Embed Size (px)

Citation preview

Bambang YuwonoBambang Yuwono

Production sharing ContractProduction sharing ContractFinancial AspectsFinancial Aspects

IntroductionIntroductionBasic PrinciplesBasic PrinciplesExploration & Development ActivitiesExploration & Development ActivitiesProduction ActivitiesProduction ActivitiesSupporting ActivitiesSupporting ActivitiesLifting Lifting –– Sharing AnalysisSharing AnalysisAccounting Procedures Accounting Procedures Fiscal Terms Fiscal Terms Budgeting & Reporting Budgeting & Reporting Budget PreparationBudget Preparation

OutlineOutline

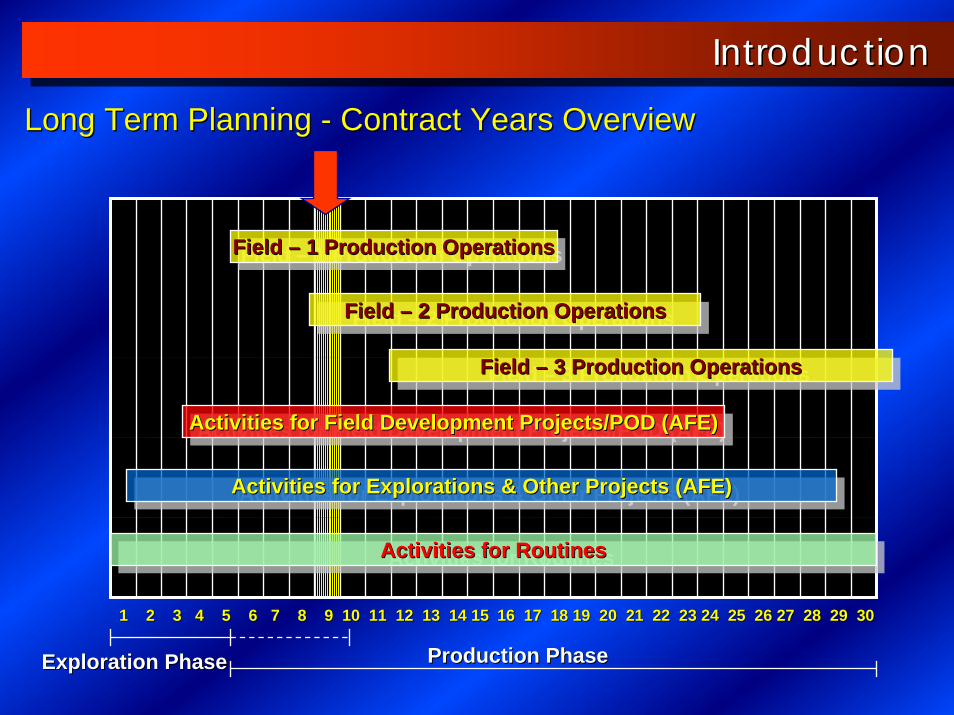

Field – 1 Production OperationsField Field –– 1 Production Operations1 Production Operations

Field – 2 Production OperationsField Field –– 2 Production Operations2 Production Operations

Field – 3 Production OperationsField Field –– 3 Production Operations3 Production Operations

Activities for Field Development Projects/POD (AFE)Activities for Field Development Projects/POD (AFE)Activities for Field Development Projects/POD (AFE)

Activities for Explorations & Other Projects (AFE)Activities for Explorations & Other Projects (AFE)Activities for Explorations & Other Projects (AFE)

Activities for RoutinesActivities for RoutinesActivities for Routines

Long Term Planning Long Term Planning -- Contract Years OverviewContract Years Overview

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Exploration PhaseExploration Phase Production PhaseProduction Phase

IntroductionIntroduction

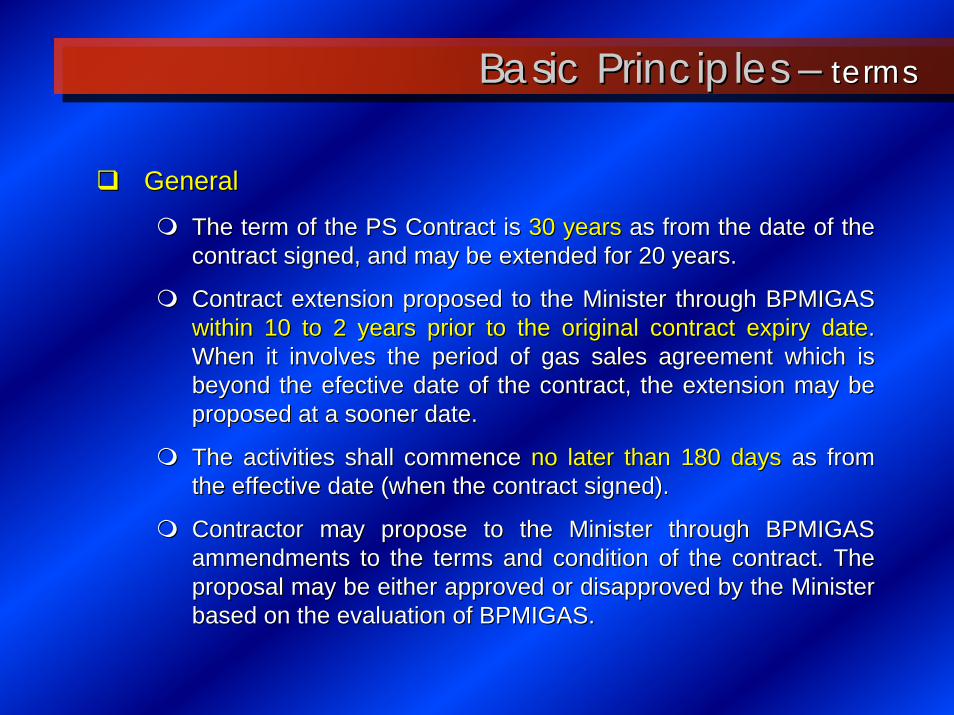

Basic Principles Basic Principles –– termsterms

GeneralGeneral

The term of the PS Contract is The term of the PS Contract is 30 years30 years as from the date of the as from the date of the contract signed, and may be extended for 20 years.contract signed, and may be extended for 20 years.

Contract extension proposed to the Minister through BPMIGAS Contract extension proposed to the Minister through BPMIGAS within 10 to 2 years prior to the original contract expiry datewithin 10 to 2 years prior to the original contract expiry date. . When it involves the period of gas sales agreement which is When it involves the period of gas sales agreement which is beyond the beyond the efectiveefective date of the contract, the extension may be date of the contract, the extension may be proposed at a sooner date.proposed at a sooner date.

The activities shall commence The activities shall commence no later than 180 daysno later than 180 days as from as from the effective date (when the contract signed).the effective date (when the contract signed).

Contractor may propose to the Minister through BPMIGAS Contractor may propose to the Minister through BPMIGAS ammendmentsammendments to the terms and condition of the contract. The to the terms and condition of the contract. The proposal may be either approved or disapproved by the Minister proposal may be either approved or disapproved by the Minister based on the evaluation of BPMIGAS.based on the evaluation of BPMIGAS.

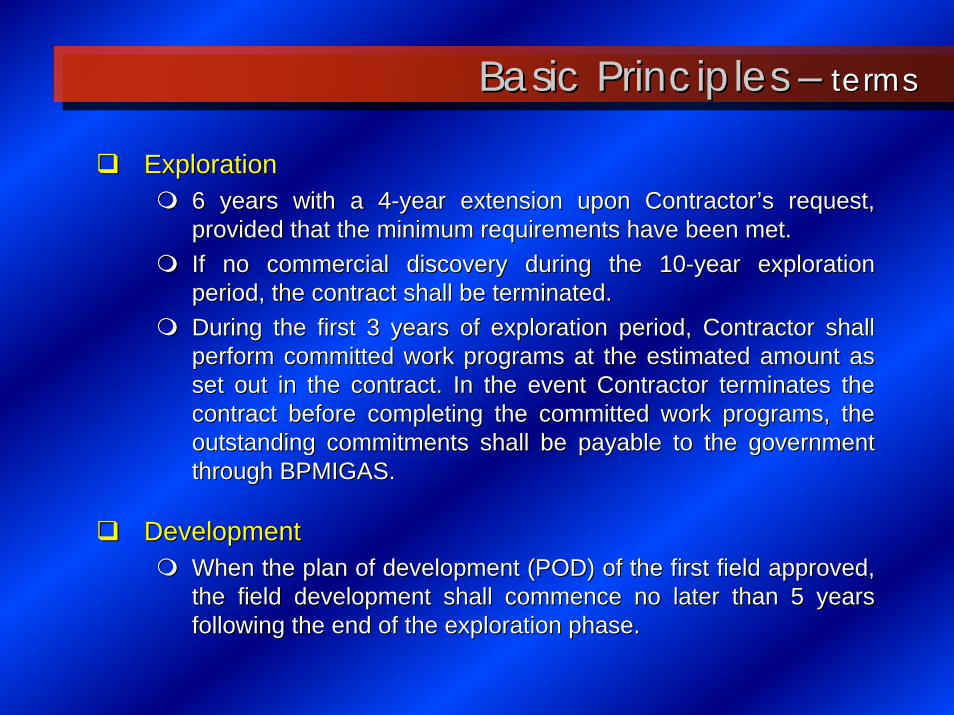

Basic Principles Basic Principles –– termsterms

ExplorationExploration6 years with a 46 years with a 4--year extension upon Contractoryear extension upon Contractor’’s request, s request, provided that the minimum requirements have been met.provided that the minimum requirements have been met.If no commercial discovery during the 10If no commercial discovery during the 10--year exploration year exploration period, the contract shall be terminated.period, the contract shall be terminated.During the first 3 years of exploration period, Contractor shallDuring the first 3 years of exploration period, Contractor shallperform committed work programs at the estimated amount as perform committed work programs at the estimated amount as set out in the contract. In the event Contractor terminates the set out in the contract. In the event Contractor terminates the contract before completing the committed work programs, the contract before completing the committed work programs, the outstanding commitments shall be payable to the government outstanding commitments shall be payable to the government through BPMIGAS.through BPMIGAS.

DevelopmentDevelopmentWhen the plan of development (POD) of the first field approved, When the plan of development (POD) of the first field approved, the field development shall commence no later than 5 years the field development shall commence no later than 5 years following the end of the exploration phase.following the end of the exploration phase.

Basic Principles Basic Principles –– Participating InterestParticipating Interest

OwnershipsOwnershipsThe holder of undivided interests in each PSC may be more The holder of undivided interests in each PSC may be more than one party.than one party.Each interest holder in a PSC is legally a single entity.Each interest holder in a PSC is legally a single entity.

AssignmentAssignmentContractor may assign all or any part of its undivided interest Contractor may assign all or any part of its undivided interest to to any any affiliated companyaffiliated company, then submit a notification to BPMIGAS., then submit a notification to BPMIGAS.Contractor may assign all or any part of its undivided interest Contractor may assign all or any part of its undivided interest to to a a nonnon--affiliated companyaffiliated company with the prior written consent of BPMIGAS.with the prior written consent of BPMIGAS.Government Regulation No.35/2004, effective 14 October 2004, Government Regulation No.35/2004, effective 14 October 2004, requires that the assignments to be approved by the Minister basrequires that the assignments to be approved by the Minister based ed on BPMIGAS evaluation. The Minister may require Contractor to on BPMIGAS evaluation. The Minister may require Contractor to prioritize the Indonesian national companiesprioritize the Indonesian national companies for the assignments to for the assignments to a nona non--affiliated company or to a nonaffiliated company or to a non--party of the PSCparty of the PSC. The majority . The majority interests cannot be assigned to a noninterests cannot be assigned to a non--affiliated company during the affiliated company during the first 3 years of exploration period.first 3 years of exploration period.

Basic Principles Basic Principles –– Participating InterestParticipating Interest

First Field DevelopmentFirst Field Development

Following the approval of the first plan of development (POD) Following the approval of the first plan of development (POD) Contractor is obligated to offer a ten percent (10%) undivided Contractor is obligated to offer a ten percent (10%) undivided interests to an Indonesian Participant.interests to an Indonesian Participant.

The Government Regulation No.35/2004 spells out that the The Government Regulation No.35/2004 spells out that the Indonesia Participant is a local government owned company.Indonesia Participant is a local government owned company.

Local companies shall response to this offer within 60 days as Local companies shall response to this offer within 60 days as from the date of the offering letter.from the date of the offering letter.

In the event no local company responses within 60 days, the In the event no local company responses within 60 days, the Contractor shall offer this participating interest to national Contractor shall offer this participating interest to national companies.companies.

National companies shall response to this offer within 60 days National companies shall response to this offer within 60 days as from the date offering letter.as from the date offering letter.

In the event no national company responses within the 60 days, In the event no national company responses within the 60 days, Contractor has no obligation to offer the 10% undivided interestContractor has no obligation to offer the 10% undivided interest..

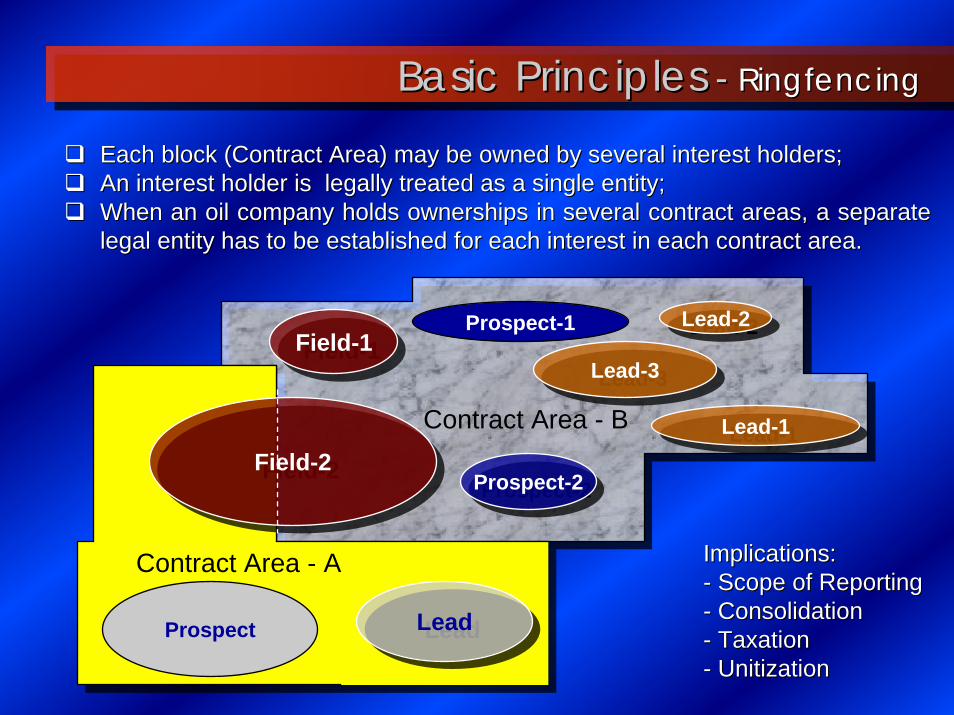

Each block (Contract Area) may be owned by several interest holdEach block (Contract Area) may be owned by several interest holders;ers;An interest holder is legally treated as a single entity;An interest holder is legally treated as a single entity;When an oil company holds ownerships in several contract areas, When an oil company holds ownerships in several contract areas, a separate a separate legal entity has to be established for each interest in each conlegal entity has to be established for each interest in each contract area.tract area.

Basic PrinciplesBasic Principles -- RingfencingRingfencing

Field-1Field-1

Lead-1Lead-1

Lead-2Lead-2

Prospect-2Prospect-2

Prospect-1

Lead-3Lead-3

Implications:Implications:-- Scope of ReportingScope of Reporting-- ConsolidationConsolidation-- TaxationTaxation-- UnitizationUnitization

Field-2Field-2

Contract Area - B

LeadLeadProspect

Contract Area - A

Basic Principles Basic Principles –– RingfencingRingfencing

Refers to the previous slideRefers to the previous slide

Contract area Contract area ‘‘AA’’ is reported separately from Contract area is reported separately from Contract area ‘‘BB’’

No consolidation with regards to revenue, costs and taxation.No consolidation with regards to revenue, costs and taxation.

FieldField--2 lays in both contract areas represents a unitized field, 2 lays in both contract areas represents a unitized field, subject to a unitization agreement between block subject to a unitization agreement between block ‘‘AA’’ and and ‘‘BB’’..

The Minister appoints the operator of unitized field based on thThe Minister appoints the operator of unitized field based on the e BPMIGAS evaluation.BPMIGAS evaluation.

When the extent of a unitized field in the adjacent area is an When the extent of a unitized field in the adjacent area is an open area, Contractor may request to the Minister through open area, Contractor may request to the Minister through BPMIGAS to extend its contract area to cover the whole field. BPMIGAS to extend its contract area to cover the whole field.

Such a request is applicable if the extent of a unitized field Such a request is applicable if the extent of a unitized field remains an open area within 5 years as from the date of remains an open area within 5 years as from the date of ContractorContractor’’s report regarding the unitized field.s report regarding the unitized field.

Basic Principles Basic Principles –– RingfencingRingfencing

Implications & Other MattersImplications & Other Matters

Operating Costs to be to be recovered from production in the Operating Costs to be to be recovered from production in the same contract area annually.same contract area annually.

Profit/loss resulted from a contract area never be consolidated Profit/loss resulted from a contract area never be consolidated with profit/loss from any other contract areas. Each interest with profit/loss from any other contract areas. Each interest holder in a PSC files for income tax separately.holder in a PSC files for income tax separately.

Costs incurred dedicated for several blocks are allocated to Costs incurred dedicated for several blocks are allocated to each block based on a method which is in accordance with each block based on a method which is in accordance with generally accepted and recognized accounting generally accepted and recognized accounting sistemssistems..

Production and costs of a unitized field to be allocated to eachProduction and costs of a unitized field to be allocated to eachblock typically based on estimated amounts of reserves.block typically based on estimated amounts of reserves.

The appointment of an operator for a unitized field is normally The appointment of an operator for a unitized field is normally based on technobased on techno--economic considerations.economic considerations.

Basic Principles Basic Principles –– RingfencingRingfencing

Field DevelopmentField Development

A Study of a field development is required to determine the scalA Study of a field development is required to determine the scale, e, exploitation designs, and its economic forecast.exploitation designs, and its economic forecast.The study, known as The study, known as Plan of Development (Plan of Development (PoDPoD)), is proposed to , is proposed to BPMIGAS for approval. BPMIGAS for approval. Note:1Note:1stst field requires Ministerfield requires Minister’’s approval.s approval.

Major Economic MeasurementsMajor Economic Measurements: : -- Government Take & Contractor Take Government Take & Contractor Take -- Internal Rate of Return (IRR)Internal Rate of Return (IRR)-- Pay Back periodPay Back periodStandStand--alone approachalone approach & & blockblock--wise approachwise approach::

StandStand--alone approach calculates the revenue & costs within alone approach calculates the revenue & costs within the field, the field, to measure the to measure the thethe fieldfield’’s economic profiles economic profile..BlockBlock--wise approach calculates the whole revenue & costs wise approach calculates the whole revenue & costs within the block, within the block, to reflect the real calculation of the PSCto reflect the real calculation of the PSC. .

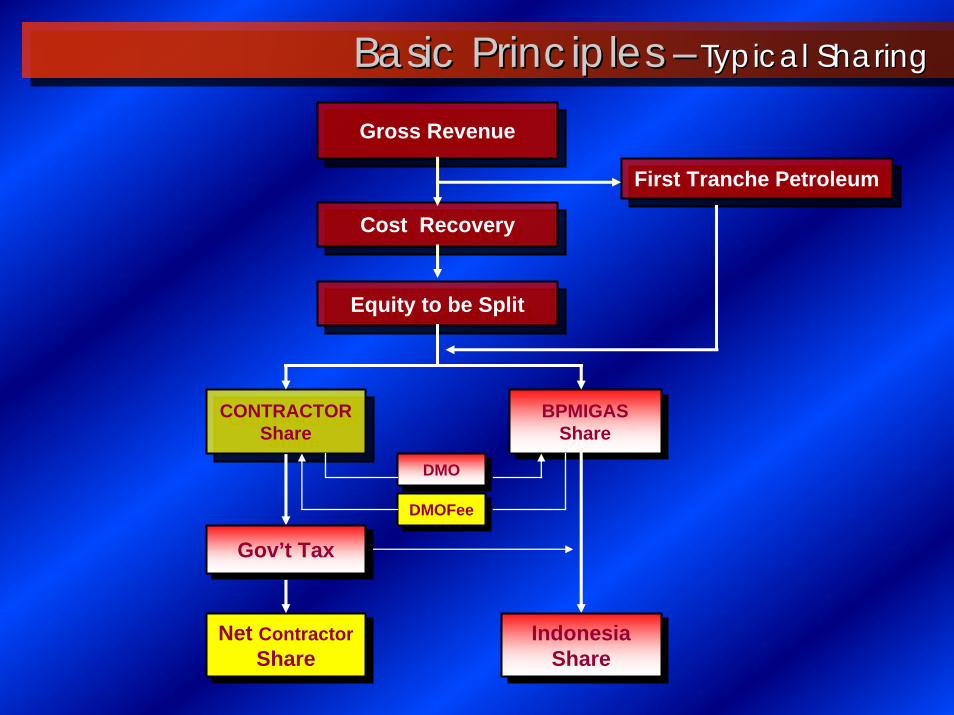

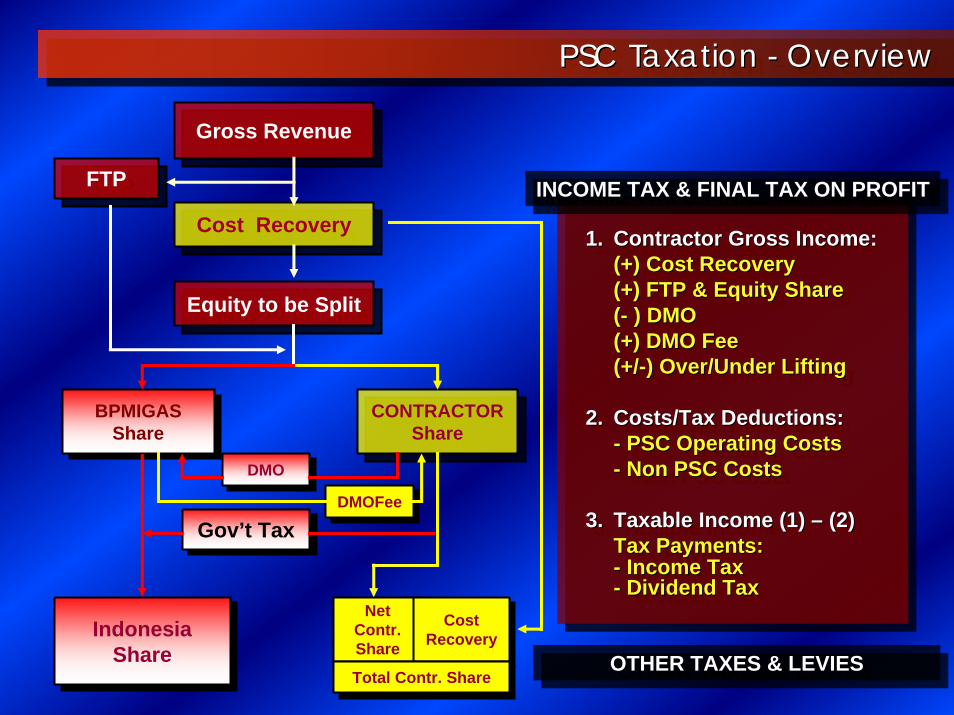

Basic Principles Basic Principles –– Typical SharingTypical Sharing

Gross RevenueGross Revenue

First Tranche PetroleumFirst Tranche Petroleum

Cost RecoveryCost Recovery

Equity to be SplitEquity to be Split

CONTRACTORShare

CONTRACTORShare

BPMIGASShare

BPMIGASShare

Net ContractorShare

Net ContractorShare

DMODMO

DMOFeeDMOFee

IndonesiaShare

IndonesiaShare

Gov’t TaxGov’t Tax

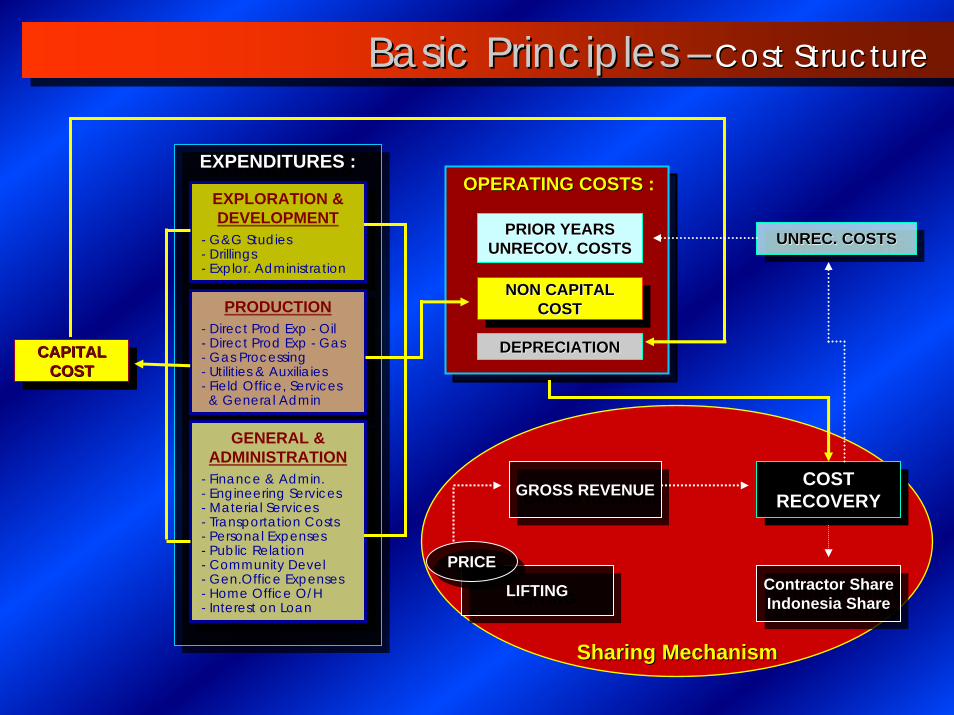

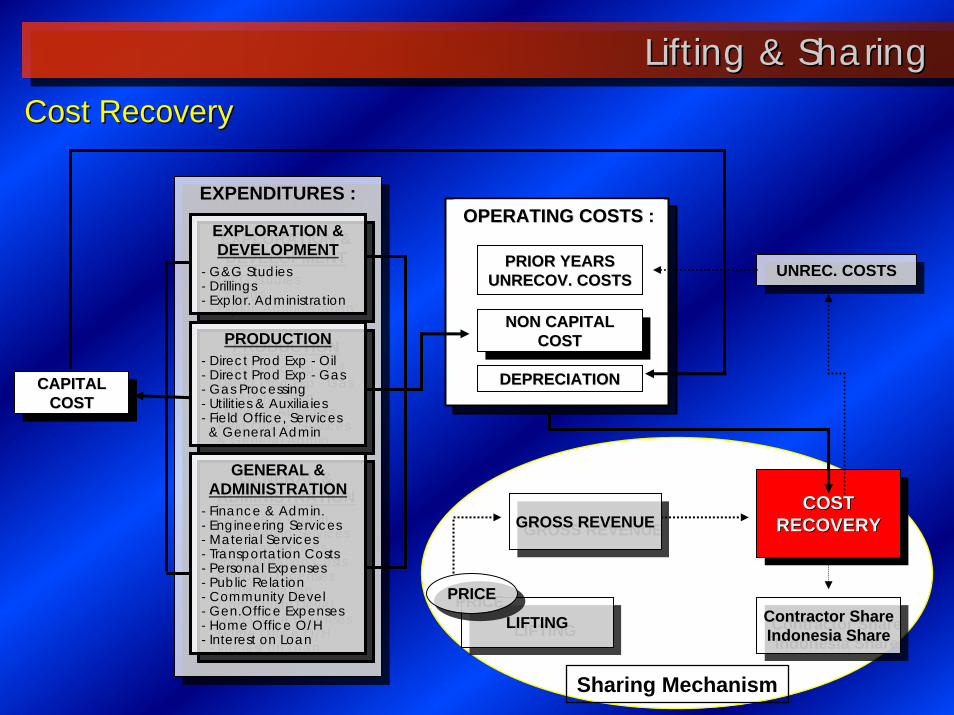

EXPENDITURES :EXPENDITURES :EXPENDITURES :

LIFTINGLIFTINGLIFTING

EXPLORATION &DEVELOPMENT

- G&G Studies- Drillings- Explor. Administration

EXPLORATION &DEVELOPMENT

- G&G Studies- Drillings- Explor. Administration

PRODUCTION- Direct Prod Exp - Oil - Direct Prod Exp - Gas- Gas Processing- Utilities & Auxiliaies- Field Office, Services & General Admin

PRODUCTION- Direct Prod Exp - Oil - Direct Prod Exp - Gas- Gas Processing- Utilities & Auxiliaies- Field Office, Services & General Admin

GENERAL & ADMINISTRATION

- Finance & Admin.- Engineering Services- Material Services- Transportation Costs- Personal Expenses- Public Relation- Community Devel- Gen.Office Expenses- Home Office O/H- Interest on Loan

GENERAL & ADMINISTRATION

- Finance & Admin.- Engineering Services- Material Services- Transportation Costs- Personal Expenses- Public Relation- Community Devel- Gen.Office Expenses- Home Office O/H- Interest on Loan

CAPITALCOST

CAPITALCAPITALCOSTCOST

COSTRECOVERY

COSTCOSTRECOVERYRECOVERYGROSS REVENUEGROSS REVENUEGROSS REVENUE

PRICEPRICEPRICE

Contractor ShareIndonesia Share

Contractor ShareContractor ShareIndonesia ShareIndonesia Share

DEPRECIATIONDEPRECIATION

PRIOR YEARSPRIOR YEARSUNRECOV. COSTSUNRECOV. COSTS UNREC. COSTSUNREC. COSTSUNREC. COSTS

NON CAPITALCOST

NON CAPITALNON CAPITALCOSTCOST

OPERATING COSTSOPERATING COSTS :

Basic Principles Basic Principles –– Cost StructureCost Structure

Sharing MechanismSharing Mechanism

Exploration & Development ActivitiesExploration & Development Activities

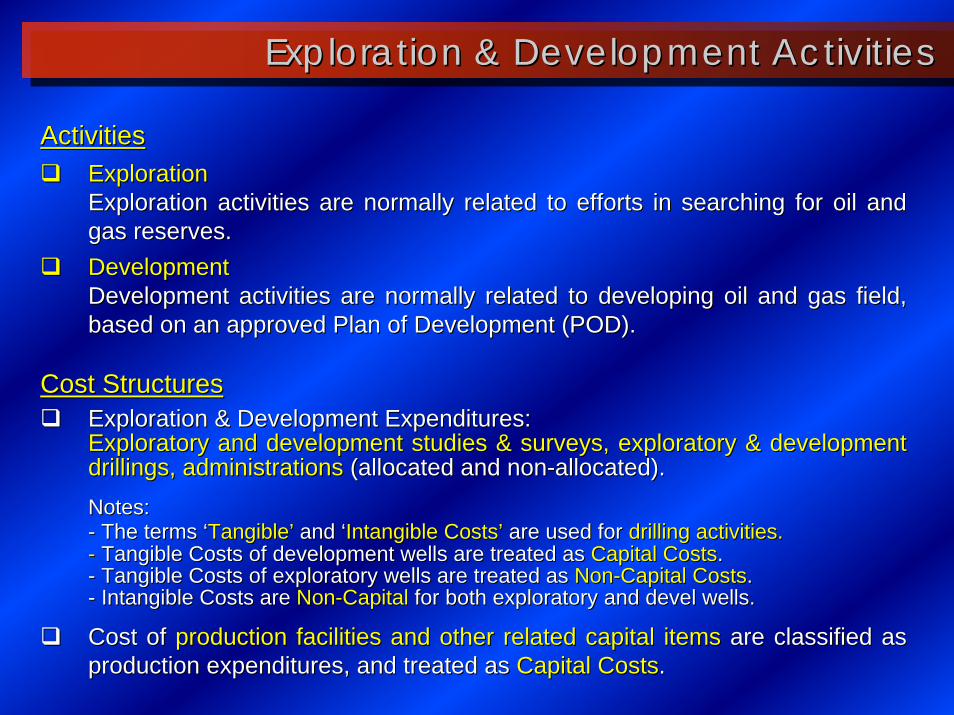

ActivitiesActivitiesExplorationExplorationExploration activities are normally related to efforts in searchExploration activities are normally related to efforts in searching for oil and ing for oil and gas reserves.gas reserves.DevelopmentDevelopmentDevelopment activities are normally related to developing oil anDevelopment activities are normally related to developing oil and gas field, d gas field, based on an approved Plan of Development (POD).based on an approved Plan of Development (POD).

