Embed Size (px)

Citation preview

In the name of Allah Who is the most beneficent

& the most merciful

Name: Nigah-e-Nazar

ID: Mc070400183

Degree: MSBA

Specialization: Finance

ACTIVITY RATIOS’ ANALYSIS OF KOHAT CEMENT, LUCKY

CEMENT AND PIONEER CEMENT IN FOR THE YEAR 2008-09-2010

Introduction of the Project

• Cement industry is indeed a highly important segment of industrial sector that plays a pivotal role in the socio-economic development. Though the cement industry in Pakistan has witnessed its lows and highs in recent past, it has recovered during the last couple of years and is buoyant once again. Activity ratio analysis to judge the financial performance of different companies whether they belong to the same industry or to the different industries is always different from each other. They vary from each other in many aspects of the recording of the transactions.

• PROJECT AIM

My Project is concern to measure the Activities ratio of Kohat Cement, Lucky Cement ,Pioneer cement for the year 2008-2009 and 2010

Objectives and Significance

• Objectives

• The reason(s) that why this company is able to manage its assets effectively.

• • The reason(s) that why this company is NOT able to manage its assets

effectively.

Significance.

• Get idea how to these companies manage their assets effectively

• Get clear picture what are various factors that companies not able to manage their assets effectively

• Data will help for both companies to understand these factors

• To fulfill my MBA degree requirement

Data Collection

Secondary Data has been used and it was collected from the

three Companies Financial statement

Data Processing

Financial ratio analysis involves the calculation and comparison of ratios

which are derived from the information given in the company's financial

statements

Date was processed and analyzed on the excel sheet for Graphically and

tabulation presentation

Data Analysis

Data was analyzed and proceed on the excel sheet. Bar

graphs were also used for interpretation of three

companies ratio analysis

Data Analysis (Cont…)

• All data are collected thorough internet with the help of following links

• http://www.luckycement.com/Financialreport%20pdf/Annual-Report-2010.pdf

• http://www.lucky-cement.com/financialreports.htm

• www.kohatcement.com/mainfinancial.htm

• http://www.kohatcement.com/pdf/30thJUNE2010.pdf

• www.researchandmarkets.com/reports/.../kohat_cement_company_ltd_08_

• http://www.kohatcement.com/pdf/30thSept2009.pdf

• http://www.pioneercement.com/accounts.html

KOHAT CEMENT LIMITED Financial Statements For Four Years.

Particulars 2010 2009 2008 2007

Rs in Thousands Rs in Thousands Rs in Thousands Rs in Thousands

Sales 3,692,038,418 3,395,580,759 1,375,972,754 1,553,733,256

Cost of sles 3,341,872,196 2,591,021,469 1,288,570,903 1,210,466,340

Gross profit 350,166,222 804,559,290 87,401,851 343,266,916

Distribution and selling

expenses 56,245,683 111,490,601 24,878,363 18,701,815

Administrative expenses 35,943,591 30,094,507 40,894,043 46,338,529

92,189,274 141,585,108 65,772,406 65,040,344

Operating Profit 257,976,948 662,974,182 21,629,445 278,226,572

Other operating Expense 4,835,758 3,291,944 20,958,970 7,640,715

253,141,190 659,682,238 670,475 270,585,857

Other operating income 23,210,906 34,218,809 35,978,496 75624748

276,352,096 693,901,047 36,648,971 346,210,605

Financial charges 658,589,707 549,902,638 48,935,320 18370018

Loss on Derivative Financial

Instruments 122,813,948 267,286,401 -

658,589,707 672,716,586 316,221,721 18,370,018

Loss/ profit before taxation (382,237,611) 21,184,461 (279,572,750) 327,840,587

KOHAT CEMENT LIMITED BALANCE SHEET FOR FOUR YEARS

Particulars 2010 2009 2008 2007

SHARE CAPITAL AND

RESERVES

Authorised Capital

150,000,000(2009 150,000000)

ord.share of Rs 10 each 1,500,000,000 1,500,000,000 1,500,000,000 15,000,000

Issued, subscribed and paid up

share capital 1,287,572,410 1,287,572,410 1,170,520,370 1017843800

Reserves 51,278,714 34,078,866 235,805,586 396306773

Accumulated Profit 622,118,747 949,895,889 922,803,191 1145242557

1,960,969,871 2,271,547,165 2,329,129,147 2,559,393,130

NON-CURRENT

LIABILITIES

Long term financing secured 3,049,320,000 2,989,387,373 2,981,785,715 2,703,308,354

