Embed Size (px)

Citation preview

Pricing Strategy Determining the Terms of Exchange

1

Marketing Mix

1. Product

2.Price 3. Distribution

4. Promotion

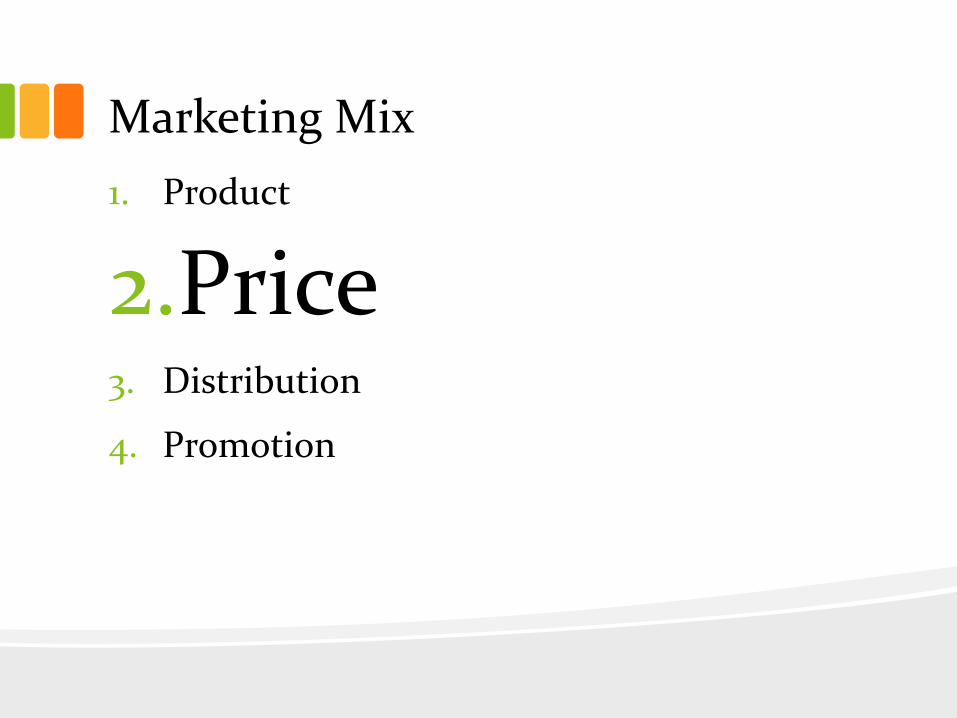

Upcoming Schedule Product Strategy

Tuesday 3/22 Lecture

Thursday 3/24 Class Discussion on “TruEarth Healthy Foods: Market Research for a New Product Introduction”

Pricing Strategy

Tuesday 3/29 Lecture

Thursday 3/31 Class Discussion on “A.1. Steak Sauce: Lawry’s Defense”

Distribution Strategy

Tuesday 4/5 Lecture

Tuesday 4/7 Class Discussion on “Natureview Farm”

Promotion Strategy

Tuesday 4/12 Lecture

Thursday 4/14 Class Discussion on “Giant Consumer Products: The Sales Promotion Resource Allocation Decision”

Price Influencers

1. Methods for Determining Price

2. Supply Factors (producers, distributors,…)

3. Competitive Environment

4. Consumer Behavior

5. Legal-Political Environment

4

Methods for Pricing

5

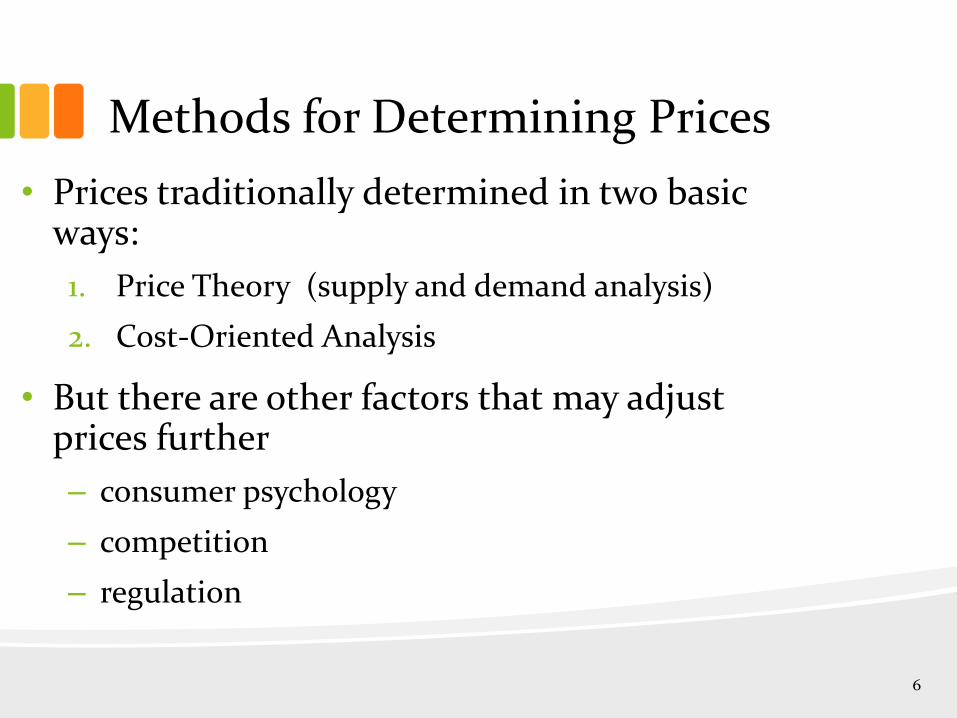

Methods for Determining Prices

• Prices traditionally determined in two basic ways:

1. Price Theory (supply and demand analysis)

2. Cost-Oriented Analysis

• But there are other factors that may adjust prices further

– consumer psychology

– competition

– regulation

6

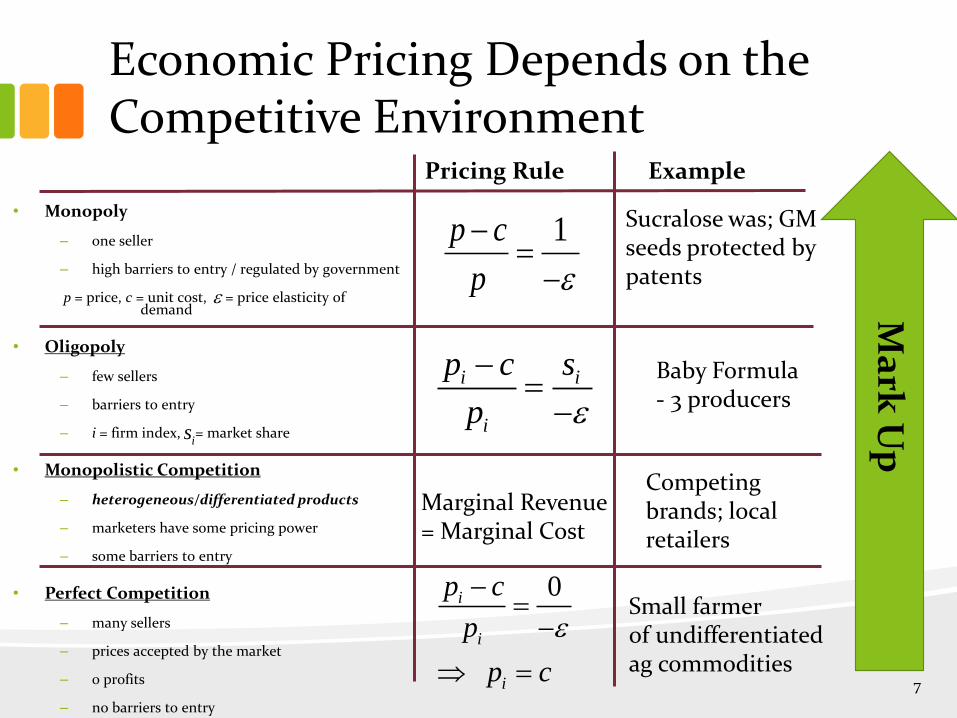

Economic Pricing Depends on the Competitive Environment

• Monopoly

– one seller

– high barriers to entry / regulated by government

p = price, c = unit cost, = price elasticity of demand

• Oligopoly

– few sellers

– barriers to entry

– i = firm index, = market share

• Monopolistic Competition

– heterogeneous/differentiated products

– marketers have some pricing power

– some barriers to entry

• Perfect Competition

– many sellers

– prices accepted by the market

– 0 profits

– no barriers to entry

7

Ma

rk U

p

1p c

p

i i

i

p c s

p

is

0

i

i

i

p c

p

p c

Marginal Revenue = Marginal Cost

Pricing Rule Example

Small farmer of undifferentiated ag commodities

Sucralose was; GM seeds protected by patents

Baby Formula - 3 producers

Competing brands; local retailers

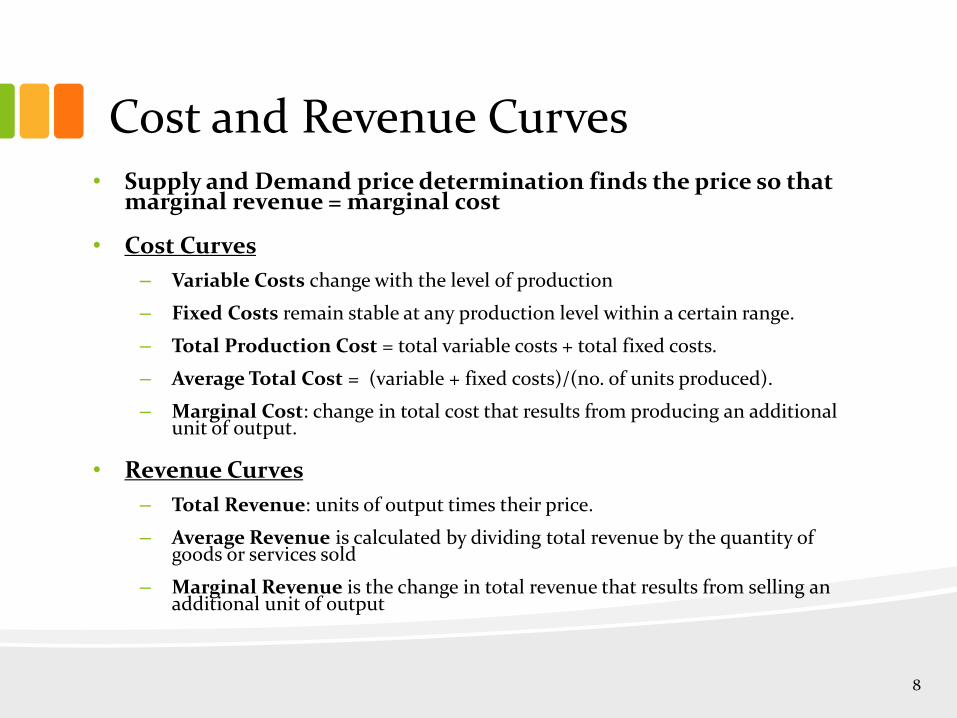

Cost and Revenue Curves • Supply and Demand price determination finds the price so that

marginal revenue = marginal cost

• Cost Curves

– Variable Costs change with the level of production

– Fixed Costs remain stable at any production level within a certain range.

– Total Production Cost = total variable costs + total fixed costs.

– Average Total Cost = (variable + fixed costs)/(no. of units produced).

– Marginal Cost: change in total cost that results from producing an additional unit of output.

• Revenue Curves

– Total Revenue: units of output times their price.

– Average Revenue is calculated by dividing total revenue by the quantity of goods or services sold

– Marginal Revenue is the change in total revenue that results from selling an additional unit of output

8

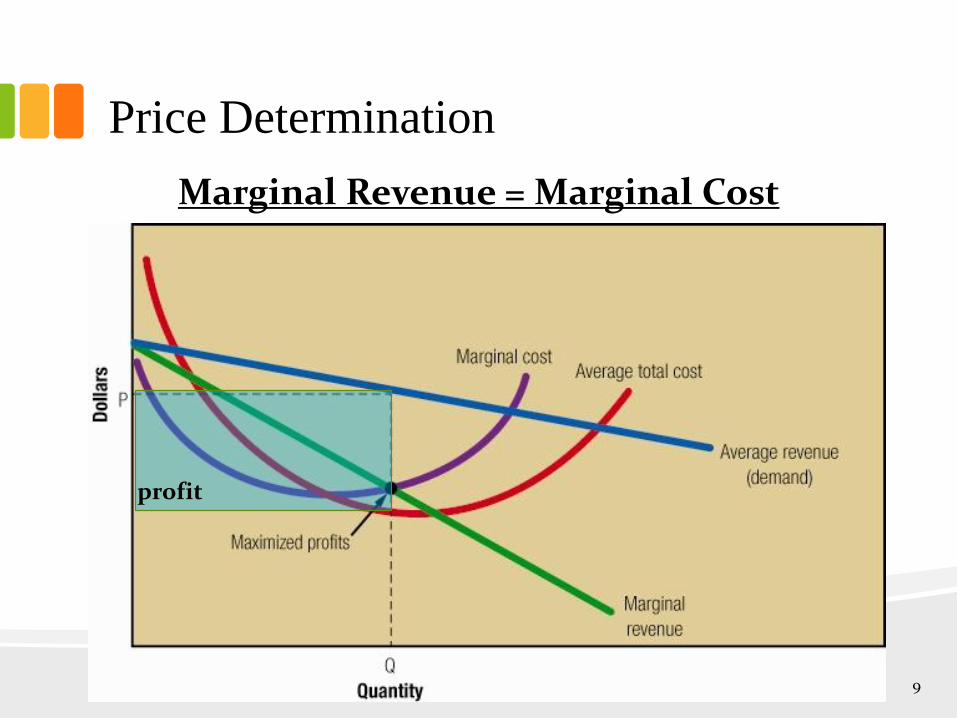

Price Determination

Marginal Revenue = Marginal Cost

9

profit

Problems with Econ Theory Pricing

• Marketers may thoroughly understand price theory concepts but still encounter difficulty in applying them in practice.

• Practical limitations interfering with price determination include: – Many firms don’t attempt to maximize profits

• Then what…?

– Estimating demand curves is a difficult process

– Dynamic effects such as habit formation are really hard to measure

– Requires a lot of consumer behavior data

– Relationships that existed yesterday might not exist today • Changes in the market may have shifted demand curves

• New products may be introduced

• Consumer preferences and perceptions might change

• Competition changes their price

10

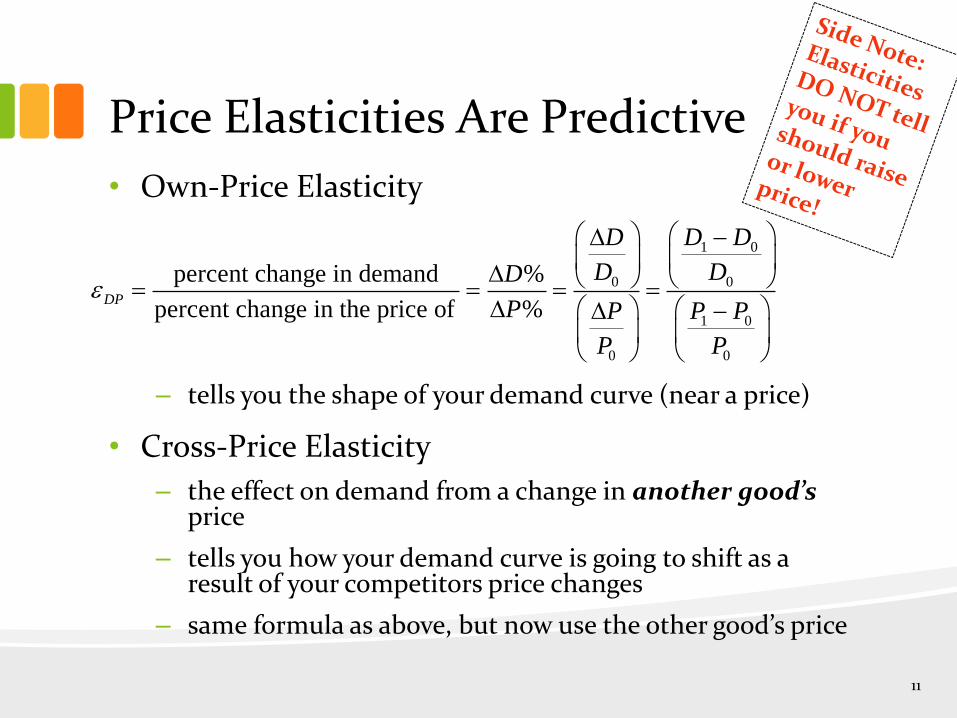

Price Elasticities Are Predictive

• Own-Price Elasticity

– tells you the shape of your demand curve (near a price)

• Cross-Price Elasticity

– the effect on demand from a change in another good’s price

– tells you how your demand curve is going to shift as a result of your competitors price changes

– same formula as above, but now use the other good’s price

1 0

0 0

1 0

0 0

percent change in demand %

percent change in the price of %DP

D D D

D DD

P P P P

P P

11

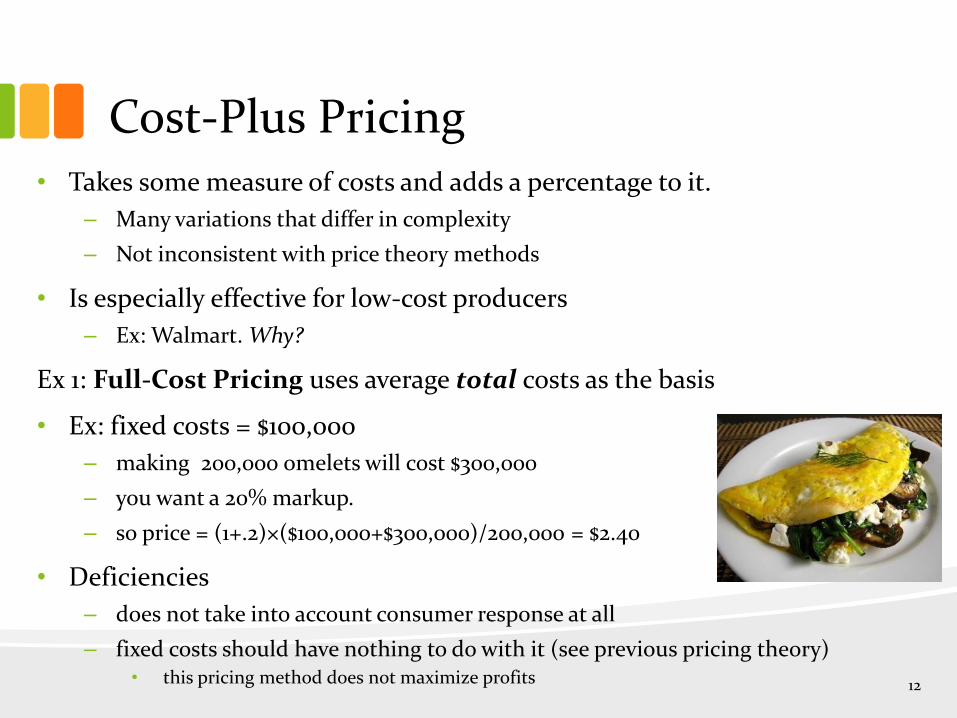

Cost-Plus Pricing • Takes some measure of costs and adds a percentage to it.

