Embed Size (px)

Citation preview

8/3/2019 Property Sector Post-ABSD (08-12-2011)

http://slidepdf.com/reader/full/property-sector-post-absd-08-12-2011 1/8

Kim Eng Research is a subsidiary of Malayan Banking Berhad

SEE APPENDIX I FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS

Sector Update 8 December 2011

Singapore Co. Reg No: 198700034E

MICA (P) : 090/11/2009

Property Sector Brace for impact

New round of tightening. The government rolled out a fifth round of

property cooling measures to keep a lid on investment demand from

locals and foreigners. Effective today, an Additional Buyer’s Stamp

Duty (ABSD) will be imposed over and above the current Buyer’s

Stamp Duty (approximately 3%) on selected transactions. Foreigners

and non-individuals will pay a 10% ABSD on all residential property

purchases, permanent residents will pay a 3% ABSD on second and

subsequent residential property purchases, and Singapore citizens willpay an ABSD of 3% on third and subsequent residential property

purchases.

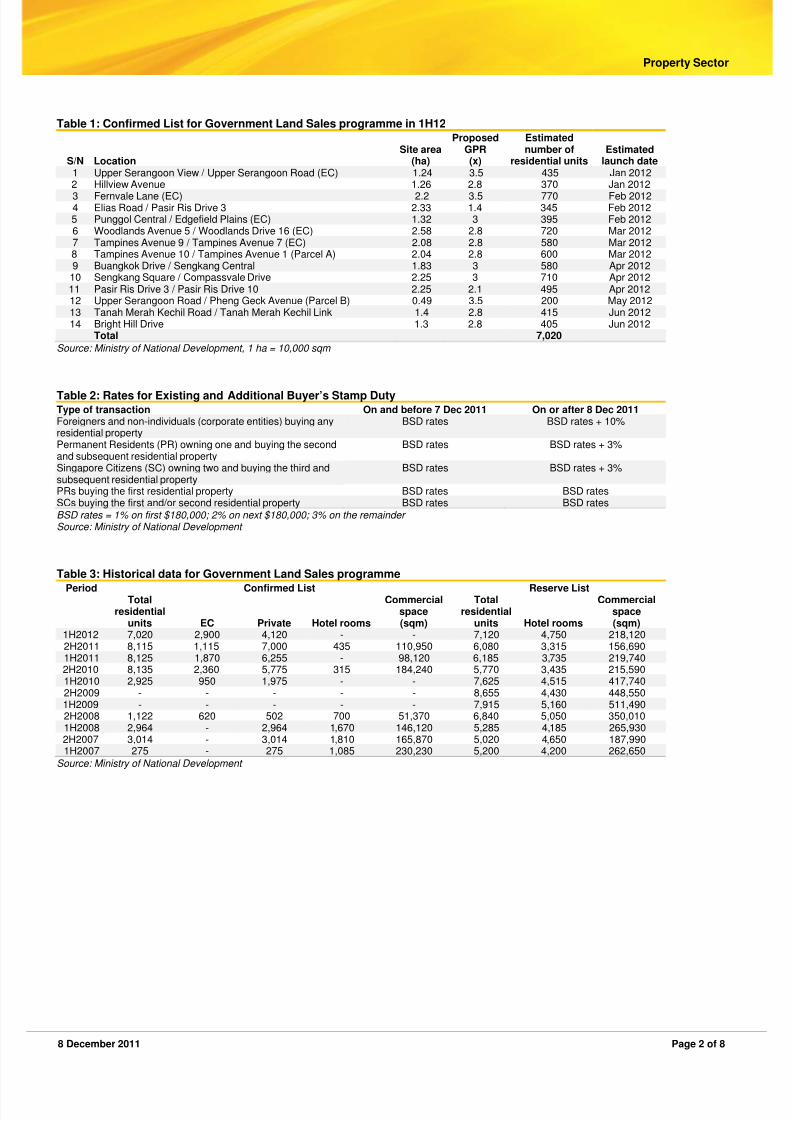

Moderated land supply. The government also released details on the

Government Land Sales (GLS) programme for 1H12. Fourteen sites

are placed on the Confirmed List, and these are expected to yield 7,020

residential units, down from 8,115 residential units in 2H11. Of note is

the supply in the Executive Condominium (EC) segment, which will be

ramped up to 2,900 units, compared with 1,115 units in 2H11. The

supply of private residential units, however, has been cut to 4,120 units,

from 7,000 units in 2H11.

Double whammy for mass market. Against the new backdrop, we

expect mass market projects to see prices slip by at least 10-20% going

into 2012. The full impact of the ramped-up supply under the GLS

programme will be felt only next year. This is when a minimum of

16,000 residential units from the record-high land sales this year will be

launched for sale. We also note that all 14 sites in the GLS 1H12 are

found in the mass market districts, with 10 located next to existing

launches. These sites are likely to attract lower bids because of the stiff

competition to be expected in a segment where margins are already

slim. Recent tender prices have implied pre-tax margins in the region of

15% and price cuts to drive sales is a probable strategy if the property

market turns frosty. The latest round of cooling measures is also ademand dampener for this segment, even though the impact is unlikely

to be very significant as up to 80% of the buyers are generally locals.

