Embed Size (px)

Citation preview

EThekwini Property Market Review 2007/2008

PPRROOPPEERRTTYY MMAARRKKEETT RREEVVIIEEWW

TTHHEE DDUURRBBAANN MMEETTRROO RREEGGIIOONN

ETHEKWINI MUNICIPALITY

ECONOMIC DEVELOPMENT UNIT

2007-2008

DDOOCCUUMMEENNTT PPRREEPPAARREEDD BBYY::

Viruly Consulting (Pty) Ltd

Contribution from Ramesh Amrit (2006)

(Letchimah Daya Mandindi)

LDM PROPERTY RESEARCHA Division of LETCHMIAH ⏐ DAYA ⏐ MANDINDI

EThekwini Property Market Review 2007/2008

0046/07/FV Page 2 24/10/2007

CONTENTS

EXECUTIVE SUMMARY 4

1. INTRODUCTION 6

1.1 THE BRIEF 7

1.2 REPORT STRUCTURE 7

2. THE SOUTH AFRICAN PROPERTY MARKET 8

2.1 THE MACRO ENVIRONMENT 8

2.2 MACRO PROPERTY TRENDS 10

3. THE ETHEKWINI MUNICIPALITY IN CONTEXT 16

3.1 THE ECONOMY 17

3.2 THE NODAL PROPERTY MARKET 21

3.2.1 THE DURBAN CBD 23

3.2.2 THE CENTRAL NODE 25

3.2.3 THE WESTERN NODES 26

3.2.4 THE NORTHERN NODES 29

3.2.5 THE SOUTHERN NODES 32

3.3 THE SIZE OF THE COMMERCIAL MARKET 34

4. PROPERTY MARKET INDICATORS 37

4.1 THE DURBAN CBD 38

4.2 THE CENTRAL NODES 39

4.3 THE WESTERN NODES 40

4.4 THE NORTHERN NODES 44

4.5 THE SOUTHERN NODES 46

5. INVESTMENT INCENTIVES AND URBAN REGENERATION 48

5.1 REGENERATION PROJECTS 50

5.2 THE POINT WATERFRONT 51

5.3 THE DURBAN INVESTMENT AGENCY 51

5.4 THE URBAN DEVELOPMENT ZONE 53

6. CONCLUDING REMARKS 55

7. REFERENCES AND NOTES 57

All care has been taken in the preparation of this document and the information contained

herein has been derived from sources believed to be accurate and reliable. Viruly Consulting

(Pty) Limited does not assume responsibility for any error, omission or opinion expressed as

well as investment decisions based on this information.

EThekwini Property Market Review 2007/2008

0046/07/FV Page 3 24/10/2007

EXECUTIVE SUMMARY

The South African property market is benefiting from a strong macro-economic

environment, characterized by a stable inflation rate and improved prospects for

economic growth. This is translating into a decline in vacancy rates, and rising

rentals and capital values in most sectors of the South African property market.

The eThekwini Municipality is underpinned by strengthening conditions in the

manufacturing, chemical and tourism sectors. Moreover, the expected growth of

the harbour will continue to pose opportunities and challenges for the demand of

suitably located land.

The eThekwini retail, office and industrial markets are currently showing strong

growth mainly due to the favourable macro commercial market fundamentals and

this has resulted in positive real investment returns in most sectors of the market.

Although the 2005 investment returns produced by the Investment Property Data

Bank (IPD) were at their highest since the data was collated in 1995, IPD indices

reporting returns to December 2006 show a slight downward adjustment in

returns, the sharpest decline being in retail which has dipped below the 30%

level. Industrial and office returns have experienced less of a drop with industrial

sector remaining above the 30% level and the office sector also showing relative

stability.

From a micro perspective, demand for industrial and office space remains buoyant

in major nodes of the eThekwini market. Such nodes include the Berea,

Umhlanga/La Lucia Ridge and Westville. Moreover, the CBD is also showing

increased demand, especially from smaller tenants, and ABSA’s decision to

reinvest in the CBD, through an upgrade to their existing building, and Standard

Bank’s decision to relocate to the Kingsmead Office node is reflective of renewed

investor confidence and the efficacy of incentives created by the UDZ tax

accelerated depreciation allowances.

Added to this, nodes such as Kingsmead are being supported by public sector

initiatives. These include the recently completed ICC Arena, being the extension

to the existing convention centre. Kingsmead is also expected to benefit from the

EThekwini Property Market Review 2007/2008

0046/07/FV Page 4 24/10/2007

development of a proposed international sports precinct supported by the

eThekwini municipality and its joint partnerships and Durban Investment

Promotion Agency. Such organisations are also involved in facilitating urban

regeneration projects such as Warwick Junction, the Point development, and the

Beachfront. The flagship development of uShaka Marine Theme Park has provided

a catalyst for the further development of the Point into a vibrant mixed-use

development. Therefore, it can be argued, that the market is benefiting from

improved market conditions resulting from strong market fundamentals and

appropriate public sector interventions. The future spatial form of the local

economy is also being influenced by the forthcoming development of the Dube

Trade Port and the King Shaka International Airport.

A disaggregation of market statistics suggests that rentals are generally on the

rise reflecting higher building costs and strong market fundamentals. In

Umhlanga/La Lucia and Westville, rentals for newer stock are driving peak rentals

to levels above R100/m² gross for new stock.

The retail market is also showing signs of strong investment returns and this is

being matched with proposals for new retail developments, especially in areas

that in the past have been under-catered for. Reflecting national trends, interest

in this sector is extending into new nodes such as Umlazi and other townships in

the municipal area.

Consequently, development activity is also spreading itself to the southern

commercial nodes. These nodes have for decades provided good locations for

industrial sector tenants that need to be located in the South Durban Basin and

the port. With the proposed relocation of Durban International airport, the

potential exists for good industrial land to be released into the market. However,

there are question marks over the future use of this land due to its potential to

accommodate port expansion.

The future success of the metropolitan property market will also rely on ensuring

that appropriate city integration is realised, and this will mean the integration of

‘home, work and play’ for different income groups. This will also require a careful

assessment of transportation requirements, a sector which seems to be lagging

EThekwini Property Market Review 2007/2008

0046/07/FV Page 5 24/10/2007

behind in the urban restructuring process. The challenge lies in ensuring that

households are able to seek locations that optimise the ability to secure

employment.

For the South African property investor, the challenge will lie in correctly reading

the major trends that drive the municipal economic base and developing

properties that support the municipal economic trajectory. Success in achieving

this requires an appropriate co-ordination between the private and public sectors.

1. INTRODUCTION

The role of the eThekwini Municipality’s Economic Development Unit (EDU) is to

guide the municipality in optimising economic development, job creation and

redistribution opportunities for the residents of the eThekwini region. A specialised

unit has also been set up to focus on private investment and development

promotions. This unit has the following roles:

To advise the local government on issues affecting the private sector and

investment.

To implement local government programmes to support private sector

development and investment.

To advise potential investors on issues affecting their business interests in the

Durban Metro Area (eThekwini Municipality).

This report aims to assist the EDU’s role in encouraging private sector investment

through the dissemination of market information to investors. The report primarily

considers the status of the Durban Property Market as well as development and

investment opportunities in the municipal property sector.

EThekwini Property Market Review 2007/2008

0046/07/FV Page 6 24/10/2007

1.1 THE BRIEF

The report is focused on the following:

An introduction to the property investment environment that includes a broad

overview of the macro South African commercial property market, paying

special attention to the major market trends impacting on the South African

property market.

Economic development, land strategy and other objectives of the eThekwini

municipality that may optimise property development and investment.

Emphasis on special features of Durban and other regional attributes such as

tourism attractions and its unique features.

Discussing the prime industrial, office and retail property nodes of Durban.

Providing updates on major property and infrastructural projects.

Highlighting institutional and other factors that investors should take into

account when considering entering the Durban property market.

1.2 REPORT STRUCTURE

The report is structured as follows:

Section 2: The section will discuss macro trends affecting the property market in

the Durban property market.

Section 3: Introduction to eThekwini Municipality – the administrative local

government of the Durban property market – an overview of the socio-economic

profile of the municipality, and general characteristics of the region. The section

will also introduce the main commercial and industrial nodes of the municipality -

their characteristics and general development trends.

Section 4: Analyses the property market nodes, characteristics, property

indicators and parameters of the different nodes in the urban property market.

Section 5: Discusses political objectives that support property development as

well as important policies in place from government level. Major development

EThekwini Property Market Review 2007/2008

0046/07/FV Page 7 24/10/2007

projects led by the public sector and supported by the private sector in eThekwini

will also be emphasised.

Section 6: Provides concluding remarks.

2. THE SOUTH AFRICAN PROPERTY MARKET

The macro economic environment has a significant impact on micro property

trends in South African cities, especially in determining the level of development

activity and where this activity occurs. But at the same time the demand for

commercial space is a function of the performance and future prospects of the

local economic base. The economic development of the municipality will have a

spatial dimension which the municipality is in a position to influence. Yet, cities

around the world are finding it increasingly difficult to foresee and react to such

trends.

2.1 THE MACRO ENVIRONMENT

The macro property market operates within an institutional framework that

comprises four main environments; these are of a socio-political, economic,

financial, technological and infrastructural nature. To this, one can add issues

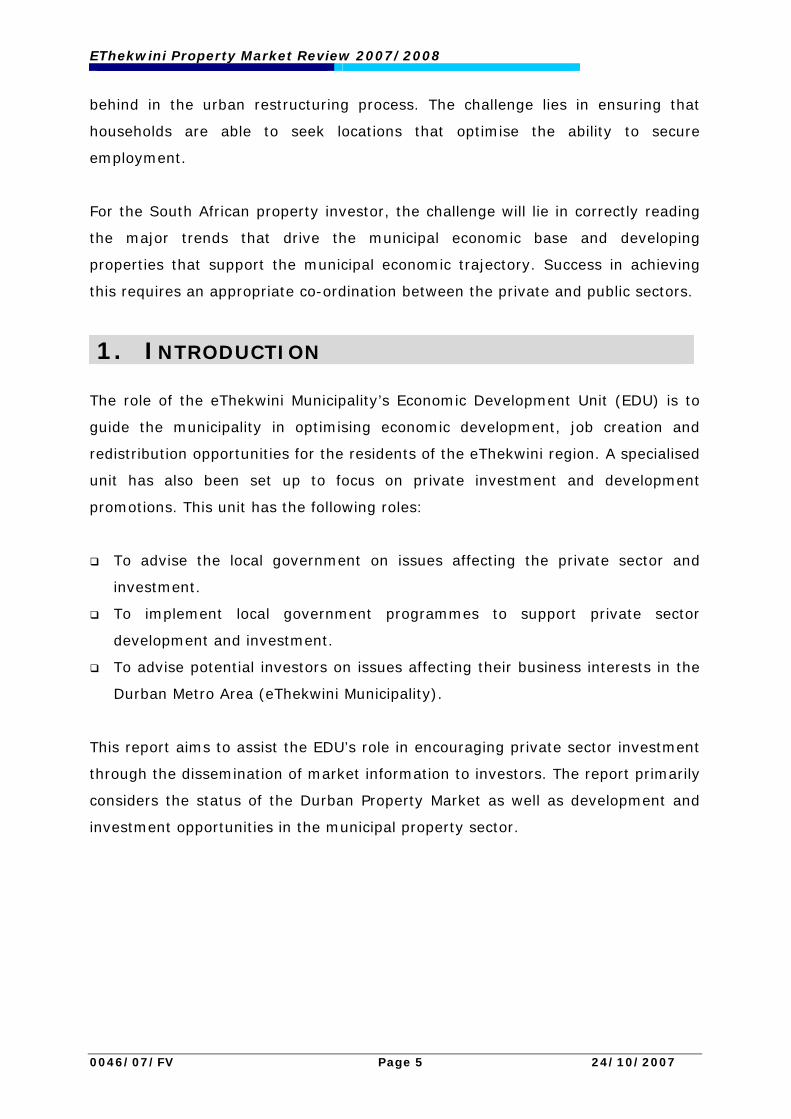

such as lifestyle as illustrated in the Figure 1. This institutional environment

influences the property market by determining:

The type of investments that occur;

The property cycle and its various peaks and lows;

Where developments occur; and

Who has access to land?

