Embed Size (px)

Citation preview

School of Insurance

®

Property & Casualty

Property & Casualty Exam Workbook

General Lines Personal Lines Exam Review

Based on the 29th Edition of the State Study Manual

"Information which is copyrighted by and proprietary to Insurance Services Office, Inc. or its

affiliates ("ISO Material") is included in this publication. Use of the ISO Material is limited to

ISO Participating Insurers and their Authorized Representatives and other licensees. Use by

ISO Participating Insurers is limited to use in those jurisdictions for which the insurer has an

appropriate participation with ISO. Use of the ISO Material by Authorized Representatives is

limited to use solely on behalf of one or more ISO Participating Insurers."

© Reicon Publishing, LLC. All rights reserved.

Thank you for choosing Gold Coast School of Insurance for your insurance educational needs. This course has been designed to help you master the material necessary to successfully pass the Florida Property & Casualty insurance licensing exam. Our goal is to prepare you to “PASS” the state exam on your “FIRST ATTEMPT”. To accomplish this, you must dedicate yourself to achieving this same goal. As you peruse through your textbooks you may become overwhelmed. Relax and take a deep breath. Gold Coast has been training insurance professionals for over 25 years so we understand the difficulties, apprehensions, and pressures you may be experiencing. We have repeatedly been selected by both local and national insurance companies and agencies as their “go-to” school for insurance pre-licensing and continuing education. The 2-20 General Lines Agent Pre-Licensing Course will provide you with the necessary knowledge to pass Florida’s Pre-Licensing Exam for the General Lines Authority. The format includes 200 intense, knowledge filled hours providing you with facts, scenarios, and a battery of online unit examinations covering topics such as general insurance, provisions, practices, ethics, rules and regulations, and much more. The course will culminate with an online cumulative final exam, which you must successfully pass. Upon successfully passing our pre-licensing course, you will be granted a certificate that will allow you to sit for the state exam (administered by Pearson Vue). Those that earn their General Lines Producer License will be able to sell, solicit, and negotiate products like: Home, Auto, Business, Workers Compensation, Bonds, and more. We look forward to having you join the ranks as a Gold Coast Schools alumni. If you have any questions, please do not hesitate to ask any Gold Coast Schools team member. Good Luck! John Greer, DBA Kevin R. Milner, MBA, CIC, ITP Gold Coast Owner Insurance Program Director

This page was intentionally left blank

Property & Casualty Exam Workbook Welcome

© Reicon Publishing LLC. All Rights Reserved. i

The Florida insurance industry is regulated by the Florida Department of Financial Services (FL-DFS). All agents, agent candidates, businesses and licensees must operate within the guidelines, statues, rules and regulations of the Department. As an approved insurance educational provider of the State of Florida, Gold Coast Schools must also adhere to these guidelines. General Information This course guide is utilized for the following courses - 2-20 Agent: General Lines Blended Course.

FL-DFS Course Approval Code: 100754 - 20-44 Agent: Personal Lines Blended Course

FL-DFS Course Approval Code: 100795 - 2-20 Agent: Conversion Blended Course

FL-DFS Course Approval Code: 100772 The following items are included with your course tuition:

• State Study Manual

• Gold Coast State Exam Study Guide

• Access to Gold Coast Property & Casualty Exam Cram

• Other classroom handouts

All material supplied with the course are subject to United States Copyright laws. Department of Financial Services regulations prohibits the use of personal communication devices during class sessions. Video or audio recording in any Gold Coast School classroom is prohibited. Class Conduct As a student of Gold Coast, you are expected to be courteous to Gold Coast faculty, staff, and other students. Inappropriate behavior cannot and will not be tolerated. Instructors and staff are empowered to ask any person not meeting this code of conduct to leave the classroom or facility. Please arrive on time and be prepared for class. Bring pencils, highlighters, notebooks, and all textbooks to every class. No other books, flashcards, learning ancillaries, laptops, tablets, newspapers, magazines, will be permitted in class. Please do not carry on private conversations while class is in session. This behavior is rude towards fellow students who are trying to master the material. During class breaks, please be aware that other classes might be in session. Please dispose of any trash or other waste appropriately. Only bottled water is permitted in the classroom. Testing All unit quizzes and the cumulative final exam are administered online via the Gold Coast website. Students will be required to complete all unit quizzes with a minimum passing score of 80%. All unit quizzes are given an unlimited time frame and may be taken as many times as necessary to achieve a passing score.

Welcome Property & Casualty Exam Workbook

ii © Reicon Publishing LLC. All Rights Reserved.

The 2-20 Agent General Lines final exam is available online once all unit quizzes are passed with the minimum score and students have recorded a minimum of 135 classroom hours. The final exam is time but may be taken as many times as necessary to pass. A minimum passing score of 70% is required on the final exam. The 20-44 Agent Personal Lines agents must complete all required quizzes and have a minimum of 45 classroom hours. The Personal Lines final exam is also timed. A minimum passing score of 70% is required on the final exam. The 2-20 Conversion course does not have a quiz requirement but does have a final exam. The final exam is time but may be taken as many times as necessary to pass. A minimum passing score of 70% is required on the final exam. Attendance The Department of Financial Services requires that Gold Coast Schools accurately record student attendance. The 2-20 General Lines class meeting schedule is as follows:

Day Class .............. Monday – Friday ................................... 9:00 am – 6:00 pm Evening Class ........ Monday, Wednesday, Thursday ........... 6:30 pm – 10:30 pm Weekend Class ...... Saturday & Sunday ............................... 9:00 am – 5:00 pm

Along with our internal records, you have been provided with a self-attendance form so that you may maintain your own attendance records. Instructors will randomly take attendance throughout each session. Each student is required to sign in and out on the instructor provided daily attendance sheet to obtain credit for that day’s class session. Students who enter late or leave early will only earn credit for the time spent in class. If the class is dismissed early for any reason (hurricane, power failure, instructor illness, etc.), you will only be awarded credit for actual hours attended. Students who fail to sign both in and out will not receive credit for any hours on that day. Once the sign-in/out sheet is submitted, no changes can be made to it. Starting times, break times, lunch, and ending times are all filed with the Department of Financial Services. The shortening of lunch and or break periods to allow early dismissal is not permitted. If a deviation between your self-attendance form and our attendance form exists, Gold Coast’s records will prevail. Students registered in a particular class may attend another scheduling format for the same course to complete additional hours or make-up missed session(s). All students are issued a Gold Coast Name Badge/Identification Badge (Gold Coast ID). You must have your Gold Coast ID with you at all times. When taking a class during another scheduling format or when taking a make-up quiz or final exam, you will need to provide both your Gold Coast ID and some other government approved photo identification. You must complete the Agent Pre-Licensing Course within 12 (twelve) months. Attendance hours and all grades more than twelve months old are void and new class tuition will be required. NO EXCEPTIONS.

Property & Casualty Exam Workbook Welcome

© Reicon Publishing LLC. All Rights Reserved. iii

Refunds Department of Financial Services requires that we advise you of Gold Coast Schools refund policy.

• DFS does not require refunds unless a class is cancelled by Gold Coast Schools. Students are advised that the payor of the course is entitled to a full tuition refund. If the student drops out by the first break on the first day of class, and have not marked or damaged any of the tuition supplied course material. If the supplied course material is used (damaged, written in, defaced) Gold Coast will deduct the cost of the item from their refund; the item may then be kept by the student. There are no refunds after the first break on the first day of class, for any reason. Your tuition allows you to attend classes you registered for, at no additional cost, for up to 12 months from the date of registration. Tuition is not transferable.

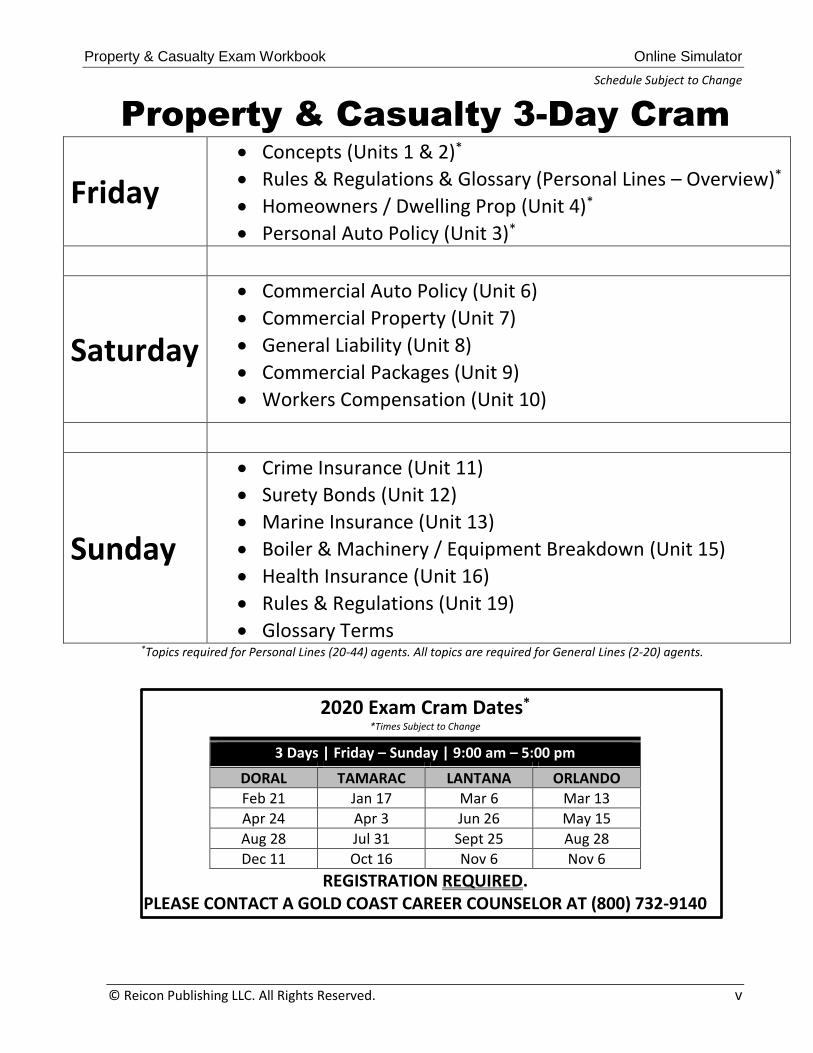

Property & Casualty Exam Workbook P&C 3 Day Exam Cram

iv © Reicon Publishing LLC. All Rights Reserved.

Property & Casualty

Online Exam Simulator

$40.00 + Tax

Contact a Gold Coast

Career Counselor

to Purchase an Access Code.

(800) 732-9140

Property & Casualty Exam Workbook Online Simulator

© Reicon Publishing LLC. All Rights Reserved. v

Schedule Subject to Change

Property & Casualty 3-Day Cram

Friday

• Concepts (Units 1 & 2)*

• Rules & Regulations & Glossary (Personal Lines – Overview)*

• Homeowners / Dwelling Prop (Unit 4)*

• Personal Auto Policy (Unit 3)*

Saturday

• Commercial Auto Policy (Unit 6)

• Commercial Property (Unit 7)

• General Liability (Unit 8)

• Commercial Packages (Unit 9)

• Workers Compensation (Unit 10)

Sunday

• Crime Insurance (Unit 11)

• Surety Bonds (Unit 12)

• Marine Insurance (Unit 13)

• Boiler & Machinery / Equipment Breakdown (Unit 15)

• Health Insurance (Unit 16)

• Rules & Regulations (Unit 19)

• Glossary Terms *Topics required for Personal Lines (20-44) agents. All topics are required for General Lines (2-20) agents.

2020 Exam Cram Dates*

*Times Subject to Change

REGISTRATION REQUIRED. PLEASE CONTACT A GOLD COAST CAREER COUNSELOR AT (800) 732-9140

3 Days | Friday – Sunday | 9:00 am – 5:00 pm

DORAL TAMARAC LANTANA ORLANDO

Feb 21 Jan 17 Mar 6 Mar 13

Apr 24 Apr 3 Jun 26 May 15

Aug 28 Jul 31 Sept 25 Aug 28

Dec 11 Oct 16 Nov 6 Nov 6

P&C Course Attendance Log Property & Casualty Exam Workbook

© Reicon Publishing LLC. All Rights Reserved. vi

Property & Casualty Exam Workbook Test Taking Techniques

© Reicon Publishing LLC. All Rights Reserved. vii

Test Taking Techniques The following techniques are designed to “boost” your results on your exam by increasing your chances of getting a correct answer to those questions that you are not very positive of the correct answer. When in doubt, fall back on these techniques; they will dramatically increase your chances of obtaining a higher score. Pace yourself on the exam, do not panic - read every question carefully! Go through the exam the first time allowing only about 1 minute per question. This will allow you to get all the “easy” points. Answer all questions the first time through. If you are not sure about the question, mark it for review. Remember, the ones you could not get are the ones you would not get anyway, but by using this technique, you have gotten as many points as possible in the time you have available. With the extra time left over, go back and examine the questions you marked for review. Do not be discouraged if the exam seems difficult, because it is supposed to be difficult. If it seems too easy to you, beware, you may be picking the obvious answers and missing the tricks and traps that are built in. Be sure to aim for 100%, but remember you are not supposed to get a perfect score. If you do not quit, you will do better than you think! Do not be paranoid and think that every question is a trick. Do not read into a question facts or presumptions that are not there. Do not place undue pressure on yourself. Read each question carefully and calmly. Read each answer before selecting one and be very wary of changing answers, since your first response is usually the best response. On many questions, especially the longer ones block the answers before you read the question. Reflect on the question and ask yourself if you had written the question, what you would expect the answer to be. Make sure you totally understand the question before you even think of looking at the answers. Often, when you look at the answers, the correct answer will jump right off the page. Try to avoid answers with absolute words in them like “must”, “never”, “all”, “always”, “only”, “would be”, etc. These types of words are usually found in incorrect answers. Words that soften a statement like “may”, “usually”, “sometimes”, “possibly”, “can”, etc., are more often found in correct answers. Remember, there are few exceptions: (e.g.: an application for a policy must be fully completed and signed by the applicant, owner and agent.) Be sure to be alert to the words “because” or “since.” these words often take a correct statement and make it incorrect. (This is this, because.) Be careful with negative questions and remember that two negatives equal a positive. When asked for the “incorrect” answer or when you have I, II, III (multi-tier) type questions, always treat each answer as a true-false question and read the question with each answer. If the question is asking, “which is” look for true answers. If the question asks, “which is not” then look for false answers. “All of the above” can help the process of elimination. If obviously there are 2 correct answers, but you are not sure of a 3rd answer, choose “all of the above”. If you are certain that one of the choices is incorrect, then “all of the above” would be eliminated as a choice. This leaves a choice of

Test Taking Techniques Property & Casualty Exam Workbook

viii © Reicon Publishing LLC. All Rights Reserved.

two, which can be decided using the true-false technique. “None of the above” is usually an incorrect response unless coupled with a double negative. When answering a question that is very unfamiliar to you, search for clues in the answers. Often a ‘key word or thought’ in a question will tie into the same ‘key word or thought’ in the correct answer. Be alert to questions with three similar or synonymous answers and one opposite answer. Often the opposite answer is correct. If two answers are direct opposites of each other, there is a good chance that one of those two answers is the correct one. (50% chance instead of the 25% chance). Determine the questioner’s point of view. Answers may differ quite drastically depending on whose point of view we are considering: (insurer vs. insured) - (state vs. federal law). Apply the “golden rule” to answers pertaining to law or principles of law. On long drawn out questions, which use confusing names or letters to identify the players (e.g.: a, b, c and d) or (Mr. Green, Mr. Blue, and Mrs. Brown) or (Smith, Jones, White and Black) etc. Be sure to write down who is who on your scratch paper before you attempt the question. Often on this type of question, it is beneficial to read the answers before you read the question. This gives you the opportunity to eliminate the “fluff’” in the question. It is often helpful to “name” the letters, especially in complicated, long questions: (a = Allen, b = Bob, c = Charles, d = David). Often, questions contain certain information that is unimportant. Cross this off mentally to reduce the long question down to the bare facts needed to determine exactly what it is that is being asked for example: “john has purchased a whole life policy from the ABC life company Fort Lauderdale, Florida providing $100,000 death benefit. If, after all of the above has failed and you have absolutely no idea, then guess “b” or “c” instead of “a” or “d”, or guess the longest answer choice given. The best method for success on any exam is preparation! Go to the exam well rested. Listen to the proctor’s instructions do the tutorial carefully. Be positive, dress for success (photo will be taken). Be slightly hungry, as a full stomach requires the blood to be used to digest food. You want the blood in your brain! Most important, have confidence in your ability! Good luck and believe in yourself.

Property & Casualty Exam Workbook Table of Contents

General Lines Agent State Exam Preparation

Materials

Table of Contents Unit 2 Property & Liability Insurance Concepts ............................................................................................... 1

Unit 3 Personal Automobile ........................................................................................................................... 21

Unit 4 Homeowners, Dwelling, & Related Coverages .................................................................................... 57

Unit 6 Commercial Automobile .................................................................................................................... 109

Unit 7 Property ............................................................................................................................................. 117

Unit 8 General Liability ................................................................................................................................. 139

Unit 9 Package Policies ................................................................................................................................. 175

Unit 10 Workers Compensation ................................................................................................................... 185

Unit 11 Crime ................................................................................................................................................ 199