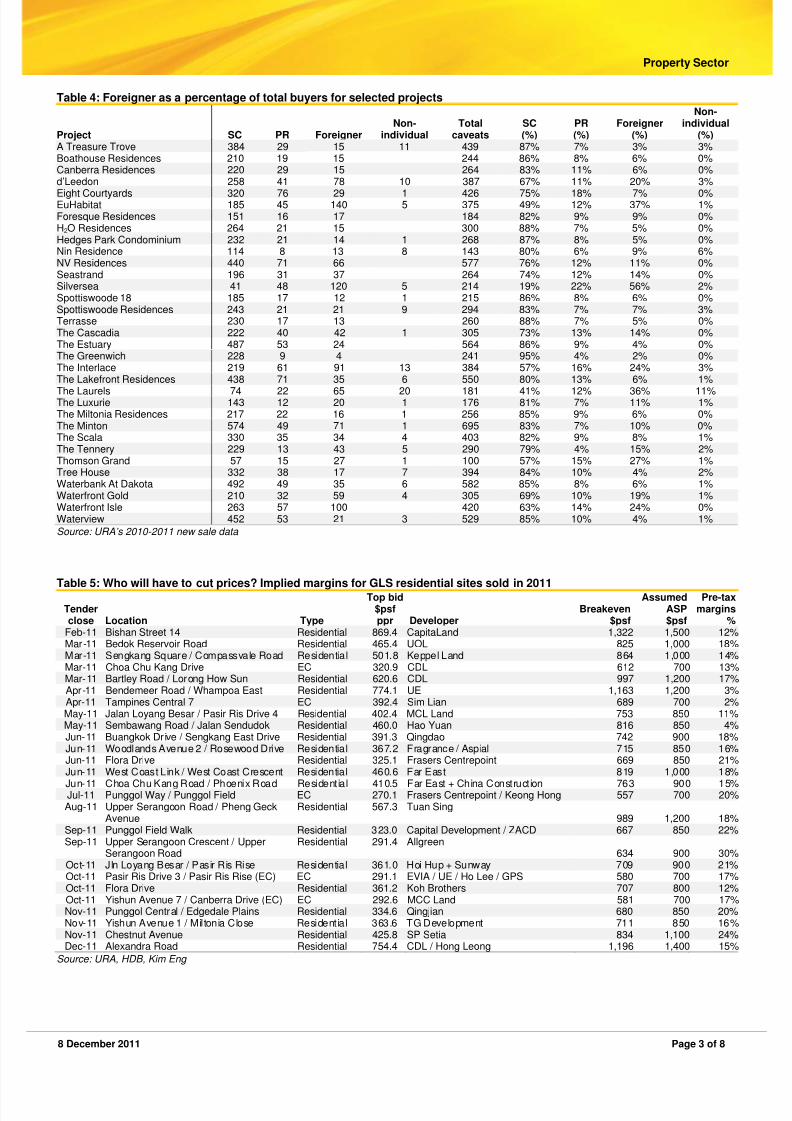

That said, we observe that some projects such as euHabitat in Eunos,

which offers a mix of housing types, has attracted higher foreigner

interest.

High-end segment to take longer to recover. About 40-80% of the

units in the high-end segment are sold to foreigners. This means the

10% ABSD is applicable to a majority of transactions in this market. But

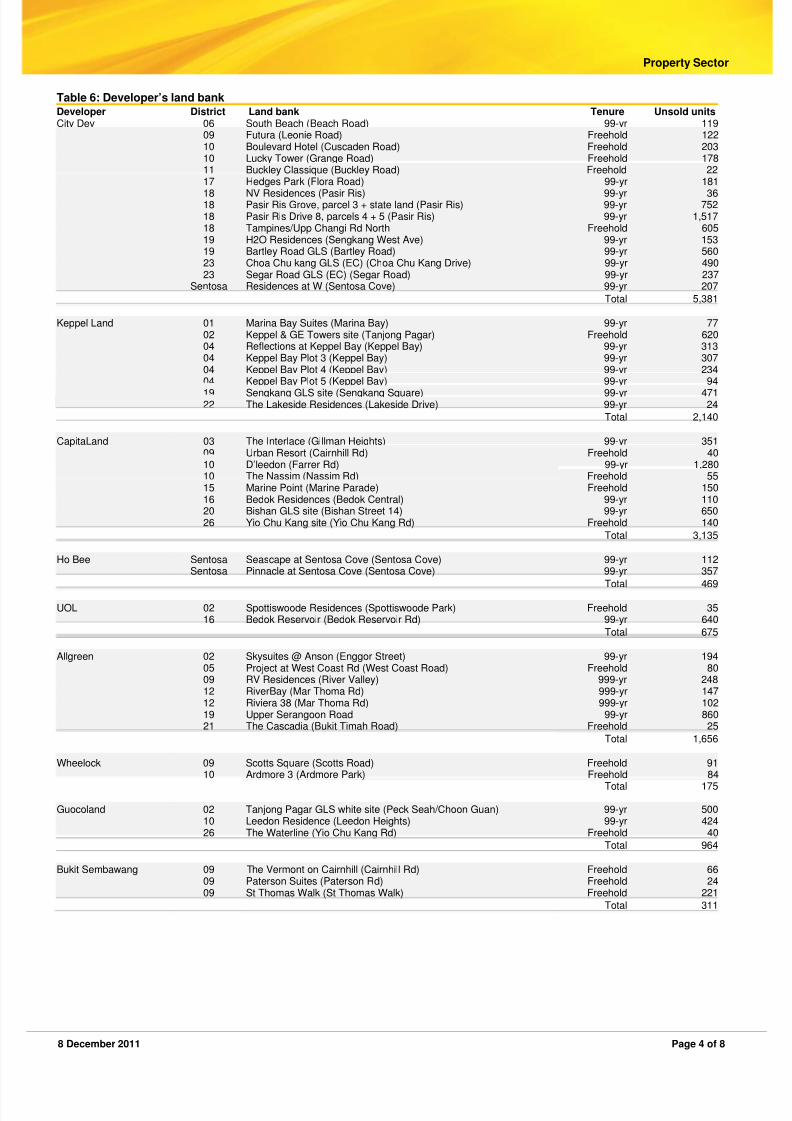

we hold the view that developers will not cut prices, given the rising

replacement cost of their inventories. The already sluggish sales in this

foreigner-led segment will be further stifled and a pickup in the nearterm has been nipped in the bud by the rollout of the ABSD. However,

we note that developers’ margins in the luxury segment are higher due

to the low cost of land from the last en bloc cycle and inventories are

largely freehold. In any case, a slowdown in sales has been anticipated.

