Embed Size (px)

DESCRIPTION

Â

Citation preview

Professional Insurance Agents/Summer 2014 1

Tennessee Edition/Summer 2014

The Changing MarkeTWhere is your agency headed?

111299 MagCover June FF.indd 5 5/12/2014 2:59:49 PM

2 Professional Insurance Agents/Summer 2014

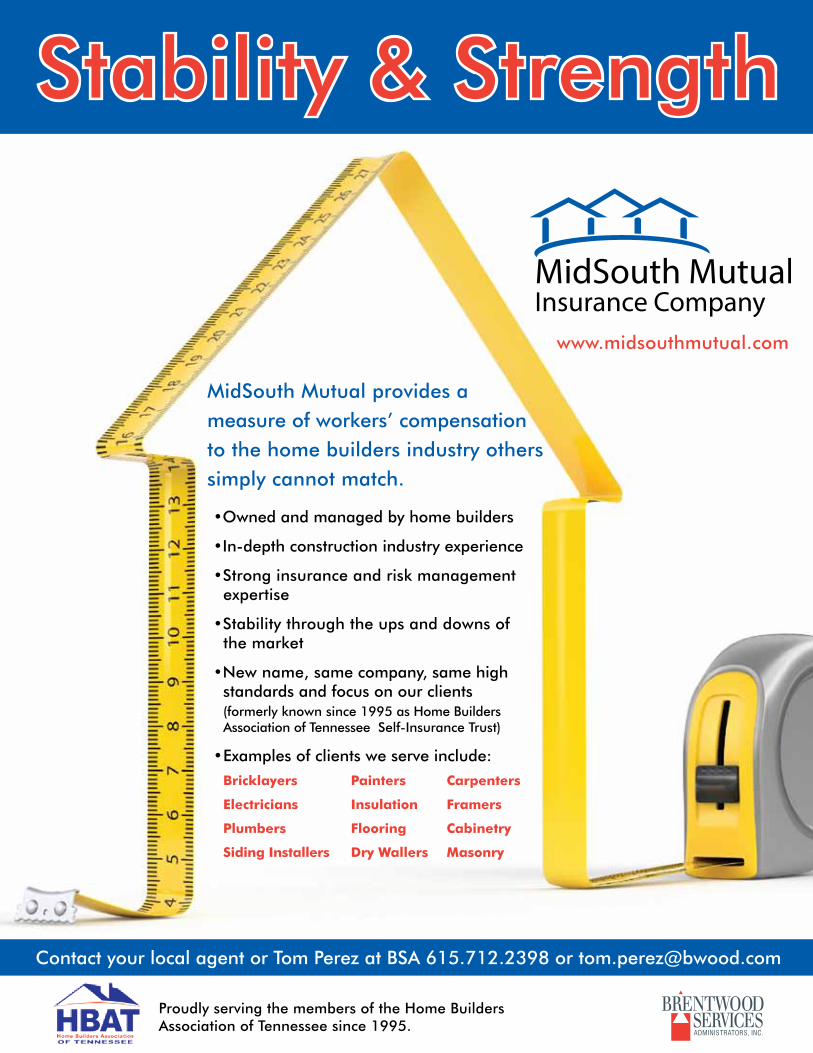

MidSouth Mutual provides a measure of workers’ compensationto the home builders industry others simply cannot match.

•Owned and managed by home builders

•In-depth construction industry experience

•Strong insurance and risk management expertise

•Stability through the ups and downs of the market

•New name, same company, same high standards and focus on our clients (formerly known since 1995 as Home Builders Association of Tennessee Self-Insurance Trust)

• Examples of clients we serve include:

Bricklayers Painters Carpenters

Electricians Insulation Framers

Plumbers Flooring Cabinetry

Siding Installers Dry Wallers Masonry

Contact your local agent or Tom Perez at BSA 615.712.2398 or [email protected]

Proudly serving the members of the Home Builders Association of Tennessee since 1995.

Stability & Strength

www.midsouthmutual.com

Professional Insurance Agents/Summer 2014 3Summer 2014

Dedicated to the advancement of knowledge and informed opinion for the professional enlightenment and growth of the men and women of the insurance industry.

Cover design: Roberta Lawrence

Departments

4 Update

7 In your corner

9 Tech talk

17 Sales and marketing

22 Readers’ service & advertising index

23 Officers and directors directory

Statements of fact and opinion in PIA magazine are the responsibility of the authors alone and do not imply an opinion on the part of the officers or the members of the Professional Insurance Agents. Participation in PIA events, activities, and/or publications is available on a nondiscriminatory basis and does not reflect PIA endorsement of the products and/or services.

President and CEO of PIA Management Services Inc. Mark LaLonde, CPIA, CIC, AAI, Communciation Director Mary E. Christiano, Senior Magazine Designer Sue Jacobsen, Member Information Manager Jaye Czupryna, Advertising Sales Executive Susan Newkirk.

Postmaster: Send address changes to: Professional Insurance Agents of Tennessee, 504 Autum Springs Court, Suite A-2, Franklin, TN 37067.

“Professional Insurance Agents” is published quarterly by PIA Management Services Inc. PIA Management Services, 25 Chamberlain St., P.O. Box 997, Glenmont, NY 12077-0997; toll-free (800) 424-4244; email [email protected].

© 2014 Professional Insurance Agents. All rights reserved. No material within this publication may be reproduced—in whole or in part—without the express written consent of the publisher.

11Trends

for 2014What’s in store for professional, independent insurance agents?

13Think about

market dynamics How to outthink (and outperform) your competitors strategically

Feature

Cover story

4 Professional Insurance Agents/Summer 2014

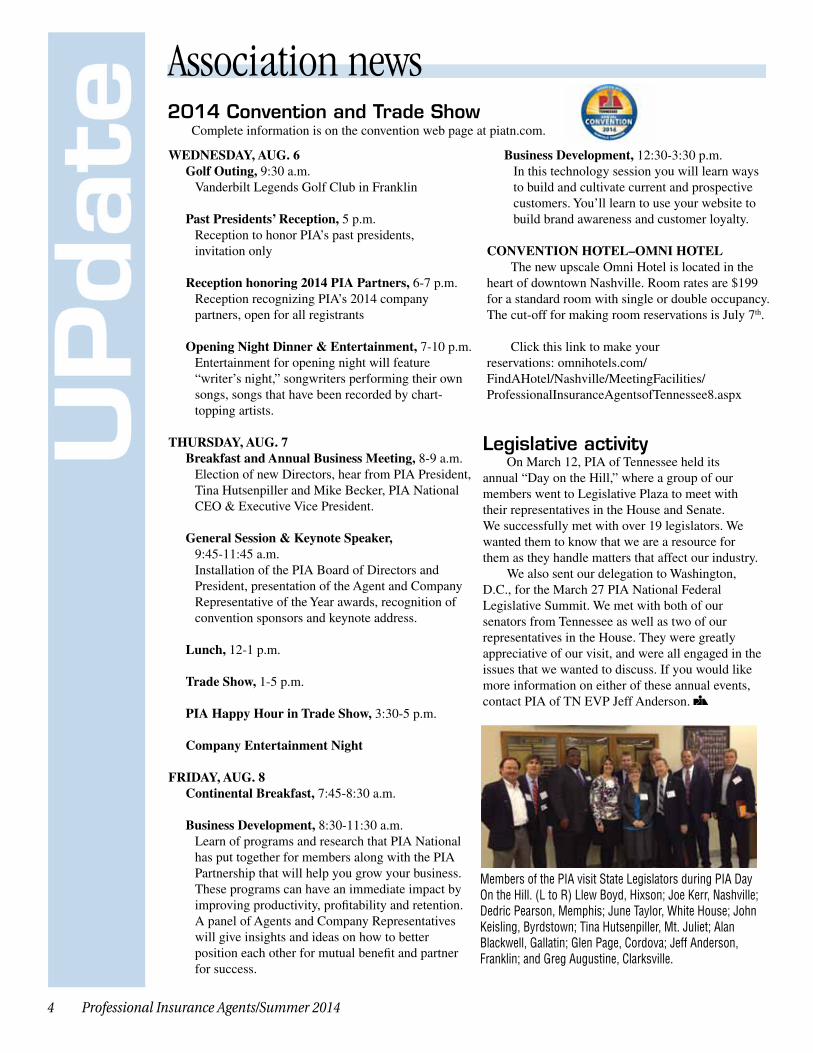

Association news

WEDNESDAY, AUG. 6 Golf Outing, 9:30 a.m. Vanderbilt Legends Golf Club in Franklin

Past Presidents’ Reception, 5 p.m. Reception to honor PIA’s past presidents,

invitation only Reception honoring 2014 PIA Partners, 6-7 p.m. Reception recognizing PIA’s 2014 company

partners, open for all registrants

Opening Night Dinner & Entertainment, 7-10 p.m. Entertainment for opening night will feature

“writer’s night,” songwriters performing their own songs, songs that have been recorded by chart-topping artists.

