Embed Size (px)

Citation preview

1

Price Discovery Mechanisms and Alternatives for Canadian Agriculture Part II: A Review of Pricing Mechanisms from the Economic Literature1

Al Mussell

February, 2003

Funding for this initiative was supplied by RBC-Royal Bank, Bank of Nova Scotia, TD Canada Trust, CIBC, BMO Bank of Montreal and National Bank, members of the CBA Agricultural Advisory Group, and through a grant from the Agricultural Adaptation Council

1 The author wishes to thank Brad Tkatchuk and Stephen Holub, who were instrumental in assembling background information for this review

2

EXECUTIVE SUMMARY

The purpose of this study is to review pricing mechanisms discussed in the academic literature. The role of a pricing mechanism in a supply chain for a specialty farm good is to: • Allocation of supply chain profits and costs • Induce effort and investment • Price according to value and product quality To review the research findings related to the above, the academic literature in economics, business organization, and accounting was reviewed. Based on the review of the transfer pricing literature, there appears to be some agreement on the following propositions: • For true commodity products moved through an aligned supply chain, the external cash

market provides a good indication of opportunity costs to internal buyers and sellers. Thus, external cash prices can be used as transfer prices.

• Marginal cost pricing as a form of transfer price is essentially an academic concept. The large amount of information required to calculate marginal cost, and the general need to have a menu of marginal cost across volumes and capacity usage renders it impractical.

• Shadow prices from linear programming models of the supply chain have information requirements at least as onerous as marginal cost. Indeed, if mathematical programs could really be used to allocate inputs and outputs in the supply chain, it is unclear what advantage there is of delegation to multiple segments in the first place.

Negotiated and cost-based transfers are the practical candidates as non-commodity transfer prices. A variety of pricing mechanisms related to costs are found in the literature. The most commonly discussed is the standard cost model. The criticisms of standard costs as a basis for pricing are the following: • If the product or the process is specialty in nature, external benchmarks are difficult to find.

If the benchmark must be developed from internal records, it can be unclear as to which time period should be used to form the benchmark.

• Standard cost models in specialized products are highly subject to misrepresentation. Full cost and cost-plus pricing either assume a procedure for auditing total costs, or use the “plus” component of pricing to induce revelation of true production costs. Full cost pricing with audit must still address the issue of valuing capital cost, which requires specification of depreciation schedules or benchmark capital returns, both of which abstract from managerial accountability. The most active area in transfer pricing research is in negotiated pricing mechanisms. The literature suggests a broader range of specific mechanisms and applications for negotiation than cost-based transfers. The apparent advantages of negotiated mechanisms over cost-based pricing cited in the literature are the following: • Greater exchange of information. With cost-based pricing, the flow of information is one

way. Negotiation results in information sharing from both cost and revenue segments of the supply chain

3

• Effort and investment incentives. There appears to be general agreement in the literature that negotiated pricing mechanisms result in better managerial incentives (when managers are compensated on segment earnings) under negotiated mechanisms than under cost-based mechanisms. This is particularly clear on direct comparison between the two (e.g. Baldenius, 2000)

• Simultaneous consideration of external and internal value added. Many of the negotiated pricing mechanisms (particularly the types suggested by Holmstrom and Tirole, and Hart) consider both value added generated in the supply chain and the value added outside the chain (i.e. opportunity costs).

The key disadvantage of negotiated pricing mechanisms is that time is required conducting the negotiation, compared with cost-based mechanisms that require little time to conclude. A major component of the design of negotiated transfer pricing mechanisms is to control the alternative actions and bargaining positions available to buyers and sellers, and thus to influence the time to negotiation. Broad propositions on the application of cost-based versus negotiated transfer pricing mechanisms are difficult to make; however, the following insights emerge from the above discussion: • Cost-based transfer prices tend to be preferred when transfers are mandated, the product is

relatively unique so that related external cash markets do not exist, and when inducing incentives for specialized investment and effort are not particularly important in generating value from the supply chain.

• Negotiated transfer prices tend to be preferred when transfers are not mandated (suppliers and purchasers freely choose to exchange), a cash market for the commodity version of the product exists, and motivating specialized investment and effort is important in generating value from the supply chain.

The literature in agricultural economics on the design of incentive pricing mechanisms indicates the following: • If incentives are presented in a pricing mechanism, and scope exists for a response, a

behavioural response will occur. • It is possible to induce action that can’t be observed through a pricing mechanism if the price

can be tied to a measurable attribute correlated with the unobservable action • Direct monitoring and input specification or supply are substitutes for incentive provisions in

a pricing mechanism • If correlated measures exist to condition a contract, mathematical tools exist to structure the

pricing mechanism that will induce efficient incentives The following observations on pricing mechanisms that induce self-selection and quality signaling are evident: • The design of these pricing mechanisms requires that both pricing and quantity are controlled • The mechanism sorts producers or consumers into “types” in such a way that the lowest

“type” is left indifferent from the exchange; higher types pay a price that is lower their value or receive a price that exceeds cost.

• The most common instrument is tournament pricing

4

• The pricing structure will typically be inequitable Because the design and use of pricing mechanisms are not mutually exclusive, robust conclusions on the application of each type are difficult to make. However, some generalizations can be made based on the literature. If we consider the applications of pricing mechanisms to farm products that have a commodity market variant versus farm products that are completely specialized or unique (no commodity market variant), and food products with specialty attributes versus generic products, we can apply some of the findings from the literature. These are summarized in the table below. • If a commodity farm product is used to produce a generic food product, it is unclear why

alignment in a supply chain is necessary. Here, spot market pricing is appropriate. • Negotiated transfer prices are best suited to the context of a farm product with a commodity

variant used to manufacture a specialty food product. This is because the opportunity cost of participating in the supply chain farmer is obvious (the commodity variant could be accessed by farmer and processor instead), and the realization of value (or generation of premium from supply chain alignment) is heavily influenced by farmer effort or investment

• Cost-based transfer prices are suited to instances of a highly specialized farm product with no commodity variant. Since no commodity variant exists, it is difficult to obtain benchmark costs or standard operating costs, so full cost pricing, or cost plus pricing is appropriate.

• Incentive pricing will find application in any context where producer effort adds value to the Farm Product

End-Use Food Product

Spot Market Pricing

Cost-based Transfer Pricing

Negotiated Transfer Pricing

Incentive Pricing

Self-selection /Quality Signal Pricing

Commodity Specialty • • Commodity Generic • • Commodity Multiple • • • Specialty Specialty • • Specialty Generic • • Specialty Multiple • • •

food product. This can occur with a specialty food product (in which the quality of the farm product is reflected in the specialty nature of the food) or a generic product (in which the quality of the farm product affects the costs of processing). Effort can also influence quantity as well as quality, which influences the value in either a generic or specialty food product.

• Self-selection/quality signal pricing is specifically designed for contexts in which there are multiple end uses, multiple customer types, multiples of quality, or multiple supplier cost structures. Thus, they will find application in contexts where a farm product (commodity variant or specialty) is manufactured into multiple uses (multiple specialty uses, multiple generic uses, or a split between specialty and generic uses) that each have a different end-use associated with them.

5

The key insight emerging from this review, relative to the review in Part I of this study2, is that the majority of transfer pricing mechanisms observed are cost-based, despite the fact that almost all farm products consumed in niche or specialty uses have a commodity variant. For products of this nature, the literature seems clear: there are advantages to using negotiated transfers. This suggests that a re-evaluation of specialty farm product pricing is warranted.

2Mussell, Al, Holly Mayer, Larry Martin, Kevin Grier, and Randy Westgren. Price Discovery Mechanisms and Alternatives for Canadian Agriculture. George Morris Centre, August, 2002.