Cost StructuresCost StructuresExploration & Development Expenditures:Exploration & Development Expenditures:Exploratory and development studies & surveys, exploratory &Exploratory and development studies & surveys, exploratory & development development drillings, administrations drillings, administrations (allocated and non(allocated and non--allocated). allocated). Notes:Notes:-- The terms The terms ‘‘TangibleTangible’’ and and ‘‘IntangibleIntangible CostsCosts’’ are used for are used for drilling activities. drilling activities. -- Tangible CostsTangible Costs ofof development wellsdevelopment wells are treated as are treated as Capital CostsCapital Costs..-- Tangible CostsTangible Costs ofof exploratory wellsexploratory wells areare treated astreated as NonNon--Capital CostsCapital Costs..-- Intangible Costs are Intangible Costs are NonNon--CapitalCapital for both exploratory and for both exploratory and develdevel wells.wells.

Cost of Cost of production facilities and other related capital itemsproduction facilities and other related capital items are classified as are classified as production expenditures, and treated as production expenditures, and treated as Capital CostsCapital Costs..

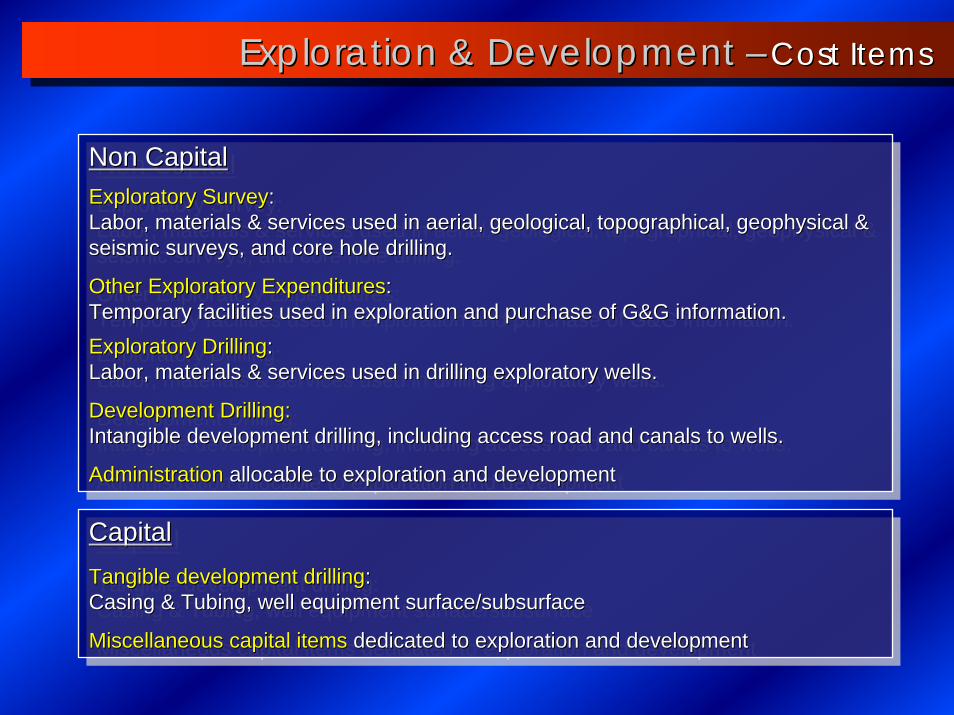

Non Capital Exploratory Survey:Labor, materials & services used in aerial, geological, topographical, geophysical & seismic surveys, and core hole drilling.

Other Exploratory Expenditures:Temporary facilities used in exploration and purchase of G&G information.Exploratory Drilling:Labor, materials & services used in drilling exploratory wells.

Development Drilling:Intangible development drilling, including access road and canals to wells.

Administration allocable to exploration and development

Non Capital Non Capital Exploratory SurveyExploratory Survey::Labor, materials & services used in aerial, geological, topograpLabor, materials & services used in aerial, geological, topographical, geophysical & hical, geophysical & seismic surveys, and core hole drilling.seismic surveys, and core hole drilling.

Other Exploratory ExpendituresOther Exploratory Expenditures::Temporary facilities used in exploration and purchase of G&G infTemporary facilities used in exploration and purchase of G&G information.ormation.Exploratory DrillingExploratory Drilling::Labor, materials & services used in drilling exploratory wells.Labor, materials & services used in drilling exploratory wells.

Development Drilling:Development Drilling:Intangible development drilling, including access road and canalIntangible development drilling, including access road and canals to wells.s to wells.

AdministrationAdministration allocable to exploration and developmentallocable to exploration and development

CapitalTangible development drilling:Casing & Tubing, well equipment surface/subsurface

Miscellaneous capital items dedicated to exploration and development

CapitalCapitalTangible development drillingTangible development drilling::Casing & Tubing, well equipment surface/subsurfaceCasing & Tubing, well equipment surface/subsurface

Miscellaneous capital itemsMiscellaneous capital items dedicated to exploration and developmentdedicated to exploration and development

Exploration & Development Exploration & Development –– Cost ItemsCost Items

Development Development –– Production CapitalProduction Capital

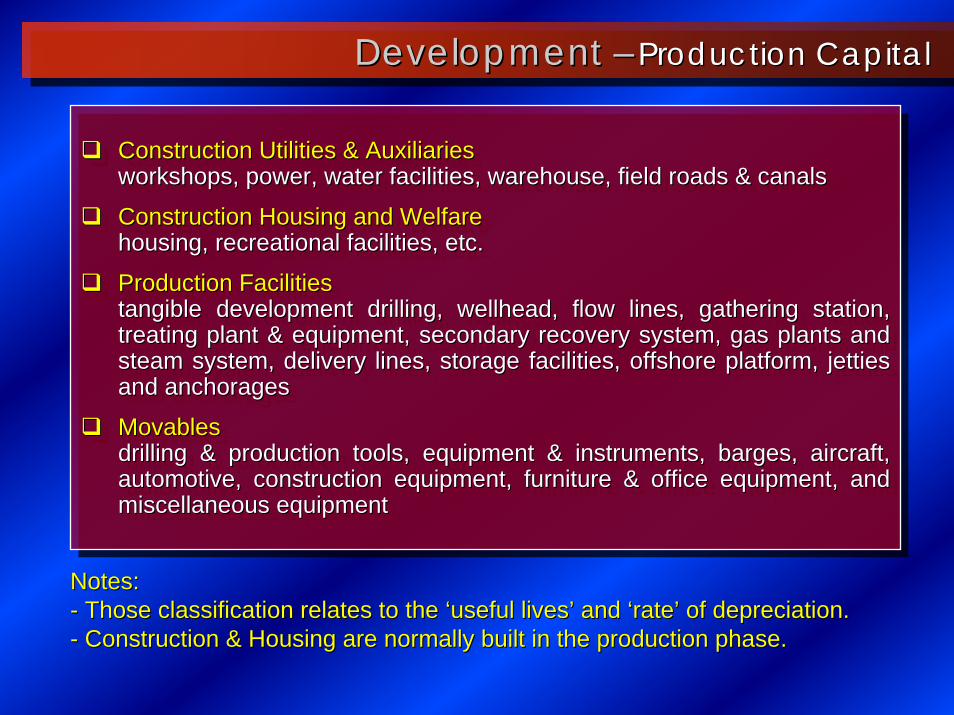

Construction Utilities & Auxiliariesworkshops, power, water facilities, warehouse, field roads & canals

Construction Housing and Welfarehousing, recreational facilities, etc.

Production Facilitiestangible development drilling, wellhead, flow lines, gathering station, treating plant & equipment, secondary recovery system, gas plants and steam system, delivery lines, storage facilities, offshore platform, jetties and anchorages

Movablesdrilling & production tools, equipment & instruments, barges, aircraft, automotive, construction equipment, furniture & office equipment, and miscellaneous equipment

Construction Utilities & AuxiliariesConstruction Utilities & Auxiliariesworkshops, power, water facilities, warehouse, field roads & canworkshops, power, water facilities, warehouse, field roads & canalsals

Construction Housing and WelfareConstruction Housing and Welfarehousing, recreational facilities, etc.housing, recreational facilities, etc.

Production FacilitiesProduction Facilitiestangible development drilling, wellhead, flow lines, gathering stangible development drilling, wellhead, flow lines, gathering station, tation, treating plant & equipment, secondary recovery system, gas planttreating plant & equipment, secondary recovery system, gas plants and s and steam system, delivery lines, storage facilities, offshore platfsteam system, delivery lines, storage facilities, offshore platform, jetties orm, jetties and anchoragesand anchorages

MovablesMovablesdrilling & production tools, equipment & instruments, barges, aidrilling & production tools, equipment & instruments, barges, aircraft, rcraft, automotive, construction equipment, furniture & office equipmentautomotive, construction equipment, furniture & office equipment, and , and miscellaneous equipmentmiscellaneous equipment

Notes:Notes:-- Those classification relates to the Those classification relates to the ‘‘useful livesuseful lives’’ and and ‘‘raterate’’ of depreciation.of depreciation.-- Construction & Housing are normally built in the production phaConstruction & Housing are normally built in the production phase.se.

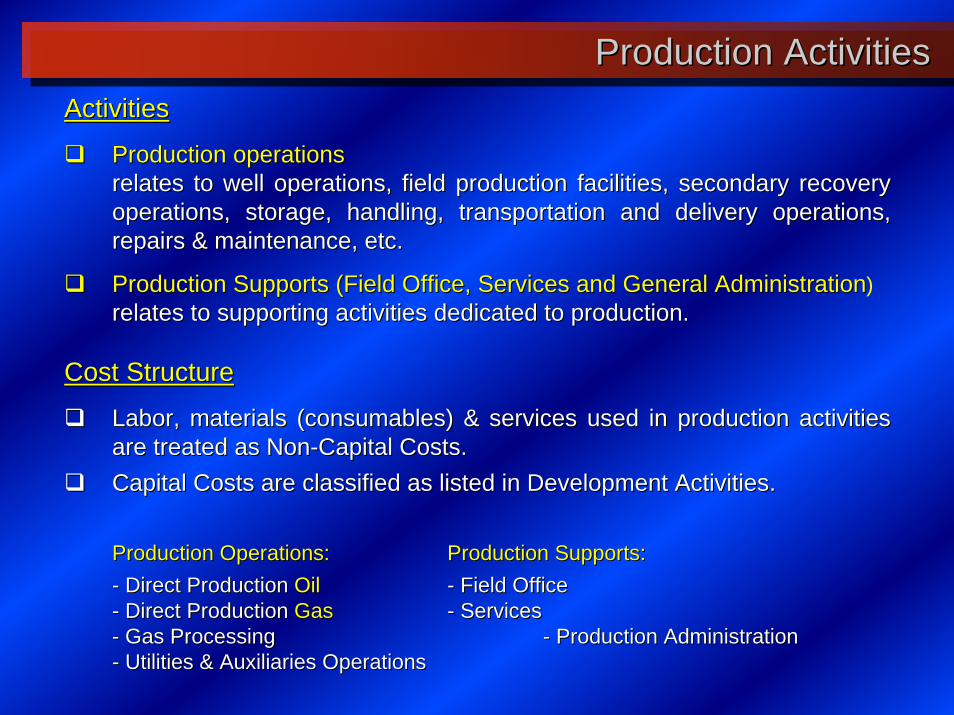

Production ActivitiesProduction ActivitiesActivitiesActivities

Production operationsProduction operationsrelates to well operations, field production facilities, secondarelates to well operations, field production facilities, secondary recovery ry recovery operations, storage, handling, transportation and delivery operaoperations, storage, handling, transportation and delivery operations, tions, repairs & maintenance, etc. repairs & maintenance, etc.

Production Supports (Field Office, Services and General AdministProduction Supports (Field Office, Services and General Administrationration)relates to supporting activities dedicated to production.relates to supporting activities dedicated to production.

Cost StructureCost Structure

Labor, materials (consumables) & services used in production actLabor, materials (consumables) & services used in production activities ivities are treated as Nonare treated as Non--Capital Costs.Capital Costs.Capital Costs are classified as listed in Development ActivitiesCapital Costs are classified as listed in Development Activities..

Production Operations: Production Operations: Production Supports:Production Supports:-- Direct Production Direct Production OilOil -- Field OfficeField Office-- Direct Production Direct Production Gas Gas -- ServicesServices-- Gas Processing Gas Processing -- Production AdministrationProduction Administration-- Utilities & Auxiliaries OperationsUtilities & Auxiliaries Operations

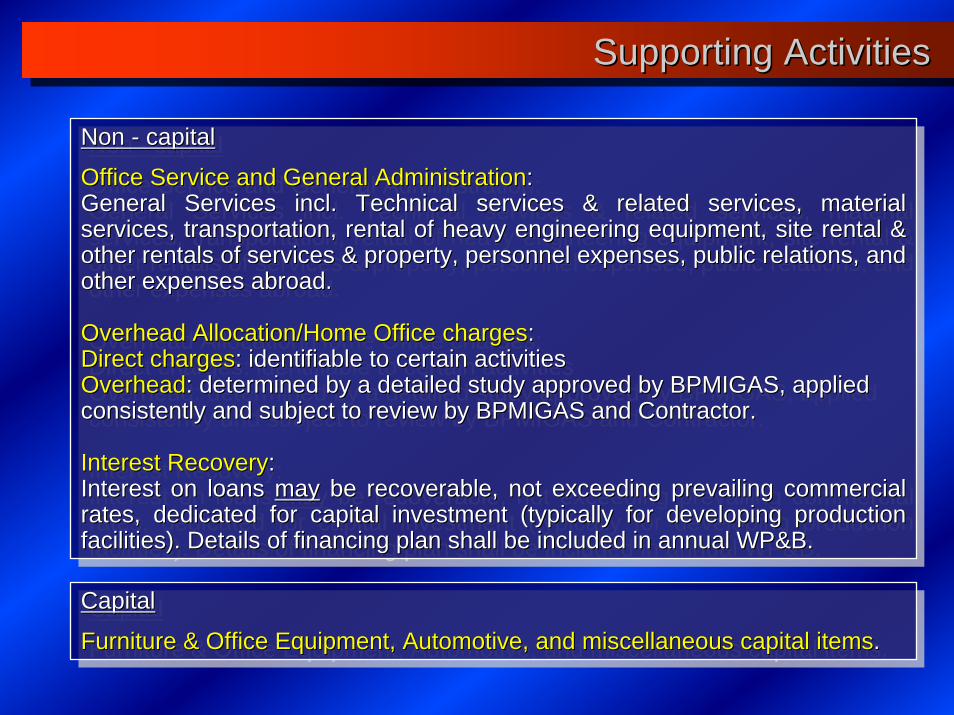

Non - capital

Office Service and General Administration:General Services incl. Technical services & related services, material services, transportation, rental of heavy engineering equipment, site rental & other rentals of services & property, personnel expenses, public relations, and other expenses abroad.

Overhead Allocation/Home Office charges:Direct charges: identifiable to certain activitiesOverhead: determined by a detailed study approved by BPMIGAS, applied consistently and subject to review by BPMIGAS and Contractor.

Interest Recovery:Interest on loans may be recoverable, not exceeding prevailing commercial rates, dedicated for capital investment (typically for developing production facilities). Details of financing plan shall be included in annual WP&B.

Non Non -- capitalcapital

Office Service and General AdministrationOffice Service and General Administration::General Services incl. Technical services & related services, maGeneral Services incl. Technical services & related services, material terial services, transportation, rental of heavy engineering equipment,services, transportation, rental of heavy engineering equipment, site rental & site rental & other rentals of services & property, personnel expenses, publicother rentals of services & property, personnel expenses, public relations, and relations, and other expenses abroad.other expenses abroad.

Overhead Allocation/Home Office chargesOverhead Allocation/Home Office charges::Direct chargesDirect charges: identifiable to certain activities: identifiable to certain activitiesOverheadOverhead: determined by a detailed study approved by BPMIGAS, applied : determined by a detailed study approved by BPMIGAS, applied consistently and subject to review by BPMIGAS and Contractor.consistently and subject to review by BPMIGAS and Contractor.

Interest RecoveryInterest Recovery::Interest on loans Interest on loans maymay be recoverable, not exceeding prevailing commercial be recoverable, not exceeding prevailing commercial rates, dedicated for capital investment (typically for developinrates, dedicated for capital investment (typically for developing production g production facilities). Details of financing plan shall be included in annufacilities). Details of financing plan shall be included in annual WP&B.al WP&B.

Capital

Furniture & Office Equipment, Automotive, and miscellaneous capital items.

CapitalCapital

Furniture & Office Equipment, Automotive, and miscellaneous capiFurniture & Office Equipment, Automotive, and miscellaneous capital itemstal items..

Supporting ActivitiesSupporting Activities

Supporting ActivitiesSupporting Activities

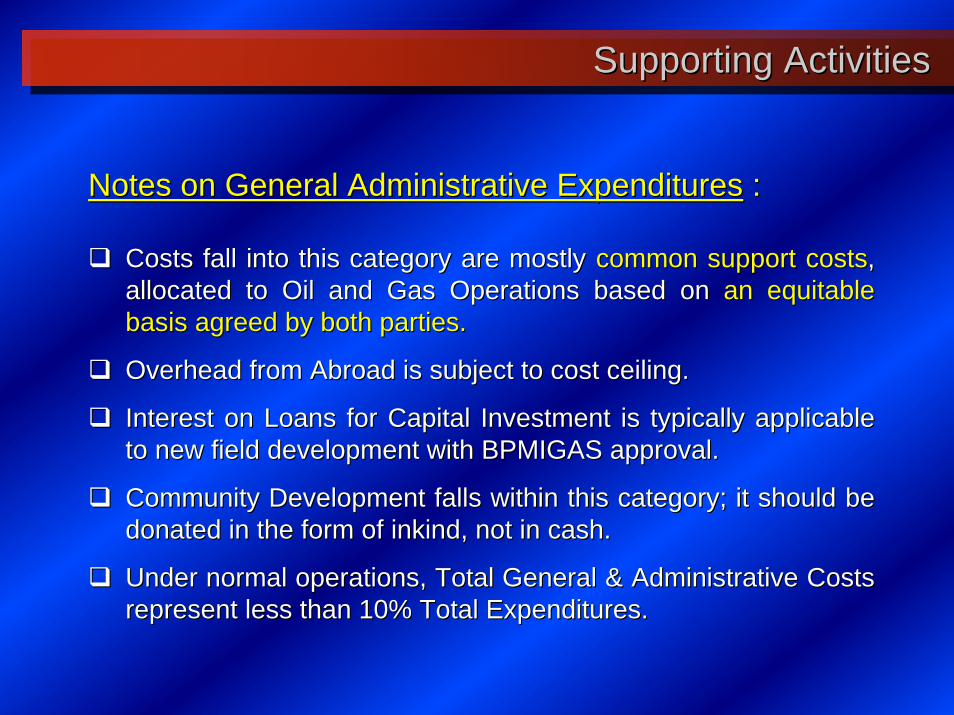

Notes on General Administrative ExpendituresNotes on General Administrative Expenditures ::

Costs fall into this category are mostly Costs fall into this category are mostly common support costscommon support costs, , allocated to Oil and Gas Operations based on allocated to Oil and Gas Operations based on an equitable an equitable basis agreed by both parties.basis agreed by both parties.

Overhead from Abroad is subject to cost ceiling.Overhead from Abroad is subject to cost ceiling.

Interest on Loans for Capital Investment is typically applicableInterest on Loans for Capital Investment is typically applicableto new field development with BPMIGAS approval.to new field development with BPMIGAS approval.

Community Development falls within this category; it should be Community Development falls within this category; it should be donated in the form of donated in the form of inkindinkind, not in cash., not in cash.

Under normal operations, Total General & Administrative Costs Under normal operations, Total General & Administrative Costs represent less than 10% Total Expenditures.represent less than 10% Total Expenditures.

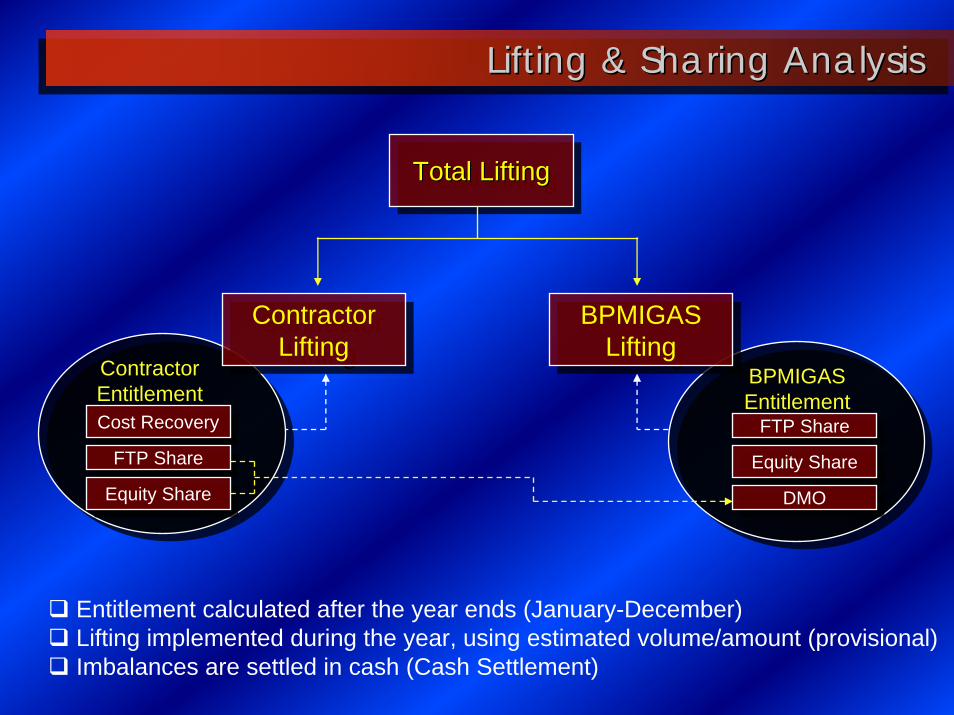

Lifting & Sharing Analysis Lifting & Sharing Analysis

Total LiftingTotal LiftingTotal Lifting

ContractorLifting

ContractorLifting

BPMIGASLifting

BPMIGASLifting

Cost RecoveryCost Recovery

FTP ShareFTP Share

Equity ShareEquity Share

FTP ShareFTP Share

Equity ShareEquity Share

DMODMO

ContractorEntitlement

BPMIGASEntitlement

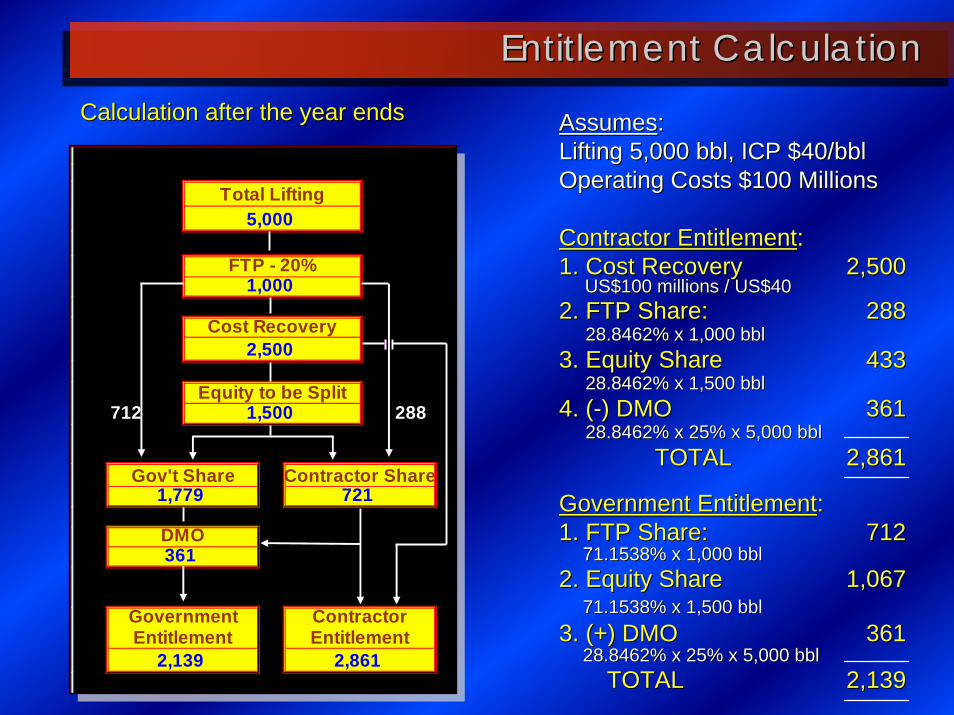

Entitlement calculated after the year ends (January-December)Lifting implemented during the year, using estimated volume/amount (provisional)Imbalances are settled in cash (Cash Settlement)

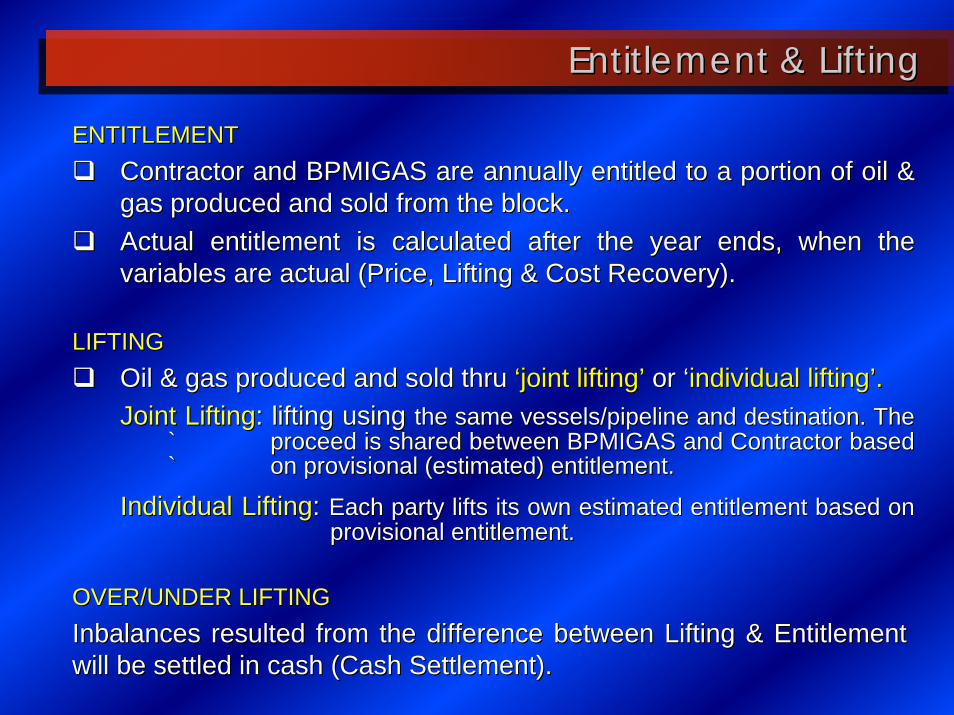

ENTITLEMENTENTITLEMENTContractor and BPMIGAS are annually entitled to a portion of oilContractor and BPMIGAS are annually entitled to a portion of oil & & gas produced and sold from the block. gas produced and sold from the block. Actual entitlement is calculated after the year ends, when the Actual entitlement is calculated after the year ends, when the variables are actual (Price, Lifting & Cost Recovery).variables are actual (Price, Lifting & Cost Recovery).

LIFTINGLIFTINGOil & gas produced and sold thru Oil & gas produced and sold thru ‘‘joint liftingjoint lifting’’ or or ‘‘individual liftingindividual lifting’’..Joint LiftingJoint Lifting: lifting using : lifting using the same vessels/pipeline and destination. The the same vessels/pipeline and destination. The

`̀ proceed is shared between BPMIGAS and Contractor based proceed is shared between BPMIGAS and Contractor based `̀ on provisional (estimated) entitlement.on provisional (estimated) entitlement.

Individual LiftingIndividual Lifting: : Each party lifts its own estimated entitlement based on Each party lifts its own estimated entitlement based on provisional entitlement. provisional entitlement.

OVER/UNDER LIFTINGOVER/UNDER LIFTINGInbalancesInbalances resulted from the difference between Lifting & Entitlement resulted from the difference between Lifting & Entitlement will be settled in cash (Cash Settlement).will be settled in cash (Cash Settlement).