EThekwini Property Market Review 2007/2008

0046/07/FV Page 8 24/10/2007

Figure 1: The Macro Drivers of the Property Market

Social and Political Environment – This relates to market and political

institutions and their impact on property investments and developments.

Although all three tiers of government influence property related policies, it is

at local government level that the property market is most directly influenced

through for instance, Integrated Development Plans (IDP’s), Spatial

Development Frameworks and Plans, Local area plans, Precinct plans and town

planning policies and practices. Urban regeneration and investment incentives,

at local government level, are similarly playing a role in directing the property

market.

The Economic Environment – The property market is influenced by

conditions in the macro as well as local economy. For instance investment

decisions are sensitive to economic growth expectations as well as the

direction of the inflation rate and interest rates. The macro economy also

influences conditions in the local economy and the corresponding demand for

space. It is however the local economic base that ultimately influences

prospects for the property market at a municipal level.

Social & Political Urban Regeneration

Housing & Environment Property

Charter Foreign Ownership Land

Restitution PP’s

Investment Incentives

Macro Economy Low Inflation Environment

Interest Rates Stable Economic Growth

Business Confidence

Lifestyle-

‘Home, Work and Play’ Mixed-use

Developments Neighbourhood Developments

Specialised Retailing

Transport

Pressure with Higher Economic Growth Traffic Congestion “A housing Issue”

Motorized/Non Motorized

The SA Property Market

EThekwini Property Market Review 2007/2008

0046/07/FV Page 9 24/10/2007

Transport and Infrastructural Environment - Infrastructure provision has

a strong influence on property development and investment decisions. For

instance, traffic congestion is becoming a critical issue in many South African

cities and has started to influence locational decisions by businesses and

households. Levels of traffic congestion have become of significance in the

northern commercial nodes of La Lucia/Ridge Umhlanga and Mount

Edgecombe. Although the trend remains unclear, there are indications that

traffic congestion and other infrastructural impediments could in due course

shift investors and tenants back to the Central Business District (CBD) and its

periphery, where infrastructure seems to be adequate. A further point is that

stricter environmental regulations could also make CBD “brownfield

developments” attractive.

2.2 MACRO PROPERTY TRENDS

This section of the report looks at the macro drivers of the property market and

how these will in due course impact on the Durban property market.

As already mentioned, the relatively good performance of the Macro economy is

underpinning the Durban Property Market. The challenge will lie in ensuring that

the Durban market captures these benefits and that the property market plays a

role in improving economic efficiencies.

The drivers for the different components of the market differ for the office, retail

and industrial markets.

The Retail Sector

The retail property sector is both dictated by trends at the macro and

micro level. Macro economic parameters influence consumption

expenditure and therefore national retail sales.

From a micro perspective, retail developments are influenced by the

performance of shopping centre catchment areas or the buying power of

nodes. In turn this is driven by the performance of specific residential

areas. Locational issues are also of importance, with for instance the CBD

EThekwini Property Market Review 2007/2008

0046/07/FV Page 10 24/10/2007

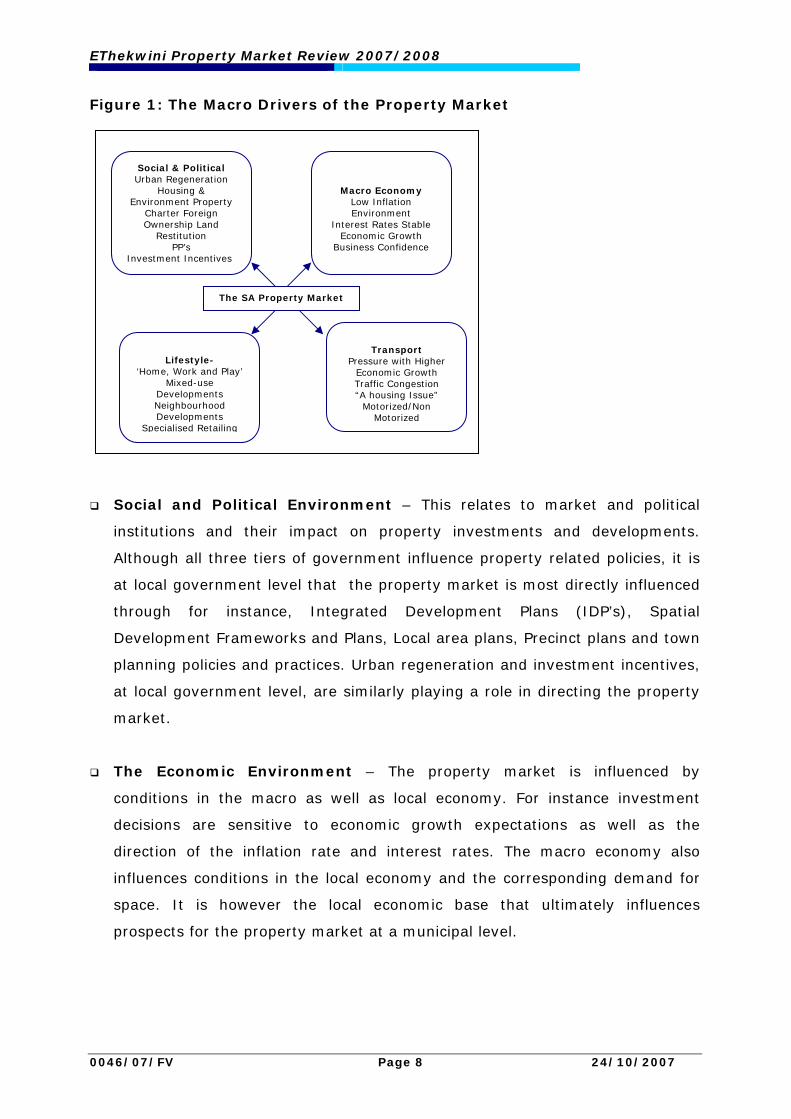

playing an important role in attracting retailers across the municipal area

and beyond.

The overall market view seems to be that the Durban property market

continues to offer significant retailing opportunities. This being equally

true for the higher income northern nodes and the lower income township

market. Large shopping centres such as The Pavilion and Gateway have

expanded, and investors are eyeing the southern nodes of the municipal

area, which have not received significant investor interest in recent years.

Several shopping centres have been proposed in and around the

Amanzimtoti area.

The Office Sector

The office sector is mainly driven by conditions in the local economy as

well as the attractiveness of a city as an office location. In the early

2000’s the macro office sector in general experienced depressed

conditions mainly reflecting a period of heightened oversupply, high

vacancy rates and a resulting decline in rental increases. This not only

affected the already depressed CBD market, but also impacted on the

performance of decentralised nodes. From 2004 onwards the sector

stabilised with vacancies starting to decline, this in turn has led to

improved prospects for rental increases and development potentials. The

vacancy trends are discussed in greater detail in other sections of this

report.

The past decade has seen a decentralization of office nodes in most South

African office markets –this in turn has left CBD’s with high vacancy rates

and low levels of investor interest. Yet, the scenario is changing with the

capital value of properties in such nodes rapidly rising and new investors

entering the market. Although there has been a growth on decentralised

office space Durban’s national share of office space in real terms has been

shrinking when compared with other centres. This suggests that growth in

decentralised nodes is more firmly linked to movement away from the

CBD rather than the absorption of new space.

EThekwini Property Market Review 2007/2008

0046/07/FV Page 11 24/10/2007

The Industrial Sector

The industrial sector tends to be a market that is not as speculative as the

office market and retail markets. Most developments in this sector of the

market tend to be tenant-driven and highly dependent on the

performance of the local manufacturing sector. This sector is also showing

an upswing, after a period of high vacancies and low rental increases.

Market data suggests that there is a shortage in the supply of well-located

industrial space and that there is demand for industrial land in the

different commercial nodes of the municipality.

The Durban property market has been at the forefront of the national

industrial sector recovery with nodes such as Briardene and Riverhorse

Valley Business Estate showing rising demand. Large national tenants

have also been keen to take up space with good highway frontage and

exposure.

Future growth of the sector will rely on the municipality stimulating

sectors that have good long-term prospects and to ensure that such

sectors are appropriately clustered. The expected growth in the port will

also remain an important parameter in determining the future demand for

industrial space.

Mixed-use Developments

The focus on mixed-use developments, which includes business estates,

with other uses is growing in popularity. Such developments are an

attempt to create an attractive life style. Mixed-use developments can

either be of a private sector nature, or created through specific public

sector interventions. The Umhlanga Node, through its New Town Centre,

is possibly a good example of this trend, with further investment being

planned in this area.

The Point Waterfront also offers an opportunity for the development of

such a mixed-use development. But, such developments come with

numerous challenges and sometimes contradictions. This relates to both

the challenges of accommodating different uses in close proximity to each

EThekwini Property Market Review 2007/2008

0046/07/FV Page 12 24/10/2007

other, and the need to create true mixed-use environments in support of

new urban lifestyle choices. Experience around the country suggests that

the success of mixed use developments is influenced by the size of such

developments and ensuring that the phasing occurs in an appropriate

fashion.

The further challenge lies in ensuring that such mixed-use developments

occur in different parts of the city. While in the more affluent areas such

developments are often initiated by the private sector, in lower income

areas this role often needs to be initiated by the public sector.

The Investment Property Data Bank (IPD) provides the following disaggregated

figures for the South African property market.

The table below illustrates the trend in property returns over an eleven-year

period.

Table 1: Total Returns for the Property Market

95 96 97 98 99 00 01 02 03 04 05 06

Retail 16.9 17.2 23.0 9.1 17.9 10.4 13.4 11.0 17.4 26.1 33.0 27.4

Offices 14.8 9.9 12.8 1.6 9.5 12.7 7.8 5.1 8.5 16.7 24.5 24.5

Industrial 13.5 17.9 16.8 2.1 8.3 7.1 7.5 8.8 17.5 24.4 33.1 31.1

Other 15.2 16.9 18.1 5.1 24.9 16.6 10.0 20.5 25.4 27.5 26.0 22.0

All property

15.3 14.1 17.5 5.1 13.7 11.2 10.6 9.5 15.1 23.4 30.1 26.7

Source: IPD, 2006

The strong returns achieved for all property sectors from 2003 to 2005 were

driven largely by the substantial reduction in interest rates and the accompanying

reduction of property capitalisation rates. This placed upward pressure on both

yields and capital values.

In 2006, the industrial sector outperformed the market as a whole recording total

returns of 31.1%, (this takes into account both capital growth and income

return). Although the strengthening of the Rand has continued to negatively

EThekwini Property Market Review 2007/2008

0046/07/FV Page 13 24/10/2007

impact on this sector, investors in this sector of the market continue to search for

land with appropriate infrastructure. But generally, it is the retail sector that

outperformed the market in recent years, on the back of declining interest rates.

Recent figures suggest that whilst the performance of the retail and industrial

sectors retracted somewhat in 2006 the performance of the office sector remained

stable.

