Embed Size (px)

Citation preview

Proprietary Bearing Technology poised to

dominate the Chinese Aerospace marketTrans-Pacific Aerospace Company, Inc. (hereinafter referred to as “TPAC” or “the

Company”) is a development stage company that is well-positioned to leverage its

innovative and proprietary technology to forge business partnerships outside the United

States (U.S.) and use its local partners’ large manufacturing facilities and distribution

resources to derive the benefit of economies of scale available to them. Currently, the

Company is focused on the production of standard spherical bearings, rod-ends and

bushings (together known as Bearings) for the commercial aerospace industry. These

Bearings reduce friction, bear loads and aid flight-critical tasks such as aircraft flight controls

and landing gear. Over 3,000 of these spherical Bearings are used in commercial aircraft

each of which typically requires lubrication. Most of these lubrication points are difficult or at

times impossible to reach. The Company’s solution is a self-lubricating liner system that

was acquired from Harbin Aerospace Company (Harbin) in February 2010. This liner

system forms an integral component of TPAC’s finished parts and eliminates the need for

further lubrication of the Bearings, thus reducing maintenance costs.

The Company produces key Bearing components through their Chinese subsidiary, Godfrey

(China) Limited (Godfrey), which are then mated with US made self-lubricating linings and

race surfaces at the Company’s manufacturing facility; in China. The Company received

Society of Automotive Engineers (SAE) certification for its products from the Naval Air

Systems Command (NAVAIR), which made TPAC China’s first and only SAE certified

bearings producer. The Company now plans to commence manufacturing operations in the

second quarter of 2014.

In terms of future expansion, the Company’s strategy is to target countries where the

Company will be the sole domestic manufacturer or where the large makers of commercial

aircraft such as Boeing, Airbus, Embraer and Bombardier have significant offset obligations,

requiring them to co-produce structural airframe components with a domestic partner, or

procure domestic parts for incorporation or installation into items sold.1 To that end, the

Company has identified China and the Middle East as its initial target markets.

Currently, the Company owns 55% of Godfrey. It is in discussions with several of China’s

largest bearing manufacturers to serve as supply chain partners. TPAC is qualified to sell its

product to Original Equipment Manufacturers (OEMs), Airlines, and Maintenance and

Repair Organizations (MROs), and is currently focusing on pre-selling and filling the sales

pipeline. The Company is expected to start marketing, distribution, and sale of Bearings in

the second quarter of 2014.

TPAC’s innovative products, state of the art production facility, and business model which

leverages strong joint venture partners, will enable the Company to fully exploit the huge

growth potential of the Chinese commercial aviation market. Over time, we expect TPAC to

leverage these same assets and strategy in additional geographic locations to establish

itself as a global brand with local roots and carve out a share of the global bearing market,

which is expected to reach US$101 billion by 2018.iii

1Arrangements in which the buyer of the aircraft obligates the seller (OEMs) to provide the former with some business

that will help them offset the huge outflow of money under the contract for sale.

Price (US$): (March 25, 2014) 0.05

Beta: 0.53

Price/Book Ratio: NM

Debt/Equity Ratio: NM

Listed Exchange: OTCQB

*Company listed on the OTCBB and is compared to S&P

500. Source: Bloomberg.

Recent News

09/09/2013: TPAC announced that its China

subsidiary has passed all qualification testing

for SAE Aerospace Standard (AS) 81820

and has received formal written qualification

approval from the U.S. Navy, becoming the

first manufacturer in China qualified to

produce Bearings under this standard and

under SAE-AS81934. This has put the

Company on the Qualified Product Listing

(QPL) supplier list which will allow them to

pursue long term competitive contracts not

only for aircraft and sub-assemblies made in

China by Airbus and Boeing, but throughout

the world.i

04/11/2013: TPAC entered into separate

Securities Purchase Agreements with former

shareholders of Godfrey to increase its

ownership stake in Godfrey (China) Limited,

Hong Kong Corporation from 25% to 55%.ii

Shares in Issue

109.29M

Market Cap

US$5.46M

52 Week (High): US$0.12

52 Week (Low): US$0.02

Trans-Pacific Aerospace Co. Inc.

(Ticker: OTCQB:TPAC)

March 25, 2014

www.RBMILESTONE.com

www.RBMILESTONE.com

1,300

1,400

1,500

1,600

1,700

1,800

0.03

0.05

0.07

0.09

0.11

0.13

0.15

Ma

r-1

3

Apr-

13

Ma

y-1

3

Jun

-13

Jul-

13

Aug

-13

Sep

-13

Oct-

13

No

v-1

3

De

c-1

3

Jan

-14

Fe

b-1

4

Ma

r-1

4

TPAC S&P 500

Equity Research and Market Intelligence

2

Investment Arguments

Rapidly Developing Chinese Market: China is expected to remain the largest market

for airplanes outside the U.S. It is expected that China will take delivery of 5,260 new

airplanes valued at US$670 billion by 2031. Additionally, China plans to spend a

quarter of a trillion dollars over next few years in order to build a robust aerospace

industry. This in turn will have a cascading effect on the spherical bearings market as

an estimated 3,000 bearings are used in every aircraft, which require regular

replacement. The country, in its 12th Five-Year Plan (2011-2015), has set building a

robust and competitive commercial aerospace sector as one of the country’s top seven

prioritiesiv.The immense potential of the Chinese market along with Government

support for the commercial aerospace industry significantly improves the prospects for

domestic component manufacturers like TPAC.

Innovative Business Model: TPAC possesses proprietary self-lubricating liner system

which is manufactured at its facility in the U.S., exported to China and then mated with

key Bearing components produced at the Company’s facility in China. The Company is

the only manufacturer of self-lubricating SAE-AS certified Bearings in China. TPAC has

an innovative business model that leverages the need for offset requirements in China

(35% of each aircraft’s purchase pricev) and the demand for a domestic supplier of

aerospace parts.

Impressive Customer Base: The Company intends to target OEMs including Boeing,

Airbus, Embraer; Airlines like Air China, China Southern, China Eastern; and MROs in

Guangzhou, Beijing, Xiamen, Shandong as potential customers. We believe that the

Company’s presence in China will help the Company gain access to this impressive

customer base, which includes some of the largest players of the industry.

Competitive Advantage: Minebea Co., Ltd and RBC Bearings are the Company’s key

competitors as they also produce self-lubricating bearings. Neither Minebea nor RBC

manufactures aerospace spherical bearings in China. A domestic manufacturer such

as TPAC is protected by a 24% import tax and duty on imported parts, and additionally

OEMs must meet offset obligations on sales made to Chinese companies. Through its

improved manufacturing techniques, TPAC also has an advantage with significantly

reduced delivery times which may be as low as 16 weeks on average (shorter if

components are in stock) versus 52 weeks on average for typical competitors.

Strong Management Team & Board Members: TPAC’s management team is highly

proficient with significant experience in the aerospace and manufacturing industry.

Additionally, the team includes members on the board that have expertise in the field of

international procurement and production, business management, program

management, government compliance and cross border business development. Some

companies TPAC’s personnel have been associated with include, but are not limited to,

Airbus, Boeing, Embraer, Timken, AVIC and Northrop Grumman. This should therefore

put TPAC in a good position to execute a model of building a distribution chain and

expanding business operations in China.

3

Trans-Pacific Aerospace Company Inc.

Company Overview

Trans-Pacific Aerospace Company, Inc. is a development stage company engaged in

designing, manufacturing, and selling SAE-AS81820, 81934 and 81935 certified Bearings

for commercial aircraft. These Bearings reduce friction and bear loads and aid in

performing critical tasks related to a number of applications including aircraft flight controls

and landing gear operation. The Company has established a manufacturing facility in the

Scientific and Technology Center in Guangzhou, China through its subsidiary, Godfrey, to

manufacture aerospace quality standard Bearings2. The Company’s key proprietary

technology, self-lubricating liner system, is manufactured at a third party U.S. facility and

then sent to TPAC’s facility in Guangzhou, China for final assembly making sure the IP

stays protected. The high quality, U.S. made material is an important component of the

Company’s finished parts that are used in aircraft where lubrication is difficult or

impossible to perform.