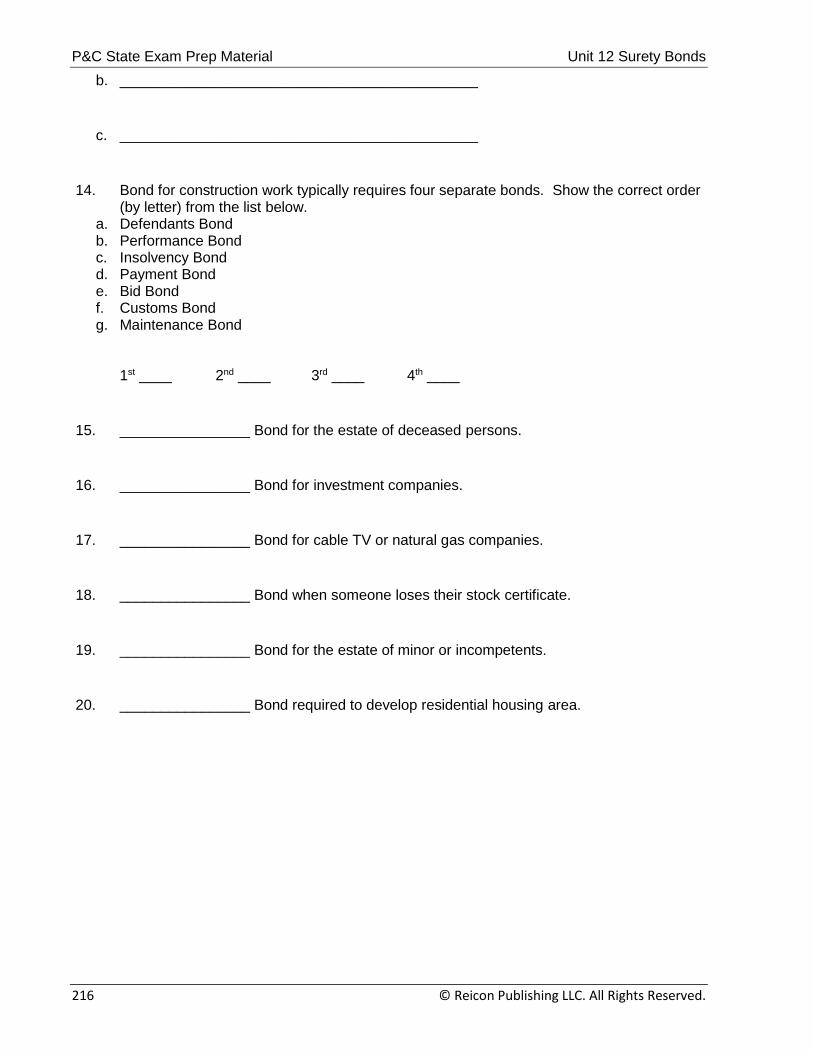

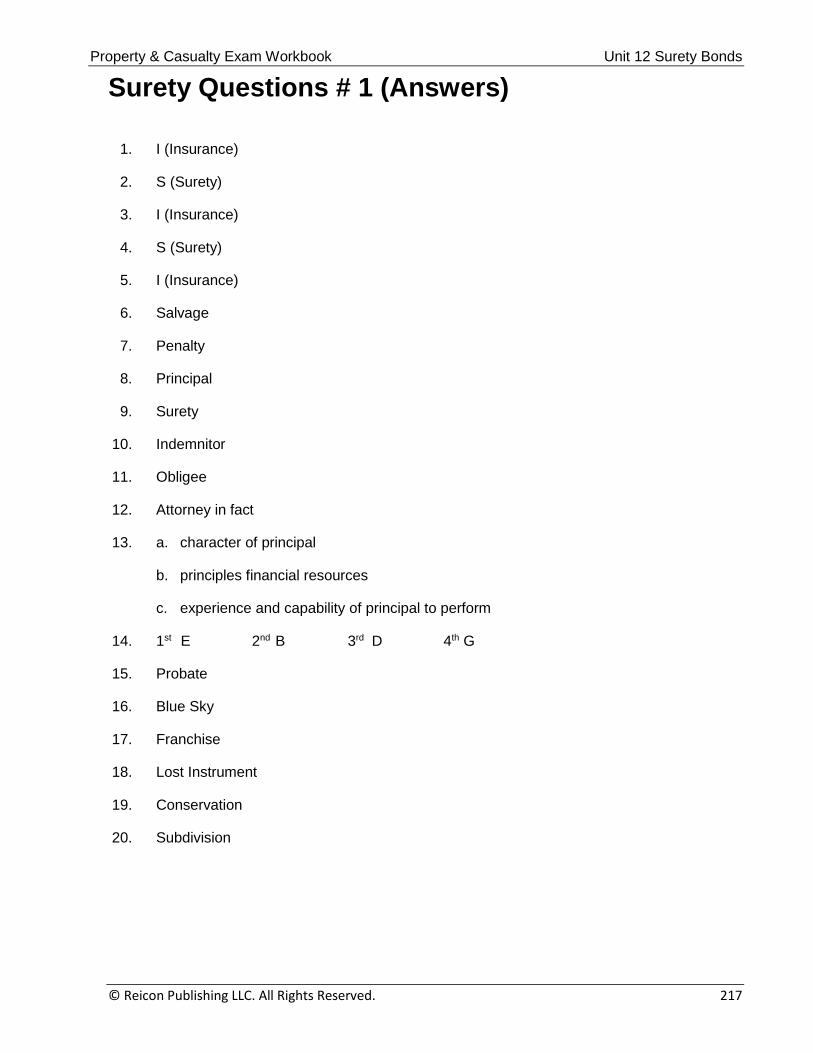

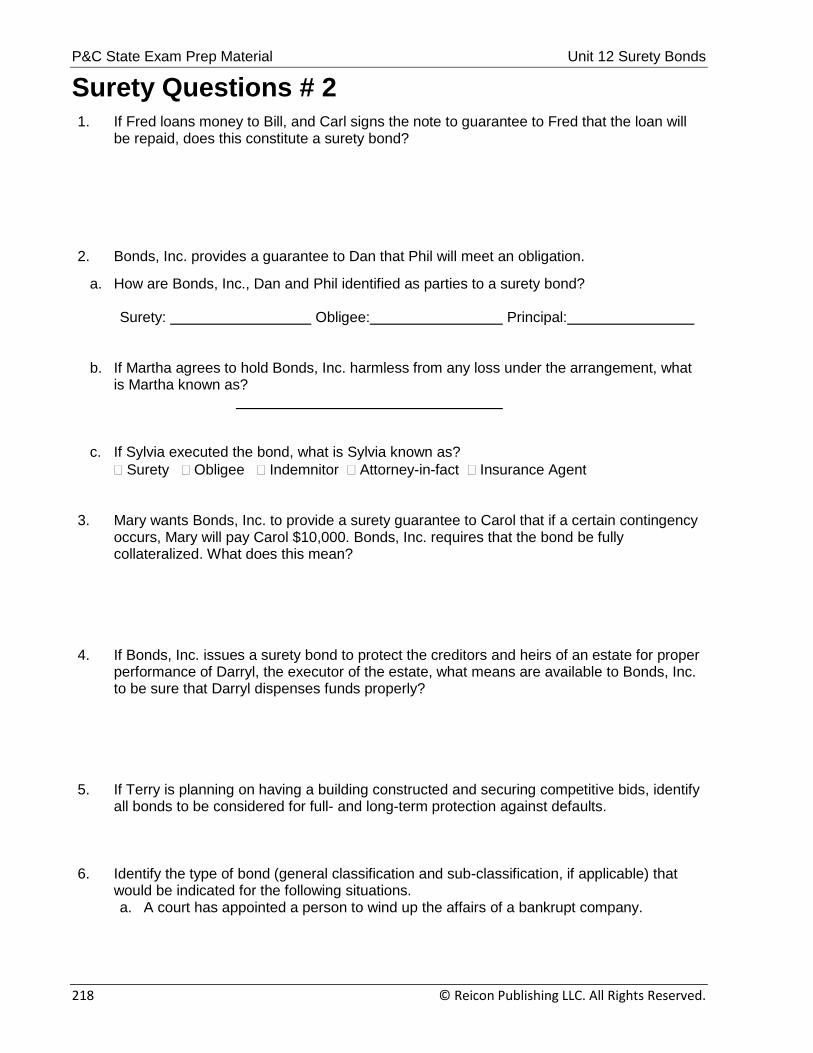

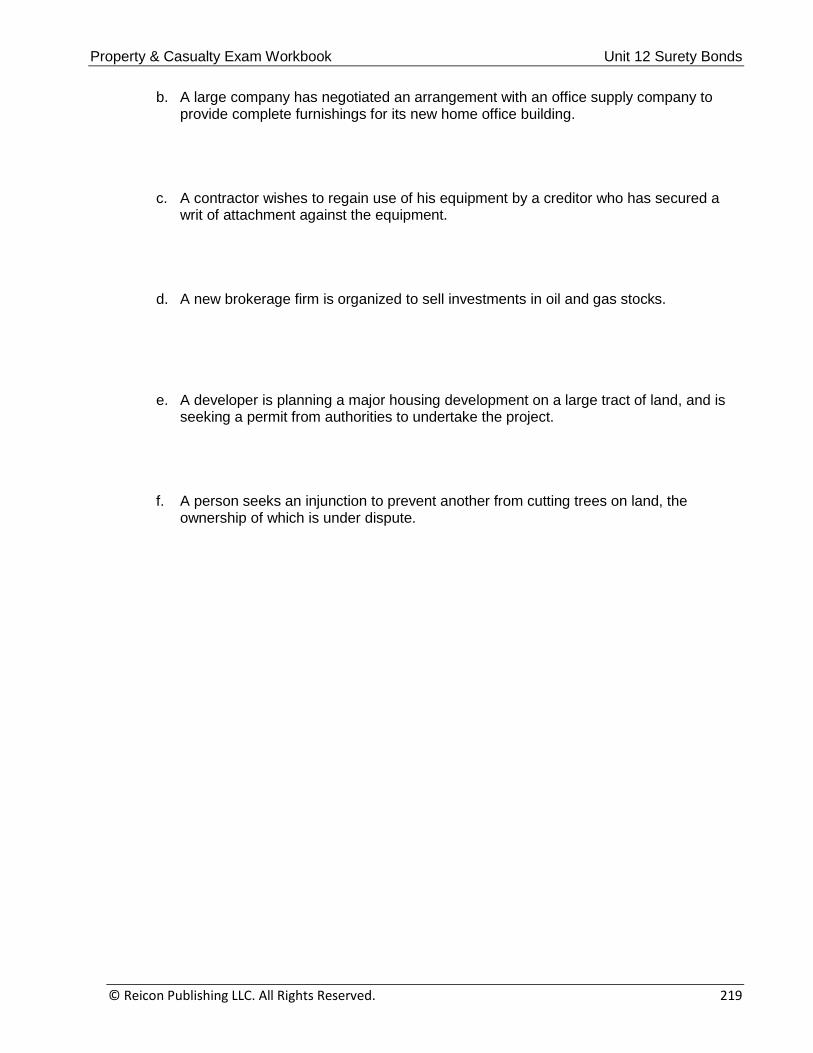

Unit 12 Surety Bonds .................................................................................................................................... 209

Unit 13 Marine ............................................................................................................................................. 221

Unit 14 Aviation ............................................................................................................................................ 235

Unit 15 Boiler & Machinery / Equipment Breakdown ................................................................................. 241

Unit 16 Health .............................................................................................................................................. 251

Unit 17 Residual Markets ............................................................................................................................. 263

