Embed Size (px)

Citation preview

FEEDBACK ON CONSULTATION PAPER NO. 8 2013

PROPOSED REVISIONS OF THE CODES OF PRACTICE FOR INVESTMENT BUSINESS WITH RESPECT TO THE REVIEW OF FINANCIAL ADVICE (“RFA”)

Proposals to address changes in the regulatory regime with respect to the provision of financial advice.

ISSUED 13 DECEMBER 2013

2 of 32 Issued: 13 December 2013

FEEDBACK ON

CONSULTATION PAPER Please note that terms in italics are defined in the Glossary of Terms.

This paper reports on the responses received by the Commission on the Consultation Paper No.8 2013 – Review of Financial Advice.

Further enquiries concerning the feedback may be directed to: John Charles Cronin Senior Manager, Funds Policy Jersey Financial Services Commission PO Box 267 14-18 Castle Street St Helier Jersey JE4 8TP

Telephone: +44 (0) 1534 822094 Email: [email protected]

Glossary of Terms

Feedback on CP08/13 Amending the IB Codes due to the RFA 3 of 32

GLOSSARY OF TERMS

the Commission means the Jersey Financial Services Commission.

CP 08/13 means Consultation Paper No. 8 2013 Proposed revisions of the Codes of Practice for Investment Business with respect to the Review of Financial Advice.

the FCA means the UK’s Financial Conduct Authority.

the FS(J)L means the Financial Services (Jersey) Law 1998, as amended.

the FSA means the UK’s former Financial Services Authority.

Guidance Note means the Commission’s Guidance Note: Professional Qualifications (Investment Business).

investment business as defined under Article 2(2) of the FS(J)L.

the IB Codes means the Codes of Practice for Investment Business.

investment employee

means an individual that meets the definition of an investment employee as provided in the Investment Business Fees Notice published on the Commission’s Website: http://www.jerseyfsc.org/the_commission/fees_notices/index.asp

Jersey Finance means Jersey Finance Limited.

MiFID means the Markets in Financial Instruments Directive 2004/39/EC.

OPEO means the Financial Services (Investment Business) (Overseas Persons – Exemption)) (Jersey) Order 2001.

Position Paper 1 means the Commission’s Position Paper No.1 2011 on the RFA issued in August 2011.

Position Paper 2 means the Commission’s Position Paper No.1 2013 on the RFA issued in June 2013.

QCF means Qualifications and Credit Framework.

RDR means the FSA Retail Distribution Review.

RFA means the Review of Financial Advice.

Trust Company Customer

means any person(s) who has:- (a) entered into an agreement for the provision of services by the registered person when carrying on trust company business; or (b) received or may receive the benefit of services provided or arranged by the registered person when carrying on trust company business.

UK means the United Kingdom.

Glossary of Terms

4 of 32 Issued: 13 December 2013

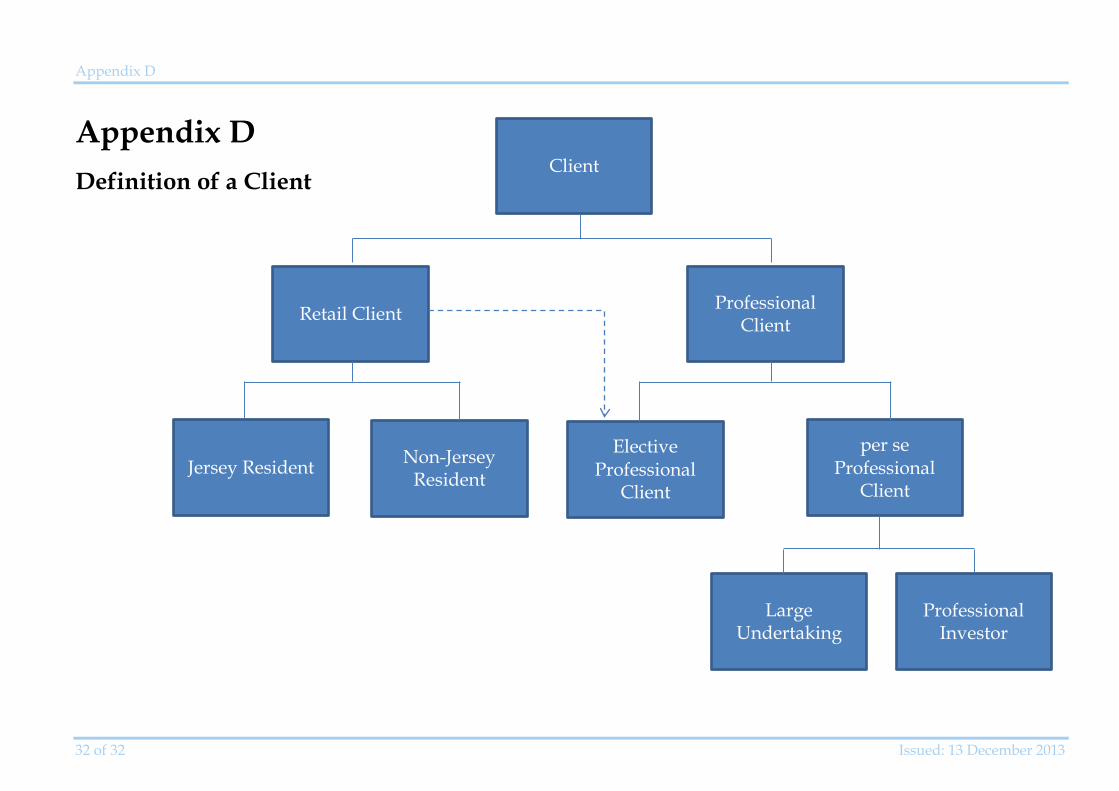

Glossary of terms relating to client classification

(Appendix D provides a pictorial representation of the interconnectedness of these definitions)

client has the same meaning as provided in Article 1 of the FS(J)L.

Retail Client means a client that is not a Professional Client.

Professional Client means a client that is a per se Professional Client or an Elective Professional Client.

Elective Professional Client means a Retail Client who has requested to be, and been reclassified by the registered person, in accordance with paragraph 3.8, as a Professional Client.

per se Professional Client means either a Large Undertaking or Professional Investor.

Professional Investor

means, • a government, local authority, public authority or

supra-national body (wherever established); or • a person, partnership, unincorporated association or

body corporate whose ordinary business or professional activity includes or it is reasonable to expect that it includes acquiring, underwriting, managing, holding or disposing of investments whether as principal or agent or the giving of advice on investments.

Large Undertaking

means a client in relation to which at least two of the following three criteria are satisfied:

• balance sheet total assets of not less than £13,000,000; • net turnover of £26,000,000 or greater; or • net assets of £1,300,000 or greater.

Contents

Feedback on CP08/13 Amending the IB Codes due to the RFA 5 of 32

CONTENTS 1 OVERVIEW ................................................................................................................................. 6

1.1 Background .................................................................................................................. 6 1.2 Feedback on CP 08/13 ................................................................................................. 6 1.3 Summary of the issues ................................................................................................ 6

2 SUMMARY OF RESPONSES .................................................................................................. 8

2.1 Structure of this section .............................................................................................. 8 2.2 Responses to Client Classification questions raised in CP 08/13 ......................... 8 2.3 Responses to Professional Qualification Requirements questions raised in

CP 08/13 ..................................................................................................................... 12 2.4 Responses to remuneration questions raised in CP 08/13 .................................. 15 2.5 Supplemental issue – the Overseas Person exemption ........................................ 17

3 NEXT STEPS ............................................................................................................................. 18

3.1 Introduction of the New Regime ............................................................................ 18

Appendix A............................................................................................................................................ 19

Persons that submitted responses (in some cases anonymised, at the respondent’s request): ................................................................................................................................. 19

Appendix B ............................................................................................................................................ 20

The IB Codes - with RFA amendments ONLY, track changed to reflect the decisions of this feedback paper ........................................................................................ 20 IB Codes Glossary ................................................................................................................ 20

Appendix C ............................................................................................................................................ 25

Updated Guidance Note: Professional Qualifications (Investment Business) track changed to reflect the decisions of this feedback paper ....................................... 25

Appendix D ........................................................................................................................................... 32

Definition of a Client ........................................................................................................... 32

Overview

6 of 32 Issued: 13 December 2013

1 OVERVIEW 1.1 Background

1.1.1 The Commission published Consultation Paper No. 8 2013 Proposed revisions of the Codes of Practice for Investment Business with respect to the Review of Financial Advice (“CP 08/13”) on 27 September 2013. CP 08/13 set out the Commission’s proposed amendments to the Codes of Practice for Investment Business (“IB Codes”); and updating of the Guidance Note: Professional Qualifications (Investment Business) (the “Guidance Note”), following the introduction of the Review of Financial Advice (“RFA”).

1.1.2 RFA is the Commission’s response to the RDR, initiated by the FSA and now being progressed by the FCA, one of the successor organisations to the FSA. The Commission considered the RDR and concluded that some of the concerns identified by the FSA also exist in Jersey.

1.1.3 The purpose of this paper is to provide feedback on responses received to CP 08/13.

1.2 Feedback on CP 08/13 1.2.1 The Commission received responses from the 16 persons listed in Appendix A.

Approximately one third of respondents answered all the questions, the reminder answered less than half of the questions in CP 08/13.