Initially, the Company was incorporated in June 2007, as Gas Salvage Corp., an Oil and

Gas (O&G) company focused on exploring and evaluating undeveloped O&G prospects

and participating in drilling activities. Later in 2008, the Company changed its name to

Pinnacle Energy Corp. During the period, 2007-2009, the Company focused on acquiring

and developing O&G resources. However, pursuant to the acquisition of aircraft design

and manufacture business of Harbin in February 2010, the Company divested its O&G

properties and shifted its business focus to the designing of aircraft component parts.

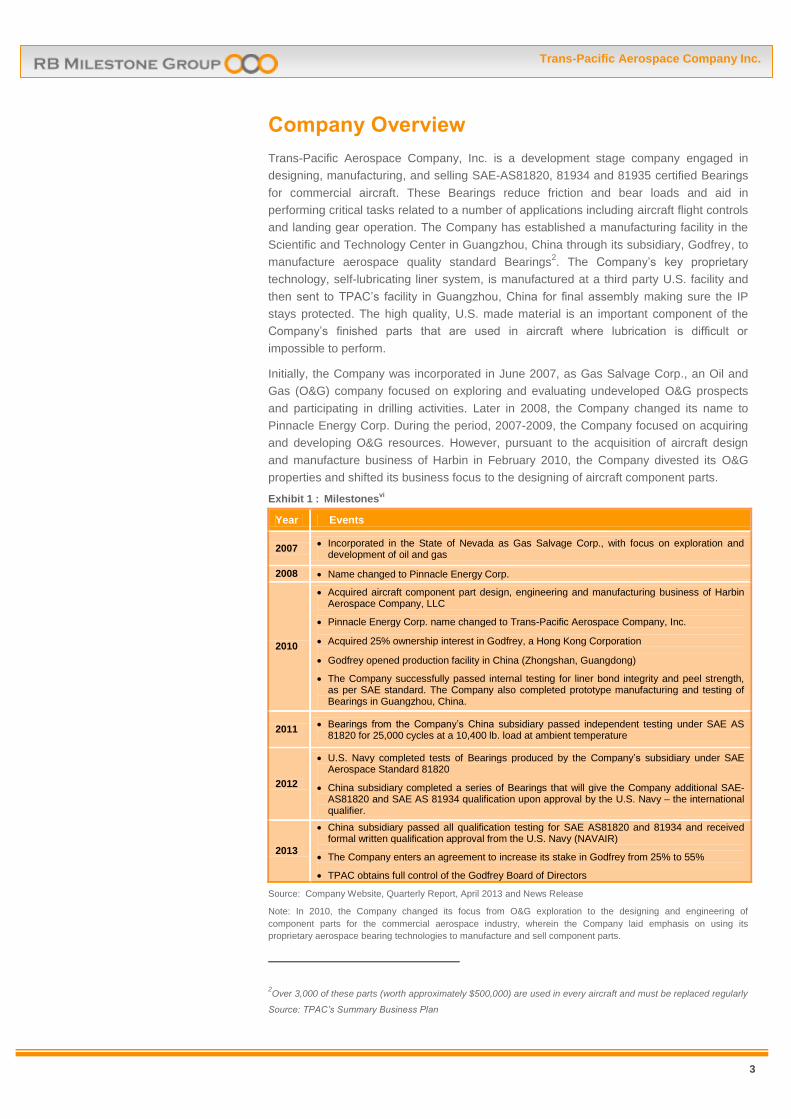

Exhibit 1 : Milestonesvi

Year Events

2007 Incorporated in the State of Nevada as Gas Salvage Corp., with focus on exploration and

development of oil and gas

2008 Name changed to Pinnacle Energy Corp.

2010

Acquired aircraft component part design, engineering and manufacturing business of Harbin Aerospace Company, LLC

Pinnacle Energy Corp. name changed to Trans-Pacific Aerospace Company, Inc.

Acquired 25% ownership interest in Godfrey, a Hong Kong Corporation

Godfrey opened production facility in China (Zhongshan, Guangdong)

The Company successfully passed internal testing for liner bond integrity and peel strength, as per SAE standard. The Company also completed prototype manufacturing and testing of Bearings in Guangzhou, China.

2011 Bearings from the Company’s China subsidiary passed independent testing under SAE AS

81820 for 25,000 cycles at a 10,400 lb. load at ambient temperature

2012

U.S. Navy completed tests of Bearings produced by the Company’s subsidiary under SAE Aerospace Standard 81820

China subsidiary completed a series of Bearings that will give the Company additional SAE-AS81820 and SAE AS 81934 qualification upon approval by the U.S. Navy – the international qualifier.

2013

China subsidiary passed all qualification testing for SAE AS81820 and 81934 and received formal written qualification approval from the U.S. Navy (NAVAIR)

The Company enters an agreement to increase its stake in Godfrey from 25% to 55%

TPAC obtains full control of the Godfrey Board of Directors

Source: Company Website, Quarterly Report, April 2013 and News Release

Note: In 2010, the Company changed its focus from O&G exploration to the designing and engineering of

component parts for the commercial aerospace industry, wherein the Company laid emphasis on using its

proprietary aerospace bearing technologies to manufacture and sell component parts.

2Over 3,000 of these parts (worth approximately $500,000) are used in every aircraft and must be replaced regularly

Source: TPAC’s Summary Business Plan

4

Trans-Pacific Aerospace Company Inc.

Key Product

Plain Spherical Bearings

Description

The Company manufactures SAE-AS81820, 81934 and 81935 certified, self-lubricating

plain spherical Bearings composed of a ball3 and a race

4. These Bearings allow a slight

degree of angular rotation and a high degree of misalignment.5

The production of spherical Bearings occurs in 6 steps:

(1) Machining of ball and race

(2) Preparation of self-lubricating liners

(3) Assembly of race and liner

(4) Swaging of ball in race

(5) Final curing; and

(6) Final machining.

These steps take approximately 14 days to complete and employ a variety of tools,

equipment, and processes, some of which can be outsourced and/or performed at

different facilities.

