Embed Size (px)

Citation preview

Eric JondeauEric Jondeau

Corporate Finance

EMBA in Management & Finance

Eric JondeauEric Jondeau

Lecture 5:

Capital Budgeting For the Levered Firm

EMBA in Management & Finance

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

Prospectus

• Recall that there are three questions in corporate finance.

• The first regards what long-term investments the firm should make (the capital budgeting question).

• The second regards the use of debt (the capital structure question).

• This chapter considers the nexus of these questions.

Eric JondeauEric JondeauEric JondeauEric Jondeau EMBAEMBAEMBAEMBA 3/293/293/293/29

1. Adjusted Present Value Approach

2. Flows to Equity Approach

3. Weighted Average Cost of Capital Method

4. Comparison of the APV, FTE, and WACC Approaches

5. Capital Budgeting when the Discount Rate Must Be Estimated

6. APV Example

7. Beta and Leverage

8. Summary and Conclusions

Eric JondeauEric JondeauEric JondeauEric Jondeau EMBAEMBAEMBAEMBA 4/294/294/294/29

OutlineCorporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

Outline

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

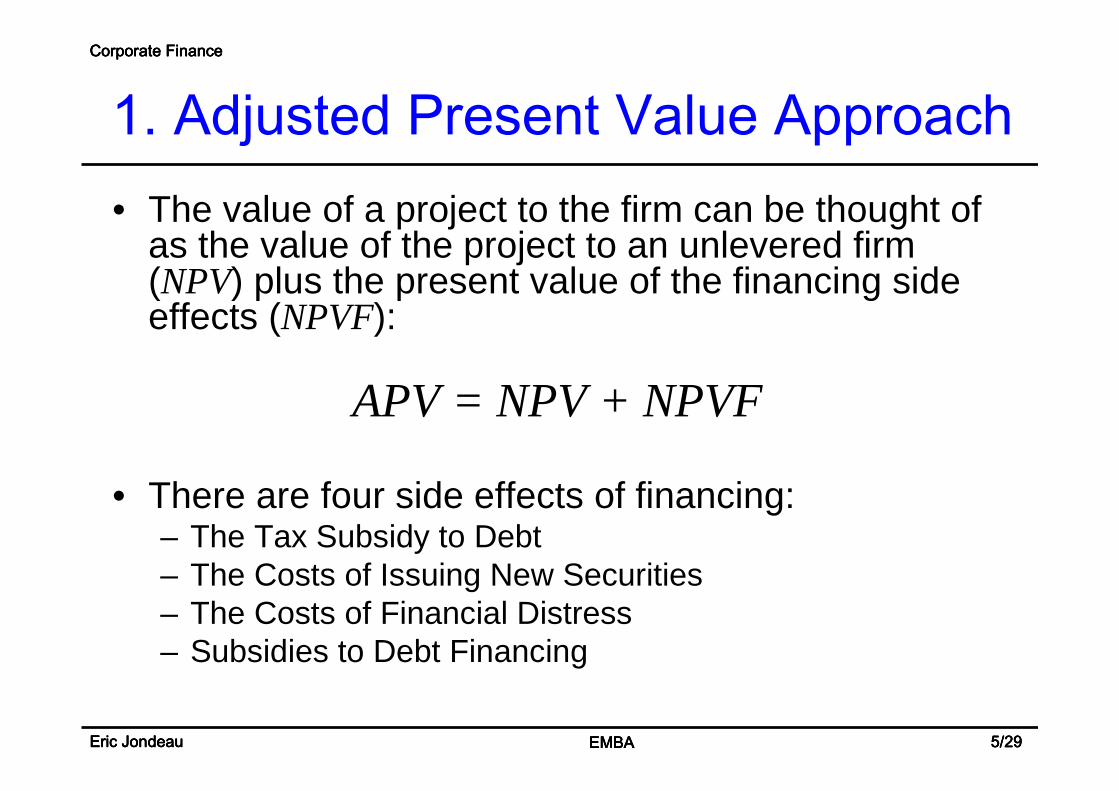

1. Adjusted Present Value Approach• The value of a project to the firm can be thought of

as the value of the project to an unlevered firm (NPV) plus the present value of the financing side effects (NPVF):

APV = NPV + NPVF

• There are four side effects of financing:– The Tax Subsidy to Debt– The Costs of Issuing New Securities– The Costs of Financial Distress– Subsidies to Debt Financing

Eric JondeauEric JondeauEric JondeauEric Jondeau EMBAEMBAEMBAEMBA 5/295/295/295/29

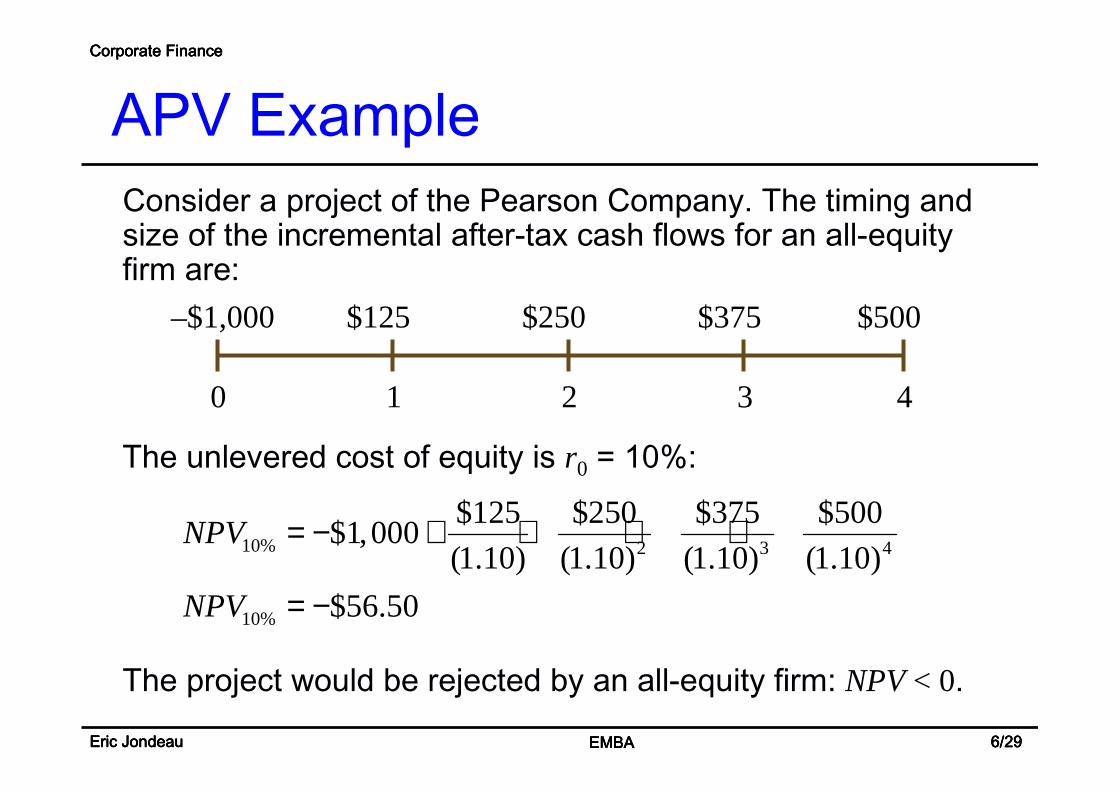

0 1 2 3 4

–$1,000 $125 $250 $375 $500

The unlevered cost of equity is r0 = 10%:

The project would be rejected by an all-equity firm: NPV < 0.

Consider a project of the Pearson Company. The timing and size of the incremental after-tax cash flows for an all-equity firm are:

10% 2 3 4

10%

$125 $250 $375 $500$1,000

(1.10) (1.10) (1.10) (1.10)

$56.50

NPV

NPV

= − + + + +

= −

Eric JondeauEric JondeauEric JondeauEric Jondeau EMBAEMBAEMBAEMBA 6/296/296/296/29

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

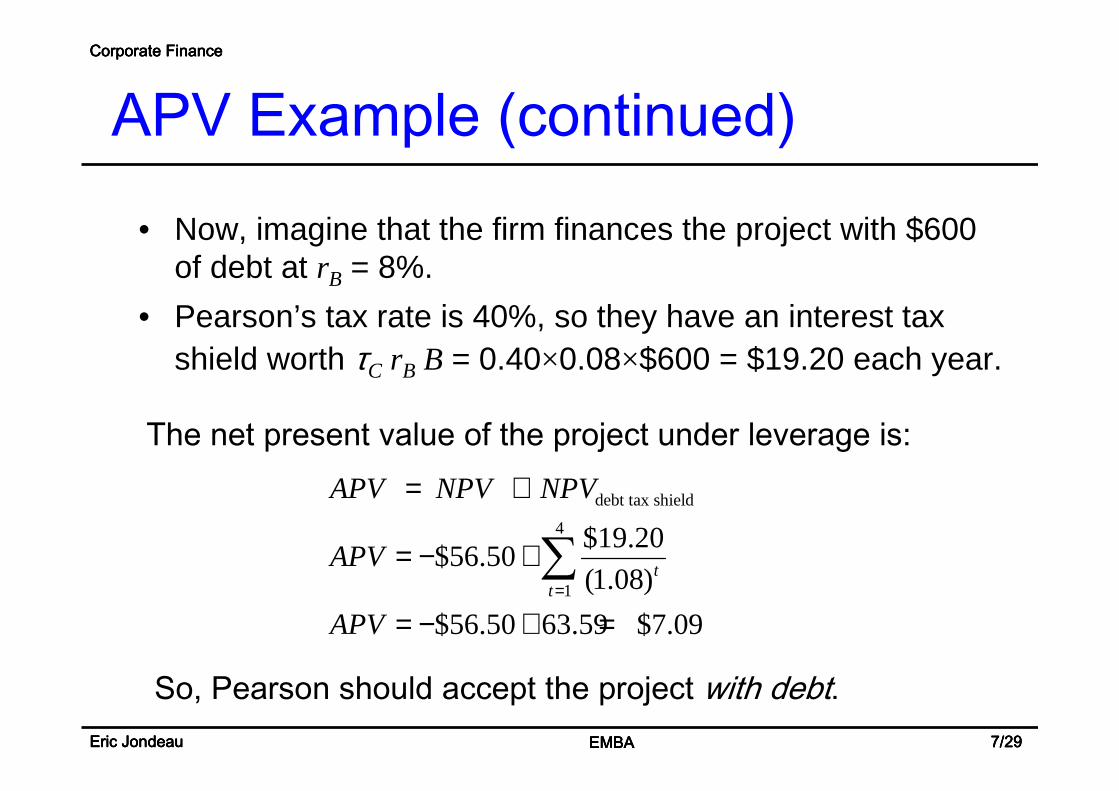

APV Example

• Now, imagine that the firm finances the project with $600 of debt at rB = 8%.