6

TABLE OF CONTENTS

1.0 Introduction............................................................................................................................ 7 1.1 Objectives ............................................................................................................................ 8 1.2 Approach ............................................................................................................................. 8

2.0 The Transfer Pricing Problem.............................................................................................. 9 2.1 Structure of Transfer Pricing Literature ....................................................................... 10 2.2 Transfer Pricing Overview .............................................................................................. 11 2.3 Transfer Prices as Mechanisms of Co-ordination ......................................................... 15 2.4 Negotiated Transfer Prices .............................................................................................. 16 2.5 Cost-based Transfer Pricing Systems............................................................................. 19 2.6 Observations on Transfer Pricing................................................................................... 22

3.0 Incentive Pricing Mechanisms............................................................................................ 24 3.1 Designing Pricing Mechanisms to Induce Effort or Investment .................................. 24 3.2 Pricing for Unobservable Effort and Investment in Agriculture.................................. 25 3.3 Observations on Incentive Pricing in Agriculture......................................................... 31

4.0 Pricing Mechanisms For Self Selection and Quality Signaling ....................................... 33 4.1 Designing Pricing Mechanisms to Induce Self Selection and Quality Signaling ......... 33 4.2 Pricing for Self Selection and Quality Signaling in Agriculture ................................... 35 4.3 Observations on Pricing For Self Selection and Quality Signaling Agriculture ........ 37

5.0 Observations and Conclusions on Pricing Mechanisms in the Economic Literature ... 39 References.................................................................................................................................... 43

7

Price Discovery Mechanisms and Alternatives for Canadian Agriculture Part II: A Review of Pricing Mechanisms from the Economic Literature

1.0 Introduction Based on the observations of price mechanisms in use in agriculture in Part I of this study, three primary tasks for a pricing mechanism emerge: • Distributing value in an aligned production system for a specialty product to encourage

incentives • Pricing products with value added traits as distinct from their “commodity” counterparts,

based on the additional effort or investment required • Pricing uniform products that have different values in end-use The first issue is the essence of the “transfer pricing” problem; the problem of pricing goods within an aligned supply chain for a specialized product when the final value is only realized at the terminal end. The obvious solution is to compensate each stage of the supply chain at a level proportional to costs; however, if the solution were this simple, it is unclear why the supply chain had to be aligned in the first place. Supply chains are aligned because commodity markets fail to accurately value their activities, or there is some form of cost complementarity between stages, so a system richer than pricing proportional to costs or market prices is generally required. The second issue is a problem of asymmetric information with respect to individual behaviour. A product is exchanged, the quality of which is dependent upon special effort or investment on behalf of the supplier. However, it is difficult or expensive to observe the level of special effort put forward by the supplier at the time of exchange, so the ultimate value of the farm product in processing is uncertain. Consequently, farm product buyers pay less for the product. To correct for this, pricing mechanisms are structured with incentives such that the supplier can do no better than to put in the required level of effort or investment, even though it is not observed. This same logic applies with respect to efforts or investments on behalf of a purchaser that are difficult to observe. The third pricing issue is also a problem of asymmetric information. Consumers of different types have a different values associated with purchases of a farm product. However, it is difficult or expensive for a seller to observe consumers types, and consumers may attempt to misrepresent their types3. As a result, prices will tend to be determined by the consumer type with the lowest willingness to pay from the product, and consumers with higher levels of value pay less for the product then are willing to. The consequence is that suppliers cannot recover the full value of the product they sell. To correct for this, the pricing mechanism is structured so that consumers can do no better than to reveal their true type, and that higher prices are charged to consumers that have a higher value for the product.

3 As discussed below, the symmetric problem results when it is difficult or expensive for buyers to differentiate between product quality attributes, and sellers can misrepresent the quality of their products

8

1.1 Objectives The purpose of this phase of the study is to review and evaluate the literature in economics relevant to the pricing in supply chains. The objectives are: • To review the relevant economic literature related to transfer pricing • To review the literature on the provision of incentives for effort and investment • To review the relevant economic literature related to signalling product attributes and

consumer types through the pricing system • To evaluate and consider applications of this literature in the context of pricing agricultural

and food products

1.2 Approach We start by considering the literature in transfer pricing. The specific nature of the transfer pricing problem is introduced, followed by a review of solutions to the problem proposed in the literature. This ranges from the organization of supply chains to specific mechanisms that solve the transfer pricing problem. Second, we review conceptual literature related to asymmetric information and signalling product quality. Next, we review the literature that applies pricing to self select buyer types and product quality. The significance of these approaches to pricing are determined, and related back to the real-world examples observed earlier. Finally the application of specific pricing mechanisms for farm and food products is evaluated. To review the research findings, the following literature search procedure is used. • The refereed journal articles written since 1988 on transfer prices that are available in the

University of Guelph, University of Waterloo, or Wilfrid Laurier University libraries are reviewed. For articles that of greater significance, material from before 1988 is reviewed. This broad search is necessary, because little research on transfer pricing has been conducted in agriculture and food.

• Papers and journal articles in the agricultural economics literature from the same period related to incentive pricing and self-selection/quality signalling are reviewed. This is appropriate because reviews of the pure economics literature already exist, and there is a growing literature applied to agriculture and food on this topic.

9

2.0 The Transfer Pricing Problem The basic transfer pricing problem is to allocate supply chain profits across segments; it can be complex because one segment’s revenue (price) constitutes the next segment’s cost. However, managers of supply chain segments receive their compensation according segment earnings, and the managers of the various segments of the chain behave strategically. Thus, allocating supply chain profit differs from allocating costs (Emmanuel and Mehafdi). The theoretical origins of transfer pricing economics stem from general equilibrium theory. General equilibrium theory relates the workings of the price system to the desirability of its outcomes. Among the significant accomplishments of this branch of economics was to rigorously prove that a market economy can give desirable social outcomes. Among these desirable outcomes is Pareto Optimality. An allocation of goods is Pareto Optimal if, as a result of the allocation, someone is made better off and no one is made worse off. The first fundamental theorem of welfare economics states that, given a particular set of “well behaved” individual preferences, using the market as a means of social allocation always produces a Pareto Optimal allocation. Related to this, a second result is that, for any specific Pareto Optimal allocation desired, there exists a set of prices capable of obtaining this allocation if lump sum transfers are allowed. Thus, the price system is capable of co-ordinating desirable allocations. The notion of transfer pricing in a supply chain for a specialized product derives from this second theorem in welfare economics. Initially, the desirable allocation for all of the segments of the supply chain may be known by the co-ordinator; the problem is to structure a transfer pricing system that will implement this allocation. Subsequently, as the supply chain develops, the transfer pricing system must give incentives for adjustment and transfer of information that will maximize the value of the end product. The problem is to find a set of prices that will induce the independent segments of the supply chain to pursue their own self interests, but produce the correct quality and quantity of product to maximize the value of the final product. Put in this way, it is clear that transfer prices do two things: • Induce an efficient allocation of intermediate products within the supply chain • Distribute the value generated by the supply chains across its segments. The transfer pricing literature is dominated by reference to the multi-divisional firm. That is, the company has (for example) a manufacturing division and an assembly division. The manufacturing division supplies the assembly division along with (possibly) other customers; the assembly division purchases from the manufacturing division and possibly from outside suppliers. The decisions related to intermediate good quantities and whether to sell/buy within the company are made by divisional managers. Each of the divisions are rewarded based on their individual earnings performance; the earnings of the company as a whole depend upon the sum of earnings in the divisions. The problem is to get the manufacturing and assembly divisions to maximize the earnings of the firm as a whole, even though they are only rewarded based on divisional performance, and (to a certain extent) increasing earnings on behalf of one division lowers the earnings of the other. The supply chain for a specialty food product differs from the multi-divisional firm in the sense

