Embed Size (px)

Citation preview

Procedural Guidelines for AEPS

Page 1 of 69 National Payments Corporation of India

PROCEDURAL GUIDELINES

FOR

AADHAAR

ENABLED

PAYMENT

SYSTEM Version 1.4

Approved for Pilot launch by the Reserve Bank of India vide letter no. DPSS. CO. PD. No. 1584/ 02.017.001/ 2010-11 dated January 11 2011.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

Amendment History

Sr. Version number Summary of Change Change Month & Year

1 1.4 Initial Version January 2011 2 3

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

Procedural Guidelines for Aadhaar Enabled Payment System

1. Short title of the Service.

The new payment service offered by the National Payments Corporation of India to banks, financial institutions using ‘Aadhaar’, the Unique Identification Authority of India (UIDAI) issued unique identification number shall be known as ‘Aadhaar Enabled Payment System’ and shall be referred to as “AEPS” hereinafter.

2. This procedural guidelines document for AEPS of the National Payments Corporation of India is based on and has references to: a) MICRO-ATM STANDARDS report of the working group on technology issues of the

Indian Banks Association and UIDAI for banking services facilitated, hardware and interbank message flow.

b) AEPS Interface Specifications of National Payments Corporation of India. c) Aadhaar Authentication API and Devices Security Specifications and Biometric

Fingerprint Scanner Specifications of the Unique Identification Authority of India for Aadhaar authentication.

3. Definitions.

The acronyms/abbreviations used in this document with their descriptions and meanings are listed in Annexure-I.

4. Objectives of AEPS:

a) To empower a bank customer to use Aadhaar as his/her identity to access his/ her respective Aadhaar enabled bank account and perform basic banking transactions like balance enquiry, Cash deposit, cash withdrawal, remittances that are intrabank or interbank in nature, through a Business Correspondent.

b) To sub-serve the goal of Government of India (GoI) and Reserve Bank of India (RBI) in

furthering Financial Inclusion.

c) To sub-serve the goal of RBI in electronification of retail payments.

d) To enable banks to route the Aadhaar initiated interbank transactions through a central switching and clearing agency.

e) To facilitate disbursements of Government entitlements like NREGA, Social Security

pension, Handicapped Old Age Pension etc. of any Central or State Government bodies, using Aadhaar and authentication thereof as supported by UIDAI.

f) To facilitate inter-operability across banks in a safe and secured manner.

g) To build the foundation for a full range of Aadhaar enabled Banking services.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

5. AEPS Membership:

a) All existing members of National Financial Switch (NFS) are eligible to participate in AEPS. NFS members intending to participate in AEPS may apply for membership in the format as given in Annexure-II.

b) A bank that is not a member of NFS can also join AEPS provided :

i) The applicant bank is a type A member of the RBI’s Real Time Gross Settlement System.

ii) The applicant bank undertakes to join NFS within 3 months on payment of a onetime membership fee of Rs. 3,00,000.00 (Rupees Three lakhs only)

iii) The applicant bank is willing to contribute to the Settlement Guarantee Fund of NPCI.

6. Certification:

a) On admission of a bank as a member to participate in AEPS, NPCI will prepare a project plan detailing steps needed for establishing Host-to-Host connectivity between a member bank and NPCI. The interface specifications would be made available to banks upon approval of the application and admission of the bank in AEPS.

b) Apart from this, the project plan will also document steps related to test plan and test

execution. The test plan will detail all the personnel involved in conducting the acceptance test.

c) If any third party on behalf of NPCI develops software application or releases new

version of the software, NPCI reserves the right to upgrade the existing system after appropriate certification. Such enhancements pertaining to software should comply with Industry Standards and will be undertaken after a notice of sixty (60) days to all member banks participating in the AEPS Network. However, NPCI will examine whether to proceed for re-certification and in such case all expenses pertaining to re-certification will be borne by the member banks. All such software enhancements and new versions of software so released will be retained by NPCI.

d) If a member bank develops software application or releases new version of the software,

the respective member bank should notify NPCI at least sixty (60) days in advance and should allow NPCI to perform re-certification. All cost associated with re-certification will be borne by the member bank migrating to new platform.

7. Customer Participation:

a) Any resident of India having an Aadhaar number with his/her bank account linked to the Aadhaar number and willing to use the services of a Business Correspondent of a Bank, can participate in AEPS service.

b) For the purpose of financial inclusion, institutions like LIC, Banks become registrars to

the UIDAI and undertake Aadhaar enrolment for their customers.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

c) Banks as registrars to UIDAI may choose to issue a card to enable Interoperability between urban ATMs and MicroATM for financial inclusion customers. In order to enable financial inclusion customers to use the urban ATM and the services of business correspondents wherever accessible seamlessly, banks as registrars to UIDAI may choose to issue a card (which can be read at regular urban ATM and swiped at MicroATMs) having the Aadhaar number and ISO BIN/IIN embedded in the card as given by NPCI. This will help the customer to have an identity card and enable him/ her to access basic banking services without the need to memorize a 12 digit Aadhaar number and 6 digits ISO IIN. The card is swiped at a regular ATM/ MicroATMs and thereafter providing his/ her biometric data (fingerprints) for authentication, the customer can avail the banking services.

d) Aadhaar can be linked to a bank account for use in carrying out banking transactions

like, balance enquiry, Cash deposit, Cash Withdrawal and Remittances including receiving of government entitlements like Social Security Pension etc. A bank account linked to an Aadhaar will be known as an Aadhaar enabled bank account.

e) For availing AEPS, a bank customer shall use his/her their respective Aadhaar enabled

Account for carrying out all Aadhaar enabled banking transactions like balance enquiry, cash deposit, cash withdrawal and remittance to another person’s Aadhaar enabled bank account. Other services may get progressively added based on member banks inputs and customer needs.

8. Issuer Identification Number - IIN:

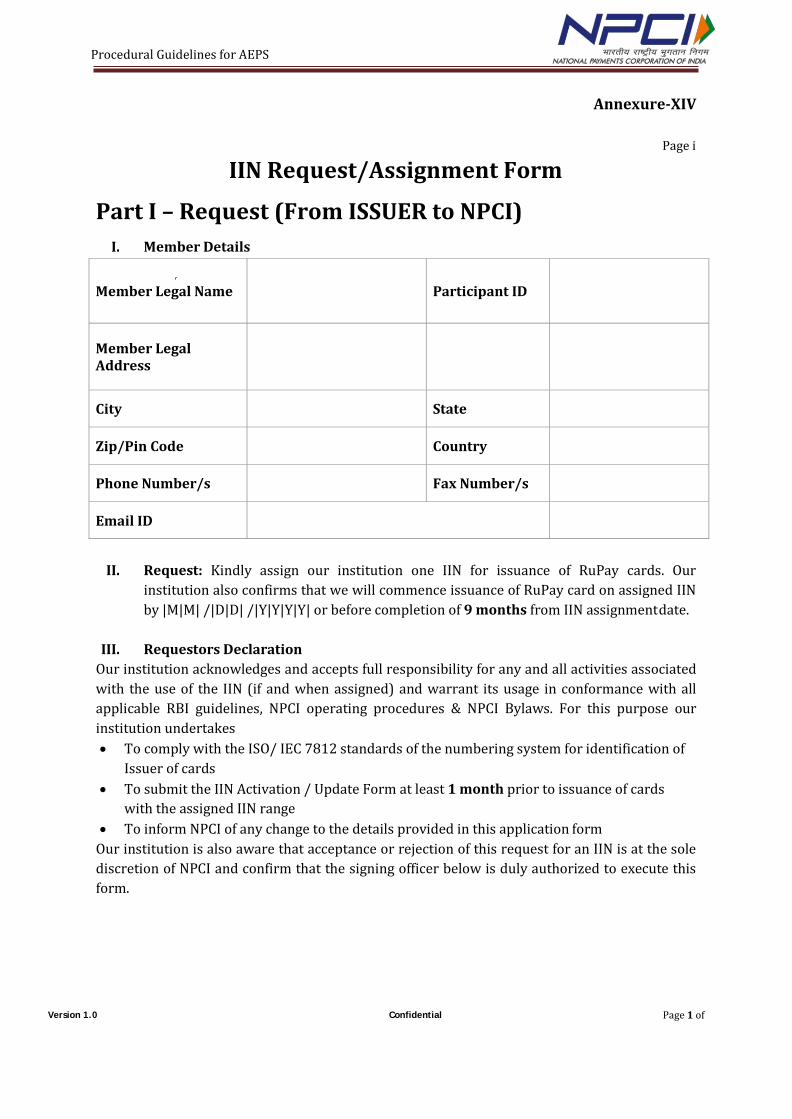

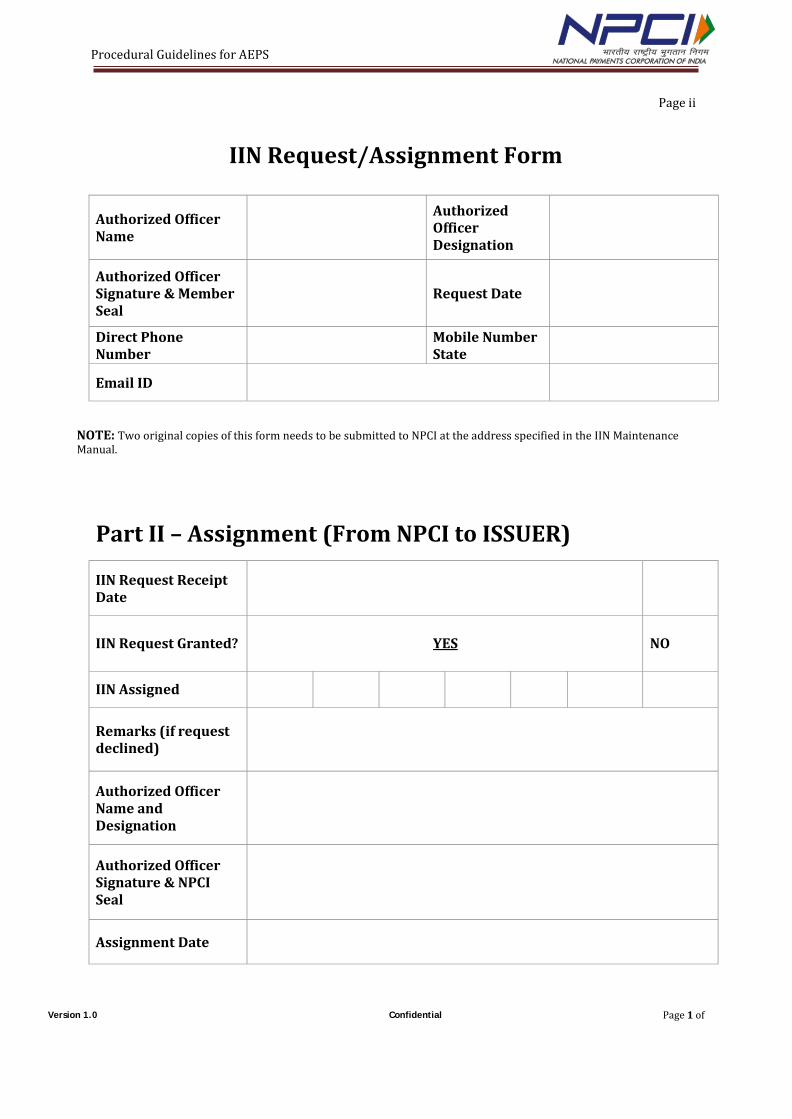

a) A Bank offering AEPS shall advise an Aadhaar enabled bank account holder its unique Issuer Identification Number (IIN) for referring to the bank in all his/her AEPS Transactions. The IIN will be a six digit number which will be allotted to a bank upon an application to NPCI from the Bank seeking IIN for AEPS. (Annexure-XIV).

b) The Aadhaar number of the beneficiary would be accompanied by the IIN of the Beneficiary’s Bank. Thus the input for uniquely referring to the beneficiary’s (or the destination) account would be:

IIN + Aadhaar number

c) IIN coupled with Aadhaar number will uniquely link to an Aadhaar enabled bank

account with that Bank. Alternatively, instead of entering the digits for IIN, it may be represented at the MicroATM level by the respective banks’ name/ logo, which may be selected from a drop down menu. This would make the customer experience richer.

9. Customer Access Point:

a) The Customer access points may have Business Correspondents (BC) using Point of Sale (POS) devices to facilitate customers to make Cash Deposit, Cash Withdrawal, Fund Transfer and Balance Enquiry and other services which may get introduced from time to

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

time based on member bank inputs and customer needs. The POS devices used by BC should adhere to the standards as specified in the document on MicroATM standards referred to in paragraph 2 a) of this document.

b) A Business Correspondent is an intermediary used by a bank to extend Banking

services in areas where they do not have a branch. The scope of activities undertaken by the Business Correspondents includes, inter alia, collection of small value deposits, Cash withdrawals and small value interbank remittances. Member banks are advised to refer to various RBI notifications on Financial Inclusion from time to time for more details.

c) Within the scope of AEPS, a BC of a bank is treated as an integral part of the Bank that it

corresponds with. The Bank will be known as its Correspondent Bank. The Bank will be responsible for all acts of commissions and omissions of its BC.

10. Intrabank (On-us) and Interbank (Off-us) Transactions:

An intrabank (On-us) transaction is one where an Aadhaar initiated transaction has effects only in accounts within one and the same Bank and does not necessitate an interbank settlement.