1.2.2 The Commission is grateful to all respondents for taking the time to consider and comment on CP 08/13.

1.2.3 The Commission also received a number of individual enquiries in response to CP 08/13, which have been attended to on an individual basis.

1.3 Summary of the issues 1.3.1 The issues identified in connection with the amendments to the IB Codes and

updated Guidance Note contained within CP 08/13 were as follows.

1.3.1.1 The responses received by the Commission suggest that for the majority of practitioners, there was very little in CP 08/13 which was unexpected. The tone of the majority of responses was to seek clarification of policy as opposed to a change in policy.

1.3.1.2 The Commission received a number of responses regarding the short notice between the publication of the definitive IB Codes and their implementation being too short for Industry to accommodate.

Overview

Feedback on CP08/13 Amending the IB Codes due to the RFA 7 of 32

1.3.2 With respect to 1.3.1.1, the Commission considered respondents comments carefully and has made some minor revisions to the IB Codes and the Guidance Note effectively to increase clarity with respect to client classification and remuneration, along with the addition of two acceptable qualifications and an amendment to the list of acceptable qualifications. These are discussed in section 2 and displayed respectively in full in Appendices B and C of this feedback paper.

1.3.3 With respect to 1.3.1.2, the Commission believes that a large percentage of Industry has accepted and largely prepared for the proposed policy changes to the IB Codes, brought on by the RFA project. Consequently, the Commission will proceed with its previously announced implementation date of 1 January 2014.

1.3.4 Notwithstanding this position, and in recognition of the short time frame between publication of this feedback paper, which contains the definitive text for the relevant paragraphs of the IB Codes, and 1 January 2014, the Commission issued a press release on 5 December 2013 confirming:

1.3.4.1 that the IB Codes text was to be materially implemented as consulted; and

1.3.4.2 that the amendments to the IB Codes resulting from the RFA project, continue to have an implementation date of 1 January 2014.

1.3.5 The press release also highlighted that this is in contrast to the position for amendments resulting from the Commission’s parallel work stream on amending seven of the issued Codes of Practice where a six-month transitional period is proposed for regulatory requirements that are either new or materially amended.

Summary of Responses

8 of 32 Issued: 13 December 2013

2 SUMMARY OF RESPONSES 2.1 Structure of this section

2.1.1 The questions posed in CP 08/13, a summary of the responses received and the Commission’s responses are set out in the following sections.

2.2 Responses to Client Classification questions raised in CP 08/13 Question 5.2.5

Do you consider that the proposed additional definitions to the IB Codes Glossary are clear and unambiguous? If not please explain your reasons and suggest alternative text which is consistent with Position Paper 2.

2.2.1 The Commission received several responses to this question, of which two considered that the definitions were clear and unambiguous. The remainder raised two separate issues; these concerned:

2.2.1.1 A suggested assumption that trust company clients (which the Commission interprets as meaning Trust Company Customers) could be automatically considered as per se Professional Clients; and

2.2.1.2 Whether the definition of a Large Undertaking would include special purpose vehicles and multiple companies held by one trust, or by one individual.

Commission response:

2.2.2 With respect to the assumption that Trust Company Customers can automatically be considered as per se Professional Clients, the Commission does not believe this is a valid assumption. As defined, a per se Professional Client is either a Large Undertaking or a Professional Investor, both of which have specific criteria against which each Class C or Class D client should be assessed.

2.2.3 As concerns the definition of a Large Undertaking and whether it would include special purpose vehicles and multiple companies held by one trust, or one individual, in ‘Feedback on Position Paper No.1’, the Commission considered a mechanism for defining clients as either a Professional Client or Retail Client. The Commission proposed a blended formula developed from the Guernsey and UK regulatory regimes; the latter being transposed from the Markets in Financial Instruments Directive 2004/39/EC (“MiFID”).

Summary of Responses

Feedback on CP08/13 Amending the IB Codes due to the RFA 9 of 32

2.2.4 A Large Undertaking and a Professional Investor are two defined terms which define a per se Professional Client; where there is a complex structure, the registered person should identify the underlying client. If the underlying client does not satisfy the criteria to be either a Large Undertaking or Professional Investor then the client must be assessed as a Retail Client, unless there are grounds for reassessing the Retail Client as an Elective Professional Client. This mechanism became the official position of the Commission in Position Paper No.2.

2.2.5 In view of respondents’ comments, the Commission will adopt the definitions proposed for the IB Codes glossary in CP 08/13.

2.2.6 To assist with understanding how the various terms associated with client classification interact please refer to Appendix D which provides a pictorial representation of the various terms.

Question 5.2.6

Do you consider the use of “net assets” rather than “own funds” an improvement which reduces the scope for ambiguity on this criterion in the Large Undertaking definition? If not please state your reasons and an alternative suggestion which is consistent with the position set out in Position Paper 2.

2.2.7 The Commission received several responses to this question; more than three quarters supported the use of the term “net assets” over “own funds”. Within those supportive responses, one asked for further clarification on the definition of “net assets”.

2.2.8 One respondent objected to the use of the term “net assets” citing that the term was more relevant to assessing the size of an entity; their preference for “own funds” was that the term refers to the capital and reserves belonging to the owners of an undertaking.

Commission response:

2.2.9 In responding to the request for further clarification of “net assets”, the Commission wishes to highlight that “net assets” is a defined term in the current IB Codes (defined as total assets less total liabilities). Albeit that the term is defined for the purpose of the registered person completing their financial resource calculation, the Commission considers that a registered person should utilise the same definition when assessing whether a client is a Large Undertaking.

2.2.10 As concerns the argument favouring “own funds” over “net assets”, the Commission re-considered this matter, and on balance concluded that its original argument as set out in paragraph 5.1.4.1.2 of CP 08/13 was valid, in that “own funds” has no meaning within the Jersey regulatory framework. The Commission is aware that “own funds” is a defined term of the UK’s regulatory regime, however the Commission understands that the definition of “own funds” is more complex than simply capital and reserves.

Summary of Responses

10 of 32 Issued: 13 December 2013

2.2.11 In view of support expressed by the majority of respondents and the complexity of “own funds”, the Commission has decided to proceed with “net assets” rather than “own funds” as one of the Large Undertaking criteria.

Question 5.2.7

Do you consider that the addition of paragraph 3.8 to the IB Codes clearly describes the requirements on registered persons, when conducting Class C or Class D investment business, to classify their clients in accordance with Position Paper 2? If not please state your reasons and an alternative suggestion which is consistent with the position set out in Position Paper 2.

2.2.12 Just over one third of the respondents answered this question, with half offering their support to the addition of proposed paragraph 3.8 of the IB Codes. The remainder broadly supported the paragraph, but sought greater clarity on a number of points, which the Commission outlines below.

2.2.13 Two respondents requested more prescriptive criteria around the assessment and opinion forming procedure for the reclassification of Retail Clients to Elective Professional Clients, to reduce the risk of inconsistent application of this procedure.

2.2.14 One respondent asked if the Commission expected the registered person to maintain a record of each client classification on file.

2.2.15 A second felt that the clear written warning, proposed in paragraph 3.8.4.1, which must be given to Elective Professional Clients that their adviser need not comply with the qualification standard as expressed in the proposed paragraph 3.3.2, gave the wrong impression on the standard of advice they may receive.

2.2.16 A third respondent, with Class C and D clients, commented on a number of aspects of the proposed paragraph 3.8 as follows:

2.2.16.1 They thought that, as drafted, paragraph 3.8.1 left scope for ambiguity, in that a registered person with Class C and D clients may have to classify all clients other than those using Class C and D investment business services.

2.2.16.2 They suggested amending paragraph 3.8.2.2 to “… transactions on which advice is being given …”, replacing “… transactions to be concluded …”.

2.2.16.3 They added that, as proposed, paragraph 3.8.2.2.2, which referenced the size of the client’s portfolio, was too restrictive, because assets that could not immediately be identified could not be included.

2.2.16.4 Lastly, with respect to proposed paragraph 3.8.6, concerning the identification of residency, the respondent objected to the requirement to identify the specific residency of all Class C and D clients. They believed that the only pertinent consideration was whether the client was a Jersey resident or not.

Summary of Responses

Feedback on CP08/13 Amending the IB Codes due to the RFA 11 of 32

Commission response:

2.2.17 As concerns the assessment and opinion forming procedure for the reclassification of a Retail Client to an Elective Professional Client; the Commission points out that the current proposal offers greater flexibility than the UK regime. The proposed paragraph 3.8 of the IB Codes does not impose the same degree of quantitative criteria imposed by the UK, thereby placing greater emphasis on the judgement of the registered person and its employees.

2.2.18 With respect to the question as to whether the registered person has to maintain a record of each client classification on file; consistent with paragraph 2.3 of the IB Codes (knowledge of client), the Commission expects every registered person to maintain an appropriate record of the classification of each Class C or D client.