• Pearson’s tax rate is 40%, so they have an interest tax shield worth τC rB B = 0.40×0.08×$600 = $19.20 each year.

The net present value of the project under leverage is:

So, Pearson should accept the project with debt.

debt tax shield

4

1

$19.20$56.50

(1.08)

$56.50 63.59 $7.09

tt

APV NPV NPV

APV

APV=

= +

= − +

= − + =

∑

Eric JondeauEric JondeauEric JondeauEric Jondeau EMBAEMBAEMBAEMBA 7/297/297/297/29

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

APV Example (continued)

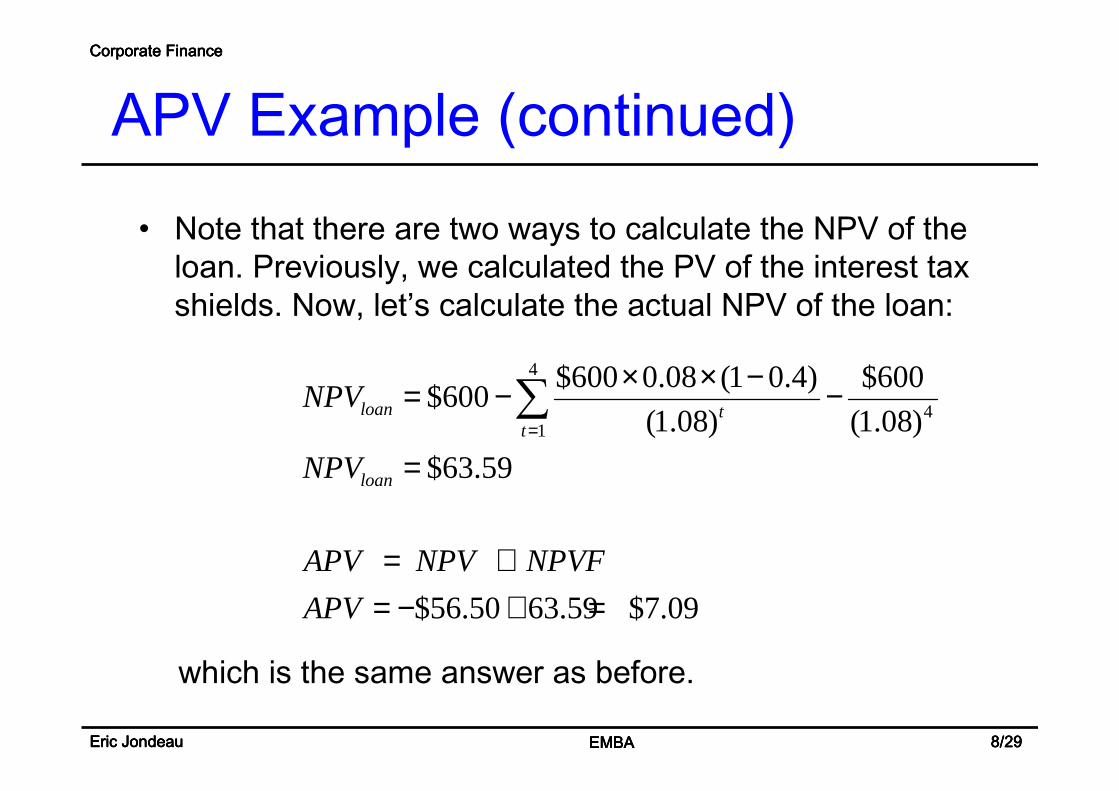

• Note that there are two ways to calculate the NPV of the loan. Previously, we calculated the PV of the interest tax shields. Now, let’s calculate the actual NPV of the loan:

which is the same answer as before.

4

41

$600 0.08 (1 0.4) $600$600

(1.08) (1.08)

$63.59

loan tt

loan

NPV

NPV=

× × −= − −

=

∑

$56.50 63.59 $7.09

APV NPV NPVF

APV

= += − + =

Eric JondeauEric JondeauEric JondeauEric Jondeau EMBAEMBAEMBAEMBA 8/298/298/298/29

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

APV Example (continued)

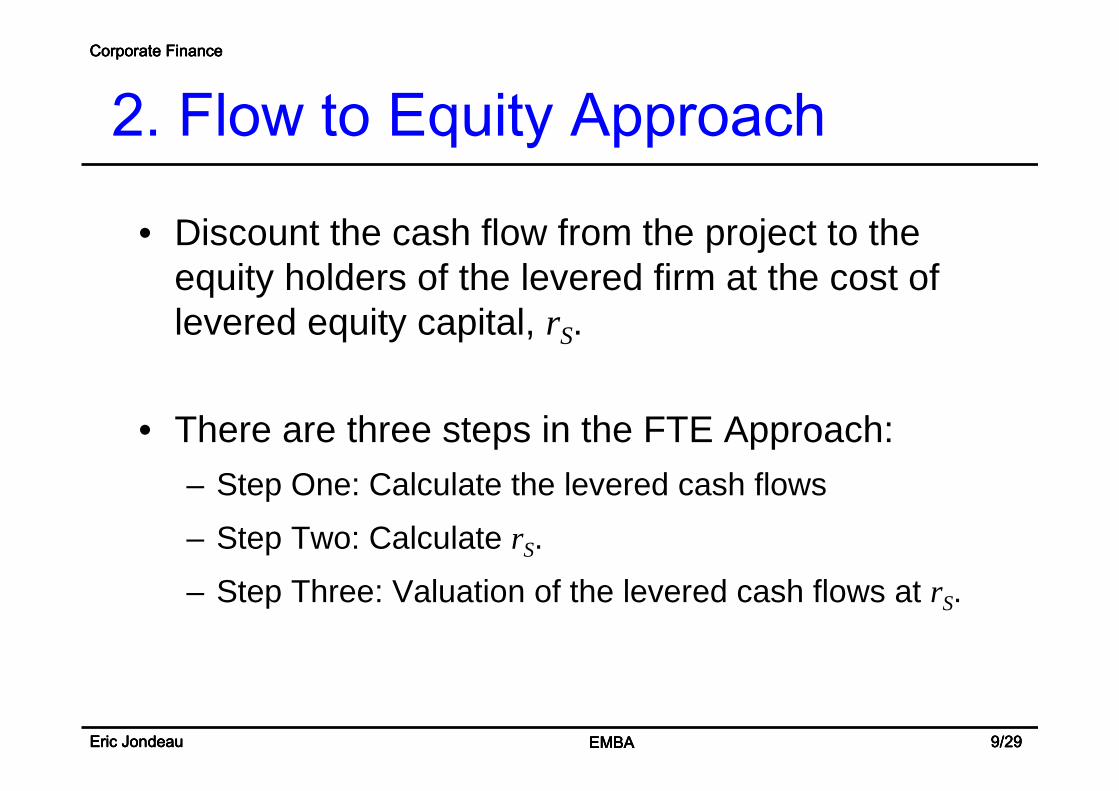

• Discount the cash flow from the project to the equity holders of the levered firm at the cost of levered equity capital, rS.

• There are three steps in the FTE Approach:– Step One: Calculate the levered cash flows

– Step Two: Calculate rS.

– Step Three: Valuation of the levered cash flows at rS.