10

that each of the “divisions” may be separately owned businesses. However, there are many similarities. In both cases, the production of intermediate products is aligned for a specific end use; the revenue from this end use is realized from a specific division (or segment of the chain). In both cases, decision making is decentralized, and there may be alternatives for exchanges outside the aligned system. In both cases, the earnings of the aligned system as a whole are dependent upon the decentralized decisions made by segments or divisions that are rewarded based on individual performance. Thus, the only differences between the agri-food context and the multi-divisional firm in other sectors in terms of transfer pricing is the ownership of assets, and that multi-divisional firms have executives (or “co-ordinators”) that can influence divisional managers using instruments other than price. The problem of co-ordinating individual decisions to maximize the earnings of the whole is essentially the same. On this basis, we draw on the transfer pricing literature from the multi-divisional firm to make inferences about farm-food supply chains. The key difference in the food supply chain context is that the “co-ordinator” is typically one of the supply chain participants itself. This is in contrast to the abstraction of the “central planner” in general equilibrium theory or the head office in the multi-divisional firm. The significance of this difference is not immediately clear. However, some of the supply chains and price mechanisms in agriculture and food reviewed earlier emulate the multi-divisional firm. For example, in the Natreon canola case, Dow Agro Sciences effectively acts as co-ordinator. Dow supplies the seed and agronomic assistance, farmers grow the specialty canola, and designated elevators receive it and store it in an identity preserved system, and finally Dow purchases the canola. This case is the exception rather than the rule; it is not obvious what (if any) difference there is between a supply chain co-ordinated by a head office and a supply chain co-ordinated by one of its participants.

2.1 Structure of Transfer Pricing Literature A literature search was conducted for scholarly papers published since 1990 under the search criteria of “transfer pricing”. Widely cited papers published prior to this time period were also reviewed. Papers that focused on the international taxation aspects of transfer prices were ignored. The literature search found the literature on transfer pricing to be diverse. Contributors include economists, business school theorists, and accounting researchers. These schools of thought bring a variety of approaches. The various approaches are not mutually exclusive, but are grouped into the following structure: • Firm-level and case-study analyses that provide an overview of alternative transfer price

schemes • Economic studies that focus on mechanisms of co-ordinating the optimal output of supply

chains • Studies that focus on negotiated transfer pricing mechanisms • Studies that focus on cost-based transfer pricing mechanisms In the sections that follow, each these are discussed and analyzed. In section 2.6, the transfer pricing literature is drawn together and assessed.

11

2.2 Transfer Pricing Overview A thorough contribution to the firm-level analysis of transfer pricing was made by Emmanuel and Mehafdi (1994). Their book, which surveys a significant portion of the transfer pricing literature, succinctly lays out the difficulties associated with establishing transfer prices. Transfer pricing inherently involves allocating the profits of an aligned supply chain; allocating profits differs from allocating costs, because profit allocations have strategic consequences when segments of the supply chain are compensated in relation to the profit of the segment. Emmanuel and Mehafdi suggest that there is no difference between allocation of costs and profits in a supply chain if: (1) all segments in the supply chain have only the supply chain as a revenue source, (2) supply chain transfer are mandated (exchanges must occur), and (3) revenue opportunities outside the aligned supply chain are constrained by the specialization of productive assets. However, these are clearly limiting cases for an agri-food supply chain. In particular, mandated transfers are unlikely unless the transfers occur within divisions of a multi-division firm, or if government regulation imposes mandated transfer. Six approaches to transfer pricing are presented. They are: • Transfer price based on standard cost product cost • Transfer price based on marginal cost • Transfer price based on full production cost, or cost-plus • Transfer price based on market price • Transfer price based on shadow values from a mathematical programming model • Transfer price negotiated based on opportunity costs Emmanuel and Mehafdi find that each of these have difficulties associated with them, and provide the following assessment: • Standard product costs are difficult and expensive to implement for specialized intermediate

goods, because a direct external reference is not available. If internal records must be used to establish the benchmark for standard costing, it is unclear what period should be used to establish the benchmark. Alternatively, if a similar product from an external source is used, it is unclear how it should be adapted to value the internal product. Finally, if the benchmark is constantly tightened, supplier segments may have a reduced incentive to invest in improved facilities.

• Marginal cost pricing follows from basic microeconomics. In practice, however, marginal cost pricing is very information intensive. It requires the supplying segment to determine and report its incremental costs at various levels of output, which may be difficult for it to calculate. Because it is relatively complex, even if the supplier can calculate its marginal cost, there is a significant opportunity to “pad” costs to increase the price it receives. Because increases in marginal costs translate immediately into additional revenue for the supplying segment, suppliers have a strong incentive to misrepresent marginal costs.

• Transferring product at full cost alleviates some of the above problems. The problem of accurately measuring opportunity costs is partly addressed by including overhead costs as a proxy for opportunity cost. It avoids the issue of a benchmark cost, and in practice the problem of strategic manipulation of costs are not significant. However, the use of accounting performance measures as part of full-cost pricing presents difficulties, because it abstracts from the use of transfer pricing as a means to motivate management by focusing on

12

short term outcomes rather than managerial effort. • Variations on full-cost transfer pricing are cost-plus pricing and pricing based on activity-

based costing. The markup portion of the cost-plus transfer price can be left to negotiation, which generates greater information sharing with few distortions due to strategic behaviour.

• Transferring product based on market prices can be a good measure of opportunity costs. However, the case must be made that the market prices are generated in a perfectly competitive market. More importantly, there must be reference prices available from the market that are relevant to the product transferred in the supply chain. Finally, there are problems with reference prices when the “buy” price and the “sell” price in the market differ- that is, how should the basis be allocated?

• The shadow prices on constraints in mathematical programming models of supply chains give the implicit (marginal) value of activities and transferred products within the immediate range of optimal supply chain output. However, the difficulty with this approach is the high level of information centralization that is required to construct the model. Also, the “optimal” solution need not mimic actual transfers that occur in the supply chain.

• Negotiation based on opportunity costs applies the “fair and neutral procedure”. It combines a standard cost approach with a means of allocating earnings in the buying segment back to selling segments. The transfer price is standard cost plus a share of the selling segment’s gross margin. Given an agreed-upon standard cost formula, the buying and selling segments estimate the level of costs in the supply segment and the output price that will be received by the buying segment; this gives the initial range of the transfer price. This initial transfer price range is used to induce the segment to trade internally (rather than use external markets). The realization of standard costs and output prices at the end of the period defines the actual transfer price for the period. Emmanuel and Mehafdi show that additional measures can be adopted that place a floor or ceiling on the eventual transfer price.

Emmanuel and Mehafdi identify 3 basic scenarios to which transfer pricing is applied: • No external market for the product exists

If no external market for the product exists, then an externally verifiable benchmark price does not exist. This means that full-cost or cost-plus type transfer prices are the most effective. However, this mechanism will introduce distortions if the supplying segment has excess capacity, and presents the potential that inefficiencies will be passed on in the costs. Among the challenges with this transfer pricing context is that it is a bilateral monopoly; no external information can be accessed to mediate conflicts.

• An external market exists, but supply chain segments do not have access to it

With an external market, external reference prices exist that can be used in transfer pricing. However, care must be taken to ensure that the market is not imperfect, and that any required adjustments for product quality between the reference and supply chain products are made. Where external prices exist, the market prices themselves or full-cost or cost-plus based transfer prices can be used. In either case, the additional information introduced from the market reference reduces conflict, even if the external market cannot be accessed.