An interbank (Off-us) transaction is one where there is movement of funds from one Bank to another necessitating an interbank settlement.

11. Issuer Bank:

Issuer Bank within the scope of AEPS is one that has an Aadhaar enabled account of a transaction initiating customer, held with it.

12. Acquirer Bank:

Acquirer bank within the scope of AEPS is one that acquires an Aadhaar enabled interbank financial transaction initiated by a person, whose Aadhaar enabled Account is not held with it, i.e. the transaction initiating person’s Aadhaar enabled bank account is held with some other bank.

13. Transaction Receipt:

For all transactions whether intrabank or interbank, a Transaction Receipt will be printed and handed over to a customer as a transaction record with its finality status, by the BC through whom the transaction was initiated. The details provided in a transaction Receipt shall be as per the AEPS Interface Specifications referred to in Para 2 b) above.

14. Aadhaar Authentication:

In any Aadhaar enabled financial transaction, whether, intrabank or interbank, a customer is required to provide his Aadhaar and biometrics on the MicroATM managed by a BC to prove his identity and get himself authenticated by the UIDAI. A transaction will be put through only when the Aadhaar authentication is successful. MicroATMs that submit Aadhaar and the related biometrics to UIDAI should adhere to the ‘Aadhaar Authentication

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

API and Devices Security Specification and Biometric Fingerprint Scanner Specifications’ of the Unique Identification Authority of India for Aadhaar authentication referred to in Para 2 c) above. A positive Aadhaar authentication is an indispensable part of any Aadhaar enabled financial transaction. An Aadhaar authentication may be declined due to various reasons. Please refer to ‘Aadhaar Authentication API and Devices Security Specification and Biometric Fingerprint Scanner Specifications’ of the Unique Identification Authority of India for Aadhaar authentication referred to in Para 2 c) of this document.

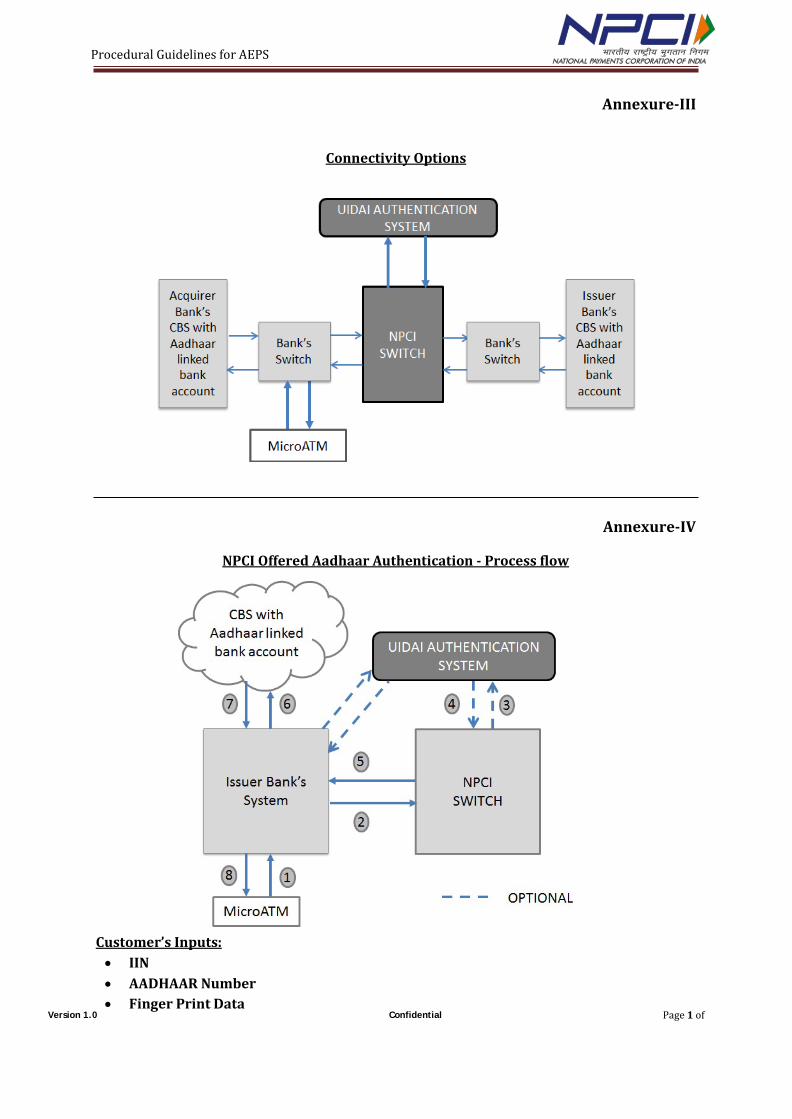

NPCI facilitates Aadhaar authentication service too. Banks, therefore, have an option to route their intrabank transactions to NPCI switch for Aadhaar Gateway Authentication or have an arrangement with UIDAI for direct Access. (Please see Annexure-IV).

15. Aadhaar enabled interbank (Off-us) Transactions:

While member banks would be offering a wide range of banking services through their Business Correspondents, an Aadhaar initiated interbank transaction would be routed through the NPCI switch only.

The four Aadhaar enabled basic types of banking transactions are as follows:- a) Cash Withdrawal b) Cash Deposit c) Aadhaar to Aadhaar Funds Transfer d) Balance Enquiry a) Cash Withdrawal through a Business correspondent:

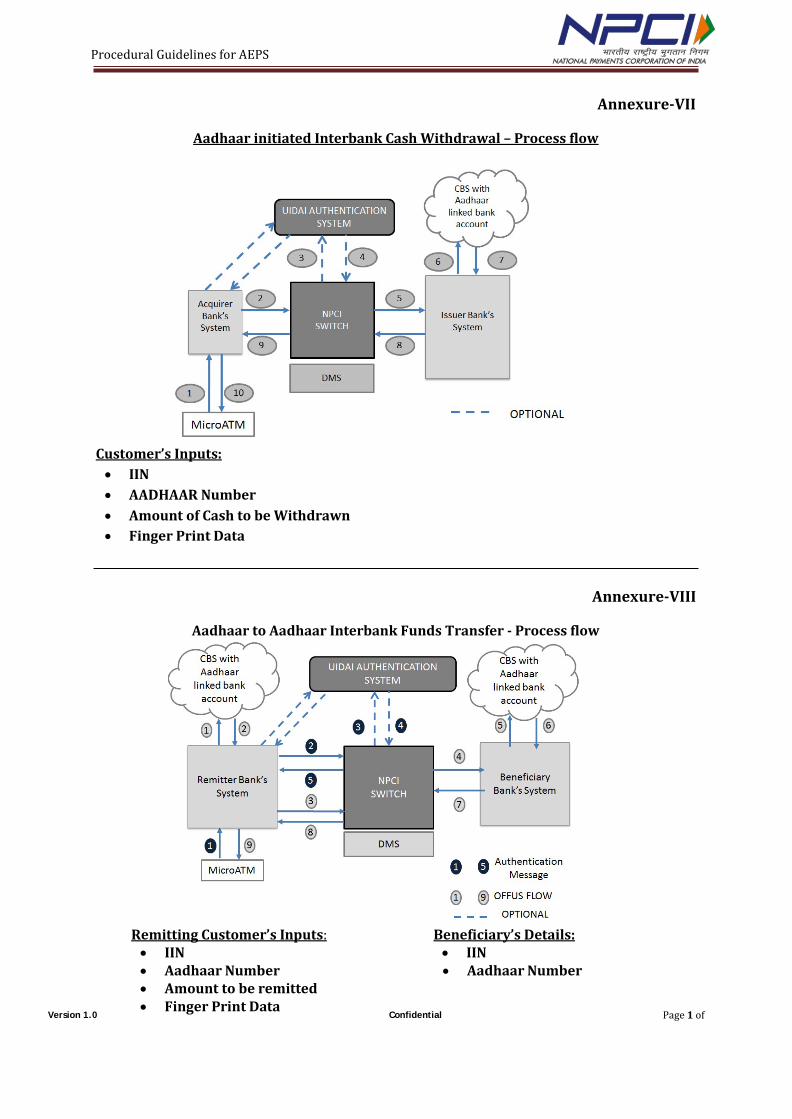

A Bank customer would make a Cash withdrawal through the MicroATM of a BC. The cash withdrawal transaction first flows to the Correspondent Bank of the BC. If the transaction is intra-bank, on successful Aadhaar Authentication, the bank will debit the customer’s account and send its positive response to the MicroATM. If it is interbank, the transaction will be forwarded to the Issuer Bank through NPCI’s switch. On successful Aadhaar Authentication, the Issuer Bank will debit the Aadhaar enabled account of the customer and send its positive response to the MicroATM of the BC through the NPCI switch. Whether intrabank or interbank, only after receipt of a positive response, cash will be dispensed.

If the response from the Issuer bank is not received within a set time limit, the issuer bank will receive reversal notification from anyone of NPCI switch or the Acquirer Bank or the MicroATM depending upon who got the response timed-out. No money will be dispensed to the initiating customer by BC; it is however, advisable that the BC initiates a balance enquiry before sending a reversal notification to the issuer if a time-out response is received by it.

A cash withdrawal is possible from the initiating customer’s own Aadhaar enabled account only. Annexure-VII shows the transaction flow in respect interbank cash withdrawal transactions.

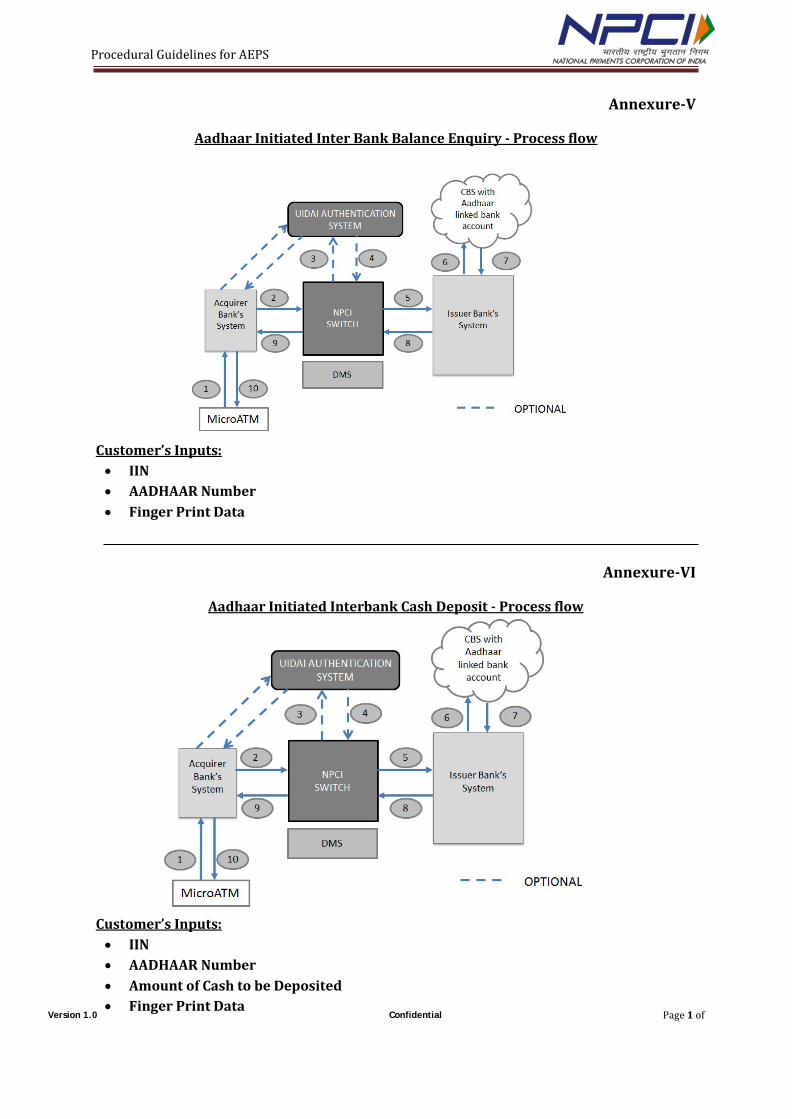

b) Cash Deposit through a Business Correspondent:

A Bank Customer would make a Cash Deposit through a BC who uses a MicroATM terminal. A cash deposit transaction initiated by a BC first flows to the Correspondent Bank of the BC. If the transaction is intra-bank, on successful Aadhaar Authentication, the bank will credit the customer’s account and send a positive response to the MicroATM. If it is inter-bank, the transaction will be forwarded to NPCI’s switch for onward submission to the Issuer Bank. On successful Aadhaar Authentication, the Issuer bank will credit the customer’s

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

Aadhaar enabled account and send its response to the MicroATM that initiated the transaction, through NPCI switch, for having credited the account.

If the response from the Issuer bank is not received within a set time limit, the issuer bank will receive a reversal notification from anyone of NPCI switch or the Acquirer Bank or the MicroATM depending upon who got the response timed-out. The BC would, in this case, return the cash to the remitting customer. However, it is advisable that the BC sends a Balance enquiry to ensure that the credit for the cash deposit has not been effected in the destination account before returning the cash.