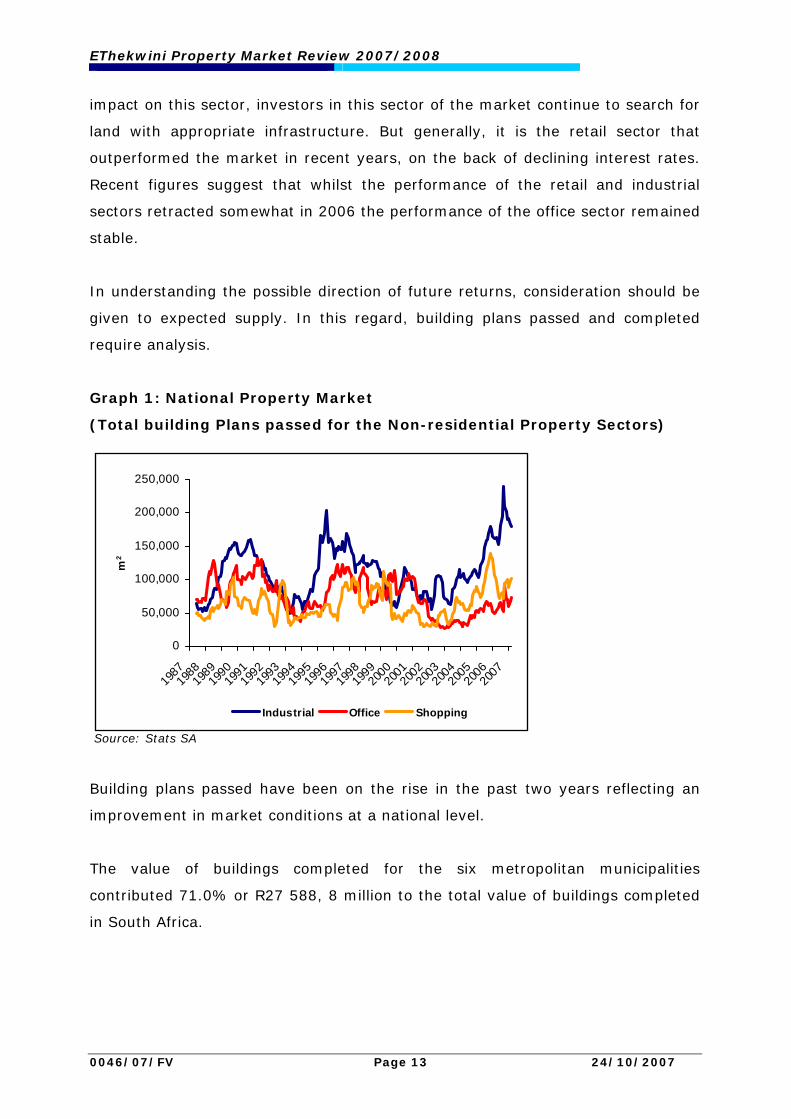

In understanding the possible direction of future returns, consideration should be

given to expected supply. In this regard, building plans passed and completed

require analysis.

Graph 1: National Property Market

(Total building Plans passed for the Non-residential Property Sectors)

Source: Stats SA

Building plans passed have been on the rise in the past two years reflecting an

improvement in market conditions at a national level.

The value of buildings completed for the six metropolitan municipalities

contributed 71.0% or R27 588, 8 million to the total value of buildings completed

in South Africa.

0

50,000

100,000

150,000

200,000

250,000

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

m2

Industrial Office Shopping

EThekwini Property Market Review 2007/2008

0046/07/FV Page 14 24/10/2007

A comparison of building plans completed in 2005 and 2006 shows that:

240,319 sqm of non-residential space was completed in 2006.

The industrial sector was responsible for 64% of total building activity,

followed by the office sector (19.89%) and shopping sector (16.36%).

The Durban-North, South and central areas showed no building activity growth

in 2006, while the Outer West operational area saw a growth of 6.51% largely

driven by the shopping sector.

The South operational sector saw a 0.38% growth in building activity driven by

the industrial sector.

This is summarized in the table below.

Table 2: Building Plans Completed for the eThekwini Municipality

Building Plans Completed - (Sqm) eThekwini Municipality 2005 2006 2005 2006 2005 2006 2005 2006

Office Shopping Industrial Total %

Chng Durban - North, South Central 11,092 7,844 26,465 17,625 114,262 83,477 151,819 108,946

-0.28

Inner West Operational 14,404 22,531 - 389 22,709 18,415 37,113 41,335 0.11 North - Operational 40,017 17,424 8,358 14,546 11,987 16,249 60,362 48,219

-0.20

Outer West Operational 899 - - 6,755 - - 899 6,755 6.51 South Operational 1,055 - 759 - 23,573 35,064 25,387 35,064 0.38

275,580 240,319 -

0.13

Source: Stats SA

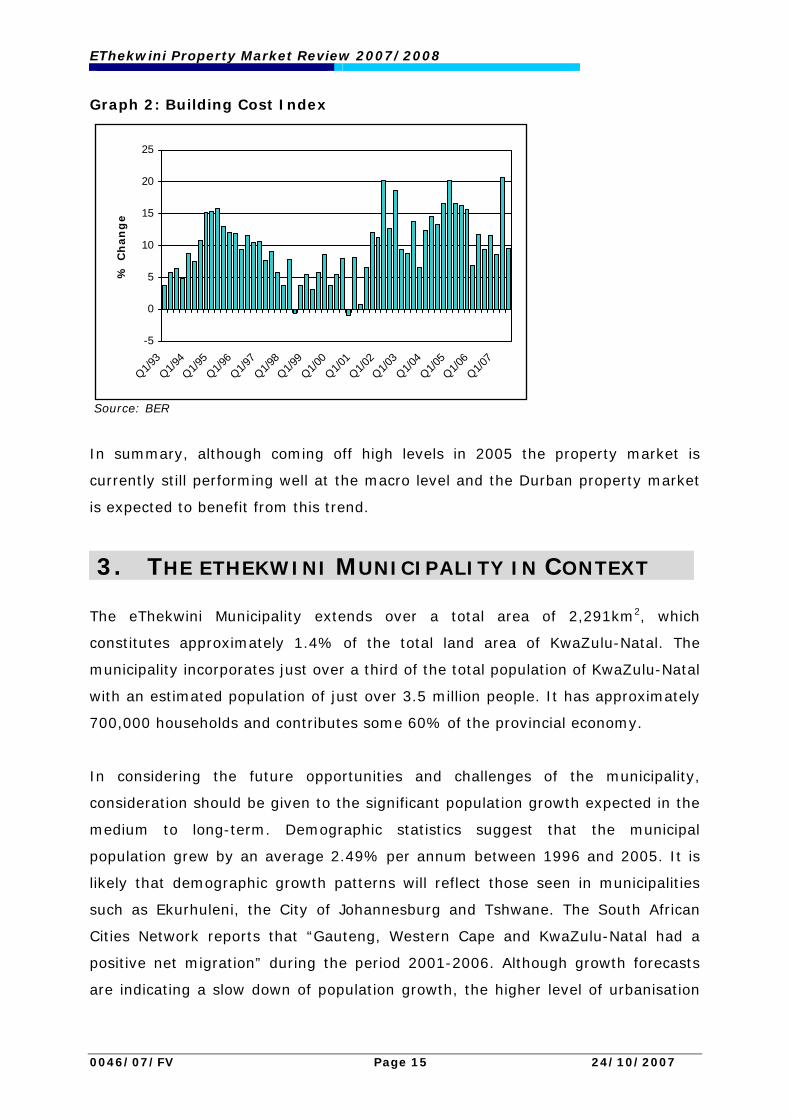

The building sector is also taking cognisance of rising building costs which could

affect the future viability of projects and the forecasts for future growth in

building activity. See graph 2.

EThekwini Property Market Review 2007/2008

0046/07/FV Page 15 24/10/2007

Graph 2: Building Cost Index

Source: BER

In summary, although coming off high levels in 2005 the property market is

currently still performing well at the macro level and the Durban property market

is expected to benefit from this trend.

3. THE ETHEKWINI MUNICIPALITY IN CONTEXT

The eThekwini Municipality extends over a total area of 2,291km2, which

constitutes approximately 1.4% of the total land area of KwaZulu-Natal. The

municipality incorporates just over a third of the total population of KwaZulu-Natal

with an estimated population of just over 3.5 million people. It has approximately

700,000 households and contributes some 60% of the provincial economy.

In considering the future opportunities and challenges of the municipality,

consideration should be given to the significant population growth expected in the

medium to long-term. Demographic statistics suggest that the municipal

population grew by an average 2.49% per annum between 1996 and 2005. It is

likely that demographic growth patterns will reflect those seen in municipalities

such as Ekurhuleni, the City of Johannesburg and Tshwane. The South African

Cities Network reports that “Gauteng, Western Cape and KwaZulu-Natal had a

positive net migration” during the period 2001-2006. Although growth forecasts

are indicating a slow down of population growth, the higher level of urbanisation

-5

0

5

10

15

20

25

Q1/93

Q1/94Q1/9

5Q1/9

6Q1/9

7Q1/9

8Q1/9

9Q1/0

0Q1/0

1Q1/0

2Q1/0

3Q1/0

4Q1/0

5Q1/0

6Q1/0

7

% C

han

ge

EThekwini Property Market Review 2007/2008

0046/07/FV Page 16 24/10/2007

in the province is expected to provide new challenges for the local property

market. It can be argued that demand for residential land will intensify, resulting

in a growing contention whether land should be used for commercial or residential

purposes.

3.1 THE ECONOMY

The eThekwini Municipality is home to South Africa‘s largest and busiets port and

the second largest industrial hub after Gauteng.

Durban plays an important role as the trade route for export and import industries

in South Africa, especially from eastern markets.

The main access route to the municipality is via the N2 freeway, which links the

municipality to the southern regions of the Eastern Cape and the northern regions

towards Mpumalanga. The N3 freeway is a direct link between the municipality

and neighbouring Pietermaritzburg as well as to the Western provinces – directly

leading to the Johannesburg market.

The Integrated Development Plan (IDP) Review of 2007/2008 indicates that the

City’s economic growth rate has performed increasingly well over the past few

years and is currently growing at a rate of 5.3% per annum, which is well in

excess of the national average . However, this is tempered by a need to double

per capita income, which experienced decline from 1990 through 1999. Currently

the City’s per capita income is R34 875 per annum, being higher than the South

African average at R17, 756. The municipality has set an economic growth target

of 7.5% being a suggested target required to address the creation of 18, 000 new

jobs before 2010 and to achieve the city’s strategic vision.

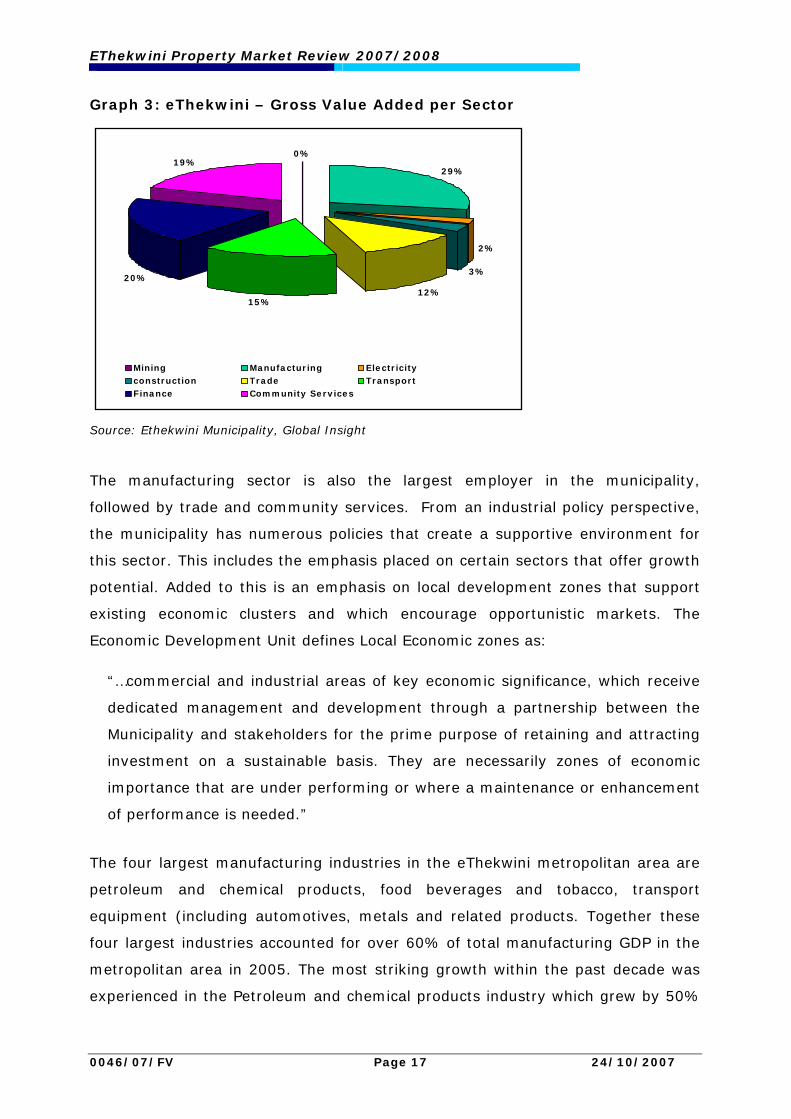

In considering the structure of the local economy; manufacturing, tourism,

finance and transport are the major economic contributors to the local economy,

with the manufacturing sector playing a dominant role; this is illustrated in the

graph below.

