Embed Size (px)

Citation preview

PROJECT REPORT

A STUDY ON WORKING CAPITAL MANAGEMENT AT HERO

MOTOCORP LTD. AMBICA MOTORS, GUJARAT.

SUBMITTED BY

PATEL CHARMIBEN VIMALBHAI

15P35H0256

UNDER THE GUIDANCE OF

Ms. RICHA PATHAK

ASSISTANT PROFESSOR,

DEPARTMENT OF MANAGEMENT STUDIES

NEW HORIZON COLLEGE

MASTER OF BUSINESS ADMINISTRATION

BHARATHIAR UNIVERSITY

COLLEGE CODE: KA 11 B 131

2015-2017

STUDENT’S DECLARATION

I hereby declare that this project entitled “A STUDY ON WORKING

CAPITAL MANAGEMENT AT HERO MOTOCORP, AMBICA

MOTORS” was prepared by me during the year 2016-17 and was submitted in

partial fulfillment of the requirements for Master Degree in Business

Management of Bharathiar University.

I also declare that this project report is original and genuine and has not

been submitted to any other university of the award of any degree, diploma or

other similar titles or purposes.

Date: Patel CharmibenVimalbhai

Bangalore 15P35H0256

COMPANY CERTIFICATE

To whom so ever it may concern

This is certify that Patel Charmiben Vimalbhai bearing registration

number 15P35H0256 of 3rd

semester MBA Bharathiar University, New Horizon

college, Bangalore has successfully carried out her project work on “A STUDY

ON WORKING CAPITAL MANAGEMENT AT HERO MOTOCORP,

AMBICA MOTORS”, during from 30th

June 2016 to 30th July 2016

We are satisfied with the project report and appreciate the commitment

towards the project preparations.

We wish all the best in the future.

Signature

Date:

GUIDE CERTIFICATE

This is to certify that the project report entitled “A STUDY ON

WORKING CAPITAL MANAGEMENT” submitted by Patel Charmiben

Vimalbhai bearing registration number 15P35H0256 to Bharathiar University

for the partial fulfillment of Master Degree in Business Management is an

outcome of genuine research work carried under my guidance and it has not

been submitted for the award of any other degree, diploma or prize.

Date: Ms. RICHA PATHAK

Bangalore Assistant Professor

HOD CERTIFICATE

This is to certify that Patel Charmiben Vimalbhai bearing registration

number 15P35H0256 is a bonafide student of this college. The project work

entitled “A STUDY ON WORKING CAPITAL MANAGEMENT” is a work

carried out by her for partial fulfillment of the requirements for Master Degree

in Business Management of Bharathiar University during the year 2016-2017. It

is certified that all corrections/suggestions have been incorporated in the project

report and a copy is deposited in the department library. This project work has

been approved as it satisfied the academic requirement of Master Degree in

Business Management.

Date: Dr. SHEELAN MISRA

Bangalore

PRINCIPAL’S CERTIFICATE

This is to certify that Patel Charmiben Vimalbhai bearing registration

number 15P35H0256 is a bonafide student of this college. The project work

entitled “A STUDY ON WORKING CAPITAL MANAGEMENT” is a work

carried out by her for partial fulfillment of the requirements for Master Degree

in Business Management of Bharathiar University during the year 2016-2017.

Date: Dr. R. BODHISATVAN

Bangalore

ACKNOWLEDGEMENT

While presenting the report of my project, I have great pleasure in

acknowledging the help rendered and guidance to me by various people during

the course of my project.

I would like to express my sincere thanks to my project external guide

Mr. Aashish kumar, Mr. Varunbhai (Financial manager) and Mr. Hemant

Patel manager of AMBICA MOTORS for providing me permission, guidance

and cooperation during the study period.

I would like to express my sincere thanks and gratitude to Ms. Richa

Pathak New Horizon College, Bangalore, for her excellent guidance and

support throughout this project work.

I would like to express my gratitude to all those who gave me the

possibilities to complete this report. I would like thank Dr. R.Bodhisatvan,

Principal and Dr.Sheelan Misra, HOD, NEW HORIZON COLLEGE.

Finally, I wish to thanks my family, friends, faculty members and all

others who have helped me in completing this project work successfully.

I thanks to all above the almighty for my successful completion of this

project.

CONTENTS

CHAPTER CONTENTS PAGE NO

EXECUTIVE SUMMARY

1 INTRODUCTION 1 - 21

1.1 DEFINITIONS 2 - 3

1.2 CLASSIFICATION OF WORKING

CAPITAL 4 - 6

1.3 DETERMINANTS OF WORKING

CAPITAL 6 -13

1.4 RATIO ANALYSIS 14 - 21

2 INDUSTRY AND COMPANY PROFILE 22 - 39

2.1 INDUSRTY PROFILE 22 - 30

2.2 COMPANY PROFILE 30 - 39

3 RESEARCH DESIGN 40 - 43

3.1 RESEARCH DESIGN 40

3.2 STATEMENT OF PROBLEM 40

3.3 SCOPE OF THE STUDY 41

3.4 METHODOLOGY OF THE STUDY 41

3.5 OBJECTIVES OF STUDY 41

3.6 SOURCES OF DATA 42

3.7 TOOLS OF ANALYSIS 42

3.8 LIMITATIONS OF THE STUDY 43

4

ANALYSIS AND INTERPRETATION OF

DATA 44 - 68

4.1 STATEMENT OF CHANGES IN

WORKING CAPITAL 44 - 47

4.2 RATIO ANALYSIS 48 - 68

5

FINDINGS, CONCLUSION AND

SUGGESTIONS 69 - 72

5.1 FINDINGS 69 - 70

5.2 CONCLUSION 71

5.3 SUGGESTIONS 72

BIBLIOGRAPHY

ANNEXURE

LIST OF TABLES

TABLES No. PARTICULARS PAGE No.

