota Lyon 2,670 566 881 Fridley Anoka 4,500 954 1,485 Lakeville Dakota 74,900 15,879 24,717 Farmington Dakota 14,200 3,010 4,686 Westonka Hennepin 4,043 857 1,334 Edina Hennepin 1,260 267 416 Minnetonka Hennepin 29,000 6,148 9,570 Orono Hennepin 4,500 954 1,485 Minneapolis Hennepin 29,500 6,254 9,735 White Bear Lake Ramsey 1,060 225 350 NE Metro Intermediate Ramsey 4,600 975 1,518 New Prague Scott 580 123 191 Prior Lake Scott 5,000 1,060 1,650 Stillwater Washington 2,000 424 660 Totals $1,707,269 $484,553 $102,725 $159,903

Appendix A

20

State Building Projects

Project County Department Amount Bonded $(000)

Estimate of Labor Costs for Work Subject to Prevailing Wage $(000)

Minimum Maximum Lino Lakes 416 Bed Offender Housing Unit Anoka Corrections 4,146 1,177 1,596 Red Lake School Additions and Renovations Beltrami Education 12,400 3,522 4,774 MSU Moorhead - New Science Building Clay MNSCU 18,955 5,383 7,298 Sibley Historic Site Preservation Dakota Historical Society 300 85 116 Hastings V.H. Renovation and Improvements Dakota

Veterans Homes Board 8,553 2,429 3,293

Asset Presevation Dakota Zoological Gardens 3,000 852 1,155

Alexandria TC - Classroom/Technology Bldg Douglas MNSCU 9,150 2,599 3,523 Northwest Metro Busway Hennepin Metro Council 20,000 5,680 7,700 Historic Fort Snelling Site Improvements Hennepin Historical Society 500 142 193 Normandale CC - Science Remodel Phase 2 Hennepin MNSCU 9,900 2,812 3,812 Mpls C&TC - Consolidation Remodel Phase 2 Hennepin MNSCU 9,000 2,556 3,465

Performance Hall Cat Walk Hennepin Perpich Center for A.E. 125 36 48

Asset Preservation Hennepin Perpich Center for A.E. 643 183 248

Nicholson Hall Hennepin University of Minnesota 10,000 2,840 3,850

Fergus Falls RTC - Upgrade Program Facilities Otter Tail Human Services 3,000 852 1,155 Fergus Falls - Solid Waste Combustor Otter Tail

Office of Env. Assist. 1,150 327 443

Office Facilities Development Pennington Natural Resources 1,500 426 578

Crookston - Bede Hall Replacement Polk University of Minnesota 7,701 2,187 2,965

Health and Agriculture Laboratories Ramsey Admin 60,000 17,040 23,100 Capitol Complex Electrical Work Ramsey Admin 3,231 918 1,244 Capitol Building: Asset Preservation Ramsey

Capital Area Arch. Pl. Bd. 646 183 249

Metro SU - Library and Info Technology Center Ramsey MNSCU 17,442 4,954 6,715 Century C&TC - Design Intermediate Space Remodel Ramsey MNSCU 2,500 710 963 St. Paul - Plant Growth Facilities, Phase II Ramsey

University of Minnesota 17,700 5,027 6,815

Shakopee - ILC Renovation and Support Space Scott Corrections 3,070 872 1,182 Metro Regional Parks Capital Improvements Metro Counties Natural Resources 6,000 1,704 2,310

Silver Bay V.H. Roof Replacement Lake Veterans Homes Board 2,345 666 903

Saint Peter Regional Treatment Center - Convert Power Plan to Low Pressure Nicollet Human Services 3,619 1,028 1,393

Asset Preservation Rice Minnesota State Academies 1,500 426 578

Duluth - Laboratory Science Building Saint Louis

University of Minnesota 25,500 7,242 9,818

Winona SU - New Science Building Winona MNSCU 30,000 8,520 11,550 MSC-SETC - Student Services Remodel

Goodhue and Winona MNSCU 1,900 540 732

Systemwide - HEAPR Systemwide University of 35,000 9,940 13,475

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

21

Project County Department Amount Bonded $(000)

Estimate of Labor Costs for Work Subject to Prevailing Wage $(000)

