Embed Size (px)

Citation preview

Project Finance (part 2)

H. Scott Matthews12-706/73-359Lecture 13 - Oct. 13, 2004

Admin Issues

Facility case out - read for Monday Brief discussion on preparing cases

Midterm

Why Finance?

Time shift revenues and expenses - construction expenses paid up front, nuclear power plant decommissioning at end.

“Finance” is also used to refer to plans to obtain sufficient revenue for a project.

Note on Taxes

Companies pay tax on net incomeIncome = Revenues - ExpensesThere are several types of expenses

that we care about Interest expense of borrowing Depreciation (can only do if own the

asset) These are also called ‘tax shields’

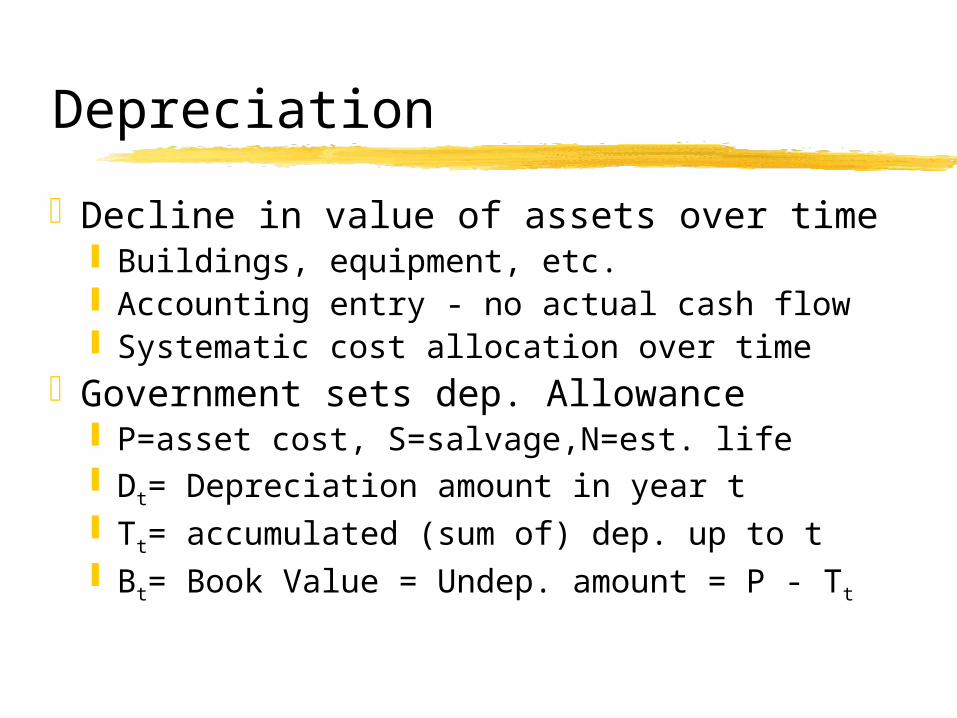

Depreciation

Decline in value of assets over time Buildings, equipment, etc. Accounting entry - no actual cash flow Systematic cost allocation over time

Government sets dep. Allowance P=asset cost, S=salvage,N=est. life Dt= Depreciation amount in year t Tt= accumulated (sum of) dep. up to t Bt= Book Value = Undep. amount = P - Tt

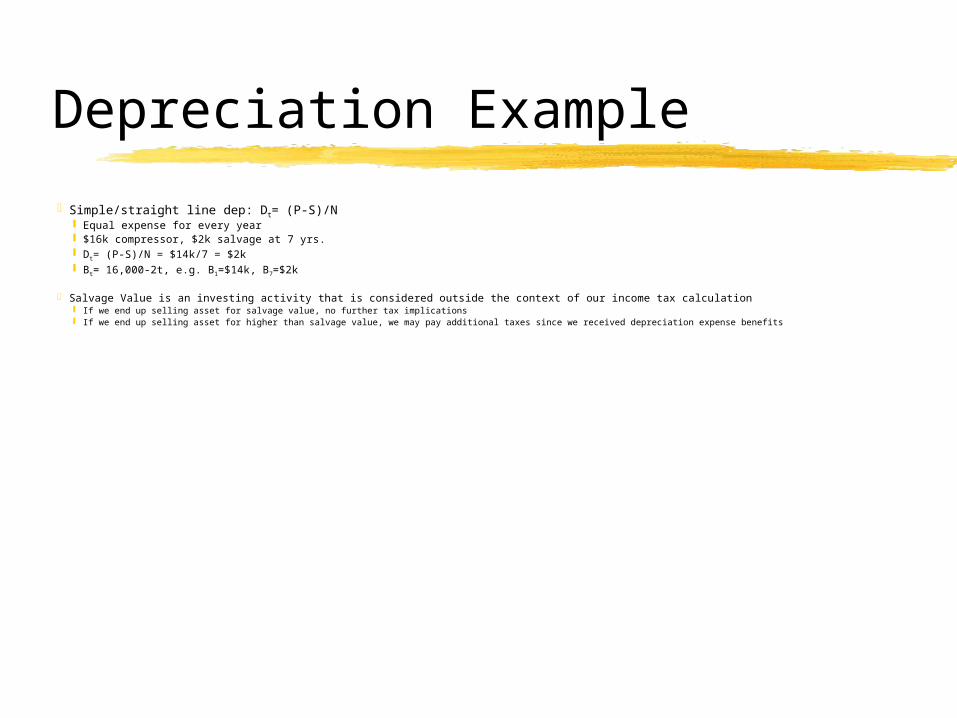

Depreciation Example

Simple/straight line dep: Dt= (P-S)/N Equal expense for every year $16k compressor, $2k salvage at 7 yrs. Dt= (P-S)/N = $14k/7 = $2k Bt= 16,000-2t, e.g. B1=$14k, B7=$2k

Salvage Value is an investing activity that is considered outside the context of our income tax calculation If we end up selling asset for salvage value, no further tax implications If we end up selling asset for higher than salvage value, we may pay additional taxes since we received depreciation expense benefits

