Embed Size (px)

Citation preview

Steadfast 1

GROUP INSURANCE

Product Information

PRODUCT DISCLOSURE STATEMENT

2 Group Insurance Product Disclosure Statement Steadfast 3

Overview 3General advice notice 3How to read this document 3How to contact us 3About MetLife 4About Steadfast 4What is group insurance? 4Reasons to consider this product 4

MetLife group insurance product summary 5Key benefits of group insurance 5Key benefits of group life insurance 6Key benefits of group income protection insurance 6Optional benefits for group income protection insurance (additional costs) 7Available terms for group income protection insurance 9Group insurance cover levels and maximum entry and insurable age 9

General conditions 10Policy document 10Eligibility 10Commencement of cover 10Automatic acceptance 10Takeover terms 11Exclusions 12

Other features 13Interim accident cover 13Extended cover 13Life events cover 14Leave of absence 14Overseas residence and travel 15Continuous review 15

Optional benefits 16Cover beyond age 65 16To age 65 benefit period - top up 16Increasing benefits option 17Accidental death benefit 17Continuation option 17

Product detail 18Terms and conditions of benefits 18Income protection benefit offsets 23Total and Permanent Disablement benefit tapering and definitions 23

Opt-out or reduction in cover 24Reinstatement of cover 24Cessation of group income protection payments 24Claims 24Payment of benefits 25

Termination and cancellation 26Cessation of cover - group life insurance 26Cessation of cover - group income protection insurance 26Termination and cancellation 27Cover after a policy terminates 27

Additional information 28Underwriting 28Forward underwriting limits 28Claims 28Premium and frequency loadings 28Waiver of premium 29Variation of terms 29Tax and stamp duty 29Profit share 29Multinational pooling 30Captive arrangements 30Statutory fund 30

Technology and services 31eApply 31eLodgement 31eQuery 32Claims and service model 32Tele-Assessment 32Claims 32

Other important information 33Cooling off period 33Your duty of disclosure 33Non-disclosure 33Additional rights 34Guaranteed renewable 34Commissions 34Complaints resolution 34 Privacy 34

Definitions 35

General advice notice

This Product Disclosure Statement (PDS) is issued and designed by MetLife to provide general information only about the benefits and other features of MetLife’s group insurance products. It has been designed without considering your objectives, financial situation or needs and is not intended to be personal financial advice. As a result, before acting on this information, you should consider the appropriateness of the information having regard to your objectives, financial situation and needs. The Policy Document and associated Policy Schedule for each Policy contains the full terms and conditions governing the Policy including benefits, definitions and exclusions.

Published: November 2014 Issuer: MetLife Insurance Limited (MetLife) (ABN 75 004 274 882, AFSL No. 238096)

How to read this document

In this PDS, references to ‘we‘, ‘our‘, ‘us‘ and ‘MetLife‘ are references to MetLife Insurance Limited. References to ‘you‘ or ‘your’ are references to the Policy Owner, as the context requires. References to ‘member’ or ‘employee’ are references to the proposed Covered Persons, as the context requires.

Words that are in bold and with capital letters at the beginning are defined in the ‘Definitions’ section.

The definitions refer to the meaning of terms in this booklet only. The terms and conditions of each Policy are set out in the relevant Policy Document.

The information contained in this PDS is current at the time of issue.

From time to time we may change or update information that is not materially adverse by providing a notice of changes on our website www.metlife.com.au.

If there is a materially significant change or omission to this PDS, we will issue you with a notice of the changes.

You can also obtain a paper copy of the updated information by calling us on 1300 319 209.

Disclaimer: For Advisers only. Not intended to be financial product advice. Products are offered by MetLife, which is an affiliate of MetLife, Inc. and operates under the “MetLife” brand. None of the obligations of MetLife are guaranteed by MetLife, Inc. (incorporated in the USA) or any other member of the MetLife group.

PEANUTS © United Feature Syndicate, Inc.

OVERVIEWCONTENTS

How to contact us

MetLife Insurance LimitedLevel 9, 2 Park Street, Sydney NSW 2000ABN 75 004 274 882AFSL No. 238096

Telephone: 1300 319 [email protected]

4 Group Insurance Product Disclosure Statement Steadfast 5

About MetLife

MetLife provides group insurance through superannuation and employer groups and individual life insurance products. In Australia, MetLife is a specialist provider of life and income protection insurance. Since its entry into the Australian market in 2005, MetLife has grown its group insurance market share, doubling the size of its group business. This product is issued and underwritten by MetLife Insurance Limited. The other members of the MetLife Group do not issue, guarantee or underwrite this product.

Globally, the MetLife companies reach more than 90 million customers throughout Asia-Pacific, the Americas and Europe. The MetLife companies include the number one life insurer in the United States (based on policies inforce), with close to 150 years of experience and relationships with more than 90 of the top 100 FORTUNE 500® companies in the United States.

About Steadfast

Steadfast Group Limited (Steadfast), ABN 98 073 659 677, AFS License No. 254928 is a public company. It includes a large network of insurance brokerages who operate in Australia as Steadfast Brokers. This PDS is available exclusively to you through a Steadfast Broker.

Steadfast does not issue, guarantee or underwrite this product.

What is group insurance?

Group insurance provides insurance solutions to groups of people associated by common factors. Employees of a company or members of a superannuation fund are the most common groups. Group insurance can add value to an employer’s employee benefits program or allow superannuation funds to provide competitive insurance cover to their members.

Reasons to consider this product

• Automatic acceptance of cover: Covered Persons may be provided with automatic cover without the need for underwriting.

• Interim accident cover: accident only cover provided if a person is being underwritten for cover.

• Retraining expense benefit: access to an approved retraining program to assist Covered Persons to return to work.

• 24 hour worldwide cover: cover provided 24 hours a day.

• Cover beyond age 65: cover available up to age 70 for both group income protection and group life insurance.

• Continuous review: benefits based on salary as at date of claim, not at last annual review.

METLIFE GROUP INSURANCE PRODUCT SUMMARYKey benefits of group insurance

BENEFIT WHAT IS IT?

Extended cover

Refer to ‘Extended cover’ on page 13

Provides cover for up to 60 days where a Covered Person ceases Employment with the Employer and ceases to be eligible for cover under a Policy.

Interim accident cover

Refer to ‘Interim accident cover’ on page 13

Provides accident only cover for up to 90 days if a person is being underwritten for cover.

Guaranteed renewable

Refer to ‘Guaranteed renewable’ on page 34

Provided the premiums are paid and the terms and conditions of the Policy are met, we guarantee to renew the Policy each year.

24 hour worldwide cover

Refer to ‘Overseas residence and travel’ on page 15

Cover for a Covered Person is provided 24 hours a day, depending on the circumstances of overseas travel.

Waiver of underwriting loadings Where a premium loading is recorded for a Covered Person, we will not charge the extra premium for the loading except if the Covered Person exercises a continuation option. This is only applicable to formula based cover and where the Policy covers 50 or more Covered Persons.

6 Group Insurance Product Disclosure Statement Steadfast 7

Key benefits of group life insurance

BENEFIT WHAT IS IT?

Death Benefit A lump sum payment upon the Covered Person’s death.

The Benefit paid is the amount of cover held as death cover.

Terminal Illness Benefit

An advancement of the death Benefit if the Covered Person is certified to be suffering from a Terminal Illness.

The Benefit paid is the amount of cover held as death cover.

Total and Permanent Disablement Benefit

A lump sum payment if the Covered Person is permanently unable to work due to Illness or Injury.

The Benefit paid is the amount of cover held as Total and Permanent Disablement cover.

Life events cover

Refer to ‘Life events cover’ on page 14

Provides additional cover without underwriting for a Covered Person when specific events occur in their life.

Key benefits of group income protection insurance

BENEFIT WHAT IS IT?

Disability Benefit A monthly benefit if the Covered Person is Disabled and unable to work due to Illness or Injury.

The Benefit paid is the amount of cover held as the Disability Monthly Benefit.

Partial Disability Benefit

A monthly benefit if the Covered Person is only able to work in a reduced capacity due to Illness or Injury.

The Benefit paid is the amount of cover held as the Partial Disability Monthly Benefit.