Entitlement & Lifting Entitlement & Lifting

288

2,861

ContractorEntitlement

361

GovernmentEntitlement

2,139

DMO

Gov't Share Contractor Share721

Cost Recovery2,500

1,500Equity to be Split

1,000

5,000Total Lifting

FTP - 20%

712

1,779

AssumesAssumes::Lifting 5,000 bbl, ICP $40/bblLifting 5,000 bbl, ICP $40/bblOperating Costs $100 MillionsOperating Costs $100 Millions

Contractor EntitlementContractor Entitlement::1. Cost Recovery1. Cost Recovery 2,5002,500

US$100 millions / US$40US$100 millions / US$402. FTP Share: 2. FTP Share: 288288

28.8462% x 1,000 bbl28.8462% x 1,000 bbl3. Equity Share3. Equity Share 433433

28.8462% x 1,500 bbl28.8462% x 1,500 bbl4. (4. (--) DMO) DMO 361361

28.8462% x 25% x 5,000 bbl28.8462% x 25% x 5,000 bblTOTALTOTAL 2,8612,861

Government EntitlementGovernment Entitlement::1. FTP Share: 1. FTP Share: 712712

71.1538% x 1,000 bbl71.1538% x 1,000 bbl2. Equity Share2. Equity Share 1,0671,067

71.1538% x 1,500 bbl71.1538% x 1,500 bbl3. (+) DMO3. (+) DMO 361361

28.8462% x 25% x 5,000 bbl28.8462% x 25% x 5,000 bblTOTALTOTAL 2,1392,139

Entitlement Calculation Entitlement Calculation Calculation after the year endsCalculation after the year ends

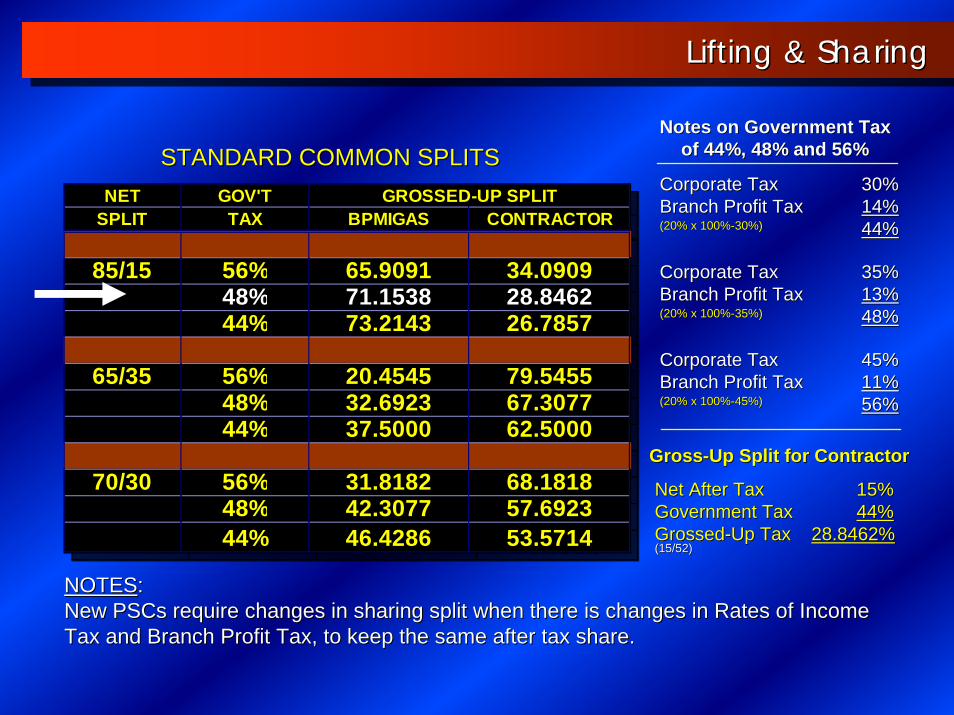

STANDARD COMMON SPLITSSTANDARD COMMON SPLITS

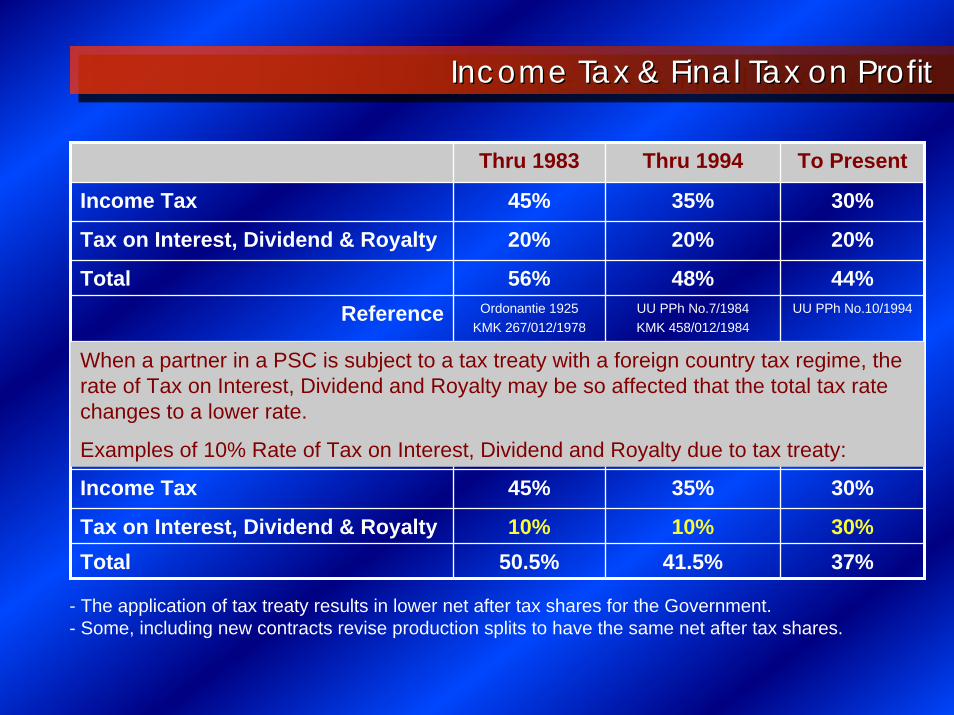

NOTESNOTES::New New PSCsPSCs require changes in sharing split when there is changes in Ratesrequire changes in sharing split when there is changes in Rates of Income of Income Tax and Branch Profit Tax, to keep the same after tax share.Tax and Branch Profit Tax, to keep the same after tax share.

NET GOV'T GROSSED-UP SPLITSPLIT TAX BPMIGAS CONTRACTOR

85/15 56% 65.9091 34.090948% 71.1538 28.846244% 73.2143 26.7857

65/35 56% 20.4545 79.545548% 32.6923 67.307744% 37.5000 62.5000

70/30 56% 31.8182 68.181848% 42.3077 57.692344% 46.4286 53.5714

NET GOV'T GROSSED-UP SPLITSPLIT TAX BPMIGAS CONTRACTOR

85/15 56% 65.9091 34.090948% 71.1538 28.846244% 73.2143 26.7857

65/35 56% 20.4545 79.545548% 32.6923 67.307744% 37.5000 62.5000

70/30 56% 31.8182 68.181848% 42.3077 57.692344% 46.4286 53.5714

Corporate TaxCorporate Tax 30%30%Branch Profit TaxBranch Profit Tax 14%14%(20% x 100%(20% x 100%--30%)30%) 44%44%

Corporate TaxCorporate Tax 35%35%Branch Profit TaxBranch Profit Tax 13%13%(20% x 100%(20% x 100%--35%)35%) 48%48%

Corporate TaxCorporate Tax 45%45%Branch Profit TaxBranch Profit Tax 11%11%(20% x 100%(20% x 100%--45%)45%) 56%56%

Notes on Government TaxNotes on Government Taxof 44%, 48% and 56%of 44%, 48% and 56%

GrossGross--Up Split for ContractorUp Split for Contractor

Net After TaxNet After Tax 15%15%Government TaxGovernment Tax 44%44%GrossedGrossed--Up Tax Up Tax 28.8462%28.8462%(15/52)(15/52)

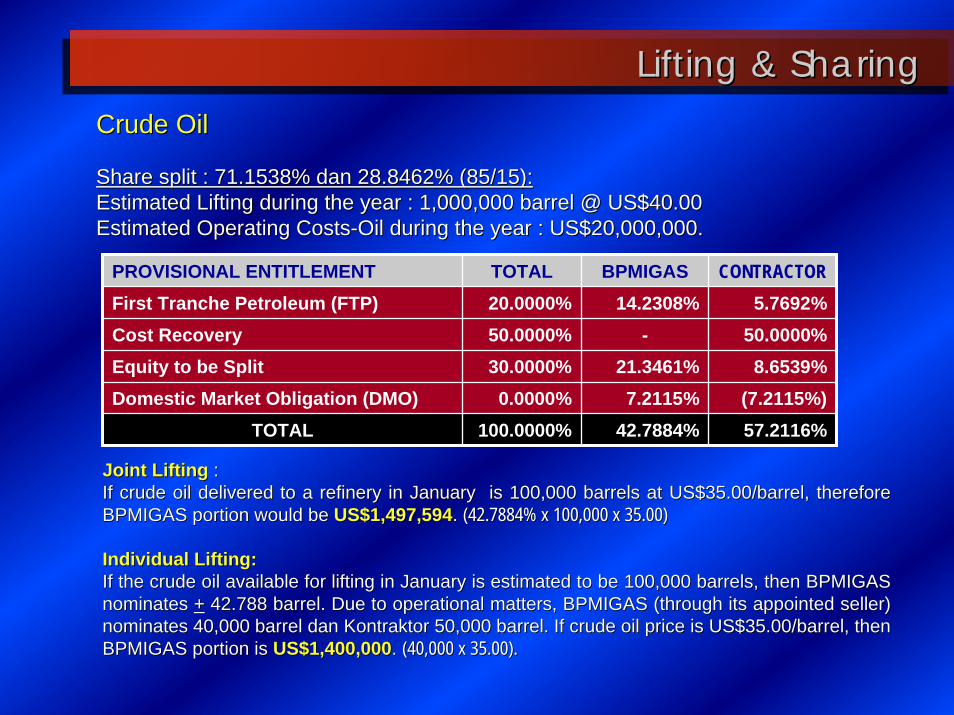

Lifting & SharingLifting & Sharing

Crude OilCrude Oil

Share split : 71.1538% Share split : 71.1538% dandan 28.8462% (85/15):28.8462% (85/15):Estimated Lifting during the year : 1,000,000 barrel @ US$40.00 Estimated Lifting during the year : 1,000,000 barrel @ US$40.00 Estimated Operating CostsEstimated Operating Costs--Oil during the year : US$20,000,000.Oil during the year : US$20,000,000.

Lifting & SharingLifting & Sharing

PROVISIONAL ENTITLEMENT TOTAL BPMIGAS CONTRACTORFirst Tranche Petroleum (FTP) 20.0000% 14.2308% 5.7692%Cost Recovery 50.0000% - 50.0000%Equity to be Split 30.0000% 21.3461% 8.6539%Domestic Market Obligation (DMO) 0.0000% 7.2115% (7.2115%)

TOTAL 100.0000% 42.7884% 57.2116%

Joint Lifting Joint Lifting ::If crude oil delivered to a refinery in January is 100,000 barrIf crude oil delivered to a refinery in January is 100,000 barrels at US$35.00/barrel, therefore els at US$35.00/barrel, therefore BPMIGAS portion would be BPMIGAS portion would be US$1,497,594US$1,497,594. . (42.7884% x 100,000 x 35.00)(42.7884% x 100,000 x 35.00)

Individual Lifting:Individual Lifting:If the crude oil available for lifting in January is estimated tIf the crude oil available for lifting in January is estimated to be 100,000 barrels, then BPMIGAS o be 100,000 barrels, then BPMIGAS nominates nominates ++ 42.788 barrel. Due to operational matters, BPMIGAS (through its42.788 barrel. Due to operational matters, BPMIGAS (through its appointed seller) appointed seller) nominates 40,000 barrel nominates 40,000 barrel dandan KontraktorKontraktor 50,000 barrel. If crude oil price is US$35.00/barrel, then 50,000 barrel. If crude oil price is US$35.00/barrel, then BPMIGAS portion is BPMIGAS portion is US$1,400,000US$1,400,000. . (40,000 x 35.00).(40,000 x 35.00).

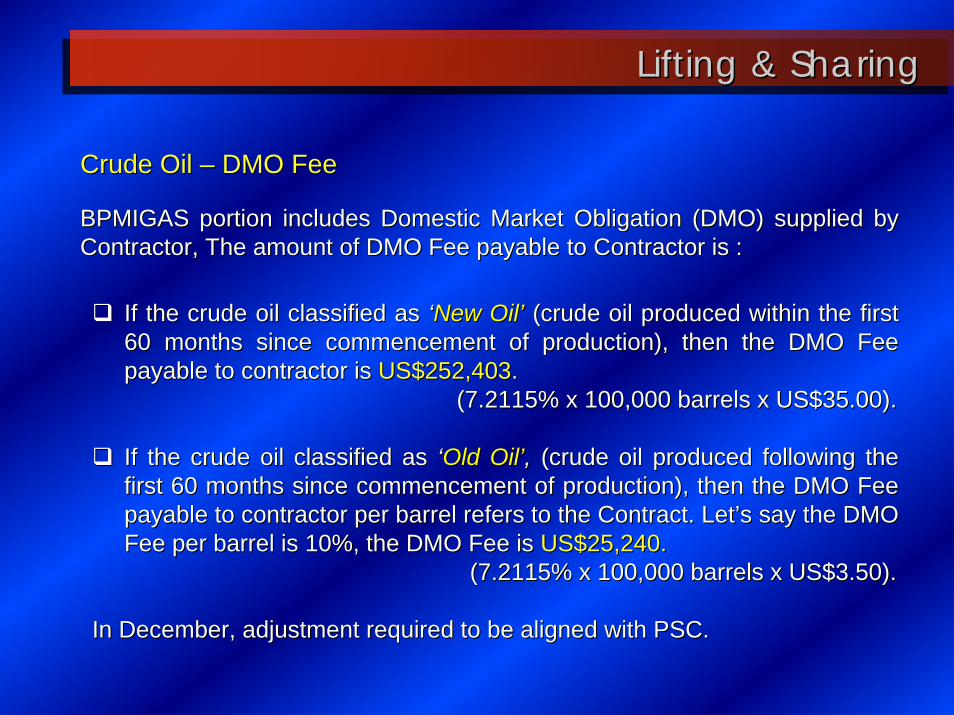

Crude Oil Crude Oil –– DMO FeeDMO Fee

BPMIGAS portion includes Domestic Market Obligation (DMO) suppliBPMIGAS portion includes Domestic Market Obligation (DMO) supplied by ed by Contractor, The amount of DMO Fee payable to Contractor is :Contractor, The amount of DMO Fee payable to Contractor is :

If the crude oil classified as If the crude oil classified as ‘‘New OilNew Oil’’ (crude oil produced within the first(crude oil produced within the first60 months since commencement of production), then the DMO Fee 60 months since commencement of production), then the DMO Fee payable to contractor is payable to contractor is US$252,403US$252,403..

(7.2115% x 100(7.2115% x 100,000 barrels x US$35.00).,000 barrels x US$35.00).

If the crude oil classified as If the crude oil classified as ‘‘Old OilOld Oil’’,, (crude oil produced following the (crude oil produced following the firstfirst 60 months since commencement of production), then the DMO Fee 60 months since commencement of production), then the DMO Fee payable to contractor per barrel refers to the Contract.payable to contractor per barrel refers to the Contract. LetLet’’s say the DMO s say the DMO Fee per barrel is 10%, the DMO Fee is Fee per barrel is 10%, the DMO Fee is US$25,240.US$25,240.

(7.2115% x 100,000 barrels x US$3.50).(7.2115% x 100,000 barrels x US$3.50).

In December, adjustment required to be aligned with PSC.In December, adjustment required to be aligned with PSC.

Lifting & SharingLifting & Sharing

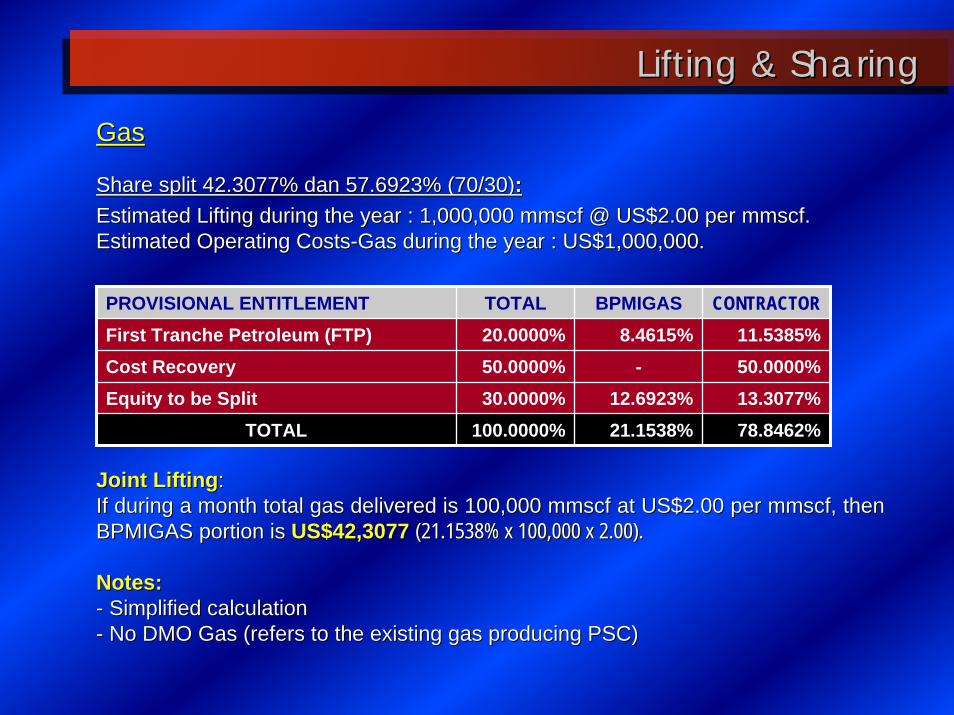

GasGas

Share split 42.3077% Share split 42.3077% dandan 57.6923% (70/30)57.6923% (70/30)::Estimated Lifting during the year : 1,000,000 Estimated Lifting during the year : 1,000,000 mmscfmmscf @ US$2.00 per @ US$2.00 per mmscfmmscf..Estimated Operating CostsEstimated Operating Costs--Gas during the year : US$1,000,000.Gas during the year : US$1,000,000.

Lifting & SharingLifting & Sharing

PROVISIONAL ENTITLEMENT TOTAL BPMIGAS CONTRACTORFirst Tranche Petroleum (FTP) 20.0000% 8.4615% 11.5385%Cost Recovery 50.0000% - 50.0000%Equity to be Split 30.0000% 12.6923% 13.3077%

TOTAL 100.0000% 21.1538% 78.8462%

Joint LiftingJoint Lifting::If during a month total gas delivered is 100,000 If during a month total gas delivered is 100,000 mmscfmmscf at US$2.00 per at US$2.00 per mmscfmmscf, then , then BPMIGAS portion is BPMIGAS portion is US$42,3077US$42,3077 (21.1538% x 100,000 x 2.00).(21.1538% x 100,000 x 2.00).

Notes:Notes:-- Simplified calculationSimplified calculation-- No DMO Gas (refers to the existing gas producing PSC)No DMO Gas (refers to the existing gas producing PSC)

Sales Agreement - 2

Sales Agreement - 2

Sales Agreement - 1

Sales Agreement - 1

Field - 1Field - 1

Field - 3Field - 3

Field - 5Field - 5

Field - 2Field - 2

Field - 4Field - 4

PSCBlock “A”

PSCBlock

“B”

PSCBlock

“C”

LNGPlantLNGPlant

LNGPlantLNGPlant

LNGBuyerLNGLNG

BuyerBuyer

LNGBuyerLNGLNG

BuyerBuyer

a. Sales Proceedsb. LNG Costs:

- Debt Service- Processing Costs- Transportation Costs- Administrative Costs

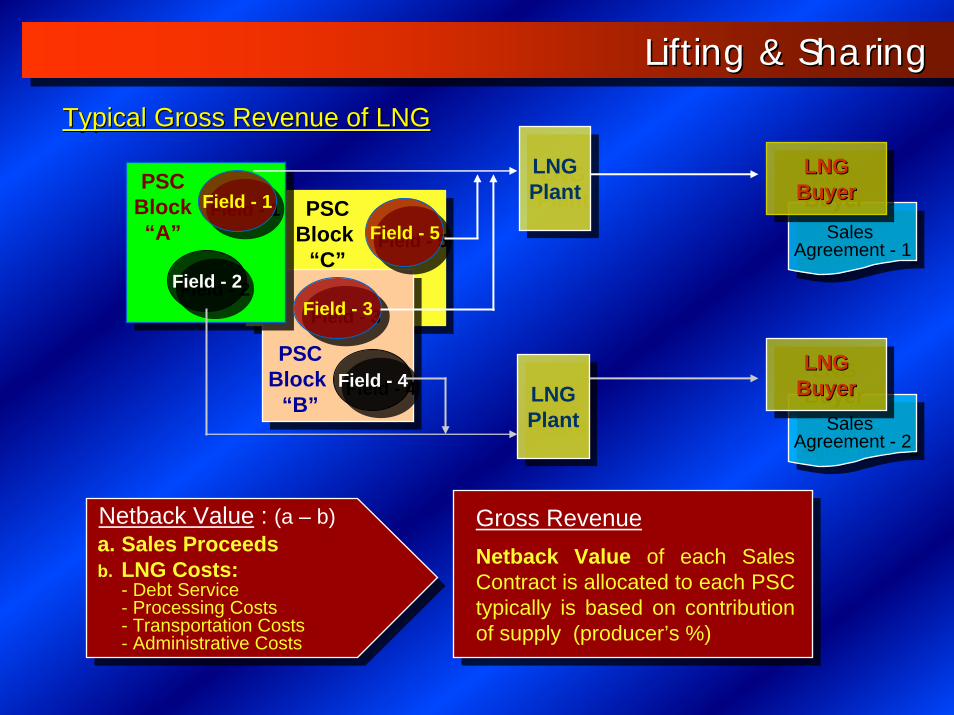

Netback Value : (a – b)

Netback Value of each Sales Contract is allocated to each PSC typically is based on contribution of supply (producer’s %)

Gross Revenue

Typical Gross Revenue of LNGTypical Gross Revenue of LNG

Lifting & SharingLifting & Sharing

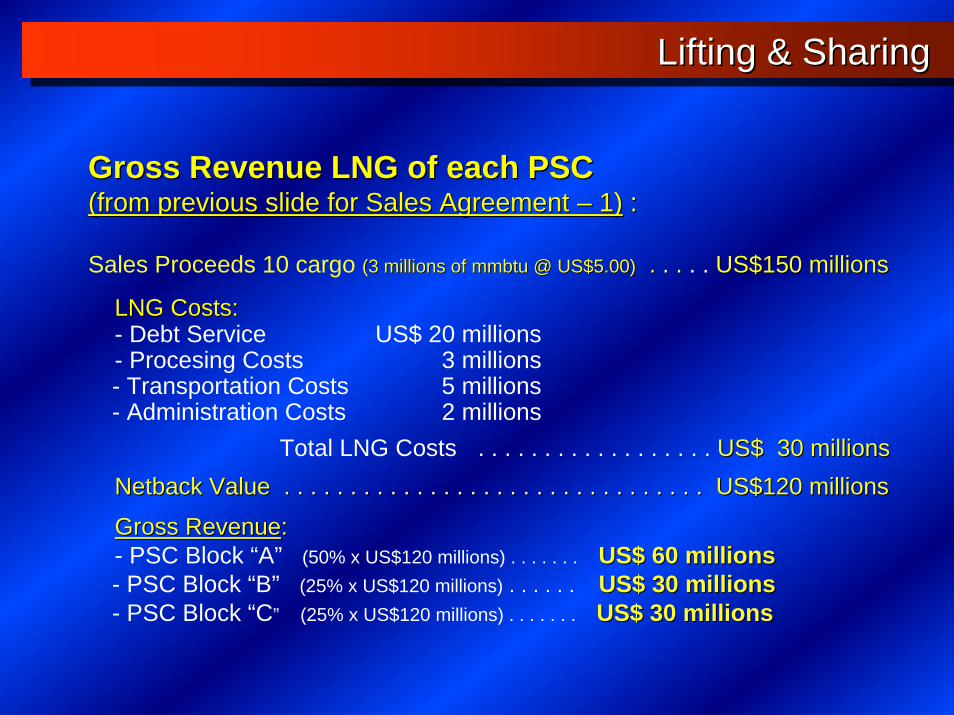

Gross Revenue LNG of each PSCGross Revenue LNG of each PSC(from previous slide for Sales Agreement (from previous slide for Sales Agreement –– 1)1) ::

Sales Proceeds 10 cargo (3 millions of (3 millions of mmbtummbtu @ US$5.00)@ US$5.00) . . . .. . . . US$150 millionsUS$150 millions

LNG Costs:LNG Costs:- Debt Service US$ 20 millions- Procesing Costs 3 millions- Transportation Costs 5 millions- Administration Costs 2 millions

Total LNG Costs . . . . . . . . . . . . . . . . . . US$ 30 millionsUS$ 30 millionsNetback Value Netback Value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . US$120 millionsUS$120 millions

Gross RevenueGross Revenue::- PSC Block “A” (50% x US$120 millions) . . . . . . . US$ 60 millionsUS$ 60 millions- PSC Block “B” (25% x US$120 millions) . . . . . . US$ 30 millionsUS$ 30 millions- PSC Block “C” (25% x US$120 millions) . . . . . . . US$ 30 millionsUS$ 30 millions

Lifting & SharingLifting & Sharing

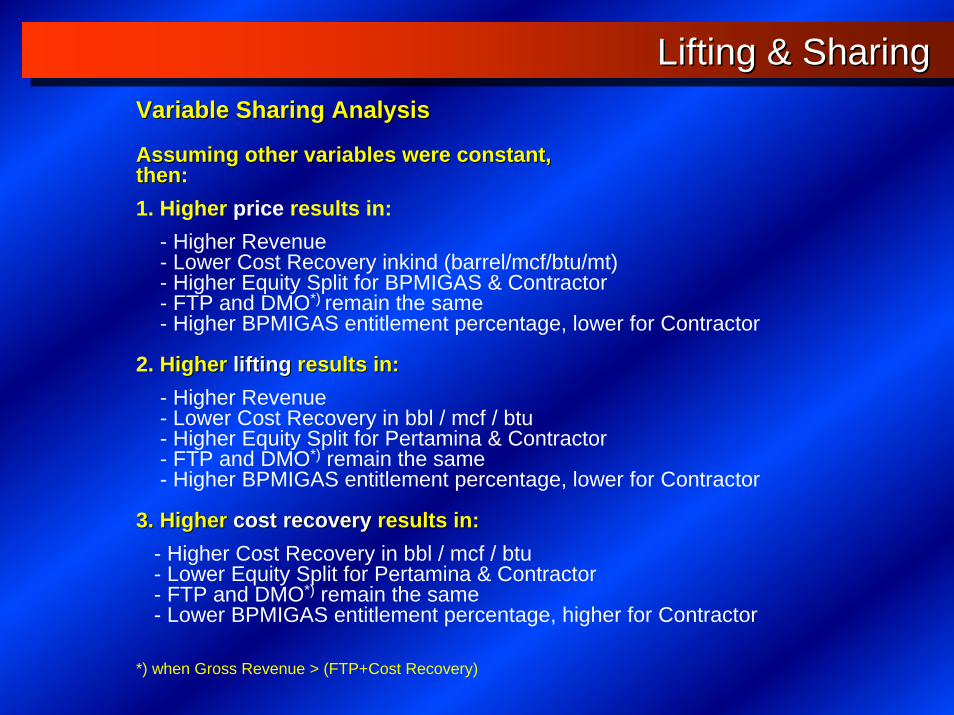

Variable Sharing AnalysisVariable Sharing Analysis

Assuming other variables were constant,Assuming other variables were constant,thenthen:1. Higher price results in:

- Higher Revenue- Lower Cost Recovery inkind (barrel/mcf/btu/mt)- Higher Equity Split for BPMIGAS & Contractor- FTP and DMO*) remain the same- Higher BPMIGAS entitlement percentage, lower for Contractor

2. Higher Higher liftinglifting results in:results in:- Higher Revenue- Lower Cost Recovery in bbl / mcf / btu- Higher Equity Split for Pertamina & Contractor- FTP and DMO*) remain the same- Higher BPMIGAS entitlement percentage, lower for Contractor

3. Higher 3. Higher cost recoverycost recovery results in:results in:- Higher Cost Recovery in bbl / mcf / btu- Lower Equity Split for Pertamina & Contractor- FTP and DMO*) remain the same- Lower BPMIGAS entitlement percentage, higher for Contractor

*) when Gross Revenue > (FTP+Cost Recovery)

Lifting & SharingLifting & Sharing

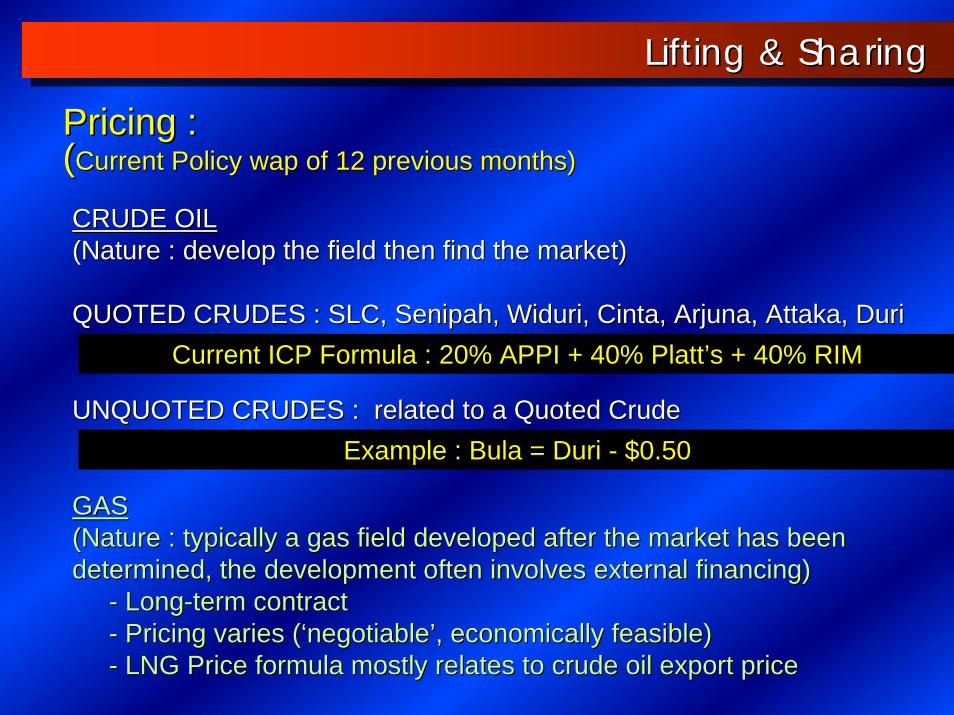

Current ICP Formula : 20% APPI + 40% Platt’s + 40% RIM

CRUDE OILCRUDE OIL(Nature : develop the field then find the market)(Nature : develop the field then find the market)

QUOTED CRUDES : SLC, Senipah, Widuri, Cinta, Arjuna, Attaka, QUOTED CRUDES : SLC, Senipah, Widuri, Cinta, Arjuna, Attaka, DuriDuri

UNQUOTED CRUDES : related to a Quoted CrudeUNQUOTED CRUDES : related to a Quoted Crude

GASGAS(Nature : typically a gas field developed after the market has b(Nature : typically a gas field developed after the market has been een determined, the development often involves external financing)determined, the development often involves external financing)