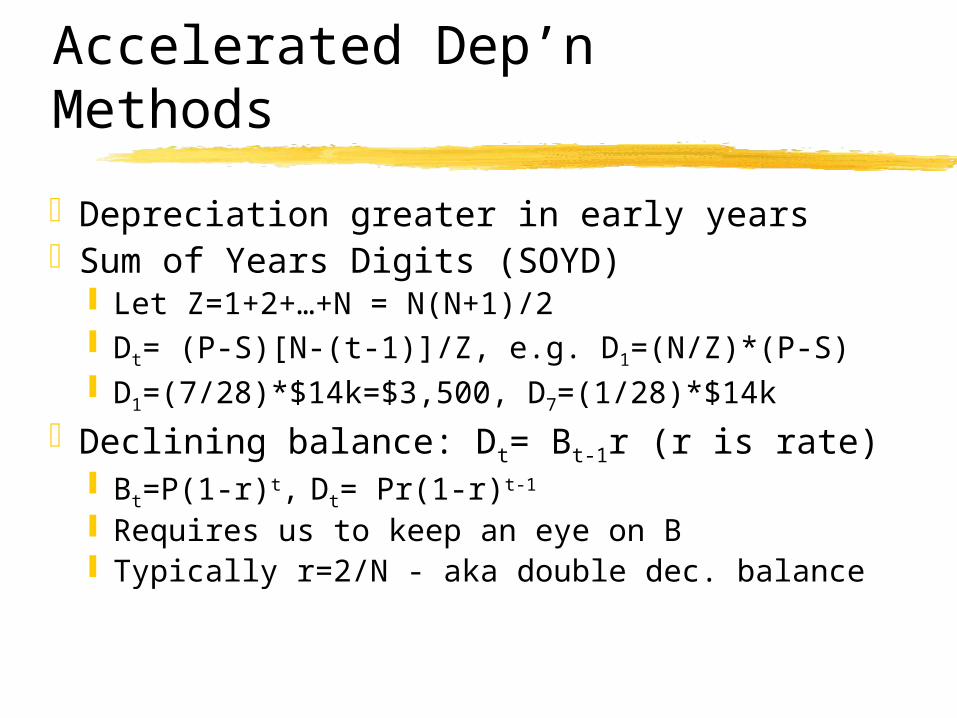

Accelerated Dep’n Methods

Depreciation greater in early yearsSum of Years Digits (SOYD)

Let Z=1+2+…+N = N(N+1)/2 Dt= (P-S)[N-(t-1)]/Z, e.g. D1=(N/Z)*(P-S) D1=(7/28)*$14k=$3,500, D7=(1/28)*$14k

Declining balance: Dt= Bt-1r (r is rate) Bt=P(1-r)t, Dt= Pr(1-r)t-1

Requires us to keep an eye on B Typically r=2/N - aka double dec. balance

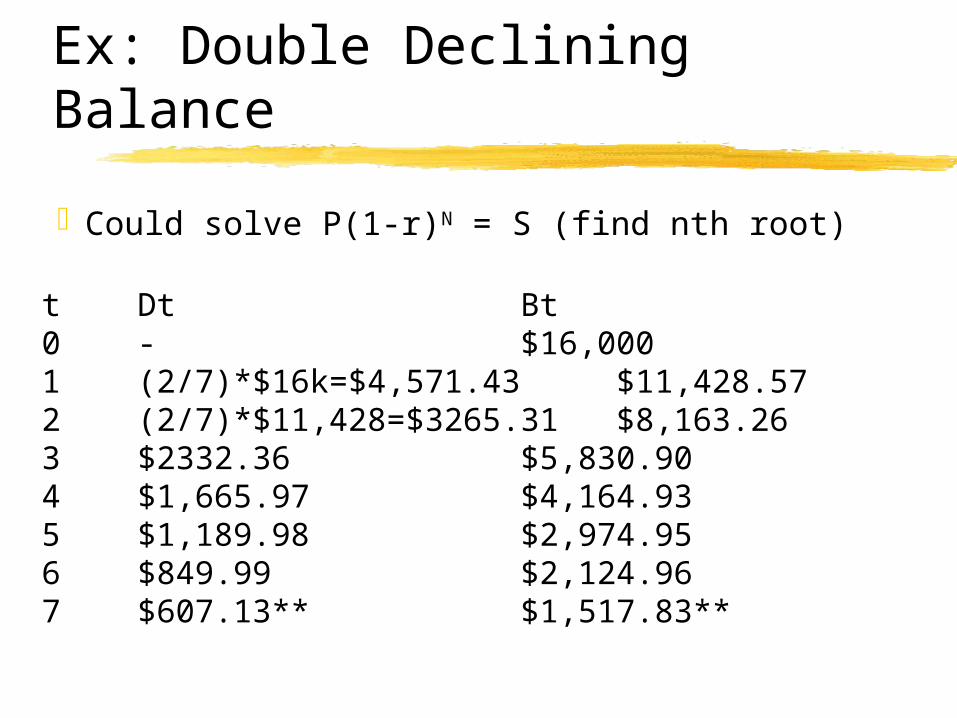

Ex: Double Declining Balance

Could solve P(1-r)N = S (find nth root)

t Dt Bt0 - $16,0001 (2/7)*$16k=$4,571.43 $11,428.572 (2/7)*$11,428=$3265.31 $8,163.263 $2332.36 $5,830.904 $1,665.97 $4,164.935 $1,189.98 $2,974.956 $849.99 $2,124.967 $607.13** $1,517.83**

Notes on Example

Last year would need to be adjusted to consider salvage, D7=$124.96

We get high allowable depreciation ‘expenses’ early - tax benefit

We will assume taxes are simple and based on cash flows (profits) Realistically, they are more complex