Retraining Expense Benefit

Additional benefit to cover the costs incurred if the Covered Person is on claim for the Disability Benefit or Partial Disability Benefit and they undergo a retraining program that we have approved. This payment is made directly to the Covered Person’s retraining program provider.

The Benefit paid is the amount of the Retraining Expenses, as approved by us.

BENEFIT WHAT IS IT?

Death Benefit A lump sum payment if the Covered Person dies whilst on claim.

For a Covered Person aged 65 or older, the Benefit paid is the lesser of:

(a) the sum of 3 times the Disability Monthly Benefit; and

(b) $30,000.

For a Covered Person aged less than 65, the Benefit paid is the sum of 3 times the Disability Monthly Benefit.

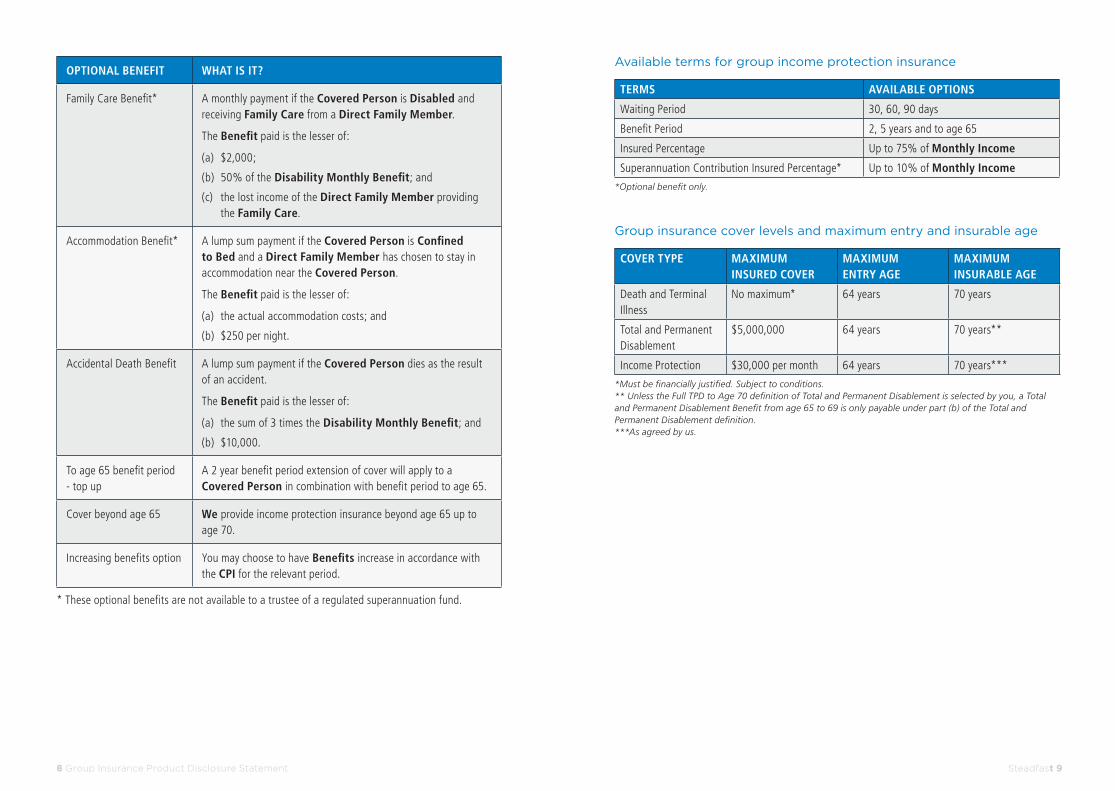

Optional benefits for group income protection insurance (additional costs)

OPTIONAL BENEFIT WHAT IS IT?

Superannuation Contribution Benefit

A continuation of superannuation contributions whilst on claim for the Disability Benefit or Partial Disability Benefit.

The Benefit paid is the amount of the Superannuation Contribution Monthly Benefit.

Crisis Benefit* A lump sum payment in addition to the Disability or Partial Disability Benefit (if applicable) if the Covered Person is diagnosed with one of the Crisis Benefit Medical Conditions.

The Benefit paid is the sum of 3 times the Disability Monthly Benefit. If the Covered Person is over age 65, the Benefit will be 3 times the lesser of:

(a) the Disability Monthly Benefit; and

(b) $10,000 per month.

Specific Injury Benefit* A monthly benefit if the Covered Person suffers one of the Specific Injury Events.

The Disability Monthly Benefit is paid for a set number of months which varies based on the Specific Injury Event suffered by the Covered Person.

Nursing Care Benefit* A daily payment if the Covered Person is Confined to Bed for 3 or more consecutive days during the Waiting Period.

The Benefit paid is the lesser of:

(a) 1/30th of the Disability Monthly Benefit; and

(b) $150.00 per day.

8 Group Insurance Product Disclosure Statement Steadfast 9

Available terms for group income protection insurance

TERMS AVAILABLE OPTIONS

Waiting Period 30, 60, 90 days

Benefit Period 2, 5 years and to age 65

Insured Percentage Up to 75% of Monthly Income

Superannuation Contribution Insured Percentage* Up to 10% of Monthly Income

*Optional benefit only.

Group insurance cover levels and maximum entry and insurable age

COVER TYPE MAXIMUM INSURED COVER

MAXIMUM ENTRY AGE

MAXIMUM INSURABLE AGE

Death and Terminal Illness

No maximum* 64 years 70 years

Total and Permanent Disablement

$5,000,000 64 years 70 years**

Income Protection $30,000 per month 64 years 70 years***

*Must be financially justified. Subject to conditions.** Unless the Full TPD to Age 70 definition of Total and Permanent Disablement is selected by you, a Total and Permanent Disablement Benefit from age 65 to 69 is only payable under part (b) of the Total and Permanent Disablement definition.***As agreed by us.

OPTIONAL BENEFIT WHAT IS IT?

Family Care Benefit* A monthly payment if the Covered Person is Disabled and receiving Family Care from a Direct Family Member.

The Benefit paid is the lesser of:

(a) $2,000;

(b) 50% of the Disability Monthly Benefit; and

(c) the lost income of the Direct Family Member providing the Family Care.

Accommodation Benefit* A lump sum payment if the Covered Person is Confined to Bed and a Direct Family Member has chosen to stay in accommodation near the Covered Person.

The Benefit paid is the lesser of:

(a) the actual accommodation costs; and

(b) $250 per night.

Accidental Death Benefit A lump sum payment if the Covered Person dies as the result of an accident.

The Benefit paid is the lesser of:

(a) the sum of 3 times the Disability Monthly Benefit; and

(b) $10,000.

To age 65 benefit period - top up

A 2 year benefit period extension of cover will apply to a Covered Person in combination with benefit period to age 65.

Cover beyond age 65 We provide income protection insurance beyond age 65 up to age 70.

Increasing benefits option You may choose to have Benefits increase in accordance with the CPI for the relevant period.

* These optional benefits are not available to a trustee of a regulated superannuation fund.

10 Group Insurance Product Disclosure Statement Steadfast 11

Policy document

If we are selected as a group insurer, the Policy Owner will be provided with a Policy and Policy Schedule/s which sets out the final terms and conditions of the group’s insurance Policy with us.

Where the Policy Owner is the trustee of a superannuation fund, benefit payments are made through the superannuation fund and may be subject to restrictions under regulated superannuation law.

Eligibility

To be eligible for group insurance, the person must:

(a) be Employed by the Employer;

(b) be an Australian Resident or a holder of a temporary work visa subclass 457 issued by the Australian Department of Immigration and Citizenship; and

(c) satisfy any further criteria specified in the Eligibility Conditions in the Policy Schedule.

Commencement of cover

A Policy will commence with us on the Commencement Date and will continue until it ceases in accordance with the terms and conditions of the Policy. No cover is provided before the Commencement Date or after the date the Policy ceases.

If the Previous Policy terms do not apply, then persons must be in Active Employment on the Commencement Date and remain in Active Employment for 30 consecutive

working days. Otherwise, New Events Cover will apply until the person is in Active Employment for 30 consecutive days.

Automatic acceptance

A person who meets the Eligibility Conditions and is aged less than the Maximum Entry Age, is eligible for cover from the day the person meets the Eligibility Conditions following the Commencement Date.

The Eligibility Conditions for each Policy will be determined during the quotation process and will be detailed in the Policy Schedule.