A cash deposit is possible for credit to the initiating customer’s own Aadhaar enabled account only. Annexure-VI shows the transaction flow in respect of an interbank cash deposit transaction.

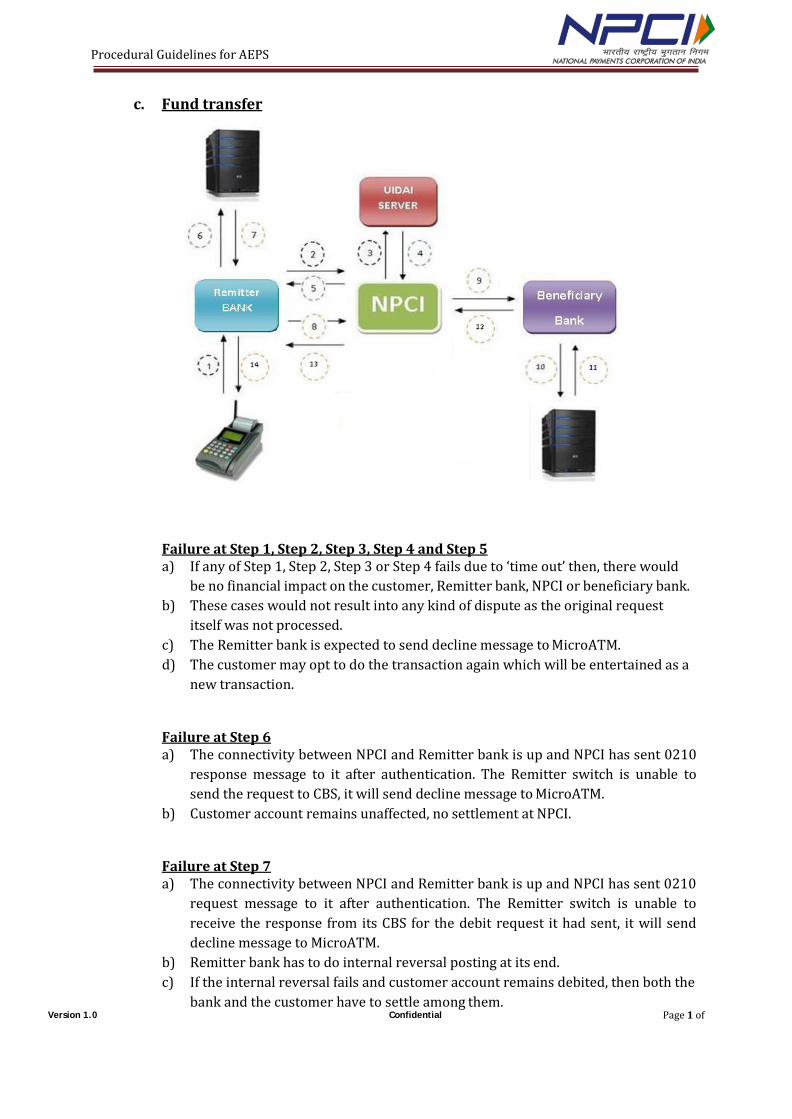

c) Aadhaar to Aadhaar Interbank Funds Transfer:

In the initial phase of AEPS implementation, an Aadhaar to Aadhaar funds transfer cannot be an acquired transaction. The Remitting customer should necessarily have his/her Aadhaar enabled Account with the Remitting Bank and the transfer will be effected only after a successful debit to this account. A Remitting Customer is required to initiate an Aadhaar enabled inter Bank remittance only from the MicroATM of a Bank with whom he/ she is holding an Aadhaar enabled Account.

When a Funds Transfer transaction is initiated from a MicroATM of a BC, the Remitting Bank firstly, gets the transaction Aadhaar authenticated. Upon successful Aadhaar Authentication, the bank debits the Aadhaar enabled account of the initiating customer with the remittance amount and sends a Payment Request to the Beneficiary’s Bank based on the IIN provided, through the NPCI Switch. Beneficiary’s Bank would credit the Beneficiary’s Aadhaar enabled account and forward its positive response to the MicroATM that initiated the request, through NPCI switch. The customer will know the finality of the remittance from the Transaction Receipt.

If the response from the beneficiary’s bank is not received within a set time limit, no reversal notification from NPCI switch or the Acquirer Bank or the MicroATM will be sent to the beneficiary’s Bank. For all interbank remittances that have got timed out, Banks are advised to use the Dispute Management System referred to herein to resolve interbank settlement issues.

In the initial phase, a Fund Transfer is possible only from one Aadhaar Enabled account to another Aadhaar enabled Account. Annexure-VIII shows the transaction flow of an Aadhaar to Aadhaar interbank Remittance.

In any typical Aadhaar to Aadhaar funds transfer, there would be six parties: i. A Customer initiating a transaction through a BC. ii. Remitting Bank’s switch iii. NPCI - AEPS Switch iv. UIDAI Authentication v. Beneficiary Bank’s Switch vi. A Beneficiary accessing his account through a BC.

In the second phase Aadhaar to non-Aadhaar interbank funds transfer would also be made possible from a BC of an acquirer bank.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

d) Aadhaar Initiated Balance Enquiry:

Balance Enquiry is a non-financial transaction. A balance enquiry may be on-us or off-us. If it is On-Us, the bank upon a successful Aadhaar Authentication, advises the balance in the customer’s account to the MicroATM that originated the Inquiry. If it is off-us, a balance request will be forwarded to the issuer Bank through NPCI. Upon successful Aadhaar Authentication, the Balance advice received from the Issuer bank will be forwarded to MicroATM that originated the Inquiry, through NPCI switch. Annexure-V shows the transaction flow of an interbank Balance Inquiry.

e) Transaction decline:

Aadhaar initiated financial transactions may fail to be effected due to various reasons like loss of network connectivity, incorrect Account holder details etc. In such a scenario, the transaction initiating MicroATM normally receives from its Correspondent Bank or NPCI switch or the destination bank, a negative response with an appropriate decline code. Details of various possible decline scenarios and the corresponding decline codes are given in the AEPS Host interface specifications. This document is available to a bank upon admission as an AEPS member.

A transaction declined by a destination bank with an appropriate decline code is deemed as a successful transaction from the NPCI switch perspective. A time-out is a treated as a decline for technical reasons. For detailed error response codes descriptions please refer to the Interface specification for Interoperable AADHAAR enabled Financial Inclusion Architecture of the National Payments Corporation of India.

For all acts of commissions and omissions of a Business Correspondent, only its Correspondent Bank would be held liable.

16. Interbank Settlements and Net Debit Cap (NDC):

All Aadhaar enabled interbank remittances, acquired Cash Deposits or Withdrawals result in interbank settlements. The interbank settlement for AEPS takes place once a day on a netted basis. These transactions are simply referred to as interbank transactions for the purpose of convenience herein below:

a) An interbank cash deposit or remittance is delivered to NPCI for routing to the Issuer

or beneficiary bank only after Deposit of Cash by the remitting Customer or a successful debit having been made to his/her Aadhaar enabled account. Therefore, there is no risk of a credit being made with the remitting customer not having adequate fund. Once the remittance request reaches the beneficiary bank, it should be treated as a “good fund” and the beneficiary bank should credit the beneficiary’s account immediately with all effects cleared. Thus, it would be a real time money transfer from the customer’s point of view.

b) NPCI would compute a member bank’s net position (payable or receivable) on

successful execution of all its interbank transactions on a real time basis.

c) The net position of a member bank so computed should always be within the “Net Debit Cap (NDC)” prescribed for that bank. Processing of outgoing transactions of a

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

bank, when its net exposure exceeds its NDC during a day, would be stopped until additional collaterals by cash or Government Securities is deposited in NPCI’s account (with the Reserve bank of India.)

d) Members can increase their collateral any time during the RTGS window by remitting

the extra collateral through RTGS to NPCI’s current account with RBI, Mumbai. The Net Debit Cap would be updated within half an hour of receipt of the confirmation of credit. Once NPCI gets PDO-NDS membership, members would have the choice of posting additional collateral in Government of India securities in favor of NPCI’s SGL Account maintained with RBI, Mumbai.

e) NDC fixed for Aadhaar enabled interbank transactions is exclusively for AEPS and no

portion of it can be shared with NPCI’s other services like NFS, Interbank Mobile Payment Service etc. and vice versa. The collaterals however, will be pooled in a single account of NPCI with respective NDC for each member bank apportioned in the NPCI switch against each service.

f) NDC would be twice the amount of collateral (in cash or Government of India

securities) posted with NPCI for Aadhaar enabled remittance service. NPCI is in the process of opening SGL account with RBI. Till that time, all collateral should be in cash.

g) Minimum collateral would be Rs.5,00,000/-(Rupees five lakhs). The collaterals

deposited with NPCI will be in form of non-interest bearing deposits.

h) The purpose of collateral would be only for guaranteeing the settlement.

i) At the close of a AEPS business cycle on any day i.e., at 23.00 Hrs., the net receivable or payable in respect of each member bank, will be generated and a Daily settlement report for all Aadhaar enabled interbank transactions will be made available for download from the AEPS DMS solution to all member Banks. The Net Settlement Amount will be inclusive of the Interchange, Transaction switching and settlement fees etc., payable by Member Banks.

j) NPCI’s Type-D membership is activated and will arrange for the necessary inter-bank

settlement of credits and debits to the banks’ respective current accounts with RBI. .

k) The settlement time would usually be the first hour (10.00-11.00 hr.) of the next working day at RBI Mumbai, through RTGS. Please refer to paragraph 3.1.5, 3.1.6, 3.1.7 of the RBI notification referred to in Annexure-XII.

l) It will be members’ responsibility to verify the accuracy of the Daily Settlement

Reports with reference to the data available at their end.

m) In case of net debit, a member bank has an obligation towards other member banks. Banks are therefore advised to ensure strict compliance to the RTGS operational instructions of RBI in this connection. Any failure to maintain the required balance in the RTGS settlement account shall attract penal action from RBI.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

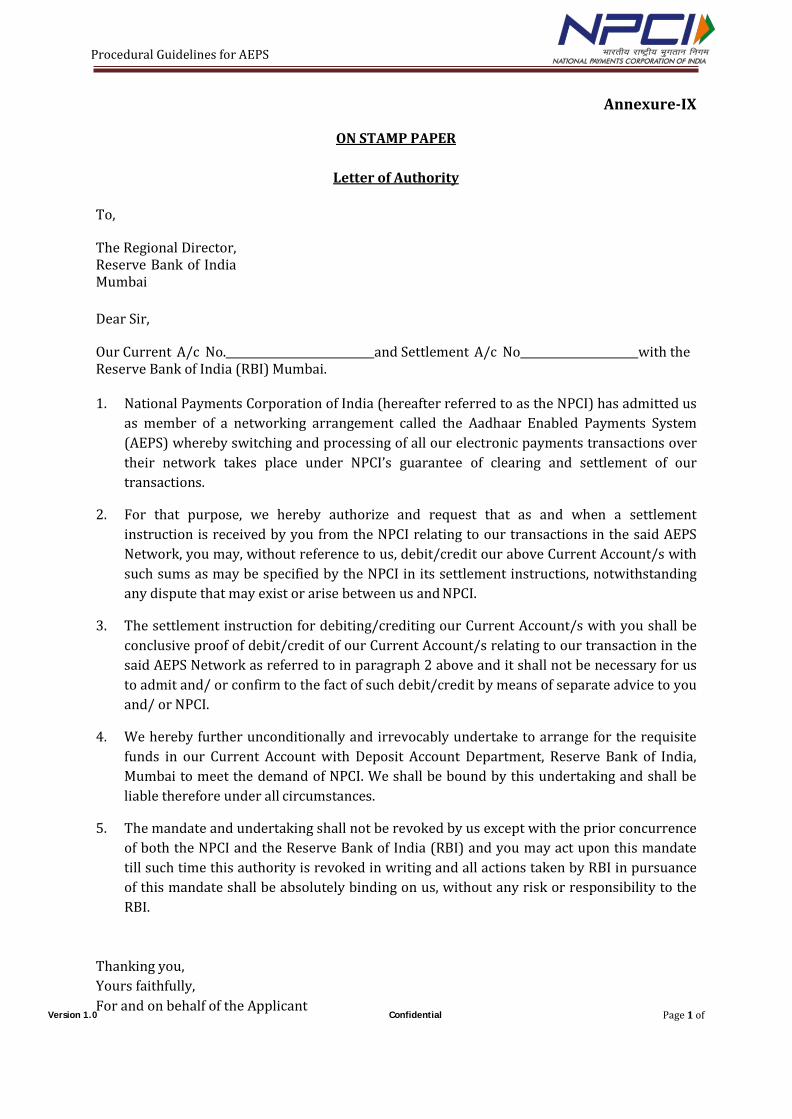

n) All banks before participating in AEPS shall issue a Letter of Authority to RBI

authorizing them for AEPS related settlements in their respective accounts by NPCI or its settlement agency, duly approved by their respective boards. (Annexure-IX).

o) If a member bank fails to meet the clearing liability at the time of settlement, RBI

would make use of the fund balance in NPCI’s Settlement Guarantee Fund account and complete the settlement. Thereafter, NPCI would initiate the process of recovering the fund from the defaulting bank with penal interest as per the terms of SGF agreed to by member banks. In this connection, Member Banks are required to be guided by paragraph 3.3 of the notification from the Department of Payments and Settlements of the Reserve Bank of India, Ref No: RBI/2010-11/218 DPSS.CO.CHD. No.695/03.01.03/2010-2011 dated 29th September, 2010 - (Annexure-XII).

p) A bank failing to meet the clearing liability more than two times in a month or three

times in a quarter would be debarred from AEPS membership.