4.1

Calculation of statement of change in

working capital for the year 2013-14 45

4.2

Calculation of statement of change in

working capital for the year 2014-15 46

4.3

Calculation of statement of change in

working capital for the year 2015-16 47

4.4 Calculation of current ratio 49

4.5 Calculation of liquid or quick ratio 51

4.6 Calculation of absolute liquid ratio 53

4.7 Calculation of gross profit ratio 55

4.8 Calculation of operating profit ratio 57

4.9 Calculation of net profit ratio 59

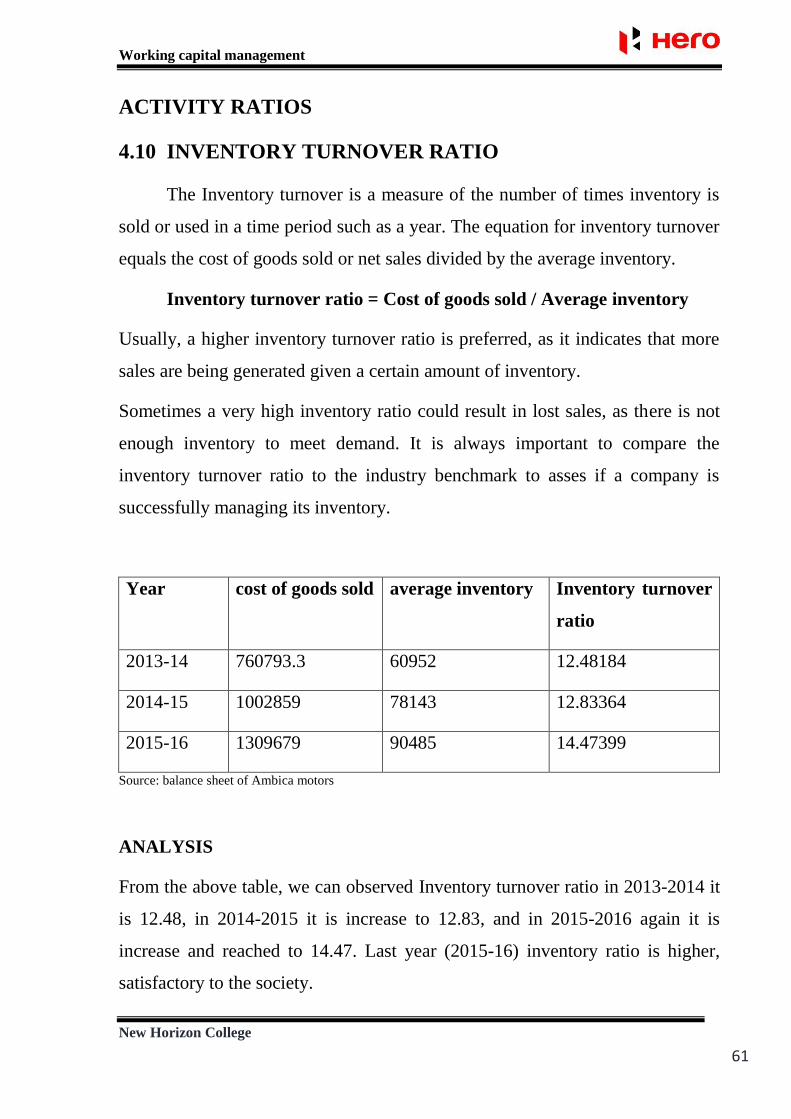

4.10 Calculation of inventory turnover ratio 61

4.11 Calculation of fixed assets turnover ratio 63

4.12 Calculation of current assets turnover ratio 65

4.13 Calculation of working capital turnover ratio 67

LIST OF GRAPHS

TABLES PARTICULARS PAGE.NO

4.1 Chart showing current ratio 50

4.2 Chart showing quick ratio 52

4.3 Chart showing absolute liquid ratio 54

4.4 Chart showing gross profit ratio 56

4.5 Chart showing operating profit ratio 58

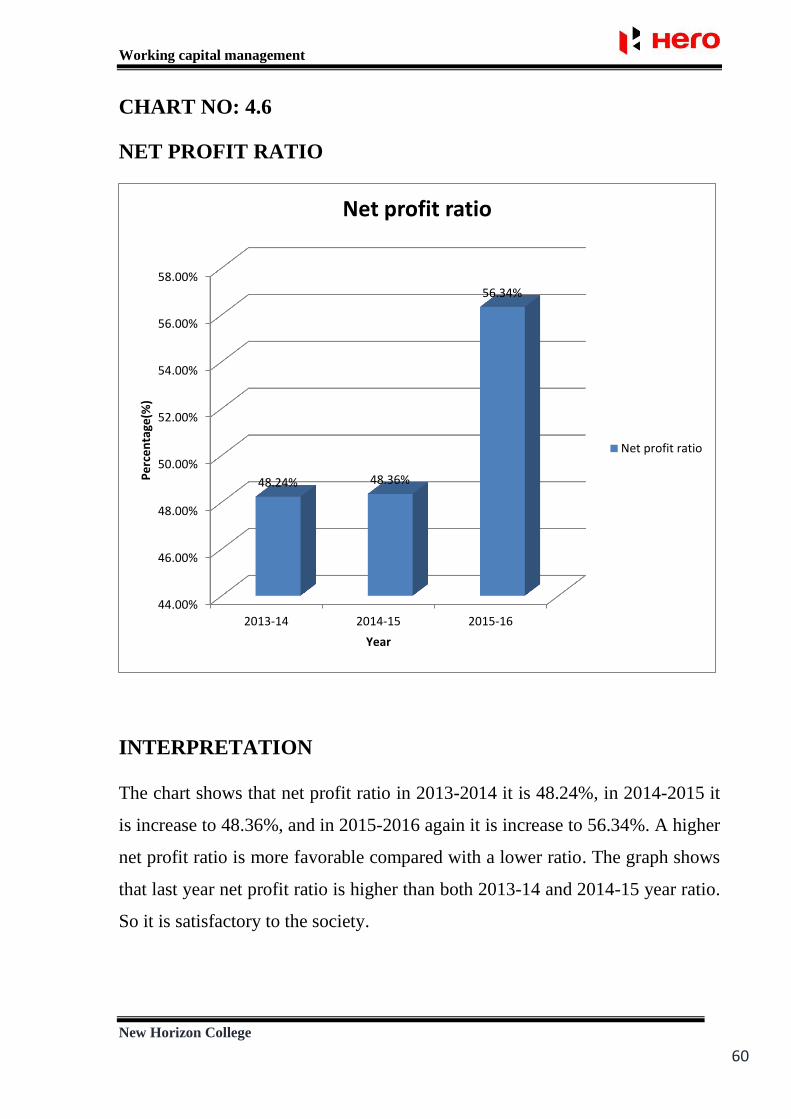

4.6 Chart showing net profit ratio 60

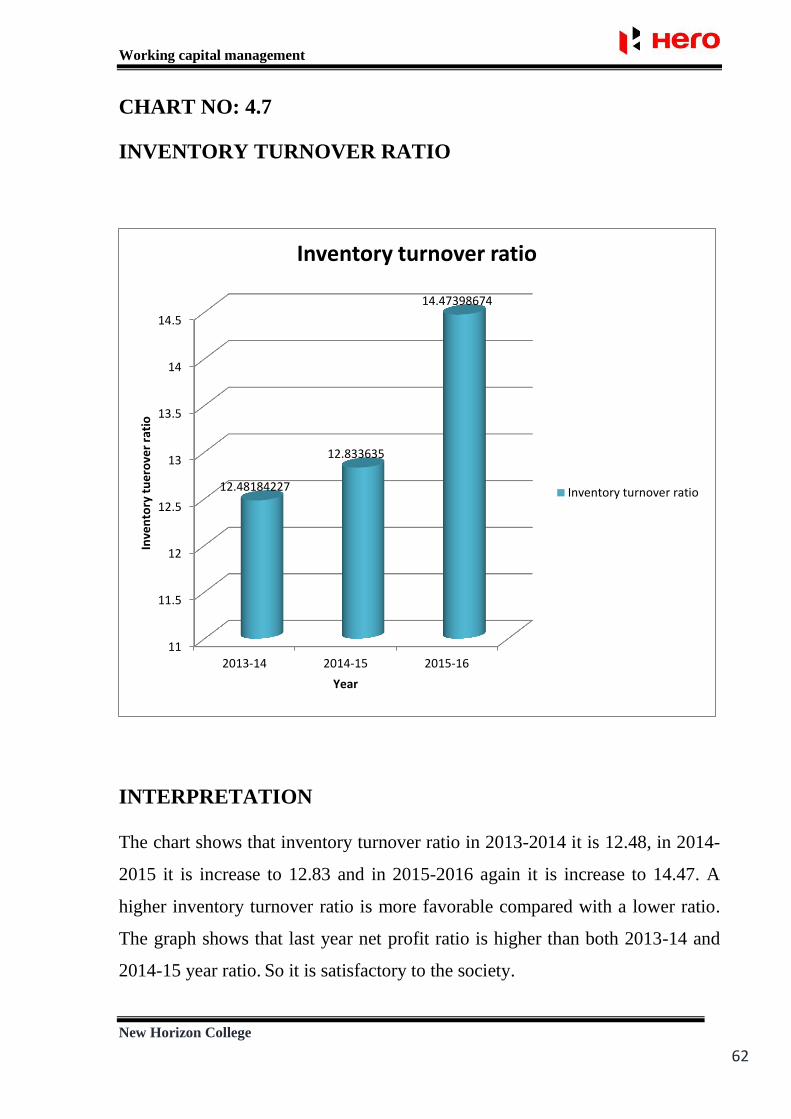

4.7 Chart showing inventory turnover ratio 62

4.8 Chart showing fixed assets turnover ratio 64

4.9

Chart showing current assets turnover

ratio 66

4.10

Chart showing working capital turnover

ratio 68

EXECUTIVE SUMMARY

This is a study conducted to focus on the short term financial

management or working capital management. Working capital refers to that part

of the firm’s capital which required for financing short term or current asset.

Adequate amount of working capital is required by the firm in the form of

different activities to continue uninterrupted and to tackle problems that may

arise. Financial viability structure and utilization of working capital in the

company is analyzed for three years from 2013-2016

The study is mainly based on the secondary data. Ratios and statement of

changes in working capital are the tools used for the study. The interpretations

are summarized and suggestions are provided based on it.

CHAPTER 1

INTRODUCTION

CHAPTER 2

INDUSTRY AND COMPANY PROFILE

CHAPTER 3

RESEARCH DESIGN

CHAPTER 4

ANALYSIS AND INTERPRETATION OF

DATA

CHAPTER 5

FINDINGS, SUGGESTIONS & CONCLUSION

BIBLIOGRAPHY

ANNEXURE

Working capital management

New Horizon College

1

1. INTRODUCTION

Working capital management refers to a company's managerial

accounting strategy designed to monitor and utilize the two components of

working capital, current assets and current liabilities, to ensure the most

financially efficient operation of the company. The primary purpose of working

capital management is to make sure the company always maintains sufficient

cash flow to meet its short-term operating costs and short-term debt obligations.

Working capital management is concerned with the problems that arise in

attempting to manage the current assets, the current liabilities and the

interrelationship that exists between them. The term current assets refer to those

assets which in the ordinary course of business can be, or will be, converted in

to cash within one year without undergoing a diminution in value and without

disrupting the operation of the firm.

The goal of working capital management is to ensure that a firm is able to

continue its operations and that it has sufficient ability to satisfy both maturing

short-term debt and upcoming operational expenses. The management of

working capital involves managing inventories, accounts receivable and

payable, and cash. The excess of ‗current assets‘ of a business organization over

its ‗current liabilities‘ is termed as the ‗working capital‘ of that organization.

The major current assets are cash, marketable security, account receivable

and inventory. Current liabilities are those liabilities which are intended, at their

inception, too be paid in the ordinary course of business, within a year, out of

the current assets or earning of the concern. The basic current liabilities are

account payable, bills payable, bank overdraft and outstanding expenses.

Working capital management

New Horizon College

2

1.1 DEFINITIONS

The term working capital is commonly used for the capital required for

day-to-day working in a business concern, such as for purchasing raw material,

for meeting day-to-day expenditure on salaries, wages, rents rates, advertising

etc. But there is much disagreement among various financial authorities

(Financiers, accountants, businessmen and economists) as to the exact meaning

of the term working capital.

Working capital is defined as, ―the excess of current assets over current

liabilities and provisions‖.

In the Annual Survey of Industries (1961), working capital is defined to include,

―Stocks of materials, fuels, semi-finished goods including work-in-progress and

finished goods and by-products; cash in hand and bank and the algebraic sum of

sundry creditors as represented by,

(a) outstanding factory payments e.g. rent, wages, interest and dividend;

(b) purchase of goods and services;

(c) short-term loans and advances and sundry debtors comprising amounts due

to the factory on account of sale of goods and services and advances towards tax

payments‖.

In the words of shubin, "working capital is the amount of funds necessary to

cover the cost of operating the enterprise."

According to Ganestenberg, "circulating capital means current assets of a

company that are changed in the ordinary course of business from one form to

another, as for example from cash to inventories, inventories to receivables,

receivables to cash."

Working capital management

New Horizon College

3

Working capital has been described as the ―life blood of any business which is a

applicable because it constitutes a cyclically flowing stream through the

business‖.

CALCULATION OF WORKING CAPITAL

The net working capital formula is calculated by subtracting the current

liabilities from the current assets. Here is what the basic equation looks like:

Net working capital = current assets - current liabilities n nb n

Typical current assets that are included in the net working capital

calculation are cash, accounts receivable, inventory, and short-term investments.

The current liabilities section typically includes accounts payable, accrued

expenses and taxes, customer deposits, and other trade debt.

A positive net working capital is better than a negative one. A positive

calculation shows creditors and investors that the company is able to generate

enough from operations to pay for its current obligations with current assets.

A negative net working capital, on the other hand, shows creditors and

investors that the operations of the business aren‘t producing enough to support

the business‘ current debts.

Working capital management

New Horizon College

4

1.2 CLASSIFICATION OF WORKING CAPITAL

Working Capital may be classified in two ways,

a) Concept based working capital

b) Time based working capital

Concepts based working capital

1. Gross Working Capital: It refers to the firm‘s investment in total current or

circulating assets.

2. Net Working Capital: The term ―Net Working Capital‖ has been defined in

two different ways:

1) It is the excess of current assets over current liabilities. This is, as a matter of

fact, the most commonly accepted definition. Some people define it as only

the difference between current assets and current liabilities.

2) Alternate definition of net working capital is that portion of a firm‘s current

assets which is financed by long-term funds.