Automatic acceptance is the acceptance of an eligible person for cover up to a pre-determined level of cover, as described in the formula for Insured Cover, without the need for underwriting.

Where a Policy has an Automatic Acceptance Limit, a person who meets the Eligibility Conditions will receive cover up to the lesser of their Insured Cover and the Automatic Acceptance Limit without the need for underwriting. Varying values of the Automatic Acceptance Limit are provided based on the group’s size, occupation mix and level of cover required.

Where a person is not in Active Employment on the date they first meet the Eligibility Conditions, they will only be provided with New Events Cover, which means they will not have cover for pre-existing conditions. New Events Cover will apply until the person returns to Active Employment for 30 continuous days.

GENERAL CONDITIONS

Where a person’s Insured Cover exceeds the Automatic Acceptance Limit or a person elects voluntary cover or is not eligible for cover by way of automatic acceptance, underwriting will be required.

We will provide an Automatic Acceptance Limit where each of the following are satisfied at all times:

(a) at least 75% of the people who meet the Eligibility Conditions are Covered Persons;

(b) there are clearly defined categories of membership which ensure that people cannot directly or indirectly choose their level of cover without our written consent; and

(c) there is a clearly defined objective formula for determining the amount of cover for all people.

In addition, where the Policy Owner is the trustee of a regulated superannuation fund, that fund must also be the ‘Default Fund’ for superannuation contributions of the Employer, as defined in the Superannuation Guarantee (Administration) Act 1992 (Cth).

Takeover terms

Existing death (including, where applicable, Terminal Illness) cover insured under the Previous Policy on the day prior to the Commencement Date will continue under the Policy for Covered Persons from the Commencement Date.

Total and Permanent Disablement cover and income protection cover will commence under the Policy from the Commencement Date for a person who was insured under a Previous Policy on the day before the Commencement Date if:

(a) the person was At Work; or

(b) the person was on a Leave of Absence other than for Illness or Injury and on the last working day before they commenced the leave they were At Work.

Such cover will not extend to an event which gives rise to a claim whilst the Covered Person was on approved leave if the event occurred between the last working day and the Commencement Date of the Policy.

A person who was insured under the Previous Policy on the day before the Commencement Date who does not meet the requirements above will have Total and Permanent Disablement, Terminal Illness and income protection cover under the terms of the Policy from the Commencement Date but only for a claim arising from an Illness or Injury which is unrelated to the reason they were not At Work.

This limitation on claims arising from an Illness or Injury related to the reason they were not At Work will no longer apply to the Covered Person’s Total and Permanent Disablement, Terminal Illness and income protection cover when the person returns to being At Work.

Any takeover of cover is limited to the Maximum Benefit/Maximum Monthly Benefit.

Where a person has previously been underwritten and exclusions or loadings apply, these may continue under the new Policy.

Takeover terms do not apply for new group insurance policies where there is no previous group insurance arrangement.

12 Group Insurance Product Disclosure Statement Steadfast 13

Exclusions

No Benefit will be paid for a Covered Person if their Illness or Injury is directly or indirectly caused by:

(a) War (for death, Terminal Illness and Total and Permanent Disablement cover, this exclusion only applies to War outside of Australia); or

(b) any other exclusion imposed by us on a Covered Person.

We will not pay a Benefit where the payment of such Benefit would expose us, the Policy Owner, or the Covered Person to any sanction, prohibition or restriction under United Nations resolutions or the trade or economic sanctions, laws or regulations of the European Union, Australia or United States of America.

We will not pay a Terminal Illness Benefit where a terminal illness or similar benefit has been paid, is payable or can be claimed in respect of the Covered Person under a Previous Policy.

In addition, the following exclusions also apply to income protection Benefits:

No Benefit will be paid for a Covered Person if their Illness or Injury is directly or indirectly caused by:

(a) intentional self-inflicted Injury or any attempt to commit suicide; or

(b) normal and uncomplicated pregnancy, caesarean birth, threatened miscarriage, participation in in-vitro fertilisation or other medically assisted fertilisation techniques and normal discomforts of pregnancy, including but not limited to morning sickness, back ache, varicose veins, ankle swelling and bladder problems.

We will not pay a Benefit if the payment of the Benefit would contravene any provision of the Private Health Insurance Act 2007 (Cth), Health Insurance Act 1973 (Cth) or the National Health Act 1953 (Cth) or any other regulated Australian legislation as amended or replaced or any preceding health insurance legislation.

Interim accident cover

Interim Accident Cover is provided from the date we receive a fully completed application for cover, while a person is being underwritten until the earliest of the following:

(a) we have accepted (on any terms) or rejected the person for the cover applied for (including closing the application due to non-receipt of our requested requirements);

(b) the person has withdrawn the request for cover;

(c) 90 days have passed from the date we receive the fully completed application for this cover; and

(d) cover otherwise ceases under the Policy for the person.

Interim Accident Cover is provided for the type of cover being applied for as long as this cover is available under the Policy. An Interim Accident Benefit is payable where the person suffers an Injury that results in death, Total and Permanent Disablement and/or Disablement or Partial Disablement (whichever is applicable to the cover being applied for).

An Interim Accident Benefit under a group life insurance Policy is only payable if the death or Total and Permanent Disablement occurs within 365 days of the Injury occurring.

An Interim Accident Benefit under an income protection insurance Policy is only payable if the Disablement or Partial

Disablement occurs immediately following the Injury. The Injury and the Disability/Partial Disability must have occurred while Interim Accident Cover applies in respect of the person. A Superannuation Contribution Benefit may also be payable if this option is selected under the Policy.

The Interim Accident Benefit will be the lesser of the amount of cover being applied for and the following maximum cover amounts (this includes any existing cover already in place with us).

COVER TYPE MAXIMUM BENEFIT

Death $2,000,000

Total and Permanent Disablement

$2,000,000

Income Protection $20,000 per month

Payment of any Benefit is subject to all other terms and conditions within the Policy.

Extended cover

We will continue to provide cover for a person whose cover has ceased due to the person ceasing Employment with the Employer, provided that the event which gives rise to a claim occurs no later than 60 consecutive days from the date the cover ceased for that person.

This extension of cover will cease on the earlier of the following:

(a) 60 consecutive days has passed since cover ceased for that person due to ceasing Employment with the Employer;

OTHER FEATURES

14 Group Insurance Product Disclosure Statement Steadfast 15

(b) the date that an application for a continuation option has been accepted or declined by us (where the continuation option feature has been selected under the Policy);

(c) the date the person obtains insurance for the same or similar Benefit provided under the Policy with any other insurer as determined by us; or

(d) the date the cover would otherwise cease under the Policy.

Life events cover

A Covered Person may increase their death or death and Total and Permanent Disablement cover without underwriting upon the occurrence of certain life events. Cover can be increased when a Covered Person:

(a) marries;

(b) adopts or has a child;

(c) takes out a mortgage on a newly purchased property in which he or she intends to reside; or

(d) divorces.

The Covered Person must apply for the additional cover and provide evidence, to our satisfaction, that any of the above events have taken place, within 60 days of the event occurring.

Where a Covered Person is not in Active Employment on the day we receive the application to increase cover, New Events Cover will apply to the amount of the increase in cover until the Covered Person returns to Active Employment for 30 consecutive days.

Any increase in cover is limited to the lesser of:

(a) 25% of the Covered Person’s current cover received under automatic acceptance;

(b) 25% of the amount of the mortgage (where applicable); or

(c) $200,000.

Where the Policy has a units based calculation for Insured Cover, then the amount which can be applied for is 1 extra unit of cover.

A Covered Person can only increase their cover under life events cover once during the lifetime of their cover with us.

Leave of absence

We will continue to provide cover where a Covered Person takes a Leave of Absence for up to 24 months where all of the following are satisfied:

(a) the Employer approves the Leave of Absence in writing before the Covered Person goes on leave; and

(b) premiums for the Leave of Absence period continue to be paid for the Covered Person.

Cover will cease for a Covered Person who is on a Leave of Absence at the earliest of when the Covered Person’s:

(a) Leave of absence commences, if a Covered Person has not satisfied the criteria set out above;

(b) Leave of Absence ceases and he or she does not return to their Employment;

(c) Leave of Absence exceeds 24 months, (unless we have agreed to an extension in writing); or

(d) cover otherwise ceases under the Policy.