• An external market exists, and supply chain segments have authority to access it

13

This is similar to the previous scenario, with the difference that the external market can be accessed, rejecting the supply chain. Thus, the market price serves as more than a reference. The threat of exit from the supply chain of either selling or buying segments gives it a natural incentive to work together. Either market-based prices or full-cost/cost-plus arrangements are observed.

Eccles and White (1988) examined transfer pricing policies in 13 manufacturing firms, mostly in the industrial chemicals industry. They identified 3 transfer pricing contexts similar to Emmanuel and Mehafdi: • Mandated full-cost transfer pricing

Under mandated full-cost pricing, buying and selling segments are barred from accessing the outside market, so buyers are unable to substitute product from lower cost sellers outside the aligned chain, and sellers cannot access higher priced markets outside the chain. Eccles and White cite a number of transfer pricing problems with this scenario. Selling segments can pass on high costs and inefficiency. If full cost is less than the market price, buying segments will consume more product and selling segments will be at peak capacity but earn lower profits that rival sellers; similarly, if full cost is higher than price, buying segments will consume less and the selling segment will operate below capacity.

Eccles and White also document a number of problems with the standard cost approach to transfer pricing. Full cost is the sum of the standard cost (estimated by time-motion studies and ingredient costs) and variance (deviation between actual and standard cost). Variances are difficult to allocate between selling segment and buying segment. Buyers can justifiably claim that selling segments must meet standard cost and that variances are not there responsibility. However, not allocating variances is also a problem because they can be caused by the buyer. In addition, they find that standard costs and variances are highly subject to strategic manipulation on behalf of selling divisions. As a result, mandated full-cost transfer pricing usually results in conflict between segments. This conflict can be beneficial, because it results in more bilateral monitoring and information sharing. • Mandated market-based transfer pricing

Under mandated market-based transfer pricing, buying and selling segments are prevented from accessing the outside spot market, but the prices discovered in that market are used as transfer prices. Eccles and White document the challenges of this approach. In specialty products, it can be difficult to find a comparable market price. Even where one exists, getting buying and selling divisions to agree on which market price to use can be difficult. In some cases, the price of the selling segment has received from external customers is used. In other cases, the purchasing segment produces price results from previous tender bids. In either case, there is significant potential for strategic behaviour. In the first case, the selling segment can manipulate its price quotes by selecting particular prices that include hidden premiums and surcharges; the opposite incentive is observed in the latter case, with the purchaser having the incentive to quote offers that include discounts and deductions. Market-based products can also have the effect of

14

discriminating against intermediate products that have a low yield in the manufacture of the specialty products. Where this is the case, because the transfer is mandated, the purchasing segment has an incentive to adjust by decreasing the volume it purchases. The result is a suboptimization of the supply chain as a whole • Exchange autonomy

Exchange autonomy means that the authority to trade (or not trade) resides with the segments of the chain, as does the authority to establish transfer prices. Eccles and White cite 3 common transfer pricing conventions that are applied under exchange autonomy: market-based pricing, competitive bidding, and cost-based pricing. When market-based transfer prices are used, the commodity reference price is first selected, and then the identity of the segments that will sell and buy at that price are determined. If a competitive bidding process is the source of the transfer price, the transfer price and the identity of the parties to the transaction are simultaneously determined. Examples of the bidding process described by Eccles and White include sealed-bid auctions, open bid auctions, and open negotiation. Under cost-based pricing, a formula related to production costs is used as the transfer price.

Cost-plus as a basis for transfer pricing derives from the concept of allocating a portion of the gross margin from the purchasing segment to the selling segment. The difficulty lies in determining a satisfactory proxy for the allocation of gross margin. Five bases for cost-plus arrangements are described: 1. Variable cost plus profit share on sale of final good 2. Variable cost plus a fixed percentage 3. Variable cost plus a fixed mark up that gives the selling segment the same gross margin that

it would have received from an alternative product 4. Variable cost plus a fixed mark up that gives the selling segment the same gross margin as

other segments of the chain 5. Variable cost plus a fixed mark up that gives the selling segment the same return on

investment as other segments of the chain Colbert and Spicer approached transfer pricing from the perspective of transactions costs. Transactions cost theory argues that the greater the level of uniqueness in the product and the assets used, the greater the incentive for vertical integration of activities. Within the supply chain, the analogy is that the greater the level of uniqueness in the product and assets, the greater the incidence of mandated transfers. The structure of transfer pricing also relates to strategic sourcing risks. These include appropriation risk- the risk that the buying (or selling) segments strategic advantage (low cost, focus, or differentiation) is threatened by a supplying (or buying) segment, and diffusion risk- the risk that information related by to one segment’s strategy will be leaked to competitors by another segment.

Colbert and Spicer tested these theoretical transfer pricing concepts using case studies of 4 US electronics manufacturers. The results of their analysis showed that • As the level of uniqueness in the assets used by the selling segment increases, the incidence

of mandated transfers increases • The greater the degree of uniqueness in the assets used by the selling segment, the greater

15

the weight placed on manufacturing costs in the transfer price Thus, the results of the analysis support the transactions costs theory of transfer pricing.

2.3 Transfer Prices as Mechanisms of Co-ordination In a foundational paper on transfer pricing, Ronen (1974) proposed a transfer pricing mechanism that purported to mitigate the divergence in interests between segments and the supply chain as a whole. Ronen laid out the following necessary functions for a transfer pricing mechanism: • Must be transparent so the a co-ordinator can evaluate the performance of supply chain

segments • Must motivate segments to pursue self-interest in a way that is consistent with supply chain

objectives • Must increase the efficiency of supply chain segments while delegating control The system proposed by Ronen to implement these functions is the following. Assume that there is a supplying segment of the chain, a consuming division of the chain, and a co-ordinator (for example, a central office) that provides oversight. The mechanism works in the following way: • The supplying segment presents to the co-ordinator a schedule of quantities and transfer

prices at which it would willing supply product • Based on this schedule, the co-ordinator computes the supply segment’s average cost

schedule and presents it as offers to the consuming division. The consuming division responds with a schedule of volumes it would purchase at the various average cost prices. This response from consuming segment reveals its margin between the final output price and its costs of production other than the price of the good transferred in the supply chain

• From the consuming segment’s bids, the co-ordinator computes the average revenue from sales of the transferred good, which is presented back to the supplying segment

• The supplying segment will choose output by optimizing incremental cost and revenue given the average revenue; similarly, the consuming segment will choose input levels by optimizing incremental product cost and output revenue given the average product cost.

• The consuming segment is charged a transfer price equal to the average cost of the supplying segment, and the supplying segment is paid the average revenue of the consuming segment. Any difference between the two is made up by the co-ordinator.

Ronen argued that under this system, the optimal output of the supplying segment will just equal the optimal input of the consuming segment so supply chain profit is maximized, and that neither supplying nor consuming segment has an incentive to misrepresent its schedule of bids and offers. In later work, this mechanism was extended to deal with transfer pricing when production costs and product revenues are uncertain (Ronen and Balachandran, 1988). However, this mechanism has some clear difficulties. It requires a significant amount of information from both buyers and sellers; in this respect it may be too cumbersome to be practical. It is also unclear how the co-ordinator is financed, and how expensive the co-ordination might be. In addition, it isn’t clear that neither party has an incentive to misrepresent bids and offers. Groves and Loeb (1976) found plausible conditions in Ronen’s transfer pricing

16

scheme in which the supplying and consuming segments would not accurately represent bids and offers, with sharply negative results for supply chain profits. Groves and Loeb proposed an alternative mechanism in which the co-ordinator imposes decisions related to supplying segment output and consuming division input based on bids and offer from the supplying and consuming segments. The co-ordinator in this scheme is financed by taxes levied on supplying and consuming divisions. Given these refinements, Groves and Loeb show that • Neither party has an incentive to misrepresent bids and offers • The co-ordinator operates at a zero cost • Supply chain profits are maximized. In response to Groves and Loeb, Ronen (1992) developed a modified transfer pricing scheme that maintains the decision autonomy of supply chain segments (as in Ronen (1974)) but prevents the misrepresentation of bids and offers through a more rigorous audit of segment costs and revenues.