Time based working capital

Permanent Working Capital:

This refers to that minimum amount of investment in all current assets

which is required at all times to carry out minimum level of business activities.

In other words, it represents the current assets required on a continuing basis

over the entire year.

Working capital management

New Horizon College

5

Temporary Working Capital:

The amount of such working capital keeps on fluctuating from time to

time on the basis of business activities. In other words, it represents additional

current assets required at different times during the operating year.

For example, extra inventory has to be maintained to support sales during peak

sales period. Similarly, receivable also increase and must be financed during

period of high sales. On the other hand, investment in inventories, receivables,

etc., will decrease in periods of depression.

NEEDS FOR WORKING CAPITAL

Working capital is needed till a firm gets cash on sale of finished

products. It depends on two factors:

1. Manufacturing cycle i.e. time required for converting the raw material into

finished product.

2 Credit policy i.e. credit period given to Customers and credit period

allowed by creditors.

Thus, the sum total of these times is called an ―Operating cycle‖ and it consists

of the following six steps:

a. Conversion of cash into raw materials.

b. Conversion of raw materials into work-in-process.

c. Conversion of work-in-process into finished products.

d. Time for sale of finished goods—cash sales and credit sales.

e. Time for realization from debtors and Bills receivables into cash.

f. Credit period allowed by creditors for credit purchase of raw materials,

inventory and creditors for wages and overheads.

Working capital management

New Horizon College

6

Debtors & Bills

Receivables

cash

raw materials

work- in- progress

finished product

Sales

Chart for operating cycle or working capital cycle.

1.3 DETERMINANTS OF WORKING CAPITAL

The factors influencing the working capital decisions of a firm may be

classified as two groups, such as

I. Internal factors

II. External factors

The internal factors include

1. Nature of business size of business,

2. Firm‘s product policy

3. Firm‘s credit policy

Working capital management

New Horizon College

7

4. Availability of credit

5. Growth and expansion of business

6. Profit margin and dividend policy

7. Operating efficiency of the firm

8. Co-ordinating activities in firm

The external factors include

1. Business fluctuations,

2. Changes in the technology,

3. Infrastructural facilities,

4. Import policy and

5. The taxation policy etc.

These factors are discussed in brief in the following lines.

I. INTERNAL FACTORS

1. Nature and size of the business

The working capital requirements of a firm are basically influenced by

the nature and size of the business. Size may be measured in terms of the scale

of operations. A firm with larger scale of operations will need more working

capital than a small firm. Similarly, the nature of the business - influence the

working capital decisions. Trading and financial firms have less investment in

fixed assets. But require a large sum of money to be invested in working capital.

Retail stores, business units require larger amount of working capital, where as ,

public utilities need less working capital and more funds to invest in fixed

assets.

Working capital management

New Horizon College

8

2. Firm’s production policy

The firm‘s production policy (manufacturing cycle) is an important factor

to decide the working capital requirement of a firm. The production cycle starts

with the purchase and use of raw material and completes with the production of

finished goods. On the other hand, production policy is uniform production

policy or seasonal production policy etc., also influences the working capital

decisions. Larger the manufacturing cycle and uniform production policy –

larger will be the requirement of working capital. The working capital

requirement will be higher with varying production schedules in accordance

with the changing demand.

3. Firm’s credit policy

The credit policy of a firm influences credit policy of working capital. A

firm following liberal credit policy to all customers require funds. On the other

hand, the firm adopting strict credit policy and grant credit facilities to few

potential customers will require less amount of working capital.

4. Availability of credit

The working capital requirements of a firm are also affected by credit

terms granted by its suppliers – i.e. creditors. A firm will need less working

capital if liberal credit terms are available to it. Similarly, the availability of

credit from banks also influences the working capital needs of the firm. A firm,

which can get bank credit easily on favorable conditions will be operated with

less working capital than a firm without such a facility.

5. Growth and expansion of business

Working capital requirement of a business firm tend to increase in

correspondence with growth in sales volume and fixed assets. A growing firm

may need funds to invest in fixed assets in order to sustain its growing

Working capital management

New Horizon College

9

production and sales. This will, in turn, increase investment in current assets to

support increased scale of operations. Thus, a growing firm needs additional

funds continuously.

6. Profit margin and dividend policy

The magnitude of working capital in a firm is dependent upon its profit

margin and dividend policy. A high net profit margin contributes towards the

working capital pool. To the extent the net profit has been earned in cash, it

becomes a source of working capital. This depends upon the dividend policy of

the firm. Distribution of high proportion of profits in the form of cash dividends

results in a drain on cash resources and thus reduces company‘s working capital

to that extent. The working capital position of the firm is strengthened if the

management follows conservative dividend policy and vice versa.

7. Operating efficiency of the firm

Operating efficiency means the optimum utilisation of a firm‘s resources

at minimum cost. If a firm successfully controls operating cost, it will be able to

improve net profit margin which, will, in turn, release greater funds for working

capital purposes.

8. Co-ordinating activities in firm

The working capital requirements of a firm is depend upon the co-

ordination between production and distribution activities. The greater and

effective the co-ordinations, the pressure on the working capital will be

minimized. In the absence of co-ordination, demand for working capital is

reduced.

Working capital management

New Horizon College

10

II. EXTERNAL FACTORS

1. Business fluctuations

Most firms experience fluctuations in demand for their products and

services. These business variations affect the working capital requirements.

When there is an upward swing in the economy, sales will increase,

correspondingly, the firm‘s investment in inventories and book debts will also

increase. Under boom, additional investment in fixed assets may be made by

some firms to increase their productive capacity. This act of the firm will

require additional funds. On the other hand when, there is a decline in economy,

sales will come down and consequently the conditions, the firm try to reduce

their short-term borrowings. Similarly the seasonal fluctuations may also affect

the requirement of working capital of a firm.

2. Changes in the technology

The technological changes and developments in the area of production

can have immediate effects on the need for working capital. If the firm wish to

install a new machine in the place of old system, the new system can utilise less

expensive raw materials, the inventory needs may be reduced there by working

capital needs.

3. Import policy

Import policy of the Government may also effect the levels of working

capital of a firm since they have to arrange funds for importing goods at

specified times.

4. Infrastructural facilities

The firms may require additional funds to maintain the levels of inventory

and other current assets, when there is good infrastructural facilities in the

company like, transportation and communications.

Working capital management

New Horizon College

11

5. Taxation policy

The tax policies of the Government will influence the working capital

decisions. If the Government follow regressive taxation policy, i.e. imposing

heavy tax burdens on business firms, they are left with very little profits for

distribution and retention purpose. Consequently, the firm has to borrow

additional funds to meet their increased working capital needs. When there is a

liberalised tax policy, the pressure on working capital requirement is minimised.

IMPORTANCE OR ADVANTAGES OF ADEQUATE

WORKING CAPITAL

Working capital is the life blood of a business. Just as circulation of blood

is essential in the human body for maintaining life, working capital is very

essential to maintain the smooth running of a business. No business can run

successfully without an adequate amount of working capital. The main

advantages of maintaining adequate amount of working capital are as follows:

1. Solvency of the business:

Adequate working capital helps in maintaining solvency of the business

by providing uninterrupted flow of production.

2. Goodwill:

Sufficient working capital enables a business concern to make prompt

payments and hence helps in creating and maintaining goodwill.

3. Easy loans:

A concern having adequate working capital, high solvency and good

credit standing can arrange loans from banks and other on easy and favourable

terms.

Working capital management

New Horizon College

12

4. Cash Discounts:

Adequate working capital also enables a concern to avail cash discounts

on the purchases and hence it reduces costs.

5. Regular supply of raw materials:

Sufficient working capital ensures regular supply of raw materials and

continuous production.

6. Regular payment of salaries, wages and other day-to-day commitments:

A company which has ample working capital can make regular payment

of salaries, wages and other day-to-day commitments which raises the morale of

its employees, increases their efficiency, reduces wastages and costs and

enhances production and profits.

7. Exploitation of favorable market conditions:

Only concerns with adequate working capital can exploit favourable

market conditions such as purchasing its requirements in bulk when the prices

are lower and by holding its inventories for higher prices.

8. Ability to face Crisis:

Adequate working capital enables a concern to face business crisis in

emergencies such as depression because during such periods, generally, there is

much pressure on working capital.

9. Quick and Regular return on Investments:

Every Investor wants a quick and regular return on his investments.

Sufficiency of working capital enables a concern to pay quick and regular

dividends to its investors as there may not be much pressure to plough back

profits. This gains the confidence of its investors and creates a favourable

market to raise additional funds i.e., the future.

Working capital management

New Horizon College

13

10. High morale:

Adequacy of working capital creates an environment of security,

confidence, high morale and creates overall efficiency in a business.

EXCESS OR INADEQUATE WORKING CAPITAL

Every business concern should have adequate working capital to run its

business operations. It should have neither redundant or excess working capital

nor inadequate or shortage of working capital. Both excess as well as short

working capital positions are bad for any business. However, out of the two, it is

the inadequacy of working capital which is more dangerous from the point of

view of the firm.

DISADVANTAGES OF INADEQUATE WORKING CAPITAL

1. A concern which has inadequate working capital cannot pay its short-term

liabilities in time. Thus, it will lose its reputation and shall not be able to get

good credit facilities.

2. It cannot buy its requirements in bulk and cannot avail of discounts, etc.

3. It becomes difficult for the firm to exploit favourable market conditions and

undertake profitable projects due to lack of working capital.

4. The firm cannot pay day-to-day expenses of its operations and its creates

inefficiencies, increases costs and reduces the profits of the business.

5. It becomes impossible to utilize efficiently the fixed assets due to non-

availability of liquid funds.

6. The rate of return on investments also falls with the shortage of working

capital.

Working capital management

New Horizon College

14

1.4 RATIO ANALYSIS

Ratio analysis is one of the most powerful tool and widely used technique

of analyzing financial statements. It is the process of computing and interpreting

relationship between the items of the financial statements for arriving at

conclusions about the financial position and performance of an enterprise. With

the help of ratios, the financial statements can be analyzed more clearly and

scientific decisions are made from such analysis.Ratio analysis can also be

defined as the yard stick that provides a measure of relationship between two

accounting figures. Ratio analysis can be used both in the trend or dynamic

analysis and statistical analysis.

