Embed Size (px)

Citation preview

Prof. DavidGreenwood

Professor, Advanced PropulsionSystems

WMG, The University of Warwick

Sponsors

Accelerating the UK Battery IndustryAutomotive needs and the Faraday Challenge

LCV17, September 2017

www.automotivecouncil.co.uk

Professor David GreenwoodAdvanced Propulsion SystemsWMG, The University of Warwick [email protected]

Battery is the defining component of an electrified vehicle

PowerPowerRangeRange

CostCost

LifeLife

Ride andHandlingRide andHandling

PackagePackage

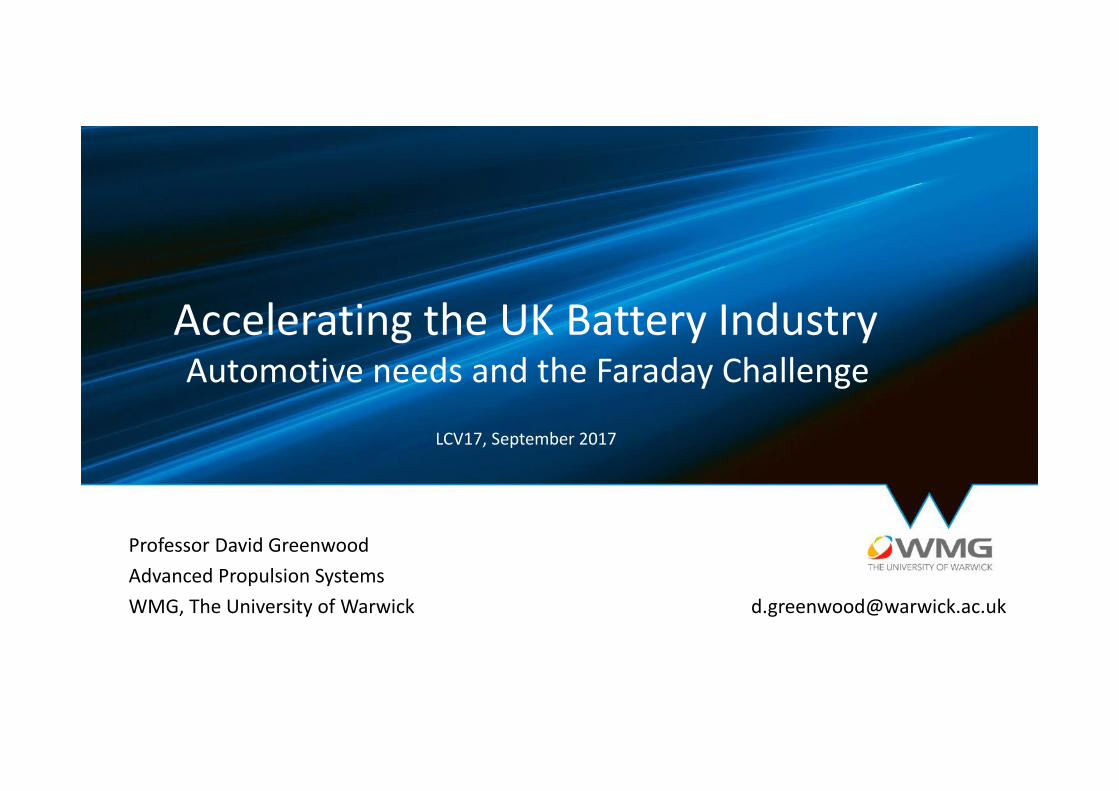

Batteries are a major commercial opportunity for UK

Conventional VehicleOne third of conventional vehicle cost is powertrainUK manufactures 1.7M cars per year, EU makes 18M per yearAssuming constant volumes and average battery pack cost of £6000 car, and 50% EV/PHEV share by 2035

This represents a UK supply chain opportunity of >£5bn/year by 2035EU supply chain opportunity of over £50bn/yr at 2035Rate of EV/PHEV market growth determined by customer uptake

Uptake will be determined by vehicle cost, range, charging infrastructure and fiscal regime

Electric Vehicle

Motor and power electronics cost around60% of conventional powertrain

Battery costs around 3-5x currentpowertrain

Rest of vehicle costs similar as before –increased costs for HVAC, brakes andsuspension systems