-- LongLong--term contract term contract -- Pricing varies (Pricing varies (‘‘negotiablenegotiable’’, economically feasible), economically feasible)-- LNG Price formula mostly relates to crude oil export priceLNG Price formula mostly relates to crude oil export price

Example : Bula = Duri - $0.50

Pricing : Pricing : ((Current Policy Current Policy wapwap of 12 previous months) of 12 previous months)

Lifting & SharingLifting & Sharing

FIELD - 6FIELD FIELD -- 66

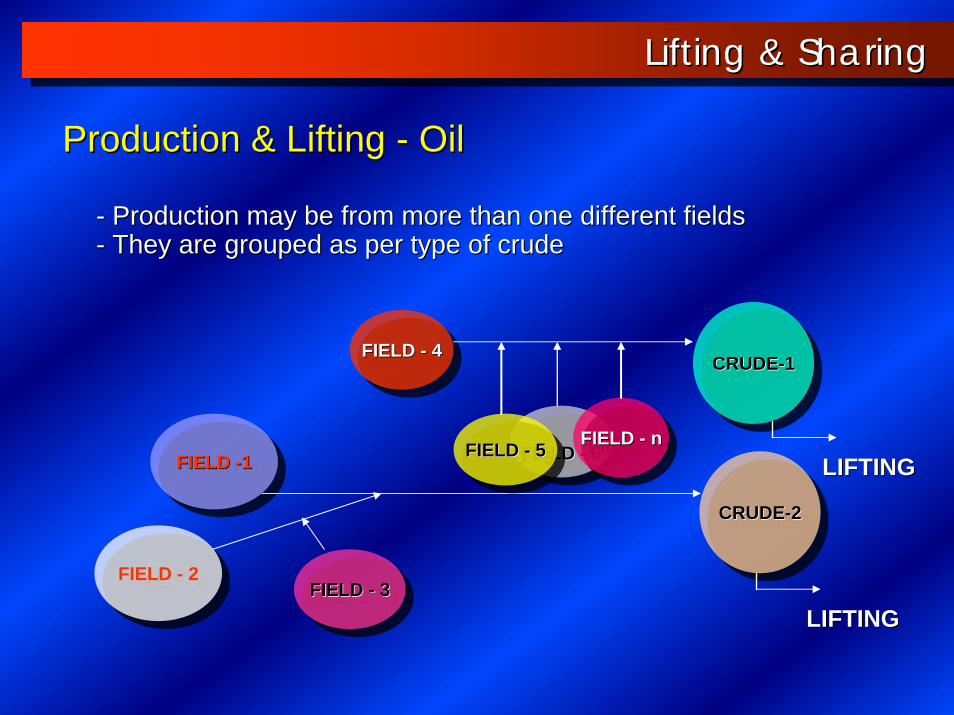

-- Production may be from more than one different fields Production may be from more than one different fields -- They are grouped as per type of crude They are grouped as per type of crude

FIELD -1FIELD FIELD --11

FIELD - 3FIELD FIELD -- 33FIELD - 2FIELD - 2

CRUDE-2CRUDECRUDE--22

LIFTINGLIFTING

CRUDE-1CRUDECRUDE--11FIELD - 4FIELD FIELD -- 44

FIELD - 5FIELD FIELD -- 55 FIELD - nFIELD FIELD -- nnLIFTINGLIFTING

Production & Lifting Production & Lifting -- OilOil

Lifting & SharingLifting & Sharing

FIELD - 6FIELD FIELD -- 66

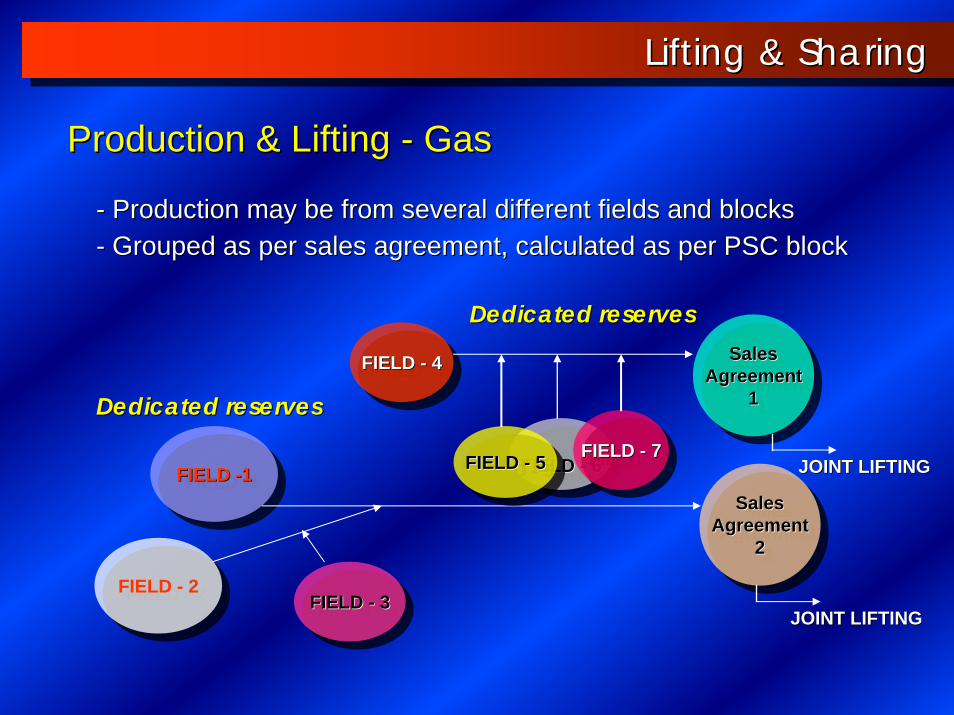

-- Production may be from several different fields and blocksProduction may be from several different fields and blocks-- Grouped as per sales agreement, calculated as per PSC block Grouped as per sales agreement, calculated as per PSC block

FIELD -1FIELD FIELD --11

FIELD - 3FIELD FIELD -- 33FIELD - 2FIELD FIELD -- 22

SalesAgreement

2

SalesSalesAgreementAgreement

22

JOINT LIFTINGJOINT LIFTING

SalesAgreement

1

SalesSalesAgreementAgreement

11FIELD - 4FIELD FIELD -- 44

FIELD - 5FIELD FIELD -- 55 FIELD - 7FIELD FIELD -- 77JOINT LIFTINGJOINT LIFTING

Dedicated reservesDedicated reserves

Dedicated reservesDedicated reserves

Production & Lifting Production & Lifting -- GasGas

Lifting & SharingLifting & Sharing

EXPENDITURES :EXPENDITURES :EXPENDITURES :

LIFTINGLIFTINGLIFTING

EXPLORATION &DEVELOPMENT

- G&G Studies- Drillings- Explor. Administration

EXPLORATION &DEVELOPMENT

- G&G Studies- Drillings- Explor. Administration

PRODUCTION- Direct Prod Exp - Oil - Direct Prod Exp - Gas- Gas Processing- Utilities & Auxiliaies- Field Office, Services & General Admin

PRODUCTION- Direct Prod Exp - Oil - Direct Prod Exp - Gas- Gas Processing- Utilities & Auxiliaies- Field Office, Services & General Admin

GENERAL & ADMINISTRATION

- Finance & Admin.- Engineering Services- Material Services- Transportation Costs- Personal Expenses- Public Relation- Community Devel- Gen.Office Expenses- Home Office O/H- Interest on Loan

GENERAL & ADMINISTRATION

- Finance & Admin.- Engineering Services- Material Services- Transportation Costs- Personal Expenses- Public Relation- Community Devel- Gen.Office Expenses- Home Office O/H- Interest on Loan

CAPITALCOST

CAPITALCAPITALCOSTCOST

COSTRECOVERY

COSTCOSTRECOVERYRECOVERYGROSS REVENUEGROSS REVENUEGROSS REVENUE

PRICEPRICEPRICE

Contractor ShareIndonesia Share

Contractor ShareContractor ShareIndonesia ShareIndonesia Share

DEPRECIATIONDEPRECIATION

PRIOR YEARSPRIOR YEARSUNRECOV. COSTSUNRECOV. COSTS UNREC. COSTSUNREC. COSTSUNREC. COSTS

NON CAPITALCOST

NON CAPITALNON CAPITALCOSTCOST

OPERATING COSTSOPERATING COSTS :

Lifting & SharingLifting & Sharing

Sharing MechanismSharing Mechanism

Cost RecoveryCost Recovery

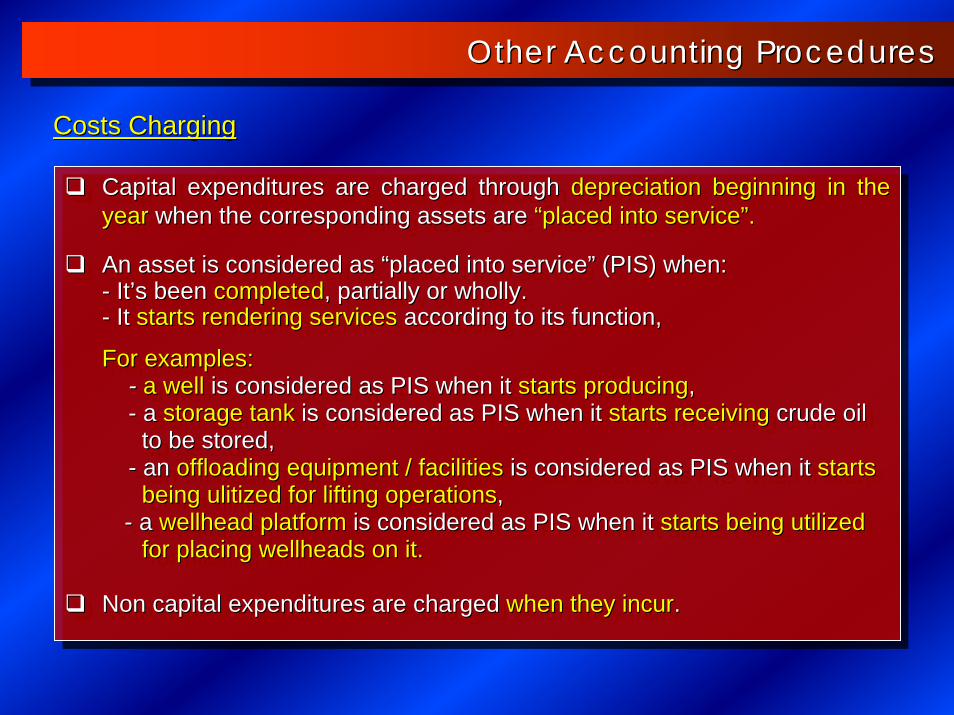

Capital expenditures are charged through depreciation beginning in the year when the corresponding assets are “placed into service”.

An asset is considered as “placed into service” (PIS) when:- It’s been completed, partially or wholly.- It starts rendering services according to its function,

For examples:- a well is considered as PIS when it starts producing,- a storage tank is considered as PIS when it starts receiving crude oil

to be stored, - an offloading equipment / facilities is considered as PIS when it starts

being ulitized for lifting operations, - a wellhead platform is considered as PIS when it starts being utilized

for placing wellheads on it.

Non capital expenditures are charged when they incur.

Capital expenditures are charged through Capital expenditures are charged through depreciation beginning in the depreciation beginning in the yearyear when the corresponding assets are when the corresponding assets are ““placed into serviceplaced into service””..

An asset is considered as An asset is considered as ““placed into serviceplaced into service”” (PIS) when:(PIS) when:-- ItIt’’s beens been completedcompleted, partially or wholly., partially or wholly.-- It It starts rendering servicesstarts rendering services according to its function,according to its function,

For examples:For examples:-- a wella well is considered as PIS when it is considered as PIS when it starts producingstarts producing,,-- a a storage tankstorage tank is considered as PIS when it is considered as PIS when it starts receivingstarts receiving crude oilcrude oil

to be stored, to be stored, -- an an offloading equipment / facilitiesoffloading equipment / facilities is considered as PIS when it is considered as PIS when it starts starts

being being ulitizedulitized for lifting operationsfor lifting operations, , -- a a wellhead platformwellhead platform is considered as PIS when it is considered as PIS when it starts being utilized starts being utilized

for placing wellheads on it.for placing wellheads on it.

Non capital expenditures are charged Non capital expenditures are charged when they incurwhen they incur..

Other Accounting ProceduresOther Accounting Procedures

Costs ChargingCosts Charging

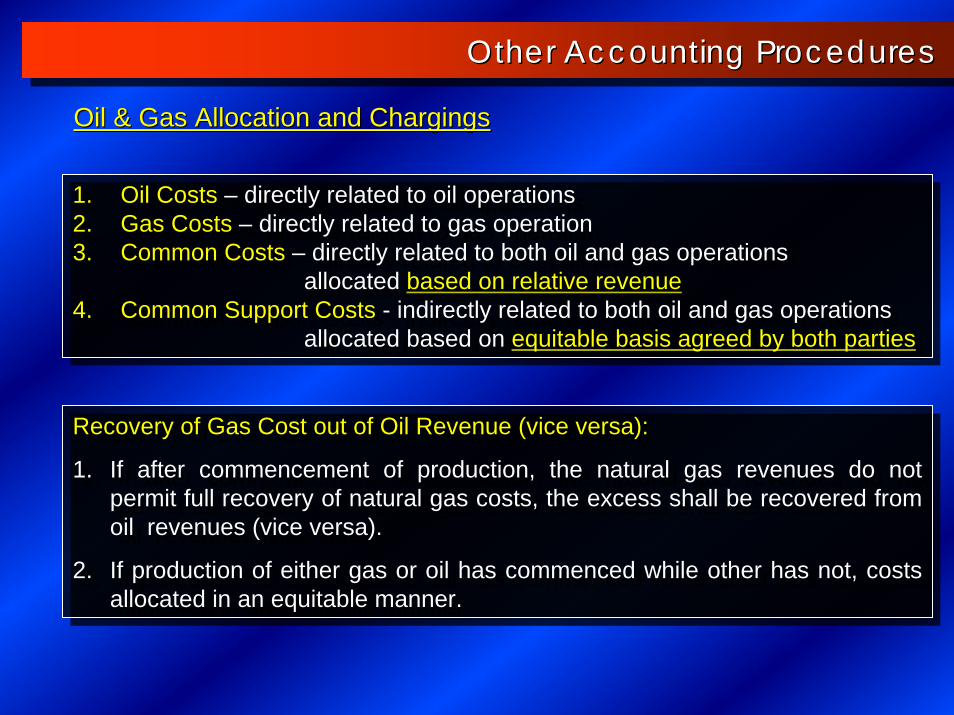

Recovery of Gas Cost out of Oil Revenue (vice versa):

1. If after commencement of production, the natural gas revenues do not permit full recovery of natural gas costs, the excess shall be recovered from oil revenues (vice versa).

2. If production of either gas or oil has commenced while other has not, costs allocated in an equitable manner.

Recovery of Gas Cost out of Oil Revenue (vice versa):

1. If after commencement of production, the natural gas revenues do not permit full recovery of natural gas costs, the excess shall be recovered from oil revenues (vice versa).

2. If production of either gas or oil has commenced while other has not, costs allocated in an equitable manner.

1. Oil Costs – directly related to oil operations2. Gas Costs – directly related to gas operation 3. Common Costs – directly related to both oil and gas operations

allocated based on relative revenue4. Common Support Costs - indirectly related to both oil and gas operations

allocated based on equitable basis agreed by both parties

1. Oil Costs – directly related to oil operations2. Gas Costs – directly related to gas operation 3. Common Costs – directly related to both oil and gas operations

allocated based on relative revenue4. Common Support Costs - indirectly related to both oil and gas operations

allocated based on equitable basis agreed by both parties

Other Accounting ProceduresOther Accounting Procedures

Oil & Gas Allocation and Oil & Gas Allocation and ChargingsChargings

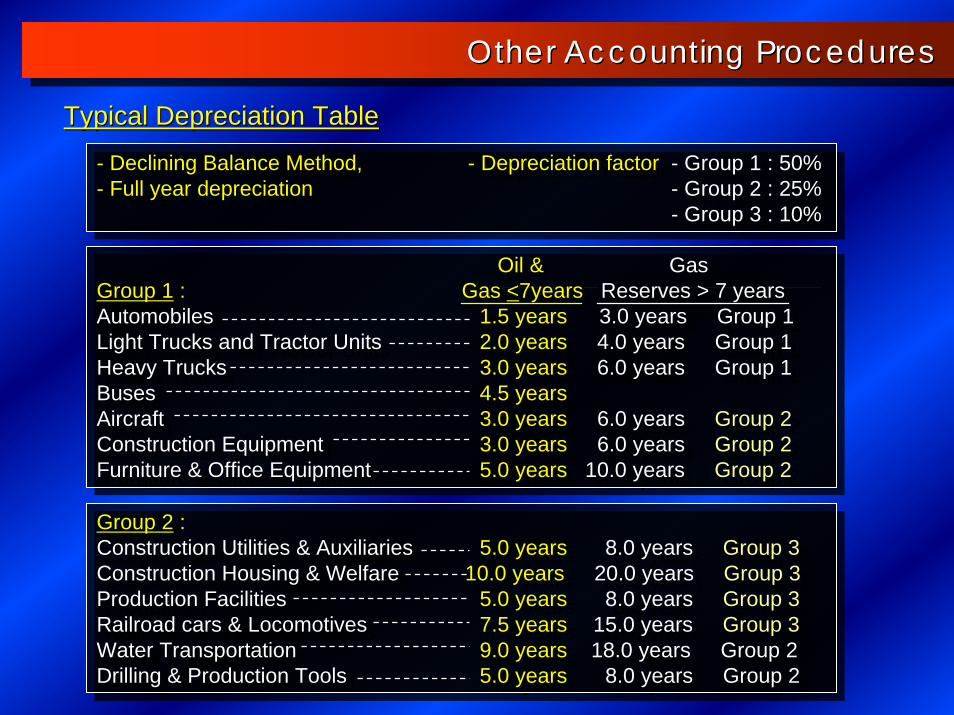

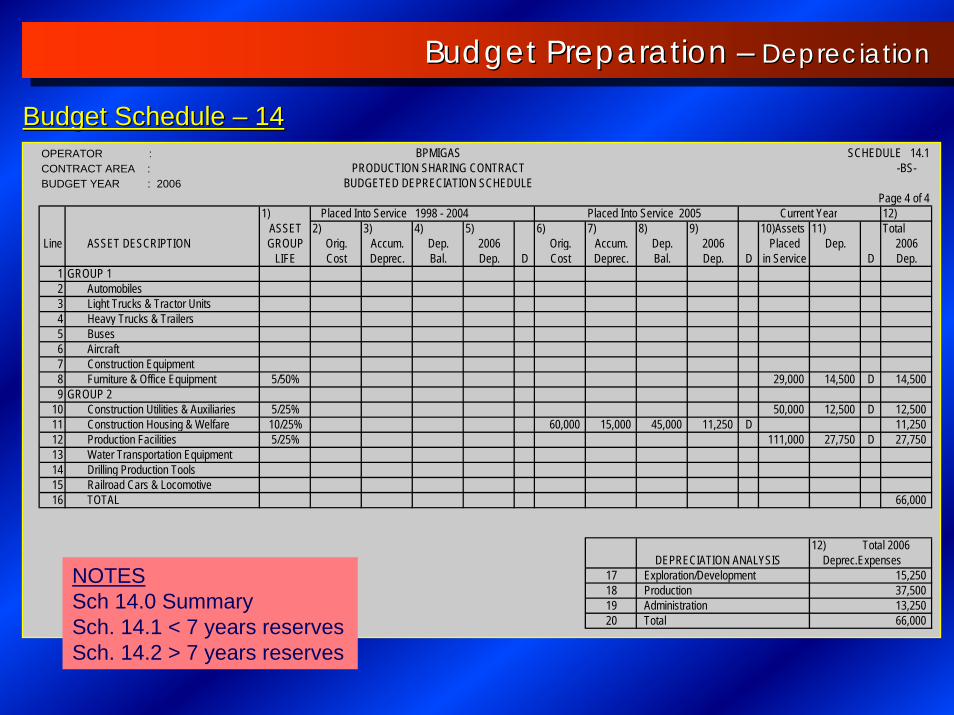

- Declining Balance Method, - Depreciation factor - Group 1 : 50%- Full year depreciation - Group 2 : 25%

- Group 3 : 10%

- Declining Balance Method, - Depreciation factor - Group 1 : 50%- Full year depreciation - Group 2 : 25%

- Group 3 : 10%

Group 2 :Construction Utilities & Auxiliaries 5.0 years 8.0 years Group 3Construction Housing & Welfare 10.0 years 20.0 years Group 3Production Facilities 5.0 years 8.0 years Group 3Railroad cars & Locomotives 7.5 years 15.0 years Group 3Water Transportation 9.0 years 18.0 years Group 2Drilling & Production Tools 5.0 years 8.0 years Group 2

Group 2 :Construction Utilities & Auxiliaries 5.0 years 8.0 years Group 3Construction Housing & Welfare 10.0 years 20.0 years Group 3Production Facilities 5.0 years 8.0 years Group 3Railroad cars & Locomotives 7.5 years 15.0 years Group 3Water Transportation 9.0 years 18.0 years Group 2Drilling & Production Tools 5.0 years 8.0 years Group 2

Oil & GasGroup 1 : Gas <7years Reserves > 7 yearsAutomobiles 1.5 years 3.0 years Group 1Light Trucks and Tractor Units 2.0 years 4.0 years Group 1Heavy Trucks 3.0 years 6.0 years Group 1Buses 4.5 yearsAircraft 3.0 years 6.0 years Group 2Construction Equipment 3.0 years 6.0 years Group 2Furniture & Office Equipment 5.0 years 10.0 years Group 2

Oil & GasGroup 1 : Gas <7years Reserves > 7 yearsAutomobiles 1.5 years 3.0 years Group 1Light Trucks and Tractor Units 2.0 years 4.0 years Group 1Heavy Trucks 3.0 years 6.0 years Group 1Buses 4.5 yearsAircraft 3.0 years 6.0 years Group 2Construction Equipment 3.0 years 6.0 years Group 2Furniture & Office Equipment 5.0 years 10.0 years Group 2

Other Accounting ProceduresOther Accounting Procedures

Typical Depreciation TableTypical Depreciation Table

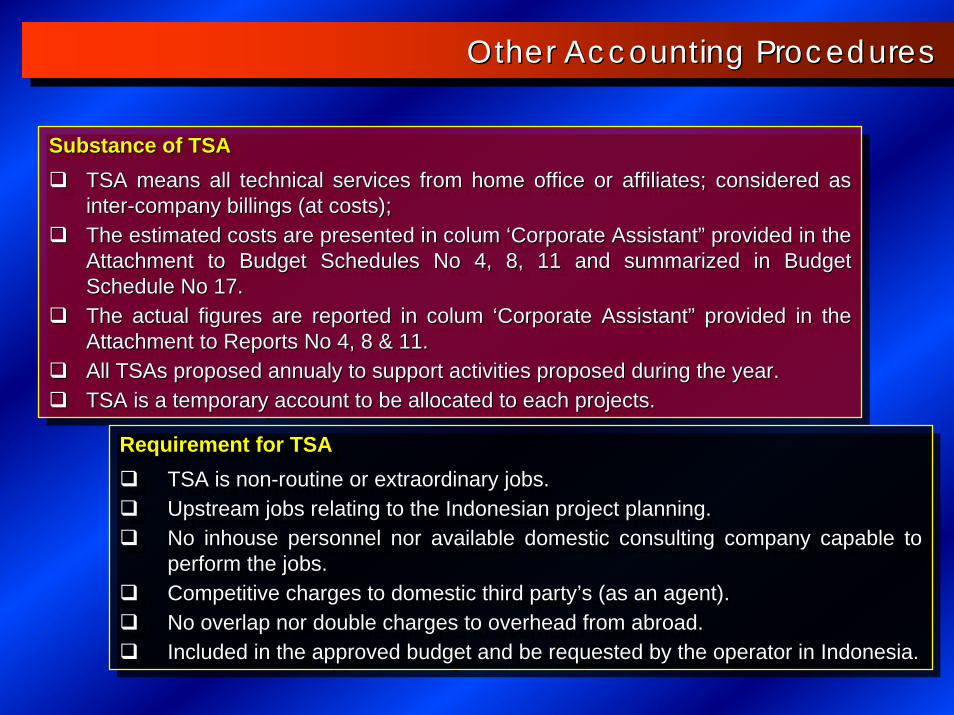

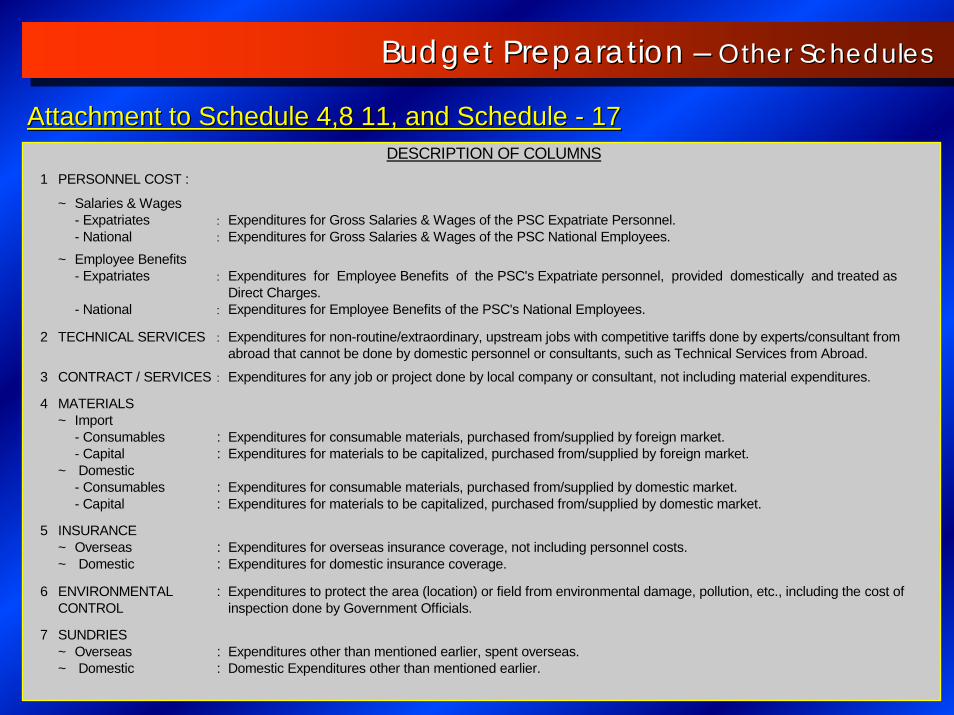

Substance of TSATSA means all technical services from home office or affiliates; considered as inter-company billings (at costs); The estimated costs are presented in colum ‘Corporate Assistant” provided in the Attachment to Budget Schedules No 4, 8, 11 and summarized in Budget Schedule No 17. The actual figures are reported in colum ‘Corporate Assistant” provided in the Attachment to Reports No 4, 8 & 11.All TSAs proposed annualy to support activities proposed during the year. TSA is a temporary account to be allocated to each projects.

Substance of TSASubstance of TSATSA means all technical services from home office or affiliates;TSA means all technical services from home office or affiliates; considered as considered as interinter--company billings (at costs); company billings (at costs); The estimated costs are presented in The estimated costs are presented in columcolum ‘‘Corporate AssistantCorporate Assistant”” provided in the provided in the Attachment to Budget Schedules No 4, 8, 11 and summarized in BudAttachment to Budget Schedules No 4, 8, 11 and summarized in Budget get Schedule No 17. Schedule No 17. The actual figures are reported in The actual figures are reported in columcolum ‘‘Corporate AssistantCorporate Assistant”” provided in the provided in the AttachmentAttachment toto Reports No 4, 8 & 11.Reports No 4, 8 & 11.All All TSAsTSAs proposed proposed annualyannualy to support activities proposed during the year. to support activities proposed during the year. TSA is a temporary account to be allocated to each projects.TSA is a temporary account to be allocated to each projects.

Requirement for TSATSA is non-routine or extraordinary jobs.Upstream jobs relating to the Indonesian project planning.No inhouse personnel nor available domestic consulting company capable to perform the jobs.Competitive charges to domestic third party’s (as an agent).No overlap nor double charges to overhead from abroad.Included in the approved budget and be requested by the operator in Indonesia.

Requirement for TSATSA is nonTSA is non--routine or extraordinary jobs.routine or extraordinary jobs.Upstream jobs relating to the Indonesian project planning.Upstream jobs relating to the Indonesian project planning.No No inhouseinhouse personnel nor available domestic consulting company capable to personnel nor available domestic consulting company capable to perform the jobs.perform the jobs.Competitive charges to domestic third partyCompetitive charges to domestic third party’’s (as an agent).s (as an agent).No overlap nor double charges to overhead from abroad.No overlap nor double charges to overhead from abroad.Included in the approved budget and be requested by the operatorIncluded in the approved budget and be requested by the operator in Indonesia.in Indonesia.