Financial ratio analysis is the calculation and comparison of ratios which

are derived from the information in a company‘s financial condition, its

operations and attractiveness as an investment. Financial ratios are calculated

from one or more pieces of information from a company‘s financial statements.

For example, the ―gross margin‖ is the gross profit from operations divided by

the total sales or revenues of a company, expressed in percentage terms. In

isolation, a financial ratio is a useless piece of information. In context, however

a financial ratio can give a financial analyst an excellent picture of a company‘s

situation and the trends that are developing.

Financial ratio analysis groups the ratio into categories which tell us

about different facets of a company‘s finances. Some ratios which are most

importance are listed below

1. Liquidity Ratio.

2. Leverage Ratio

3. Profitability Ratio.

4. Activity Ratio

Working capital management

New Horizon College

15

LIQUIDITY RATIO

Liquidity refers to the ability of the concern to meet its current obligations

as and when they become due. These ratios are calculated to comment upon the

short term paying capacity of the concern or the firm‘s ability to meet its current

obligations. Much insight could be obtained into the present cash solvency of

the firm and its ability to remain solvent in the event of emergent i.e. the firm

should ensure that it does not suffer from any lack of liquidity and also that it is

necessary to strike a proper balance between high liquidity and lack of liquidity.

The various liquidity ratios are:

Current Ratio

Current ratio may be defined as the relationship between current assets

and current liabilities. This ratio is also known as working capital ratio, is a

measure of general liquidity and is most widely used to make the analysis of a

short term financial position or liquidity of a firm. It is calculated by dividing

the total of current assets to the total of current liabilities.

Current Ratio = Current Assets / Current Liabilities

Liquid Ratio

It is also known as acid test ratio. Liquid ratio is more rigorous test of

liquidity than the current ratio. The term liquidity refers to the ability of a firm

to pay its short term obligations as and when they become due. An asset is said

to be liquid if it can be converted into cash within a short period without loss of

value. Liquid ratio may be defined as the relationship between liquid assets and

current liabilities.

Liquid Ratio = Liquid Assets / Current Liabilities

Working capital management

New Horizon College

16

Absolute Liquid ratio

Some authors are of the opinion that the absolute liquid ratio should also be

calculated together with current ratio and acid test ratio so as to exclude even

receivables from the current assets and find out the absolute liquid assets.

Absolute Liquid Ratio = Absolute Liquid Assets / Current Liabilities

LEVERAGE RATIOS

The short term creditors like the bankers and the suppliers of the raw

materials are more concerned with the firm‘s current debt paying ability. On the

other hand long-term creditors like debenture holders, financial institutions, etc

are more concerned with the firm‘s long term financial position. To judge the

long term financial position of the firm, financial leverage or capital structure

ratio is used. The shareholders, debenture holders and other long term creditors

like financial institutions are more interested in the long term financial position

or long term solvency of the firm. Leverage or solvency ratios are used to

analyze the capital structure of a company; it is also known as capital structure

ratios. The term solvency generally refers to the firm‘s ability to pay the interest

regularly and repay the principal amount of debt on due date.

Accordingly, there are two types of leverage ratios. The first type of

leverage ratio is based on the relationship between owned capital and borrowed

capital. These ratios are calculated from the balance items. The second type of

leverage ratio is coverage ratio. These are computed from profit and loss

account.

Working capital management

New Horizon College

17

Debt-equity ratio

Debt-equity ratio is also known as external-internal equity ratio. It is

calculated to measure the relative claims of outsiders and the owners against the

firm‘s assets. This ratio indicates the relationship between the external equities

or the outsiders fund and the internal equities or shareholders fund.

Debt-equity ratio = Outsider‘s fund / Shareholders fund

Primarily Interpretation of this ratio depends upon the financial policy of the

firm and the firm‘s nature of business. A ratio of 1:1 may be usually considered

to be satisfactory ratio although there cannot be any rule of thumb or standard

norm for all types of business.

Capital gearing ratio

The term capital gearing is used to describe the relationship between

equity share capital including reserves and surpluses to preference share capital

and other fixed interest bearing loans. If preference share capital and other fixed

interest bearing loans exceed the equity share capital including reserves, the

firm is said to be highly geared. The firm is said to be in low gear if preference

share capital and other fixed interest bearing loans are less than equity capital

and reserves.

Capital gearing ratio= (ESC + R & S)/(PSC - TDBFI)

Where , ESC = equity share capital

R&S = reserve and surplus

PSC = preferenceshare capital-term debt bearing

TDBFI = term debt bearing fixed interest

Working capital management

New Horizon College

18

PROFITABILITY RATIOS

Profit reflects the final result of the business operations. There is two

types of profitability ratios namely margin ratio and ratio on returns rates. Profit

margin ratios show the relation between sales and profits.

The ultimate aim of any business enterprise is to earn maximum profit.

Lord Keens remarked, ―Profit is the engine that drives the business enterprise ―,

a firm should earn profit to survive and grow for a long period of time. To the

management profit is a measurement of efficiency and control. To the owners it

is to measure the worth of their investment. To the creditors it is margin of

safety.

The management of the company should know how efficiently they carry

out business operation. In other words, the management of the company is very

much interested in the profitability of the company. Beside management,

creditors and owners are also interested in the profitability of the firm, as they

want to get interest and repayment of principal amount regularly. Owners want

to get a reasonable return on their investment. The profitability ratio measures

the ability of the firm to earn and on sales, total assets and invested capital.

Profitability ratios are generally calculated either in relation to sales or in

relation to investment.

The following profitability ratios are calculated in relation to sales:

Gross profit ratio

Gross profit ratio measures the relationship of gross profit to net sales and

is usually represented as percentage. Thus it is calculated by dividing gross

profit by sales.

Gross profit ratio = gross profit / net sales

Working capital management

New Horizon College

19

Operating profit ratio

This ratio is calculated by dividing operating profit by sales. Operating

profit is the excess of net sales over operating costs. Operating cost is the

cumulative of cost of goods sold, administrative and office expenses and selling

and distribution expenses.

Operating profit ratio = operating profits /net sales

Net profit ratio

Net profit ratio establishes the relationship between net profit (after taxes)

and sales, and it indicates the efficiency of the management in manufacturing,

selling, administrative and other activities of the firm. This ratio is the overall

measure of firm‘s profitability and is calculated as:

Net profit ratio = net profit / net sales

ACTIVITY RATIOS

Funds of the owners and creditors are invested in various assets to

generate sales and profits. Activity ratios are employed to evaluate the

efficiency with which the firm‘s managers utilize their assets. These ratios is

also called turnover ratio because they indicate the speed with the assets are

being converted or turn over into sales.

The various activity ratios are:

Debtors turnover ratio

Debtor‘s turnover ratio indicates the velocity of debt collection of a firm.

In simple words, it indicates the number of times average debtors are turned

over during a year.

Debtors turnover ratio = Net credit annual sale / Average trade debtors

Working capital management

New Horizon College

20

Creditors turnover ratio

This ratio indicates the velocity with which the creditors are turned over

the relation to purchases.

Creditors turnover ratio = Net credit purchases / Average trade creditors

Inventory turnover ratio

It is also known as stock velocity, is normally calculated as sales/average

inventory or cost of goods sold /average inventory. It indicates whether the

inventory has been efficiently used or not. The purpose is to see whether only

the required minimum funds have been locked up in inventory. Inventory

turnover ratio indicates the number of times the stock has been turned over

during the period and evaluates the efficiency with which a firm is able to

manage its inventory.

Inventory turnover ratio = Cost of goods sold / Average inventory at cost

Usually, a high inventory turnover indicates efficient management of inventory

because more frequently the stocks are sold; the lesser amount of money is

required to finance the inventory.

Fixed assets turnover ratio

This ratio indicates the extent to which the investments in fixed assets

contribute towards sales. If it is compared with a previous period, it indicates

whether the investment in fixed assets has been judicious or not. The ratio is

calculated as follows:

Fixed assets turnover ratio = Net sales / Fixed assets (Net)

Working capital management

New Horizon College

21

Working capital turnover ratio

It indicates the velocity of the utilization of net working capital. This ratio

indicates the number of times the working capital is turned over in the course of

a year. It measures the efficiency with which the working capital is being used

by a firm.

This ratio is calculated as:

Working capital turnover ratio = Cost of sales / Average working capital

A higher ratio indicates efficient utilization of working capital and a low

ratio indicates vice versa. But a very high working capital turnover ratio is not a

good situation for any firm and hence care must be taken while interpreting the

ratio.

Working capital management

New Horizon College

22

2. INDUSTRY AND COMPANY PROFILE

2.1 INDUSTRY PROFILE

The automotive industry is a wide range of companies and organizations

involved in the design, development, manufacturing, marketing, and selling of

motor vehicles. The term automotive was created from Greek autos (self), and

Latin motives (of motion) to represent any form of self-powered vehicle. This

term was proposed by SAE member Elmer Sperry.

The automotive industry does not include industries dedicated to the

maintenance of automobiles following delivery to the end-user, such as

automobile repair shops and motor fuel filling stations.

HISTORY

The automotive industry began in the 1890s with hundreds of

manufacturers that pioneered the horseless carriage. For many decades, the

United States led the world in total automobile production. In 1929 before the

Great Depression, the world had 32,028,500 automobiles in use, and the U.S.

automobile industry produced over 90% of them.

In 1768, the first steam-powered automobile capable of human transportation

was built by Nicolas-Joseph Cugnot.

In 1807, Francois Isaac de Rivaz designed the first car powered by an internal

combustion engine fueled by hydrogen.

In 1864, Siegfried Marcus created the first gasoline powered combustion

engine, which he placed on a pushcart.

1880, introduced innovations such as a four-cycle, gasoline-powered engine, an

ingenious carburetor design, and magneto ignition.

Working capital management

New Horizon College

23

In 1886, Karl Benz developed a petrol- or gasoline-powered automobile. This is

also considered to be the first "production" vehicle as Benz made several other

identical copies.

At the turn of the 20th century electrically powered automobiles appeared but

only occupied a niche market until the turn of the 21st century.

After World War II, the U.S. produced about 75 percent of world's auto

production. In 1980, the U.S. was overtaken by Japan and became world's leader

again in 1994. In 2006, Japan narrowly passed the U.S. in production and held

this rank until 2009, when China took the top spot with 13.8 million units.