OOI Yi [email protected](65) 6433 5712

8/3/2019 Property Sector Post-ABSD (08-12-2011)

http://slidepdf.com/reader/full/property-sector-post-absd-08-12-2011 2/88 December 2011 Page 2 of 8

Property Sector

Table 1: Confirmed List for Government Land Sales programme in 1H12

S/N LocationSite area

(ha)

ProposedGPR(x)

Estimatednumber of

residential unitsEstimated

launch date1 Upper Serangoon View / Upper Serangoon Road (EC) 1.24 3.5 435 Jan 2012

2 Hillview Avenue 1.26 2.8 370 Jan 20123 Fernvale Lane (EC) 2.2 3.5 770 Feb 20124 Elias Road / Pasir Ris Drive 3 2.33 1.4 345 Feb 20125 Punggol Central / Edgefield Plains (EC) 1.32 3 395 Feb 20126 Woodlands Avenue 5 / Woodlands Drive 16 (EC) 2.58 2.8 720 Mar 20127 Tampines Avenue 9 / Tampines Avenue 7 (EC) 2.08 2.8 580 Mar 20128 Tampines Avenue 10 / Tampines Avenue 1 (Parcel A) 2.04 2.8 600 Mar 20129 Buangkok Drive / Sengkang Central 1.83 3 580 Apr 201210 Sengkang Square / Compassvale Drive 2.25 3 710 Apr 201211 Pasir Ris Drive 3 / Pasir Ris Drive 10 2.25 2.1 495 Apr 201212 Upper Serangoon Road / Pheng Geck Avenue (Parcel B) 0.49 3.5 200 May 201213 Tanah Merah Kechil Road / Tanah Merah Kechil Link 1.4 2.8 415 Jun 201214 Bright Hill Drive 1.3 2.8 405 Jun 2012

Total 7,020

Source: Ministry of National Development, 1 ha = 10,000 sqm

Table 2: Rates for Existing and Additional Buyer’s Stamp DutyType of transaction On and before 7 Dec 2011 On or after 8 Dec 2011Foreigners and non-individuals (corporate entities) buying anyresidential property

BSD rates BSD rates + 10%

Permanent Residents (PR) owning one and buying the secondand subsequent residential property

BSD rates BSD rates + 3%

Singapore Citizens (SC) owning two and buying the third andsubsequent residential property

BSD rates BSD rates + 3%

PRs buying the first residential property BSD rates BSD ratesSCs buying the first and/or second residential property BSD rates BSD ratesBSD rates = 1% on first $180,000; 2% on next $180,000; 3% on the remainder Source: Ministry of National Development

Table 3: Historical data for Government Land Sales programmePeriod Confirmed List Reserve List

Totalresidential

units EC Private Hotel rooms

Commercialspace(sqm)

Totalresidential

units Hotel rooms

Commercialspace(sqm)

1H2012 7,020 2,900 4,120 - - 7,120 4,750 218,1202H2011 8,115 1,115 7,000 435 110,950 6,080 3,315 156,6901H2011 8,125 1,870 6,255 - 98,120 6,185 3,735 219,7402H2010 8,135 2,360 5,775 315 184,240 5,770 3,435 215,5901H2010 2,925 950 1,975 - - 7,625 4,515 417,7402H2009 - - - - - 8,655 4,430 448,5501H2009 - - - - - 7,915 5,160 511,4902H2008 1,122 620 502 700 51,370 6,840 5,050 350,0101H2008 2,964 - 2,964 1,670 146,120 5,285 4,185 265,9302H2007 3,014 - 3,014 1,810 165,870 5,020 4,650 187,990

1H2007 275 - 275 1,085 230,230 5,200 4,200 262,650Source: Ministry of National Development

8/3/2019 Property Sector Post-ABSD (08-12-2011)

http://slidepdf.com/reader/full/property-sector-post-absd-08-12-2011 3/88 December 2011 Page 3 of 8

Property Sector

Table 4: Foreigner as a percentage of total buyers for selected projects

Project SC PR ForeignerNon-

individualTotal

caveatsSC(%)

PR(%)

Foreigner(%)

Non-individual

(%)A Treasure Trove 384 29 15 11 439 87% 7% 3% 3%Boathouse Residences 210 19 15 244 86% 8% 6% 0%Canberra Residences 220 29 15 264 83% 11% 6% 0%d’Leedon 258 41 78 10 387 67% 11% 20% 3%Eight Courtyards 320 76 29 1 426 75% 18% 7% 0%EuHabitat 185 45 140 5 375 49% 12% 37% 1%Foresque Residences 151 16 17 184 82% 9% 9% 0%H2O Residences 264 21 15 300 88% 7% 5% 0%Hedges Park Condominium 232 21 14 1 268 87% 8% 5% 0%Nin Residence 114 8 13 8 143 80% 6% 9% 6%NV Residences 440 71 66 577 76% 12% 11% 0%Seastrand 196 31 37 264 74% 12% 14% 0%Silversea 41 48 120 5 214 19% 22% 56% 2%Spottiswoode 18 185 17 12 1 215 86% 8% 6% 0%Spottiswoode Residences 243 21 21 9 294 83% 7% 7% 3%Terrasse 230 17 13 260 88% 7% 5% 0%The Cascadia 222 40 42 1 305 73% 13% 14% 0%The Estuary 487 53 24 564 86% 9% 4% 0%The Greenwich 228 9 4 241 95% 4% 2% 0%The Interlace 219 61 91 13 384 57% 16% 24% 3%The Lakefront Residences 438 71 35 6 550 80% 13% 6% 1%The Laurels 74 22 65 20 181 41% 12% 36% 11%The Luxurie 143 12 20 1 176 81% 7% 11% 1%The Miltonia Residences 217 22 16 1 256 85% 9% 6% 0%The Minton 574 49 71 1 695 83% 7% 10% 0%The Scala 330 35 34 4 403 82% 9% 8% 1%The Tennery 229 13 43 5 290 79% 4% 15% 2%Thomson Grand 57 15 27 1 100 57% 15% 27% 1%Tree House 332 38 17 7 394 84% 10% 4% 2%Waterbank At Dakota 492 49 35 6 582 85% 8% 6% 1%Waterfront Gold 210 32 59 4 305 69% 10% 19% 1%Waterfront Isle 263 57 100 420 63% 14% 24% 0%Waterview 452 53 21 3 529 85% 10% 4% 1%