THURSDAY, AUG. 7Breakfast and Annual Business Meeting, 8-9 a.m. Election of new Directors, hear from PIA President,

Tina Hutsenpiller and Mike Becker, PIA National CEO & Executive Vice President.

General Session & Keynote Speaker,

9:45-11:45 a.m. Installation of the PIA Board of Directors and

President, presentation of the Agent and Company Representative of the Year awards, recognition of convention sponsors and keynote address.

Lunch, 12-1 p.m.

Trade Show, 1-5 p.m.

PIA Happy Hour in Trade Show, 3:30-5 p.m.

Company Entertainment Night

FRIDAY, AUG. 8Continental Breakfast, 7:45-8:30 a.m.

Business Development, 8:30-11:30 a.m. Learn of programs and research that PIA National

has put together for members along with the PIA Partnership that will help you grow your business. These programs can have an immediate impact by improving productivity, profitability and retention. A panel of Agents and Company Representatives will give insights and ideas on how to better position each other for mutual benefit and partner for success.

Business Development, 12:30-3:30 p.m. In this technology session you will learn ways

to build and cultivate current and prospective customers. You’ll learn to use your website to build brand awareness and customer loyalty.

CONVENTION HOTEL–OMNI HOTEL The new upscale Omni Hotel is located in the heart of downtown Nashville. Room rates are $199 for a standard room with single or double occupancy. The cut-off for making room reservations is July 7th.

Click this link to make your reservations: omnihotels.com/FindAHotel/Nashville/MeetingFacilities/ProfessionalInsuranceAgentsofTennessee8.aspx

2014 Convention and Trade Show Complete information is on the convention web page at piatn.com.

Members of the PIA visit State Legislators during PIA Day On the Hill. (L to R) Llew Boyd, Hixson; Joe Kerr, Nashville; Dedric Pearson, Memphis; June Taylor, White House; John Keisling, Byrdstown; Tina Hutsenpiller, Mt. Juliet; Alan Blackwell, Gallatin; Glen Page, Cordova; Jeff Anderson, Franklin; and Greg Augustine, Clarksville.

Legislative activity On March 12, PIA of Tennessee held its annual “Day on the Hill,” where a group of our members went to Legislative Plaza to meet with their representatives in the House and Senate. We successfully met with over 19 legislators. We wanted them to know that we are a resource for them as they handle matters that affect our industry. We also sent our delegation to Washington, D.C., for the March 27 PIA National Federal Legislative Summit. We met with both of our senators from Tennessee as well as two of our representatives in the House. They were greatly appreciative of our visit, and were all engaged in the issues that we wanted to discuss. If you would like more information on either of these annual events, contact PIA of TN EVP Jeff Anderson.

Professional Insurance Agents/Summer 2014 5

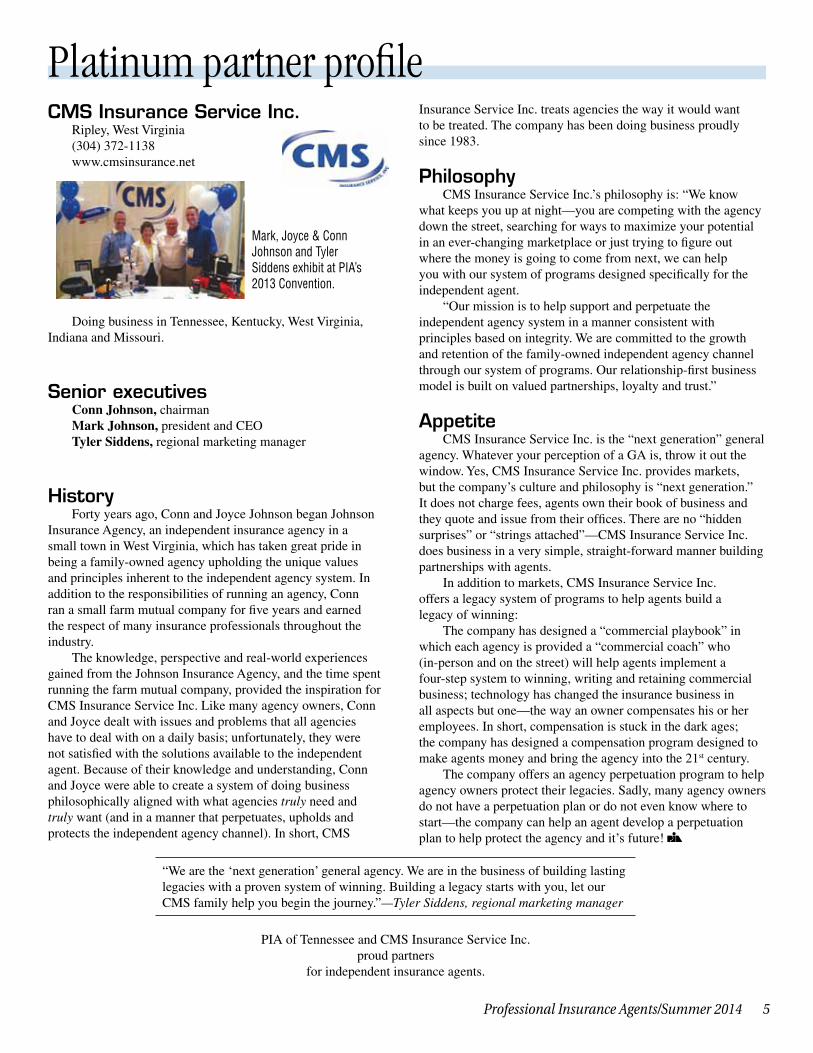

Platinum partner profileCMS Insurance Service Inc. Ripley, West Virginia (304) 372-1138 www.cmsinsurance.net

Doing business in Tennessee, Kentucky, West Virginia, Indiana and Missouri.

Senior executives Conn Johnson, chairman Mark Johnson, president and CEO Tyler Siddens, regional marketing manager

History Forty years ago, Conn and Joyce Johnson began Johnson Insurance Agency, an independent insurance agency in a small town in West Virginia, which has taken great pride in being a family-owned agency upholding the unique values and principles inherent to the independent agency system. In addition to the responsibilities of running an agency, Conn ran a small farm mutual company for five years and earned the respect of many insurance professionals throughout the industry. The knowledge, perspective and real-world experiences gained from the Johnson Insurance Agency, and the time spent running the farm mutual company, provided the inspiration for CMS Insurance Service Inc. Like many agency owners, Conn and Joyce dealt with issues and problems that all agencies have to deal with on a daily basis; unfortunately, they were not satisfied with the solutions available to the independent agent. Because of their knowledge and understanding, Conn and Joyce were able to create a system of doing business philosophically aligned with what agencies truly need and truly want (and in a manner that perpetuates, upholds and protects the independent agency channel). In short, CMS

Insurance Service Inc. treats agencies the way it would want to be treated. The company has been doing business proudly since 1983.

Philosophy CMS Insurance Service Inc.’s philosophy is: “We know what keeps you up at night—you are competing with the agency down the street, searching for ways to maximize your potential in an ever-changing marketplace or just trying to figure out where the money is going to come from next, we can help you with our system of programs designed specifically for the independent agent. “Our mission is to help support and perpetuate the independent agency system in a manner consistent with principles based on integrity. We are committed to the growth and retention of the family-owned independent agency channel through our system of programs. Our relationship-first business model is built on valued partnerships, loyalty and trust.”

Appetite CMS Insurance Service Inc. is the “next generation” general agency. Whatever your perception of a GA is, throw it out the window. Yes, CMS Insurance Service Inc. provides markets, but the company’s culture and philosophy is “next generation.” It does not charge fees, agents own their book of business and they quote and issue from their offices. There are no “hidden surprises” or “strings attached”—CMS Insurance Service Inc. does business in a very simple, straight-forward manner building partnerships with agents. In addition to markets, CMS Insurance Service Inc. offers a legacy system of programs to help agents build a legacy of winning: The company has designed a “commercial playbook” in which each agency is provided a “commercial coach” who (in-person and on the street) will help agents implement a four-step system to winning, writing and retaining commercial business; technology has changed the insurance business in all aspects but one—the way an owner compensates his or her employees. In short, compensation is stuck in the dark ages; the company has designed a compensation program designed to make agents money and bring the agency into the 21st century. The company offers an agency perpetuation program to help agency owners protect their legacies. Sadly, many agency owners do not have a perpetuation plan or do not even know where to start—the company can help an agent develop a perpetuation plan to help protect the agency and it’s future!

PIA of Tennessee and CMS Insurance Service Inc. proud partners

for independent insurance agents.

Mark, Joyce & Conn Johnson and Tyler Siddens exhibit at PIA’s 2013 Convention.