If a Covered Person suffers an Illness or sustains an Injury while on a Leave of Absence (or paid maternity or paternity leave) income protection Benefits will not be paid until the later of the end of the Waiting

Period or the end of the Leave of Absence for the relevant Covered Person.

Overseas residence and travel

Cover is generally provided worldwide, 24 hours a day, seven days a week, whilst the Policy remains in force with us.

We will continue to provide cover to Australian Residents who are temporarily Employed overseas by their Employer as long as premiums continue to be paid.

Where a Covered Person is not an Australian Resident and is temporarily Employed overseas, we will continue to provide cover whilst overseas for a maximum period of 90 days from the date they leave Australia as long as premiums continue to be paid.

Should a Covered Person submit a claim for any type of Benefit other than a death Benefit, we may require the Covered Person to return to Australia (at their own expense) for medical assessment. Where we require the Covered Person to return to Australia for assessment of a claim and the Covered Person does not return to Australia within 6 months of our request, the claim will be closed and will not be re-opened until the Covered Person returns to Australia and has requested a re-assessment in writing.

We will only pay an income protection Benefit for a maximum period of 12 months from the end of the Waiting Period while the Covered Person is overseas. Income protection Benefit payments may resume if the Covered Person returns to Australia and requests a re-assessment in writing and is still Disabled or Partially Disabled.

Continuous review

Where the Policy Schedule shows that continuous review applies to the Policy, a Covered Person’s amount of cover will increase or decrease automatically in line with the calculation of Insured Cover. For example, if the formula for Insured Cover under a Policy was dependent on income (i.e. 2 x income), cover for that group would automatically increase or decrease in line with their income. Any increase or decrease in cover will be effective from the date of the change that affected the cover amount. Premiums will also be adjusted to take into account the variation in cover.

Continuous review will only apply to the extent that it does not, during each period between Annual Review Dates, result in a Covered Person’s cover increasing in total by the greater of 25% or $75,000 (or $1,000 per month for income protection) of the cover which applied on the later of the date cover commenced for the Covered Person and the most recent Annual Review Date, unless otherwise agreed to in writing by us.

If the Policy Schedule does not indicate that continuous review applies to the Policy, the amount of cover will be the lesser of the Covered Person’s Insured Cover and their Insured Cover at the last Annual Review Date.

16 Group Insurance Product Disclosure Statement Steadfast 17

Cover beyond age 65

Where the Policy Owner has selected a Maximum Insurable Age greater than age 65, a Covered Person with a benefit period of 2 years or 5 years will be eligible for cover up to age 70 if all of the following are satisfied:

(a) a Covered Person is less than age 60 at commencement of Employment with the Employer and cover under the Policy;

(b) a Covered Person is in Permanent Employment and Active Employment on their 65th birthday; and

(c) a Covered Person has not previously claimed under the Policy or any other life insurance policy.

If a Covered Person’s Disability commences on or after the Covered Person’s 65th birthday, any Disability Benefits or Partial Disability Benefits will be paid until the earliest of:

(a) 2 years; or

(b) the Maximum Insurable Age.

This will not apply if any Disability or Partial Disability Benefit commenced prior to the Covered Person’s 65th birthday.

The Maximum Monthly Benefit payable is limited to the lesser of:

(a) 75% of the Covered Person’s Monthly Income (plus Superannuation Contribution Benefit if applicable); or

(b) $10,000 monthly Benefit.

This will not apply if any Disability or Partial Disability Benefit commenced prior to the Covered Person’s 65th birthday.

To age 65 benefit period - top up

Where this option is selected as stated in the Policy Schedule, a 2 year benefit period extension of cover will apply to a Covered

Person in combination with a benefit period to age 65. A Covered Person will be eligible for the extension if all of the following are satisfied:

(a) a Covered Person is less than age 60 at commencement of Employment with the Employer and cover under the Policy;

(b) a Covered Person is in Permanent Employment and Active Employment on their 65th birthday; and

(c) a Covered Person has not previously claimed under the Policy or any other life insurance policy.

If a Covered Person’s Disability commences on or after the Covered Person’s 63rd birthday, any Disability or Partial Disability Benefits will be paid until the earliest of:

(a) 2 years; or

(b) the Maximum Insurable Age.

The Maximum Monthly Benefit payable is limited to the lesser of:

(a) 75% of the Covered Person’s Monthly Income (plus Superannuation Contribution Monthly Benefit if applicable); or

(b) $10,000 monthly Benefit.

Any Disability or Partial Disability Benefit commencing prior to the Covered Person’s 63rd birthday, benefits payable will cease at age 65.

Increasing benefits option

Where this option is selected as stated in the Policy Schedule, we will increase the amount of the Disability Benefit or Partial Disability Benefit payable in respect of a Covered Person when the Covered Person has been paid a Benefit for a continuous period of 12 months by the lesser of:

OPTIONAL BENEFITS

(a) the percentage increase in CPI for that period; or

(b) 5%.

The above shall apply for every 12 month period the Covered Person remains on claim.

Accidental death benefit

Where this option is selected as stated in the Policy Schedule, we will pay an accidental death Benefit where a Covered Person dies as a result of an accident. The accidental death Benefit will be payable regardless of whether the Covered Person was in receipt of a Disability or Partial Disability Benefit. The amount payable is 3 times the Disability Monthly Benefit to a maximum of $10,000. We will pay this Benefit in addition to any other Benefits payable to the Covered Person including a death Benefit.

Continuation option

Where this option is selected as stated in the Policy Schedule, we will provide a Covered Person whose cover is going to cease the opportunity to continue their group life or income protection cover with us if all of the following circumstances are satisfied:

(a) the Policy the person was covered under is still in force;

(b) the person is under age 60;

(c) the person is an Australian Resident;

(d) the person is no longer an employee of the Employer;

(e) the person is not leaving Employment due to Injury or Illness;

(f) the person is no longer a member of the fund (superannuation policies only);

(g) at the time his or her cover ended under the Policy, the person was in Permanent Employment;

(h) the person does not join any military forces, (other than the Australian Armed Forces Reserve and is not on active duty outside Australia);

(i) no Benefit is, or is about to be, payable for the person under the Policy issued by us and no circumstances exist which, if the subject of a claim under the Policy and any other policy issued by us, would result in a Benefit being payable for the person under the Policy or any other policy issued by us in respect of the person;

(j) the premium payable in respect of the person’s cover under the Policy is not overdue at the time his or her cover ends;

(k) our minimum policy issue requirements are met;

(l) our occupation and pastimes underwriting requirements are met; and

(m) within 60 days of cover ending in respect of the Covered Person under the Policy, we receive the application and the correct premium for the cover being applied for.

Cover under any continuation option will not exceed the amount that applied to the person on the day their cover ceased under the Policy. For income protection continuation policies, the same Waiting Period and Maximum Benefit Period that applied for the Covered Person under the Policy will continue. Any exclusions or loadings that were recorded against the cover but not applied whilst cover was provided under the Policy will be applied to the continuation option policy.

The premium rates and terms of the continuation option policy will be those available under the continuation option policy at the time the continuation is issued. Premium rates and terms may change for the continuation option policy after it is in force.

18 Group Insurance Product Disclosure Statement Steadfast 19

Terms and conditions of benefits

The following table shows the terms and conditions for Benefits that may be available under a Policy with us.

GROUP LIFE

Death Benefit Payment of the death Benefit upon a Covered Person’s death.

Terminal Illness Benefit Payment of the Terminal Illness Benefit when a Covered Person is certified by us as having a Terminal Illness.

Total and Permanent Disablement Benefit

Payment of the Total and Permanent Disablement Benefit where a Covered Person is determined by us to be suffering from Total and Permanent Disablement.

Interim Accident Benefit Payment of the Interim Accident Benefit where a Covered Person dies or suffers Total and Permanent Disablement whilst being underwritten.

Refer to ’Interim accident cover’ on page 13.

GROUP INCOME PROTECTION

Disability Benefit Payment of the Disability Benefit where a Covered Person is Disabled at the end of the Waiting Period. The amount of the Disability Benefit is the Disability Monthly Benefit which is the lesser of:

(a) the Insured Percentage multiplied by Monthly Pre-Disability Income;

(b) the Covered Person’s Insured Cover*; and

(c) the Maximum Monthly Benefit.