Source: URA’s 2010-2011 new sale data

Table 5: Who will have to cut prices? Implied margins for GLS residential sites sold in 2011

Tenderclose Location Type

Top bid$psfppr Developer

Breakeven$psf

AssumedASP$psf

Pre-taxmargins

%Feb-11 Bishan Street 14 Residential 869.4 CapitaLand 1,322 1,500 12%Mar-11 Bedok Reservoir Road Residential 465.4 UOL 825 1,000 18%Mar-11 Sengkang Square / Compassvale Road Residential 501.8 Keppel Land 864 1,000 14%Mar-11 Choa Chu Kang Drive EC 320.9 CDL 612 700 13%Mar-11 Bartley Road / Lorong How Sun Residential 620.6 CDL 997 1,200 17%Apr-11 Bendemeer Road / Whampoa East Residential 774.1 UE 1,163 1,200 3%Apr-11 Tampines Central 7 EC 392.4 Sim Lian 689 700 2%May-11 Jalan Loyang Besar / Pasir Ris Drive 4 Residential 402.4 MCL Land 753 850 11%May-11 Sembawang Road / Jalan Sendudok Residential 460.0 Hao Yuan 816 850 4%Jun-11 Buangkok Drive / Sengkang East Drive Residential 391.3 Qingdao 742 900 18%

Jun-11 Woodlands Avenue 2 / Rosewood Drive Residential 367.2 Fragrance / Aspial 715 850 16%Jun-11 Flora Drive Residential 325.1 Frasers Centrepoint 669 850 21%Jun-11 West Coast Link / West Coast Crescent Residential 460.6 Far East 819 1,000 18%Jun-11 Choa Chu Kang Road / Phoenix Road Residential 410.5 Far East + China Construction 763 900 15%Jul-11 Punggol Way / Punggol Field EC 270.1 Frasers Centrepoint / Keong Hong 557 700 20%Aug-11 Upper Serangoon Road / Pheng Geck

AvenueResidential 567.3 Tuan Sing

989 1,200 18%Sep-11 Punggol Field Walk Residential 323.0 Capital Development / ZACD 667 850 22%Sep-11 Upper Serangoon Crescent / Upper

Serangoon RoadResidential 291.4 Allgreen

634 900 30%Oct-11 Jln Loyang Besar / Pasir Ris Rise Residential 361.0 Hoi Hup + Sunway 709 900 21%Oct-11 Pasir Ris Drive 3 / Pasir Ris Rise (EC) EC 291.1 EVIA / UE / Ho Lee / GPS 580 700 17%Oct-11 Flora Drive Residential 361.2 Koh Brothers 707 800 12%Oct-11 Yishun Avenue 7 / Canberra Drive (EC) EC 292.6 MCC Land 581 700 17%Nov-11 Punggol Central / Edgedale Plains Residential 334.6 Qingjian 680 850 20%Nov-11 Yishun Avenue 1 / Mil tonia Close Residential 363.6 TG Development 711 850 16%

Nov-11 Chestnut Avenue Residential 425.8 SP Setia 834 1,100 24%Dec-11 Alexandra Road Residential 754.4 CDL / Hong Leong 1,196 1,400 15%

Source: URA, HDB, Kim Eng

8/3/2019 Property Sector Post-ABSD (08-12-2011)

http://slidepdf.com/reader/full/property-sector-post-absd-08-12-2011 4/88 December 2011 Page 4 of 8

Property Sector

Table 6: Developer’s land bankDeveloper District Land bank Tenure Unsold unitsCity Dev 06 South Beach (Beach Road) 99-yr 119 09 Futura (Leonie Road) Freehold 122

10 Boulevard Hotel (Cuscaden Road) Freehold 20310 Lucky Tower (Grange Road) Freehold 17811 Buckley Classique (Buckley Road) Freehold 2217 Hedges Park (Flora Road) 99-yr 18118 NV Residences (Pasir Ris) 99-yr 3618 Pasir Ris Grove, parcel 3 + state land (Pasir Ris) 99-yr 75218 Pasir Ris Drive 8, parcels 4 + 5 (Pasir Ris) 99-yr 1,51718 Tampines/Upp Changi Rd North Freehold 60519 H2O Residences (Sengkang West Ave) 99-yr 15319 Bartley Road GLS (Bartley Road) 99-yr 56023 Choa Chu kang GLS (EC) (Choa Chu Kang Drive) 99-yr 49023 Segar Road GLS (EC) (Segar Road) 99-yr 237

Sentosa Residences at W (Sentosa Cove) 99-yr 207

Total 5,381

Keppel Land 01 Marina Bay Suites (Marina Bay) 99-yr 77

02 Keppel & GE Towers site (Tanjong Pagar) Freehold 62004 Reflections at Keppel Bay (Keppel Bay) 99-yr 31304 Keppel Bay Plot 3 (Keppel Bay) 99-yr 30704 Keppel Bay Plot 4 (Keppel Bay) 99-yr 23404 Keppel Bay Plot 5 (Keppel Bay) 99-yr 9419 Sengkang GLS site (Sengkang Square) 99-yr 47122 The Lakeside Residences (Lakeside Drive) 99-yr 24