Liabilities against assets subject

to finance lease secured 2,040,128 3,686,712 -

Long term Security Deposite and

retention money 155,923,337 154,209,127 135,837,621 106808320

LUCKY CEMENT LIMITED

FINANCIAL STATEMENTS OF FOUR YEARS

Particulars 2010 2009 2008 2007

Rs in Thousands Rs in Thousands Rs in Thousands

Rs in

Thousands

Sales

24,508,793

26,330,404 16,957,879 12,521,861

Cost of sles

16,529,932

16,519,138 12,595,158 8,846,706

Gross profit 7,978,861 9,811,266 4,362,721 3,675,155

Distribution and selling expenses 3,433,047 2,427,837 1,155,054 497,729

Administrative expenses 303,244 165,936 131,300 111,311

3,736,291 2,593,773 1,286,354 609,040

Operating Profit 4,242,570 7,217,493 3,076,367 3,066,115

Financial charges 569,184 1,236,971 126,743 862,847

Other operating income (1,902)

(23,255)

(1,293)

(629,289)

Other Charges 257,774 826,776 644,388 142,204

825,056 2,040,492 769,838 375,762

Profit/Loss before taxation 3,417,514 5,177,001 2,306,529 2,690,353

Taxation

Current 195,697 156,744 85,394 63,146

Prior year - 4,216

LUCKY CEMENT LIMITED BALANCE SHEET FOR FOUR YEARS

Particulars 2010 2009 2008 2007

SHARE CAPITAL AND RESERVES Issued, subscribed and paid up share

capital 3,233,750 3,233,750 3,233,750 2,633,750 Reserves 21,862,179 20,018,222 15,421,673 6,719,800 25,095,929 23,251,972 18,655,423 9,353,550

NON-CURRENT LIABILITIES Long term financing 1,658,600 4,300,000 6,633,333 8,335,604 Long term deposit 31,957 28,589 30,252 25,863 Deferred tax liability 319,217 234,633 174,171 147,245 Deferred tax tax 1,562,850 1,478,490 1,058,998 1,515,535 3,572,624 6,041,712 7,896,754 10,024,247

CURRENT LIABILITIES Trade and other payables 3,043,320 2,677,356 3,549,543 1,546,699 Accrued mark-up 155,500 233,381 288,977 326,181 Short term borrowings 6,267,112 6,187,941 3,606,710 2,864,397 Current portion of non-current liabilities 175,759 - 241,667 1,615,152 9,641,691 9,098,678 7,686,897 6,352,429

PIONER CEMENT LIMITED FINANCIAL STATEMENTS OF FOUR YEARS

Particulars 2010 2009 2008 2007

Rs in

Thousands

Rs in

Thousands

Rs in

Thousands Rs in Thousands

Sales 3,872,834 5,000,235 4,853,764 3,185,418

Cost of sles 3,953,814 3,667,343 4,340,151 2,813,309

Gross profit

(80,980) 1,332,892 513,613 372,109

Selling /Distribution expenses 158,842 359,975 466,047 108,405

Administrative expenses 78,835 97,654 89,978 86,876

General / Other expenses 168,289 277,539 149,029 7,108

Other operating income

(20,285)

(28,047)

(30,630) (11,687)

Operating Profit/ loss

(466,661) 625,771

(160,811) 181,407

Financial charges 392,658 451,465 413,203 365,848

loss / Profit before tax

(859,319) 174,306

(574,014)

(184,441)

Provision for taxation 268,394 138,192 394,043 90,947

PIONER CEMENT LIMITED BALANCE SHEET FOR FOUR YEARS

Particulars 2010 2009 2008 2007

SHARE CAPITAL AND RESERVES Authorised Share Capital 3,500,000 2,500,000 2,500,000 2,500,000 Issued, subscribed and paid up share capital 2,227,552 1,995,324 1,995,324 1,698,148 Reserves