Battery is >50% of overall vehicle value

£

Report Ref: p.1; p.9

Lithium Ion batteries are improving rapidlyCosts have fallen dramatically due totechnology, production volume andmarket dynamicsPack cost fallen from $1,000/kWh to$250/kWh in less than 8 years

Nykvist et al 2014

Volumetric energy density is increasingdue to better materials and cell structureDoubled in 15 yearsRequires continuous chemistry andmaterials innovation to continue

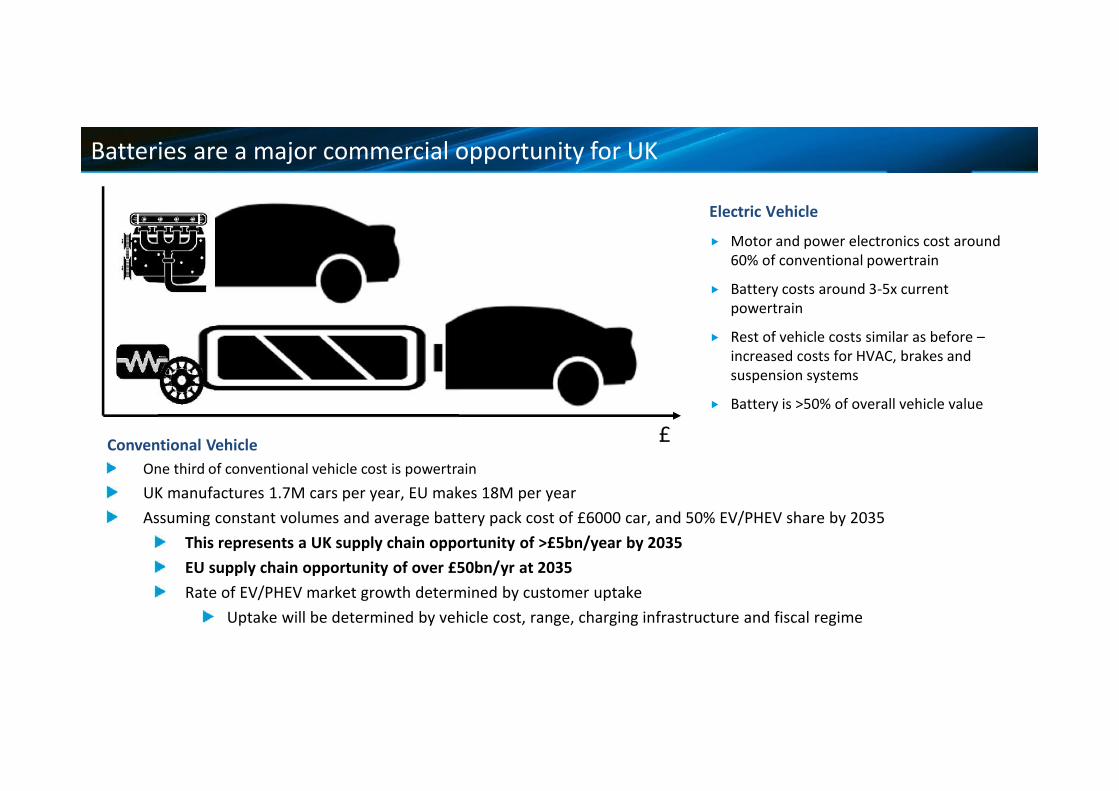

Industry structure for automotive batteries

Raw Materials Materials andElectrochemistry

Electrode,electrolyte,

separator, etc.Cell Manufacture Module,

Pack and BMS Vehicle Application 2nd life /Recycling

High Vol OEM

Tier 1 Low Vol OEM

Materials supplier (e.g. JM)

Cell Supplier (e.g. Panasonic)

Recycler

2nd User ?Industrial Chemists (e.g. 3M)

Mining/refining

Possible UK Industry Engagement for Automotive Batteries

Raw Materials Materials andElectrochemistry

Electrode,electrolyte,

separator, etc.Cell Manufacture Module,

Pack and BMS Vehicle Application 2nd life /Recycling

UK does not havemineral resources tosupport mining andrefinement of rawmaterials.

No import challenges.

Abundance of rawmaterials is not a majorconcern.

Infrastructure to mineand refine may notgrow fast enough.