Total 2,140

CapitaLand 03 The Interlace (Gillman Heights) 99-yr 351

09 Urban Resort (Cairnhill Rd) Freehold 4010 D’leedon (Farrer Rd) 99-yr 1,28010 The Nassim (Nassim Rd) Freehold 5515 Marine Point (Marine Parade) Freehold 15016 Bedok Residences (Bedok Central) 99-yr 11020 Bishan GLS site (Bishan Street 14) 99-yr 65026 Yio Chu Kang site (Yio Chu Kang Rd) Freehold 140

Total 3,135

Ho Bee Sentosa Seascape at Sentosa Cove (Sentosa Cove) 99-yr 112Sentosa Pinnacle at Sentosa Cove (Sentosa Cove) 99-yr 357

Total 469

UOL 02 Spottiswoode Residences (Spottiswoode Park) Freehold 35

16 Bedok Reservoir (Bedok Reservoir Rd) 99-yr 640

Total 675

Allgreen 02 Skysuites @ Anson (Enggor Street) 99-yr 194

05 Project at West Coast Rd (West Coast Road) Freehold 8009 RV Residences (River Valley) 999-yr 24812 RiverBay (Mar Thoma Rd) 999-yr 14712 Riviera 38 (Mar Thoma Rd) 999-yr 10219 Upper Serangoon Road 99-yr 86021 The Cascadia (Bukit Timah Road) Freehold 25

Total 1,656

Wheelock 09 Scotts Square (Scotts Road) Freehold 91

10 Ardmore 3 (Ardmore Park) Freehold 84Total 175

Guocoland 02 Tanjong Pagar GLS white site (Peck Seah/Choon Guan) 99-yr 500

10 Leedon Residence (Leedon Heights) 99-yr 42426 The Waterline (Yio Chu Kang Rd) Freehold 40

Total 964

Bukit Sembawang 09 The Vermont on Cairnhill (Cairnhill Rd) Freehold 66

09 Paterson Suites (Paterson Rd) Freehold 2409 St Thomas Walk (St Thomas Walk) Freehold 221

Total 311

8/3/2019 Property Sector Post-ABSD (08-12-2011)

http://slidepdf.com/reader/full/property-sector-post-absd-08-12-2011 5/88 December 2011 Page 5 of 8

Property Sector

Table 6: Developer’s land bank (cont’d)Developer District Land bank Tenure Unsold unitsFrasers Centrepoint 09 StarHub Centre 99-yr 240

15 Flamingo Valley (Siglap Rd) Freehold 22016 Waterfront Gold (Bedok Reservoir Rd) 99-yr 416 Waterfront Isle (Bedok Reservoir Rd) 99-yr 8118 Seastrand (Pasir Ris Drive 3) 99-yr 21518 Pasir Ris GLS site (Flora Drive) 99-yr 38019 Boathouse Residences (Upper Serangoon Road) 99-yr 29119 Esparina Residences (Sengkang) 99-yr 119 Punggol GLS mixed site (Punggol Central) 99-yr 68527 Eight Courtyards (Yishun Ave 2) 99-yr 141

Total 2,258 Wing Tai 03 Ascentia Sky (Redhill) 99-yr 47

09 HELIOS Residence (Cairnhill Circle) Freehold 6409 Belle Vue Residences (Oxley Walk) Freehold 3810 Le Nouvel Ardmore (Ardmore Park) Freehold 4210 Anderson 18 (Ardmore Park) Freehold 15711 L'VIV (Newton Rd) Freehold 4023 Foresque Residences (Petir Road) 99-yr 299

Total 687 MCL Land 10 NOB Hill (Ewe Boon Rd) Freehold 70

15 Casa Nassau (East Coast Rd) Freehold 6517 Pasir Ris GLS site (Jalan Loyang Besar) 99-yr 58019 Terrasse (Hougang Ave 2) 99-yr 122

Total 837 SC Global 9 The Marq (Paterson Hill) Freehold 37

9 Hilltops (Cairnhill Circle) Freehold 2089 Martin No. 38 (Martin Rd) Freehold 2310 The Ardmore (Ardmore Road) Freehold 50

Sentosa Seven Palms (Sentosa Cove) 99-yr 31

Total 349Source: Kim Eng

Table 7: Valuations

Name Price RNAVDisc/ Prem to

RNAV NTA/share*Disc/

Prem to NTA/shareCapitaLand 2.43 3.92 -38% 3.18 -24%CityDev 9.22 13 -29% 7.31 26%Ho Bee 1.135 2.69 -58% 2.22 -49%HPL 1.78 4.39 -59% 2.7 -34%KepLand 2.44 5.08 -52% 2.78 -12%SC Global 1.095 4.74 -77% 1.6 -32%SingLand 5.85 9.82 -40% 10.74 -46%UOL 4.04 N.A. N.A. 6.43 -37%Wheelock 1.585 N.A. N.A. 2.35 -33%Wing Tai 1.005 2.85 -65% 2.49 -60%

N.A. = No Coverage *As at latest reported

8/3/2019 Property Sector Post-ABSD (08-12-2011)

http://slidepdf.com/reader/full/property-sector-post-absd-08-12-2011 6/88 December 2011 Page 6 of 8

Property Sector

ANALYSTS’ COVERAGE / RESEARCH OFFICES

MALAYSIAWONG Chew Hann, CA Head of Research (603) 2297 8686 [email protected] Strategy Construction & Infrastructure