Budget Preparation Budget Preparation –– Other SchedulesOther SchedulesOther Accounting ProceduresOther Accounting Procedures

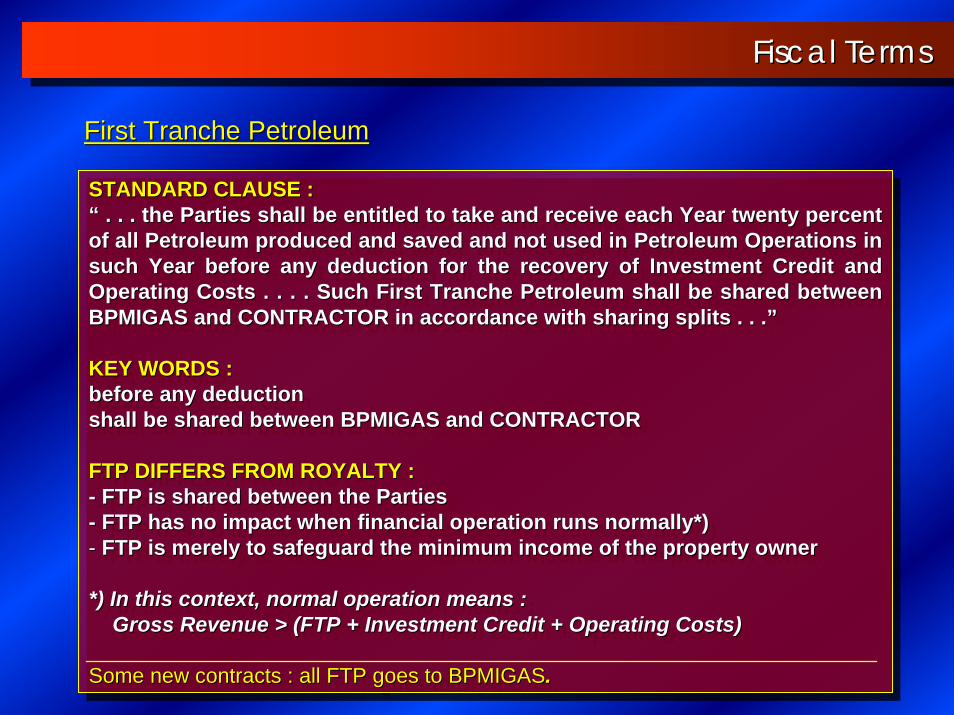

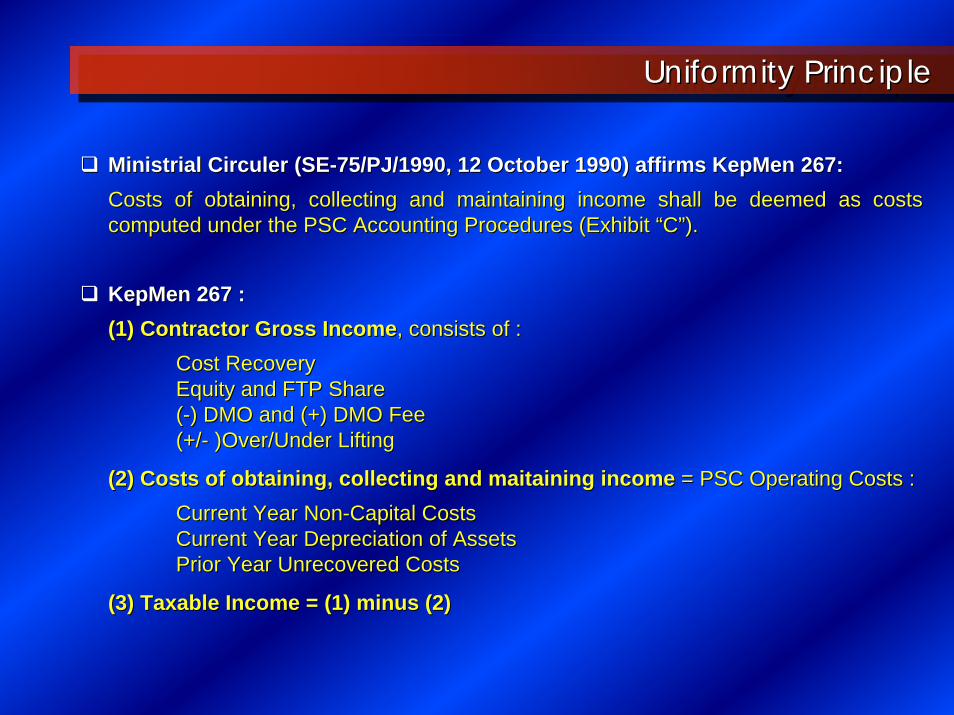

STANDARD CLAUSE :“ . . . the Parties shall be entitled to take and receive each Year twenty percent of all Petroleum produced and saved and not used in Petroleum Operations in such Year before any deduction for the recovery of Investment Credit and Operating Costs . . . . Such First Tranche Petroleum shall be shared between BPMIGAS and CONTRACTOR in accordance with sharing splits . . .”

KEY WORDS :before any deductionshall be shared between BPMIGAS and CONTRACTOR

FTP DIFFERS FROM ROYALTY :- FTP is shared between the Parties- FTP has no impact when financial operation runs normally*)- FTP is merely to safeguard the minimum income of the property owner

*) In this context, normal operation means :Gross Revenue > (FTP + Investment Credit + Operating Costs)

Some new contracts : all FTP goes to BPMIGAS.

STANDARD CLAUSE :STANDARD CLAUSE :““ . . . the Parties shall be entitled to take and receive each Ye. . . the Parties shall be entitled to take and receive each Year twenty percent ar twenty percent of all Petroleum produced and saved and not used in Petroleum Opof all Petroleum produced and saved and not used in Petroleum Operations in erations in such Year before any deduction for the recovery of Investment Crsuch Year before any deduction for the recovery of Investment Credit and edit and Operating Costs . . . . Such First Tranche Petroleum shall be shOperating Costs . . . . Such First Tranche Petroleum shall be shared between ared between BPMIGAS and CONTRACTOR in accordance with sharing splits . . .BPMIGAS and CONTRACTOR in accordance with sharing splits . . .””

KEY WORDS :KEY WORDS :before any deductionbefore any deductionshall be shared between BPMIGAS and CONTRACTORshall be shared between BPMIGAS and CONTRACTOR

FTP DIFFERS FROM ROYALTY :FTP DIFFERS FROM ROYALTY :-- FTP is shared between the PartiesFTP is shared between the Parties-- FTP has no impact when financial operation runs normally*)FTP has no impact when financial operation runs normally*)-- FTP is merely to safeguard the minimum income of the property oFTP is merely to safeguard the minimum income of the property ownerwner

*) In this context, normal operation means :*) In this context, normal operation means :Gross Revenue > (FTP + Investment Credit + Operating Costs)Gross Revenue > (FTP + Investment Credit + Operating Costs)

Some new contracts : all FTP goes to BPMIGASSome new contracts : all FTP goes to BPMIGAS..

First First TrancheTranche PetroleumPetroleum

Fiscal TermsFiscal Terms

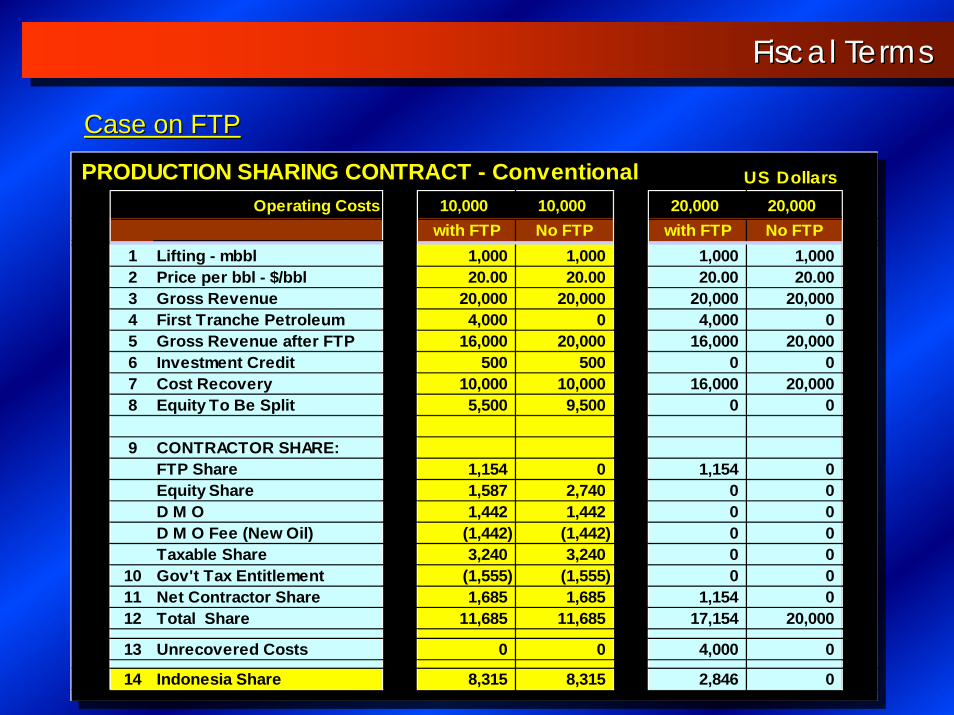

US DollarsOperating Costs 10,000 10,000 20,000 20,000

with FTP No FTP with FTP No FTP1 Lifting - mbbl 1,000 1,000 1,000 1,0002 Price per bbl - $/bbl 20.00 20.00 20.00 20.003 Gross Revenue 20,000 20,000 20,000 20,0004 First Tranche Petroleum 4,000 0 4,000 05 Gross Revenue after FTP 16,000 20,000 16,000 20,0006 Investment Credit 500 500 0 07 Cost Recovery 10,000 10,000 16,000 20,0008 Equity To Be Split 5,500 9,500 0 0

9 CONTRACTOR SHARE:FTP Share 1,154 0 1,154 0Equity Share 1,587 2,740 0 0D M O 1,442 1,442 0 0D M O Fee (New Oil) (1,442) (1,442) 0 0Taxable Share 3,240 3,240 0 0

10 Gov't Tax Entitlement (1,555) (1,555) 0 011 Net Contractor Share 1,685 1,685 1,154 012 Total Share 11,685 11,685 17,154 20,000

13 Unrecovered Costs 0 0 4,000 0

14 Indonesia Share 8,315 8,315 2,846 0

PRODUCTION SHARING CONTRACT - Conventional

Case on FTPCase on FTP

Fiscal TermsFiscal Terms

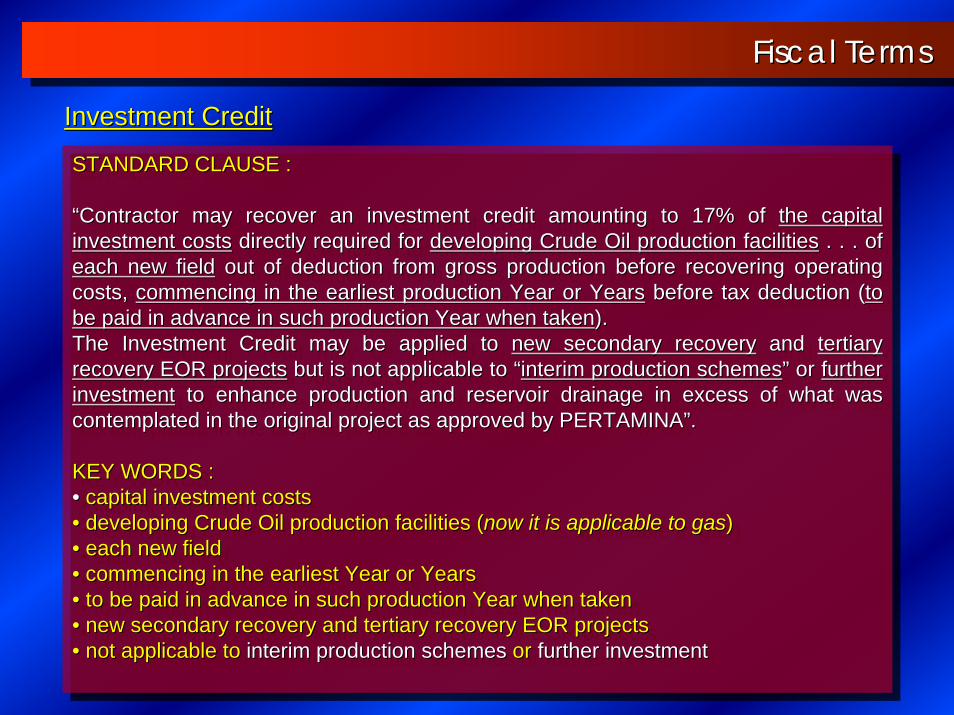

STANDARD CLAUSE :

“Contractor may recover an investment credit amounting to 17% of the capital investment costs directly required for developing Crude Oil production facilities . . . of each new field out of deduction from gross production before recovering operating costs, commencing in the earliest production Year or Years before tax deduction (to be paid in advance in such production Year when taken).The Investment Credit may be applied to new secondary recovery and tertiary recovery EOR projects but is not applicable to “interim production schemes” or further investment to enhance production and reservoir drainage in excess of what was contemplated in the original project as approved by PERTAMINA”.

KEY WORDS :• capital investment costs• developing Crude Oil production facilities (now it is applicable to gas)• each new field• commencing in the earliest Year or Years• to be paid in advance in such production Year when taken• new secondary recovery and tertiary recovery EOR projects• not applicable to interim production schemes or further investment

STANDARD CLAUSE :STANDARD CLAUSE :

““Contractor may recover an investment credit amounting to 17% of Contractor may recover an investment credit amounting to 17% of the capital the capital investment costsinvestment costs directly required for directly required for developing Crude Oil production facilitiesdeveloping Crude Oil production facilities . . . of . . . of each new fieldeach new field out of deduction from gross production before recovering operatout of deduction from gross production before recovering operating ing costs, costs, commencing in the earliest production Year or Yearscommencing in the earliest production Year or Years before tax deduction (before tax deduction (to to be paid in advance in such production Year when takenbe paid in advance in such production Year when taken).).The Investment Credit may be applied to The Investment Credit may be applied to new secondary recoverynew secondary recovery and and tertiary tertiary recovery EOR projectsrecovery EOR projects but is not applicable to but is not applicable to ““interim production schemesinterim production schemes”” or or further further investmentinvestment to enhance production and reservoir drainage in excess of what to enhance production and reservoir drainage in excess of what was was contemplated in the original project as approved by PERTAMINAcontemplated in the original project as approved by PERTAMINA””..

KEY WORDS :KEY WORDS :•• capital investment costscapital investment costs•• developing Crude Oil production facilities (developing Crude Oil production facilities (now it is applicable to gasnow it is applicable to gas))•• each new fieldeach new field•• commencing in the earliest Year or Yearscommencing in the earliest Year or Years•• to be paid in advance in such production Year when takento be paid in advance in such production Year when taken•• new secondary recovery and tertiary recovery EOR projectsnew secondary recovery and tertiary recovery EOR projects•• not applicable to not applicable to interim production schemesinterim production schemes or or further investmentfurther investment

Investment CreditInvestment Credit

Fiscal TermsFiscal Terms

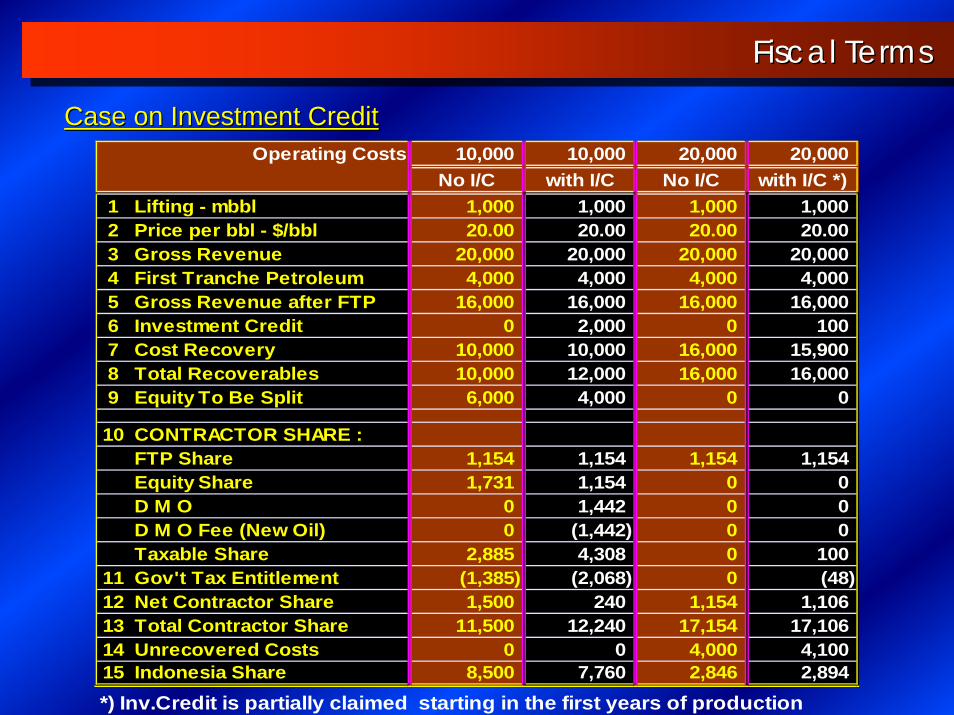

Operating Costs 10,000 10,000 20,000 20,000No I/C with I/C No I/C with I/C *)

1 Lifting - mbbl 1,000 1,000 1,000 1,0002 Price per bbl - $/bbl 20.00 20.00 20.00 20.003 Gross Revenue 20,000 20,000 20,000 20,0004 First Tranche Petroleum 4,000 4,000 4,000 4,0005 Gross Revenue after FTP 16,000 16,000 16,000 16,0006 Investment Credit 0 2,000 0 1007 Cost Recovery 10,000 10,000 16,000 15,9008 Total Recoverables 10,000 12,000 16,000 16,0009 Equity To Be Split 6,000 4,000 0 0

10 CONTRACTOR SHARE :FTP Share 1,154 1,154 1,154 1,154Equity Share 1,731 1,154 0 0D M O 0 1,442 0 0D M O Fee (New Oil) 0 (1,442) 0 0Taxable Share 2,885 4,308 0 100

11 Gov't Tax Entitlement (1,385) (2,068) 0 (48)12 Net Contractor Share 1,500 240 1,154 1,10613 Total Contractor Share 11,500 12,240 17,154 17,10614 Unrecovered Costs 0 0 4,000 4,10015 Indonesia Share 8,500 7,760 2,846 2,894*) Inv.Credit is partially claimed starting in the first years of production

Case on Investment CreditCase on Investment Credit

Fiscal TermsFiscal Terms

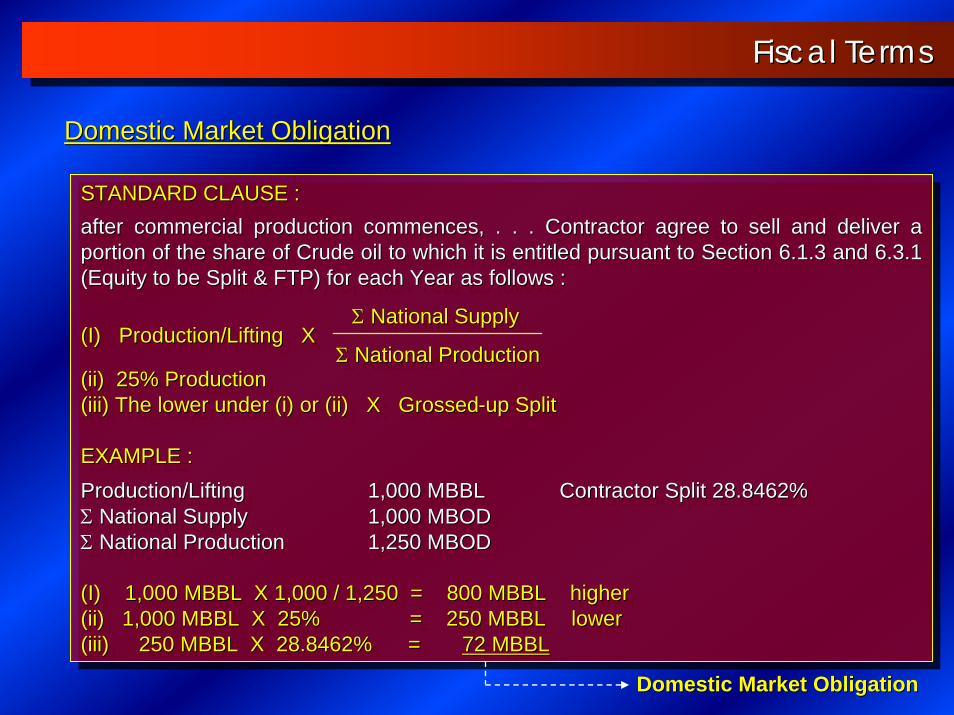

STANDARD CLAUSE :after commercial production commences, . . . Contractor agree to sell and deliver a portion of the share of Crude oil to which it is entitled pursuant to Section 6.1.3 and 6.3.1 (Equity to be Split & FTP) for each Year as follows :

Σ National Supply(I) Production/Lifting X

Σ National Production(ii) 25% Production(iii) The lower under (i) or (ii) X Grossed-up Split

EXAMPLE :Production/Lifting 1,000 MBBL Contractor Split 28.8462% Σ National Supply 1,000 MBODΣ National Production 1,250 MBOD

(I) 1,000 MBBL X 1,000 / 1,250 = 800 MBBL higher(ii) 1,000 MBBL X 25% = 250 MBBL lower(iii) 250 MBBL X 28.8462% = 72 MBBL

STANDARD CLAUSE :STANDARD CLAUSE :after commercial production commences, . . . Contractor agree toafter commercial production commences, . . . Contractor agree to sell and deliver a sell and deliver a portion of the share of Crude oil to which it is entitled pursuaportion of the share of Crude oil to which it is entitled pursuant to Section 6.1.3 and 6.3.1 nt to Section 6.1.3 and 6.3.1 (Equity to be Split & FTP) for each Year as follows :(Equity to be Split & FTP) for each Year as follows :

ΣΣ National SupplyNational Supply(I) Production/Lifting X (I) Production/Lifting X

ΣΣ National ProductionNational Production(ii) 25% Production(ii) 25% Production(iii) The lower under (i) or (ii) X Grossed(iii) The lower under (i) or (ii) X Grossed--up Splitup Split

EXAMPLE :EXAMPLE :

Production/LiftingProduction/Lifting 1,000 MBBL1,000 MBBL Contractor Split 28.8462% Contractor Split 28.8462% ΣΣ National SupplyNational Supply 1,000 MBOD1,000 MBODΣΣ National ProductionNational Production 1,250 MBOD1,250 MBOD

(I) 1,000 MBBL X 1,000 / 1,250 = 800 MBBL higher(I) 1,000 MBBL X 1,000 / 1,250 = 800 MBBL higher(ii) 1,000 MBBL X 25%(ii) 1,000 MBBL X 25% = 250 MBBL= 250 MBBL lowerlower(iii) 250 MBBL X 28.8462% = (iii) 250 MBBL X 28.8462% = 72 MBBL72 MBBL

Domestic Market ObligationDomestic Market Obligation

Domestic Market ObligationDomestic Market Obligation

Fiscal TermsFiscal Terms

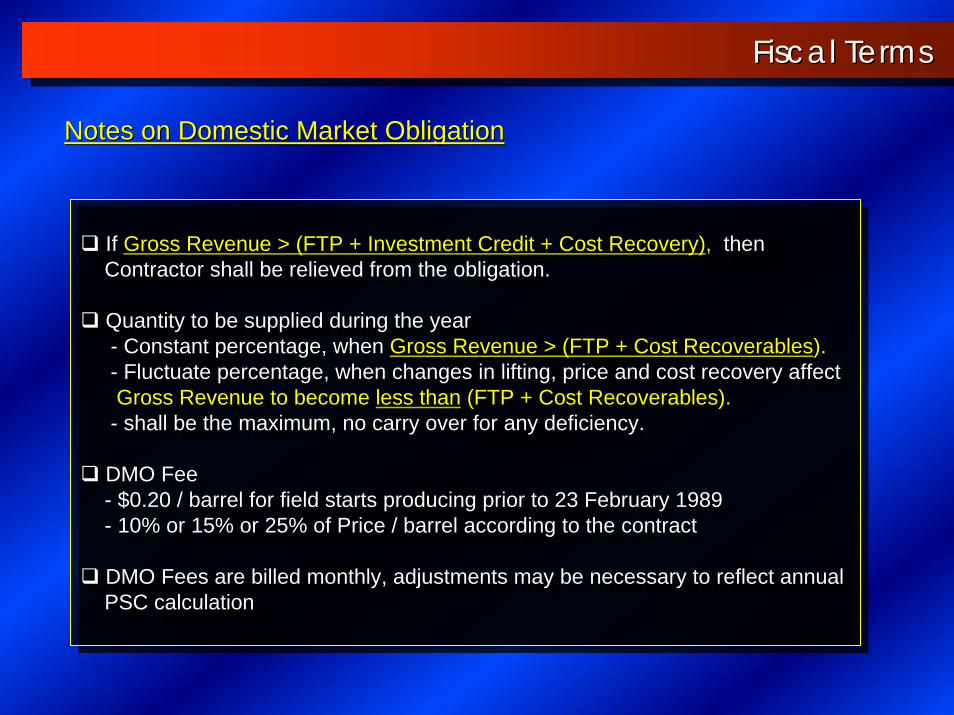

If Gross Revenue > (FTP + Investment Credit + Cost Recovery), thenContractor shall be relieved from the obligation.

Quantity to be supplied during the year- Constant percentage, when Gross Revenue > (FTP + Cost Recoverables).- Fluctuate percentage, when changes in lifting, price and cost recovery affectGross Revenue to become less than (FTP + Cost Recoverables).- shall be the maximum, no carry over for any deficiency.

DMO Fee - $0.20 / barrel for field starts producing prior to 23 February 1989- 10% or 15% or 25% of Price / barrel according to the contract

DMO Fees are billed monthly, adjustments may be necessary to reflect annualPSC calculation

If If Gross Revenue > (FTP + Investment Credit + Cost Recovery), thenthenContractor shall be relieved from the obligation.Contractor shall be relieved from the obligation.

Quantity to be supplied during the yearQuantity to be supplied during the year-- Constant percentage, when Constant percentage, when Gross Revenue > (FTP + Cost Recoverables).-- Fluctuate percentage, when changes in lifting, price and cost rFluctuate percentage, when changes in lifting, price and cost recovery affectecovery affectGross Revenue to become less than (FTP + Cost Recoverables).-- shall be the maximum, no carry over for any deficiency.shall be the maximum, no carry over for any deficiency.

DMO Fee DMO Fee -- $0.20 / barrel for field starts producing prior to 23 February $0.20 / barrel for field starts producing prior to 23 February 19891989-- 10% or 15% or 25% of Price / barrel according to the contract10% or 15% or 25% of Price / barrel according to the contract

DMO Fees are billed monthly, adjustments may be necessary to reDMO Fees are billed monthly, adjustments may be necessary to reflect annualflect annualPSC calculationPSC calculation

Notes on Domestic Market ObligationNotes on Domestic Market Obligation

Fiscal TermsFiscal Terms

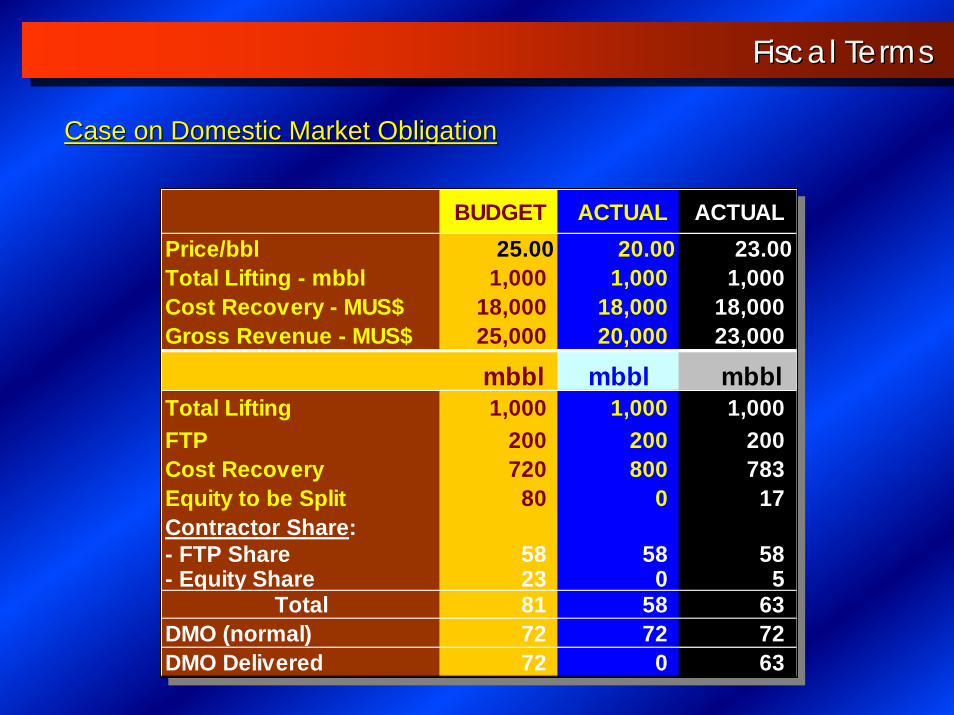

BUDGET ACTUAL ACTUALPrice/bbl 25.00 20.00 23.00Total Lifting - mbbl 1,000 1,000 1,000 Cost Recovery - MUS$ 18,000 18,000 18,000 Gross Revenue - MUS$ 25,000 20,000 23,000

mbbl mbbl mbblTotal Lifting 1,000 1,000 1,000 FTP 200 200 200 Cost Recovery 720 800 783 Equity to be Split 80 0 17 Contractor Share:- FTP Share 58 58 58- Equity Share 23 0 5

Total 81 58 63DMO (normal) 72 72 72DMO Delivered 72 0 63

Case on Domestic Market ObligationCase on Domestic Market Obligation

Fiscal TermsFiscal Terms

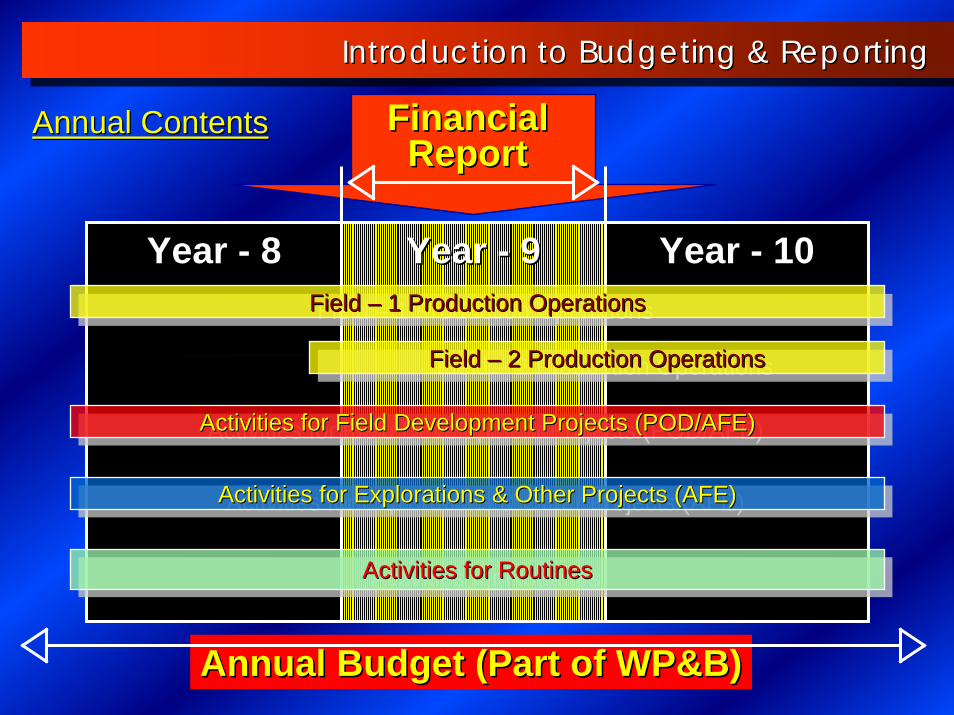

Year Year -- 88 Year Year -- 99 Year Year -- 1010

Annual Budget (Part of WP&B)Annual Budget (Part of WP&B)

Introduction to Budgeting & ReportingIntroduction to Budgeting & Reporting

FinancialFinancialReportReport

Field – 1 Production OperationsField Field –– 1 Production Operations1 Production Operations

Field – 2 Production OperationsField Field –– 2 Production Operations2 Production Operations

Activities for Field Development Projects (POD/AFE)Activities for Field Development Projects (POD/AFE)Activities for Field Development Projects (POD/AFE)

Activities for Explorations & Other Projects (AFE)Activities for Explorations & Other Projects (AFE)Activities for Explorations & Other Projects (AFE)

Activities for RoutinesActivities for RoutinesActivities for Routines

Annual ContentsAnnual Contents

Budgeting & ReportingBudgeting & Reporting

Financial Control starts from Financial Reporting.Financial Control starts from Financial Reporting.