The Disability Benefit is paid monthly in arrears.

The Disability Benefit may be offset or reduced in certain circumstances. Refer to ‘Income protection benefit offsets’ on page 23.

PRODUCT DETAIL

GROUP INCOME PROTECTION

Partial Disability Benefit Payment of the Partial Disability Benefit where a Covered Person becomes Partially Disabled during the Waiting Period. The amount of the Partial Disability Benefit is the Partial Disability Monthly Benefit which is calculated in accordance with the following formula:

(A – B) x C

A

Where:

A is the Monthly Pre-Disability Income;

B is the Disability Income; and

C is the Disability Monthly Benefit.

The Partial Disability Benefit is paid monthly in arrears.

The Partial Disability Benefit may be offset or reduced in certain circumstances. Refer to ‘Income protection benefit offsets’ on page 23.

Superannuation Contribution Benefit

Payment of the Superannuation Contribution Benefit where a Covered Person is eligible for a Disability Benefit or Partial Disability Benefit and where this option is selected. The amount of the Superannuation Contribution Benefit is the lesser of:

(a) the Superannuation Contribution Insured Percentage multiplied by Monthly Income; and

(b) the actual average monthly compulsory employer superannuation entitlement the Covered Person benefited from in the 12 month period prior to Disability.

The Superannuation Contribution Benefit will be reduced by any superannuation guarantee contributions made on the Covered Person’s behalf.

The Superannuation Contribution Benefit will not be paid or will be reduced, when the total Disability Monthly Benefit exceeds the Maximum Monthly Benefit.

* Not applicable where the continuous review option has been selected.

20 Group Insurance Product Disclosure Statement Steadfast 21

GROUP INCOME PROTECTION

Retraining Expense Benefit Payment of the Retraining Expense Benefit where a Covered Person incurs Retraining Expenses. The amount of the Retraining Expense Benefit is the equal amount of the Retraining Expenses incurred in respect of a Covered Person. The Retraining Expense Benefit is only payable if:

(a) the Covered Person is Disabled or Partially Disabled;

(b) we approve the Retraining Expenses in writing before they are incurred; and

(c) the Retraining Expenses are incurred to:

(i) directly assist the Covered Person to return to work in his or her Occupation or any gainful occupation; or

(ii) undertake a vocational retraining program.

The Retraining Expense Benefit is paid directly to the provider of the applicable service relating to the Retraining Expenses or as we may approve on a case-by-case basis.

Recurrent Disability Benefit Payment of the recurrent Disability Benefit where a Covered Person has returned to employment with the Employer and becomes Disabled or Partially Disabled for the same or related Illness or Injury during the 6 months from the last date the Covered Person was entitled to receive a Benefit. The payment of the recurrent Disability Benefit will be treated as a continuation of the previous claim. However, the payment of Benefits shall not exceed the Maximum Benefit Period. If a Covered Person returns to employment with their Employer and becomes Disabled or Partially Disabled for the same or related Illness or Injury more than 6 months after the date the Covered Person was entitled to receive a Benefit, then the following will apply:

(a) the Covered Person must satisfy a new Waiting Period;

(b) the recurring Disability will be a continuation of the previous claim; and

(c) the successive periods of Disability or Partial Disability will be regarded as continuous for the purpose of determining the remaining portion of the Maximum Benefit Period.

GROUP INCOME PROTECTION

Death Benefit Payment of the death Benefit where a Covered Person who was entitled to receive a Disability Benefit or Partial Disability Benefit dies. For a Covered Person aged 65 or older, the amount of the death benefit is equal to the lesser of:

(a) the sum of 3 times the Disability Monthly Benefit and the Superannuation Contribution Monthly Benefit (if applicable); and

(b) $30,000.

For a Covered Person who is less than 65 years of age, the amount of the death Benefit is the sum of 3 times the Disability Monthly Benefit and the Superannuation Contribution Monthly Benefit (if applicable).

The death Benefit is not payable if the date of death is within 3 months of a crisis Benefit being payable to a Covered Person.

Interim Accident Benefit Payment of the Interim Accident Benefit where a Covered Person suffers an accidental Injury which results in the person being Disabled or Partially Disabled whilst being underwritten.

Refer to ‘Interim accident cover’ on page 13.

The Interim Accident Benefit may be offset or reduced in certain circumstances. Refer to ‘Income protection benefit offsets’ on page 23.

Crisis Benefit* Payment of the crisis Benefit where a Covered Person suffers one of the Crisis Benefit Medical Conditions. The amount of the crisis Benefit is paid as a lump sum and is equal to 3 times the Disability Monthly Benefit and the Superannuation Contribution Monthly Benefit (if applicable).

Refer to the definition of Crisis Benefit Medical Conditions in the ‘Definitions’ for a list of covered medical conditions.

Specific Injury Benefit* Payment of the specific injury Benefit where a Covered Person suffers a Specific Injury Event. The specific injury Benefit is paid even if the Covered Person is working. The amount of the specific injury Benefit is equal to the sum of the Disability Benefit and Superannuation Contribution Monthly Benefit (if applicable) and can only be paid up to the applicable payment period.

Refer to the definition of Specific Injury Event in ‘Definitions’ for the types of injuries covered and applicable payment periods.

22 Group Insurance Product Disclosure Statement Steadfast 23

GROUP INCOME PROTECTION

Nursing Care Benefit* Payment of the nursing care Benefit where a Covered Person is Confined to Bed for 3 or more consecutive days during the Waiting Period. The daily amount of the nursing care Benefit is equal to the lesser of:

(a) 1/30th of the Disability Benefit and the Superannuation Contribution Monthly Benefit (if applicable); and

(b) $150.00 per day.

The nursing care Benefit will not be paid for more than 30 days.

Family Care Benefit* Payment of the Family Care Benefit where a Covered Person is Disabled and is receiving Family Care for at least 3 consecutive days. The monthly amount of the Family Care Benefit is equal to the lesser of:

(a) $2,000;

(b) 50% of the Disability Benefit and the Superannuation Contribution Monthly Benefit (if applicable); and

(c) the amount we consider is the monthly income lost by the Direct Family Member directly resulting from the Direct Family Member’s provision of Family Care.

The Family Care Benefit may be paid for a maximum period of up to 6 months.

Accommodation Benefit* Payment of the accommodation Benefit where a Direct Family Member has chosen to stay at a place near where the Covered Person is Confined to Bed (other than the Covered Person’s home of residence). The amount of the accommodation Benefit is the lesser of:

(a) the actual accommodation costs; and

(b) $250.00 per night.

The accommodation Benefit is payable once for up to 30 days in any 12 month period.

Income protection benefit offsets

We will reduce any Disability Benefit, Partial Disability Benefit or Interim Accident Benefit payable for a Covered Person by the amount of any income and the commutation of income paid or payable in respect of a Covered Person as a result of Disability or Partial Disability including any amounts payable:

(a) through workers compensation or any similar legislation or any settlement under common law;

(b) sick leave (paid only);

(c) in respect of loss of income (whether legislated or otherwise);

(d) under any statutory accident compensation scheme; or

(e) any disability, injury or illness policy (other than lump sum total and permanent disablement).

In addition, a Benefit may be reduced by the amount of any income we believe the Covered Person could reasonably be expected to earn in his or her Occupation whilst Disabled or Partially Disabled.

Any income received in the form of a lump sum or exchanged for a lump sum has a monthly income equivalent of 1/60th of the lump sum (i.e. the lump sum is amortised over a period of 60 months).

The Superannuation Contribution Monthly Benefit will be reduced by:

(a) the amount of any employer superannuation contributions paid to a Covered Person’s superannuation account; and

(b) the amount of any benefits payable under any other income protection policy but only to the extent that the benefit payable under any other income protection policy is designed to replace in whole or in part

the compulsory employer superannuation entitlements the Covered Person would have benefited from had he or she not been Disabled.

Total and Permanent Disablement benefit tapering and definitions

Where the Total and Permanent Disablement Benefit is provided and where a sum insured scale exists, the Total and Permanent Disablement cover will reduce each year from the Covered Person’s 61st birthday. The amount of the Total and Permanent Disablement Benefit is dependent on the Maximum Insurable Age in the Policy Schedule. The following table displays the percentage the Total and Permanent Disablement cover will change by each birthday.