Desmond CH’NG, ACA(603) 2297 8680 [email protected] Banking - Regional LIAW Thong Jung(603) 2297 8688 [email protected] Oil & Gas Automotive ShippingONG Chee Ting(603) 2297 8678 [email protected] PlantationsMohshin AZIZ (603) 2297 8692 [email protected] Aviation Petrochem PowerYIN Shao Yang, CPA(603) 2297 8916 [email protected] Gaming – Regional Media PowerWONG Wei Sum(603) 2297 8679 [email protected] Property & REITsLEE Yen Ling(603) 2297 8691 [email protected] Building Materials Manufacturing TechnologyFarouq Azizul MAHMUD (603) 2297 8687 [email protected] Automotive

LEE Cheng Hooi Head of Retail [email protected] Technicals

HONG KONG / CHINAEdward FUNG Head of Research (852) 2268 0632 [email protected] ConstructionIvan CHEUNG (852) 2268 0634 [email protected] Property IndustrialIvan LI (852) 2268 0641 [email protected] Banking & FinanceJacqueline KO (852) 2268 0633 [email protected] Consumer StaplesAndy POON (852) 2268 0645 [email protected] Telecom & related servicesSamantha KWONG (852) 2268 0640 [email protected] Consumer DiscretionariesAlex YEUNG (852) 2268 0636 [email protected]

Industrial

INDIAJigar SHAH Head of Research (91) 22 6623 2601 [email protected]. in Oil & Gas Automobile CementAnubhav GUPTA (91) 22 6623 2605 [email protected]. in Metal & Mining Capital goods PropertyHaripreet BATRA (91) 226623 2606 [email protected] Software MediaGanesh RAM (91) 226623 2607 [email protected] Telecom

Contractor

SINGAPOREStephanie WONG Head of Research (65) 6432 1451 [email protected] Strategy Small & Mid Caps

Gregory YAP (65) 6432 1450 [email protected] Conglomerates Technology & Manufacturing Telcos - Regional Rohan SUPPIAH (65) 6432 1455 [email protected] Airlines Marine & OffshoreWilson LIEW (65) 6432 1454 [email protected] Hotel & Resort Property & ConstructionAnni KUM (65) 6432 1470 [email protected] Conglomerates REITsJames KOH (65) 6432 1431 [email protected] Finance Logistics ResourcesEric ONG (65) 6432 1857 [email protected] Marine & Offshore Transportation EnergyOOI Yi Tung(65) 6433 5712 [email protected] Property & ConstructionYEAK Chee Keong, CFA(65) 6433 5730 [email protected] Retail & Consumer Engineering InfrastructureAlison FOK (65) 6433 5745 [email protected] Services

INDONESIAKatarina SETIAWAN Head of Research (62) 21 2557 1125 [email protected] Consumer Strategy TelcosRahmi MARINA (62) 21 2557 1128 [email protected] Banking MultifinanceLucky ARIESANDI, CFA (62) 21 2557 1127 [email protected] Base metals Coal Heavy Equipment Oil & gasAdi N. WICAKSONO (62) 21 2557 1130 [email protected] GeneralistArwani PRANADJAYA

(62) 21 2557 1129 [email protected] Technicals

THAILANDMayuree CHOWVIKRAN Head of Research (66)-2658-6300 ext 1440 [email protected] StrategySuttatip PEERASUB (66)-2658-6300 ext 1430 [email protected] Media CommerceSutthichai KUMWORACHAI (66)-2658-6300 ext 1400 [email protected] Energy PetrochemTermporn TANTIVIVAT (66)-2658-6300 ext 1520 [email protected] PropertyWoraphon WIROONSRI (66)-2658-6300 ext 1560 [email protected]

BankJaroonpan WATTANAWONG (66)-2658-6300 ext 1404 [email protected] Transportation Small cap.

PHILIPPINESLuz LORENZO Head of Research +63 2 849 8836 [email protected] StrategyLaura DY-LIACCO

(63) 2 849 8840 [email protected] Utilities Conglomerates TelcosLovell SARREAL (63) 2 849 8841 [email protected] Consumer Media Cement MiningKenneth NERECINA (63) 2 849 8839 [email protected] Conglomerates Property Ports/ LogisticsKatherine TAN (63) 2 849 8843 [email protected] Banks Construction

VIETNAMMichael Kokalari, CFA Head of Research (84) 838 38 66 36 x [email protected] StrategyNguyen Thi Ngan Tuyen(84) 838386636 x163 [email protected] Conglomerates Confectionary and Beverage Oil and GasNgo Bich Van(84) 838 38 66 36 x 171 [email protected] Banking InsuranceNguyen Quang Duy(84) 838386636 x162 [email protected]

Industrial PropertyTrinh Thi Ngoc Diep(84) 422 21 22 08 x 102 [email protected] Property & Construction PowerDang Thi Kim Thoa(84) 838 38 66 36 x 164 [email protected]

Consumer Services

ECONOMICSSuhaimi ILIAS Chief Economist (603) 2297 8682 [email protected]

Luz LORENZO Economist (63) 2 849 8836 [email protected] Philippines Indonesia

REGIONAL

ONG Seng Yeow(65) 6432 1832 [email protected] Regional Products & Planning

8/3/2019 Property Sector Post-ABSD (08-12-2011)

http://slidepdf.com/reader/full/property-sector-post-absd-08-12-2011 7/88 December 2011 Page 7 of 8

Property Sector

APPENDIX 1

Definition of Ratings

Kim Eng Research uses the following rating system:

BUY Total return is expected to be above 10% in the next 12 months

HOLD Total return is expected to be between -5% to 10% in the next 12 months

SELL Total return is expected to be below -5% in the next 12 months

Applicability of Ratings

The respective analyst maintains a coverage universe of stocks, the list of which may be adjusted according to needs. Investment ratings are

only applicable to the stocks which form part of the coverage universe. Reports on companies which are not part of the coverage do not

carry investment ratings as we do not actively follow developments in these companies.