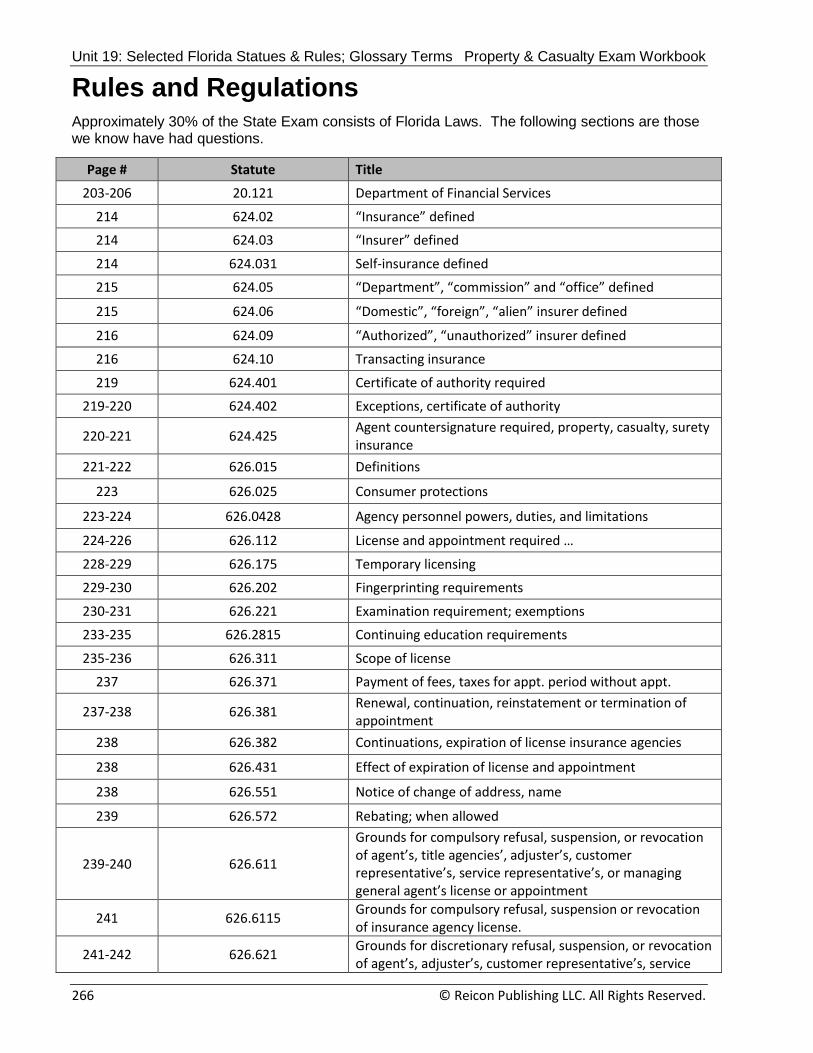

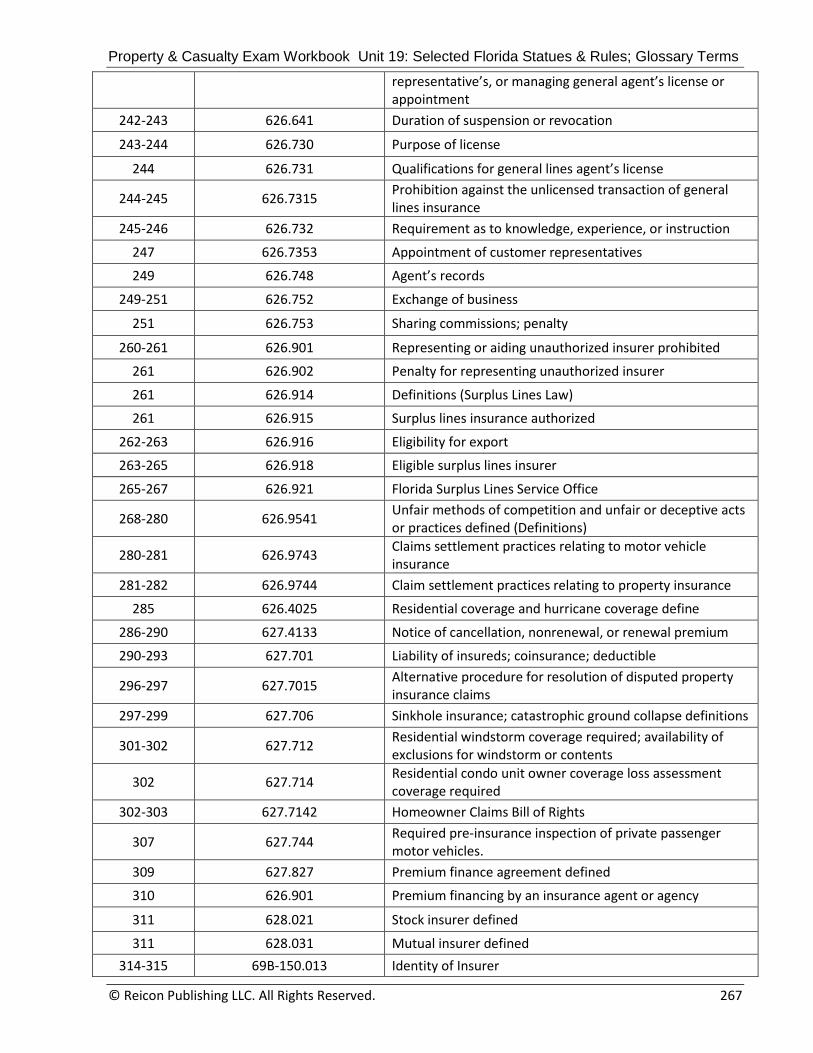

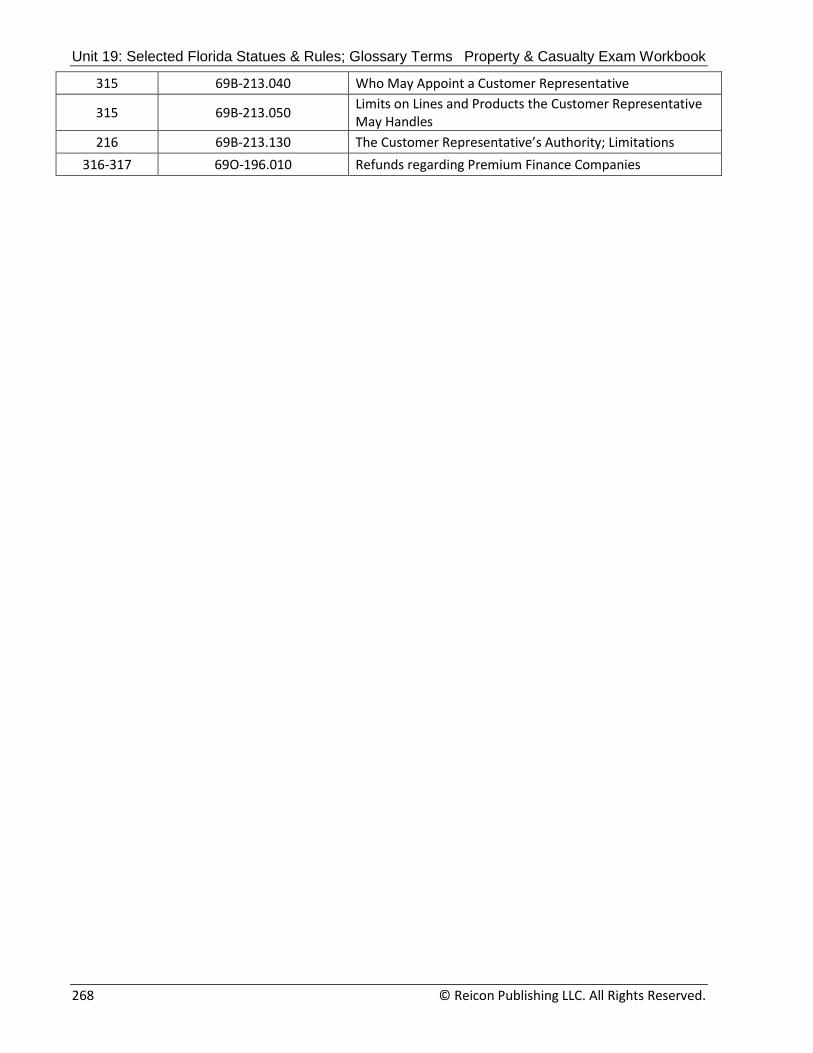

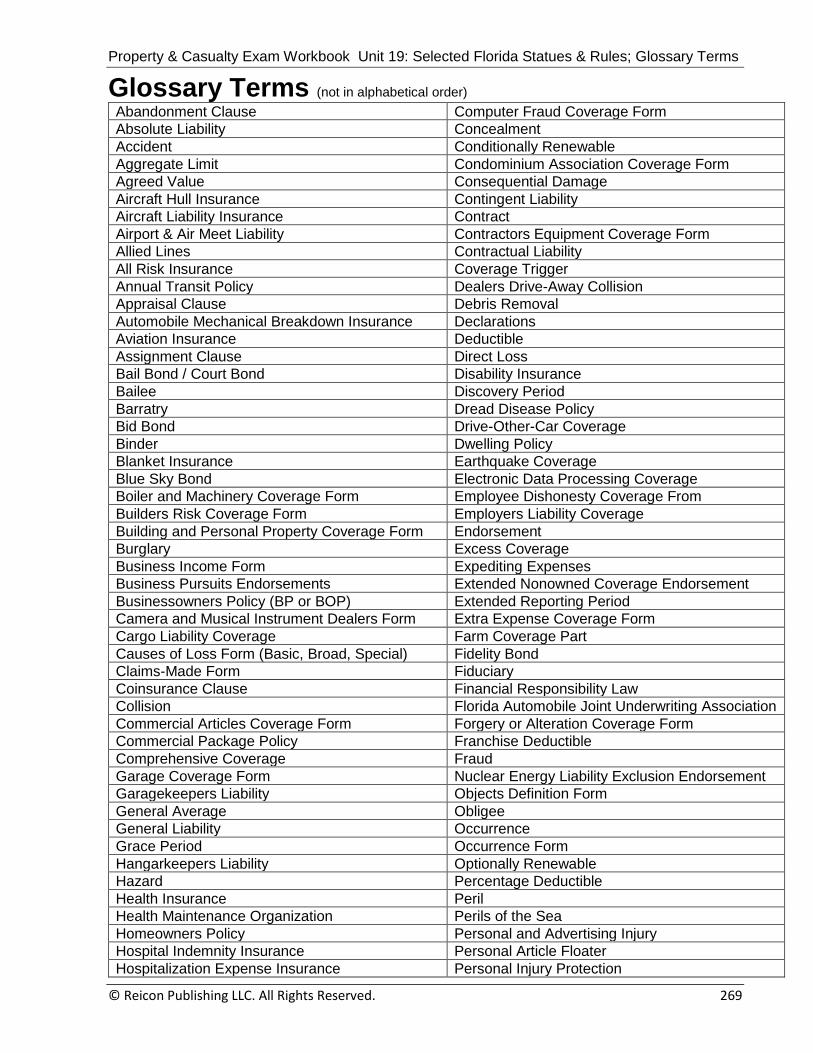

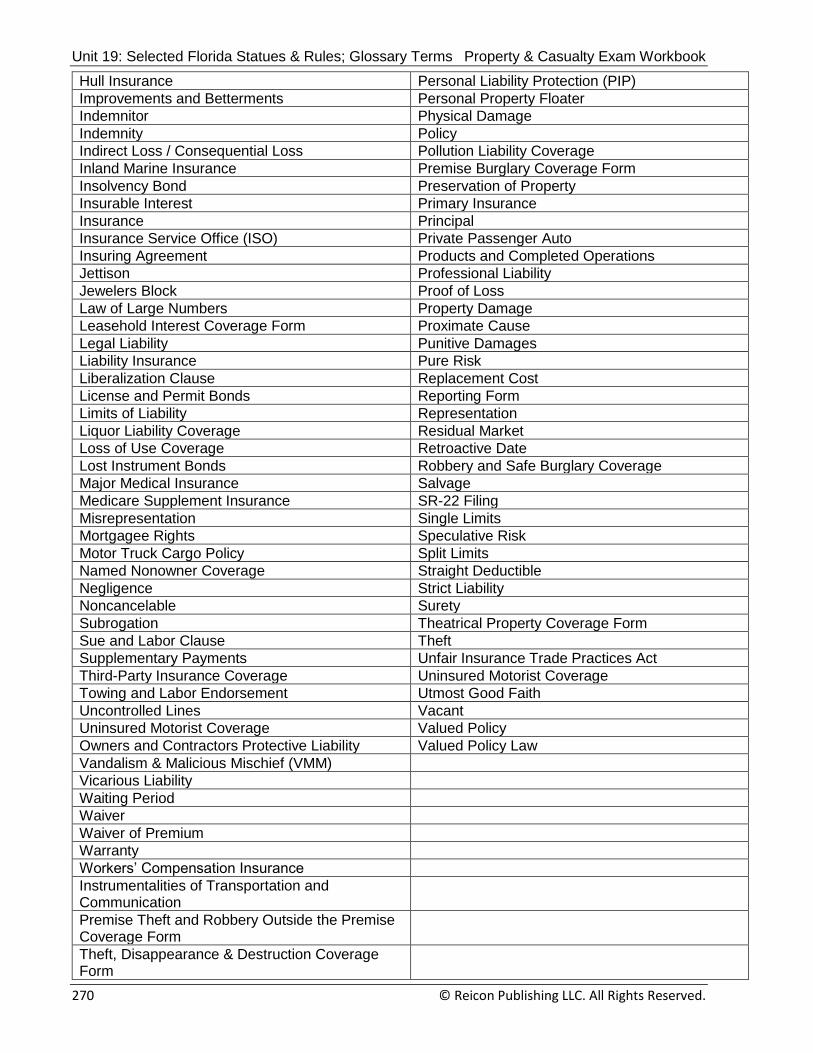

Unit 19 Selected Florida Statutes & Rules, Glossary Terms ......................................................................... 265

Surplus Lines Pre-Licensing Course Information Packet ............................................................................. 271

Table of Contents Property & Casualty Exam Workbook

This page was intentionally left blank

Property & Casualty Exam Workbook Unit 2: Property & Liability Insurance Concepts

© Reicon Publishing, LLC. All Rights Reserved. 1

UNIT

PROPERTY & LIABILITY INSURANCE CONCEPTS

OVERVIEW

This unit reviews basic concepts that generally underlie contracts of property and

liability insurance. The importance of all insurance practitioners understanding these

principles cannot be overemphasized. One might read and fully understand every word

of a policy contract; yet failure to understand concepts and underlying principles could

lead to incorrect conclusions about the respective rights and responsibilities of the

parties

OBJECTIVES

After completing this chapter, you should be able to understand:

• Risk

• What is an insurance policy?

• Binders

• “Property & Liability” Insurance

• Insurance Contract Characteristics

• Property Insurance Concepts

• Liability Insurance Concepts

• Bases for Insurer Avoidance of Performance

Unit 2: Property & Liability Insurance Concepts Property & Casualty Exam Workbook

2 © Reicon Publishing, LLC. All Rights Reserved.

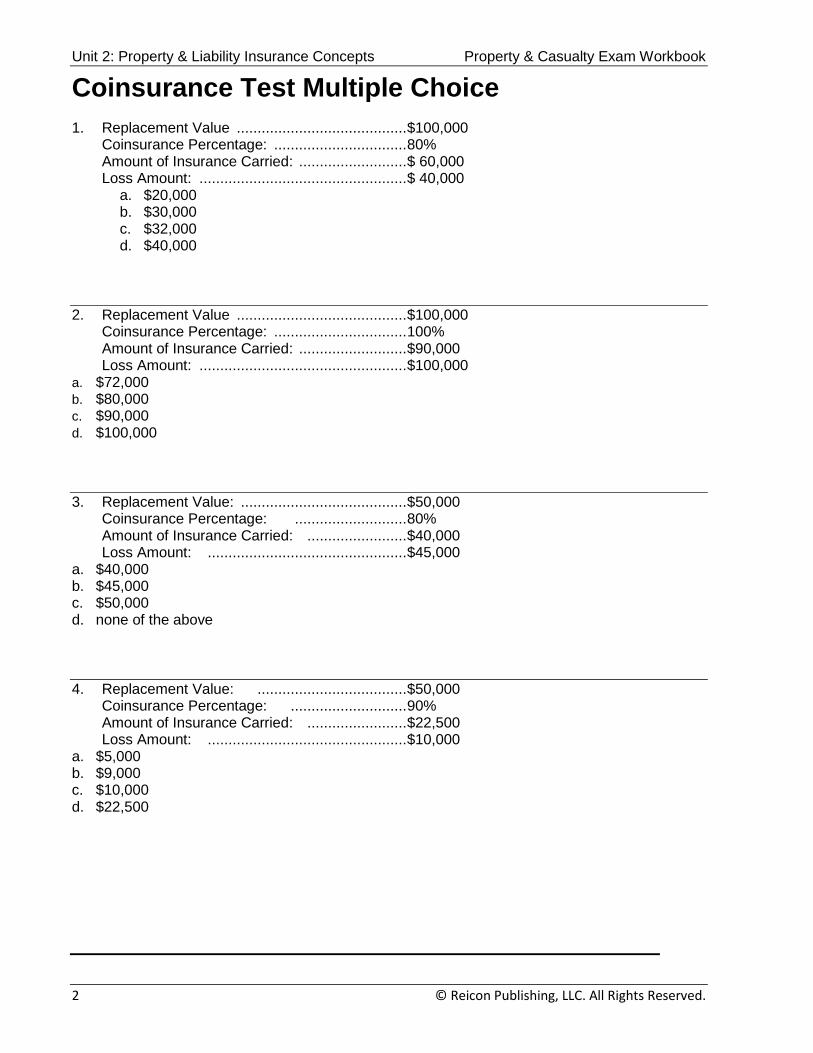

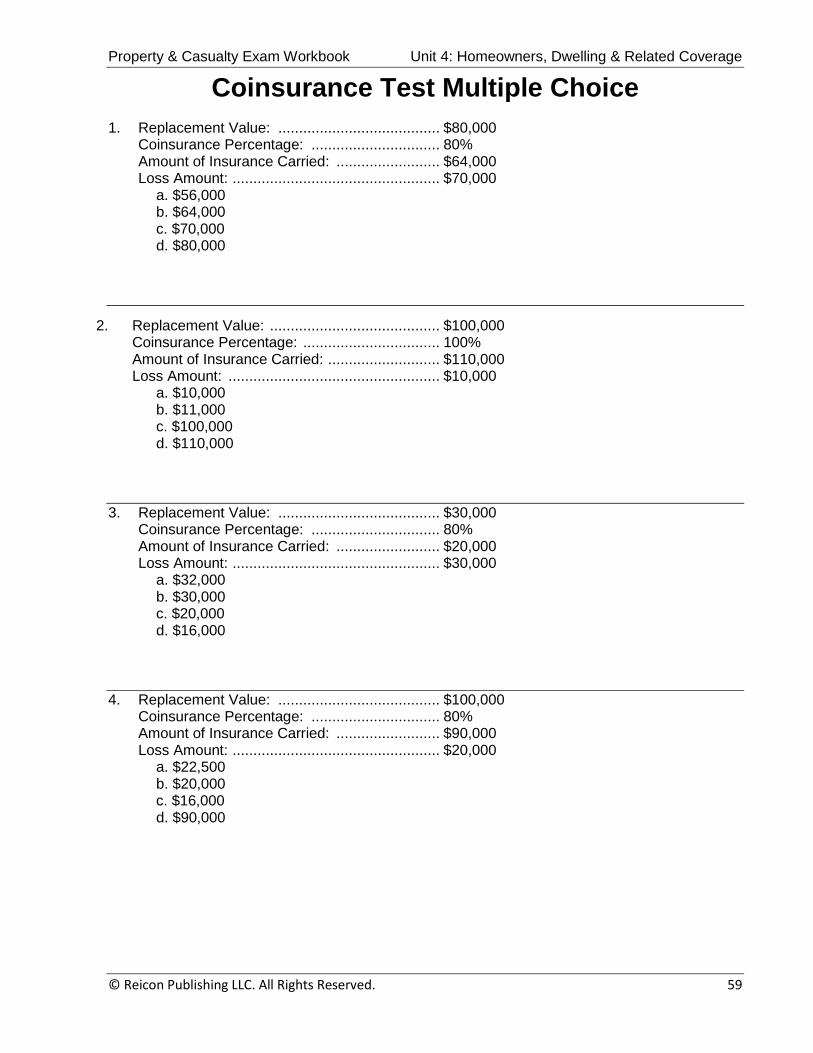

Coinsurance Test Multiple Choice 1. Replacement Value ......................................... $100,000 Coinsurance Percentage: ................................ 80% Amount of Insurance Carried: .......................... $ 60,000 Loss Amount: .................................................. $ 40,000

a. $20,000 b. $30,000 c. $32,000 d. $40,000

2. Replacement Value ......................................... $100,000 Coinsurance Percentage: ................................ 100% Amount of Insurance Carried: .......................... $90,000 Loss Amount: .................................................. $100,000 a. $72,000 b. $80,000 c. $90,000 d. $100,000

3. Replacement Value: ........................................ $50,000 Coinsurance Percentage: ........................... 80% Amount of Insurance Carried: ........................ $40,000 Loss Amount: ................................................ $45,000 a. $40,000 b. $45,000 c. $50,000 d. none of the above

4. Replacement Value: .................................... $50,000 Coinsurance Percentage: ............................ 90% Amount of Insurance Carried: ........................ $22,500 Loss Amount: ................................................ $10,000 a. $5,000 b. $9,000 c. $10,000 d. $22,500

Property & Casualty Exam Workbook Unit 2: Property & Liability Insurance Concepts

© Reicon Publishing, LLC. All Rights Reserved 3

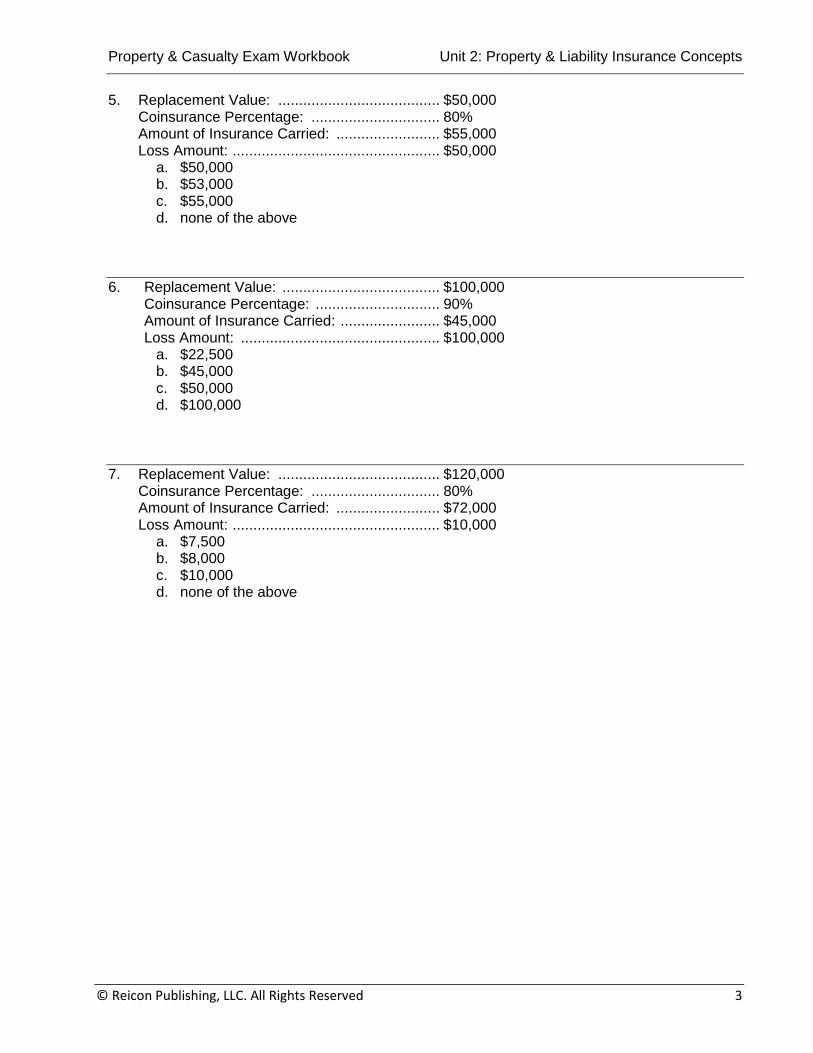

5. Replacement Value: ....................................... $50,000 Coinsurance Percentage: ............................... 80% Amount of Insurance Carried: ......................... $55,000 Loss Amount: .................................................. $50,000

a. $50,000 b. $53,000 c. $55,000 d. none of the above

6. Replacement Value: ...................................... $100,000 Coinsurance Percentage: .............................. 90% Amount of Insurance Carried: ........................ $45,000 Loss Amount: ................................................ $100,000

a. $22,500 b. $45,000 c. $50,000 d. $100,000

7. Replacement Value: ....................................... $120,000 Coinsurance Percentage: ............................... 80% Amount of Insurance Carried: ......................... $72,000 Loss Amount: .................................................. $10,000

a. $7,500 b. $8,000 c. $10,000 d. none of the above

Unit 2: Property & Liability Insurance Concepts Property & Casualty Exam Workbook

4 © Reicon Publishing, LLC. All Rights Reserved.

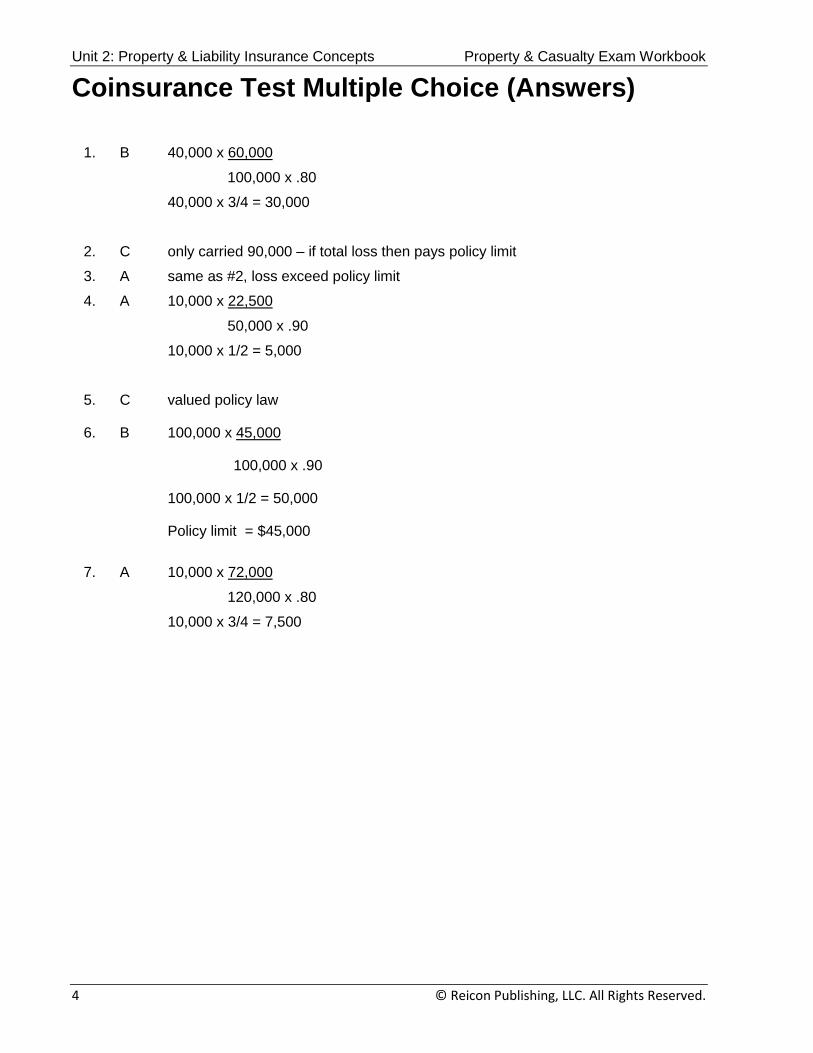

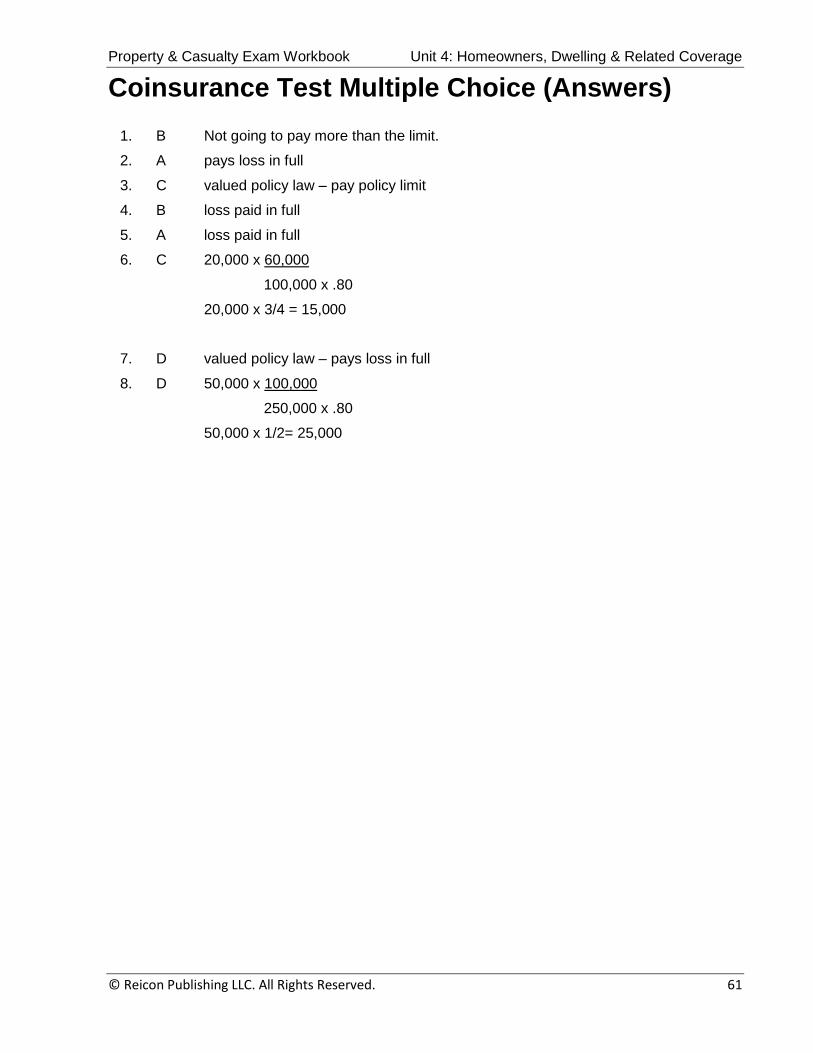

Coinsurance Test Multiple Choice (Answers)