Contribution of recycledmaterials in the future

UK academia and spin-outcompanies developmaterials for future.

Industrial chemicalscompanies (e.g. JM, BASF,3M) could produce powdermaterials in the UK fromimported raw materials.

Latent capability identifiedin adjacent sectors, e.g.paints, water treatment.

Alternatively, could beimported without difficulty.

Large companies (e.g. JM,Nissan) could producecoated electrodes,electrolytes andseparators in the UK

JV’s between OEMs andexisting overseasmanufacturers possible

Manufacturing processequipment can bedeveloped in the UK.

Comprises 50% of cell costand significant IP value.Best co-developed withcells

Alternatively, could beimported but have shelflife and transport issues.

Large scale cell assemblycompanies located inthe UK.Fastest achievedthrough foreign directinvestment/capability ?

Will be driven by UKdemand, and commoncell formats would easebusiness case

Possible route throughcollaborations betweenUK OEMs?

UK manufactured cellscould be export to EU.

Cells could be importedfrom Asia but with longlead time and transportissues, and maybe notlatest technology

Passenger car OEMs inUK could manufacturemodules and packs line-side to support vehiclesassembled in the UK.

UK based Tier 1 supplychain required tosupport lower volumeapplications (CV, OHV,taxi, etc.)

Alternatively modulesand/or packs can beimported but withsignificant logistics andcost impact.

Would increaselikelihood of cellassembly in UK.

High volume: vehicle andpack assembly highlylikely to be co-located.

Keep batteries, keepvehicle assembly. Losebatteries, possibly losevehicle assembly. Cellassembly investmentlikely to pivot on moduleand pack assemblylocations.

Manufacturing scale uprepresents a technicaland commercial risk.

End of life batterydisposal recognised assignificant economic andenvironmental concern.

2nd Life applicationsdemonstrated technicallybut commercial modelsuncertain.

Technologies lacking forlarge scale recycling andmaterials recovery.

Scarce and valuablematerials in particularrequire attention (rareearths, cobalt, etc.)

Report Ref: p.9-10

Significant improvements are necessary and possible in 20 year horizon

Cost

Now $130/kWh (cell)$280/kWh (pack)

2035 $50/kWh (cell)$100/kWh (pack)

Energy Density

Now 700Wh/l,250Wh/kg (cell)

2035 1400Wh/l, 500Wh/kg(cell)

Power Density

Now 3 kW/kg (pack)

2035 12 kW/kg (pack)

Safety

2035 eliminate thermalrunaway at pack level toreduce pack complexity

1st Life

Now 8 years (pack)

2035 15 years (pack)

Temperature

Now -20° to +60°C (cell)

2035 -40° to +80°C (cell)

Predictability

2035 full predictive modelsfor performance and aging

of battery

Recyclability

Now 10-50% (pack)

2035 95% (pack)