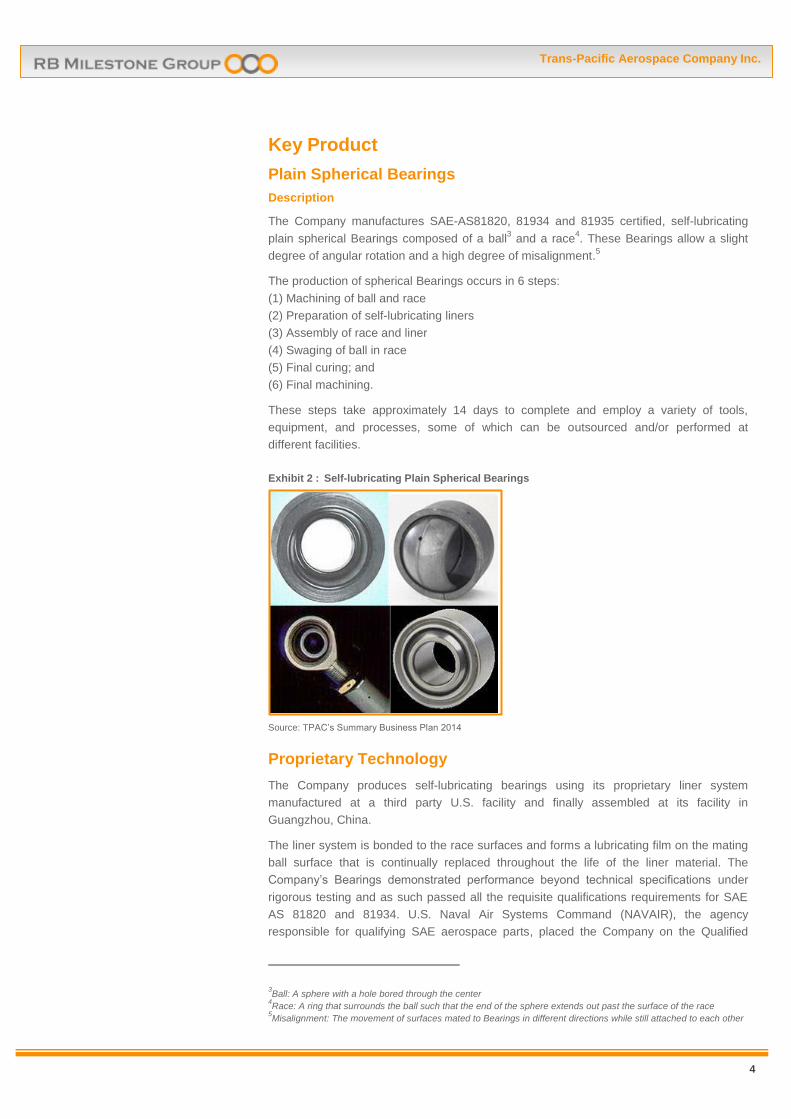

Exhibit 2 : Self-lubricating Plain Spherical Bearings

Source: TPAC’s Summary Business Plan 2014

Proprietary Technology

The Company produces self-lubricating bearings using its proprietary liner system

manufactured at a third party U.S. facility and finally assembled at its facility in

Guangzhou, China.

The liner system is bonded to the race surfaces and forms a lubricating film on the mating

ball surface that is continually replaced throughout the life of the liner material. The

Company’s Bearings demonstrated performance beyond technical specifications under

rigorous testing and as such passed all the requisite qualifications requirements for SAE

AS 81820 and 81934. U.S. Naval Air Systems Command (NAVAIR), the agency

responsible for qualifying SAE aerospace parts, placed the Company on the Qualified

3Ball: A sphere with a hole bored through the center

4Race: A ring that surrounds the ball such that the end of the sphere extends out past the surface of the race

5Misalignment: The movement of surfaces mated to Bearings in different directions while still attached to each other

5

Trans-Pacific Aerospace Company Inc.

Product Listing as a supplier making TPAC the first and only manufacturer of SAE certified

Bearings in China. The Bearings conform to SAE AS specifications and can operate under

dynamic load at temperatures ranging between -65°F and 350°F while being exposed to

contaminants such as jet fuel, de-icing chemicals, water and oil.6

TPAC uses an exotic blend of aerospace quality raw materials 1) Stainless Steel: 15-5 ph,

17-4 ph, 13-8 ph, and 2) Carbon Steel: 440C; 4,130, 4,340 and 52,100 for the

manufacture of all its products. A proprietary production process coupled with its state-of-

the-art facilities is expected to result in a very high degree of precision, which in turn will

result in scrap rates being less than 1%, enabling the Company to deliver orders as little

as 16 weeks on average (shorter with components in stock) compared to 52 weeks

typically required by its competitors while maintaining gross profit margins of

approximately 67%.

With final approval received from NAVAIR, it expects to commence manufacturing

operations in the second quarter of 2014.

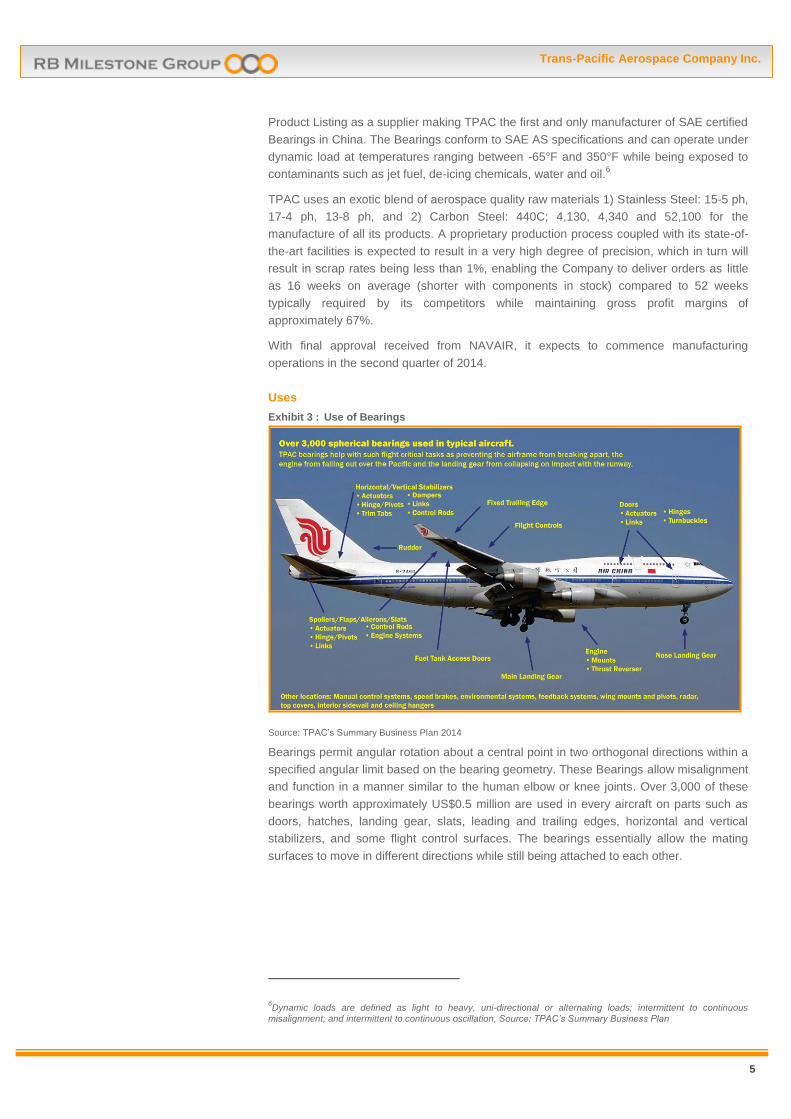

Uses

Exhibit 3 : Use of Bearings

Source: TPAC’s Summary Business Plan 2014

Bearings permit angular rotation about a central point in two orthogonal directions within a

specified angular limit based on the bearing geometry. These Bearings allow misalignment

and function in a manner similar to the human elbow or knee joints. Over 3,000 of these

bearings worth approximately US$0.5 million are used in every aircraft on parts such as

doors, hatches, landing gear, slats, leading and trailing edges, horizontal and vertical

stabilizers, and some flight control surfaces. The bearings essentially allow the mating

surfaces to move in different directions while still being attached to each other.

6Dynamic loads are defined as light to heavy, uni-directional or alternating loads; intermittent to continuous

misalignment; and intermittent to continuous oscillation, Source: TPAC’s Summary Business Plan

6

Trans-Pacific Aerospace Company Inc.