1. B 40,000 x 60,000

100,000 x .80

40,000 x 3/4 = 30,000

2. C only carried 90,000 – if total loss then pays policy limit

3. A same as #2, loss exceed policy limit

4. A 10,000 x 22,500

50,000 x .90

10,000 x 1/2 = 5,000

5. C valued policy law

6. B 100,000 x 45,000

100,000 x .90

100,000 x 1/2 = 50,000

Policy limit = $45,000

7. A 10,000 x 72,000

120,000 x .80

10,000 x 3/4 = 7,500

Property & Casualty Exam Workbook Unit 2: Property & Liability Insurance Concepts

© Reicon Publishing, LLC. All Rights Reserved 5

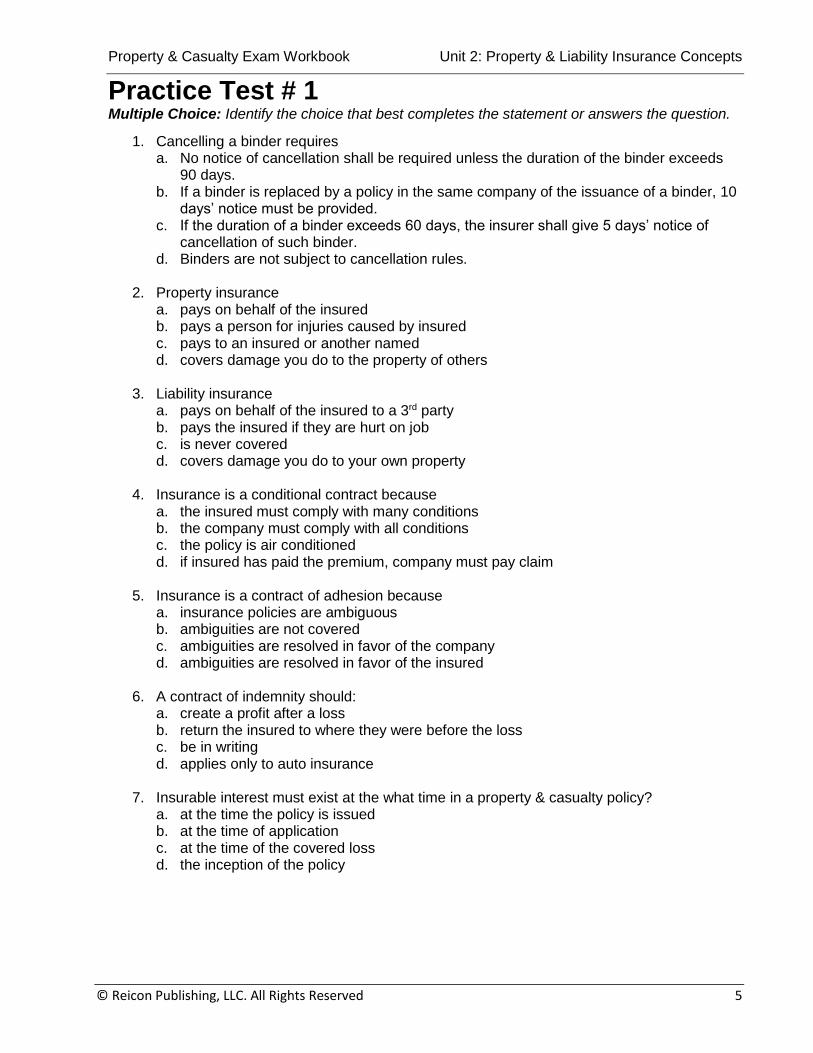

Practice Test # 1 Multiple Choice: Identify the choice that best completes the statement or answers the question.

1. Cancelling a binder requires a. No notice of cancellation shall be required unless the duration of the binder exceeds

90 days. b. If a binder is replaced by a policy in the same company of the issuance of a binder, 10

days’ notice must be provided. c. If the duration of a binder exceeds 60 days, the insurer shall give 5 days’ notice of

cancellation of such binder. d. Binders are not subject to cancellation rules.

2. Property insurance

a. pays on behalf of the insured b. pays a person for injuries caused by insured c. pays to an insured or another named d. covers damage you do to the property of others

3. Liability insurance a. pays on behalf of the insured to a 3rd party b. pays the insured if they are hurt on job c. is never covered d. covers damage you do to your own property

4. Insurance is a conditional contract because a. the insured must comply with many conditions b. the company must comply with all conditions c. the policy is air conditioned d. if insured has paid the premium, company must pay claim

5. Insurance is a contract of adhesion because a. insurance policies are ambiguous b. ambiguities are not covered c. ambiguities are resolved in favor of the company d. ambiguities are resolved in favor of the insured

6. A contract of indemnity should: a. create a profit after a loss b. return the insured to where they were before the loss c. be in writing d. applies only to auto insurance

7. Insurable interest must exist at the what time in a property & casualty policy?

a. at the time the policy is issued b. at the time of application c. at the time of the covered loss d. the inception of the policy

Unit 2: Property & Liability Insurance Concepts Property & Casualty Exam Workbook

6 © Reicon Publishing, LLC. All Rights Reserved.

8. Which of the following is not a peril?

a. fire b. oily rags c. windstorm d. explosion

9. All the following are hazards except: a. grease fire b. oily rags c. loose carpeting d. too many electrical plugs in one outlet

10. A fire ensues with resultant smoke and water damage, the proximate cause would be the a. smoke damage b. water damage c. fire

11. Which of the following is an example of a direct loss? a. A taxi company loses money after their cab is damaged b. Renting a car when yours is damaged in an accident c. Not being able to get into a store caused by an overturned vehicle in front of the store d. Fire damage to tangible property

12. An example of an indirect loss would be a. A taxi company loses money after their cab is damaged b. hurricane damage to an insured building c. aircraft crashes into house damaging furniture d. collision damages to an insured auto

13. Actual cash value “ACV” is defined as a. full replacement cost b. cost to replace with like kind and quality c. purchase price less depreciation d. today’s replacement cost less depreciation

14. The Florida valued policy law applies to a. total loss to personal property b. total loss to a building or structure c. partial loss to a building or structure d. requires company pay full value for jewelry covered

15. The Florida valued policy law requires

a. the insured must pay the full cost to replace property b. the insurer must pay policy limit for total losses to buildings, mobile homes, structures

and manufactured housing units c. the insurer must pay 80% of the amount insured d. nothing, does not apply in Florida

16. Coinsurance penalizes the insured who a. carries less than the required minimum amount of coverage b. carries more than the required amount of coverage c. carries only liability insurance d. carries the minimum amount of coverage required

Property & Casualty Exam Workbook Unit 2: Property & Liability Insurance Concepts

© Reicon Publishing, LLC. All Rights Reserved 7

17. A percentage deductible is

a. a percentage of the value of the property b. a percentage of the amount of loss c. a flat deductible regardless of loss amount d. does not apply to insurance policies

18. A franchise deductible a. pays loss in full if loss amount is below deductible b. pays loss less amount of deductible c. requires a percentage of value for windstorm in Florida d. pays loss in full if loss amount exceeds deductible

19. The date a policy begins is called the a. start date b. date of policy beginning c. inception date d. expiration date

20. The date a policy ends is called the a. end date b. date of policy ending c. inception date d. expiration date

21. The liberalization clause applies a. to the forms costing less than $10 b. to form revisions that broaden coverage at no cost c. to form revisions that restrict coverage at no cost d. to both B & C above

22. The severability clause a. denies coverage to all insureds if one insured is excluded b. denies coverage to insureds if an exclusion applies but covers any other insured not

excluded c. requires company to sever relations with a client who has had too many claims d. is a severe warning not to lie on an application

23. An insurance company can deny a claim for the following a. not telling about flood claim on a homeowners’ policy not revealing that applicant had

escaped from jail while held on arson charges b. honestly completing an application for insurance c. any reason it wishes with 60 days written notice d. the insured provided an accurate claims history to the agent.

24. A company may deny a claim for any of the following reasons a. it is fraudulent b. it is material c. if the company had known they would have not issued the policy or charged a higher

premium d. all the above

Unit 2: Property & Liability Insurance Concepts Property & Casualty Exam Workbook

8 © Reicon Publishing, LLC. All Rights Reserved.

Practice Test # 1 (Answer)

1. C

2. C

3. A

4. A

5. D

6. B

7. C

8. B

9. A

10. C

11. D

12. A

13. D

14. B

15. B

16. A

17. A

18. D

19. C

20. D

21. B

22. B

23. A

24. D

Property & Casualty Exam Workbook Unit 2: Property & Liability Insurance Concepts

© Reicon Publishing, LLC. All Rights Reserved 9

Practice Test # 2 Provide a statement that best answers the question.

1. How does the state of Florida define an insurance policy?

2. What is insurance?

3. Assume an applicant for insurance requests coverage, and the property and liability insurance agent orally accept the offer. Is this oral acceptance just as legally binding on the insurer as a written acceptance? Explain why or why not.

4. How many days prior notice must the insurance company give of cancellation of an auto insurance binder?

5. Property insurance and liability insurance can be differentiated with regard to or for whom an insurance claim is paid. Explain.

Unit 2: Property & Liability Insurance Concepts Property & Casualty Exam Workbook

10 © Reicon Publishing, LLC. All Rights Reserved.

6. Insurance contracts have several common characteristics. Identify the common characteristic that applies to:

a. The insurance contract, which is prepared by the insurer, is either accepted or rejected by the applicant, and, although endorsements or riders may be added to modify the contract's terms, the applicant has little control over them.

b. Insurance contracts do not cover property or operations, although we may say we have, "insured our car", "insured our home", or "insured our business."

c. Insurance contracts are interpreted and enforced with the objective of reimbursement for loss -conferring a benefit that is not greater in value than the loss that is suffered.

d. If an insured fails to perform according to the contract's conditions as agreed to, generally the insurer may refuse to pay a claim.

7. In property insurance, when must an insurable interest exist: when the policy is issued; at the time of loss; or both when the policy is issued and at the time of a loss covered by the policy?

8. Insurance is purchased to offset risk of a peril occurring, which results from a hazard exposing

a person to loss. Identify each of the following as a peril, physical hazard, moral hazard or morale hazard: a. Use of drugs - b. Driver who has several drinks during the evening, but refuses to admit he or she is

intoxicated and drives home. -

c. Fire breaks out in a home - d. Defective steering mechanism on an auto - e. Dishonest business practices - f. Legal liability - g. Because the insured is covered by a theft policy, there is no conscious concern about

large sums of money being left on a counter where customers could steal them. -

Property & Casualty Exam Workbook Unit 2: Property & Liability Insurance Concepts

© Reicon Publishing, LLC. All Rights Reserved 11

9. Assume A, with the insurer's knowledge, leases the insured building to B, an accountant. The

building is larger than B needs, so B subsequently sublets the upper floor to C, who uses it for the business of baking goods for sale to restaurants. If a loss from a peril insured against occurs, why will the loss likely not be covered?

10. When a covered peril occurs and an insured suffers a loss to the insured property, that loss

may, be direct, indirect, or both. Explain what is meant by: a. Direct loss.

b. Indirect loss.

11. How much could the insured collect under each of the following deductibles? a. $50 straight deductible; amount of loss is $150. _______________ b. $50 straight deductible; amount of loss is $50. _______________ c. $500 franchise deductible; amount of loss is $250. _______________ d. $500 franchise deductible; amount of loss is $1,000 _______________

12. In Florida, the term "actual cash value" (ACV) may be considered to mean a property item's reasonable, fair cash, or fair market value. However, what is the generally understood meaning of ACV?

13. Buildings are usually (and personal property sometimes) insured under replacement cost

coverage. a. What is a “replacement cost valuation” policy?

b. What major requirement does such a policy contain as a primary safeguard?

c. Does the same safeguard apply to losses settled under ACV?

Unit 2: Property & Liability Insurance Concepts Property & Casualty Exam Workbook

12 © Reicon Publishing, LLC. All Rights Reserved.

14. Besides replacement cost valuation, there are other factors which result in a departure from

the strict application of the principle of indemnity. It is often difficult to establish the ACV or replacement value of antiques or fine arts, for example, so such items may be insured under a valued policy issued by the insurer under its own terms. How does the valued policy loss settlement differ from the ACV loss settlement?

15. Determine the amount of settlement in each of the following situations.

a. An insured has $60,000 insurance coverage on a building that is valued at $90,000. An

80% coinsurance clause applies. A $24,000 loss occurs. _______________

b. An insured has $60,000 insurance coverage on a building that is valued at $70,000. An 80% coinsurance clause applies. A $30,000 loss occurs. _______________

16. Identify each of the following statements pertaining to legal liability and liability insurance as "true” or "false."

a. True False The purpose of standard liability policies is to indemnify insureds for injury or damage they have suffered.

b. True False Liability policies pay whether or not the insured is legally liable for injury or damage.

c. True False It is not generally necessary for a lawsuit to be filed and followed to conclusion to establish liability and set damages.

17. Is the legal representative of the insured generally covered by the insured's liability policy while acting within the scope of his or her duties?

18. Property and liability policies require the insured to give prompt notice, cooperate with the

insurer and act in a way to preserve the insurer's rights. More specifically:

a. What is required of the insured under liability policies?

b. What is required of the insured under property policies?

Property & Casualty Exam Workbook Unit 2: Property & Liability Insurance Concepts

© Reicon Publishing, LLC. All Rights Reserved 13

19. Regarding subrogation:

a. When and to what extent is an insurer subrogated to the insured's right of action against a third party responsible for the loss?

b. Why should an insured be concerned with subrogation?

c. What are the basic purposes for the subrogation clause found in many kinds of insurance policies?

20. With respect to the "other insurance" condition, explain the terms:

a. Pro rata

b. Primary

c. Excess

d. Equal shares

21. The liberalization condition, found in many standard policies, applies to all the following, EXCEPT: a. Policy revisions adopted by the insurer b. Policy revisions that broaden coverage. c. Policy revisions for which additional premium is due. d. Policy revisions within a specified time prior to the policy period or during it.

Unit 2: Property & Liability Insurance Concepts Property & Casualty Exam Workbook

14 © Reicon Publishing, LLC. All Rights Reserved.

22. What is the purpose of?

a. the appraisal condition common to most property contracts?

b. the appraisal process?

23. What is meant by the term “abandonment” in property insurance? 24. What three things must be true for misrepresentation or concealment to prevent recovery

under a policy?

Property & Casualty Exam Workbook Unit 2: Property & Liability Insurance Concepts

© Reicon Publishing, LLC. All Rights Reserved 15

Practice Test # 2 (Answers)

1. An insurance policy is a written contract or agreement for insurance which includes all clauses, riders, endorsements and papers that are a part of the agreement.

2. An insurance policy is a contract whereby one party (the insurance company) agrees to indemnify another party (the insured) or to allow a specific amount or a determinable benefit upon occurrence of certain contingencies.

3. Yes. Under Florida statues, binders or other contracts for temporary marine, casualty or surety insurance may be made orally or in writing. They are deemed to include all the usual terms of the policy for which the binder was given, along with any applicable endorsements designated in the binder, except as superseded by the express terms of the binder.

4. Five days, unless it is replaced by a policy or another binder.

5. Property insurance is insurance wherein the insurance company makes payment directly

to the insured or other specifically named interest. Liability insurance means payment will be on behalf of the insured to another, based upon the insured’s liability to the recipient.

6. a. Contract of Adhesion b. Personal Contract c. Indemnity Contract (or Principle of Indemnity) d. Conditional Contract

7. At the time of loss 8. a. Moral hazard

b. Morale hazard c. Peril d. Physical hazard e. Moral hazard f. Peril g. Morale hazard

9. Because subletting the upper floor to B for such purposes constitutes a material increase

of hazard, which can suspend coverage. 10. a. Damage sustained immediately to tangible property, thereby causing need for its

repair or replacement.

b. Loss which results as a consequence of direct loss, such as loss of profits from loss of use of premises.

11. a. $100 ($150 loss - $50 deductible)

b. $0 ($50 loss - $50 deductible) c. $0 (No payment made until loss equals or exceeds $500) d. $1,000 (Pays loss in full when it equals or exceeds $500)

Unit 2: Property & Liability Insurance Concepts Property & Casualty Exam Workbook

16 © Reicon Publishing LLC. All Rights Reserved.

12. Current cost to replace the item, less allowance for depreciation. 13.

a. The insurer agrees to settle the loss based on current replacement cost of the property, without deduction for depreciation.

b. The requirement that replacement actually take place. c. No; the insured is entitled to the ACV of the loss, whether or not replacement takes

place.

14. Under a valued policy, the insurer agrees in advance (rather than at the time of loss) as to the value of an insured item, and agrees to pay the face amount of the policy in the event of total loss.

15.

a. $20,000 loss settlement. ($24,000 loss x $60,000 insurance $72,000 [$90,000 x 80%])

b. $30,000 (The property is insured for more than the coinsurance amount [$70,000 value x 80% = $56,000])

16.

a. False. They do not indemnify insureds; they pay based on legal liability. b. False. The insuring agreement states that the insurer agrees "to pay on behalf of

the insured all sums the insured becomes legally obligated to pay as damages ... " c. True

17. Yes

18.

a. Notify the insurer of names and addresses of claimants and witnesses to an accident, promptly forward all legal papers received, aid the insurer in settlements, and avoid voluntary payments or assumptions of obligations.

b. Inventory the damaged property, use reasonable means in protecting against further loss, show the damaged property, provide records and documents, submit to questions under oath, report thefts to the police, reveal any other insurance which exists, and submit a proof of loss within a given period after the loss occurs.

19. a. The insurer is subrogated to the insured's legal rights only after it makes payment

to the insured for the loss, and only to the extent of the amount paid. b. If the insured, without consent of the insurer, settles with the third party involved,

thereby cutting off the insurer's subrogation rights, the insurer has no legal obligation to pay.

c. It prevents the insured from collecting twice and places ultimate responsibility for payment on the party primarily liable to the insured.

20.

a. The insurer will pay the proportion which its limit bears to total of all limits. b. The policy applies first, up to its limit, before others apply. c. All other insurance must be exhausted before the policy will apply. d. Contribution based on the number of policies, without regard to their limits.

Unit 2: Property & Liability Insurance Concepts Property & Casualty Exam Workbook

© Reicon Publishing LLC. All Rights Reserved. 17

21. “C” The liberalization condition applies only to such policy revisions that broaden coverage without additional premiums.

22. a. To avoid the time, inconvenience and expense involved in litigation. b. To resolve differences between the insurer and insured about the amount of loss.

23. The procedure whereby an insured may seek to turn over damaged property to the insurer

and claim full payment of the value of the property at the time of loss.

24. Statements and descriptions are fraudulent; they are material either to the acceptance of the risk or to the hazard assumed by the insurer; or the insurer in good faith would either not have issued the policy, would not have issued it at the same premium rate or in as large amount, or would not have covered the hazard resulting in the loss, if the true facts had been known.

Property & Casualty Exam Workbook Unit 2: Property & Liability Insurance Concepts

18 © Reicon Publishing LLC. All Rights Reserved.