Minimum Maximum Minnesota

System Wide Classroom Improvements (All 4 campuses) Systemwide

University of Minnesota 2,000 568 770

Statewide Capital Asset Preservation and Replacement Account Statewide Admin 14,000 3,976 5,390 Energy Investment Loan Program Statewide Commerce 5,000 1,420 1,925 Asset Preservation and Kitchen Repair Statewide Military Affairs 2,500 710 963 Americans with Disabilities Act Statewide Military Affairs 357 101 137 State Park Initiative Statewide Natural Resources 23,500 6,674 9,048 Field Office Renovation and Improvements Statewide Natural Resources 1,000 284 385 Statewide Asset Preservation Statewide Natural Resources 2,600 738 1,001 ADA Compliance Statewide Natural Resources 500 142 193 Forest Roads and Bridges Statewide Natural Resources 1,200 341 462 RIM - Consolidated Wildlife/Critical Habitat Statewide Natural Resources 1,000 284 385 State Trail Acquisition and Development Statewide Natural Resources 900 256 347 Well Sealing Statewide Natural Resources 600 170 231 Flood Hazard Mitigation Grants Statewide Natural Resources 15,000 4,260 5,775

State Matching Funds Statewide Trade and Econ Dev 16,000 4,544 6,160

Local Bridge Replacement and Rehabilitation Statewide Transportation 30,000 8,520 11,550 System-Wide Roof Replacement Systemwide Human Services 2,789 792 1,074 System-Wide Asset Preservation Systemwide Human Services 4,000 1,136 1,540 HEAPR Systemwide MNSCU 60,000 17,040 23,100

Asset Preservation Systemwide Veterans Homes

Board 2,000 568 770 Asset Preservation Various Corrections 17,000 4,828 6,545 System-Wide Building/Structure Demolition Various Human Services 2,750 781 1,059 Asset Preservation - Historic Sites Network Various Historical Society 2,442 694 940

Closed Landfill Bonding Various Pollution Control Agency 10,000 2,840 3,850

Totals $547,614 $155,522 $210,831

State Transportation Projects Project Number County Department Bid Amount

$(000) Estimate of Labor Costs for Work Subject to Prevailing Wage $(000)

Minimum Maximum 90-080-11 Anoka Park and Ride Lot 14,501 5,104 6,526

0212-41 and 0212-02015 Anoka

Grading, Aggt Base, Bit Surfacing, Landscaping, Bridge 6,052 2,130 2,723

0208-102 Anoka

Auxiliary and Turn Lanes, Signals and Lighting 3,304 1,163 1,487

02-596-04 Anoka ??? 1,692 596 762

0215-56 Anoka

Grading, Bituminous Milling and Surfacing and TMS 1,165 410 524

0283-21 and 0283-02806 Anoka

Bituminous Milling and Overlay, Lighting, Signals, Bridge 628 221 283

0208-107 Anoka

Signal System, Turn Lane Extension and Misc Widening 403 142 181

Appendix A

22

Project Number County Department Bid Amount $(000)

Estimate of Labor Costs for Work Subject to Prevailing Wage $(000)

Minimum Maximum

8825-52 Anoka/Chisago/Dakota/Ramsey Group Relamping 371 131 167

8825-71 Anoka/Hennepin/Ramsey

Traffic Management Changeable Messages Signs and Signing 418 147 188

0205-78 and others Anoka/Washington

Signal Systems Interconnect and Electric Lighting System 125 44 56

0416-27 and others Beltrami Grading, Bit Surfacing, Signals, Bridges 4,324 1,522 1,946

04-605-25 Beltrami Agg Base and Shoulder, Bit Surf 737 260 332

04-615-15 Beltrami

Signal Systems, Shldr Widening, Agg Base, Bit Surf 444 156 200

8822-15 Beltrami Traffic Signs and Devices 305 107 137 0406-49 Beltrami Drainage Ditch 39 14 17

0502-89 and 0502-05016 Benton Grading, Surfacing, Retaining Wall, Drainage 7,926 2,790 3,567

05-604-20 Benton Grading, Agg base, Bit Surfacing 1,817 640 818

05-596-01 Benton Grading, Base, Bituminous Surfacing 899 316 405

8823-30 Benton/Stearns Signal Revisions 108 38 48

0713-71 Blue Earth

Grading, Bit Surfacing, Lihgting and Retaining Wall 1,669 587 751

137-090-04 Blue Earth North Minnesota River Trail 990 349 446

0702-108 and 8103-45 Blue Earth/Waseca

Grading, Base, Bituminous and Concrete Surfacing 13,425 4,726 6,041

0707-11 and 8105-19 Blue Earth/Waseca Seal Coat 245 86 110

0910-26 and 0916-09 Carlton

Grading, Bit Mill and Surfacing, Lighting and Utilities 2,074 730 933

0980-135 Carlton Bituminous Mill and Inlay 490 173 221

0980-133 Carlton De-Icing System 158 56 71 0980-09819 and 5580-58816 Carlton/Olmsted Bridge Painting 235 83 106

