Embed Size (px)

Citation preview

1Private equity briefing: SEA

Private equitybriefing:Southeast AsiaJune 2015

2Private equity briefing: SEA

This quarterly briefing offersyou a roundup of the privateequity deals and capitalactivities across majorsectors in the quarter andtrends that are shapinginvestment decisions today.

It distills the perspectives ofour team of subject-matterprofessionals in the regioninto pertinent insights tokeep you ahead in navigatingthe private equity landscape.

3Private equity briefing: SEA

01Outlook

02Investments

03Exits

04Fund-raising

05Sector infocus:education

06Ourservices:CorporateFinanceStrategy

Contents4 6 8 9 11 13

4Private equity briefing: SEA

Outlook

The first quarter of 2015 has seen private equity (PE) activitycontinue where it left off in 2014, with deal volumes remaining high.This level of activity is expected to increase further with PE housesaggressively pursuing both investments and exits.There was a total of 33 PE deals executed in 1Q15, 43% higher than the same period in 2014, while the overallvalue was also considerably higher at US$672m compared with US$263m in 2014. This particularly positiveoutlook is set to continue in 2015.

Technology sector activity on the riseThe first quarter saw the continued rise of PE and venture capital (VC) investment into technology companies.In 1Q15, 22% (seven deals) of the total number deals involved the technology sector, continuing the trend thatstarted in 2014, which saw 34 of such deals across the year. The majority of these deals were sub-US$5minvestments.

This increased activity is not surprising, given the significant number of technology funds that have establisheda presence in the region, particularly in Singapore, over the past 24 months. These funds have taken the formof both new and established global funds looking to take advantage of the Southeast Asian market.

Another key trend is the increasing number of US$100m-plus investments. In the past 12 months, technologycompanies such as GrabTaxi, Garena and Lazada have attracted worthy levels of investments, and this looks toincrease in the forthcoming months.

Clearly, now is the time for PE and VC investments into the technology sector. Funds looking to get ahead needto act quickly to establish a strong reputation in the technology sector so as to build their portfolio and gain afoothold in the market. Funds that stall will likely struggle to compete with their more successful counterpartsand new market entrants.

01

5Private equity briefing: SEA

Heightened competitionDry powder across Asia is understood to be in the excess of US$100b, with Southeast Asia remaining as one ofthe key target geographies. With investors pouring in cash, there is increasing pressure on PE houses to investcapital, resulting in considerable competition for prize assets.

The abundance of capital is resulting in the willingness by PE houses to increase the multiples paid forinvestments, particularly in an auction process, with valuations further supported by the current low-cost debtenvironment. As a result, PE houses are spending considerable efforts to identify off-market deals.

EY‘s 2015 global private equity survey, which surveyed 256 CFOs and investors, has highlighted that globallyand regionally, PE houses are preparing for an influx of capital into Asia-Pacific, which will only serve toheighten the level of competition.

For PE funds to succeed, they need to focus on differentiation, whether by geography, sub-sector, people orbranding. Innovative strategies including partnerships, carve-outs and roll-ups will increasingly play a part in thesuccess of deals. It is also important to focus on value creation, and this is where specialist portfolio managersand advisors can provide investment professionals with deep insights.

The outlook for 2015 remains very exciting. We expect a continued increase in PE deals across Asia, particularlySoutheast Asia.

Luke PaisAsean Leader,M&A

“Private equity activity has got off to a confident start in 2015. If the first quarteris anything to go by, the new investment theme for 2015 is ‘the rise of tech’.”

6Private equity briefing: SEA

Investments02

Figure 1: Investment activity

Source: Thomson One, Dealogic and Mergermarket

0

10

20

30

40

0

400

800

1,200

1,600

2,000

Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015

Dea

lcou

nt

Dea

lval

ue(U

S$m

)

Small Mid

• The first quarter of 2015 saw the continued increasein the number of investments, with a total of 32 deals.Despite the large number of deals, the total reportedamount of investments was only US$209m, as thevalues of 26 deals were not disclosed.

• The consumer sector, which saw seven completeddeals, continues to dominate PE investments. One ofthe most notable deals was KV Asia’s investment intoAalst Chocolate in March.

• The first quarter also saw a significant number (sevendeals) of technology deals, which includes Garena and99.co. Garena, Singapore-based online gamingplatform, completed a new round of funding led byThe Ontario Teachers’ Pension Plan, while Singaporeproperty site 99.co, raised an additional round offunding led by Sequoia Capital. The sizes of both dealswere not disclosed.