2.4 Negotiated Transfer Prices Holmstrom and Tirole (1991) considered transfer pricing for a specialty product under alternative firm or supply chain organizational forms. They treat the problem of transfer pricing and organization together, since the degree to which segments can trade outside the supply chain affects the pricing mechanism (as suggested above). Four firm/supply chain structures are considered: • a system in which the supply chain is co-ordinated by a central office, but segments have

liberty to negotiate transfer prices and exchange outside the supply chain • a system in which the supply chain is co-ordinated by a central office, transfers between

segments are mandated but transfer prices are negotiated by segments • a system in which the supply chain is co-ordinated by a central office, transfers between

segments are mandated with set transfer prices (full-cost based, no negotiation) • A system with no co-ordinator or alignment in the supply chain and freely negotiated transfer

prices. Under the first structure, since alternatives outside the chain are relevant to the segments, the transfer price that is negotiated will depend on both the value added within the chain and the value that would have been added if external transactions were pursued by the buying and selling segments. Holmstrom and Tirole show that negotiation will lead to a transfer price to equal to one-half the difference between the value added within the chain and the value added under external transfers. Under the second structure external value added is irrelevant, so negotiation leads to a transfer price that allocates half the value added from transfers within the chain to each party. Under the third alternative, the transfer price is full cost. Under a system with no co-ordinator, the negotiated price is identical to the first scenario with co-ordinated system with the potential for external exchange and negotiation. Thus, provided the supply chain for the specialty product generates higher value added than external alternatives (which it should), the transfer price will be highest under either the first or fourth structure, followed by the second, then the third.

17

Hart (1995) explored similar transfer pricing issues as Holmstrom and Tirole, focusing on the co-ordinated chain with negotiated transfer prices and the option and trading outside the specialty supply chain. His results show a similar structure for transfer prices. Hart’s analysis implies that, under the above transfer pricing scheme: • The internal transfer price for the specialty product increases proportionally with the price of

its commodity counterpart in the external market • The internal transfer price for the specialty product increases proportionally with the

production cost of the specialty product • The internal transfer price for the specialty product increases proportionally with the revenue

realized by the purchasing segment of the chain • The internal transfer price for the specialty product decreases proportionally when the

production cost of its commodity counterpart in the external market increases • The internal transfer price for the specialty product decreases proportionally when the

revenue realized from its commodity counterpart in the external market increases

Edlin and Reichelstein (1995) investigated the impact of negotiated transfer prices on incentives to make investment specific to a specialty product supply chain. The context is such that specific investment by the supplying segment reduces costs for transfers within the chain, but has no impact on costs for products sold by the supplying segment outside the chain. This context presents an obvious disincentive for the supplying segment to invest, since the buying segment can take advantage of it in transfer price negotiation. Because of this, it is common for the supply chain co-ordinator to impose an administered transfer pricing rule, such as standard cost.

However, in a simplified model in which supplying and purchasing segments observe the same information but find it expensive to verify information about each other, Edlin and Reichelstein show that negotiated transfer pricing gives an efficient investment incentive that is an improvement over an administered transfer pricing rule. In their model of the supply chain, the supplier and purchaser establish transfer prices and quantities to trade in an initial period, then make investment decisions. In a later period, the conditions characterizing costs and benefits are observed, and the two parties bargain over the transfer price, using the initial transfer price as the status quo point. Under these conditions, bargaining over the transfer price gives investment incentives if profits in each of the segments are accounted for separately, and the managers of the segments are compensated in a linear relationship to segment profits. Transfer pricing in a Dutch hog-pork supply chain was investigated by den Ouden (1996). The purpose of the study was to analyze the distribution of costs and benefits and the interstage relations in a Dutch pork supply chain. A related objective was to determine if the chain as a whole would suboptimize under transfer pricing schemes based on results at the individual stage level. The stages (or activities) delineated were farrowing, fattening, transportation, and slaughtering. Transfer prices were fixed using market averages. The scale at which each stage operated was based on the assumed management capacity of 1 full-time equivalent person. The capacity of the slaughtering stage was set at 400 hogs/hour. The results showed that the production costs of the supply chain were unevenly distributed with farrowing accounting for 34% of costs, fattening 53%, and slaughtering 13%. Extensive sensitivity analyses were done to test how changes in certain stages affected the pork supply

18

chain. The supply chain was sensitive to changes in pork and hog prices and to stocking rates in transportation. A scenario was explored in which the farrowing stage forward integrated into fattening. This increased farrowing and fattening stage profits, but reduced profits in slaughtering. Other changes in individual stages did not affect the profitability of other stages. The conclusion was that transfer pricing schemes between stages are important in generating correct incentives for integration and consolidation, and that transfer prices can be used to disproportionately distribute supply chain profits and induce investment incentives. Vaysman (1998) investigated the theoretical basis for negotiated transfer prices. He demonstrated that if segment managers are compensated at a linear function of segment earnings and the co-ordinator has imperfect information on segment costs and revenues, negotiated transfer prices are capable of implementing efficient incentives. In a structure such that the co-ordinator specifies a transfer pricing rule and allows segment managers to negotiate the specific transfer price using the prescribed rule, the supply chain achieves its efficient profit and transfer price disputes requiring co-ordinator intervention never occur.

Cheng (2002) has proposed a transfer pricing approach based on option theory to induce efficient incentives in the segment of a supply chain. Described as the Renegotiate Any Time (RAT) transfer pricing system, it is designed to price internal transfers for which a representative external market price does not exist. The purpose of RAT is to induce supply chain segments to price intermediate products at marginal cost. Setting transfer prices equal to marginal costs directly is difficult, because there is an incentive to misrepresent costs and pass on inefficiencies. At the same time, marginal cost transfer prices are optimal because they maximize the profit of the supply chain as a whole. RAT works in the following way. The supplying segment proposes a transfer price t1. The purchasing division proposes another (presumably lower) price t2, which is the equivalent of an option strike price. The purchasing segment can purchase at t2 if it wishes, in return for a premium, p, paid to the selling segment. The buying and selling segments negotiate over the strike price and the premium. If πS is the profit of the selling segment and πB is the profit of the buying segment: • The minimum premium the selling segment will accept to transfer price at t2 is Minimum p = πS(t1) - πS(t2) • The maximum premium the purchasing segment will pay to transfer price at t2 is Maximum p = πB(t2) – πB(t1) • If the maximum premium the purchaser would pay exceeds the minimum the purchaser will

accept, there exists an option contract that will make both parties better off. The actual premium that is negotiated will lie between the above maximum and minimum.

• The negotiated transfer price is paid on delivery, while the premium is paid at the end of the period over which the option is fixed. This allows the segments to renegotiate the premium as cost and revenue conditions change during the period of the contract.

Cheng shows that this negotiation over both the strike price t2 and the premium leads to a transfer price closer to the true marginal cost than could otherwise be attained, and that it establishes a flexible process in which the transfer price will converge toward marginal cost.

