Embed Size (px)

Citation preview

Proposed supermarket and shops Eastern Road, Turramurra

Retail Impact Assessment

Prepared for: ALDI Stores Ltd

August 2015

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd i

Principal Chris Abery [email protected] 03 8825 5877 Senior Associate Alexandra Hopley Project Code DA1519 Date 8 August 2015

Disclaimer This report has been prepared by Deep End Services Pty Ltd solely for use by the party to whom it is addressed. Accordingly, any changes to this report will only be notified to that party. Deep End Services Pty Ltd, its employees and agents accept no responsibility or liability for any loss or damage which may arise from the use or reliance on this report or any information contained therein by any other party and gives no guarantees or warranties as to the accuracy or completeness of the information contained in this report. This report contains forecasts of future events. These forecasts are based upon numerous sources of information, including historical and forecast data provided by organisations such as ALDI Stores Ltd, Australian Bureau of Statistics, Deloitte Access Economics, MapInfo Australia and Market Data Systems. It is not always possible to verify that this information is accurate or complete. It should be noted that the factors influencing the findings in this report may change and hence Deep End Services Pty Ltd cannot accept responsibility for reliance upon such findings beyond a date that is six months from the date of this report. Beyond that date, a review of the findings contained in this report may be necessary. This report should be read in its entirety, as reference to part only may be misleading.

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd ii

Table of Contents

1. Introduction ................................................................................................................. 1 1.1 Background ........................................................................................................... 1 1.2 Retail impact report .............................................................................................. 2

2. ALDI proposal ............................................................................................................... 3 2.1 ALDI profile ........................................................................................................... 3 2.2 Eastern Road proposal .......................................................................................... 6 2.2.1 Site description ..................................................................................................... 6 2.2.2 Proposed development ......................................................................................... 7

3. Existing centres .......................................................................................................... 10 3.1 Overview ............................................................................................................. 10 3.2 Neighbourhood Centres...................................................................................... 12 3.2.1 Eastern Road Turramurra.................................................................................... 12 3.2.2 Bannockburn Road Turramurra .......................................................................... 12 3.2.3 North Turramurra ............................................................................................... 13 3.2.4 Colonial Centre, St Ives Chase ............................................................................. 13 3.2.5 East Wahroonga .................................................................................................. 14 3.2.6 Waitara, East Hornsby ........................................................................................ 14 3.3 Local Centres....................................................................................................... 15 3.3.1 Turramurra ......................................................................................................... 15 3.3.2 St Ives .................................................................................................................. 16 3.3.3 Pymble ................................................................................................................ 17 3.3.4 Wahroonga ......................................................................................................... 17 3.4 Conclusions ......................................................................................................... 18

4. Trade area analysis ..................................................................................................... 19 4.1 Regional population growth ............................................................................... 19 4.2 Trade area definition .......................................................................................... 19 4.3 Trade area population ........................................................................................ 21 4.4 Population characteristics ................................................................................... 21 4.5 Retail spending ................................................................................................... 24

5. Supermarket supply and demand ............................................................................... 27 5.1 Supermarket floorspace provision by municipality ............................................. 27 5.2 Supermarket accessibility ................................................................................... 29 5.3 Supermarket distribution .................................................................................... 30

6. Retail impact assessment ........................................................................................... 31 6.1 Projected sales .................................................................................................... 31 6.2 Trading impacts .................................................................................................. 32 6.3 Impact conclusions ............................................................................................. 35 6.4 Benefits of ALDI development ............................................................................ 36 6.4.1 Employment benefits .......................................................................................... 36 6.4.2 Other benefits ..................................................................................................... 37

7. Conclusions ................................................................................................................ 38

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd iii

Tables

Table 1: Centres floorspace summary by category ................................................................ 11 Table 2: Trade area population.............................................................................................. 21 Table 3: Trade area characteristics ........................................................................................ 23 Table 4: Trade area spending estimates ................................................................................ 26 Table 5: Eastern Rd, Turramurra development projected sales (2017) ................................. 31 Table 6: ALDI Eastern Rd, Turramurra site market shares – 2017 ......................................... 32 Table 7: ALDI Eastern Rd, Turramurra site trading impacts ................................................... 33

Figures

Figure 1: Site location ............................................................................................................... 1 Figure 2: ALDI store network, Sydney ....................................................................................... 3 Figure 3: Eastern Rd, Turramurra site ....................................................................................... 6 Figure 4: Eastern Road indicative elevation .............................................................................. 8 Figure 5: Tennyson Avenue indicative elevation....................................................................... 8 Figure 6: Site plan – ground level .............................................................................................. 9 Figure 7: Roof top car park ....................................................................................................... 9 Figure 8: Centres hierarchy and supermarkets ....................................................................... 10 Figure 9: Centres floorspace mix ............................................................................................ 11 Figure 10: Ku-ring-gai LGA population ...................................................................................... 19 Figure 11: ALDI Eastern Rd, Turramurra trade area .................................................................. 20 Figure 12: FLG spend per capita variation to Sydney average .................................................. 25 Figure 13: Per capita spending rate comparisons ..................................................................... 25 Figure 14: Supermarket provision by local government area ................................................... 28 Figure 15: Sydney supermarket accessibility ............................................................................ 29 Figure 16: Trade area supermarket accessibility ....................................................................... 30 Figure 17: ALDI Eastern Rd, Turramurra source of sales - 2017 ................................................ 35

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 1

1. Introduction

1.1 Background

ALDI Stores is seeking the rezoning of land partly bounded by Eastern Rd, Tennyson Ave and Alice St, Turramurra from the Low Density Residential 2 (R2) Zone to the Neighbourhood Centre (B1) Zone. The rezoning will facilitate the development of an ALDI supermarket of 1,585 sqm (GFA) and two shops (370 sqm). It effectively extends the existing Eastern Road neighbourhood centre north, over land currently used for commercial purposes.

Figure 1: Site location

Source: Deep End Services; Ausway

Under the Ku-ring-gai Local Environmental Plan (LEP) 2015, the objective of the ‘Zone B1 Neighbourhood Centre’ is:

• To provide a range of small-scale retail, business and community uses that serve the needs of people who live or work in the surrounding neighbourhood.

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 2

Under ‘Part 6 Additional Local Provisions’ of the LEP, Clause 6.9 ‘Development in Zone B1’ states the following:

(1) The objective of this clause is to maintain the commercial hierarchy of Ku-ring-gai by encouraging retail development of an appropriate scale within neighbourhood centres.

(2) Development consent must not be granted to development for the purposes of commercial premises on land in Zone B1 Neighbourhood Centre if the development would result in the premises having a gross floor area of more than 1,000 square metres.

(3) In deciding whether to grant development consent referred to in subclause (2) to development for the purposes of commercial premises having a gross floor area of 500 square metres or more, in either one separate tenancy or any number of tenancies, the consent authority must consider the economic impact of the development

Deep End Services has been instructed by Milestone Management on behalf of ALDI Stores Ltd to prepare an independent retail impact report for the purpose of accompanying the rezoning application and any concurrent or subsequent development application.

1.2 Retail impact report

The objective of this report is to assess the need and demand for the proposed ALDI store and assess the likely trading impacts on other centres in the catchment area. Future employment and other benefits are also considered.

In the preparation for this report, the subject site and other retail centres in the area were inspected in June 2015.

This report contains the following sections:

• Section 2 discusses the site and proposed development.

• Section 3 reviews the size and composition of existing centres and how the ALDI proposal sits in the centres hierarchy.

• Section 4 defines the trade area for the site with population and retail spending forecasts and demographic characteristics.

• Section 5 examines supply and demand for supermarket floorspace in the region and concludes whether the region can support the ALDI proposal based on population growth and industry benchmarks.

• Section 6 presents the retail impact assessment including projected sales for the proposed development, estimated trading effects and implications on surrounding centres. The employment, consumer and other community benefits are also presented.

• Section 7 presents the overall conclusions.

All references to spending and sales / turnover levels in this report are at constant 2015 prices and include GST.

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 3

2. ALDI proposal

This section outlines ALDI’s profile and business model and the proposed development at Eastern Rd, Turramurra.

2.1 ALDI profile

ALDI is an international retail chain with over 8,000 stores across 15 European countries, the United States and Australia. Since the first Australian store opened in January 2001, ALDI’s network has grown to 374 stores in Victoria, New South Wales, ACT and Queensland. In 2012, ALDI announced its expansion into South Australia and Western Australia commencing in 2016.