EThekwini Property Market Review 2007/2008

0046/07/FV Page 17 24/10/2007

0%

29%

3%

12%15%

19%

2%

20%

Mining Manufacturing Electricityconstruction Trade TransportFinance Community Services

Graph 3: eThekwini – Gross Value Added per Sector

Source: Ethekwini Municipality, Global Insight

The manufacturing sector is also the largest employer in the municipality,

followed by trade and community services. From an industrial policy perspective,

the municipality has numerous policies that create a supportive environment for

this sector. This includes the emphasis placed on certain sectors that offer growth

potential. Added to this is an emphasis on local development zones that support

existing economic clusters and which encourage opportunistic markets. The

Economic Development Unit defines Local Economic zones as:

“…commercial and industrial areas of key economic significance, which receive

dedicated management and development through a partnership between the

Municipality and stakeholders for the prime purpose of retaining and attracting

investment on a sustainable basis. They are necessarily zones of economic

importance that are under performing or where a maintenance or enhancement

of performance is needed.”

The four largest manufacturing industries in the eThekwini metropolitan area are

petroleum and chemical products, food beverages and tobacco, transport

equipment (including automotives, metals and related products. Together these

four largest industries accounted for over 60% of total manufacturing GDP in the

metropolitan area in 2005. The most striking growth within the past decade was

experienced in the Petroleum and chemical products industry which grew by 50%

EThekwini Property Market Review 2007/2008

0046/07/FV Page 18 24/10/2007

in the past seven years. The automotive industry in the metropolitan area and in

the province is based around the output of the Toyota SA plant in Prospecton.

Toyota South Africa is the country’s biggest car producer with the largest

domestic market share.

These interventions are complemented with spatial incentives such as the recently

initiated Urban Development Zones (UDZ’s) which aim at stimulating property

investments in demarcated areas – UDZ’S details will be discussed in later

sections of the report.

The services sector, more specifically finance, business and real estate; wholesale

and retail trade and transport and communication have grown in relative

importance. The eThekwini Municipality reflects the largest share of the national

transport and communication industry of any single metropolitan area in South

Africa.

It is estimated that the informal sector in Durban employs approximately 25% of

the municipal labour force. This is equivalent to approximately 300,000 people,

and the challenge lies in formulating industrial and urban development policies

that support this sector of the market, and here the built environment has a role

to play.

The ward workshops held during the previous IDP review (2005/2006) process

indicated that households in the municipality were most in need of:

Housing and household services;

Safety and security;

Jobs/economic development;

Community infrastructure;

Health services;

Governance issues;

Transport;

Education and

Social issues and employment opportunities

This collates with information collected through the Municipality’s annual Quality

EThekwini Property Market Review 2007/2008

0046/07/FV Page 19 24/10/2007

of Life Survey referred to in the 2007/2008 review. This survey indicates that the

problems that are of most concern to residents are:

Poverty

Unemployment

Crime and feeling unsafe

Health problems

In addition the spatial analysis of needs has indicated that communities who are

worse off are located in the historically under-invested township areas where a

great deal of informal dwelling infill has occurred, and similarly that communities

on the rural periphery have the lowest level of service access. The future of the

property market will to a degree lie in improving the townships and integrating

these areas in the overall economy.

Thus, the challenges faced by the eThekwini municipality include the need to

strengthen its economic base and creating conditions that will translate in

improved socio-economic conditions for all. The key challenges to development

are identified as being:

Low economic growth and high unemployment

Poor access to basic household services;

High levels of poverty;

Low levels of literacy and skills development;

HIV/AIDS;

Crime

Unsustainable development practices and,

Ineffective and inward looking local government

Responding to these needs, the long-term development framework for the city

aims to accomplish a balance between meeting basic needs, strengthening the

economy and building appropriate human skills. More specifically, this translates

into interventions that stimulate:

Sustainable economic growth and job creation;

Fully serviced, well-maintained, quality environments;

EThekwini Property Market Review 2007/2008

0046/07/FV Page 20 24/10/2007

Safe and secure environments;

Healthy and empowered citizens;

Embracing culture diversity;

Sustaining the natural built environment and

Democratising local government.

South Africa has experienced a tourism boom since the 1990’s. KwaZulu-Natal

has the largest number of trips from domestic tourists in the country and is

capturing a growing share of international tourism. In 2005, KwaZulu Natal

attracted 11.6 tourism trips – 32% share of the South African Tourism Market.

The municipality was visited by 1.1 million foreign tourists or approximately 16%

of foreign tourists in South Africa. The municipality’s significant source markets

are from Africa (56%) and Europe (33%). The Durban hotel market is the third

most important in South Africa, after Cape Town and Johannesburg.

Looking ahead, the municipality wishes to stimulate economic growth in key

activity sectors aligned with the KwaZulu- Natal Industrial Development Strategy,

namely the automotive sector, ICT, tourism, agriculture and agri-processing,

chemicals, creative industries, clothing and textiles, and wood, pulp and paper.

With the maritime sector playing an important role in the local economy, this

sector will also receive strong focus.

The development of the King Shaka International Airport and Dube Trade Port,

together with its proposed Free Trade Zone, is the most important economic

project for the region and is projected to provide between 150 000 to 240 000

direct and indirect job opportunities.

3.2 THE NODAL PROPERTY MARKET

The Durban property market expanded from the traditional Central Business

District (CBD) focussed around the port. With time the city developed to the

south, the west, and more recently to the northern regions of the municipality.

The eThekwini Municipality area forms the consolidation of a number of areas that

previously functioned as separate local authority areas. Historically the CBD has

EThekwini Property Market Review 2007/2008

0046/07/FV Page 21 24/10/2007

played the role of a traditional service centre to the municipal region with most

offices and retail outlets situated in the node. Secondary commercial nodes

developed in relation to this centre and included commercial developments on the

Berea, which attracted some of the first commercial nodes outside of the CBD. To

this can be added Westville, Pinetown, Kloof and Hillcrest further to the west

Durban North, and line suburbs in the south. Pinetown/New Germany has been

historically important as an industrial node. Umhlanga and Amamzimtoti are two

coastal nodes respectively north and south of the CBD which historically

performed a service and tourism function. The Southern nodes are primarily of an

industrial nature and are located around the development of the port and the

airport. In addition a number of township areas were developed as a result of

apartheid spatial organisation. These include Umlazi and Chatsworth in the south

and Phoenix and KwaMashu in the North.

Growth in the past decade has consolidated to the north of the CBD with the

creation of a significant commercial cluster, which includes the commercial nodes

of La Lucia/Umhlanga and Mount Edgecombe. Industrial nodes located in this

northern region include Briardine, Springfield Park, Umgeni and the fast

developing Riverhorse Valley Business Estate.

The important point is that these different functional areas largely complement

each other and offer different opportunities for tenants and property investors

alike.

Thus, the main property market nodes of the Durban Metro can be broadly

divided into the following functional areas:

Table 3: The Nodal Property Market

Node Areas

CBD Durban CBD

Central nodes Berea, Musgrave and other centrally located commercial nodes.

Western nodes Westville, Pinetown, including industrial nodes such as New

Germany, West and Mahogany Ridge, Cato Ridge, etc.

Northern nodes Umhlanga/La Lucia Ridge. Mount Edgecombe, Briardine,

Springfield Park, Riverhorse Valley Business Estate.

EThekwini Property Market Review 2007/2008

0046/07/FV Page 22 24/10/2007

33..22..11 TTHHEE DDUURRBBAANN CCBBDD

The Durban CBD was the first major commercial node established in eThekwini.

Like other major CBD’s in South Africa, the decentralisation of commercial

property developments have in recent decades negatively impacted on CBD

vacancy rates and property values. The characteristic of investors in this market

has also changed with smaller, private investors, playing a more pronounced role.

The positive impacts of urban regeneration initiatives are starting to be felt with

vacancies declining and investors showing greater interest in investment

opportunities. A further positive trend has been the rise in the number of

renovations seen in the CBD, with investors taking advantage of Urban

Development Zone (UDZ) fiscal advantages. Of importance is that ABSA, a

leading financial bank has relocated its operations and consolidating most of their

current decentralised departments to the CBD on Smith and Gardiner Street.

The retail sector continues to play a critical role in the CBD, serving different

income groups, and anchoring the property market; the retail offering is also

highly accessible to shoppers without private transport. The Workshop and the

Wheel Shopping Centres are important shopping destinations in this node, but

street level retail in much of the CBD plays a critical role.

The CBD office sector caters both the private and public

sectors with the movement of the province. While the

public sector plays an important role in maintaining the

market in the CBD, this will be reduced with the

movement of provincial department to Pietermaritzburg.

Micro-locational issues such as the affordability of space, makes it attractive for

tenants to either stay, relocate or expand in the CBD.

In general the CBD shows a shortage of A-grade office space, with by far most of

the rentable office space being in the C-grade category. This is largely related to

the age of buildings, the quality of infrastructure, and perceptions of locality,

when compared to new decentralised nodes. The exit of corporates from the CBD

EThekwini Property Market Review 2007/2008

0046/07/FV Page 23 24/10/2007

is also associated with a shift to private ownership. Parking has also become a

problem in the CBD related primarily to increasing car ownership. This has

stimulated the construction of additional parking in new developments including

part of the redevelopment of the Old Mutual building on Gardiner Street to

provide 857 parking bays in conjunction with a new retail arcade.

Industrial developments extend to the southern nodes of the municipality,

adjacent to the CBD, this also means that the CBD offers industrial space in

relatively close proximity.

The CBD is complemented by recent investment on its

northern edge. While interest in the Kingsmead office park

began slowly, take up has resulted in some of the last

available sites reaching the R1000/m² mark. Although

effectively an office park development, it tends to complement

the offering of the CBD. Also on the northern edges of the

CBD is the Durban ICC, a premier convention centre that has

recently undergone a major extension with the development

of the ICC Arena. These and other initiatives, suggest that the Durban CBD

continues to offer a vibrant property market offering both commercial and

residential opportunities. Such opportunities are being strengthened by urban

regeneration policies such as the Urban Development Zone Tax Incentives (to be

discussed later in the report).

A number of key events may influence the future of the CBD.

Increasing traffic congestion, particularly in the north and potentially around

other nodes, may result in a shift back towards the centre;

Rising income levels and increased investment keen to service township areas

may negatively affect CBD rejuvenation;

The success of strategic projects within the Inner City may unlock further

investment;

Land shortage and environmental pressure on new “greenfield” developments

means that in future developers will target land that has already been

developed, encouraging new developments or renovations in the CBD.

EThekwini Property Market Review 2007/2008

0046/07/FV Page 24 24/10/2007

33..22..22 TTHHEE CCEENNTTRRAALL NNOODDEESS

The central node comprises the Berea and adjacent areas. The Berea comprises a

number of nodal areas that have typically concentrated around shopping centres

with the retail sector playing an important role. The Berea has a strong upper

income residential component, which acts as a critical anchor, especially for the

retail sector. The Berea is readily accessible through N3 via Berea Road, and is

well linked with the city centre and the western suburbs such as Westville.

The Musgrave Centre was developed in 1956 and has

since been an important retailing facility in the Durban

market, and has generated commercial growth along

Musgrave and Essenwood Roads and is relatively

central on the Berea.

Musgrave Road provides a link with the Florida Road strip to the north, which

operates in conjunction with Windermere, Stamfordhill, and Umgeni roads to

provide a mix of office, hospitality, discount and high end retail, and light

industrial activity in close proximity to each other. There has been strong demand

for office and retail space to locate here in recent years. Most of these

are converted homes.