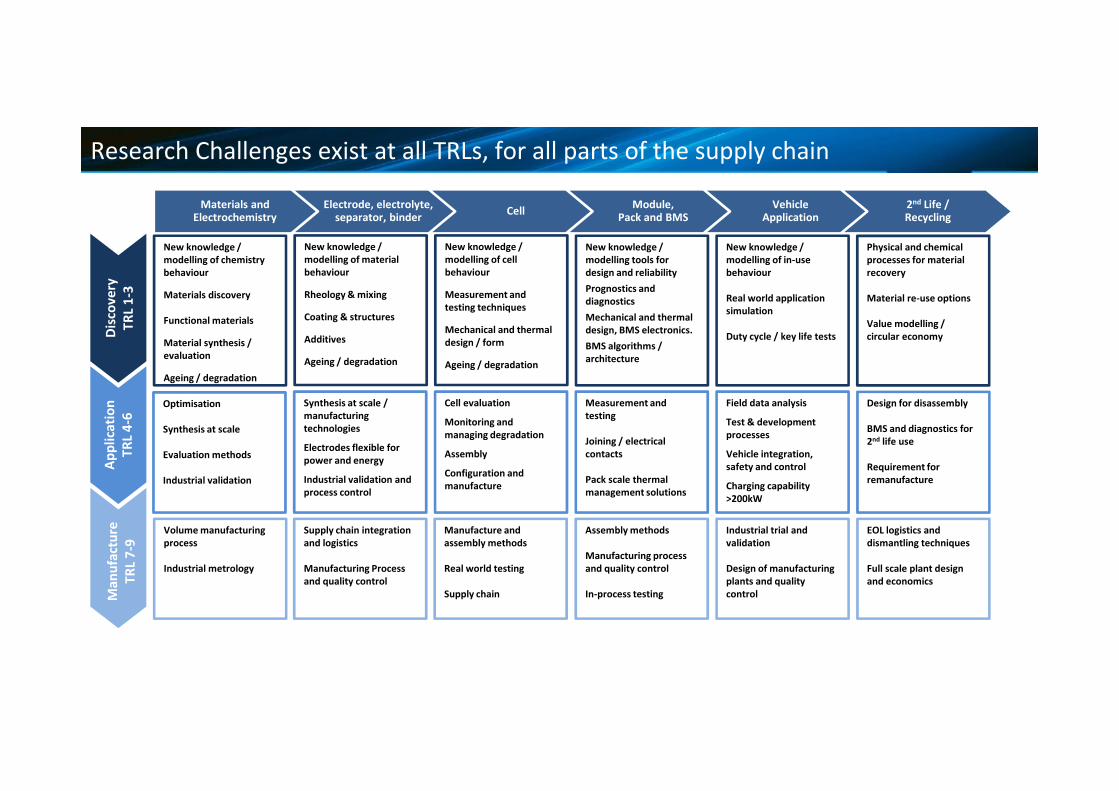

Research Challenges exist at all TRLs, for all parts of the supply chain

Disc

over

yTR

L 1-

3Ap

plic

atio

nTR

L 4-

6M

anuf

actu

reTR

L 7-

9

Materials andElectrochemistry

Electrode, electrolyte,separator, binder Cell Module,

Pack and BMSVehicle

Application2nd Life /Recycling

New knowledge /modelling of chemistrybehaviour

Materials discovery

Functional materials

Material synthesis /evaluation

Ageing / degradation

New knowledge /modelling of materialbehaviour

Rheology & mixing

Coating & structures

Additives

Ageing / degradation

New knowledge /modelling of cellbehaviour

Measurement andtesting techniques

Mechanical and thermaldesign / form

Ageing / degradation

New knowledge /modelling tools fordesign and reliabilityPrognostics anddiagnosticsMechanical and thermaldesign, BMS electronics.BMS algorithms /architecture