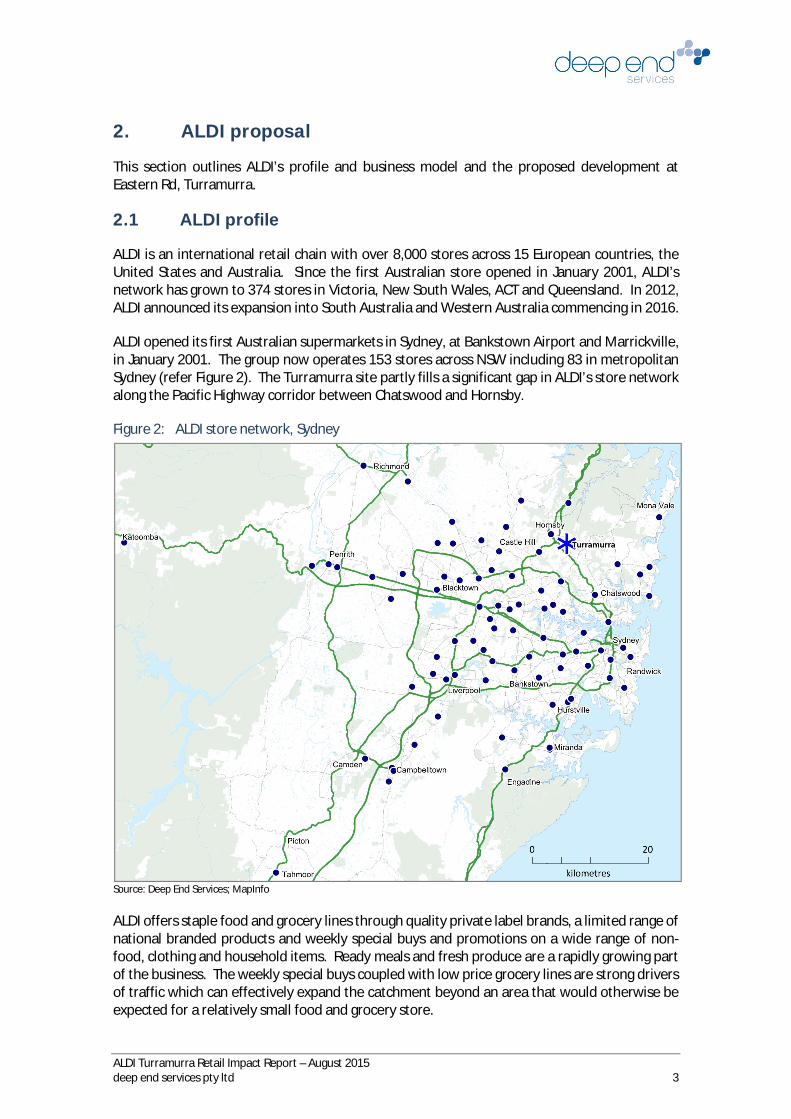

ALDI opened its first Australian supermarkets in Sydney, at Bankstown Airport and Marrickville, in January 2001. The group now operates 153 stores across NSW including 83 in metropolitan Sydney (refer Figure 2). The Turramurra site partly fills a significant gap in ALDI’s store network along the Pacific Highway corridor between Chatswood and Hornsby.

Figure 2: ALDI store network, Sydney

Source: Deep End Services; MapInfo

ALDI offers staple food and grocery lines through quality private label brands, a limited range of national branded products and weekly special buys and promotions on a wide range of non-food, clothing and household items. Ready meals and fresh produce are a rapidly growing part of the business. The weekly special buys coupled with low price grocery lines are strong drivers of traffic which can effectively expand the catchment beyond an area that would otherwise be expected for a relatively small food and grocery store.

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 4

The business model aims to reduce operating costs through the supply chain, store development and layouts, merchandising, store operations and marketing with savings passed to the consumer through lower prices. ALDI is the only ‘hard discount’ food and grocery chain in Australia.

In June 2015, the national consumer group, ‘Choice’, published the results of a price comparison of 31 grocery items sold by Coles, Woolworths and ALDI across 93 supermarkets in Australia. The sample of supermarkets was spread across 17 cities and clustered to ensure there was local competition between stores. The published results showed that ALDI’s basket of groceries was:

• 23% cheaper than Coles’ and 26% cheaper than Woolworths’ on comparable home brand or private label products; and

• 46% cheaper than Coles’ and 50% cheaper than Woolworths’ on comparable national or leading brand products.

The ALDI model can be readily distinguished from traditional supermarkets on offer in Australia. For example, each ALDI store has a product range of approximately 1,500 separate stock keeping units (SKUs) compared with the 20,000-30,000 SKUs on offer at national full-line supermarket chains such as Woolworths or Coles. The size of an ALDI store is much smaller at approximately 1,550 sqm compared to 3,000-4,000 sqm (gross retail floor area) for a new full-line store operated by Coles or Woolworths.

This unique customer proposition and differentiated format enables ALDI to successfully operate in close proximity to the major chains. In Australia, ALDI has direct competition from Coles and/or Woolworths in approximately 80% of its locations.

The smaller store format also allows ALDI to establish in small markets and neighbourhood centres providing choice and convenience for local communities.

Internal images of a typical new store are shown on the following page.

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 5

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 6

2.2 Eastern Road proposal

2.2.1 Site description

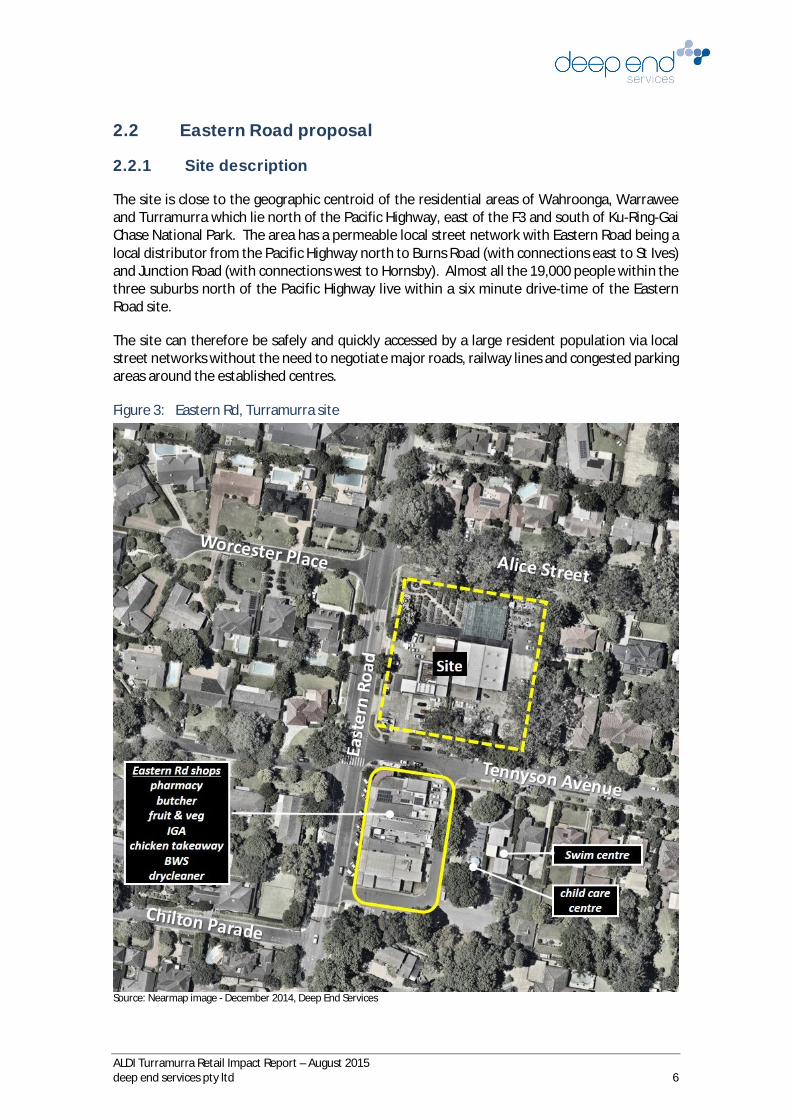

The site is close to the geographic centroid of the residential areas of Wahroonga, Warrawee and Turramurra which lie north of the Pacific Highway, east of the F3 and south of Ku-Ring-Gai Chase National Park. The area has a permeable local street network with Eastern Road being a local distributor from the Pacific Highway north to Burns Road (with connections east to St Ives) and Junction Road (with connections west to Hornsby). Almost all the 19,000 people within the three suburbs north of the Pacific Highway live within a six minute drive-time of the Eastern Road site.

The site can therefore be safely and quickly accessed by a large resident population via local street networks without the need to negotiate major roads, railway lines and congested parking areas around the established centres.

Figure 3: Eastern Rd, Turramurra site

Source: Nearmap image - December 2014, Deep End Services

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 7

The square-shaped site of approximately 5,129 sqm is situated directly north of the existing Eastern Road shops in Turramurra. It has frontages to Tennyson Avenue, Eastern Rd, and Alice Street (refer Figure 3).

The site is currently used by a petrol station incorporating a motor mechanic and Parkers of Turramurra garden centre, which includes a gift shop and café.

Surrounding uses include:

• The Eastern Road Turramurra shops directly south of the site across Tennyson Avenue. This small neighbourhood shopping strip has a small IGA supermarket, pharmacy, butcher, green grocer, BWS liquor store, drycleaner and takeaway food.

• A child care centre and car parking south and to the rear of the existing shops.

• A small private swim school off Tennyson Avenue.

Within 700 metres of the site is Wahroonga Public School, Knox Grammar Sports Fields, Turramurra Memorial Park and Turramurra Oval and tennis courts. The surrounding residential area is characterised by attractive, tree-lined streets with large established homes and gardens.

Site looking west from corner Tennyson Ave & Eastern Road

2.2.2 Proposed development

The proposed development is a freestanding ALDI supermarket (1,585 sqm GLA), specialty shops (370 sqm GLA) and associated car parking. The retail buildings are set close to the Eastern Road and Tennyson Avenue frontages presenting a glazed or activated built form with articulated setbacks providing a forecourt and raised seating area on the street corner and a tree preservation and landscaped area on Tennyson Avenue.