Some common terms abbreviated in this report (where they appear):

Adex = Advertising Expenditure FCF = Free Cashflow PE = Price EarningsBV = Book Value FV = Fair Value PEG = PE Ratio To Growth

CAGR = Compounded Annual Growth Rate FY = Financial Year PER = PE RatioCapex = Capital Expenditure FYE = Financial Year End QoQ = Quarter-On-QuarterCY = Calendar Year MoM = Month-On-Month ROA = Return On AssetDCF = Discounted Cashflow NAV = Net Asset Value ROE = Return On EquityDPS = Dividend Per Share NTA = Net Tangible Asset ROSF = Return On Shareholders’ FundsEBIT = Earnings Before Interest And Tax P = Price WACC = Weighted Average Cost Of CapitalEBITDA = EBIT, Depreciation And Amortisation P.A. = Per Annum YoY = Year-On-YearEPS = Earnings Per Share PAT = Profit After Tax YTD = Year-To-Date

EV = Enterprise Value PBT = Profit Before Tax

APPENDIX I: TERMS FOR PROVISION OF REPORT, DISCLOSURES AND DISCLAIMERS

This report, and any electronic access to it, is restricted to and intended only for clients of Kim Eng Research Pte. Ltd. ("KER") or a related entity to KER (as thecase may be) who are institutional investors (for the purposes of both the Singapore Securities and Futures Act (“SFA”) and the Singapore Financial Advisers Act(“FAA”)) and who are allowed access thereto (each an "Authorised Person") and is subject to the terms and disclaimers below.

IF YOU ARE NOT AN AUTHORISED PERSON OR DO NOT AGREE TO BE BOUND BY THE TERMS AND DISCLAIMERS SET OUT BELOW, YOU SHOULD

DISREGARD THIS REPORT IN ITS ENTIRETY AND LET KER OR ITS RELATED ENTITY (AS RELEVANT) KNOW THAT YOU NO LONGER WISH TORECEIVE SUCH REPORTS.

This report provides information and opinions as reference resource only. This report is not intended to be and does not constitute financial advice, investmentadvice, trading advice or any other advice. It is not to be construed as a solicitation or an offer to buy or sell any securities or related financial products. Theinformation and commentaries are also not meant to be endorsements or offerings of any securities, options, stocks or other investment vehicles.

The report has been prepared without regard to the individual financial circumstances, needs or objectives of persons who receive it. The securities discussed inthis report may not be suitable for all investors. Readers should not rely on any of the information herein as authoritative or substitute for the exercise of their ownskill and judgment in making any investment or other decision. Readers should independently evaluate particular investments and strategies, and areencouraged to seek the advice of a financial adviser before making any investment or entering into any transaction in relation to the securities mentioned in thisreport. The appropriateness of any particular investment or strategy whether opined on or referred to in this report or otherwise will depend on an investor’sindividual circumstances and objectives and should be confirmed by such investor with his advisers independently before adoption or implementation (either asis or varied). You agree that any and all use of this report which you make, is solely at your own risk and without any recourse whatsoever to KER, its related andaffiliate companies and/or their employees. You understand that you are using this report AT YOUR OWN RISK.

This report is being disseminated to or allowed access by Authorised Persons in their respective jurisdictions by the Kim Eng affiliated entity/entities operatingand carrying on business as a securities dealer or financial adviser in that jurisdiction (collectively or individually, as the context requires, "Kim Eng") which has,vis-à-vis a relevant Authorised Person, approved of, and is solely responsible in that jurisdiction for, the contents of this publication in thatjurisdiction.

Kim Eng, its related and affiliate companies and/or their employees may have investments in securities or derivatives of securities of companies mentioned inthis report, and may trade them in ways different from those discussed in this report. Derivatives may be issued by Kim Eng its related companies orassociated/affiliated persons.

Kim Eng and its related and affiliated companies are involved in many businesses that may relate to companies mentioned in this report. These businessesinclude market making and specialised trading, risk arbitrage and other proprietary trading, fund management, investment services and corporate finance.

Except with respect the disclosures of interest made above, this report is based on public information. Kim Eng makes reasonable effort to use reliable,comprehensive information, but we make no representation that it is accurate or complete. The reader should also note that unless otherwise stated, none of KimEng or any third-party data providers make ANY warranties or representations of any kind relating to the accuracy, completeness, or timeliness of the data theyprovide and shall not have liability for any damages of any kind relating to such data.

Proprietary Rights to Content. The reader acknowledges and agrees that this report contains information, photographs, graphics, text, images, logos, icons,typefaces, and/or other material (collectively “Content”) protected by copyrights, trademarks, or other proprietary rights, and that these rights are valid andprotected in all forms, media, and technologies existing now or hereinafter developed. The Content is the property of Kim Eng or that of third party providers ofcontent or licensors. The compilation (meaning the collection, arrangement, and assembly) of all content on this report is the exclusive property of Kim Eng and

is protected by Singapore and international copyright laws. The reader may not copy, modify, remove, delete, augment, add to, publish, transmit, participate inthe transfer, license or sale of, create derivative works from, or in any way exploit any of the Content, in whole or in part, except as specifically permitted herein.If no specific restrictions are stated, the reader may make one copy of select portions of the Content, provided that the copy is made only for personal,information, and non-commercial use and that the reader does not alter or modify the Content in any way, and maintain any notices contained in the Content,such as all copyright notices, trademark legends, or other proprietary rights notices. Except as provided in the preceding sentence or as permitted by the fairdealing privilege under copyright laws, the reader may not reproduce, or distribute in any way any Content without obtaining permission of the owner of thecopyright, trademark or other proprietary right. Any authorised/permitted distribution is restricted to such distribution not being in violation of the copyright of KimEng only and does not in any way represent an endorsement of the contents permitted or authorised to be distributed to third parties.