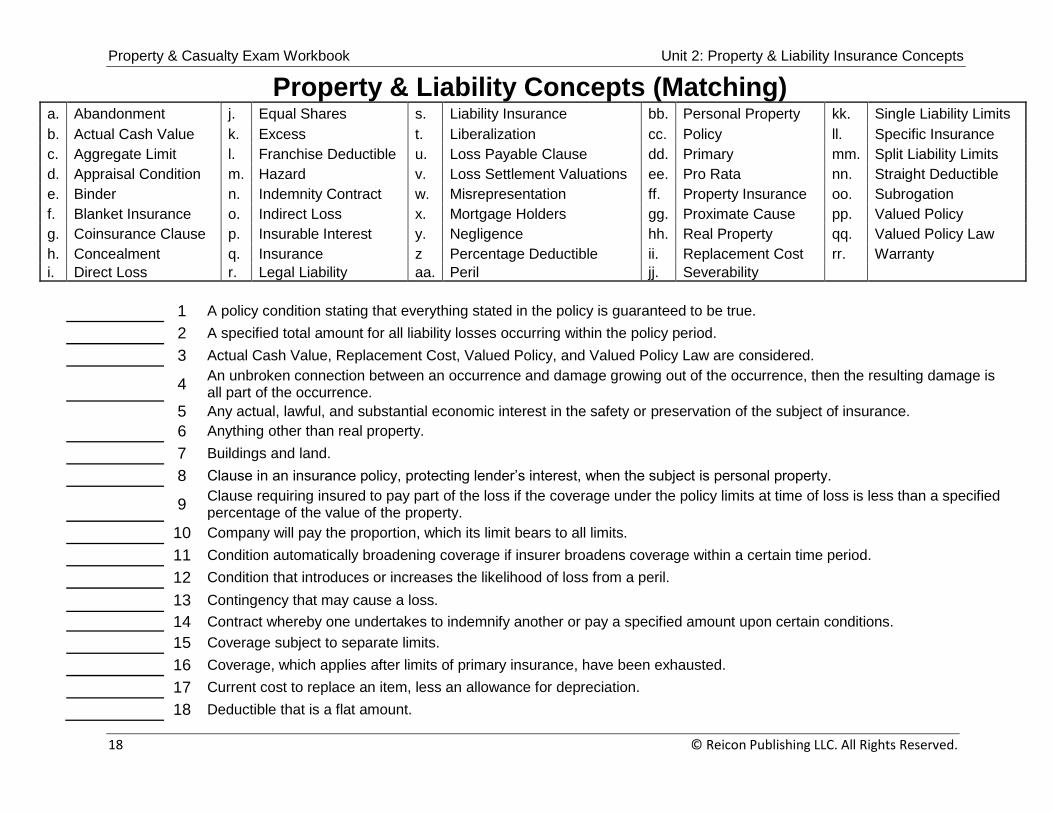

Property & Liability Concepts (Matching) a. Abandonment j. Equal Shares s. Liability Insurance bb. Personal Property kk. Single Liability Limits

b. Actual Cash Value k. Excess t. Liberalization cc. Policy ll. Specific Insurance

c. Aggregate Limit l. Franchise Deductible u. Loss Payable Clause dd. Primary mm. Split Liability Limits

d. Appraisal Condition m. Hazard v. Loss Settlement Valuations ee. Pro Rata nn. Straight Deductible

e. Binder n. Indemnity Contract w. Misrepresentation ff. Property Insurance oo. Subrogation

f. Blanket Insurance o. Indirect Loss x. Mortgage Holders gg. Proximate Cause pp. Valued Policy

g. Coinsurance Clause p. Insurable Interest y. Negligence hh. Real Property qq. Valued Policy Law

h. Concealment q. Insurance z Percentage Deductible ii. Replacement Cost rr. Warranty

i. Direct Loss r. Legal Liability aa. Peril jj. Severability

1 A policy condition stating that everything stated in the policy is guaranteed to be true.

2 A specified total amount for all liability losses occurring within the policy period.

3 Actual Cash Value, Replacement Cost, Valued Policy, and Valued Policy Law are considered.

4 An unbroken connection between an occurrence and damage growing out of the occurrence, then the resulting damage is all part of the occurrence.

5 Any actual, lawful, and substantial economic interest in the safety or preservation of the subject of insurance.

6 Anything other than real property.

7 Buildings and land.

8 Clause in an insurance policy, protecting lender’s interest, when the subject is personal property.

9 Clause requiring insured to pay part of the loss if the coverage under the policy limits at time of loss is less than a specified percentage of the value of the property.

10 Company will pay the proportion, which its limit bears to all limits.

11 Condition automatically broadening coverage if insurer broadens coverage within a certain time period.

12 Condition that introduces or increases the likelihood of loss from a peril.

13 Contingency that may cause a loss. 14 Contract whereby one undertakes to indemnify another or pay a specified amount upon certain conditions.

15 Coverage subject to separate limits.

16 Coverage, which applies after limits of primary insurance, have been exhausted.

17 Current cost to replace an item, less an allowance for depreciation.

18 Deductible that is a flat amount.

Property & Casualty Exam Workbook Unit 2: Property & Liability Insurance Concepts

© Reicon Publishing LLC. All Rights Reserved. 19

19 Deductions from the loss of a percentage of the value of the property.

20 Economic loss, which flows as a consequence of, direct loss.

21 Failure of insured to reveal relevant facts.

22 Failure to exercise that degree of care that the law requires to protect others from an unreasonable risk of harm.

23 Insurance applies separately to each insured.

24 Insurance paid to insured.

25 Insurance paid to others on insured’s behalf.

26 Insured cannot dump damaged property on insurer and demand full value.

27 Insurer agrees that coverage limit on item will be considered its value.

28 Maximum liability of insurer expressed by two figures.

29 No payments made unless the loss equals or exceeds prescribed amount, then loss paid in full.

30 One should not profit from the response provided by the policy.

31 Physical harm to tangible property.

32 Policy applies first up to its limit.

33 Provision in a property insurance policy covering real property, which protects the lender’s interest.

34 Rules of law dictate that a person must pay for damages done to another.

35 Settlement in which the condition of replacement must actually be met.

36 Single amount is the maximum liability of insurer with respect to any one accident or occurrence.

37 Single amount of insurance applies to two or more coverage items.

38 Temporary insurance.

39 The transfer to the insurance company of the insured’s rights to collect for damages.

40 Total loss by insured peril to a building, structure, mobile home or manufactured housing unit, the insurer must pay amount provided in policy for which premium has been paid.

41 Untrue statement made by insured. 42 Used when insured and insurer are in disagreement regarding amount of loss.

43 When other insurance is involved, the loss payment is based on the number of policies not their limits.

44 Written contract or agreement effecting insurance, including, clauses, riders, endorsements and papers.

Property & Casualty Exam Workbook Unit 2: Property & Liability Insurance Concepts

20 © Reicon Publishing LLC. All Rights Reserved.

Property & Liability Concepts Answers (Matching)

1. rr 2. c 3. v 4. gg 5. p 6. bb 7. hh 8. u 9. g 10. ee 11. t 12. m 13. aa 14. q 15. ll 16. k 17. b 18. nn 19. z 20. o 21. h 22. y

23. jj 24. ff 25. s 26. a 27. pp 28. mm 29. l 30. n 31. i 32. dd 33. x 34. r 35. ii 36. kk 37. f 38. e 39. oo 40. qq 41. w 42. d 43. j 44. cc

Property & Casualty Exam Workbook Unit 3: Personal Automobile

© Reicon Publishing LLC. All Rights Reserved.

21

UNIT

PERSONAL AUTOMOBILE

OVERVIEW

This section reviews the different forms of automobile policies used to provide

coverage to individuals and businesses. Automobile insurance is generally regarded as

the most important of the property and liability insurance lines. Exposures to loss exist

for virtually every individual, family, and business. The requirements of Florida law and

economic realities make auto insurance a primary necessity. While there are numerous

independently developed policy forms, this review deals with the standard provisions

contracts promulgated by Insurance Services Office, Inc.

OBJECTIVES

After completing this chapter, you should be able to understand:

• Financial Responsibility

• No-Fault

• Personal Auto Policy

• PAP Declarations

• PAP Definitions

• Part A – Liability Coverage

• Part B – Medical Payments

• Part C – Uninsured Motorist Coverage

• Part D – Coverage for Damage to Your Auto

• Part E & F – Other Provisions

• Endorsements

• Rating

• Miscellaneous Florida Automobile Laws

• Mechanical Breakdown Insurance

Property & Casualty Exam Workbook Unit 3: Personal Automobile

22 © Reicon Publishing LLC. All Rights Reserved.

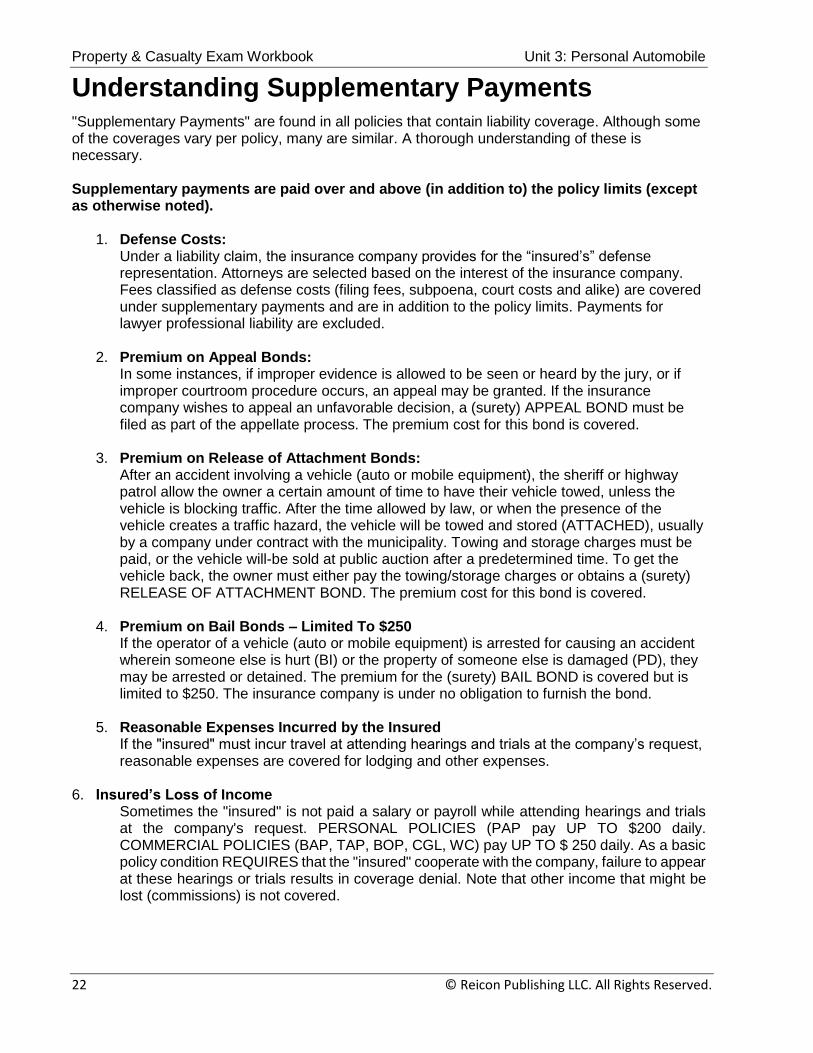

Understanding Supplementary Payments "Supplementary Payments" are found in all policies that contain liability coverage. Although some of the coverages vary per policy, many are similar. A thorough understanding of these is necessary. Supplementary payments are paid over and above (in addition to) the policy limits (except as otherwise noted).

1. Defense Costs: Under a liability claim, the insurance company provides for the “insured’s” defense representation. Attorneys are selected based on the interest of the insurance company. Fees classified as defense costs (filing fees, subpoena, court costs and alike) are covered under supplementary payments and are in addition to the policy limits. Payments for lawyer professional liability are excluded.

2. Premium on Appeal Bonds:

In some instances, if improper evidence is allowed to be seen or heard by the jury, or if improper courtroom procedure occurs, an appeal may be granted. If the insurance company wishes to appeal an unfavorable decision, a (surety) APPEAL BOND must be filed as part of the appellate process. The premium cost for this bond is covered.

3. Premium on Release of Attachment Bonds: After an accident involving a vehicle (auto or mobile equipment), the sheriff or highway patrol allow the owner a certain amount of time to have their vehicle towed, unless the vehicle is blocking traffic. After the time allowed by law, or when the presence of the vehicle creates a traffic hazard, the vehicle will be towed and stored (ATTACHED), usually by a company under contract with the municipality. Towing and storage charges must be paid, or the vehicle will-be sold at public auction after a predetermined time. To get the vehicle back, the owner must either pay the towing/storage charges or obtains a (surety) RELEASE OF ATTACHMENT BOND. The premium cost for this bond is covered.

4. Premium on Bail Bonds – Limited To $250 If the operator of a vehicle (auto or mobile equipment) is arrested for causing an accident wherein someone else is hurt (BI) or the property of someone else is damaged (PD), they may be arrested or detained. The premium for the (surety) BAIL BOND is covered but is limited to $250. The insurance company is under no obligation to furnish the bond.

5. Reasonable Expenses Incurred by the Insured If the "insured" must incur travel at attending hearings and trials at the company’s request, reasonable expenses are covered for lodging and other expenses.

6. Insured’s Loss of Income Sometimes the "insured" is not paid a salary or payroll while attending hearings and trials at the company's request. PERSONAL POLICIES (PAP pay UP TO $200 daily. COMMERCIAL POLICIES (BAP, TAP, BOP, CGL, WC) pay UP TO $ 250 daily. As a basic policy condition REQUIRES that the "insured" cooperate with the company, failure to appear at these hearings or trials results in coverage denial. Note that other income that might be lost (commissions) is not covered.

Property & Casualty Exam Workbook Unit 3: Personal Automobile

© Reicon Publishing LLC. All Rights Reserved.

23

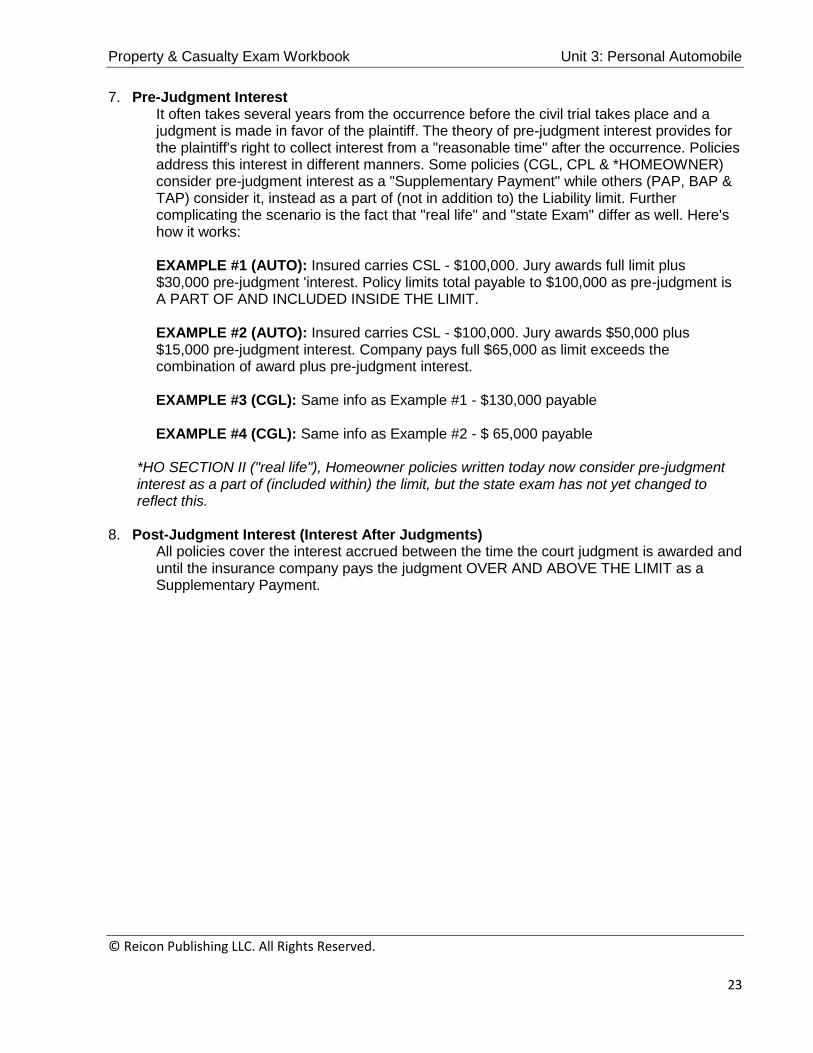

7. Pre-Judgment Interest

It often takes several years from the occurrence before the civil trial takes place and a judgment is made in favor of the plaintiff. The theory of pre-judgment interest provides for the plaintiff's right to collect interest from a "reasonable time" after the occurrence. Policies address this interest in different manners. Some policies (CGL, CPL & *HOMEOWNER) consider pre-judgment interest as a "Supplementary Payment" while others (PAP, BAP & TAP) consider it, instead as a part of (not in addition to) the Liability limit. Further complicating the scenario is the fact that "real life" and "state Exam" differ as well. Here's how it works: EXAMPLE #1 (AUTO): Insured carries CSL - $100,000. Jury awards full limit plus $30,000 pre-judgment 'interest. Policy limits total payable to $100,000 as pre-judgment is A PART OF AND INCLUDED INSIDE THE LIMIT. EXAMPLE #2 (AUTO): Insured carries CSL - $100,000. Jury awards $50,000 plus $15,000 pre-judgment interest. Company pays full $65,000 as limit exceeds the combination of award plus pre-judgment interest. EXAMPLE #3 (CGL): Same info as Example #1 - $130,000 payable EXAMPLE #4 (CGL): Same info as Example #2 - $ 65,000 payable

*HO SECTION II ("real life"), Homeowner policies written today now consider pre-judgment interest as a part of (included within) the limit, but the state exam has not yet changed to reflect this.

8. Post-Judgment Interest (Interest After Judgments) All policies cover the interest accrued between the time the court judgment is awarded and until the insurance company pays the judgment OVER AND ABOVE THE LIMIT as a Supplementary Payment.

Unit 3: Personal Automobile Property & Casualty Exam Workbook

24 © Reicon Publishing LLC. All Rights Reserved.