19

Wielenberg (2000) proposes an alternative approach to motivate investment in a supply chain for a specialty product using a negotiated transfer price. He notes that if the demand for the final product is uncertain and the investment undertaken by the supplying segment is unobservable, the supplying segment will either underinvest in technology or produce at an inefficiently low capacity. This occurs with a transfer price in which price and quantity are fixed. He proposes a pricing mechanism in which the purchaser commits to buy a minimum volume. Quantities over this minimum, and the transfer price are freely negotiated. Wielenberg shows that fixing the minimum quantity is sufficient to induce efficient investment in technology on behalf of the supplier, and that the price negotiation after the final volume has been set induces the efficient capacity choice. Ghosh (2000) considered negotiated transfer prices as determined by the complementary (mutually reinforcing nature) of managerial compensation and external transfers in a supply chain. The notion is that segments of the supply chain that have managerial compensation and policies on trade outside of the supply chain that are in congruence with one another experience less conflict in negotiation. Segments that only trade internally and have a compensation based on supply chain profits are complementary, because the exchange policy and compensation induce co-operation; segments that can trade externally and compensated based on segment profits are also complementary because the exchange policy and compensation induces competition. Ghosh tests 4 hypotheses related to this: • Negotiated transfer prices are perceived as more fair when compensation packages and

external trade policies are the same for the supplying and purchasing segment • There will be less conflict in transfer prices negotiation if compensation packages and

external trade policies are the same for the supplying and purchasing segment • Supply chains with complementary compensation and exchange policies that induce

competition between segments are more profitable than others. • When both supplying and purchasing segments have the same form of complimentary

exchange and compensation packages, less time spent negotiating transfer prices. Ghosh tested these hypotheses experimentally, with subjects assuming the role of seller or purchaser. Statistical analysis of the results supported (i.e. failed to reject) the 4 hypotheses.

2.5 Cost-based Transfer Pricing Systems

Vaysman (1996) analyzed the theory behind cost-based transfer pricing. He found no basis in reality for marginal cost-based transfer prices suggested by economists, despite the fact that transfers at marginal cost yield efficient incentives. Instead, the co-ordinator of the supply chain invariably lacks some of the information possessed by the chain segments. Transfer prices are used as a means to delegate authority for the co-ordinator to the segments. However, this delegation results in some loss of control on behalf of the co-ordinator; the balance between the flexibility gained through delegation relative to the loss of control determines the structure of the transfer price. The detailed analysis of cost-based transfer prices shows that cost-plus transfer prices arise as a result of incomplete or expensive communication between the segments and the co-ordinator. In this context, the markup above incremental cost in the transfer price can be interpreted as the payment required to induce revelation of the true incremental cost on behalf of

20

the supplying segment. Lehman and Weisman (1996) examined pricing in telephone networks. The challenge in telephone networks is that local phone companies originate long-distance phone calls that require a larger network for connectivity. Some means is required for local phone companies and other firms in the network to share revenues from long-distance calls. Typically, revenue sharing from long-distance calls is facilitated by pooling. Pooling is characterized by the following relationship: Net revenue pool = sum of revenues reported by members of the pool, less operating costs reported by members of the pool Members of the pool obtain earnings from their individual share of pool revenue less actual operating costs. Pool net revenue is distributed among member telephone companies according to a firm’s share of calls generated in the pool, the firm’s relative investment cost, or based on a fixed share. Regardless of the mechanism used to allocate pool revenue, Lehman and Weisman find that pools provide good incentives to promote the demand for long distance calls. However, regardless of the allocation rule, pool participants can have an incentive to overstate their operating costs for the purposes of pooling, thereby increasing their private profit and decreasing the net revenue in the pool. This is prevalent if there are private benefits associated with expenditures above the minimum operating cost. Lehman and Weisman propose the following solutions to this problem: • Compensation of individual pool members’ operating costs based on a benchmark of

reported operating costs of other members. Under this approach, in the allocation of pool revenue, an individual telephone company would be compensated according to the weighted average of all other members’ costs. This removes the incentive to overstate costs in reporting, and provides the incentive to beat the average cost.

• Compensation of individual pool members’ operating costs based on historical costs, with adjustments for price changes and technological improvements. This approach removes the incentives for firms to pad reported costs, as the above approach. A disadvantage of this design is that it tends to reward inefficient pool members that have historically high costs, at the expense of firms that have a long history of cost efficiency.

• Compensation to individual pool members based on a fixed share of pool net revenue. If the pool is sufficiently large that an individual firm’s reported costs do not significantly alter the net revenue in the pool, there is no impact on cost reporting incentives of fixing the payment share.

• Transfer pricing arrangements between local telephone networks can be used in lieu of the pooling scheme. Under this arrangement, the telephone network that originates long distance phone calls pays the network that completes the connection according to a prescribed schedule. Lehman and Weisman find many forms of alternative access charges (transfer pricing arrangements), but typically they involve the reported costs of initiating and terminating phone companies. As a result, they suffer from incentives to misreport costs and poor incentives to reduce cost. The primary benefit of the access charges relative to pooling is administrative simplicity and a reduction in pool abuse (private costs assessed to the pool).

21

Baldenius, Richelstein and Sahay (1999) extended Vaysman’s analysis to investigate the effectiveness of alternative transfer pricing mechanisms in contexts where comprehensive contracts are difficult or expensive to enforce. This contractual incompleteness arises when specialized investments are made to produce a unique product with limited value outside an aligned supply chain. Transfer prices are used to create incentives for relationship-specific investments by segments of the supply chain, and to enhance transfers of specialized intermediate goods.

In their study, Baldenius et al investigated transfer prices based on standard cost parameters and negotiated transfer prices. They consider a simplified supply chain with a supplying segment and a consuming segment. Each segment must make investment decisions (in assets, equipment, human resources, etc,) in the current period in anticipation of future costs and revenues that are uncertain. Investment by the supplying segment decreases cost, and investment by the consuming segment increase revenues. In their model, investment decisions are made in an initial period, then the conditions characterizing later transfers are observed (e.g. crop conditions), then the transfer price rule is applied and the product transfer occurs, and finally the true cost of the supplying segment is realized.

In this theoretical framework, Baldenius et al observe the following: • Negotiated transfer prices result in under investment in relationship-specific assets. This is

because each segment only receives a portion of the benefits from its investment. • Transfer prices that are based on a standard cost model have the problem that the selling

segment can exaggerate costs, and the buying segment can understate revenue. • If only the selling segment makes a dedicated investment, then if a standard-cost pricing

approach is used the transfer price will tend to be too high and the volume traded too low relative to an efficient level. Under this scenario, the selling segment holds a monopoly over the buying segment. The inefficiency of this monopoly outweighs any stemming benefit to the selling segment from having a captive market for its output. Thus, negotiation is preferred to standard cost transfers.

• If only the buying segment invests in specialized facilities, the supplying segment has every incentive to exaggerate its cost, and the buying segment will reduce its purchases. Consequently, negotiation is preferred to standard cost transfers.

• The only scenario in which standard cost models are preferred to negotiated transfer prices is when the seller has very little scope to exaggerate prices (such as when there are third party cost audits).

Baldenius (2000) generalizes these insights. Under standard-cost transfer pricing, the transfer price only reflects information supplied by the selling segment; negotiated transfer prices involve information supplied both buyer and seller. As a result, there are relatively few scenarios under which the standard-cost model of transfer pricing provides better incentives than negotiation. The exception to this occurs when only the selling segment makes specialized investments, and the seller is knowledgeable about the revenue stream realized by the buying segment. In such cases, little additional knowledge results from information introduced by the buyer in negotiation, and standard-cost transfers provide more efficient incentives.