New knowledge /modelling of in-usebehaviour

Real world applicationsimulation

Duty cycle / key life tests

Physical and chemicalprocesses for materialrecovery

Material re-use options

Value modelling /circular economy

Synthesis at scale /manufacturingtechnologies

Electrodes flexible forpower and energy

Industrial validation andprocess control

Cell evaluation

Monitoring andmanaging degradation

Assembly

Configuration andmanufacture

Measurement andtesting

Joining / electricalcontacts

Pack scale thermalmanagement solutions

Field data analysis

Test & developmentprocesses

Vehicle integration,safety and control

Charging capability>200kW

Design for disassembly

BMS and diagnostics for2nd life use

Requirement forremanufacture

Volume manufacturingprocess

Industrial metrology

Supply chain integrationand logistics

Manufacturing Processand quality control

Industrial trial andvalidation

Design of manufacturingplants and qualitycontrol

EOL logistics anddismantling techniques

Full scale plant designand economics

Manufacture andassembly methods

Real world testing

Supply chain

Assembly methods

Manufacturing processand quality control

In-process testing

Optimisation

Synthesis at scale

Evaluation methods

Industrial validation

Report Ref: p.12-13

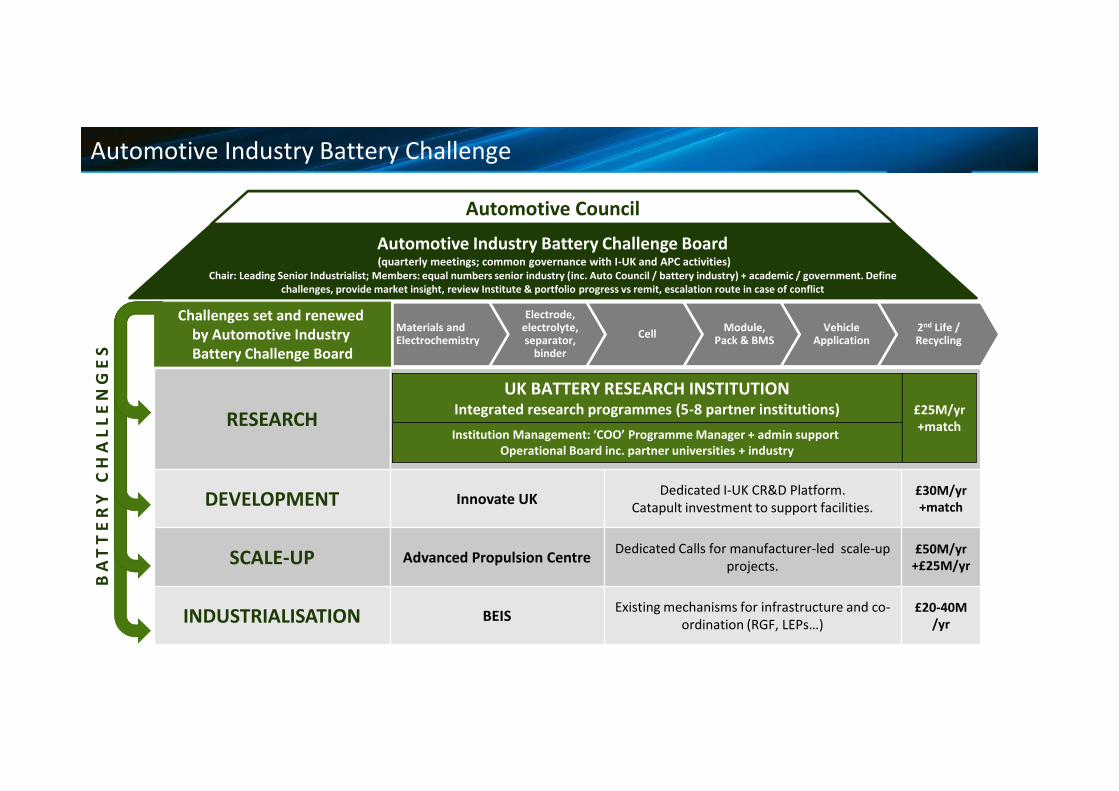

Automotive Industry Battery Challenge

Automotive Industry Battery Challenge Board(quarterly meetings; common governance with I-UK and APC activities)

Chair: Leading Senior Industrialist; Members: equal numbers senior industry (inc. Auto Council / battery industry) + academic / government. Definechallenges, provide market insight, review Institute & portfolio progress vs remit, escalation route in case of conflict

RESEARCH

DEVELOPMENT Innovate UK Dedicated I-UK CR&D Platform.Catapult investment to support facilities.

£30M/yr+match

SCALE-UP Advanced Propulsion Centre Dedicated Calls for manufacturer-led scale-upprojects.

£50M/yr+£25M/yr

INDUSTRIALISATION BEIS Existing mechanisms for infrastructure and co-ordination (RGF, LEPs…)

£20-40M/yr

Challenges set and renewedby Automotive IndustryBattery Challenge Board

BA

TT

ER

Y C

HA

LLE

NG

ES

Institution Management: ‘COO’ Programme Manager + admin supportOperational Board inc. partner universities + industry

UK BATTERY RESEARCH INSTITUTIONIntegrated research programmes (5-8 partner institutions)

Materials andElectrochemistry

Electrode,electrolyte,separator,

binder

Cell Module,Pack & BMS

VehicleApplication

2nd Life /Recycling

Automotive Council

£25M/yr+match

• Research networks: ESRN, Supergen, Midlands ERA, STFC• Catapult investments – HVMC (WMG, MTC, CPI, NCC)• APC Spoke network (WMG led) and EPSRC Energy Storage CDT

(Sheffield / Southampton)• National cell scale-up facility at WMG• Module and pack manufacturing pilot at WMG• Diamond synchrotron, Archer computing facility

UK has much of the critical research infrastructure required to succeed

• Innovate UK mechanisms exist to support this• Dedicated electrification theme within/alongside IDP programme could cover

both product and manufacturing technologies at TRL 3-6• Key themes

• Development of materials and manufacturing techniques for cell components andcells