(9,334) 405,217 310,136 398,076

Total equity 2,218,218 2,400,541 2,305,460 2,096,224

Surplus on Revalution on fixed Assets 2,120,629 2,180,889 2,239,856 574,203

NON-CURRENT LIABILITIES Long term financing secured 41,191 76,851 72,603 Laibility Against asset subject to finance lease 120,797 215,480 237,795 486,577 Long term musharika finance 50,000 Long term Deposit 1,168 1,068 1,841 5,247 Long Term Creditors Un Secured 2,348 8,731 15,114 21,497 Deferred liability 487,764 923,120 906,186 1,010,587 Long term Loan loan 466,231 1,087,583 1,701,777 2,293,709

1,078,308 2,277,173 2,939,564 3,940,220

CURRENT LIABILITIES

Creditors against expansion Project 29,594 283,428 Trade and other payables 903,936 629,132 863,265 392,894

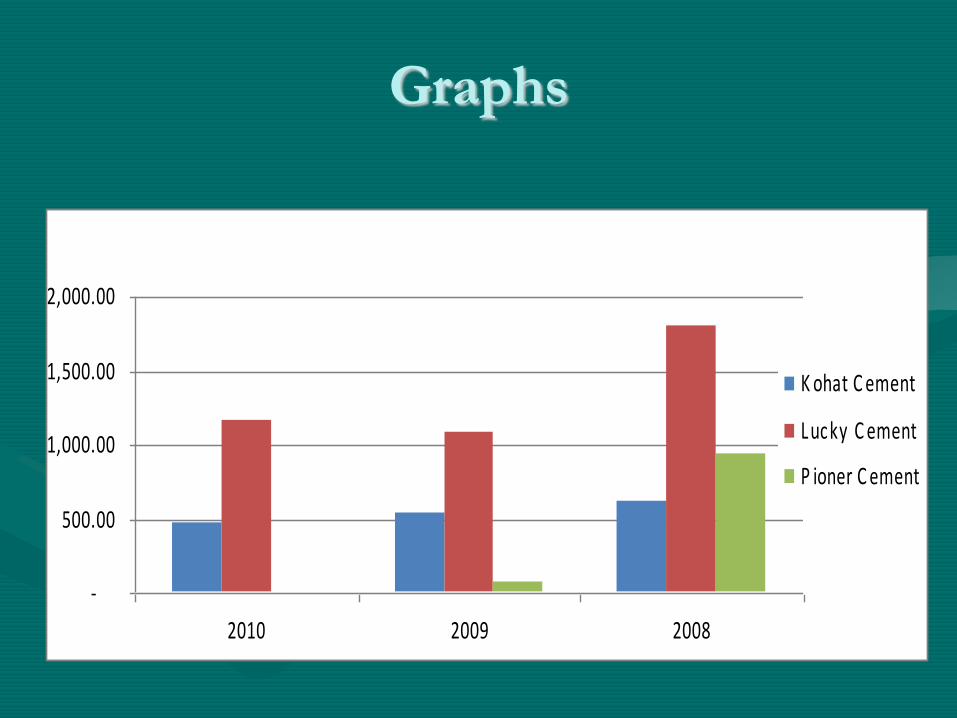

Activity Ratio Analysis Account Receivable Turnover Ratio : Total Credit Sales / Average Account Receivable

Company’s 2010 2009 2008

Kohat Cement

369,203,8418 / ((20010133+

17792165) / 2) = 195.33

times

=3395580759/((17792165+1

5341081)/2) = 204.96 times

=1375972754 /((15341081

+21381453)/2) =74.93

times

Lucky Cement 24,508,793 /

((779305+1267248)/2) =

23.95 times

=26303404/((1267248+7203

14)/2) = 26.47 times

=16957879 /

((720314+476667)/2

28.33 times

Pioneer

Cement

= 38,72,834 /

((36851+37802)/2) =

103.75 times

=5000235/

((37402+40124)/2) =

128.99 times

=4853764

/((40124+29717)/ 2)

=138.99 times

Graphs

Activity Ratio Analysis Average collection period Ratio : 365 / Receivable turnover ratio.