“We are the ‘next generation’ general agency. We are in the business of building lasting legacies with a proven system of winning. Building a legacy starts with you, let our CMS family help you begin the journey.”—Tyler Siddens, regional marketing manager

6 Professional Insurance Agents/Summer 2014

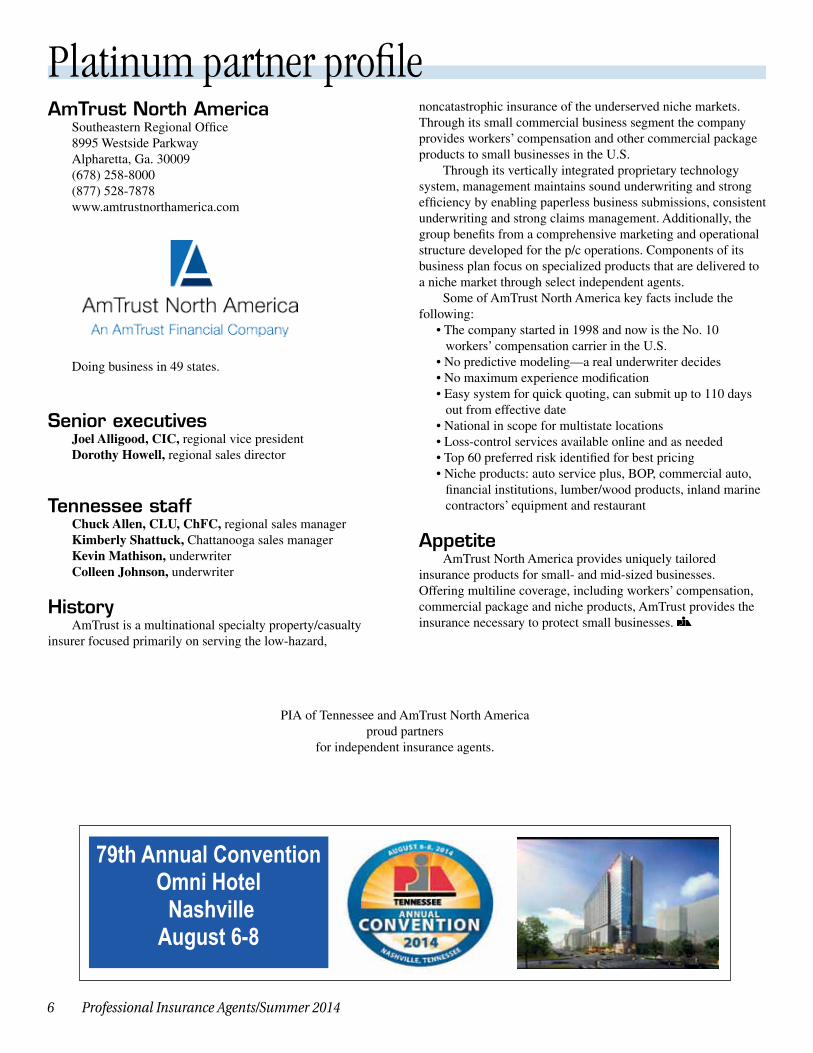

Platinum partner profileAmTrust North America Southeastern Regional Office 8995 Westside Parkway Alpharetta, Ga. 30009 (678) 258-8000 (877) 528-7878 www.amtrustnorthamerica.com

Doing business in 49 states.

Senior executives Joel Alligood, CIC, regional vice president Dorothy Howell, regional sales director

Tennessee staff Chuck Allen, CLU, ChFC, regional sales manager Kimberly Shattuck, Chattanooga sales manager Kevin Mathison, underwriter Colleen Johnson, underwriter

History AmTrust is a multinational specialty property/casualty insurer focused primarily on serving the low-hazard,

noncatastrophic insurance of the underserved niche markets. Through its small commercial business segment the company provides workers’ compensation and other commercial package products to small businesses in the U.S. Through its vertically integrated proprietary technology system, management maintains sound underwriting and strong efficiency by enabling paperless business submissions, consistent underwriting and strong claims management. Additionally, the group benefits from a comprehensive marketing and operational structure developed for the p/c operations. Components of its business plan focus on specialized products that are delivered to a niche market through select independent agents. Some of AmTrust North America key facts include the following:

• The company started in 1998 and now is the No. 10 workers’ compensation carrier in the U.S.

• No predictive modeling—a real underwriter decides• No maximum experience modification• Easy system for quick quoting, can submit up to 110 days

out from effective date• National in scope for multistate locations• Loss-control services available online and as needed• Top 60 preferred risk identified for best pricing• Niche products: auto service plus, BOP, commercial auto,

financial institutions, lumber/wood products, inland marine contractors’ equipment and restaurant

Appetite AmTrust North America provides uniquely tailored insurance products for small- and mid-sized businesses. Offering multiline coverage, including workers’ compensation, commercial package and niche products, AmTrust provides the insurance necessary to protect small businesses.

PIA of Tennessee and AmTrust North America proud partners

for independent insurance agents.

79th Annual Convention Omni Hotel Nashville August 6-8

Professional Insurance Agents/Summer 2014 7

Sullivanis senior partner of The Sullivan & Klein, LLP. He can be reached at (212) 695-0910.

Solutions in claims handling and reporting By Robert M. Sullivan, Esq.

In YourCorner

[Editor’s note: This is part two of a two-part article. Part one appeared in the Spring issue of PIA magazine. It focuses on the issues that may arise when agents take on additional responsibilities regarding claims handling.]

The easiest way to avoid errors-and-omissions liability arising from claims handling is to tell your insureds to notify the insurer of all claims or suits directly. Absent some contractual obligation in the agency or producer agreement, that certainly can be done and is common in personal lines. However, such a massive void in customer service in commercial lines would keep the agency in business for about 90 days. Insureds merely would go to competitors who would offer better service. The fact of the matter is, insureds do not expend substantial sums of money on insurance simply

to decrease their bottom line. Rather, they buy insurance coverage (usually at a level less than what you have recommended), so that they are afforded protection against loss and to protect their assets and financial well-being. If payment on a claim is denied, most insureds care little whether the denial by the carrier is justified. If the insured is left without insurance protection, the insured will look to blame the insurer and the agent or broker, the latter for failing to obtain requested insurance. Therefore, the mission is to ensure that

Help Build Your Family’s Financial Future With

PIA Trust Insurance PlansINSURANCE PLANS DESIGNED WITH LOCAL AGENTS IN MIND

As a PIA Member* serving Main Street America, you and your employees have access to a variety of high-

quality, competitively priced insurance plans.

Plans available include:

Basic Term Life** Voluntary Term Life Dependent Term Life Hospital Indemnity Long Term Disability Short Term Disability

Business Overhead Expense Accidental Death & Dismemberment

PIA SERVICES GROUPINSURANCE FUND

For more information about PIA Trust Insurance Plans, please contact your local PIA Affiliate or call the Plan Administrator at 1-800-336-4759. Additional information is also available on-line at www.piatrust.com.

Policies or provisions may vary or be unavailable in some states. Policies have exclusions or limitations which may affect any benefits payable.Underwritten by Unimerica Insurance Company, Portland, ME. Administered by Lockton Risk Services.

*PIA National membership, when required, must be current at all times.**Only available if 100% employer paid and if the employer and 100% of the employees enroll.

No medical underwriting necessary up to guaranteed issue limits.

8 Professional Insurance Agents/Summer 2014

insurers pay legitimate claims, which eliminates needless E&O claims.

The claim presentation Agents and brokers have to do a great deal of work when placing coverage. The insured has to be interviewed (hopefully), underwriting information has to be obtained (hopefully), exposures have to be identified (hopefully), and applications and submissions have to be made to the insurer. Yet, we would submit, the most important consideration in the insuring process—ensuring that a claim is honored by an insurer—often is left as a clerical act and done without much thought. Print up an ACORD form, attach a lawyer’s letter or a summons and complaint and fire it off to the insurer with only a comment “Please see attached claim.” Indeed, many claims can be submitted pro forma and are self-explanatory. However, many, particularly in the commercial contract, are more complex and require the experience and problem solving of the entire account team from producer, to account executive/CSR assigned to account, to the claims person responsible for submitting the claim. What is important in order to prevent a claim from going off the rails is to avoid the temptation of submitting a pro-forma submission for a complex claim and hoping that the insurer figures it out. What is required is at least some modicum of effort to develop and submit information to the insurer in the same way underwriting information is developed in submitting the risk. Develop salient facts. When the insured reports the claim, get on the telephone and develop the basic information to implicate coverage. For example, rather than write on an ACORD form: “Insured represents worker on property fell off ladder and landed on head 2 years ago ...” wouldn’t it be important to determine:

• When the insured found out about the fall (to avoid late notice).

• What the worker was doing (e.g., clearing leaves out of a gutter or putting a new roof on the property) (to determine if any operations are excluded).

• Was there a written contract of indemnity?