The ALDI store is positioned mid-block on Eastern Road with its pedestrian entry off the Eastern Road forecourt. The store is laid out as a 5-aisle non-generic footprint with a fully glazed shop-front to Eastern Road. Storage, amenities and loading dock areas are shielded by the two shops and landscaping along Tennyson Avenue.

The larger shop (200 sqm) of the two, has a corner location with three glazed external walls and access to the forecourt and seating area. This shop is well suited to a café or restaurant use. The second shop (170 sqm) is at the eastern end of the Tennyson Street frontage set back behind

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 8

the landscaped area and accessed by its own footbath around the preserved Eucalypt. This shop would suit a hairdresser, beautician or other personal service tenancy.

On-site parking is provided for 83 spaces at the rate of 4.25 spaces per 100 sqm of retail floorspace. Given the normally high turnover of spaces in a small neighbourhood centre, this is an acceptable parking level for the operation of the supermarket and shops.

All on-site parking is provided at roof top level which is accessed via a two-way vehicle ramp from Eastern Road on the north side of the supermarket. Customers can access the supermarket and shops from the roof top car park via pedestrian ramps, stairs or lift which drop to the forecourt area on the Eastern Road and Tennyson Avenue corner.

Delivery vehicles enter the site off Eastern Road via a separate driveway between the ALDI store and the vehicle ramp and utilise a truck turntable under the parking deck to access the enclosed, rear loading dock area. This arrangement ensures that customer parking and pedestrian movements are separated from delivery vehicles and loading areas.

The overall proposal of 1,955 sqm (retail GLA) constitutes a small supermarket and two shops which are a continuous extension to the existing strip of seven shops on Eastern Road – separated only by Tennyson Avenue. The total retail area of the Eastern Road neighbourhood centre would therefore increase from approximately 1,512 sqm to 3,467 sqm GLA.

Figure 4: Eastern Road indicative elevation

Source: Donaldson Worrad

Figure 5: Tennyson Avenue indicative elevation

Source: Donaldson Worrad

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 9

Figure 6: Site plan – ground level

Figure 7: Roof top car park

Source: Donaldson Worrad

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 10

3. Existing centres

3.1 Overview

The hierarchy of centres in the Ku-ring-gai council area is expressed through the LEP and the application of two business zones, namely:

• The ‘Local Centre’ (B2) zone which is applied to the larger centres of Turramurra, Wahroonga, Pymble, Gordon and Lindfield along the Pacific Highway corridor and St Ives. The objectives of the Local centre zone are to provide for the needs of people who live in, work in and visit the area, to encourage employment, maximise public transport use, provide for housing close to services and encourage mixed use buildings.

• The ‘Neighbourhood Centre’ (B1) zone which is applied to the lower tier of centres where the objective is to provide small scale retail, business and community uses that serve the needs of people who live or work in the surrounding neighbourhood. Mainly situated off major roads and away from public transport hubs, neighbourhood centres in the northern part of Ku-ring-gai include Eastern Road Turramurra, East Wahroonga, North Turramurra, St Ives Chase and Bannockburn Road Turramurra.

The pattern of local and neighbourhood centres in north Ku-ring-gai is shown in Figure 8.

Figure 8: Centres hierarchy and supermarkets

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 11

Outside Ku-ring-gai, East Hornsby has been classified as a neighbourhood centre and Hornsby Town Centre is a Major Centre.

An inventory of existing ground floor retail premises in the area was undertaken in June 2015 to establish the size, tenancy mix and vacancy level of existing centres.

Table 1 and Figure 9 summarise the retail, non-retail and vacant floorspace in nearby centres that could compete with, or could be potentially affected by, the proposed supermarket and specialty shops at Eastern Rd, Turramurra. Floorspace data for the larger Westfield Hornsby, St Ives and Turramurra Plaza was sourced from the latest Property Council Shopping Centre directory. Floor space estimates were drawn from field notes and inspections, measurement of aerial images and existing data held by this office on major retailers in the area.

Table 1: Centres floorspace summary by category

Figure 9: Centres floorspace mix

* Includes St Ives Shopping Village and St Ives shopping strip. Source: Deep End Services, Property Council of Australia

Food

Retail area Smkts

Other food & drink

Non-food &

servicesTotal retail

Non-retail Vacant

Total floorspace

Vacant % of total Major tenants

Westfield Hornsby 10,787 6,120 67,478 84,385 15,275 207 99,867 0.2%DJs, Myer, Target, Kmart, ALDI, Coles,

Local centresTurramurra 2,991 2,735 5,944 11,670 2,435 864 14,969 5.8% Coles, IGASt Ives* 5,282 5,534 8,321 19,137 3,316 - 22,453 0.0% Woolworths, Supa IGAWahroonga 471 1,965 2,189 4,625 1,993 - 6,618 0.0% IGAPymble - 1,235 1,573 2,808 2,402 165 5,375 3.1%

Neighbourhood centresEastern Rd Shopping Village 572 715 225 1,512 - - 1,512 0.0% IGABannockburn Rd, Turramurra - 775 145 920 65 - 985 0.0%North Turramurra 400 1,268 492 2,160 140 - 2,300 0.0% IGAColonial Centre, St Ives Chase - 413 106 519 106 - 625 0.0%East Wahroonga 150 510 210 870 100 - 970 0.0% IGA XpressWaitara, East Hornsby - 1,450 270 1,720 150 260 2,130 12.2%

Total 20,653 22,719 86,954 130,326 25,982 1,496 157,804 0.9%

* Includes St Ives Shopping Village and St Ives shopping stripSource: Deep End Services June 2015 survey

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 12

3.2 Neighbourhood Centres

The five small neighbourhood centres in Ku-Ring-Gai within a 2.5 km radius of the ALDI site, all have relatively strong tenancy profiles, low vacancy rates and visible signs of refurbished and improved tenancies.

3.2.1 Eastern Road Turramurra

The small strip of seven shops occupies a central location in the broader residential area of north Ku-ring-gai and has the largest potential catchment of the five neighbourhood centres in the region. The main Turramurra centre is 1.3 km south along Eastern Road while the Wahroonga local centre is a similar distance to the west.

Eastern Road is an important local distributor road and the centre benefits from a steady flow of passing traffic including commuters and residents moving between the Pacific Highway at Turramurra and local east-west road connections to St Ives and Hornsby. There centre is close to local schools, reserves and playing fields and has a child care centre on adjoining land.

These attributes and an affluent local population base have underpinned a strong tenancy mix of well-presented businesses including a small refurbished IGA (approx. 570 sqm), BWS liquor store, dry cleaners, takeaway food (chicken), chemist, butcher and green grocer. The fully occupied retail floorspace at Eastern Road is measured at approximately 1,512 sqm.

The centre has angle parking (12 spaces) on the east side of Eastern Road against the shops and off street parking off the laneway to the south of the shops.

3.2.2 Bannockburn Road Turramurra

The Bannockburn Road neighbourhood centre is a similar sized strip centre embedded in the residential area east of Bobbin Head Road, 1.5 km by road east of the Eastern Road centre. The 10 retail premises are fully occupied with the largest business being a Clancy’s food store of approximately 260 sqm.

Despite its location in a quiet residential area, the centre supports four other specialty food shops, a café, liquor store and gift shop. Other services include a hairdresser and veterinary clinic. A child care centre is situated on Bannockburn Road behind the centre. New landscaping and paving has been recently undertaken by Council improving the local amenity of the footpath area outside the shops.

The full occupancy of a small centre (including specialty food tenancies) with just local street frontages and a small, confined catchment underlines the demand for retailing in this area, the

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 13

higher than average spending capacity of residents and, to some extent, a lack of choice and low convenience in the larger, local centres along the Pacific Highway.

3.2.3 North Turramurra

North Turramurra (2.1 km north-east of the ALDI site) is the largest of the five neighbourhood centres in north Ku-ring-gai with strip retailing lining both sides of Bobbin Head Road. The centre has a captive local market of 4,500 people on the narrow ridge line north of Burns Road, surrounded by the national park. The 22 retail premises (all occupied) offer a good range of food and personal services and a number of cafes and restaurants (8) which give the centre a unique leisure and entertainment ambience, not evident in the other smaller centres. The total retail and services floorspace is measured at approximately 2,300 sqm.

The centre has a small, refurbished IGA supermarket of approximately 400 sqm which is complemented by a butcher, bakery and fruit shop. Traffic and custom is generated by the adjoining Turramurra North Public School, several retirement villages which provide daily business for the local cafes, a golf course and hospital further north on Bobbin Head Road.

3.2.4 Colonial Centre, St Ives Chase

The Colonial Centre on Warrimoo Avenue serves the narrow urban peninsula of St Ives Chase, jutting north into the national park. The centre is small comprising a single stand-alone retail building (625 sqm) with a convenience store, medical centre, bottle shop, restaurant and pharmacy. It has an off-street car park to the front with 25 spaces and an adjoining auto repairs business in a former Caltex fuel station.

The centre operates in a distinct and isolated local catchment, 4.2 km by road from the Eastern Road centre and is much closer to the main St Ives centre, located 2.3 km south.

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 14

3.2.5 East Wahroonga

The East Wahroonga neighbourhood centre is on the corner of Hampden Avenue and Gladys Avenue, both local streets in the far northern area of Ku-Ring-Gai, close to the national park. The centre has eight tenancies including a pharmacy, two restaurants, bakery, newsagent, liquor store and professional office. A former independent grocery store / supermarket is currently being fitted out as an IGA Express which appears to be no larger than 200 sqm. The centre is set back with a large off-street car park.