22

2.6 Observations on Transfer Pricing The transfer pricing problem in a supply chain initially appears quite transparent- the upstream stage’s revenue is the downstream stage’s cost, which creates a natural conflict. At the same time, the very reason that a supply chain is aligned is so that its segments will work cooperatively to maximize the earnings of the chain as a whole, so a contradiction exists. But in fact, the transfer pricing problem is not as transparent as this. As discussed above, it involves complications in the pricing function related to accessing external markets, whether a related external market exists, and whether there is an incentive for segments to misrepresent costs and revenues. A variety of solutions are proposed, analyzed, and criticized above. Based on the literature review, there appears to be some agreement on the following propositions: • For true commodity products moved through an aligned supply chain, the external cash

market provides a good indication of opportunity costs to internal buyers and sellers. Thus, external cash prices can be used as transfer prices.

• Marginal cost pricing as a form of transfer price is essentially an academic concept. The large amount of information required to calculate marginal cost, and the general need to have a menu of marginal cost across volumes and capacity usage renders it impractical.

• Shadow prices from linear programming models of the supply chain have information requirements at least as onerous as marginal cost. Indeed, if mathematical programs could really be used to allocate inputs and outputs in the supply chain, it is unclear what advantage there is of delegation to multiple segments in the first place.

This leaves negotiated and cost-based transfers as the remaining candidates for transfer prices in contexts where the product transferred is not a commodity. The desirability of cost-based vs. negotiated prices is influenced by the nature of compensation and specialized investment in the supply chain. In a farm-food supply chain, some observations can be made on compensation and investment. • Farms are commonly sole proprietorships, so farm managers (as firm owners) are effectively

compensated based on farm profits, rather than in some proportion to the overall earnings of the supply chain. Compensation proportional to supply chain profits probably only exists in niche or very specialized food products.

• Investments made by farmers that are dedicated to a specific use are the exception rather than the rule. However, this is changing. It becoming more common to observe farm investments catered to a particular market, but can be reallocated into the production of commodity product at some loss or expense. Livestock and perennial crop genetics, along with some types of equipment and buildings are examples.

• In specialty farm products, transfers are almost always mandated (via some form of contract between a farmer and processor) in the short term. In the longer term, transfers are almost never mandated, so farm product buyers and sellers have choice.

A variety of pricing mechanisms related to costs are found in the literature. The most commonly discussed is the standard cost model. The criticisms of standard costs as a basis for pricing are the following: • If the product or the process is specialty in nature, external benchmarks are difficult to find.

23

If the benchmark must be developed from internal records, it can be unclear as to which time period should be used to form the benchmark.

• Standard cost models in specialized products are highly subject to misrepresentation. Baldenius et al suggest that standard cost models will only be effective when they are backed up by audit procedures, which presumably adds expense.

Full cost and cost-plus pricing either assume a procedure for auditing total costs, or use the “plus” component of pricing to induce revelation of true production costs. Full cost pricing with audit must still address the issue of valuing capital cost, which requires specification of depreciation schedules or benchmark capital returns, both of which abstract from managerial accountability. The most active area in transfer pricing research is in negotiated pricing mechanisms. The literature suggests a broader range of specific mechanisms and applications for negotiation than cost-based transfers. The apparent advantages of negotiated mechanisms over cost-based pricing cited in the literature are the following: • Greater exchange of information. With cost-based pricing, the flow of information is one

way. Negotiation results in information sharing from both cost and revenue segments of the supply chain

• Effort and investment incentives. There appears to be general agreement in the literature that negotiated pricing mechanisms result in better managerial incentives (when managers are compensated on segment earnings) under negotiated mechanisms than under cost-based mechanisms. This is particularly clear on direct comparison between the two (e.g. Baldenius, 2000)

• Simultaneous consideration of external and internal value added. Many of the negotiated pricing mechanisms (particularly the types suggested by Holmstrom and Tirole, and Hart) consider both value added generated in the supply chain and the value added outside the chain (i.e. opportunity costs).

The key disadvantage of negotiated pricing mechanisms is that time is required conducting the negotiation, compared with cost-based mechanisms that require little time to conclude. A major component of the design of negotiated transfer pricing mechanisms is to control the alternative actions and bargaining positions available to buyers and sellers, and thus to influence the time to negotiation. Broad propositions on the application of cost-based versus negotiated transfer pricing mechanisms are difficult to make; however, the following insights emerge from the above discussion: • Cost-based transfer prices tend to be preferred when transfers are mandated, the product is

relatively unique so that related external cash markets do not exist, and when inducing incentives for specialized investment and effort are not particularly important in generating value from the supply chain.

• Negotiated transfer prices tend to be preferred when transfers are not mandated (suppliers and purchasers freely choose to exchange), a cash market for the commodity version of the product exists, and motivating specialized investment and effort is important in generating value from the supply chain.

24

3.0 Incentive Pricing Mechanisms The problem of getting someone to do what they are supposed to do when their activities cannot be observed is called moral hazard in the economics literature. It is really a problem of unobservable behaviour that impacts the quality or volume of a product produced. There is a voluminous literature in economics related to moral hazard; one which is well beyond the scope of this review. A thorough review of this literature is provided by Prendergast (1999). Instead, we review the basics of designing pricing mechanisms to police moral hazard and induce effort or investment when it is unobservable, and review related research applied in the agricultural economics literature. These insights are drawn together to suggest applications in pricing farm and food products in Canada.

3.1 Designing Pricing Mechanisms to Induce Effort or Investment In an exchange relationship, certain responsibilities are delegated from buyer to seller (or vice versa). It is common that the extent to which these responsibilities are actually carried out is unobservable or unverifiable. The purpose of a pricing mechanism in this context is to structure payment so that the seller carries out his responsibility, even though this activity is not directly observed. The method of devising such a mechanism is the following4. The buyer wants the seller to take a certain kind of action that cannot be readily observed5. The buyer has a known objective from the exchange relationship (maximize sales, maximize the quality of product purchased, minimize procurement cost, etc.). The buyer attempts to attain this objective, but requires the co-operation of the seller to do so. The buyer cannot observe the actions taken by the seller; however, the buyer can observe variables correlated with the unobservable action. By designing pricing as a function of the observable variable, it will induce the seller to take the unobserved action that is desired. In this context, the nature of the seller forms a constraint from the perspective of the buyer. In its simplest form, there are two constraints related to the seller: (1) the seller must be at least as well off from selling as not selling, and (2) the seller must prefer to take appropriate action (as conditioned on the observable variable) at least as well as inappropriate actions. Put differently, the form of the payment made from the buyer to the seller must give the seller the incentive to do choose “correct” actions, but guarantee his payment at some threshold level. To the extent that these objectives and constraints can be characterized mathematically, we can solve for the pricing parameters that advance the objective and satisfy the constraints. This approach is used to formulate and analyze contracts to motivate effort and investment. Pricing mechanisms of this type typically have two parts. There is a fixed component (a base 4 For a more thorough and technical presentation on the design of incentive pricing mechanisms, see Salanié (1997) 5 It should be clear that this concept applies equally to a seller attempting to get a buyer to take unobservable action; the issue is entirely symmetric

25

price) and additional variable components paid proportional to the observed variables correlated with the desired unobservable action. The problem of determining the correct weights to place on the fixed and incentive components of the price is solved using a mathematical optimization procedure of the buyer’s objective given the constraints presented by the seller.