• Was the worker taken to a hospital (to determine a belief in nonliability to overcome a late-notice defense)?

Involve the entire team involved with the account. The producer knows the account’s exposures best, since he or she is most likely closest to the insured and may have personal knowledge of the risk. The producer and account executives know the policy coverages on the account much better and understand the questions to ask in order to implicate coverage. Explore alternatives to indemnity. Does the fact pattern implicate other policies that conceivably apply to the loss? Is there an E&O or D&O policy that might respond to the fact pattern of the claim?

Legal issues Often in connection with the processing of claims, there are a number of legal issues that need to be recognized and addressed. One of these issues is the issuance by the insurer of a so-called “reservation of rights.” In general terms, a reservation of rights is a legal position taken by an insurer to allow the insurer to investigate a claim or defend an action without a waiver of defenses available to coverage due either to a violation by the insured of a policy condition or due to the operation of an exclusion contained in the policy. It is important to note that a reservation of rights is not the same as a disclaimer of coverage. The reservation of rights allows the insurer time to investigate the issue of coverage, but once the insurer has completed the investigation, it is incumbent upon the insurer to disclaim properly and not prejudice the insureds defense by relying upon the possibility of coverage. Indeed, in New York, with respect to personal injury and wrongful death claims, there is a specific statute that requires an insurer to issue a prompt disclaimer.1 Sometimes, a reservation of rights and/or a disclaimer can be pro forma and about which not much can be done. For example, if the complaint contains an allegation of fraud or punitive damages, these generally are not insurable anyway, so there is

no purpose in trying to contest them. However, substantive reservations that may result in no coverage such as late notice or perhaps a construction or employee exclusion, need to be addressed promptly if they are in error. Otherwise when it comes time to pay a judgment or settle the case (i.e., when the insurer’s money is needed), the insured will not have any recourse.

All is not lost Even if a disclaimer is valid, often the disclaimer can be overcome if the insured already has undertaken the insured’s defense without having issued a reservation of rights. Courts view the right of an insured to mount its own defense as sacred. However, where the insurer has deprived the insured of that right while at the same time leading the insured into believing its right to a defense and indemnity would continue, the courts will stop the insurer from disclaiming. In addition, as noted in the preceding section, an insurer can be deemed to have waived its right to disclaim by mere delay in issuing its disclaimer. The point to be made here is that there are ways to trigger coverage based upon procedural errors in the insurer’s handling of the claim that can inure to the insured’s benefit. This also inures to the agent or broker’s benefit as well by avoiding the inevitable E&O claim.

Conclusion The reality is that most all insurance agencies or brokerages take on the function of dealing with the claims of their insureds, to some degree. The level of involvement is dependent upon the firm’s business model and desire to offer enhanced services to its clients. We hope that the take-away from our discussions is that undertaking claims handling imposes certain obligations upon an agent or broker that must be addressed with the same attention to detail that the original placement of coverage received. Taking steps to ensure that a claim is processed properly can be an excellent loss-prevention strategy to protect against E&O claims.

1 N.Y. Ins. Law §3420

Professional Insurance Agents/Summer 2014 9

Tech Talk

Corbinis PIA Management Services’ director of research.

BIC for the lessee By Dan Corbin, CIC, CPCU, LUTC

Consider the following scenario: An insured business is operating in part of a building leased from its owner. A property loss occurred at the building, but there was no damage to the premises occupied by the insured. The insured wanted to recover income lost for the time access to the business premises was denied or obstructed. What would happen if the insured’s undamaged portion of the building had to be demolished in order to comply with the local building ordinance? How could a professional, independent insurance agent write business income coverage to make the insured whole in these scenarios?

Business income Both the Insurance Services Office Inc. Businessowners Coverage Form (BP 00 03) and the Business Income and Extra Expense Coverage Form (CP 00 30) require the necessary suspension of operations to be caused by direct physical loss to property located at the premises described on the declarations. In the cases presented above, there was no damage to that part of the building occupied by the insured or to personal property belonging to the insured. Obviously, standard business income coverage is not going to produce the result the insured desired.

Civil authority Civil authority coverage does not require damage to property at the described premises, so this additional coverage may offer some benefit. A civil authority could be the fire department, the police or the town building department. One court said that the term encompasses “civil officers in whom a portion of the sovereignty is vested and in whom the enforcement of municipal regulations or the control of the general interest of society is confided.” Access to the insured premises must be denied, not just impaired, because there is damage to property located off the insured’s premises, which was caused by an insured peril. Denial of access must be in response to a dangerous condition caused by damage to

the property or to give the civil authority unimpeded access to the damaged property. If a building inspector denies occupancy of the insured’s premises while reconstruction of the building takes place, civil authority coverage will be triggered. However, if occupancy is permitted, but access is restricted to a more inconvenient route, civil authority coverage will not be triggered. Depending on the circumstances, the insured may recover income lost for up to four weeks. Better yet, this time limit can be extended up to 180 days by means of the Civil Authority Increased Coverage Period (CP 15 32) endorsement.

Dependent property Let’s suppose that access to the insured’s premises has not been denied. Nevertheless, sales decline because the other business where damage occurred in the building had to cease operations and the insured depends on the customer traffic generated by the other business. This other business is called a “leader location” and lost income resulting from physical damage to a “leader location” caused by a covered cause of loss can be recovered by means of the Business Income From Dependent Properties–Broad Form (CP 15 08) endorsement.¹ The endorsement reads as follows:

The “suspension” must be caused by direct physical loss of or damage to “dependent property” at the premises described in the Schedule caused by or resulting from a Covered Cause of Loss.

“Dependent property” means property operated by others whom you depend on to: … d. Attract customers to your business (Leader Locations).

This is a great solution to the business income loss when property damage occurs to “dependent property.” Unfortunately, this coverage may not

10 Professional Insurance Agents/Summer 2014

go far enough for all scenarios. The endorsement contains the following exclusion:

“Period of restoration” does not include any increased period required due to the enforcement of or compliance with any ordinance or law that: a. Regulates the construction, use or repair, or requires the tearing down, of any property. …

If a building ordinance requires the entire building to be demolished, including the insured’s undamaged premises, there will be no recovery of income lost after the date when the property at the premises of the “dependent property” should be repaired,

rebuilt or replaced with reasonable speed and similar quality (which does not include the additional time to comply with the ordinance). As a result, there will be a business income coverage gap.

Ordinance or law At this point, you might suggest adding the Ordinance or Law–Increased Period of Restoration (CP 15 31) endorsement in order to fill the gap. However, the endorsement specifically states that it modifies the Business Income and Extra Expense Coverage Form (CP 00 30), with no mention of the Business Income from Dependent Properties–Broad Form (CP 15 08) endorsement. In addition, the CP 15 31 endorsement states that income loss resulting from the enforcement of an

ordinance or law is covered only “if a Covered Cause of Loss occurs to property at the premises described in the Declarations.” Darn, we just can’t get there from here.

Described premises Oh, but there is a way to have it all. (Aren’t you glad you stuck with me and kept reading this article?) For business income coverage only, name the entire building as the described premises. Now, all coverages are triggered when damage occurs to any part of the building, not just the premises occupied by the insured. When the building is damaged, there is automatic business income coverage, eliminating the need for civil authority coverage or dependent property coverage. If the policy is endorsed with the Ordinance Or Law–Increased Period Of Restoration (CP 15 31) endorsement, that too will apply to the entire building. Don’t you love a simple solution! Yeah, I know, you still have to get the underwriter to approve it. Most will, though. I’d recommend that you make it a point from now on to designate the entire building as the described premises when applying for business income coverage and spare your client the gap in protection.

¹ The CP 15 08 endorsement follows the business income limits applicable to property damage at the insured’s premises. ISO also provides a Business Income from Dependent Properties–Limited form (CP 15 09) endorsement that insures the same type of loss, but allows designated limits that are independent of the limits applicable to the insured’s premises under the Business Income and Extra Expense Coverage Form (CP 00 30). In fact, it’s unnecessary to cover income loss from damage to property at the insured’s premises in order to insure dependent property under this endorsement.

Includes copyrighted material of Insurance Services Office Inc. with its permission. Copyright, Insurance Services Office Inc. 2012.

For Transportation visitwww.insurewithnai.com

• General Liability • Premium Finance

• Liquor Liability• Transportation

• Garage • Property

Call NAI for quick quotes or visit us on the web1 - 8 0 0 - 8 2 4 - 1 7 4 0 o r w w w . n a i 1 9 8 2 . c o m

Our primary goal has been to provide the best of service to the specialty lines insurance marketplace. Understanding the needs and providing rapid response to the independent agent has been and remains our number one priority.