2.2.19 With regards the point raised concerning the clear and written warning required in the proposed paragraph 3.8.4.1 and the potential to convey the wrong impression of the standard of advice of an investment employee to an Elective Professional Client; the Commission notes that, when complying with the IB Codes, the registered person has the implicit option to disclose to the client the professional qualifications of their nominated investment employee, which may be of a higher, lower or equal standard, should the client wish to become an Elective Professional Client. Consequently, the Commission does not believe that the obligations of proposed paragraph 3.8.4.1 will convey “the wrong impression” to Elective Professional Clients, hence it has decided to maintain the text as drafted.

2.2.20 In response to the point raised that there may be some confusion that registered persons with Class C and D investment business will have to classify all clients, including those in other Classes of investment business, the Commission recognises the possibility of this misunderstanding. Consequently the Commission has decided to amend the wording in paragraph 3.8.1, illustrated in the track change text below:

Amended Paragraph

3.8.1 Where a registered person carries on Class C or Class D investment business, the registered person must establish, implement and maintain internal policies, procedures and controls to classify its Class C or Class D clients as Retail Clients or Professional Clients.

2.2.21 As concerns the request to amend the text in proposed paragraph 3.8.2.2, to read “… transactions on which advice is being given …”, replacing “… transactions to be concluded …”. The Commission agrees that the clarity of the paragraph could be improved. Consequently, the Commission has decided to amend paragraph 3.8.2.2, using text from the current version of MiFID, illustrated in the track change text below:

Summary of Responses

12 of 32 Issued: 13 December 2013

Amended Paragraph

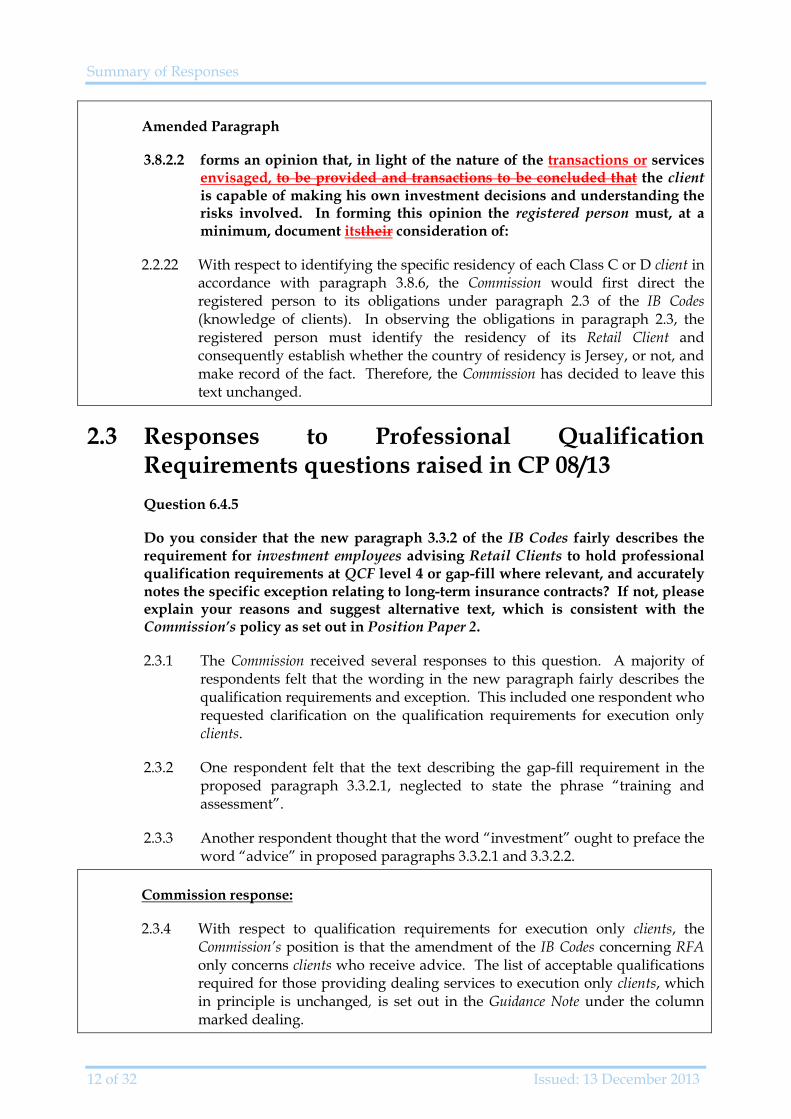

3.8.2.2 forms an opinion that, in light of the nature of the transactions or services envisaged, to be provided and transactions to be concluded that the client is capable of making his own investment decisions and understanding the risks involved. In forming this opinion the registered person must, at a minimum, document itstheir consideration of:

2.2.22 With respect to identifying the specific residency of each Class C or D client in accordance with paragraph 3.8.6, the Commission would first direct the registered person to its obligations under paragraph 2.3 of the IB Codes (knowledge of clients). In observing the obligations in paragraph 2.3, the registered person must identify the residency of its Retail Client and consequently establish whether the country of residency is Jersey, or not, and make record of the fact. Therefore, the Commission has decided to leave this text unchanged.

2.3 Responses to Professional Qualification Requirements questions raised in CP 08/13 Question 6.4.5

Do you consider that the new paragraph 3.3.2 of the IB Codes fairly describes the requirement for investment employees advising Retail Clients to hold professional qualification requirements at QCF level 4 or gap-fill where relevant, and accurately notes the specific exception relating to long-term insurance contracts? If not, please explain your reasons and suggest alternative text, which is consistent with the Commission’s policy as set out in Position Paper 2.

2.3.1 The Commission received several responses to this question. A majority of respondents felt that the wording in the new paragraph fairly describes the qualification requirements and exception. This included one respondent who requested clarification on the qualification requirements for execution only clients.

2.3.2 One respondent felt that the text describing the gap-fill requirement in the proposed paragraph 3.3.2.1, neglected to state the phrase “training and assessment”.

2.3.3 Another respondent thought that the word “investment” ought to preface the word “advice” in proposed paragraphs 3.3.2.1 and 3.3.2.2.

Commission response:

2.3.4 With respect to qualification requirements for execution only clients, the Commission’s position is that the amendment of the IB Codes concerning RFA only concerns clients who receive advice. The list of acceptable qualifications required for those providing dealing services to execution only clients, which in principle is unchanged, is set out in the Guidance Note under the column marked dealing.

Summary of Responses

Feedback on CP08/13 Amending the IB Codes due to the RFA 13 of 32

2.3.5 As concerns adding the phrase “training and assessment” to gap-fill in paragraph 3.3.2.1 of the amended IB Codes, the Commission has studied the terminology used by the FSA and believes that its phraseology is correct. The term gap-fill is described as a process of structured learning and verification of completion of that structured learning by the awarding body, formal examination is not an obligatory part of the gap-fill process.

2.3.6 With regards to the suggestion to preface the word “investment” ahead of “advice” in paragraphs 3.3.2.1 and 3.3.2.2, the Commission agrees with this suggestion and will amend the IB Codes and Guidance Note accordingly.

Question 6.4.6

In paragraph 6.1.6.2 of this consultation paper, the Commission has not adopted the FCA’s gap-fill completion date, but has adopted the date of 31 December 2013, so as not to impose retrospective regulation. However, this could cause administrative difficulties for qualifications providers and non-Jersey competent authorities. Do you consider this is a valid concern?

2.3.7 The Commission received several responses to this question, including one from the FCA. All respondents saw no administrative difficulties in having different dates in the UK and Jersey for the requirement to have completed gap-fill.

2.3.8 One respondent suggested that there should be no cut-off date for the completion of gap-fill.

Commission response:

2.3.9 The Commission notes the observation of the FCA that the employees of registered persons, who completed gap-fill after the RDR deadline of 31 December 2012, may only be Jersey qualified and not UK qualified. Their status under the UK regime will depend on when they were level 3 qualified, when they entered the investment advisory business and the specific gap-fill they completed.

“I can’t speak for the qualification providers, and I would suggest that you seek their views directly. So far as the FCA is concerned, we see no difficulty with the approach that you are taking, given that it will qualify advisers to your standards to practice in Jersey. The only potential problem could be if there was some confusion between the UK qualification and the Jersey qualification, but this should not arise so long as it is made clear to the candidates for gap fill that it is the Jersey qualification that they are being assessed to meet”.

Dermot Whelan, Manager / Governance & Professionalism Team / Policy, Risk and Research Division, FCA

2.3.10 With respect to not imposing a cut-off date for the completion of gap-fill, the Commission has adopted implementation arrangements similar to those set by the FSA and maintained by the FCA, with the same aims: firstly to minimalize disruption to clients, to registered persons and to investment employees; and secondly to implement the benefits of the new qualification standards as quickly as possible.

Summary of Responses

14 of 32 Issued: 13 December 2013

Question 6.4.7

If the date for gap-fill completion was set retrospectively how many investment employees would be affected and what percentage of total investment employees would this represent?

2.3.11 The Commission received four responses to this qualification. Only one respondent indicated that setting the gap-fill date retrospectively would have a material impact on their investment employees.

Commission response:

2.3.12 The Commission is pleased to note that based on the responses received it understands that many investment employees in Jersey were QCF Level 4 compliant by the FSA cut-off date.

Question 6.4.8

Can you suggest any improvements to the Guidance Note set out in Appendix B [of CP08/13]? If so, please state your reasons and your alternative suggested text.

2.3.13 Just under half of the respondents answered this question, of which two offered no further improvements to the Guidance Note.