• Development of module and pack designs and systems, including advanced BMSalgorithms

• Vehicle electrification concepts – including off-highway, bus and commercialvehicles

• Technology likely to be Li-ion based for next 8-10 years – short term focusshould be here

• For battery system future, can be used to build supply chain competencies• Skills development (design and manufacturing engineering) are a critical

output• HVM Catapult network can be used to develop manufacturing technologies

and opportunities for SMEs

Industry Strategy ChallengeFunds (ISFC)

Provide opportunity for projects inthis area. Energy Storage understoodto be a priority area, but mechanismto access not yet clear

CR&D develops promising technologies and new supply chains

Report Ref: p.4; p.7

• Design and manufacturing technologies for modules and packs areimmature with much potential for cost and performance improvement

• Techniques such as cell handling and testing, cell to bus-bar welding, inprocess testing, and end of line testing require development

• Centralised scale-up facilities such as WMG allow for sharing of capital costand acceleration of manufacturing learning

• Prior to full plant investment, pilot plants will be required by individualOEM’s to trial and develop high volume manufacturing processes,demonstrating “run-at-rate” with flexibility to cell and module format.Allows development of manufacturing KPIs and plant “blueprints”

• Advanced Propulsion Centre / Catapult mechanisms can be leveraged forsupport

• Process and skills (manufacturing engineering) development are a criticaloutput. Currently no clear mechanism for their delivery. Suggest APC remitcould be extended for apprentice / practitioner level training

Industrial scale-up delivers manufacturing competitiveness

Report Ref: p.4; p.7

• Low volume module and pack manufacture can be delivered with modestinvestment <£10M

• High volume cell, module and pack manufacturing plants cost £X00M to £XBn• Requires land, power, infrastructure, planning approval and local skills

(manufacturing)• Regional, high value investments via RGFs, LEPs, etc.

• Once investment made, easier to increase capacity than build new plant (locks inbenefit)

• Strong incentives present in many countries have influenced large scaleinvestment decisions. Cost of capital is critical

• Tesla/Panasonic “Gigafactory” claims 50GWh/year, $3.5bn, 500,000 cars/yr, 6,500 jobs

• Nissan Sunderland 2GWh/year, £250M, 60,000 cars/yr capacity, 350 jobs

• LG Chem to manufacture in Wroclaw, Poland, £300M, 100,000 cars

• Samsung to manufacture in Goed, Hungary, 2.5GWh/yr £300M, 50,000 vehicles

• A123 to build factory in Ostrava, Czech Republic for 12V and 48V Li-Ion systems

Significant investment required to build high volume battery factories

Report Ref: p.5; p.8

• Rapid growth of industry leaves skills shortage at all levels• Focus on skills and resources as well as technologies and facilities

• Undergraduate and postgraduate courses and intake needs to grow• Supported by STEM acceleration in primary and secondary education

• PhD/EngDs needed from academia for research and development• Mechanisms exist but volume needs to increase

• More design engineers required to support product development• Innovate UK projects assist this. Aligned EngDs would increase impact

• Manufacturing engineers required with experience in relevant processes• APC projects can help develop manufacturing design skills• Pilot plant investments could be aligned to apprenticeship training to increase

manufacturing skills

• Aftersales skills (servicing, repair and recovery) required to support growing fleet• Apprenticeships for new staff and re-skilling of existing staff

Skills

Report Ref: p.7-8

Linkage to other Sectors

• Many longer term electrochemistry developments (e.g. Li-Air) mayhave higher potential in grid storage applications than automotive

• Energy industry currently lags automotive with regard to mobilisingindustrial actors

• Same / similar academic actors will be relevant butdifferent industrial actors required (including digital)

• No desire to build parallel structure for this in future• Suggest future action to extend this mechanism to grid scale

storage as industrial actors emerge• Create parallel governance structure with required actors

• Similar situation exists for rail, marine and aerospace• Propose to extend remit of this activity once established and

new “customer base” emerges• Same challenge mechanism could be used to take research from other

sectors into UK battery research institution model

Report Ref: p.11

Thank you

www.automotivecouncil.co.uk

Professor David GreenwoodAdvanced Propulsion SystemsWMG, The University of Warwick [email protected]