Company Strategy and Business Model

The Company owns a proprietary technology which is not subject to export restrictions

established by the U.S. Department of Commerce or Commerce Control List. This permits

the Company to manufacture aerospace approved self-lubricating commercial aircraft

consumable component parts. The Company now aims to monetize its proprietary

technology. The Company is currently focusing on leveraging its product design and

engineering expertise with manufacturers in international markets and forming business

relations to gain access to their manufacturing facilities or distribution network. By

collaborating with foreign partners that have a strong local presence, the Company will

benefit from local economies of scale. This model is particularly well suited to emerging

nations such as China and the Middle East. The Company’s business model is to target

only those countries where the resulting Company entity is the sole domestic manufacturer

and where commercial aircraft manufacturers have offset obligations.7

Partnership Agreements vii

Godfrey - Manufacturing

On March 30, 2010, the Company acquired 25% ownership interest in Godfrey, a Hong

Kong corporation, in exchange for providing Godfrey with the technology for designing and

producing SAE-AS81820, SAE-AS81934 and SAE-AS 81935 Bearings. In September

2010, Godfrey established a manufacturing facility in the Scientific and Technology Center

in Guangzhou, China. In April 2013, Godfrey Guangzhou Aerospace Bearings, a wholly

owned subsidiary of Godfrey, received qualification approval for SAE AS81820 and

AS81934 from the U.S. Navy, confirming the facility as the first and only SAE qualified

manufacturing facility in China. The approval has provided the Guangzhou facility with a

position in the Qualified Product Listing (QPL) as a supplier.

In April 2013, the Company entered into a separate securities purchase agreement with

shareholders of Godfrey China, which gave the Company majority ownership interest in

Godfrey: from 25% to 55%.viii

Future Plans

The Company is negotiating with some of China’s largest bearing manufacturers and

expects to sign joint ventures and/or supply chain partnership agreements. TPAC is

planning to enter joint ventures on the terms that its foreign partners will provide the

manufacturing labor, the requisite raw materials as well as machinery and equipment. The

Company in turn will provide the manufacturing facility, the manufacturing know-how, the

blueprints for approximately 1,500 parts and the use of the proprietary self-lubricating liner

system.

Sales and Marketing Strategy

The Company intends to implement a strategic brand management initiative that will

position it as a global brand with local roots. The Company expects this brand building

exercise to support sales activities while building a strong sales pipeline. Additionally, the

Company also plans on reaching out to leading bearing distributors and the sub-assembly

industry among others. As part of its marketing strategy, the Company aims at the

following:

7Arrangements in which the buyer of the aircraft obligates the seller (OEMs) to provide the former with some

business that will help them offset the huge outflow of money under the contract for sale.

7

Trans-Pacific Aerospace Company Inc.

1) Participating in major air and aerospace trade shows

2) Participating in trade shows for Airlines and MRO’s

3) Undertaking trade publicity in order to create market buzz about the Company

4) Touring key markets when government sponsored expositions are being held

5) Sponsoring “best practice” seminars for airlines and MRO’s

6) Updating its website with “best practice” webcasts

7) Creating sales support material such as product DVD’s for its distributors

8) Launching a turnkey product financing program

The Company will target its initial marketing efforts at OEM’s, China based airlines and

MROs. The Company expects to commence the marketing, distribution and sale of

Godfrey’s initial line of Bearings in the second quarter of 2014.ix

Pricing Strategyx

The Company intends to price its products competitively with the market. As the sole local

source to China-based airlines and MROs, the purchasers will not need to pay the 24%

import taxes and duties on bearings brought into China, which will enable its customers to

effectively receive a 24% discount over what they are paying now, while the Company’s

prices remain competitive with the market. The combination of the strategy to price at

prevailing market rates and the exemption from import duties will enable the Company to

maintain a gross profit margin of 67% and will provide an incentive for Chinese companies

to purchase from TPAC.

Competitive Strategyxi xii

Minebea Co., Ltd and RBC Bearings, both of whom produce self-lubricating bearing are

TPAC’s primary competitors. Minebea Co., Ltd is a Japanese Multinational Corporation,

producing machinery components and electronic devices. It is the world’s largest

manufacturer of small ball bearings with a global market share of 60%. While Minebea

has plants in Shanghai and Zhuai, these facilities produce easy-to-make ball bearings, DC

motors etc., but do not have required capacity or technology to make self-lubricating

bearings in China. RBC Bearings is based in the USA and is involved in the manufacture

of various types of bearings and rod-ends for its defense and aerospace customers

commanding an estimated market share of 9%. RBC, on the other hand, has not disclosed

any plans to enter China.

The Company also plans to partner with existing aerospace companies in emerging

markets and utilize their manufacturing facilities and distribution networks. In order to

reduce their own capital requirements, the Company’s focus remains on providing design

and engineering expertise to the larger players. As the Company’s facility commences full

operations, it will be the only manufacturer of SAE-AS certified aircraft component parts in

China.

8

Trans-Pacific Aerospace Company Inc.

Industry Overview

Aerospace

The Aerospace industry produces military and commercial fixed wing aircraft, rotary-wing

aircraft, business and general aviation aircraft, gas turbine engines, unmanned aerial

vehicles and drones, space/launch vehicles and missiles covering a broad range of

sectors. According to the Global A&D Industry Financial Performance Study, June 2013

published by Deloitte, the global A&D industry revenue increased by 5.9% from US$653.7

billion in 2011 to US$692.5 billion in 2012.xiii

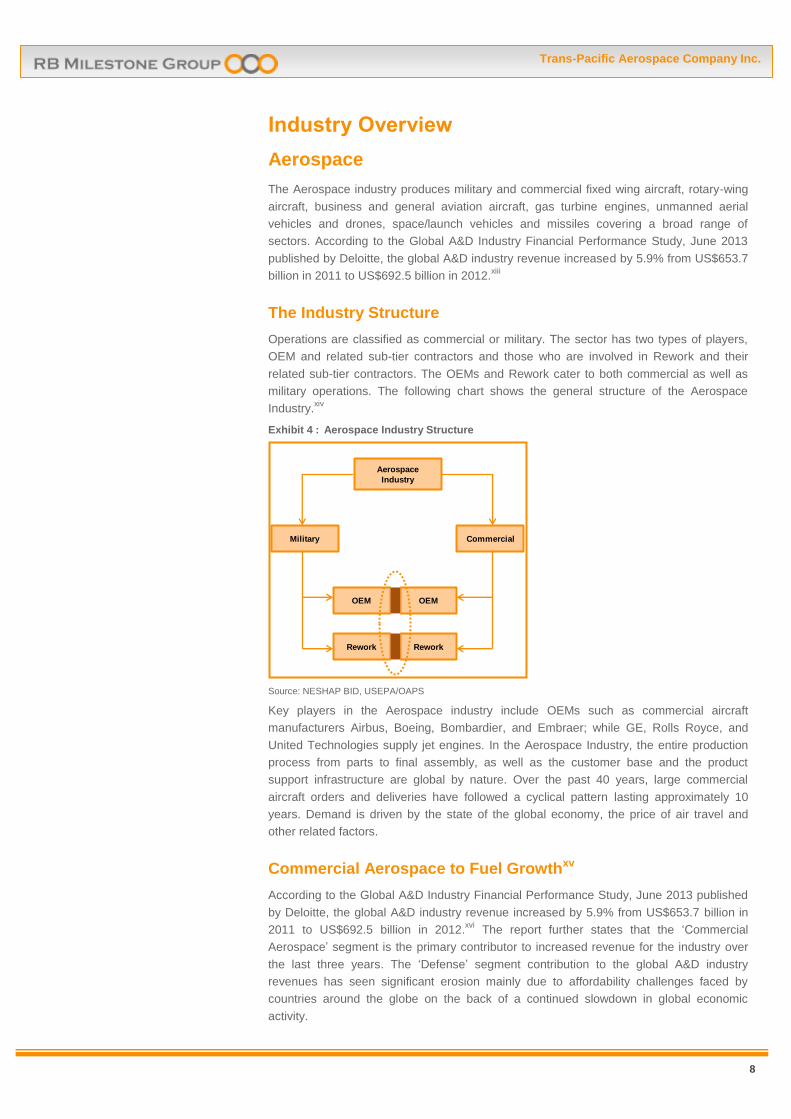

The Industry Structure

Operations are classified as commercial or military. The sector has two types of players,

OEM and related sub-tier contractors and those who are involved in Rework and their

related sub-tier contractors. The OEMs and Rework cater to both commercial as well as

military operations. The following chart shows the general structure of the Aerospace

Industry.xiv

Exhibit 4 : Aerospace Industry Structure

Source: NESHAP BID, USEPA/OAPS

Key players in the Aerospace industry include OEMs such as commercial aircraft

manufacturers Airbus, Boeing, Bombardier, and Embraer; while GE, Rolls Royce, and

United Technologies supply jet engines. In the Aerospace Industry, the entire production

process from parts to final assembly, as well as the customer base and the product

support infrastructure are global by nature. Over the past 40 years, large commercial

aircraft orders and deliveries have followed a cyclical pattern lasting approximately 10

years. Demand is driven by the state of the global economy, the price of air travel and

other related factors.