Eric JondeauEric JondeauEric JondeauEric Jondeau EMBAEMBAEMBAEMBA 9/299/299/299/29

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

2. Flow to Equity Approach

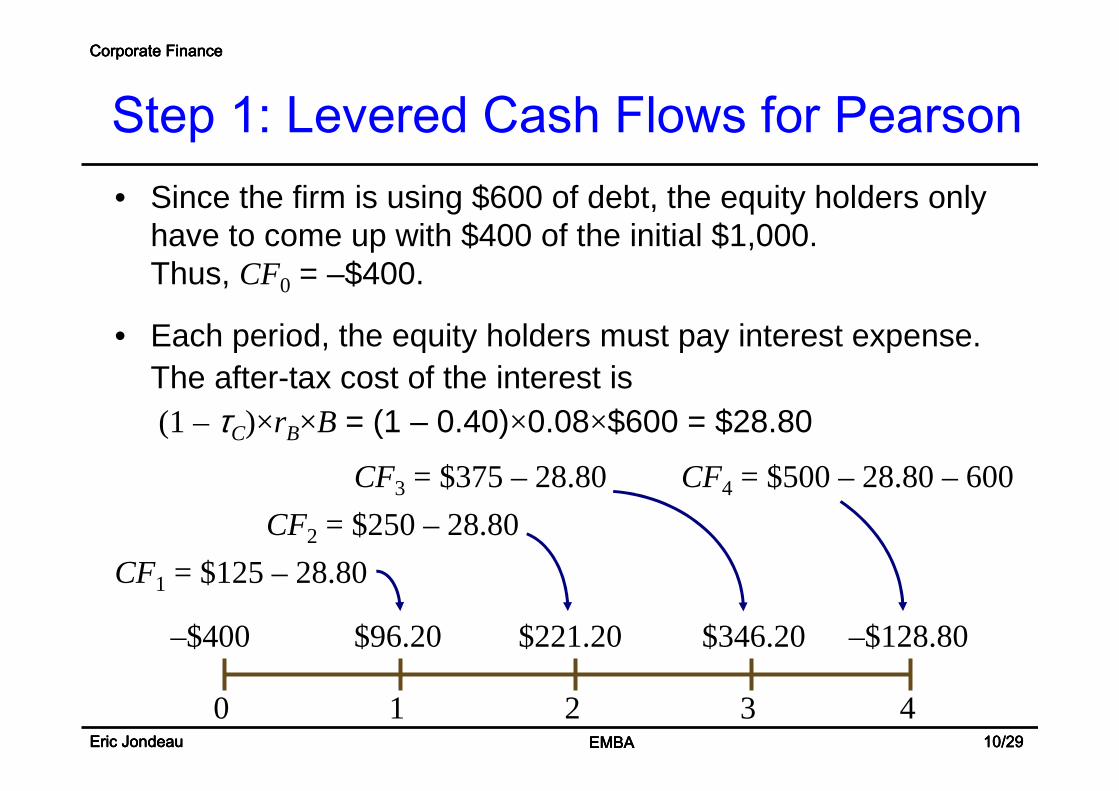

• Since the firm is using $600 of debt, the equity holders only have to come up with $400 of the initial $1,000. Thus, CF0 = –$400.

• Each period, the equity holders must pay interest expense. The after-tax cost of the interest is (1 –τC)×rB×B = (1 – 0.40)×0.08×$600 = $28.80

0 1 2 3 4

–$400 $221.20

CF2 = $250 – 28.80

$346.20

CF3 = $375 – 28.80

–$128.80

CF4 = $500 – 28.80 – 600

CF1 = $125 – 28.80

$96.20

EMBAEMBAEMBAEMBA 10/2910/2910/2910/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

Step 1: Levered Cash Flows for Pearson

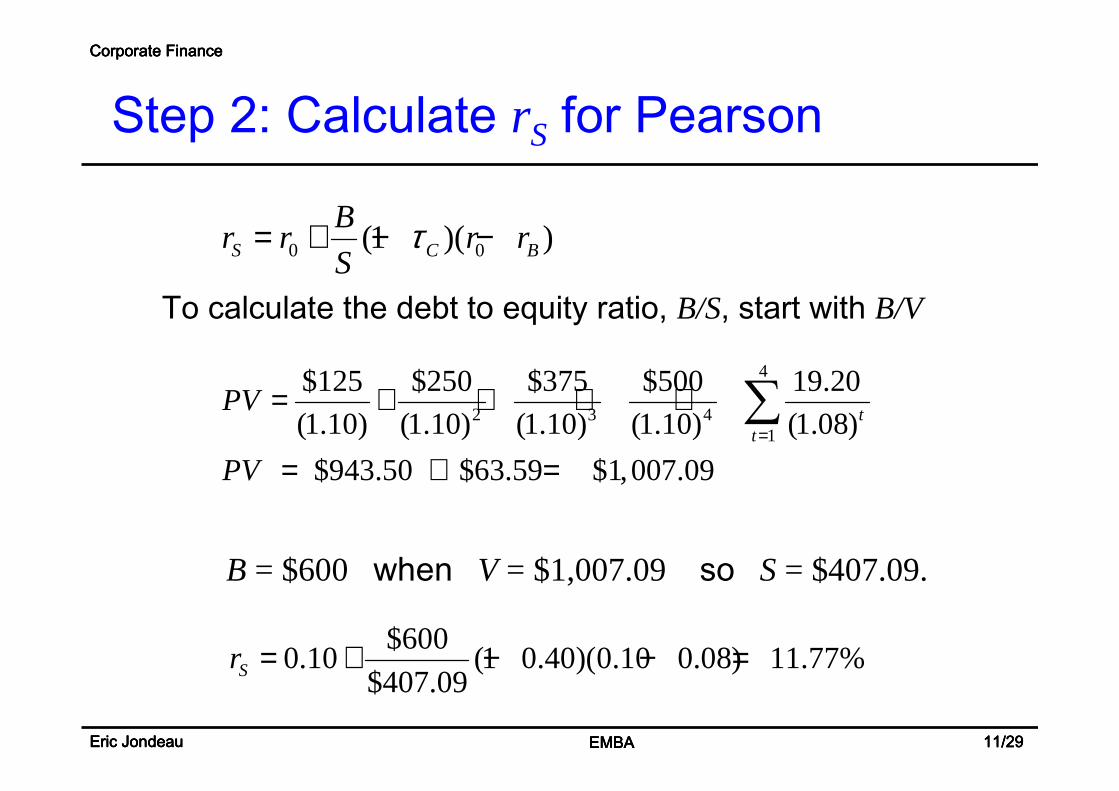

B = $600 when V = $1,007.09 so S = $407.09.

To calculate the debt to equity ratio, B/S, start with B/V

0 0(1 )( )S C B

Br r r r

Sτ= + − −

4

2 3 41

$125 $250 $375 $500 19.20

(1.10) (1.10) (1.10) (1.10) (1.08)

$943.50 $63.59 $1,007.09

tt

PV

PV=

= + + + +

= + =

∑

$6000.10 (1 0.40)(0.10 0.08) 11.77%

$407.09Sr = + − − =

EMBAEMBAEMBAEMBA 11/2911/2911/2911/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

Step 2: Calculate rS for Pearson

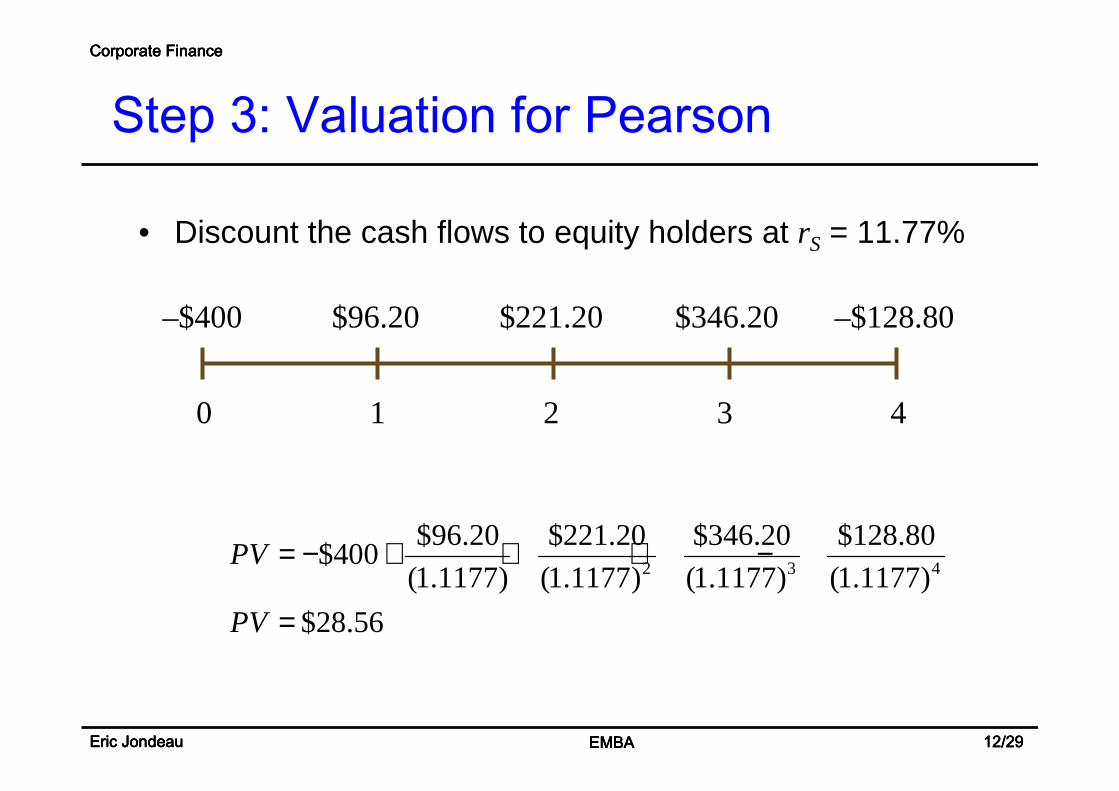

• Discount the cash flows to equity holders at rS = 11.77%

0 1 2 3 4

–$400 $96.20 $221.20 $346.20 –$128.80

2 3 4

$96.20 $221.20 $346.20 $128.80$400

(1.1177) (1.1177) (1.1177) (1.1177)

$28.56

PV

PV

= − + + + −

=

EMBAEMBAEMBAEMBA 12/2912/2912/2912/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