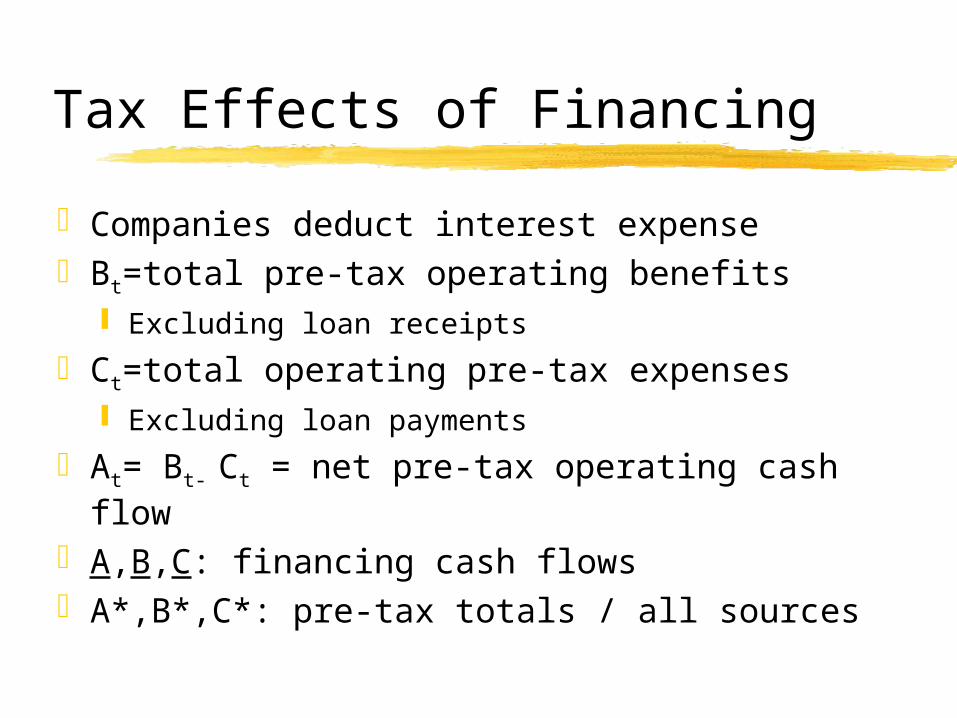

Tax Effects of Financing

Companies deduct interest expenseBt=total pre-tax operating benefits

Excluding loan receipts

Ct=total operating pre-tax expenses Excluding loan payments

At= Bt- Ct = net pre-tax operating cash flow A,B,C: financing cash flowsA*,B*,C*: pre-tax totals / all sources

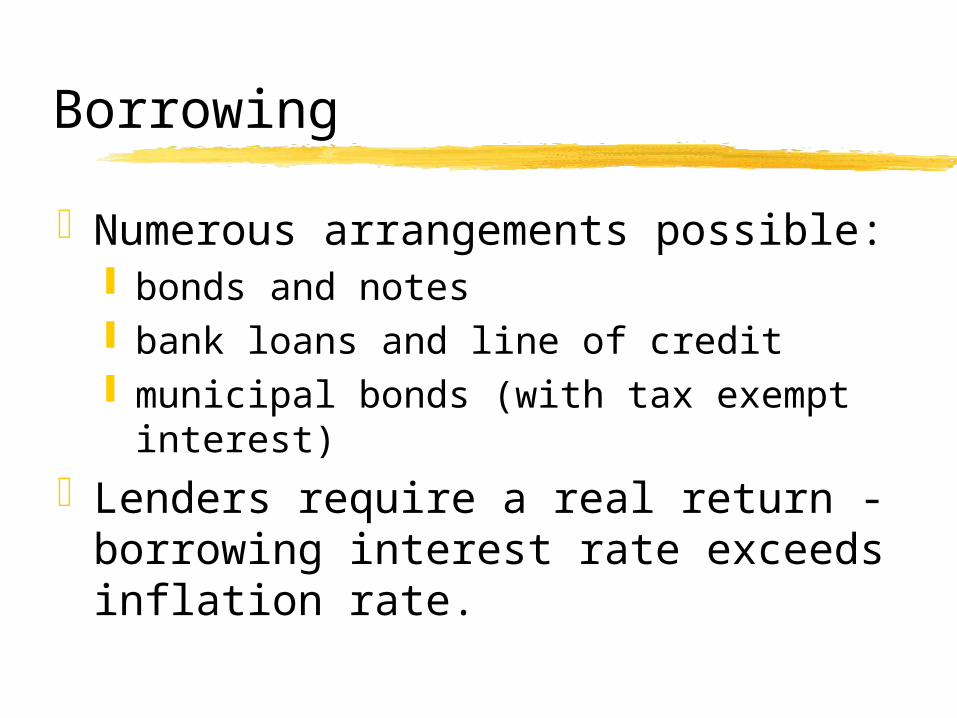

Borrowing

Numerous arrangements possible: bonds and notes bank loans and line of credit municipal bonds (with tax exempt

interest)Lenders require a real return -

borrowing interest rate exceeds inflation rate.

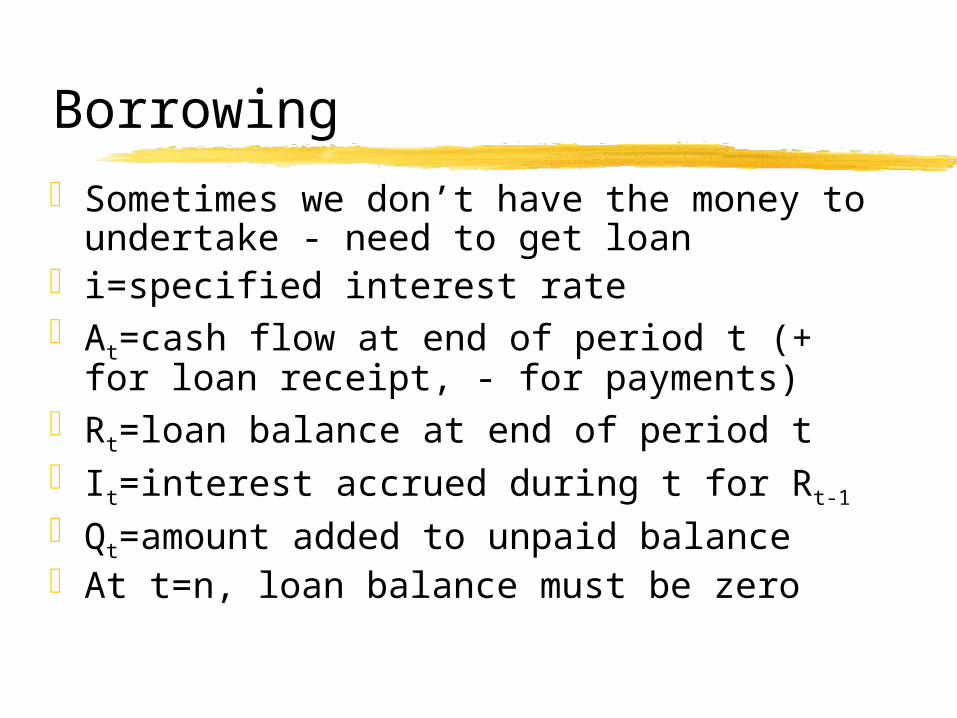

Borrowing

Sometimes we don’t have the money to undertake - need to get loan

i=specified interest rateAt=cash flow at end of period t (+ for loan

receipt, - for payments)Rt=loan balance at end of period tIt=interest accrued during t for Rt-1