• Investments have remained focused on the smalland mid-market and into companies based inSingapore (14) and Indonesia (13).

7Private Equity Briefing: SEA

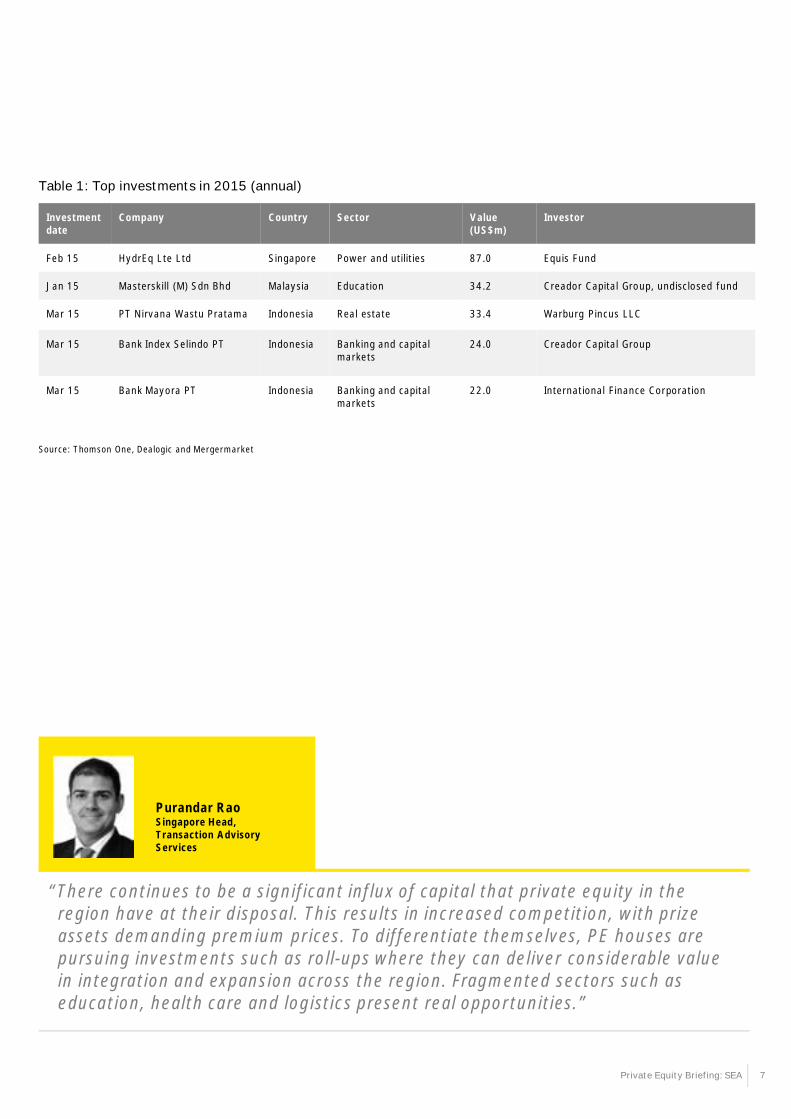

Table 1: Top investments in 2015 (annual)

Investmentdate

Company Country Sector Value(US$m)

Investor

Feb 15 HydrEq Lte Ltd Singapore Power and utilities 87.0 Equis Fund

Jan 15 Masterskill (M) Sdn Bhd Malaysia Education 34.2 Creador Capital Group, undisclosed fund

Mar 15 PT Nirvana Wastu Pratama Indonesia Real estate 33.4 Warburg Pincus LLC

Mar 15 Bank Index Selindo PT Indonesia Banking and capitalmarkets

24.0 Creador Capital Group

Mar 15 Bank Mayora PT Indonesia Banking and capitalmarkets

22.0 International Finance Corporation

Purandar RaoSingapore Head,Transaction AdvisoryServices

“There continues to be a significant influx of capital that private equity in theregion have at their disposal. This results in increased competition, with prizeassets demanding premium prices. To differentiate themselves, PE houses arepursuing investments such as roll-ups where they can deliver considerable valuein integration and expansion across the region. Fragmented sectors such aseducation, health care and logistics present real opportunities.”

