Embed Size (px)

Citation preview

Pull, Push, Pipes: Sustainable Capital Flows for a New World Order

Mark Carney

Governor, Bank of England

6th June 2019

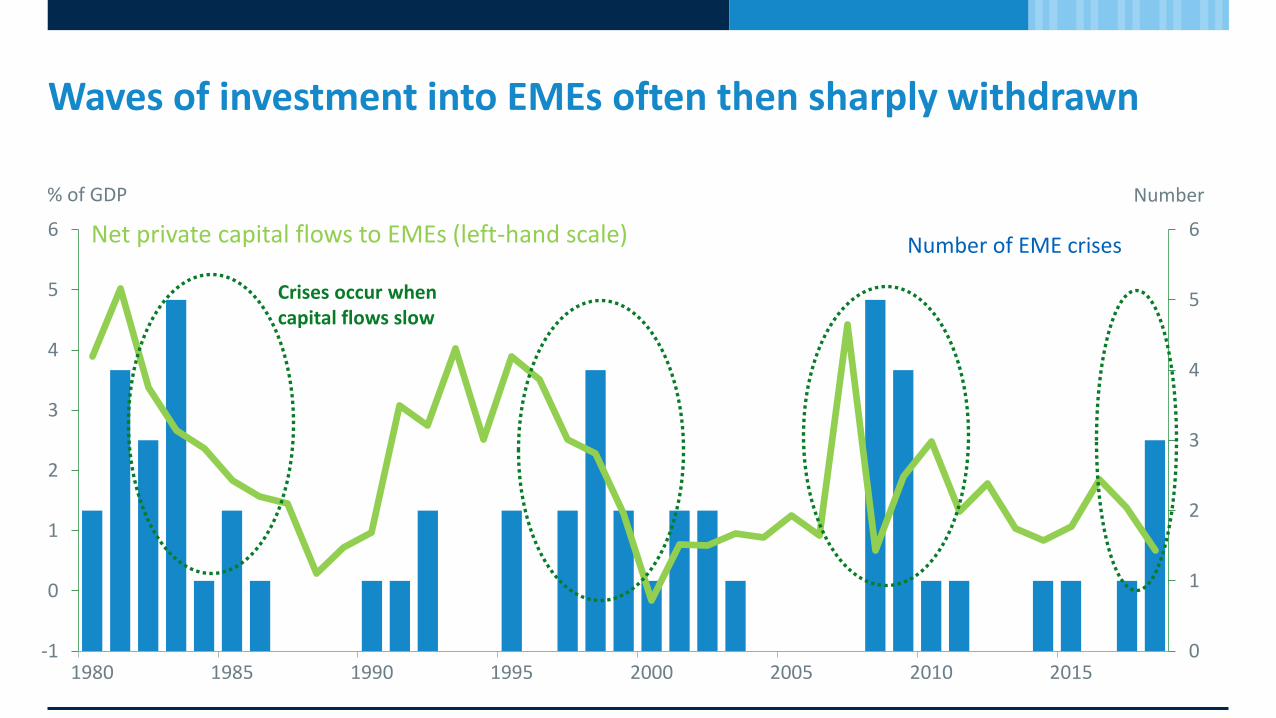

Waves of investment into EMEs often then sharply withdrawn

-1

0

1

2

3

4

5

6

0

1

2

3

4

5

6

1980 1985 1990 1995 2000 2005 2010 2015

Number% of GDP

Crises occur when capital flows slow

Number of EME crisesNet private capital flows to EMEs (left-hand scale)

EMEs have increased financial openness by considerably less than AEs

0

50

100

150

200

250

300

1980 1985 1990 1995 2000 2005 2010 2015

External liabilities as % of GDP

Emerging market economies

Advanced economies

A holistic Capital Flows-at-Risk frameworkPull, Push, Pipes

Pull factorsDomestic institutional frameworks

The PipesStructure of the global financial system

Push factorsDeterminants of global risk appetite and conditions

The distribution of capital flows to emerging market economies

Negative pull shock

Unconditional distribution

Probability density

Capital flows as a % of GDP

-8 -6 -4 -2 0 2 4 6 8 10 12 14 16 18

0.00

0.02

0.04

0.06

0.08

0.10

0.12

AB

Reducing reliance on foreign investors and foreign currency borrowing dampens capital flow volatility

0.0

0.5

1.0

1.5

2.0

0 5 10 15 20 25 30 35 40 45 50

Volatility of capital flows

Share of non-financial corporate debt denominated in $

Higher share of $ debt is associated with greater volatility

NFC dollar debt (% of NFC total debt)

-4

-2

0

2

1996 1999 2002 2005 2008 2011 2014 2017

Capital Flows-at-Risk as a % of GDP

Improving Pull Factors have reduced Capital Flows-at-RiskG

ross

infl

ow

sG

ross

ou

tflo

ws

Contribution of pull factors

Average Capital Flows-at-Risk

Share of FX-denominated debt has increased sharply

12

13

14

15

16

17

18

19

20

21

22

95 97 99 01 03 05 07 09 11 13 15 17

Per cent of GDPEM (excluding China) – FX debt of non-bank borrowers

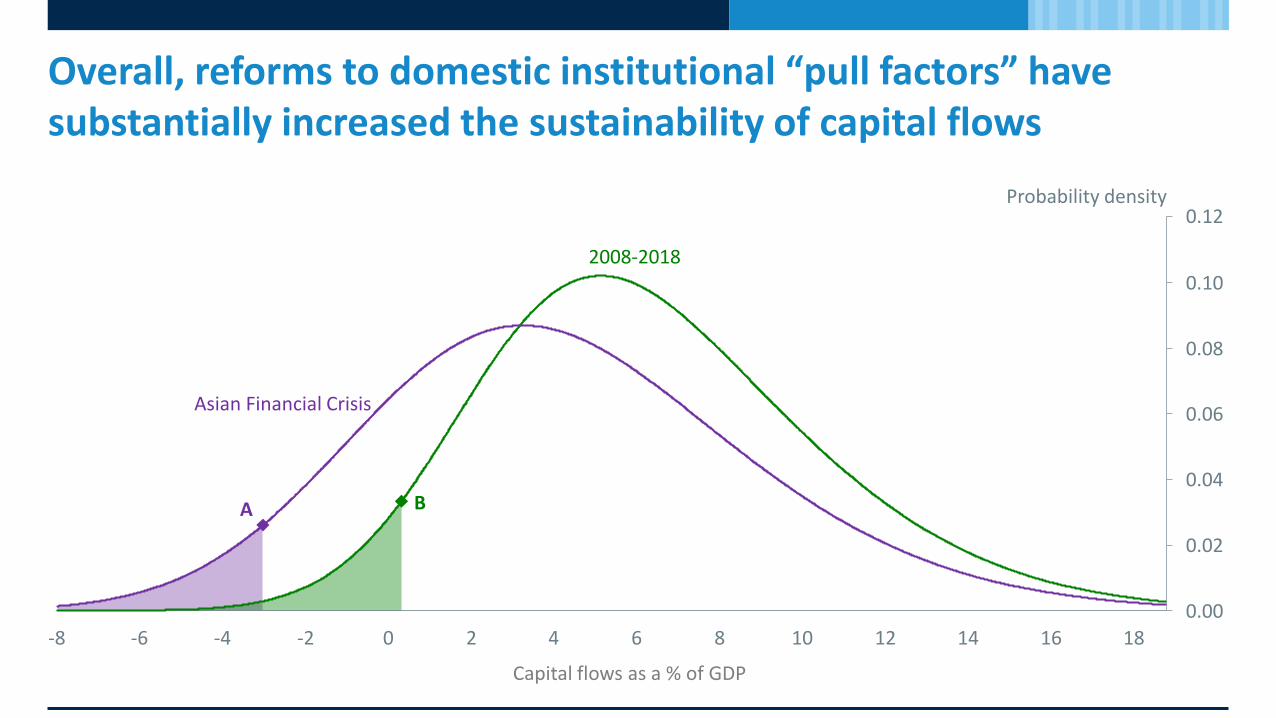

Overall, reforms to domestic institutional “pull factors” have substantially increased the sustainability of capital flows

Probability density

Capital flows as a % of GDP

-8 -6 -4 -2 0 2 4 6 8 10 12 14 16 18

0.00

0.02

0.04

0.06

0.08

0.10

0.12

Asian Financial Crisis

2008-2018

A B

Global economy is rapidly becoming multi-polar, while the transition of the international monetary financial system has barely begun

US dollar share of global markets

US share of the global economy

-8

-6

-4

-2

0

2

1996 1999 2002 2005 2008 2011 2014 2017

Capital Flows-at-Risk as a % of GDP

Impact of push factors has increasedG

ross

infl

ow

sG

ross

ou

tflo

ws

Contribution of pull factors

Contribution of push factors

Total Capital Flows-at-Risk

Push factors weighed more heavily over the past decade, offsetting some of the improvement in pull factors

Probability density

Capital flows as a % of GDP

-8 -6 -4 -2 0 2 4 6 8 10 12 14 16 18

0.00

0.02

0.04

0.06

0.08

0.10

0.12

2008-2018 distribution

Negative push shock

AB

Market-based finance accounted for all the increase in foreign lending to EMEs since crisis as bank lending has declined

Bank

36.4%

18.5%

4.6%

40.5%

Market-basedFund

Market-basedNon-Fund

Bank

FDI

24.0% 23.0%

9.4%

43.6%

Market-basedFund

Market-basedNon-Fund

Bank

FDI

FDI Market-based Non-fund Market-based Fund

20172008

Market-based finance and investment fund flows more volatile than other types of flows

Market-based finance

-5

-4

-3

-2

-1

0

FDI Banking MBF of which: Mutual funds

Median

5th percentile

% of GDP

of which: investment funds

Structural changes in the global financial system are increasing Capital Flows-at-Risk

-4

-3

-2

-1

1

2006 2018 2030a 2030b

Capital Flows-at-Risk as a % of GDP

Pre-crisis baseline

∆ FX share

∆ Flow composition

∆ Mutual funds

Total

Impact of the increasing role of investment funds

Impact of the shift towards market-based finance

Impact of a higher share of FX-denominated debt in EMs

Total

2030 excluding growth in EME external balance

sheets

2030 including growth in EME external balance

sheets

Global financial safety net more fragmented and less reliable

0

2

4

6

8

10

12

0

1

2

3

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

IMF Permanent IMF Temporary

RFAs FX Reserves (lhs)

Per cent of global external liabilities

Per cent of global external liabilities (rhs)

(rhs)(rhs)

Macroprudential policy in EMEs can reduce Capital Flows-at-Risk

Probability density

Capital flows as a % of GDP

-8 -6 -4 -2 0 2 4 6 8 10 12 14 16 18

0.00

0.02

0.04

0.06

0.08

0.10

0.12

Average macro-prudential stance

AB

Tighter macro-prudential stance

Pull, Push, Pipes: Sustainable Capital Flows for a New World Order

Mark Carney

Governor, Bank of England

6th June 2019