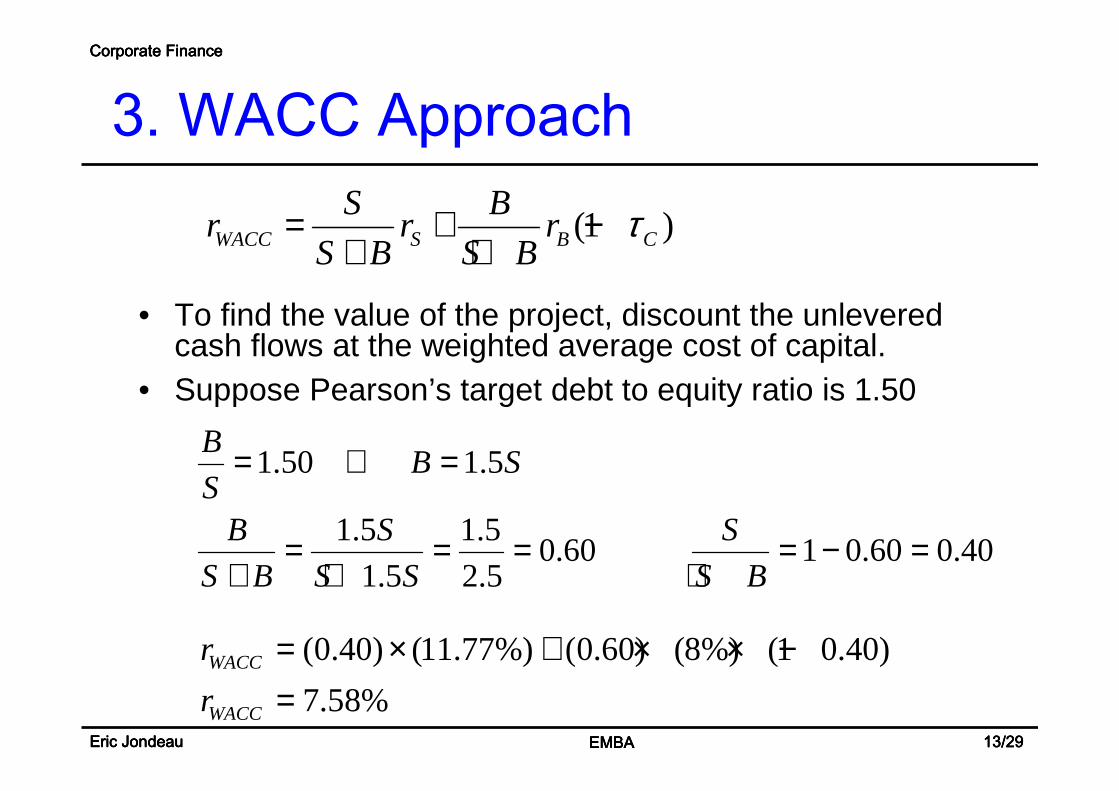

Step 3: Valuation for Pearson

• To find the value of the project, discount the unlevered cash flows at the weighted average cost of capital.

• Suppose Pearson’s target debt to equity ratio is 1.50

(1 )WACC S B C

S Br r r

S B S Bτ= + −

+ +

1.50 1.5

1.5 1.50.60 1 0.60 0.40

1.5 2.5

BB S

SB S S

S B S S S B

= ⇔ =

= = = = − =+ + +

EMBAEMBAEMBAEMBA 13/2913/2913/2913/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

3. WACC Approach

(0.40) (11.77%) (0.60) (8%) (1 0.40)

7.58%WACC

WACC

r

r

= × + × × −=

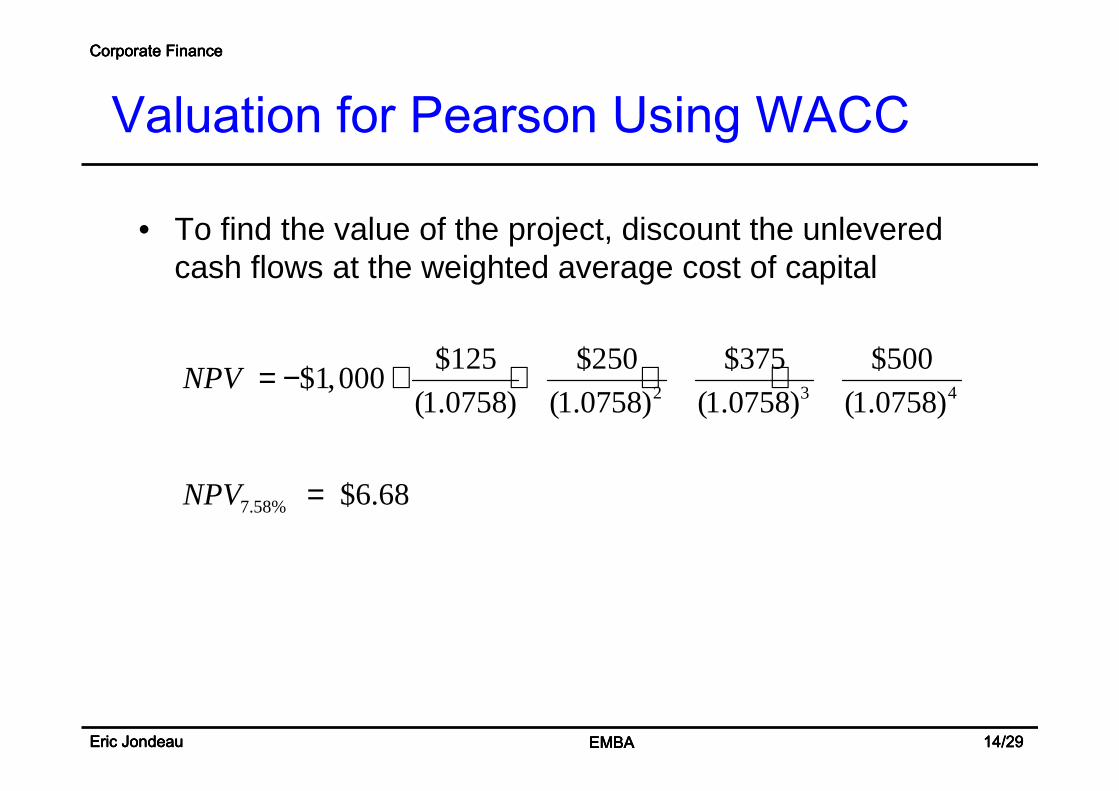

• To find the value of the project, discount the unlevered cash flows at the weighted average cost of capital

2 3 4

7.58%

$125 $250 $375 $500$1,000

(1.0758) (1.0758) (1.0758) (1.0758)

$6.68

NPV

NPV

= − + + + +

=

EMBAEMBAEMBAEMBA 14/2914/2914/2914/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

Valuation for Pearson Using WACC

• All three approaches attempt the same task: Valuation in the presence of debt financing.

• Guidelines:– Use WACC or FTE if the firm’s target debt-to-value ratio

applies to the project over the life of the project.– Use the APV if the project’s level of debt is known over

the life of the project.

• In the real world, the WACC is the most widely used by far.

EMBAEMBAEMBAEMBA 15/2915/2915/2915/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

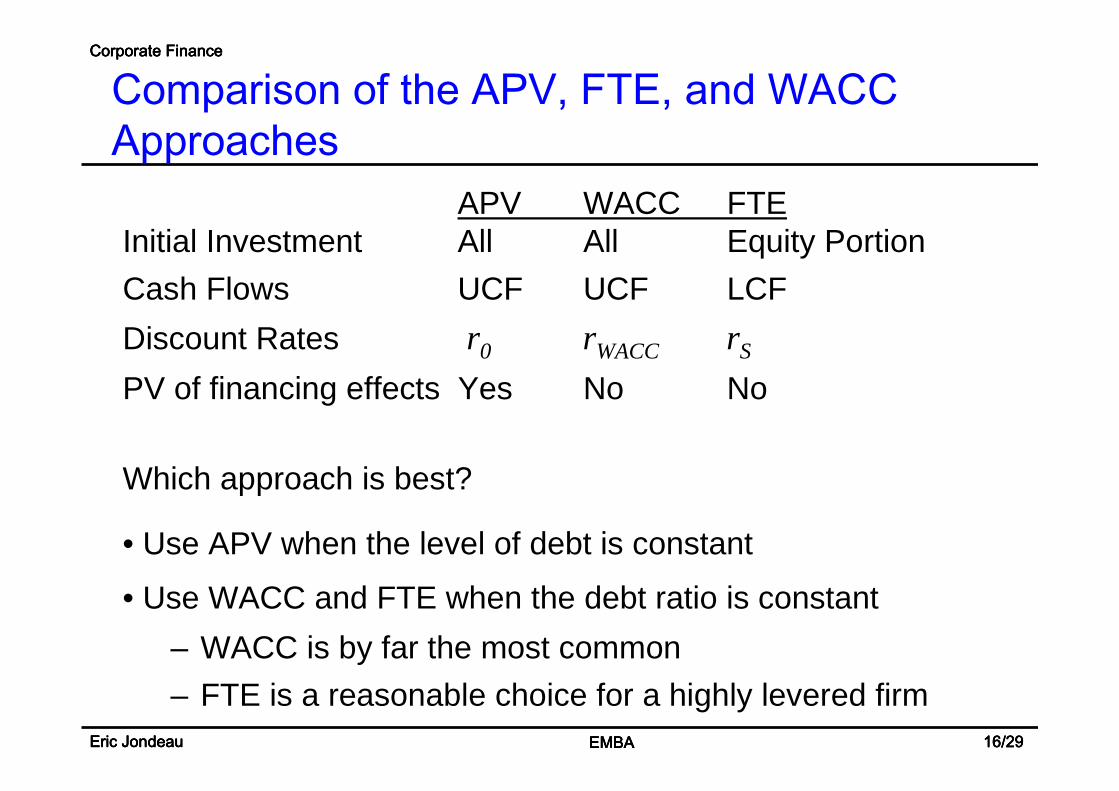

4. Comparison of the APV, FTE, and WACC Approaches

APV WACC FTEInitial Investment All All Equity Portion

Cash Flows UCF UCF LCF

Discount Rates r0 rWACC rS

PV of financing effects Yes No No

Which approach is best?