17. Fees charged by NPCI for AEPS:

Transaction Fee:

a) The Fees charged per transaction shall be as under: i) Aadhaar Authentication through NPCI ii) Acquired Balance Inquiry iii)Acquired Cash withdrawal iv) Acquired Cash Deposit v) Aadhaar interbank Remittance

b) The charges mentioned below are exclusive of UIDAI authentication fee, if any.

c) In the case of Intrabank (On-US) transactions for Aadhaar gateway authentication

routed through NPCI, the fees will be Rs 0.10 per authentication request routed through NPCI to UIDAI. This fee does not take into account any authentication fees levied by UIDAI separately.

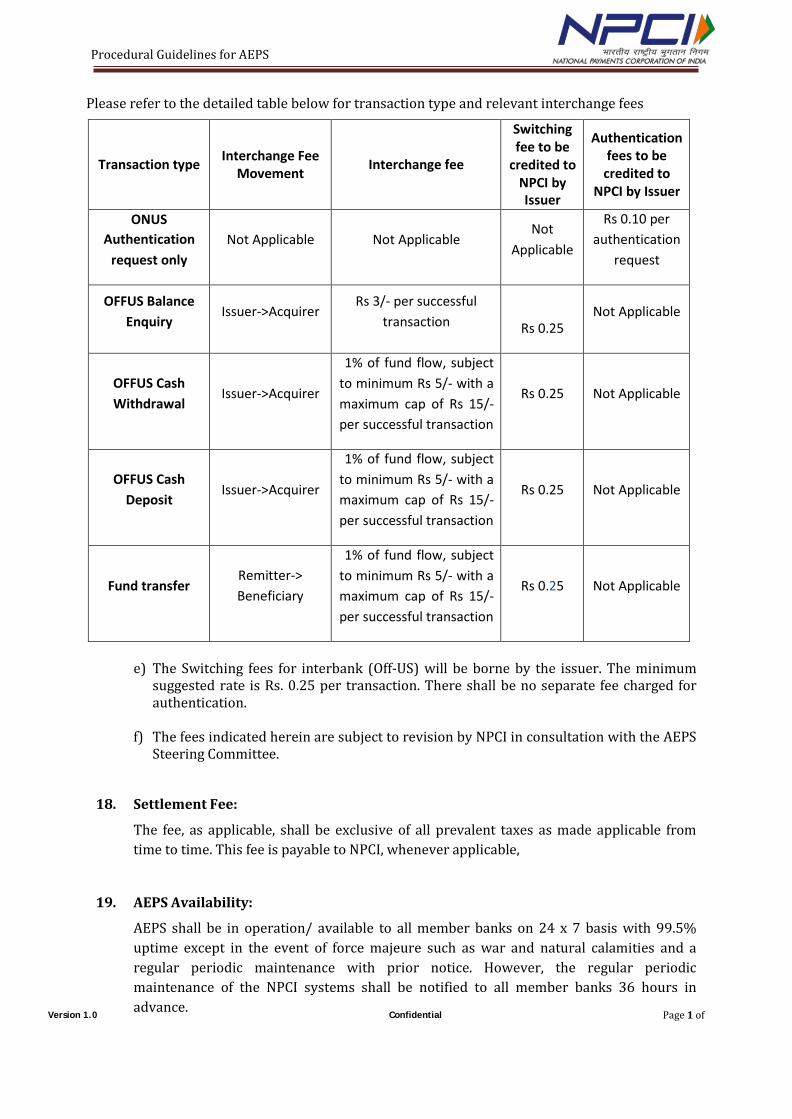

d) The interchange per offus transactions, as per the Meeting conducted by IBA on 17th

March 2012 would be the following:-

i) Financial transactions through AEPS 1% of fund flow ( value of transaction) per transaction, subject to • Minimum interchange of Rs. 5 per transaction • Maximum interchange of Rs. 15 per transaction

ii) Non- Financial transactions through AEPS Rs. 3 per transaction

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

Please refer to the detailed table below for transaction type and relevant interchange fees

Transaction type

Interchange Fee Movement

Interchange fee

Switching fee to be

credited to NPCI by Issuer

Authentication fees to be

credited to NPCI by Issuer

ONUS Authentication

request only

Not Applicable

Not Applicable

Not Applicable

Rs 0.10 per authentication

request

OFFUS Balance Enquiry

Issuer->Acquirer

Rs 3/- per successful transaction

Rs 0.25

Not Applicable

OFFUS Cash Withdrawal

Issuer->Acquirer

1% of fund flow, subject to minimum Rs 5/- with a maximum cap of Rs 15/- per successful transaction

Rs 0.25

Not Applicable

OFFUS Cash

Deposit

Issuer->Acquirer

1% of fund flow, subject to minimum Rs 5/- with a maximum cap of Rs 15/- per successful transaction

Rs 0.25

Not Applicable

Fund transfer

Remitter-> Beneficiary

1% of fund flow, subject to minimum Rs 5/- with a maximum cap of Rs 15/- per successful transaction

Rs 0.25

Not Applicable

e) The Switching fees for interbank (Off-US) will be borne by the issuer. The minimum

suggested rate is Rs. 0.25 per transaction. There shall be no separate fee charged for authentication.

f) The fees indicated herein are subject to revision by NPCI in consultation with the AEPS

Steering Committee.

18. Settlement Fee:

The fee, as applicable, shall be exclusive of all prevalent taxes as made applicable from time to time. This fee is payable to NPCI, whenever applicable,

19. AEPS Availability:

AEPS shall be in operation/ available to all member banks on 24 x 7 basis with 99.5% uptime except in the event of force majeure such as war and natural calamities and a regular periodic maintenance with prior notice. However, the regular periodic maintenance of the NPCI systems shall be notified to all member banks 36 hours in advance.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

20. Choice of Connectivity:

Member Banks have to connect to AEPS directly from their own Switch or through their respective Financial Inclusion Service Provider’s Switch located at the bank’s premises. Member banks shall establish connectivity with NPCI switch only on NPCINET.

21. Message Formats:

All Aadhaar transactions routed through the NPCI switch should comply with the message formats specified by NPCI as a part of AEPS Interface specification referred to in paragraph 2.b. hereof, with modifications if any communicated to member banks from time to time.

22. Transaction Logging:

NPCI shall maintain logs of all Aadhaar transactions passing through the NPCI switch. Member Banks are also advised to store transactions logs as per their own policies in force.

23. Member Notification:

NPCI shall notify all the member banks regarding:

a) Inclusion of a new member participating in AEPS

b) Cessation of membership of any bank.

c) Suspension/Termination of any member bank.

d) Amendments in the AEPS Procedural Guidelines.

e) New enhancement of the software and hardware released pertaining to the AEPS.

f) Changes in the periodic maintenance hours.

g) Any other issues deemed important by NPCI for the member banks.

24. Steering Committee for AEPS:

An AEPS Steering Committee would be dedicated for discussion on the operational issues relating to Aadhaar enabled banking services and would consist of:

a) Select Member banks b) NPCI

The steering committee meetings may optionally have invitees from UIDAI and other organizations involved in promoting Aadhaar enabled banking services and industry experts as required, to get better insight and improve AEPS. The committee shall meet at least once in a quarter in addition to two user group meetings in a year which would be attended by all the members. The list of members and the calendar of meetings in a year would be published in the website of NPCI in the beginning of the year.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

25. Reports and Reconciliation: Following reports will be made available to the member banks:

a) Aadhaar Authentications through NPCI.

b) Intrabank & Interbank balance Inquiry (Acquirer and Issuer)

c) Intrabank & Interbank Cash deposits (Acquirer and Issuer)

d) Intrabank & Interbank Cash withdrawals (Acquirer and Issuer)

e) Intrabank & Interbank Remittances (Remitter/ beneficiary)

f) Intrabank & Interbank Net Settlement (Payables and receivables)

Member banks shall ensure that they download these reports and keep their settlement accounts reconciled on a daily basis.

Besides these reports, Raw Transaction Data files, Settlement Files, Verification Files and Daily settlement Reports of all the Originating and responding transactions of a bank will also be available to the banks for download. In case of any discrepancy in the raw transaction data file, the reports cited above will be deemed as authentic.

26. Operating Procedure:

a) Member banks participating in the AEPS shall maintain connectivity of their network for the AEPS services on 24x7 basis with an uptime of 99.5% of their respective SWITCHES.

b) Banks shall ensure their own Switch generates accurate input data with reference to

the NPCI - AEPS Interface Specification for all AEPS transactions.

c) Ensure Security of Transactions between the MicroATM, Bank’s Switch and NPCI switch.

d) All member banks shall monitor and ensure adequacy of their collateral with NPCI as

detailed in paragraph 16 on Inter-bank settlement and Net Debit Cap.

e) All Member banks shall ensure that they download their respective transactions and settlement reports from the AEPS DMS solution and shall keep their books of accounts reconciled on a daily basis.

f) Each member bank shall conduct annual internal audits of itself and their Business

Correspondents in order to comply with the AEPS Procedural guidelines.

g) If any member fails to fulfill its commitment towards other members participating in AEPS, thereby, incurring any loss in the form of settlement or transaction fees, it would be completely borne by the defaulting member. In such a case, funds available in the defaulting member’s Settlement Account will be used to settle the claims at the earliest.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

h) A member may resign from the AEPS at any time on giving a notice of ninety (90) days in writing to NPCI of such member's intention to do so. On receipt of such notice, NPCI shall inform the other members, of its resignation. On the expiration of such a notice, the member resigning shall cease to be a member of AEPS. NPCI will also disconnect its Network service to such a member.

i) A member bank shall cease to be a member in any of the following events:

i) If it’s banking license has been cancelled by RBI. ii) If it stops or suspends payment of its debts generally or ceases to carry on

business, or goes into liquidation. iii) If it is granted moratorium or prohibited from accepting fresh deposits.

27. Risk Management at Originating and Responding Banks:

a) Transaction Originating Bank shall be responsible for the following (as applicable to an issuer or an acquirer or both):

i) Limits on the Transaction amount if any ii) Balance authorisation before effecting a Payment Request iii) Aadhaar Number and account Validations/Verifications. iv) Validation of Number of Transactions in a day, if any v) Multiple Requests from same MicroATM within X time period with same

reference/transaction number (This is to avoid responding to multiple requests

for one and the same transaction) vi) Maximum customer level limits, if any vii) Adequacy of Collateral posted with NPCI towards NDC compliance. viii) Adequacy of contribution to Settlement Guarantee Funds ix) AML related validations for Funds Transfer transaction for the debit leg (online or

offline) x) Fraud Check (online or offline) & reporting xi) All acts of commissions and omissions of the Bank’s BC.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

b) Transaction Responding Bank shall be responsible for the following (As applicable to an issuer or an acquirer or both): i) Limits on the Transaction amount if any. ii) Incoming message validation iii) Issuer Aadhaar Authentication and posting of transaction to an Aadhaar enabled

Account in respect of Cash Deposit, Cash Withdrawal and Remittance. iv) Posting of transaction to the beneficiary’s account in respect of interbank funds

transfer between two Aadhaar enabled accounts. v) Declining of a remittance, if necessary, if a beneficiary is unable to respond to

Bank’s remittance enquiry if any. vi) Declining of a remittance, in case the beneficiary account is on lien or blocked or

credit is banned by any regulatory Authority. vii) Checks on Multiple Requests for one and same Aadhaar Remittance within X time

period with same ref/transaction number (This is to avoid responding to multiple

requests for a single Payment Request) viii) Maximum permissible limit in a day, if any. ix) AML related validations for Funds Transfer transaction for credit leg (online or

offline). x) Fraud Check (online or offline) & reporting.