The centre is 1.5 km by road from the ALDI site.

3.2.6 Waitara, East Hornsby

The final neighbourhood centre falling within a 2.5 km radius of the ALDI site is a small group of shops on Edgeworth David Avenue in East Hornsby, 700 metres west of the Pacific Motorway (F3). The centre has 11 retail and service tenancies with the largest being a grocery store (Waitara Friendly Grocer) and a separate large bottle shop.

The small group of retail buildings has a main road frontage with high levels of passing traffic to and from Westfield Hornsby and other parts of the Hornsby centre which is 900 metres to the west. The F3 marks a physical and demographic shift between Wahroonga and Turramurra to the east and Hornsby to the west. It is the only local centre surveyed in the broader area with a vacant tenancy.

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 15

3.3 Local Centres

3.3.1 Turramurra

Turramurra is a large but fragmented local centre which straddles the railway infrastructure and Pacific Highway with three distinct precincts:

• The local shopping area on the north side of Rohini Street and Pacific Highway, north of the railway line. The retail area opposite the railway station has a mix of food, personal services, cafes, restaurants and banks. There is a cluster of community health, senior citizens, and church and child care facilities in and around the centre.

• The central Ray Street / Forbes Lane area between the railway line and Pacific Highway which includes a small and dated freestanding Coles supermarket (approx. 1,700 sqm), low intensity retailing on the highway, some offices and Council library. This small, tightly configured precinct with railway parking area can only be accessed from Pacific Highway. The Coles supermarket building dates back to 1965 and has had one small extension completed in 2002.

• On the south side, some limited retailing on the highway either side of Turramurra Plaza, an enclosed mall-based centre (2,640 sqm) developed in 1993 which now has a Supa IGA (1,300 sqm) and 14 specialty shops. The centre opens out to the highway and is cantilevered over an under-croft car park with 150 car bays. In view of the major rail and road barriers, the catchment for this centre would be heavily oriented to Turramurra, south of the highway, where the centre can be accessed from the local street network and there are no competing supermarkets.

Overall, the Turramurra centre has some 92 ground level retail and service premises or 14,969 sqm. There were seven vacancies recorded amounting to about 864 sqm or 5.8% of the total centre. These include the former post office building on Rohini Street and three shops in Turramurra Arcade, an old, little-used mall between the Highway and the rear Council car park.

A long standing proposal by Coles to redevelop and expand its Turramurra supermarket was not supported by Council and ultimately withdrawn before reaching the Joint Regional Planning Panel.

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 16

The Turramurra Town Centre Public Domain Plan 2010 provides, amongst other things, for:

• A new centrally located town square on the western side of the railway with entertainment facilities.

• A new community building including a new youth centre and library adjacent to the proposed town square.

• A public space overlooking Granny Springs Reserve.

• Protection and enhancement of distinctive streetscape of Rohini Street

• Traffic and transport improvements including: new and widened streets, bus improvements and bicycle connections.

The Plan sets out a range of long-term proposals to improve the streetscape and appearance, public amenities and circulation of the Turramurra centre. Importantly, there are no apparent initiatives or proposals to expand or improve the size or quality of the two existing supermarkets and clearly no obvious development opportunities to accommodate ALDI in or near the centre.

3.3.2 St Ives

The major element of the St Ives local centre is St Ives Shopping Village, a 2-level mall-based centre of 16,750 sqm which includes Woolworths (3,200 sqm), Romeo’s Supa IGA (2,080 sqm) and 111 specialty shops.

The initial stage of the centre was developed in 1960 and has been successively expanded and refurbished to its current form. It is a busy and strong-performing centre with 5.5 million pedestrians per annum and annual sales by reporting retailers of $218m – resulting in a very high average sales per sqm across the centre of at least $13,600. These trading levels would place St Ives Village in the top 5% of peer group centres of its type in Australia.

The centre has some high quality specialty food retailers clustered around Woolworths at the eastern end of the centre and around Supa IGA on level 1.

As our inspection for this study (and others) revealed, the centre is trading so strongly that the 1,050 car bays are heavily used and shoppers experience congestion and a shortage of parking during peak and other daily periods.

Outside the main centre there is some 43 retail premises on Mona Vale Road, Denley Lane and Village Green Parade. In total, St Ives has an estimated 22,453 sqm of retail and services

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 17

floorspace. At the time of our survey there were no vacant tenancies recorded in or outside the main centre.

The proposed ALDI site on Eastern Road is approximately 3.6 km by road from the St Ives centre.

3.3.3 Pymble

The local centre at Pymble also straddles the Pacific Highway and railway line which intersect and cross each other at this rising point on the highway. The local retail precinct stretching along the north side of the highway and continuing along Grand View Street opposite the railway station has a limited retail mix with a high proportion of non-retail uses, services, offices and low intensity businesses attracted to the high exposure and passing traffic.

Fresh food and grocery options include a milk bar, green grocer, and patisserie / café and liquor store.

A second, smaller group of shops is isolated in a narrow strip between the railway line and Pacific Highway. The 12 shops here are occupied by services, offices and low scale retailers.

Overall, the Pymble centre has approximately 5,375 sqm of retail-type tenancy space with one vacancy (3%) but a high 45% occupied by non-retail uses – the highest of all centres surveyed.

3.3.4 Wahroonga

Wahroonga is the fifth and northern most local centre in Ku-Ring-Gai along the Pacific Highway corridor. The compact and vibrant strip centre on Railway Avenue and Redleaf Avenue is situated between the highway and railway line and is surrounded by seven school campuses and various local leisure and community facilities.

The ‘village style’ centre has an upmarket image with numerous cafes and restaurants, small homewares and clothing boutiques and a range of personal, health and wellbeing services. The 63 retail tenancies surveyed (or 6,618 sqm) had no recorded vacancies.

Food and grocery retailing is limited to an IGA supermarket of just 470 sqm with no on-site parking, three bakeries, a butcher and liquor store. The centre thrives on its compact form with good connections over the rail line to the north and direct signalised access across the highway from the south into an affluent local catchment. It has a large central off-street car park which serves the centre.

The small IGA supermarket however would cater to a very small proportion of the needs of this catchment and residents would, most likely, be directing their food shopping to Hornsby, the poor supermarket offering at Turramurra or more distant locations.

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 18

3.4 Conclusions

The overall observations from the inspection and occupancy survey of centres generally within 2.5 km of the ALDI site are as follows:

• The small neighbourhood centres scattered through the residential areas of north Ku-ring-gai appear particularly strong with almost full occupancy levels, reinvestment in older tenancies and a much higher ‘shop’ component than would normally be found in centres of this type.

• The strength of the smaller neighbourhood centre tier – often found to be the weakest in metropolitan areas – is attributed to a range of interrelated factors including:

§ Very high household and disposable incomes in the area. § The fragmented land use and retailing pattern of the larger centres on the highway

which are difficult to access, have limited or disconnected parking and have limited specialty food offerings which can be reached in a compact and accessible area.

§ Neighbourhood centres offering small, specialty food retailers which are comparable or at least more convenient than those in the larger, fragmented centres.

• Very low levels of supermarket provision across the range of centres. The available options are either of poor quality and difficult to access (Turramurra) or distant with congested parking and low convenience (St Ives, Gordon and Hornsby).

• Despite the structural issues at some centres and the relatively poor aspect and external environment of some centres (e.g. Highway noise, limited parking etc.), vacancy levels are at extremely low levels suggesting there is an under supply of retail floorspace in the area.

• There has been little or no change to the overall supply and quality of retail floorspace in the surveyed centres for many years. The constraints imposed by existing land use, heritage buildings, topography and road and rail infrastructure and a review of Local Centre Domain Plans suggest the larger local centres have very limited capacity or opportunity for meaningful expansion.

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 19

4. Trade area analysis

This section defines the expected trade area for the proposed ALDI store and includes an assessment of population, demographic characteristics and retail spending levels.

4.1 Regional population growth

The Ku-ring-gai local government area had an estimated resident population of 120,440 people in 2014. It has grown by 1.8% per annum between 2006 and 2014, slightly above than the metropolitan Sydney average of 1.6% per annum.

The most recent NSW Government Planning & Environment population projections (2014) indicate a slowing but still high long term growth rate in Ku-ring-gai, averaging 1.6% or 2,000 people per annum to 2021. The population of Ku-ring-gai is forecast to increase by 14,000 people over the next 7 years to 134,450 by 2021.

Figure 10: Ku-ring-gai LGA population

Source: NSW Government P&E, State and Local Government Area Population, Household and Dwelling Projections: 2014

4.2 Trade area definition

In view of the geography, road networks and the distribution and quality of existing centres across the north Ku-ring-gai area and being mindful of ALDI’s unique product mix and competitive pricing, the likely catchment characteristics for ALDI at Eastern Road are likely to be:

• Drawing strongly into a localised area within 1.5 km of the site; and

• Drawing thinly across a more extensive area within a 5-10 minute drive-time including to the F3, Mona Vale Road and south of the Pacific Highway.

