Embed Size (px)

Citation preview

Pass It On! Protecting and Passing on Tax-Deferred Assets

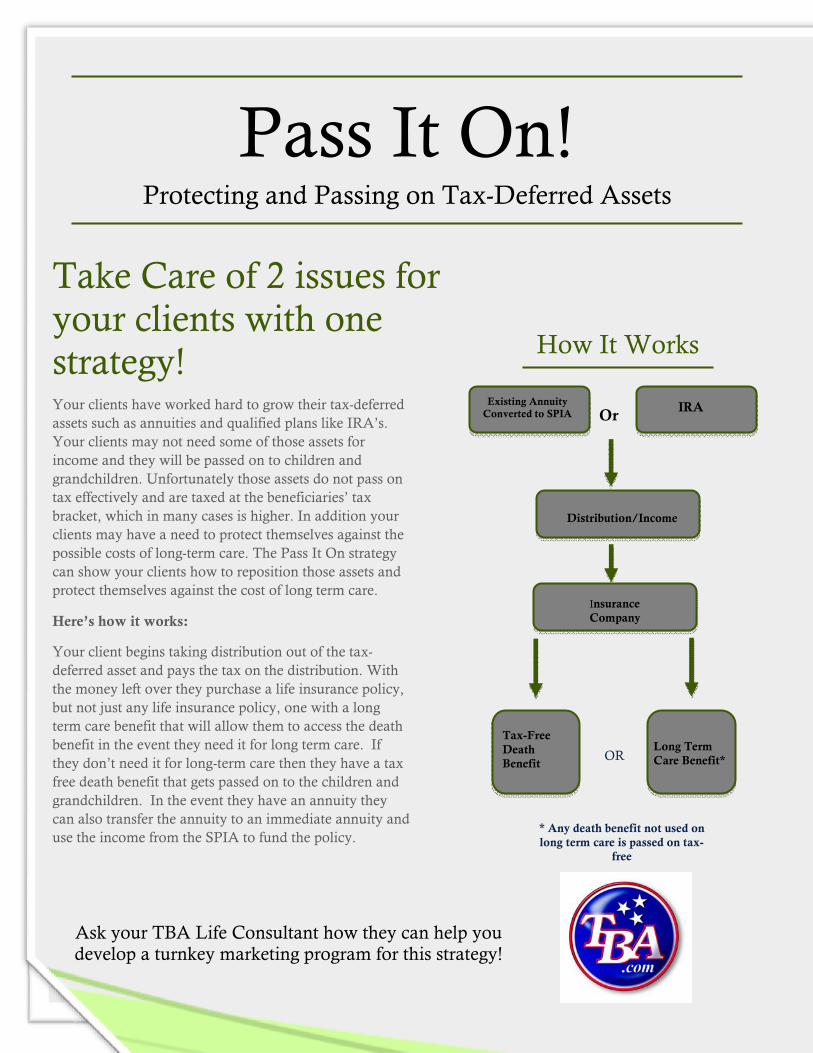

How It Works

Ask your TBA Life Consultant how they can help you develop a turnkey marketing program for this strategy!

Take Care of 2 issues for your clients with one strategy! Your clients have worked hard to grow their tax-deferred assets such as annuities and qualified plans like IRA’s. Your clients may not need some of those assets for income and they will be passed on to children and grandchildren. Unfortunately those assets do not pass on tax effectively and are taxed at the beneficiaries’ tax bracket, which in many cases is higher. In addition your clients may have a need to protect themselves against the possible costs of long-term care. The Pass It On strategy can show your clients how to reposition those assets and protect themselves against the cost of long term care.

Here’s how it works:

Your client begins taking distribution out of the tax-deferred asset and pays the tax on the distribution. With the money left over they purchase a life insurance policy, but not just any life insurance policy, one with a long term care benefit that will allow them to access the death benefit in the event they need it for long term care. If they don’t need it for long-term care then they have a tax free death benefit that gets passed on to the children and grandchildren. In the event they have an annuity they can also transfer the annuity to an immediate annuity and use the income from the SPIA to fund the policy.