Since the availability of land on the Berea is limited, new developments are more

likely to occur through renovations and the conversion of residential to office

space. However, high property prices being demanded for residential property on

the Berea may however, have started to affect the viability of this.

Davenport Centre, south of Berea Road and close to the residential area of

Glenwood, has also encouraged the incremental concentration of commercial

development in its environs.

Recent new major renovations include a refurbishment of

the Price WaterHouseCoopers Building. The Berea Centre

is also due for renovations into a retail and residential

EThekwini Property Market Review 2007/2008

0046/07/FV Page 25 24/10/2007

mixed-use development, involving the conversion of 4, 620 m² in its office

tower to residential use. The Berea centre has a few vacancies but tenants such

as as Pick ‘n Pay, PEP, a gymnasium and the Millenia School of Business are still

operating in the centre.

33..22..33 TTHHEE WWEESSTTEERRNN NNOODDEESS

Westville, in the western sector of the Durban metropolitan region, is

characterised by a mixture of residential and dispersed commercial uses. Direct

access to Westville is via the N3 highway, and the M13 Jan Smuts Highway. The

node is also highly accessible from and to the Berea, the Durban CBD, and the far

western commercial Pinetown node.

The office sector in Westville comprises a number of

relatively dispersed office parks. Generally the node has

developed as a decentralized commercial node. Prime

office developments include the Westway Office Park,

located off the St. James Road off-ramp, on the N3.

Examples, of other office nodes in the Westville area are

Derby Downs and Essex Terrace Tenants in such

developments tend to be medium-sized and include IT

companies, advertising agencies, and professional

practices. Essex Terrace for example offers B-grade

office space and rentals are more competitive than at

found and Westway and Derby Downs.

Notable national tenants include:

In Essex Terrace, tenants include the Masters Builders Association and Old

Mutual Properties.

In Derby Downs, the office developments comprise low-rise office parks which

houses tenants such as Discovery, Odyssey, Verimark and Harbour Marine

Group.

Westway, which includes tenants such as Dimension Data, Pick ‘n Pay, Murray

EThekwini Property Market Review 2007/2008

0046/07/FV Page 26 24/10/2007

& Roberts and Santam. Four new office developments are occurring within the

Westway node.

A small office node, which consists of office parks, has also developed next to the

Westville Mall on Buckingham Terrace Road and includes tenants such as Business

Partners and WSP.

The Pavilion Shopping Centre is the main shopping centre in the region - it is

100’000m2 in extent and serves a wide catchment area. The centre is currently

completing nearly 4’000m² of extensions. The Westville CBD is also characterised

by a variety of convenience retail facilities, giving the node a “village” feel.

Market commentators suggest that Westville is facing

stiff competition from Umhlanga as a commercial and

retail node – but, at the same time there is a view that

Westville has relatively low levels of traffic congestion

compared to that experienced in Umhlanga/La Lucia

which should underpin its place in the market.

Pinetown offers a commercial node at the far western extremity of the

municipality. The Pinetown CBD is accessed from the N3 via the St John’s Avenue

off ramp. The Old Main Road is the main activity spine for commercial property in

the node and nearby industrial nodes include New Germany, Mahogany Ridge and

Westmead.

Land uses found in the node include commercial developments as well as civic

uses. Car dealerships for various car manufacturers including Toyota, Renault,

BMW and Mercedes Benz are situated along the main road. Other uses include

semi-industrial activity selling building products to the public.

Retail facilities include the Sanlam Centre with tenants such as Game, Pick ‘n Pay,

Woolworths and Clicks. A new retail development is also being built on Kings

Road.

EThekwini Property Market Review 2007/2008

0046/07/FV Page 27 24/10/2007

In terms of industrial nodes, New Germany is one of

the more developed and older industrial nodes in

Durban. New Germany is made up of four distinct

areas, namely North Industria, Pineside, Falcon

Industrial Park and Mountain Ridge, which is adjacent

to the New Germany Nature Reserve. The wider node

is characterised by a variety of light manufacturing activities including, inter alia:

foods, textiles, metals, machinery, automotive components, paints, chemicals and

pharmaceuticals.

Westmead and Mahogany Ridge to the west offer light

industrial and distribution uses. To this should be added

warehousing and packaging and logistics related

services tenants in Westmead include MAN Truck and

Euro Steel. The older part of Westmead includes tenants

such as Hi Q; Nissan; Waltons; GSA (Glass South Africa)

and Shatterprufe.

Suitable vacant land in these areas and particularly the more developed

Westmead node is scarce. In these areas land may be expected to fetch

R 850/m².

The industrial sites are well serviced with generally good accessibility to the N2.

The next push for industrial land appears to be taking place further west with lots

of interest being directed toward Cato Ridge, in particularly, with current land

owners driving the process of delivering industrial land to the market. The local

authority has experienced significant pressure both in terms of rezonings and the

take up of zoning rights in the outer west. Cato Ridge however suffers from an

underdeveloped infrastructure, including the need for a sewerage works, poor

accessibility and remoteness. The outer west also contains much of Durban’s

sensitive environmental assets.

EThekwini Property Market Review 2007/2008

0046/07/FV Page 28 24/10/2007

33..22..44 TTHHEE NNOORRTTHHEERRNN NNOODDEESS

The Umhlanga node is located to the north of Durban. It

is a growing office node concentrated on the eastern and

western sides of Umhlanga Rocks Drive. The node has a

strong residential base, which has grown significantly in

recent years due to new residential developments driven

by lifestyle choice, and which simultaneously has been

complemented with retail and office developments.

In close proximity, the La Lucia Ridge Office Estate has

become Durban’s premier decentralised office location.

It attracts blue-chip companies, and includes companies

in the financial sector such as Deloitte & Touche,

Alexander Forbes, Ernst and Young. To this list one can

add Cell C and Unilever.

New and recent office developments include:

Lot 65 Sinembe Park – approximately 2,241m²;

Park 9 – approximately 920m²;

Park 10 – approximately 1,020m²; and

92 Armstrong Avenue.

Shortages in prime office space have resulted in the resale of sea-facingland to be

used for offices, for an approximate value of R3000/m².

Looking at the municipal area as a whole, the Umhlanga/La Lucia node has shown

rapid commercial and upmarket residential take up. A large proportion of

relocations of companies from the Durban CBD have been absorbed in this

market. The 110,000m2 Gateway shopping and entertainment centre situated in

the node is the fourth largest shopping centre in the country after Sandton City

(127,380m²) in Sandton, Gauteng; Canal Walk (125,000m²) in Milnerton,

Western Cape and Menlyn Park Shopping Centre (115,000m²) in Tshwane,

Gauteng. The Gateway centre is to undergo additional expansion of its south mall

EThekwini Property Market Review 2007/2008

0046/07/FV Page 29 24/10/2007

with an addition of 7, 900m². There is also still demand for retail space around

the centre as indicated by the location of the Mr. Price Sports on a stand-alone

site on Umhlanga Rocks Drive.

Office developments in Umhlanga are characterised by low-bulk and landscaped

office parks which has a relatively high owner-occupancy compared to rented

stock. Numerous car dealerships have located in the node to benefit from the

relatively affluent demographic characteristics of the node.

The Umhlanga New Town Centre is a project envisioned to enhance the

attractiveness of the node and to anchor developments around it. The new town

centre is a mixed-use development built around a series of squares, parks and

boulevards surrounding the Gateway Theatre of Shopping. The precinct is one of

the largest property development projects in South Africa.

Umhlanga Ridge and La Lucia Ridge Office Estate are the premier destination for

corporates in KwaZulu-Natal who are prepared to pay higher prices for the

strategic location with good exposure and accessibility. The ridge is also the

location for the proposed development of the remaining 140 ha sea-facing site

known as the Umhlanga Triangle. This would involve the delivery of 100 000m² of

land for prime office space through the development of Ridgeside Office Park as

part of the first phase of development.

Further north of the La Lucia Ridge office node is a smaller office node in Mount

Edgecombe, which is a strip of office developments with tenants such as MTN,

Barloworld, Illovo Sugar and SARS. Car dealerships are also common in this

location.

The industrial sector in the northern regions is located off

the N2 freeway along both the Umgeni and Inanda Roads,

and includes established nodes such as Springfield Park,

Umgeni and Briardene and also includes the fast growing

River Horse Valley Business offering prime industrial land

with good highway accessibility and exposure and

includes tenants, which require

EThekwini Property Market Review 2007/2008

0046/07/FV Page 30 24/10/2007

distributions and warehouse space such as Mr Price, Tren Tyre, Gestetner,

Mercedes Benz, Berco Express and Xerox. On completion Riverhorse Valley will

comprise a 160ha industrial business park consisting of separate mixed-use

business parks. Riverhorse Valley has experienced significant exponential increase

in value as stock levels have decreased. The recent sale of a property in July with

an elevated platform of 1,6852 ha, and excellent access on to the N2 was

reported to have reached a price in the order of R 1, 700/m² for net platform

area.

Further from the Umgeni Road off-ramp are established

nodes such as Briardene, located mainly along North

Coast Road. These nodes consist of mainly tenants who

require warehousing and light manufacturing space.

There are also some high levels of industrial

developments in this node.

The Umgeni node, which is an older node, includes a high component of retailing

– typically wholesalers and value centres with tenants such as Furniture City, Dial

a Bed, Duratile, Hisrch’s, Waltons and Panasonic found in this location. A recent

property sold here, based on net platform area, for in the order of R 950/m².

The movement of commercial property in the north will likely be influenced by the

development of the new airport and the Dube tradeport on the La Mercy site, and

which is intended to be completed by 2010. It is likely that industrial demand for

land will move further north in conjunction with these developments.

However, take-up of industrial land released in Ballito adjacent to the N2, outside

the metro has to date been slow.

33..22..55 TTHHEE SSOOUUTTHHEERRNN NNOODDEESS

The southern nodes of Durban are accessible via the N2 freeway and the M4.

These access routes also offer excellent accessibility to the South Coast holiday

EThekwini Property Market Review 2007/2008

0046/07/FV Page 31 24/10/2007

resorts. The southern nodes cater for a diversity of income groups, from families

living in Umlazi to those residing in upmarket apartment blocks.

Amanzimtoti offers a vibrant high street, which runs

parallel to the beach. The CBD attracts national tenants

and businesses and it serve as a commercial centre for

the southern regions of the municipality. Examples of

tenants include banks, real estate businesses, doctors

and lawyers.

Shopping centres in the Amanzimtoti area include the Seadoone Mall, anchored by

Clicks and Checkers and the Amanzimtoti Sanlam Centre.

The expansion of the Amanzimtoti CBD has been

constrained by physical factors such as the coast, the

Amanzimtoti River, the railway line to the west of the CBD,

and the N2 freeway. The Spatial Development Framework

for eThekwini recognises the importance of Amanzimtoti as

a major commercial centre of the south of the municipal

area and its ability to serve areas such as Umlazi.

A major retail, commercial and residential development is proposed around

Umbogintwini Village, near Amanzintoti with the release of 93 hectares of land by

AECI to developers.

The South Durban Basin (SDB) is one of the main established industrial nodes in

Durban property sector. The industrial nodes that make up the South Durban

Basin are located south of the Durban International Airport (DIA). The Industrial

nodes include Prospecton, Isipingo and Umbogintwini.

The dominant industrial location in the southern region lies between the Durban

Port and Airport, with activities such as shipping and engineering, warehousing,

and logistics companies. With the view that the airport will be relocated to La

Mercy, there is an expectation that in due course there will be a substantial

release of land (300 ha developable) into the industrial market. The eThekwini

EThekwini Property Market Review 2007/2008

0046/07/FV Page 32 24/10/2007

Municipality is currently reviewing the impact of the relocation of the airport in the

Spatial Development Plan for this region. Likewise, there is a good chance that

the land may be purchased by Transnet and land banked while feasibility over a

dugout port is considered.

Other important industrial activities include motor-related

businesses. Toyota SA has a large presence in the area and

has attracted relates services to support the manufacturing

of motor vehicles. A Durban Auto Supplier Park is also under

consideration. In general, Toyota is an important anchor for

the node. Other industrial activities include manufacturing of paper, plastic

processing, wood and furniture and chemicals. Mondi, a major paper

manufacturer, is also an important tenant in the SDB.