28. AEPS Dispute Management System and Exceptions handling:

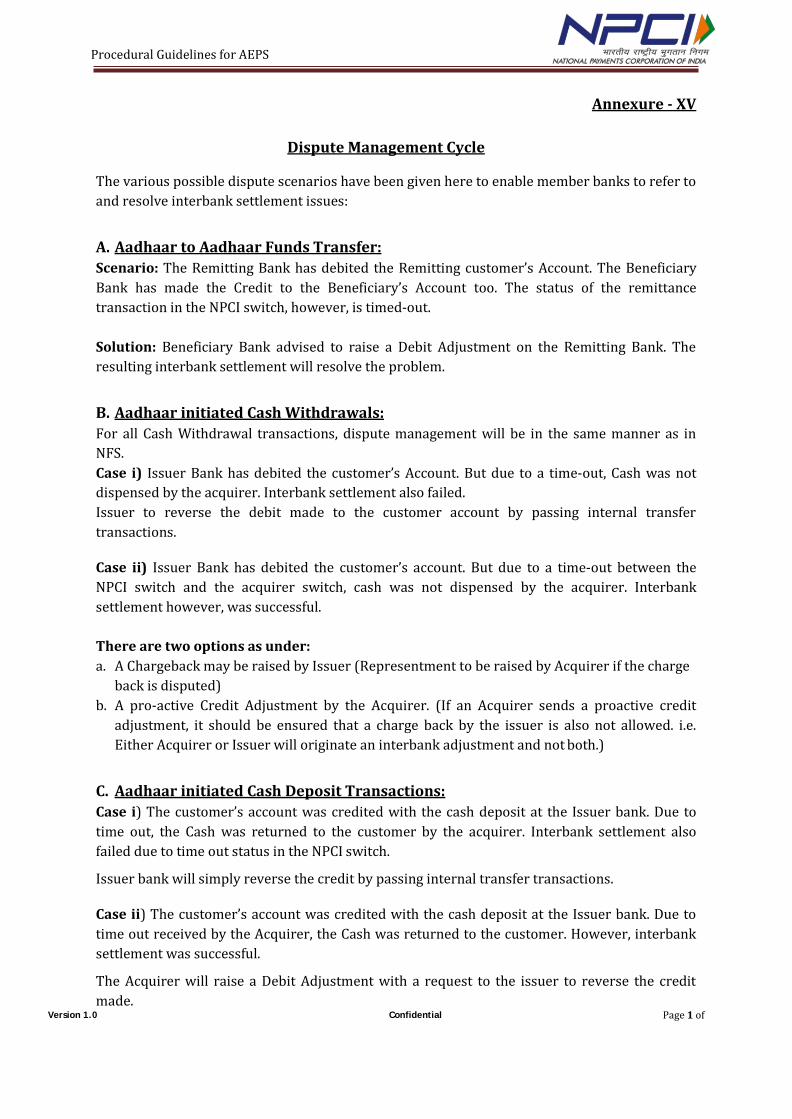

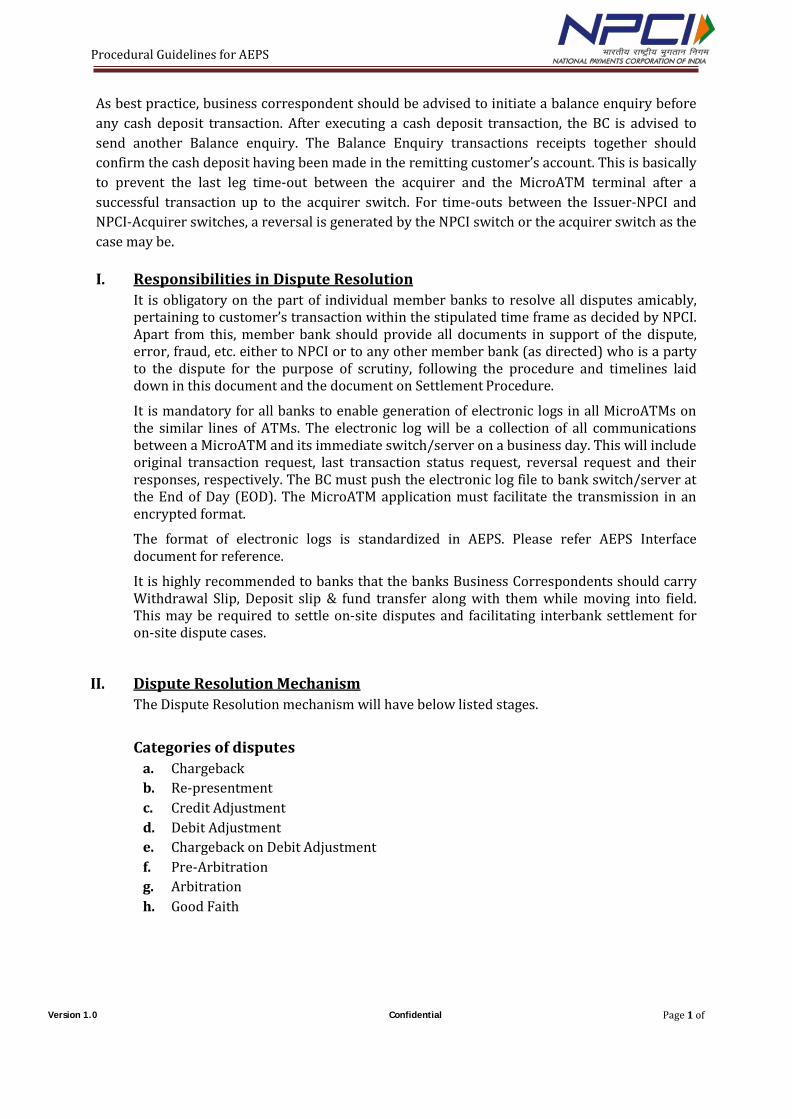

Exception Transactions are those that are reported as unreconciled for a long time in the settlement accounts of the member banks or erroneous by customers. NPCI has provided Dispute Management systems on similar lines as DMS for NFS to help member banks raise charge back/ re-presentments or make credit/debit adjustments to resolve all disputes arising out of Aadhaar enabled banking transactions. (Annexure-XV)

Member banks shall collaboratively endeavor to settle discrepancies in Settlement, if raised by other member banks. Where necessary, NPCI shall provide transaction logs as logged by the SWITCH, if any, relating to the transaction reported as exception to facilitate settlement of the same.

Exception handling for onus transactions in case of authentication failure by UIDAI for absence of last mile connectivity or extremely worn out biometrics of customers even after repeated attempts etc. banks need to put in place appropriate internal exception handling mechanisms in view of customer service

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

29. Customer Complaints:

Aadhaar transactions are similar to ATM transactions. Therefore, any complaint about debit without cash being dispensed or cash deposited/ debit made without corresponding credit to the beneficiary account should be conclusively and bilaterally dealt with by the remitting and beneficiary banks within 12 days from the date of receipt of a complaint as per the guidelines on ATM transactions.

30. Audit by NPCI:

NPCI reserves the right to audit the AEPS related systems (including Hardware and software) of the member banks or their Business Correspondents if found necessary.

31. NPCI service Provider Liability:

The owner and co-coordinator of AEPS is NPCI. NPCI reserves the right either to operate & maintain the AEPS and the Network on its own or obtain necessary services from third party service providers.

32. Non-Disclosure Agreement:

All members participating in the AEPS Network should sign a non-disclosure agreement with NPCI as given in Annexure-X. Each member should treat AEPS related documents strictly as confidential and should not disclose to alien parties without prior written permission from NPCI, failing to comply with, shall invite severe penalties. However, the participating members can disclose the AEPS Procedural Guidelines within its employees or agents related to the specific areas.

33. Interpretational Disputes and Arbitration:

It will be NPCI’s endeavor to resolve amicably any disputes or differences that may arise from misconstruing the meaning and the operation of this document. NPCI has set up a Panel for Resolution of Disputes (PRD) consisting of four member banks and the Chief Operating Officer of NPCI as the President to look into interbank disputes as per the directives of the Department of Payments and Settlement Systems of the Reserve bank of India, notification Ref: DPSS.CO.CHD.No:654/03.01.03/2010-2011 dated 24th September, 2010. Please see Annexure-XIII, attached hitherto.

The AEPS Network shall continue to work under the contract during the PRD proceedings unless the matter is such that the work cannot possibly be continued until the decision of the PRD or the Appellate Authority at RBI, as the case may be is obtained.

34. Indemnification:

It is binding on all members, including NPCI, participating in AEPS to defend and

indemnify themselves from all loss and liabilities if any, arising out of the following:

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

a) Member’s failure to perform its duties and responsibilities as per the Procedural

guidelines for AEPS.

b) Malfunctioning of Member’s equipment.

c) Fraud or negligence on the part of member.

d) Unauthorized access to AEPS Network.

e) Member’s software, hardware or any other equipment violating copyright, patent laws

and UIDAI authentication policy etc.

All members should comply with the AEPS Procedural Guidelines as framed by NPCI. NPCI reserves the right to impose penalty on the members either by suspending or terminating (Host-to-Host) connectivity for frequent violations of the AEPS Procedural Guidelines.

35. Termination of services:

Criteria for Termination/ Suspension of AEPS Membership:

AEPS under the following circumstances may terminate/suspend the AEPS membership:

a) The member has failed to comply with or violated any of the provisions of the AEPS

Procedural guidelines, as amended from time-to-time.

b) Member commits a material breach of AEPS Operating Procedures, which remains un-

remedied for thirty (30) days after giving notice.

c) The current account with RBI of the member bank is closed or frozen.

d) The member bank is amalgamated or merged with another member bank.

e) Steps have been initiated for winding up the business of the member bank.

f) Suspension or cancellation of RTGS membership.

36. Process of AEPS Membership’s Termination/Suspension:

a) NPCI shall inform in writing to the member bank regarding termination/suspension of its membership to AEPS.

b) If NPCI is of the opinion that the breach is not curable, it may suspend/terminate the

AEPS membership with immediate effect. However, the member bank shall be given an opportunity to be heard within thirty (30) days and confirming or revoking the termination/suspension passed on earlier.

c) NPCI may at any time, if it is satisfied, either on its own motion or on the representation

of the member that the order of suspension/termination of its membership may be revoked, it may pass on accordingly.

d) If the breach is capable of remedy but cannot be reasonably cured within thirty (30)

days period, termination/suspension will not be effective if the member in default

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

commences cure of the breach within thirty (30) days and thereafter diligently peruses such cure to the completion within sixty (60) days of such notice of breach.

e) The member bank whose termination of membership has been revoked shall be entitled

to apply for membership afresh in accordance with AEPS Procedural guidelines.

37. Prohibition to Use NPCI Logo/ Trademark /Network:

Upon termination from AEPS, the bank shall abstain from further using the AEPS Trademark with immediate effect and failure to comply with the same, shall invite legal proceedings.

Banks that have been terminated from AEPS membership shall be deprived of the privilege to use NPCI Switch for any transactions.

Any pending dispute pertaining to transaction errors not resolved before the member bank is terminated will be retrieved from the respective bank’s settlement account.

The terminated member bank shall not disclose any information regarding the AEPS Network or any knowledge gained through participation in the AEPS Network to the external world. Failure to comply with the same shall be treated as breach of trust and will invite legal penalties. This rule shall be binding on the terminated member bank for One (1) year from the date of the termination.

38. Fines:

NPCI reserves the right to impose a fine of an amount of equal to the One-Time Membership Fee on member banks participating in the AEPS Network upon violating the Common Operating Procedures for AEPS.

39. Frequent Deviation from AEPS Operating Procedures:

In the event of non-compliance with the Operating Procedures-AEPS, NPCI reserves the right either to notify the member bank or shall directly impose penalty on the member bank depending on its past record. No fines shall be imposed, if the rectification is done within the stipulated time frame, as set by NPCI, failing to abide by shall be subject to steering committee recommendations/legal penalties.

40. Pending Dues:

It is obligatory on the part of all member banks to clear all pending dues i.e. fines, etc. within the stipulated time frame as set by NPCI, failure to comply with, shall result in suspension/termination from further participation.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

41. Invoicing:

Fines will be billed separately and shall be sent to the respective member banks. The fines shall be payable to NPCI in accordance with the terms and conditions as defined in the invoice.

42. Compliance to Regulatory Guidelines by Reserve Bank of India:

All member banks shall strictly comply with the RBI’s notifications on financial inclusion business correspondent guidelines from time to time.

The Regulatory Guidelines of Reserve Bank of India shall have over-riding effect over the provisions made in these Guidelines.

43. Amendment to the Procedural Guidelines:

NPCI may issue amendments to these Guidelines from time to time by way of circular. The revised versions of the Guidelines may also be issued incorporating the new provisions periodically.

44. KYC/ AML Compliance as per RBI guidelines:

It would be the responsibility of the remitting and beneficiary banks to check any unusual pattern of remittance if any in respect of their respective customers. We have given in Annexure XI, a declaration to be signed and submitted to NPCI in this connection, by the member banks.

45. Inclusion of Regional Rural Banks (RRBS) in AEPS

NABARD has been very keen to include Regional Rural Banks in Aadhaar Enabled

Payment System (AEPS) to strengthen the financial inclusion network in rural areas.

Hence, Regional Rural Banks (RRBs) are proposed to join AEPS as per the “Sponsor Bank

Model” subject to RBI approval

The RRBs have adopted the Application Service Provider (ASP) model to implement Core

Banking Solutions (CBS). This has been supported both technically and financially by the

Sponsor Banks who typically have a 35 % share in the RRBs. Taking in to view the limited

IT and financial resources of the RRBs, NPCI has devised a sponsor bank model for

implementation of AEPS and RuPay AADHAAR MicroATM & ATM cards for RRB

customers.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

The main features of this model are:

• The Sponsor Bank must be a member of the AEPS service i.e. sponsor bank should be a direct AEPS member bank. The sponsor bank may have its own AEPS /FI switch.

• In AEPS, a transaction can be initiated from a MicroATM either manually or through

a card. We recommend issuance of RuPay AADHAAR card to customers as it will facilitate customer in performing a transaction. Customer is not required to remember its AADHAAR number & even IIN.

• A unique IIN will be issued to RRB by NPCI.

• Sponsor Bank will provide an IIN (BIN) update form to NPCI to update the said IIN

under their IIN list.

• NPCI would ask all the AEPS Member Banks to populate the IIN across AEPS network.

• IIN would be linked by Sponsor Bank to CBS of RRBs.

• NPCI will settle all RRB transactions (excluding On-Us which come through sponsor

bank to NPCI for UIDAI authentication gateway) with the Sponsor Bank as a part of the existing AEPS Settlement for the direct AEPS members.