Commercial Aerospace to Fuel Growthxv

According to the Global A&D Industry Financial Performance Study, June 2013 published

by Deloitte, the global A&D industry revenue increased by 5.9% from US$653.7 billion in

2011 to US$692.5 billion in 2012.xvi

The report further states that the ‘Commercial

Aerospace’ segment is the primary contributor to increased revenue for the industry over

the last three years. The ‘Defense’ segment contribution to the global A&D industry

revenues has seen significant erosion mainly due to affordability challenges faced by

countries around the globe on the back of a continued slowdown in global economic

activity.

Military

Aerospace

Industry

Rework

OEM

Rework

OEM

Commercial

9

Trans-Pacific Aerospace Company Inc.

The chart below depicts the contribution made by the commercial aerospace and defense

segments over the last 3 years:

Exhibit 5 : Contribution by Segment to Global A&D Industry Revenuexvii

Source: Boeing Current Market Outlook2012-2031xviii

Aerospace Industry in Chinaxix

Over the next few years, China aims to spend a quarter of a trillion dollars in order to

develop its domestic aerospace industry with the country currently accounting for two-

thirds of all airports under construction globally.xx

With an expected delivery of 5,260 new

airplanes valued at US$670 billion by 2031, China is clearly poised to be the largest

market for airplanes outside the U.S.xxi

According to a PWC report, the global commercial aircraft fleet is expected to nearly

double to 40,000 units by 2030 with emerging market demand forecasted to grow at

double the pace of the developed market demand. Most of the growth is expected to occur

in Asia, Latin America, Middle East, China, and India. In particular, China states in its 12th

Five-Year Plan (2011-2015) that building a robust and competitive commercial aerospace

sector is one of the country’s top seven priorities.xxii

The report also indicates a change in

the country’s aerospace strategy in the coming years from being a buyer of western

technologies to a domestic developer of aerospace technologies. The country is now

channeling its human and capital resources into the aerospace industry in order to achieve

its long-term goal of building and developing commercial aircraft instead of just being a

supplier to leading aerospace companies like Boeing, Airbus, and the others.

Exhibit 6 : China Aircraft Fleet by Sizexxiii

Source: Boeing Current Market Outlook_2012-2031

39.4% 41.9% 45.9%

60.6% 58.1% 54.1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012

Commercial Aerospace Defense

1,490

4,220 280

1,310

140

450

0

1,000

2,000

3,000

4,000

5,000

6,000

2011 Fleet 2031 Fleet

5,980

1,910

Total

Total

Other

Other Twin Aisle

Twin Aisle

Single Aisle

Single Aisle

10

Trans-Pacific Aerospace Company Inc.

The Bearing Industryxxiv

The Global bearing industry, a multi-billion dollar market, is highly fragmented in nature.

Manufacturers of commercial and military aerospace equipment, automotive and

commercial truck manufacturers, agricultural machinery manufacturers, industrial

equipment and machinery manufacturers and construction, mining and specialized

equipment manufacturers are the major buyers of bearings. According to a report by

Global Industry Analysts, Inc., the global bearings market is forecasted to reach US$101

billion by 2018, aided primarily by a strong recovery in aerospace, automotive and

industrial machinery industries as well as a supportive capital investment climate.xxv

The different types of standard bearings include journal bearings, spherical bearings,

rolling element bearings and rod-ends (“Bearings”) all of which are manufactured by the

Company. Within the standard bearings group, approximately 3,000 Bearings are used on

every aircraft. Annual sales of these Bearings for commercial aircraft are estimated to

increase to US$1.5 billion in 2014, and subsequently grow at a compounded annual

growth rate (CAGR) of 5.4% to 1.8 billion in 2018xxvi

. A new World Bearings study from

The Freedonia Group indicates that although the automotive and machinery markets will

remain the largest segments through 2016, their overall share will decline as sales of

bearings used in aerospace and other applications will increase at slightly faster rate.xxvii

Major players in the industry include EnPro Industries Inc., Federal-Mogul Corporation,

JTEKT Corporation, NSK Ltd., NTN Corp., igus, LM-Tabell Inc., Minebea Co., Ltd., Misumi

USA Inc., RBC France SAS, RBC Bearings USA, Schaeffler Technologies, SKF Group,

The Timken Company, and Spyraflo Inc.

Primary Drivers of Bearing Demandxxviii xxix

The demand for bearings is largely dynamic and depends mainly on global Gross

Domestic Product (GDP) trends due to their extensive use in the capital goods,

engineering, and automotive sectors. In the Defense Market, the demand for bearings

hinges on the spending patterns of countries on new equipment and the extent of

utilization of existing equipment to support the demand for replacement bearings. Within

the Aerospace Market, traffic growth of carriers and the aging of existing commercial fleet

determine the demand for bearings.

China: To lead the next phase of Growthxxx xxxi

The Global Bearing Industry went through a difficult phase during the global financial crisis

of 2008 as major end users including the automotive, aerospace and industrial machinery

industries suffered major setbacks during the recessionary period. The emergence of the

sovereign debt crisis in Europe, sluggish recovery of growth in the U.S. and contraction in

the Japanese economy led to a further drop in demand during 2011-2012. A gradual

recovery in economic activity is expected to drive demand in the long term, while the short

term poses significant risks due to the increased financial pressures on several end users.

A recent report by Global Industry Analysts, Inc.xxxii

, states that manufacture of rail

equipment, electronic devices, aircrafts and motorcycles in the developing regions would

determine demand for bearings with the Asia-pacific region representing the largest and

fastest growing market for bearings. The report further states that China tops the list of the

fastest and largest growing bearings market in the Asia Pacific region. The bearings

industry in China is extremely fragmented with the main international bearing companies

covering about one third of the market and the remaining two-thirds covered by the local

manufacturers.

11

Trans-Pacific Aerospace Company Inc.

Some of the largest Chinese players include Wafangdian, Luoyang, Zhejiang Tianma

(TMB), Wanxiang Qianchao, and C&U. While high-paced industrialization and urbanization

have fuelled the demand for bearing from the automotive and industrial machinery

industries, the country’s massive investment in aviation markets has ensured a buoyant

aerospace market. Thus, any deceleration in Chinese growth would heavily impact the

global bearings market.

Growth Factorsxxxiii

Proprietary Technology

The key to the Company’s growth in China lies in its proprietary self-lubricating liner

system and manufacturing and design technologies. The self-lubricating liner is an integral

component of the Company’s finished parts used in an aircraft where lubrication is difficult

or impossible to perform. In practice, the liner system is bonded to race surfaces and

during use forms a lubricating film on the mating ball surface that is continually replaced

throughout the life of the liner material. This proprietary technology remains a primary

growth driver for the Company, providing it a significant competitive advantage since none

of the China-based manufacturers have been successful in making these parts or

producing a similar liner, thereby making TPAC the first and only manufacturer of SAE-

certified bearings in China.