Company’s 2010 2009 2008

Kohat Cement

365/195.33

=1.87 Days

365/204.96

= 1.78 days

365/74.93

=4.87 days

Lucky Cement 365/ 23.95

=15.24 days

=365/ 26.47

=13.79 days

365/28.33

=12.88 days

Pioneer

Cement

365/ 103.75

= 3.52 days

365/128.99

=2.83 days

365/138.99

=2.63 days

Graph

Activity Ratio Analysis Accounts payable turnover:

Total Supplier Purchase / Average Account Payable.

Company’s 2010 2009 2008

Kohat Cement

(568942559)

/((734312487+554458612)/2)= 1

times

(375463440)/((554458612+2444

65133)/2)

=0.93 times

(146216758)

/((244465133+178982959)/2)=

0 .69 times

Lucky Cement

959358/(3043320+2677356)/2

=0.33 times

(899891)/((3549543+2677356)/2)

=0.29 times

(717439) /

((1546699+3549543)/2)

=0.28 times

Pioneer

Cement

(3953814+132072146066)/((9039

36+629132)/2)

= 5.13 times

(3667343+146066-

68691)/((863265+629132)/2)=

5.01 times

(266895) /

((392894+863265)/2)

=0.42 times

Graphs

-

500.00

1,000.00

1,500.00

2,000.00

2010 2009 2008

K ohat C ement

L ucky C ement

P ioner C ement

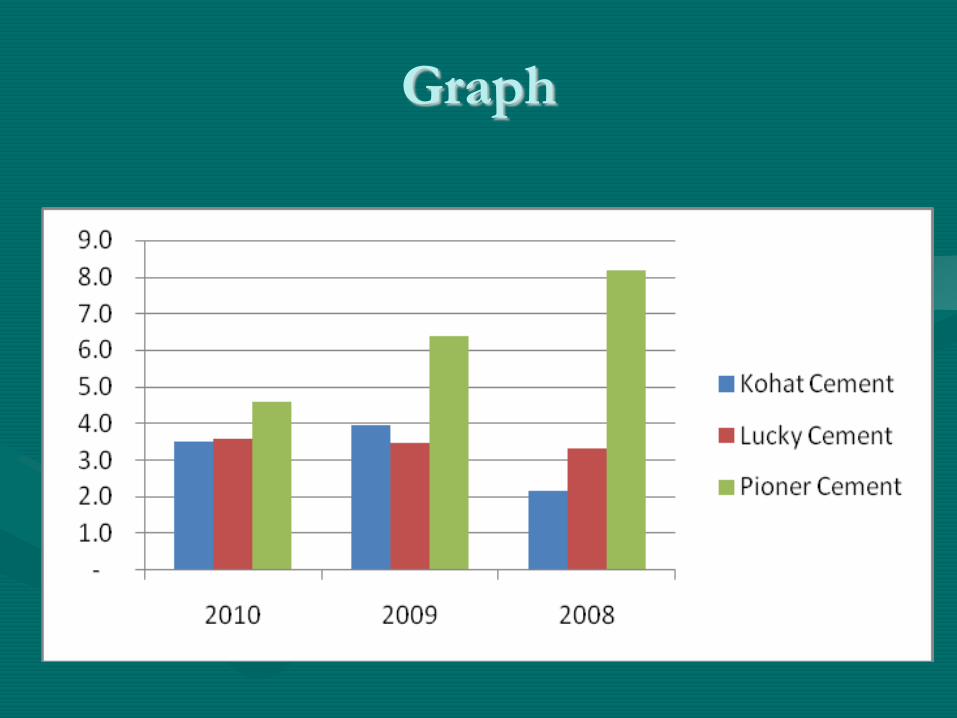

Activity Ratio Analysis Inventory turnover : Cost of goods sold / Average inventory

.