Source: Thomson One, Dealogic and Mergermarket

8Private Equity Briefing: SEA

• Exit activity remained low in 1Q15, with only one dealrecorded. A number of exits continue to be executedbut go unreported.

• The one deal that was reported is TPG Capital’s andNorthstar Pacific Partners’ partial exit from theirinvestment in Bank Tabungan Pensiunan Nasional ina US$463m-deal with Sumitomo Corporation.

• This deal reflects the continued trend of bankingand capital markets providing the larger exits inthe region.

• It is becoming evident that a number of PE housesare holding on to investments for a period longerthan initially anticipated in order to generate themoney multiple required. This creates additional riskfor PE when undertaking investments, since there isan increased likelihood that these investments willincur a change in the business cycle during theholding period.

• Driven by this and the ever-increasing amount of drypowder, a rise in the level of secondary buy-outs inSoutheast Asia in the coming years is expected.

Exits03

Figure 2: Exit activity

Source: Thomson One, Dealogic and Mergermarket

0

4

8

12

0

500

1,000

1,500

2,000

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Dea

lcou

nt

Dea

lval

ueU

S$m

Small Mid Large Deal count

Joongshik WangAsean Leader,Corporate FinanceStrategy

“Due to mixed views on asset valuation in Southeast Asia, various scheduled exitshave been discussed but delayed. One of the important momentums for deal exitswill be driven by strategic investors who are less price-sensitive but look for long-term synergies.”

9Private Equity Briefing: SEA

Fund-raising04

• The first quarter of 2015 saw a resurgence in the levelof funds being closed. There were four funds closed ata total commitment in excess of US$5b.

• This level of activity in the opening quarter of 2015 isconsistent with what has been observed in previousperiods as fund-raising activity peaks in the first halfof the year.

• The largest fund closed was Baring Asia VI, raising astaggering US$4b. This was the largest private equity

fund ever raised by an Asia-based PE firm, withinvestors having to be scaled back from the first closedue to the excess demand. This reflects the highinvestment interest into Asia, and increasingrecognition by investors on the value of regionallybased funds.

Figure 3: PE fund-raising with Southeast Asia focus

0

1

2

3

4

5

6

7

0

2,000

4,000

6,000

8,000

Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015

Cou

nt

US$

m

10Private Equity Briefing: SEA

Table 2: Top funds closed with Southeast Asia focus in 2015 (annual)