The South Durban Basin (SDB) is also characterised by relatively heavy, older

industrial areas if compared to prime nodes in the western and northern areas of

the municipal area.

The most notable development in the node is the 127ha

Southgate Business Park. The main investors and tenants

at Southgate Business Park include Old Mutual, Volvo

South African Transport Industries, Aunde Car Trim, Auto

Carriers, Standers Transport, Royal Swazi Distillers, Celtic

Freight and Siyaphambile Transport.

3.3 THE SIZE OF THE COMMERCIAL MARKET

An attempt to quantify the size of the Durban property market is made difficult

due to a lack of reliable data. The accuracy of data also varies from one sector of

the market to the next.

SAPOA (the South African Property Owners Association) and the South African

Council of Shopping Centres provide statistics that provide an estimate of the size

of the office and retail markets for various nodes in the study area.

EThekwini Property Market Review 2007/2008

0046/07/FV Page 33 24/10/2007

According to the SAPOA Office Vacancy Survey the distribution of office space in

Durban’s major nodes is as follows;

Table 4: Size of the Office Market in m²

Type of Space Durban CBD Berea Westville Umhlanga/La

Lucia

P-grade 8,298

A-grade 114,038 31,596 54,784 143,879

B-grade 140,689 37,817 76,590 22,932

C-grade 433.446 24,452 0

Total 688,123 93,865 131,374 175,109

Source: SAPOA, 2007

The table illustrates that the greatest concentration of office space in the

municipal area lies in the Durban CBD. However, the bulk of this is C-grade type

accommodation, with comparison with previous data indicating a general

degrading of B-grade space into C-grade space. Although the CBD offers the

highest concentration of office stock in Durban at 688,123m² in total office stock,

this is down from 709,334m² in 2005. In the case of premier grade office space

and A-grade office space, a high concentration is found in the Umhlanga/La Lucia

node with 86% of office space in this node in these categories - The CBD and

Berea also offer a significant amount of lower (B and C) grade space with the

trend of B-grade space degrading to C-grade also evident here. This suggests that

improvement in market conditions could in due course offer opportunities for

renovations.

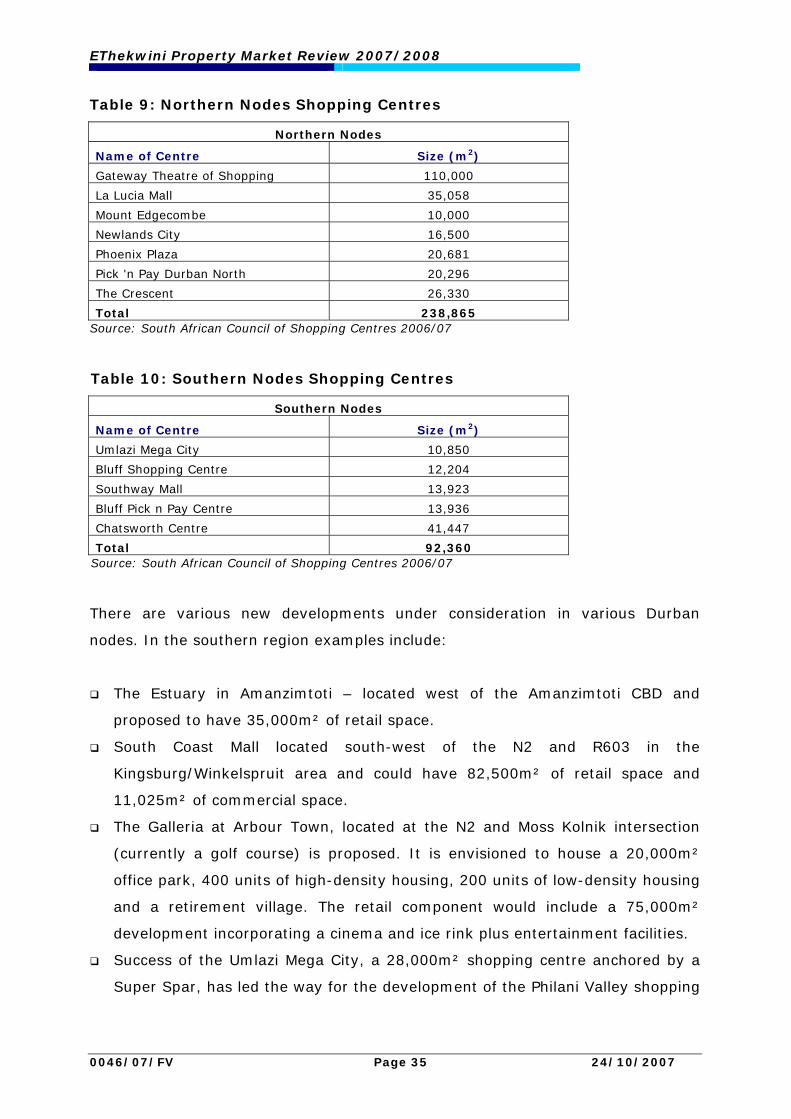

In terms of the concentration of shopping centres, the northern nodes stand out

with approximately 238,865 m², followed by the Western nodes at 221,757m².

This data does not take into account freestanding retailers or street front retail

properties, which are found mainly in the Durban CBD and smaller CBD centres

such as Pinetown and Amanzimtoti. Shopping centres smaller than 10’000 sqm

have also been excluded.

EThekwini Property Market Review 2007/2008

0046/07/FV Page 34 24/10/2007

Table 5: The Size of the Shopping Centre Sector

Durban CBD Central

nodes

Western

nodes

Northern

nodes

Southern

nodes

Total space 50,295 161,281 221,757 238,865 92,360

Source: South African Council of Shopping Centres 2006/7

The distribution of shopping centres is highlighted in the Tables 7 to 11 below.

Table 6: Durban CBD Shopping Centres

Durban CDB

Name of Centre Size (m2)

The Wheel Shopping Centre 20,216

The Workshop 20,079

Ushaka Village Walk 10,000

Total 50,295 Source: South African Council of Shopping Centres 2006/07

Table 7: Central Nodes Shopping Centres

Central Nodes

Name of Centre Size (m2)

Game City Grayville 42,370

Musgrave centre 32,122

New Berea Centre 21,877

Overport City 26,727

The Home Centre Springfield 18,298

Value Centre Springfield 19,887

Total 161,281 Source: South African Council of Shopping Centres/2006/07

Table 8: Western Nodes Shopping Centres

Western Nodes

Name of Centre Size (m2)

The Pavillion - Westville 108,000

Sanlam Centre - Pinetown 38,980

Knowles Centre - Pinetown 15,038

Westville Shopping Centre 12,567

The Village Market 11,143

Malvern shopping Centre 12,203

Waterfall Shopping centre 12,000

Montclair Mall 11,826

Total 221,757 Source: South African Council of Shopping Centres 2006/07

EThekwini Property Market Review 2007/2008

0046/07/FV Page 35 24/10/2007

Table 9: Northern Nodes Shopping Centres

Northern Nodes

Name of Centre Size (m2)

Gateway Theatre of Shopping 110,000

La Lucia Mall 35,058

Mount Edgecombe 10,000

Newlands City 16,500

Phoenix Plaza 20,681

Pick 'n Pay Durban North 20,296

The Crescent 26,330

Total 238,865 Source: South African Council of Shopping Centres 2006/07

Table 10: Southern Nodes Shopping Centres

Southern Nodes

Name of Centre Size (m2)

Umlazi Mega City 10,850

Bluff Shopping Centre 12,204

Southway Mall 13,923

Bluff Pick n Pay Centre 13,936

Chatsworth Centre 41,447

Total 92,360 Source: South African Council of Shopping Centres 2006/07

There are various new developments under consideration in various Durban

nodes. In the southern region examples include:

The Estuary in Amanzimtoti – located west of the Amanzimtoti CBD and

proposed to have 35,000m² of retail space.

South Coast Mall located south-west of the N2 and R603 in the

Kingsburg/Winkelspruit area and could have 82,500m² of retail space and

11,025m² of commercial space.

The Galleria at Arbour Town, located at the N2 and Moss Kolnik intersection

(currently a golf course) is proposed. It is envisioned to house a 20,000m²

office park, 400 units of high-density housing, 200 units of low-density housing

and a retirement village. The retail component would include a 75,000m²

development incorporating a cinema and ice rink plus entertainment facilities.

Success of the Umlazi Mega City, a 28,000m² shopping centre anchored by a

Super Spar, has led the way for the development of the Philani Valley shopping

EThekwini Property Market Review 2007/2008

0046/07/FV Page 36 24/10/2007

centre with a phased total lettable space of 12, 930 m². The centre is 6km

from Umlazi Mega City and also has a Super Spar as anchor tenant.

The Durban property market remains dynamic and is in

flux. Prime nodes have, and continue to develop in the

western and northern areas while newer nodes are also

being built on the periphery of the CBD. These would

include the Point Development and the Kingsmead

node. Section 4 of the report will highlight some of the

property indicators in these nodes.

4. PROPERTY MARKET INDICATORS

This section of the report highlights some of the property indicators for the

different nodes in the eThekwini Municipality. Each geographical location is

discussed separately namely - the Durban CBD, Central nodes, Western nodes,

Northern nodes and the Southern nodes as described in Section 3.

4.1 THE DURBAN CBD

The Durban CBD, vacancy rates have in recent years hovered around the 20%

level. It should be noted that these figures only reflect “A’ and “B” grade

buildings.

EThekwini Property Market Review 2007/2008

0046/07/FV Page 37 24/10/2007

Graph 5: Durban CBD - Office Vacancy Rates

Source: SAPOA, 2007:1

In terms of the rental market, rentals are stable with A-grade rentals averaging

between R50/m² and R55/m², however there are a few properties peaking just

above R60/m² and lower grades of property are achieving rentals below R40/m²

as illustrated in the graph below.

Graph 6: Durban CBD - Gross Office Rentals

Source: Rode’s Report

New office developments at the Point are expected to achieve rentals of about

R75-R85/ m², with these rentals largely being reflective of building costs and

expected yields.

R 15

R 25

R 35

R 45

R 55

R 65

2000

:1

2001

:1

2002

:1

2003

:1

2004

:1

2005

:1

2006

:1

2007

:1

R/

m2

A+ A B C

0%

5%

10%

15%

20%

25%

30%

35%

Q1/90

Q1/91

Q1/92

Q1/93

Q1/94

Q1/95

Q1/96

Q1/97

Q1/98

Q1/99

Q1/00

Q1/01

Q1/02

Q1/03

Q1/04

Q1/05

Q1/06

Q1/07

%

TOTAL GRADE A GRADE B

EThekwini Property Market Review 2007/2008

0046/07/FV Page 38 24/10/2007

The shortage of well located office land, with appropriate infrastructure may, in

the longer term encourage the redevelopment of existing CBD office properties.

For the retail market in the CBD, brokers report that rentals are achievable

between R150/m²and R180/m² at the upper end. Although this sector of the

market offers considerable opportunities, there is growing competition from

shopping centres located in for instance Umlazi.