Financial Reporting captures all activities in each contract areFinancial Reporting captures all activities in each contract area a during reporting periods, including sharing of production, preseduring reporting periods, including sharing of production, presented nted mostly in a currency unit (US Dollars).mostly in a currency unit (US Dollars).

Main Financial Reporting :Main Financial Reporting :

Annual BudgetAnnual BudgetPart of Work Program and Budget (WP&B) itemizing planned Part of Work Program and Budget (WP&B) itemizing planned activities during the year.activities during the year.

Financial Report Financial Report Reporting the actual figures of all activities approved in the Reporting the actual figures of all activities approved in the Annual Budget (WP&B), presented quarterly for monitoring & Annual Budget (WP&B), presented quarterly for monitoring & controlling purposes.controlling purposes.

Annual Budget & Financial ReportAnnual Budget & Financial Report

ContentsBudget Year Overview summarizes forecast activities during the budget year. Areas subject to considerable variation should be discussed in the overview together with the possible impact.Annual Work Program provides technical descriptions of proposed exploratory, development, exploitation and supporting activities. Maps and other supporting documents are to be attached as appropriate.Submissions, at least 3 months prior to the beginning of each calendar year,or at such other time as agreed by the parties.Revisions/ChangesBPMIGAS may propose a revision within 30 days after receipt.Details of work program may be changed, provided they do not change the general objective nor increase the approve expenditures.In the event of emergency requiring immediate actions, proper actions may be taken, and costs incurred included as operating costs.Revisions on the WP&B should be submitted to BPMIGAS in the mid budget year (no later than August).

Budgeting & ReportingBudgeting & ReportingBudgeting & Reporting

The summary of quarterly expenditures, operating costs, cost recovery, sharing of production & others based on actuals.

Legal permanent document, source of reference for actual data.

Submitted to BPMIGAS not later than 20th calendar day after quarter-end. For the 4th quarter Report, it will be necessary to submit the corrected report not later than the following 1st of March.

Inclusion of estimated expenditures for the third month of any quarter. In the next succeeding quarterly reports the adjustment to convert estimated to actuals should be made in ‘This Quarter’ figures.

Expressed in US dollars, rounded off to the nearest thousand dollars, except for Report 16 and project control reports 18 to 26 should be rounded off to the nearest US dollar amount.

Explains variances, generally when YTD variance is + 10% or more, provided that it exceeds US$500,000.

Budgeting & ReportingBudgeting & ReportingBudgeting & Reporting

The actual figures of expenditures estimated in the Work ProgramThe actual figures of expenditures estimated in the Work Program & Budget are & Budget are reported inreported in Financial Report:Financial Report:

Budgeting & ReportingBudgeting & Reporting

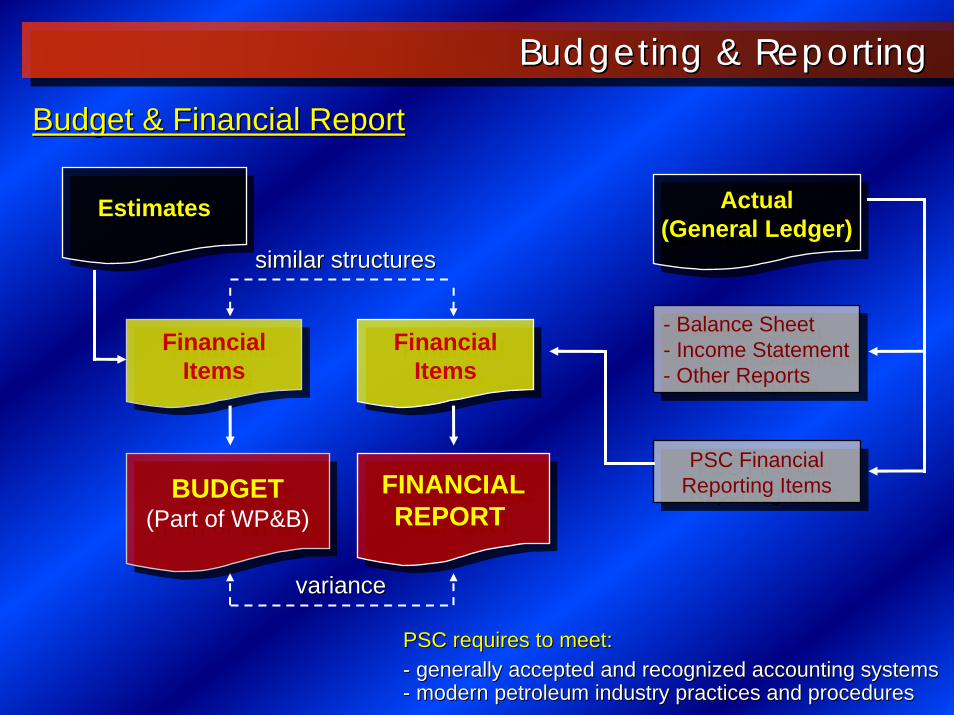

Budget & Financial ReportBudget & Financial Report

BUDGET(Part of WP&B)

BUDGET(Part of WP&B)

FINANCIALREPORT

FINANCIALREPORT

Actual(General Ledger)

Actual(General Ledger)

FinancialItems

FinancialItems

EstimatesEstimates

FinancialItems

FinancialItems

similar structuressimilar structures

variancevariance

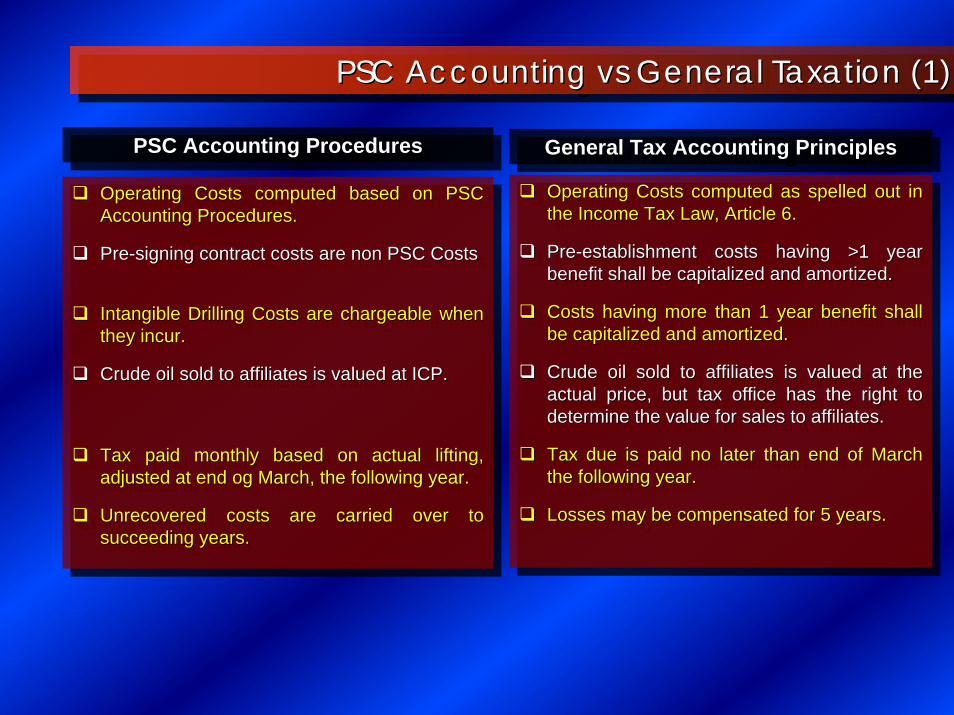

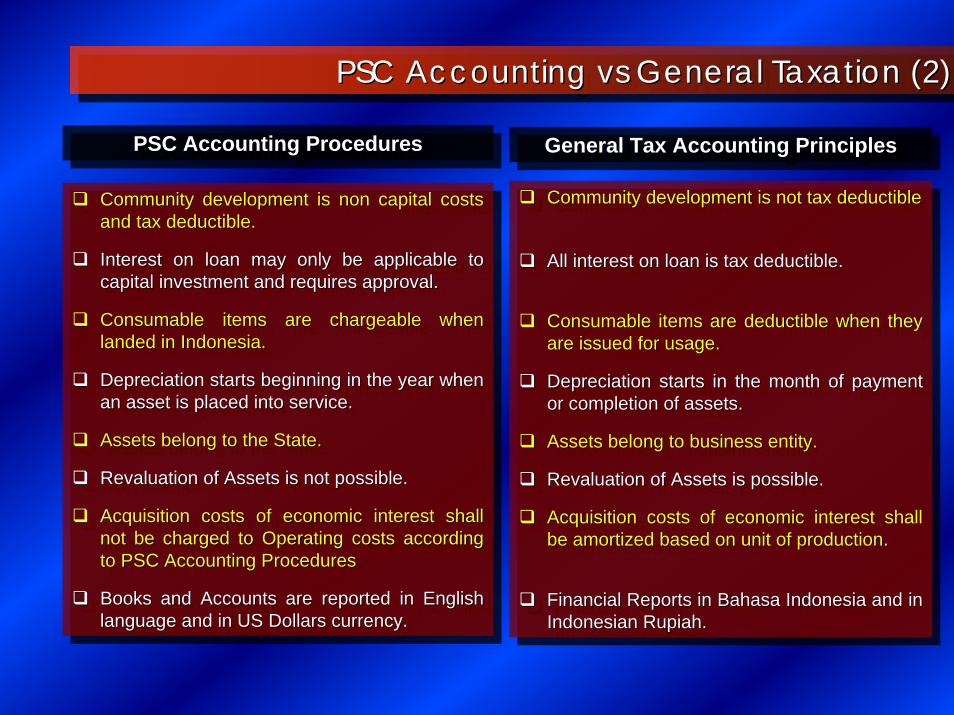

PSC requires to meet:PSC requires to meet:-- generally accepted and recognized accounting systemsgenerally accepted and recognized accounting systems-- modern petroleum industry practices and proceduresmodern petroleum industry practices and procedures

- Balance Sheet- Income Statement- Other Reports

- Balance Sheet- Income Statement- Other Reports

PSC FinancialReporting ItemsPSC Financial

Reporting Items

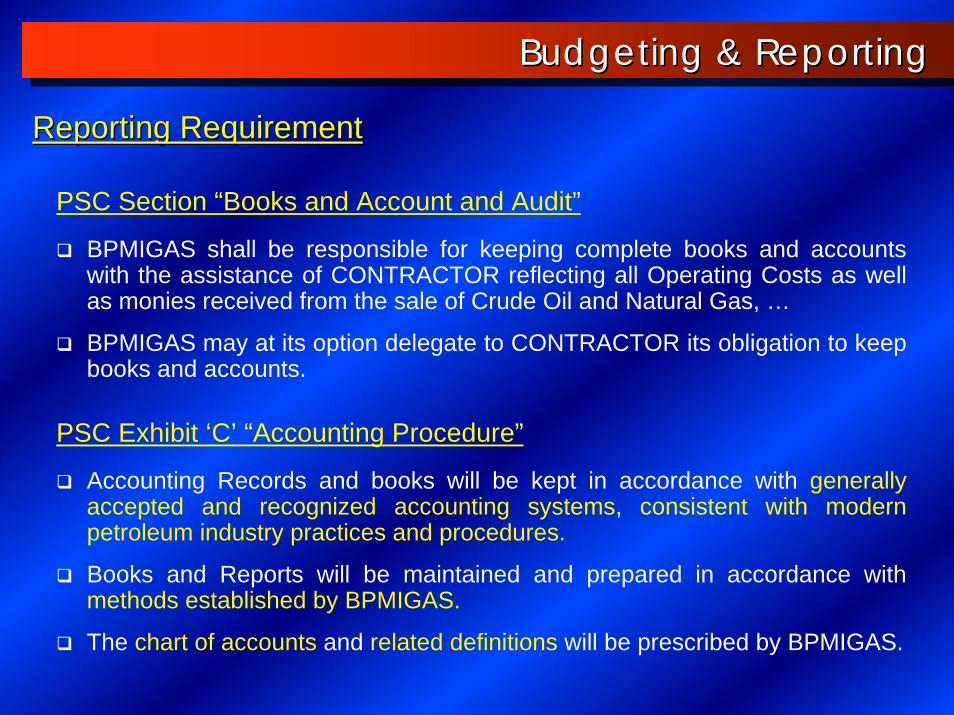

PSC Section “Books and Account and Audit”

BPMIGAS shall be responsible for keeping complete books and accounts with the assistance of CONTRACTOR reflecting all Operating Costs as well as monies received from the sale of Crude Oil and Natural Gas, …

BPMIGAS may at its option delegate to CONTRACTOR its obligation to keep books and accounts.

PSC Exhibit ‘C’ “Accounting Procedure”

Accounting Records and books will be kept in accordance with generally accepted and recognized accounting systems, consistent with modern petroleum industry practices and procedures.

Books and Reports will be maintained and prepared in accordance with methods established by BPMIGAS.

The chart of accounts and related definitions will be prescribed by BPMIGAS.