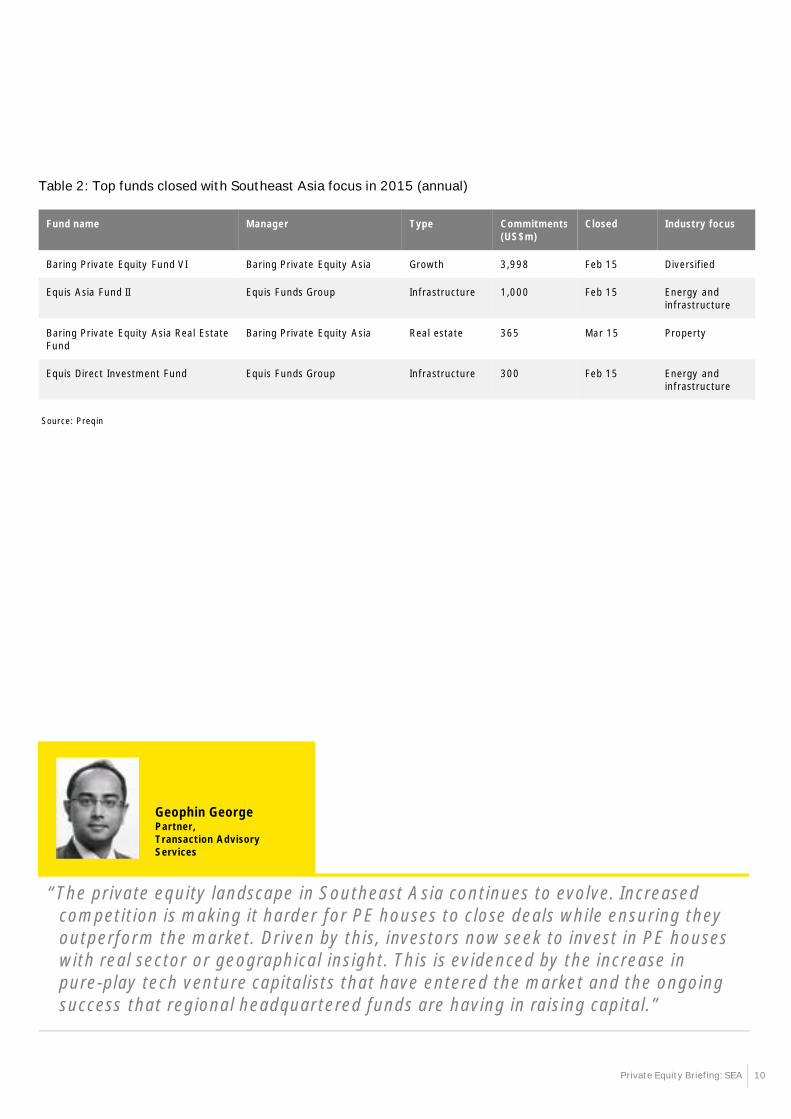

Fund name Manager Type Commitments(US$m)

Closed Industry focus

Baring Private Equity Fund VI Baring Private Equity Asia Growth 3,998 Feb 15 Diversified

Equis Asia Fund II Equis Funds Group Infrastructure 1,000 Feb 15 Energy andinfrastructure

Baring Private Equity Asia Real EstateFund

Baring Private Equity Asia Real estate 365 Mar 15 Property

Equis Direct Investment Fund Equis Funds Group Infrastructure 300 Feb 15 Energy andinfrastructure

Geophin GeorgePartner,Transaction AdvisoryServices

“The private equity landscape in Southeast Asia continues to evolve. Increasedcompetition is making it harder for PE houses to close deals while ensuring theyoutperform the market. Driven by this, investors now seek to invest in PE houseswith real sector or geographical insight. This is evidenced by the increase inpure-play tech venture capitalists that have entered the market and the ongoingsuccess that regional headquartered funds are having in raising capital.”

Source: Preqin

11Private Equity Briefing: SEA

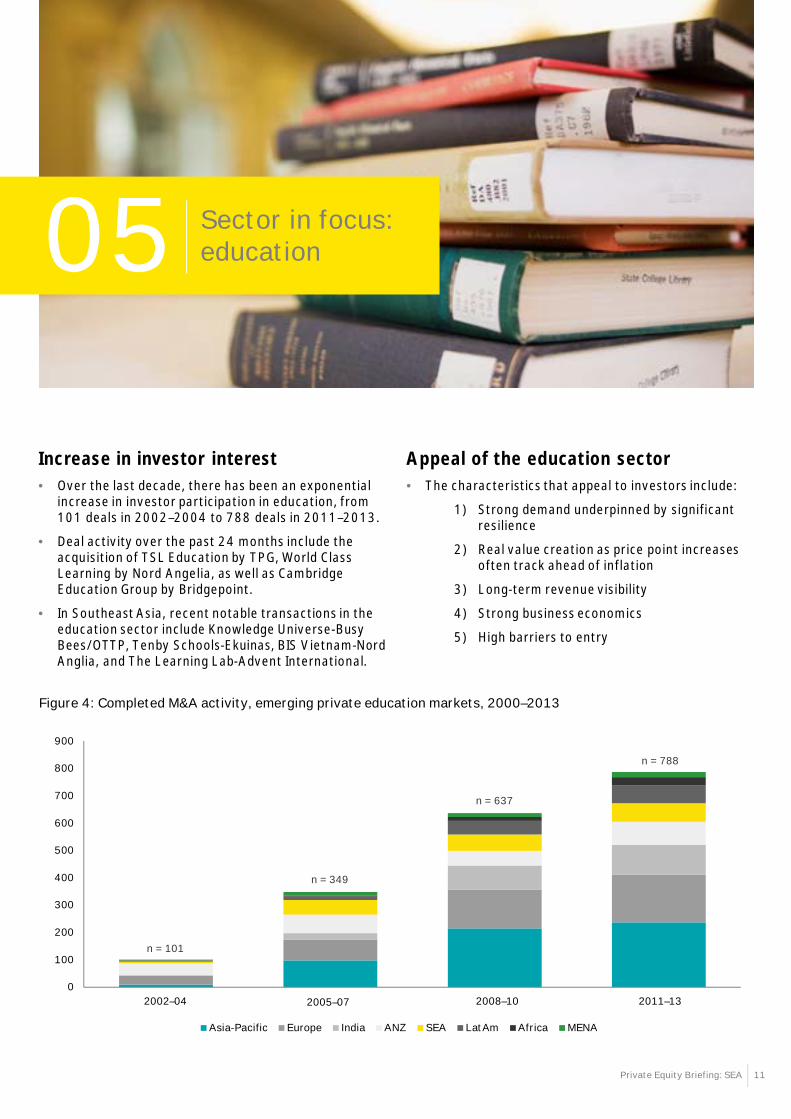

Increase in investor interest• Over the last decade, there has been an exponential