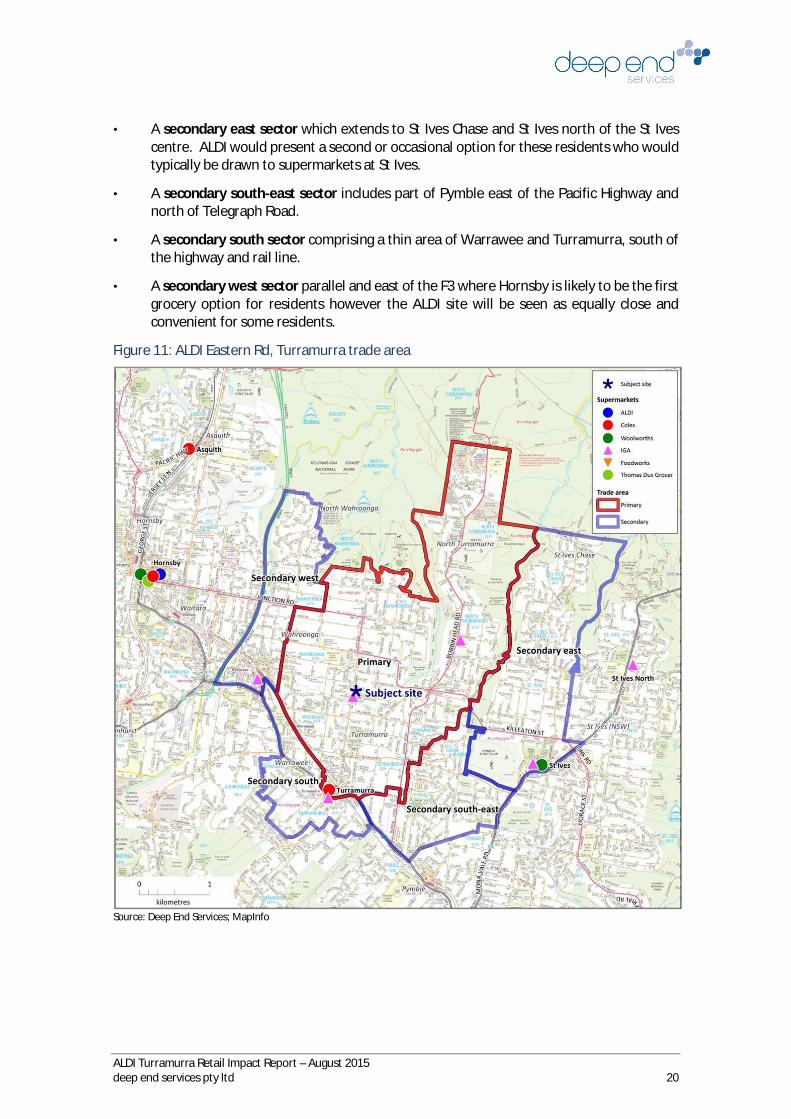

The defined trade area (refer Figure 11) includes:

• A primary sector covering parts of Turramurra, Wahroonga and Warrawee north and east of the railway line, within 1.5 km of the site. It extends 3 km north along Bobbin Head Road into North Turramurra. For many households in this area, ALDI will be the closest and most convenient supermarket, accessible via the local street networks.

104,459114,600

124,700134,450

143,350151,100

2006 2011 2016 2021 2026 2031

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 20

• A secondary east sector which extends to St Ives Chase and St Ives north of the St Ives centre. ALDI would present a second or occasional option for these residents who would typically be drawn to supermarkets at St Ives.

• A secondary south-east sector includes part of Pymble east of the Pacific Highway and north of Telegraph Road.

• A secondary south sector comprising a thin area of Warrawee and Turramurra, south of the highway and rail line.

• A secondary west sector parallel and east of the F3 where Hornsby is likely to be the first grocery option for residents however the ALDI site will be seen as equally close and convenient for some residents.

Figure 11: ALDI Eastern Rd, Turramurra trade area

Source: Deep End Services; MapInfo

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 21

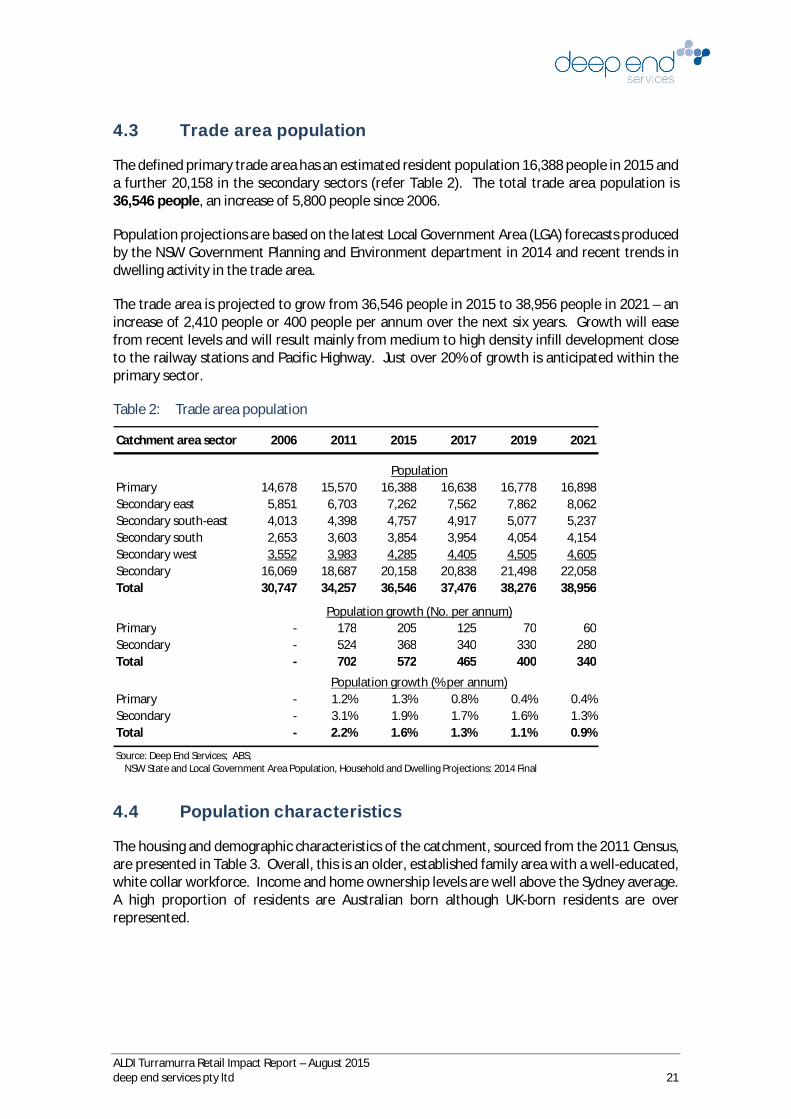

4.3 Trade area population

The defined primary trade area has an estimated resident population 16,388 people in 2015 and a further 20,158 in the secondary sectors (refer Table 2). The total trade area population is 36,546 people, an increase of 5,800 people since 2006.

Population projections are based on the latest Local Government Area (LGA) forecasts produced by the NSW Government Planning and Environment department in 2014 and recent trends in dwelling activity in the trade area.

The trade area is projected to grow from 36,546 people in 2015 to 38,956 people in 2021 – an increase of 2,410 people or 400 people per annum over the next six years. Growth will ease from recent levels and will result mainly from medium to high density infill development close to the railway stations and Pacific Highway. Just over 20% of growth is anticipated within the primary sector.

Table 2: Trade area population

4.4 Population characteristics

The housing and demographic characteristics of the catchment, sourced from the 2011 Census, are presented in Table 3. Overall, this is an older, established family area with a well-educated, white collar workforce. Income and home ownership levels are well above the Sydney average. A high proportion of residents are Australian born although UK-born residents are over represented.

Catchment area sector 2006 2011 2015 2017 2019 2021

PopulationPrimary 14,678 15,570 16,388 16,638 16,778 16,898Secondary east 5,851 6,703 7,262 7,562 7,862 8,062Secondary south-east 4,013 4,398 4,757 4,917 5,077 5,237Secondary south 2,653 3,603 3,854 3,954 4,054 4,154Secondary west 3,552 3,983 4,285 4,405 4,505 4,605Secondary 16,069 18,687 20,158 20,838 21,498 22,058Total 30,747 34,257 36,546 37,476 38,276 38,956

Population growth (No. per annum)Primary - 178 205 125 70 60Secondary - 524 368 340 330 280Total - 702 572 465 400 340

Population growth (% per annum)Primary - 1.2% 1.3% 0.8% 0.4% 0.4%Secondary - 3.1% 1.9% 1.7% 1.6% 1.3%Total - 2.2% 1.6% 1.3% 1.1% 0.9%

Source: Deep End Services; ABS;NSW State and Local Government Area Population, Household and Dwelling Projections: 2014 Final

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 22

The primary sector has the following characteristics:

• 83% of dwellings are detached houses compared to 60% across Sydney. This results in a high proportion of ‘couples with children’ and a large average household size of 2.93 persons (Sydney 2.74).

• The established family structure has an older population profile (average age 43.2 years) with 42% aged over 50 years (Sydney average of 30%) and a higher proportion of children in teenage years (17% vs Sydney 12%). A high 23% of the population is also aged over 65 years (Sydney 13%) pointing to a large retiree base.

• The population is well educated with 40% aged over 15 years having a bachelor degree (Sydney 24%) which is, in turn, reflected in the high proportion of the workforce employed as ‘managers’ or ‘professionals’ (59% vs Sydney 40%).

• Household income levels are 37% above the Sydney average and 53% of dwellings are fully owned (Sydney 31%).

