Embed Size (px)

Citation preview

Consultation Paper 16

Public Consultation on

IPO grading and Independent Equity Research 25 June 2012

SECURITIES AND EXCHANGE COMMISSION OF SRI LANKA

2 Securities and Exchange Commission of Sri Lanka | Public Consultation on IPO grading and Independent Equity Research

25 June 2012

1.0 FOREWORD

This paper discusses the concept of IPO grading and Independent Equity Research Schemes adopted in other stock markets, and seeks public comment on implementing IPO Grading with respect to new equity listings on

the Colombo Stock Exchange (CSE) and the need for Independent Equity Research on listed companies. The Securities and Exchange Commission of Sri Lanka (SEC) would like to invite the public and other market

participants to submit written comments on the questions posed in this consultation paper (refer Section 4.0 for

further details), to reach the SEC on or before 31st July 2012, under the title “Public Consultation on IPO grading and Independent Equity Research”. Comments received may be publicly available and will not be

treated as confidential unless a special request is made in that respect.

2.0 IPO GRADING 2.1 Current Requirements for listing on the Colombo Stock Exchange A company seeking to list equity and corporate debt securities on the CSE has the following options :

To list Corporate Debt Securities – Main Board or Second Board (the Second Board has less stringent

eligibility criteria in comparison to the Main Board)

To List Equity – Main Board or Diri Savi Board (the Diri Savi Board has less stringent eligibility criteria in

comparison to the Main Board)

For a Company to be eligible to list corporate debt securities on the Second Board of the Colombo Stock Exchange (CSE), the applicant entity must obtain a rating for the corporate debt security to be listed, from a

Rating Agency registered with the Securities and Exchange Commission of Sri Lanka (The SEC). Also the applicant entity should have been in business for a minimum period of three years, immediately preceding the

date of application to the CSE.

In order to be eligible to list on the Main Board of the CSE, the corporate debt security to be listed should

either have an investment grade rating obtained from a Rating Agency registered with the SEC, or alternatively, the Issuer must provide a guarantee for the repayment of capital and interest, from either a Bank licensed by the

Central Bank of Sri Lanka (which has an A– rating or a rating equivalent or better, obtained from a Rating

Agency registered with the SEC), or from an international multilateral, bilateral or other agency acceptable to the CSE. Additionally, the applicant entity is required to appoint a Trustee which meets the criteria specified under

the listing rules, for the benefit of the holders of corporate debt securities which are to be listed.

Currently, there is no equivalent rating requirement to be eligible to list equity on the CSE. The eligibility requirements for an applicant entity seeking to list equity on the Diri Savi Board of the CSE are,

a. Stated Capital of not less than Rs.100mn at the time of listing, b. Positive Net Assets as per the consolidated audited financial statements for the financial year immediately

preceding the date of application, c. A minimum ‘Public Holding’ of 10% and a minimum of 100 ‘public’ shareholders holding not less than 100

shares each, and,

d. An operating history of at least one year immediately preceding the date of application to the CSE.

In this context ‘Net Assets’ is defined as total assets after deducting total liabilities, preference share capital and advance against share capital. ‘Public Holding’ is defined under the Listing Rules of the CSE.

To be eligible to list equity on the Main Board of the CSE, the applicant entity should have,

(a) Stated Capital of not less than Rs.500mn at the time of listing, (b) Net profit after tax for three consecutive years immediately preceding the date of application,

(c) Positive Net Assets as per the consolidated audited financial statements for the last two financial years immediately preceding the date of application, and,

(d) A minimum ‘Public Holding’ of 25% and a minimum of 1,000 ‘public’ shareholders holding not less than 100

shares each.

