Embed Size (px)

Citation preview

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

1. Bali2. Bangka-Belitung3. Banten4. Bengkulu5. Daerah Istimewa Yogyakarta6. Daerah Khusus Ibukota Jakarta7. Gorontalo8. Irian Jaya Barat9. Jambi10. Jawa Barat11. Jawa Tengah

12. Jawa Timur13. Kalimantan Barat14. Kalimantan Selatan15. Kalimantan Tengah16. Kalimantan Timur17. Kepulauan Riau18. Lampung19. Maluku20. Maluku Utara21. Nangroe Aceh Darussalam22. Nusa Tenggara Barat

23. Nusa Tenggara Timur24. Papua25. Riau26. Sulawesi Selatan27. Sulawesi Tengah28. Sulawesi Tenggara29. Sulawesi Utara30. Sumatera Barat31. Sumatera Selatan32. Sumatera Utara

Averting an Infrastructure Crisis:A Framework for Policy and Action

THE WORLD BANK OFFICE JAKARTA.

Jakarta Stock Exchange Building Tower II/12th. Fl.Jl. Jend. Sudirman Kav. 52-53Jakarta 12910.Tel: (6221) 5299-3000.Fax: (6221) 5299-3111.Website: www.worldbank.or.id

THE WORLD BANK.

1818 H Street N.W.Washington, D.C. 20433, U.S.A.Tel: (202) 458-1876.Fax: (202) 522-1557/1560.Email: [email protected]: www.worldbank.org

A copublication of the World Bank East-Asia Infrastructure Departmentand Indonesia Country Program

Printed in June 2004

Cover and book design: Arif Wicaksono - Grha Info Kreasi

All photographs used in this publications are from Jez O'Hare Photography,except photos on page 12 and 41 (World Bank collection) and somephotos on the cover (see below)

Cover photographs: Power Line; © Jez O'Hare. Bus Passenger; © Jez O'Hare.The photographs of children, old woman, and telephone-man are fromWorld Bank collection.

This volume is a product of the staff of the World Bank. The findings,interpretations, and conclucions expressed herein do not necessarily reflectthe views of the Board of Executive Directors of the World Bank or thegovernments they represent.

The World Bank does not guarantee the accuracy of the data included inthis work. The boundaries, colors, denominations, and other informationshown on any map in this work do not imply any judgment on the part ofthe World Bank concerning the legal status of any territory or theendorsement or acceptance of such boundaries.

v

ForewordCountries around the world are again recognizing the crucial role of infrastructure in promoting development. Strong infrastructureprograms spur economic growth, create jobs, and help improve the quality of life. Neglect of infrastructure, in contrast, acts as adrag on growth and job creation, and perpetuates poverty.

In today’s Indonesia, due to the economic crisis of 1998-2002 and other factors, the state of infrastructure is a hindrance rather thana help to development. Risks of power outages are discouraging investors in new factories, traffic congestion is eroding the qualityof urban life, and longer travel times are making businesses uncompetitive as they seek to get their goods to market. Forty sevenpercent of households are still not connected to the grid, and 6,000 villages lack electricity altogether. Forty five percent ofhouseholds suffer unsanitary conditions and 22 percent have no access to safe water. As a result health conditions and workerproductivity compare unfavorably with comparator countries.

The good news is that Indonesia is well positioned to reverse this situation. Recent macroeconomic successes imply that financialshortages are easing, and new legislation and policies offer the possibility of better managed infrastructure and a renewed role forprivate investment in the sector. This report Averting an Infrastructure Crisis: A Framework for Policy and Action has been preparedto support the Government’s efforts to take advantage of this opportunity. It has been developed in close collaboration withBappenas and other key agencies. It complements the ‘Infrastructure Book’, developed under BAPPENAS to provide a long terminfrastructure development scenario that encompasses all major infrastructure sectors.

The path ahead will not be easy. Policy reforms will need to be implemented firmly, and investment in infrastructure will need tobe increased by an amount equivalent to 2 percent of GDP per year. Money cannot substitute for policy and institutional reforms,or vice versa. Both are required, and both public and private sectors will need to play a larger role. The report provides optionsrather than blueprints. The main report addresses cross-cutting issues that affect all infrastructure sectors. Background reports areavailable on roads, telecommunications, electric power, water supply and sanitation.

The World Bank is privileged to work in partnership with the Government as it works for deeper and more equitable development.We stand ready to further support the efforts of the Government to implement an ambitious infrastructure reform agenda.

Finally, the report attempts to provide an integrated approach to infrastructure development that goes beyond sector-specific issues.This cross-sectoral analysis forms the first part of the report (first six chapters). It draws on a study of four specific sectors –namelytelecommunications, power, water supply and sanitation, and roads, which are presented in the second part of the report (fourbackground sector reports). Similar approaches are being undertaken for other Asian countries. In addition, a thematic infrastructurestrategy report undertaken in collaboration with JBIC and the ADB, will also cover the emerging challenges facing the whole EastAsia region. We hope that this effort will enhance our understanding of infrastructure issues in East Asia and thus help policy makersthroughout the region.

Andrew D. Steer Christian DelvoieCountry Director, Indonesia Director, Infrastructure DepartmentEast Asia and Pacific Region East Asia and Pacific Region

Averting an Infrastructure Crisis: A Framework for Policy and Actionvi

AcknowledgmentThis report was prepared by a core team led by Ani Dasgupta and consisting of Michel Kerf (co-team leader), David Hawes, andAndre Bald. The following people formed the larger team and contributed to or drafted parts of the report: Migara Jayawardena,Phil Gray, Bill Paterson, Peter Roberts, Mohammad Farhandi, Geoffrey Read, Tenzin Norbhu, Peter Smith, Phil Lam, DemetriosPapathanasiou, Ann Thomas, Janelle Plummer, Jan Drozdz, Menno Pradhan, P S Srinivas, Naseer Rana, and Jonathan Walters. Thereport was prepared under the overall guidance of Christian Delvoie, Director, East Asia and Pacific Infrastructure Department andAndrew Steer, Country Director, Indonesia.

The report benefited from consultation and advice from numerous reviewers including: Antonio Estache, Jenifer Wishart, ChristinaE. Malmberg Calvo, Vivien Foster, C. Fallert Kessides (as peer reviewers); Bert Hofman, Jit Bajpai, Keshav Varma, Juinhui Wu, JoelHellman, Rick Pollard, Yoichiro Ishihara, Albert Wright, John Besant Jones, Jonathan Halpern, Cecilia Briceno, Axel Baumler,Barbara Lee, Homi Kharas, Arvind Gupta, Jeffrey Gutman, Michel Bellier, Baher El Hifnawy, Hatim Hajj, Alberto Nogales, LuizTavares, Songsu Choi, Raja Iyer, Hiroaki Suzuki, Ming Zhang, Noureddine Berrah, Robert Taylor, Barry Trembath, Elisa Muzzini,Abhas Kumar Jha, and Mark Baird. Editorial and production support was provided by Melissa Morris.

We would like to thank the Norwegian Trust Fund for Private Sector and Infrastructure for financial support for this project, andMarianne Bergstrom for her good natured support.

This report was developed in close collaboration with Bappenas and Committee for Acceleration of InfrastructureInvestments (KKPPI) in Indonesia. Many staff from these departments provided invaluable advice, and we wouldlike to especially thank Suyono Dikun, Deputy Minister for Infrastructure, BAPPENAS; Jinny Katuuk, DeputyMinister for Fiscal and Economic Decentralization and Infrastructure Development, Coordinating Ministry forEconomic Affairs; and Bambang Susantono, Assistant Deputy for Communication and Telecommunication,Coordinating Ministry for Economic Affairs for their support and guidance. This report complements the“Infrastructure Indonesia: before, during and after the crisis, (2003)”, edited by Mr Dikun and developed byBAPPENAS which seeks to provide a long term infrastructure development scenario and encompasses all majorinfrastructure sectors.

KKPPI organized four workshops to discuss the background sector papers with a diverse group of sectoral experts.We would like to acknowledge the contribution from all of the participants of these workshops. Our understandingof each sector was greatly enhanced by their candid examination of the bottlenecks and solutions from a variety ofperspectives. These events brought together over 100 of the leading experts from government agencies, the privatesector, the NGO and academic communities, and the press. The background sector papers are included at the endof this report. The discussion from these workshops shaped our report, and the positive feedback prompted us toco-host with KKPPI a larger national conference to share and discuss the cross-cutting policy issues emerging fromour analysis of Indonesia’s infrastructure. Conclusions and comments from this conference shaped the mainreport. We want to thank Mr Susantono for taking the initiative to arrange these events and Hardini Puspasari andSri Oktorini for handling the logistical details.

vii

Table of ContentForeword vAcknowledgment vi

OverviewIntroduction 1The Problem 2Towards a Solution 4Need for Action on Multiple Fronts 6The Way Forward 15

Chapter 1Achievements, Challenges,and OpportunitiesIntroduction 17The Infrastructure Challenge 18Public Management of Infrastructure 26Business Environment for Infrastructure 27Corruption 28Financing Challenge 29

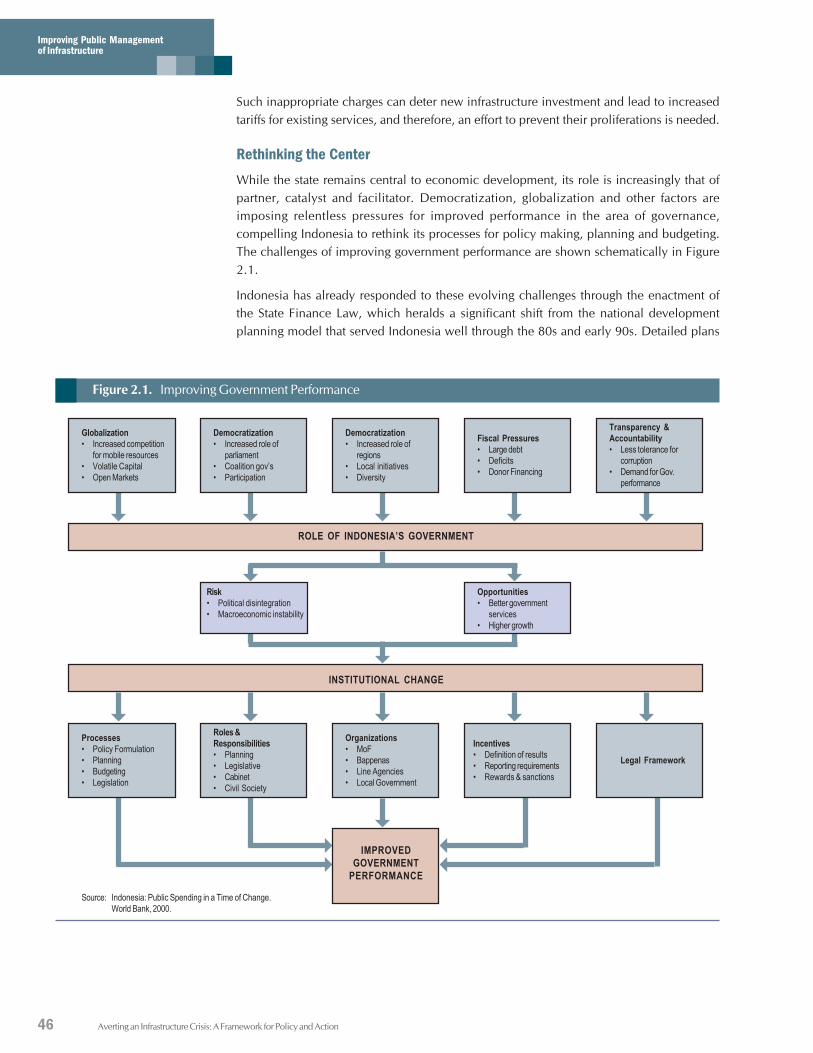

Chapter 2Improving Public Managementof InfrastructureIntroduction 31Commercializing, Corporatizing and Privatization 32Making Decentralization Work 34Evolving Role of the Center 39Recommendations 43

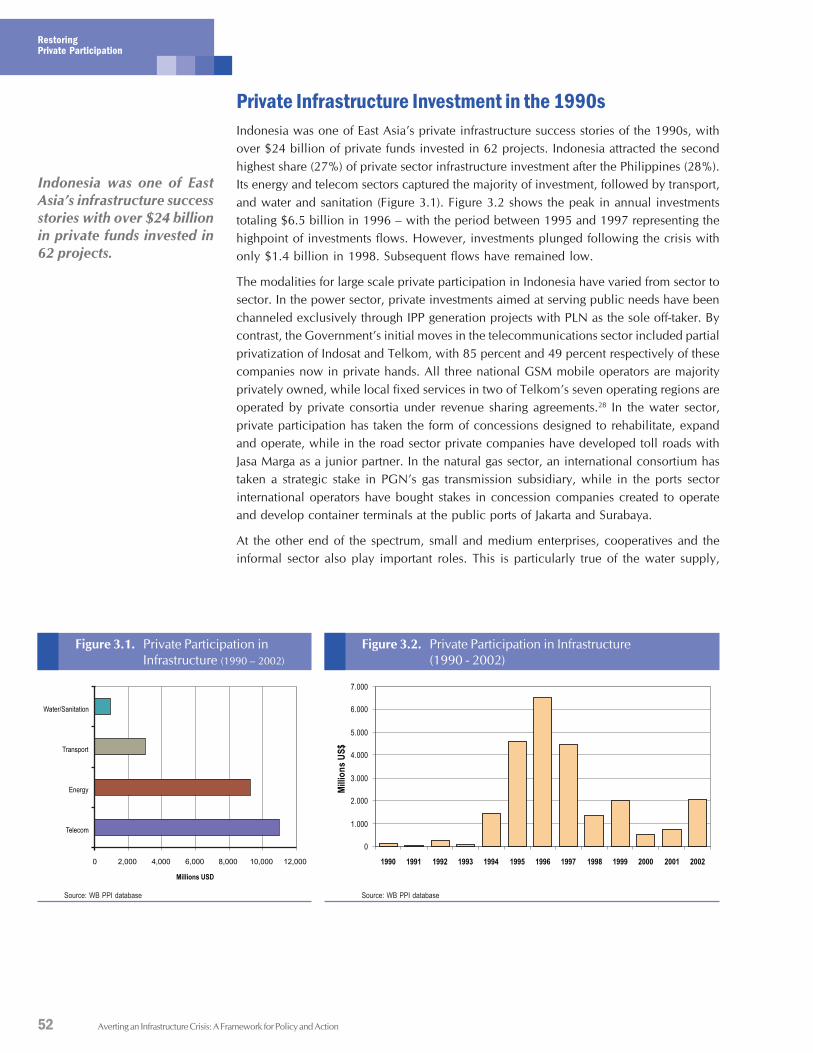

Chapter 3Restoring Private ParticipationIntroduction 49Private Infrastructure Investment in the 1990s 52The Promise of Private Service Provision 53Setting Objectives 54Ensuring the Financial Sustainability of Service Provision 55Maximizing Competitive Discipline 57Balancing Users and Operators’ Interests through

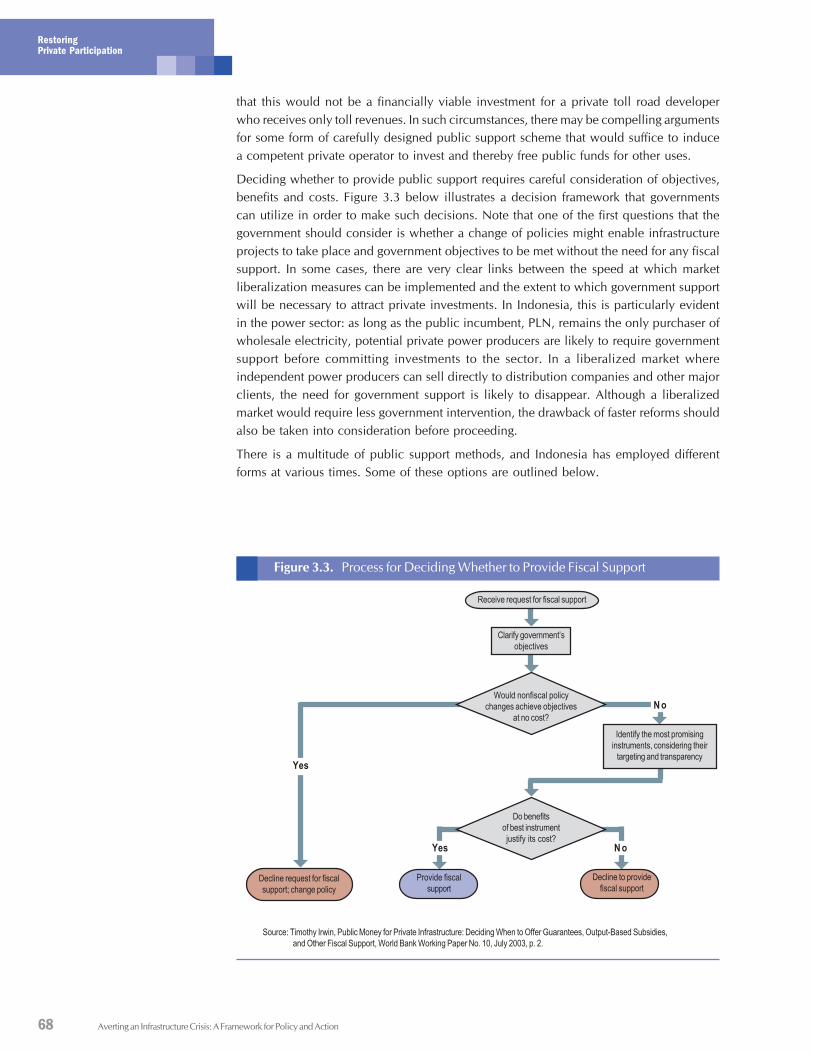

Adequate Regulation 62Allocating and Managing Risks 64Public Support for Private Projects 67Recommendations 73

Chapter 4Getting a Grip on CorruptionIntroduction 75Anatomy of Corruption in the Infrastructure Sectors 76Recommendations 85

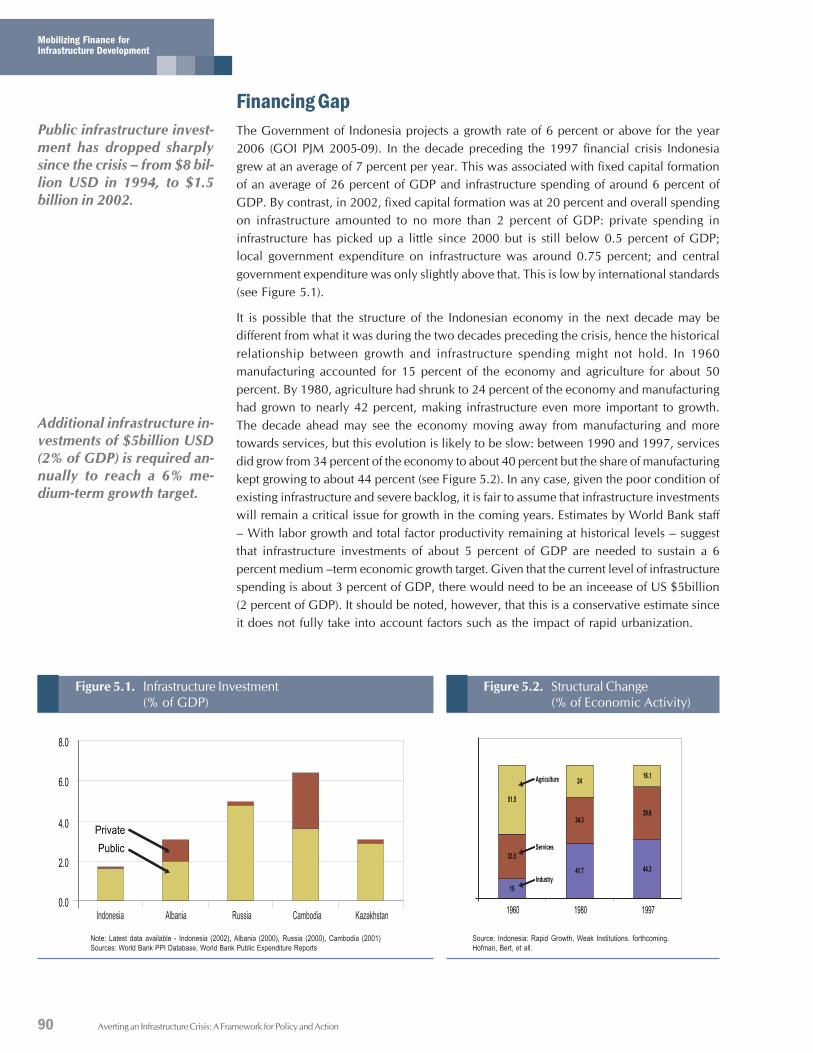

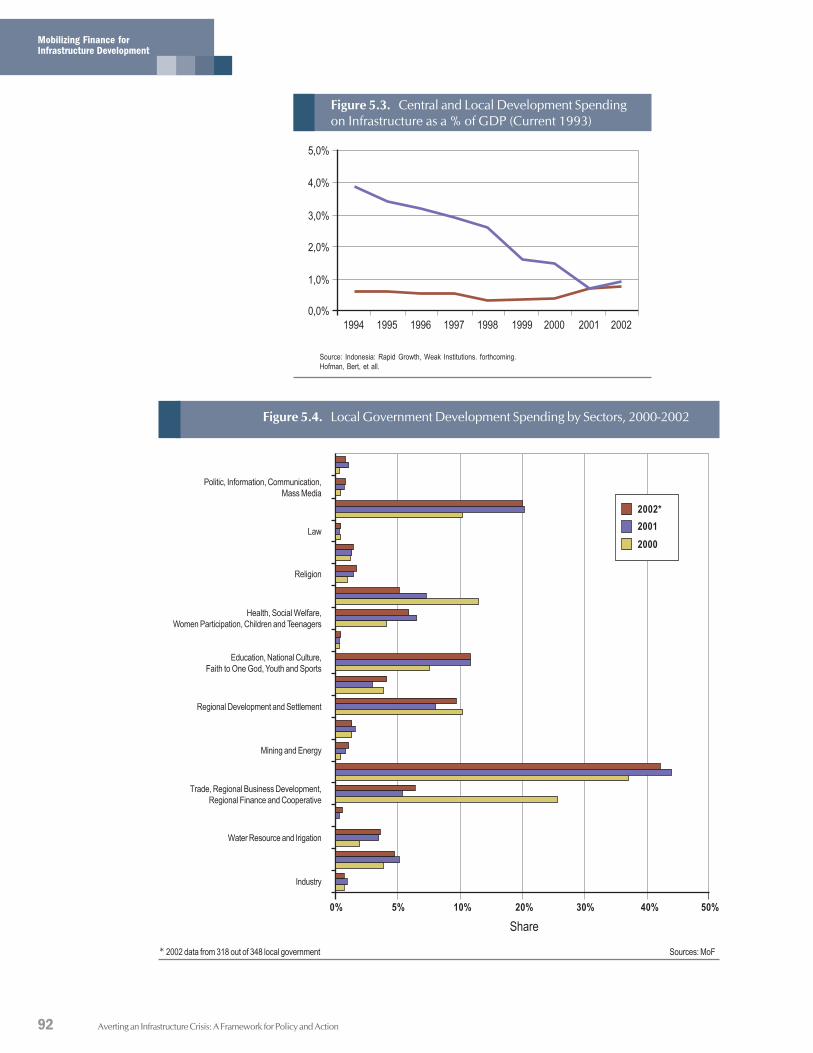

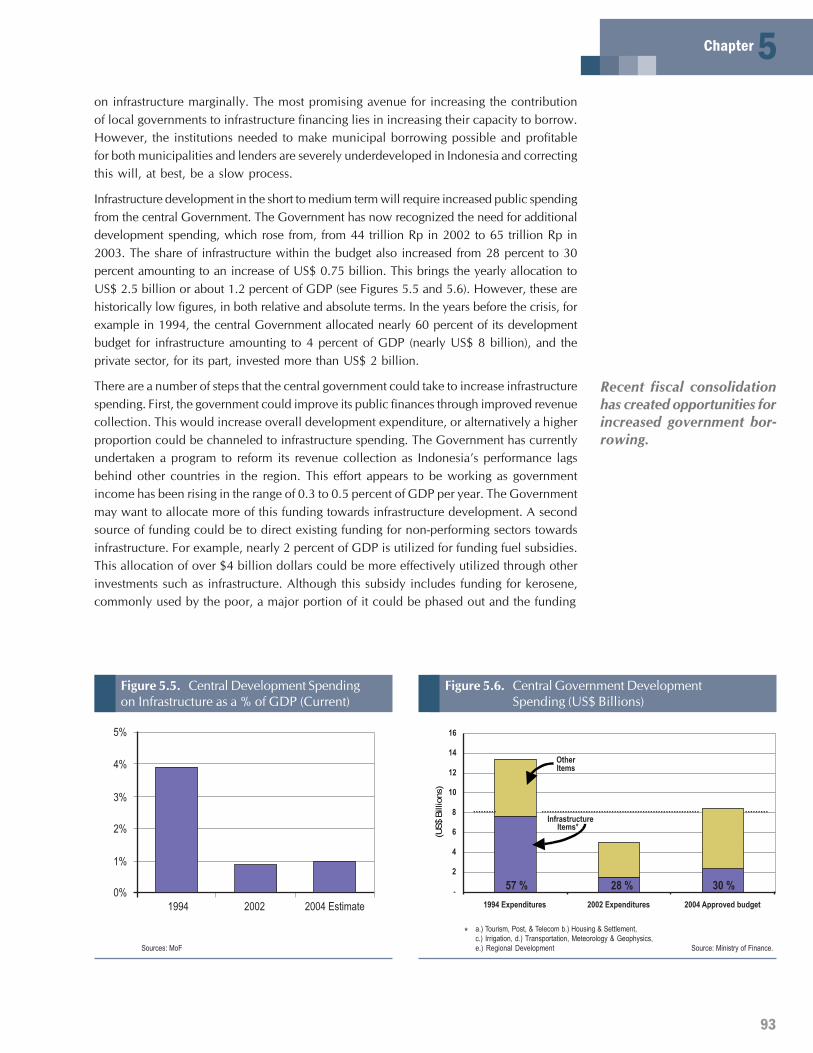

Chapter 5Mobilizing Finance for InfrastructureDevelopmentIntroduction 89Financing Gap 90Options for Bridging the Financing Gap 91Targeting Public Finances to Protect the Poor 98Recommendations 102

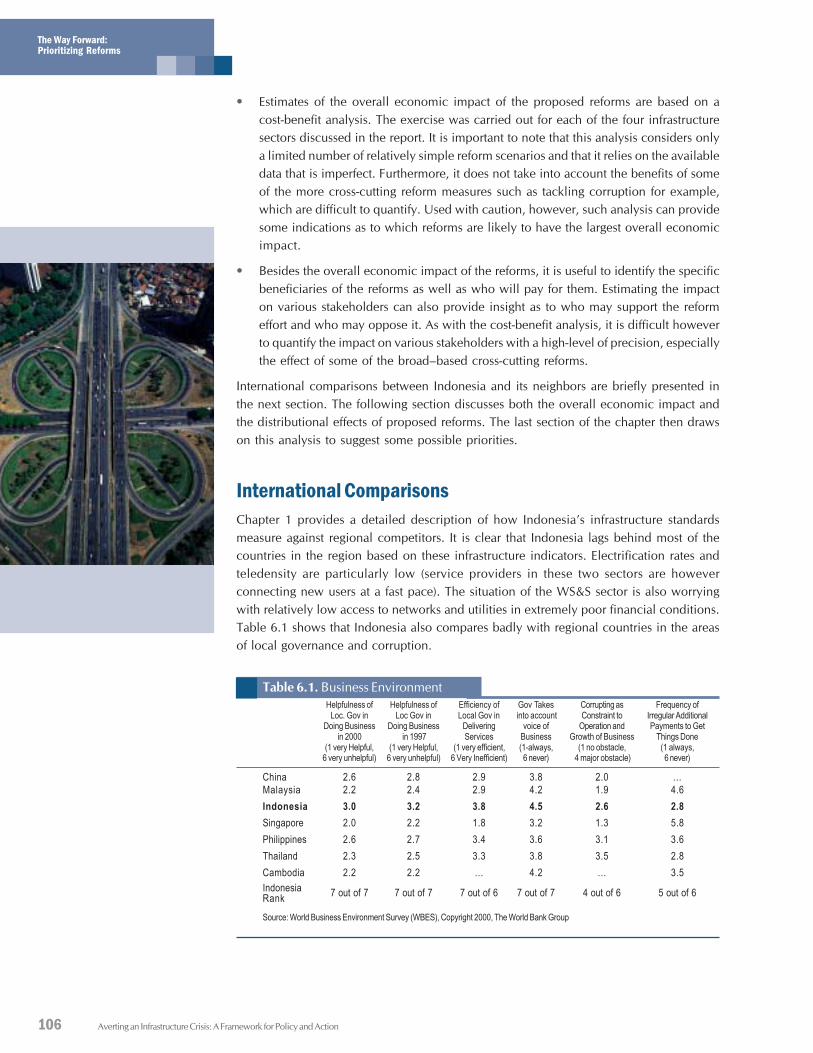

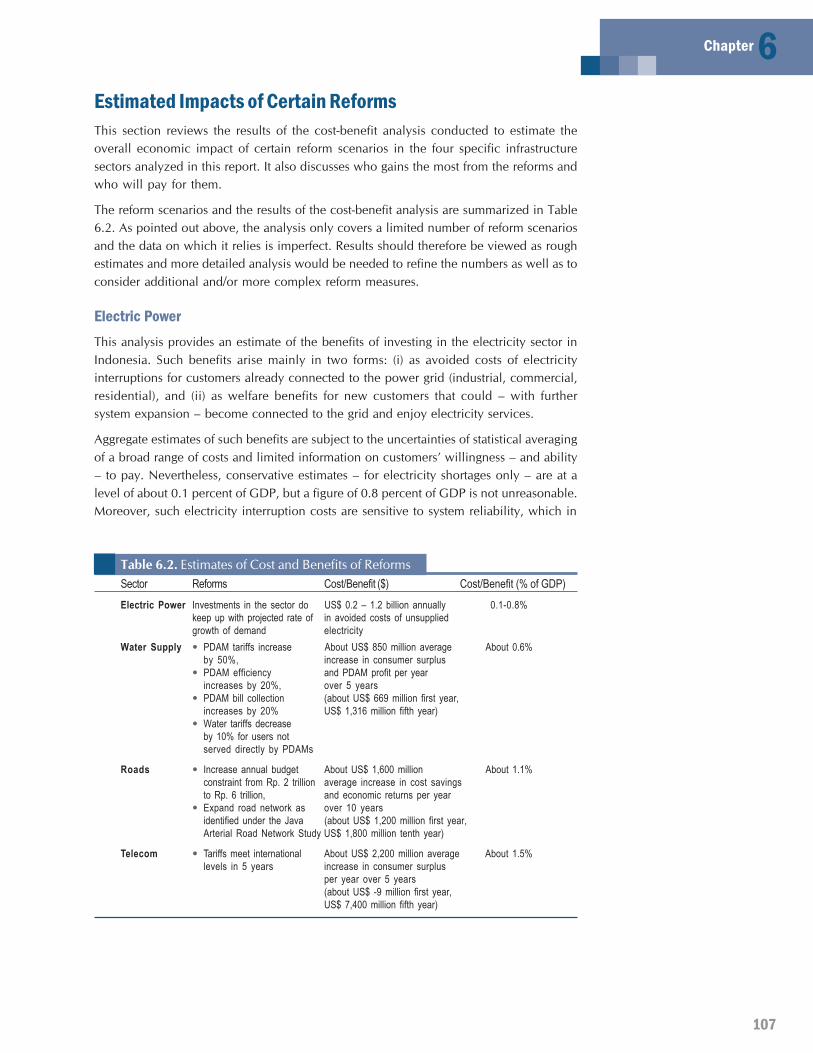

Chapter 6The Way Forward: Prioritizing ReformsIntroduction 105International Comparisons 106Estimated Impacts of Certain Reforms 107Prioritizing Reforms 110

List of Abbreviations 229End Notes 231Bibliography 239

viii Averting an Infrastructure Crisis: A Framework for Policy and Action

List of FiguresFigure 1. Total Infrastructure Expenditures

($US Billions, nominal) 2Figure 2. Access to Infrastructure by Income for 'Safe Water' 3Figure 3. Central Government Development Spending

(US$ Billions) 4Figure 4. Private Participation in Infrastructure ($US millions) 8Figure 5. Filling the Gap - Infrastructure Spending (% of GDP) 11Figure 6. Infrastructure Spending as a % of GDP) 11

Figure 1.1. Fewer firms are set up(percentage in total companies) 21

Figure 1.2. Growth and Infrastructure Investment(% of GDP) 21

Figure 1.3. Household Access to Safe Waterby Income (%) 22

Figure 2.1. Improving Government Performance 46

Figure 3.1. Private Participation in Infrastructure (1990 – 2002) 52Figure 3.2. Private Participation in Infrastructure (1990 - 2002) 52Figure 3.3. Process for Deciding Whether to Provide

Fiscal Support 68

Figure 5.1. Infrastructure Investment (% of GDP) 90Figure 5.2. Structural Change (% of Economic Activity) 90Figure 5.3. Central and Local Development Spending

on Infrastructure as a % of GDP (Current 1993) 92Figure 5.4. Local Government Development Spending

by Sectors, 2000-2002 92Figure 5.5. Central Development Spending on Infrastructure

as a % of GDP (Current) 93Figure 5.6. Central Government Development Spending

(US$ Billions) 93Figure 5.7. Fiscal Consolidation 94

List of TablesTable 1. Infrastructure Performance 2Table 2. Sector Issues 3

Table 1.1. Infrastructure Service Delivery– Power and Telecom 18

Table 1.2. Infrastructure Service Delivery– Water, Sanitation and Roads 18

Table 1.3. Urbanization in East Asia 22

Table 3.1. Main Forms and Potential Benefits of InfrastructurePrivatization 53

Table 3.2. Options Most Likely to Address GovernmentObjectives 70

Table 6.1. Business Environment 106Table 6.2. Estimates of Cost and Benefits of Reforms 107

List of Text BoxesBox 1. taking action – on Public Management 7Box 2. taking action – on Restoring Private Participation 10Box 3. taking action – on Tackling Corruption 11Box 4. taking action – Mobilizing Finance for Infrastructure

Development 14

Box 1.1. Infrastructure and the Business Climate 20

Box 2.1. Financing Schemes to Pursue National Objectives inDecentralized Contexts: The State RevolvingFund Model 36

Box 2.2. Financing Schemes Using Apex Institutions to Select“Good” Projects - The case of FINDETER in Colombia 37

Box 3.1. Achieving Economies of Scale in Waterand Sanitation in Brazil 61

Box 3.2. Assessing the Fiscal Impact of ColombianGovernment Guarantees 71

Box 3.3. South Africa – Taking into Account Public ExpenditureImpact of Public-private Partnerships in Infrastructure 72

Box 4.1. Procurement in the Second Sulawesi UrbanDevelopment Project 79

Box 4.2. Year-end moves to protect budgets 83

Box 5.1. Using Pension Funds in Chile to Finance Infrastructure 96Box 5.2. Malaysia: The Case of the Employees Provident Fund 97Box 5.3. Cross-subsidizing New Connections Under

the Buenos Aires Water and Sanitation Concession 100Box 5.4. Output-based Aid Scheme to Extend the Teledensity

in Chile 101

Table of Content

ix

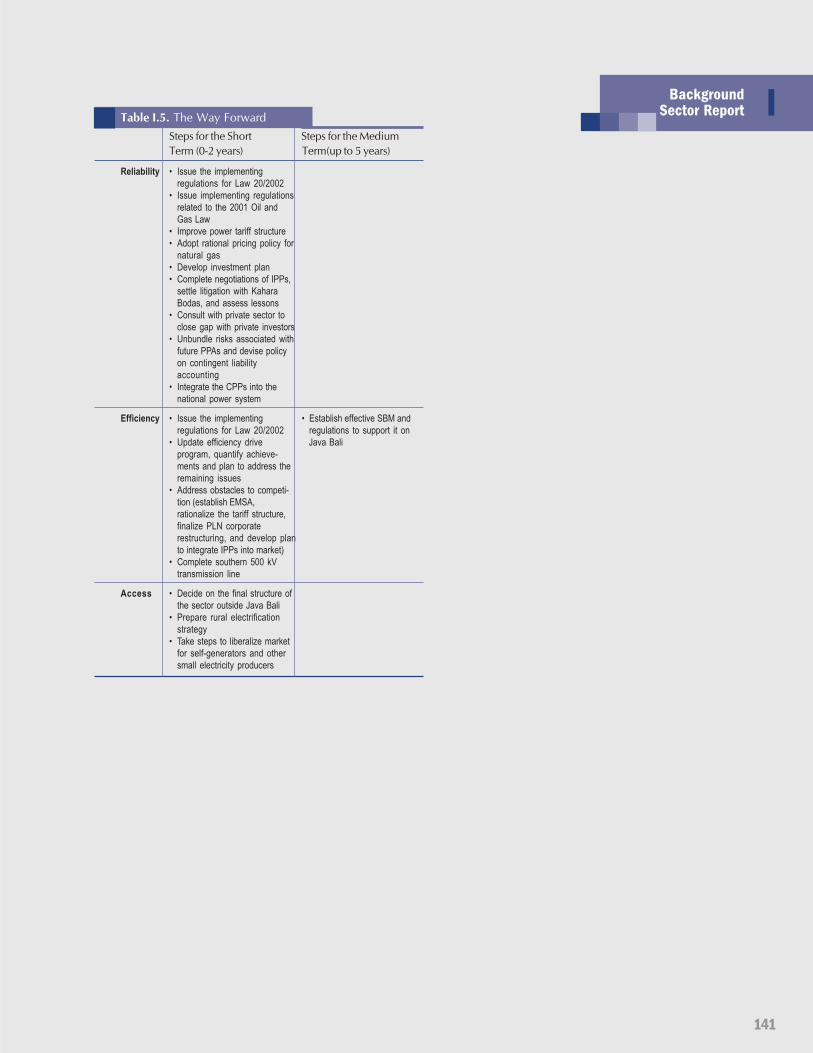

Background Sector Report IElectric PowerIntroduction 121Policy and Institutional Framework 124Sector Structure and Ownership 126Investment Needs and Financing 129Sector Performance 131Main Sector Issues 133The Way Forward 137

Annex I.1Cost Benefit Analysis – Electric Power 140

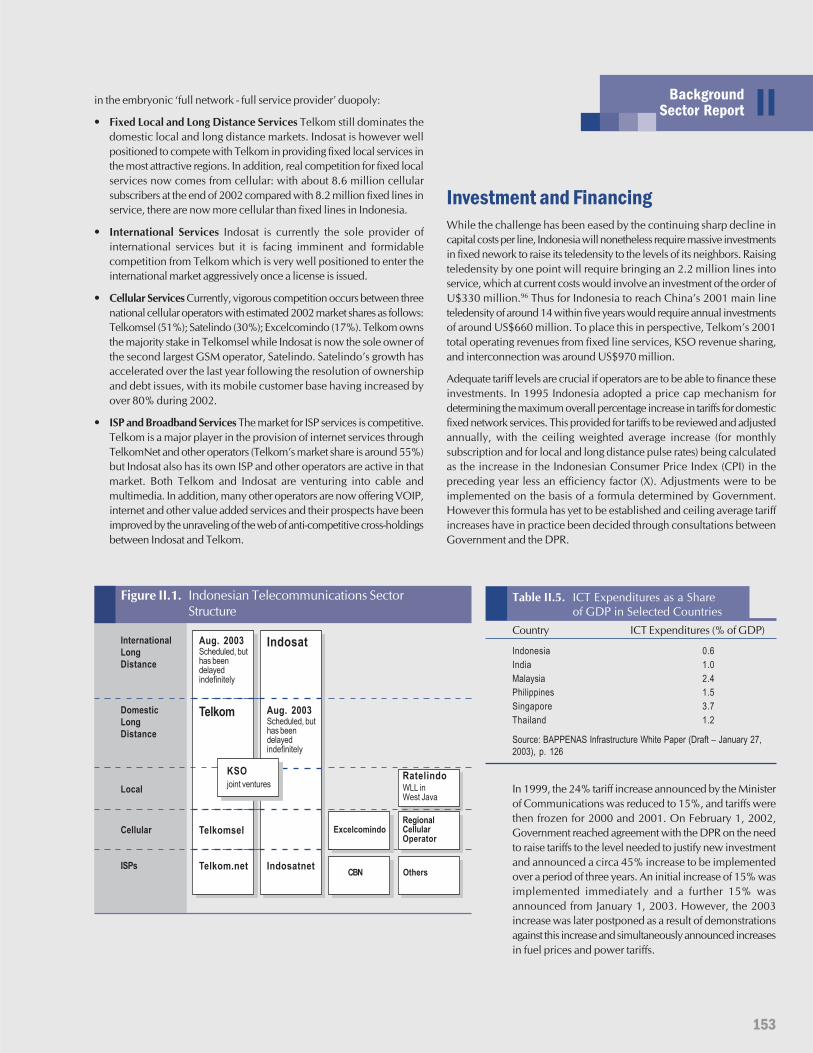

Background Sector Report IITelecommunicationsIntroduction 149Policy and Institutional Framework 150Sector Structure and Ownership 151Investment and Financing 153Sector Performance 154Main Issues 156The Way Forward 158

Annex II.1Cost Benefit Analysis – Telecommunications 160

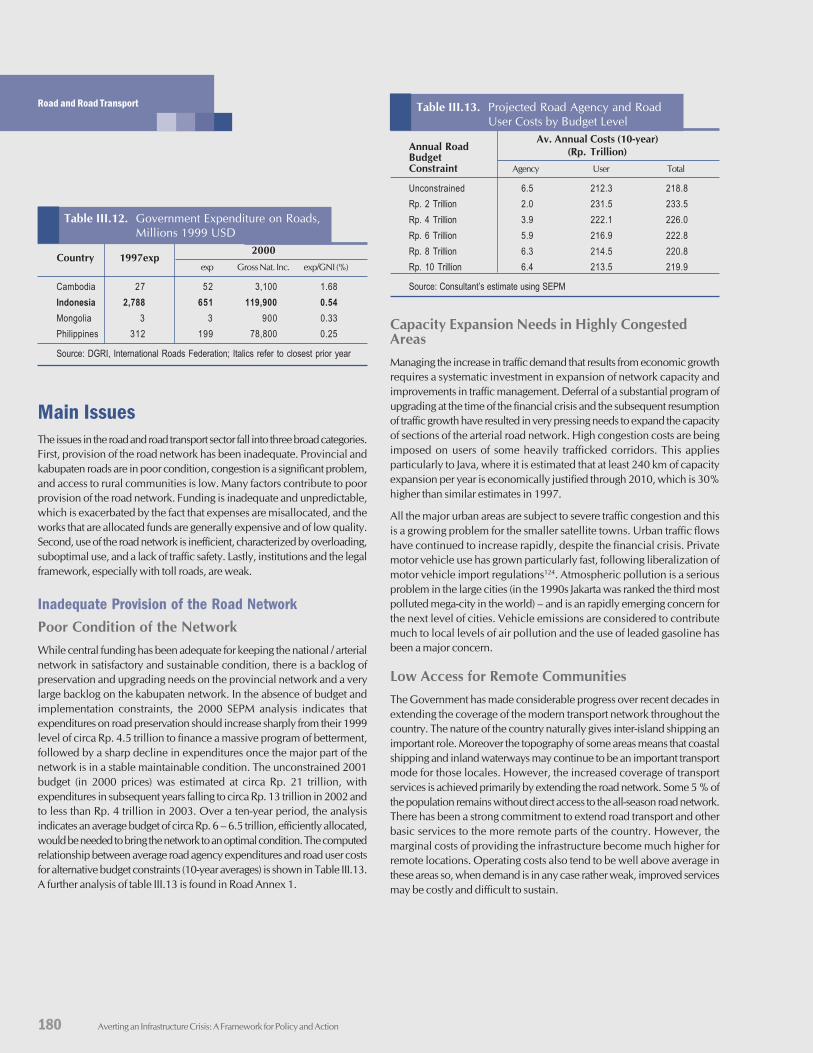

Background Sector Report IIIRoad and Road TransportOverview 171Policy and Institutional Framework 173Sector Structure and Ownership 174Investment and Financing 175Sector Performance 178Main Issues 180The Way Forward 182

Annex III.1Cost Benefit Analysis – Road and Road Transport 190

Background Sector Report IVWater Supply and SanitationOverview 193PART A: WATER SUPPLY

Policy and Institutional Framework (Water) 195Sector Structure and Ownership (Water) 196Investment and Financing (Water) 199Sector Performance (Water) 200Main Sector Issues (Water) 202

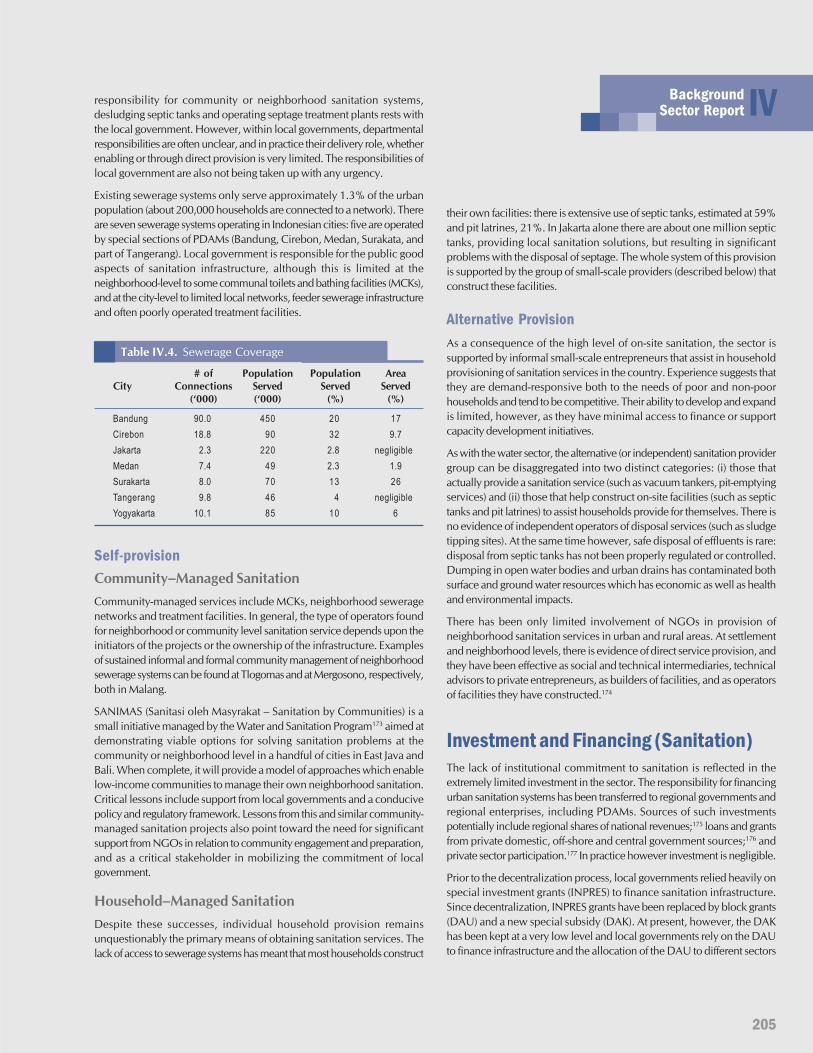

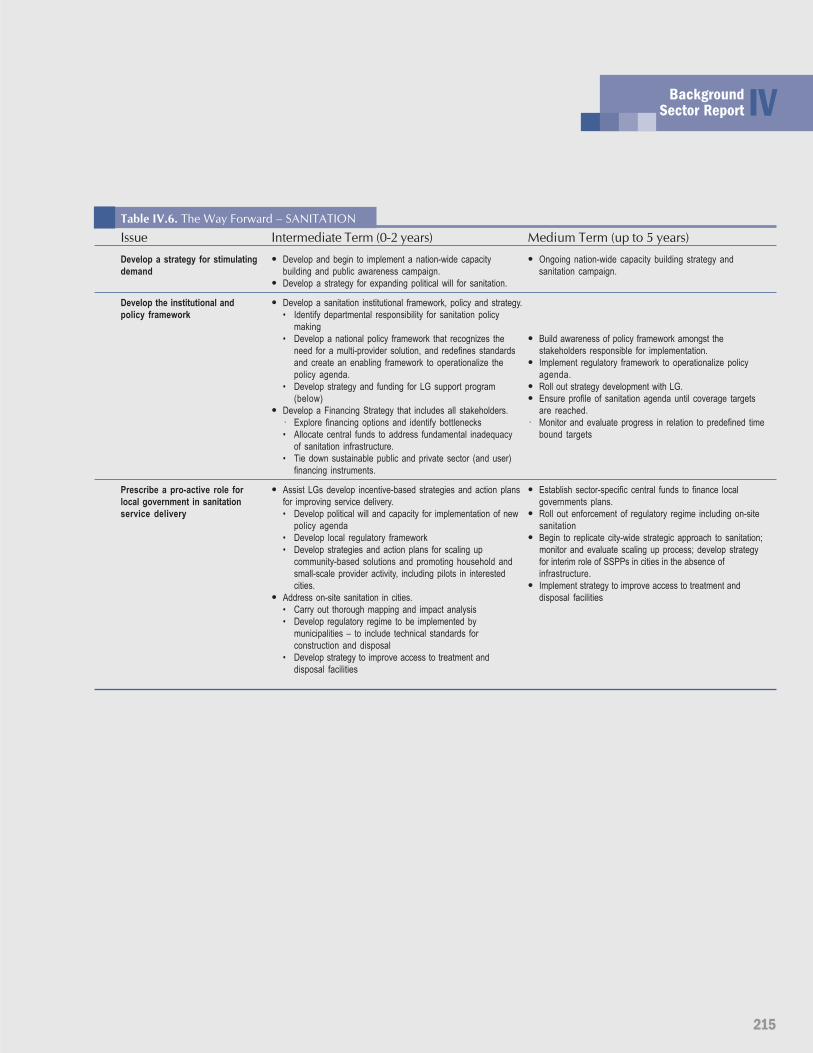

PART B: SANITATIONPolicy and Institutional Framework (Sanitation) 204Sector Structure and Ownership (Sanitation) 204Investment and Financing (Sanitation) 205Main Sector Issues (Sanitation) 208The Way Forward ( Water and Sanitation) 209

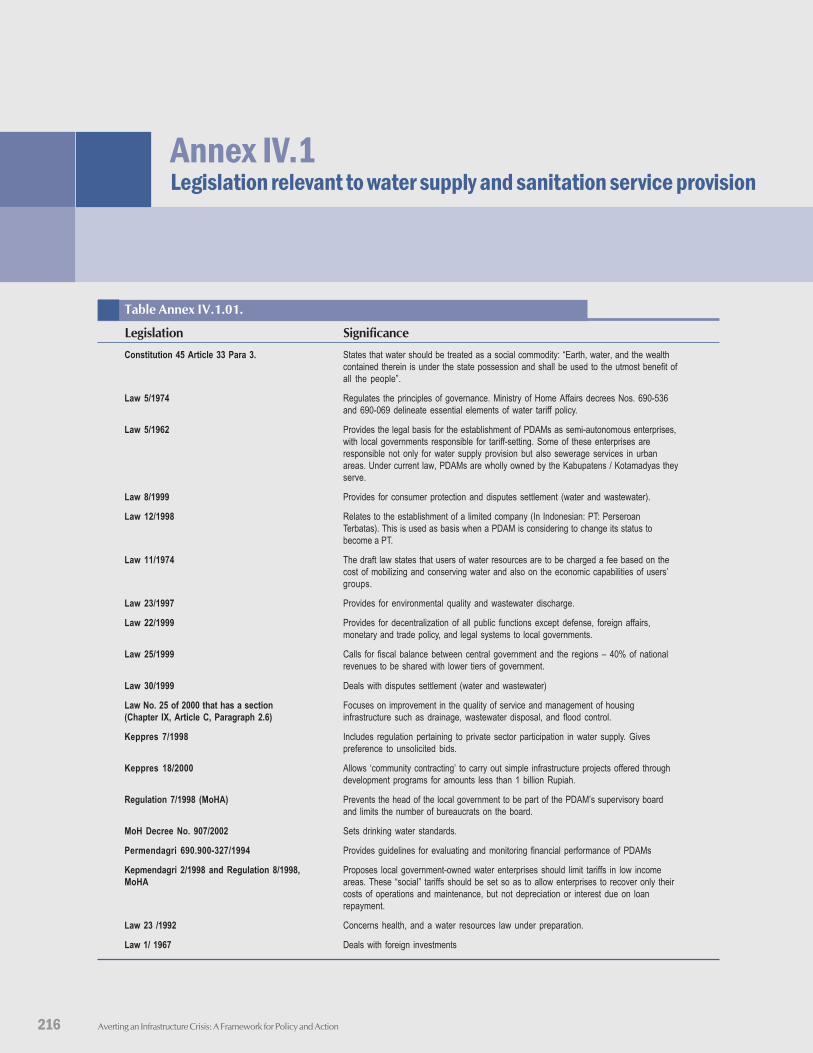

Annex IV.1Legislation relevant to water supplyand sanitation service provision 216

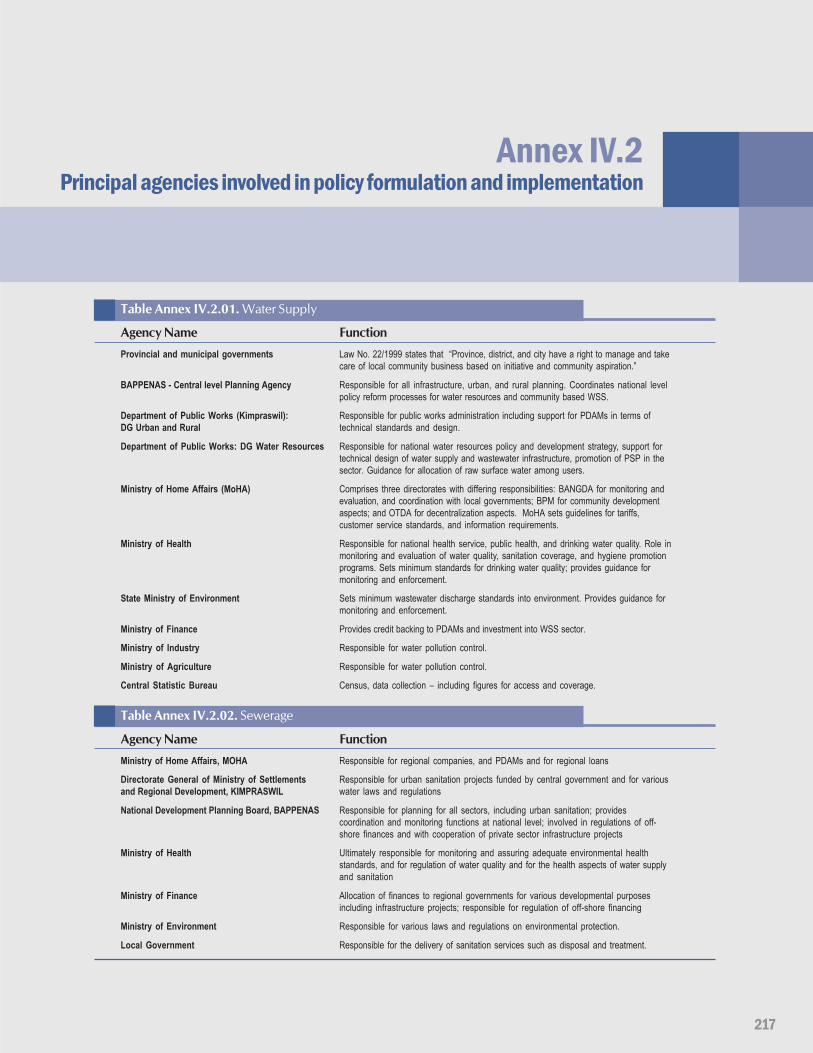

Annex IV.2Principal agencies involved in policy formulationand implementation 217

Annex IV.3The Jakarta Concessions 218

Annex IV.4Financial Recovery Action Plan (FRAP) 219

Annex IV.5Corporatization of PDAMs 221

Annex IV.6Cost Benefit Analysis – Water Supply 222

Table of Content

x Averting an Infrastructure Crisis: A Framework for Policy and Action

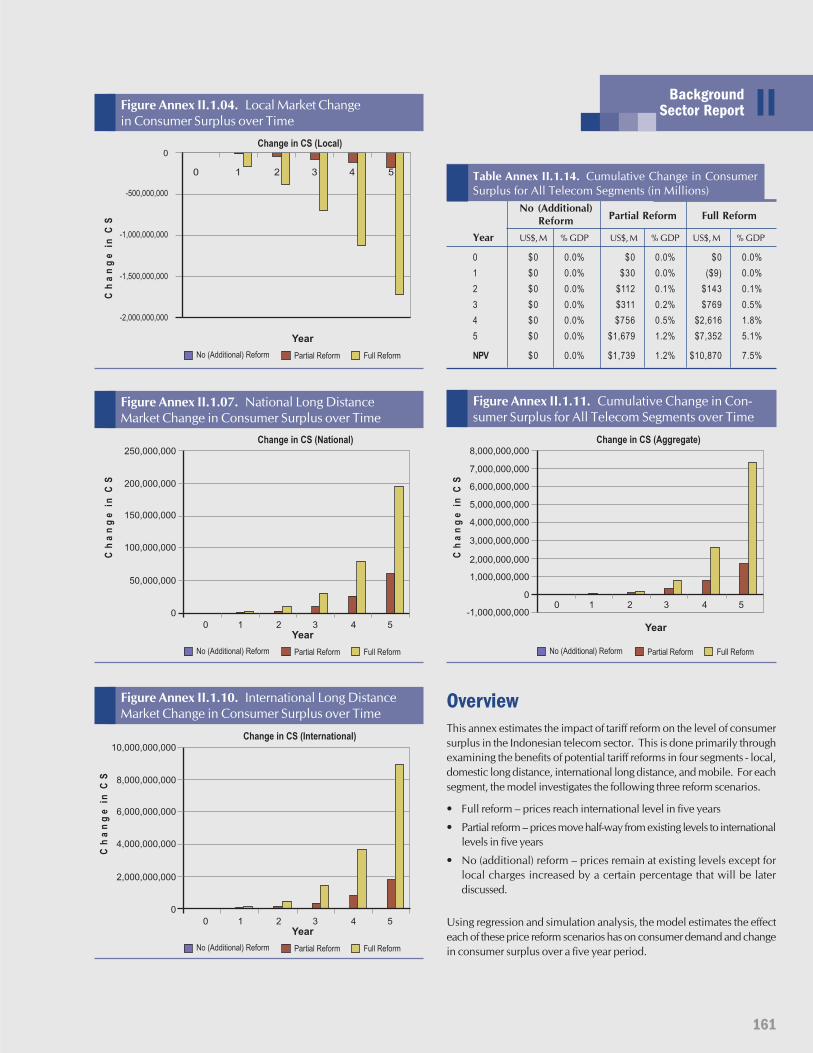

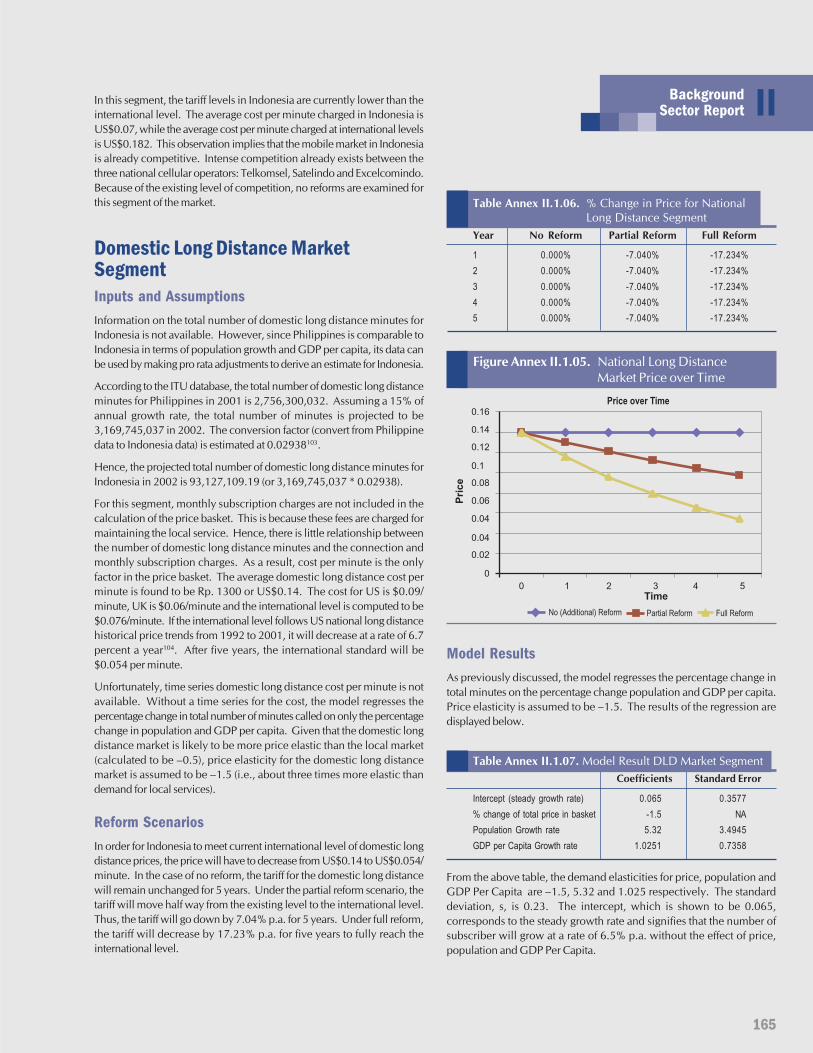

List of FiguresFigure II.1. Indonesian Telecommunications Sector Structure 153Figure Annex II.1.01. Model simulation - Price elasticity 162Figure Annex II.1.02. Local Market Price vs. Time 163Figure Annex II.1.03. Local Market Quantity Demanded

over Time 164Figure Annex II.1.04. Local Market Change in Consumer

Surplus over Time 164Figure Annex II.1.05. National Long Distance Market Price

over Time 165Figure Annex II.1.06. National Long Distance Market Quantity

Demanded over Time 166Figure Annex II.1.07. National Long Distance Market Change

in Consumer Surplus over Time 166Figure Annex II.1.08. International Long Distance Market

Price over Time 167Figure Annex II.1.09. International Long Distance Market

Quantity Demanded over Time 168Figure Annex II.1.10. International Long Distance Market

Change in Consumer Surplus over Time 168Figure Annex II.1.11. Aggregate Change in Consumer Surplus

over Time 168

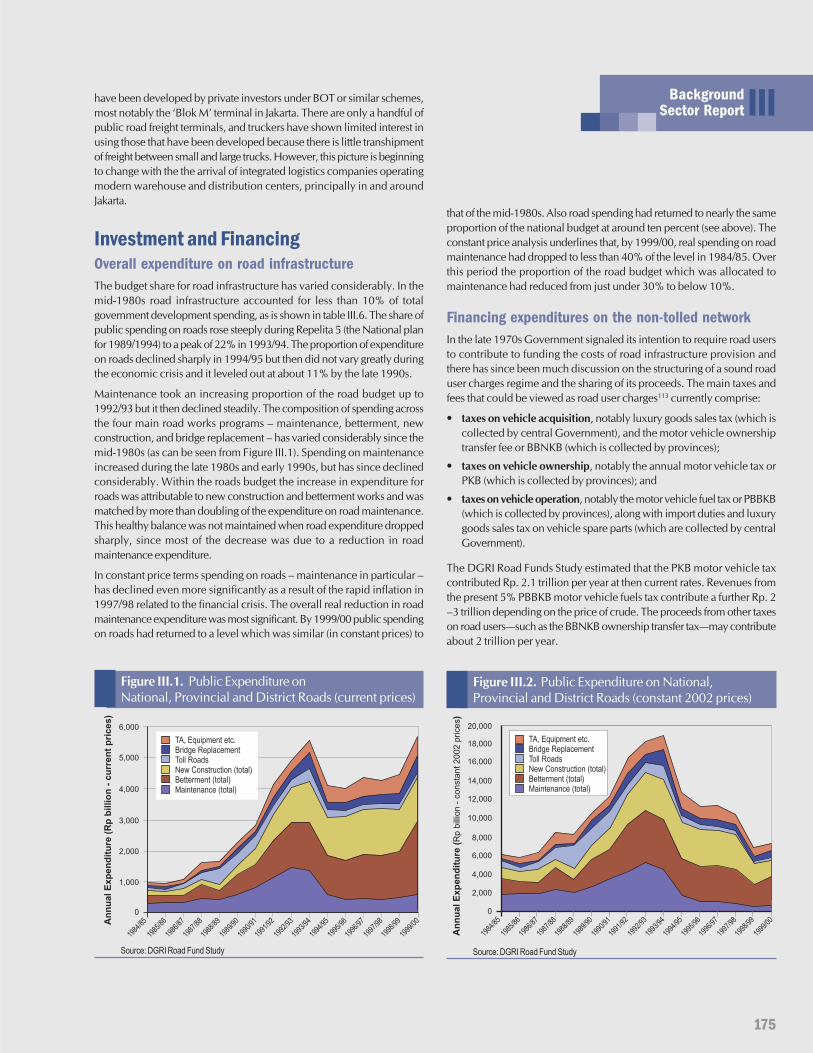

Figure III.1. Public Expenditure on National, Provincialand District Roads (current prices) 175

Figure III.2. Public Expenditure on National, Provincial andDistrict Roads (constant 2002 prices) 175

Figure III.3. Adequacy and Allocation of Resources for RoadPreservation 180

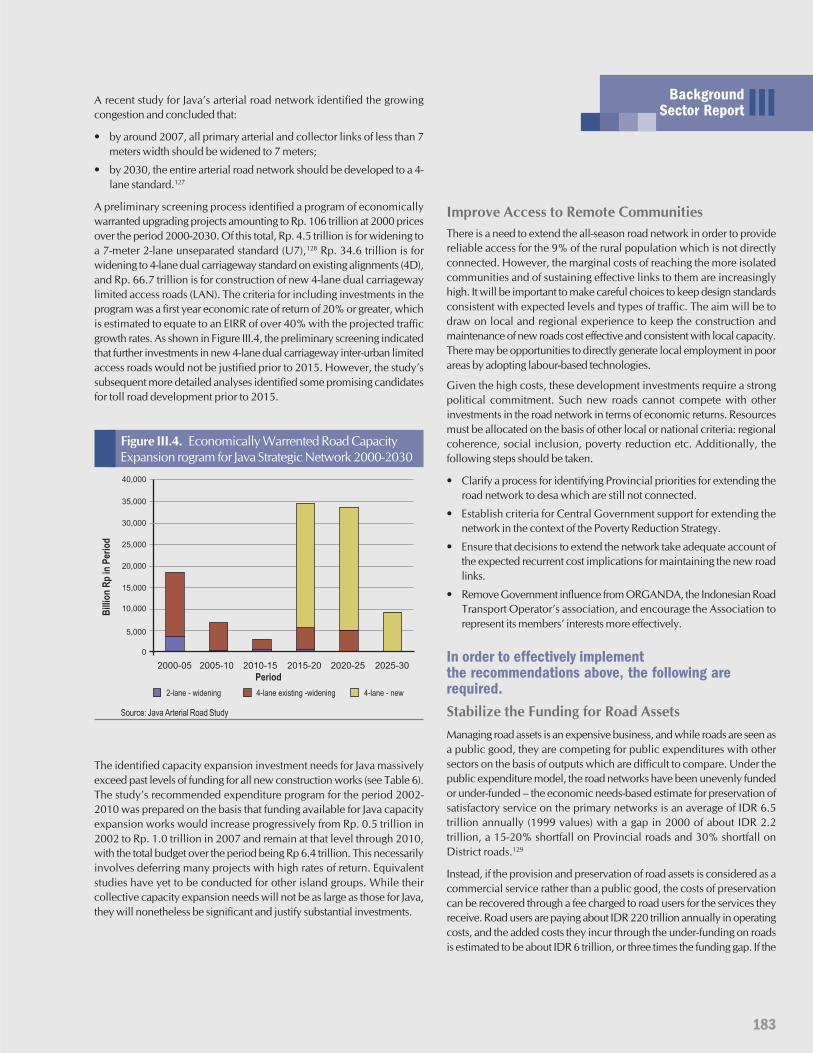

Figure III.4. Economically Warrented Road Capacity ExpansionProgram for Java Strategic Network 2000-2030 183

Figure Annex III.1.01 191

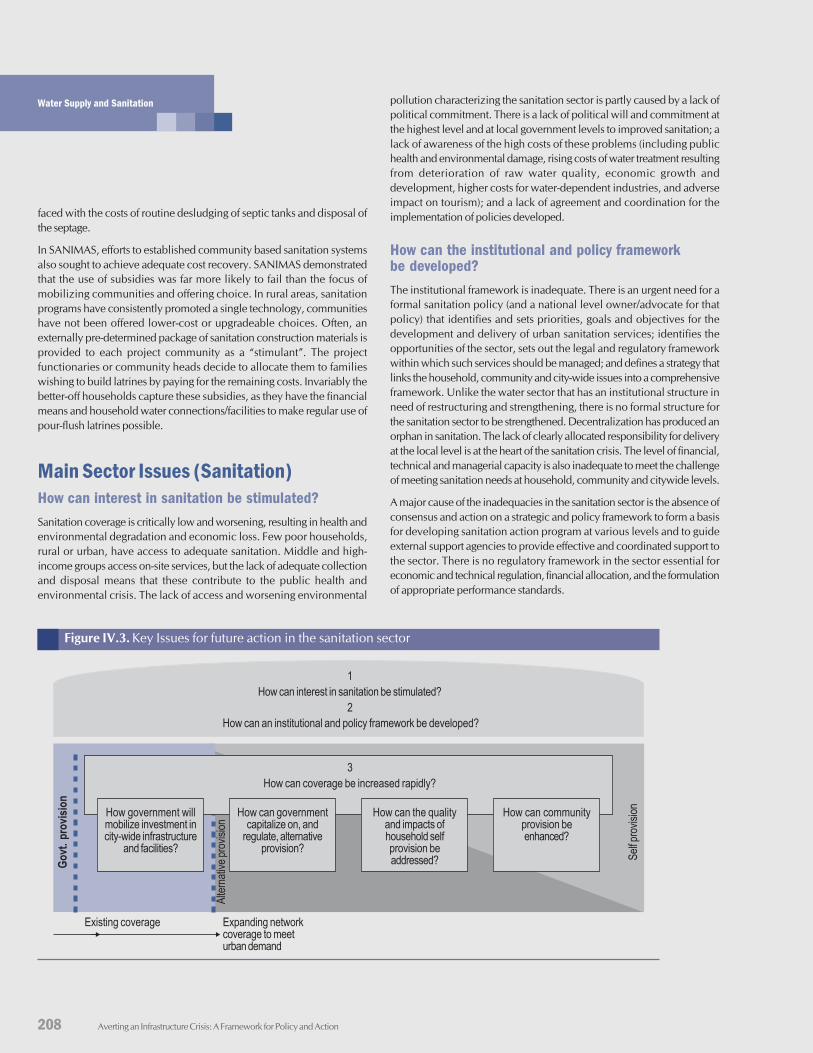

Figure IV.1. Sector Structure and Ownership 196Figure IV.2. Key Issues for future action in the water sector 202Figure IV.3. Key Issues for future action in the sanitation sector 208

List of TablesTable I.1: Main Legal and Regulatory Provisions 124Table I.2: Electrification Rates (%) 131Table I.3. Quality of Electricity Supply (Scale of 1-7), 2002 132Table I.4. Transmission and Distribution Losses (%) 132Table I.5. The Way Forward 141Table Annex I.1.01. Cost to sector due to power shortage 145

Table II.1. Key Reforms Introduced by Law 36/1999 150Table II.2. Allocation of Policy and Regulatory Responsibilities 151Table II.3. Telkom and Indosat – Transition to two Full-Service

Providers 151Table II.4 Investment in KSO Regions 152Table II.5. ICT Expenditures as a Share of GDP in Selected

Countries 153Table II.6. Teledensities in Selected Countries 155Table II.7. Internet Use in Selected Countries 2001 155Table II.8. Telephone Faults per 100 Lines per month 155Table II.9. Telephone Main Lines per Employee 155Table II.10. Fixed and Analog Cellular Fees 2001 156Table II.11. Fixed and Analog Cellular Fees as Percentage

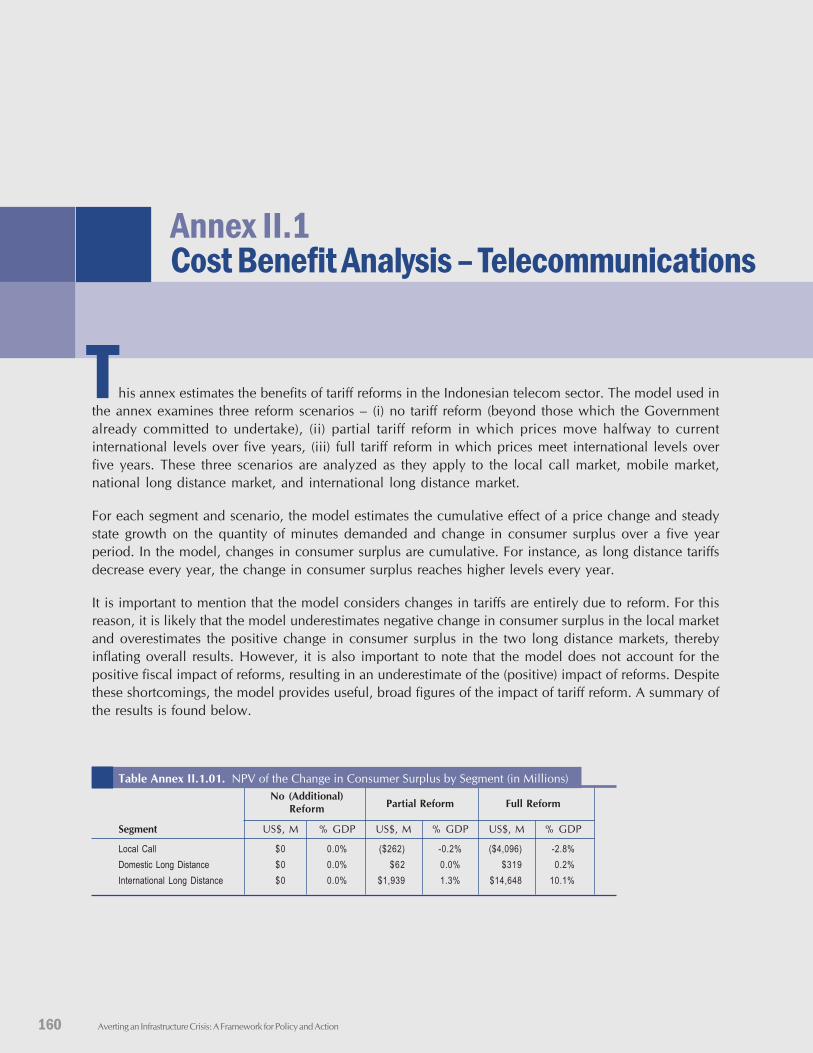

of Per Capita GNI 2001 156Table II.12. The Way Forward 159Table Annex II.1.01. NPV of the Change in Consumer Surplus by

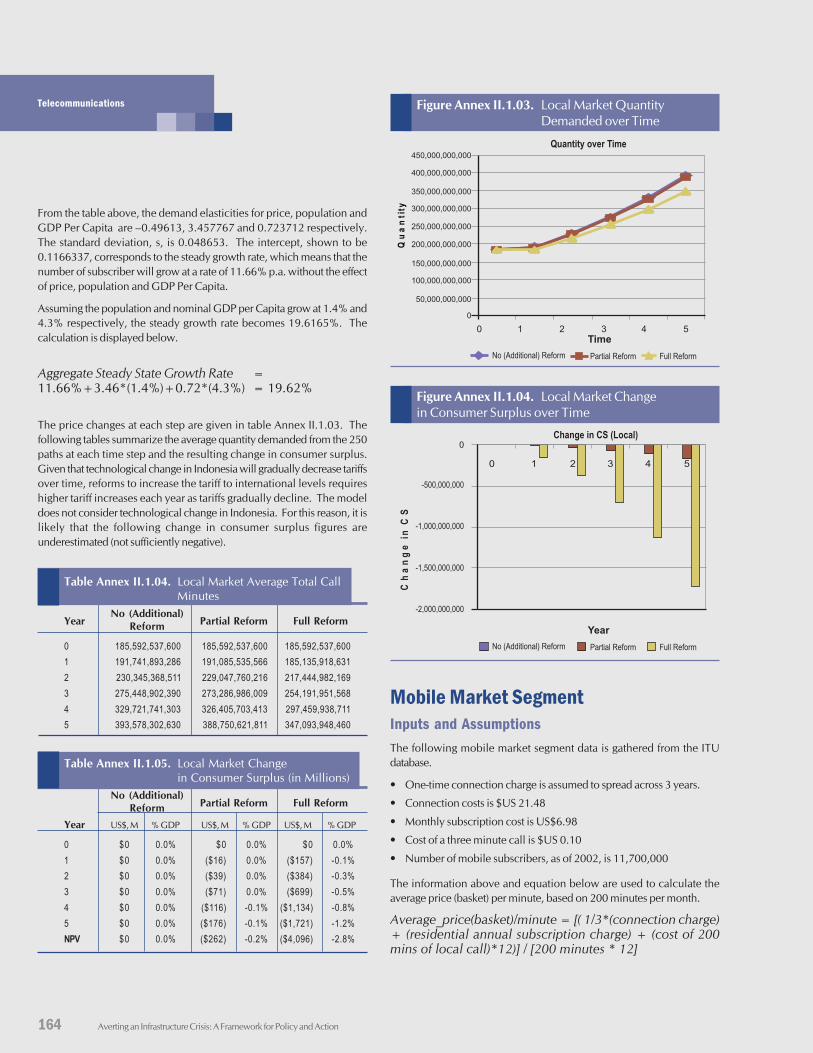

Segment (in Millions) 160Table Annex II.1.02. % Change in Price for Local Segment 163Table Annex II.1.03. Model Result - Local Market Segment 163Table Annex II.1.04. Local Market Average Total Call Minutes 164Table Annex II.1.05. Local Market Change in Consumer

Surplus (in Millions) 164Table Annex II.1.06. % Change in Price for National Long

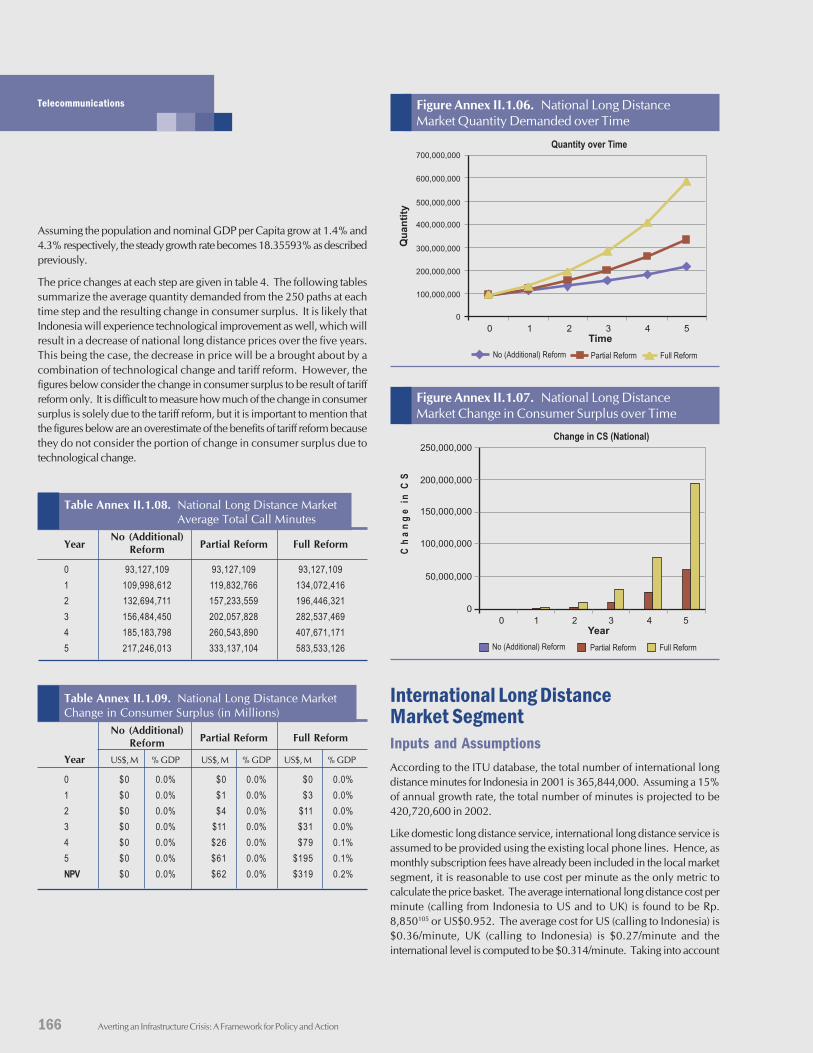

Distance Segment 165Table Annex II.1.07. Model Result DLD Market Segment 165Table Annex II.1.08. National Long Distance Market Average

Total Call Minutes 166Table Annex II.1.09. National Long Distance Market Change

in Consumer Surplus (in Millions) 166Table Annex II.1.10. % Change in Price for International Long

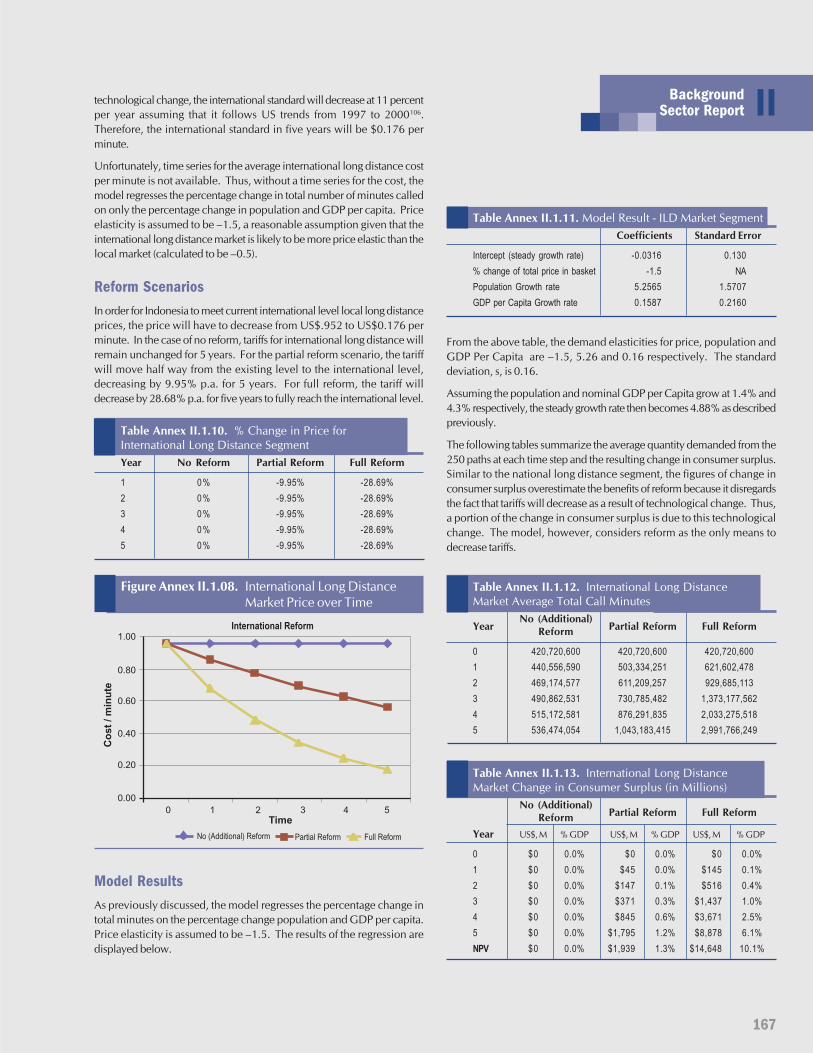

Distance Segment 167Table Annex II.1.11. Model Result - ILD Market Segment 167Table Annex II.1.12. International Long Distance Market

Average Total Call Minutes 167Table Annex II.1.13. International Long Distance Market

Change in Consumer Surplus (in Millions) 167Table Annex II.1.14. Aggregate Change in Consumer Surplus

(in Millions) 168

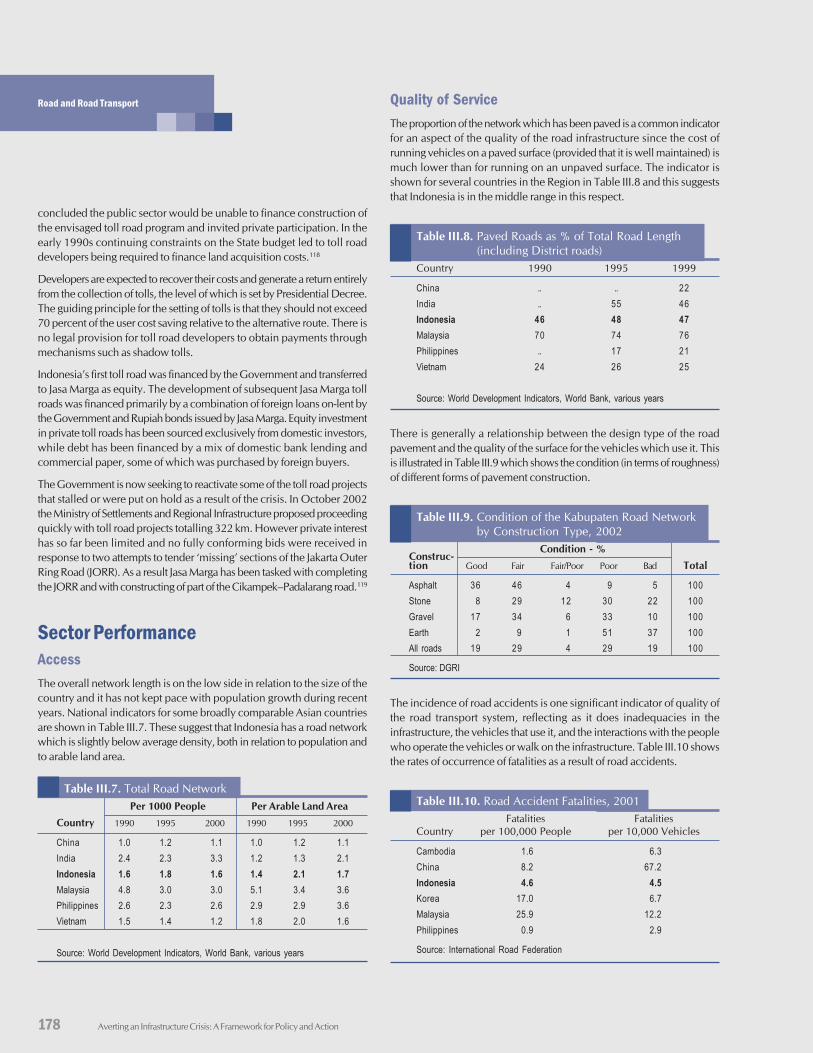

Table III.1. Classification of Roads and Allocation ofResponsibilities for Development and Maintenance 172

Table III.2. Main Legal and Regulatory Provisions 172Table III.2. Main Legal and Regulatory Provisions 172

Table of Content

xi

Table III.3. Allocation of Policy and Regulatory Responsibilities 173Table III.4. Length of the Public Non-Tolled Road Network (Km) 174Table III.5. Regional Shares of Classified Road Network,

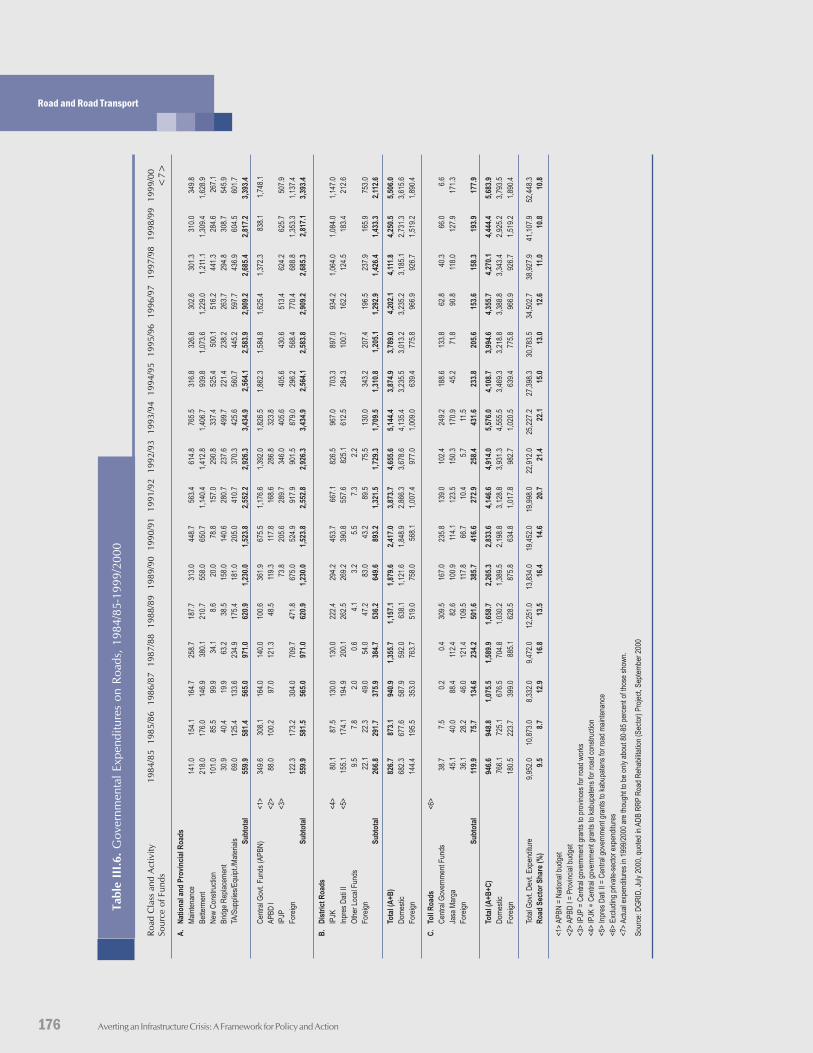

Land Area and Population, 2000 (%) 174Table III.6. Governmental Expenditures on Roads,

1984/85-1999/2000 176Table III.7. Total Road Network 178Table III.8. Paved Roads as % of Total Road Length (including

District roads) 178Table III.9. Condition of the Kabupaten Road Network by

Construction Type, 2002 178Table III.10. Road Accident Fatalities, 2001 178Table III.11. Condition of the National and Provincial Road

Network by Region, 2001 (%) 179Table III.12. Government Expenditure on Roads,

Millions 1999 USD 180Table III.13. Projected Road Agency and Road User Costs

by Budget Level 180Table III.14. The Way Forward 188Table Annex III.1.01. NPV of the Change in Consumer Surplus by

Segment (in Millions) 190Table Annex III.1.02. Projected Road Agency and Road User Costs

Assuming 80% Efficiency 191

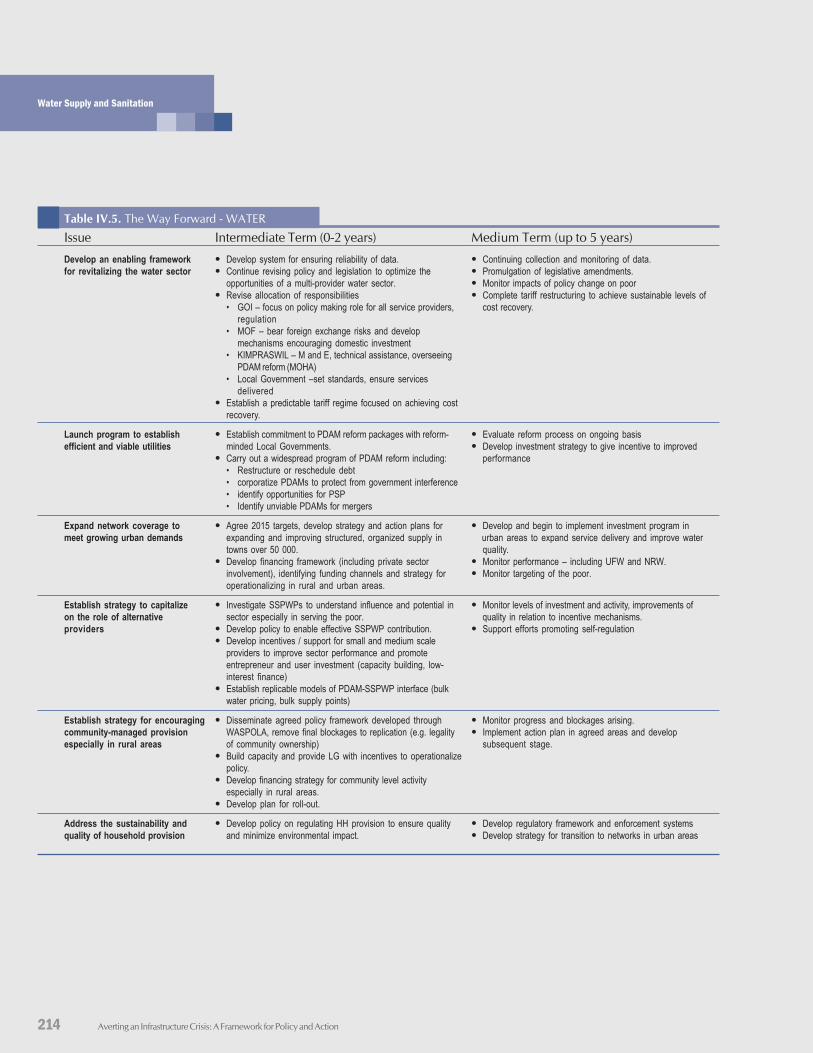

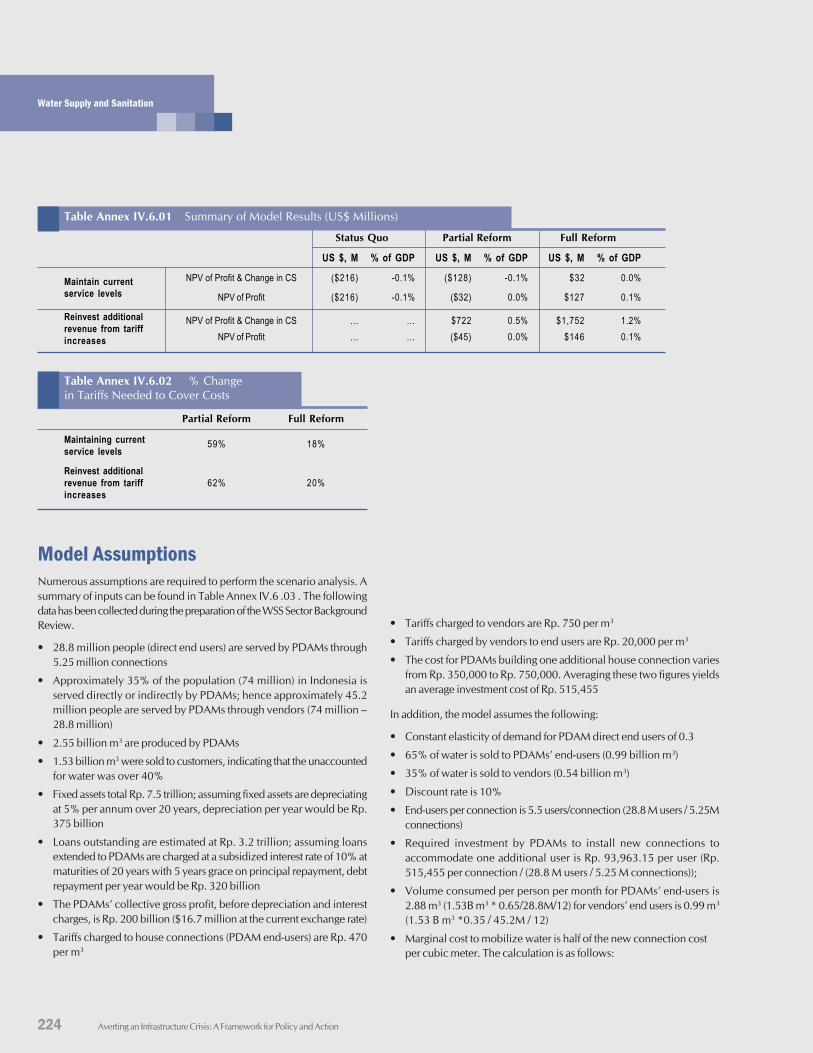

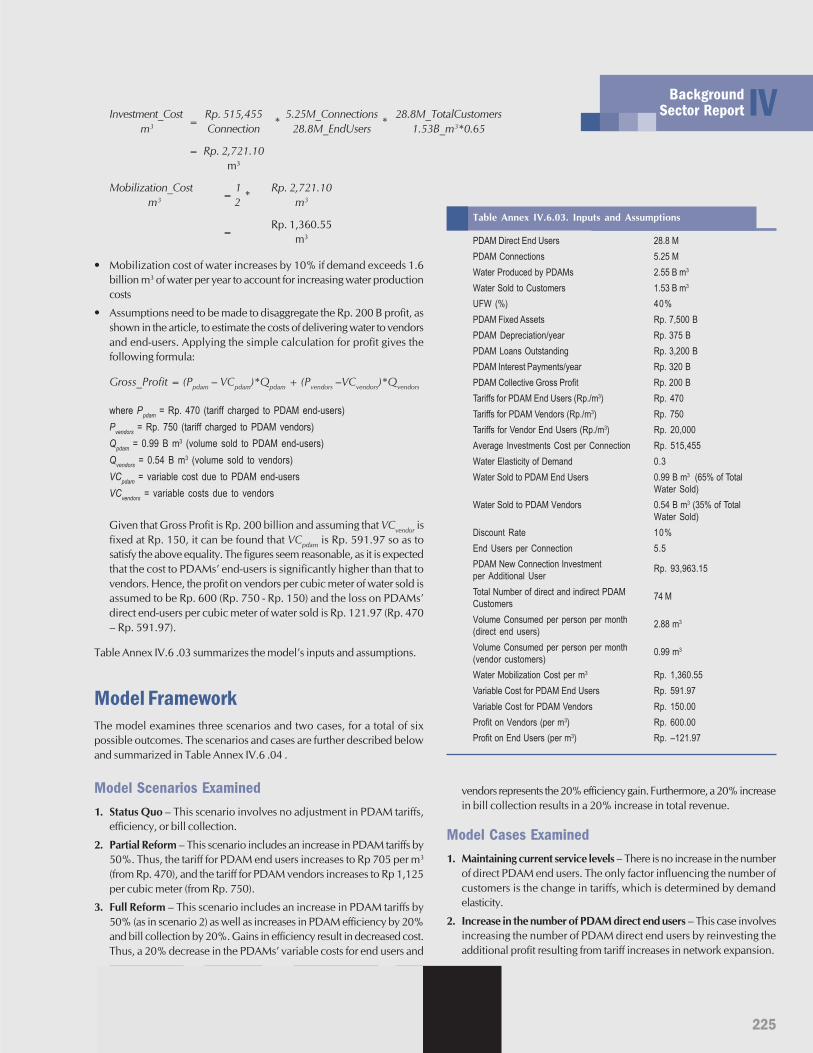

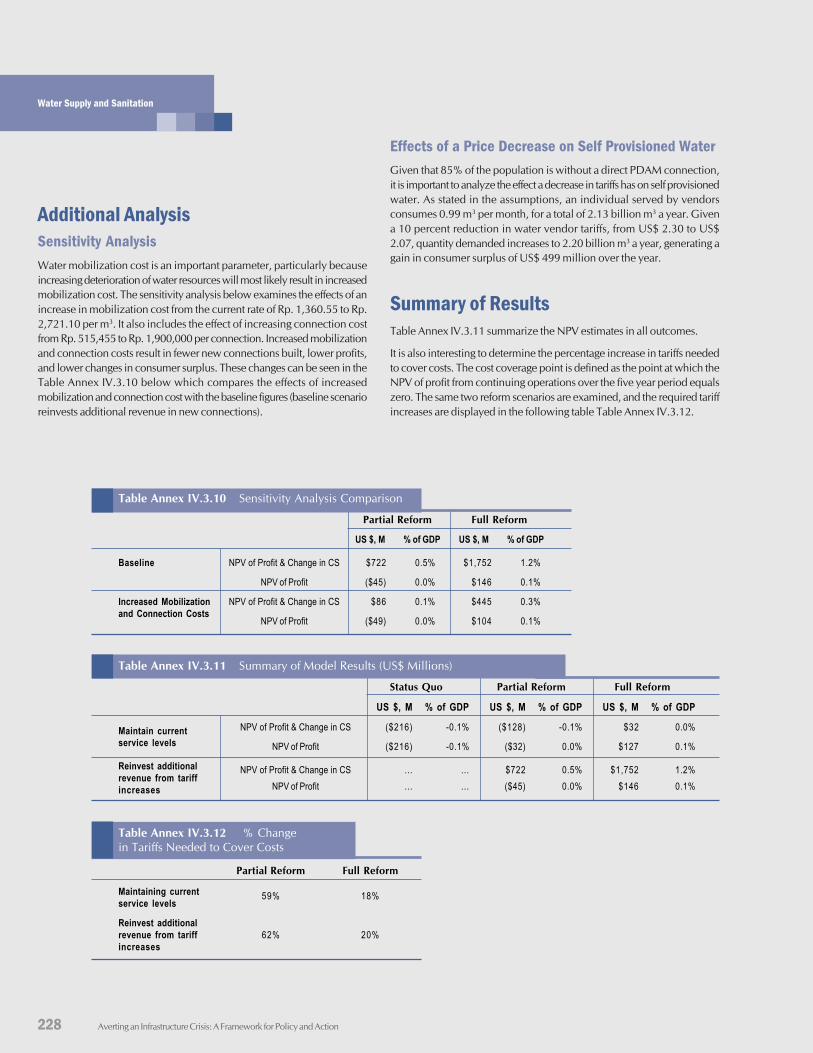

Table IV.1. Estimated distribution in urban areas 197Table IV.2. Estimated distribution in rural areas 197Table IV.3. Coverage Statistics for PERPAMSI Member PDAMs 197Table IV.4. Sewerage Coverage 204Table IV.5. The Way Forward - WATER 214Table IV.6. The Way Forward – SANITATION 215Table Annex IV.1.01.Legislation relevant to water supply

and sanitation service provision 216Table Annex IV.2.01.Water Supply 217Table Annex IV.2.02.Sewerage 217Table Annex IV.6.01.Summary of Model Results (US$ Millions) 224Table Annex IV.6.02.% Change in Tariffs Needed to Cover Costs 224Table Annex IV.6.03. Inputs and Assumptions 225Table Annex IV.6.04.Model Outcomes 226Table Annex IV.6.05.Scenario 1 - Status Quo:

Maintain current service level 227Table Annex IV.6.06.Scenario 2 - Partial Reform:

Maintain current service level 227Table Annex IV.6.07.Scenario 2 - Partial Reform: Reinvest

additional revenue to expand access 227Table Annex IV.6.08.Scenario 3 - Full Reform:

Maintain current service level 227Table Annex IV.6.09.Scenario 3 - Full Reform: Reinvest

additional revenue to expand access 227Table Annex IV.6.10.Sensitivity Analysis Comparison 228Table Annex IV.6.11.Summary of Model Results (US$ Millions) 228Table Annex IV.6.12.% Change in Tariffs Needed to Cover Costs 228

List of Text BoxesBox I.1. Integrating Captive Power Plants (CPPs) in the

Power Sector 127Box I.2. What About Using Captive Power to Increase

Reliability? 135Box I.3. Indonesia IPP Debacle 136

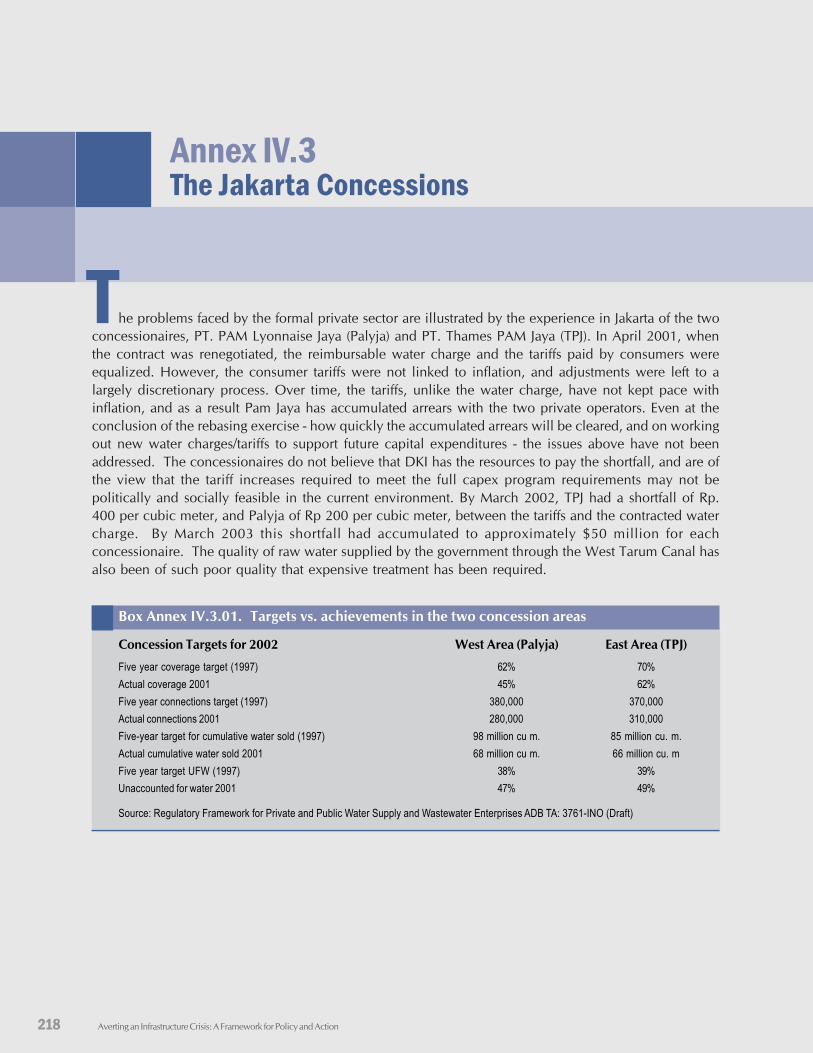

Box Annex IV.3.01. Targets vs. achievements in the twoconcession areas 218

Table of Content

Averting an Infrastructure Crisis:A Framework for Policy and Actionov

ervi

ew

1

Indonesia is turning a corner, from crisis management towards growth.For the first time, after the crisis, Indonesia is able to focus on longer-termdevelopment policies. Reversing the trend of deteriorating infrastructureis one of the top priorities. How did Indonesia, a country that hadsuccessfully used infrastructure development as a path out of poverty andtowards economic growth, find itself struggling in almost everyinfrastructure sector? Infrastructure played a key role in driving growthand poverty reduction in the 30 years prior to the 1997 crisis. But followingthe crisis, the government had to focus on fixing more immediate problemssuch as currency devaluation, capital flight, and an unstable political andsocial environment. The government had to reduce development spending,and infrastructure suffered across the board. Indonesia’s infrastructurequality ranks among the lowest in the region and is affecting growth, povertyreduction, foreign investment, and the environment.

Indonesia has recovered from the crisis, and the government is wellpositioned to refocus on infrastructure. Recent progress – such as fiscalconsolidation, political stability, and some improvement of the regulatoryframework – sets the stage for Indonesia to move beyond the currentinfrastructure impasse. To avert a major infrastructure crisis, further actionis urgent. Additional infrastructure investments of about 2% of GDP arerequired in the short and medium-term. But additional spending alone isnot enough, the government will also have to address the longer termissues of improving public management, the regulatory environment, andworking out the complications from decentralization.

Public infrastructure invest-ment has dropped sharplysince the crisis — from $8billion USD in 1994, to $1.5billion in 2002.

2

Averting an Infrastructure Crisis:A Framework for Policyand Action

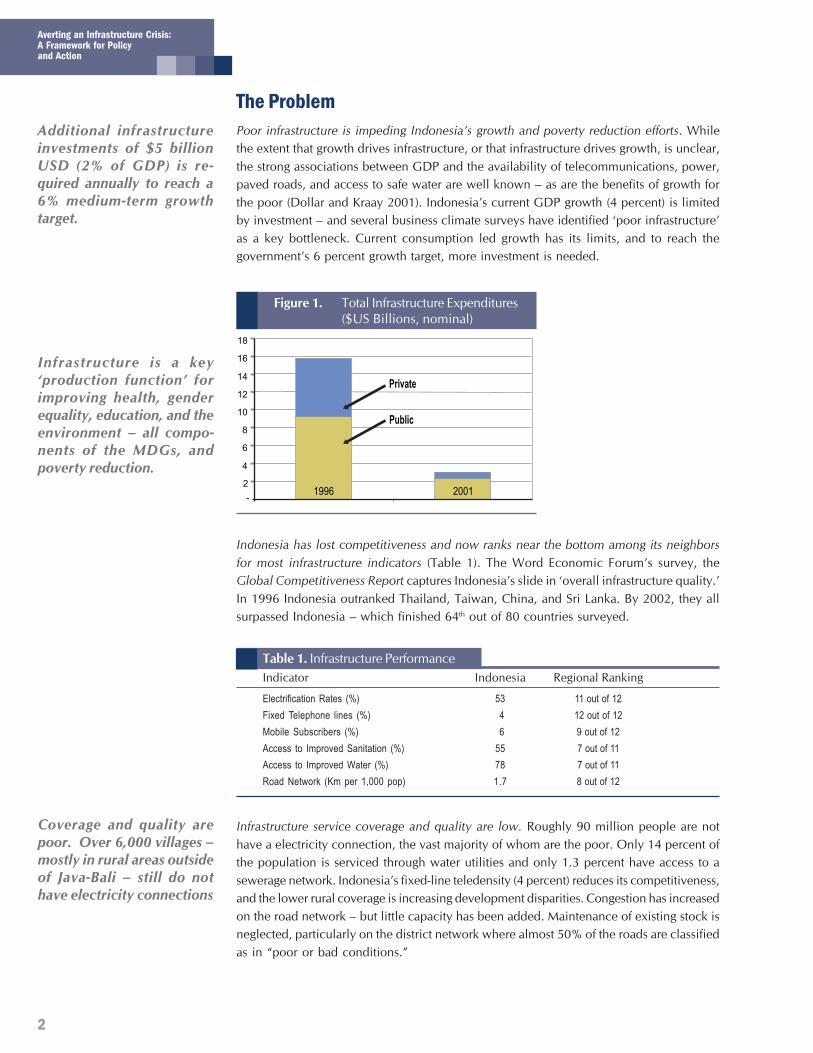

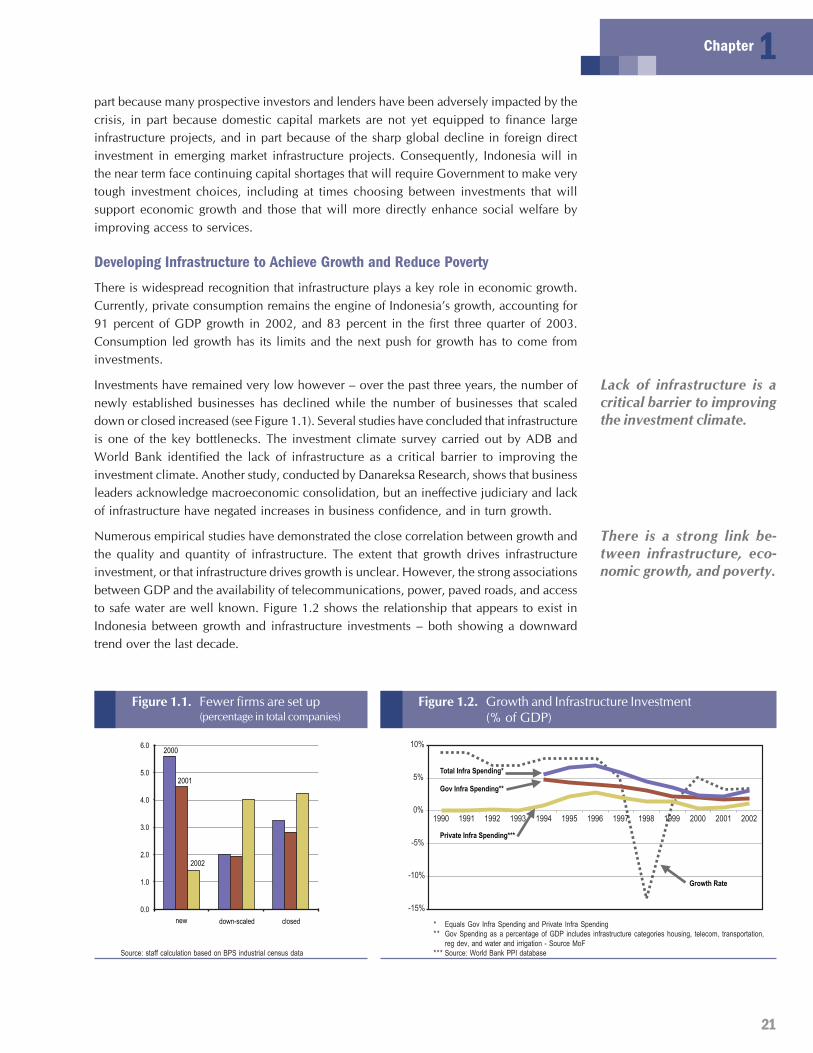

The ProblemPoor infrastructure is impeding Indonesia’s growth and poverty reduction efforts. Whilethe extent that growth drives infrastructure, or that infrastructure drives growth, is unclear,the strong associations between GDP and the availability of telecommunications, power,paved roads, and access to safe water are well known – as are the benefits of growth forthe poor (Dollar and Kraay 2001). Indonesia’s current GDP growth (4 percent) is limitedby investment – and several business climate surveys have identified ‘poor infrastructure’as a key bottleneck. Current consumption led growth has its limits, and to reach thegovernment’s 6 percent growth target, more investment is needed.

Infrastructure is a key‘production function’ forimproving health, genderequality, education, and theenvironment – all compo-nents of the MDGs, andpoverty reduction.

Figure 1. Total Infrastructure Expenditures($US Billions, nominal)

-

2

4

6

8

10

12

14

16

18

1996 2001

Private

Public

Indonesia has lost competitiveness and now ranks near the bottom among its neighborsfor most infrastructure indicators (Table 1). The Word Economic Forum’s survey, theGlobal Competitiveness Report captures Indonesia’s slide in ‘overall infrastructure quality.’In 1996 Indonesia outranked Thailand, Taiwan, China, and Sri Lanka. By 2002, they allsurpassed Indonesia – which finished 64th out of 80 countries surveyed.

Table 1. Infrastructure PerformanceIndicator Indonesia Regional Ranking

Electrification Rates (%) 53 11 out of 12Fixed Telephone lines (%) 4 12 out of 12Mobile Subscribers (%) 6 9 out of 12Access to Improved Sanitation (%) 55 7 out of 11Access to Improved Water (%) 78 7 out of 11Road Network (Km per 1,000 pop) 1.7 8 out of 12

Infrastructure service coverage and quality are low. Roughly 90 million people are nothave a electricity connection, the vast majority of whom are the poor. Only 14 percent ofthe population is serviced through water utilities and only 1.3 percent have access to asewerage network. Indonesia’s fixed-line teledensity (4 percent) reduces its competitiveness,and the lower rural coverage is increasing development disparities. Congestion has increasedon the road network – but little capacity has been added. Maintenance of existing stock isneglected, particularly on the district network where almost 50% of the roads are classifiedas in “poor or bad conditions.”

Additional infrastructureinvestments of $5 billionUSD (2% of GDP) is re-quired annually to reach a6% medium-term growthtarget.

Coverage and quality arepoor. Over 6,000 villages –mostly in rural areas outsideof Java-Bali – still do nothave electricity connections

3

Overview

Table 2. Sector Issues

Water and Sanitation Telecommunications

• Water access is low – 22% of the population do not • Fixed line access is the lowest in the region –have access to “improved” water, and only 14% only 4% of the population, mostly in urban areas,are connected to PDAMs is covered

• Sanitation service is lacking – only 1.3% of the • Massive investment is needed, but funding ispopulation are reached by a sewerage network a challenge – raising teledensity 1% will cost •

• PDAMs are struggling – over 2/3 operate in the $330 millionred, unaccounted for water is over 40%, and • The mobile sector continues to expand,tariffs are well below costs averaging 77% annual growth since 1995

Power Roads and Road Transport

• Access is low - 43% of population is without power • Spending has declined – from 22% of the national(roughly 90 million people, of which 90% are poor) development budget in 1993, to 11% in 2000

• Connection costs are 33% higher in rural areas • Maintenance is lacking – the proportion of road• Investment needs are high – an estimated budget for maintenance reduced from 30% to

US $15-17 billion is required before 2012 for below 10% from 1985 to 2000an additional 9,700 MW of capacity, expanded • Congestion is a problem – significant capacitytransmission, and distribution for 1.6 million expansion is needed, but little has been added,connections annually and urbanization trends will only increase the

problem

Infrastructure is critical to support rapid urbanization trends. More than 60 million people(from 80 million in 2000 to 140 million in 2020) will be added to Indonesia’s urbanpopulation in the next two decades. The primary urban areas in the country already sufferfrom lack of clean water, sanitation and adequate urban transportation. Yet, urban areasare the key drivers of the economy – contributing 70 percent of non-oil. Additionally,providing basic services to the large numbers of urban poor (over 13 million were belowthe poverty line in 2002) must be a focus of Indonesia’s poverty reduction strategy.

Poor infrastructure has reduced the quality of life and the environment. The lack of seweragesystems and solid waste facilities have caused widespread contamination of surface andground water, as well as the destruction of sensitive eco-systems. During the dry season,10% of the river flow of the Brantas river (the direct source of Surabaya’s water supply)consist of untreated industrial wastewater. Further, about half of Surabaya’s solid wasteand most of the human waste are dumped into the river. These conditions are commonthroughout Indonesia, and are the prime reason Indonesia has the highest incidence oftyphoid in East Asia.

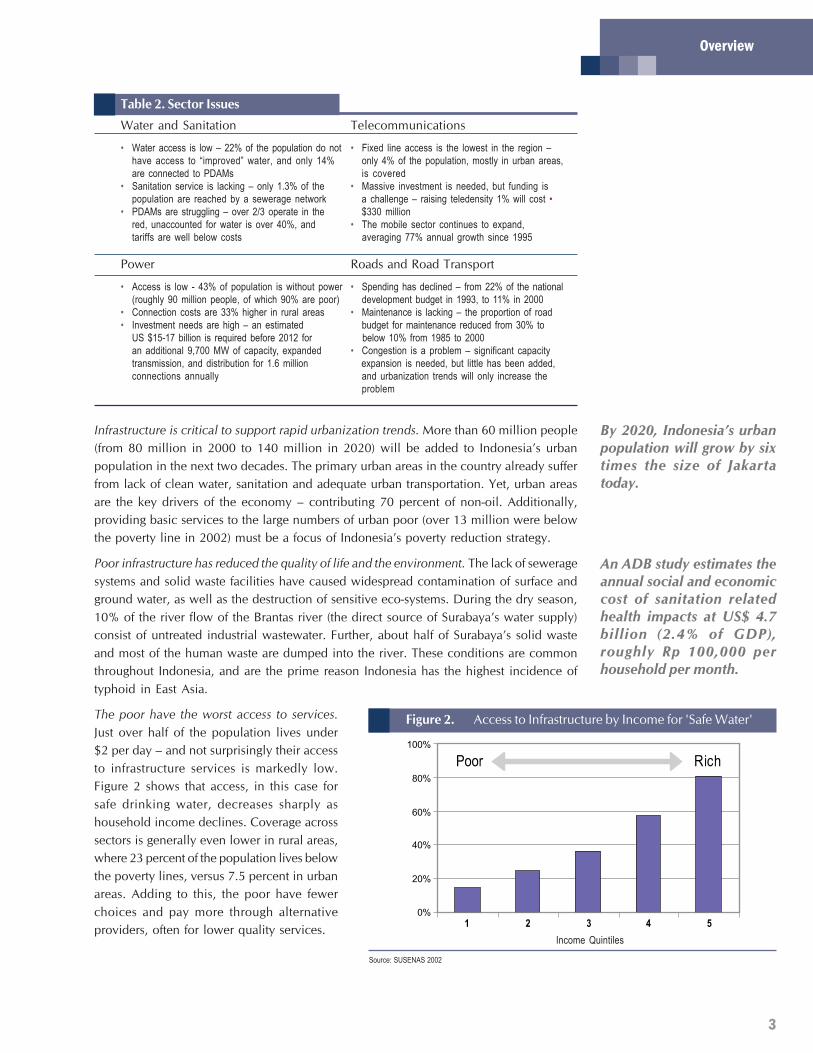

The poor have the worst access to services.Just over half of the population lives under$2 per day – and not surprisingly their accessto infrastructure services is markedly low.Figure 2 shows that access, in this case forsafe drinking water, decreases sharply ashousehold income declines. Coverage acrosssectors is generally even lower in rural areas,where 23 percent of the population lives belowthe poverty lines, versus 7.5 percent in urbanareas. Adding to this, the poor have fewerchoices and pay more through alternativeproviders, often for lower quality services.

By 2020, Indonesia’s urbanpopulation will grow by sixtimes the size of Jakartatoday.

0%

20%

40%

60%

80%

100%

1 2 3 4 5

Figure 2. Access to Infrastructure by Income for 'Safe Water'

Income Quintiles

Source: SUSENAS 2002

An ADB study estimates theannual social and economiccost of sanitation relatedhealth impacts at US$ 4.7billion (2.4% of GDP),roughly Rp 100,000 perhousehold per month.

4

Averting an Infrastructure Crisis:A Framework for Policyand Action

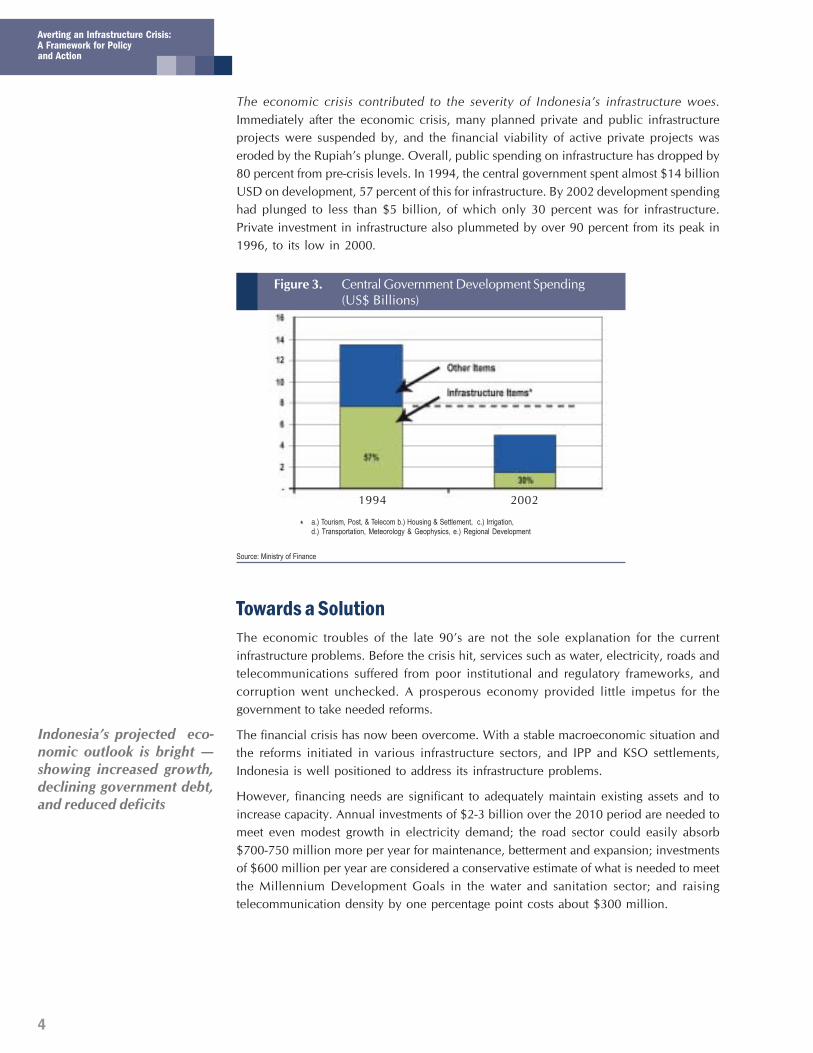

The economic crisis contributed to the severity of Indonesia’s infrastructure woes.Immediately after the economic crisis, many planned private and public infrastructureprojects were suspended by, and the financial viability of active private projects waseroded by the Rupiah’s plunge. Overall, public spending on infrastructure has dropped by80 percent from pre-crisis levels. In 1994, the central government spent almost $14 billionUSD on development, 57 percent of this for infrastructure. By 2002 development spendinghad plunged to less than $5 billion, of which only 30 percent was for infrastructure.Private investment in infrastructure also plummeted by over 90 percent from its peak in1996, to its low in 2000.

Figure 3. Central Government Development Spending(US$ Billions)

* a.) Tourism, Post, & Telecom b.) Housing & Settlement, c.) Irrigation,d.) Transportation, Meteorology & Geophysics, e.) Regional Development

Source: Ministry of Finance

1994 2002

Towards a SolutionThe economic troubles of the late 90’s are not the sole explanation for the currentinfrastructure problems. Before the crisis hit, services such as water, electricity, roads andtelecommunications suffered from poor institutional and regulatory frameworks, andcorruption went unchecked. A prosperous economy provided little impetus for thegovernment to take needed reforms.

The financial crisis has now been overcome. With a stable macroeconomic situation andthe reforms initiated in various infrastructure sectors, and IPP and KSO settlements,Indonesia is well positioned to address its infrastructure problems.

However, financing needs are significant to adequately maintain existing assets and toincrease capacity. Annual investments of $2-3 billion over the 2010 period are needed tomeet even modest growth in electricity demand; the road sector could easily absorb$700-750 million more per year for maintenance, betterment and expansion; investmentsof $600 million per year are considered a conservative estimate of what is needed to meetthe Millennium Development Goals in the water and sanitation sector; and raisingtelecommunication density by one percentage point costs about $300 million.

Indonesia’s projected eco-nomic outlook is bright —showing increased growth,declining government debt,and reduced deficits

5

Overview

Infrastructure has been an integral part of the agenda for policy makers in the past fewyears. This has resulted in various reform initiatives, including the following:

• a modern electricity law was adopted in 2002, implementing regulations have beenprepared, electricity tariffs have been increased substantially, and contentious issueswith the Independent Power Producers have been settled;

• a new oil and natural gas law was passed, that introduced downstream competitionand market pricing;

• the water sector has seen progress in implementing a debt work out program tostrengthening PDAMs’ finances; and

• in telecommunications, a new law adopted in 1999 paved the way for the progressiveintroduction of competition in all market segments, and dramatic growth in thenumber mobile subscribers since 1997 has been accompanied by solid increases inthe number of fixed lines in service, public payphones, teleshops, and internet shops.

Despite the significance of the reforms, the resulting overall impact has been rather limited.A key impediment is the lack of an overall government strategy for infrastructure andpredictable policies in these critical infrastructure sectors. For example, most of the keylaws that were passed still do not have implementing regulations. In addition, credibilityof public policies from the point of view of the private investors remains historically low.

6

Averting an Infrastructure Crisis:A Framework for Policyand Action

Indonesia must address the various facets of this policy-credibility issue in order to attractthe financial resources that its infrastructure sectors currently lack. In particular, moreefficient management of public infrastructure assets will help contain costs and optimizeuse of public funds; with progressive implementation of cost-covering tariffs, internallygenerated funds could be made available for investment; and an overall environmentmore conducive to private participation would help rekindle the interest of private financiersfor Indonesian infrastructure. Such reforms will take time, however, and a substantialfinancing gap is likely to remain. In order to fill this gap, government spending oninfrastructure will have to increase. In addition, steps can be taken to promote greatermobilization of domestic savings for infrastructure investment, and better targeting ofpublic resources towards the poor.

Need for Action on Multiple FrontsImproving Public Management of InfrastructureMost of Indonesia’s infrastructure is still developed and managed by the public sector,and this will remain the case for some time to come. Hence, better public managementof infrastructure will have by far the most positive impact. However, the role played bythe public sector will change in three major ways. First, Indonesia has moved tocommercialize and corporatize delivery and management of key public infrastructure,hence, the role is changing from provision to regulation (discussed in the next section).Second, Indonesia has launched an ambitious decentralization program that has transferredmany responsibilities relating to infrastructure provision to sub-national entities. Third,and in part as a consequence of the above two changes, the role of central agencies withrespect to infrastructure is evolving, thus requiring the Government to rethink how itcoordinates policy and strategic planning.

Rethinking the Role of Central Authorities

In the road sector, for example, what is needed is an effective National Roads Strategy. Astrategy that is understood by all, with a clear financing plan, clear articulation ofresponsibilities, clear links between planning, new investments, management of use andmaintenance, and a clear path ahead for capacity building and institutional reform. To dothis, the central government will have to quickly readjust its role to the post decentralizationenvironment. In addition to decentralization, many government agencies will now haveto move from being a service provider to a facilitator, as greater corporitization andprivatization is introduced. Emphasis is needed on policy formulation and support tolocal authorities rather than on design and implementation of civil works, or on directprovision of services. These new functions need to be defined with precision for each ofthe main sector ministries, and organizational structures and staffing needs will need tobe reviewed accordingly.

Indonesia also faces the challenge of redefining its mechanisms for coordinating policyand strategy for infrastructure development in an environment with more dispersed roles.In the past, Bappenas prepared the national five-year development plans and, along withthe Coordinating Ministry for the Economy and Industry (EKUIN), also coordinatedIndonesia’s policy development and reform initiatives. Currently, Bappenas, whose powersare now more circumscribed, functions as a planning advisor for those committees, andthe Coordinating Ministry of Economic Affairs (EKUIN’s successor) focuses more on short

Today, responsibilities forinfrastructure provision andoperating decisions arewidely dispersed between aproliferation of special pur-pose coordination commit-tees – several of which haveoverlapping roles.

7

Overview

term implementation matters. A key challenge for Indonesia is to craft a framework forcoordinating policy and strategic planning in an environment with a much wider dispersionof responsibilities than in the past.

Making Decentralization Work

In 2001, Indonesia launched a “big bang” decentralization program. The legislative andregulatory provisions needed to implement such a program are still incomplete. In theinfrastructure sectors, decentralization has created uncertainty as to which level ofgovernment is responsible for the provision of various services. The situation is exacerbatedby the fact that some decentralization implementing regulations are inconsistent withothers, as well as with existing national sector regulations. Capacity within the localgovernments also needs to be developed so that they can effectively provide servicescommensurate with their new responsibilities.

The way in which financial resources have so far been transferred to decentralized authoritiesis unsatisfactory. First, the current allocation of resources between regions tends toexacerbate rather than reduce regional inequalities. Modifying the current allocation ofresources is political and difficult – but in the present situation, many poorer regionsreceive just enough to pay wages and are left with little funding for infrastructure or othertypes of expenditures. In addition, the central government lacks instruments to promotethe pursuit of national objectives by local authorities. Funds available for matching grantschemes are very limited. In addition, at present two distinct matching grant mechanisms,with different application and evaluation criteria, and different terms and conditions arein use, these need to be harmonized. Finally, the current framework for regional governmentborrowing is unduly restrictive. Local governments should be encouraged to borrow fromthe market. This will require, among others, modern financial management at the locallevel and institutions that can rate local government credit worthiness. This is muchneeded, as constraints on financial transfers from the center and on borrowing opportunitieshave already led some regional governments to impose arbitrary fees and taxes that tendto introduce economic distortions and conflict with national legislation.

Box 1. Taking action – on Public Management• The role, organization and staffing of main sector ministries need to reflect the new decentralized environment.

Overall policy planning and coordination functions also need to be strengthened.• The government needs to expand its efforts to operate on a commercial basis. PDAMs especially need

attention to be more transparent, and to operate more autonomously from local governments.• UU22/1999 and earlier sector laws should be amended to better define the role and responsibilities

between the levels of government, and for infrastructure provision. The provinces need to be empoweredto play a much stronger coordinating role vis-à-vis municipalities.

• Procedures for on-lending of foreign loans need to be streamlined by amending KMK.35. (the policy thatgoverns local borrowing) The current bottom-up process is complex, and has the potential to impede thechanneling of funds for urgent and justified infrastructure at the sub-national level.

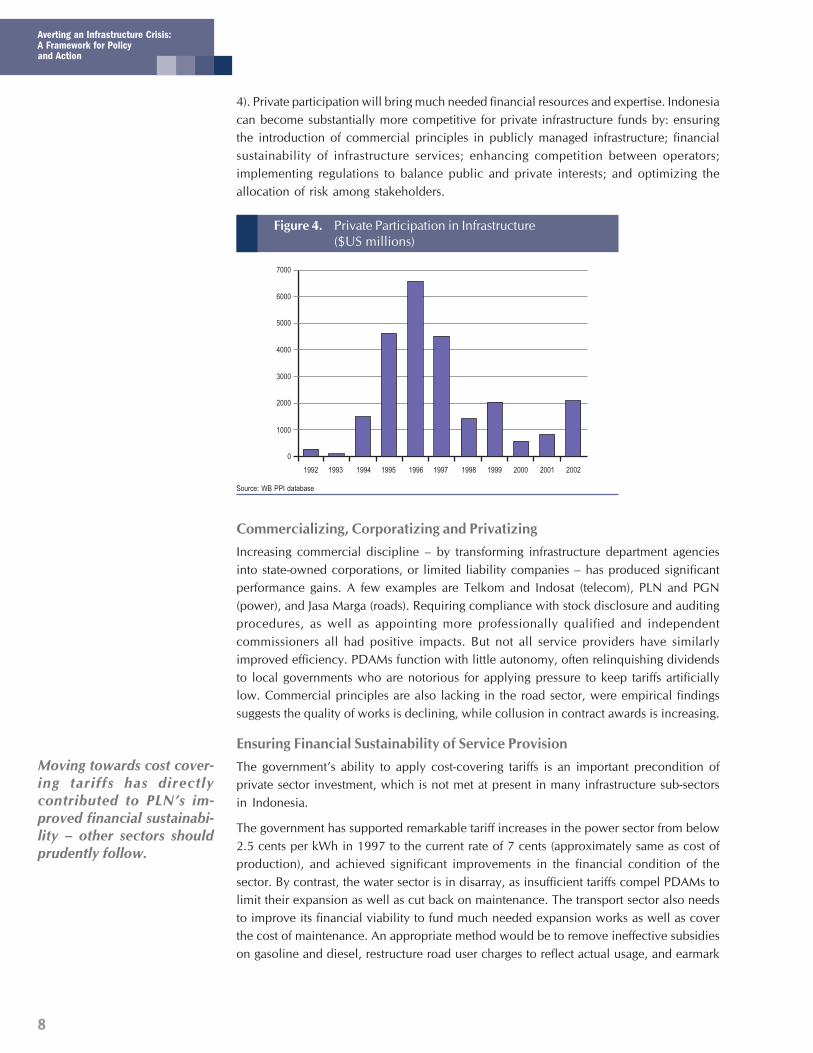

Restoring Private ParticipationIndonesia needs to mobilize private investments for infrastructure if it wants to rapidlyimprove service coverage, maintain international competitiveness, and support theexpanding economy. There has been a substantial decline in private participation ininfrastructure in Indonesia after a dramatic increase in the first half of the 1990’s, (Figure

Coordinating between the400 local governments andmunicipalities will necessi-tate empowering provincialgovernments to have alarger role.

Decentralization has exacer-bated regional inequalities –budget receipts per capitafor rich regions are 30 timeshigher than the poorest re-gions.

8

Averting an Infrastructure Crisis:A Framework for Policyand Action

4). Private participation will bring much needed financial resources and expertise. Indonesiacan become substantially more competitive for private infrastructure funds by: ensuringthe introduction of commercial principles in publicly managed infrastructure; financialsustainability of infrastructure services; enhancing competition between operators;implementing regulations to balance public and private interests; and optimizing theallocation of risk among stakeholders.

Commercializing, Corporatizing and PrivatizingIncreasing commercial discipline – by transforming infrastructure department agenciesinto state-owned corporations, or limited liability companies – has produced significantperformance gains. A few examples are Telkom and Indosat (telecom), PLN and PGN(power), and Jasa Marga (roads). Requiring compliance with stock disclosure and auditingprocedures, as well as appointing more professionally qualified and independentcommissioners all had positive impacts. But not all service providers have similarlyimproved efficiency. PDAMs function with little autonomy, often relinquishing dividendsto local governments who are notorious for applying pressure to keep tariffs artificiallylow. Commercial principles are also lacking in the road sector, were empirical findingssuggests the quality of works is declining, while collusion in contract awards is increasing.

Ensuring Financial Sustainability of Service ProvisionThe government’s ability to apply cost-covering tariffs is an important precondition ofprivate sector investment, which is not met at present in many infrastructure sub-sectorsin Indonesia.

The government has supported remarkable tariff increases in the power sector from below2.5 cents per kWh in 1997 to the current rate of 7 cents (approximately same as cost ofproduction), and achieved significant improvements in the financial condition of thesector. By contrast, the water sector is in disarray, as insufficient tariffs compel PDAMs tolimit their expansion as well as cut back on maintenance. The transport sector also needsto improve its financial viability to fund much needed expansion works as well as coverthe cost of maintenance. An appropriate method would be to remove ineffective subsidieson gasoline and diesel, restructure road user charges to reflect actual usage, and earmark

Moving towards cost cover-ing tariffs has directlycontributed to PLN’s im-proved financial sustainabi-lity – other sectors shouldprudently follow.

Figure 4. Private Participation in Infrastructure($US millions)

Source: WB PPI database

7000

6000

5000

4000

3000

2000

1000

0

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

9

Overview

these funds to cover sector expenditures. Charges for international telecommunicationsare expected to decrease due to enhanced competition in the sector but the price of localcalls are currently below costs and will have to rise in the future. It is important that anyfuture tariff increases in infrastructure sectors be phased in cautiously with correspondingimprovements in services. Ensuring social acceptance of these reforms, where the rationaleand timing are clearly articulated to the public, is also critical for the long-term success inthe sector.

Maximizing Competition

Indonesia has not fully taken advantage of the benefits of competition, yet the intensity ofcompetitive pressures is one of the most important determinants of performance ininfrastructure service provision. The scope for ‘head to head’ competition in the market –where consumers can choose their supplier, and suppliers compete to serve them – varies.However, the one market where competition is easily feasible, telecommunication, it hasbeen postponed. Similarly in power, Indonesia Power and PLN continue to operate moreas partners than head-to-head competitors. Consequently, power is more costly than itwould be with competition. Indonesia’s new 2002 electric power law does howeverrecognize the potential for competition in generation and supply, and provides for itsprogressive introduction on a regional basis.

When direct, head-to-head competition is not feasible, competition for the market (e.g.franchise bidding) can be used to select operators. However, numerous opportunitieshave been lost in Indonesia: water supply concessions have been awarded through directnegotiations; numerous unsolicited IPP projects were also negotiated quickly and non-transparently; and the same practices are widespread in the toll road sector. The cost forthe Indonesian economy has been enormous – when a number of IPP projects werefinally competitively tendered, the offered tariff was well below the previously negotiatedone for similar projects.

Finally, competitive discipline can be derived from yardstick competition, wherebyregulators use comparative performance data from other similar enterprises to regulatemonopoly network industries. This is a tool that has been used effectively by variouscountries, especially in sectors characterized by the existence of multiple operators holdingmonopolistic positions in different regions. Some fragmented efforts have been made inIndonesia to introduce yardstick competition in the water distribution sector, but muchmore systematic efforts should be undertaken in that sector and elsewhere.

Establishing Adequate Regulation

Sound regulation is needed for private participation as it promotes economic efficiency,fosters innovation, and creates incentive for system expansion. A credible regulatory body,however, needs autonomy and independence to perform its function. This can be achievedby providing regulators with distinct statutory authority, appointing them for fixed-terms,preventing their removal except in predefined circumstances, and providing funding throughlevies on the regulated industry.

Indonesia is at an early stage in developing its regulatory agencies and more effort isneeded to develop adequate, independent regulatory bodies. To move forward, thegovernment must appoint the regulators, issue and implement the regulations stated inthe laws, and provide these agencies with adequate resources so that they can begin toestablish a track record. Regulation by contract will have to be the norm in the interim.

Indonesia’s mobile phonemarket is the best example ofcompetitiveness (and conse-quently private investment),and consumers have bene-fited from better technology,more choices, and lowerprices.

Laws have been passed inboth the telecommunicationand energy sector that ena-bles the creation of regula-tory entities.

10

Averting an Infrastructure Crisis:A Framework for Policyand Action

Allocating and Managing Risk

Rewards for investors are commensurate with risks – but Indonesia’s reputation as acountry, filled with red tape, a weak judicial system, arbitrary taxes, and corruption hasmade many investors reluctant to invest. Their reluctance also stems from political andeconomic events beyond their control. But if these services were to be provided by thepublic sector instead, the government would, in fact, be implicitly bearing all of the risks.Therefore, the government should develop a framework for identifying and assessing variousinvestment risks, and a methodology to help determine which are acceptable to undertake.Involving the Ministry of Finance in this process would also better ensure that the expectedfiscal exposure of risk sharing arrangements are properly evaluated and financially feasible.

Box 2. Taking action – on Restoring Private Participation• Amendments to Keppres 7 (or a similar regulation) need to be completed, and supplemented with a sound

policy framework on public support for private projects, including a framework for realistic risk allocationbetween public and private sector.

• Develop a comprehensive plan to restore tariffs to cost-reflective levels, and improve on socializing tariffchanges to the public.

• Develop sector-by-sector plans for restructuring and promoting competition – with the adoption of competitivetendering as the norm for all PPI projects, and benchmarking mainstreamed as a means to pressure localmonopolies

Tackling CorruptionCorruption remains pervasive in Indonesia, and despite the government’s attempts toaddress the issue, little progress has been made. The post-Soeharto and post-decentralizationenvironment is often perceived to have made matters worse, as corruption is more diffused,and even “less effective” in producing intended results. Corruption is a major factordetermining investor confidence. Indonesia’s ranking, well below its neighbors (China,Thailand, Philippines, and Vietnam) in Transparency International’s Corruption PerceptionIndex (CPI), illuminates some of the reasons for its lagging investment climate.

Infrastructure presents ‘opportunities’ for rent seekers at every stage, from projectidentification and negotiation, to implementation and operation. The results are costly–a significant amount of public funds are lost annually through corrupt procurement practicesin Indonesia. Eliminating corruption requires fundamental changes in the accountabilityframework that will take considerable time to design and implement. However, there aresignificant opportunities for reducing corruption in the infrastructure sectors in the shortterm – these require limiting rent-seeking opportunities, improving detection, increasingthe consequences of being caught, and creating incentives for non-corrupt behavior.

Box 3. taking action – on Tackling Corruption• Considerable effort has gone into improved procurement regulations for central and regional government

by replacing Keppres 18/2000 with Keppres 80/2003. The new regulation establishes an Institution forDevelopment of Public Procurement Policy (LPKPP), requires procurement certification for bid committees,removes pre-qualification for contracts below $6 million, and introduces ‘integrity pacts’ for suppliers andcontractors. Keppres 80 a positive step – but the government needs to work out the many unresolveddetails to ensure implementation and enforcement are carried through.

• The revision to Kepress 7/1998 on Public Private Partnerships for Infrastructure Provision is overdue. Thisis needed to improve guidelines for project identification and more transparent and competitive solicitationof private partners.

Indonesia ranked 138th outof 146 countries in the 2002World Investment Report forForeign Direct Investment.

Indonesia ranked 122 out of133 countries on the Cor-ruption Perception Index(CPI)

But curbing corruption is notimpossible – by increasingcompetition with improvedcomplaint mechanisms andadvertising, a recent WorldBank infrastructure projectin Bali has saved almost 20%of the government owner’sestimate in procurement.

11

Overview

Mobilizing Finance for InfrastructureThe reforms discussed above will help address, to some extent, the lack of financing thatcurrently affects the provision of infrastructure. Cost covering tariffs, in particular, areultimately key to ensure financial sustainability. But all such reforms will take time andthere will therefore remain, a significant financing gap. This can, in part, be filled fromthree sources: increased government spending, greater mobilization of domestic savings,and better targeting of public resources towards the poor.

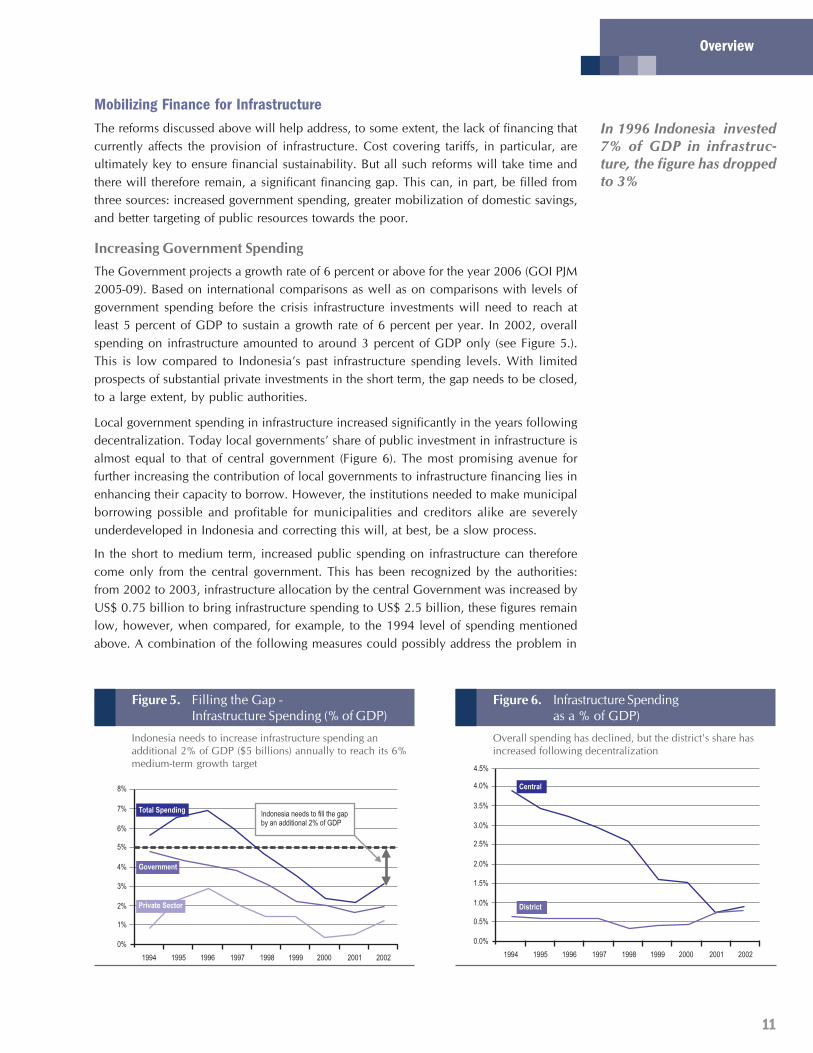

Increasing Government SpendingThe Government projects a growth rate of 6 percent or above for the year 2006 (GOI PJM2005-09). Based on international comparisons as well as on comparisons with levels ofgovernment spending before the crisis infrastructure investments will need to reach atleast 5 percent of GDP to sustain a growth rate of 6 percent per year. In 2002, overallspending on infrastructure amounted to around 3 percent of GDP only (see Figure 5.).This is low compared to Indonesia’s past infrastructure spending levels. With limitedprospects of substantial private investments in the short term, the gap needs to be closed,to a large extent, by public authorities.

Local government spending in infrastructure increased significantly in the years followingdecentralization. Today local governments’ share of public investment in infrastructure isalmost equal to that of central government (Figure 6). The most promising avenue forfurther increasing the contribution of local governments to infrastructure financing lies inenhancing their capacity to borrow. However, the institutions needed to make municipalborrowing possible and profitable for municipalities and creditors alike are severelyunderdeveloped in Indonesia and correcting this will, at best, be a slow process.

In the short to medium term, increased public spending on infrastructure can thereforecome only from the central government. This has been recognized by the authorities:from 2002 to 2003, infrastructure allocation by the central Government was increased byUS$ 0.75 billion to bring infrastructure spending to US$ 2.5 billion, these figures remainlow, however, when compared, for example, to the 1994 level of spending mentionedabove. A combination of the following measures could possibly address the problem in

In 1996 Indonesia invested7% of GDP in infrastruc-ture, the figure has droppedto 3%

Figure 5. Filling the Gap -Infrastructure Spending (% of GDP)

Indonesia needs to increase infrastructure spending anadditional 2% of GDP ($5 billions) annually to reach its 6%medium-term growth target

6%

5%

4%

3%

2%

1%

0%

1994 1995 1996 1997 1998 1999 2000 2001 2002

7%

8%

Total Spending

Government

Private Sector

Indonesia needs to fill the gapby an additional 2% of GDP

Figure 6. Infrastructure Spendingas a % of GDP)

Overall spending has declined, but the district's share hasincreased following decentralization

3.0%

2.5%

2.0%

1.5%

1.0%

0.5%

0.0%

1994 1995 1996 1997 1998 1999 2000 2001 2002

3.5%

4.0% Central

4.5%

District

12

Averting an Infrastructure Crisis:A Framework for Policyand Action

the medium term. First, the central government needs to increase its overall revenueenvelope, especially through increased compliance. Second, existing allocation in non-performing sectors could be directed towards infrastructure (for example, various fuelsubsidies account for nearly 2 percent of GDP). Finally, the impressive fiscal consolidationof the last few years has created some space for increased borrowing. Indonesia’s debt toGDP ratio is steadily decreasing and the deficit has been kept to a bare minimum. Thisdiscipline has resulted in upgrades by investment rating agencies. Government can borrowat below 7 percent in the market today and, as discussed in the next section, the domesticmarket is relatively un-tapped for infrastructure related borrowing. However, beforeborrowing from the market, the Government should maximize the use of cheaper donorfunds first.

Mobilizing Domestic FinanceDomestic funds are the key to the long-term health of infrastructure finance. Three largeretirement funds (for police and defense personnel, for civil servants, and for employeesin the private sector and in SOEs), several hundreds of funds established by individualemployers for their employees and the life insurance sector have combined assets ofabout Rp. 100 trillion contributed by almost 26 million participants.

Various steps can be taken to increase the flow of domestic fund to infrastructure.International experience shows that contractual savings institutions, notably pensionschemes (which are allowed to invest in non-governmental assets) are essential instrumentsto channel domestic savings into infrastructure financing. Pension funds and insurancecompanies have long-lived liabilities denominated in local currency, making themparticularly suited for investing in infrastructure instruments that provide returns in local

13

Overview

currency over long periods of time. The Indonesian Government should therefore considermodification of the investment regulations that govern institutions such as the pensionfunds and insurance firms in order to enable such institutions to invest in infrastructuresecurities. It cannot be overemphasized, however, that an attractive investment climatefor infrastructure is a precondition for tapping domestic capital markets; institutionalreform in the capital markets alone will achieve little. It is also absolutely crucial thatfund managers have incentives – and be free to – make investment decisions on the basisof commercial rather than political considerations.

To develop products that these funds can invest in, the central Government may considerusing public resources to strengthen the capacity of sub-national entities – especiallymunicipalities – to borrow on the local markets. The Government of Colombia, forexample, created a municipal finance institution, Findeter, designed to promote longterm lending from commercial banks to municipalities. A bank that made a long termloan to a municipality can borrow from Findeter up to 85 percent of the loan at subsidizedrates. This facilitates access by municipalities to commercial loans while relying on theproject appraisal skills of commercial banks (banks are liable to Findeter if their borrowersdefault). To the extent possible, government schemes for municipal finance should involvethe financial sector in allocating credit and sharing risk. This in turn requires that localbanks possess sufficient capacity in assessing the expected returns of projects. Finally,municipal finance schemes can only be viable if municipalities have a positive and roughlypredictable revenue stream through taxes, services charge, ect.

To bring together supply and demand, the Government will have to focus on creating orupgrading certain aspects of financial market infrastructure. Establishing a sound governmentbond market – in which sovereign issues in domestic currency of various maturities areissued at predictable regular intervals is another important aspect of market infrastructure:a well functioning government debt market allows the creation of benchmark bond priceswhich would then form the basis on which instruments of different risks can be priced.Lastly, a sound legal framework and credible dispute resolution mechanisms are key toattracting long-term investments from private sources.

Protecting the PoorCross-subsidization between users of infrastructure services is very common in Indonesia.However, current cross-subsidization schemes in Indonesia present major drawbacks;

• they are not well targeted at the poor and tend to subsidize the already low variableconsumption costs of existing users while the poor often have no access to the service;

• they entail rather large resource transfers and therefore introduce important allocationdistortions,

• and they force a given service provider to operate transfers between different categoriesof its own users, therefore requiring that monopolistic arrangements be maintained toprevent new entrants from “stealing” the customers who are currently over-chargedand who provide the source of the cross-subsidies.

Cross-subsidization schemes should be better targeted at the truly poor – e.g. existingusers could contribute part of the costs of expanding the system to reach new users. Inaddition, to breaking up monopolies, the government could impose a uniform levy on allcompanies participating in the market and redistribute those resources to the operatorswho provide services to the poor.

Sound and credible creditrating institutions whichwould provide an independ-ent assessment to investorsof the risks and returnsoffered by the bonds areimportant players in thisprocess.

14

Averting an Infrastructure Crisis:A Framework for Policyand Action

Among the mechanisms that rely on taxpayers to subsidize certain services, output-basedsubsidies can be most precisely targeted at poor users. Since service providers receive thesubsidy only after actual delivery of the desired services, such schemes enhance theoperators’ incentives to perform. Indonesia has started to explore such schemes in thepower sector. It should also design such schemes in ways that maximize competitivepressures between operators. This can be done by organizing competitive bidding processesto identify, on the basis of the lowest subsidy required, the operator that will have theright to provide the subsidized services. The Government could also establish a system of“portable subsidies,” whereby operators compete for customers and any operator thatprovides the agreed upon service to the targeted population receives a pre-determinedsubsidy.

Box 4. Taking action – Mobilizing Finance for InfrastructureDevelopment

• Indonesia needs to increase investments in infrastructure by about 2 percent of GDP. In the short/mediumterm, increased spending by the central government will be required to bridge this gap. This would bepossible through a combination of: improved tax collection, re-allocation of unproductive spending, andincrease in borrowing made possible by the impressive fiscal consolidation.

• Steps should be taken to tap domestic savings for infrastructure investments.• To the extent that cross-subsidy schemes remain necessary in the short term to enable the poor to have

access to infrastructure, they should be more limited and better targeted at the truly poor

The Way ForwardIndonesia has already started to undertake ambitious reforms in infrastructure. At thesame time, the severity of current and potential future problems can not be underestimated.The reform agenda is potentially huge and no government can possibly address all issuessimultaneously. There are limits, for example, to the number of new laws that can possiblybe simultaneously drafted and then considered by the DPR. Also, tariffs cannot be increasedall at once given the strain that it would put on household budgets. In addition, theGovernment has already committed to give high priority to an ambitious agenda of policyand legal reform measures included in the White Paper. In light of these constraints, thisreport attempts to prioritize between reform measures.

There are no simple solutions ahead. But we believe that any strategy will need to focuson three pillars: First, better public management, planning and consistent policies forinfrastructure development will be key to reestablish credibility, service provision andimpact on the population. The new decentralization agenda lends added complexity tothis agenda. Second, while the public sector is likely to remain dominant in manyinfrastructure sectors, steps will need to be taken to re-attract the private sector in order toprovide vital expertise, foster competition (or appropriate regulation) to improve efficiency,and because the financing constraints will remain large for some time. Finally, efficiencyin implementing public projects will be key to improve impacts. This will require aconsistent drive to improve transparency, competitive bidding and root out corrupt practices,which are prevalent in infrastructure projects throughout the world and also in particularin many sectors in Indonesia.

Over the short to medium term, we envisage a financing gap of around two to threepercent of GDP to fully reestablish infrastructure expenditures to the level required to

Output-based schemes linkthe payment of the subsidyto the effective provision, byan operator, of the servicethat qualifies for obtainingthe subsidy.

It is imperative for Indonesiato press forward on the pathof reform if infrastructure isto foster rather than hinderits fragile economic recoveryand its efforts to tacklepoverty.

15

Overview

both support growth prospects, and to expand the provision of basic infrastructure servicesto the population. This is a conservative estimate, but we believe it is within reach withappropriate policies and improved efficiency. Indonesia has made impressive progress infiscal consolidation over the last few years, and additional measures are identified toreach this goal. While increased public spending will be key, especially to reach the poorand lagging areas, this should not be considered a substitute for policy reforms, but acomplement. In addition, this should also provide a good platform to develop moresustainable forms of mobilizing long term funding from domestic financing sources.

Without minimizing the challenges ahead, we are therefore optimistic about the future.A feasible path exists, and the government is aware of what needs to be done. The reportdoes not attempt to provide a blueprint for such a path, as searching for this path, includingsequencing of actions, priorities for investments, and building constituencies for reforms,is by nature a political exercise. Rather, it tries to highlight key issues that the decisionmakers may want to consider when preparing and implementing their next steps. Key inthis regard will simply be a consistency of signals and determination in forging ahead.We are honored to have been associated to this effort through this report and stand readyto assist in implementing it.

Achievements, Challenges,and Opportunitiesc

ha

pte

r1

17

ndonesia’s past economic achievements are commendable. Theeconomy grew impressively for 30 years until the 1997 financial crisis.The poverty headcount during the period of 1975 to 1995 declined from64.3 to 11.4 percent. Despite the hardships endured as a result of thefinancial crisis, the fiscal consolidation policies that followed are widelyviewed as sound. The infrastructure sector was a significant factor thatpaved the way for poverty reduction and economic development. GivenIndonesia’s dependence on infrastructure to reduce poverty and developin the past, one must ask why the infrastructure sectors are substantiallylagging behind today?

It would be inaccurate to blame the financial crisis as the sole reason forthe current state of the infrastructure sector in Indonesia. The issues in thesector arise from a complex set of issues rather than a single uniqueincident. The sector has required substantial structural and institutionalimprovements for quite some time, but the economic boom prior to thecrisis overshadowed the urgency of the reforms. Adequate public policieson infrastructure were never put in place and as a result, the sector is nowunable to attract the necessary investments. With the economy now poisedto rebound, Indonesia’s infrastructure sector is at a cross roads, and itsactors face a unique opportunity to implement the much needed reformsin time to sustain the recovery.

This report analyses the sector and suggests that the lack of quick progressacross the infrastructure sectors will affect Indonesia’s ability to achieveeconomic growth targets and further reduce poverty. It recognizes theconsiderable progress made thus far, but contends that reforms have

I Infrastructure was signifi-cant for Indonesia's gains inpoverty reduction and eco-nomic development.

The past economic boomovershadowed the urgencyfor infrastructure sector re-forms.

18

Achievements, Challenges,and Opportunities

Averting an Infrastructure Crisis: A Framework for Policy and Action

been insufficient, scattered, and uncoordinated. Hence, the overall benefits from thesereforms are limited with little generated momentum. The report calls for a large scale,well coordinated reform effort to overcome the current infrastructure challenges. Althoughthe authorities now recognize the importance of improving the sector, the true scale ofthe challenge may not be clear, especially at different levels of government. Hence, thesolutions are not discussed and deliberated at the appropriate levels. The issues are usuallystill dealt with a single sectoral view that produces short-term, uncoordinated solutionswith artificial boundaries.

A close examination reveals that there are many similar issues across the infrastructuresectors, therefore requiring cross sectoral solutions. Common issues that transcend individualinfrastructure sectors include a lack of credibility to mobilize private investments, poorpublic management, insufficient user charges, inadequate financing, difficultdecentralization challenges, and weak governance. The government now faces anopportunity to press forward with an organized effort to address these cross-cutting issueswhich will help a majority of the sectors to reap synergistic benefits. This report strives toidentify and analyze these cross-sector issues, and to present the policy maker withrecommendations to confront and solve them. The concluding chapter illustrates the wayforward by identifying the most pressing cross-sector reforms that are needed. In addition,the final chapter summarizes the key sector-specific improvements discussed in four separatereports that accompany this report, which are specifically focused on electric power, roadand road transportation, water and sanitation and telecom-munications.

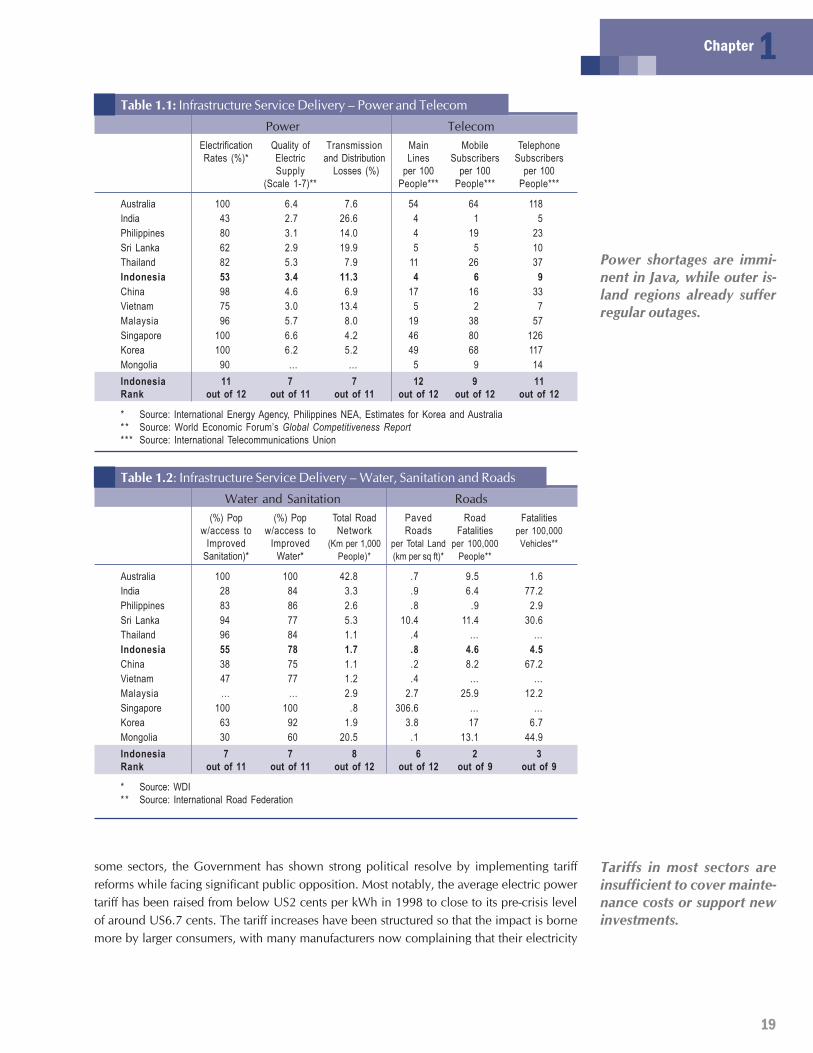

The Infrastructure ChallengeImproving Access and Quality of ServiceIndonesia faces major challenges in its infrastructure sectors as it seeks to consolidate andaccelerate its still fragile economic recovery, improve its international competitiveness,and increase access to basic public services. Symptoms of these challenges are found inevery infrastructure sector. Roads in and around major cities are heavily congested throughoutthe day, while many inter-urban and rural roads are in poor and deteriorating condition.Jakarta’s urban transport system is severely stressed, with poorly-maintained and highlyoverloaded buses jostling for scarce road space, while its sparse suburban railway systemis underutilized. The prospect of imminent power shortages hangs over Java while manyouter island regions are suffering regular outages. PLN has recently been adding newcustomers at rates exceeding 1 million per year but has so far managed to connect onlyslightly over half of all households, although many more have informal connections vianeighbors. Far fewer household have access to piped potable water, let alone to publicsewage systems. While the picture is brighter in the telecommunications sector, whichhas seen explosive growth in mobile phone use since the market opened, Indonesia’steledensity lags well behind that of its neighbors and low internet connectivity carrieswith it the threat of being left on the wrong side of the digital divide. Summary comparativeperformance indicators in the four sectors are presented in Table 1.1 and Table 1.2 below.

In seeking to address these challenges through mobilizing the required investment, theGovernment is forced to confront the sensitive issue of tariffs. Tariffs in many sectors havelong been well below the level needed to support new investment, and the Rupiah’s sharpdecline in value in 1997-98 and subsequent rise in inflation made the situation worse. In

There are common issuesfacing all infrastructure sec-tors that can be addressedthrough cross sectoral solu-tions.

Indonesia's infrastructureperformance lags behind theregion.

19

Chapter 1Table 1.1: Infrastructure Service Delivery – Power and Telecom

Power TelecomElectrification Quality of Transmission Main Mobile TelephoneRates (%)* Electric and Distribution Lines Subscribers Subscribers

Supply Losses (%) per 100 per 100 per 100(Scale 1-7)** People*** People*** People***

Australia 100 6.4 7.6 54 64 118India 43 2.7 26.6 4 1 5Philippines 80 3.1 14.0 4 19 23Sri Lanka 62 2.9 19.9 5 5 10Thailand 82 5.3 7.9 11 26 37Indonesia 53 3.4 11.3 4 6 9China 98 4.6 6.9 17 16 33Vietnam 75 3.0 13.4 5 2 7Malaysia 96 5.7 8.0 19 38 57Singapore 100 6.6 4.2 46 80 126Korea 100 6.2 5.2 49 68 117Mongolia 90 … … 5 9 14Indonesia 11 7 7 12 9 11Rank out of 12 out of 11 out of 11 out of 12 out of 12 out of 12

* Source: International Energy Agency, Philippines NEA, Estimates for Korea and Australia* * Source: World Economic Forum’s Global Competitiveness Report*** Source: International Telecommunications Union

Table 1.2: Infrastructure Service Delivery – Water, Sanitation and Roads

Water and Sanitation Roads(%) Pop (%) Pop Total Road Paved Road Fatalities

w/access to w/access to Network Roads Fatalities per 100,000Improved Improved (Km per 1,000 per Total Land per 100,000 Vehicles**

Sanitation)* Water* People)* (km per sq ft)* People**

Australia 100 100 42.8 .7 9.5 1.6India 28 84 3.3 .9 6.4 77.2Philippines 83 86 2.6 .8 .9 2.9Sri Lanka 94 77 5.3 10.4 11.4 30.6Thailand 96 84 1.1 .4 … …Indonesia 55 78 1.7 .8 4.6 4.5China 38 75 1.1 .2 8.2 67.2Vietnam 47 77 1.2 .4 … …Malaysia … … 2.9 2.7 25.9 12.2Singapore 100 100 .8 306.6 … …Korea 63 92 1.9 3.8 17 6.7Mongolia 30 60 20.5 .1 13.1 44.9Indonesia 7 7 8 6 2 3Rank out of 11 out of 11 out of 12 out of 12 out of 9 out of 9

* Source: WDI* * Source: International Road Federation

some sectors, the Government has shown strong political resolve by implementing tariffreforms while facing significant public opposition. Most notably, the average electric powertariff has been raised from below US2 cents per kWh in 1998 to close to its pre-crisis levelof around US6.7 cents. The tariff increases have been structured so that the impact is bornemore by larger consumers, with many manufacturers now complaining that their electricity

Power shortages are immi-nent in Java, while outer is-land regions already sufferregular outages.

Tariffs in most sectors areinsufficient to cover mainte-nance costs or support newinvestments.

20

Achievements, Challenges,and Opportunities

Averting an Infrastructure Crisis: A Framework for Policy and Action

rates are higher than elsewhere in the region (see Box 1.1 for business concerns regardinginfrastructure). The Government has also moved to assist the poor by simultaneouslyimplementing an output based subsidy scheme where PLN is compensated for providingpower to very small users at sub-commercial rates. But further tariff increases will likelybe necessary to finance the massive investments required to serve a projected doubling ofdemand by 2010, especially if PLN is unable to conclude new gas sales agreementsquickly and is forced to burn more oil. However, with elections scheduled for 2004, thefinal quarterly power tariff increase planned for 2003 has been cancelled. Concerns aboutpossible social unrest have previously led to the postponement or restriction of tariffincreases for other services, including water, phone, and rail transport. The poorest urbandwellers nonetheless pay much more per liter for their water than do those who are muchbetter off. For many cash-strapped operators, continuing low tariffs have necessitatedsubstantial cut-backs in maintenance and deferral of well justified new investments. Thisin turn is translating into poorer and sometimes less safe services for those who alreadyhave access and, of course, into longer waits for those who don’t.