Qt=amount added to unpaid balanceAt t=n, loan balance must be zero

Equations

i=specified interest rateAt=cash flow at end of period t (+ for

loan receipt, - for payments)It=i * Rt-1

Qt= At + ItRt= Rt-1 + Qt <=> Rt= Rt-1 + At + It Rt= Rt-1 + At + (i * Rt-1)

Option: Uniform payments

Assume a payment of U each year for n years on a principal of P

Rn=-U[1+(1+i)+…+(1+i)n-1]+P(1+i)n

Rn=-U[( (1+i)n-1)/i] + P(1+i)n

Uniform payment functions in ExcelSame basic idea as earlier slide

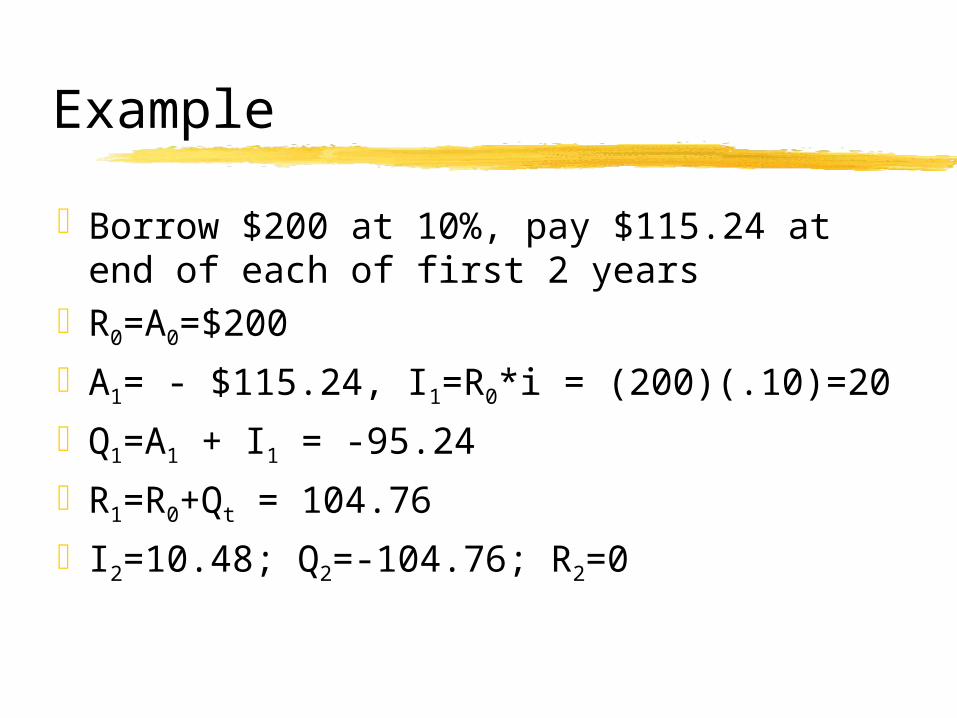

Example

Borrow $200 at 10%, pay $115.24 at end of each of first 2 years

R0=A0=$200

A1= - $115.24, I1=R0*i = (200)(.10)=20

Q1=A1 + I1 = -95.24

R1=R0+Qt = 104.76

I2=10.48; Q2=-104.76; R2=0

Repayment Options

Single Loan, Single payment at end of loan

Single Loan, Yearly PaymentsMultiple Loans, One repayment

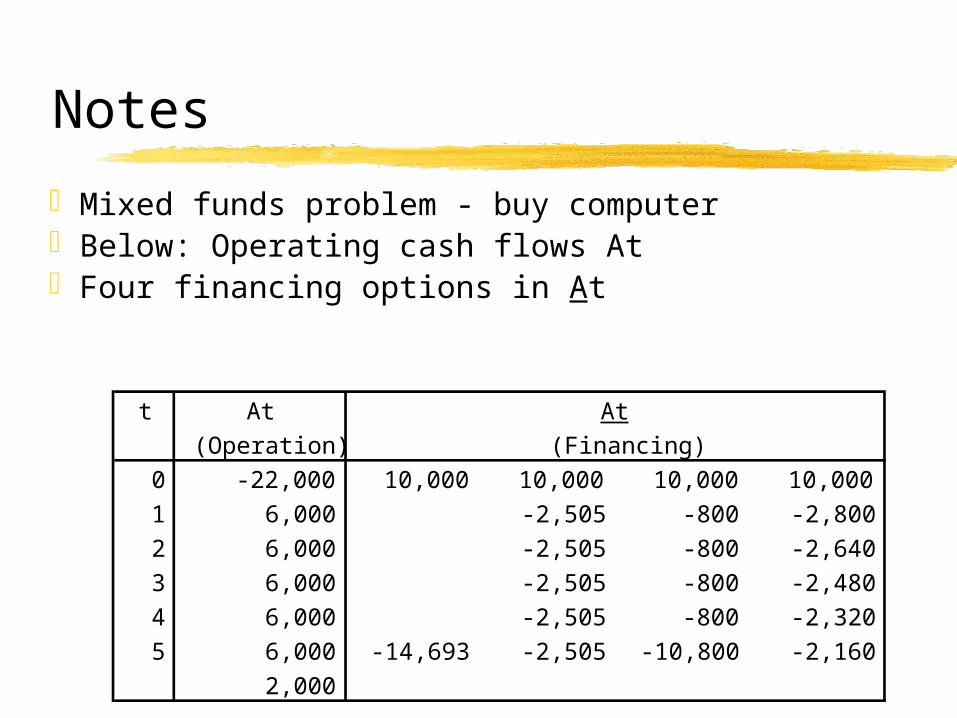

Notes

Mixed funds problem - buy computerBelow: Operating cash flows AtFour financing options in At

t At(Operation)

0 -22,000 10,000 10,000 10,000 10,0001 6,000 -2,505 -800 -2,8002 6,000 -2,505 -800 -2,6403 6,000 -2,505 -800 -2,4804 6,000 -2,505 -800 -2,3205 6,000 -14,693 -2,505 -10,800 -2,160

2,000

At(Financing)