Given the uniform geography and housing profile across the broader catchment area – through Wahroonga, Pymble and St Ives - there are only minor variations in the socio economic characteristics between the primary and secondary trade areas.

The main variation is the secondary south sector where there are more apartments (39%) around the railway stations at Turramurra and Warrawee and a higher 28% of dwellings are rental properties.

Notwithstanding the affluent population base across the trade area, ALDI will have a strong attraction for larger families with high grocery bills and retirees on fixed incomes.

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 23

Table 3: Trade area characteristics

Demographic characteristic - 2011 Census Primary

Secondary east

Secondary south-east

Secondary south

Secondary west

Total catchment Sydney

Usually resident population 14,806 6,328 4,213 3,533 3,782 32,662 4,390,956At same address: (1)

• 1 year ago 88% 87% 87% 80% 85% 87% 86%• 5 years ago 64% 63% 60% 50% 58% 61% 61%

Total private dwellings (6) 5,404 2,285 1,520 1,315 1,473 11,997 1,720,342• % unoccupied 6% 6% 7% 7% 6% 6% 7%Persons per dwelling (7) 2.93 2.94 2.99 2.88 2.74 2.91 2.74

Participation rate (2) 57% 62% 61% 60% 62% 59% 62%Unemployment rate (2) 4.8% 5.0% 4.5% 5.9% 5.5% 5.0% 5.7%White collar workers (2) 74% 75% 77% 75% 76% 75% 56%Bachelor degree or higher (2)(3) 40% 40% 45% 44% 41% 41% 24%SEIFA 1,158 1,164 1,169 1,140 1,148 1,157 1,002Age group0-9 11% 13% 12% 12% 12% 12% 13%10-19 17% 16% 16% 16% 14% 16% 12%20-34 10% 13% 14% 17% 15% 12% 22%35-49 19% 21% 22% 21% 20% 20% 22%50-64 19% 19% 22% 17% 19% 19% 17%65+ 23% 18% 14% 16% 20% 20% 13%Average age 43.2 40.0 39.3 39.6 41.5 41.5 37.6Annual household income (1)(3)(5)

<$41,700 18% 15% 15% 17% 16% 17% 28%$41,700 - $78,200 19% 16% 14% 16% 19% 17% 23%$78,200 - $156,400 31% 35% 35% 36% 35% 33% 33%>$156,400 32% 33% 36% 31% 31% 32% 16%

Average household income $126,694 $130,156 $137,150 $123,153 $124,041 $127,925 $91,983Variation from Sydney average 37.7% 41.5% 49.1% 33.9% 34.9% 39.1% -

Average household loan repayment $36,962 $35,993 $35,770 $35,970 $35,622 $36,342 $28,323% of household income 21% 22% 21% 21% 22% 21% 23%

Average household rent payment $25,868 $31,152 $29,528 $27,114 $26,682 $27,609 $19,357% of household income 23% 26% 23% 24% 21% 23% 25%Country of birth (1)

Australia 68% 57% 64% 59% 64% 64% 64%United Kingdom 9% 8% 7% 8% 8% 9% 4%South Africa 4% 10% 4% 2% 4% 5% 1%China 2% 3% 3% 4% 3% 3% 4%Other 17% 22% 22% 27% 21% 20% 28%Occupied private dwelling tenure (1)(4)(5)(6)

Fully owned 53% 48% 45% 35% 47% 48% 31%Being purchased 36% 39% 39% 36% 32% 36% 36%Rented 11% 13% 16% 28% 20% 15% 33%Dwelling type (1)(4)(7)

Separate house 83% 81% 84% 53% 67% 77% 60%Townhouse/semi-detached 7% 4% 3% 7% 8% 6% 13%Apartment 10% 15% 13% 39% 25% 16% 27%Household composition (4)(5)

Couples with children 44% 49% 51% 41% 41% 45% 37%Couples without children 28% 31% 25% 29% 30% 29% 25%One parent family 8% 7% 8% 10% 8% 8% 12%Lone person 19% 12% 14% 19% 19% 17% 22%Group 1% 1% 2% 2% 1% 1% 4%Motor vehicle ownership per dwelling (1)(5)

None 5% 2% 3% 7% 4% 4% 12%One 29% 25% 28% 45% 36% 31% 40%Two 45% 50% 50% 36% 44% 46% 34%Three or more 20% 23% 20% 12% 15% 19% 14%

Notes:(1) Excludes not stated (5) Occupied private dwellings(2) 15 years and over and excludes not stated (6) Includes visitor only households(3) Excludes inadequately described and/or partially stated (7) Excludes visitor only households(4) Excludes other Source: Deep End Services; Australian Bureau of Statistics

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 24

4.5 Retail spending

For the purpose of this report, consumer spending on commodities and services sold by shop-based retailers is grouped under the following categories:

Broad category Spending group Items / services

Food, liquor, groceries & catering (FLG&C)

Food & Groceries Edible supermarket goods (ESGs), non-food groceries inc. health & beauty, magazines & stationery.

Packaged Liquor Take-home liquor Food Catering Take-away food, dining-in. Non-food & retail services

Non-food Auto accessories, fashion, furniture & furnishings, hardware & garden, pharmaceuticals, home appliances & entertainment, homewares, reading & writing, recreational goods.

Retail services Hairdressing & personal care, repairs & alterations, dry cleaning, optical, photo developing, video hire.

To establish the spending potential of a catchment area, Deep End Services uses small area data supplied by Market Data Systems (MDS). The MDS product, known as MarketInfo, estimates spending propensity on retail categories at the small area level using a micro-simulation model and data sets including the ABS’ Household Expenditure Survey (HES), the Census of Population and Housing and Australian National Accounts.

MarketInfo models the effects of demographic variables such as income, ethnicity, age and education level and geographic location on a household’s propensity to purchase products and services. The results are generally regarded as the best proprietary data base of its type in Australia.

Figure 12 maps the variation in per capital spending levels on Food, Liquor and Groceries (FLG) at the small area (SA1) level compared to the Sydney average. FLG spending is strongly correlated with income and significantly higher in inner Sydney, the north shore and northern suburbs. The Turramurra site sits within an area that has amongst the highest levels of FLG spending in Sydney.

A comparison of per capita spending levels in the Turramurra trade area against metropolitan Sydney is set out in Figure 13. It shows average spending on Food, Liquor, Groceries and Catering (FLG&C) in the primary and secondary sectors is just over $9,000 per person per annum which is, on average, 11.4% above the Sydney average.

Similarly, spending on ‘Non-Food & Retail Services’ is also well above the Sydney average in the primary sector (+35.6%) and secondary sectors (+36.2%).

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 25

Figure 12: FLG spend per capita variation to Sydney average

Source: Deep End Services; MapInfo

Figure 13: Per capita spending rate comparisons

Source: Deep End Services, MDS (MarketInfo); Deloitte Access Economics

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 26

Combining population estimates with per capita spending levels in the catchment area, generates the retail spending market for each of the major product groups for 2014/15 and future years (refer Table 4).

In 2015, the catchment generated $330.5 million in FLG&C spending and $332.5 million in Non-Food and Retail Services. Total expenditure was $663.0 million in 2015.

With moderate population growth, the spending market is forecast to increase by about $67.0 million between 2015 and 2021 (at $2015 constant) with FLG&C spending accounting for about 76% of the growth (or $50.8 million). By 2021, spending on FLG&C is projected to increase to $381.3 million.

Table 4: Trade area spending estimates

Average change (%pa)Spending category 2015 2017 2019 2021 2015-17 2017-21

FLG & CateringPrimary 147.8 153.7 160.3 164.9 2.0% 1.8%Secondary 182.7 193.4 206.5 216.4 2.9% 2.8%Total 330.5 347.1 366.8 381.3 2.5% 2.4%

Non-Food & Retail ServicesPrimary 148.7 152.6 152.9 150.7 1.3% -0.3%Secondary 183.8 192.1 197.0 198.0 2.2% 0.8%Total 332.5 344.6 350.0 348.7 1.8% 0.3%

TotalPrimary 296.5 306.2 313.2 315.6 1.6% 0.8%Secondary 366.5 385.5 403.5 414.4 2.6% 1.8%Total 663.0 691.7 716.7 730.0 2.1% 1.4%

Source: Deep End Services; ABS; Market Data Systems; Deloitte Access Economics

Spending market (constant 2015 $m)

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 27

5. Supermarket supply and demand

This section assesses the levels of supermarket floorspace supply and demand in the Ku-ring-gai local government area, the distribution of supermarkets around the site and levels of accessibility to supermarket floorspace by small area.

5.1 Supermarket floorspace provision by municipality

A general measure of the rate of supermarket provision in an area is made by dividing the resident population into the total supply of floorspace (sqm). The rate of provision (expressed as sqm per 1,000 residents) for each local government area in Sydney is shown in the Figure 14.

Ku-ring-gai Council area has an estimated 18,196 sqm of supermarket floorspace1 for a population of 123,180 people (June 2015), which yields a rate of 148 sqm per 1,000 residents. This is the 7th lowest rate of provision of Sydney’s 41 municipalities. In small local government areas, low levels of provision are less significant if the population can access nearby supermarkets outside the area however in the case of Ku-ring-gai, the deficiency is acute and significant considering its large population base.