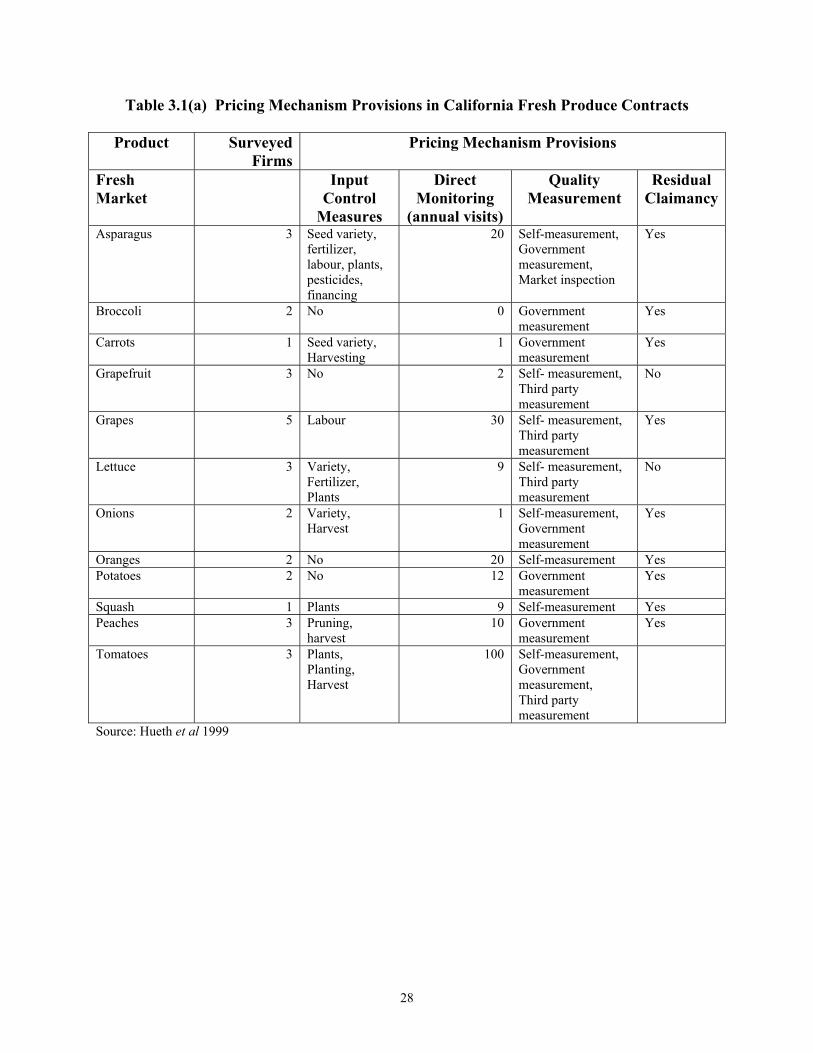

3.2 Pricing for Unobservable Effort and Investment in Agriculture Many examples of these types of pricing mechanism exist in agriculture. Much of the research work has focused on vegetable pricing. Alexander et al examined the impact of California processing tomato contract provisions on tomato quality. Tomato contracts between growers and processors in California are negotiated on behalf of growers by the California Tomato Growers Association. Negotiated contracts are presented directly to growers by processors. Under contracts, tomatoes are graded on the basis of damage (worm damage, colour, mold, material other than tomatoes, percentage green tomatoes, and percentage limited use tomatoes), and on tomato solids content. Under the contracts, both base price and quality incentive payments are negotiated. Growers have a choice among a number of agronomic actions that influence product damage and tomato solids content. Tomato quality is influenced by the timing of harvest, the decision to pre-sort and method of sorting, the choice of tomato variety, and the rate of fertilizer application. In the study, the quality level of tomatoes purchased under a contract that specifies a base price and quality schedule was compared with tomatoes purchased at a fixed price. The comparison involved over 30,000 loads purchased at a single plant over the period 1994-97. The results showed that for all quality parameters, the tomatoes purchased on contract had a higher level of quality. Tomato solids were the only component that was ambiguous in the comparison, and it was found that natural variation in weather makes it very difficult for growers to control. Hueth and Ligon (2001) analyzed the optimal structure of California processing tomato contracts. Existing tomato contracts use a base price combined with a deduction for the damage measures above, and a premium for tomato solids. Using data on agronomic actions taken by growers and the resulting product damage and quality, Hueth and Ligon estimate the optimal schedule of damage deductions and tomato solids premiums. The results showed that existing contracts are similar to the estimated optimal tomato contract, but vary widely in the parameters used for specific damage and tomato solids parameters. Hueth and Melkonyan analyzed sugar beet contracts in use in the US. Sugar beets are grown extensively in 5 separable production regions: the Red River Valley (Minnesota and North Dakota), Michigan and Ohio, the Great Plains (Montana and Colorado), the Northwest (Idaho and Oregon), and the Southwest (primarily California). They considered the differences between sugar beet the Red River Valley and Michigan/Ohio regions relative to other production regions. Sugar beet contracts in the Red River Valley and Michigan/Ohio provide compensation based on a base price per ton, with quality adjustments for total sugar content and percentage extractable sugar. In all other regions, sugar beet contracts contain a base price with a premium for sugar content but not adjustment for extractable sugar.

26

Hueth and Melkonyan found that the difference in contract pricing mechanisms related to the impact of irrigation, which is used in sugar beet production in all regions except those with the extractable sugar provision. They show that application of nitrogen fertilizer increases sugar beet yield, but decreases the sugar content. However, irrigation increases the productivity of nitrogen, so nitrogen fertilizer applied under irrigated conditions does not reduce sugar content the same way. Thus, the problem is to give farmers to reduce nitrogen use when it reduces sugar beet yield. The additional provision of extractable sugar induces farmers to reduce nitrogen applications in non-irrigated areas; this is unnecessary in irrigated regions. Hueth and Melkonyan present evidence from periods with and without the extractable sugar contract provisions, and show that extraction rates at American Crystal Sugar (a Red River Valley processor) have increased by almost 10%. They also show that sugar beet yields are significantly lower in non-irrigated areas, and that less fertilizer is applied in the non-irrigated areas, which is consistent with the incentives in the contract. Chu et al analyzed the problem of designing seed corn production contracts to encourage reduced nitrogen fertilizer use. The context for the study was seed corn production in Michigan. Typical seed corn contracts in Michigan contain a payment with a base commercial grain corn yield, with an adjustment for the difference between a producer’s seed corn yield relative to a regional benchmark. This seed yield is valued at a price set proportional to the spot corn price. The base yield and price ensures that the seed grower is at least as well off growing seed corn as in commercial corn production. The component that rewards a producer’s seed yield relative to the regional benchmark is the incentive to obtain higher yields. The result of the incentives on yield in the pricing mechanism can induce growers to over apply nitrogen, causing leaching problems. Chu et al propose three approaches to reducing nitrate leaching within the pricing mechanism. First, the maximum permissible level of nitrogen application can be directly specified in the contract. Secondly, the pricing mechanism can include a provision for a penalty tax on nitrogen use. The third option uses a penalty deduction from the payment if the nitrogen applied exceeds a level at which leaching would occur, based on the observed relationship between nitrogen and nitrate leaching. All options assume some degree of nitrogen audit after application. Hueth and Ligon (1999) analyzed fresh market tomato contracts in California. Fresh market tomato pricing contracts are complex arrangements called Joint Venture Agreements. The mechanism uses a base price, with an adjustment for realized downstream revenue relative to a preset bonus target, with an adjustment for packing and freight. The yield is adjusted for underweight or off-size tomatoes (culls). Gross revenue (adjusted price times adjusted revenue) is adjusted for a sales commission. The final producer settlement price is the base price plus 50% of the greater of gross revenue adjusted for commission, sorting and transportation , and zero. Hueth and Ligon solve for a simpler contract design that provides the same incentives to the producer, and leaves the purchaser indifferent. Hueth et al (1999) investigated the incentive provisions of California fruit and vegetable pricing mechanisms. The focus of their study was on the provisions for agronomic and product quality

27