3 Securities and Exchange Commission of Sri Lanka | Public Consultation on IPO grading and Independent Equity Research

25 June 2012

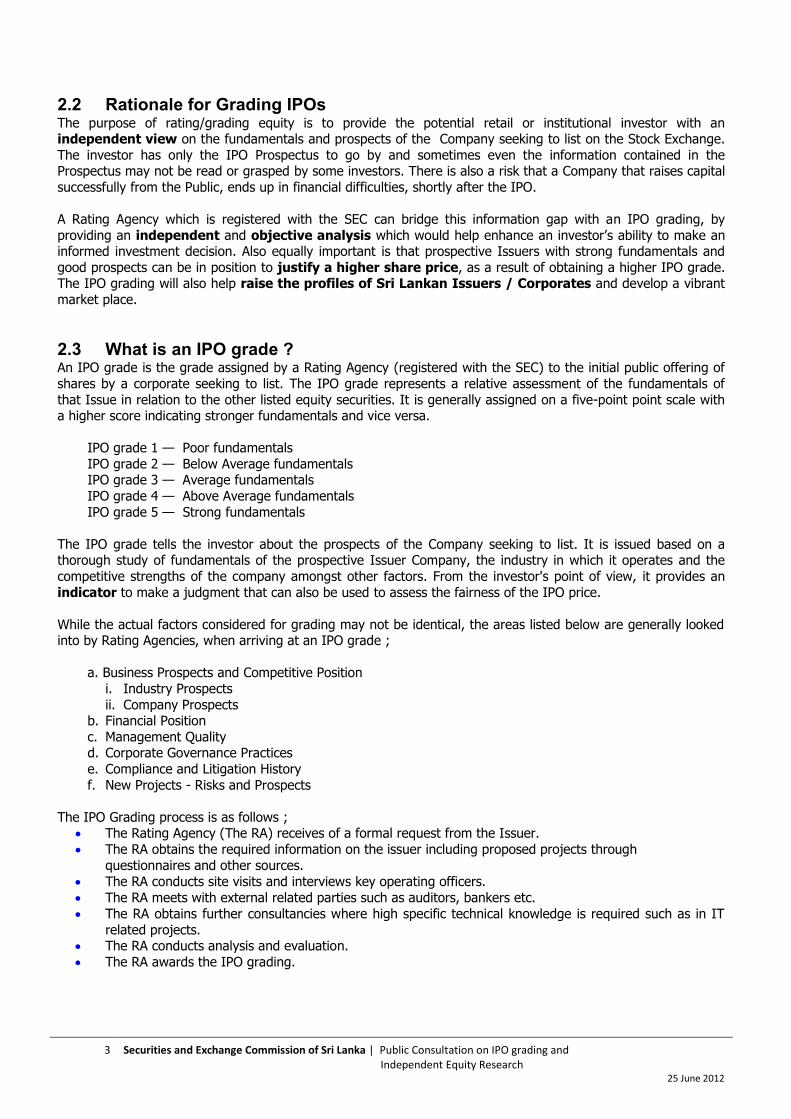

2.2 Rationale for Grading IPOs The purpose of rating/grading equity is to provide the potential retail or institutional investor with an independent view on the fundamentals and prospects of the Company seeking to list on the Stock Exchange.

The investor has only the IPO Prospectus to go by and sometimes even the information contained in the Prospectus may not be read or grasped by some investors. There is also a risk that a Company that raises capital

successfully from the Public, ends up in financial difficulties, shortly after the IPO.

A Rating Agency which is registered with the SEC can bridge this information gap with an IPO grading, by

providing an independent and objective analysis which would help enhance an investor’s ability to make an informed investment decision. Also equally important is that prospective Issuers with strong fundamentals and

good prospects can be in position to justify a higher share price, as a result of obtaining a higher IPO grade. The IPO grading will also help raise the profiles of Sri Lankan Issuers / Corporates and develop a vibrant

market place.

2.3 What is an IPO grade ? An IPO grade is the grade assigned by a Rating Agency (registered with the SEC) to the initial public offering of

shares by a corporate seeking to list. The IPO grade represents a relative assessment of the fundamentals of

that Issue in relation to the other listed equity securities. It is generally assigned on a five-point point scale with a higher score indicating stronger fundamentals and vice versa.

IPO grade 1 — Poor fundamentals

IPO grade 2 — Below Average fundamentals IPO grade 3 — Average fundamentals

IPO grade 4 — Above Average fundamentals

IPO grade 5 — Strong fundamentals

The IPO grade tells the investor about the prospects of the Company seeking to list. It is issued based on a thorough study of fundamentals of the prospective Issuer Company, the industry in which it operates and the

competitive strengths of the company amongst other factors. From the investor's point of view, it provides an

indicator to make a judgment that can also be used to assess the fairness of the IPO price.

While the actual factors considered for grading may not be identical, the areas listed below are generally looked into by Rating Agencies, when arriving at an IPO grade ;

a. Business Prospects and Competitive Position

i. Industry Prospects

ii. Company Prospects b. Financial Position

c. Management Quality d. Corporate Governance Practices

e. Compliance and Litigation History

f. New Projects - Risks and Prospects

The IPO Grading process is as follows ; The Rating Agency (The RA) receives of a formal request from the Issuer.

The RA obtains the required information on the issuer including proposed projects through

questionnaires and other sources.

The RA conducts site visits and interviews key operating officers.

The RA meets with external related parties such as auditors, bankers etc.

The RA obtains further consultancies where high specific technical knowledge is required such as in IT

related projects. The RA conducts analysis and evaluation.

The RA awards the IPO grading.

4 Securities and Exchange Commission of Sri Lanka | Public Consultation on IPO grading and Independent Equity Research

25 June 2012

However, it is important to note that IPO grading does not consider the IPO issue price. The IPO

grade is an independent and credible input to aid the investor in the investment process and the investor needs to make his/her own independent decision regarding investing in the IPO. The test of the IPO grading is not in

the market price, but in the overall financial performance of the Company, as prices can vary depending on extraneous conditions. However the grading could be a useful indicator to justify whether the IPO price is fair or

overpriced.

In order to implement this mechanism, the pricing for IPO Grading will be relatively minimal and would be based

on the size (value in Rs.) of the Issue.

India IPO grading was initially implemented by the Securities and Exchange Board of India (SEBI) on a voluntary basis

and then made mandatory from 1st May 2007. Currently, any Issuer who decides to offer shares or any other

security which may be converted into or exchanged with shares at a later date through an IPO, is required to obtain a grade for the IPO from at least one Credit Rating Agency registered with SEBI (CRA). The IPO grading is

obtained before filing the Draft Prospectus with SEBI. IPO Prospectus must contain the grades given to the IPO by all CRAs approached by the Company for grading the IPO. The IPO grade represents a relative assessment of

the fundamentals of that Issue in relation to the other listed equity securities in India. The Issuer is required to

bear the expenses incurred for grading an IPO. The fee applicable is based on the value of the IPO.

3.0 INDEPENDENT EQUITY RESEARCH SCHEMES

Stock Exchanges in the Asian region have initiated Independent Equity Research Schemes for listed companies

with the aim of providing unbiased research reports, with in-depth analysis of the fundamentals and valuation of listed companies, to encourage informed investment decision making by investors. The Independent Research

Scheme is funded mainly through the Stock Exchange or the market development fund relating to the Stock

Exchange. Details on Independent Equity Research Schemes launched in India, Singapore, Malaysia, Indonesia, Australia, the United States and Europe are provided on pages 6 to 10 of this document.

Independent analyst advice is of crucial importance as they provide investors with an unbiased, analytical view

by a third party.

IOSCO’s Executive Committee entrusted the IOSCO Implementation Task Force (ITF) to revise the IOSCO Objectives and Principles of Securities Regulation (Principles) to take into account the emerging consensus

regarding Regulatory Concerns that the recent global financial crisis in October 2008 raises. At the 35th Annual

Conference of IOSCO on 10th June 2010, the Presidents’ Committee approved the revised IOSCO Principles and added eight new Principles to the current 30. Two Principles addressing Systemic Risk in Markets were added

and importantly a specific Principle addressing Entities that offer investors Analytical or Evaluation Services was included.

Relevant Principles include ; Principle 8: The Regulator should seek to ensure that conflicts of interest and misalignment of incentives

are avoided, eliminated, disclosed or otherwise managed;

Principle 23: Entities that offer investors Analytical or Evaluative Services should be subject to Oversight and Regulation appropriate to the impact their activities have on the market or the degree to

which the Regulatory System relies on them.

Additionally, IOSCO Statement of Principles for addressing Sell-Side Securities Analyst Conflicts of Interest

(dated 25th September 2003) has prescribed the following Principles that identify key areas that the Overall Oversight System should address ;

Principle 1 : Analyst Trading and Financial Interests Mechanisms should exist so that Analysts’ trading activities or financial interests do not

prejudice their Research and Recommendations.

5 Securities and Exchange Commission of Sri Lanka | Public Consultation on IPO grading and Independent Equity Research

25 June 2012

Principle 2 : Firm Financial Interests and Business Relationships

Mechanisms should exist so that Analysts’ Research and Recommendations are not prejudiced by the trading activities, financial interests or business relationships of the Firms that employ

them.

Principle 3 : Analysts’ Reporting Lines and Compensation

Reporting Lines for Analysts and their Compensation Arrangements should be structured to eliminate or severely limit actual and potential conflicts of interest.

Principle 4 : Firms’ Compliance Systems and Senior Management Responsibility

Firms that employ Analysts should establish Written Internal Procedures or Controls to identify

and eliminate, manage or disclose actual and potential conflicts of interest on the part of Analysts.

Principle 5 : Outside Influence

The undue influence of Issuers, Institutional Investors and Other Outside Parties upon Analysts

should be eliminated or managed.

Principle 6 : Clarity, Specificity and Prominence of Disclosure

Disclosures of actual and potential conflicts of interest should be Complete, Timely, Clear,

Concise, Specific and Prominent.

Principle 7 : Integrity and Ethical Behavior Analysts should be held to high integrity standards.

Principle 8 : Investor Education Investor education should play an important role in managing Analyst conflicts of interest.

6 Securities and Exchange Commission of Sri Lanka | Public Consultation on IPO grading and Independent Equity Research 25 June 2012

Independent Equity Research Schemes launched in Other Stock Markets ASIA

INDIA Name of

Scheme

BSE Sponsored Independent Equity Research Scheme

(BSE IER)

NSE Sponsored Independent Equity Research (IER) Scheme

Under BSE IER, small and mid-cap companies are covered by Research / Rating firms.

Research reports contain analysis and views on company

fundamentals including an industry overview and the company’s business, profitability and competitive landscape

and do not include any investment ratings or forward looking statements.

Research reports are disseminated in a standardized format

and are available free of charge to all investors on the BSE website.

The scheme is funded by the BSE Investors' Protection Fund.

BSE also provides free access to IPO research reports on the

BSE website.

National Stock Exchange of India (NSE) has commissioned CRISIL (a Standard & Poor’s company), to provide in depth analysis on the

fundamentals and valuation of selected listed companies.

A base report is provided by CRISIL for all listed companies, which is updated on a quarterly basis.

This scheme is funded by the NSE Investor Protection Fund Trust.

An IER report includes the following : CRISIL’s Fundamental grade

and Valuation grade on the company’s shares, company background, industry overview, key strengths, peer analysis,

financial analysis, key stock indicators, stock performance and benchmarking with NIFTY, detailed financials for last 3 years

including ratio analysis, and shareholding pattern.

The IER reports are available free of charge to all investors on the

NSE website and at www.ier.co.in.

7 Securities and Exchange Commission of Sri Lanka | Public Consultation on IPO grading and Independent Equity Research 25 June 2012

ASIA

SINGAPORE MALAYSIA Name of

Scheme

SGX Equity Research Insights (SERI)

Capital Market Development Fund-Bursa Research Scheme

(CBRS)

SERI is administered by SGX and each participating listed company is covered regularly by the SGX appointed research

firm for a period of 2 years. The research reports are available free of charge to all investors

on the SGX website.

Participating listed companies pay an annual fee to SGX based on its market capitalisation and the research firm is

compensated by SGX using these funds. SGX and The Monetary Authority of Singapore jointly subsidise

companies with a market cap of below S$301 mn. SERI consists of two modules ;

The Structured Module – This module provides research reports by Standard & Poor's

LLC on listed companies with little or no research coverage.

Research reports have standardised format, facilitating

comparison. Contain analysis and views on company fundamentals

including industry prospects, its business and management,

performance, earnings outlook and competitive landscape.

Reports do not feature any investment ratings.

The Sector Module –

This module provides fully-rated research reports by DnB

Nor Markets (investment banking arm of Norway's largest financial services group) to meet the needs of investors in

sectors where specialized industry knowledge is critical in the analysis of the companies.

SGX identified Energy, Offshore and Marine as the sectors to

initiate this module.

CBRS is a joint effort, launched in June 2005, between Bursa Malaysia and the Capital Market Development Fund (CMDF) where

the Exchange serves as the Administrator. CBRS aims at increasing the profile of listed companies with quality

coverage provided by Licensed professional Analysts and

increasing investor confidence through a well-informed investment community (Research Providers in Malaysia cover only the top 100

stocks listed and listed companies which receive little or no research coverage are likely to be negatively impacted as they

would not appear on investors’ radar). All companies listed on Bursa Malaysia are eligible to participate.

Research companies licensed as Investment Advisors under the

Capital Market Securities Act 2007 are eligible to participate, subject to the approval of the Exchange and currently there are 8

research companies that compile research reports. Independence and integrity of CBRS is achieved via the allocation

of participating listed companies to Research Houses being done

by the Exchange, after considering sector expertise and conflicts of interest (the Exchange does not receive revenue from CMDF for its

role in providing administrative support and facilitating distribution of the research reports generated).

The research reports are available free of charge on the Exchange website (Bursa Malaysia Research Repository).

The CMDF subsidises 50% of the cost of coverage. The cost of

research coverage is defrayed through economies of scale. Listed companies pay a total fee of RM16,800 (including service

tax) for which they receive research coverage for a period of two years.

The expected contents of reports have been specified by Bursa

Malaysia and reports have a valuation and recommendation.

8 Securities and Exchange Commission of Sri Lanka | Public Consultation on IPO grading and Independent Equity Research 25 June 2012

MALAYSIA (continued)

Capital Market Development Fund-Bursa Research Scheme (continued)

The frequency of the research coverage should take into account developments and events that would impact the participating

company’s financial position, liquidity and prospects of the company including, amongst others, material acquisitions/divestments of

assets, change in business direction, change in management team, takeover of the company, etc. At minimum, the research company is required to produce the following reports for each of the participating listed company allocated

to them during the two-year period ; One Initiation of Coverage Report within three months from commencement date

At least eight Coverage of Results Reports, corresponding to the listed company’s quarterly results and full-year results

announcements

At least two Update Reports per year issued at the discretion of the research company

Non-CBRS Research Reports In addition, the Exchange Research Repository hosts (free) research reports generated by research companies as part of their normal

course of business. The purpose of including these research reports is to increase the quantity of listed companies covered and to offer diversity in

research perspective to the investment community. The non-CBRS research reports are reproduced 'as is' with permission from the Research Houses and is not reviewed or monitored by

Bursa Malaysia. The research companies who contribute their research reports to this platform are Licensed as Investment Advisors

under the Capital Market Securities Act 2007.

9 Securities and Exchange Commission of Sri Lanka | Public Consultation on IPO grading and Independent Equity Research 25 June 2012

ASIA

INDONESIA AUSTRALIA Name of Scheme

Indonesia Stock Exchange Initiative ASX

Reference Share Price Target reports are prepared by Credit

Rating Agency, PT Pefindo’s Equity Research Division. The

high and low share price targets are based on fundamentals. These reports are prepared with the objective of enhancing

shares price transparency of listed companies on the Indonesia Stock Exchange (IDX).

Reports are issued twice per year and are available free of charge to all investors on the IDX website and at

www.pefindo.com. The report includes a disclosure that the report is free from

influence, pressure or force either from IDX or the listed company reviewed

The Exchange also hosts updated company reports on the listed companies which include a detailed performance

summary, financial ratios and historical trade data.

In financial year 2013, the Exchange will provide $1mn to fund a

12-month trial for an Equity Research Scheme.

The Scheme will improve the listed company’s ability to communicate to and raise capital from a broader set of investors

and would benefit small and mid-cap companies, many of whom have not been covered by research.

It is designed to fund the production of high-quality, independent research for ASX-listed entities with a market capitalisation below

$1bn (around 1,800 or 92% of all listed companies).

The proposed Equity Research Scheme will provide the following; For companies with a market capitalisation below $50mn

(around 1,200 or 62% of listed companies) – a fact note

with information drawn from publicly available sources by an exclusive Research Provider;

For companies with a market capitalisation between $50mn

and $200mn who do not already have sufficient retail

research coverage – a standard retail research report with analysis and commentary from an established Licensed Retail

Research Provider; For companies with a market capitalisation between

$200mn and $1bn who don’t already have sufficient

institutional research coverage – a standard institutional report that includes a formal recommendation by an ASX

market participant with an established Institutional Research

function. ASX will assess how the Equity Research Scheme could be

expanded, if this trial is successful.

10 Securities and Exchange Commission of Sri Lanka | Public Consultation on IPO grading and Independent Equity Research 25 June 2012

EUROPE / UNITED STATES

Exchange

NASDAQ OMX NYSE Euronext

NASDAQ OMX initially began by offering Morningstar basic profile reports, financed by NASDAQ OMX, for both NASDAQ- and Nordic-listed companies (more than 3,600),

which filled a research void that has existed for some time, particularly among small- to mid-cap companies.

(Morningstar is one of the largest Independent sources for Stock Analysis in the world)

The basic profile report included a lengthy company profile, comprehensive data about

the company and its industry, and industry context written by a Morningstar Analyst. It did not include Morningstar's more detailed analyst research report, a

Morningstar Rating, or a buy/sell/hold recommendation. From January 2010 onwards, qualified listed companies are able to contract with

NASDAQ OMX for Morningstar's institutional analyst research report ;

Morningstar's institutional equity analyst reports provide thorough qualitative and

quantitative analysis, including an investment thesis and discussions about valuation, management, risks, and competitive advantage. It also includes the Morningstar

Rating(TM) for Stocks, a Fair Value Estimate, Consider Buying and Consider Selling prices, Uncertainty Rating, Economic Moat(TM) Rating, and full pro-forma analyst

forecasts.