• Use APV when the level of debt is constant

• Use WACC and FTE when the debt ratio is constant

– WACC is by far the most common

– FTE is a reasonable choice for a highly levered firmEMBAEMBAEMBAEMBA 16/2916/2916/2916/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

Comparison of the APV, FTE, and WACC Approaches

• A scale-enhancing project is one where the project is similar to those of the existing firm.

• In the real world, executives would make the assumption that the business risk of the non-scale-enhancing project would be about equal to the business risk of firms already in the business.

• No exact formula exists for this. Some executives might select a discount rate slightly higher on the assumption that the new project is somewhat riskier since it is a new entrant.

EMBAEMBAEMBAEMBA 17/2917/2917/2917/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

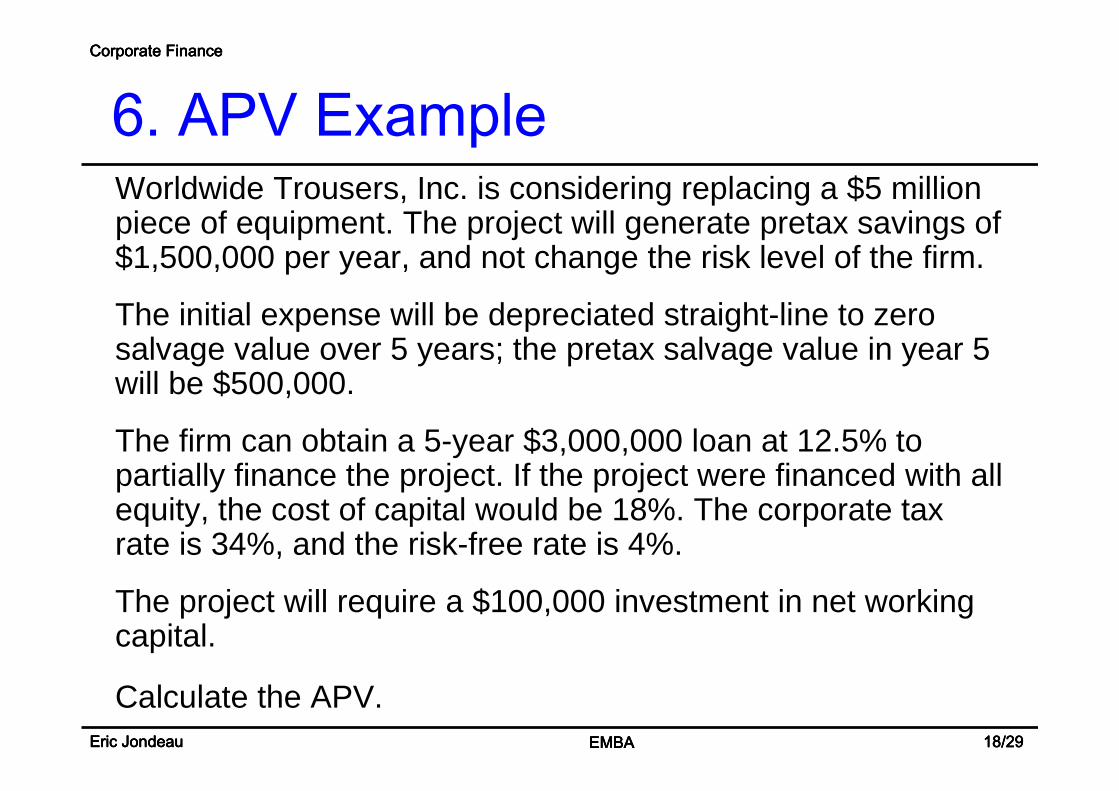

5. Capital Budgeting When the Discount Rate Must Be Estimated

Worldwide Trousers, Inc. is considering replacing a $5 million piece of equipment. The project will generate pretax savings of $1,500,000 per year, and not change the risk level of the firm.

The initial expense will be depreciated straight-line to zero salvage value over 5 years; the pretax salvage value in year 5 will be $500,000.

The firm can obtain a 5-year $3,000,000 loan at 12.5% to partially finance the project. If the project were financed with all equity, the cost of capital would be 18%. The corporate tax rate is 34%, and the risk-free rate is 4%.

The project will require a $100,000 investment in net working capital.

Calculate the APV.EMBAEMBAEMBAEMBA 18/2918/2918/2918/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

6. APV Example

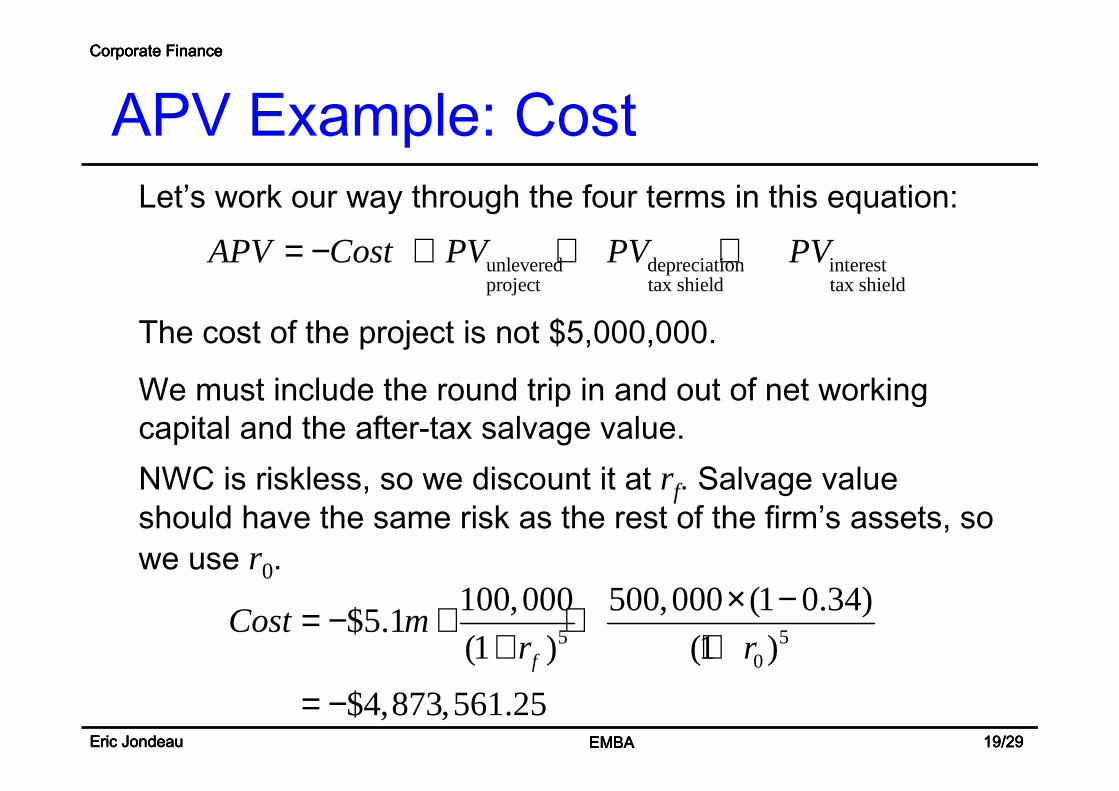

The cost of the project is not $5,000,000.

We must include the round trip in and out of net working capital and the after-tax salvage value.

Let’s work our way through the four terms in this equation:

NWC is riskless, so we discount it at rf. Salvage value should have the same risk as the rest of the firm’s assets, so we use r0.

unlevered depreciation interestproject tax shield tax shield

APV Cost PV PV PV= − + + +

5 50

100,000 500,000 (1 0.34)$5.1

(1 ) (1 )

$4,873,561.25f

Cost mr r

× −= − + ++ +

= −EMBAEMBAEMBAEMBA 19/2919/2919/2919/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

APV Example: Cost

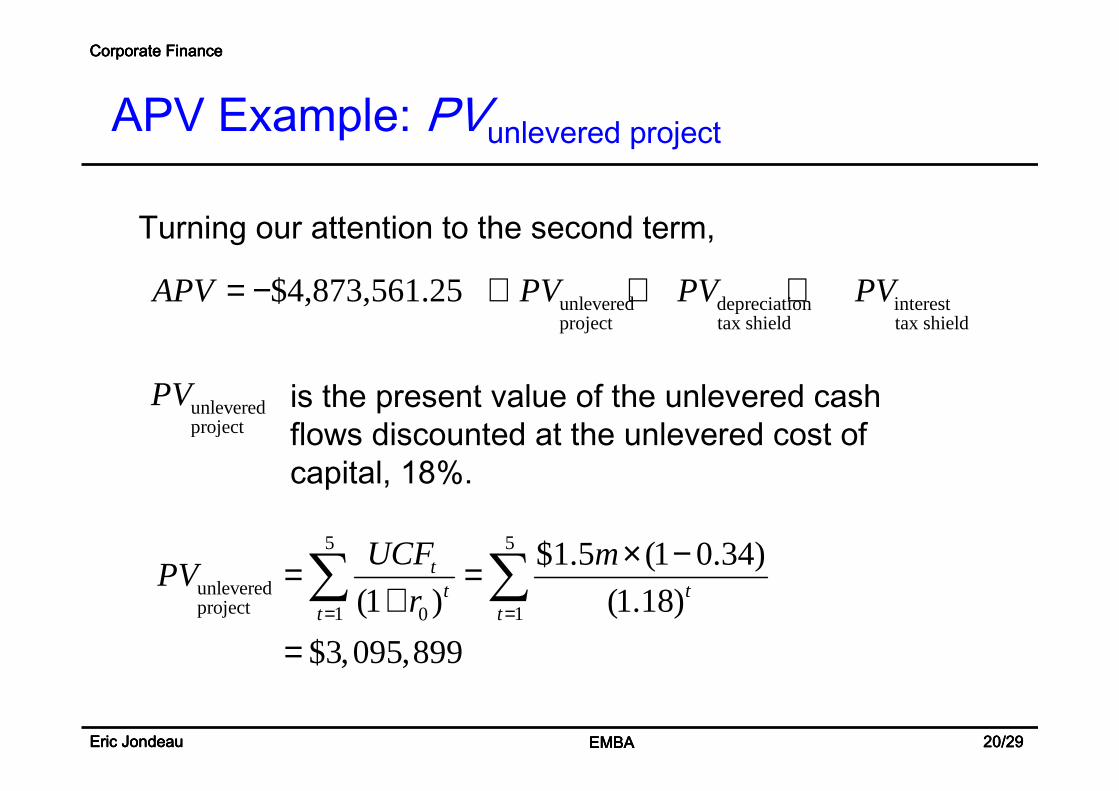

is the present value of the unlevered cash flows discounted at the unlevered cost of capital, 18%.