Distribution/Income

Insurance Company

Tax-Free Death Benefit

Long Term Care Benefit* OR

* Any death benefit not used on long term care is passed on tax-

free

Or Existing Annuity

Converted to SPIA IRA

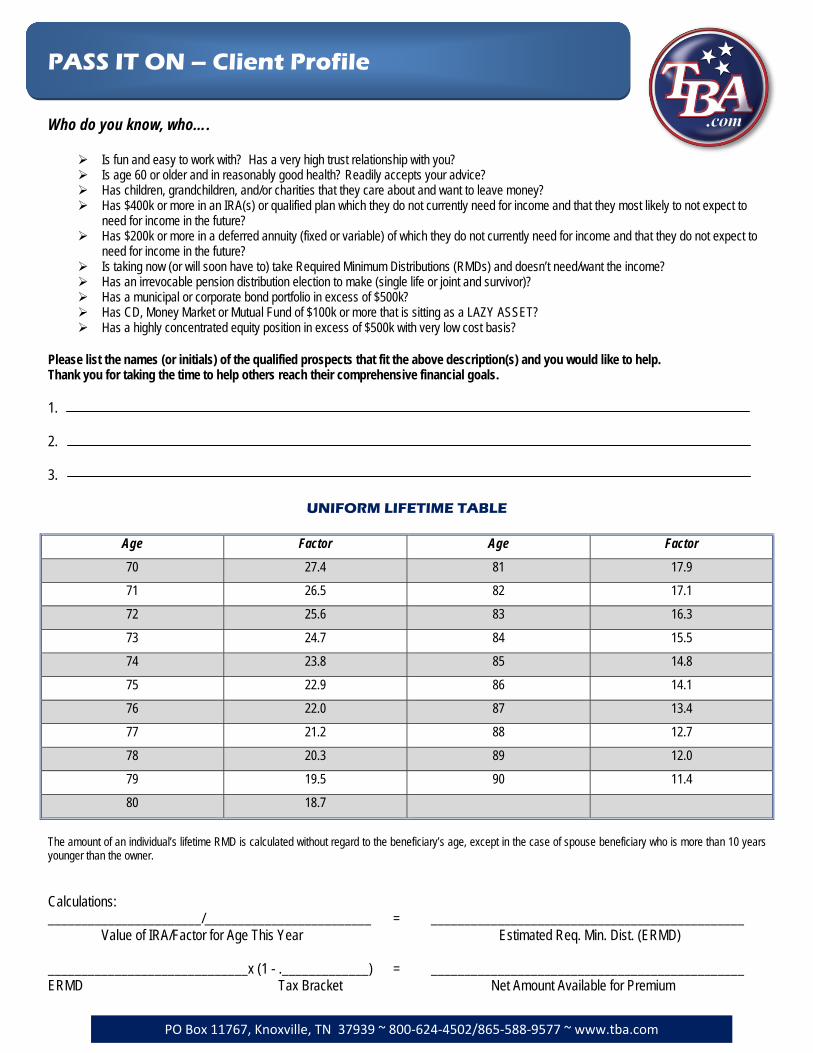

PASS IT ON – Client Profile Who do you know, who….

Is fun and easy to work with? Has a very high trust relationship with you? Is age 60 or older and in reasonably good health? Readily accepts your advice? Has children, grandchildren, and/or charities that they care about and want to leave money? Has $400k or more in an IRA(s) or qualified plan which they do not currently need for income and that they most likely to not expect to

need for income in the future? Has $200k or more in a deferred annuity (fixed or variable) of which they do not currently need for income and that they do not expect to

need for income in the future? Is taking now (or will soon have to) take Required Minimum Distributions (RMDs) and doesn’t need/want the income? Has an irrevocable pension distribution election to make (single life or joint and survivor)? Has a municipal or corporate bond portfolio in excess of $500k? Has CD, Money Market or Mutual Fund of $100k or more that is sitting as a LAZY ASSET? Has a highly concentrated equity position in excess of $500k with very low cost basis?

Please list the names (or initials) of the qualified prospects that fit the above description(s) and you would like to help. Thank you for taking the time to help others reach their comprehensive financial goals. 1. 2. 3.

UNIFORM LIFETIME TABLE

Age Factor Age Factor 70 27.4 81 17.9

71 26.5 82 17.1

72 25.6 83 16.3

73 24.7 84 15.5

74 23.8 85 14.8

75 22.9 86 14.1

76 22.0 87 13.4

77 21.2 88 12.7

78 20.3 89 12.0

79 19.5 90 11.4

80 18.7

The amount of an individual’s lifetime RMD is calculated without regard to the beneficiary’s age, except in the case of spouse beneficiary who is more than 10 years younger than the owner. Calculations: _______________________/_________________________ = _______________________________________________ Value of IRA/Factor for Age This Year Estimated Req. Min. Dist. (ERMD) ______________________________x (1 - ._____________) = _______________________________________________ ERMD Tax Bracket Net Amount Available for Premium

PO Box 11767, Knoxville, TN 37939 ~ 800‐624‐4502/865‐588‐9577 ~ www.tba.com

CLIENT PREAPPROACH LETTER

Client Name

Address

City, State Zip

Dear Client,

You have worked hard to accumulate assets and have taken advantage of tax deferral with some of those assets such as retirement plans and annuities. In some cases you may not need to use the income of those assets for your retirement and you will simply pass them on to your children and grandchildren. Unfortunately if it is your intention to do that, there may be a surprise tax bill waiting for your children and grandchildren. Tax‐deferred assets pass onto your beneficiaries at their tax bracket, which in many cases could be higher than yours. In some cases as much as 50% of those assets will get eaten up by taxes. This is certainly not what you had envisioned in passing these assets on.