2.3.14 One respondent made an observation of possible inconsistencies in the referencing of paragraphs 3.3.3 and 3.3.6. This respondent also queried the description of the acceptable qualification criteria of the CISI’s1 “Investment Advice Diploma”. Notably the reference that the “employee holds three modules including: the private client advice module, the securities module and the derivatives module”. The same respondent asked for a definition of what constitutes advice as this was important for firms providing execution only business.

2.3.15 A second respondent reiterated the concern they had raised in question 6.4.5, referencing an examination requirement for completion of gap-fill.

2.3.16 A third respondent requested the inclusion of two additional acceptable professional qualifications: CFA plus Investment Management Certificate (Level 4) Unit 1 (post 2010) and Level 1 of CFA Program plus Investment Management Certificate (Level 4) (post 2010).

2.3.17 The remainder of responses took the form of individual enquiries which were addressed individually by email.

1 Chartered Institute for Securities and Investment

Summary of Responses

Feedback on CP08/13 Amending the IB Codes due to the RFA 15 of 32

Commission response:

2.3.18 The Commission thanks the respondent for their observations on the referencing of the paragraphs and can confirm that paragraph 3.3.6 should read 3.3.4. However paragraph 3.3.3 is correct due to the insertion of new paragraph 3.3.2.

2.3.19 With respect to the description of the acceptable qualification criteria for the Investment Advice Diploma, the Commission understands that candidates have to sit and pass three modules to gain the Diploma. When studying for their third module, the candidate must select one of three specialisations: private client advice, securities or derivatives. Hence, the Commission notes this module specialisation in the Guidance Note, by the applicability of specific regulated functions that an Investment Advice Diploma holder may perform dependent on their third module selection.

2.3.20 With respect to defining “advice”, the Commission acknowledges that the word “advice” should be prefaced by “investment” in 2.3.14 above. “Investment Advice” is defined at Article 2(2)(c) of the FS(J)L.

2.3.21 The Commission agrees with the request to add the two CFA qualifications: CFA plus Investment Management Certificate (Level 4) Unit 1 and Level 1 of CFA Program plus Investment Management Certificate (Level 4) to its table of approved qualifications, as they are recognised by the FCA as meeting the Level 4 professional qualification criteria.

2.4 Responses to remuneration questions raised in CP 08/13 Question 7.3.3

Do you consider that the changes to Section 4 of the IB Codes, through the amendment of paragraph 4.6 and the addition of paragraphs 4.8 and 4.9, accurately describe the requirement that, other than in specific circumstances, registered persons can no longer be remunerated through commission? If not, please state your reasons and your alternative suggested text, which is consistent with Position Paper 2.

2.4.1 Over three quarters of respondents answered this question. One quarter of those respondents felt that the proposed amendments to Section 4 of the IB Codes accurately described the requirement that a registered person may no longer be remunerated by commission for Class C and D investment business, other than in specific circumstances, after 31 December 2013.

Summary of Responses

16 of 32 Issued: 13 December 2013

2.4.2 One respondent asked for a detailed definition of the term commission, and what portion of an upfront/one-off fee or recurring fee would be considered as a commission payment. This respondent cited examples of annual management charges at a portfolio level, annual management charges at a fund level and upfront fees on structured products. On a related matter, two other respondents requested detail on permissible adviser charges. A further respondent asked if receiving commission in respect of structured products was permissible.

2.4.3 Other respondents asked whether a ban on receiving commission was applicable to execution only and discretionary portfolio management services.

2.4.4 One respondent raised a question on whether a trust company, without an IB licence, which was placing client money in the absence of investment advice, could still receive retrocession payments; subject to the disclosure requirements in paragraph 4.2 of the Codes of Practice for Trust Company Business.

2.4.5 Two respondents raised a question on the permissibility of product providers facilitating adviser charging.

2.4.6 The remainder of responses took the form of individual enquiries which were addressed individually by email.

Commission response:

2.4.7 In response to the enquiry on the definition of commission, the permissibility of receiving up front, one-off, recurring fees and adviser charges and the question on permissibility of receiving commission from structured products, the Commission cannot offer an exhaustive list of circumstances that define commission payments and consequently does not define the term. In broad terms, the registered person cannot receive commission payments from product providers when providing investment advice to Jersey resident Retail Clients.

2.4.8 The Commission reiterates that registered persons will not be able to receive commission payments from product providers as a result of providing investment advice (Class C and Class D investment business) after 31 December 2013, subject to the limited exceptions set out in paragraphs 4.8.1 to 4.8.3 of the amended IB Codes. Remuneration in respect of execution only and discretionary investment management investment business is unaffected by the RFA.

2.4.9 With respect to the question as to whether trust companies, which the Commission interprets to mean persons registered to conduct Trust Company Business under the FS(J)L, could receive retrocession payments while placing client money in the absence of investment advice. The Commission agrees that this is permissible as this is not categorised as Class C or D investment business.

Summary of Responses

Feedback on CP08/13 Amending the IB Codes due to the RFA 17 of 32

2.4.10 As concerns the permissibility of product providers facilitating adviser charges, the Commission accepts that such practice is permissible. However, differences in adviser charges should be justifiable, to maintain the ethical integrity of the relationship between investment employee and Jersey resident Retail Client.

Question 8.3.2

Do you have any comments on our analysis of the costs and benefits?

2.4.11 The Commission did not receive any responses to this question.

Commission response:

2.4.12 Based on the absence of any comment on this question, the Commission concludes that nothing in CP 08/13 has changed the understanding of the costs and benefits associated with these amendments to the IB Codes.

2.5 Supplemental issue – the Overseas Person exemption 2.5.1 One issue drawn to the attention of the Commission outside the scope of the

questions in CP 08/13 concerned the Financial Services (Investment Business) (Overseas Persons – Exemption)) (Jersey) Order 2001 (“OPEO”) and how the OPEO interacts with the IB Codes post implementation of the RFA.

2.5.2 The issue concerns what constitutes relevant standards for the purpose of Article 1(5)(b) of the OPEO.

2.5.3 The Commission acknowledges that this is a potential concern however, the issue is not isolated to RFA and accordingly the Commission will give the matter further consideration as part of a separate piece of work in the context of overseas persons doing financial services business in Jersey.

Next Steps

18 of 32 Issued: 13 December 2013

3 NEXT STEPS 3.1 Introduction of the New Regime

3.1.1 The Commission has considered the comments received to CP 08/13 and will enact the necessary amendments to the IB Codes and updated Guidance Note with effect from 1 January 2014.

Appendix A

Feedback on CP08/13 Amending the IB Codes due to the RFA 19 of 32

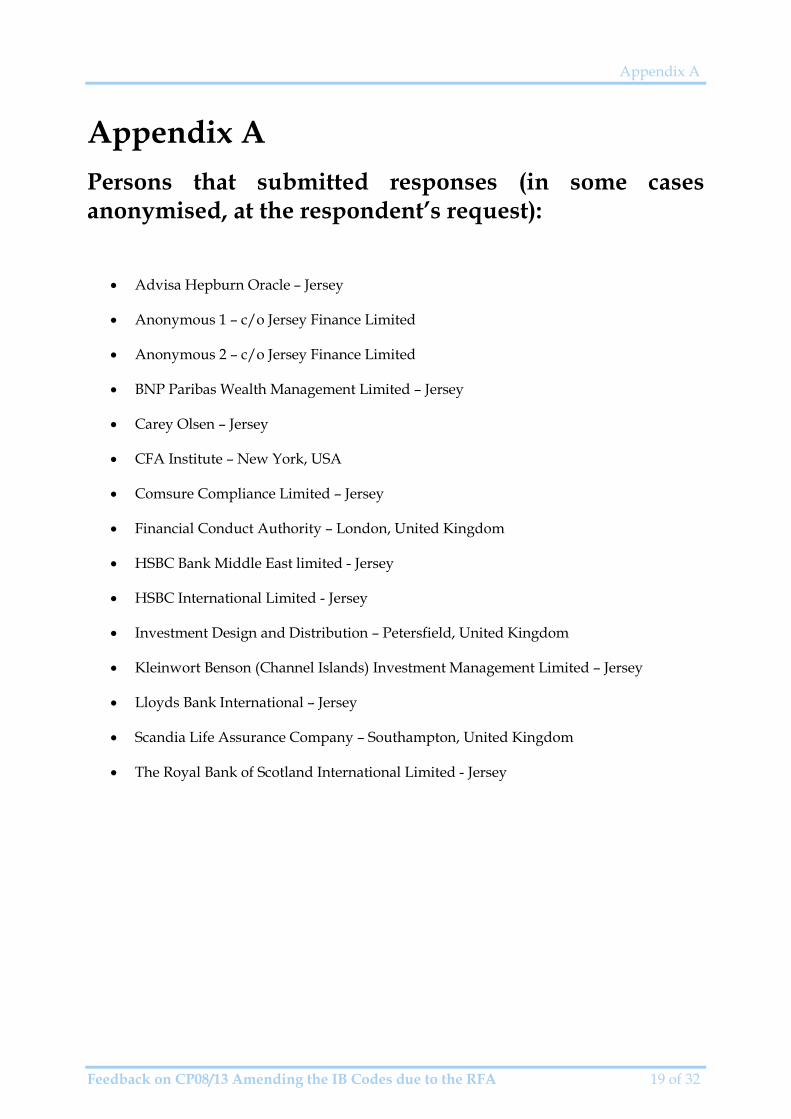

Appendix A Persons that submitted responses (in some cases anonymised, at the respondent’s request):