Offset Requirements

One of TPAC’s primary business strategies includes targeting only those countries where

the three largest makers of commercial aircraft have significant offset obligations8. As per

the 35% offset requirements in China, OEMs such as Airbus and Boeing are obligated to

spend more than US$16 billion which would have to be fulfilled through the purchase of

locally-sourced materials. This opens a window of opportunity for TPAC as it could tap

some portion of this potential $16 billion worth of demand. This would not only ensure

exponential growth in revenues in the future due to the sustainability of orders from the

larger OEMs, but also eliminate a fair share of business risk that the Company would have

been exposed to in the absence of orders.

Strong Partnerships

Having a qualified manufacturing facility in China exposes the Company to leading OEMs

(e.g. Boeing, Airbus, Embraer), Airlines (e.g. Air China, China Southern and China

Eastern), and MROs in the cities of Beijing, Guangzhou, Xiamen, and Shandong. Apart

from AVIC, the Company is already negotiating with several of the largest bearing

manufacturers in China as potential joint venture or supply chain partners. An established

set of business relationships will thus enable the Company to capture valuable market

share from its competitors as it commences operations in the future.

8 Arrangements in which the buyer of the aircraft obligates the seller (OEMs) to provide the former with some business that will help them offset the huge outflow of money under the contract for sale.

12

Trans-Pacific Aerospace Company Inc.

SWOT

Strengths

Qualification Approvals. TPAC has recently received formal written qualification

approval for SAE AS81820 and 81934. This qualification approval that the Company

received made it the first and only qualified SAE-certified Bearing manufacturer in

China, paving the way for all Chinese and international airframe manufacturers, sub-

tier suppliers, MRO facilities, airlines and distributors to purchase aerospace

component parts from its facility in China. The qualifier, US Navy or NAVAIR, has

placed TPAC on the Qualified Product Listing as an official supplier of these bearings

allowing it to begin marketing and selling its products. Towards the end of 2014 the

Company plans to seek NAVAIR approval under SAE-AS81935, which should open

up additional sales opportunities.xxxiv

Import Tax Advantage. Imported component parts in China are subjected to 24%

import tax and duty. Since the Company has established a manufacturing facility in

China, China-based airlines and MROs can source Bearings from TPAC avoiding the

minimum 24% import duty, giving the Company a significant competitive

advantage.xxxv

Experienced Technical and Management Team. The Company’s management

team is highly proficient with significant experience in the aerospace and

manufacturing industries. Additionally, the team also includes board members with

significant expertise in the fields of international procurement and production,

business management, program management, government compliance, and cross-

border business development. Some companies in the aerospace industry that

management and board members have been associated with include, but are not

limited to Airbus, Boeing, Timken, Bombardier and Northrop Grumman.xxxvi

Weaknesses

Losses Resulting in Dilution of Shareholder Base. The Company has not

generated any commercial revenues, and has financed operations to date through

equity and debt offerings. The need to further finance operations in the future could

lead to a dilution of shareholders wealth.

Patent: Currently, the Company does not hold any patents for its proprietary

technology. TPAC’s technology is protected by trade secrets. Critical manufacturing

processes, including liner production, are conducted in the USA in order to prevent

the compromise of this trade secret. The Company management believes that while

bearing manufacturers in China have been attempting to build a self-lubricating liner

system for the past 20 years, they have not yet been successful. Not filing a patent for

its system and processes is quite common in this industry as there’s no information

that will eventually become public knowledge. However, competitors may, over time,

develop similar self-lubricating bearings.

Opportunities

Commercial Aerospace on the Priority List: According to Boeing estimates made

in 2012, China is expected to take delivery of 5,260 new airplanes valued at US$670

billion by 2031. This is consistent with China’s plans to spend a quarter of a trillion

dollars to build a robust aerospace industry, and would make it the largest market for

airplanes outside the U.S. In its 12th

Five-Year Plan (2011-2015), China has indicated

13

Trans-Pacific Aerospace Company Inc.

that building a robust and competitive commercial aerospace sector is one of the

country’s top seven priorities.xxxvii

The emergence of Aerospace as a national priority

in China is expected to result in increased government and private sector spending

which will provide substantial room for domestic component manufacturers to grow

and expand their operations.

Benefits of the Offset Agreements: As a part of the offset agreement, OEMS such

as Boeing and Airbus owe more than US$16 billion to China. These offset

agreements protect Chinese manufacturers as OEMS are obliged to purchase

domestic Chinese products in order to offset the huge outflow of money resulting from

the purchase of aircrafts and associated components. These agreements provide a

huge opportunity to local domestic manufacturers not only from a sales perspective

but also from the point of establishing valuable business relations with the large

players of the aerospace market for orders in the future.

Limited Domestic Competition: Minebea Co., Ltd and RBC Bearings, the

Company’s primary competitors, both manufacture self-lubricating bearings. While

Minebea has plants in Shanghai and Zhuai, these facilities essentially produce easy-

to-make ball bearings, DC motors, etc. It however, does not have the requisite

technology or capacity to make self-lubricating bearings in China. RBC, on the other

hand, does not have any plans to enter the Chinese market. Thus, limited competition

from the large players presented an open Chinese market for small players like Trans-

Pacific Aerospace to commence their operations and gradually capture valuable

market share in order to counter any kind of competition which might arise from other

local domestic manufacturers in the future.

Threats

Possibility of a Hard Landing in China: From an average annual Gross Domestic

Product (GDP) growth of 9.8% for the last three decades,xxxviii

the country’s economy

has seen decelerating growth for 13 consecutive quarters with the GDP growing at

7.5% Y-o-Y in the second quarter of the current yearxxxix

. With 50% of GDP coming

from gross fixed capital formation, rising corporate and private sector debt and huge

excess capacity are emerging signs of an imbalanced economy. As the country goes

through this transition phase, from being an investment-driven economy to a

consumption led one, any slowdown in investment would adversely affect the capital

intensive sectors of the economy. This poses a threat to the aerospace industry in the

country as aviation spending plans could get reduced in the future, with a

corresponding effect on domestic component manufacturers like TPAC.

14

Trans-Pacific Aerospace Company Inc.

Financial Performance

Exhibit 7 : Latest Income Statement (Consolidated)

In US$ '000, Ending October 31

FY2013 FY2012 Y-o-Y (%)

EXPENSES

Professional fees 94 140 (33%)

Consulting - 26 NM

Other general and administrative

1,688 1,312 29%

Total Operating Expenditure

1,782 1,478 21%

Impairment of Acquisition 528 - NM

Bad Debt Expense - 36 NM

Net Finance Cost 26 18 (44%)

Total Non-Operating Expenditure

554 54 926%

Loss Before Income Taxes (2,336) (1,533) NM

Income Tax 0.9 4 (78%)

Net Loss (2,337) (1,537) 52%

Basic and Diluted Profit (Loss) per Share

(0.03) (0.02) NM

Source: Company Filings

Results for Fiscal Year Ended October 31, 2013: The Company has not commenced

revenue producing operations to date; it has incurred a net loss from operations of

US$1.78 million during FY2013 and has an accumulated deficit of US$9.09 million since

inception (June 2007). During FY2013, the Company’s operating expenses primarily

consisting of professional fees, consulting fees, and other general and administrative

expenses which increased 21% Y-o-Y, primarily due to the issuance of common stock to

the board of directors and consultants. Net Loss rose to US$2.337 million in FY2013 from

US$1.537 million in FY2012.

Exhibit 8 : Latest Balance Sheet (Consolidated)

In US$ '000 31-Oct-13 31-Oct-12

Current assets 29 19

Non-current assets 8 5

TOTAL ASSETS 37 24

Current Liabilities 516 379

Non-current Liabilities - -

TOTAL LIABILITIES 516 379

Total Shareholder's Equity (479) (355)

TOTAL LIABILITIES & EQUITY 37 24

Source: Company Filings

Trans-Pacific had about US$0.03 million of cash on its balance sheet as on October 31,

2013, which increased by 52% on a Y-o-Y basis. Due to continuing losses from

operations, the Company has a working capital deficit of US$0.48 million. In order to fund

its expected marketing and distribution of the initial line of aircraft component products to

be manufactured by Godfrey and to fund its expected operating losses, the Company is

expected to require approximately US$2 million of additional working capital over the next

twelve months either through sale of equity or debt securities, or the formation of a joint

venture with a Chinese or international partner.