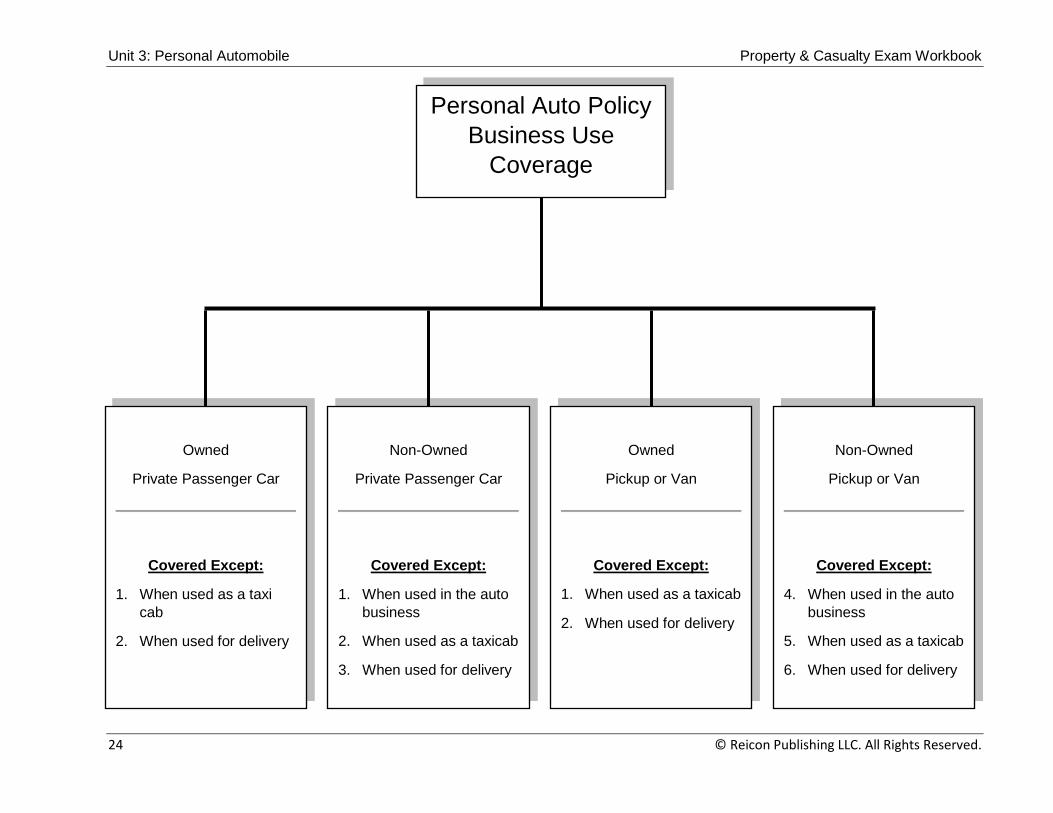

Personal Auto Policy

Business Use

Coverage

Owned

Private Passenger Car

Covered Except:

1. When used as a taxi

cab

2. When used for delivery

Non-Owned

Private Passenger Car

Covered Except:

1. When used in the auto

business

2. When used as a taxicab

3. When used for delivery

Owned

Pickup or Van

Covered Except:

1. When used as a taxicab

2. When used for delivery

Non-Owned

Pickup or Van

Covered Except:

4. When used in the auto

business

5. When used as a taxicab

6. When used for delivery

Property & Casualty Exam Workbook Unit 3: Personal Automobile

© Reicon Publishing LLC. All Rights Reserved. Page 25

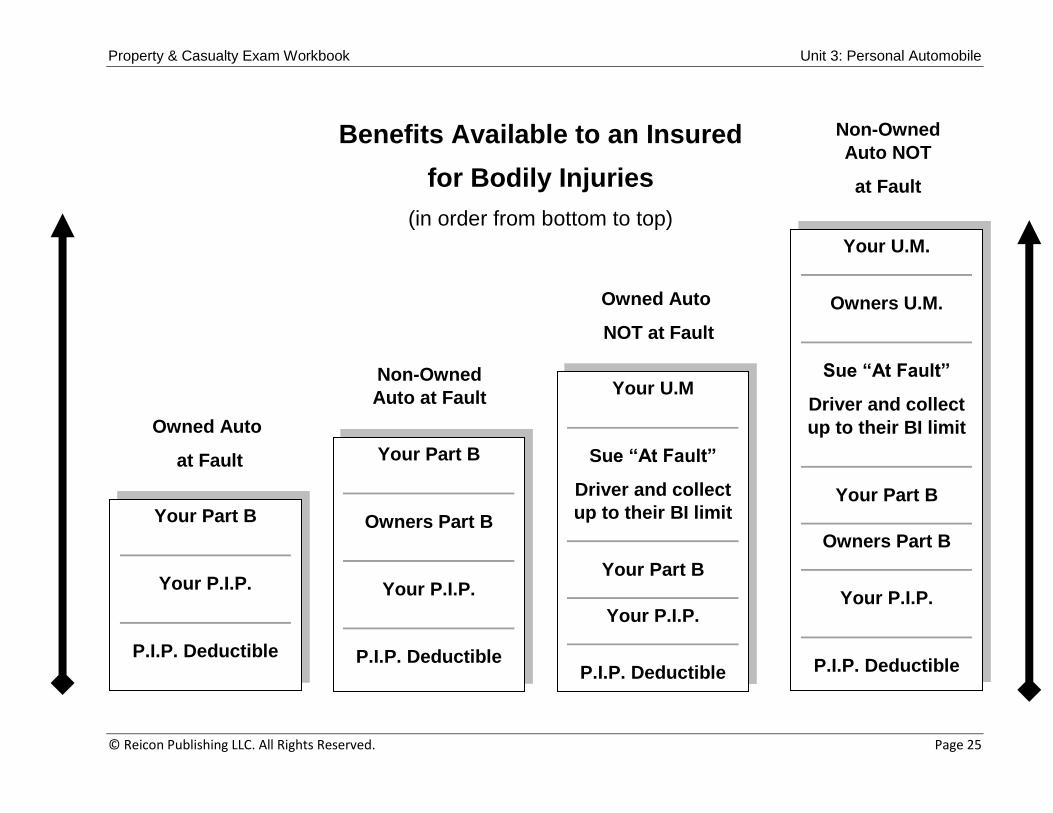

Owned Auto

at Fault

Non-Owned

Auto at Fault

Non-Owned

Auto NOT

at Fault

Owned Auto

NOT at Fault

Your Part B

Your P.I.P.

P.I.P. Deductible

Your Part B

Owners Part B

Your P.I.P.

P.I.P. Deductible

Your U.M

Sue “At Fault”

Driver and collect

up to their BI limit

Your Part B

Your P.I.P.

P.I.P. Deductible

Your U.M.

Owners U.M.

Sue “At Fault”

Driver and collect

up to their BI limit

Your Part B

Owners Part B

Your P.I.P.

P.I.P. Deductible

Benefits Available to an Insured

for Bodily Injuries

(in order from bottom to top)

Unit 3: Personal Automobile Property & Casualty Exam Workbook

26 © Reicon Publishing LLC. All Rights Reserved.

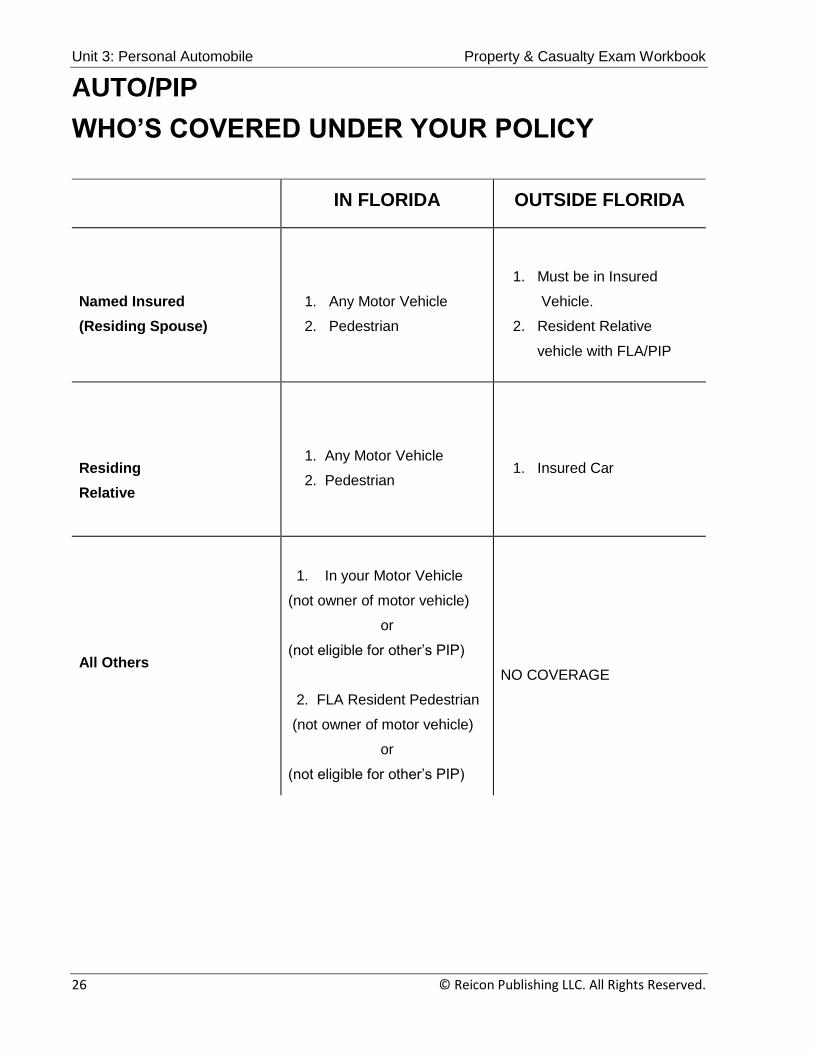

AUTO/PIP

WHO’S COVERED UNDER YOUR POLICY

IN FLORIDA OUTSIDE FLORIDA

Named Insured

(Residing Spouse)

1. Any Motor Vehicle

2. Pedestrian

1. Must be in Insured

Vehicle.

2. Resident Relative

vehicle with FLA/PIP

Residing

Relative

1. Any Motor Vehicle

2. Pedestrian

1. Insured Car

All Others

1. In your Motor Vehicle

(not owner of motor vehicle)

or

(not eligible for other’s PIP)

2. FLA Resident Pedestrian

(not owner of motor vehicle)

or

(not eligible for other’s PIP)

NO COVERAGE

Property & Casualty Exam Workbook Unit 3: Personal Automobile

© Reicon Publishing LLC. All Rights Reserved. 27

Personal Auto Policy (PAP)

Present Coverages on Declarations

Replacement Vehicle for VEH #1 & 2 on

Declarations

Replacement VEH Time Limit on

Coverage

Additional VEH /

(Broadest on Policy)

Temporary substitute

(no time limit)

Non-Owned VEH

VEH #1 VEH #2

VEH #1 VEH #2

VEH #1 VEH #2 VEH #3 Time Limit Temp for

#1 Temp for

#2 Non-Owned

BI

PIP

UM

MEDPAY

BI

PIP

UM

BI

PIP

UM

MEDPAY

BI

PIP

UM

Endorse on to Policy

Endorse on to Policy

BI

PIP

UM

MEDPAY

14 Days

BI

PIP

UM

MEDPAY

BI

PIP

UM

BI

PIP

UM

MEDPAY

COLL

OTC

COLL

OTC

COLL

OTC 14 Days 14 Days

COLL

OTC

Only 4 days if

…

No COLL/OTC on any other

vehicle on the policy

COLL

OTC

COLL

OTC

Collision OTC

Property & Casualty Exam Workbook Unit 3: Personal Automobile

28 © Reicon Publishing LLC. All Rights Reserved.

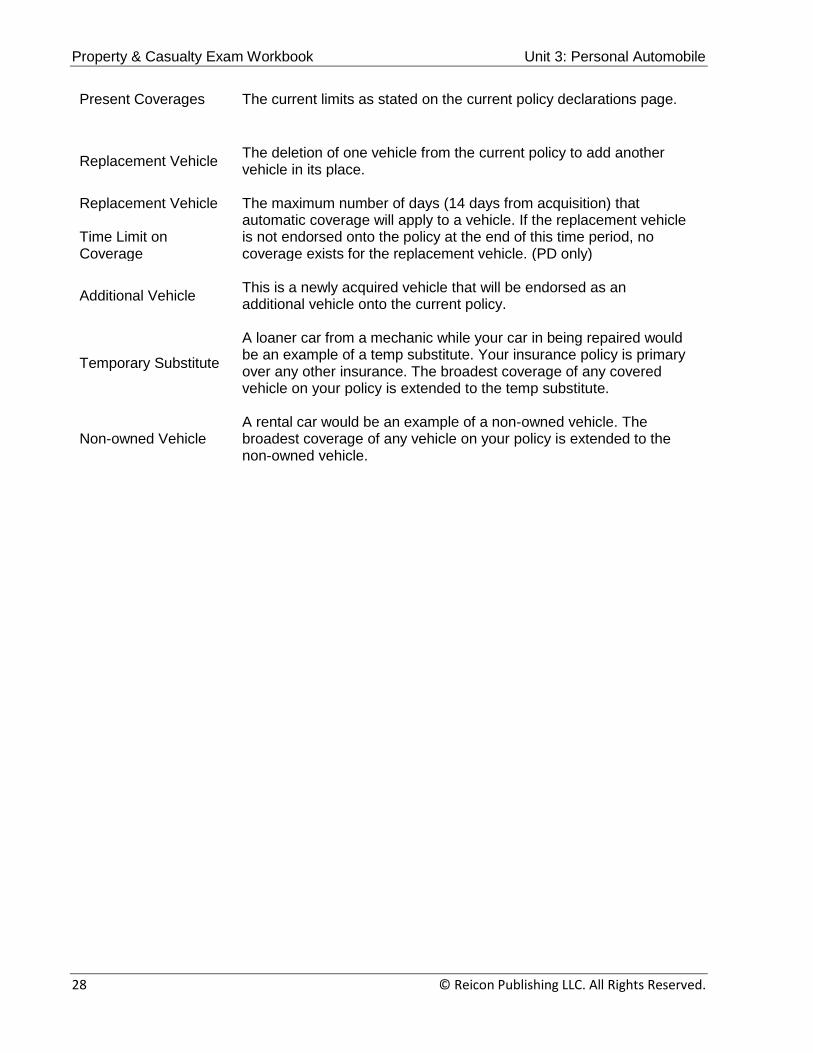

Present Coverages The current limits as stated on the current policy declarations page.

Replacement Vehicle The deletion of one vehicle from the current policy to add another vehicle in its place.

Replacement Vehicle Time Limit on Coverage

The maximum number of days (14 days from acquisition) that automatic coverage will apply to a vehicle. If the replacement vehicle is not endorsed onto the policy at the end of this time period, no coverage exists for the replacement vehicle. (PD only)

Additional Vehicle This is a newly acquired vehicle that will be endorsed as an additional vehicle onto the current policy.

Temporary Substitute

A loaner car from a mechanic while your car in being repaired would be an example of a temp substitute. Your insurance policy is primary over any other insurance. The broadest coverage of any covered vehicle on your policy is extended to the temp substitute.

Non-owned Vehicle A rental car would be an example of a non-owned vehicle. The broadest coverage of any vehicle on your policy is extended to the non-owned vehicle.

Unit 3: Personal Automobile Property & Casualty Exam Workbook

© Reicon Publishing LLC. All Rights Reserved. 29

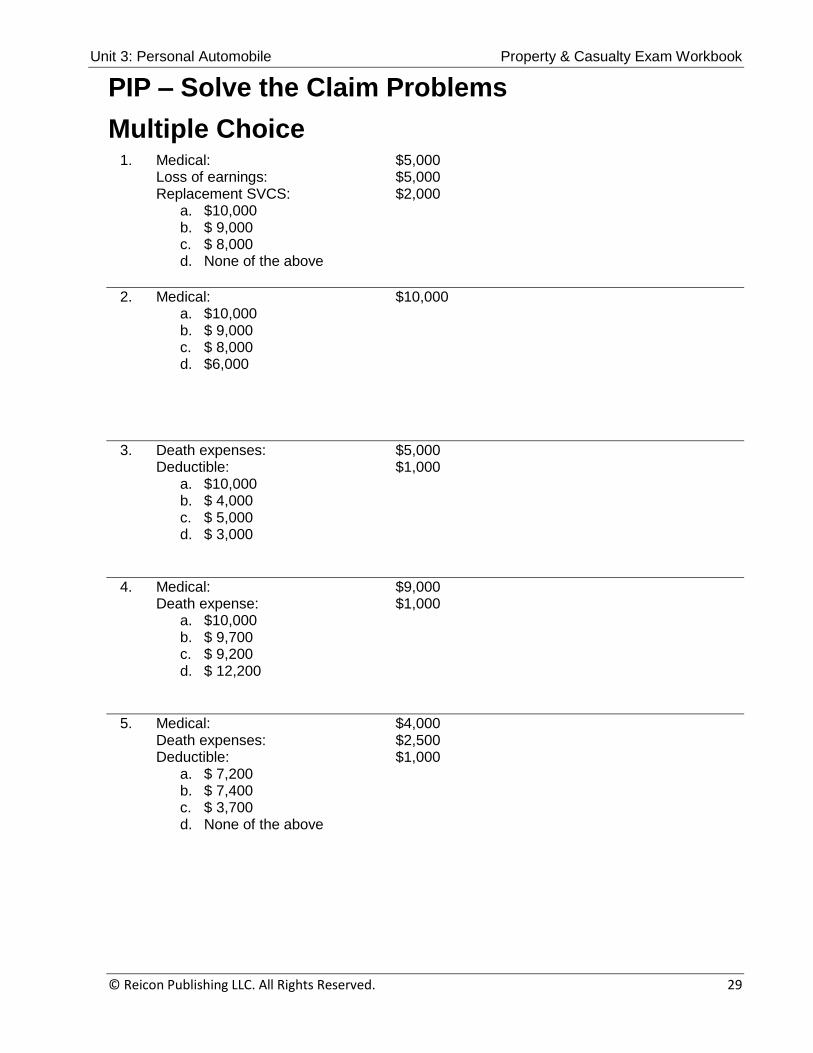

PIP – Solve the Claim Problems

Multiple Choice 1. Medical: $5,000

Loss of earnings: $5,000 Replacement SVCS: $2,000

a. $10,000 b. $ 9,000 c. $ 8,000 d. None of the above

2. Medical: $10,000 a. $10,000 b. $ 9,000 c. $ 8,000 d. $6,000

3. Death expenses: $5,000 Deductible: $1,000

a. $10,000 b. $ 4,000 c. $ 5,000 d. $ 3,000

4. Medical: $9,000 Death expense: $1,000

a. $10,000 b. $ 9,700 c. $ 9,200 d. $ 12,200

5. Medical: $4,000 Death expenses: $2,500 Deductible: $1,000

a. $ 7,200 b. $ 7,400 c. $ 3,700 d. None of the above

Property & Casualty Exam Workbook Unit 3: Personal Automobile

30 © Reicon Publishing LLC. All Rights Reserved.