Professional Insurance Agents/Summer 2014 11

Trends for 2014What’s in store for professional, independent insurance agents

By Mark Shlien

First a review: The year 2013 was good for the insurance industry. Growth in premiums was 4.2

percent. There were fewer catastrophes (no Sandy) and a good prior-year reserve. These conditions resulted in a $10.5 billion underwriting profit and a combined ratio of 95.8 vs. 100.7 in 2012. In addition, there was strong performance in financial markets, which assisted insurance carriers to improve results. For 2014, pricing may level off. Insurance agents reported a slight slowdown of commercial property/casualty pricing increases in the fourth quarter, according to The Council of Insurance Agents & Brokers’ quarterly Commercial P/C Market Index Survey. On average, pricing rose for large, medium and small accounts at a rate of 2.1 percent compared with 3.4 percent in the third quarter of 2013. What this means for professional, independent insurance agencies: Growth will need to come from new business, rather than pricing increases.

Agencies A study that looked at professional independent insurance agents in 2012 showed the number of agents actually increased to 38,500. However, the percentage of agencies has shifted to fewer small agencies (28 percent less than $150,000 in revenue) and larger agencies (4 percent with revenues from $2.5 to $9.9 million). Many small agencies have no perpetuation plans, so selling is the way they will finance their retirement. For others, the market in recent years has been a challenge, as carriers have closed smaller agencies, as they have struggled

to invest in producers or technology, or have tired of chasing new business while holding on to renewals. The shift to larger agencies creates a challenge for mid-sized agencies that do not have the carriers, technical resources or capital to compete. The need to focus on key accounts is critical larger firms will target those accounts.

Marketing The study also showed agencies have made a transition to more sophisticated marketing as all agencies that showed growth had a marketing budget and 23 percent of the budget was spent on social media. In addition, 25 percent of the agencies reported using Facebook for marketing. It is

important to use data to analyze the potential in the current book of business, in either developing niches or creating opportunities to up-sell or cross-sell. It also is important to identify growth opportunities in the agencies’ territory by accessing data available from various sources. Once that data is analyzed, agencies need to determine where and how to spend money to attract and manage leads (i.e., developing specialized niches rather than concentrating on selling general insurance).

Technology Professional, independent insurance agents should use social media and digital marketing—and so should their

Professional Insurance Agents/Summer 2014 11

12 Professional Insurance Agents/Summer 2014

customers. However, agents need to discuss the issues that may arise from technology with their customers. Cyber liability coverage is considered a “must have” for businesses. As recent national events have shown (e.g., Target’s data breach, Heartbleed, etc.), the need for businesses to safeguard their client’s personal information has never been more important.

The economy We do not expect 2014 to produce anything more than a lackluster economy and have few job gains, as well as a lower-than-anticipated GDP. More new sales will need to come from producers. It is important to have someone available to help experienced people make the transition, and new producers will need coaching and assistance on sales calls. Because producer productivity is so

critical to growing the business, many agencies now have people in part-time or full-time sales management roles.

M&A Merger and acquisition activity for 2013 showed the most active buyers were private equity firms, followed by independent agencies and regional and national brokers. Bank acquisitions have tapered off, and some banks have sold the agencies they have acquired. This trend will continue in 2014, since private equity firms believe insurance agencies have good profit potential and national and regional brokers who have the available to capital to make acquisitions. Many smaller- and mid-sized agencies will continue to sell because they do not have perpetuation plans or because their agencies have declined. As more deals are done, the resulting agents and brokers will be larger in size with the need to make more acquisitions and the structure to reach profit targets. The need to increase revenues has encouraged agency owners and managers to have annual planning sessions to strategize about how to grow the business. Discussions about hiring producers, making acquisitions, or opening new offices are helping the planning team decide what strategies are best for their organization. There still are thousands of independent agencies that are potential sellers. Additionally, there are sales people in other agencies or other companies interested in making a career change.

The marketplace For 2014, the challenges of the marketplace will not change. The potential for stronger results, though, may be greater with more sophisticated marketing, targeted sales and investing time and money in sales people. The need for the annual business planning session is important to analyzing last year’s results and making decisions about what to do in the future to improve those results.

Shlien is principal of iPeople® LLC. He can be reached at [email protected] or (202) 544-7675.

Stability. Longevity.

Integrity

Coverage available in Alabama, Arkansas, Georgia, Florida, Kentucky, Louisiana, Mississippi, North Carolina, South Carolina, Tennessee and Texas.

1-800-971-2667 • www.summitholdings.com

12 Professional Insurance Agents/Summer 2014

Professional Insurance Agents/Summer 2014 13

As Aretha Franklin says, “Think!”In today’s mile-a-minute,

e-connected, global, frenetic, here-today-gone-tomorrow world of commerce, it is no surprise that many of us don’t take enough time to think—and I mean really think, in a deep and focused way—about our business. We have become reactionary experts, essentially sucker-punched by our clients, by our competitors, by 24-hours-a-day “connectedness,” and by the pundits who espouse turn-on-a-dime flexibility as the panacea for 21st century business success. Well, the pundits are at least partially right: Flexibility is important. But, not at the expense of a well-thought strategy and a logical plan of execution. This, is at once, both the challenge and the opportunity with great potential to impact your performance and competitive position. If you are thinking to yourself, “My agency is too small to need a strategy” or “I’ve gotten this far without a plan,” you might want to consider whether you are thinking too small. Acknowledging that what got you where you are today isn’t necessarily going to get you where you want to be in the future is the first step. Committing to some form of disciplined thinking and planning process is the next. Sustained competitive advantage is linked to implementing continual change and, as both research-based and anecdotal evidence illustrate, the odds of doing that successfully plummet without a well-thought plan. According to Theodore Levitt, former editor of the Harvard Business Review, the job of every manager is to

“think rather than just to act, react or administer.” The question to consider is: How much time do you actually spend thinking versus acting and reacting? If you are almost always acting and reacting, what are the potential risks associated with not taking the time to really think? Although finding the time to think and plan often is posed as an obstacle by agency owners I’ve met, the time commitment for a structured process—similar to the one I will outline for you in this article—can be as little as 10 to 12 hours per month. That’s just three hours per week to spend working “on” your business instead of “in” your business. There are two major components to understand: strategic planning and tactical planning. Strategic planning is a thinking process that helps clarify and then merge your concept of what you want your business to achieve with the external realities of the marketplace and the internal realities of your organization. The result is vastly improved precision regarding direction and focus, and realistic assessment of your organization’s strengths, limitations, opportunities and threats. Tactical planning becomes much easier when a big picture has been defined—not just in terms of what must be accomplished, but importantly why it matters. Business planning—the combination of strategic planning and then tactical planning—sets the stage for competitive advantage. It also facilitates the integration of your plan, your people issues, and your processes into a single set of tasks specifically designed to

get your agency where you want it to go. An effective plan gathers no dust on the shelf. Rather, it is a day-to-day communication, decision-making, monitoring and tracking tool to hold yourself and your team accountable to accomplish your objectives. Here are the steps required to create a comprehensive and practical plan for your agency: Identify your vision and clarify your values. Research shows vision-driven leaders and their companies significantly outperform their competitors. Your vision has two functions. First, it serves as a source of information, involvement and motivation. Second, it both informs and guides your decisions and the choices of your staff. For example, I have a client whose vision is to “Automate, innovate, integrate and simplify.” After the management team communicated the vision clearly to the organization, it began to impact the myriad day-to-day decisions and choices they and their people were making—moving them toward their objectives. If vision is the “what” you are trying to achieve, then your values are “how” you expect your organization to behave along the way. They serve as guide posts for the members of your staff who, through their individual efforts, will collectively achieve your agency’s goals. Values are the principles by which you do business; and once established, should be nonnegotiable. As you think about your values, consider what you know to be right, as well as how you want to be perceived by others. Values are demonstrated through behavior, and behavior creates lasting

Think about market dynamicsHow to outthink (and outperform) your competitors strategically