TAPERING PERCENTAGE (OF DEATH INSURED COVER)

AGE LAST BIRTHDAY

COVER CESSATION AGE - 65

COVER CESSATION AGE - 70

Up to 60 100% 100%61 80% 90%62 60% 80%63 40% 70%64 20% 60%65 0% 50%66 N/A 40%67 N/A 30%68 N/A 20%69 N/A 10%70 N/A 0%

We may support a non-tapering Total and Permanent Disablement option at an additional cost and where this is selected, this will be detailed in the Policy Schedule.

* These optional benefits are not available to a trustee of a regulated superannuation fund.

24 Group Insurance Product Disclosure Statement Steadfast 25

We offer the following options in relation to Total and Permanent Disablement definitions:

(a) working definition to age 65 and activities of daily living definition for age 65 to 70; and

(b) full working definition to age 70.

Opt-out or reduction in cover

A Covered Person may opt-out or reduce any cover provided to them at any time by submitting the request in writing to the Policy Owner. Where the request is received by the Policy Owner within 60 days of cover commencing then any premium payments for that person will be refunded to the Policy Owner and cover will be deemed not to have ever commenced under the Policy for that person. No claims will be considered against the cover that the person had opted-out from.

Where the request is received more than 60 days after cover commenced then the opt-out or reduction will only be effective from the last day that the current premium payment has been made to and there will be no refund of premiums to the Policy Owner unless otherwise agreed by us. No claims will be considered against the cover that the person had opted-out from on or after the date that the premiums for the cover had been paid to.

Any future cover for the person must be fully underwritten by us and no cover will be provided under automatic acceptance.

Reinstatement of cover

Where cover for a Covered Person ceases due to one of the following reasons, reinstatement of cover will be at our discretion and determined on a case-by-case basis:

(a) the Covered Person commences duty with the military services (other than the Australian Armed Forces Reserve and is not on active duty outside of Australia) of any country;

(b) premium remains unpaid for a period of 30 days or more after the Due Date; or

(c) an administration error.

Cessation of group income protection payments

We will cease to pay a Disability Benefit, Partial Disability Benefit or Superannuation Contribution Monthly Benefit in respect of a Covered Person at the time the Covered Person:

(a) is no longer Disabled or Partially Disabled;

(b) dies;

(c) attains the Maximum Insurable Age;

(d) has been Disabled or Partially Disabled from the end of the Waiting Period for the Maximum Benefit Period for the same or related Illness or Injury; or

(e) is no longer an Australian Resident, no longer permanently in Australia or not eligible to work in Australia.

Claims

We must be notified in writing as soon as is reasonably practicable after an event entitling a Covered Person to a Benefit.

It is a condition of payment of any Benefit that the Covered Person provides us with such evidence to substantiate the claim as we may reasonably require.

A Covered Person must submit at our expense to any medical examinations we reasonably consider required. Any medical examinations will be conducted by a Medical Practitioner or other health professional appointed by us as we deem necessary.

Satisfactory proof of age may be required prior to any payment of Benefits.

Payment of benefits

Any Benefit will be paid to the Policy Owner or a person nominated by the Policy Owner in the manner set out in the Policy Schedule. The Policy Owner may hold the monies in trust for the Covered Person in accordance with any Trust Deed. Where we determine that a Covered Person is eligible for the payment of a Benefit, the amount payable will be the Covered Person’s Insured Cover at their Incident Date.

Income protection Benefits will be paid monthly in arrears. Benefits payable for a period of less than 30 days will be paid at a daily rate of 1/30th of the Benefit payable.

All payments will be made in Australian currency.

26 Group Insurance Product Disclosure Statement Steadfast 27

Cessation of cover - group life insurance

A Covered Person will cease to be covered under a Policy effective from the earliest date of any of the following:

(a) the Covered Person ceases to be Employed by the Employer (unless extended cover applies);

(b) the Covered Person ceases to be a member of the employer sponsored division of the fund;

(c) when a Benefit has been paid to the Policy Owner in respect of that Covered Person;

(d) the Covered Person commences duty with the military services (other than the Australian Armed Forces Reserve and is not on active duty outside Australia) of any country;

(e) the Covered Person attains the Maximum Insurable Age for the relevant Benefit;

(f) the Policy is cancelled or terminated for any reason;

(g) we receive a written request from the Policy Owner to cancel or terminate the Covered Person’s cover and we agree to terminate or cancel the cover for this Covered Person;

(h) premium remains unpaid (by an individual or Policy Owner) for a period of 30 days or more after the Due Date;

(i) the date the Covered Person no longer meets the conditions for continued cover whilst overseas;

(j) the date the Covered Person no longer meets the conditions for continued cover whilst on a Leave of Absence;

(k) we accept or decline the Covered Person’s continuation option application (where applicable);

(l) if the Covered Person is Employed on a Casual Basis and 60 consecutive days have passed since the Covered Person was last At Work, actively performing all the duties of his or her Occupation with the Employer;

(m) the date the Covered Person is no longer an Australian Resident, is no longer permanently in Australia or is not eligible to work in Australia; or

(n) for a holder of a temporary work visa subclass 457 issued by the Australian Department of Immigration and Citizenship – the date the visa expires.

Cessation of cover - group income protection insurance

A Covered Person will cease to be covered under a Policy effective from the earliest date of any of the following:

(a) the Covered Person ceases to be Employed by the Employer (unless extended cover applies);

(b) the Covered Person ceases to be a member of the employer sponsored division of the fund;

(c) the Covered Person dies;

(d) the Covered Person commences duty with the military services (other than the Australian Armed Forces Reserve and is not on active duty outside Australia) of any country;

(e) the person attains age 65 subject to cover continuing under the ‘Cover beyond age 65’ or the ‘To age 65 benefit period - top up’ features;

TERMINATION AND CANCELLATION

(f) the Covered Person attains the Maximum Insurable Age;

(g) the Policy is cancelled or terminated for any reason;

(h) we receive a written request from the Policy Owner to cancel or terminate the Covered Person’s cover and we agree to terminate or cancel the cover for this Covered Person;

(i) premium remains unpaid (by an individual or Policy Owner) for a period of 30 days or more after the Due Date;

(j) the date the Covered Person no longer meets the conditions for continued cover whilst overseas;

(k) the date the Covered Person no longer meets the conditions for continued cover whilst on a Leave of Absence;

(l) we accept or decline the Covered Person’s continuation option application (where applicable);

(m) if the Covered Person is Employed on a Casual Basis and 60 consecutive days have passed since the Covered Person was last At Work, actively performing all the duties of his or her Occupation with the Employer;

(n) the date the Covered Person is no longer an Australian Resident, is no longer permanently in Australia or not eligible to work in Australia; or

(o) for a holder of a temporary work visa subclass 457 issued by the Australian Department of Immigration and Citizenship – the date the visa expires.

Termination and cancellationThe Policy Owner may terminate a Policy at any time by giving prior written notice and we will refund any premium paid for the unexpired period of risk.

We may cancel the cover provided under a Policy at any time when any premium (or any instalment of premium) has not been paid within 30 days of the Due Date.

Cover after a policy terminatesDeath and Terminal Illness cover will cease the day a Policy terminates. If a Covered Person is not At Work on the day a Policy terminates, then we will continue their Total and Permanent Disablement and income protection cover subject to the following:

(a) the Covered Person is covered only for the reason they were not At Work on the last working day before the termination of the Policy.

Total and Permanent Disablement and income protection cover continued in this manner will cease on the earliest of the following:

(a) the Covered Person returns to work after the termination of the Policy and is actively performing all the duties of their Occupation and working their usual hours free from any limitation due to Illness or Injury and is not entitled to or is not receiving income support benefits of any kind;

(b) the Covered Person attains age 65 subject to cover continuing under the ‘Cover beyond age 65’ or the ‘To age 65 benefit period - top up’ features;

(c) the Covered Person attains the Maximum Insurable Age;

(d) the person no longer meets the requirements to be a Covered Person under the Policy; or

(e) we make a decision on any claim for the Covered Person.

28 Group Insurance Product Disclosure Statement Steadfast 29

Underwriting

We may request additional information required to assess the person’s eligibility for cover and the terms of any cover accepted.

Underwriting is the process of assessing a person’s insurability by obtaining information about their medical history, occupation, pastimes, family history and other information we may require.