• Advisa Hepburn Oracle – Jersey

• Anonymous 1 – c/o Jersey Finance Limited

• Anonymous 2 – c/o Jersey Finance Limited

• BNP Paribas Wealth Management Limited – Jersey

• Carey Olsen – Jersey

• CFA Institute – New York, USA

• Comsure Compliance Limited – Jersey

• Financial Conduct Authority – London, United Kingdom

• HSBC Bank Middle East limited - Jersey

• HSBC International Limited - Jersey

• Investment Design and Distribution – Petersfield, United Kingdom

• Kleinwort Benson (Channel Islands) Investment Management Limited – Jersey

• Lloyds Bank International – Jersey

• Scandia Life Assurance Company – Southampton, United Kingdom

• The Royal Bank of Scotland International Limited - Jersey

Appendix B

20 of 32 Issued: 13 December 2013

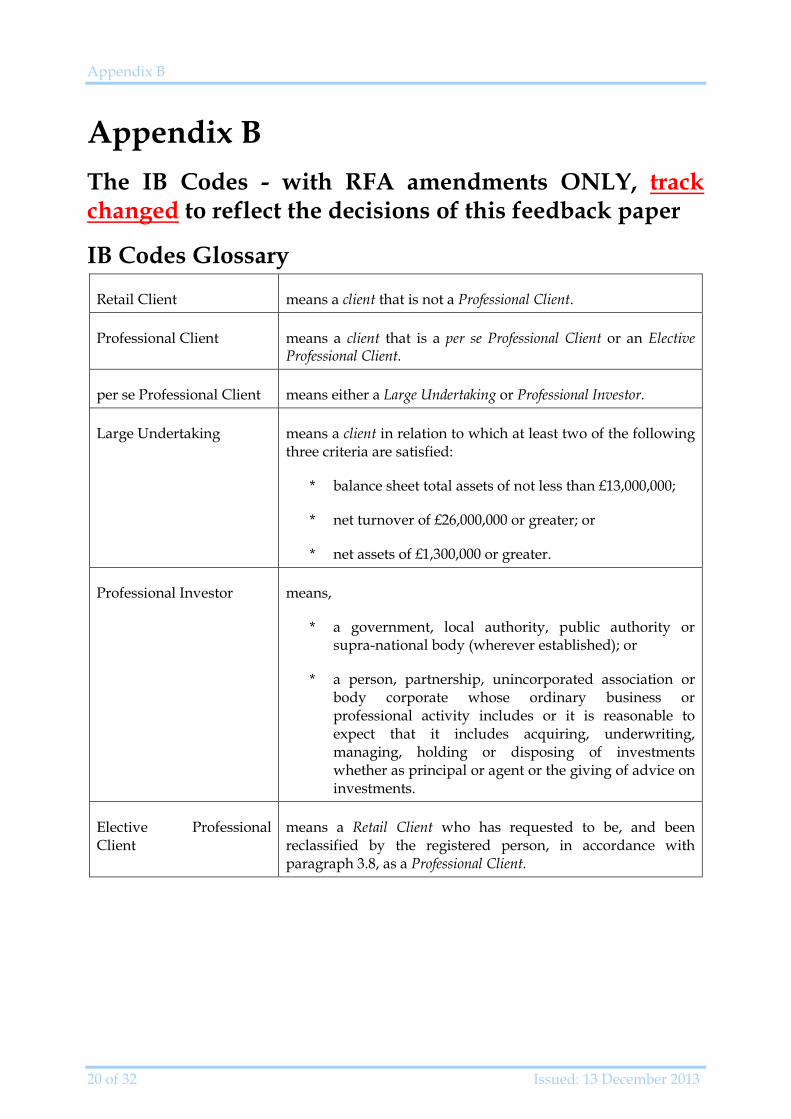

Appendix B The IB Codes - with RFA amendments ONLY, track changed to reflect the decisions of this feedback paper

IB Codes Glossary

Retail Client means a client that is not a Professional Client.

Professional Client means a client that is a per se Professional Client or an Elective Professional Client.

per se Professional Client means either a Large Undertaking or Professional Investor.

Large Undertaking means a client in relation to which at least two of the following three criteria are satisfied:

* balance sheet total assets of not less than £13,000,000;

* net turnover of £26,000,000 or greater; or

* net assets of £1,300,000 or greater.

Professional Investor means,

* a government, local authority, public authority or supra-national body (wherever established); or

* a person, partnership, unincorporated association or body corporate whose ordinary business or professional activity includes or it is reasonable to expect that it includes acquiring, underwriting, managing, holding or disposing of investments whether as principal or agent or the giving of advice on investments.

Elective Professional Client

means a Retail Client who has requested to be, and been reclassified by the registered person, in accordance with paragraph 3.8, as a Professional Client.

Appendix B

Feedback on CP08/13 Amending the IB Codes due to the RFA 21 of 32

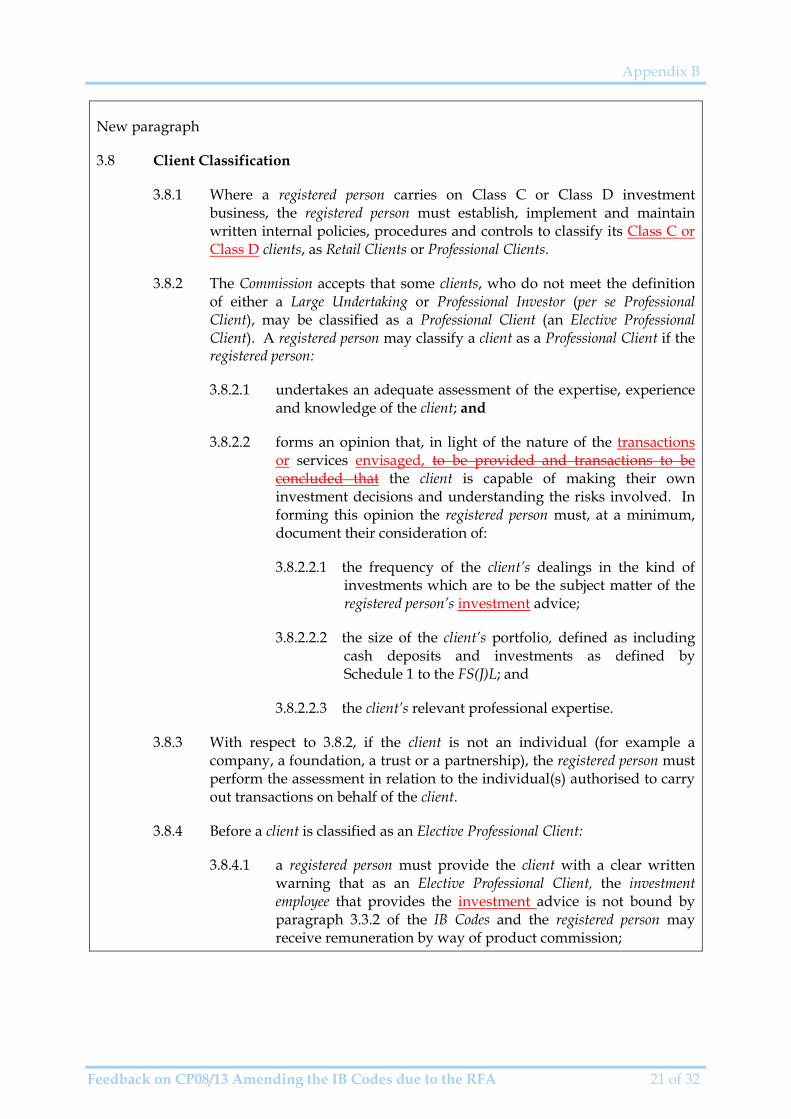

New paragraph

3.8 Client Classification

3.8.1 Where a registered person carries on Class C or Class D investment business, the registered person must establish, implement and maintain written internal policies, procedures and controls to classify its Class C or Class D clients, as Retail Clients or Professional Clients.

3.8.2 The Commission accepts that some clients, who do not meet the definition of either a Large Undertaking or Professional Investor (per se Professional Client), may be classified as a Professional Client (an Elective Professional Client). A registered person may classify a client as a Professional Client if the registered person:

3.8.2.1 undertakes an adequate assessment of the expertise, experience and knowledge of the client; and

3.8.2.2 forms an opinion that, in light of the nature of the transactions or services envisaged, to be provided and transactions to be concluded that the client is capable of making their own investment decisions and understanding the risks involved. In forming this opinion the registered person must, at a minimum, document their consideration of:

3.8.2.2.1 the frequency of the client’s dealings in the kind of investments which are to be the subject matter of the registered person’s investment advice;

3.8.2.2.2 the size of the client’s portfolio, defined as including cash deposits and investments as defined by Schedule 1 to the FS(J)L; and

3.8.2.2.3 the client’s relevant professional expertise.