By Mark E. Green

Professional Insurance Agents/Summer 2014 13

14 Professional Insurance Agents/Summer 2014

perceptions. Examples of core values are: trustworthiness: we do what we say; fun; customers first; and respect for individuals. Your vision and your values cannot be over communicated to your staff. In addition, they directly should influence your thinking in the four remaining steps of the planning process. Assess external market and competitive conditions and trends. The first area to explore in the external assessment is customer segmentation. That is, who your customers are now and who you want to have as your customers in the future. There are many demographic dimensions to consider here, for example, industry, revenue and location for commercial lines; and income, home value and driving record for personal lines—just to name a few. Consider psychographics—emotions, wants, fears, etc.—as well to crisply define your core customer. With deliberate focus on segmentation and the needs and expectations of your core customer, you will see opportunities more clearly. Once you’ve clearly identified your customer segments, it is time to focus on your competition. In doing this, there is value to looking at comparative strengths and weaknesses—both yours and theirs. The ultimate objective is to find ways to leverage your key strengths against their weaknesses. Although this exercise can be painful, understanding how you measure-up in terms of carriers, products, service, response time, sales skills, convenience and value-added knowledge exposes opportunities and potential liabilities that your plan should address. The final component of the external assessment is trend analysis. Here you’ll be striving to understand the trends that are taking place—in the insurance industry, among your customers, in our nation, around the world—that could have an impact on your business. What is changing around you and how can you adapt? You’ll pick this up in your trend analysis and it will help you minimize the impact of external events and capitalize on favorable developments. Assess internal structure and resources. Your organization must be structured to respond rapidly to the needs of your customers. Sounds great, but is

it? In evaluating your organization you may want to ask yourself some of these questions: Are we easy to do business with? Do we really add value, or just talk about it? How do we react when we make a mistake? The structure of your organization and the clarity of roles, responsibilities and processes within it have a direct impact on your ability to provide value and positive, differentiated customer experiences. When you consider your available resources, don’t just think about people. The resources at your disposal also might include real estate, equipment, growth capacity, service, technology, capital, intellectual capital and expertise. How you utilize them in aggregate is critical to understand, since business results are directly linked to your choices of how you acquire and deploy resources. Understanding your market segments is another important dimension in the evaluation of your resources. Think back to customer segmentation and ask yourself: Do I have the right resources in place to meet my customers’ needs? Are my sales producers and service staff sufficiently experienced in the segments we serve? Document your SLOT (strengths, limitations, opportunities, threats). Your external and internal appraisals identified concerns to be addressed and strengths upon which you can build. The thinking you did about your competition, trends, organization structure and resources highlighted areas that will have an impact on your ability to succeed in your chosen market segments. Your SLOT analysis will help you summarize these issues and begin to conceive actionable ideas to maximize your strengths and opportunities, while minimizing your limitations and threats. Strengths are defined as areas where your organization excels. Limitations usually are weak points in your organization. Opportunities represent significant and favorable situations in your markets that can help you be more successful. Threats are like ticking time bombs that must be defused before they explode and do their damage. While you may be tempted to focus on eliminating limitations, be sure to place an equal—if

not greater—emphasis on exploiting your strengths. This is how competitive advantages are built. Identify annual priorities and quarterly goals. Annual priorities are the three to four things that must happen or must be in place for you to advance the business in the next 12 months. Some examples of annual priorities are: customer service, book growth, technology, staff development, new market penetration and sales effectiveness. Ideally, your agency should have no more than four to create focus and advance the business. Your quarterly goals should be recorded in a spreadsheet, including due dates and—for each individual goal—the name of the person who will be held accountable to complete it. The results of steps one to four of the planning process now can be converted into specific, measurable and attainable goals for your agency, forming a tactical road map with quarterly accountability—perfectly aligned with your strategic thinking—that will lead you to the results you seek. As Confucius said, “A man who does not think and plan long ahead will find trouble right at his door.” Centuries later, his wisdom still holds true—particularly for many agencies in today’s market. Whether you employ two or 200, a right-sized, well-thought, appropriately executed plan dramatically will improve your competitive positioning and your performance regardless of market conditions. Find a way to remove the obstacles that are preventing you from investing an appropriate amount of time in a disciplined thinking and planning process for your agency. Your ability to outthink and outperform your competitors depends on it.

Green, founder of Performance Dynamics Group LLC, is a business growth expert who works with companies to help them escape the “Growth Trap” by implementing a proven, easy-to-use framework to run and grow the business faster and more profitably, while expending less effort and less time. He can be reached through the website, www.time-for-change.biz, or by phone at (732) 537-0381.

14 Professional Insurance Agents/Summer 2014

Professional Insurance Agents/Summer 2014 15

A.M. Best rating of “A”(Excellent) FSC “XI”

Connect with us

I AmTrusted

From answering underwriting questions to assisting in risk evaluation, AmTrust employees provide the best customer service to agents like you. That’s how you are able to provide the best small-businessinsurance coverage to your customers, and it’s why AmTrust is the 8th largest workers’compensationcoverage insurance provider in the nation with an “A” rating from A.M. Best.

to help agents provide the best coverage.

To learn more about AmTrust, visit us at amtrustnorthamerica.com or call 877.528.7878.

16 Professional Insurance Agents/Summer 2014

Flexible payment plans for any policy

■ Full payment (no installments)

■ Two payments — 50% down, one installment of 50% due three months later

■ 40/30/30 — 40% down, two installments of 30% each due every other month

■ Quarterly — 25% down, three installments of 25% each due quarterly

■ Monthly — 20% down, five installments of 16% each due monthly

Available payment plans by premium level

■ Premium up to $1,000 — full payment or two payments

■ Premium of $1,001 to $5,000 — full payment,two payments, 40/30/30 or quarterly

■ Premium greater than $5,000 — any payment option

Applicable fees

■ Service fees: No service fee will be added to theinitial payment. A $4 service fee will be added toeach installment billing.

Key Features

■ Excess over underlying E&O

■ Personal umbrella coverage for owners,partners and officers, including members of their families. Sub-limit does not affect total limit.

■ Employment practices liability providingexcess limits on a following-form basis.Sub-limit does not affect total limit.

■ Excess over business coverage

■ Defense coverage outside policy limits

■ Affordable minimum premiums for 9employees or fewer

■ One source for all excess coverages

■ Blanket protection for most risks

■ Flexibility to meet the needs of any agent, including flexible pay plans

Rating

■ Staff rating for agencies with 9 or feweremployees

■ Excess rated for agencies with 10+ employees or special acceptance categories

■ Refer to state rate pages

Coverage limits (higher limits may be available)

■ Up to $10 million for commercial and professional liability

■ Up to $5 million for personal exposures of owners and officers

Core Coverage

■ Business operations — broadened coverage and excess limits protection for agent/agency’sbusiness and employees for liability incurred as aresult of normal business activities. Policy providescoverage over an agency’s commercial generalliability or businessowners, employers liability andcommercial auto.

Coverage features

■ Personal injury

■ Libel, slander and advertising offense

■ First-dollar legal defense provided for claims not covered by underlying insurance

■ Professional liability — excess limits protectionon a following-form basis for errors and omissionsin the course of the agency’s business as aninsurance professional. Coverage can be writtenover occurrence or claims-made forms of a varietyof primary E&O carriers.

Coverage features on a following-form basis

■ Full prior-acts coverage

■ Covers any person acting in a capacity as a realestate agent or notary.

■ Options unique to this program:

• Personal coverage — broadened and excesspersonal protection for owners, partners andofficers, including members of their families.(Submit ACORD Personal Umbrella Application.)

• Employment practices liability — excess limitsprotection for liability incurred by named insuredor employees for wrongful employment practices.Coverage can be written on a claims-made basis over a number of approved EPL carriers.Maximum available as a sub-limit is $2 million.(Submit a copy of underlying EPL application.)

What is the PIA/Penn National Insuranceagents’ umbrella program?

Written

by agents

for agents.

■ Comprehensive excess insurance protection

■ Packaged in one easy-to-manage policy

■ Affordable rates

Coverage Payment Plans & Fees

Contact UsContact your local PIA producer. To find yours,visit the PIA Main Street Store at www.PIANET.com

Professional Insurance Agents/Summer 2014 17

Trust trumps all: The perfect sale By Charles A. Butler III, CPIA, CIC

Sales and Marketing

Butler is a member of PIA of Tennessee. He can be reached at (615) 351-2418 or butler111@ comcast.net.

Recently, I sold my office building—to the first prospect who looked at it. It sold for a fair price, which was much higher than similar properties in the area. In fact, I raised the price above the listing real-estate agent’s suggestion. In the negotiations, the buyer asked for some minor repairs; I complied with some and denied others. My total investment in repairs to the building was less than $1,000. The buyer is happy. I am happy. The real-estate agents are happy. Everyone is, as they say on the popular TV series Duck Dynasty, “Happy, happy, happy!” What does this have to do with selling insurance? Quite a bit. However, the sales people involved and the buyer did not have a clue about what happened. In fact, I asked my agent about the ease of the sale and his response was, “We just got lucky and had the perfect buyer matched to the right property.” I disagree. The popular sales model explains the process like this:

1.) Get the prospect’s attention.2.) Explain or demonstrate the benefits.3.) Create desire by pointing out how the product or

service satisfies the needs.4.) Finally, close the sale by asking the prospect to

take action. Most of these events did not happen in this sale. They don’t happen in many sales situations. What did happen that made this sale so easy? Was it just luck? Billions of dollars have been spent on consumer behavior research. Over the past two decades, social psychologists, behavioral economists, biologists and medical researchers have given us many new tools that reveal how consumers make decisions. Those new insights and tools, which are incorporated into CPIA Insurance Success Seminars, helped make this real-estate sale easy. They can help you close more insurance sales, too. This new research tells us that people form complicated networks of impressions. These impressions influence the success or failure of any sales process. They are important because they influence the buyer’s degree of trust in the seller. Trust is the key element of the sales process.