15

Trans-Pacific Aerospace Company Inc.

Key Risk Factors

Financial Risk. As a development stage company, TPAC has not yet established a

consistent source of revenues that are adequate to cover its operating costs and

facilitate the Company to continue as a going concern. Therefore, it may be

necessary for the Company to raise additional funds to cover operating losses.

Moreover, if the Company fails to obtain the required amount of capital, it may not be

able to meet its working capital requirements. Nevertheless, in the past, the Company

has proved its ability to raise adequate funds to mitigate this risk through private

placements.

Regulatory Risk. The Company operates in a sector that requires a substantial

number of regulatory product approvals and qualifications. The Company’s inability to

obtain or maintain regulatory qualifications or approvals for its products could be a

barrier to commercial sales. However, the Company’s China subsidiary Godfrey has

passed all qualification testing for SAE Aerospace Standard 81820, 81934 and 81935,

and has received formal written qualification approval from the U.S. Navy.

Patent Risk: Currently, the Company holds no patent rights for the technology used

in the designs and processes for its spherical Bearing products. Also, it is believed

that the other players in the market are aware of the technology used in the process

of producing spherical products. Some competitors in the market currently make

similar spherical Bearing products. However, in order to protect the proprietary rights,

the Company relies on the combination of confidentiality agreements and trade secret

law. TPAC believes its technology and processes will be protected moreso in this

manner than if it filed for a patent, which eventually becomes public knowledge. This

strategy is standard in this type of industry.

Competition and Margin Erosion Risk. The bearing industry is run by 7 qualified

players, one of which is TPAC. The barriers to entry are quite high; however, the other

6 players are well-established with better financial resources and the ability to

efficiently manage their costs. As a result of this competition, the Company may find it

difficult to increase prices of their products to recover the costs incurred during the

operating process and eventually eroding the Company’s margins and profitability.

16

Trans-Pacific Aerospace Company Inc.

Management Team & Board of Directorsxl

The management team has experts with significant experience in the aerospace spherical

bearing industry. The team consists of accomplished professionals with experience in

successfully handling procurement and supply chains, re-organizing manufacturing

operations & managing the deliveries time, and reducing working capital requirements.

Furthermore, the management team also includes members involved in cross-border

business development, providing the Company with the substantial support to manage

business relations in foreign countries. Some companies in the aerospace industry that

management and board members have been associated with include, but are not limited

to Airbus, Boeing, Timken, Bombardier and Northrop Grumman.

Mr. Bill McKay, CEO and Chairman of Board of Director

Mr. McKay has served as Chairman and Chief Executive Officer since February 2010. Mr.

McKay has 25 years’ experience in the aerospace/manufacturing industry, holding many

senior management positions including General Counsel, General Manager,

Manufacturing Manager, COO and CEO of both private and public companies. Mr. McKay

was founder and Chief Executive Officer of Harbin Aerospace Company, LLC, an aircraft

component part design, engineering and manufacturing company acquired by Trans-

Pacific Aerospace in 2010. Prior to forming Harbin, he was an aerospace industry

consultant involved in aerospace projects in China and other aspects of the industry (2008

to 2009). From 2006 to 2008, Mr. McKay served as Chief Operating Officer for Acromil

Corporation, an aerospace structural component manufacturing company. Within 3

months of commencing his tenure at Acromil, Mr. McKay turned the company around from

monthly losses of approximately $1 million to monthly profits in excess of $600,000.

During the same time period, he improved on-time deliveries from 0% to 90%. Prior to

Acromil, Mr. McKay served (from 1986 to 2006) in a variety of senior management roles

with Southwest Products Company, a specialized engineering consulting firm and

designer and manufacturer of plain spherical bearings used primarily in aerospace, naval

and sophisticated commercial applications. He started as General Counsel (1986), and

was promoted to Executive Vice President and General Manager (1987) and Chief

Executive Offices (1991). As part of the acquisition of Southwest Products Company by

Sunbase Asia, Inc., a Hong Kong-based aerospace company, Mr. McKay also took on the

role of President-CEO of Sunbase Asia. He received a B.A. in History (Magna Cum Laude

and Phi Beta Kappa) as well as a JD and an MBA from the University of Southern

California. He is a member of the California State Bar.

Mr. Greg Archer, Director

Mr. Archer has over 24 years of aerospace industry experience as an executive with

Northrop Grumman Corporation. From December 2002 through March 2010, he served as

director of procurement/global supply chain for the Aerospace Systems sector of Northrup

Grumman. Mr. Archer was responsible for the procurement of goods and services valued

in excess of one billion dollars and some thirty million parts across multiple programs and

platforms. In his role as the executive for procurement/global supply chain, he developed

and deployed a purchasing model that was responsive to program needs across the

sector. He was the Chief Procurement Officer for the sector and directed an organization

made up of professional buyers responsible for a wide range of products and services. In

addition to his procurement responsibilities, he was also responsible for commodity

engineering, managing and supplier of technical solutions across all programs leading an

organization made up of engineering professionals from the disciplines of manufacturing

engineering, industrial engineering and electrical engineering. Prior to his position as the

17

Trans-Pacific Aerospace Company Inc.

director of procurement, Mr. Archer held leadership positions in international procurement

and production, business management, subcontracts, program management and

government compliance. He spent several years supporting company litigation and dispute

resolution and was member of a company executive board of reviewers. He is a graduate

of California State Polytechnic State University at Pomona.

Mr. Kevin Gould, Director

Mr. Gould has over 25 year of management experience in aerospace, manufacturing, high

tech and law. Currently he is President of BendixKing, manufacturer of avionics for

General Aviation aircraft. Previously he served as President and CEO of Piper Aircraft,

Inc. During his tenure, Piper doubled its market share, outsourced its spare parts

distribution, beat its competition to market with the highly successful PiperSport,

overhauled and globalized its sales and distribution channel, initiated social networking

marketing programs, and re-launched development of its PiperJet aircraft. Earlier, Mr.

Gould served as VP of Operations at Piper where he was a member of the executive team

that turned around and sold the company. Prior to joining Piper, Mr. Gould was VP of

Operations at startup aircraft manufacturer Adam Aircraft where he set up production

operations for the company's carbon fiber piston and jet airplanes. Earlier he spent 12

years at Boeing in a variety of leadership roles including manufacturing, supply chain,

engineering, program management, finance and facilities expansion. Prior to that, Mr.

Gould spent three years as an attorney at a major Los Angeles law firm practicing

business and real estate law. He holds an MBA from Harvard University, an MS in

management from Stanford Graduate School of Business, a JD from University of

Southern California and a BA from Washington State University. He is an instrument rated

pilot.

Mr. Jason Arnold, Director xli

Mr. Arnold has over 25 years of experience in the aerospace manufacturing industry,

regularly conducting business with such companies as Airbus, Boeing, Lockheed Martin

and Northrop Grumman. At Arnold Engineering, he developed a growth strategy that

increased sales from $500k to over $30 million annually, providing customers with world

class machined and assembled aero structures for both the commercial and defense

markets. Mr. Arnold orchestrated the successful sale of Arnold Engineering in 2009 to a

Private Equity firm. He currently is an active Chairman for aircraft manufacturing

organization as well as a Trans- Pacific Board Member.