3.8.3 With respect to 3.8.2, if the client is not an individual (for example a company, a foundation, a trust or a partnership), the registered person must perform the assessment in relation to the individual(s) authorised to carry out transactions on behalf of the client.

3.8.4 Before a client is classified as an Elective Professional Client:

3.8.4.1 a registered person must provide the client with a clear written warning that as an Elective Professional Client, the investment employee that provides the investment advice is not bound by paragraph 3.3.2 of the IB Codes and the registered person may receive remuneration by way of product commission;

Appendix B

22 of 32 Issued: 13 December 2013

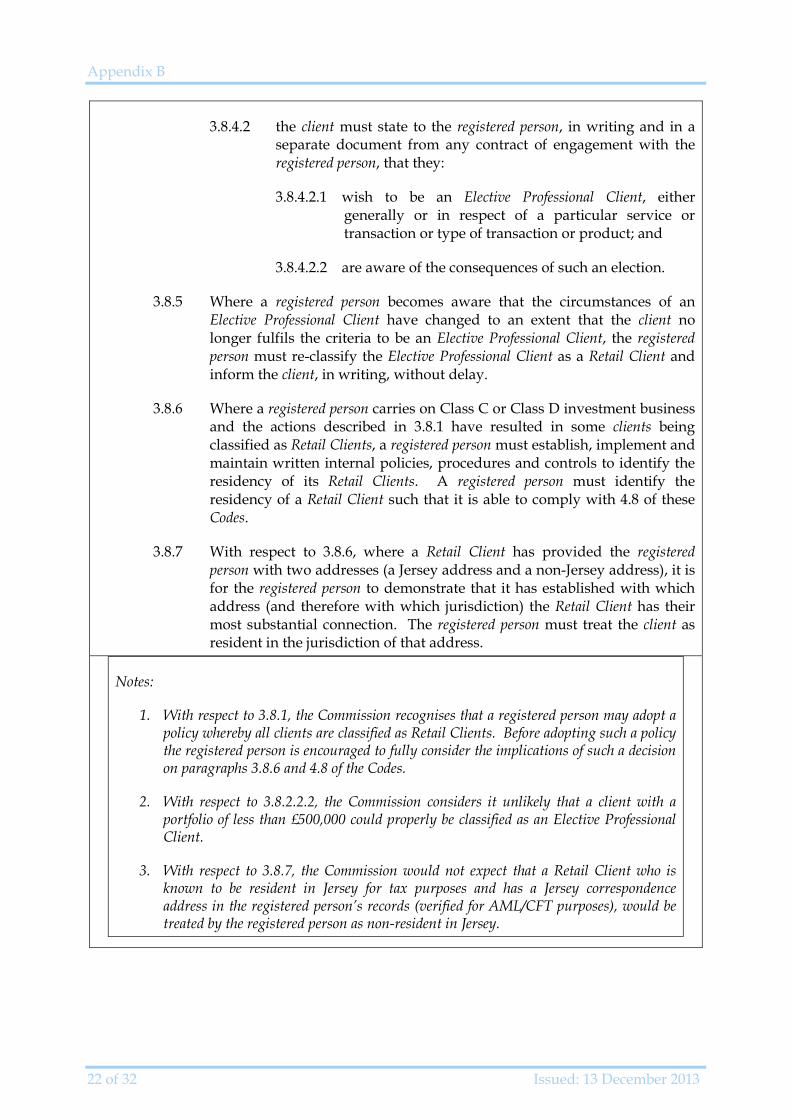

3.8.4.2 the client must state to the registered person, in writing and in a separate document from any contract of engagement with the registered person, that they:

3.8.4.2.1 wish to be an Elective Professional Client, either generally or in respect of a particular service or transaction or type of transaction or product; and

3.8.4.2.2 are aware of the consequences of such an election.

3.8.5 Where a registered person becomes aware that the circumstances of an Elective Professional Client have changed to an extent that the client no longer fulfils the criteria to be an Elective Professional Client, the registered person must re-classify the Elective Professional Client as a Retail Client and inform the client, in writing, without delay.

3.8.6 Where a registered person carries on Class C or Class D investment business and the actions described in 3.8.1 have resulted in some clients being classified as Retail Clients, a registered person must establish, implement and maintain written internal policies, procedures and controls to identify the residency of its Retail Clients. A registered person must identify the residency of a Retail Client such that it is able to comply with 4.8 of these Codes.

3.8.7 With respect to 3.8.6, where a Retail Client has provided the registered person with two addresses (a Jersey address and a non-Jersey address), it is for the registered person to demonstrate that it has established with which address (and therefore with which jurisdiction) the Retail Client has their most substantial connection. The registered person must treat the client as resident in the jurisdiction of that address.

Notes:

1. With respect to 3.8.1, the Commission recognises that a registered person may adopt a policy whereby all clients are classified as Retail Clients. Before adopting such a policy the registered person is encouraged to fully consider the implications of such a decision on paragraphs 3.8.6 and 4.8 of the Codes.

2. With respect to 3.8.2.2.2, the Commission considers it unlikely that a client with a portfolio of less than £500,000 could properly be classified as an Elective Professional Client.

3. With respect to 3.8.7, the Commission would not expect that a Retail Client who is known to be resident in Jersey for tax purposes and has a Jersey correspondence address in the registered person’s records (verified for AML/CFT purposes), would be treated by the registered person as non-resident in Jersey.

Appendix B

Feedback on CP08/13 Amending the IB Codes due to the RFA 23 of 32

New paragraph

3.3.2 With respect to 3.3.1.4.1:

3.3.2.1 All investment employees (apart from those that meet the exemption criteria of 3.3.2.2) providing investment advice to Retail Clients must hold a professional qualification at Qualifications and Credit Framework (“QCF”) level 4 or above, or level 3 with gap-fill where relevant.

3.3.2.2 Paragraph 3.3.2.1 does not apply to investment employees providing investment advice to Retail Clients on long term insurance contracts which fall within classes I, II or IV of Part 1 of Schedule 1 to the Insurance Business (Jersey) Law 1996, where the amount paid out does not depend on investment performance.

Amending paragraph

4.6 A registered person is required to demonstrate in writing that the client has been made aware of all associated fees and charges including commissions (both initial and recurring), where these are permissible, and any payments to or from third parties (such as introductory fees or commission sharing arrangements) - effectively a “no surprises” policy. This information must be disclosed prior to transactions being effected and information concerning commissions, fees and charges must include either a monetary or percentage figure. Any implications in relation to cancellation, failure to meet premiums and the ability and effect of making changes must also be made clear to the client in writing.

New paragraphs

4.8 A registered person carrying on Class C or Class D investment business is not permitted to receive remuneration by way of commission from product providers for investment advice services provided to Jersey resident Retail Clients, with the following exceptions:

4.8.1 where the Retail Client enters into or has entered into a long term insurance contract, as described in paragraph 3.3.2.2.;

4.8.2 where the Retail Client received investment advice and based on that investment advice entered into an investment, on or before 31 December 2013, for which trail commission remains payable; and

4.8.3 with respect to Retail Clients that transfer a portfolio of investments to a registered person, the registered person may be remunerated by trail commission payable on the existing investment portfolio in the following circumstances:

4.8.3.1 the investment permits the transference of trail commission to another registered person;

Appendix B

24 of 32 Issued: 13 December 2013

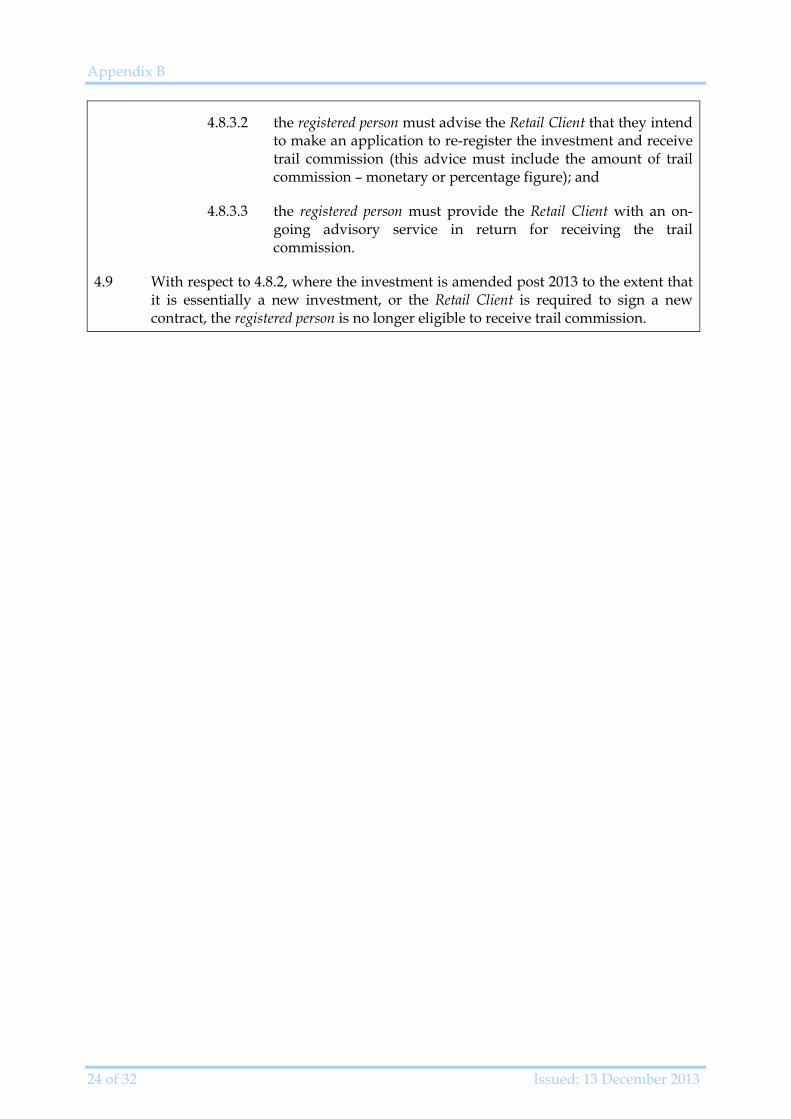

4.8.3.2 the registered person must advise the Retail Client that they intend to make an application to re-register the investment and receive trail commission (this advice must include the amount of trail commission – monetary or percentage figure); and

4.8.3.3 the registered person must provide the Retail Client with an on-going advisory service in return for receiving the trail commission.