increase in investor participation in education, from101 deals in 2002–2004 to 788 deals in 2011–2013.

• Deal activity over the past 24 months include theacquisition of TSL Education by TPG, World ClassLearning by Nord Angelia, as well as CambridgeEducation Group by Bridgepoint.

• In Southeast Asia, recent notable transactions in theeducation sector include Knowledge Universe-BusyBees/OTTP, Tenby Schools-Ekuinas, BIS Vietnam-NordAnglia, and The Learning Lab-Advent International.

Appeal of the education sector• The characteristics that appeal to investors include:

1) Strong demand underpinned by significantresilience

2) Real value creation as price point increasesoften track ahead of inflation

3) Long-term revenue visibility

4) Strong business economics

5) High barriers to entry

0

100

200

300

400

500

600

700

800

900

2002-2004 2005-2007 2008-2010 2011-2013

Asia-Pacific Europe India ANZ SEA LatAm Africa MENA

Figure 4: Completed M&A activity, emerging private education markets, 2000–2013

Sector in focus:education05

n = 101

n = 349

n = 637

n = 788

2002–04 2008–10 2011–132005–07

12Private Equity Briefing: SEA

Key themes for investors

• Successful education platforms generate revenue and profit scale by rollingup smaller institutions.

• Significant value can be generated through sharing of best practicesacross institutions.

• Platforms outgrow single institutions due to scale and competitiveadvantage accrued from scale in student acquisition and marketing.

• A portfolio of education assets across geographies to mitigate any impactof country-specific macroeconomic, regulatory and competitive risk shouldbe considered.

• Successful platforms have globally diversified portfolios.

• Premium-priced higher education and K-12 assets generate 30–40%EBITDA margins.

• Certain education companies depend on a small proportion of highlyprofitable premium schools to generate a disproportionate share of EBITDA.

• Business: top-line initiatives, operational best practices.

• Financial: five characteristics of education, scarcity of scale assets,premium for entry.

Platform play

Multi-geographicfocus

Premium price points

Value-creation drivers

Karan KhemkaManaging Director,Pathenon-EY

“The education sector offers investors opportunities to benefit from the demandfor quality education by the middle class. Typically, demand for private educationgrows at a multiple of GDP growth and can be very predictable.”

13Private Equity Briefing: SEA

Our services:Corporate FinanceStrategy06

Our Corporate Finance Strategy teamsupports PE clients across the deal cycle.We help clients enter new markets andindustries, perform commercial duediligence on targets and create value intheir portfolio companies.

► Focus: Deliver value creationservices across the PE investmentlife cycle

► Dedicated PE experience:Dedicated team comprising formerPE operating partners, seasonedoperating executives andmanagement consultants

► Broad functional knowledge:Capabilities in strategy, M&A andall core operating functions;experience in revenueenhancement, cost reduction,human capital andchange management

► Deep sector experience: Primaryfocus in oil and gas, consumer,industrial, and health care; ability totap into sub-sector specialists

► Accelerated approach: Customizedapproach that is highly responsiveand provides accelerated realizationof benefits

► Global capabilities: Dedicated teamthat has extensive cross-borderexperience with access to morethan 30,000 consultants operatingin 140 countries with deep industryand functional know-how

Our capabilities

The two key pillars of our value proposition: sector know-howand unmatched platform

Our team in Singapore comprises 25 seasoned global strategyconsultants with deep knowledge in consumer goods, naturalresources and financial services.

Within these industry segments, we have detailedunderstanding of the Southeast Asian market landscape and astrong network of contacts. Collectively, we have conductedmore than 100 commercial due diligence projects in theregion. At the same time, the EY platform gives us access toextensive cross-border experience with approximately 30,000consultants operating in 140 countries with outstandingfunctional capability across geographies. Our platform allowsus to span strategy and operations seamlessly.