Consumers gather impressions constantly. Usually, these are formed below the conscious level. They are powerful and can last a lifetime. Were you ever embarrassed by someone as a child? If you recall that situation today, your face may flush, even though the incident occurred 30-plus years ago. Neuroscience studies tell us these strong emotions can be cued up and mentally replayed instantly. As a salesperson, you want to present the right cues, so your prospect is comfortable in making a decision. Wrong cues=negative emotions=mistrust=no sale. In this sale, we skimped on advertising or “getting attention.” However, an accurate written description and quality pictures are necessary when selling a tangible product like real estate. We focused on quickly building trust and making the buying experience pleasant. That can be difficult in “buyer-beware” markets, such as real estate and insurance. Here is how we targeted and used trust as our primary sales tool:

• We took time to take many photos of the furnished building, inside and out, for a web presentation on a multiple-listing site. The agent developed a quality description to accompany the photos. This is standard sales positioning, but then we went further.

• We removed furniture from the building, but left the conference room with all our business awards and photographs intact. We also left in place the artwork and photos in offices, restrooms, hallways, break room and kitchen. The idea was to establish trust and influence the buyer by showing that our customers and peers trusted us. We wanted the buyers to know we were successful in our profession. That helped establish trust, too. We wanted the buyers to know we were good people, just like themselves, so we left the artwork in place (so they could get to know us better).

• We removed our outside signage. This let the prospects begin to imagine the property as theirs, not ours.

• We gave prospects complete access to the building at any time (without their agent or us)

18 Professional Insurance Agents/Summer 2014

so they could explore and see things for themselves. We wanted them to start imagining how their office would look in this new environment. Our demonstration of trust in them was reciprocated by their trust in us. This became an important factor when their inspector claimed the roof was 13 years old. We explained it was less than one year old. We gave them the name and telephone

number of the roofer. We later learned they never called the roofer to verify our statements.

• We did little things that let them see our desire for them to be happy with their purchase. For example, I painted one small office and left my tools out, so if they visited they could see my work and smell new paint. They did visit, and were delighted that I had volunteered to

paint the little office. My agent told me this wasn’t necessary. What do you think?

• When the buyers began asking questions, we provided a notebook that detailed our improvements, and included spreadsheets with utility costs. We even told them building and neighborhood shortcomings, so they were aware of any potential problems.

We never overtly pointed out the benefits of the building (or how it would fit their needs). We did not know their needs and did not ask. We left that to their real-estate agents. We focused on earning their trust—something we focus on in all of our CPIA classes—and on letting their imagination create the desire for the building. Our real-estate agent’s job was to help their agent get any information about the building the prospective buyer wanted, even if it seemed ridiculous or was less than flattering. Our takeaway is this: The latest consumer research tells us consumers form impressions, and those impressions have meaning and value to the consumer. Those meanings and values have more influence on the sale process than any other factor—including price. What kind of impression does your agency make? What feeling does the prospect get when he or she visits? What kind of impression do you make when you meet a prospect? Your technical knowledge means nothing. Your super-duper policy means nothing, and your market access means nothing, if the prospective buyer does not trust you and your agency. Trust trumps screaming, “I am different!” Trust triggers pleasant emotions. Trust makes sales— every time.

Don’t lose grounD in a tough economyThe fact is, this is the time to invest in advertising. Now, more than ever, you need to retain existing clients and attract new ones. And, while you may lack the bottomless pockets of direct writers, well-crafted, well-placed, affordable marketing can punch through the noise and get your message out. Whether you’re looking for brand new marketing materials, our customized consumer materials or Spanish-language pieces, Think PIA first for the marketing advantage you still need to succeed.

logon to www.pia.org or call (800) 424-4244.

s • e • r • v • i • c • e • s

Professional Insurance Agents/Summer 2014 19

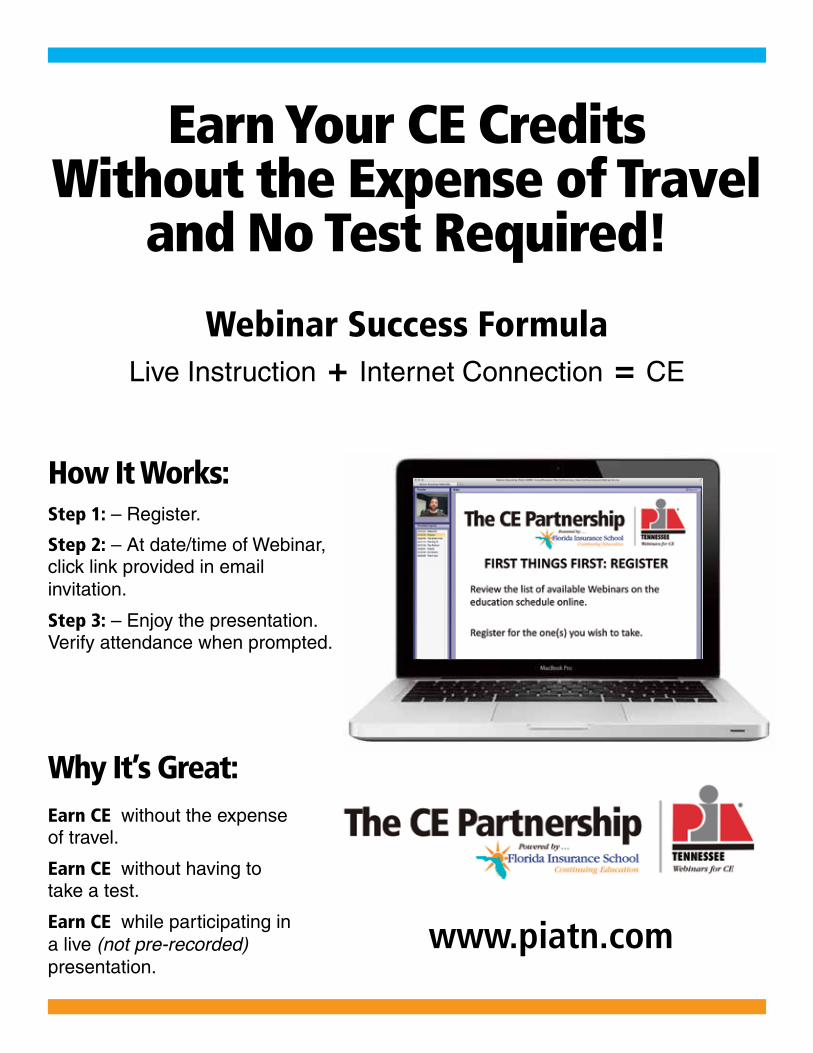

Earn Your CE Credits Without the Expense of Travel

and No Test Required!

How It Works:

www.piatn.com

Step 1: – Register.

Step 2: – At date/time of Webinar,click link provided in emailinvitation.

Step 3: – Enjoy the presentation.Verify attendance when prompted.

Why It’s Great:Earn CE without the expenseof travel.

Earn CE without having totake a test.

Earn CE while participating ina live (not pre-recorded)presentation.

Webinar Success FormulaLive Instruction + Internet Connection = CE

20 Professional Insurance Agents/Summer 2014

s • e • r • v • i • c • e • s

Looking for someone to design your exhibit materiaLs?Let PIA get you ready for the upcoming trade show. Exhibitors, make the most of your participation in PIA trade shows. Let PIA Creative Services design all your printed materials.

We speak insurance.If you’ve ever worked with an ad agency, you know the frustration of explaining your business, only to have the final product prove something was lost in the translation.

PIA Creative Services writes, designs and produces original and on‑target promotion, always building on a fundamental understanding of the insurance industry. We know creativity and we know your business. Turn to PIA Creative Services to get your message out … for a fraction of what you’d pay an outside firm.

Think PIA first for …brochures•postcards•handouts •banner stands•trade‑show booths•and more•

check out our Work onLine—www.pia.org/COMM/creative/

Susan Newkirk Advertising sales executive (800) 424‑4244, ext. 231

Phone: (800) 424-4244Fax: (888) 225-6935

Email: [email protected]: www.pia.org

1095

78

Professional Insurance Agents/Summer 2014 21

SILVER

BRONZE

AFCO Prime Rate Arlington / Roe & Co. Burns & Wilcox Utica National Insurance Group

Argos Group, Inc. Bailey Special Risks Hanover Insurance Group Mid South Mutual Insurance Co.

National Security Fire & Casualty Penn National Insurance RPS of Lexington Tennessee Underwriters

Access Insurance Co. Accident Fund Ins. Co. of America Appalachian Claims Service Applied Underwriters Bituminous Insurance Donegal Insurance Group EMC Insurance Cos. Genesee General Ink Underwriting

J.M. Wilson Kentucky National Insurance Co. Mapfre Insurance Risk Innovations Safeway Insurance Co. Sharp & Robbins Construction, LLC Southern Cross Underwriters Southern Trust Insurance Co. Tenn. Agents Alliance Group

2014 PARTNERS2014 PARTNERS2014 PARTNERS

PLATINUM

22 Professional Insurance Agents/Summer 2014

Readers’ service & advertising index

Check advertisers of interest, complete form and fax or mail to: PIATN magazine, 504 Autumn Springs Court, Suite A-2, Franklin, TN 37067.