The average rate of supermarket provision across Sydney is 245 sqm per 1,000 residents – the lowest of all state capitals in Australia. Ku-ring-gai’s rate of provision is 40% below the Sydney average and less than half the other Australian capital cities average (334 sqm per 1,000 residents).

If Ku-ring-gai’s supermarket provision was raised to the Sydney average, a further 12,000 sqm of supermarket floorspace would be comfortably supported based on current population levels. The deficiency is even larger if population growth is considered over the next 10-20 years.

The implications of a low level of supply and choice in supermarkets across a large area such as Ku-ring-gai are:

• A lack of diversity and choice in supermarket banners that can offer differentiated products, pricing and customer satisfaction.

• As shown in Figure 12, FLG per capita spending levels across Ku-ring-gai are particularly high. Combined with a low floorspace provision existing supermarkets are trading at very high levels per sqm resulting in longer periods of congestion, queuing and severe parking shortages for longer periods.

• Residents may elect to travel outside the area to access a wider range and choice of operators – this is particularly the case with ALDI where its lower prices are a strong attraction. ALDI’s customer surveys show that many Ku-ring-gai residents make costly and time consuming trips on major roads to access ALDI stores at Hornsby, Chatswood and Frenchs Forest.

• Lost employment opportunities for Ku-ring-gai residents.

1 Includes floorspace operated by all bannered supermarkets and independents across Sydney including Woolworths, Coles, ALDI, IGA, Foodworks, Spar, Supabarn, About Life, Thomas Dux.

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 28

Figure 14: Supermarket provision by local government area

Source: Deep End Services

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 29

5.2 Supermarket accessibility

The low provision of supermarket floorspace in Ku-ring-gai is also illustrated by the thematic map (Figure 15) which shows the amount of supermarket floorspace (sqm) accessible within a 5 minute off peak drive-time of each ABS-defined small Statistical Area (SA1).

The areas shaded yellow and light yellow have low rates of supermarket accessibility from the place of residence compared to areas with darker orange shading which have either larger or more supermarket options close to home.

The entire Ku-ring-gai Council area is shown to have low levels of access to supermarket floorspace. It suggests there is limited supply and choice in Ku-ring-gai itself and that supermarket options outside the Council area are generally no closer or more convenient.

Figure 15: Sydney supermarket accessibility

Source: Deep End Services; MapInfo

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 30

5.3 Supermarket distribution

The distribution and size of supermarkets around the Turramurra catchment is shown in Figure 16 together with the supermarket accessibility shading. The supermarket distribution in the trade area is characterised by the following:

• In Ku-ring-gai, the larger supermarkets are clustered around the railway stations and activity centres along the main transport corridors – the Pacific Highway and Mona Vale Rd.

• Within the trade area, Woolworths has the largest store at St Ives (3,202 sqm).

• Coles (1,691 sqm) and IGA (1,300 sqm) both have small stores at Turramurra. An application by Coles to expand the Turramurra store was withdrawn in May 2014.

• A number of IGA stores are situated throughout the area. The larger IGAs (ex-Franklins) are located near the major chains in the key centres, whilst smaller stores have localised residential catchments.

• The larger supermarkets are situated outside the area at Hornsby (north-west), Macquarie (south-west) or Chatswood (south).

Figure 16: Trade area supermarket accessibility

Source: Deep End Services; MapInfo

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 31

6. Retail impact assessment

This section assesses the potential trading impacts from the proposed ALDI and shops at Eastern Road Turramurra on other centres in or near the trade area. The analysis draws on the assumptions, data and commentary from earlier sections and considers the positive employment and other benefits to the community.

The analysis and findings are presented as a series of sequential steps including:

• Projected retail turnover levels for the 1,585 sqm ALDI store and 370 sqm of shops for the assumed first year of opening (2017);

• Projected sales redirected from competing centres are modelled and expressed in dollar and percentage terms; and

• New employment and other positive benefits from the proposed development.

6.1 Projected sales

The projected sales for ALDI and the retail shops are assessed at $16.43 million in 2017 (constant $2015) or $8,405 per sqm. ALDI is estimated to generate sales of around $14.48 million or $9,200 per sqm. Approximately 80% of ALDI’s sales will be in food and groceries and 20% in general merchandise lines reflecting the weekly special buys.

Tenants for the adjoining shops fronting Eastern Rd are unknown at this stage however a café and personal service (hairdresser) could be expected in this location and with the tenancy layouts. With the uncertainty around actual tenancies and the possibility that a non-retail use (e.g. office) could also potentially occupy one of the two shops, a conservative sales rate of $5,000 per sqm is applied resulting in a sales projection of $1.85 million per annum for the two shops.

Table 5: Eastern Rd, Turramurra development projected sales (2017)

Table 6 shows the projected sales in the form of market shares of available food and non-food spending from catchment area residents in 2017. The relatively small scale of the proposed development in the context of the catchment’s large spending capacity is evident where it requires just 2.1% of total retail spending by catchment area residents, including:

• 3.5% of retail spending by primary trade area residents; and

• 1.0% of retail spending from residents in the secondary sectors.

TenancyFloorspace(sqm GLA)

Sales 2016/17$m (constant $2015)

Trading level($/sqm)

ALDI 1,585 14.58 $9,200

Specialty shops 370 1.85 $5,000

Total Retail 1,955 16.43 $8,405Source: Deep End Services

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 32

Table 6: ALDI Eastern Rd, Turramurra site market shares – 2017

By broad product group, ALDI and the proposed shops should attract just 3.3% of food, liquor, grocery and catering expenditure and 0.9% of non-food and retail services spending. These are very small shares of available spending which are proportional to the scale of the proposal.

In addition to spending from permanent trade area residents, ALDI can expect to generate approximately 12% of sales from customers originating from outside the trade area.

6.2 Trading impacts

The method of determining trading impacts on surrounding centres is based on the following:

• Projected sales by product group (Food & Non-food) for ALDI are modelled by trade area sector (refer Table 6).

• For each trade area sector, the projected sales are allocated away from various centres within, or close to, each sector on the basis of the strength of the competing centre (measured by size and number of competing food retailers and known or estimated sales levels), relative distance and accessibility and the general appearance and vitality of each centre.

• Sales which are derived from beyond the defined trade area are also notionally allocated away from some centres in the trade area, although a proportion will also be new sales to the development.

• The sum of the individual product group and trade area sector assessments generates a total sales level diverted from competing centres and retailers. This is expressed in dollar terms in 2017 and as a percentage of the sales that would otherwise have been achieved by that centre in that year.

It should be noted that the impacts are modelled on the overall centre and shown in terms of impacts to total sales. It is generally not the role of retail impact reports to specify impacts on individual operators as this is not usually a matter that a planning authority or review body would have regard to. The more important consideration is whether or not the proposal would result in significant economic impact to an existing centre that could, for example, cause a

Spending ($m 2016/17) Market share (%) Turnover ($m)

Catchment area sectorFLG &

CateringNon-food

& Serv.Total

RetailFLG &

CateringNon-food

& Serv.Total

RetailFLG &

CateringNon-food

& Serv.Total

Retail

Primary 153.7 152.6 306.2 5.5% 1.5% 3.5% 8.5 2.2 10.7

SecondarySecondary east 69.4 69.9 139.3 1.5% 0.4% 0.9% 1.0 0.3 1.3Secondary south-east 45.8 47.8 93.6 1.7% 0.4% 1.1% 0.8 0.2 1.0Secondary south 36.9 34.5 71.4 1.4% 0.4% 0.9% 0.5 0.1 0.7Secondary west 41.3 39.8 81.1 1.6% 0.4% 1.0% 0.7 0.2 0.8

Total Secondary 193.4 192.1 385.5 1.5% 0.4% 1.0% 3.0 0.8 3.8

Total catchment area 347.1 344.6 691.7 3.3% 0.9% 2.1% 11.5 3.0 14.5Beyond trade area (% sales) 12.0% 12.0% 12.0% 1.6 0.4 2.0Total 13.0 3.4 16.4

Source: Deep End Services

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 33

significant increase in vacancy rates or economic and retail blight to the extent that the community is not better off – even after the positive effects of the development are considered.

The estimated trading impacts are presented in Table 7. The main centres where ALDI (and to a lesser extent the specialty shops) are likely to draw sales from are those containing medium to large-scale supermarkets at St Ives and Turramurra within the trade area and Westfield Hornsby outside the catchment.

As the proposal is for a supermarket with only limited specialty shops, the sales impact is likely to fall mainly on supermarkets in each centre, with little or no change to specialty shop sales.

Table 7: ALDI Eastern Rd, Turramurra site trading impacts

In relation to impacts on individual centres:

• St Ives (which includes St Ives Shopping Village and St Ives shopping strip) is expected to incur the highest impact in dollar terms given its proximity to the proposal and the provision of two supermarkets (Woolworths and Supa IGA). The impact on the centre is modelled at -$4.9m or -1.8% of sales that the centre would otherwise have achieved in 2017. The sales impact is a one-off re-allocation to ALDI and sales levels should recover in the following years. The impact will fall disproportionately on Supa IGA and Woolworths who are large, well-resourced retailers that can withstand small sales fluctuations from occasional changes to their competitive position. The specialty shops within St Ives will experience little or no effects.