Turning our attention to the second term,

unlevered depreciation interestproject tax shield tax shield

$4,873,561.25 APV PV PV PV= − + + +

unleveredproject

PV

5 5

unleveredproject 1 10

$1.5 (1 0.34)

(1 ) (1.18)

$3,095,899

tt t

t t

UCF mPV

r= =

× −= =+

=

∑ ∑

EMBAEMBAEMBAEMBA 20/2920/2920/2920/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

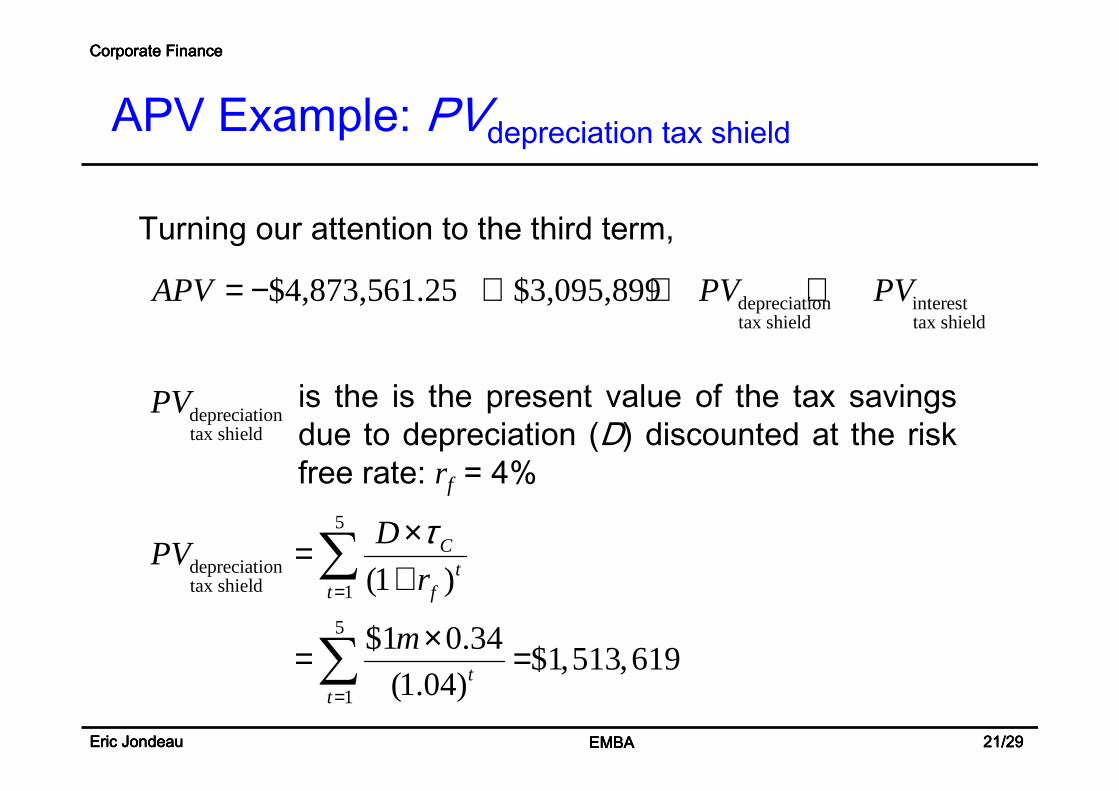

APV Example: PVunlevered project

is the is the present value of the tax savings due to depreciation (D) discounted at the risk free rate: rf = 4%

Turning our attention to the third term,

depreciation interesttax shield tax shield

$4,873,561.25 $3,095,899 APV PV PV= − + + +

depreciationtax shield

PV

5

depreciationtax shield 1

5

1

(1 )

$1 0.34$1,513,619

(1.04)

Ct

t f

tt

DPV

r

m

τ=

=

×=+

×= =

∑

∑EMBAEMBAEMBAEMBA 21/2921/2921/2921/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

APV Example: PVdepreciation tax shield

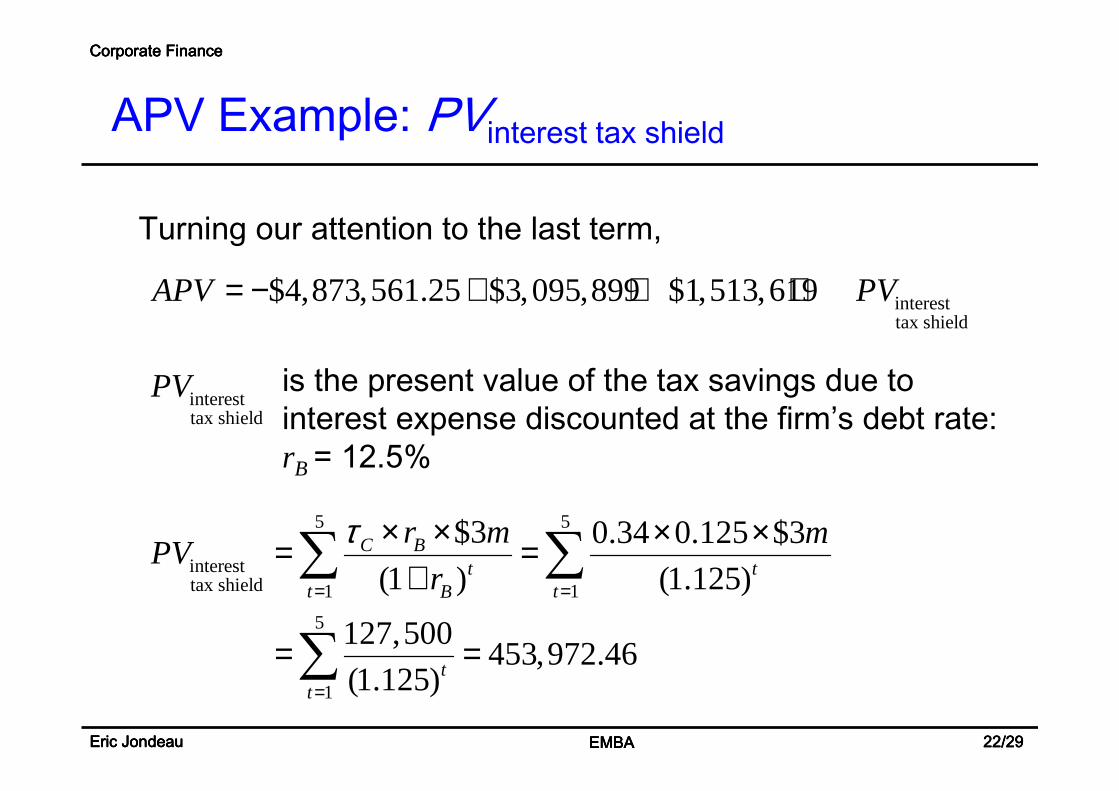

is the present value of the tax savings due to interest expense discounted at the firm’s debt rate: rB = 12.5%

Turning our attention to the last term,

interesttax shield

$4,873,561.25 $3,095,899 $1,513,619 APV PV= − + + +

interesttax shield

PV

5 5

interesttax shield 1 1

5

1

$3 0.34 0.125 $3

(1 ) (1.125)

127,500453,972.46

(1.125)

C Bt t

t tB

tt

r m mPV

r

τ= =

=

× × × ×= =+

= =

∑ ∑

∑

EMBAEMBAEMBAEMBA 22/2922/2922/2922/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