4.9 With respect to 4.8.2, where the investment is amended post 2013 to the extent that it is essentially a new investment, or the Retail Client is required to sign a new contract, the registered person is no longer eligible to receive trail commission.

Appendix C

Feedback on CP08/13 Amending the IB Codes due to the RFA 25 of 32

Appendix C Updated Guidance Note: Professional Qualifications (Investment Business) track changed to reflect the decisions of this feedback paper 1 Guidance

1.1 Section 3.3 of the Codes of Practice for Investment Business (the “IB Codes”) requires a registered person to assess and monitor the competence of its employees. Paragraph 3.3.1.4 of the IB Codes details the competency requirements for a registered person’s employees.

1.2 One method by which competence can be assessed is by reference to professional qualifications that an employee may hold. Paragraph 3.3.1.4.1 of the IB Codes states that all investment employees must have obtained a professional qualification appropriate to their role.

1.3 The Review of Financial Advice (“RFA”), a key part of the Commission’s consumer protection strategy, identified a need to raise the professional standards of investment employees. Accordingly, the IB Codes require that, from 1 January 2014, any investment employee providing investment advice to Retail Clients (as defined in the IB Codes) must hold an appropriate professional qualification at Qualifications and Credit Framework level 4 or above, or level 3 with gap-fill where relevant, as described in paragraph 3.3.2 of the IB Codes.

1.4 This Guidance Note contains, within section 2 below, details of professional qualifications that are acceptable to the Commission when held by investment employees who perform various regulated functions within investment businesses. This Guidance Note should be read in conjunction with the IB Codes.

1.5 The IB Codes state that a registered person is responsible for ensuring that its employees are appropriately qualified for the role (or roles) that they perform. Registered persons should be aware that a qualification that is suitable, for example, for an employee that provides investment advice to professional clients may not be acceptable for a different activity, such as managing investments or providing investment advice to Retail Clients.

1.6 The Commission is aware of the availability of many accredited investment related professional qualifications. Qualifications that are not listed within this Guidance Note (for example, qualifications provided by overseas awarding bodies or others included in the Appropriate Qualification Tables2 of the UK Financial Conduct Authority (the “FCA”)) may be accepted by the Commission as equivalent to those referenced in the table below. When considering the FCA Appropriate Qualification Table, reference is necessary to the FCA list of Appropriate Qualification Activities3.

2 www.fshandbook.info/FS/html/FCA/TC/App/4/1 3 www.fshandbook.info/FS/html/handbook/TC/App/1/1

Appendix C

26 of 32 Issued: 13 December 2013

1.7 Paragraph 3.3.46 of the IB Codes details the process by which an application may be made to the Commission for alternative qualifications to receive consideration.

1.8 Where paragraph 3.3.3 of the IB Codes is relevant (complex transactions are undertaken or complex investments are advised upon, for example derivatives), a registered person may wish to refer to the list of the FCA’s list of Appropriate Qualifications Activities and Appropriate Qualification Tables to consider whether the qualification of an investment employee is compatible with a particular investment activity.

1.9 The table of qualifications contained in section 2 of this Guidance Note will be reviewed and updated periodically to take into account changes to qualifications, including the addition of new relevant qualifications, and comments received from the investment business industry.

1.10 Please note that some qualifications may only be considered appropriate for “Advising Retail Clients” when combined with qualification gap-fill. Gap-fill constitutes additional structured continuing professional development, which need not involve examination, completed by an investment employee, and verified by an accredited body as approved by the FCA. Consequently, the table of qualifications includes two columns relating to “Advising Retail Clients” to highlight those qualifications where gap-fill is relevant.

Appendix C

Feedback on CP08/13 Amending the IB Codes due to the RFA 27 of 32

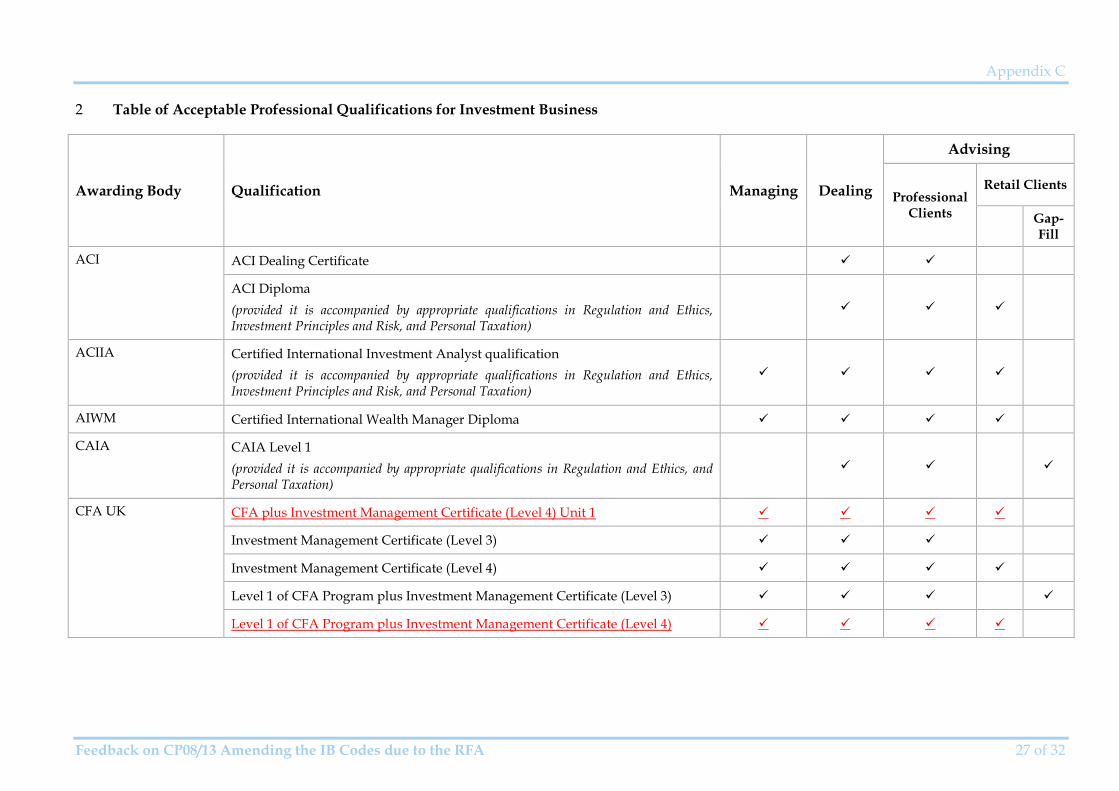

2 Table of Acceptable Professional Qualifications for Investment Business

Awarding Body Qualification Managing Dealing

Advising

Professional Clients

Retail Clients

Gap-Fill

ACI ACI Dealing Certificate

ACI Diploma (provided it is accompanied by appropriate qualifications in Regulation and Ethics, Investment Principles and Risk, and Personal Taxation)

ACIIA Certified International Investment Analyst qualification (provided it is accompanied by appropriate qualifications in Regulation and Ethics, Investment Principles and Risk, and Personal Taxation)

AIWM Certified International Wealth Manager Diploma

CAIA CAIA Level 1 (provided it is accompanied by appropriate qualifications in Regulation and Ethics, and Personal Taxation)

CFA UK CFA plus Investment Management Certificate (Level 4) Unit 1

Investment Management Certificate (Level 3)

Investment Management Certificate (Level 4)

Level 1 of CFA Program plus Investment Management Certificate (Level 3)

Level 1 of CFA Program plus Investment Management Certificate (Level 4)

Appendix C

28 of 32 Issued: 13 December 2013

Awarding Body Qualification Managing Dealing

Advising

Professional Clients

Retail Clients

Gap-Fill

CII Certificate in Financial Planning

Certificate in Mortgage Advice4

Certificate in Securities Advice and Dealing

Certificate in Discretionary Investment Management

Mortgage Advice Qualification5

Advanced Financial Planning Certificate

Diploma in Financial Planning

Diploma in Regulated Financial Planning

Advanced Diploma in Financial Planning

Fellow (FCII) (where investment employee holds an appropriate life module)

Fellow (FLIA Dip)

CISI Certificate in Investment Management

4 This qualification is only acceptable for providing advice on long–term insurance contracts where such advice is directly related to a mortgage. 5 This qualification is only acceptable for providing advice on long–term insurance contracts where such advice is directly related to a mortgage.