• The existing reports of Daily Net Settlement Report and Raw Data Files sent to the

AEPS Members should be used for daily reconciliation.

• The access to the DMS would be given to a designated personnel nominated by the sponsor bank. However, sponsor bank would be responsible for all dispute handling on DMS on behalf of RRB whom they are facilitating.

• The transactions conducted at sponsor bank MicroATMs by the customers of RRBs

will be treated as on-us transactions.

• The transactions conducted between RRBs of the same sponsor bank will also be treated as on-us transactions.

• All AEPS settlements for RRB transactions would be settled by Sponsor Bank ONLY.

• The Sponsor Bank has to ensure that all guidelines of RBI / any regulatory authority

would be adhered to by the RRBs before connecting the RRB MicroATMs to the sponsor bank.

• Any RRB that chooses to use its own infrastructure such as MicroATMs or kiosk

would be issued a separate acquirer ID.

• If a RRB avails services of sponsor bank infrastructure then the acquirer ID of sponsor bank would be populated in the transaction request from bank.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

I. SET OF TRANSACTIONS

Currently, NPCI facilitate 4 types of transaction in AEPS. They are: • Balance Enquiry

• Cash Withdrawal

• Cash Deposit

• Aadhaar to Aadhaar Fund Transfer

We have envisaged 6 possible ways of performing a transaction as below:

i. TYPE 1- RRB CUSTOMER ON SAME RRB MICROATM

• In this type of transaction the RRB customer will visit its RRB MicroATM. • RRB MicroATM will send the encrypted packet to RRB switch/ASP

switch/Sponsor bank switch • The switch will forward the request to NPCI for getting the customer

authenticated from UIDAI. This will be used if the sponsor bank is not directly connected to UIDAI.

• Upon getting the response from UIDAI, NPCI will send the transaction back to sponsor bank

• Sponsor bank will send the transaction to RRB/ASP switch which will send it to CBS for necessary action as per the transaction type.

• The response of the transaction will be send to MicroATM and receipt will be generated.

• This will be an ON-US transaction for NPCI & will be charged for authentication service only.

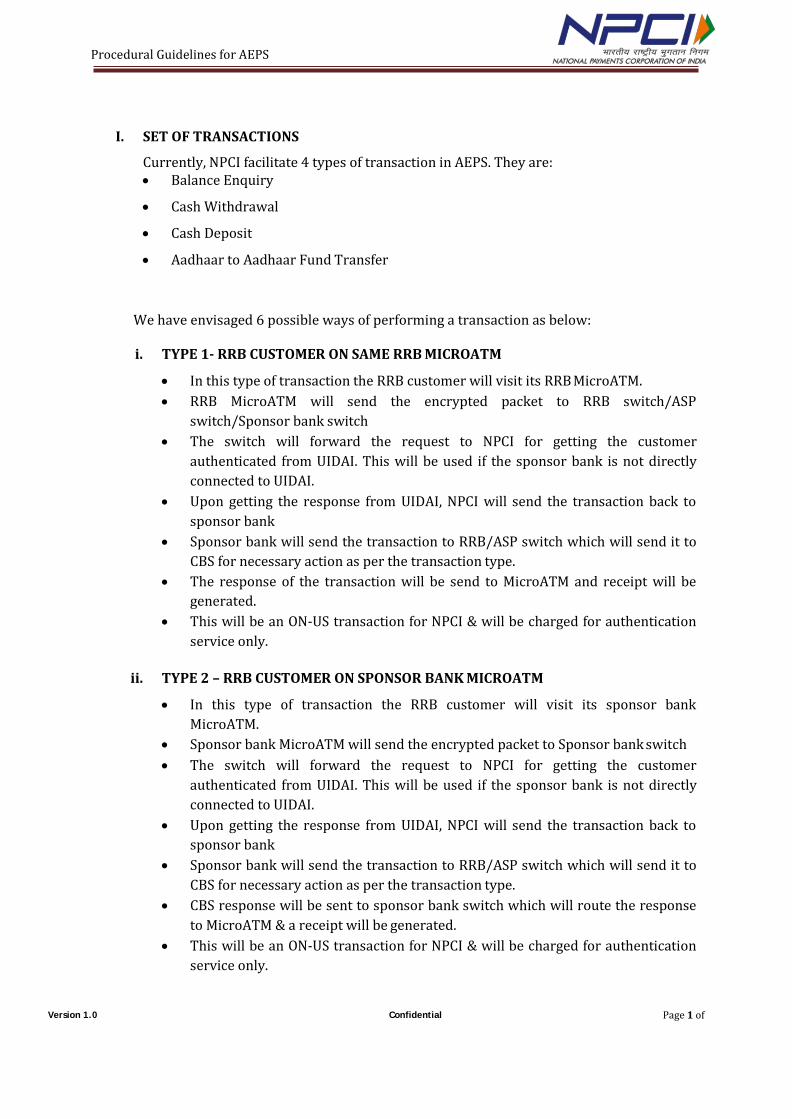

ii. TYPE 2 – RRB CUSTOMER ON SPONSOR BANK MICROATM

• In this type of transaction the RRB customer will visit its sponsor bank MicroATM.

• Sponsor bank MicroATM will send the encrypted packet to Sponsor bank switch • The switch will forward the request to NPCI for getting the customer

authenticated from UIDAI. This will be used if the sponsor bank is not directly connected to UIDAI.

• Upon getting the response from UIDAI, NPCI will send the transaction back to sponsor bank

• Sponsor bank will send the transaction to RRB/ASP switch which will send it to CBS for necessary action as per the transaction type.

• CBS response will be sent to sponsor bank switch which will route the response to MicroATM & a receipt will be generated.

• This will be an ON-US transaction for NPCI & will be charged for authentication service only.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

Transaction flow will be as below:

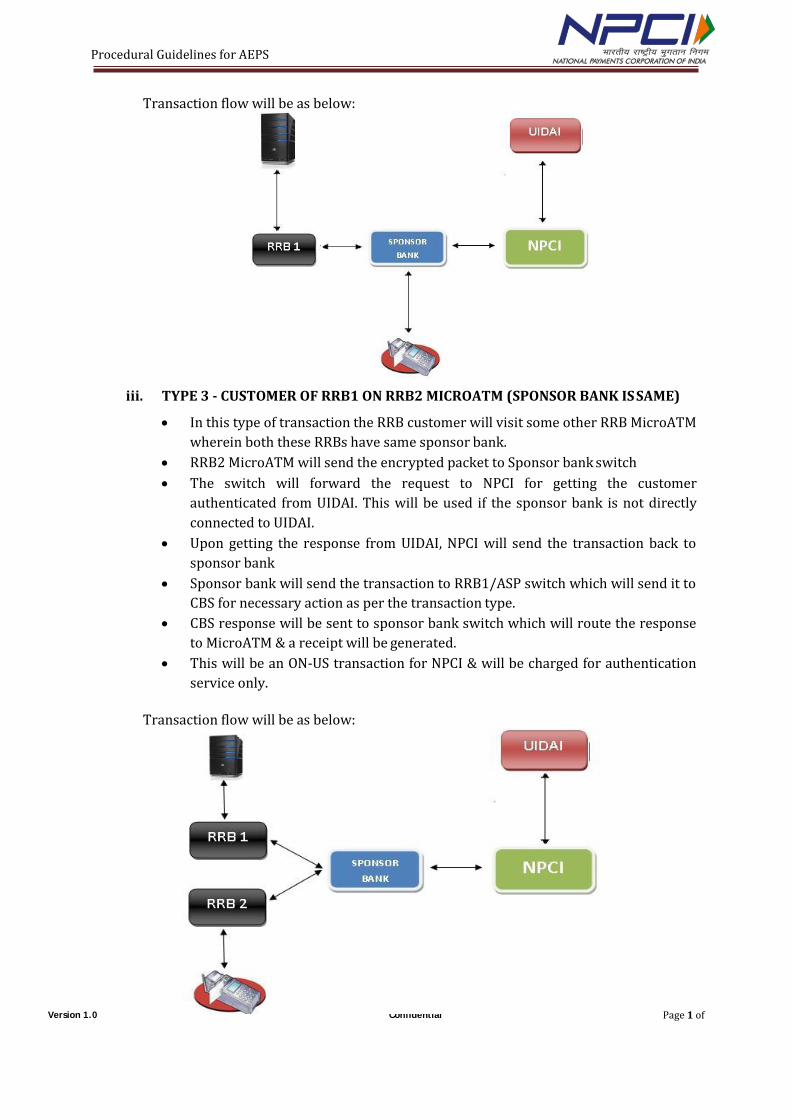

iii. TYPE 3 - CUSTOMER OF RRB1 ON RRB2 MICROATM (SPONSOR BANK IS SAME)

• In this type of transaction the RRB customer will visit some other RRB MicroATM wherein both these RRBs have same sponsor bank.

• RRB2 MicroATM will send the encrypted packet to Sponsor bank switch • The switch will forward the request to NPCI for getting the customer

authenticated from UIDAI. This will be used if the sponsor bank is not directly connected to UIDAI.

• Upon getting the response from UIDAI, NPCI will send the transaction back to sponsor bank

• Sponsor bank will send the transaction to RRB1/ASP switch which will send it to CBS for necessary action as per the transaction type.

• CBS response will be sent to sponsor bank switch which will route the response to MicroATM & a receipt will be generated.

• This will be an ON-US transaction for NPCI & will be charged for authentication service only.

Transaction flow will be as below:

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

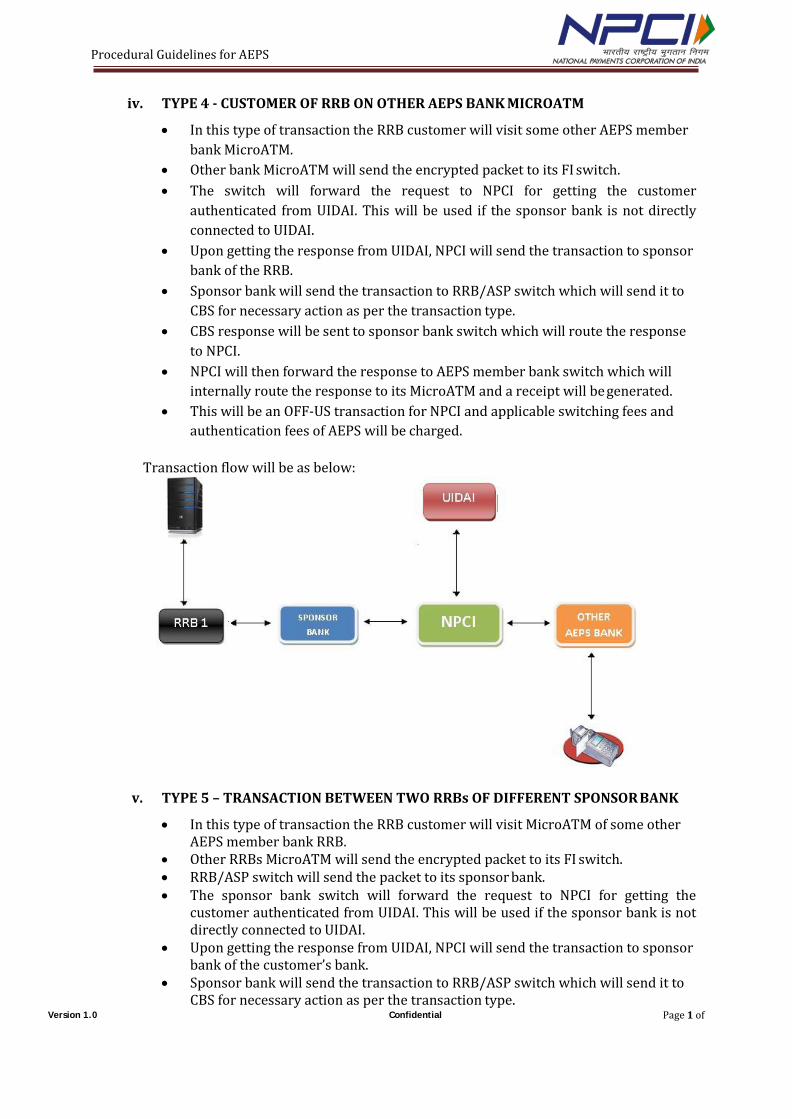

iv. TYPE 4 - CUSTOMER OF RRB ON OTHER AEPS BANK MICROATM

• In this type of transaction the RRB customer will visit some other AEPS member bank MicroATM.

• Other bank MicroATM will send the encrypted packet to its FI switch. • The switch will forward the request to NPCI for getting the customer

authenticated from UIDAI. This will be used if the sponsor bank is not directly connected to UIDAI.

• Upon getting the response from UIDAI, NPCI will send the transaction to sponsor bank of the RRB.

• Sponsor bank will send the transaction to RRB/ASP switch which will send it to CBS for necessary action as per the transaction type.

• CBS response will be sent to sponsor bank switch which will route the response to NPCI.

• NPCI will then forward the response to AEPS member bank switch which will internally route the response to its MicroATM and a receipt will be generated.

• This will be an OFF-US transaction for NPCI and applicable switching fees and authentication fees of AEPS will be charged.