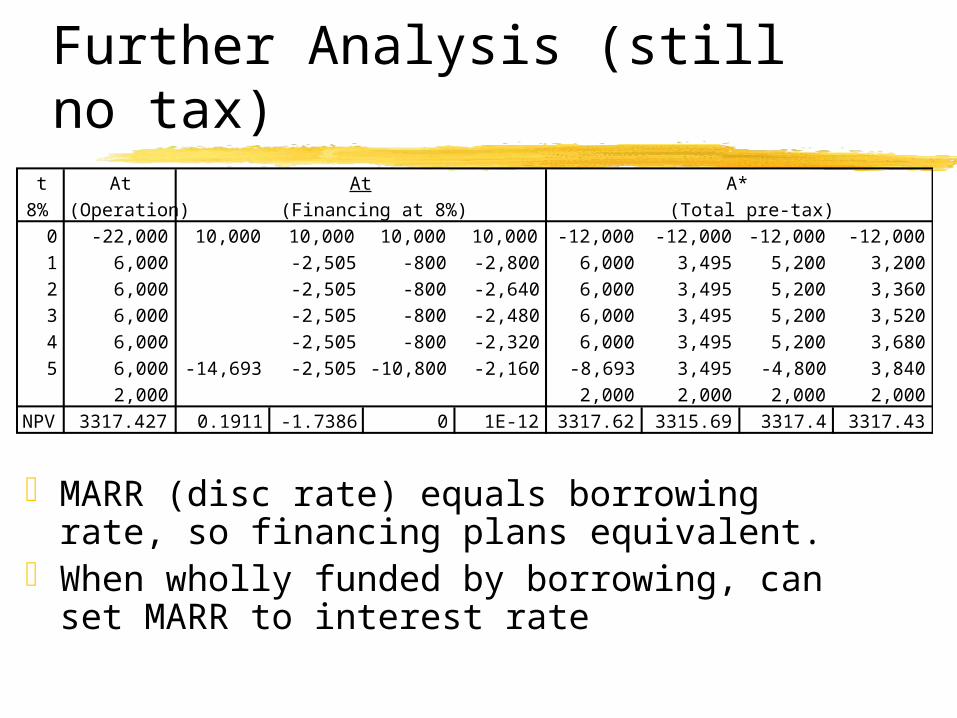

Further Analysis (still no tax)t At

8% (Operation)0 -22,000 10,000 10,000 10,000 10,000 -12,000 -12,000 -12,000 -12,0001 6,000 -2,505 -800 -2,800 6,000 3,495 5,200 3,2002 6,000 -2,505 -800 -2,640 6,000 3,495 5,200 3,3603 6,000 -2,505 -800 -2,480 6,000 3,495 5,200 3,5204 6,000 -2,505 -800 -2,320 6,000 3,495 5,200 3,6805 6,000 -14,693 -2,505 -10,800 -2,160 -8,693 3,495 -4,800 3,840

2,000 2,000 2,000 2,000 2,000NPV 3317.427 0.1911 -1.7386 0 1E-12 3317.62 3315.69 3317.4 3317.43

At(Financing at 8%)

A*(Total pre-tax)

MARR (disc rate) equals borrowing rate, so financing plans equivalent.

When wholly funded by borrowing, can set MARR to interest rate

Effect of other MARRs (e.g. 10%)t At

10% (Operation)0 -22,000 10,000 10,000 10,000 10,000 -12,000 -12,000 -12,000 -12,0001 6,000 -2,505 -800 -2,800 6,000 3,495 5,200 3,2002 6,000 -2,505 -800 -2,640 6,000 3,495 5,200 3,3603 6,000 -2,505 -800 -2,480 6,000 3,495 5,200 3,5204 6,000 -2,505 -800 -2,320 6,000 3,495 5,200 3,6805 6,000 -14,693 -2,505 -10,800 -2,160 -8,693 3,495 -4,800 3,840

2,000 2,000 2,000 2,000 2,000NPV 1986.563 876.8 504.08 758.16 483.69 2863.37 2490.64 2744.7 2470.25

At A*(Financing at 8%) (Total pre-tax)

‘Total’ NPV higher than operation alone for all options All preferable to ‘internal funding’ Why? These funds could earn 10% ! First option ‘gets most of loan’, is best

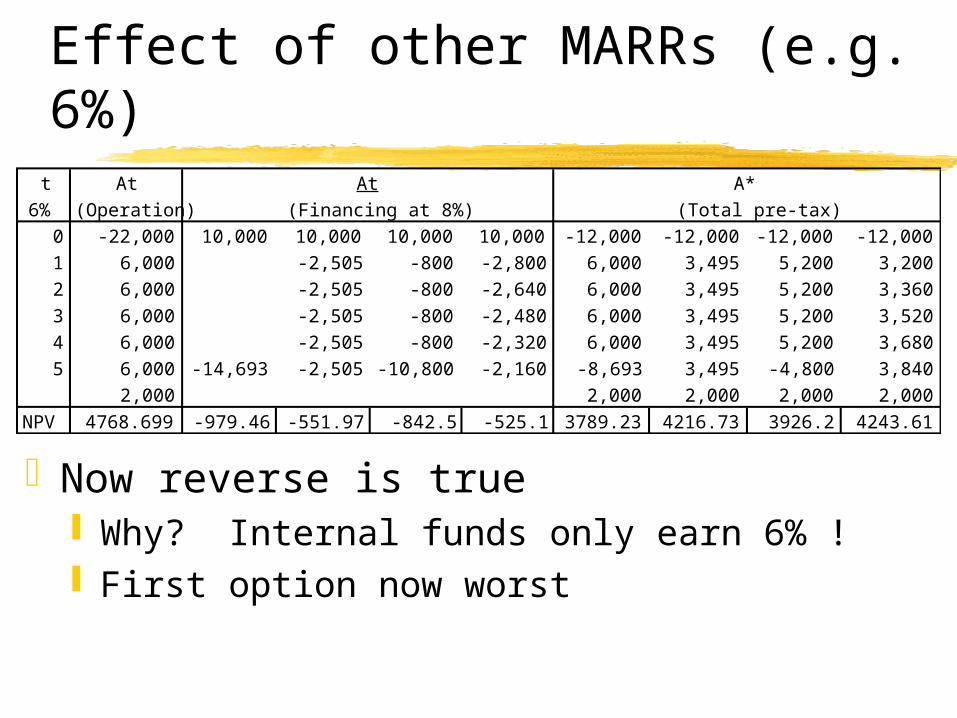

Effect of other MARRs (e.g. 6%)t At

6% (Operation)0 -22,000 10,000 10,000 10,000 10,000 -12,000 -12,000 -12,000 -12,0001 6,000 -2,505 -800 -2,800 6,000 3,495 5,200 3,2002 6,000 -2,505 -800 -2,640 6,000 3,495 5,200 3,3603 6,000 -2,505 -800 -2,480 6,000 3,495 5,200 3,5204 6,000 -2,505 -800 -2,320 6,000 3,495 5,200 3,6805 6,000 -14,693 -2,505 -10,800 -2,160 -8,693 3,495 -4,800 3,840