Company’s 2010 2009 2008

Kohat Cement

=3341872196

/((290433057+139293693)/2)

=15.55 times

2591021469/((174317806+13929

3693)/2)

=16.52 times

=1288570903

/((174317806+125147740)/2)

=8.6 times

Lucky Cement

16529932/((608813+1196608)/2)

=18.31 times

16519138/((1196608+709372)/2)

=17.33 times

=12595158 /

((709372+676256)/2)

=18.1 times

Pioneer

Cement

=3953814/((132072+146066)/2)=

28.4 times

=3667343/((146066+68691)/2)

=34.15 times

=4340151 /

((68691+150294)/2)

=39.6 times

Graph

-

5.0

10.015.0

20.0

25.0

30.035.0

40.0

45.0

2010 2009 2008

K ohat C ement

L ucky C ement

P ioner C ement

Activity Ratio Analysis

Inventory turnover : Cost of goods sold / Average inventory

.

Company’s 2010 2009 2008

Kohat Cement

=3341872196

/((290433057+139293693)/2)

=15.55 times

=2591021469/((174317806+1392

93693)/2

16.52 times

=1288570903

/((174317806+125147740)/2)

=8.6 times

Lucky Cement

16529932/((608813+1196608)/2)

=18.33 times

16519138/((1196608+709372)/2)

=17.33 times

=12595158 /

((709372+676256)/2)

=18.07 times

Pioneer

Cement

=3953814/((132072+146066)/2)

=28.43 times

=3667343/((146066+68691)/2)

=34.15 times

=4340151 /

((68691+150294)/2)

=39.63 times

Graph

Activity Ratio Analysis Average age of inventory = 365 days / inventory turnover. .

Company’s 2010 2009 2008

Kohat Cement

=365/ 15.6=23.4 Days

=365/16.5=22.1 Days

=365/8.6=42.4 Days

Lucky Cement

=365/ 18.3=20 Days

=365/ 17.3=21.1 days

=365/18.2=20.1 days

Pioneer

Cement

=365/28.4=12.9 days

=365/34.2=10.7 days

=365/39.6=9.2 days

Graph

-

5.0

10.0

15.0

20.025.0

30.0

35.0

40.0

45.0

2010 2009 2008

K ohat C ement

L ucky C ement

P ioner C ement

Activity Ratio Analysis

Operating Cycle = (DIO + DSO – DPO). DSO represents day sales outstanding DIO represents days inventory outstanding DPO represents days Payables outstanding DPO = (Average accounts payables / cost sales) * 365 DIO = (Average inventories / cost of sales) * 365 DSO = (Average accounts receivables / net sales) * 365

.

Company’s 2010 2009 2008

Kohat Cement

=(23.4+1.87-471)

=-445.73 days

=(22.12+1.78-539)

= -515 days

= (42.44+4.87-610 )

= - 562 days

Lucky Cement

=(19.95+15.24-1157)

= -1121days

=21.1+13.79-1085

= -1050 days

=(20.05+12.88-1805)

= -1772 days

Pioneer

Cement

=(12.85+3.51-83.74)

= -0.89 days

=(10.67+2.82-61.32)

= -1.29 days

=(9.22+2.62-935)

= -23 days

Sample for Presenting Ratio Analysis After presenting the table for working of ratio, you are

required to present the graph of that ratio

(2,000.00)

(1,800.00)

(1,600.00)

(1,400.00)

(1,200.00)

(1,000.00)

(800.00)

(600.00)

(400.00)

(200.00)