Transaction flow will be as below:

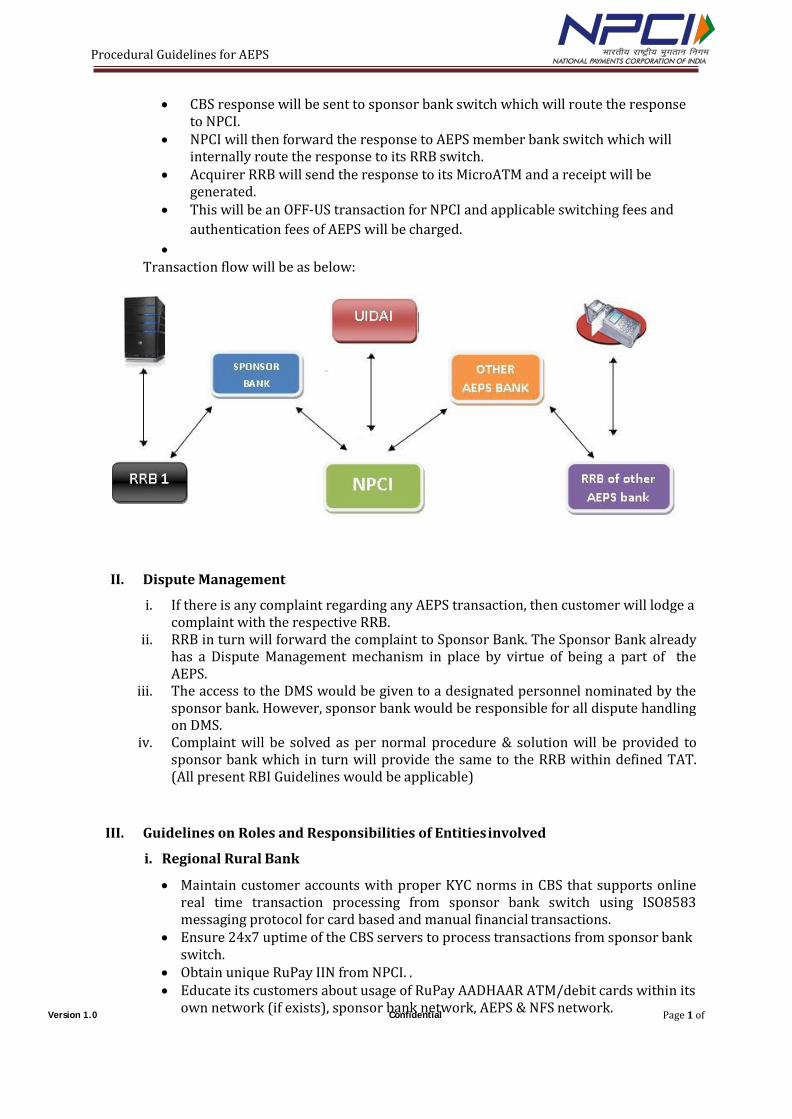

v. TYPE 5 – TRANSACTION BETWEEN TWO RRBs OF DIFFERENT SPONSOR BANK

• In this type of transaction the RRB customer will visit MicroATM of some other AEPS member bank RRB.

• Other RRBs MicroATM will send the encrypted packet to its FI switch. • RRB/ASP switch will send the packet to its sponsor bank. • The sponsor bank switch will forward the request to NPCI for getting the

customer authenticated from UIDAI. This will be used if the sponsor bank is not directly connected to UIDAI.

• Upon getting the response from UIDAI, NPCI will send the transaction to sponsor bank of the customer’s bank.

• Sponsor bank will send the transaction to RRB/ASP switch which will send it to CBS for necessary action as per the transaction type.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

• CBS response will be sent to sponsor bank switch which will route the response to NPCI.

• NPCI will then forward the response to AEPS member bank switch which will internally route the response to its RRB switch.

• Acquirer RRB will send the response to its MicroATM and a receipt will be generated.

• This will be an OFF-US transaction for NPCI and applicable switching fees and authentication fees of AEPS will be charged.

• Transaction flow will be as below:

II. Dispute Management

i. If there is any complaint regarding any AEPS transaction, then customer will lodge a complaint with the respective RRB.

ii. RRB in turn will forward the complaint to Sponsor Bank. The Sponsor Bank already has a Dispute Management mechanism in place by virtue of being a part of the AEPS.

iii. The access to the DMS would be given to a designated personnel nominated by the sponsor bank. However, sponsor bank would be responsible for all dispute handling on DMS.

iv. Complaint will be solved as per normal procedure & solution will be provided to sponsor bank which in turn will provide the same to the RRB within defined TAT. (All present RBI Guidelines would be applicable)

III. Guidelines on Roles and Responsibilities of Entities involved

i. Regional Rural Bank

• Maintain customer accounts with proper KYC norms in CBS that supports online real time transaction processing from sponsor bank switch using ISO8583 messaging protocol for card based and manual financial transactions.

• Ensure 24x7 uptime of the CBS servers to process transactions from sponsor bank switch.

• Obtain unique RuPay IIN from NPCI. . • Educate its customers about usage of RuPay AADHAAR ATM/debit cards within its

own network (if exists), sponsor bank network, AEPS & NFS network.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

• Establish a reliable network link with fall back/auto-failover options between their CBS servers and the Sponsor bank/ASP switch.

• Open a current account with sponsor bank for daily settlement of transactions carried out by its customers on AEPS. A corresponding reconciliation account will be maintained in the CBS of the Regional Rural Bank. The CBS system may have alerting mechanism via email/SMS/online dashboard that can alert the bank officials when the balance in this account falls below a threshold value.

• Maintain sufficient funds in the settlement account with sponsor bank as mutually decided by sponsor bank and RRB.

• Provide a 24x7 helpline number to its customers to address any issues they may face in using their card on their own or AEPS or NFS network. This helpline should be able to register a complaint raised by the customers and provide feedback on the complaints previously registered by them.

ii. Sponsor Bank

• The Sponsor Bank is responsible for sharing its switch with its RRBs and establishing a link with AEPS for routing all RRB transactions. This linkage should be as per specifications and requirements intimated from time to time by AEPS and must be configurable.

• Carry out settlement of AEPS transactions on behalf of its member RRBs. • Provide the operational and technical support to the RRB for reconciliation and

dispute resolution. If the RRB needs to raise a dispute on behalf of its customer for a transaction carried out on AEPS, the same should be raised through the sponsor bank.

• Host and provide a standard AEPS switch to Regional Rural Banks • Ensure that all off-us transactions are routed via AEPS. • Provide daily settlement and reconciliation reports to each RRB and provide

complete transaction record for dispute resolution. • Maintain a network link with fall back/auto-failover options to RRB CBS. • Provide reconciliation reports to sponsor bank and each RRB for transactions

routed to and from AEPS. • To ensure strict compliance of AEPS guidelines and RBI guidelines by the RRBs

sponsored by them.

• Important points to be considered: i. All Risk Management would be done by the Sponsor Bank Switch as per the

requirement of the AEPS Member Banks ii. All settlement would be done at Sponsor Bank Settlement Account (Existing)

and no separate report would be provided by AEPS to the Sponsor banks. iii. The settlements are done on a T + 1 Basis. iv. All regulations of RBI/AEPS related to the Switching Issued by AEPS from

time to time would be binding on Sponsor Bank ASP Switch. v. NPCI would certify the sponsor bank Switch as and when required by them.

vi. Sponsor bank’s switch to comply with AEPS Interface specification and other requirements to get certified for AEPS Switch.

vii. The Sponsor Bank Switch, RRB will at all times comply with the AEPS operating procedures.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

Definitions & Abbreviations Annexure-I

i) Aadhaar: A Unique Identification number issued by the Unique Identification Authority of India to a resident in India.

ii) AML: Anti Money Laundering

iii) ATM: Automated Teller Machine

iv) BC: Business Correspondent.

v) Correspondent Bank: The Bank whom a BC represents and corresponds with.

vi) Customer: Customer shall refer to an Aadhaar enabled account holder of a bank.

vii) DMS: Dispute Management System - an on-line application for resolving disputes arising out of

interbank AEPS transaction.

viii) FI: Financial Inclusion.

ix) IBA: Indian Banks Association.

x) IDRBT: Institute for Development and Research in Banking Technology.

xi) KYC: Know Your Customer.

xii) MicroATM: A Point of Sale (POS) device used by a Business Correspondent for handling customer initiated cash and transfer transactions.

xiii) IIN: Issuer Identification Number issued by National Payments Corporation of India for the

specified service.

xiv) NFS: National Financial Switch of National Payments Corporation of India.

xv) NPCI: National Payments Corporation of India.

xvi) NREGA: National Rural Employment Guarantee Act

xvii) PDO-NDS: Negotiated Dealing System of Public Debt Office, RBI.

xviii) SGL Account: Subsidiary General Ledger Account.

xix) RBI: Reserve Bank of India.

xx) RTGS: Real Time Gross Settlement System of RBI.

xxi) AEPS: Aadhaar Enabled Payment System.

xxii) SGF: Settlement Guarantee Fund.

xxiii) SMS: Small Messaging Service.

xxiv) UIDAI: Unique Identification Authority of India.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

Annexure-II (On the Letter Head of the Applicant Bank)

Application for AEPS Membership

The Chief Executive Officer National Payments Corporation of India C-9, 8th Floor, RBI Premises, Bandra Kurla Complex, Bandra (E), Mumbai-400 051

Dear Sir,

Subject: Aadhaar Enabled Payment System (AEPS) Membership.

We would like to participate in the Aadhaar Enabled Payment System (AEPS) and agree to the Terms & Conditions stipulated thereof.

Kindly take a note of details provided below: Name of the Bank

Connectivity Option Bank Switch/ Primary Single Service Provider’s Switch

Location of the Switch AEPS Contact Person Name (A Single point of contact)

Telephone Number Fax Number Email Id Brief Details (Hardware, Software & Network)

Test Switch IP Address: Port Production switch IP Address: Port

The above application is being made under the Authority of our Board and certified true copy of the Board Resolution shall be submitted once we receive an In Principle approval from NPCI.

The documents required in this connection as under are submitted herewith: i) Mandate to RBI - (Stamped in Duplicate) (Annexure-IX) ii) Non-Disclosure Agreement - (Stamped) (Annexure-X) iii) KYC/ AML Undertaking - (Annexure-XI) iv) General Undertaking - (Annexure-XVI)

Authorised signatory

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

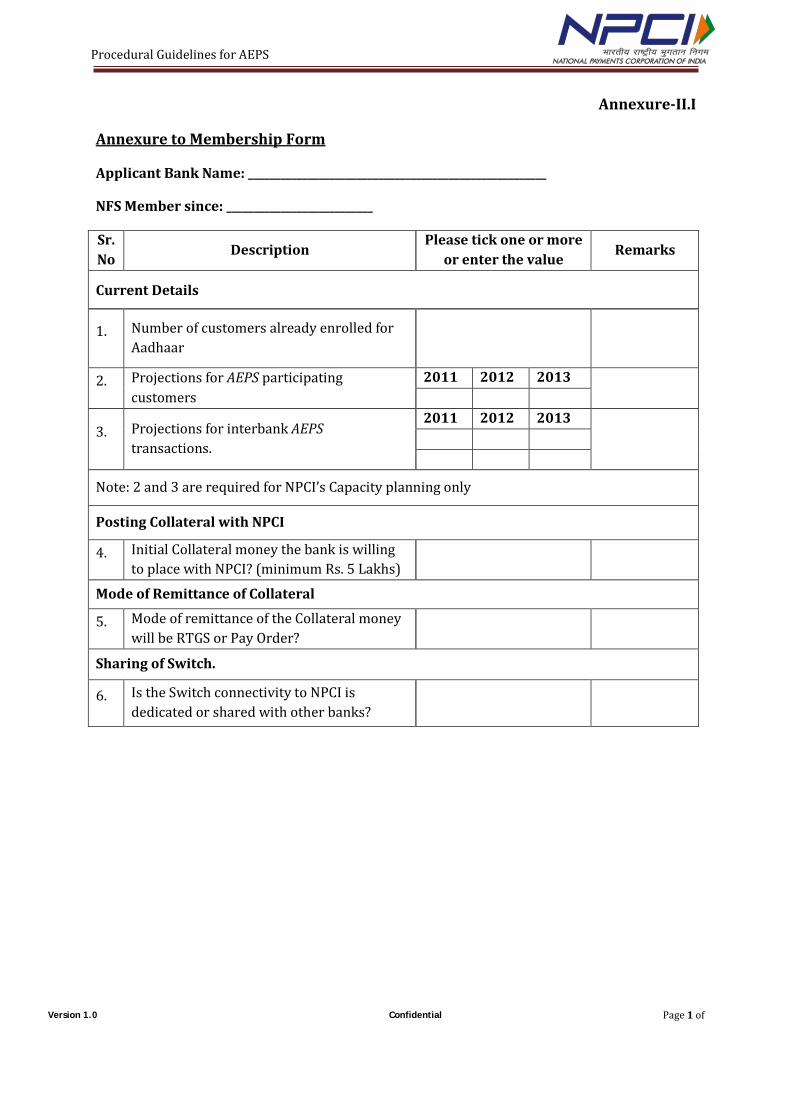

Annexure-II.I

Annexure to Membership Form

Applicant Bank Name: _______________________________________________________

NFS Member since: ___________________________

Sr. No Description

Please tick one or more or enter the value Remarks

Current Details

1. Number of customers already enrolled for Aadhaar

2. Projections for AEPS participating customers

2011 2012 2013

3. Projections for interbank AEPS transactions.

2011 2012 2013

Note: 2 and 3 are required for NPCI’s Capacity planning only

Posting Collateral with NPCI

4. Initial Collateral money the bank is willing to place with NPCI? (minimum Rs. 5 Lakhs)

Mode of Remittance of Collateral

5. Mode of remittance of the Collateral money will be RTGS or Pay Order?

Sharing of Switch.