Budgeting & ReportingBudgeting & Reporting

Reporting RequirementReporting Requirement

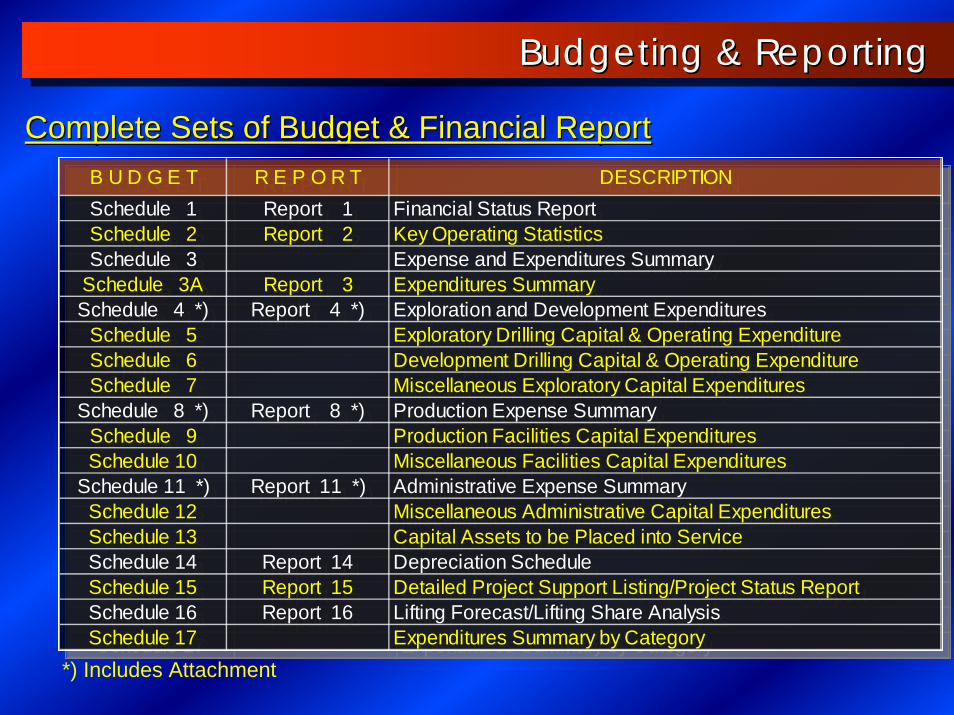

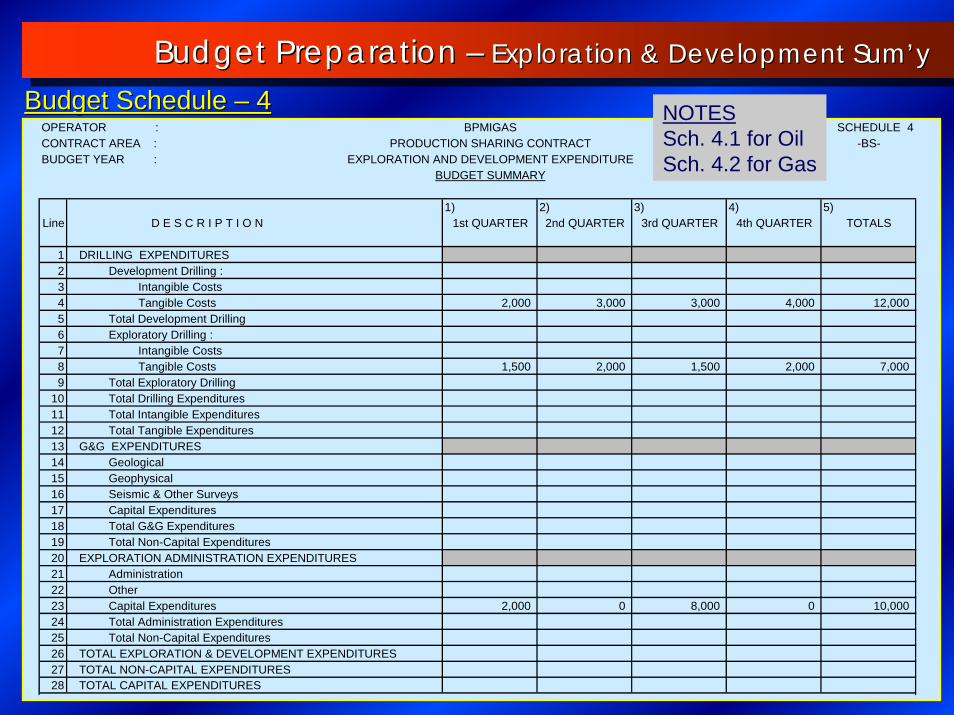

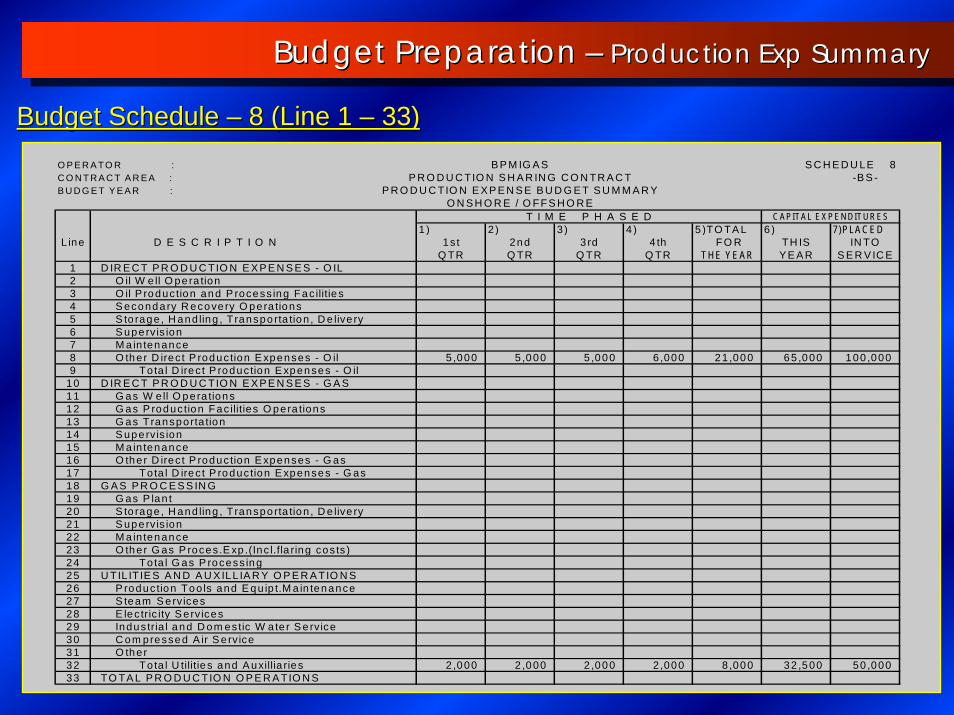

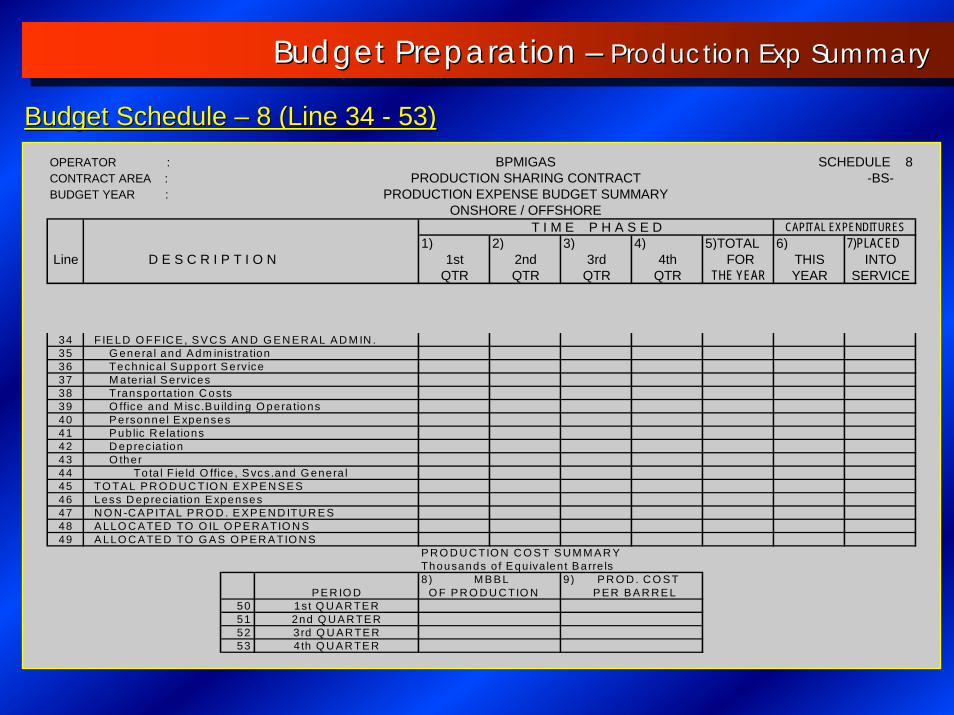

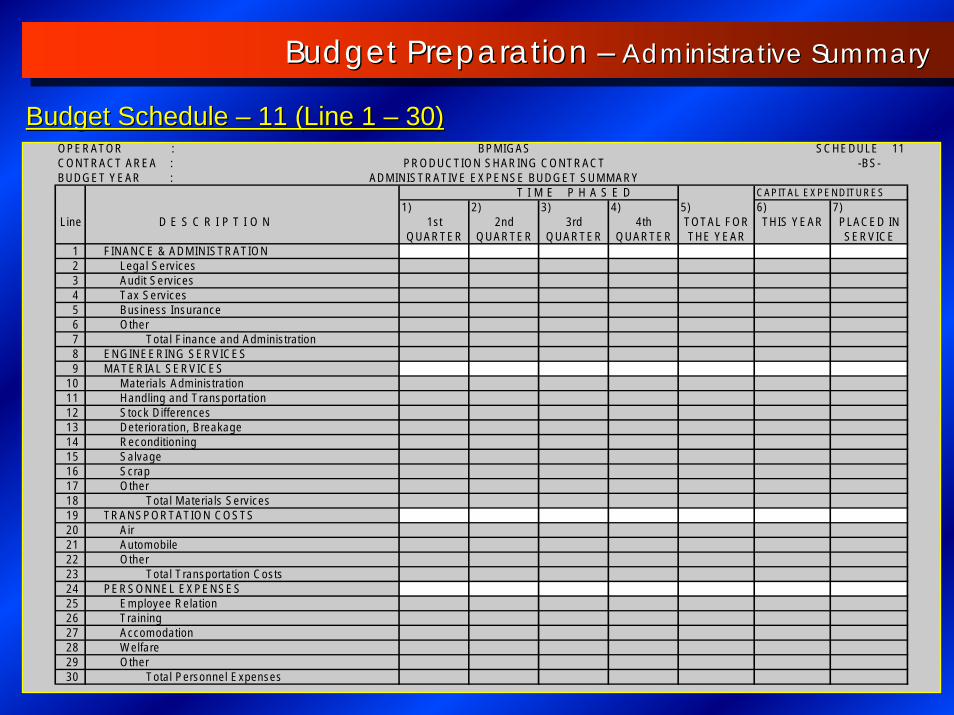

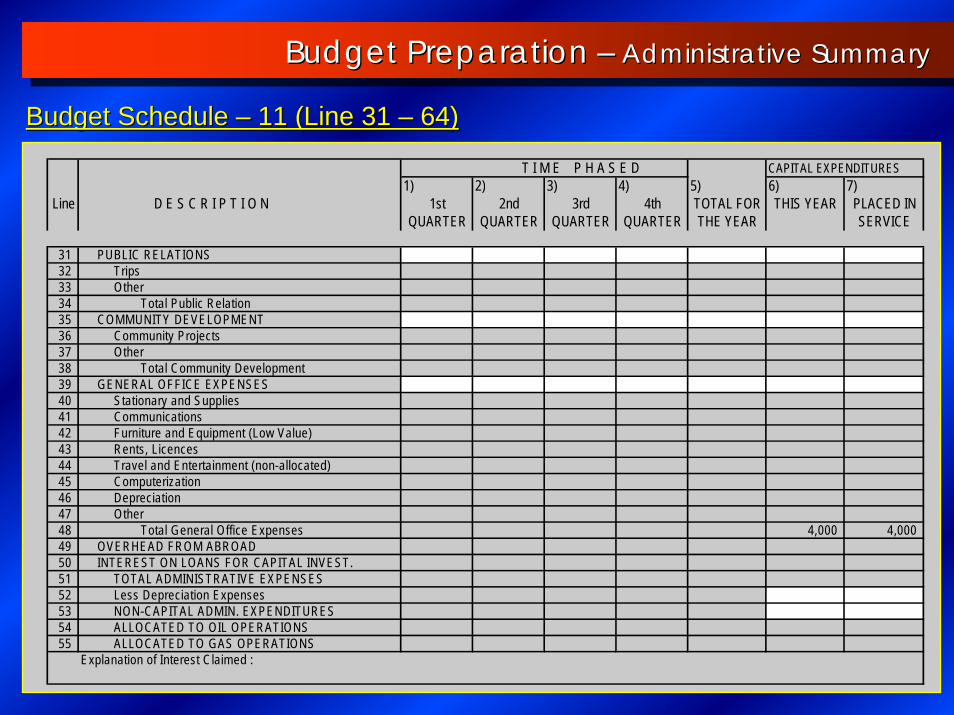

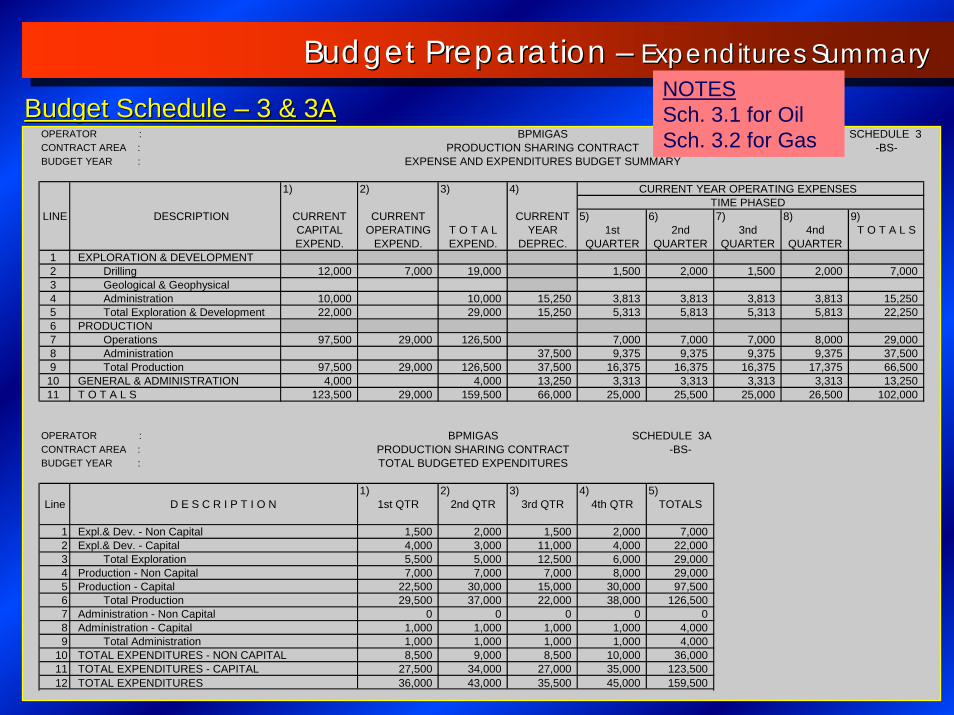

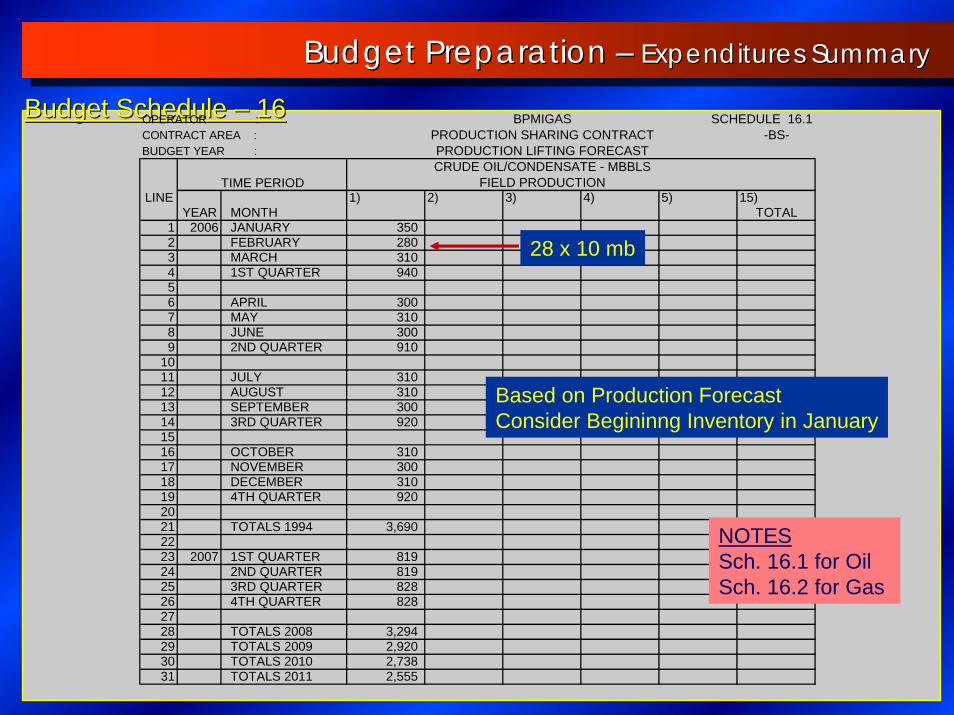

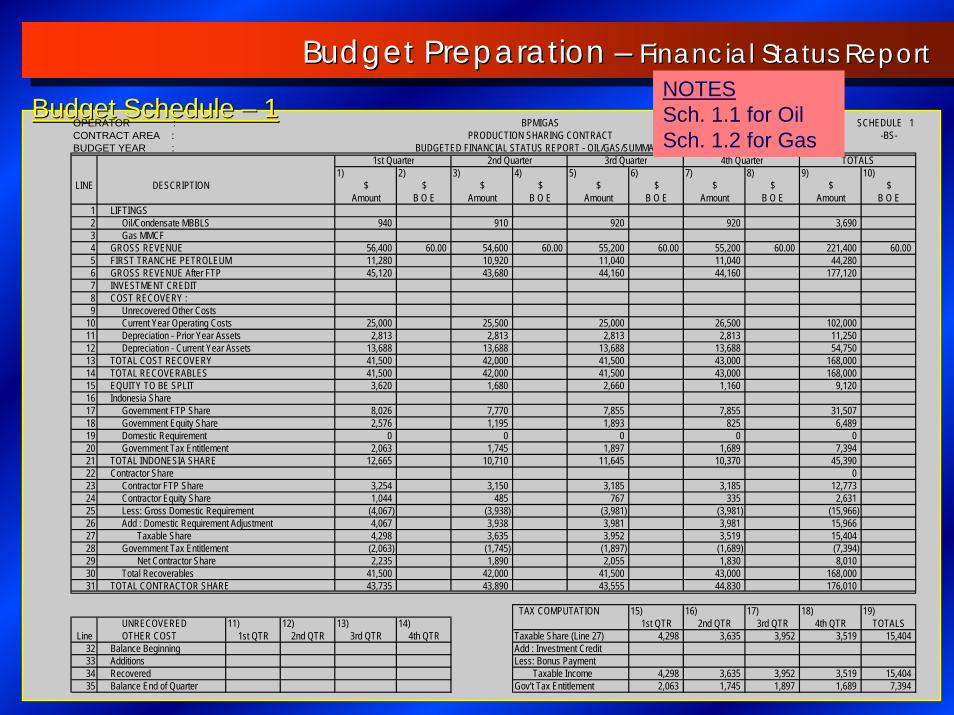

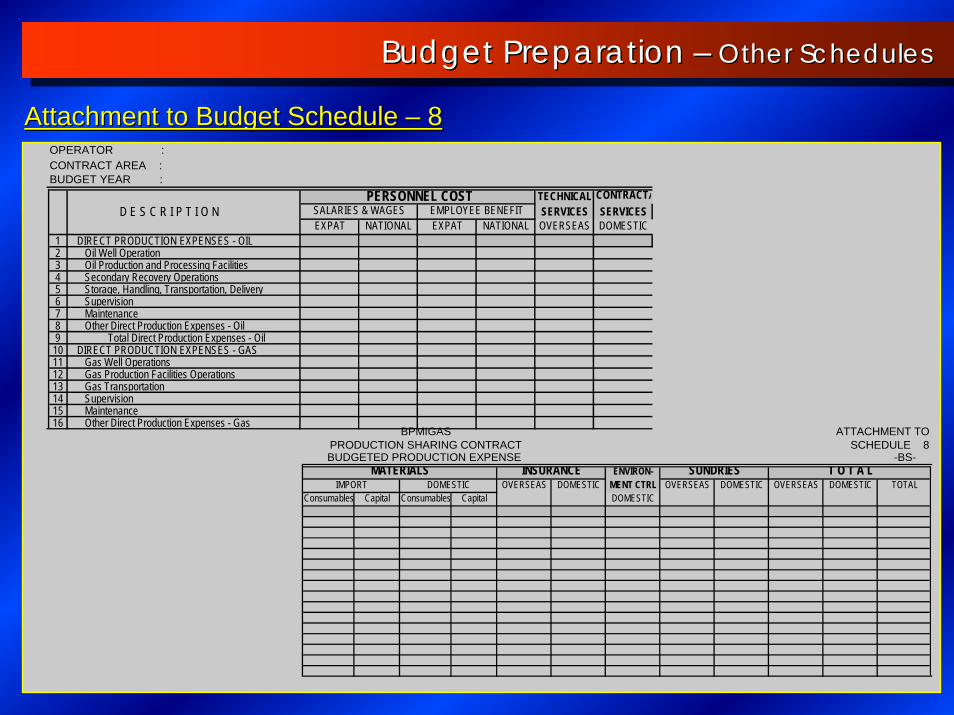

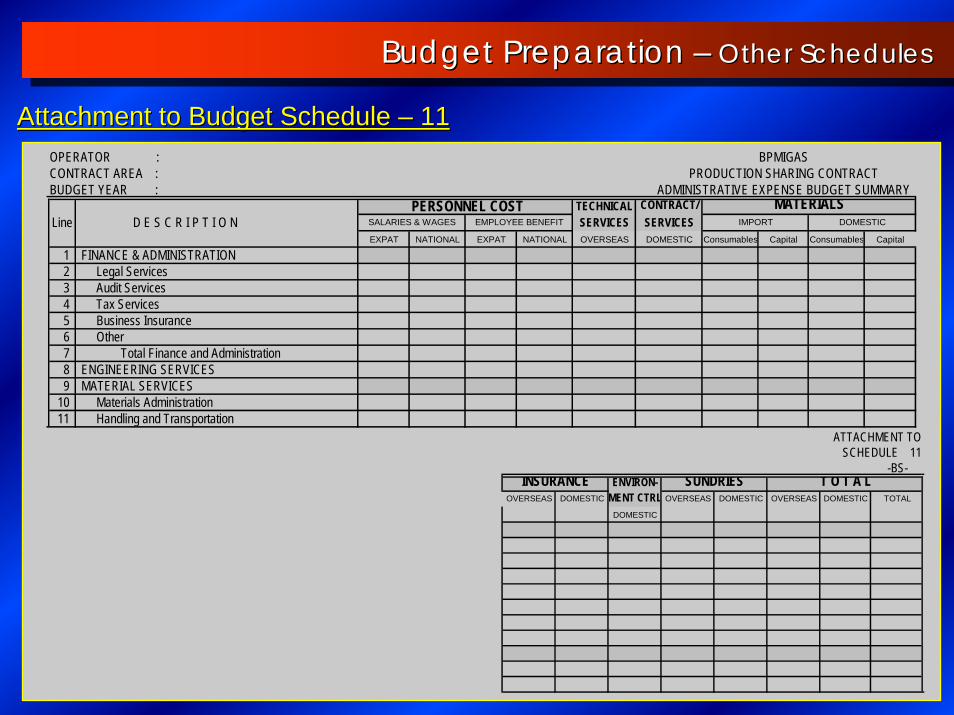

B U D G E T R E P O R T DESCRIPTIONSchedule 1 Report 1 Financial Status ReportSchedule 2 Report 2 Key Operating StatisticsSchedule 3 Expense and Expenditures Summary

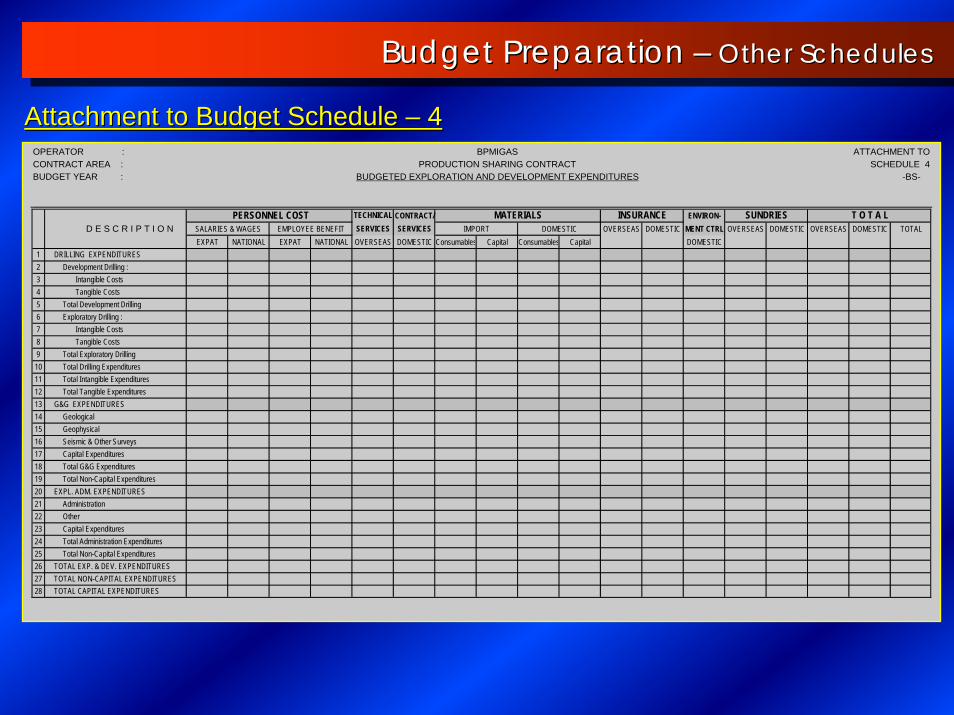

Schedule 3A Report 3 Expenditures SummarySchedule 4 *) Report 4 *) Exploration and Development Expenditures

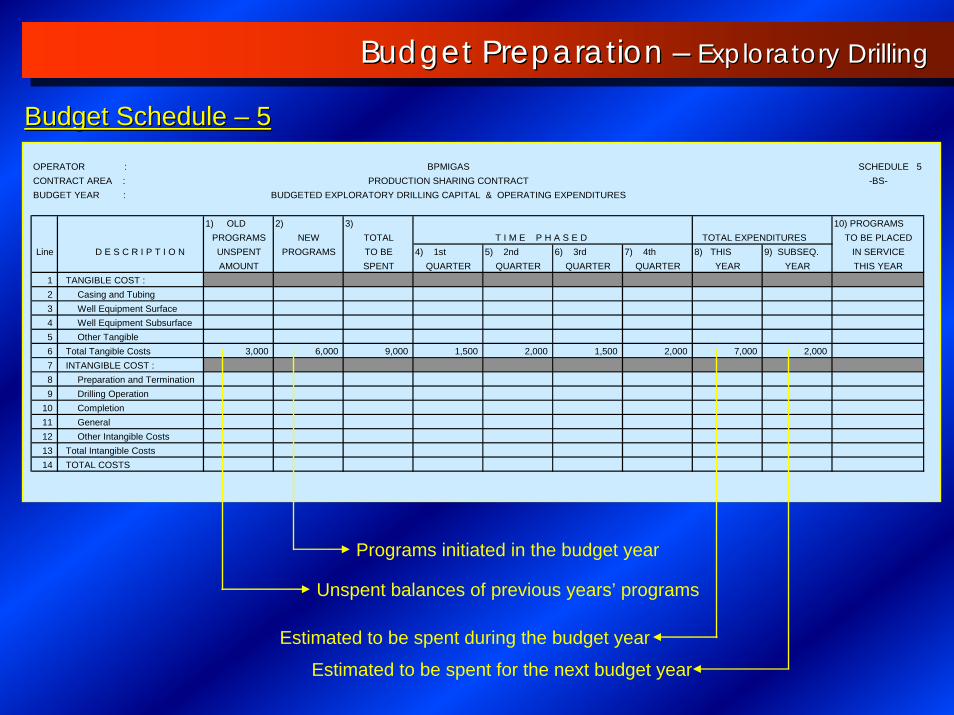

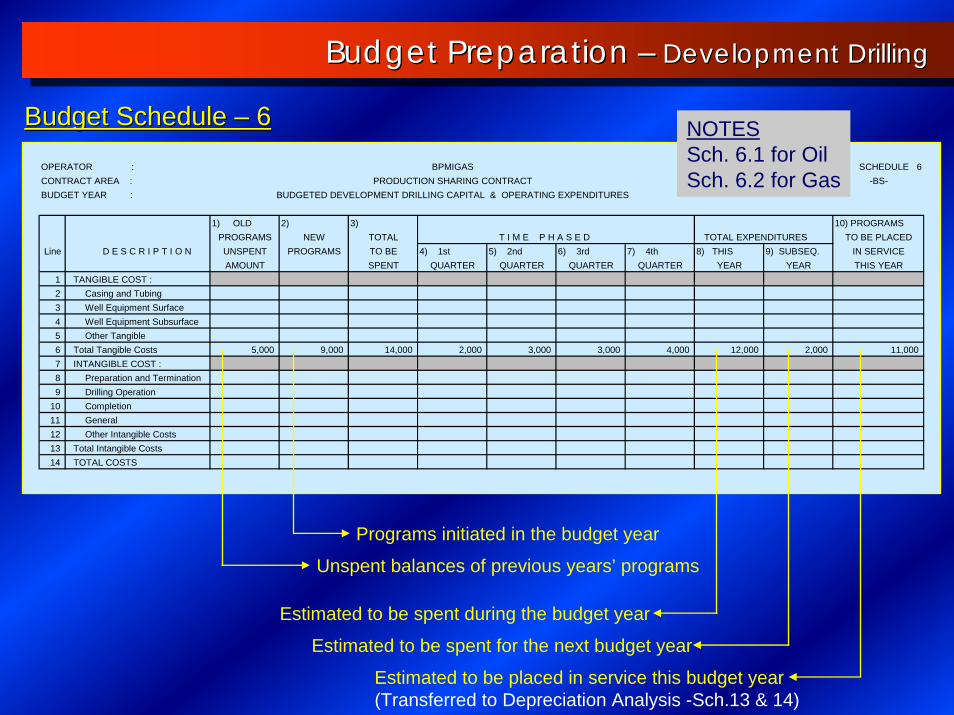

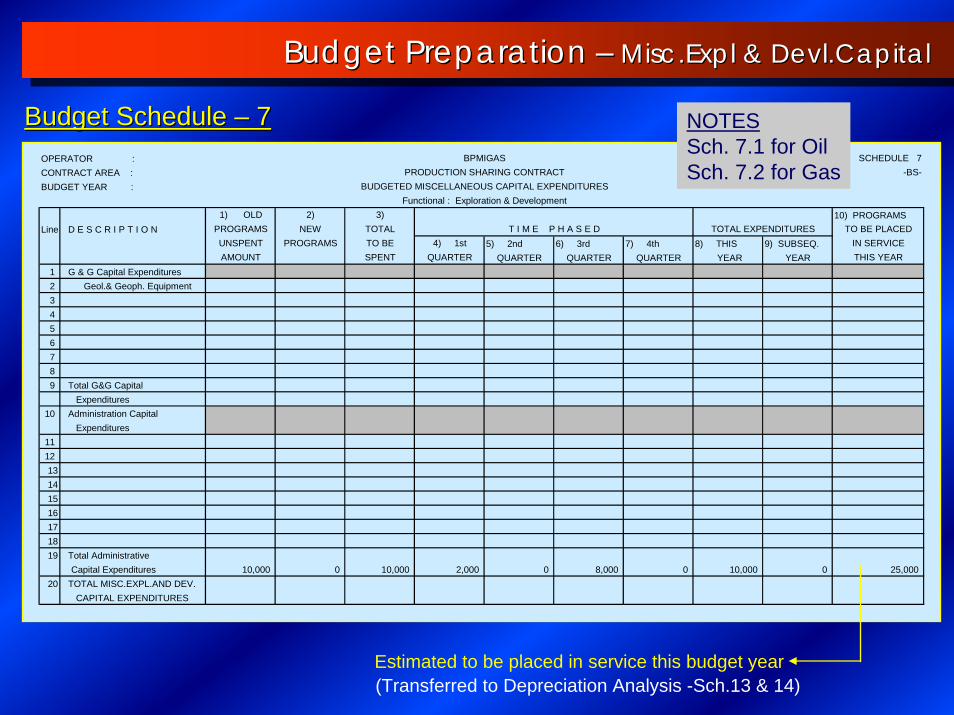

Schedule 5 Exploratory Drilling Capital & Operating ExpenditureSchedule 6 Development Drilling Capital & Operating ExpenditureSchedule 7 Miscellaneous Exploratory Capital Expenditures

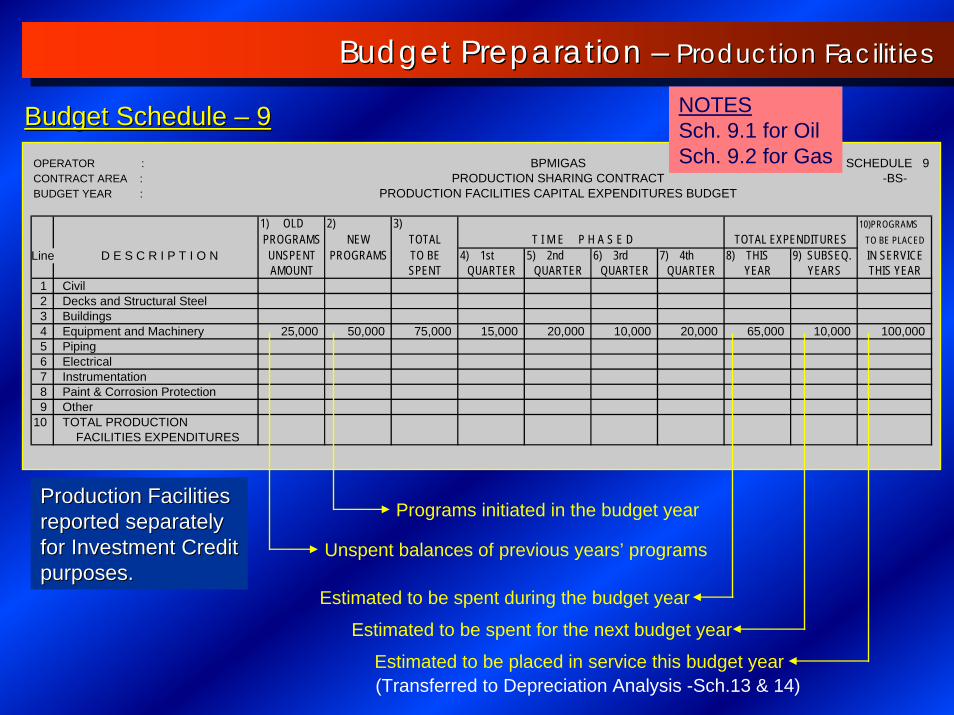

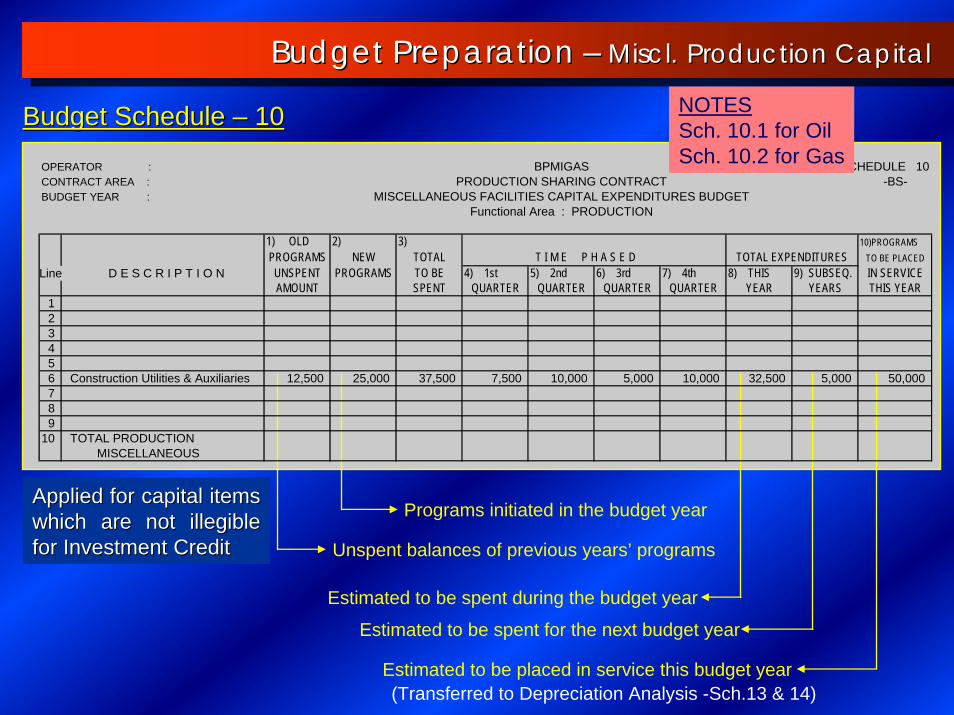

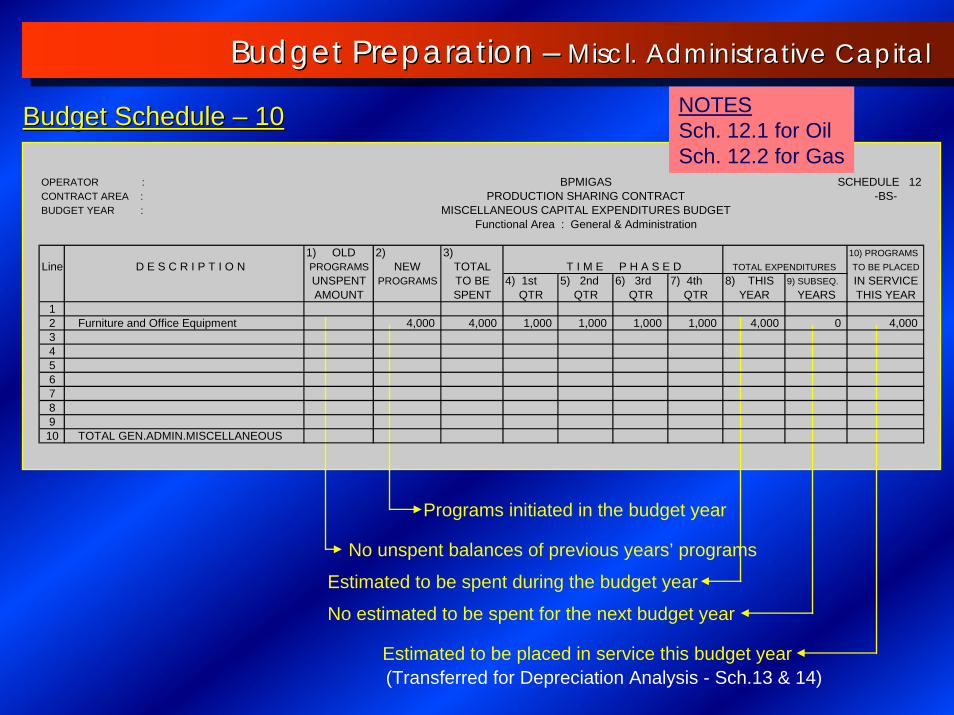

Schedule 8 *) Report 8 *) Production Expense SummarySchedule 9 Production Facilities Capital ExpendituresSchedule 10 Miscellaneous Facilities Capital Expenditures

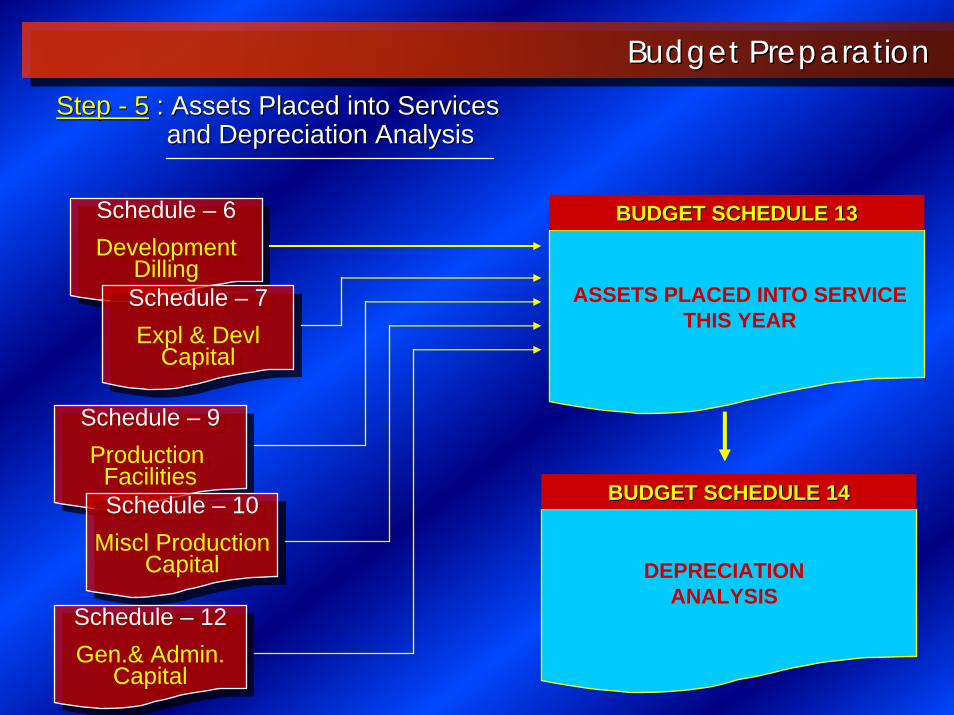

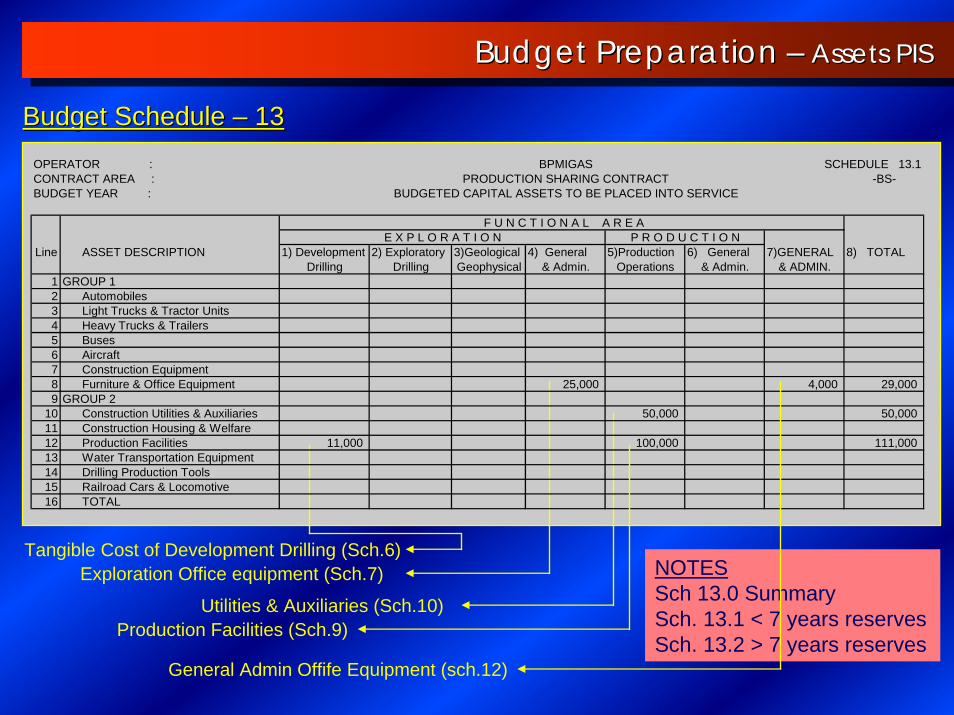

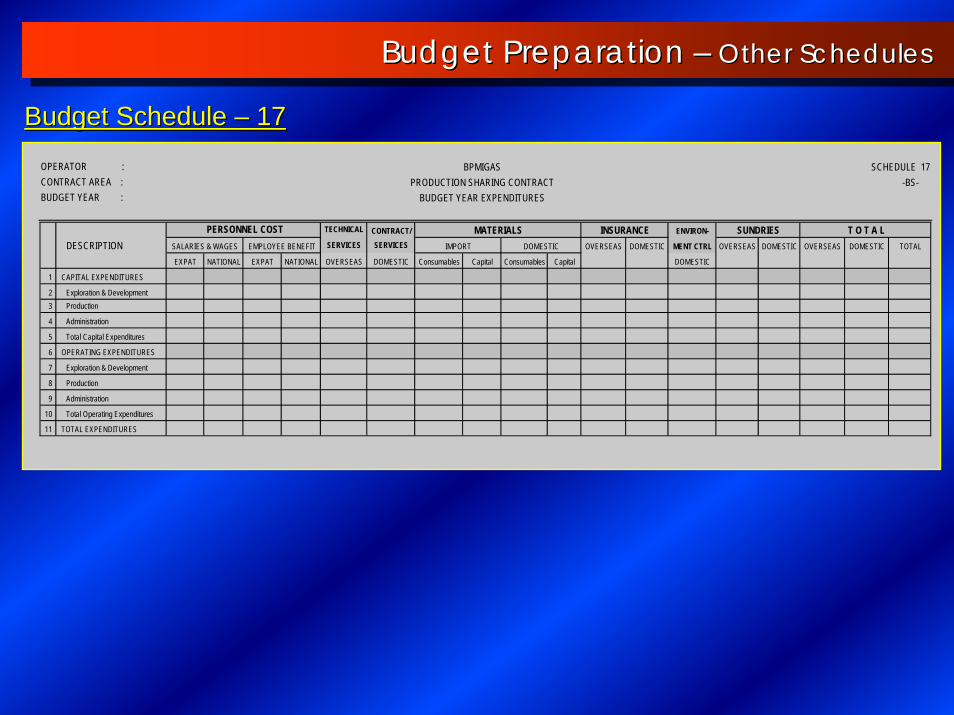

Schedule 11 *) Report 11 *) Administrative Expense SummarySchedule 12 Miscellaneous Administrative Capital ExpendituresSchedule 13 Capital Assets to be Placed into ServiceSchedule 14 Report 14 Depreciation ScheduleSchedule 15 Report 15 Detailed Project Support Listing/Project Status ReportSchedule 16 Report 16 Lifting Forecast/Lifting Share AnalysisSchedule 17 Expenditures Summary by Category

B U D G E T R E P O R T DESCRIPTIONSchedule 1 Report 1 Financial Status ReportSchedule 2 Report 2 Key Operating StatisticsSchedule 3 Expense and Expenditures Summary

Schedule 3A Report 3 Expenditures SummarySchedule 4 *) Report 4 *) Exploration and Development Expenditures

Schedule 5 Exploratory Drilling Capital & Operating ExpenditureSchedule 6 Development Drilling Capital & Operating ExpenditureSchedule 7 Miscellaneous Exploratory Capital Expenditures

Schedule 8 *) Report 8 *) Production Expense SummarySchedule 9 Production Facilities Capital ExpendituresSchedule 10 Miscellaneous Facilities Capital Expenditures

Schedule 11 *) Report 11 *) Administrative Expense SummarySchedule 12 Miscellaneous Administrative Capital ExpendituresSchedule 13 Capital Assets to be Placed into ServiceSchedule 14 Report 14 Depreciation ScheduleSchedule 15 Report 15 Detailed Project Support Listing/Project Status ReportSchedule 16 Report 16 Lifting Forecast/Lifting Share AnalysisSchedule 17 Expenditures Summary by Category

Complete Sets of Budget & Financial ReportComplete Sets of Budget & Financial Report

Budgeting & ReportingBudgeting & Reporting

*) Includes Attachment

Budgeting & ReportingBudgeting & Reporting

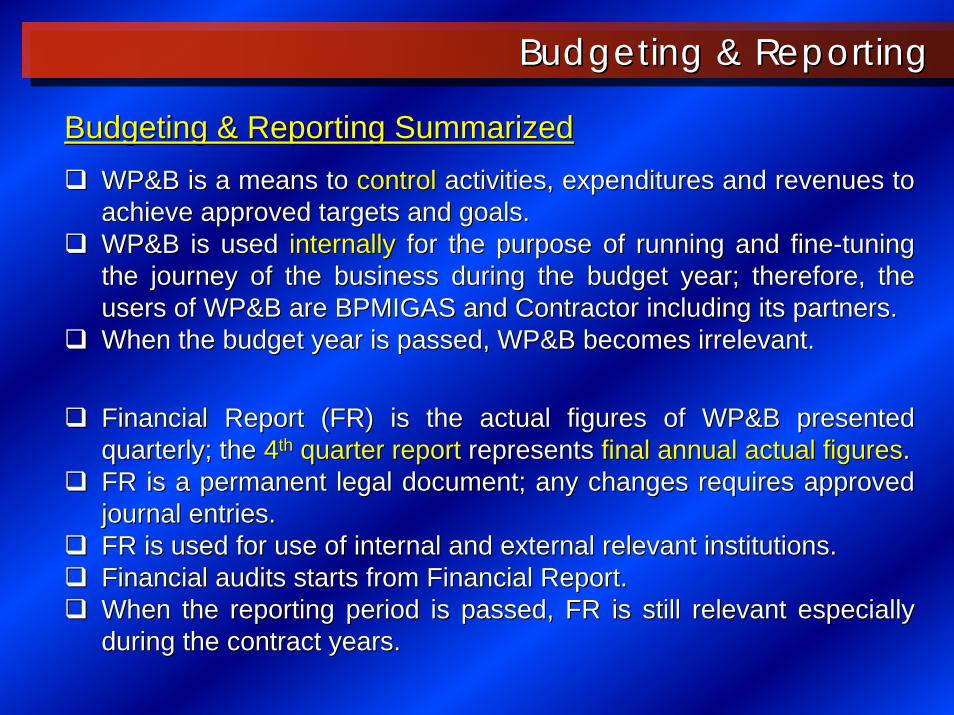

Budgeting & Reporting SummarizedBudgeting & Reporting SummarizedWP&B is a means to WP&B is a means to controlcontrol activities, expenditures and revenues to activities, expenditures and revenues to achieve approved targets and goals.achieve approved targets and goals.WP&B is used WP&B is used internallyinternally for the purpose of running and finefor the purpose of running and fine--tuning tuning the journey of the business during the budget year; therefore, tthe journey of the business during the budget year; therefore, the he users of WP&B are BPMIGAS and Contractor including its partners.users of WP&B are BPMIGAS and Contractor including its partners.When the budget year is passed, WP&B becomes irrelevant.When the budget year is passed, WP&B becomes irrelevant.