6. Medical: $2,000 Loss of earnings: $1,000 Deductible: $1,000

a. $ 3,000 b. $ 1,200 c. $ 1,000 d. $ 1,400

7. Medical: $ 5,000 Replacement SVCS: $ 4,500 Deductible: $ 1,000

a. $ 9,500 b. $ 7,500 c. $ 7,700 d. $ 5,200

8. Medical: $12,000 Deductible: $ 1,000

a. $10,000 b. $ 9,000 c. $ 8,800 d. $ 8,600

9. Medical: $ 3,000 Loss of earnings: $15,000

a. $10,000 b. $ 9,000 c. $ 8,000 d. None of the above

10. Medical: $ 1,000 Loss of earnings: $ 3,000 Replacement SVCS: $ 1,000 Death expenses: $ 1,000

a. $10,000 b. $ 8,600 c. $ 6,000 d. None of the above

Unit 3: Personal Automobile Property & Casualty Exam Workbook

© Reicon Publishing LLC. All Rights Reserved. 31

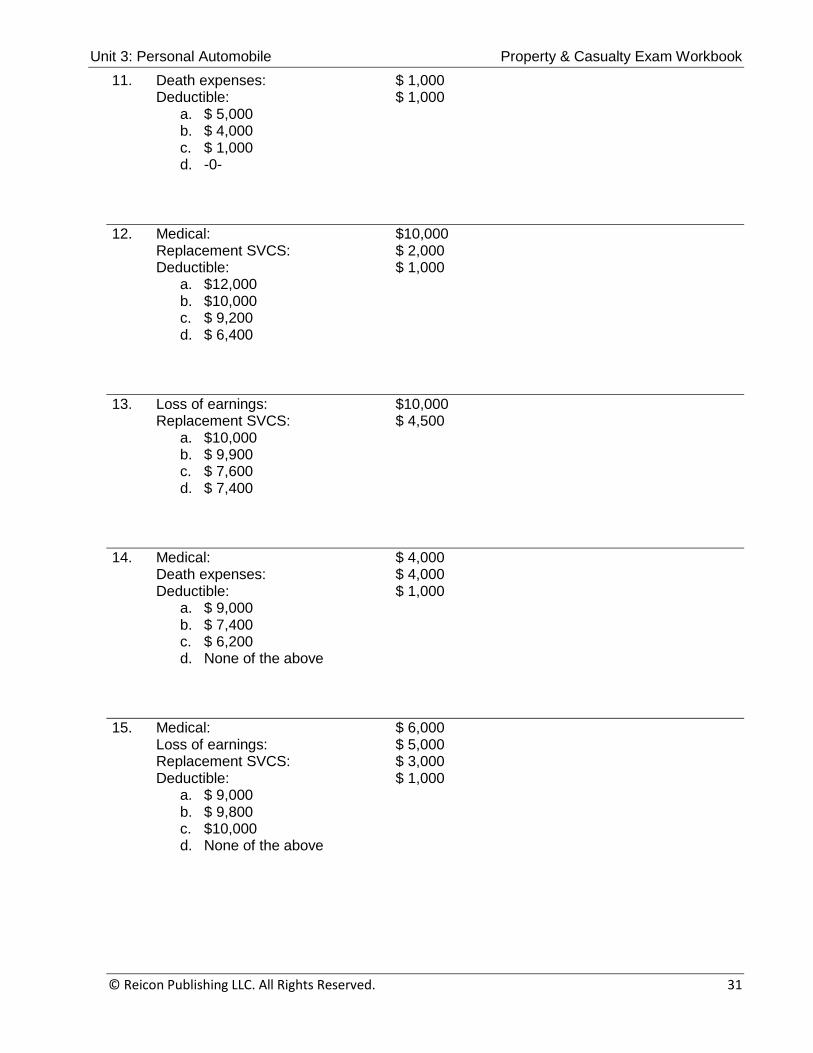

11. Death expenses: $ 1,000 Deductible: $ 1,000

a. $ 5,000 b. $ 4,000 c. $ 1,000 d. -0-

12. Medical: $10,000 Replacement SVCS: $ 2,000 Deductible: $ 1,000

a. $12,000 b. $10,000 c. $ 9,200 d. $ 6,400

13. Loss of earnings: $10,000 Replacement SVCS: $ 4,500

a. $10,000 b. $ 9,900 c. $ 7,600 d. $ 7,400

14. Medical: $ 4,000 Death expenses: $ 4,000 Deductible: $ 1,000

a. $ 9,000 b. $ 7,400 c. $ 6,200 d. None of the above

15. Medical: $ 6,000 Loss of earnings: $ 5,000 Replacement SVCS: $ 3,000 Deductible: $ 1,000

a. $ 9,000 b. $ 9,800 c. $10,000 d. None of the above

Property & Casualty Exam Workbook Unit 3: Personal Automobile

32 © Reicon Publishing LLC. All Rights Reserved.

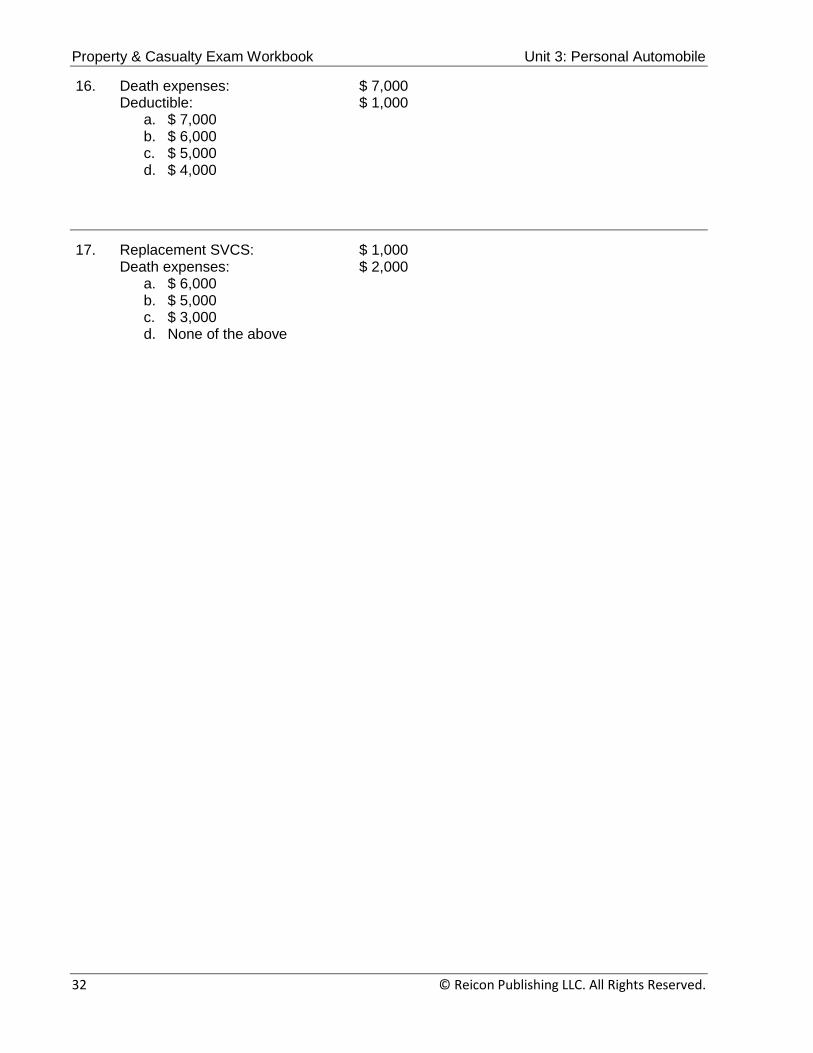

16. Death expenses: $ 7,000 Deductible: $ 1,000

a. $ 7,000 b. $ 6,000 c. $ 5,000 d. $ 4,000

17. Replacement SVCS: $ 1,000 Death expenses: $ 2,000

a. $ 6,000 b. $ 5,000 c. $ 3,000 d. None of the above

Unit 3: Personal Automobile Property & Casualty Exam Workbook

© Reicon Publishing LLC. All Rights Reserved. 33

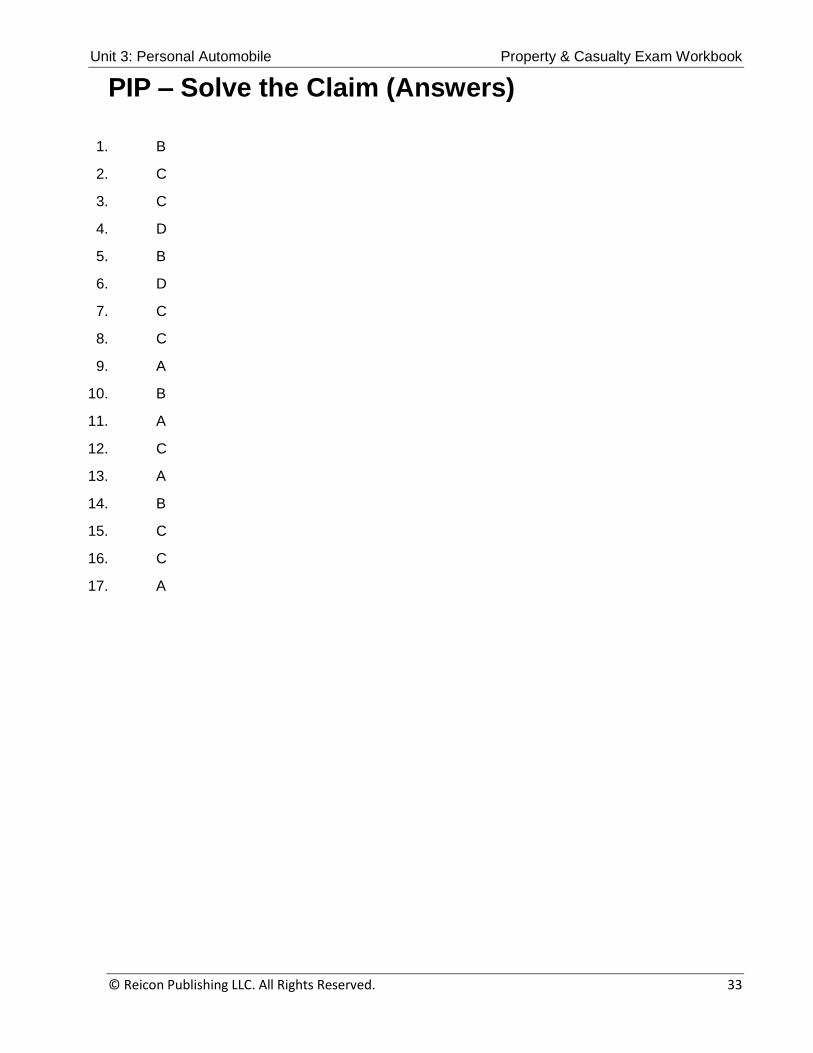

PIP – Solve the Claim (Answers)

1. B

2. C

3. C

4. D

5. B

6. D

7. C

8. C

9. A

10. B

11. A

12. C

13. A

14. B

15. C

16. C

17. A

Property & Casualty Exam Workbook Unit 3: Personal Automobile

34 © Reicon Publishing LLC. All Rights Reserved.

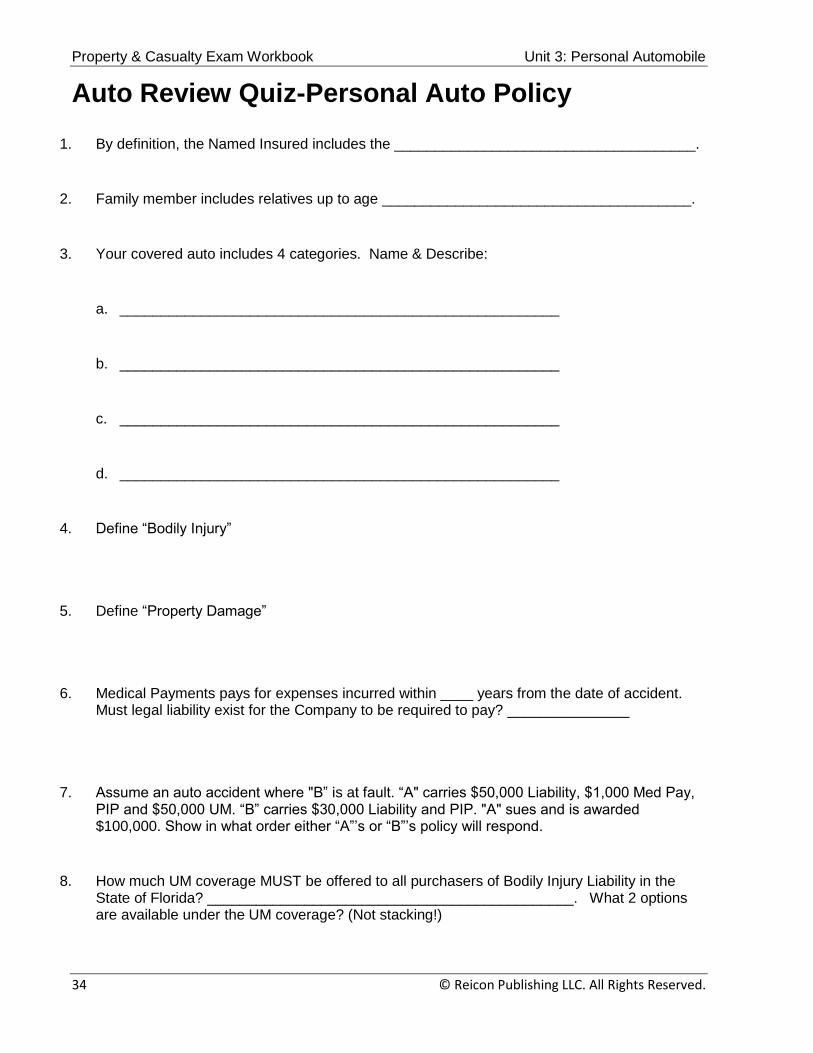

Auto Review Quiz-Personal Auto Policy

1. By definition, the Named Insured includes the _____________________________________.

2. Family member includes relatives up to age ______________________________________.

3. Your covered auto includes 4 categories. Name & Describe:

a. ______________________________________________________

b. ______________________________________________________

c. ______________________________________________________

d. ______________________________________________________

4. Define “Bodily Injury”

5. Define “Property Damage”

6. Medical Payments pays for expenses incurred within ____ years from the date of accident. Must legal liability exist for the Company to be required to pay? _______________

7. Assume an auto accident where "B” is at fault. “A" carries $50,000 Liability, $1,000 Med Pay, PIP and $50,000 UM. “B” carries $30,000 Liability and PIP. "A" sues and is awarded $100,000. Show in what order either “A”’s or “B”’s policy will respond.

8. How much UM coverage MUST be offered to all purchasers of Bodily Injury Liability in the State of Florida? _____________________________________________. What 2 options are available under the UM coverage? (Not stacking!)

Unit 3: Personal Automobile Property & Casualty Exam Workbook

© Reicon Publishing LLC. All Rights Reserved. 35

9. What is “stacking?”

What options can be offered?

10. When your car is being repaired and you rent one while yours is in the shop this replacement vehicle is called a _______________________________________. What coverages apply to it?

11. What 3 uses does the Extended Non-Owned coverage endorsement have?

a. ______________________________________________________

b. ______________________________________________________

c. ______________________________________________________

12. Describe Transportation Expense benefit under Part D.

13. What does the Named Non-Owner coverage endorsement provide?

14. Define "Motor Vehicle” under Fla. No-Fault Law.

Property & Casualty Exam Workbook Unit 3: Personal Automobile

36 © Reicon Publishing LLC. All Rights Reserved.

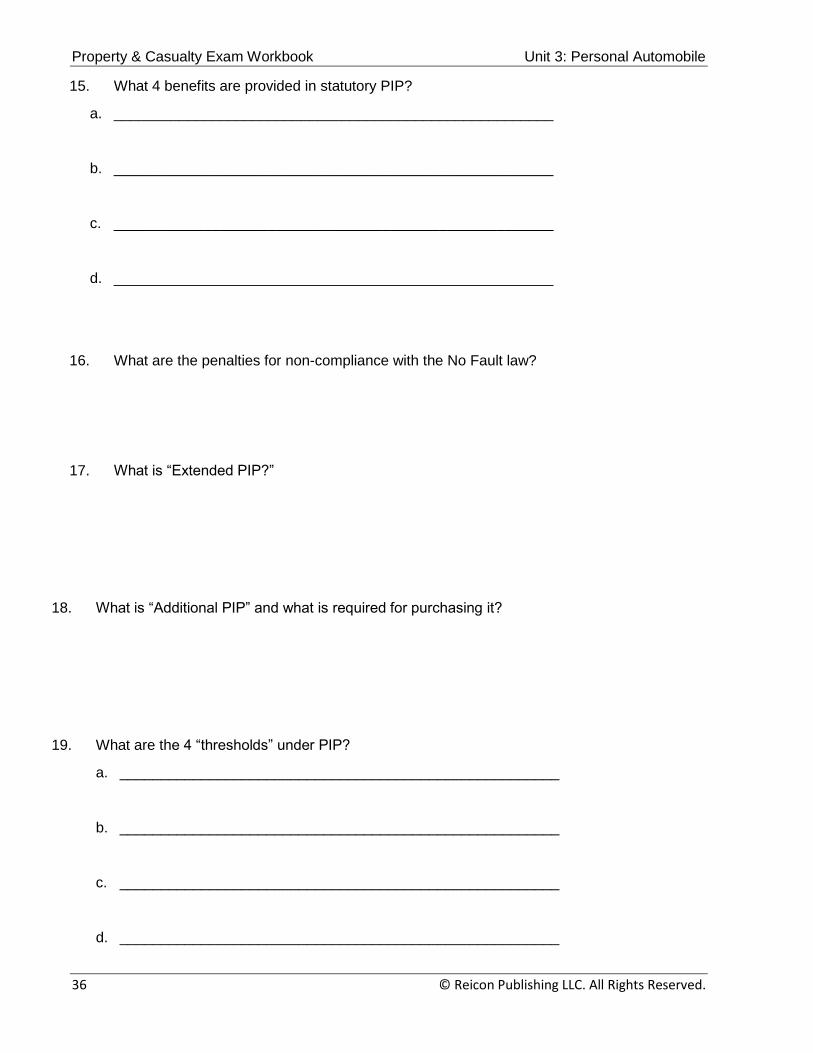

15. What 4 benefits are provided in statutory PIP?

a. ______________________________________________________

b. ______________________________________________________

c. ______________________________________________________

d. ______________________________________________________

16. What are the penalties for non-compliance with the No Fault law?

17. What is “Extended PIP?”

18. What is “Additional PIP” and what is required for purchasing it?

19. What are the 4 “thresholds” under PIP?

a. ______________________________________________________

b. ______________________________________________________

c. ______________________________________________________

d. ______________________________________________________

Unit 3: Personal Automobile Property & Casualty Exam Workbook

© Reicon Publishing LLC. All Rights Reserved. 37

20. Assume “A" purchases PIP with $1,000 deductible and incurs costs as follows:

$7,000 Medical

$5,000 Wage Loss

$2,000 Replacement Services

How much can “A” collect? _______________

21. “A” carries $30,000 Liability, PIP with a $1,000 Deductible, $1,000 Medical Payments and $30,000 UM. “A” causes an accident and injures himself only. There are no other injuries or damage. If his injuries are $30,000 how much can he collect? Be specific.

22. Who is eligible for PIP benefits under the policy?

23. What type of damages can be sued for without "piercing the tort threshold?"

24. When will Florida Financial Responsibility Law be invoked?

25. What must someone do to comply with the Florida Financial Responsibility Law?

26. What is the Cancellation/Non-Renewal requirements under PAP Florida Statue?

27. What deductibles apply to glass breakage of a windshield?

28. What coverages are available under the FJUA for Private Passenger Vehicles (liability)?

Property & Casualty Exam Workbook Unit 3: Personal Automobile

38 © Reicon Publishing LLC. All Rights Reserved.

29. What coverages are available under the FJUA, for Commercial Vehicles (liability)?

Unit 3: Personal Automobile Property & Casualty Exam Workbook

© Reicon Publishing LLC. All Rights Reserved. 39

Auto Review Quiz-Personal Auto Policy (Answers)

1. Residing spouse

2. Any age

3. a. Cars on declaration pages b. Newly acquired auto c. Any trailer you own d. Any vehicle or trailer being used as a temporary substitute

4. Physical harm including sickness and disease

5. Physical injury to tangible property (not your property) and/or loss of use

6. 3 years, no

7. “A” wins. “A” receives the following payments:

PIP - $10,000 – A policy

MP - $1,000 – A policy

L - $30,000 – B policy

UM - $50,000 – A policy

8. Amount equal to liability limits 1. Reject 2. Lower limits

9. Coverages on two or more vehicles are added together

1. Reject 2. Lower limits

10. Temporary substitute vehicle; the best you have

11. a. Non-owned autos used in business b. Non-owned autos used to carry persons or property for a fee c. Non-owned autos furnished or available for use on a regular basis

12. $20 per day - $600 maximum

13. Liability, medical payments, uninsured motorist – for those who do not own a vehicle 14. Self-propelled 4-wheel vehicle and designed for use on Florida highways

15. Medical – household services – loss of income – death

Property & Casualty Exam Workbook Unit 3: Personal Automobile

40 © Reicon Publishing LLC. All Rights Reserved.