Name ___________________________________________________________

Agency _________________________________________________________

Address _________________________________________________________

City/Town & State________________________ZIP ____________________

Phone Number ___________________________________________________

❏ 18, 20 PIA Creative Services❏ 7 PIA Trust Insurance Plans❏ 6 PIATN Annual Convention 2014❏ 19 PIATN Webinars for CE❏ 12 Summit❏ 22 Utica National Insurance Group

❏ 15 AmTrust North America❏ 2 MidSouth Mutual Insurance Co.❏ 10 M.J. Kelly of Tennessee❏ 10 NAI❏ 16 Penn National Insurance❏ BC PIA Branding Program

Continuous E&O protection since 1966.

stronger customer satisfaction

strongercoverage

strongerloss control

strongerdefense

fromthe people

who

know.504 Autumn Springs Court

Suite A-2 • Franklin, TN 37067Phone: 615-771-1177 • Fax: 615-771-3456

Contact: Sandy Clive, [email protected]: www.piatn.com

TENNESSEE

Show your true colorsShow your true colors

Enhance your ad with the impact of color. Call our sales representative at [email protected].

Professional Insurance Agents/Summer 2014 23

PIATN officers and directorsDirectoryOFFICERSPresidentTina Hutsenpiller, CPIAHutsenpiller Insurance Services LLCMt. Juliet, TN(615) [email protected]

President-electJohn Keisling, CPIA, CISRKeisling Insurance Agency Inc.Byrdstown, TN(931) [email protected]

Vice PresidentJoe Kerr, CIC, CPIAKerr Insurance ServicesBrentwood, TN(615) [email protected]

SecretaryHerbert MontgomeryClay and Land Insurance Agency Inc.Memphis, TN(901) 767-3600, ext. [email protected]

TreasurerDonnie Hogan, CICFred M. Smith & Son Inc.Springfield, TN(615) [email protected]

Immediate Past PresidentSteve PeayBoyle Insurance Agency Inc.Memphis, TN(901) [email protected]

NATIONAL DIRECTORJune Taylor, CIC, CPIA, CPIW, DAEWilkinson Insurance AgencyWhite House, TN(615) [email protected]

DIRECTORSGreg Augustine, CPIAThe Augustine Insurance GroupClarksville, TN(931) [email protected]

Llew BoydSouthern Insurance AssociatesChattanooga, TN(423) [email protected]

Carl Butcher, CIC, CPAC.L. Butcher Insurance AgencyKnoxville, TN(865) [email protected]

Andrea Bond Johnson, CPIAGolden Circle Insurance AgencyBrownsville, TN(731) [email protected]

Britt Linder, CICPeterson-Linder Insurance ServicesBartlett, TN(901) [email protected]

Chris Mills, CPCU, CICMills Insurance AgencyNashville, TN(615) [email protected]

Bill Richards, CPIA, LUTCFCommunity InsuranceGreeneville, TN(423) [email protected]

EXECUTIVE VICE PRESIDENTJeff AndersonPIA of Tennessee 504 Autumn Springs Ct, A-2Franklin, TN 37067(615) [email protected]

STAFFPam Cass, CPIAConvention, Education, Membership(615) [email protected]

Sandy Clive, CPIAE&O, Member Services(615) [email protected]

24 Professional Insurance Agents/Summer 2014

���� ��������� ���������� ����������� �������� ��������� ���������� ����������� ����

��������������������������������

���������������

�������������������������������������������������������������������

���������������������������������������������������������������

��������������������������������������������������������������

�� ����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

�� �������������������������������������������������������������������������������������������������������������������������������������������� ���������������������������������������������������������������

���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

�����������������������������������������������������������������������������������

����������������������������

�����������������������������������

�������������������������

�����������������������������

���������������������������������

�������������������������������

������������������������������

���� ��������� ���������� ����������� ����

�� ����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

�� ���������������������������������������������������������������������������������������������������������������� ��������������� ������������� ���������������������������������������������������������������

���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

�������� ������������������� ��������������������������� ����� ����� ���������������������� ��������������

��� ����������� ����� ���� ������� ���� �������� ��� ����� ������� �������� ���� ����

���������������

���������������������������������������������������������������������������

������ �� ������ ������������ ��� ������� ����� ��� ���� ���� ��� ����� ������ ������

�������������������������������������������������������������������������������

������������� ��� ������ ��� ���������� ���� ��������������������������� ������ ����

���������������

��������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������

National Association of Professional Insurance Agents400 N. Washington St. • Alexandria, VA 22314-2353(703) 836-9340 (phone) • (703) 836-1279 (fax)www.PIANET.com • [email protected]

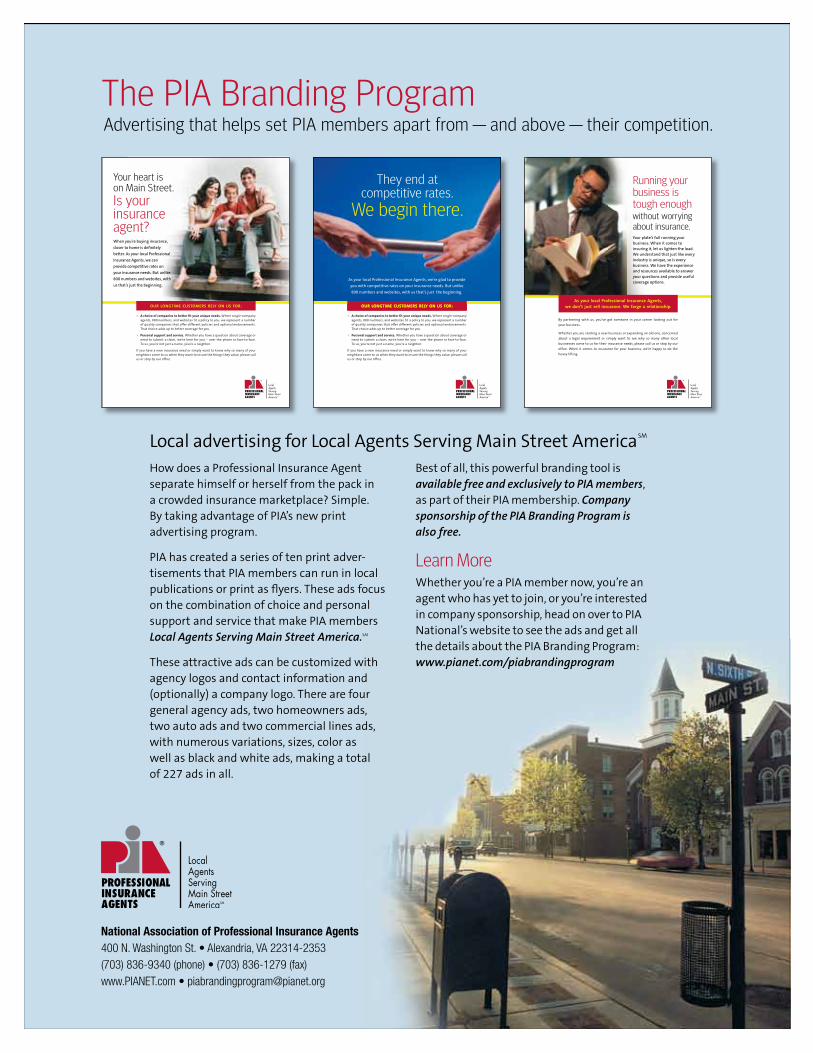

The PIA Branding Program

How does a Professional Insurance Agent separate himself or herself from the pack in a crowded insurance marketplace? Simple. By taking advantage of PIA’s new print advertising program.

PIA has created a series of ten print adver-tisements that PIA members can run in local publications or print as fl yers. These ads focus on the combination of choice and personal support and service that make PIA members Local Agents Serving Main Street America.SM

These attractive ads can be customized with agency logos and contact information and (optionally) a company logo. There are four general agency ads, two homeowners ads, two auto ads and two commercial lines ads, with numerous variations, sizes, color as well as black and white ads, making a total of 227 ads in all.

Best of all, this powerful branding tool is available free and exclusively to PIA members, as part of their PIA membership. Company sponsorship of the PIA Branding Program is also free.

Learn MoreWhether you’re a PIA member now, you’re an agent who has yet to join, or you’re interested in company sponsorship, head on over to PIA National’s website to see the ads and get all the details about the PIA Branding Program: www.pianet.com/piabrandingprogram

Advertising that helps set PIA members apart from — and above — their competition.

Local advertising for Local Agents Serving Main Street America SM