Underwriting is required for cover above the Automatic Acceptance Limit, where a person is not eligible for automatic acceptance and where there is any voluntary cover available under a Policy.

When we underwrite a person for cover, we may decide to:

(a) accept on standard terms;

(b) accept with an exclusion (eg. of a specific condition);

(c) accept with a loading (eg. +50% of the standard premium);

(d) accept with a combination of an exclusion and a loading; or

(e) decline cover.

For formula based cover and where the Policy covers 50 or more Covered Persons, any loading will be recorded but not applied by us unless a Covered Person effects a continuation option.

Forward underwriting limits

We also offer Forward Underwriting Limits for cover above the Automatic Acceptance Limit. A Forward

Underwriting Limit allows a Covered Person’s cover to increase in line with the formula for Insured Cover under the Policy up to a pre-accepted amount as advised by us in writing without the need for underwriting. The amount of a Covered Person’s Forward Underwriting Limit will be as advised by us. A Forward Underwriting Limit will only be available where the Policy has a formula for the calculation of Insured Cover.

Claims

The Policy Owner must notify us in writing as soon as is reasonably practicable of an event entitling the Policy Owner to a Benefit. Covered Persons must provide us with evidence to substantiate the claim as we may reasonably require. Covered Persons must submit at our expense to any medical or other examinations as we deem necessary. We will pay the fees and costs for such examinations or tests that a Covered Person undergoes at our request. We will not pay any costs in relation to the attendance of such an examination or test such as fees incurred for travel or non-attendance fees.

Satisfactory proof of identity and age may be required prior to the payment of any Benefit.

Premium and frequency loadings

Where we receive premiums in any instalments other than annual, a 3% loading will be applied to the premium rates quoted.

We reserve the right to alter this percentage at any time once the Premium Guarantee Period has expired.

ADDITIONAL INFORMATION

Waiver of premium

Whilst a Covered Person is receiving any income protection Benefit payment from us and a premium falls due during that period, we will not require the premium to be paid at that time. Once the income protection Benefit payment ceases, a premium for that Covered Person will be payable from that time onwards.

Variation of terms

We generally provide a 3 year Premium Guarantee Period. The Premium Guarantee Period is noted in the Policy Schedule. We may however change the premium or Automatic Acceptance Limit where:

(a) the number of Covered Persons covered under the Policy changes by more than 25% from the number of Covered Persons at the commencement of the latest Premium Guarantee Period;

(b) it becomes impractical or impossible to carry out our obligations;

(c) our Policy is inconsistent with the law;

(d) Government Charges relating to the Policy are imposed or changed; or

(e) at any time after the end of the Premium Guarantee Period upon us giving 60 days written notice to the Policy Owner.

For (a), (b), (c) and (d) any change in premium will be effective immediately.

We also reserve the right to vary premiums under the Policy in respect of any or all

Covered Persons upon written notification to the Policy Owner with immediate effect in the event of any invasion or an outbreak of War which involves Australia. Should that right be exercised and the Policy Owner fails to pay any increase in premium we will not be liable to pay any Benefit with respect to a Covered Person when the event giving rise to the claim arose either directly or indirectly from War.

Tax and stamp duty

Taxation of premiums and Benefits may vary depending on the structure of the plan and whether the Policy Owner is the trustee of a superannuation fund or an employer arranging benefits directly for its employees. Goods and Services Tax (GST) currently does not apply to life insurance premiums. State Governments also impose stamp duties on some policies and where these apply we will include it in, or add it to, the premium.

This information is based on our current interpretation of the tax laws. Should changes in the law result in any new or additional taxes, duties or charges in relation to the Policy, these amounts may be added to the premium or charged to the Policy Owner.

We recommend that the Policy Owner should consult a professional tax adviser for advice regarding their individual circumstances.

Profit share

For larger policies with at least 1,000 Covered Persons we may offer a self experience profit share formula. Consideration of a rebate

30 Group Insurance Product Disclosure Statement Steadfast 31

will be based upon the experience of the Policy Owner’s individual group insurance arrangements. A premium loading may apply for participation in this arrangement. If self experience applies, it will be noted in the Policy Schedule.

Multinational pooling

Multinational pooling is a method global companies use to aggregate and manage the risk of their employee benefit plans throughout the world. Employee benefit programs of the same company in multiple geographical insurance markets are combined to form a multinational pool. MetLife is part of the MAXIS Global Benefits Network (MAXIS GBN). MAXIS GBN is a global joint venture partnership between AXA France Vie S.A., Paris, France (AXA) and MetLife that offers multinational companies a full range of flexible solutions to fulfil their employee benefit commitments and insurance needs. MAXIS GBN combines the global purchasing power of two world insurance leaders and has a network throughout more than 110 insurance markets. Generally, multinational pooling and captive arrangements provide improved benefits due to enhanced economies of scale.

We routinely work with clients in assisting in the formation and maintenance of a MAXIS GBN multinational pool or captive arrangement that best suits our customer’s requirements. If a multinational pooling or captive facility is provided, it will be stated in the Policy Schedule.

Captive arrangements

A captive is an insurance company set up by its owners, primarily to insure against its own specific risks. Organisations that have taken such a considered, strategic approach have reaped considerable rewards in reduced costs and improved coverage and governance. Many international businesses have found that an insurance subsidiary is the best means of creating and administering a global risk management program. MAXIS GBN is a leader in supporting global organisations in successfully managing their captive arrangements.

Statutory fund

The Policy is issued in the MetLife Insurance Limited Statutory Fund No. 1.

Our technology offering is setting the industry benchmark in Australia. Everything we do enhances our partner and member experience. To support our service offering, we developed the eToolKit. eToolKit is a customer focused technology solution designed to provide a wide range of online tools for our partners and their customers. The eToolKit is a set of sophisticated technology based solutions designed to help the Policy Owner or their representatives work smarter and faster, making insurance so much easier. These include:

• eApply

• eLodgement

• eQuery

Our eToolKit offers a secure online service, providing the Policy Owner or their representatives complete access to all the tools they need and an outstanding member experience. We continue to build a reputation of trust by ensuring the security of information. The eToolKit may be customised and tailored to the Policy Owner or their representatives specific business requirements and we will work with them to provide the eToolkit that meets their needs.

eApply

eApply is a dynamic online application, providing straight-through processing for insurance applications. We make doing business easier by tailoring the application to the Policy Owner or their representatives needs. The application process is supported by a rules underwriting engine and the integration of member information is designed around

the Policy Owner or their representatives needs from a number of options. Our preferred model provides:

• a dynamically built electronic application supporting all products;

• a customised and branded application, meeting the specific requirements of our partners;

• the ability to receive data direct from an administrator to pre-populate fields and feed a decision straight back;

• only relevant questions are asked using a reflexive question style;

• Underwriters are empowered to Tele-Underwrite - calling customers on their preferred number and time;

• a rules based underwriting engine delivering an immediate response;

• designed specifically for group insurance; and

• an outstanding customer experience.

eLodgement

eLodgement provides our partners with a smart and fast process of lodging claims, insurance applications and submission of additional information.

• Secure online service available 24 hours a day, seven days a week.

• Smart and simple process of lodging claims and underwriting applications.

• Removes e-mail, paper and fax submission.

• Direct submission to our workflow system which maximises efficiency.

TECHNOLOGY AND SERVICES

32 Group Insurance Product Disclosure Statement Steadfast 33

eQuery

eQuery provides instant information for the Policy Owner or their representatives to track the status of individual claims and insurance applications. eQuery also provides detailed reports that are updated daily.

• Secure and fast online service available 24 hours a day, seven days a week.

• Up-to-date information from our systems.

• Underwriting and claims status, pending requirements, follow-ups and decisions.

• Access to underwriting activity and forecast reports.

Claims and service model

We have a “direct to member” model for claims, see ‘Tele-Assessment’ below. Our belief is that by engaging with the member directly at the time of claim we can:

• provide the Covered Person with a personal service and greater understanding of the claims process;

• improve the information gathering process;

• drive down the claims cycle times for decision; and

• improve the overall member experience.

Importantly, even when we have direct contact with members, relevant administrators are able to obtain up to date information on all contact via eQuery ensuring they are always aware of a member’s situation.