The Parthenon-EY edgeIn September 2014, The Parthenon Group – a global strategyconsultancy with 300 professionals in offices in Boston,London, Mumbai, San Francisco, Shanghai and Singapore –joined EY’s Corporate Finance practice.

Parthenon-EY is a leading advisor to the global educationsector, and has completed more than 150 sector projects eachyear across 80 countries. Parthenon-EY advises at the C-suiteor Managing Partner level of the largest operators andinvestors in the education sector. Over the last two years,Parthenon-EY has advised on the largest transactions in theeducation sector, which saw capital investment of over US$5b.

Key driver for superior investment returns in Southeast AsiaOne of the largest areas of value creation for PE is operationalimprovement. A value creation thesis and plan is key tosuccessful PE investing in Southeast Asia. Our experiencesuggests that advisors who have proven to deliver valueshould be involved very early on in the life cycle of aportfolio investment.

Our value creation capabilities cover key operating areas,namely revenue enhancement, margin improvement andcapital efficiency. Our typical results target 3–5% revenuegrowth, 8–15% EBITDA increase and 4–7% cash flow release,giving a rapid payback period on our fee investment for clients.

14Private Equity Briefing: SEA

Contact usService line contactsM&A

Luke [email protected]+ 65 6309 8094

Ching [email protected]

+ 65 6309 8995

Corporate Finance Strategy

Vikram [email protected]

+ 65 6309 8809

Joongshik [email protected]

+ 65 6309 8078

Transaction Support

Purandar [email protected]

+ 65 6309 6560

Geophin [email protected]

+ 65 6309 8168

Transaction Tax

Eng Ping [email protected]

+ 603 7495 8288

Darryl [email protected]

+ 65 6309 6800

Valuation & Business Modelling

Andre [email protected]

+ 65 6309 6214

Wouter van [email protected]

+ 65 6309 8878

Country contactsIndonesia

David [email protected]

+ 62 21 5289 5025

Sahala [email protected]

+ 62 21 5289 5210

Malaysia

George [email protected]

+ 60 3 7495 8700

Preman [email protected]

+ 60 3 7495 7811

Philippines and Guam

Renato [email protected]

+ 63 2 891 0307

Singapore

Purandar [email protected]

+ 65 6309 6560

Luke [email protected]

+ 65 6309 8094

Geophin [email protected]

+ 65 6309 8168

Sanjeev [email protected]

+ 65 6309 8688

Karan [email protected]

+ 65 6922 9460

Joongshik [email protected]

+ 65 6309 8078

Thailand

Ratana [email protected]

+ 66 2 264 0777

Piyanuch [email protected]

+ 66 2 264 9090

Vietnam

Anthony [email protected]

+ 84 8 3824 5252

Global contactsGlobal

Jeffrey [email protected]

+ 1 212 773 2889

Michael [email protected]

+ 1 214 969 0675

15Private Equity Briefing: SEA

16Private Equity Briefing: SEA

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transactionand advisory services. The insights and qualityservices we deliver help build trust and confidencein the capital markets and in economies the worldover. We develop outstanding leaders who team todeliver on our promises to all of our stakeholders.In so doing, we play a critical role in building abetter working world for our people, for our clientsand for our communities.

EY refers to the global organization, and mayrefer to one or more, of the member firms ofErnst & Young Global Limited, each of which is aseparate legal entity. Ernst & Young GlobalLimited, a UK company limited by guarantee,does not provide services to clients. For moreinformation about our organization, please visitey.com.

About EY’s Transaction Advisory Services

How you manage your capital agenda today willdefine your competitive position tomorrow. Wework with clients to create social and economicvalue by helping them make better, more-informeddecisions about strategically managing capital andtransactions in fast changing-markets. Whetheryou're preserving, optimizing, raising or investingcapital, EY’s Transaction Advisory Servicescombine a unique set of skills, insight andexperience to deliver focused advice. We help youdrive competitive advantage and increased returnsthrough improved decisions across all aspects ofyour capital agenda

© 2015 EYGM Limited.All Rights Reserved.

EYG no. FR0164

ED None

This material has been prepared for general informationalpurposes only and is not intended to be relied upon as accounting,tax, or other professional advice. Please refer to your advisorsfor specific advice.

ey.com