– Many variations that differ in complexity

– Not inconsistent with price theory methods

• Is especially effective for low-cost producers

– Ex: Walmart. Why?

Ex 1: Full-Cost Pricing uses average total costs as the basis

• Ex: fixed costs = $100,000

– making 200,000 omelets will cost $300,000

– you want a 20% markup.

– so price = (1+.2)×($100,000+$300,000)/200,000 = $2.40

• Deficiencies

– does not take into account consumer response at all

– fixed costs should have nothing to do with it (see previous pricing theory) • this pricing method does not maximize profits

12

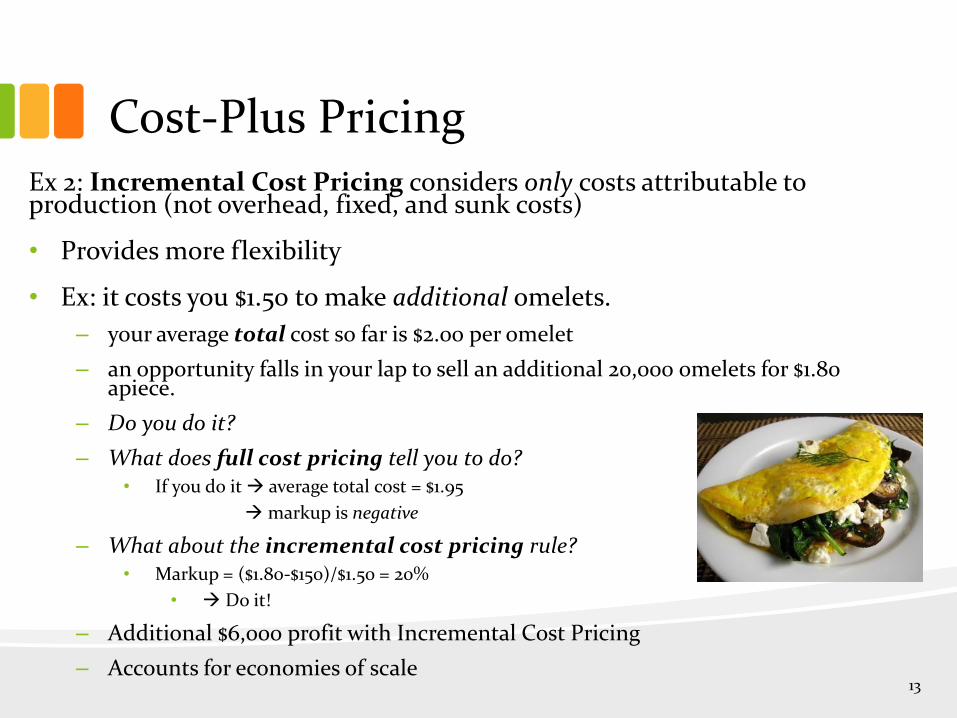

Cost-Plus Pricing Ex 2: Incremental Cost Pricing considers only costs attributable to production (not overhead, fixed, and sunk costs)

• Provides more flexibility

• Ex: it costs you $1.50 to make additional omelets.

– your average total cost so far is $2.00 per omelet

– an opportunity falls in your lap to sell an additional 20,000 omelets for $1.80 apiece.

– Do you do it?

– What does full cost pricing tell you to do? • If you do it average total cost = $1.95

markup is negative

– What about the incremental cost pricing rule? • Markup = ($1.80-$150)/$1.50 = 20%

• Do it!

– Additional $6,000 profit with Incremental Cost Pricing

– Accounts for economies of scale

13

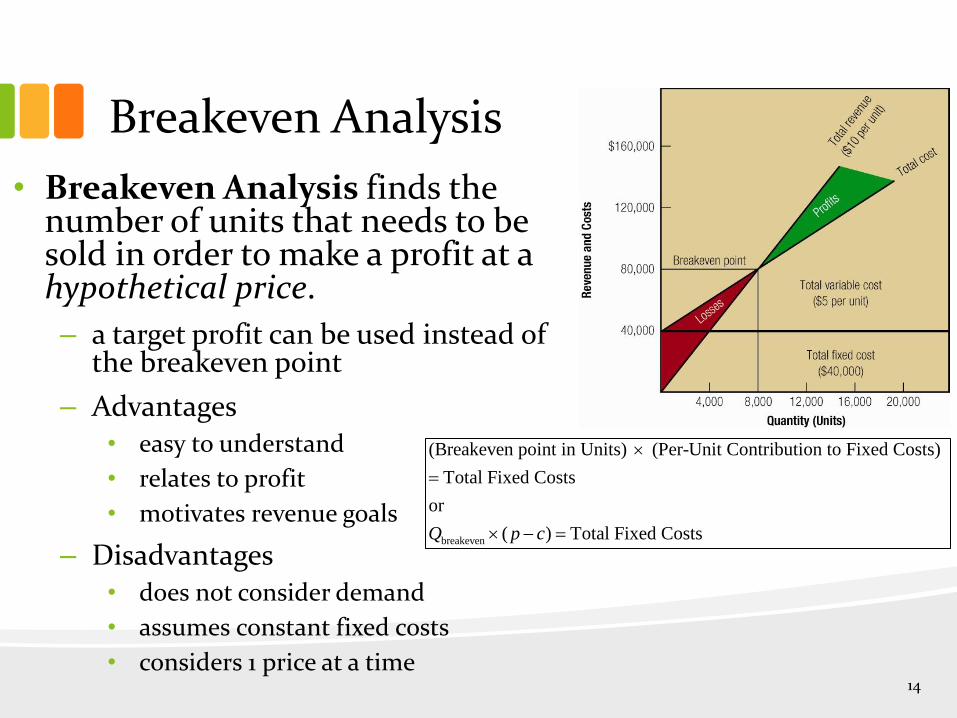

Breakeven Analysis

• Breakeven Analysis finds the number of units that needs to be sold in order to make a profit at a hypothetical price.

– a target profit can be used instead of the breakeven point

– Advantages • easy to understand

• relates to profit

• motivates revenue goals

– Disadvantages • does not consider demand

• assumes constant fixed costs

• considers 1 price at a time

breakeven

(Breakeven point in Units) (Per-Unit Contribution to Fixed Costs)

Total Fixed Costs

or

( ) Total Fixed CostsQ p c

14

Modified Breakeven Analysis

• Modified Breakeven Analysis – do breakeven analysis for an array of hypothetical prices.

• Can include consumer responses (demand)

• Demand considerations include:

– Degree of price elasticity

– Consumer price expectations

– Existence and size of specific market segments

– Buyer perceptions of strengths and weaknesses of substitute products

15

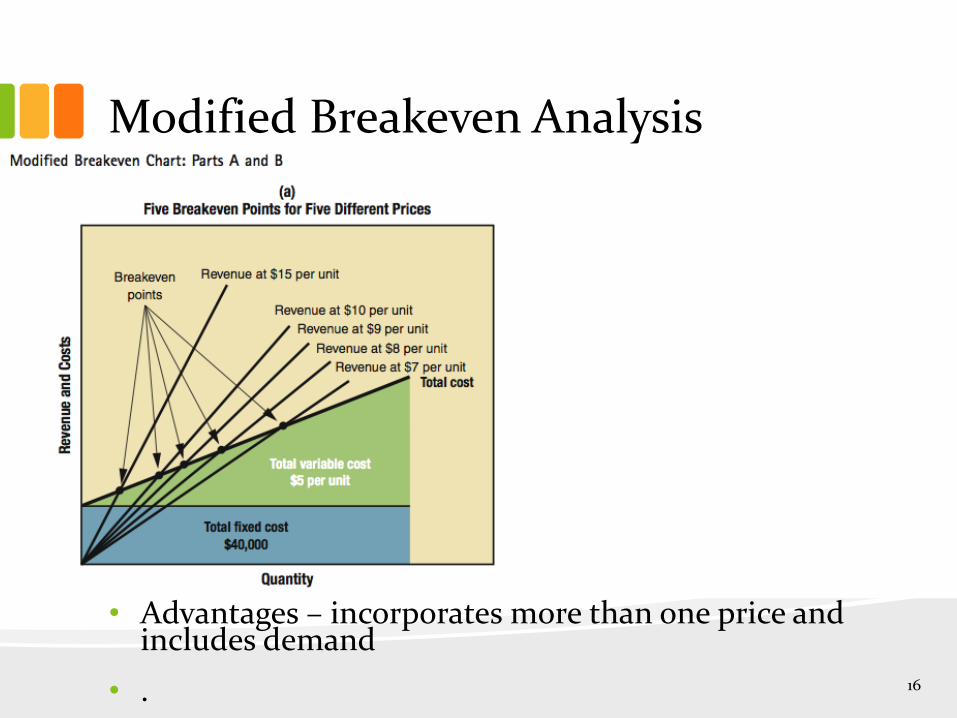

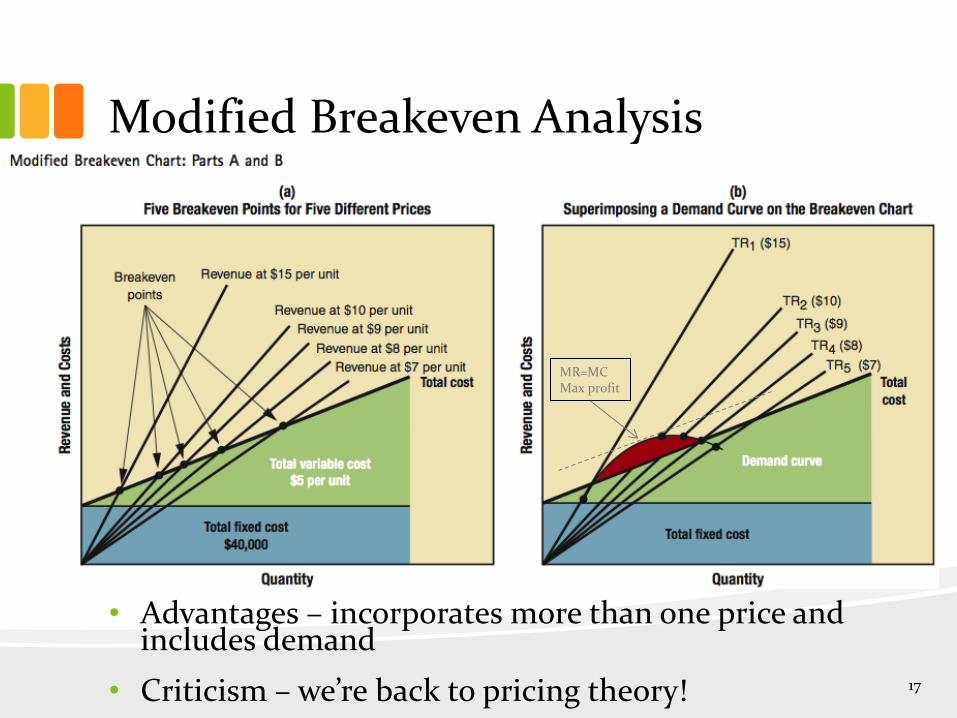

Modified Breakeven Analysis

• Advantages – incorporates more than one price and includes demand

• .

MR=MC Max profit

16

Modified Breakeven Analysis

• Advantages – incorporates more than one price and includes demand

• Criticism – we’re back to pricing theory!

MR=MC Max profit

17

Pricing and the Competition Environment

18

Pricing Strategies

• Skimming – setting prices initially high and slowly decreasing prices to attract people with decreasing willingness-to-pay

– form of price discrimination (for nondurables)

– typically used with new and novel products

– most effective with durable goods but can be useful for food

– Ex: Pom has had high prices but they are decreasing

• first adopters tend to have high willingnesses-to-pay and be evangelical about the product

• has allowed them to ramp up production

19

Competitive Pricing Strategy • Simply matching the prices of comparable competitors.

• 2/3 of firms use competitive pricing

• De-emphasizes price as a competitive variable – unless you have a production cost advantage, it is unlikely you can

maintain a low price advantage for very long any ways

– avoids price wars • Who wins in a price war?

• Characteristic of “old” market spaces where price battles have been played out (mature markets)

• Allows for marketing resources to be used elsewhere

• Step Out – raises prices to see if competitors follow – if they don’t, prices are lowered back to original levels

– is this tacit collusion?

20

Penetration Pricing Strategies

• Sets an artificially low price as a marketing weapon

– used when increasing volume or market share are the objectives

– not a long-term strategy

• Examples:

– Set a low price during introduction to gain consumer recognition • works best with elastic demand

– Set a low price to attract a large market before competitors mimic • increases first movers advantage and creates solid brand loyalty

– Set a low price to deter a potential entrants

21

EDLP vs. Hi-Lo

• Everyday Low Pricing (EDLP) uses continuously low and stable prices rather than short-term price cuts – You know that Walmart will have the lowest prices

– Is not a sure fire way to gain an advantage because competitors can easily counter and low prices might mean lower profit • requires a cost advantage

• Contrast with Hi-Lo Pricing – high prices with short periods of sales – a way to price discriminate

• price sensitive consumers will wait for deals while insensitive consumers will pay the high prices

• Examples?

22

Temporary Discounts

• Manufactures often give retailers discounts so that the retail price will be lowered – Called Trade Allowances

• Pass-Through: The amount of a manufacturer’s discount that is passed though the retailer to the consumer (the intended target)

• Retailers take ownership of products when they obtain them from producers, distributors, etc. – it’s up to them if they want to pass a discount on

– Why wouldn’t the retailer pocket all the discount?

23

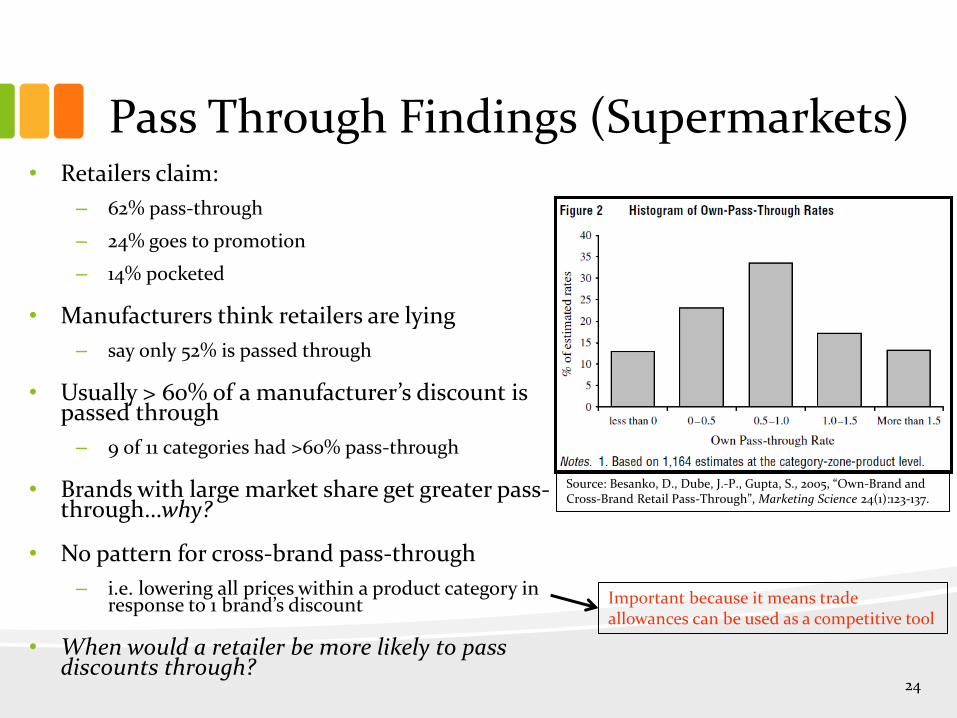

Pass Through Findings (Supermarkets) • Retailers claim:

– 62% pass-through

– 24% goes to promotion

– 14% pocketed

• Manufacturers think retailers are lying

– say only 52% is passed through

• Usually > 60% of a manufacturer’s discount is passed through

– 9 of 11 categories had >60% pass-through

• Brands with large market share get greater pass- through…why?

• No pattern for cross-brand pass-through

– i.e. lowering all prices within a product category in response to 1 brand’s discount

• When would a retailer be more likely to pass discounts through?

Source: Besanko, D., Dube, J.-P., Gupta, S., 2005, “Own-Brand and Cross-Brand Retail Pass-Through”, Marketing Science 24(1):123-137.

Important because it means trade allowances can be used as a competitive tool

24

Opening Price Point

• The practice of retailers setting a low price for an item within a category thereby giving consumers a high value option

• Gives the impression more expensive items in the category are also a good bargain

• Grocers increasingly use their private labels to set opening price points – “The opening price point is clearly a foundation of

who we are and how we interact with our customers” – Ray Bracy, Walmart VP

– Gives the impression the entire store is full of bargains Why? • Private labels are tightly tied to the store’s brand image

25

Loss Leaders • Products that are offered below supplier costs to attract consumers

to the store

• Often placed in the far back of the store to induce consumers to walk past other goods

• Consumer stockpiling is often deterred by… What?

– using highly perishable foods (e.g. milk, bananas)

– imposing purchasing maximums

• Frequently purchased items are used. Why?

– so people are familiar with typical prices and recognize the opportunity

– will attract more shopping trips

• Fast food restaurant discount menu items are loss leaders

– they make their money off the pop

• Gas is a loss leader for many gas stations!

– gas accounts for 70% of revenue but 30% of profit

– they make their money on food and tobacco on the inside of the store

26

Pricing Strategies

• Quantity Discounts – lower unit prices for larger purchasing orders Why? – a way to implement a multi-segmentation strategy to

product-related market segments

– reflects potential per item production/marketing cost savings from larger orders

– accommodates decreasing marginal rates of substitution of consumer utility (i.e. diminishing returns)

– careful, ~10% of larger sizes cost more per unit. Why? • sometimes larger sizes provide convenience or are desired by

inelastic segments

• Ex: larger cans of tuna fish are often more expensive than smaller cans on a per ounce basis

$3.64/gal

$3.74/gal

21.75 cents/oz

19.8 cents/oz

27

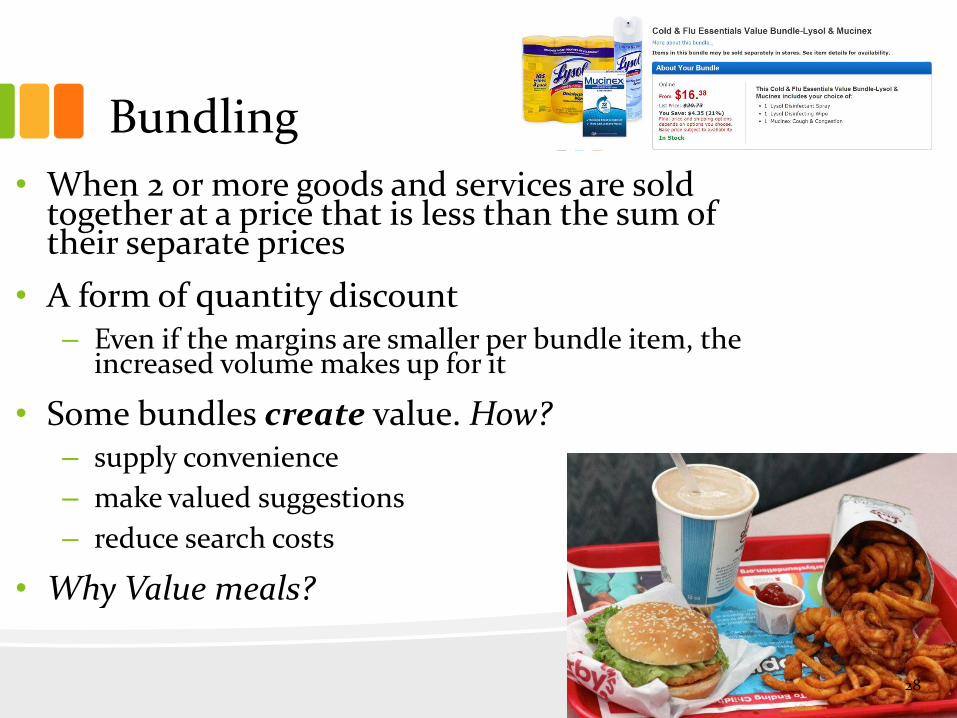

Bundling

• When 2 or more goods and services are sold together at a price that is less than the sum of their separate prices

• A form of quantity discount – Even if the margins are smaller per bundle item, the

increased volume makes up for it

• Some bundles create value. How? – supply convenience

– make valued suggestions

– reduce search costs

• Why Value meals?

28

Consumer Behavior and Pricing Usually Not Your Usual Demand Curves

29

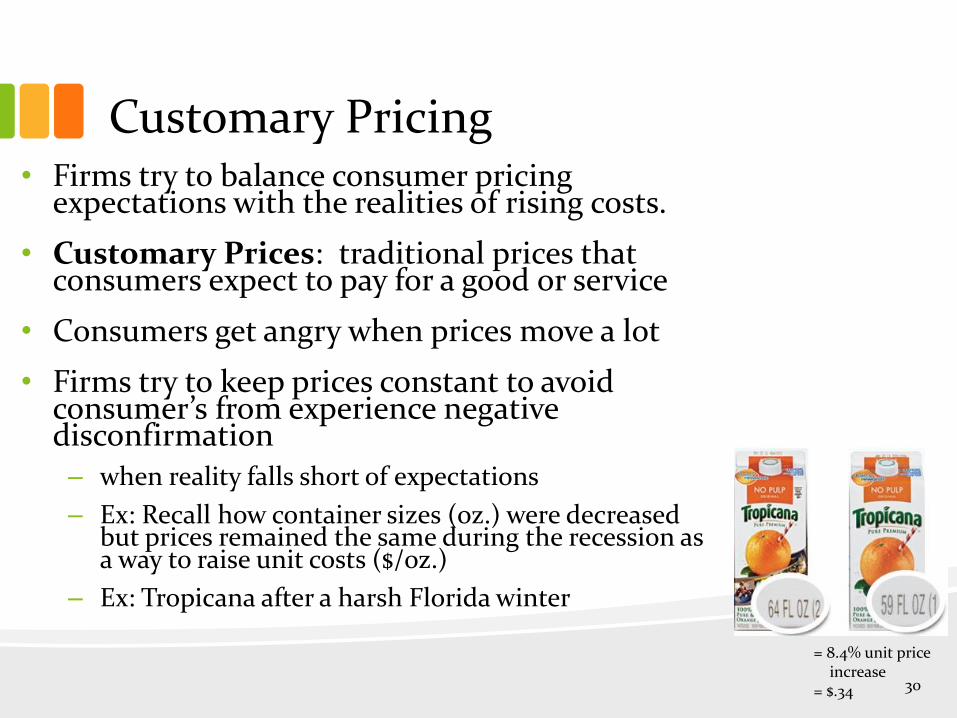

Customary Pricing • Firms try to balance consumer pricing

expectations with the realities of rising costs.

• Customary Prices: traditional prices that consumers expect to pay for a good or service

• Consumers get angry when prices move a lot

• Firms try to keep prices constant to avoid consumer’s from experience negative disconfirmation – when reality falls short of expectations

– Ex: Recall how container sizes (oz.) were decreased but prices remained the same during the recession as a way to raise unit costs ($/oz.)

– Ex: Tropicana after a harsh Florida winter

= 8.4% unit price increase = $.34 30

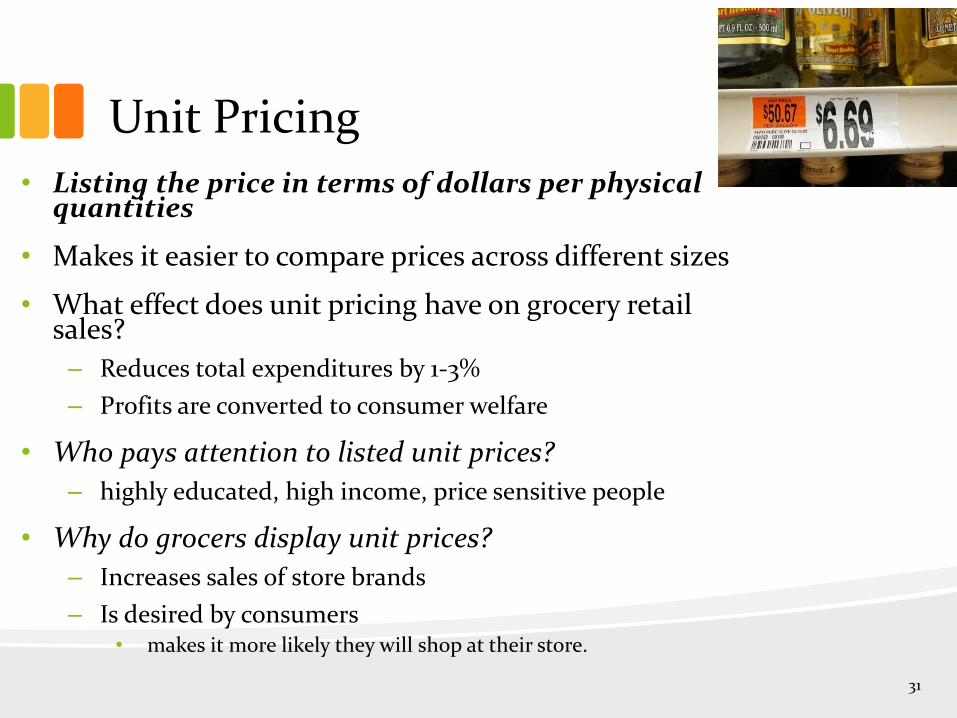

Unit Pricing • Listing the price in terms of dollars per physical

quantities

• Makes it easier to compare prices across different sizes

• What effect does unit pricing have on grocery retail sales?