2,000 2,000 2,000 2,000 2,000NPV 4768.699 -979.46 -551.97 -842.5 -525.1 3789.23 4216.73 3926.2 4243.61

At A*(Financing at 8%) (Total pre-tax)

Now reverse is true Why? Internal funds only earn 6% ! First option now worst

Bonds

Done similar to loans, but mechanically different

Usually pay annual interest only, then repay interest and entire principal in yr. n Similar to financing option #3 in previous

slides There are other, less common bond

methods

After-tax cash flows

Dt= Depreciation allowance in t

It= Interest accrued in t + on unpaid balance, - overpayment Qt= available for reducing balance in t

Wt= taxable income in t; Xt= tax rate

Tt= income tax in t

Yt= net after-tax cash flow

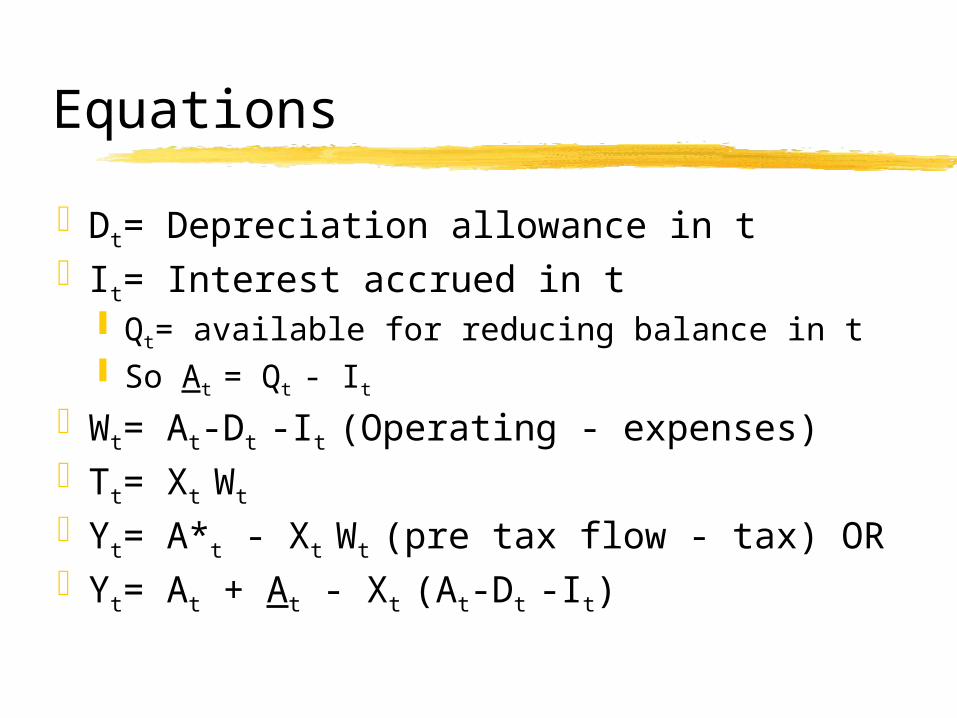

Equations

Dt= Depreciation allowance in tIt= Interest accrued in t

Qt= available for reducing balance in t So At = Qt - It

Wt= At-Dt -It (Operating - expenses)Tt= Xt Wt

Yt= A*t - Xt Wt (pre tax flow - tax) ORYt= At + At - Xt (At-Dt -It)

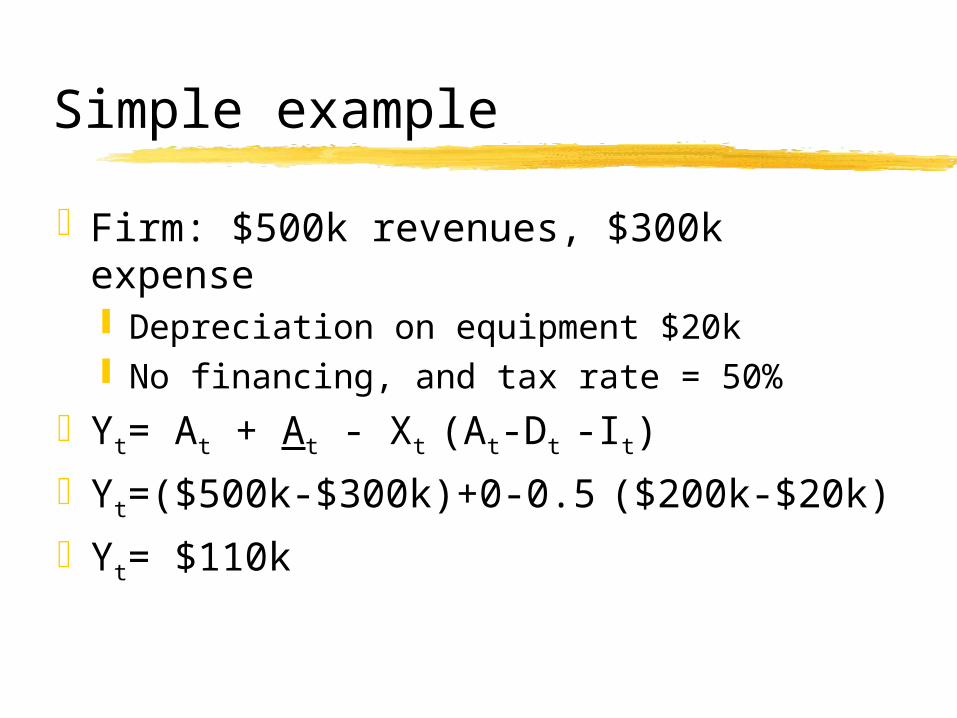

Simple example

Firm: $500k revenues, $300k expense Depreciation on equipment $20k No financing, and tax rate = 50%

Yt= At + At - Xt (At-Dt -It)

Yt=($500k-$300k)+0-0.5 ($200k-$20k)

Yt= $110k

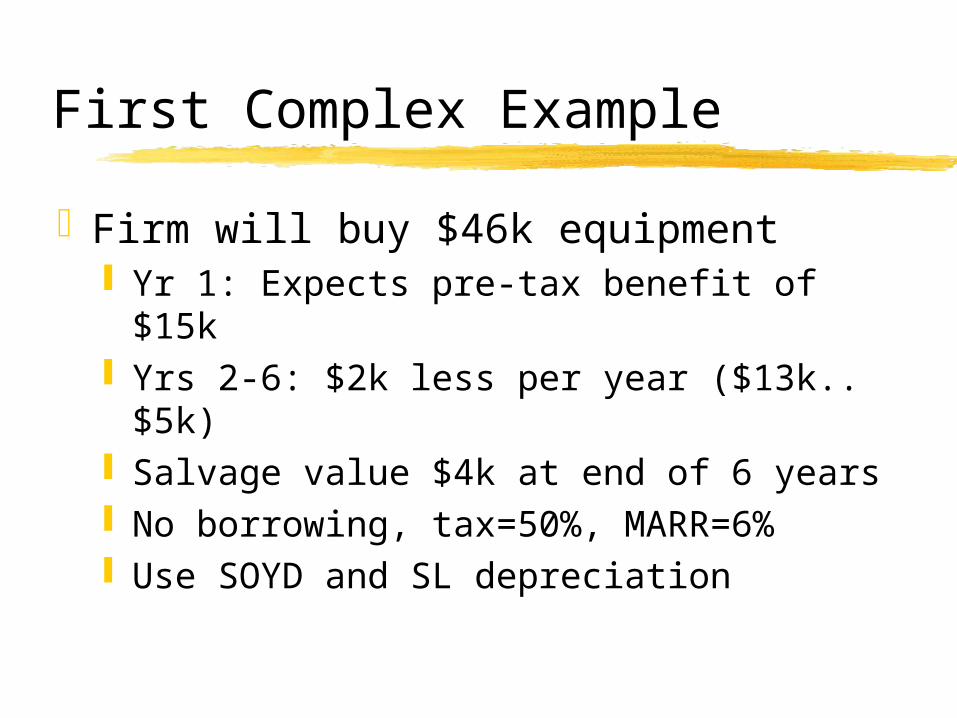

First Complex Example

Firm will buy $46k equipment Yr 1: Expects pre-tax benefit of $15k Yrs 2-6: $2k less per year ($13k..$5k) Salvage value $4k at end of 6 years No borrowing, tax=50%, MARR=6% Use SOYD and SL depreciation

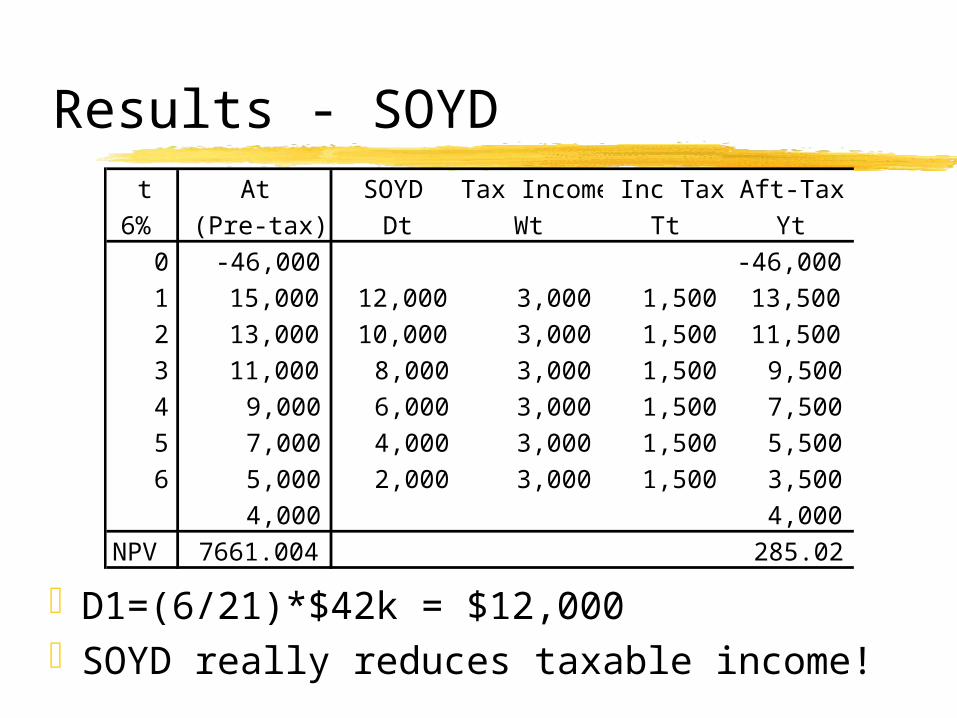

Results - SOYD

D1=(6/21)*$42k = $12,000SOYD really reduces taxable income!

t At SOYD Tax Income Inc Tax Aft-Tax6% (Pre-tax) Dt Wt Tt Yt

0 -46,000 -46,0001 15,000 12,000 3,000 1,500 13,5002 13,000 10,000 3,000 1,500 11,5003 11,000 8,000 3,000 1,500 9,5004 9,000 6,000 3,000 1,500 7,5005 7,000 4,000 3,000 1,500 5,5006 5,000 2,000 3,000 1,500 3,500

4,000 4,000NPV 7661.004 285.02

Results - Straight Line Dep.