There is however a better option, by repositioning these assets you can pass these tax deferred assets on in a much more efficient manner and you may also be able to protect yourself from the costs of long term care. This strategy is examined in the accompanying brochure. This is a great way to pass on most of your tax‐deferred assets income tax free and allow you to cover the costs of long term care in the event that you need it.

If you would like to discuss this strategy and how we might work together to achieve it please give me a call and set up a time for us to sit down together.

Sincerely,

Producer

Protection What about Long Term

Care protection? You can also use this strategy to

protect yourself against the costs of long term care. By using the

distributions to pay for a long term care insurance policy you protect

yourself against long term care costs. You can also purchase a life insurance

policy that will give you access to your death benefit in the event you

need long term care. Here you get the best of both worlds; protection and

tax efficient transfer of your tax-deferred assets.

We Can Help You Examine the Options

We can help you determine what might be best for you and also show you the impact taxes may have on

your tax-deferred assets. By looking at the various options available we can help you pass on your assets in

the most efficient way while also protecting yourself against the costs

of long term care. Call us today to set up a time to review your options!

Pass It On! Protecting and Transferring

Tax-Deferred Assets

Your Logo Here

John Agent 123 Any Street Anytown, MA

37919

Protecting and Passing on Tax-Deferred Assets

What Are Tax-Deferred Assets? They are assets that you have accumulated without paying taxes on their growth. These would include annuities, and any qualified plans such as IRA’s and 401K’s.

Do you need the income? In the event that you don’t need the income from your tax-deferred assets and want to pass them onto your children or grandchildren one of the best ways to do that is to begin taking income or distributions from those tax-deferred assets and repositioning those assets into a pool of money that would pass on to your heirs tax free. This pool of money is life insurance; life insurance is a great vehicle to use to pass on

assets to your heirs because it passes on income tax free.

How Does it Work? The best way to use this strategy is to take income or distributions from your tax-deferred assets and pay the tax on the distribution or income; then use the remainder to pay a premium on the life insurance policy. When you die the death benefit from the life insurance policy will pass on to your heirs income tax free and whatever is left from your tax-deferred assets will pass on to them and be taxed. You can maximize what gets passed on to your heirs this way without having any out of pocket cost to you. You simply reposition your assets.

Pass it On! You’ve worked hard to accumulate your assets, and your tax-deferred assets have allowed you to grow those assets without the impact of taxes. Unfortunately all good things must come to an end. When you start to take income off of those assets you must pay taxes on them. And in the event that you die and pass those assets on to your beneficiaries those assets will be taxed at your beneficiaries tax bracket, which in many cases is higher.

IRA MaximizationIRA MaximizationThe following is a comparison of a current traditional IRA Maximization. This can help reduce estate taxes and increase the accountvalue that is passed on to the heirs.

Withdrawals can be taken from the traditional IRA to pay the premiums on a life insurance policy that will reposition assets and allowbeneficiaries to receive the death benefit income tax free and potentially avoid estate taxes upon a death.

Current IRA Value$1,000,000

Continue IRA Rollover IRA to SPIAMinimum Distributions Purchase $1,866,878 Life Insurance

Projected IRA Value ‐ $1,306,123Reinvested Distributions ‐ $ 883,291

Projected Insurance ‐ $1,866,878

Estate Tax ‐ $1,204,178Income Tax ‐ $ 164,572

Estate Tax ‐ $0Income Tax ‐ $0

Net Value to Heirs ‐ $820,665 Net Value to Heirs ‐ $1,866,878

Advantage for Heirs

The IRA illustrated does not reflect applicable sales and management fees or administrative costs charged by the current issuer. The charges, if included, would affect the figures illustrated. The assumed rate of growth ofthe IRA is 5%.

The estate tax calculation shown in this illustration are based upon the estimated size of your estate and the estate tax rates found in Section 2001 of the Internal Revenue Code. All rates illustrated are subject to change.Calculations assume use of the Unified Credit and assume no marital deduction is available. Estate tax calculations reflect the Economic Growth and Tax Relief Reconciliation Act of 2001 resulting in reduced estate taxes in2002 th h 2009 d li i ti f th t t t i 2010 I 2011 d b d th l l ti th t t t l i l i t th A t U l l i l ti i d th A t ill b l d i 2011

g$1,046,213

2002 through 2009 and elimination of the estate tax in 2010. In year 2011 and beyond, the calculations assume the estate tax law in place prior to the Act. Unless new legislation is passed, the Act will be repealed in 2011and estate tax in effect prior to the Act will be reinstated.

Either the total IRA payment, the after tax payment or a specified amount can be used as premium toward the life insurance policy.

Calculations assume all premiums qualify for the gift tax annual exclusion. To the extent that this is not true, estate taxes could be understated and gift tax consequences would not be illustrated.

The net surrender value and net death benefit amounts illustrated are based on current policy interest rate and cost assumptions. The values illustrated are not guaranteed. They assume that the illustrated non-guaranteedelements of the policy will continue unchanged for all years shown. This is not likely to occur, and actual results may be more or less favorable than those shown.