8/3/2019 Property Sector Post-ABSD (08-12-2011)

http://slidepdf.com/reader/full/property-sector-post-absd-08-12-2011 8/88 December 2011 Page 8 of 8

Property Sector

Malays ia

Maybank Investment Bank Berhad(A Participating Organisation of Bursa Malaysia Securities Berhad)33rd Floor, Menara Maybank,100 Jalan Tun Perak,50050 Kuala Lumpur

Tel: (603) 2059 1888;Fax: (603) 2078 4194

Singapore

Kim Eng Securities Pte Ltd Kim Eng Research Pte Ltd9 Temasek Boulevard#39-00 Suntec Tower 2Singapore 038989

Tel: (65) 6336 9090Fax: (65) 6339 6003

London

Maybank Kim Eng Securities(London) Ltd 6/F, 20 St. Dunstan’s HillLondon EC3R 8HY, UK

Tel: (44) 20 7621 9298

Dealers’ Tel: (44) 20 7626 2828Fax: (44) 20 7283 6674

Ne w Y o rk

Maybank Ki m Eng SecuritiesUSA Inc 777 Third Avenue, 21st Floor New York, NY 10017, U.S.A.

Tel: (212) 688 8886

Fax: (212) 688 3500

Stockbroking Business:Level 8, Tower C, Dataran Maybank,No.1, Jalan Maarof 59000 Kuala Lumpur Tel: (603) 2297 8888Fax: (603) 2282 5136

Hong Kong

Kim Eng Securities (HK) Ltd Level 30,Three Pacific Place,1 Queen’s Road East,Hong Kong

Tel: (852) 2268 0800Fax: (852) 2877 0104

Indones ia

PT Kim Eng Securities Plaza BapindoCitibank Tower 17th Floor Jl Jend. Sudirman Kav. 54-55Jakarta 12190, Indonesia

Tel: (62) 21 2557 1188Fax: (62) 21 2557 1189

Ind ia

Kim Eng Securities India Pvt Ltd2nd Floor, The International 16,Maharishi Karve Road,Churchgate Station,Mumbai City - 400 020, India

Tel: (91).22.6623.2600Fax: (91).22.6623.2604

Phi l ippines

Maybank ATR Kim Eng SecuritiesInc.

17/F, Tower One & Exchange PlazaAyala Triangle, Ayala AvenueMakati City, Philippines 1200

Tel: (63) 2 849 8888Fax: (63) 2 848 5738

Tha i land

Maybank Kim Eng Securities(Thailand) Public Company

Limited 999/9 The Offices at Central World,20th- 21st Floor,Rama 1 Road Pathumwan,Bangkok 10330, Thailand

Tel: (66) 2 658 6817 (sales)Tel: (66) 2 658 6801 (research)

Vie tnamIn association with

Kim Eng Vietnam SecuritiesCompany

1st Floor, 255 Tran Hung Dao St.District 1Ho Chi Minh City, Vietnam

Tel : (84) 838 38 66 36Fax : (84) 838 38 66 39

Saudi ArabiaIn association with

Anfaal CapitalVilla 47, Tujjar Jeddah

Prince Mohammed bin AbdulazizStreet P.O. Box 126575Jeddah 21352

Tel: (966) 2 6068686Fax: (966) 26068787

South Asia Sales Trading

Connie [email protected]: (65) 6333 5775US Toll Free: 1 866 406 7447

Nor th As ia Sa les Trad ing

Eddie [email protected]: (852) 2268 0800US Toll Free: 1 866 598 2267

www.maybank-ib.com | www.kimengresearch.com.sg

APPENDIX I

Additional information on mentioned securities is available on request.

Jurisdiction Specific Additional Disclaimers:

THIS RESEARCH REPORT IS STRICTLY CONFIDENTIAL TO THE RECIPIENT, MAY NOT BE DISTRIBUTED TO THE PRESS OR OTHER MEDIA, ANDMAY NOT BE REPRODUCED IN ANY FORM AND MAY NOT BE TAKEN OR TRANSMITTED INTO THE REPUBLIC OF KOREA, OR PROVIDED ORTRANSMITTED TO ANY KOREAN PERSON. FAILURE TO COMPLY WITH THIS RESTRICTION MAY CONSTITUTE A VIOLATION OF SECURITIES LAWSIN THE REPUBLIC OF KOREA. BY ACCEPTING THIS REPORT, YOU AGREE TO BE BOUND BY THE FOREGOING LIMITATIONS.

THIS RESEARCH REPORT IS STRICTLY CONFIDENTIAL TO THE RECIPIENT, MAY NOT BE DISTRIBUTED TO THE PRESS OR OTHER MEDIA, ANDMAY NOT BE REPRODUCED IN ANY FORM AND MAY NOT BE TAKEN OR TRANSMITTED INTO MALAYSIA OR PROVIDED OR TRANSMITTED TO ANYMALAYSIAN PERSON. FAILURE TO COMPLY WITH THIS RESTRICTION MAY CONSTITUTE A VIOLATION OF SECURITIES LAWS IN MALAYSIA. BYACCEPTING THIS REPORT, YOU AGREE TO BE BOUND BY THE FOREGOING LIMITATIONS.

Without prejudice to the foregoing, the reader is to note that additional disclaimers, warnings or qualifications may apply if the reader is receiving or

accessing this report in or from other than Singapore.

As of 8 December 2011, Kim Eng Research Pte. Ltd. and the covering analyst do not have any interest in the companies.

Analyst Certification:

The views expressed in this research report accurately reflect the analyst's personal views about any and all of the subject securities or issuers; and no part ofthe research analyst's compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in the report.

© 2011 Kim Eng Research Pte Ltd. All rights reserved. Except as specifically permitted, no part of this presentation may be reproduced or distributed in anymanner without the prior written permission of Kim Eng Research Pte. Ltd. Kim Eng Research Pte. Ltd. accepts no liability whatsoever for the actions of thirdparties in this respect.

Stephanie Wong

CEO, Kim Eng Research