In 1897, the first car ran on an Indian road. Through the 1930s, cars were

imports only, and in small numbers. Hindustan Motors was launched in 1942,

long-time competitor Premier in 1944, building Chrysler, Dodge, and Fiat

products respectively.

In 1952, the government appointed the first Tariff Commission, and one

of the purpose was to come out with the feasible plan for indigenization of the

Indian automobile industry.

ECONOMY

Around the world, there were about 806 million cars and light trucks on

the road in 2007, consuming over 980 billion litres of gasoline and diesel fuel

yearly.The automobile is a primary mode of transportation for many developed

economies. The Detroit branch of Boston Consulting Group predicts that, by

2014, one-third of world demand will be in the four BRIC markets (Brazil,

Russia, India and China). Meanwhile, in the developed countries, the

automotive industry has slowed down. It is also expected that this trend will

continue, especially as the younger generations of people (in highly urbanized

countries) no longer want to own a car anymore, and prefer other modes of

Working capital management

New Horizon College

24

transport. Other potentially powerful automotive markets are Iran and

Indonesia. Emerging auto markets already buy more cars than established

markets. According to a J.D. Power study, emerging markets accounted for 51

percent of the global light-vehicle sales in 2010. The study, performed in 2010

expected this trend to accelerate. However, more recent reports (2012)

confirmed the opposite; namely that the automotive industry was slowing down

even in BRIC countries. In the United States, vehicle sales peaked in 2000, at

17.8 million units.

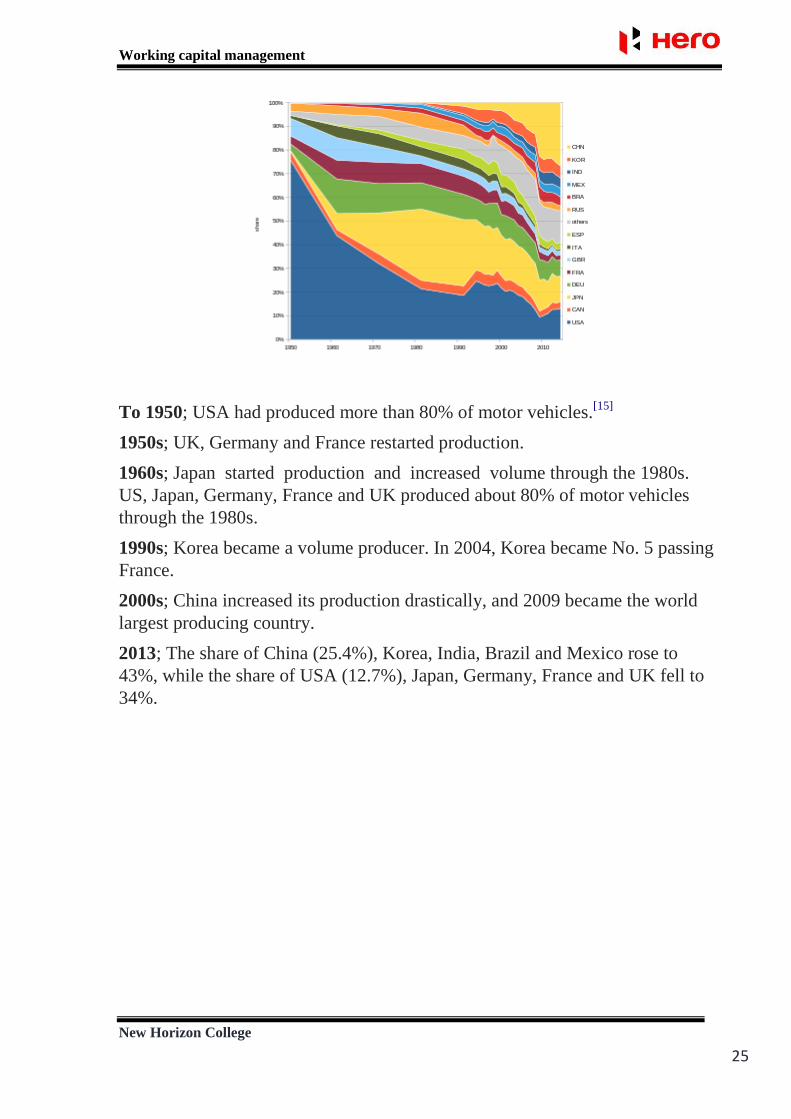

World Motor Vehicle Production

Production volume (1000 vehicles)

1960s; Post war increase

1970s; Oil crisis and tighter safety and emission regulation.

1990s; production started in NICs

2000s; rise of China as top producer

Automotive industry crisis of 2008–2010

Working capital management

New Horizon College

25

To 1950; USA had produced more than 80% of motor vehicles.[15]

1950s; UK, Germany and France restarted production.

1960s; Japan started production and increased volume through the 1980s.

US, Japan, Germany, France and UK produced about 80% of motor vehicles

through the 1980s.

1990s; Korea became a volume producer. In 2004, Korea became No. 5 passing

France.

2000s; China increased its production drastically, and 2009 became the world

largest producing country.

2013; The share of China (25.4%), Korea, India, Brazil and Mexico rose to

43%, while the share of USA (12.7%), Japan, Germany, France and UK fell to

34%.

Working capital management

New Horizon College

26

AUTOMOTIVE INDUSTRY IN INDIA

In 1897, the first car ran on an Indian road. Through the 1930s, cars were

imports only, and in small numbers. in 1954, General Motors, Ford and Roots

Group who has assembly plants in Mumbai to India decided to move out of

India.

The automotive industry in India is one of the largest in the world with an

annual production of 23.37 million vehicles in FY 2014-15, following a growth

of 8.68 per cent over the last year. India is also a prominent auto exporter and

has strong export growth expectations for the near future. In FY 2014-15,

automobile exports grew by 15 per cent over the last year.

In addition, several initiatives by the Government of India and the major

automobile players in the Indian market are expected to make India a leader in

the Two Wheeler (2W) and Four Wheeler (4W) market in the world by 2020.

The Government of India encourages foreign investment in the

automobile sector and allows 100 per cent FDI under the automatic route.

Some of the major initiatives taken by the Government of India are:

The Government of India aims to make automobile manufacturing the main

driver of "Make in India" initiative, as it expects the passenger vehicles

market to triple to 9.4 million units by 2026, as highlighted in the Auto

Mission Plan (AMP) 2016-26.

In the Union budget of 2015-16, the Government has announced plans to

provide credit of Rs 850,000 crore (US$127.5 billion) to farmers, which is

expected to boost sales in the tractors segment.

The government plans to promote eco-friendly cars in the country—i.e.

CNG-based vehicles, hybrid vehicles, and electric vehicles—and also to

make mandatory 5 per cent ethanol blending in petrol.

Working capital management

New Horizon College

27

The government has formulated a Scheme for Faster Adoption and

Manufacturing of Electric and Hybrid Vehicles in India, under the National

Electric Mobility Mission 2020, to encourage the progressive introduction of

reliable, affordable, and efficient electric and hybrid vehicles into the

country.

The Automobile Mission Plan (AMP) for the period 2006–2016, designed

by the government is aimed at accelerating and sustaining growth in this

sector. Also, the well-established Regulatory Framework under the Ministry

of Shipping, Road Transport and Highways, plays a part in providing a boost

to this sector.

THE 1952 TARIFF COMMISSION

In 1952, the government appointed the first Tariff Commission, and one

of the purpose was to come out with the feasible plan for indigenization of the

Indian automobile industry.

In 1953 the commission submitted the report which recommended

categorizing the existing Indian companies according to their then infrastructure

with license capacity to manufacture a certain number of vehicle with capacity

increase allowable as per demands in future.

The Tariff commission along with similar restriction applied to other

Industries can to be known as the license that later proved to be the greatest

undoing for the Indian automotive industry where bureaucratic(official) red tape

ended up making demand outstripping supply with month long waiting period

for cars, scooter and motorcycles.

Working capital management

New Horizon College

28

PASSENGER CARS

Hindustan Motors, Calcutta - technical collaboration with Morris Motors to

manufacture Morris Oxford models that would later become HM

Ambassador.

Premier Automobiles, Bombay - technical collaboration with Chrysler to

manufacture Dodge, Plymouth and Desoto models and with Fiat to

manufacture the 1100D models which would later with Premier Padmini

range.

Standard Motor Products of India, Madras - technical collaboration from

Standard-Triumph to manufacture Standard Vanguard, Standard 8, 10 and

later Standard Herald.

UTILITY AND LIGHT COMMERCIAL VEHICLES

Mahindra & Mahindra, Bombay - technical collaboration with Willys to

manufacture CJ Series Jeep.

Bajaj Tempo, Poona now Force Motors - technical collaboration with Tempo

(company) to manufacture Tempo Hanseat, a three-wheeler and Tempo

Viking and Hanomag, later known as Tempo Matador in India.

Standard Motor Products of India - technical collaboration from Standard has

licence to manufacture the Standard Atlas passenger van with panel van and

one-tonne one tonne pickup variants.

MEDIUM AND HEAVY COMMERCIAL VEHICLES

Tata Motors, Poona, then known as TELCO - technical collaboration with

Mercedes Benz to manufacture medium to heavy commercial vehicles both

Bus and Trucks.

Ashok Motors, later Ashok Leyland, Madras - technical collaboration with

Leyland Motors to manufacture medium to heavy commercial vehicles both

Working capital management

New Horizon College

29

Bus and Trucks. Ashok Motors also discontinued its Austin venture formed

in 1948 to sell Austin A40 and retooled the factory to make trucks and buses.

Hindustan Motors - technical collaboration with General Motors to

manufacture the Bedford range of medium lorry and bus chassis.

Premier Automobiles - technical collaboration with Chrysler to manufacture

the Dodge, Fargo range of medium lorry, panel vans, mini-bus and bus

chassis.

SCOOTERS, MOPEDS AND MOTORCYCLE

known as Bajaj Chetak, by Bajaj became the largest sold scooter in the world

Many of the two-wheelers manufacturers were granted licenses in early 60's

well after the tariff commission was enabled.

Royal Enfield (India), Madras - technical collaboration with Royal Enfield,

UK to manufacture the Enfield Bullet range of motorcycles.