NASDAQ serves as the intermediary and listed companies pay NASDAQ a fee for the

ongoing coverage, which is part of the overall package of fees they pay to NASDAQ for their listing services.

NASDAQ in turn pays Morningstar a fee for analyst coverage of each company

covered. The service includes a comprehensive initiation report and a minimum of three

quarterly updates.

The reports are distributed through the websites of the covered listed companies and

all of Morningstar's research distribution channels. (Morningstar’s research and ratings are distributed to 8 mn individual investors, more than 250,000 plus financial advisors, and 4,500 institutional investors worldwide)

Listed companies may not review the content of Morningstar's analyst research or

ratings prior to publication. The reports includes a disclosure that the listed company

has commissioned the Exchange for the research.

NYSE Euronext and Virtua Research have initiated a project to facilitate more

independent research for a group of NYSE- and NYSE Amex-listed companies,

through interactive financial modeling

tools that are accessible to all investors. (Virtua Research is a financial services technology company which develops and builds leading-edge research modeling tools and products)

Relying on public information such as 8-K,

10-K and 10-Q filings as well as transcripts

of quarterly earnings calls, the 200 research analysts at Virtua Research

provide a financial model with base-line data for a selected company’s revenues,

earnings, earnings per share and a range

of analytical tools enabling peer comparisons.

Virtua Research tools do not offer “Buy”, “Sell” or “Hold” recommendations, but

leave it up to the investor’s own data

inputs to project numerical outcomes for a company’s stock price.

Models can be accessed for free from the websites of NYSE Euronext

(www.nyse.com/virtua) as well as

Virtua Research.

11 Securities and Exchange Commission of Sri Lanka | Public Consultation on IPO grading and Independent Equity Research

25 June 2012

4.0 HOW TO SUBMIT COMMENTS

The Securities and Exchange Commission of Sri Lanka (The SEC) would like to invite the public and other

market participants to submit written comments on the following questions posed :

Please submit your written comments on the above-mentioned questions, to reach the SEC on or before

31st July 2012, under the title “Public Consultation on IPO grading and Independent Equity Research”.

Written comments may be sent by any one of the following methods :

By Registered Post :

Director Capital Market Development Securities and Exchange Commission of Sri Lanka

Level 28, East Tower, World Trade Centre Echelon Square, Colombo 01

Sri Lanka

Your comments should be submitted in an envelope marked “Public Consultation on

IPO grading and Independent Equity Research” on the top left-hand corner of the envelope.

IPO Grading (rating quality of the Issue and not the price of the Offer) (A) The SEC is contemplating implementing IPO Grading for new listings. Do you think IPO

grading is necessary?

(B) Will your decision to subscribe/not subscribe to an IPO be benefitted by an independent “grading system”?

(C) If yes, who should be responsible for doing the grading (i.e. credit rating houses, independent research houses, etc.)?

(D) Should the grading companies be registered and monitored by the SEC?

(E) Are there any other risk concerns that need to be highlighted by grading companies apart from the areas generally looked into (refer Section 2.3)?

Independent Equity Research (analysis of both quality and price; applicable once listed)

(F) Do you think research reports of companies already listed, produced by independent research report providers, will be useful for better investment decision making?

(G) What should be the criteria for companies to be covered by independent research report

providers? (H) What benefits would you derive through such independent research reports?

(I) How would you define an independent research report provider?

(J) Do you think entities that offer investors analytical or evaluative services should be subject

to oversight and regulation by the SEC?

(K) Please indicate your current role at the Colombo Stock Exchange [e.g. retail investor, local institutional investor, foreign institutional investor, custodian bank, listed company, stockbroker, stockdealer, unit trust, IPO manager, research report provider, etc.]

12 Securities and Exchange Commission of Sri Lanka | Public Consultation on IPO grading and Independent Equity Research

25 June 2012

By Fax :

(011) 2331016

E-mail : [email protected] ; [email protected]

If you wish to provide comments in the capacity of a representative of an organisation, you should specify the name of the organisation whose views you represent. Participants submitting comments should include their

personal/company particulars including their name, correspondence address, contact phone number and email address, on the cover page of their submissions.

The comments received would be subject to consideration by the Securities and Exchange Commission of

Sri Lanka. Comments received may be publicly available and will not be treated as confidential, unless a special request is made in that respect.