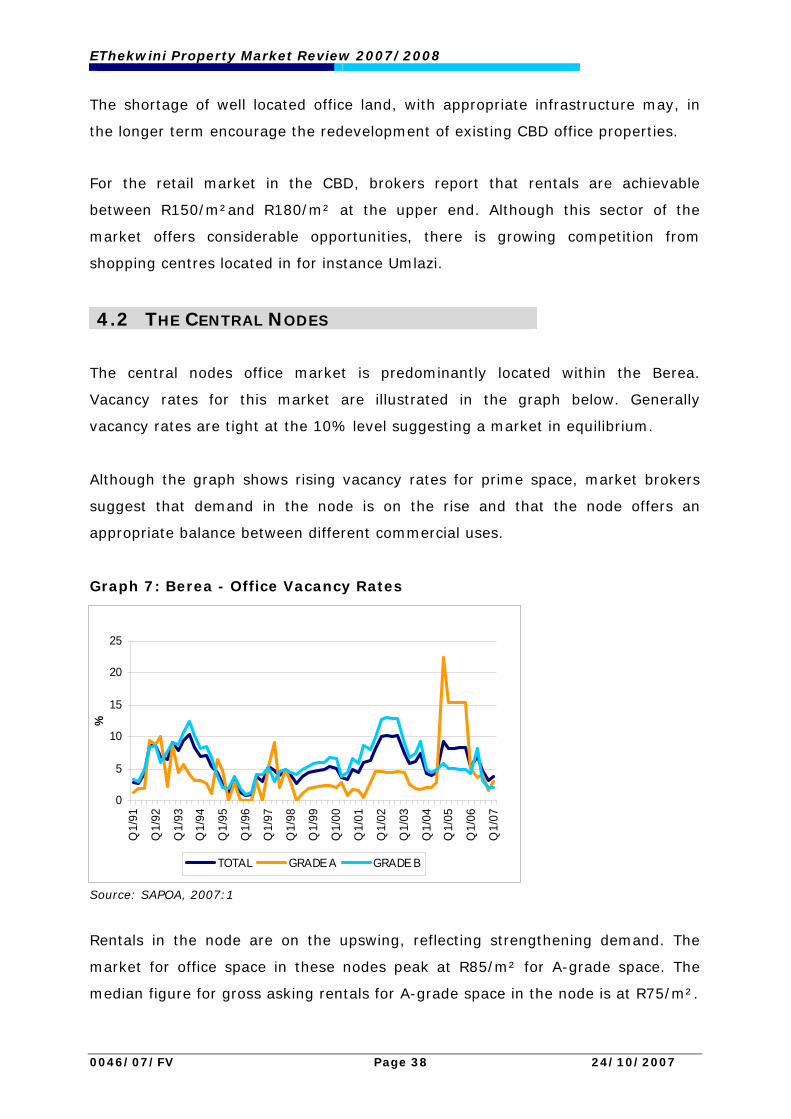

4.2 THE CENTRAL NODES The central nodes office market is predominantly located within the Berea.

Vacancy rates for this market are illustrated in the graph below. Generally

vacancy rates are tight at the 10% level suggesting a market in equilibrium.

Although the graph shows rising vacancy rates for prime space, market brokers

suggest that demand in the node is on the rise and that the node offers an

appropriate balance between different commercial uses.

Graph 7: Berea - Office Vacancy Rates

Source: SAPOA, 2007:1

Rentals in the node are on the upswing, reflecting strengthening demand. The

market for office space in these nodes peak at R85/m² for A-grade space. The

median figure for gross asking rentals for A-grade space in the node is at R75/m².

0

5

10

15

20

25

Q1/

91

Q1/

92

Q1/

93

Q1/

94

Q1/

95

Q1/

96

Q1/

97

Q1/

98

Q1/

99

Q1/

00

Q1/

01

Q1/

02

Q1/

03

Q1/

04

Q1/

05

Q1/

06

Q1/

07

%

TOTAL GRADE A GRADE B

EThekwini Property Market Review 2007/2008

0046/07/FV Page 39 24/10/2007

R 25

R 35

R 45

R 55

R 65

R 75

2000

:1

2001

:1

2002

:1

2003

:1

2004

:1

2005

:1

2006

:1

2007

:1

R/

m2

A+ A B C

Graph 8: Berea - Gross Office Rentals

Source: Rode’s Report

In terms of the retail market, areas such as Musgrave Centre are averaging a

rental of R79/m², although the rental can be significantly higher for smaller, well-

located space.

4.3 THE WESTERN NODES

Official market data suggests that vacancy rates have declined. This is

corroborated by property professionals and brokers reporting on the Western

node market especially in numerous buildings and new developments which are

being undertaken in the at Westway Office Park.

Graph 9: Westville - Office Vacancy Rates

Source: SAPOA, 2007

0%5%

10%15%20%25%

30%35%40%45%50%

Q1/90

Q1/91

Q1/92

Q1/93

Q1/94

Q1/95

Q1/96

Q1/97

Q1/98

Q1/99

Q1/00

Q1/01

Q1/02

Q1/03

Q1/04

Q1/05

Q1/06

Q1/07

%

TOTAL GRADE A GRADE B

EThekwini Property Market Review 2007/2008

0046/07/FV Page 40 24/10/2007

R 10

R 15

R 20

R 25

R 30

R 35

2000

:1

2000

:3

2001

:1

2001

:3

2002

:1

2002

:3

2003

:1

2003

:3

2004

:1

2004

:3

2005

:1

2005

:3

2006

:1

2006

:3

2007

:1

R/

m2

250 500 1,000 2,500 5,000

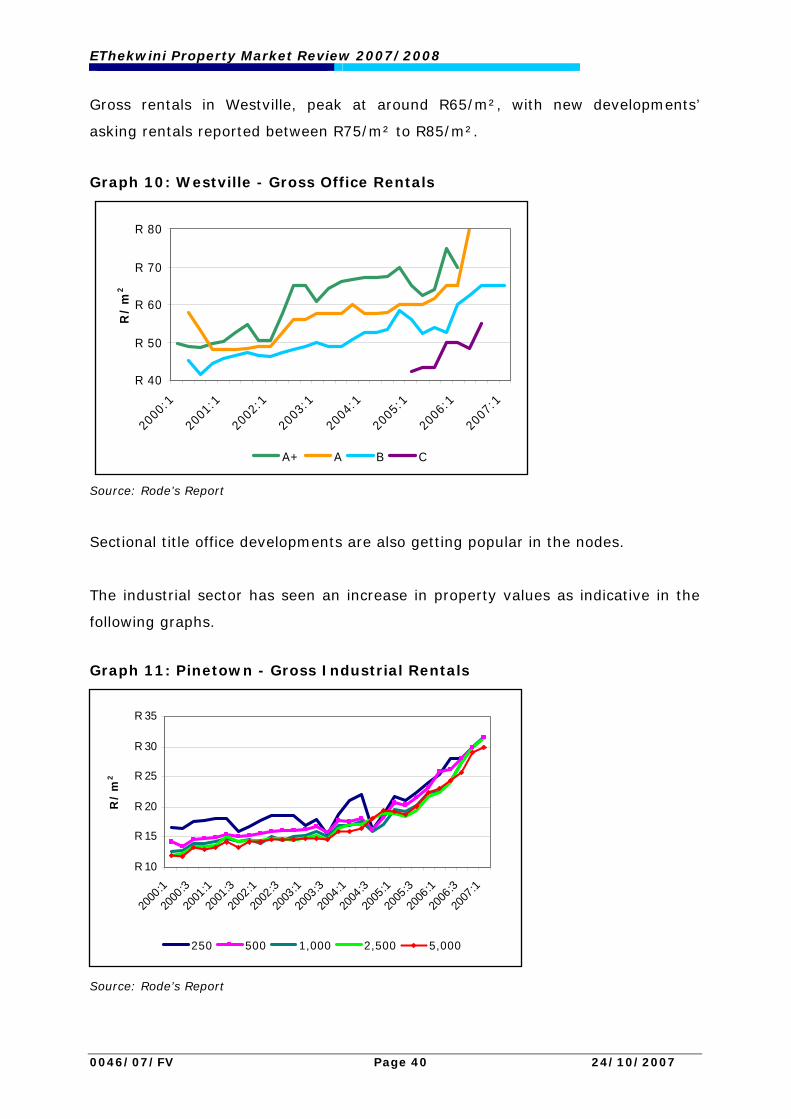

Gross rentals in Westville, peak at around R65/m², with new developments’

asking rentals reported between R75/m² to R85/m².

Graph 10: Westville - Gross Office Rentals

Source: Rode’s Report

Sectional title office developments are also getting popular in the nodes.

The industrial sector has seen an increase in property values as indicative in the

following graphs.

Graph 11: Pinetown - Gross Industrial Rentals

Source: Rode’s Report

R 40

R 50

R 60

R 70

R 80

2000

:1

2001

:1

2002

:1

2003

:1

2004

:1

2005

:1

2006

:1

2007

:1

R/

m2

A+ A B C

EThekwini Property Market Review 2007/2008

0046/07/FV Page 41 24/10/2007

R 10

R 15

R 20

R 25

R 30

R 35

2000

:1

2000

:3

2001

:1

2001

:3

2002

:1

2002

:3

2003

:1

2003

:3

2004

:1

2004

:3

2005

:1

2005

:3

2006

:1

2006

:3

2007

:1

R/m

2

250 500 1,000 2,500 5,000

R 9

R 12

R 15

R 18

R 21

R 24

R 27

R 30

R 33

2000

:1

2000

:3

2001

:1

2001

:3

2002

:1

2002

:3

2003

:1

2003

:3

2004

:1

2004

:3

2005

:1

2005

:3

2006

:1

2006

:3

2007

:1

R/m

2

250 500 1,000 2,500 5,000

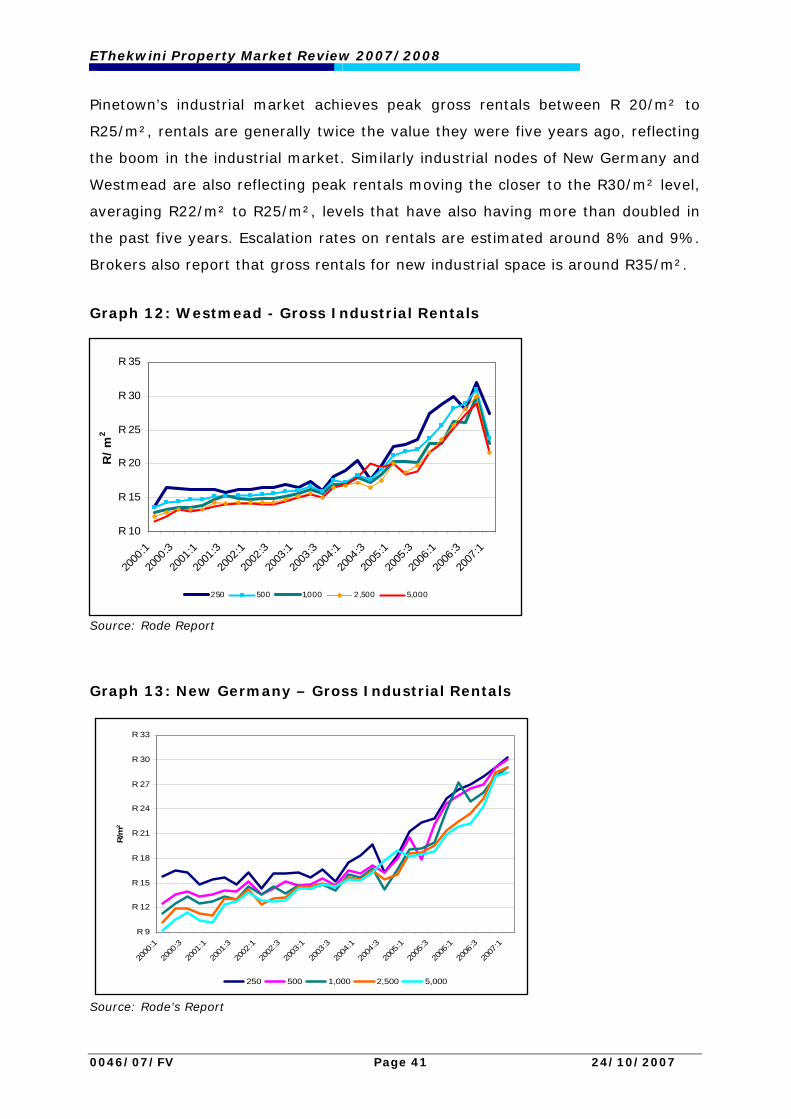

Pinetown’s industrial market achieves peak gross rentals between R 20/m² to

R25/m², rentals are generally twice the value they were five years ago, reflecting

the boom in the industrial market. Similarly industrial nodes of New Germany and

Westmead are also reflecting peak rentals moving the closer to the R30/m² level,

averaging R22/m² to R25/m², levels that have also having more than doubled in

the past five years. Escalation rates on rentals are estimated around 8% and 9%.

