Embed Size (px)

Citation preview

© LCP Consulting

© LCP Consulting Ltd, The Stables, Ashlyns Hall,Chesham Road, Berkhamsted, HP4 2ST UK

Tel: +44 (0)1442 872298 Fax: +44 (0)1442 873896

Julian Mosquera

Director, LCP Consulting

May, 2014

Property and the changing faceof RetailSEGRO Investor and Analyst Event

© LCP Consulting

What’s keeping retail boards awake?

• Continued pressure on consumerspending

• Rising commodity costs, coupledwith environmental and ethicalconcerns

• Technology continuing to changethe way consumers shop

• Retailers must adapt or fall away

• Increasing costs of operatingstores

• The search for growth:

• New channels

• New categories

• International7 May 2014 SEGRO Investor and Analyst Event2

© LCP Consulting

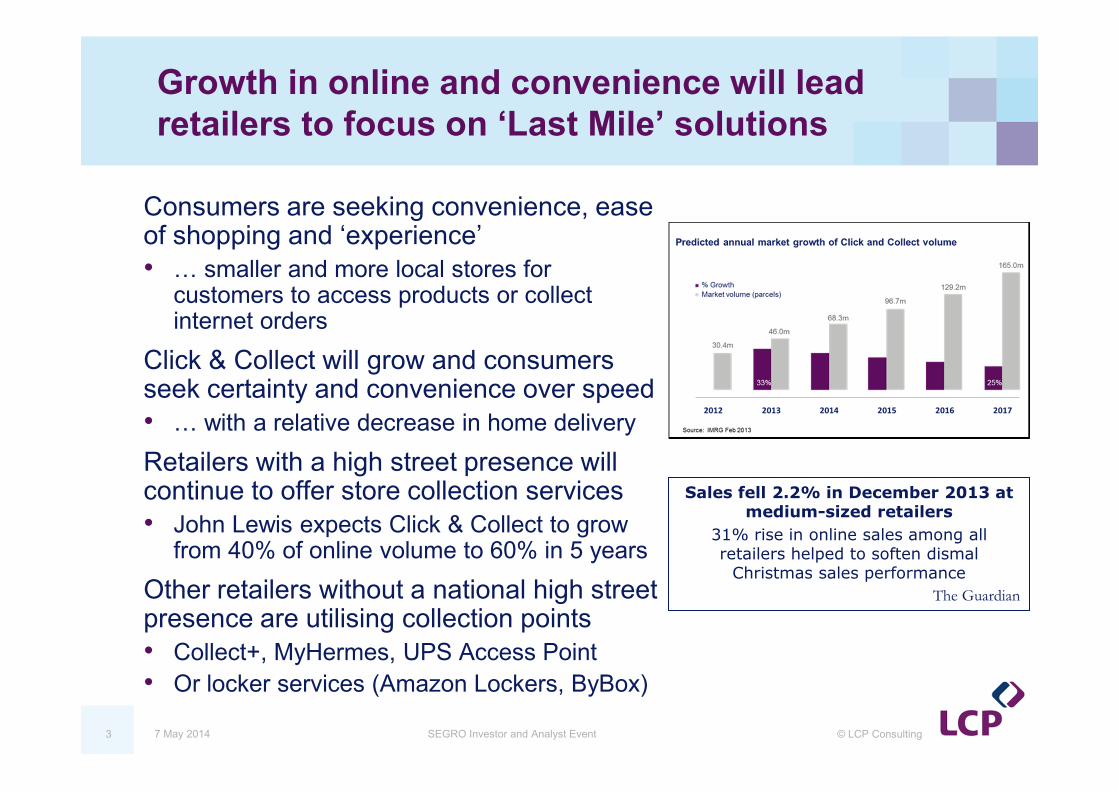

Growth in online and convenience will leadretailers to focus on ‘Last Mile’ solutions

Consumers are seeking convenience, easeof shopping and ‘experience’• … smaller and more local stores for

customers to access products or collectinternet orders

Click & Collect will grow and consumersseek certainty and convenience over speed• … with a relative decrease in home delivery

Retailers with a high street presence willcontinue to offer store collection services• John Lewis expects Click & Collect to grow

from 40% of online volume to 60% in 5 years

Other retailers without a national high streetpresence are utilising collection points• Collect+, MyHermes, UPS Access Point

• Or locker services (Amazon Lockers, ByBox)

7 May 2014 SEGRO Investor and Analyst Event3

Sales fell 2.2% in December 2013 atmedium-sized retailers

31% rise in online sales among allretailers helped to soften dismal

Christmas sales performance

The Guardian

© LCP Consulting

What are we hearing?

7 May 2014 SEGRO Investor and Analyst Event4

“Convenience for customers is going to be one of thebiggest drivers that shapes retail operations” GroceryRetailer

“For the next 3-4 years online growth will be the maintrigger for overall business growth“ Clothing / GMRetailer

“Retailers are starting to recognise that Click andCollect is a service that their customers want as itprovides convenience and certainty for their customer”Online Fulfilment Carrier

“With the congestion lobby getting stronger, there willbe fewer routes going into town, so city hubconsolidation centres will gain importance” 3PL

© LCP Consulting

What challenges do these changes present tolast mile delivery?

• Distribution Centres (DCs) pick for stores in cases and distribute onroll cages / pallets

… Online DCs pick in singles and pack for home delivery

• Both require high availability at lowest cost and are challenged by:

• Urban congestion, limits on emissions and restricted deliverywindows

• Convenience requires smaller, more frequent deliveries

• Multi temperature delivery requirements

• This has implications for:

• DC design in terms of location, building size and function, docks

• Vehicle types

• However, the biggest challenge for online is returns

7 May 2014 SEGRO Investor and Analyst Event5

© LCP Consulting

The ‘Returns’ challenge

7 May 2014 SEGRO Investor and Analyst Event6

• In the ‘Omni’ world, consumers require flexible return channels to fit theirimmediate circumstances

• A real value and margin ‘protector’, increasingly integrated into networks

• Peaks present many challenges e.g. at Christmas

• Boomerang Thursday (2013) immediately after Black Monday – I have orderedthe wrong item or have found it cheaper

• Immediate pre-Christmas return – it is the wrong item or I have worn it for theChristmas party and I am now returning it !

• Boxing Day to mid-January – unwanted gifts

• End of January blip – return of items used throughout Christmas e.g. TVs,Beds, some clothes !

• Online returns typically run at 30% - 40% … a retailer’s biggest supplier

• Focus on speedy capture of product into a nominated return route

• Sites are often co-located with major retail e-commerce DCs – the fastestchannel to resale

© LCP Consulting

What types of property will be in demand?

• Supply chain principles will govern the retail responses …

• … which are mostly predictable and there are existingexamples:

• Customer Delivery Hubs

• City Hubs

• Dark Stores

• Convenience DCs

• Returns Centres

• Mega Sheds

• eDCs

7 May 2014 SEGRO Investor and Analyst Event7

© LCP Consulting

Implications for property providers

• Omni-channel retail and customer convenience will be a key driverof logistics set up

... but there is no standard approach – capitalising on these changesrequires a close relationship with retailers and service providers

• Flexible and targeted build will be essential for the future

• In addition to regional location, properties must be evaluatedagainst multiple criteria

• Roads, size, labour, access, parking, hours of use, sell-on etc.

• These will vary greatly by retail operation type

• Urbanisation and its environmental impacts will start to create newapproaches to logistics

• An opportunity sites on the edge of major conurbations

• Success requires deep insight of specific retailers’ andservice providers’ requirements

7 May 2014 SEGRO Investor and Analyst Event8