Bajaj Auto, Poona - technical collaboration with Piaggio, Italy to

manufacture their best-selling Vespa range of scooters and three wheelers

with commercial option as well.

Automobile Products of India, Bombay (Better known for API Lambretta -

technical colloboration with Innocenti of Milan, Italy to manufacture their

Lambretta range of mopeds, scooters adn three-wheelers. This company was

actually the Rootes Group car plant that was bought over by M. A.

Chidambaram family.

Mopeds India Limited, Tirupathi - technical collaboration with Motobecane,

France to manufacture their best-selling Mobility mopeds.

Escorts Group, New Delhi - technical collaboration with CEKOP of Poland

to manufacture the Rajdoot 175 motorcycle whose origin was DKW RT 125

Ideal Jawa, Mysore - in technical collaboration with CZ - Jawa of

Czechoslovakia for its Jawa and Yezdi range of motorcycles.

Working capital management

New Horizon College

30

2.2 COMPANY PROFILE

Hero MotoCorp Ltd. (Formerly Hero Honda Motors Ltd.) is the world's

largest manufacturer of two - wheelers, based in India.

In 2001, the company achieved the coveted position of being the largest

two-wheeler manufacturing company in India and also, the 'World No.1' two-

wheeler company in terms of unit volume sales in a calendar year. Hero

MotoCorp Ltd. continues to maintain this position till date.

Hero Motocorp Ltd., formerly Hero Honda, is an Indian motorcycle

(<250cc) and scooter manufacturer based in New Delhi, India. The company is

the largest two wheeler manufacturer in India. In India, it has a market share of

about 46% share in 2-wheeler category. The 2006 Forbes 200 Most Respected

companies list has Hero Honda Motors ranked at #108. On 31 March 2013, the

market capitalisation of the company was ₹308 billion

Hero MotoCorp, the country's largest two-wheeler maker by volume,

continue to dominate the top 10 selling two-wheelers list in financial year 2014-

15 with its four products - Splendor, Passion, HF Deluxe, and Glamour ranked

at 1st, 3rd, 4th, 8th spots respectively, according to the sales data released by

Society of India Automobiles Manufacturers (SIAM) recently.

VISION

The story of Hero Honda began with a simple vision - the vision of a

mobile and an empowered India, powered by its two wheelers. Hero MotoCorp

Ltd., company's new identity, reflects its commitment towards providing world

class mobility solutions with renewed focus on expanding company's footprint

in the global arena.

Working capital management

New Horizon College

31

MISSION

Hero MotoCorp's mission is to become a global enterprise fulfilling its

customers' needs and aspirations for mobility, setting benchmarks in

technology, styling and quality so that it converts its customers into its brand

advocates. The company will provide an engaging environment for its people to

perform to their true potential. It will continue its focus on value creation and

enduring relationships with its partners.

STRATEGY

Hero MotoCorp's key strategies are to build a robust product portfolio

across categories, explore growth opportunities globally, continuously improve

its operational efficiency, aggressively expand its reach to customers, continue

to invest in brand building activities and ensure customer and shareholder

delight.

BRAND

The new Hero is rising and is poised to shine on the global arena.

Company's new identity "Hero MotoCorp Ltd." is truly reflective of its vision to

strengthen focus on mobility and technology and creating global footprint.

Building and promoting new brand identity will be central to all its initiatives,

utilizing every opportunity and leveraging its strong presence across sports,

entertainment and ground-level activation.

MANUFACTURING

Hero MotoCorp two wheelers are manufactured across 4 globally

benchmarked manufacturing facilities. Two of these are based at Gurgaon and

Dharuhera which are located in the state of Haryana in northern India. The third

manufacturing plant is based at Haridwar, in the hill state of Uttrakhand; the

Working capital management

New Horizon College

32

latest addition is the state-of-the-art Hero Garden Factory in Neemrana,

Rajasthan.

DISTRIBUTION

The Company's growth in the two wheeler market in India is the result of an

intrinsic ability to increase reach in new geographies and growth markets. Hero

MotoCorp's extensive sales and service network now spans over to 6000

customer touch points. These comprise a mix of authorized dealerships, service

& spare parts outlets, and dealer-appointed outlets across the country.

SPORTS ASSOCIATION

Hero MotoCorp began its association with the prestigious Indian Open

Golf tournament in 2005.

In 2010, Hero MotoCorp extended its support to Hockey by sponsoring

the 'Hockey World Cup 2010' that was held in India.

Hero MotoCorp has in the past sponsored major cricket tournaments in

association with International Cricket Council (ICC), including the cricket

World Cup and the Champions Trophy. Hero has also been associated with IPL.

EMPLOYEES

As on 31 March 2014, the company had 6,782 employees, out of which

66 were women (1.1%). It also had approx. 13,800 temporary employees on that

date. The company had an attrition rate of 5.1% in the FY 2012-13. The

company spent ₹8.21 billion (US$120 million) on employee benefits during the

FY 2012-13.

Working capital management

New Horizon College

33

HIERARCHY

CSR COMMITTEE

Mr. Pawan MunjalChair

man

Chairman, Managing Director &

CEO

Gen. (Retd.) V. P. Malik

Member

Non-executive & Independent

Director

Mr. Pradeep

Dinodia

Member

Non-executive &

Independent Director

STAKEHOLDERS' RELATIONSHIP

COMMITTEE

Dr. Pritam Singh

Chairman

Non-executive & Independent

Director

Mr. M. Damodaran

Member

Non-executive & Independent

Director

Mr. Ravi Nath

Member

Non-executive & Independent

Director

RISK MANAGEMENT

COMMITTEE

Mr. M. DamodaranC

hairman

Non-executive & Independent

Director

Mr. Pradeep

Dinodia

Member

Non-executive & Independent

Director

Mr. Ravi NathMember

Non-executive &

Independent Director

AUDIT COMMITTEE

Mr. Pradeep Dinodia

Chairman

Non-executive & Independent

Director

Gen. (Retd.) V. P. Malik

Member

Non-executive & Independent

Director

Dr. Pritam Singh

Member

Non-executive & Independent

Director

Mr.M.

DamodaranMember

Non-executive & Independent

Director

NOMINATION AND

REMUNERATION COMMITTEE

Gen. (Retd.) V. P.

MalikChairman

Non-executive & Independent

Director

Mr. Pradeep Dinodia

Member

Non-executive &

Independent Director

Mr. Ravi Nath

Member

Non-executive & Independent

Director

Working capital management

New Horizon College

34

OPERATIONS

Hero MotoCorp has four manufacturing facilities based at Dharuhera,

Neemrana and Gurgaon in Haryana and at Haridwar in Uttarakhand. These

plants together have a production capacity of 7.6 million 2-wheelers per year.

Hero MotoCorp has a sales and service network with over 6,000

dealerships and service points across India. It has a customer loyalty program

since 2000, called the Hero Honda Passport Program which is now known as

Hero GoodLife Program.

It is reported that Hero MotoCorp has five joint ventures or associate

companies, Munjal Showa, AG Industries, Sunbeam Auto, Rockman Industries

and Satyam Auto Components, that supply a majority of its components.

The company has a stated aim of achieving revenues of $10 billion and

volumes of 10 million two-wheelers by 2016–17. This in conjunction with new

countries where they can now market their two-wheelers following the

disengagement from Honda.

COMPETITION

Name Last

Price

Market

Cap.

(Rs. cr.)

Sales

Turnover

Net

Profit

Total

Assets

Bajaj Auto 2,981.60 86,277.67 23,883.20 3,929.67 12,454.14

Hero

Motocorp

3,588.70 71,663.28 30,700.88 3,161.52 7,944.75

TVS Motor 338.35 16,074.57 11,243.87 432.14 2,695.26

Mah

Scooters

1,485.45 1,697.66 8.97 101.00 312.00

Atul Auto 432.35 979.27 531.04 47.40 154.59

LML 8.00 65.59 156.13 -78.36 -662.45 Source: https://en.wikipedia.org/wiki

Working capital management

New Horizon College

35

The above chart shows comparison with competitor

29

81

.6

35

88

.7

33

8.3

5

14

85

.45

43

2.3

5

8

86

27

7.6

7

71

66

3.2

8

16

07

4.5

7

16

97

.66

97

9.2

7

65

.59

23

88

3.2

30

70

0.8

8

11

24

3.8

7

8.9

7

53

1.0

4

15

6.1

3

39

29

.67

31

61

.52

43

2.1

4

10

1

47

.4

-78

.36

12

45

4.1

4

79

44

.5

26

95

.26

31

2

15

4.5

9

-66

2.4

5

-10000

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

BAJAJ AUTO HEROMOTOCROP

TVS MOTOR MAH SCOOTER ATUL AUTO LML

Rs.

Cr

Company

Chart Title

LAST PRIC MARKET CAP SALES TURNOVER NET PROFIT TOTAL ASSET

Working capital management

New Horizon College

36

AMBICA HERO PROFILE

MANAGEMENT

At Ambica Hero, they believe in a customer centric approach towards

their business. This has enabled us to provide the very best after sales services.

they determination to achieve the highest standards has led us to be one of the

leading Hero MotoCorp dealers in India.

They state of the art service centre with modern equipment and their team

of dedicated staff are there to provide a satisfying experience to their customers.

AWARDS

In 2010 at the Hero Inter School Athletic Meet, Hero MotoCorp awarded a

Certificate of Appreciation to Kumar Hero.

At the National Mechanics Contest in 2005, Rakesh Machhi of Ambica Hero

was awarded a Certificate of Appreciation at the National Training Centre,

Gurgaon.

A Certificate of Excellence was awarded to Ambica Hero as a winner for his

overall performance in the 'Hero Stars' Contest for the year 2003-04.

A Certificate of Excellence was awarded to Mr. Jayant Shah as a winner for his

overall performance in the 'HH' Contest for the year 2007-08.

The first runner-up trophy was awarded to Ambica Hero, Baroda for the west

zone in 1987.

The Top 10 Technicians Award was presented to Mr. Gautam Shah of Ambica

Hero, for his excellence in the National Technician's Contest.

Working capital management

New Horizon College

37

EMPLOYEES

At Ambica Hero, we draw on each other‘s capabilities and experiences, to

inspire and motivate one another. We are a tight knit family of professionals

with the expertise to help us meet and surpass the expectations of our customers.