Financial Report (FR) is the actual figures of WP&B presented Financial Report (FR) is the actual figures of WP&B presented quarterly; the quarterly; the 44thth quarter reportquarter report represents represents final annual actual figuresfinal annual actual figures..FR is a permanent legal document; any changes requires approved FR is a permanent legal document; any changes requires approved journal entries.journal entries.FR is used for use of internal and external relevant institutionFR is used for use of internal and external relevant institutions.s.Financial audits starts from Financial Report.Financial audits starts from Financial Report.When the reporting period is passed, FR is still relevant especiWhen the reporting period is passed, FR is still relevant especially ally during the contract years.during the contract years.

FinancialStatus

FinancialStatus

Exploration &Development

Exploration &Development

ProductionExpense

ProductionExpense

General &Administrative

General &Administrative

ExpendituresSummary

ExpendituresSummary

DepreciationDepreciation LiftingLifting

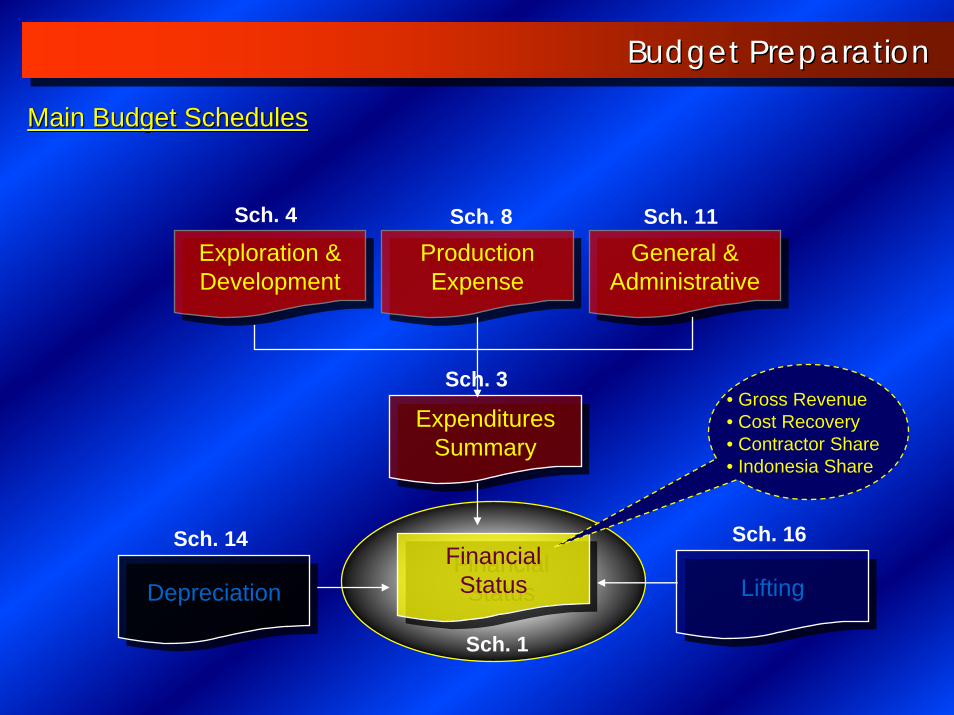

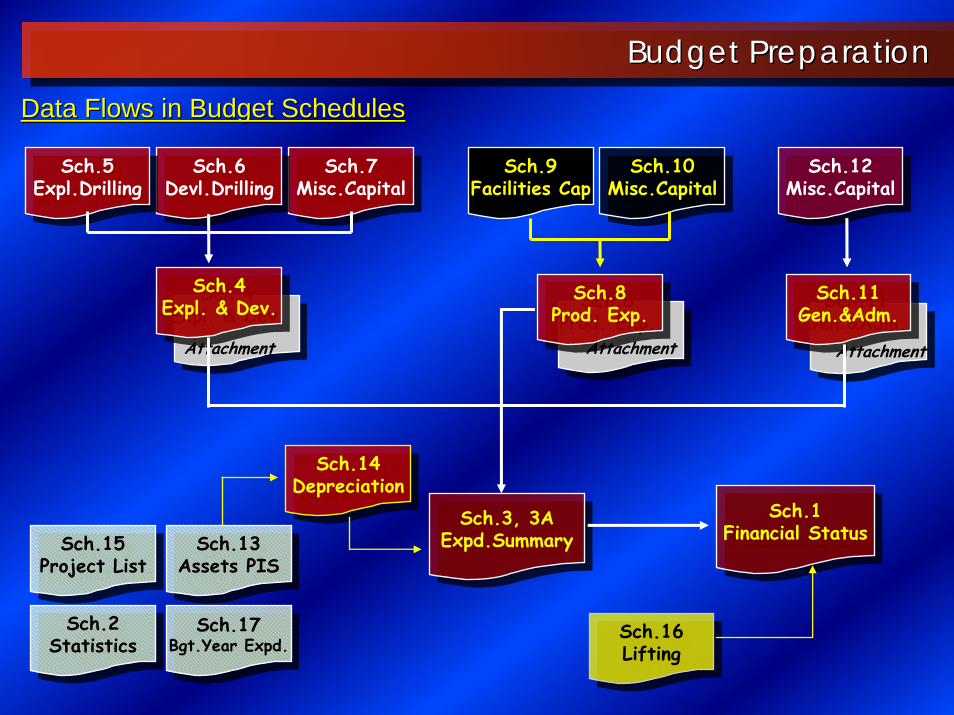

Main Budget SchedulesMain Budget Schedules

Sch. 4 Sch. 8 Sch. 11

Sch. 3

Sch. 1

Sch. 14 Sch. 16

Budget PreparationBudget Preparation

• Gross Revenue• Cost Recovery• Contractor Share• Indonesia Share

Budget PreparationBudget Preparation

Sch.7Misc.Capital

Sch.7Misc.Capital

Sch.6Devl.Drilling

Sch.6Devl.Drilling

Sch.5Expl.Drilling

Sch.5Expl.Drilling

Sch.10Misc.CapitalSch.10

Misc.CapitalSch.9

Facilities CapSch.12

Misc.CapitalSch.12

Misc.Capital

Sch.4Expl. & Dev.

Sch.4Expl. & Dev.

Attachment

Sch.8Prod. Exp.Sch.8

Prod. Exp.

Attachment

Sch.11Gen.&Adm.Sch.11

Gen.&Adm.

Attachment

Sch.3, 3AExpd.SummarySch.3, 3A

Expd.SummarySch.1

Financial StatusSch.1

Financial Status

Sch.14DepreciationSch.14

Depreciation

Sch.16Lifting

Sch.16Lifting

Sch.15Project ListSch.15

Project ListSch.13

Assets PISSch.13

Assets PIS

Sch.17Bgt.Year Expd.

Sch.17Bgt.Year Expd.

Sch.2StatisticsSch.2

Statistics

Data Flows in Budget Schedules Data Flows in Budget Schedules

Step Step –– 11 : Identify planned activities as routines & projects: Identify planned activities as routines & projects

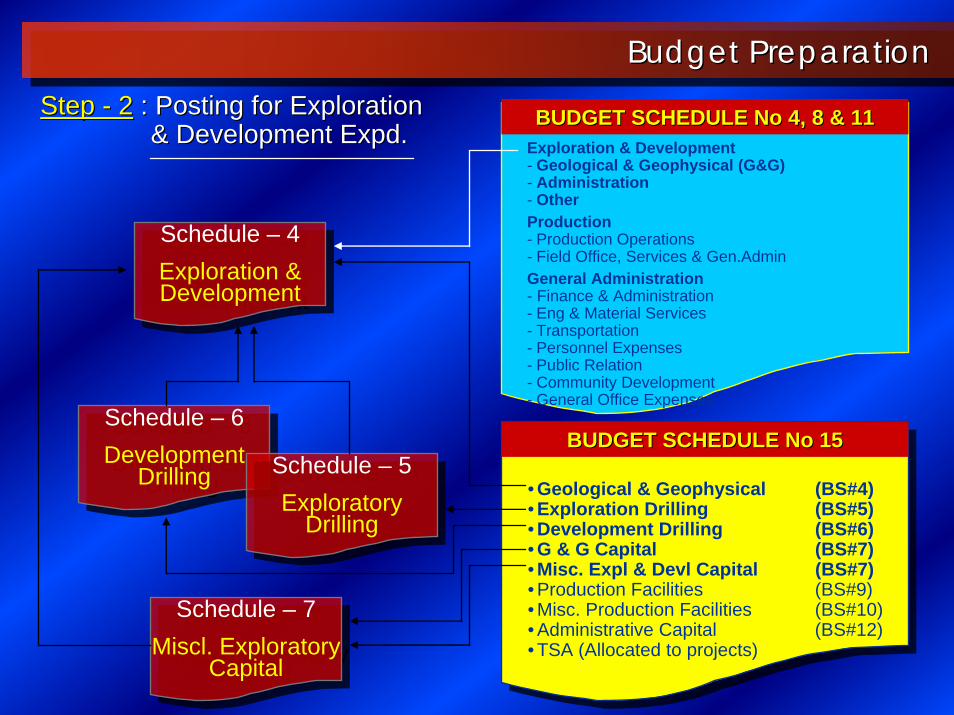

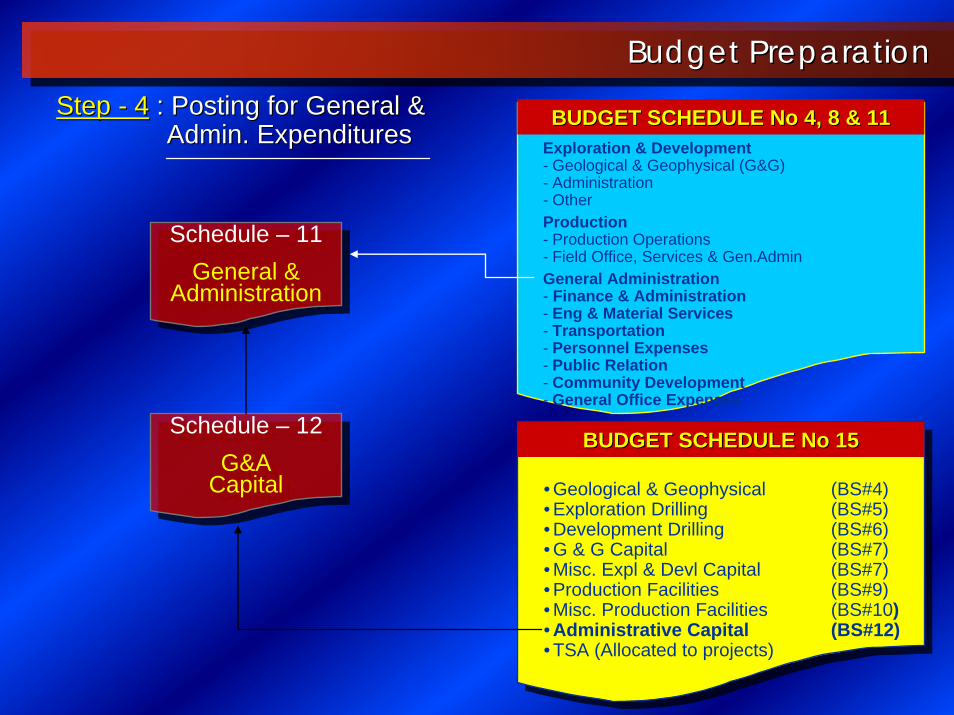

Step Step –– 22 : : Posting Exploration & Development ExpendituresPosting Exploration & Development Expenditures

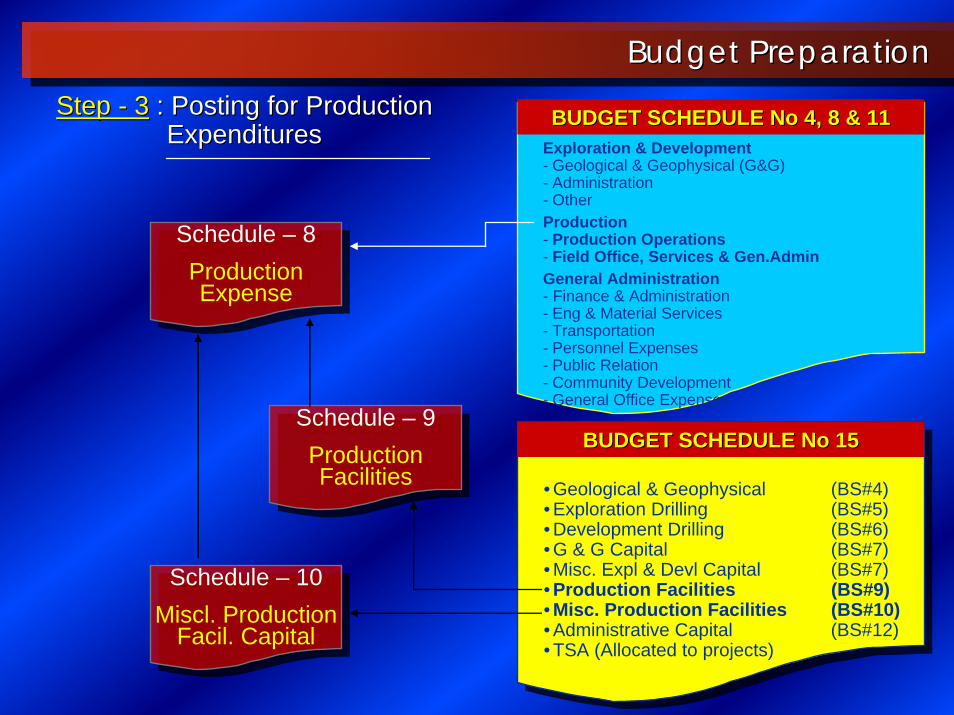

Step Step –– 33 : Posting Production Expenditures: Posting Production Expenditures

Step Step –– 44 : : Posting General & Administration ExpendituresPosting General & Administration Expenditures

Step Step –– 55 : Classifying Assets Placed Into Service and Depreciation: Classifying Assets Placed Into Service and Depreciation

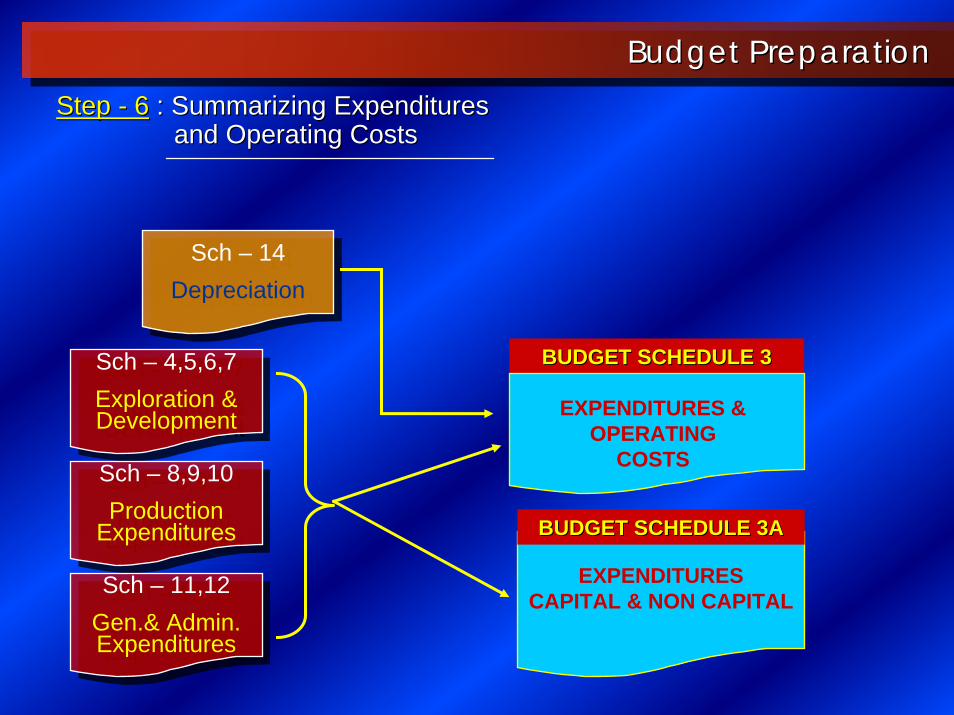

Step Step –– 66 : : Summarizing Expenditures & Operating CostsSummarizing Expenditures & Operating Costs

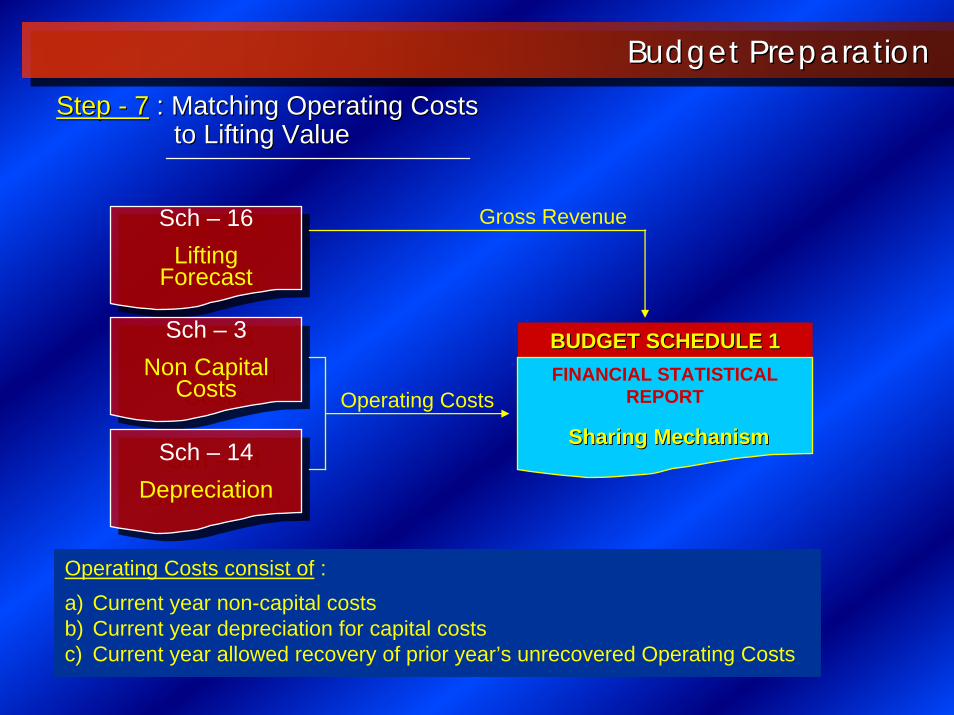

Step Step –– 77 : Matching Operating Costs to Lifting Value: Matching Operating Costs to Lifting Value

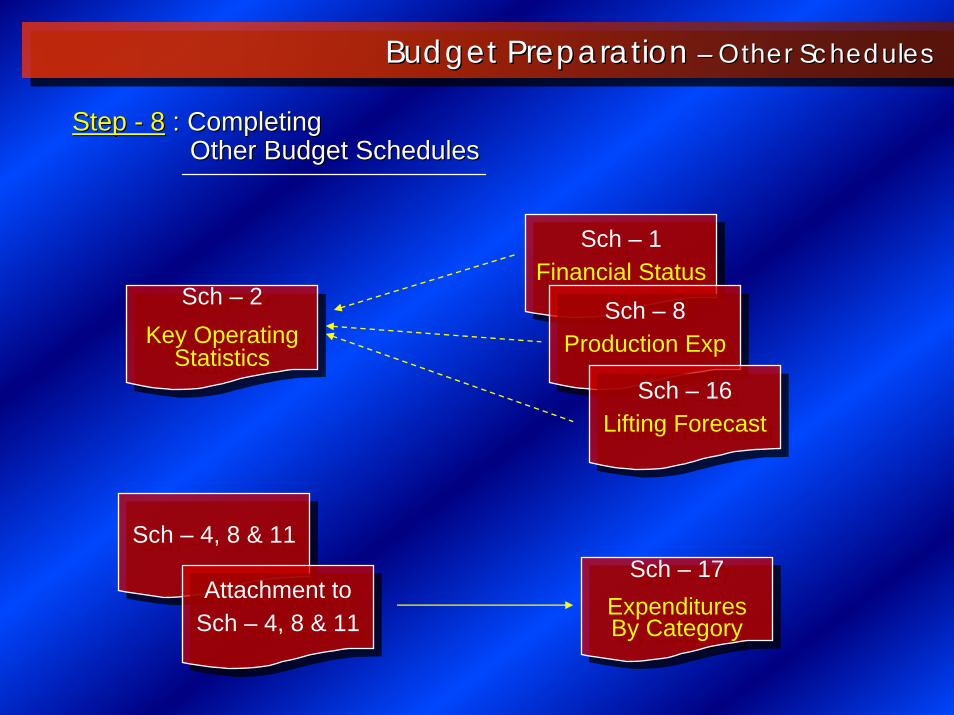

Step Step –– 88 : : Completing Other SchedulesCompleting Other Schedules

Budget PreparationBudget Preparation

Developing BudgetDeveloping Budget

Budget PreparationBudget Preparation

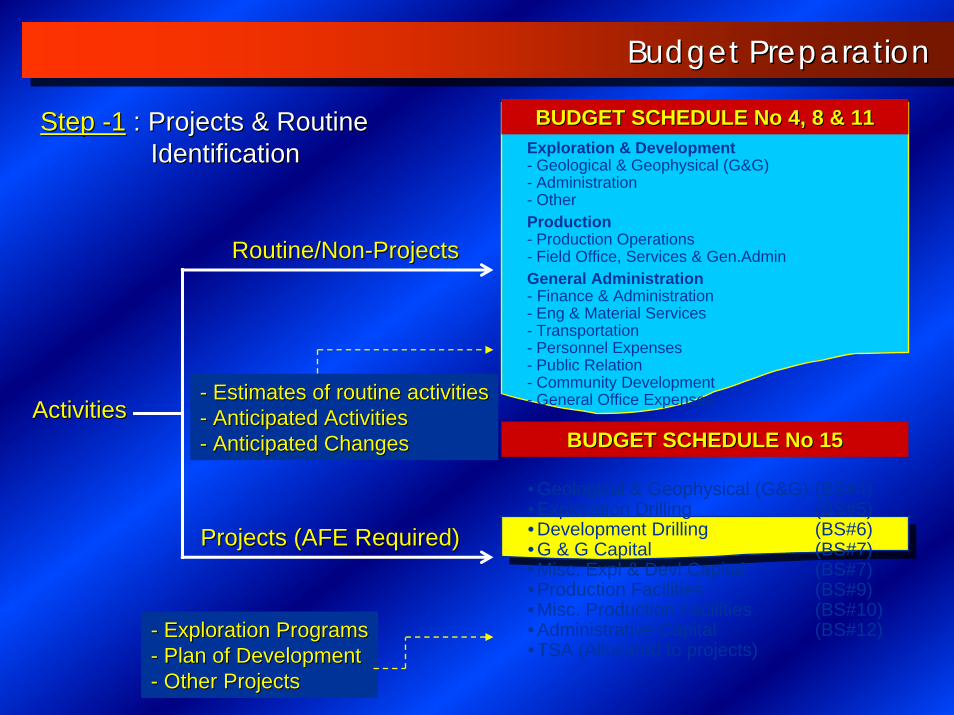

Step Step --11 : Projects & Routine : Projects & Routine IdentificationIdentification

ActivitiesActivities

• Geological & Geophysical (G&G) (BS#4)• Exploration Drilling (BS#5)• Development Drilling (BS#6)• G & G Capital (BS#7)• Misc. Expl & Devl Capital (BS#7)• Production Facilities (BS#9)• Misc. Production Facilities (BS#10)• Administrative Capital (BS#12)• TSA (Allocated to projects)

BUDGET SCHEDULE No 15BUDGET SCHEDULE No 15

Exploration & Development- Geological & Geophysical (G&G)- Administration- OtherProduction- Production Operations- Field Office, Services & Gen.AdminGeneral Administration- Finance & Administration- Eng & Material Services- Transportation- Personnel Expenses- Public Relation- Community Development- General Office Expenses

BUDGET SCHEDULE No 4, 8 & 11BUDGET SCHEDULE No 4, 8 & 11

Routine/NonRoutine/Non--ProjectsProjects

Projects (AFE Required)Projects (AFE Required)

-- Exploration ProgramsExploration Programs-- Plan of DevelopmentPlan of Development-- Other ProjectsOther Projects

-- Estimates of routine activitiesEstimates of routine activities-- Anticipated ActivitiesAnticipated Activities-- Anticipated ChangesAnticipated Changes

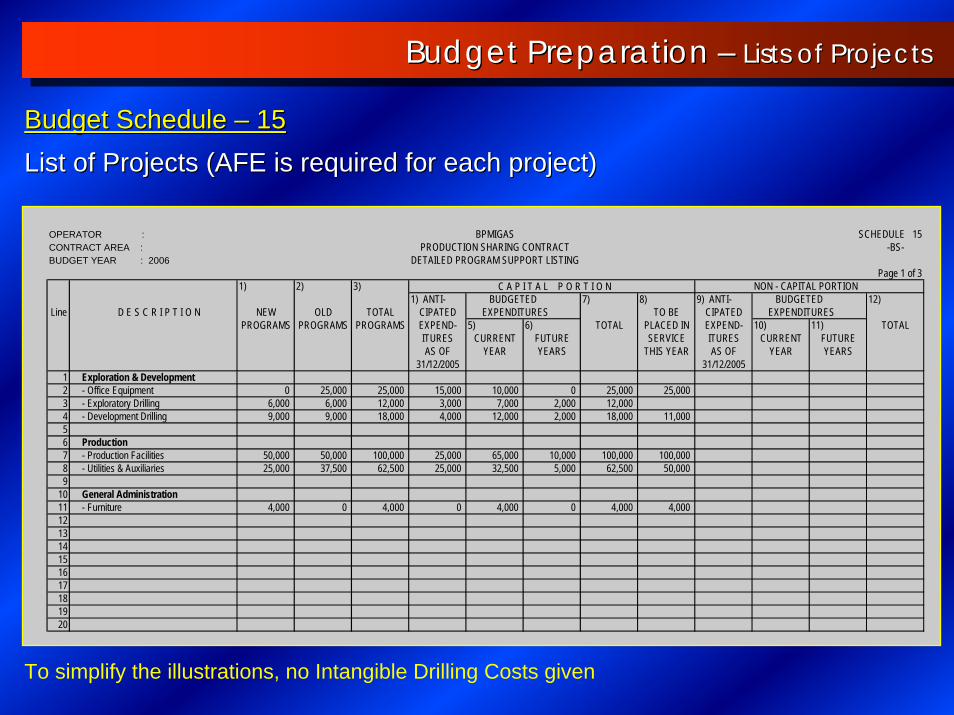

Budget Preparation Budget Preparation –– Lists of ProjectsLists of Projects

Budget Schedule Budget Schedule –– 1515List of Projects (AFE is required for each project) List of Projects (AFE is required for each project)

To simplify the illustrations, no Intangible Drilling Costs given

OPERATOR : BPMIGAS SCHEDULE 15CONTRACT AREA : PRODUCTION SHARING CONTRACT -BS-BUDGET YEAR : 2006 DETAILED PROGRAM SUPPORT LISTING

Page 1 of 31) 2) 3) C A P I T A L P O R T I O N NON - CAPITAL PORTION

1) ANTI- BUDGETED 7) 8) 9) ANTI- BUDGETED 12)Line D E S C R I P T I O N NEW OLD TOTAL CIPATED EXPENDITURES TO BE CIPATED EXPENDITURES

PROGRAMS PROGRAMS PROGRAMS EXPEND- 5) 6) TOTAL PLACED IN EXPEND- 10) 11) TOTALITURES CURRENT FUTURE SERVICE ITURES CURRENT FUTUREAS OF YEAR YEARS THIS YEAR AS OF YEAR YEARS

31/12/2005 31/12/20051 Exploration & Development2 - Office Equipment 0 25,000 25,000 15,000 10,000 0 25,000 25,0003 - Exploratory Drilling 6,000 6,000 12,000 3,000 7,000 2,000 12,0004 - Development Drilling 9,000 9,000 18,000 4,000 12,000 2,000 18,000 11,00056 Production7 - Production Facilities 50,000 50,000 100,000 25,000 65,000 10,000 100,000 100,0008 - Utilities & Auxiliaries 25,000 37,500 62,500 25,000 32,500 5,000 62,500 50,0009

10 General Administration11 - Furniture 4,000 0 4,000 0 4,000 0 4,000 4,000121314151617181920

Budget PreparationBudget PreparationStep Step -- 22 : Posting for Exploration: Posting for Exploration

& Development & Development ExpdExpd..