– Reduces total expenditures by 1-3%

– Profits are converted to consumer welfare

• Who pays attention to listed unit prices?

– highly educated, high income, price sensitive people

• Why do grocers display unit prices?

– Increases sales of store brands

– Is desired by consumers • makes it more likely they will shop at their store.

31

Coupons • Used to give temporary price reductions with minimal effect on consumer price

expectations.

• Allows for targeted discounts. How?

• Increases own-price elasticities. Why?

– Attracts new price sensitive consumers

– Makes existing consumers more price aware

• Used to induce repeat purchases

– Recall learning theory (a.k.a. behavior modification) purchase customer satisfaction repeat purchasing will occur.

• the more times a behavior results in a positive outcome, the more likely the behavior will be repeated.

• Pavlovian response

– Problem: getting customers to initiate the desired behavior

– Solutions

• make barriers to purchase unusually low

• lower price

• make more salient

• increase reinforcement

• induce greater purchasing quantities to increase more eating occasions

32

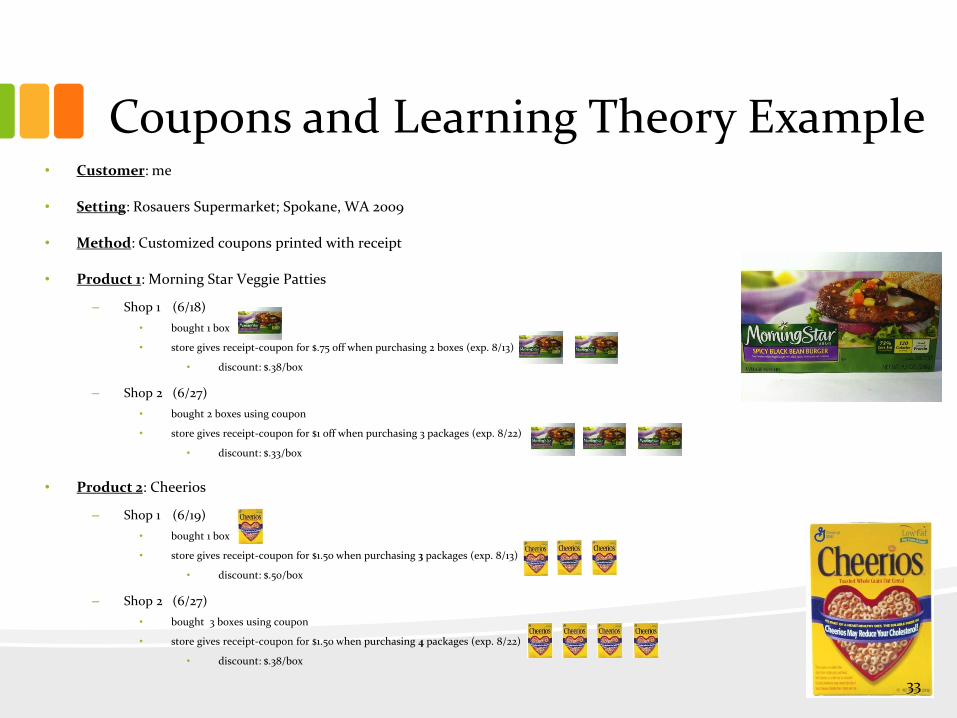

Coupons and Learning Theory Example • Customer: me

• Setting: Rosauers Supermarket; Spokane, WA 2009

• Method: Customized coupons printed with receipt

• Product 1: Morning Star Veggie Patties

– Shop 1 (6/18)

• bought 1 box

• store gives receipt-coupon for $.75 off when purchasing 2 boxes (exp. 8/13)

• discount: $.38/box

– Shop 2 (6/27)

• bought 2 boxes using coupon

• store gives receipt-coupon for $1 off when purchasing 3 packages (exp. 8/22)

• discount: $.33/box

• Product 2: Cheerios

– Shop 1 (6/19)

• bought 1 box

• store gives receipt-coupon for $1.50 when purchasing 3 packages (exp. 8/13)

• discount: $.50/box

– Shop 2 (6/27)

• bought 3 boxes using coupon

• store gives receipt-coupon for $1.50 when purchasing 4 packages (exp. 8/22)

• discount: $.38/box

33

Odd Pricing

• Setting prices to odd numbers just under round whole numbers.

• Originally was used to prevent pilfering

– forced cashiers to use the cash register to get change

• 60-90% of products have odd retail prices

• Used to give the impression of lower prices

– Ex: $1.99 may be associated with a $1 price range while $2.00 may be associated with a $2 price range

– Theory: People read left to right and do not want to waste their time on smaller digits*

* Basu, K., 2006, “Consumer Cognition and the Pricing in the Nines in Oligopolistic Markets,” Journal of Economics and Management Strategy, Vol 15(1) 125-141.

34

Does Odd Pricing Work?

• Historically, evidence has been weak.

• Odd pricing results in people recalling lower prices*

• Recent well designed studies have shown significant increases in demand

– Catalogs with carefully varied prices found a 35% increase in demand**

* Shindler, R., and Wiman, A., 1989. “Effects of odd pricing on price recall,” Journal of Business Research, 19(3): 165–17. ** Anderson, E., and Simester, D., 2003, “Effects of $9 Price Endings on Retail Sales: Evidence from Field Experiments,” Quantitative Marketing and Economics, 1(1): 93-110. 35

Pricing New Products

• Because the quality is unknown, prices play an especially strong role as quality signals.

• Because quality expectations have a powerful effect on taste perception, low prices may result in lower taste evaluations and satisfaction

• Subjects in an fMRI machine were given identical wines but told they were differently priced.*

– Subjects reported higher flavor satisfaction for the “high” priced wines.

– The part of the brain where “experienced pleasantness during experiential tasks” was more active when they thought the wine was high priced

* Plassmann, H., O'Doherty, J., Shiv, B., & Rangel, A. (2008). “Marketing actions can modulate neural representations of experienced pleasantness.” Proceedings of the National Academy of Sciences, 105(3), 1050-1054. 36

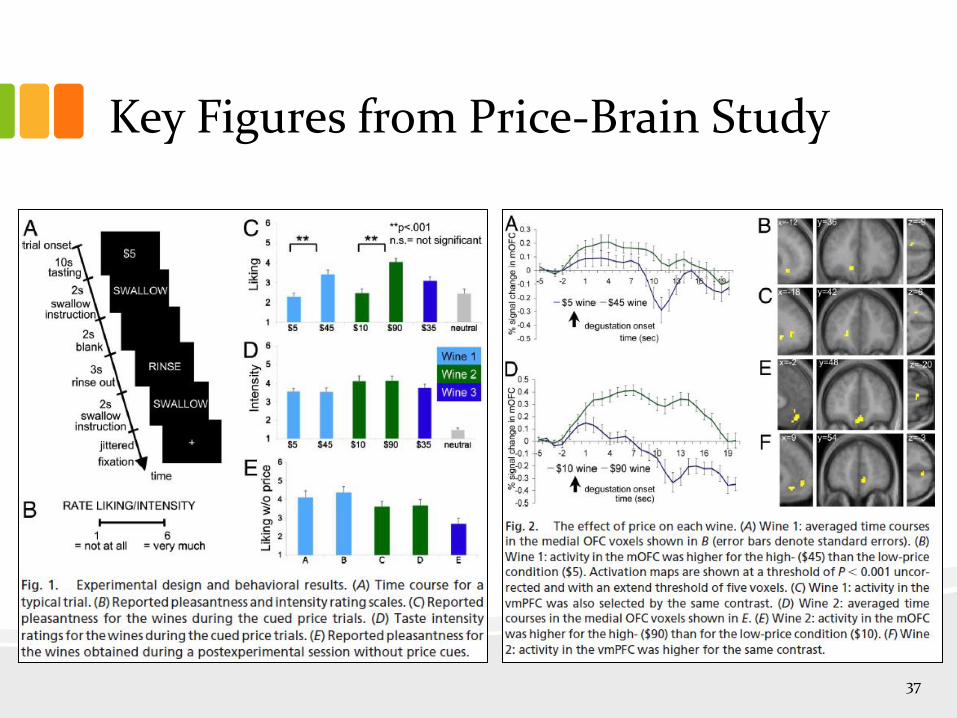

Key Figures from Price-Brain Study

37

Are Prices a Good Signal of Objective-Quality?

• Surprisingly, prices and Objective Quality measures are not often correlated

• Objective measures: laboratory tests, controlled-use tests, expert judgment of purchased samples, and user opinion surveys

• Riesz (1979) uses Consumer Reports for 679 brands in 40 packaged food categories over 15 years and concludes the correlation was near zero

– Subsequent research has found the correlation to be weak at best* - 30 other research papers

– For frozen foods it was negative. Why?

• This does not stop people from believing and perceiving higher priced goods are superior

• Prices that signal low quality may end up being self-fulfilling

– especially with food!