Key functional heads are ably supported by a team of more than 65 people in

the areas of sales , servicing , spare parts and administration.

CAREERS

Ambica Hero is a dynamic, growth-oriented environment that provides

exciting opportunities to grow as a professional. We have , from time to time ,

across multiple departments such as :-

Sales

Customer Care

Administration

Accounting Finance

Spare Parts Accessories

SERVICES

GENERAL SERVICES

Washing

Denting & Painting

Fuel Lines Inspection

Throttle Inspection

Carburetor Inspection

Working capital management

New Horizon College

38

Air Cleaner Inspection

Drain Tube Inspection

Spark Plug Inspection

Engine Oil Replacement

Valve Inspection

Engine Oil Inspection

Battery Inspection

Suspension Check

Wheel Balance Check

Tyre Pressure Check

Steering Inspection

Brake Inspection

Engine Overhauling

Rubbing and Polishing

Ignition Systems

Cylinder Reboring and Honing

Gearbox Repairs

Porting & Gasflow Testing

Accident Repairs

Working capital management

New Horizon College

39

EVENTS

Cricket Tournament

Diwali Sweets Distribution

Doodh Mandli Activity

Service Har Jagah Activity

VALUE ADDED SERVICES

At Hero MotoCorp, they believe in meeting and exceeding the

expectations of the customers. This extends beyond providing the best products

and unmatched service in the market. It includes a host of value added services

to enhance customers riding experience.

Working capital management

New Horizon College

40

3. RESEARCH DESIGN

3.1 RESEARCH DESIGN

Research design is the arrangement of conditions for collection and

analysis of data in a manner that aims to combine relevance to the research

purpose with economy in procedure. It constitutes the blueprint for the

collection, measurement and analysis of data. The design adopted in the study is

both descriptive and analytical done at branch level.

3.2 STATEMENT OF PROBLEM

This project deals with the study about ―Working Capital Management‖

in Hero MotoCorp Ltd. AMBICA MOTORS authorized representative of

dealer kumar hero.

The working capital management is very important term. It involves the

study of day-to-day affairs of the company. The motive behind the study is to

develop an understanding about the working capital management in the running

business organization and to help the company in developing the efficient

working capital management. Therefore, it helps in future planning and control

decisions.

If we look at any financial statement it will be evident that the investment

in fixed assets remains more or less static but the working capital is constantly

changing. A healthy working capital position is the thing that is absolutely

necessary of a successful business. This is reflected in adequate inventories,

lowest level of debtors, minimum utilization of bank facilities for working

capital, etc. thus the study of working capital management occupies an

important place in financial management.

Working capital management

New Horizon College

41

3.3 SCOPE OF THE STUDY

The study is conducted at Hero MotoCorp Ltd. AMBICA MOTORS. The

study of working capital management is purely based on secondary data and all

the information is available within the company itself in the form of records. To

get proper understanding of this concept, I have done the study of the balance

sheets, profit and loss A/C. So, scope of the study is limited up to the

availability of official records and information provided by the finance

department. The study is supposed to be related to the period of last three years.

The main scope of the study was to put into practical the theoretical

aspect of the study into real lifework experience.

The study of working capital is based on tools like Ratio Analysis,

Statement of changes in working capital. Further the study is based on last three

years balance sheet.

3.4 METHODOLOGY OF THE STUDY

Research methodology describes about the research objectives, design

and methodology adopted to conduct the study. The data collected can be either

primary or secondary. The above information is carried on with the cooperation

of management of Hero MotoCorp Ltd. AMBICA MOTORS.

3.5 OBJECTIVES OF STUDY

To analyze the effective utilization of working capital

To evaluate the performance of receivables and cash

To study the structure of working capital

To study the sources of working capital finance

To study need of working capital requirement in organization

Working capital management

New Horizon College

42

3.6 SOURCES OF DATA

The analysis of financial viability of the company necessitates accurate

and reliable data. Therefore, the methodology used for the collection of

information. There are mainly two types of data.

1 Primary data

2. Secondary data

PRIMARY DATA:

Most of the information is collected from internal discussion with various

officials in the finance department and concerned executive of other department.

SECONDARY DATA:

The information collection from:

Annual reports, published records and reference books, official websites.

Executive and staff of financial accounting department.

3.7 TOOLS OF ANALYSIS

There are some of the tools, which are relevant for the study of ration

analysis and performance of Hero MotoCorp Ltd. AMBICA MOTORS.

Net working capital

Ratio analysis

Balance sheet

Working capital management

New Horizon College

43

3.8 LIMITATIONS OF THE STUDY

The study is restricted for a period of three years only commencing from

2013-2016. So it shows limited period data is considered.

As the financial information is confidential, they do not want to share

accurate data or information.

Study duration is very short (one month only).

Limited interaction with concerned head because of their busy schedule.

Working capital management

New Horizon College

44

4. ANALYSIS AND INTERPRETATION OF DATA

4.1 STATEMENT OF CHANGES IN WORKING CAPITAL

Working capital means the excess of current assets over current liabilities.

Statement of changes in working capital is calculated for comparing the figure

of two consecutive years.

THE GENERAL RULE

a) An increase in current asset will increases working capital

b) A decrease in the current asset will decreases working capital

c) An increase in current liabilities will decreases working capital

d) A decrease in current liabilities will increases working capital.

The change in the amount of any current asset or current liability in the

current balance sheet as compared to that of previous balance sheet either results

in increase or decrease in working capital. The difference is recorded for each

individual current asset and current liability.

In case, current assets in the current period are more than in the previous

period, the effect is an increase in working capital and it is recorded in the

increase column. If a current liability in the current period is more than in the

previous period, the effect is decrease in working capital and it is recorded in

the decrease column.