• The highest impact in percentage terms will be on Eastern Rd Shopping Village which is adjacent to the site. The centre includes a small IGA supermarket, two fresh food retailers and a liquor store that will be presented with increased competition. The other retailers (pharmacy, dry cleaner and café) are unlikely to be negatively impacted – in fact these

Retail floorspace (sqm) Retail sales ($m) ALDI Turramurra

Centre2015 2017 2015

2017 -no ALDI

Turramurra

2017 -post ALDI

Turramurra($m) (%)

ALDI Eastern Rd, Turramurra - 1,955 - - 16.4 n/a n/a

Westfield Hornsby 84,385 84,385 627.5 654.6 650.0 -4.6 -0.7%

Local centresTurramurra 11,670 11,670 115.4 120.4 117.9 -2.5 -2.1%St Ives* 19,137 19,137 256.6 267.7 262.8 -4.9 -1.8%Wahroonga 4,625 4,625 44.8 46.8 46.3 -0.5 -1.0%Pymble 2,808 2,808 20.1 21.0 20.8 -0.2 -1.0%

Neighbourhood centresEastern Rd Shopping Village 1,512 1,512 14.9 15.5 14.7 -0.8 -5.0%Bannockburn Rd, Turramurra 920 920 8.2 8.5 8.4 -0.2 -2.0%North Turramurra 2,160 2,160 19.6 20.5 20.2 -0.3 -1.5%Colonial Centre, St Ives Chase 519 519 5.5 5.7 5.7 0.0 -0.5%East Wahroonga 870 870 7.6 8.0 7.8 -0.2 -2.0%Waitara, East Hornsby 1,720 1,720 16.2 16.9 16.8 0.0 -0.2%

Other / beyond trade area - - - - - -2.3 -

Total 130,326 130,326 1,136 1,186 1,171 -16.4

* Includes St Ives Shopping Village and St Ives shopping stripSource: Deep End Services

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 34

businesses will almost certainly benefit from the increased traffic and shoppers drawn to the Eastern Road centre. Even the butcher who is understood to provide specialist and fine meat cuts and value added products could also benefit from ALDI’s presence. On balance, between the retailers who will benefit and those potentially impacted, the modelled overall impact is -5.0%, amounting to -$0.8m in sales. The strong tenancy mix at the Eastern Road centre and generally limited competition in the area suggests that the overall impact is not significant and may in fact be less if individual businesses can capture the benefits of the higher visitation levels.

• The Turramurra supermarkets are difficult to access from this area as Coles is located between the highway and railway line and IGA is south of the highway. Residents of the primary catchment and other secondary sectors must therefore cross or drive along the Pacific Highway to access these small and generally poorly conditioned stores. Elsewhere, Turramurra has a small provision of fresh and specialty food stores. The impact from ALDI and the shops on the Turramurra centre is modelled at -$2.5m or -2.1% of sales, mainly redirected from Coles.

• Westfield Hornsby is situated a short distance west of the trade area but is thought to draw supermarket and grocery sales from Wahroonga where there is no major supermarket and a low market share across the rest of the trade area. The centre includes Woolworths, Coles, ALDI and a Thomas Dux Grocer which are thought to achieve combined sales of approximately $200m – these are very high volumes underlining the lack of quality supermarket options in the area. The modelled impact on the overall sales at Westfield Hornsby is -$4.6m or -0.7% of sales.

• The small, vibrant village centre of Wahroonga has only a small limited range IGA serving small convenience purchases. The balance of the centre has a small range of specialty food shops. Overall impacts on Wahroonga will be low amounting to an estimated -1.0% of sales or -$0.5m.

• The smaller Pymble Local Centre and other neighbourhood centres will experience little or no impacts due to their limited retail mix and competitive positioning. Small supermarket and convenience stores in these centres and the occasional fresh food retailer are used mainly for ‘top-up’ shopping.

• Approximately 14% of the projected sales (or $2.3 million) is unallocated from specific centres and will be drawn from a range of other retailers/centres across the broader area, including Gordon, Macquarie and Chatswood. It also includes part of ALDI’s general merchandise and non-food sales that could be drawn from a wide range of bulky goods and showroom retailers, hardware stores, and other retail formats outside the nominated centres who sell similar products to ALDI’s unique weekly specials range.

A summary of the sales at major centres in 2017 highlighting the post-ALDI development volume of re-allocated sales is shown in Figure 17.

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 35

Figure 17: ALDI Eastern Rd, Turramurra source of sales - 2017

* St Ives includes St Ives Shopping Village and St Ives shopping strip ** Other Minor centres includes Eastern Rd, Bannockburn Rd, North Turramurra, St Ives Chase, East Wahroonga, East Hornsby

6.3 Impact conclusions

The development of a new centre or supermarket of any size or category inevitably results in sales moving from a range of existing centres and retailers to the new location. Importantly, this comes about from consumers electing to change their normal shopping patterns, permanently or occasionally, as a result of:

• An improvement in the range and choice of supermarkets in a local area including better value and pricing;

• Improved accessibility and reduced travel time; and / or

• Perceptions of improved amenity, convenience, parking, design and layout.

The proposed ALDI at Eastern Rd, Turramurra will provide an additional supermarket option for residents in the area but will not result in significant trading impacts or the closure of multiple retailers at existing centres for the following reasons:

• High occupancy levels. Despite the physical constraints and limitations of some centres in the area, shop vacancy levels are very low averaging about 2% across the surrounding local and neighbourhood centres. This suggests a strong and vibrant range of centres that are trading at strong levels.

• A small provision of floorspace. The proposed supermarket floorspace is just 1,585 sqm representing about 14% of existing supermarket space in the trade area. The size is smaller than Woolworths and Supa IGA at St Ives and comparable to Coles and Supa IGA at Turramurra. ALDI’s projected sales are quite low in the context of other larger centres / supermarkets across the region.

4.6

4.9

2.5

0.50.2

1.5

0

100

200

300

400

500

600

700

WestfieldHornsby

St Ives* Turramurra Wahroonga Pymble Other MinorCentres**

Reta

il sa

les

($M

)

Turnover redirected to proposal ($M)

Turnover post-impact ($M)

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 36

• Supermarket provision. The existing provision of supermarkets in the trade area and generally across Ku-ring-gai is very low compared to metropolitan Sydney averages and other national benchmarks. This situation is exacerbated by high per capita food and grocery spending levels in the trade area. The addition of ALDI raises the average rate of provision in the catchment and provides additional supermarket choice for residents in the area.

• Proposed mix. ALDI comprises 82% of the proposed retail floorspace and will provide a convenient option and point of difference to existing supermarkets in, or just outside, the catchment. Most of the projected impacts are likely to fall disproportionately on supermarkets in the area, some of which have limited competition compared to other metropolitan areas and can readily absorb the relatively small sales transfers.

• Limited specialty shops. The small provision of specialty shops in the development will ensure that residents of the catchment will continue to visit and use other centres where small businesses, operating from specialty shops, will be largely unaffected. This should protect the generally high occupancy levels at surrounding centres.

• Population growth. Moderate population growth from medium density development in the railway corridor and around Local Centres will continue. This will ensure that small sales impacts from new developments, such as ALDI Eastern Rd, should be quickly recovered in the short term through local population and spending growth.

In overall terms, the projected sales and accompanying range of impacts are relatively small and proportional to the role and incremental change in floorspace at Eastern Rd, Turramurra. The sales re-allocations at all centres are within the tolerance levels of a normal competitive environment where retail turnover naturally fluctuates with changes in economic and market conditions. Impacts are distributed amongst a range of different centres and individual retailers across the hierarchy.

6.4 Benefits of ALDI development

6.4.1 Employment benefits

Total direct on-site retail employment generated by the proposed ALDI and retail shops is estimated at 34 full-time equivalent (FTE) positions, which includes 25 FTE positions for ALDI. Applying retail and commercial employment multipliers developed by the Australian Bureau of Statistics, the total number of indirect FTE jobs generated by the retail development is estimated at 21, resulting in an estimated 55 FTE jobs created in the local and broader economy from the proposed development.

The new retail employment opportunities on-site will benefit the local economy and many will be filled by local residents living close to the centre.

Unemployed people, students, semi-retired people and those looking to work close to home with part-time hours in conjunction with family care and duties are strong candidates for retail employment opportunities. Many of these jobs may be taken by local residents who would otherwise not work in the absence of ALDI.

ALDI Turramurra Retail Impact Report – August 2015 deep end services pty ltd 37

The employment positions offered by ALDI are reliable, stable and provided in a safe and professional work place where extensive training is provided and new skills are developed which can lead to further career opportunities in the retail industry.

The increase in local employment will increase wages and salaries in the area which should be spent in part, with local retailers.

The construction phase will also generate employment opportunities, including both on-site full-time jobs as well as indirect employment or multiplier effects from wages and salaries paid to construction workers.

6.4.2 Other benefits

A new ALDI store at the Eastern Rd, Turramurra site will provide other economic and community benefits for catchment area residents.

Turramurra will have the first and only ALDI store for Ku-ring-gai’s 123,000 residents. Ku-ring-gai is by far the largest of six local government areas in Sydney that have no ALDI presence.

The new supermarket will be a contemporary format reflecting the latest in ALDI’s standards and in-store concepts. It will underpin an existing neighbourhood centre and reinforce the existing commercial and community assets in the area. The site will increase the existing employment base already established on the site.

ALDI will improve the quality, choice and convenience of supermarket shopping and new customers drawn to the site will generate additional patronage for other retailers in Eastern Rd. Average travel times (and travel costs) for residents to access a well-ranged supermarket will fall considerably and in turn ease congestion in some areas.