Riesz, P. 1979, “Price-Quality Correlations for Packaged Food Products.” Journal of Consumer Affairs 13(2):236-247. * Gerstner, E., 1985, “Do Higher Prices Signal Higher Quality?” Journal of Marketing Research 22(2):209-215. See handout

38

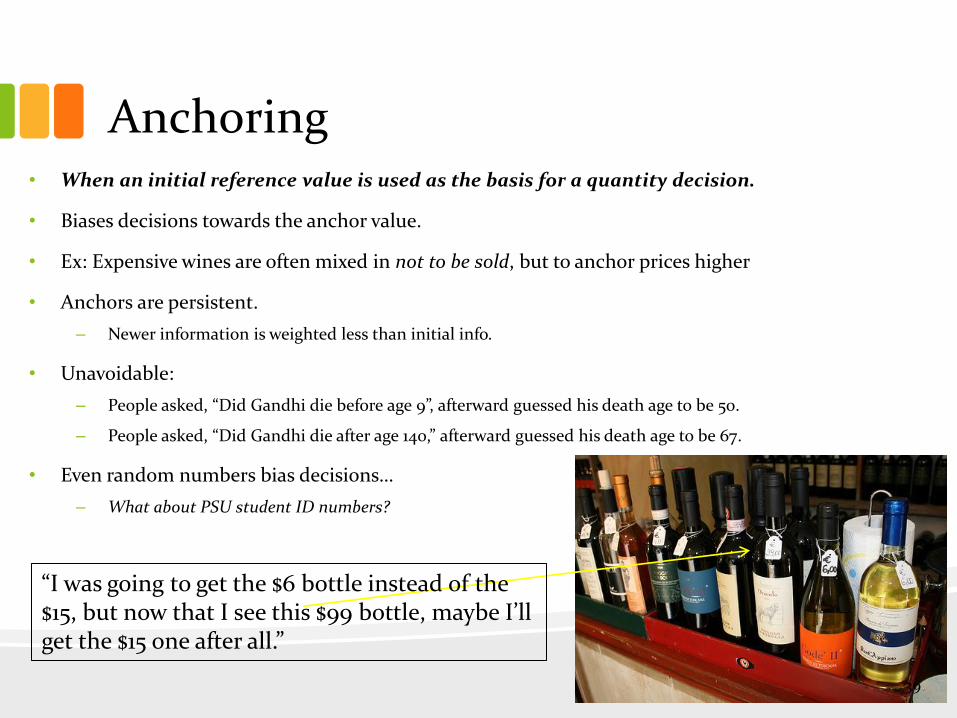

Anchoring • When an initial reference value is used as the basis for a quantity decision.

• Biases decisions towards the anchor value.

• Ex: Expensive wines are often mixed in not to be sold, but to anchor prices higher

• Anchors are persistent.

– Newer information is weighted less than initial info.

• Unavoidable:

– People asked, “Did Gandhi die before age 9”, afterward guessed his death age to be 50.

– People asked, “Did Gandhi die after age 140,” afterward guessed his death age to be 67.

• Even random numbers bias decisions…

– What about PSU student ID numbers?

“I was going to get the $6 bottle instead of the $15, but now that I see this $99 bottle, maybe I’ll get the $15 one after all.”

39

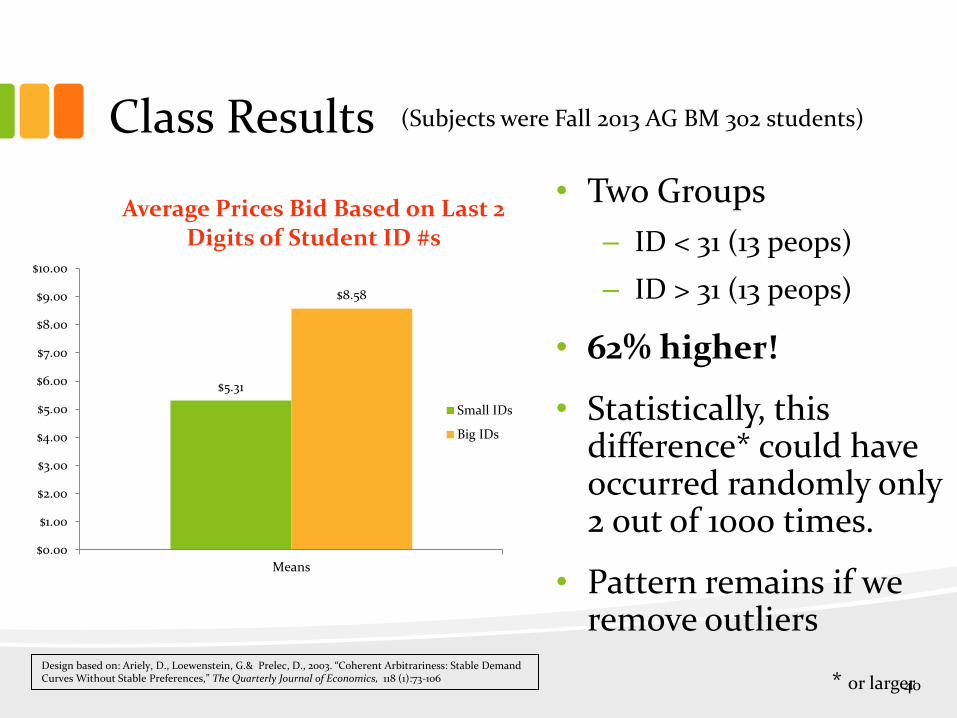

Class Results

• Two Groups

– ID < 31 (13 peops)

– ID > 31 (13 peops)

• 62% higher!

• Statistically, this difference* could have occurred randomly only 2 out of 1000 times.

• Pattern remains if we remove outliers

$5.31

$8.58

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

$10.00

Means

Average Prices Bid Based on Last 2 Digits of Student ID #s

Small IDs

Big IDs

* or larger Design based on: Ariely, D., Loewenstein, G.& Prelec, D., 2003. “Coherent Arbitrariness: Stable Demand Curves Without Stable Preferences,” The Quarterly Journal of Economics, 118 (1):73-106

(Subjects were Fall 2013 AG BM 302 students)

40

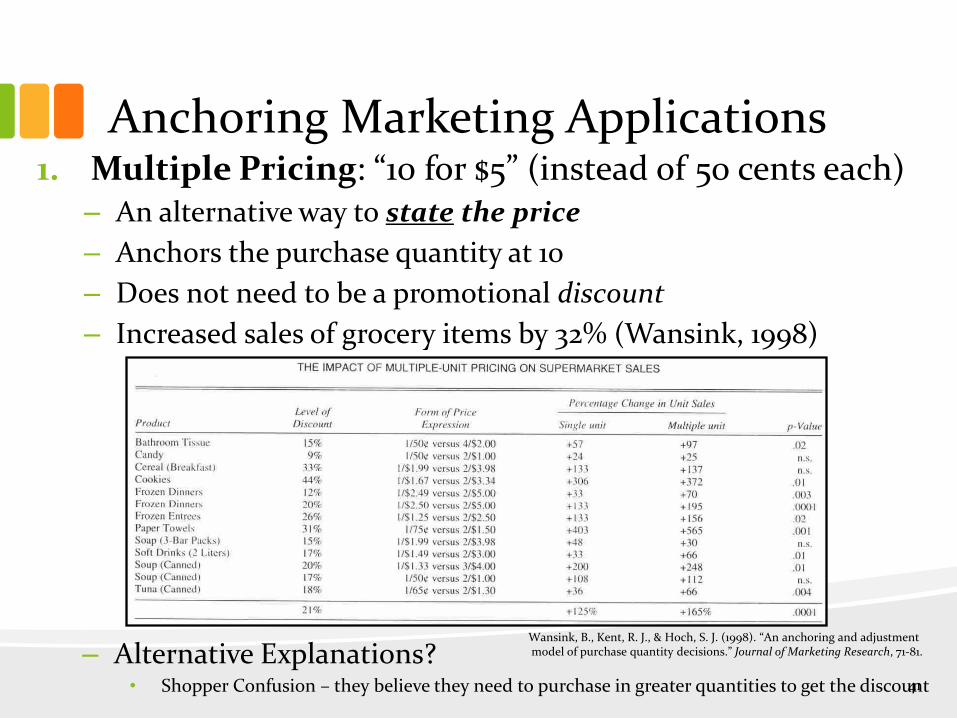

Anchoring Marketing Applications 1. Multiple Pricing: “10 for $5” (instead of 50 cents each)

– An alternative way to state the price

– Anchors the purchase quantity at 10

– Does not need to be a promotional discount

– Increased sales of grocery items by 32% (Wansink, 1998)

– Alternative Explanations? • Shopper Confusion – they believe they need to purchase in greater quantities to get the discount

Wansink, B., Kent, R. J., & Hoch, S. J. (1998). “An anchoring and adjustment model of purchase quantity decisions.” Journal of Marketing Research, 71-81.