6. Is the Switch connectivity to NPCI is dedicated or shared with other banks?

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

Annexure-III

Connectivity Options

Annexure-IV

NPCI Offered Aadhaar Authentication - Process flow

Customer’s Inputs: • IIN • AADHAAR Number • Finger Print Data

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

Annexure-V

Aadhaar Initiated Inter Bank Balance Enquiry - Process flow

Customer’s Inputs: • IIN • AADHAAR Number • Finger Print Data

Annexure-VI

Aadhaar Initiated Interbank Cash Deposit - Process flow

Customer’s Inputs: • IIN • AADHAAR Number • Amount of Cash to be Deposited • Finger Print Data

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

Annexure-VII

Aadhaar initiated Interbank Cash Withdrawal – Process flow

Customer’s Inputs: • IIN • AADHAAR Number • Amount of Cash to be Withdrawn • Finger Print Data

Annexure-VIII

Aadhaar to Aadhaar Interbank Funds Transfer - Process flow

Remitting Customer’s Inputs: Beneficiary’s Details: • IIN • IIN • Aadhaar Number • Aadhaar Number • Amount to be remitted • Finger Print Data

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

Annexure-IX

ON STAMP PAPER

Letter of Authority

To,

The Regional Director, Reserve Bank of India Mumbai

Dear Sir,

Our Current A/c No. and Settlement A/c No with the Reserve Bank of India (RBI) Mumbai.

1. National Payments Corporation of India (hereafter referred to as the NPCI) has admitted us

as member of a networking arrangement called the Aadhaar Enabled Payments System (AEPS) whereby switching and processing of all our electronic payments transactions over their network takes place under NPCI’s guarantee of clearing and settlement of our transactions.

2. For that purpose, we hereby authorize and request that as and when a settlement instruction is received by you from the NPCI relating to our transactions in the said AEPS Network, you may, without reference to us, debit/credit our above Current Account/s with such sums as may be specified by the NPCI in its settlement instructions, notwithstanding any dispute that may exist or arise between us and NPCI.

3. The settlement instruction for debiting/crediting our Current Account/s with you shall be conclusive proof of debit/credit of our Current Account/s relating to our transaction in the said AEPS Network as referred to in paragraph 2 above and it shall not be necessary for us to admit and/ or confirm to the fact of such debit/credit by means of separate advice to you and/ or NPCI.

4. We hereby further unconditionally and irrevocably undertake to arrange for the requisite funds in our Current Account with Deposit Account Department, Reserve Bank of India, Mumbai to meet the demand of NPCI. We shall be bound by this undertaking and shall be liable therefore under all circumstances.

5. The mandate and undertaking shall not be revoked by us except with the prior concurrence of both the NPCI and the Reserve Bank of India (RBI) and you may act upon this mandate till such time this authority is revoked in writing and all actions taken by RBI in pursuance of this mandate shall be absolutely binding on us, without any risk or responsibility to the RBI.

Thanking you, Yours faithfully, For and on behalf of the Applicant

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

Annexure-X

(On Rs. 100/- Stamp paper)

NON-DISCLOSURE AGREEMENT

This Non-Disclosure Agreement is made and entered into at Mumbai as of <Date in words> (DD-MM-YYYY), the (“Effective Date”) By and Between having its registered office < Bank Name>, carrying on the business of Banking, having its registered office at <Bank Registered Office Address(herein referred to as “Bank”)

And

National Payments Corporation of India (NPCI), a company incorporated under Section 25 of the Companies Act, 1956 and having its registered office at C9, 8th Floor, RBI Building, Bandra- Kurla Complex, Bandra (East), Mumbai – 400 051 (herein referred to as “NPCI”).

Each of Bank and NPCI is sometimes referred to herein as a “Party” and together as the “Parties”, each of which expression shall, unless repugnant to the context or meaning thereof, shall mean and includes its respective successors and permitted assigns.

RECITALS

WHEREAS, NPCI an umbrella organization, is inter alia engaged in catering the banking sector requirements in the areas of Retail Payments and Settlements, and providing National Financial Switch(NFS), Interbank Mobile Payment Service(IMPS) and Aadhaar Enabled Payment System (AEPS); And

WHEREAS, Bank is inter alia engaged in the business of Banking; And

WHEREAS, NPCI has and is in the process of entering into agreements with various Banks admitting the Banks in NFS, IMPS and AEPS; And

WHEREAS, the Parties presently desire to discuss and/or consult with each other's business for the purposes of entering into Agreements for use of AEPS services. And

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

WHEREAS, the Parties recognize that each other’s business involves specialized and proprietary knowledge, information, methods, processes, techniques and skills peculiar to their security and growth and that any disclosure of such methods, processes, skills, financial data, or other confidential and proprietary information would substantially injure a Party’s business, impair a Party’s investments and goodwill, and jeopardize a Party’s relationship with a Party’s clients and customers; And

WHEREAS, in the course of consultation with respect to the potential business venture, the Parties anticipate disclosing to each other certain information of a novel, proprietary, or confidential nature, and desire that such information be subject to all of the terms and conditions set forth herein below.

NOW, THEREFORE, the Parties hereto, in consideration of the premises and other good and valuable consideration, agree such information shall be treated as follows:

1. Confidential Information. “Confidential Information” shall mean and include any

information which relates to the financial and/or business operations of each Party, including but not limited to, specifications, drawings, sketches, models, samples, reports, forecasts, current or historical data, computer programs or documentation and all other technical, financial or business data, including, but not limited to, information related to each Party's customers, products, processes, financial condition, employees, intellectual property, manufacturing techniques, experimental work, trade secrets.

2. Use of Confidential Information. Each Party agrees not to use the other's Confidential

Information for any purpose other than for the specific consultation regarding the potential business venture. Any other use of such Confidential Information by any party shall be made only upon the prior written consent from an authorized representative of the other Party which wishes to disclose such information (the “Disclosing Party”) or pursuant to subsequent agreement between the Parties hereto.

3. Restrictions. Subject to the provisions of paragraph 4 below, the Party receiving

Confidential Information (the “Receiving Party”) shall, for a period of five (5) years from the date of the last disclosure of Confidential Information made under this Agreement 1(except for personal customer data which shall remain confidential forever), use the same care and discretion to limit disclosure of such Confidential Information as it uses with similar confidential information of its own and shall not disclose, lecture upon, publish, copy, modify, divulge either directly or indirectly, use(except as permitted above under clause 2) or otherwise transfer the Confidential Information to any other person or entity, including taking reasonable degree of care and steps to: a. restrict disclosure of Confidential Information solely to its concerned employees,

agents, advisors, consultants, contractors and /or subcontractors with a need to know and not disclose such proprietary information to any other parties; and

b. advise all receiving Party employees with access to the Confidential Information of the obligation to protect Confidential Information provided hereunder and obtain from agents, advisors, contractors and/ or consultants an agreement to be so bound.

c. use the Confidential Information provided hereunder only for purposes directly related to the potential business venture.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

4. Exclusions. The obligations imposed upon either Party herein shall not apply to information, technical data or know how, whether or not designated as confidential, that:

a. is already known to the Receiving Party at the time of the disclosure without an

obligation of confidentiality; b. is or becomes publicly known through no unauthorized act of the Receiving Party; c. is rightfully received from a third Party without restriction and without breach of this

Agreement; d. is independently developed by the Receiving Party without use of the other Party’s

Confidential Information and is so documented; e. is disclosed without similar restrictions to a third party by the Party owning the

Confidential Information; f. is approved for release by written authorization of the Disclosing Party; or g. is required to be disclosed pursuant to any applicable laws or regulations or any order

of a court or a governmental body; provided, however, that the Receiving Party shall first have given notice to the Disclosing Party and made a reasonable effort to obtain a protective order requiring that the Confidential Information and/or documents so disclosed by used only for the purposes for which the order was issued..

5. Return of Confidential Information. All Confidential Information and copies and extracts

of it shall be promptly returned to the Disclosing Party at any time within thirty (30) days of receipt of a written request by the Disclosing Party for the return of such Confidential Information.

6. Ownership of Information. The Parties agree that all Confidential Information shall remain

the exclusive property of the Disclosing Party and its affiliates, successors and assigns.

7. No License Granted. Nothing contained in this Agreement shall be construed as granting or conferring any rights by license or otherwise in any Confidential Information disclosed to the Receiving Party or to any information, discovery or improvement made, conceived, or acquired before or after the date of this Agreement. No disclosure of any Confidential Information hereunder shall be construed to be a public disclosure of such Confidential Information by either Party for any purpose whatsoever.

8. Breach. In the event the Receiving Party discloses, disseminates or releases any

Confidential Information received from the Disclosing Party, except as provided above, such disclosure, dissemination or release will be deemed a material breach of this Agreement and the Disclosing Party shall have the right to demand prompt return of all Confidential Information previously provided to the Receiving Party. The provisions of this paragraph are in addition to any other legal right or remedies the Disclosing Party may have.

9. Arbitration and Equitable Relief.

a. Arbitration. The Parties shall attempt to settle any disputes arising out of or relating to this Agreement through consultation and negotiation. In the event no settlement can be reached through such negotiation and consultation, the Parties agree that such disputes shall be referred to and finally resolved by arbitration under the provisions of the Arbitration and Conciliation Act, 1996 or any statutory modification thereof shall apply. The arbitration shall be held in Mumbai. The language used in the arbitral proceedings shall be English. The Parties shall appoint their own arbitrators.

b. Equitable Remedies. The Parties agree that it would be impossible or inadequate to

measure and calculate the Disclosing Party's damages from any breach of the

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

covenants set forth herein. Accordingly, the Parties agree that in event of breach of any of the covenants contained in this Agreement, the affected Party shall have, in addition to any other right or remedy available, the right: i) to obtain an injunction from a court of competent jurisdiction restraining such breach or threatened breach; and ii) to specific performance of any such provisions of this Agreement. The Parties further agree that no bond or other security shall be required in obtaining such equitable relief and the Parties hereby consent to the issuance of such injunction and to the ordering of specific performance.

c. Legal Expenses. If any action and proceeding is brought for the enforcement of this

Agreement, or because of an alleged or actual dispute, breach, default, or misrepresentation in connection with any of the provisions of this Agreement, each Party shall bear its own expenses, including the attorney's fees and other costs incurred in such action.

10. Term. This Agreement may be terminated by either Party giving sixty (60) days' prior

written notice to the other Party; provided, however, the obligations to protect the Confidential Information in accordance with this Agreement shall survive for a period of five (5) years from the date of the last disclosure of Confidential Information made under this Agreement (except for personal customer data which shall remain confidential forever).

11. No Formal Business Obligations. This Agreement shall not constitute create, give effect to

or otherwise imply a joint venture, pooling arrangement, partnership, or formal business organization of any kind, nor shall it constitute, create, give effect to, or otherwise imply an obligation or commitment on the part of either Party to submit a proposal or to perform a contract with the other Party or to refrain from entering into an agreement or negotiation with any other Party. Nothing herein shall be construed as providing for the sharing of profits or loss arising out of the efforts of either or both Parties. Neither Party will be liable for any of the costs associated with the other's efforts in connection with this Agreement. If the Parties hereto decide to enter into any licensing arrangement regarding any Confidential Information or present or future patent claims disclosed hereunder, it shall only be done on the basis of a separate written agreement between them.

12. General Provisions.

a. Governing Law. This Agreement shall be governed by and construed in accordance with the laws of India.

b. Severability. If one or more of the provisions in this Agreement is deemed void by law,

the remaining provisions shall continue in full force and effect. c. Successors and Assigns. This Agreement shall be binding upon the successors and/or

assigns of the Parties, provided however that neither Party shall assign its rights or duties under this Agreement without the prior written consent of the other Party.

d. Headings. All headings used herein are intended for reference purposes only and shall

not affect the interpretation or validity of this Agreement.

e. Entire Agreement. This Agreement constitutes the entire agreement and understanding of the Parties with respect to the subject matter of this Agreement. Any amendments or modifications of this Agreement shall be in writing and executed by a duly authorized representative of the Parties.

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

f. Two original sets of Non-Disclosure Agreement are executed and retained by either parties, Bank and NPCI.

The Parties, by the signature of their authorized representatives appearing below, acknowledge that they have read and understand each and every term of this Agreement and agree to be bound by its terms and conditions.

ACCEPTED AND AGREED TO BY: NATIONAL PAYMENTS CORPORATION OF INDIA

(Signature)

Print Name:

Title: IN WITNESS WITH:

(TYPE BANK’s NAME)

(Signature)

Print Name:

Title: IN WITNESS WITH:

Bank:

(Signature)

Print Name:

Title:

NPCI:

(Signature)

Name:

Title:

Procedural Guidelines for AEPS

Version 1.0 Confidential Page 1 of

Annexure-XI

Bank’s Letter Head.

KYC/AML Undertaking By Banks

We (Name of the bank) with registered office at