Appendix C

Feedback on CP08/13 Amending the IB Codes due to the RFA 29 of 32

Awarding Body Qualification Managing Dealing

Advising

Professional Clients

Retail Clients

Gap-Fill

CISI (cont.) Certificate in Securities (CISI’s Certificate programme is the replacement for the SFA Registered Representative qualification.)

Certificate in Securities & Financial Derivatives

Investment Advice Certificate

International Certificate in Financial Advice

Certificate in Private Client Investment Advice and Management

Diploma (where investment employee holds three modules as recommended by the registered person)

Investment Advice Diploma: where investment employee holds three modules including:

the private client advice module

the securities module

derivatives module

Diploma in Wealth Management (Level 6)

Masters in Wealth Management Post 2010 examination standards

Pre 2010 examination standards

Appendix C

30 of 32 Issued: 13 December 2013

Awarding Body Qualification Managing Dealing

Advising

Professional Clients

Retail Clients

Gap-Fill

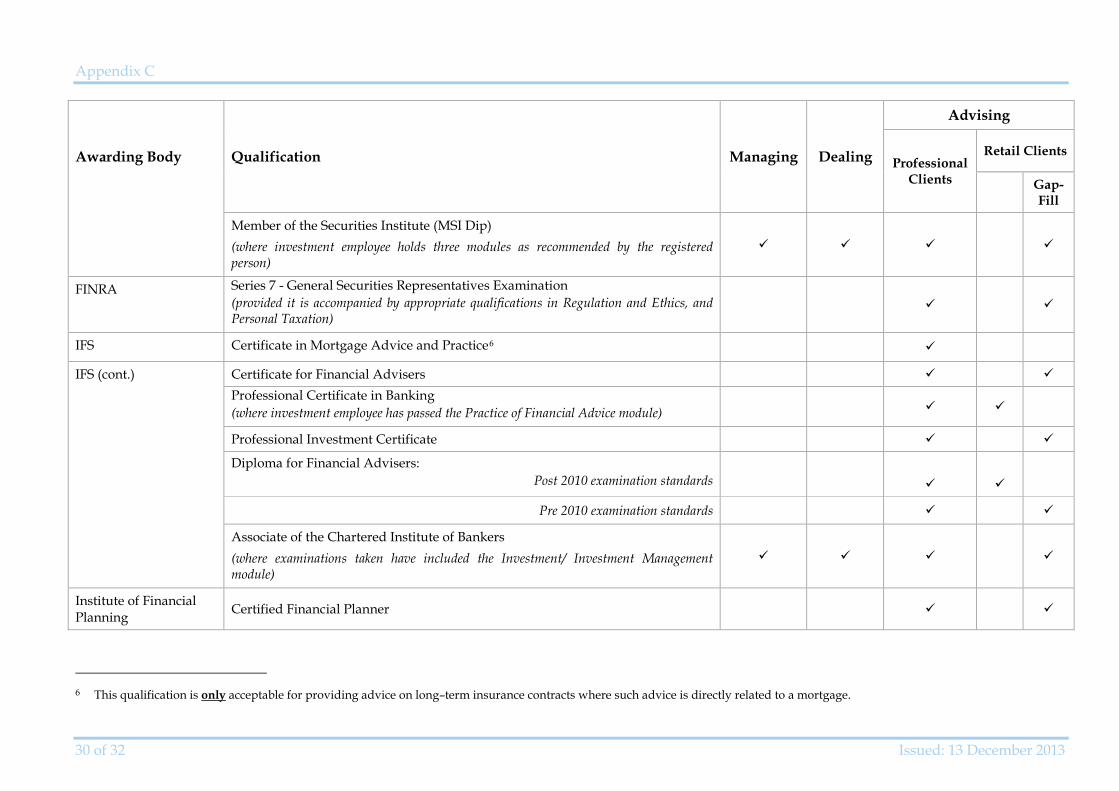

Member of the Securities Institute (MSI Dip) (where investment employee holds three modules as recommended by the registered person)

FINRA Series 7 - General Securities Representatives Examination (provided it is accompanied by appropriate qualifications in Regulation and Ethics, and Personal Taxation)

IFS Certificate in Mortgage Advice and Practice6

IFS (cont.) Certificate for Financial Advisers Professional Certificate in Banking (where investment employee has passed the Practice of Financial Advice module)

Professional Investment Certificate

Diploma for Financial Advisers: Post 2010 examination standards

Pre 2010 examination standards

Associate of the Chartered Institute of Bankers (where examinations taken have included the Investment/ Investment Management module)

Institute of Financial Planning Certified Financial Planner

6 This qualification is only acceptable for providing advice on long–term insurance contracts where such advice is directly related to a mortgage.

Appendix C

Feedback on CP08/13 Amending the IB Codes due to the RFA 31 of 32

Awarding Body Qualification Managing Dealing

Advising

Professional Clients

Retail Clients

Gap-Fill

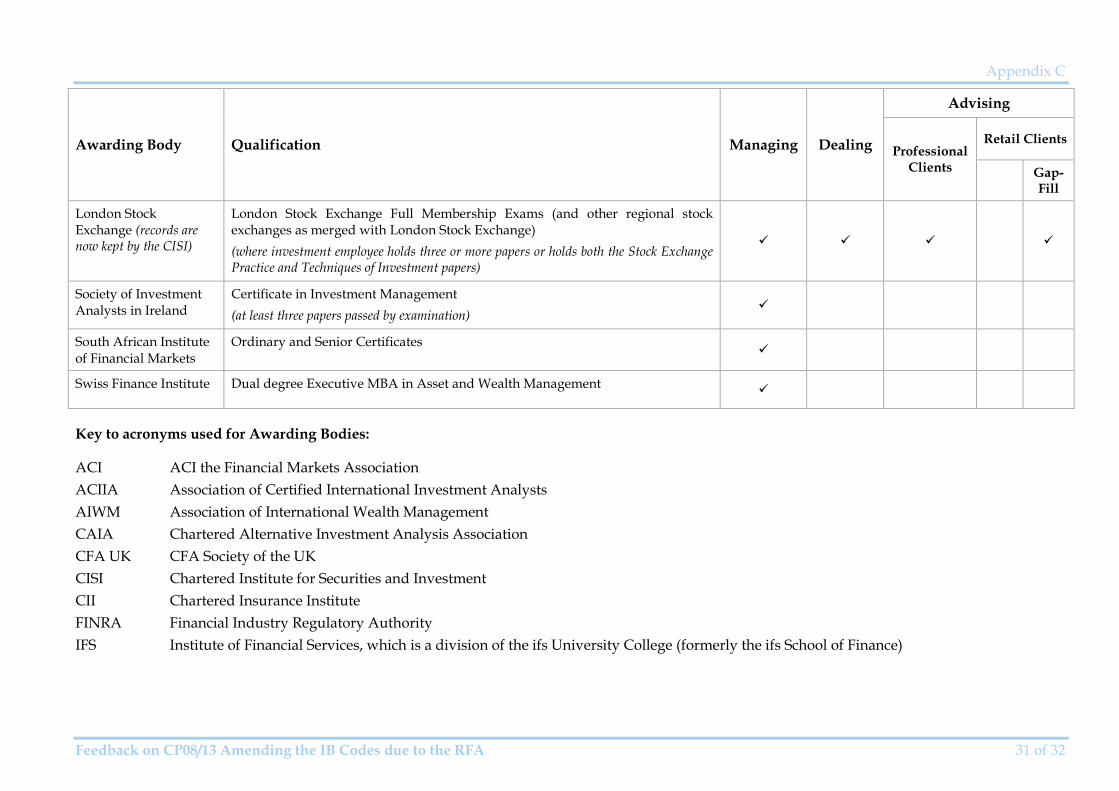

London Stock Exchange (records are now kept by the CISI)

London Stock Exchange Full Membership Exams (and other regional stock exchanges as merged with London Stock Exchange) (where investment employee holds three or more papers or holds both the Stock Exchange Practice and Techniques of Investment papers)

Society of Investment Analysts in Ireland

Certificate in Investment Management (at least three papers passed by examination)

South African Institute of Financial Markets

Ordinary and Senior Certificates

Swiss Finance Institute Dual degree Executive MBA in Asset and Wealth Management

Key to acronyms used for Awarding Bodies:

ACI ACI the Financial Markets Association ACIIA Association of Certified International Investment Analysts AIWM Association of International Wealth Management CAIA Chartered Alternative Investment Analysis Association CFA UK CFA Society of the UK CISI Chartered Institute for Securities and Investment CII Chartered Insurance Institute FINRA Financial Industry Regulatory Authority IFS Institute of Financial Services, which is a division of the ifs University College (formerly the ifs School of Finance)

Appendix D

32 of 32 Issued: 13 December 2013

Appendix D Definition of a Client

Client

Retail Client

Jersey Resident Non-Jersey Resident

Professional Client

Elective Professional

Client

per se Professional

Client

Large Undertaking

Professional Investor