41

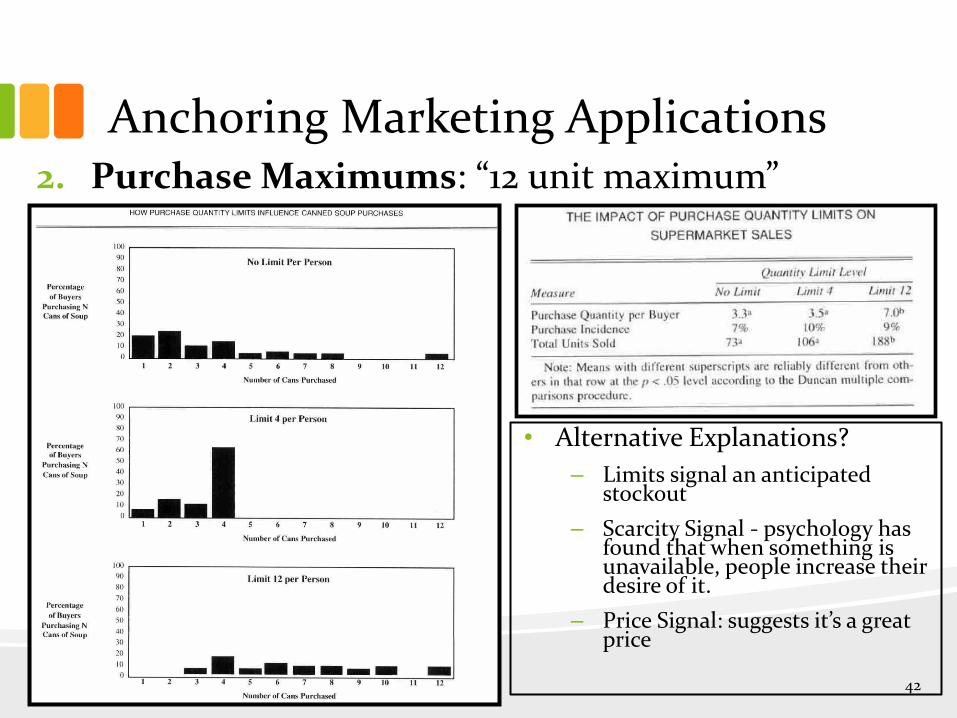

Anchoring Marketing Applications 2. Purchase Maximums: “12 unit maximum”

• Alternative Explanations?

– Limits signal an anticipated stockout

– Scarcity Signal - psychology has found that when something is unavailable, people increase their desire of it.

– Price Signal: suggests it’s a great price

42

Anchoring Marketing Applications

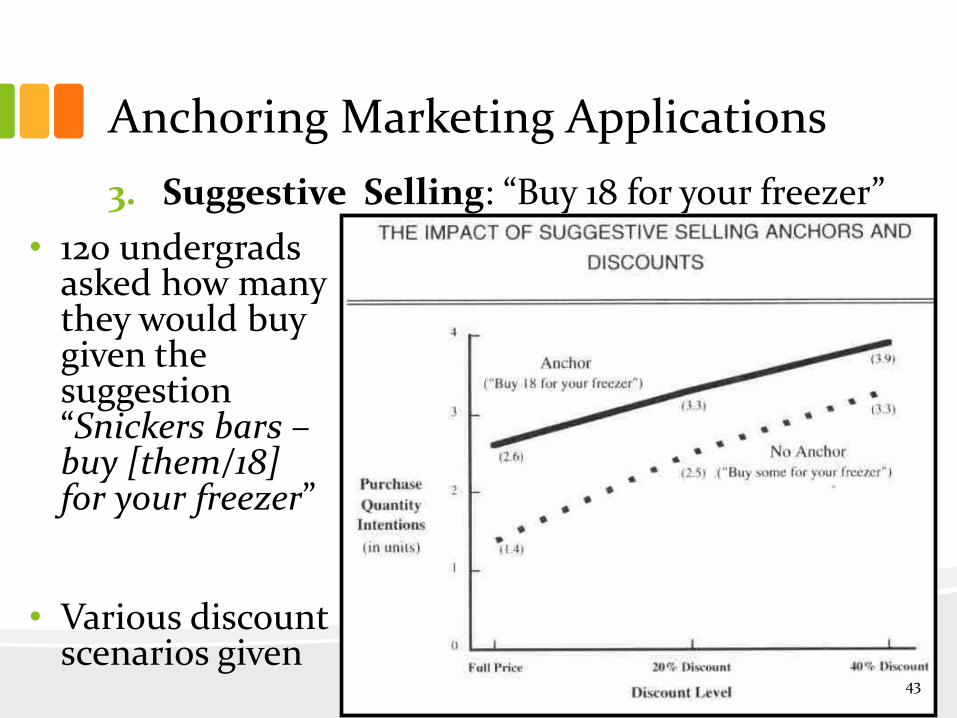

3. Suggestive Selling: “Buy 18 for your freezer”

• 120 undergrads asked how many they would buy given the suggestion “Snickers bars – buy [them/18] for your freezer”

• Various discount scenarios given

43

Prestige Pricing and Behavior • Prestige pricing involves setting high prices to maintain a

desirable image

– Ex: Your over-priced fancy restaurant

• Prestige can augment a product in (at least) 2 ways:

1. Direct increase in social prestige

2. Change perception of the product through individual factors • recall perceptions are composed of (i) stimulus factors (physical

attributes of the product), and (ii) individual factors that reflect all the non-sensory stuff that affects how people view the object.

• Would a person be willing to pay the same amount for the same product at 7-Eleven as they would at Whole Foods?

• How about soda at a run-down grocery store versus a fancy hotel?

– Doing the same thing but with beer, it was found that* • Fancy resort hotel median price = $2.65

• Run-down grocery store median price = $1.50

* Thaler, R. (1985). Mental accounting and consumer choice. Marketing science,4(3), 199-214.

44

Pricing Legal-Political Environment The Rules of the Game

45

Prices and Laws

• Federal, state, and local laws all influence pricing decisions.

• Government Regulations that Affect Prices – Robinson-Patman Act (1936) – Cannot have different prices for

different buyers that are at the same level of the food chain for the purpose of harming competition. • limits third degree price discrimination (different prices for different

commercial segments)

– Resale Price Maintenance (a.k.a. “Fair Trade Law”) is NOW LEGAL. • Upstream firms can force resale prices on downstream firms if doing so

follows the “rule of reason” (Supreme Court, 2007)

– Unfair-Trade Laws - State laws requiring sellers to maintain minimum prices for comparable merchandise. • Protect producers and retail specialty stores from Loss Leaders

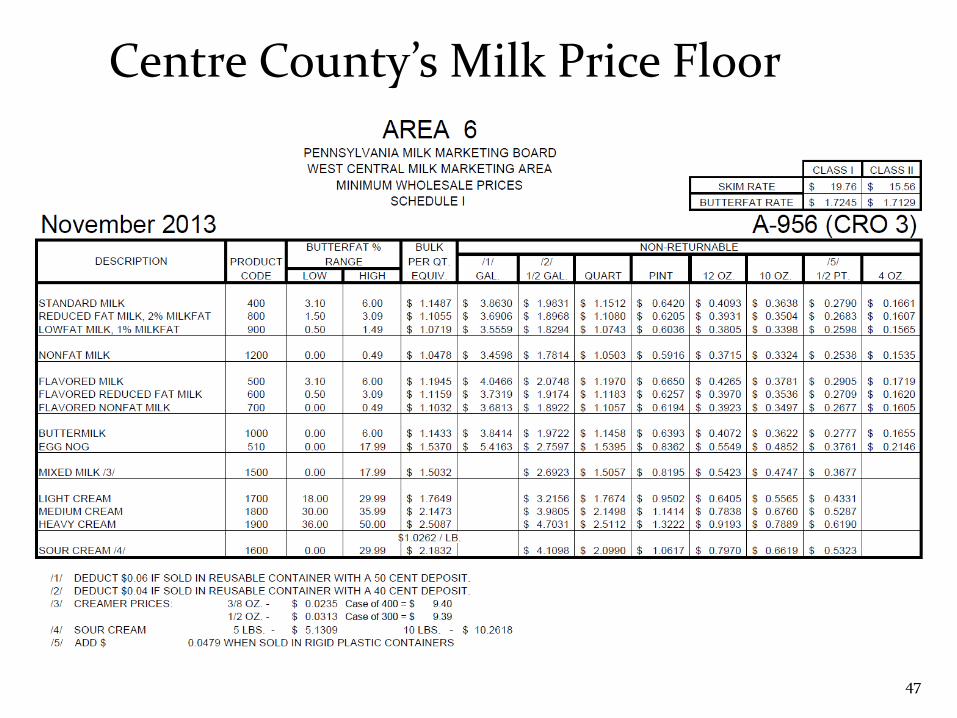

• Ex: Pennsylvania Milk Price floors

46

Centre County’s Milk Price Floor

47

Tariffs and Taxes

• Tariffs affect food prices – Tariff: a tax on imported goods and services

– Implemented to protect domestic producers

– Average tariff on fruits and veggies: >50%

– US fruit and veggie tariffs • 10-20% from EU (likely to be eliminated)

• 0% with Mexico and Canada (NAFTA)

– No state tariffs

• Food Taxes – “Food at home” food is not taxed (in most jurisdictions)

– Restaurant food is taxed

48

General Procedure For Price Determination

1. Find out what is allowed legally

2. Use cost-plus pricing or a competitive pricing strategy

3. Modify your price to account for consumer behavior

– make it closer to price theory

– adjust for behavioral effects

49