1002-74 Carver

Bit Mill and Overlay, Turn Lane and Shld Widening and Signing 550 194 248

91-090-02 Carver Bike Trail Underpass 427 150 192

1012-22 Carver Bituminous Mill and Overlay 53 19 24

1004-24 and others Carver/Hennepin

Shld and Turn Lane Const, Bit Overlay, Bridge, Utilities 6,030 2,123 2,713

1119-32 Cass Bituminous Milling and Overlay and Turn Lanes 1,027 362 462

1115-20 Cass Grading and Bituminous Surfacing 218 77 98

1104-21 and 3106-23 Cass/Itasca

Bit Mill and Overlay, Culvert Replacement, Turn Lane Const 2,298 809 1,034

1115-18 and others Cass/Morrison

Grading, Crack and Seat Conc, Bit Surfacing, Culv, Bridge 3,821 1,345 1,719

8823-31 Cass/Todd Bituminous Seal Coat 210 74 94

1207-18 and 3409-17 Chippewa/Kandiyohi Bituminous Overlay 520 183 234

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

23

Project Number County Department Bid Amount $(000)

Estimate of Labor Costs for Work Subject to Prevailing Wage $(000)

Minimum Maximum

8828-46 Chippewa/Kandiyohi Seal Coat Surfacing 141 50 63

1402-15 Clay

Bit Mill and Overlay, Turn lane Const, Culvert Replacement 1,826 643 822

1504-10 Clearwater

Milling, Bit Overlay, Culvert Replacement, Crack Treatment 715 252 322

1602-38 Cook

Grading, Bit Surfacing, Drainage Structures, Box Culvert 6,341 2,232 2,854

1601-59 Cook

Bituminous Milling and Surfacing, Turn Lanes, Drainage 1,224 431 551

1604-38 Cook Const Fish Ladder in Box Culvert 36 12 16

8821-80 Cook/Carlton/Itasca/Koochiching/Pine

Bit Mill and Overlay, Turn Lanes, Replace Strip Seal, etc. 327 115 147

8821-83

Cook/Carlton/Itasca/Koochiching/St. Louis/Pine Message Striping 32 11 14

8821-69 Cook/Pine/Saint Louis/Koochiching

District Wide Culvert Repair and Replacement 1,798 633 809

1703-64 and 1706-24 Cottonwood

Mill, Bit Overlay, Aggregate Shoulders, Culvert Extensions 2,790 982 1,256

1809-58 and 1809-18006 Crow Wing

Grading, Bituminous Sirfacing and Bridge # 18066 4,658 1,640 2,096

1809-65 Crow Wing Landscaping 318 112 143

1923-08 Dakota

Bit Milling and Overlay, Guardrail, Culvert Improvements 1,257 443 566

1928-47 Dakota

Bituminous Mill and Overlay and Guardrail Improvements 918 323 413

1982-19859A Dakota Shoulder Reinforcement and Bridge Rehab 896 315 403

1980-64 Dakota Traffic Management System 631 222 284

1980-19848 Dakota Bridge # 19848 and Approaches 442 155 199

8825-61 Dakota Traffic Signs and Devices 171 60 77

1909-83 Dakota Traffic Control Signal and Interconnect Systems 132 46 59

8825-111 Dakota/Ramsey/Washington

Traffic Management Changeable Message Signs 435 153 196

20-599-85 Dodge Bridge and Approach Grading 525 185 236

2007-35 Dodge Traffic Control Signal System 110 39 50

2002-30 Dodge Landscaping 70 25 31

2003-11 and others Dodge/Freeborn/Mower

Bituminous Mill and Overlay and Ditch Cleaning 177 62 80

2106-34 and 2106-21002 Douglas Lake Channel and Grading for Bridge 342 120 154

2204-23 Faribault Bituminous Overlay 320 112 144

2208-39 Faribault Remove and Replace Bituminous Shoulders 100 35 45

2307-16 and others Filllmore Grading, Bit Surfacing, 2,326 819 1,047

Appendix A

24

Project Number County Department Bid Amount $(000)

Estimate of Labor Costs for Work Subject to Prevailing Wage $(000)