NPV negative - shows effect of depreciation Negative tax? Typically treat as credit not cash back Projects are usually small compared to overall size of

company - this project would “create tax benefits”

t At SL Tax Income Inc Tax Aft-Tax6% (Pre-tax) Dt Wt Tt Yt

0 -46,000 -46,0001 15,000 7,000 8,000 4,000 11,0002 13,000 7,000 6,000 3,000 10,0003 11,000 7,000 4,000 2,000 9,0004 9,000 7,000 2,000 1,000 8,0005 7,000 7,000 0 0 7,0006 5,000 7,000 -2,000 -1,000 6,000

4,000 4,000NPV 7661.004 -548.9

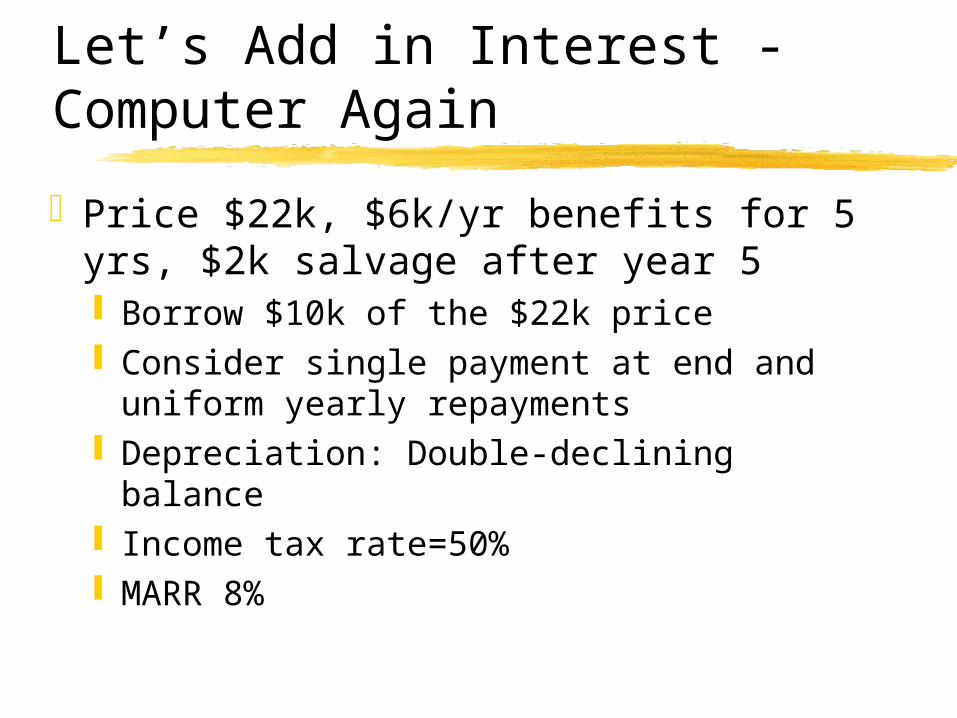

Let’s Add in Interest - Computer Again

Price $22k, $6k/yr benefits for 5 yrs, $2k salvage after year 5 Borrow $10k of the $22k price Consider single payment at end and

uniform yearly repayments Depreciation: Double-declining balance Income tax rate=50% MARR 8%

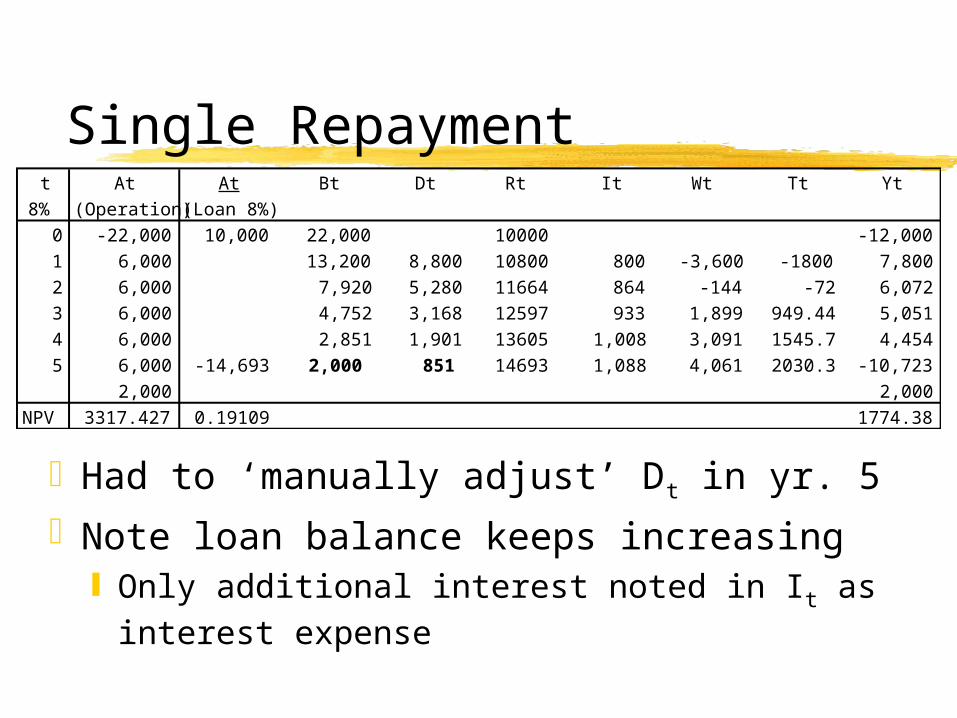

t At At Bt Dt Rt It Wt Tt Yt8% (Operation) (Loan 8%)

0 -22,000 10,000 22,000 10000 -12,0001 6,000 13,200 8,800 10800 800 -3,600 -1800 7,8002 6,000 7,920 5,280 11664 864 -144 -72 6,0723 6,000 4,752 3,168 12597 933 1,899 949.44 5,0514 6,000 2,851 1,901 13605 1,008 3,091 1545.7 4,4545 6,000 -14,693 2,000 851 14693 1,088 4,061 2030.3 -10,723

2,000 2,000NPV 3317.427 0.19109 1774.38

Single Repayment

Had to ‘manually adjust’ Dt in yr. 5Note loan balance keeps increasing

Only additional interest noted in It as interest expense

Uniform paymentst At At Bt Dt Rt It Wt Tt Yt

8% (Operation) (Loan 8%)0 -22,000 10,000 22,000 10000 -12,0001 6,000 -2,505 13,200 8,800 8295 800 -3,600 -1800 5,2952 6,000 -2,505 7,920 5,280 6453.6 664 56 28.2 3,4673 6,000 -2,505 4,752 3,168 4464.9 516 2,316 1157.9 2,3374 6,000 -2,505 2,851 1,901 2317.1 357 3,742 1871 1,6245 6,000 -2,505 2,000 851 -2.555 185 4,964 2481.8 1,013

2,000 2,000NPV 3317.427 -1.7386 974.707

Note loan balance keeps decreasingNPV of this option is lower - should

choose previous (single repayment at end).. not a general result

Leasing

‘Make payments to owner’ instead of actually purchasing the asset Since you do not own it, you can not

take depreciation expense Lease payments are just a standard

expense (i.e., part of the Ct stream) At= Bt - Ct ; Yt= At - At Xt

Tradeoff is lower expenses vs. loss of depreciation/interest tax benefits