APV Example: PVinterest tax shield

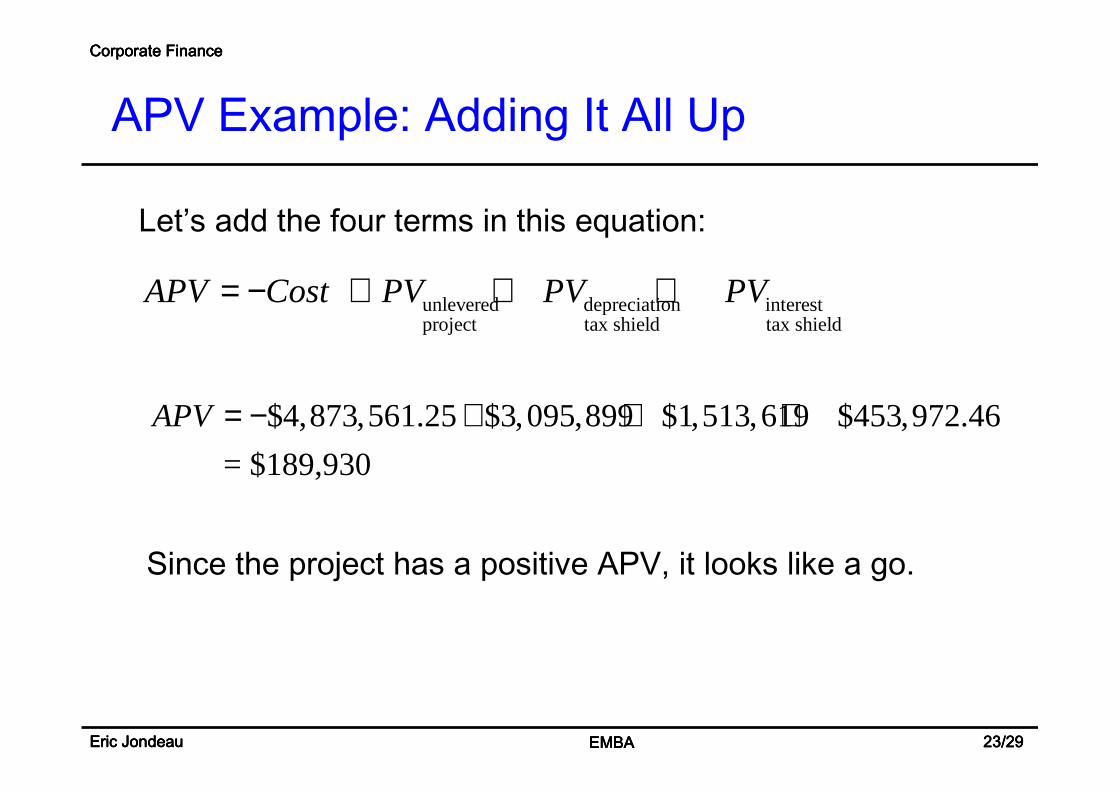

Since the project has a positive APV, it looks like a go.

Let’s add the four terms in this equation:

unlevered depreciation interestproject tax shield tax shield

APV Cost PV PV PV= − + + +

$4,873,561.25 $3,095,899 $1,513,619 $453,972.46

= $189,930

APV = − + + +

EMBAEMBAEMBAEMBA 23/2923/2923/2923/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

APV Example: Adding It All Up

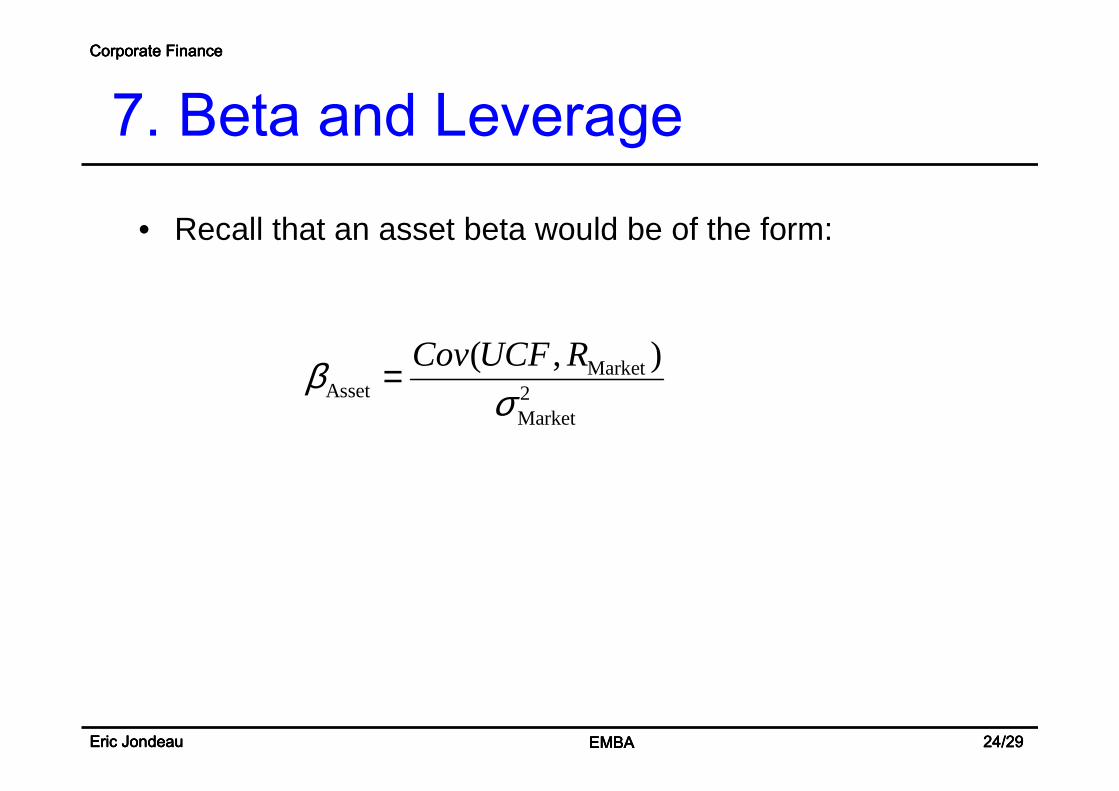

• Recall that an asset beta would be of the form:

MarketAsset 2

Market

( , )Cov UCF Rβσ

=

EMBAEMBAEMBAEMBA 24/2924/2924/2924/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

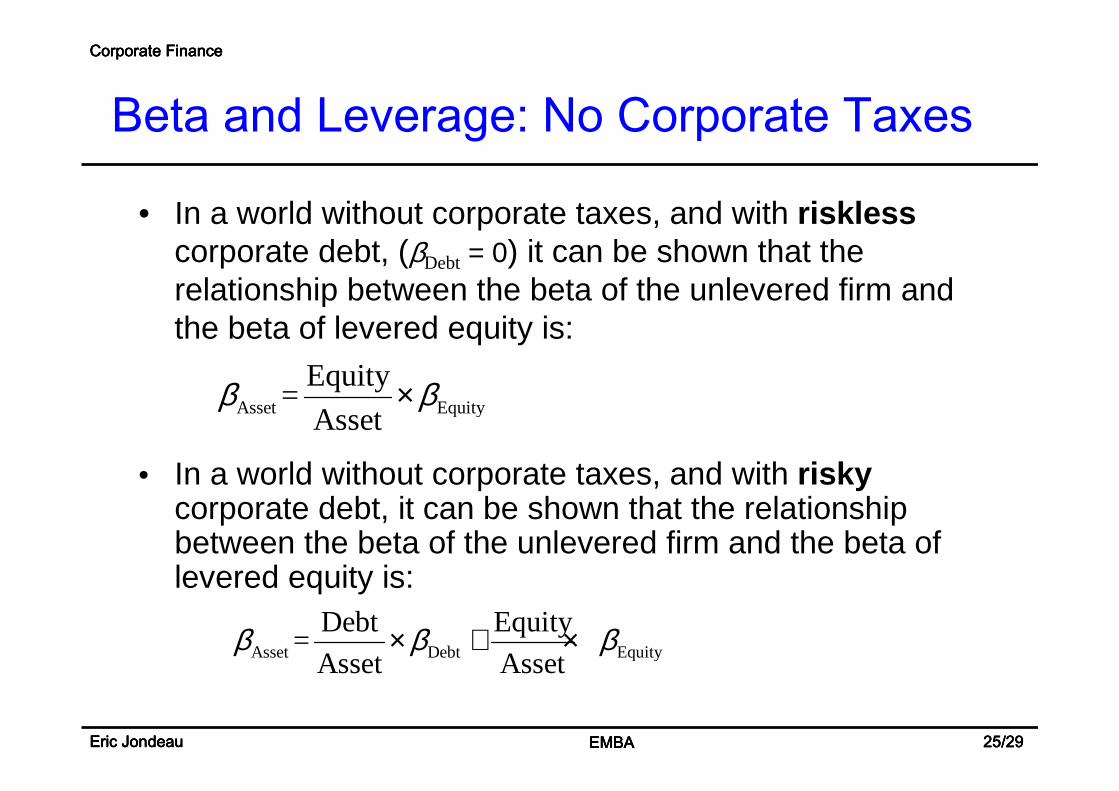

7. Beta and Leverage

• In a world without corporate taxes, and with risklesscorporate debt, (βDebt = 0) it can be shown that the relationship between the beta of the unlevered firm and the beta of levered equity is:

• In a world without corporate taxes, and with riskycorporate debt, it can be shown that the relationship between the beta of the unlevered firm and the beta of levered equity is:

Asset Equity

Equity=

Assetβ β×

Asset Debt Equity

Debt Equity=

Asset Assetβ β β× + ×

EMBAEMBAEMBAEMBA 25/2925/2925/2925/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