Minimum Maximum Bridges

2304-44 Filllmore Bituminous Mill and Overlay 360 127 162

2480-81 and others Freeborn

Unbonded Conc Overlay with Bit Shld and Bridge Repair 14,684 5,169 6,608

8826-20 Freeborn

Bit and Conc Mill, Bit Overlay, Turn Lanes, Pavement 680 239 306

2480-96 Freeborn Landscaping 74 26 34 2401-34 Freeborn Jacking of Drainage Tile 25 9 11 2516-9040A Goodhue Bridge Painting 2,844 1,001 1,280

2502-22 Goodhue Bituminous Mill and Overlay 250 88 112

2514-113 Goodhue Traffic Control Signal System 206 72 93

2506-63 Goodhue Bituminous Pavement Crack Repair 39 14 17

2512-10 and 7902-18 Goodhue/Wabasha

Right Turn Lanes, Bituminous Mill and Overlay 1,108 390 499

2610-10 Grant Grading, Bituminous and Concerte Surfacing 6,948 2,446 3,127

2603-09 Grant Landscaping 34 12 15

2785-327 and others Hennepin Grading, Conc and Bit Surfacing 28,623 10,075 12,881

2786-115 Hennepin

Grading, Conc and Bit Surfacing, Drainage, Noise Walls, etc 20,514 7,221 9,231

2735-172 Hennepin Grading, Surfacing, Signals, Bridge # 27283 15,426 5,430 6,942

2780-53 and others Hennepin

SHLG Replacement and Widening and various bridges 7,198 2,534 3,239

2774-07 and others Hennepin

Bit Mill and Overlay, Storm Sewer, Median Barrier, Br Painting 3,870 1,362 1,742

2781-337 and 2781-400 Hennepin

Lowry Hill and Portland Tunnel Lighting Modifications 3,778 1,330 1,700

2785-27V33A and 2785-27V34A Hennepin Bridges (steel only) 3,625 1,276 1,631

2785-332 Hennepin

Misc Grading, Bit Surfacing, Retaining Wall, Signal, etc 3,241 1,141 1,458

2758-60 Hennepin

Mill and Overlay, Bit Surfacing, Conc Pavt Rehab 2,929 1,031 1,318

2744-54 Hennepin

Bituminous Mill and Overlay, Guardrail and Drainage 1,528 538 687

2772-39 Hennepin Noise Wall and Retaining Wall 1,482 522 667

116-090-01 Hennepin Ped/Bike Br. 1,335 470 601 2782-6652 and others Hennepin Bridge Painting 1,068 376 481

2785-325 Hennepin

Bituminous Mill and Overlay, TMC and Striping 979 345 440

2724-113 Hennepin Landscaping 530 187 239

2714-138 Hennepin Turn Lane, Revise Traffic Signals and Interconnect 505 178 227

2758-9600A Hennepin Bridge Painting 419 147 188

Prevailing Wage Rates in Minnesota, Minnesota Taxpayers Association

25

Project Number County Department Bid Amount $(000)

Estimate of Labor Costs for Work Subject to Prevailing Wage $(000)

Minimum Maximum 2724-112 Hennepin Landscaping 372 131 167 2758-9600B Hennepin Bridge 341 120 154 2775-09 Hennepin Traffic Signs and Devices 285 100 128 8825-63 Hennepin Traffic Signs and Devices 284 100 128 2762-22 Hennepin Landscaping 269 95 121 2783-103 Hennepin Shoreline Repair 171 60 77

2755-79 Hennepin

Grading Base, Bit Surfacing, Signing, Temp Traffic Signal 146 52 66

2782-280 Hennepin Landscaping and Irrigation Plan 135 47 61

2780-27967B and others Hennepin Furnish Bridge Steel 117 41 52 2706-200 Hennepin Landscaping 108 38 49 27-030-06 Hennepin Signal Painting 99 35 45 2713-99D Hennepin Building Removal 66 23 30 2713-99E Hennepin Building Removal 63 22 28 2713-99F Hennepin Building Removal 61 21 27 2713-99B Hennepin Building Removal 59 21 27 2713-99C Hennepin Building Removal 53 19 24 2713-86 Hennepin Drainage Correction 45 16 20

8825-91 Hennepin/Anoka/Ramsey/Dakota Queue Loop Detectors 608 214 274

2801-64 and others Houston Grading, Bit Surfacing, Box Culverts, Bridges 12,291 4,326 5,531

2802-61 Houston Bituminous Spot Overlays 173 61 78