-

2010 2009 2008

K ohat C ement

L ucky C ement

P ioner C ement

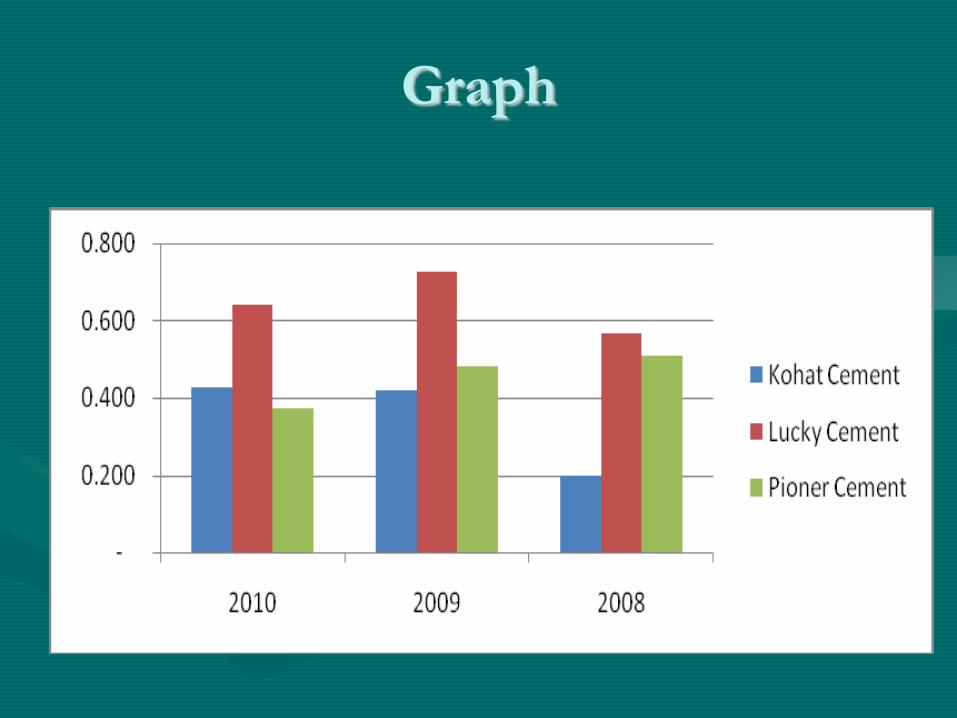

Activity Ratio Analysis Total asset turnover = Total sales / Total Assets

.

Company’s

2010 2009 2008

Kohat Cement

=3692038418

/((8673379806+8624894242)/

2)

= 0.42 times

=3395580759/((8624894242

+7623920500)/2) = 0.41

times

=1375972754

/((7623920500

+6153376959)/2) = 0.19

times

Lucky Cement

=24508793/((38310244+3839

2362)/2)

= 0.64 times

=26303404/((38,392362+34,

239074)/2)=0.724 times

=16957879 / ((34239074+

25730226)/2)

= 0.56 times

Pioneer

Cement

=3872834/((10325494+10347

734)/2)

= 0.37 Times

=5000235/((10347734+1047

2589)/2)

=0.480

=4853764

/((10472589+8610497)/2)

= 0.50 times

Graph

Activity Ratio Analysis Fixed Asset turnover = sales / Average fixed Assets

.

Company’s

2010 2009 2008

Kohat Cement

=3692038418/((7229393785+

6937818150)/2)

= 0.52 times

=3395580759/((6937818150

+6248719954)/2)

= 0.51 times

=1375972754

/((6248719954+551890568

9)/2) = 0.23 times

Lucky Cement

=24508793/((31378255+3047

6872)/2) = 0.79 times

=26303404/((25829520+304

76872)/2) = 0.93 times

=16957879 /

((20318908+25829520)/2)

= 0.73 times

Pioneer

Cement

=3872834/((8937904+925467

4)/2)

= 0.42 times

=5000235/((9254674+95708

65)/2)

= 0.53 times

=4853764 /

((7510640+9570865)/2)

= 0.56 times

Graph

Conclusion/Findings

• Three companies are performing well in their respective norms according to their mission and objectives

• At the end of 2007 2008 and 2010 the Pioneer cement and in the year ended 2008 and 2010 the Kohat Cement both have negative profit. The fact that the company has negative profit could indicate that the company will have problems in expanding.

• However, positive working capital in and of itself is good and could

indicate that the companies have less financial subsidiaries

Recommendations

1. Maintain proper budget of every accounts like sales

production labor material and other expenses.

2. Enhance the quality of the product

3. Maintain proper collection strategy and cash basis sales

can improve the cash flow of the company

4. Three companies should required to com out from the last years and

decrease previous years effect and should improve its PAT through

increasing its efficiency by reducing the operating expense down

Thank You