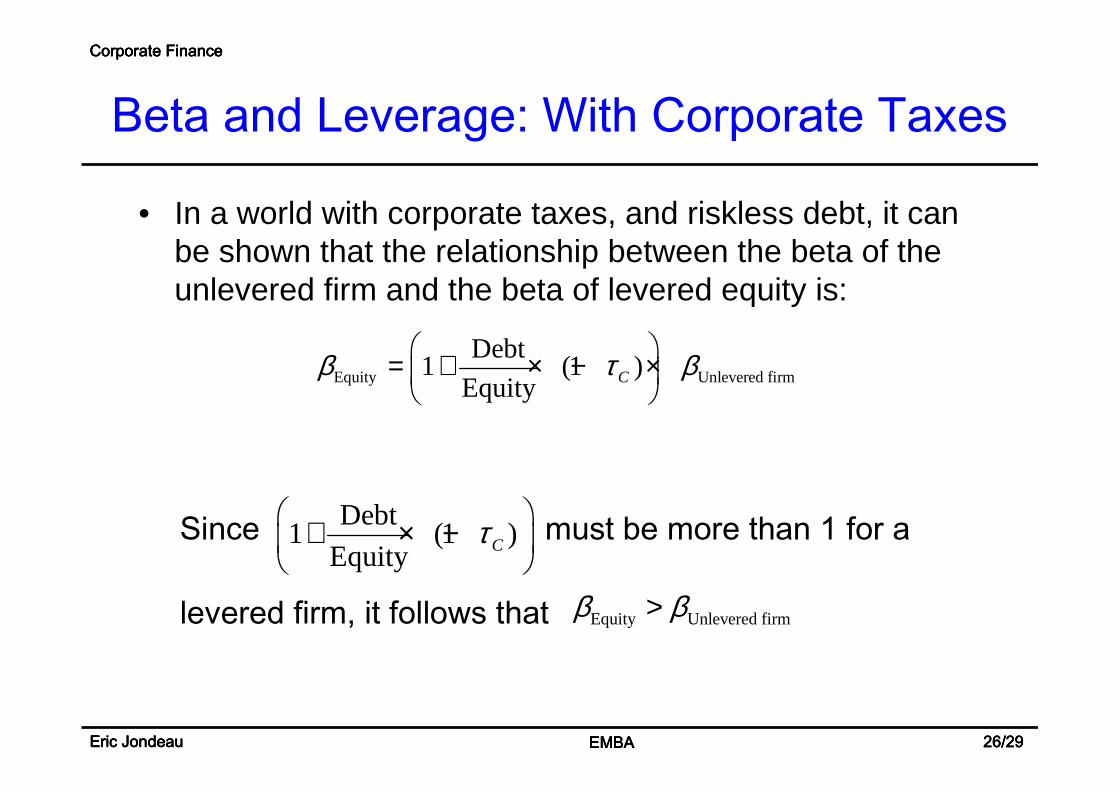

Beta and Leverage: No Corporate Taxes

• In a world with corporate taxes, and riskless debt, it can be shown that the relationship between the beta of the unlevered firm and the beta of levered equity is:

Since must be more than 1 for a

levered firm, it follows that

Equity Unlevered firm

Debt1 (1 )

Equity Cβ τ β = + × − ×

Debt1 (1 )

Equity Cτ + × −

Equity Unlevered firmβ β>

EMBAEMBAEMBAEMBA 26/2926/2926/2926/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

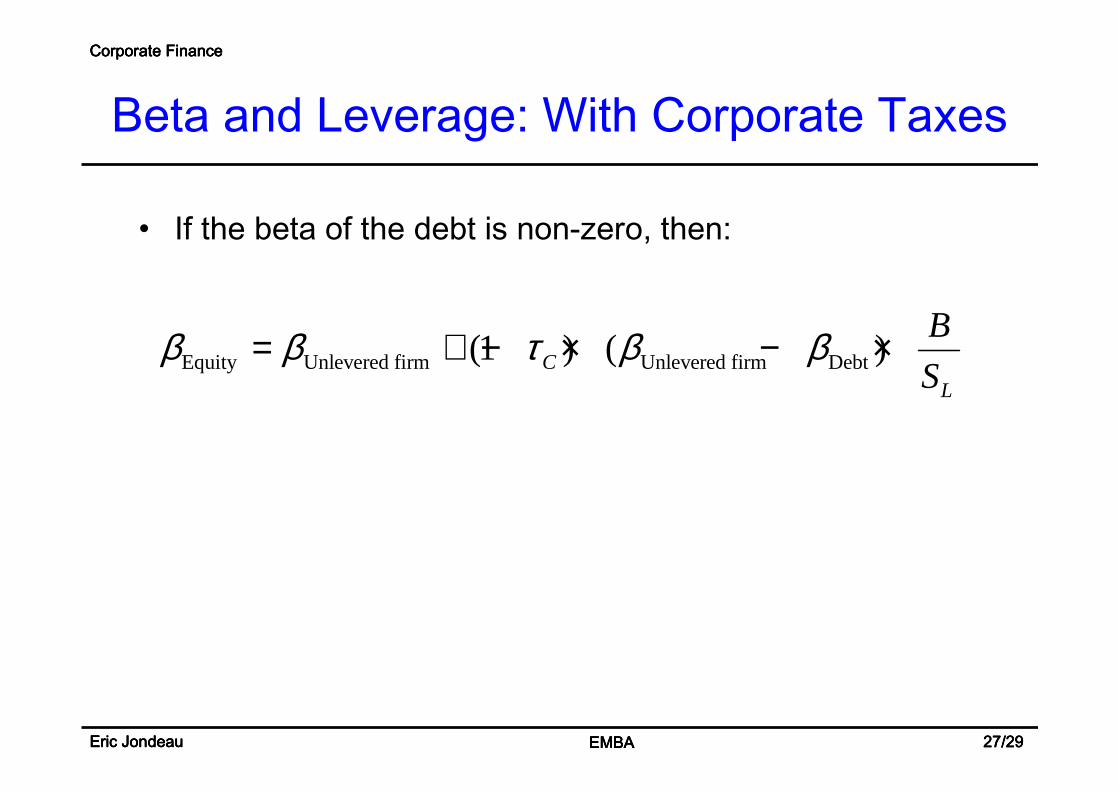

Beta and Leverage: With Corporate Taxes

• If the beta of the debt is non-zero, then:

Equity Unlevered firm Unlevered firm Debt(1 ) ( )CL

B

Sβ β τ β β= + − × − ×

EMBAEMBAEMBAEMBA 27/2927/2927/2927/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

Beta and Leverage: With Corporate Taxes

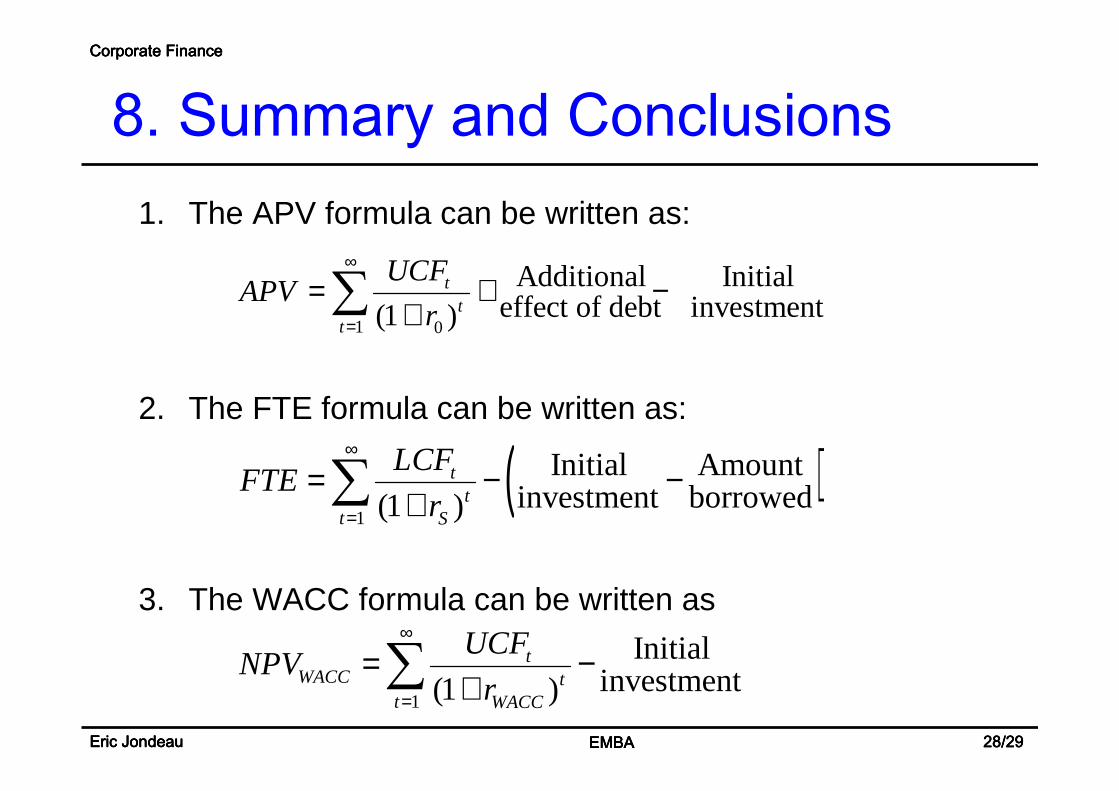

1. The APV formula can be written as:

2. The FTE formula can be written as:

3. The WACC formula can be written as

1 0

Additional Initialeffect of debt investment(1 )

tt

t

UCFAPV

r

∞

=

= + −+∑

( )1

Initial Amountinvestment borrowed(1 )

tt

t S

LCFFTE

r

∞

=

= − −+∑

1

Initialinvestment(1 )

tWACC t

t WACC

UCFNPV

r

∞

=

= −+∑

EMBAEMBAEMBAEMBA 28/2928/2928/2928/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

8. Summary and Conclusions

4. Use the WACC or FTE if the firm's target debt to value ratio applies to the project over its life.• WACC is the most commonly used by far.• FTE has appeal for a firm deeply in debt.

5 The APV method is used if the level of debt is known over the project’s life.• The APV method is frequently used for special

situations like interest subsidies, LBOs, and leases.

6 The beta of the equity of the firm is positively related to the leverage of the firm.

EMBAEMBAEMBAEMBA 29/2929/2929/2929/29Eric JondeauEric JondeauEric JondeauEric Jondeau

Corporate FinanceCorporate FinanceCorporate FinanceCorporate Finance

Summary and Conclusions