Mr. Clairmont Griffith, Director xlii

Clairmont Griffith, an aerospace devotee and specifically spherical bearings, is an

entrepreneur. He has been engaged with TPAC since early 2010, becoming a member of

TPAC's advisory board and now director. Mr. Griffith is also Director of Godfrey China

Aerospace. He currently has a minor investment interests in mining, and oil and gas

equipment. Mr. Griffith is a medical doctor and assistant professor who is a diplomat of the

American Board of Anesthesiology and National Board of Medical Examiners. He served

in various leadership roles including recent Chairman of Anesthesiology at Howard

University Hospital and becoming the first Chief of Perioperative Services there. Mr.

Griffith has also served as Chief of Obstetric Anesthesia, Vice Chairman of

Anesthesiology, Chief of Clinical Affairs, and Chief of Quality Assurance and Patient

Safety. While engaged in medical research and academics, Mr. Griffith has also been

team leader on numerous hospital committees and a member of numerous National

Medical Associations. Clairmont Griffith has received his BS in chemistry and a Medical

Degree from Howard University. He attributes his enlightened entrepreneurial vision to his

kids Alex, Quincy and Alison.

18

Trans-Pacific Aerospace Company Inc.

Disclaimer

Some of the information in this report relates to future events or future business and

financial performance. Such statements constitute forward-looking information within the

meaning of the Private Securities Litigation Act of 1995. Such statements can be only

estimations and the actual events or results may differ from those discussed due to,

among other things, the risks described Trans-Pacific Aerospace Company Inc. reports.

The content of this report with respect to Trans-Pacific Aerospace Company Inc. has

been compiled primarily from consultations and, information provided by Trans-Pacific

Aerospace Company Inc. and information available to the public released by Trans-

Pacific Aerospace Company Inc. through news releases and SEC (if applicable) or other

actual government regulatory filings. Although RBMG may verify certain aspects of

information provided to it, Trans-Pacific Aerospace Company Inc. is solely responsible

for the accuracy of that information. Information as to other companies has been

prepared from publicly available information and has not been independently verified by

Trans-Pacific Aerospace Company Inc. or RBMG. Certain summaries of scientific or

other activities and outcomes have been condensed to aid the reader in gaining a

general understanding. For more complete information about Trans-Pacific Aerospace

Company Inc. the reader is directed to the Company's website at

http://www.tpacbearings.com/. RBMG is a corporate communications firm the operations

of which seek to increase investor awareness to the small cap community. RBMG

research analysts do not invest in or own shares of companies analyzed and reported on

by them. RBMG is not responsible for any claims or losses sustained by an investor

resulting from any of its reports, company profiles or in any other investor relations

materials disseminated by them. This report is published solely for information purposes

and is not to be construed as advice designed to meet the investment needs of any

particular investor or as an offer to sell or the solicitation of an offer to buy any security in

any state. Investing in the Stock Market is a high-risk endeavor, and past performance

does not guarantee future performance. This report is not to be copied, transmitted,

displayed, distributed (for compensation or otherwise), or altered in any way without

RBMG's prior written consent. RBMG is not compensated for the analytical research and

evaluation services that were performed in connection with the preparation of this report

for Trans-Pacific Aerospace Company Inc.; but RBMG has received stock compensation

(three million shares) in exchange for other segregated services.

We strongly urge all investors to conduct their own research before making any

investment decision.

19

Trans-Pacific Aerospace Company Inc.

Sources

ihttp://www.businesswire.com/news/home/20130311005410/en/Trans-Pacific-Aerospace-Company-Receives-SAE-AS81820-SAE iihttp://www.sec.gov/Archives/edgar/data/1422295/000101968713001281/transpacific_8k-040513.htm

iiihttp://www.prweb.com/releases/plain_bearings/ball_roller_bearings/prweb10436256.htm

ivhttp://www.pwc.com/en_US/us/industrial-products/assets/pwc-gaining-attitude-issue-4-sustain-growth.pdf

vTPAC’s Summary Business Plan 2014

vihttp://www.4-traders.com/TRANS-PACIFIC-AEROSPACE-C-6033330/news-history/

vii Company Annual Filing, Company Summary Business Plan

ixQuarterly Report, April 5, 2013

xTPAC’s Summary Business Plan 2014

xiTPAC’s Summary Business Plan 2014

xiiAnnual Report, October 31, 2012

xiii http://www.deloitte.com/assets/Dcom-

UnitedStates/Local%20Assets/Documents/AD/us_AD_wrap_up_infographic_6202013.pdf

xiv http://www.epa.gov/Compliance/resources/publications/assistance/sectors/notebooks/aersn.pdf

xv http://www.deloitte.com/assets/Dcom-

UnitedStates/Local%20Assets/Documents/AD/us_AD_wrap_up_infographic_6202013.pdf

xvi http://www.deloitte.com/assets/Dcom-

UnitedStates/Local%20Assets/Documents/AD/us_AD_wrap_up_infographic_6202013.pdf

xvii http://www.deloitte.com/assets/Dcom-

UnitedStates/Local%20Assets/Documents/AD/us_AD_wrap_up_infographic_6202013.pdf

xviiihttp://libraryonline.erau.edu/online-full-text/books-online/Boeing_Current_Market_Outlook_2012.pdf xix

http://www.pwc.com/en_US/us/industrial-products/assets/pwc-gaining-attitude-issue-4-sustain-growth.pdf

xxTPAC’s Summary Business Plan 2014

xxiTPAC’s Summary Business Plan 2014

xxiihttp://www.pwc.com/en_US/us/industrial-products/assets/pwc-gaining-attitude-issue-4-sustain-growth.pdf

xxiiihttp://libraryonline.erau.edu/online-full-text/books-online/Boeing_Current_Market_Outlook_2012.pdf

xxiv RBC bearings annual report for the fiscal year ended 30th March 2013

xxvhttp://www.prweb.com/releases/plain_bearings/ball_roller_bearings/prweb10436256.htm

xxviTPAC’s Summary Business Plan 2014

xxviihttp://www.prnewswire.com/news-releases/world-bearings-market-162562406.html

xxviiiRBC bearings annual report for the fiscal year ended March 30, 2013

xxixhttp://www.prweb.com/releases/plain_bearings/ball_roller_bearings/prweb10436256.htm

xxxhttp://www.prweb.com/releases/plain_bearings/ball_roller_bearings/prweb10436256.htm

xxxihttp://www.skf.com/group/investors/bearings-market

xxxii http://www.prweb.com/releases/plain_bearings/ball_roller_bearings/prweb10436256.htm

xxxiiiTPAC’s Summary Business Plan 2014

20

Trans-Pacific Aerospace Company Inc.

xxxivhttp://www.businesswire.com/news/home/20130909005569/en/Trans-Pacific-Aerospace-Company-Receives-

Additional-NAVAIR-Approvals

xxxvTPAC’s Summary Business Plan 2014

xxxviTPAC’s February 2014 Investor Presentation

xxxviihttp://www.pwc.com/en_US/us/industrial-products/assets/pwc-gaining-attitude-issue-4-sustain-growth.pdf

xxxviiihttp://www.china.org.cn/opinion/2013-08/07/content_29646629.htm

xxxixhttp://www.bbc.co.uk/news/business-23310975

xl Company Website, Annual Results Filing and Company Summary Business Plan

xlihttp://investing.businessweek.com/research/stocks/people/person.asp?personId=224657972&ticker=TPAC&previo

usCapId=39791544&previousTitle=TRANS-PACIFIC%20AEROSPACE%20CO%20I

xliihttp://investing.businessweek.com/research/stocks/people/person.asp?personId=224657979&ticker=TPAC&previo

usCapId=39791544&previousTitle=TRANS-PACIFIC%20AEROSPACE%20CO%20I

![India Poised[1]](https://img.pdfslide.net/doc/110x75/54c0db9c4a7959ff248b45d2/india-poised1.jpg)