Working capital management

New Horizon College

45

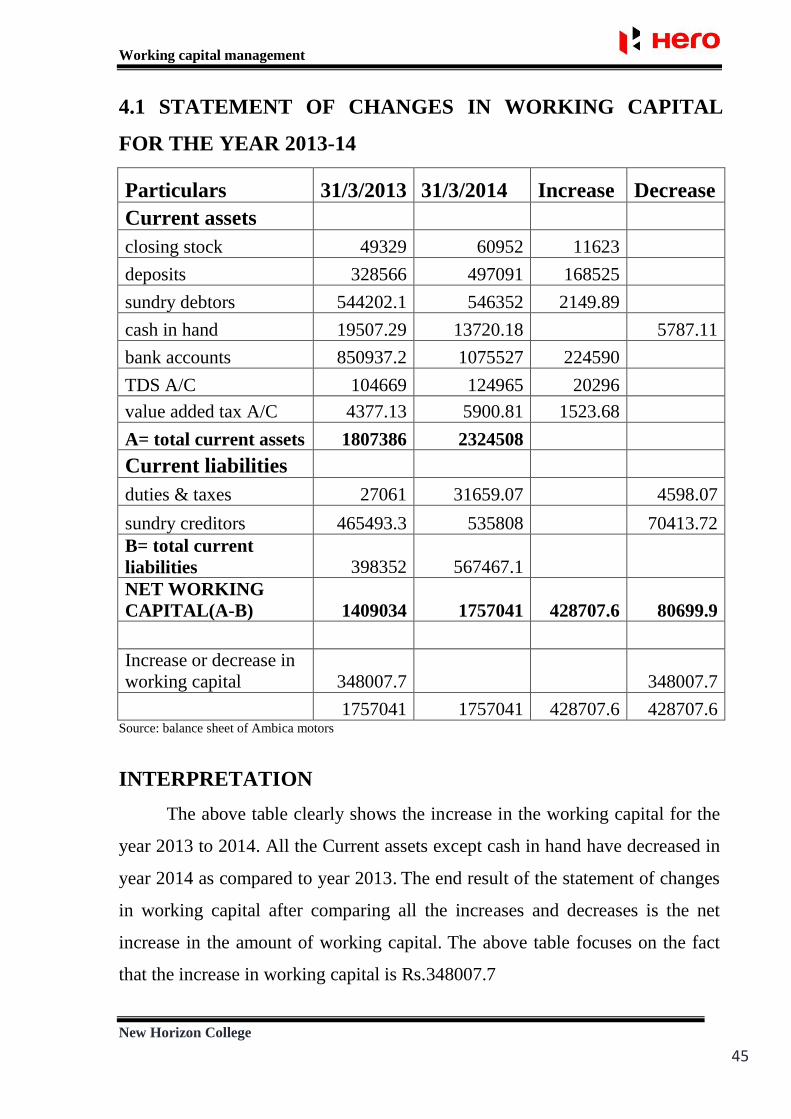

4.1 STATEMENT OF CHANGES IN WORKING CAPITAL

FOR THE YEAR 2013-14

Particulars 31/3/2013 31/3/2014 Increase Decrease

Current assets

closing stock 49329 60952 11623

deposits 328566 497091 168525

sundry debtors 544202.1 546352 2149.89

cash in hand 19507.29 13720.18 5787.11

bank accounts 850937.2 1075527 224590

TDS A/C 104669 124965 20296

value added tax A/C 4377.13 5900.81 1523.68

A= total current assets 1807386 2324508

Current liabilities

duties & taxes 27061 31659.07 4598.07

sundry creditors 465493.3 535808 70413.72

B= total current

liabilities 398352 567467.1

NET WORKING

CAPITAL(A-B) 1409034 1757041 428707.6 80699.9

Increase or decrease in

working capital 348007.7 348007.7

1757041 1757041 428707.6 428707.6 Source: balance sheet of Ambica motors

INTERPRETATION

The above table clearly shows the increase in the working capital for the

year 2013 to 2014. All the Current assets except cash in hand have decreased in

year 2014 as compared to year 2013. The end result of the statement of changes

in working capital after comparing all the increases and decreases is the net

increase in the amount of working capital. The above table focuses on the fact

that the increase in working capital is Rs.348007.7

Working capital management

New Horizon College

46

4.2 STATEMENT OF CHANGES IN WORKING CAPITAL

FOR THE YEAR 2014-15

Particulars 31/3/2014 31/3/2015 Increase Decrease

Current assets

closing stock 60952 90485 29533

deposits 497091 1193568 696477

sundry debtors 546352 549272 2919.79

cash in hand 13720.18 31116.68 17396.5

bank accounts 1075527 669936.3 405591

TDS A/C 124965 146221 21256

value added tax A/C 5900.81 5883.24 17.57

A= total current assets 2324508 2686482

Current liabilities

duties & taxes 31659.07 5000 26659.07

sundry creditors 535808 256890 278918

B= total current liabilities 567467.1 261890

NET WORKING

CAPITAL(A-B) 17757041 2424592 1073159 405608.6

Increase or decrease in

working capital 667550.8 667550.8

2424592 2424592 1073159 1073159 Source: balance sheet of Ambica motors

INTERPRETATION

The above table clearly shows the increase in the working capital for the

year 2014 to 2015. All the Current assets except bank account and value added

tax A/C have decreased in year 2015 as compared to year 2014. The end result

of the statement of changes in working capital after comparing all the increases

and decreases is the net increase in the amount of working capital. The above

table focuses on the fact that the increase in working capital is Rs.667550.8

Working capital management

New Horizon College

47

4.3 STATEMENT OF CHANGES IN WORKING CAPITAL

FOR THE YEAR 2015-16

Particulars 31/3/2015 31/3/2016 Increase Decrease

Current assets

stock 90485 78143 12342

deposits 1193568 2290545 1096977

sundry debtors 549272 565969 16697

cash in hand 31116.68 5787.29 25329.39

bank accounts 669936.3 811997.8 142061.5

TDS A/C 146221 169068.8 22847.8

value added tax A/C 5883.24 12249.33 6365.09

A= total current assets 2686482 3933760

Current liabilities

duties & taxes 5000 4500 500

sundry creditors 256890 327989 71099

B= total current

liabilities 261890 332489 NET WORKING

CAPITAL(A-B) 2424592 3601271 1285448 106770.4

Increase or decrease in

working capital 11176679 1176678

3601271 3601271 1285448 1285448 Source: balance sheet of Ambica motors

INTERPRETATION

The above table clearly shows the increase in the working capital for the

year 2015 to 2016. All the Current assets except stock and cash in hand have

decreased in year 2016 as compared to year 2015. The end result of the

statement of changes in working capital after comparing all the increases and

decreases is the net increase in the amount of working capital. The above table

focuses on the fact that the increase in working capital is Rs.11176679.

Working capital management

New Horizon College

48

4.2 RATIO ANALYSIS

A ratio is a relationship expressed in mathematical terms between two

individual groups of data connected with each other in some logical manner.

Ratio analysis is widely used tool of financial analysis. This systematic method

helps to interpret the financial statement so that the strengths and weakness of a

firm as well as the historical performance and current financial condition can be

determined.

A ratio can be used as a yardstick for evaluating the financial position and

performance of a concern, because the absolute accounting data cannot provide

meaningful understanding and Interpretation. A ratio is the relationship between

two accounting items expressed mathematically. Ratio analysis helps the analyst

to make quantitative judgment with regard to concern's financial position and

performance.

Purpose of the ratio analysis

To study the short term solvency of the firm- liquidity of the firm.

To study the long term solvency of the firm- leverage position of the firm.

To interpret the profitability of the firm- profit earning capacity of the firm.

To identify the operating efficiency of the firm- turnover of the ratios.

STEPS INVOLVED IN RATIO ANALYSIS

STEP 1

Calculation of ratios from the information obtained from financial statements

according to the requirement of decision.

STEP 2

Compare the calculated ratios with pre-determined standard ratios. They may be

a past ratio of the same organization average ratio or a projected ratio or the

ratio of the most successful organization in the industry.

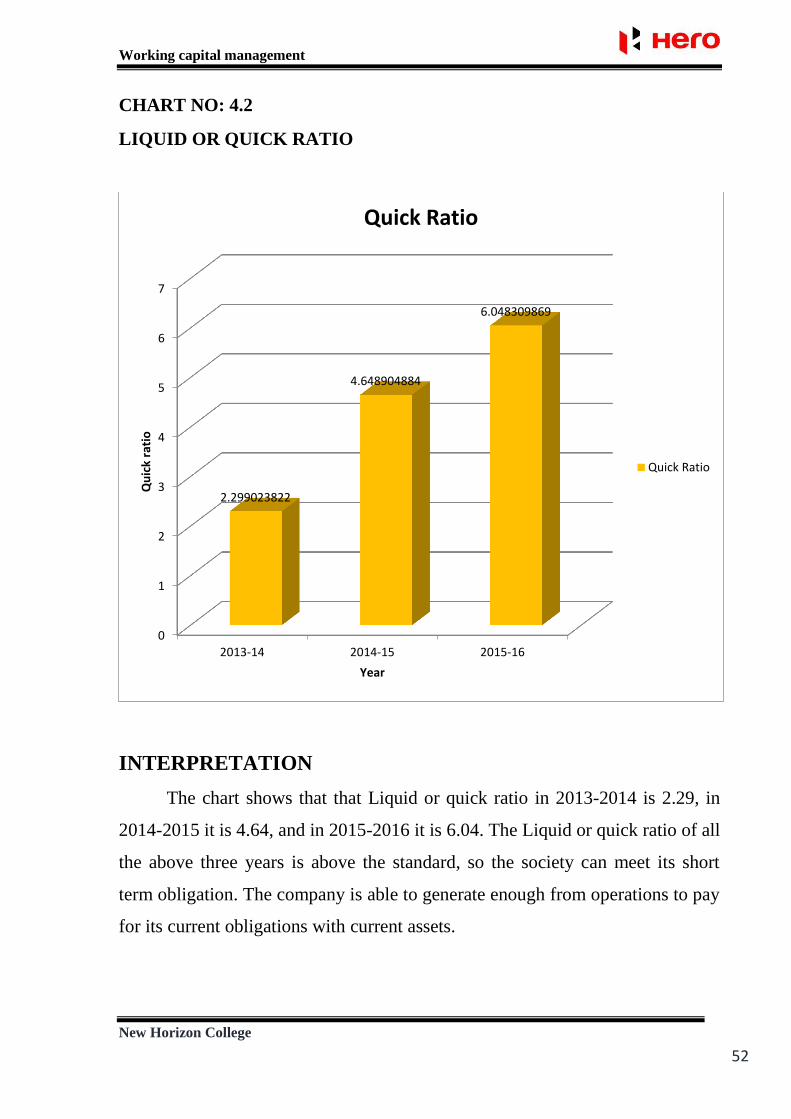

Working capital management

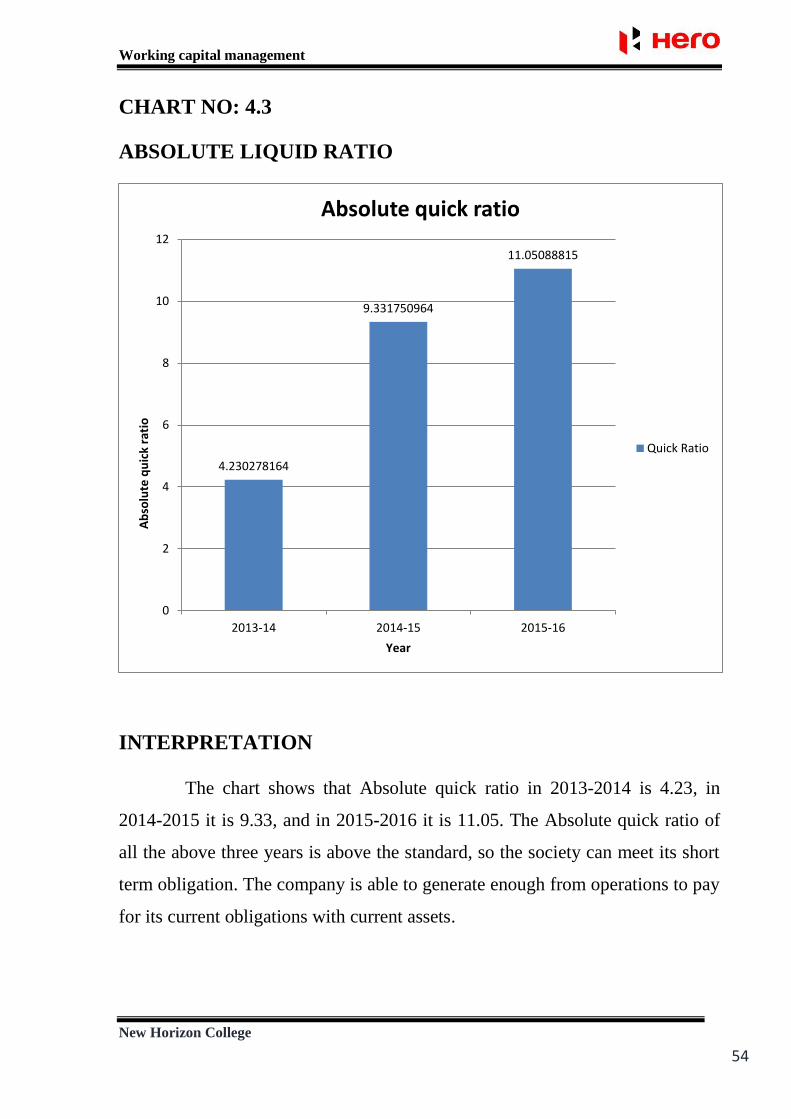

New Horizon College

49

LIQUIDITY RATIO

4.4 CURRENT RATIO

Current ratio may be defined as a relationship between current assets and

current liabilities. It is a measure of general liquidity and is most widely used to

make the analysis of short term financial position of a firm.

The ideal value of current ratio is 2:1

Current Ratio = Current Assets / Current Liabilities

Year Current

assets

Current

liabilities

Current

ratio

2013-14 1220002 504148.9 2.41

2014-15 1307987 261890 4.99

2015-16 2089140 332489 6.28

Source: balance sheet of Ambica motors

ANALYSIS

From the above table, we can observed that current ratio in 2013-2014 it is 2.41,

in 2014-2015 it is 4.99, in 2015-2016 it is 6.28. This is higher than ideal ratio.

The ideal value of current ratio is 2:1

Working capital management

New Horizon College

50

CHART NO: 4.1

CURRENT RATIO

INTERPRETATION

The chart shows that current ratio in 2013-2014 is 2.41, in 2014-2015 it is

4.99 and in 2015-2016 it is 6.28. The current ratio of all the above three years is

above the standard, so the society can meet its short term obligation. The