16. Loss of tort exemption, owner becomes personally responsible and loss of license and registration

17. 80% increased to 100% medical, 60% increased to 80% for lost income

18. Increase PIP coverage of $10,000 by $10,000, $25,000, $40,000 or $90,000, extended PIP is required

19. a. Significant scaring and disfigurement b. Loss of bodily function c. Permanent injury other than scaring and disfigurement. d. Death

20. $9,800.

21. $10,000 PIP + $1,000 medical pay = $11,000 total

22. Insured, family members and those Florida residents without owned autos

23. Any amount above $10,000 that is an economic loss

24. When there is bodily injury or property damage, when vehicle is rendered inoperative and any serious crime takes place like DUI or felony.

25. Carry at least 10/20/10

26. 45-day notice and 10-day for non-payment if not subject to PIP

27. None

28. 100/300/50

29. 100/300/50

Property & Casualty Exam Workbook Unit 3: Personal Automobile

© Reicon Publishing LLC. All Rights Reserved. 41

Personal Auto Policy Multiple Choice 1. Which of the following triggers the financial responsibility law?

a. an accident

b. an accident involving BI or PD that renders a vehicle inoperative, certain serious traffic offenses

c. running your car into a building

2. Which are the minimum limits required by Florida

a. 10,000/20,000/10,000

b. 10,000 PIP /10,000 PD

3. Which are the alternate ways to satisfy the FR law?

a. Live outside of Florida and only drive your car in Florida

b. Drive somebody else's car

c. Cash, bond, qualified self-insured

d. Obtain a PIP endorsement

4. What is the purpose of an SR22?

a. Similar to a vehicle title, which shows ownership of a vehicle

b. It is mandatory insurance for ownership of a SUV pulling a trailer

c. Provides proof of financial ability for future accidents

5. What is required for an operator who does not own an auto but needs an SR22? a. Obtain a personal auto policy b. Exercise the death benefit of PIP c. Purchase a Named Non-Owner Policy

6. Violations of the law such as making misstatements, committing forgery, filing false

affidavits are punishable as...? a. Loss of drivers’ license b. 1st degree misdemeanor c. 2nd degree misdemeanor

7. Which of the following entities administers the Financial Responsibility Law?

a. NCCI b. Florida Department of Financial Services c. Florida Department of Highway Safety and Motor Vehicles d. Florida State Police

8. Which coverage is "No Fault"?

a. Bodily Injury/Property Damage b. Personal Injury Protection

9. Which is the definition of a Motor Vehicle?

a. All motorized vehicles both designed and licensed for highway use b. Motorized vehicles with 4 or more wheels both designed and licensed for highway use c. Taxis, limousines, buses, motorcycles, trucks, cars, SUVs

Unit 3: Personal Automobile Property & Casualty Exam Workbook

42 © Reicon Publishing LLC. All Rights Reserved.

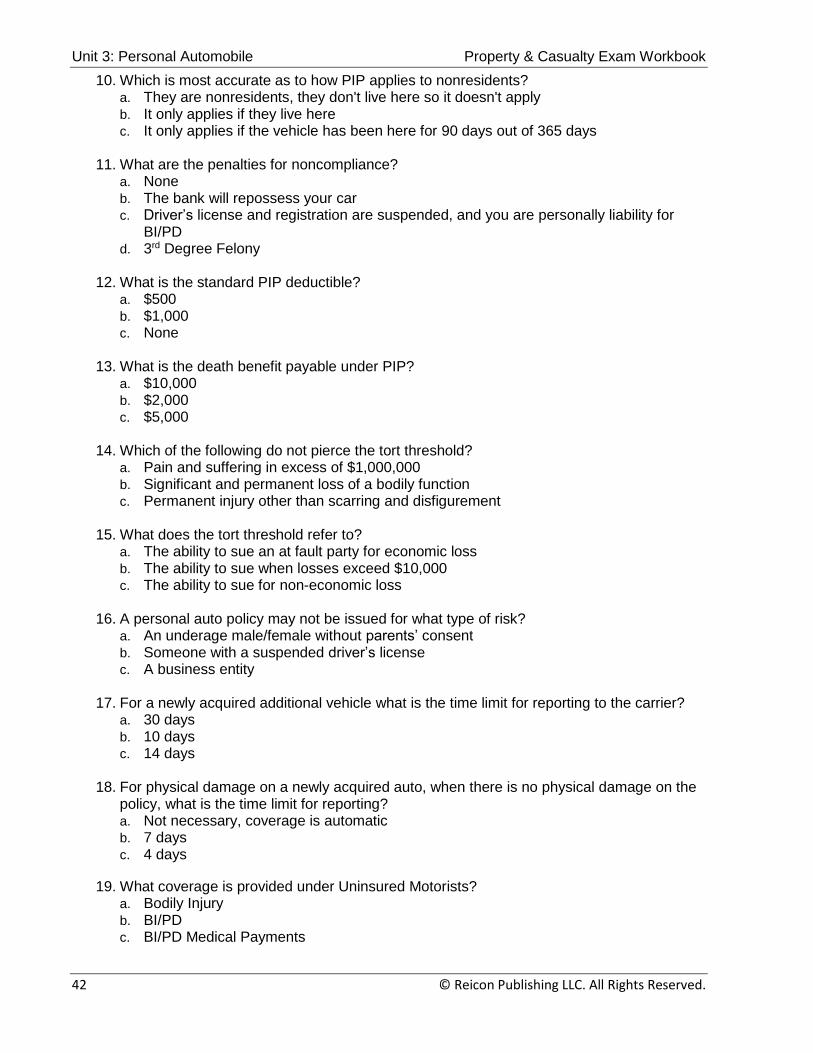

10. Which is most accurate as to how PIP applies to nonresidents? a. They are nonresidents, they don't live here so it doesn't apply b. It only applies if they live here c. It only applies if the vehicle has been here for 90 days out of 365 days

11. What are the penalties for noncompliance?

a. None b. The bank will repossess your car c. Driver’s license and registration are suspended, and you are personally liability for

BI/PD d. 3rd Degree Felony

12. What is the standard PIP deductible?

a. $500 b. $1,000 c. None

13. What is the death benefit payable under PIP?

a. $10,000 b. $2,000 c. $5,000

14. Which of the following do not pierce the tort threshold?

a. Pain and suffering in excess of $1,000,000 b. Significant and permanent loss of a bodily function c. Permanent injury other than scarring and disfigurement

15. What does the tort threshold refer to?

a. The ability to sue an at fault party for economic loss b. The ability to sue when losses exceed $10,000 c. The ability to sue for non-economic loss

16. A personal auto policy may not be issued for what type of risk?

a. An underage male/female without parents’ consent b. Someone with a suspended driver’s license c. A business entity

17. For a newly acquired additional vehicle what is the time limit for reporting to the carrier?

a. 30 days b. 10 days c. 14 days

18. For physical damage on a newly acquired auto, when there is no physical damage on the policy, what is the time limit for reporting? a. Not necessary, coverage is automatic b. 7 days c. 4 days

19. What coverage is provided under Uninsured Motorists? a. Bodily Injury b. BI/PD c. BI/PD Medical Payments

Property & Casualty Exam Workbook Unit 3: Personal Automobile

© Reicon Publishing LLC. All Rights Reserved. 43

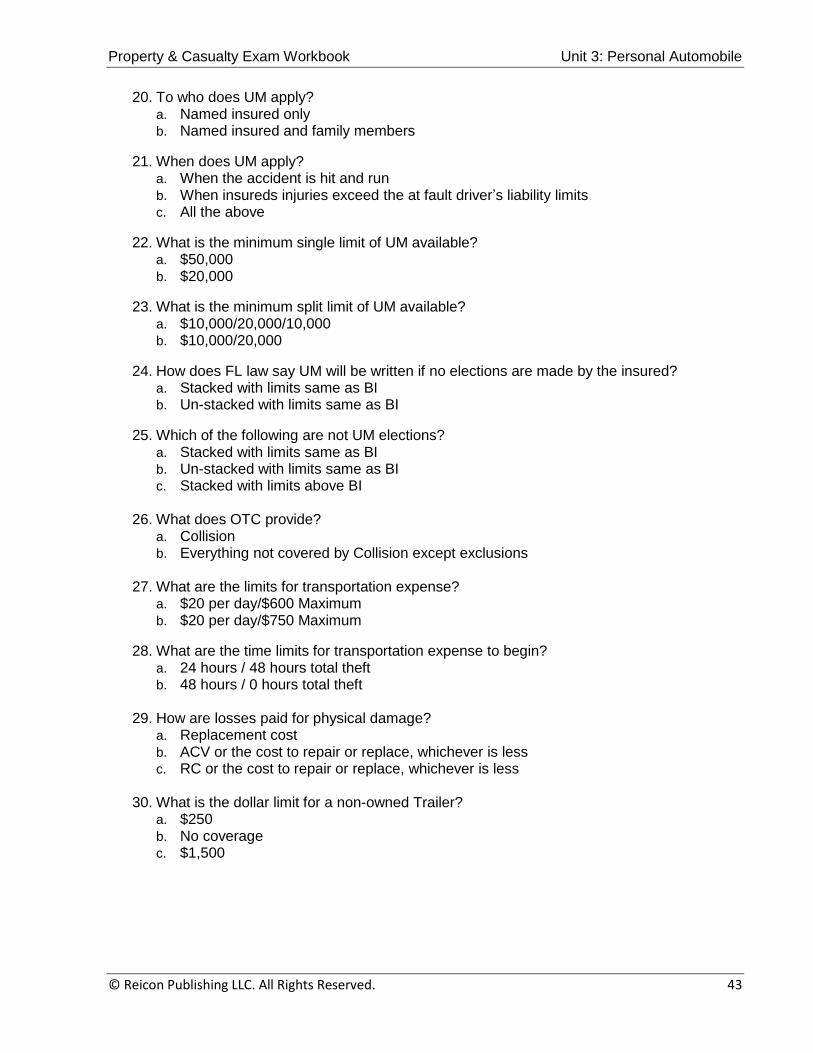

20. To who does UM apply?

a. Named insured only b. Named insured and family members

21. When does UM apply? a. When the accident is hit and run b. When insureds injuries exceed the at fault driver’s liability limits c. All the above

22. What is the minimum single limit of UM available? a. $50,000 b. $20,000

23. What is the minimum split limit of UM available? a. $10,000/20,000/10,000 b. $10,000/20,000

24. How does FL law say UM will be written if no elections are made by the insured? a. Stacked with limits same as BI b. Un-stacked with limits same as BI

25. Which of the following are not UM elections? a. Stacked with limits same as BI b. Un-stacked with limits same as BI c. Stacked with limits above BI

26. What does OTC provide?

a. Collision b. Everything not covered by Collision except exclusions

27. What are the limits for transportation expense?

a. $20 per day/$600 Maximum b. $20 per day/$750 Maximum

28. What are the time limits for transportation expense to begin? a. 24 hours / 48 hours total theft b. 48 hours / 0 hours total theft

29. How are losses paid for physical damage? a. Replacement cost b. ACV or the cost to repair or replace, whichever is less c. RC or the cost to repair or replace, whichever is less

30. What is the dollar limit for a non-owned Trailer? a. $250 b. No coverage c. $1,500

Unit 3: Personal Automobile Property & Casualty Exam Workbook

44 © Reicon Publishing LLC. All Rights Reserved.

31. What is the policy territory?

a. US, it's territories or possessions, Puerto Rico, Canada, Mexico and while being transported between these ports

b. US, it's territories or possessions, Puerto Rico, Mexico and while being transported between these ports

c. US, it's territories or possessions, Puerto Rico, Canada and while being transported between these ports

32. The Towing and Labor endorsement cover the cost of labor at which location?

a. The place of disablement b. The “insured’s” residence c. An automobile dealership for the make of automobile disabled.

33. Which of the following endorsements cover for Liability/Medical expenses for a non-owned auto furnished or available for regular use, using the vehicle in business, or when carrying persons or property for a fee? a. No endorsement available. Must have business auto policy b. Hired/Non-owned endorsement c. Extended Non-owned endorsement

34. Which endorsement provides, liability, med pay and UM for a named individual who does not own an auto, for the operation of autos of others? a. Hired/Non-Owned Auto endorsement b. Extended Liability Endorsement c. Named Non-Owner Endorsement

35. Which endorsement covers Motor Homes, Motorcycles, and Golf Carts ATVs? a. None. Must purchase a separate policy b. None, Automatic coverage provided in the policy c. Miscellaneous Type Vehicle Endorsement

36. Which endorsement increases PIP from 80% to 100% and work loss from 60% to 80%? a. No such endorsement b. Extended PIP c. Additional PIP

37. Which endorsement increases the Dollar Limit of PIP? a. Cannot be increased. Maximum payable is $10,000 b. Extended c. Additional PIP

Property & Casualty Exam Workbook Unit 3: Personal Automobile

© Reicon Publishing LLC. All Rights Reserved. 45

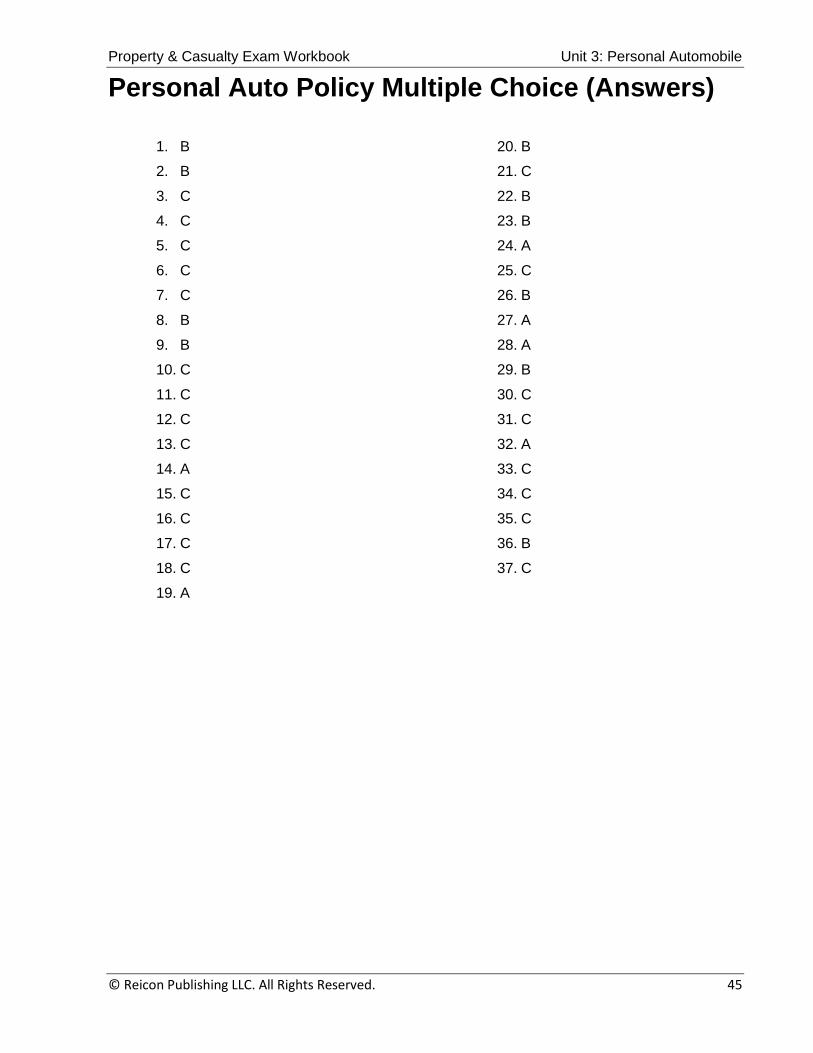

Personal Auto Policy Multiple Choice (Answers)

1. B

2. B

3. C

4. C

5. C

6. C

7. C

8. B

9. B

10. C

11. C

12. C

13. C

14. A

15. C

16. C

17. C

18. C

19. A

20. B

21. C

22. B

23. B

24. A

25. C

26. B

27. A

28. A

29. B

30. C

31. C

32. A

33. C

34. C

35. C

36. B

37. C

Unit 3: Personal Automobile Property & Casualty Exam Workbook

46 © Reicon Publishing LLC. All Rights Reserved.

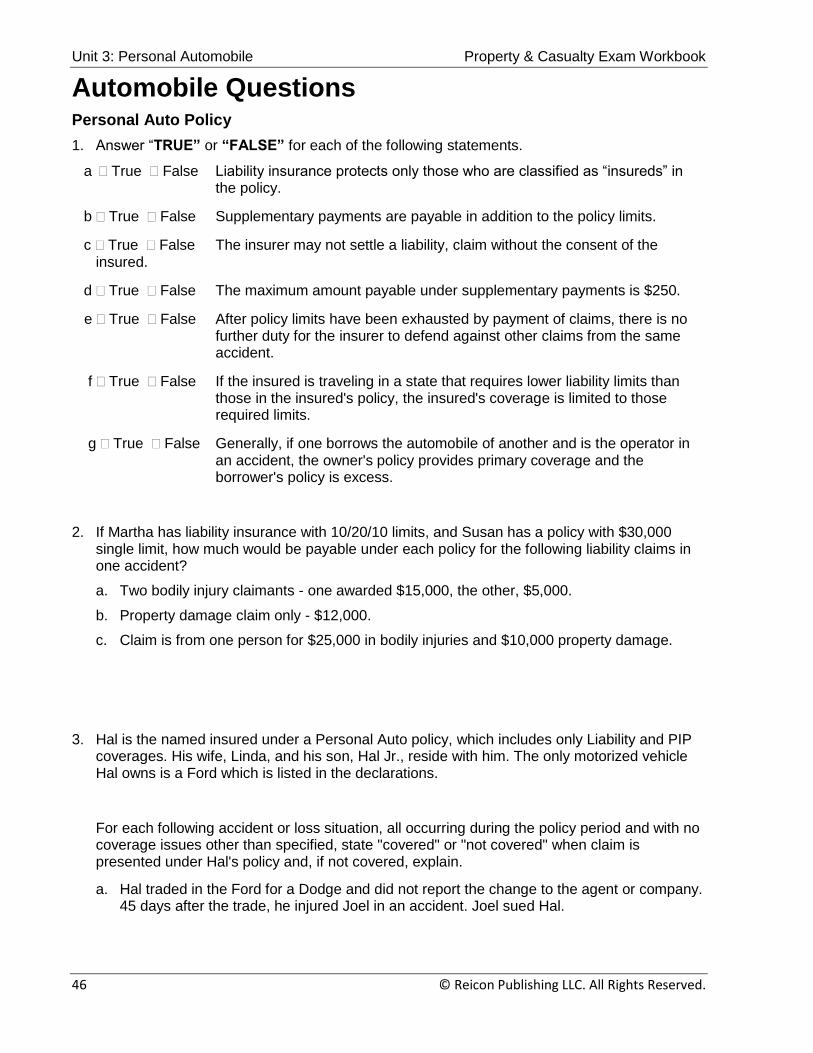

Automobile Questions Personal Auto Policy

1. Answer “TRUE” or “FALSE” for each of the following statements.

a True False Liability insurance protects only those who are classified as “insureds” in the policy.

b True False Supplementary payments are payable in addition to the policy limits.

c True False The insurer may not settle a liability, claim without the consent of the insured.

d True False The maximum amount payable under supplementary payments is $250.

e True False After policy limits have been exhausted by payment of claims, there is no further duty for the insurer to defend against other claims from the same accident.

f True False If the insured is traveling in a state that requires lower liability limits than those in the insured's policy, the insured's coverage is limited to those required limits.

g True False Generally, if one borrows the automobile of another and is the operator in an accident, the owner's policy provides primary coverage and the borrower's policy is excess.

2. If Martha has liability insurance with 10/20/10 limits, and Susan has a policy with $30,000 single limit, how much would be payable under each policy for the following liability claims in one accident?

a. Two bodily injury claimants - one awarded $15,000, the other, $5,000.

b. Property damage claim only - $12,000.