Brokers also report that gross rentals for new industrial space is around R35/m².

Graph 12: Westmead - Gross Industrial Rentals

Source: Rode Report

Graph 13: New Germany – Gross Industrial Rentals

Source: Rode’s Report

EThekwini Property Market Review 2007/2008

0046/07/FV Page 42 24/10/2007

Although rentals have strengthened in recent months, brokers report that

industrial users tend to prefer buying industrial space than leasing space.

In terms of industrial values for vacant land The Rode Report reflect the following

rates:

Table 11: Western Nodes: Industrial Land Values (Vacant Land)

1,000m² 2,000m² 5,000m² 10”000m²

Pinetown R500/m2 R475/m2 R450/m2 R400/m2

New Germany R400/m2 R400/m2 R375/m2 R350/m2

New Westmead/Mahogany

Ridge R500/m2 R475/m2 R525/m2 R400/m2

Source: Rode’s Report

Table 11 suggests industrial land values are generally being achieved between

R200/m² and R350/m² in these areas, higher rentals are being achieved for

newer industrial nodes.

Brokers report few sales for vacant space in the node, mainly due to scarcity of

industrial land in the nodes and that land prices could be sitting closer to

R400/m².

4.4 THE NORTHERN NODES

From the late 1990’s the Umhlanga commercial node has been one of the fastest

growing office nodes in South Africa. The latest SAPOA data as of the third quarter

of 2005 indicates a slight weakening of lower office grade vacancy rates. As

discussed earlier in the report the Westville node offers competition to

Umhlanga/La Lucia nodes.

EThekwini Property Market Review 2007/2008

0046/07/FV Page 43 24/10/2007

R 45

R 55

R 65

R 75

R 85

2000

:1

2001

:1

2002

:1

2003

:1

2004

:1

2005

:1

2006

:1

2007

:1

R/

m2

A+ A B

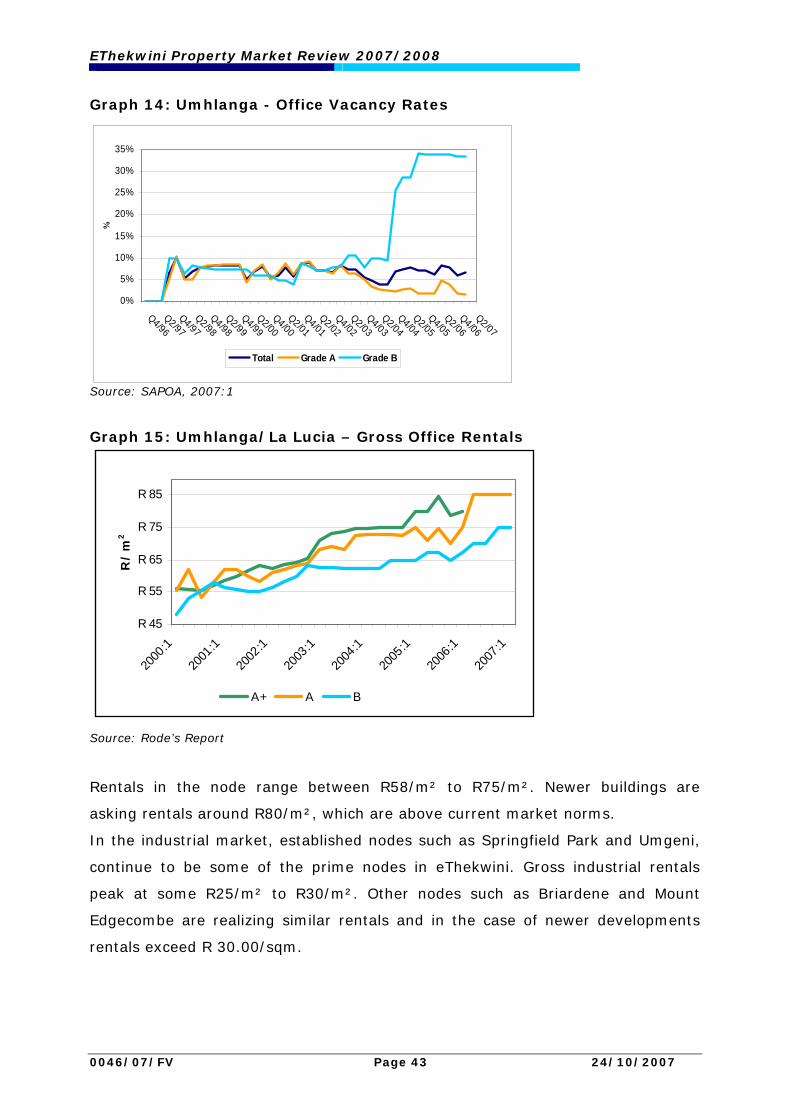

Graph 14: Umhlanga - Office Vacancy Rates

Source: SAPOA, 2007:1

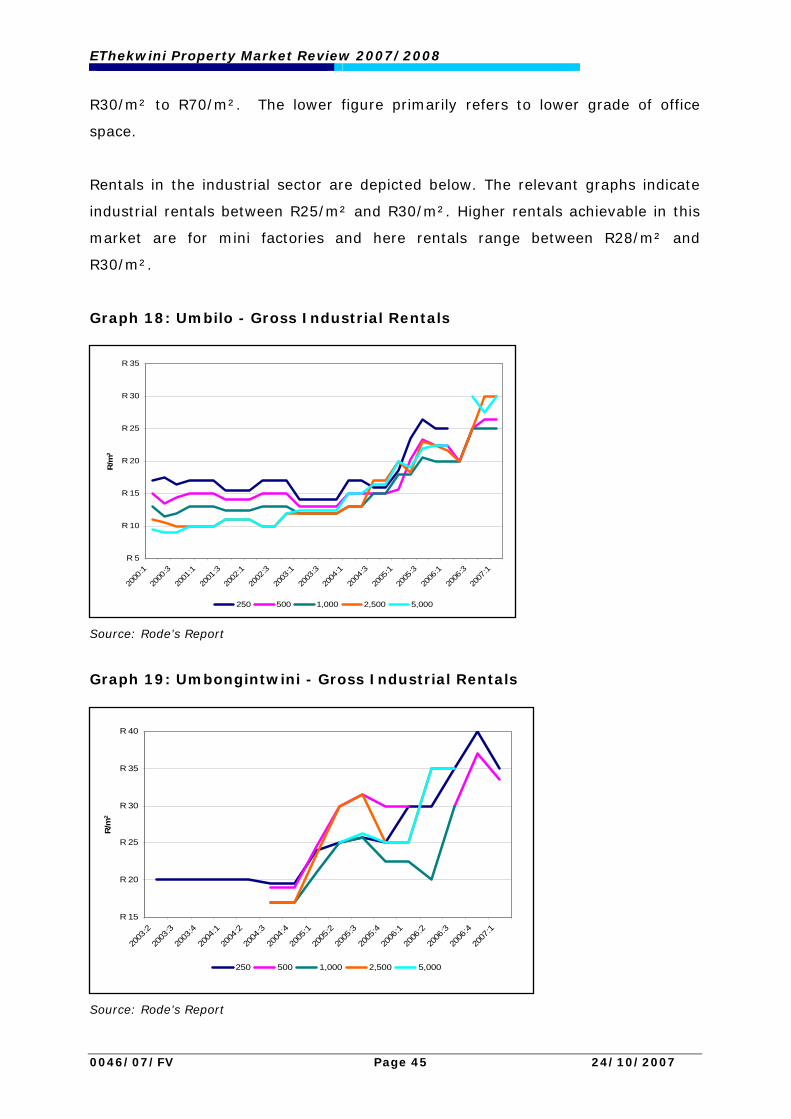

Graph 15: Umhlanga/La Lucia – Gross Office Rentals

Source: Rode’s Report

Rentals in the node range between R58/m² to R75/m². Newer buildings are

asking rentals around R80/m², which are above current market norms.

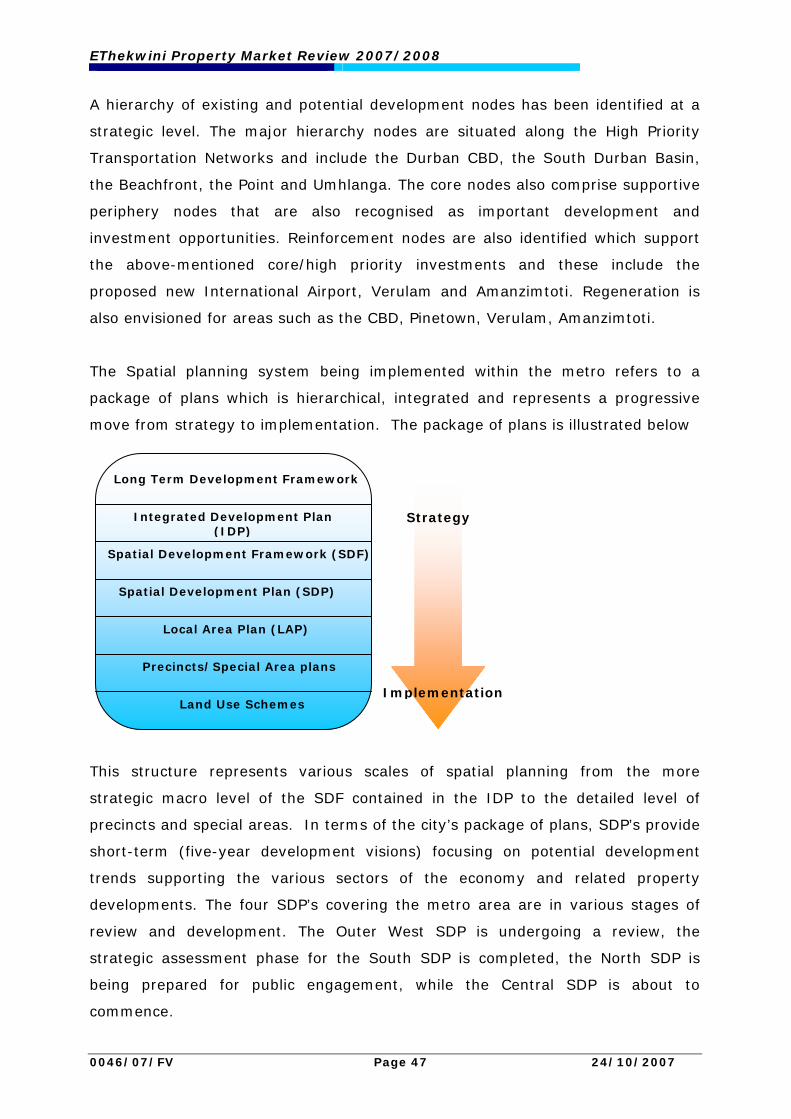

In the industrial market, established nodes such as Springfield Park and Umgeni,

continue to be some of the prime nodes in eThekwini. Gross industrial rentals

peak at some R25/m² to R30/m². Other nodes such as Briardene and Mount

Edgecombe are realizing similar rentals and in the case of newer developments

rentals exceed R 30.00/sqm.

0%

5%

10%

15%

20%

25%

30%

35%

Q4/96Q2/97

Q4/97Q2/98

Q4/98Q2/99

Q4/99Q2/00

Q4/00Q2/01

Q4/01Q2/02

Q4/02Q2/03

Q4/03Q2/04

Q4/04Q2/05

Q4/05Q2/06

Q4/06Q2/07

%

Total Grade A Grade B

EThekwini Property Market Review 2007/2008

0046/07/FV Page 44 24/10/2007

R 10

R 15

R 20

R 25

R 30

R 35

R 40

2000

:1

2000

:3

2001

:1

2001

:3

2002

:1

2002

:3

2003

:1

2003

:3

2004

:1

2004

:3

2005

:1

2005

:3

2006

:1

2006

:3

2007

:1

R/m

2

250 500 1,000 2,500 5,000

R 15

R 20

R 25

R 30

R 35

R 40

2001

:3

2002

:1

2002

:3

2003

:1

2003

:3

2004