Tele-Assessment

By using a Tele-Assessment claims service, we are able to keep cycle times and administration to a minimum whilst ensuring an exceptional member experience. By assessing claims directly over the phone with the member,

our assessors can make faster decisions and provide a more personal and efficient service for the member.

Claims

We ensure that our partners and members are at the heart of everything we do, every day. We understand that making a claim comes at one of the most traumatic times in the life of a member or their family. We aim to provide simplicity, clarity and support.

Our priorities are:

• assessment - to assess claims quickly, efficiently and fairly;

• guidance - to provide empathy and understanding and to make things as simple as possible by only asking details relevant to the claim;

• skills and expertise - our claims assessors and supporting medical experts are passionate about what they do and are highly trained in claims and customer service;

• ownership and empowerment - claims staff take ownership of their work and are empowered to guide members through every stage of their claim; and

• decisions - we aim to pay valid claims promptly.

Cooling off period

You have 14 days in which to notify us in writing that you want to return the product and have the premiums repaid to you. This is known as the cooling off period. The 14 days commences:

• 5 days after we receive your letter confirming that you have accepted our quote;

• the date you receive our letter confirming the issue of the Policy;

whichever is earlier.

However, you cannot return the product if you have exercised rights or powers under the product (for example, if you have made a claim). If you cancel the Policy within the cooling off period we will refund your premiums less:

• the reasonable administrative and transaction costs (including taxes and duties) we have incurred in setting up the Policy; and

• that proportion of the premium which relates to cover provided before we received your notice.

Your duty of disclosure

Before you enter into a contract of insurance with us, you have a duty, under the Insurance Contracts Act 1984, to disclose to us every matter that you know or could reasonably be expected to know is relevant to our decision whether to accept the risk of the insurance and if so, on what terms. You have the same duty to disclose those matters to us before you extend, vary or reinstate a contract of life insurance.

This duty, however, does not require disclosure of a matter:

• that diminishes the risk to be undertaken by us;

• that is common knowledge;

• that we know or, in the ordinary course of our business, ought to know; and

• as to which compliance is waived by the us.

Non-disclosure

If you fail to comply with your duty of disclosure, there may be consequences for the payment of a claim.

• If you fail to comply with your duty of disclosure and we would not have entered into the same contract of insurance if the failure had not occurred, we may avoid the contract within 3 years of entering into it.

• If your non-disclosure is fraudulent, we may avoid the contract at any time.

In exercising our rights we may have to treat different cover held by you as individual contracts of life insurance and elect whether to apply our rights to each contract separately.

Additional rights

If you fail to comply with your duty of disclosure and we have not avoided your contract, we may elect to:

• Reduce your sum insured

- For a contract of life insurance which does not provide death cover, we can elect to reduce your sum insured according to the formula prescribed by law at any time; or

OTHER IMPORTANT INFORMATION

34 Group Insurance Product Disclosure Statement Steadfast 35

- For a contract of life insurance which does provide death cover, we can elect to reduce your sum insured according to the formula prescribed by law within 3 years of entering into the contract with you.

• Vary your contract

- For a contract of life insurance which does not provide death cover, we can vary the contract in a way that places us in the same position we would have been if the non-disclosure or misrepresentation had not occurred.

We have all of the above rights if you make a misrepresentation to us.

Guaranteed renewable

Provided you continue to pay your premiums, the Policy will continue until you reach the Maximum Insurable Age, unless the Policy ends earlier (refer to ‘Termination and cancellation’).

Commissions

When you purchase a group insurance Policy from us, the premium is paid to us. When an Adviser is involved, they may request that a commission be applied to the premium for their services. This commission rate, between 0% and 30% of the annual premium plus GST, will be added on to the premiums due to us under the Policy and we will then pay the commission to the Adviser. It is the responsibility of the Adviser to advise you if there is any commission being applied under a Policy for their service.

Commission cannot be applied to a Policy where the Policy Owner is a trustee of a regulated superannuation fund.

Complaints resolution

It is our commitment that we will always attempt to satisfactorily answer any questions

and resolve any problems or complaints you may have regarding the Policy or our services. If you wish to make a complaint about this product or our services, please contact us on 1300 319 209, email [email protected] or write to:

Dispute Resolution Officer MetLife Insurance Limited Reply Paid 3319, Sydney NSW 2001

You may contact the Financial Ombudsman Service (FOS) if you are not satisfied with how we respond to your complaint. FOS is an independent body whose services are available to you at no cost. They can be contacted by calling 1300 780 808, email [email protected] or write to:

The General Manager Financial Ombudsman Service GPO Box 3, Melbourne VIC 3001

Privacy

We collect, use and retain personal information in accordance with the Australian Privacy Principles and the Privacy Act 1988 (Cth). We collect, use, process and store personal information and, in some cases, sensitive information about you, in order to comply with our legal obligations, to assess your application for insurance cover, to administer the insurance cover provided, to enhance customer service or products and to manage claims. If you do not agree to provide us with the information, we may not be able to process your application, administer your cover or assess your claims.

In dealing with us, you agree to us using and disclosing your personal information as set out in this section and in our Privacy Policy. For further information about how we handle your personal information, details of how you can access or correct the information we hold about you or make a complaint, you can access our Privacy Policy at www.metlife.com.au/privacy or contact us on 1300 319 209.

These definitions are a guide only and reflect our standard policy definitions at the time of publication. The terms and definitions that apply are contained in the Policy Document issued to the Policy Owner.

Active Employment means a person who is Employed by the Employer and in our opinion is capable of performing their identifiable duties without restriction by any Illness or Injury for at least 35 hours per week (whether or not they are actually working those hours).

Annual Review Date means the “Annual Review Date” stated in the Policy Schedule.

At Work means actively performing all the duties of their Occupation, working their usual hours free from any limitation due to Illness or Injury and not entitled to or receiving income support benefits of any kind.

Australian Resident means:

(a) a person who resides in Australia and is either an Australian citizen or the holder of a permanent visa as identified by the Australian Department of Immigration and Citizenship; or

(b) is a citizen of New Zealand and the holder of a Special Category Visa while residing in Australia indefinitely.

Automatic Acceptance Limit or AAL means the amount determined by us and notified to the Policy Owner from time to time as stated in the Policy Schedule for which we may accept a person for Insured Cover without underwriting.

Benefit for group life insurance cover means one or more of the following benefits as the

context of the Policy requires; death Benefit, Total and Permanent Disablement Benefit, Interim Accident Benefit or Terminal Illness Benefit.

Benefit for group income protection insurance means one or more of the following benefits as the context of the Policy requires; Disability Benefit, Partial Disability Benefit, Superannuation Contribution Monthly Benefit, Retraining Expense Benefit, recurrent Disability Benefit, Interim Accident Benefit, crisis Benefit, specific injury Benefit, nursing care Benefit, Family Care Benefit, accommodation Benefit, death Benefit or accidental death Benefit.

Casual Basis means employed by the Employer other than in Permanent Employment or on a Long Term Casual Basis.

Chronic Renal Failure means chronic irreversible failure of both kidneys requiring permanent dialysis or kidney transplant.

Commencement Date means the “Commencement Date” stated in the Policy Schedule.

Confined to Bed means a Covered Person is Disabled and a Medical Practitioner has certified that they require the continuous full time care of a Registered Nurse.

Consumer Price Index or CPI means the consumer price index (weighted average of 8 capital cities combined) as published by the Australian Bureau of Statistics or its successor. If the Index is not published the increase shall be calculated by reference to such other retail price index which in our opinion most closely replaces it.

DEFINITIONS

36 Group Insurance Product Disclosure Statement Steadfast 37

Coronary Artery Angioplasty Multiple Vessel means angioplasty of the coronary arteries performed to correct a narrowing or blockage to:

(a) 3 or more coronary arteries within the same surgical procedure; or

(b) the left anterior descending coronary artery together with any coronary artery within the same surgical procedure.

The treatment must be the most appropriate based on angiographic evidence.

Coronary Artery Bypass Surgery means medically necessary coronary artery bypass graft surgery performed to correct coronary artery disease but does not include laser therapy, angioplasty or any other intra-arterial procedure or other non-surgical technique.

Covered Person means a person who meets the Eligibility Conditions and is accepted by us for insurance cover in accordance with the provisions of the Policy.

Crisis Benefit Medical Condition means a condition listed below: