Embed Size (px)

Citation preview

Pulse of the industryDifferentiating differently

Medical technology report 2014

In the last three issues, we have described how the drive to value in health care, combined with the growing power of patients, is transforming the sector. This year, our opening article, “Differentiating differently,” focuses on an additional risk that has emerged: the commoditization of many medtech product segments. For medtech developers, the specter of commoditization upends their business models and creates a scenario in which competition is no longer based on historical value drivers — brand, quality and design — but on a single element, price.

To understand how commoditization is playing out now and in the future, we surveyed medtech companies’ main customers in four major markets: the US, the UK, Germany and Spain. Through interviews and case studies, we also explored the various strategies medtech companies can adopt to differentiate their products in an increasingly difficult health care market.

Not all of the strategies we outline in this report will apply to every company; nor are any of these strategies mutually exclusive. What we can say is that the

old ways of differentiating products appear less valuable to customers. This means that medtechs must transition to differentiating differently, placing greater emphasis on mechanisms that allow them to distinguish products based on value and outcomes.

We recognize that differentiating differently will require changes to medtech business models and can only be accomplished in conjunction with other strategic financial objectives. With that in mind, we have drawn linkages, where applicable, to noteworthy financial performance, financing and M&A trends that surfaced over the past 12 months.

As ever, we are grateful for the insights, opinions and perspectives of some of the industry’s leading insiders in helping us develop this year’s Pulse of the industry. We hope this report offers plenty of food for thought and discussion. We look forward to continuing the conversation with you in one-on-one discussions and via social media. Please visit our blog (lifesciencesblog.ey.com) and our Twitter feed (@EY_LifeSciences) for more.

— EY Global Life Sciences Sector

To our clients and friends,Welcome to the 2014 edition of Pulse of the industry, EY’s annual report on the medical technology industry.

Connect with us@EY_LifeSciences lifesciencesblog.ey.com

ContentsPerspectives

Appendix

Industry performance

05 Point of view: Differentiating differently11 To improve medtech R&D, take a system-wide approach

Dr. Olaf Schermeier, Fresenius Medical Care14 Building a better model for health care

Brent Shafer, Philips North AmericaDr. James V. Rawson, Georgia Regents Medical Center

18 Collaborative contractingMark West, SharedClarity

20 Sea change in China’s medtech industry

21 Why medtech should embrace commoditizationRob ten Hoedt, Eucomed and Medtronic

22 Taking a new approachJosé Almeida, AdvaMed and Covidien

23 Strength, resilience and energyJohn J. Greisch, Hill-Rom

24 Charting a new courseJoseph M. DeVivo, AngioDynamics

70 Scope of this report: defining medical technology

71 Acknowledgments

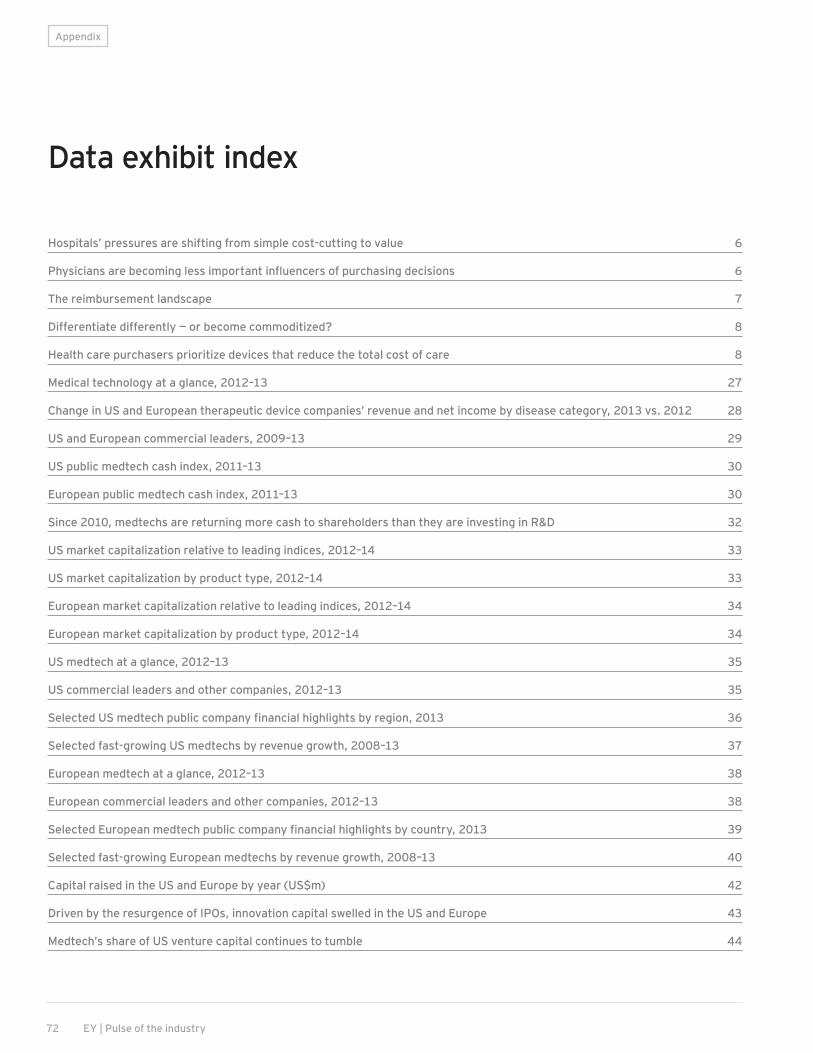

72 Data exhibit index

74 Contacts

26 Financial performance | Holding steady

41 Financing | Financing the future

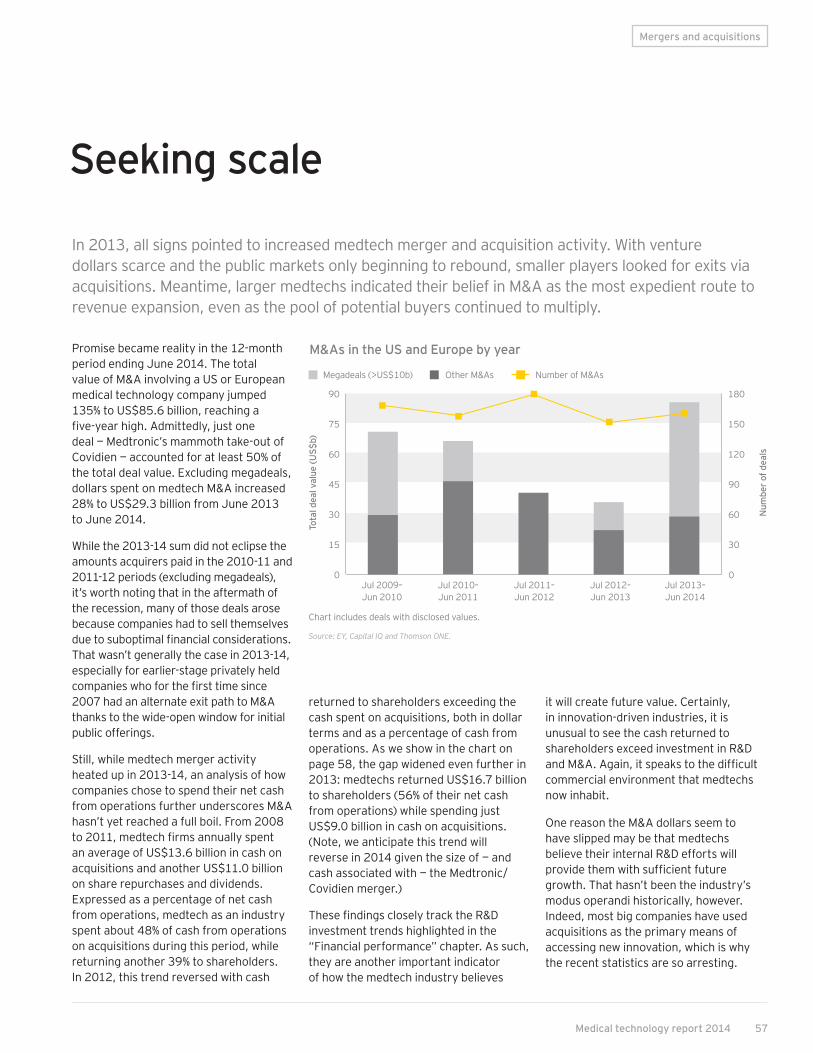

56 Mergers and acquisitions | Seeking scale68 Medtronic/Covidien: Emblematic of what medtech is buying now

PerspectivesPart 1

Part

1

| Pe

rspe

ctiv

es

As a result of these two trends, patients and payers are more influential, and companies must respond with new approaches and business models to succeed. At a minimum, companies must now measure health outcomes and demonstrate the value of their products to payers and providers. To accomplish this, they may also have to expand their traditional offerings by moving beyond the product (expanding into services and solutions), beyond the hospital (enabling care delivery wherever patients happen to be) and beyond treatment (providing prevention, remote monitoring and more).

But medtech companies’ strategies will also need to account for an additional risk emerging from this confluence of trends: the threat of commoditization in many product segments. How to address this challenge is a central theme of this year’s Pulse report.

Commoditization Commoditization is the process by which products become undifferentiated and therefore interchangeable in customers’ perceptions. For manufacturers, this

process fundamentally changes the nature of competition in a business segment. Instead of competing on attributes such as brand, quality and design, products in a commoditized industry compete largely along just one dimension: price. Generally speaking, the journey to commoditization and price competition takes place in three steps: (1) a shift in customer perception; (2) lowered barriers to market entry; and (3) full-on price competition.

This process is beginning to play out in medtech, in several ways.

A shift in customer perceptionThe first step to commoditization is for products to become undifferentiated in the eyes of consumers. This can result when products are functionally identical — for instance, high octane and low octane gasoline. But commoditization can also occur when products still have distinguishing attributes, but customers become unwilling to pay a premium price for these features. This happened in the 1990s with desktop personal computers. Until the mid-1980s, IBM computers commanded a premium price because of Big Blue’s reputation and its long history in computing. Over time, the features distinguishing one PC from another became less and less important to customers, and the market was driven by narrow margins and aggressive price competition. By 2004, the industry had become so commoditized that

IBM sold its PC division to the Chinese manufacturer Lenovo.

To evaluate the extent to which this dynamic is playing out in medtech, we conducted a survey of US and European health care buyers in four major markets: the US, the UK, Germany and Spain. In particular, we focused on two constituencies within these organizations: practicing physicians and procurement officers.1 Providers, of course, have traditionally been the main buyers of medical devices. This remains true even in an outcomes-driven world where payers have more influence and the physicians themselves have become the salaried employees of health care systems. To get a sense of the direction and momentum of change, we asked these respondents questions about buying patterns today as well as their perceptions of how buying decisions will be made three years from now.

The survey reveals some clear attitudinal shifts, with potential implications for the nature of competition and how customers’ perceptions of medtech products will change. When asked about the biggest pressures on their institutions, for instance, respondents indicated that simple cost-cutting issues will become relatively less important over the next three years. Instead, they expect a significant increase in the importance of health care reform initiatives focused on value and outcomes (e.g., value-based purchasing and pay-for-performance).

1 The survey, conducted in August 2014, was taken by 162 respondents in total — 71 in the US, 33 each in the UK and Germany and 25 in Spain. Of those, 85 occupied clinical roles (chief of cardiology, department head, etc.) and 77 were in administrative or managerial roles (purchasing, supply chain, etc.).

Differentiating differently

For several years, we have written about two trends in health care that are transforming the medical technology business. The first of these — an increasing emphasis on value and the concomitant need to demonstrate improved outcomes — was something we explored in our 2011 Pulse of the industry report. The following year, we discussed the second transformative trend: patient-empowering, information-leveraging technologies (PI technologies) such as connected devices, smartphone apps, sensor-embedded objects and social media platforms.

Perspectives

5Medical technology report 2014

As shown in Chart 1, 34% of respondents expect these measures to be among the three factors placing the most pressure on hospitals in three years’ time (up from 21% today). Meanwhile, respondents expect a relative decline in the focus on cost-cutting (down from 44% today to 37% in three years), imaging costs (22% today, 12% in three years) and other such issues.

Respondents also see a clear shift in the most important influencers of purchasing decisions over the next three years. As shown in Chart 2, physicians are expected to become significantly less influential, while the influence of hospital managers and administrators (e.g., the CFO/finance department or procurement/purchasing department) is expected to rise. Insurers and other payers are expected to see the most significant increase in influence, albeit from a low base — this constituency is the least influential category by far, and this will remain the case in three years. Meanwhile, as indicated in Chart 3, procurement decisions are becoming more centralized in many major markets.

These shifts have clear implications for the ways in which medtech companies market their wares and how customers perceive their products. If individual physicians become less influential, and purchasing decisions are instead increasingly made by managers and administrators — whose prime focus is on measuring and rewarding value — then it seems likely that companies will need to demonstrate the value of their devices in terms of measurable improved outcomes for patients and lower total system costs if they are to make the cut.

Indeed, this is exactly what we see in Chart 4 and Chart 5 on page 8. As we have discussed in past issues of Pulse, medtech companies have traditionally “innovated at the bedside,” working in close conjunction with practicing

Perspectives

Higher scores indicate influencers who are more influential — today or in three years’ time — in hospitals’ purchasing decisions. Source: EY Pulse Hospital Survey.

2.5

2.0

1.5

1.0

0.5

0Physicians

2.4

1.9

1.7

1.9

CFO, finance department

0.2

0.5

Payers, insurers

1.61.7

Procurement, purchasing department

Chart 2. Physicians are becoming less important influencers of purchasing decisions

Today In three years

Declining: Simple cost-cutting

1 e.g., Value-based purchasing, pay-for-performance

Numbers show percentage of respondents who selected each factor in response to the following question: “Please select the three factors that place the most pressure on your institution today, and the three factors that you anticipate will place the most pressure on your institution three years from now.”

Source: EY Pulse Hospital Survey.

50%

40%

30%

20%

10%

0%

21%

34%

Cost-cutting

44%

37%

Increasing: Value/outcomes

41% 40%

Cost of upgrading or

maintaining IT systems

Health care reform

initiatives1

22%

12%

Imaging costs

33%

27%

Rising drug costs

38%37%

High-end medical technology costs

(non-imaging)

Chart 1. Hospitals’ pressures are shifting from simple cost-cutting to valueToday In three years

Rank

ing

6 EY | Pulse of the industry

physicians and surgeons to develop new variants of products that met the specific needs and preferences of these end users. But as individual doctors become less influential over the next three years, survey respondents expect that features targeted at these buyers will become less important in purchasing decisions. As shown in Chart 4, “physician preference for specific device,” “user-friendly design” and “training in use” are all expected to become less important in purchasing decisions.

Instead, respondents expect that measures that target value and outcomes (e.g., “data demonstrating clinical outcomes,” “data demonstrating value,” “beyond-the-product services,” “risk-sharing agreements”) will become significantly more important influencers of purchasing decisions.

And, as we show in Chart 5, when medtech purchasers were asked about the economic outcomes they see as most important when differentiating new products, the leading metric was

“reduced total costs of care.” Indeed, purchasers ranked this as much more important than other factors, including reduced hospital stays or increased surgical efficiency.

For medtech companies, the repercussions are clear: to succeed, firms will need to design and market their products to appeal not just to the preferences of physicians in the field, but also to the value-driven considerations that are becoming top-of-mind for administrators and managers.

Perspectives

Chart 3. The reimbursement landscape

CountryProcurement of medical devices carried out at the national level

Availability of national list of approved medical devices for procurement or reimbursement

Remarks

UK Yes No

NHS trusts can purchase products through one of five main routes: 1. Directly from suppliers using National Framework Contracts2. From the NHS Supply Chain which provides end-to-end supply chain services

incorporating procurement, logistics, e-commerce, and customer and supplier support

3. Collaborative Procurement Hubs/Confederations (regional multi-trust purchasing)

4. Local contracts managed by individual trusts5. Pan-government National Framework Contracts

France No Yes

The French Government is promoting the formation of regional procurement collectives, as a cost-cutting measure. Ten such collectives are currently in operation in France. The RESAH-IDF network, one of the largest procurement collectives in France, is in the process of establishing a European collective procurement platform known as Healthy Ageing in Public Procurement Innovation (HAPPI), through which more than €3 billion of purchases may be made annually.

Germany N/A N/A Procurement hubs are common in Germany. They have been consolidating in recent years: there are around 35 hubs, down from 100 in the early 2000s.

Spain No Yes Procurement is being centralized at the provincial level (for several hospitals).

Italy No YesProcurement is being rationalized in Italy. Four procurement regions are planned (North-East, North-West, Central and South), which will replace several agencies at local and regional levels.

US No No

Purchasing decision-making is shifting from individual clinicians to central purchasing staff focused on economic cost/benefits. Hospitals are also seeking preferred provider contracts and/or deploying standardized purchasing initiatives. Group purchasing organizations continue to negotiate contracts with suppliers.

China Yes Yes

The National Health and Family Planning Commission is responsible for procurement of medical equipment at the provincial level, including overseeing the bidding and tendering process for medical devices sold to state-run hospitals. High-value medical devices are increasingly purchased through a centralized purchasing system.

Japan No Yes

Private hospitals dominate the market and make their own purchasing decisions. Public hospitals procure equipment through invitations to tender using an approved list system. Hospitals are increasingly collaborating to raise procurement efficiencies by forming group purchasing organizations.

Source: EY.

7Medical technology report 2014

However, this will not always be easy to pull off, for a couple of reasons.

• Iterative innovation. In the search for value, payers and providers are most interested in highly differentiated medtech products that represent a significant improvement over the standard of care. The reality, however, is that such breakthroughs are rare. Innovation in this sector is often an iterative process that yields relatively small improvements over existing products. So far, this approach has worked for medtech companies as long as the physicians for whom new iterations were designed valued these improvements.

Demonstrating the value of these products to payers and procurement departments may not be as easy. While the process of iterative innovation has often generated huge improvement in health outcomes over time, any one iteration may not be enough of an advance to be valued by buyers. In many cases, purchasers will prefer a “good enough” product with fewer features at a lower price point.

• Different product segments. In our 2014 report Progressions: navigating the payer landscape, we warned that companies ought not regard payers as monolithic in their approaches. As medtechs seek to understand the changing purchaser landscape, they will find that buyers may have very different attitudes to products depending on the deployment of those technologies in the care spectrum. Differentiation will be more difficult depending on where medtechs aim their products.

Perspectives

1 e.g., patient support

Numbers show percentage of respondents who selected each factor in response to the following question: “Please select the three most important factors in your medical device purchasing decisions today, and three factors you anticipate will be most important three years from now.”

Source: EY Pulse Hospital Survey.

Respondents were asked to rank the three economic outcomes that are most important in differentiating new medical devices. The lower the score, the more important the economic outcome in differentiating a medtech product.

Source: EY 2014 Pulse Hospital Survey.

100%

80%

60%

40%

2.5

2.0

1.5

1.0

0.5

0

20%

0%

77% 77%

Price of device

55%

27%

Physician preference

for specific device

32%

22%

User-friendly design

31%35%

“Beyond the

product” services1

22%18%

Training in use

6%

25%

Risk- sharing

agreements

51%

62%

Data demonstrating

clinical outcomes

27%

35%

Data demonstrating

value

Price remains the top factor

Old ways of differentiation are less relevant

Differentiation will have to be based on data and value

Chart 4. Differentiate differently — or become commoditized?

Chart 5. Health care purchasers prioritize devices that reduce the total cost of care

Today In three years

Reduced total costs

of care

Reduced hospital

stay

Improved surgical

efficiency

Reduced pharmaceutical

utilization

Reduced readmission

rates

1.6

2.02.1

2.4 2.4

Rank

ing

8 EY | Pulse of the industry

The reality, therefore, is that many products may find themselves caught in no man’s land. The features medtech companies have traditionally emphasized in order to differentiate their products may no longer be valued by customers, and in many segments, it may not be easy to make the transition to “differentiating differently” — distinguishing products based on value and outcomes. In these situations, products will be left with only one variable on which to compete: price.

Low barriers to market entryThe pressure on price becomes even greater when the barriers to market entry are low. To return to the example of the personal computer industry in the 1990s, for instance, the move to price competition was accelerated by the ease with which other manufacturers were able to reverse-engineer the IBM PC and develop computers that were functionally equivalent. The same process has repeated itself with various information technology products, from semiconductors to hard drives to tablet computers.

This is relevant for medtech because medical devices are also engineered products with shorter product cycles. Western manufacturers who decide to compete on price will be in a business with razor-thin margins. Some might decide to apply “reverse innovation” — developing relatively inexpensive, stripped-down products for emerging markets and then deploying them in the West as well. But companies should also prepare for the possibility of an additional challenge — competition from new entrants with the ability to deliver products at far lower price points. China’s medtech industry, for instance, is in a relatively early stage of development, but there is no reason why such manufacturers would not be able to learn quickly, improve quality to meet global regulatory standards and create products that would meet the needs of most patients at much lower price points than in the West. Chinese firms in other engineering and manufacturing-based industries have already followed precisely this path, and there is little reason to think that medtech will be much different. (For more, see “Sea change in China’s medtech industry” on page 20.)

Full-on price competitionOnce a segment has been commoditized, a company must choose one of three directions:

1. Move downstream into the lower-margin, price competition space and compete aggressively on price. Strategies to remain competitive could include partnering with companies in emerging markets, reverse innovation or acquiring scale to gain bargaining power and economies of scale.

2. Move upstream into a higher-value segment, innovating within existing product lines or adding new products. This is the preferred approach for companies with products that are already well differentiated and that want to continue to demonstrate that their products add value and merit premium pricing.

3. Create stickiness. Explore other ways to create customer loyalty and differentiate your offering. This could include expanding into services, solutions and complementary product categories.

9Medical technology report 2014

New bases of competitionIf the old ways of differentiation are becoming less relevant, companies must develop strategies for competition on these new bases of differentiation. Broadly speaking, these tactics fall into one of four categories:

1. Achieve superior outcomes via technological advances

2. Increase scope through services and solutions

3. Increase scope by adding product offerings (within a disease area or across multiple disease areas)

4. Take costs out of the health care system

Of course, these strategies will not apply equally to every medtech company. Whether they apply will depend on a range of factors, including the company’s therapeutic focus and stage of development. Moreover, to be successful, companies may find it beneficial to develop a strategic plan that incorporates multiple differentiation mechanisms.

As medtechs consider which tactics to prioritize, one commonality is how each helps address the needs of its customers.

Meeting those needs will require medtech firms to engage with health care buyers on the buyers’ terms, spending time on-site to understand concerns such as workflow efficiency or the ways in which current devices are used to deliver care.

This is the path Fresenius Medical Care took when it restructured its R&D operations in 2013. As Dr. Olaf Schermeier, the company’s Chief Officer for Global Research and Development, explains on page 11, Fresenius mandated that every one of the company’s engineers spend a minimum of two days annually in the clinic, working alongside medical teams to gain a first-hand understanding of how to optimize the care delivery for renal patients.

As they reconsider their strategic priorities to adopt one or more of the new bases for competition, companies are likely to consider reallocating their R&D spending. Philips Healthcare, for example, which has embarked on a 15-year project with Georgia Regents Medical Center aimed at improving clinical outcomes, has already done so. Brent Shafer, Chief Executive Officer of Philips North America, explains that tackling initiatives such as improving patient experience requires redistributing resources. “In the past, Philips might spend about 8% of our total health care sales on

product research and development,” he says. “Now, it might be 5%, with 3% going toward R&D for commercial innovation, working with our customers to develop better solutions that they can implement in their protocols for delivering care.” (See “Building a better model for health care” on page 14.)

1. Achieve superior outcomes via technological advances

In certain therapeutic areas, it has become difficult to improve upon existing devices — at least in ways that buyers care most strongly about. That said, there are green field areas where new product R&D can catalyze a new standard of care.

Second Sight Medical Products’ Argus II retinal prosthesis system is a case in point. The device — a retinal implant accompanied by a wireless processing unit, glasses and a video camera — can partially restore vision to people blinded by the rare genetic condition retinitis pigmentosa (RP). The device was approved for use in Europe in 2011, and in February 2013, it won approval from the U.S. Food and Drug Administration (FDA).

Sophisticated devices such as Argus II, which represent a technological step-change, don’t come cheaply. As the company’s Vice-President of Business Development, Brian Mech, told Reuters in February, getting Argus II to the market took 14 years, US$200 million and “intestinal fortitude.” Second Sight is now working with insurers, the US Centers for Medicare & Medicaid Services and governments in Europe to underwrite the device’s US$100,000 price tag. In August, the French Ministry of Health approved financial support for the system, which is also available in Germany, the Netherlands, Switzerland, Italy, Saudi Arabia and the UK.

Perspectives

To be successful, companies may find it beneficial to develop a strategic plan that incorporates multiple differentiation mechanisms.

10 EY | Pulse of the industry

Fresenius Medical Care’s success is based on great inventions. Polysulfone fiber, for example, was key to creating the first truly effective dialyzer. This kind of innovation was driven by creative engineers, many of whom are still with the company, and this is still one of our biggest assets.

of the overall treatment, not just the cost of a specific product. Thus, reducing the overall cost of therapy must be one of our key innovation targets. Vertical integration — from a complete renal product portfolio to owning the dialysis center network — has been a clear benefit for Fresenius Medical Care, not only in developing new products but also for the overall economies of scale.

A key differentiator for Fresenius Medical Care is the way that R&D interacts with the clinical part of the business. Our 3,200 dialysis centers not only provide an incredible data pool, they also offer an opportunity for our R&D engineers to visit a clinic, where they can get an in-depth understanding of the optimization potential that can then be addressed in the technology and in the development process. In fact, every one of our engineers worldwide is required to spend a minimum of two days per year in a clinic, observing therapies and processes and discussing them with clinic staff and patients. This enables them to get an in-depth understanding of the optimization potential they can address in new technology developments.

Our clinics treat around 280,000 ESRD patients worldwide, three times per week, and we conduct regular surveys to learn how we can help to improve their quality of life. On questions of care, the patients play an increasingly important role in the overall decision-making process. Therefore, it is crucial for us to understand their needs. Home patients,

for example, are unwilling to use bulky and complex clinical machines. We have to understand that we cannot simply take a clinical system, adapt it slightly and assume the patient will be happy to have it in his or her home. What is the impact on patients’ flexibility? Can they use the system when they travel? How simple is the user interface? These are huge decision points for all home patients, and our engineers have to incorporate this kind of thinking in the product development process.

The renal care space is still growing, but the logical question is, where to go from here? Many of our patients have comorbidities: more than 40% of dialysis patients have diabetes, 70% have high blood pressure, and nearly all have some kind of cardiovascular disease.

For us, this is clearly an opportunity to expand our services into chronic care coordination, by incorporating elements of general practice, cardiology, diabetology and even psychology to improve our overall patient care. This makes sense not only from a service perspective, by making use of our clinical infrastructure, but also from a product and technology perspective.

Guest article

To improve medtech R&D, take a system-wide approachDr. Olaf Schermeier

CEO Global R&D, Member of the Management Board, Fresenius Medical Care

As engineers, we have long been accustomed to innovating by looking at individual products — the best-in-class dialyzer, for example. But we now understand that even more value is created when we try to improve a specific therapeutic system in its entirety, by taking a more holistic view of a therapy. We now ask: What is the outcome for patients? What is the reimbursement structure? What kind of therapy can I apply, and how can I make it as cost-effective as possible?

This approach goes beyond individual products. It clearly represents the biggest innovation potential in dialysis.

The various elements of Fresenius Medical Care’s portfolio — dialysis machines, disposables, drugs, dialyzers and IT solutions — all interact with each other to create value and improved therapies for end-stage renal disease (ESRD). A good example is our Online hemodiafiltration (HDF) therapy. HDF is based on the ultrafiltration of large amounts of plasma across the dialyzer membrane. The removed volume is then replaced by ultra-pure substitution fluid. Developed by engineers working very closely with medical doctors, Online HDF therapy is a big advance in care that provides clear advantages to patients. As a result, many countries have increased their reimbursement for this specific therapy.

When it comes to reimbursement, the key decision-makers are increasingly basing their decisions on the cost-effectiveness

Perspectives

Key decision-makers are increasingly

basing their decisions on the cost-

effectiveness of the overall treatment,

not just the cost of a specific product.

11Medical technology report 2014

Second Sight’s highly specialized technology represents innovation as medtech has typically defined it: a new therapeutic device to help solve an important unmet medical need. Another kind of technological advance is embodied by AliveCor, a much different kind of company. In 2012, the privately-held San Francisco company introduced a smartphone case that doubles as an electrocardiogram (ECG) for people suffering from heart disease. Sensors on the case turn electrical impulses in the user’s body into ultrasound signals, which are then recorded via an app and allow real-time monitoring.

Since early 2013, AliveCor has collected anonymous ECG data, building a database of more than 1 million recordings, with more data being gathered each month. Using these data, the company has developed an algorithm, approved by the FDA in August 2014, to detect in real time atrial fibrillation, the most common form of cardiac arrhythmia. The algorithm moves AliveCor’s product beyond monitoring to facilitating intervention, so that providers can take action before a patient suffers a more serious and costly event, such as a stroke.

It’s hardly surprising that these innovations came out of smaller, venture-backed endeavors. Rob ten Hoedt, Chairman of Eucomed and President

EMEA & Canada at Medtronic, notes, “Innovation in medtech will continue to be driven primarily by small to medium-sized enterprises (SMEs) and start-ups.” That said, these companies aren’t immune to the challenges of commoditization affecting larger medtechs. “SMEs need to be extremely careful to remain competitive and to differentiate their products from those of larger companies,” says ten Hoedt. Put another way, SMEs need to make sure they have a solution that not only addresses a need in the marketplace but can easily be tucked into a larger entity.

2. Increase scope through services and solutions

As bundled payments become one of the leading strategies for reducing health care costs, an increasingly obvious tactic for medical technology companies is to try to “own” more of the bundle. Medtech companies have, for some time, offered additional services alongside their products as an incentive to purchasers. That’s a problem, according to Dr. James Rawson, Chair of Radiology at Georgia Regents Medical Center in Atlanta. “Many of the services developed by vendors are focused on transactions, rather than relationships and partnerships,” he says. “The endpoint of the relationship between a medtech company and a care provider

is no longer a sale. The endpoint is an improved patient outcome. That’s where the industry has to go.”

Proving his point, Georgia Regents last year embarked upon a 15-year, US$300 million agreement with Philips Healthcare in which Philips is paid for supplying and maintaining equipment — including that of rival firms — as well as for improving patient care. (See “Building a better model for health care” on page 14.) Philips has embarked on a similar agreement with the Karolinska University Hospital, in Sweden. As part of that 14-year agreement, which Philips won in May 2014 after a Europe-wide tender, the conglomerate will invest in R&D and a provider education program, while also overseeing the procurement, installation and maintenance of the imaging equipment at the Karolinska’s new site in Solna.

As Philips’ collaborations with Georgia Regents and the Karolinska suggest, beyond-the-product services must serve a clear purpose, for instance addressing operational efficiencies, if they are to succeed. Medtechs also need to be willing to manage and support the service well beyond the life of an individual product, while being agnostic about where the technology originated.

12 EY | Pulse of the industry

To date, the companies that have embarked on the most ambitious attempts to own more of the bundle are the largest medtechs. The big imaging specialists such as Philips and GE Healthcare led the way, in part because they had to. They were among the first to come under pressure from cost-conscious hospital systems given the centralization of big capital equipment purchases.

Therapeutic device companies are now moving in this direction as well. In December 2013, Stryker bought Patient Safety Technologies for US$120 million in order to gain access to traceability software and hardware that reduce the possibility of post-surgery complications caused by medical errors.

Meanwhile, Medtronic’s US$200 million acquisition in 2013 of Cardiocom, a telehealth company that provides home monitoring, shows how Medtronic is expanding its cardiovascular franchise beyond implantable devices to the provision of services. Just a month after the acquisition, Medtronic established a new business unit, Medtronic Hospital Solutions, to partner directly with hospitals to increase the quality and efficiency of service delivery. And in August this year, the company pushed further into the hospital sector when it acquired NGC Medical, an Italian

company that offers services such as hospital infrastructure design and equipment management.

3. Increase scope by adding product offerings

The move from volume to value means medical technology firms that offer health care buyers an end-to-end solution in a given disease area may have a competitive edge. By having a suite of offerings designed to address the continuum of care in a given disease area, medtechs provide their customers additional value in two related ways. First, by providing a full range of clinically tested products, medtechs assist in ensuring provider groups can meet important care metrics that are now a necessary precursor for their own reimbursement. Second, by offering a spectrum of solutions in a given disease area, medtechs with the right portfolio of offerings can help simplify the contracting complexity health care buyers face.

Surveys of health care payers and purchasers we conducted in 2014 suggest that they have so many strategic priorities to accomplish in the near term that they don’t have the bandwidth to engage with multiple medical technology makers in meaningful conversations about value — especially if that value won’t be realized

within the current budgetary cycle. By establishing relationships with fewer suppliers, these health care buyers can begin to address the issue, negotiating new payment contracts that provide their organizations with improved pricing around the total cost of care.

The deeper a medtech supplier is in a therapeutic area, the more development, regulatory and marketing costs it can leverage across its various departments. Further out, one can imagine how these deep relationships might shift, such that a medtech developer contracts to provide devices for a fixed fee, whether the device is a simpler hip joint or a more complicated total hip replacement. Such innovative contracts are, for now, just talk, but senior medtech executives should start to understand how owning a disease could enable their companies to move away from unit-based pricing to a payment system that enables market access.

In many ways, the service-plus relationships struck by Philips Healthcare and Fresenius illustrate how increasing product scope (broadly defined) might facilitate new commercial models that are less transactional at the unit level and more relationship-driven. The question is how such a model will be applied in the therapeutic device category, especially implants.

Medical technology firms that offer health care buyers an end-to-end

solution in a given disease area may have a competitive edge.

13Medical technology report 2014

Guest article

We’ve partnered with many hospitals around the world, but those partnerships have been based more on managed equipment services. This is different. It has a managed services component, but it is also tied in with a very strategic risk-sharing component and other financial factors.

Under the terms of our relationship, the first thing Georgia Regents was able to do was reduce their cost of procurement. They didn’t have to bid for equipment with three different vendors; they didn’t have to schedule on-site visits. And we manage all the equipment, whether it’s our equipment or a competitor’s. We guarantee certain performance metrics, but at the core of the risk-sharing component of the relationship, our common goals are improved patient outcomes, shorter length of stay and greater patient satisfaction.

Our contract is for 15 years. There are three areas of focus tied to patient satisfaction. The first is based on patients’ experience once they get to the institution. Second, we are partnering

with Cerner to integrate electronic medical records. And third, we will work on our hospital-to-home strategy, developing and deploying remote monitoring capabilities and other solutions for home care.

Philips is in a good position to tackle these initiatives. It’s just a matter of how we want to use our resources. In the past, Philips might spend about 8% of our total health care sales on product research and development. Now, it might be 5%, with 3% going toward R&D for commercial innovation, working with our customers to develop better solutions that they can implement in their protocols for delivering care.

We want to establish many more of these partnerships, but they won’t necessarily work everywhere. We have to look at what is in the best interests of the customer and in the best interests of Philips, and at what strengths we hope to achieve through a partnership. Our relationship with Georgia Regents means that we can do what we do best — innovate, deliver and manage equipment capable of gauging, diagnosing and recording everything from a patient’s vitals to remarkably detailed images, giving the clinicians more time to deliver expert one-on-one care for each patient.

We expect this type of model to become very attractive to hospitals across the world. Each hospital is going to have different needs, but this is a model from which we can build.

Building a better model for health care

Brent ShaferChief Executive Officer Philips North America

In 2013, Philips Healthcare and Georgia Regents Medical Center entered into a 15-year, US$300 million agreement to improve outcomes and deliver care more efficiently to patients. Here, Brent Shafer, Chief Executive Officer of Philips North America, and Dr. James Rawson, Chair of Radiology at Georgia Regents, discuss the rationale behind the deal, and its ambitions.

We’ve partnered with many hospitals around the world, but those partnerships have been based more on managed equipment services. This is different.

Philips’ alliance with Georgia Regents leverages our joint strengths — Philips’ equipment, services and revenue cycle management and Georgia Regents’ ability to serve patients and provide better outcomes. With Georgia Regents, we were looking at a partnership from a much broader perspective than just a hospital entity. We were able to bring Philips’ whole portfolio, from dental care to lighting, not just to the hospital and the university, but also to the community.

Perspectives

14 EY | Pulse of the industry

Guest article

Dr. James RawsonProfessor and Chair of Radiology, Georgia Regents Medical Center

The relationship between Georgia Regents and Philips is based on common values. When we compared our priorities, we saw an overlap in the areas of improving patient health, lowering costs and increasing efficiency. We both wanted to build a better model for health care.

One challenge we had was in teaching people that this wasn’t just a big equipment deal, but something very different. But it is now part of our day-to-day operations across the organization, not the responsibility of a single team.

What Philips saw in us was alignment. In many hospitals, there is a lack of alignment between hospital staff and physicians. In our case, rather than having different departments fight over types of equipment to be used, or workflow, our departments work collaboratively and have done so for decades. In that type of environment, Philips doesn’t get stuck in the middle of a debate between what the doctors want or what different specialists want.

The success of the partnership, in my view, is working with a partner on the good days and the bad days, helping to move the ball forward to improve health. It’s no longer about being sold a piece of equipment or a technology. I no longer look at projects as being completed; I look at them as journeys. We installed a new Philips IntelliSpace PACS system for storing and viewing and processing image data six months ago, and we continue to innovate and improve that process. It is now hard-wired into our operations. The time we used to spend on buying and selling equipment we can now reinvest into innovation and improving the care given to each patient.

When we installed the PACS system, we decided this was not going to be a radiology project, but an enterprise-wide project. We thought a great deal about the methods our physicians would use to access images in the hospital, in the clinic and at external locations, and how easily they needed to be able to interact with that image data to make patient care decisions. It was about changing the way images would move in the entire health system for everybody.

Because we have Philips and our patient advisors sitting at the design

table with us, I think we’re able to make much better decisions.

We’re both learning — from each other, from our patients and from our staff. Georgia Regents was an early pioneer in patient- and family-centered care. We look at new equipment from an efficiency and care delivery point of view, but also from the patient’s perspective. How do we make getting a scan a good experience for the patient, and how does that fit into a larger context of the patient’s overall experience in our hospital? Because we have Philips and our patient advisors sitting at the design table with us, I think we’re able to make much better decisions.

We went live in January with the first phase of the PACS project, and we’re continuing to improve that workflow. Entering year two, we plan to accelerate the pace of innovation. As we keep at this for the remainder of the 15 years, we are creating a very different model of care delivery in which innovations are built on previous learnings. We expect this to lower costs and to improve outcomes, efficiency and, most important, the patient experience.

Perspectives

15Medical technology report 2014

Creating scope in a single disease areaTwo deals in the 12-month period ending 30 June 2014 showcase how therapeutic device companies are broadening the scope of their product offerings.

The first is Zimmer Holdings’ proposed acquisition of Biomet; the second is the Medtronic/Covidien megadeal, which is an even more ambitious effort to create scale across multiple disease areas.

The US$13.4 billion Zimmer/Biomet deal creates an orthopedic player with the critical mass to rival Johnson & Johnson’s DePuy Synthes. As Pulse went to press, European regulators were assessing the anti-trust implications of the Zimmer/Biomet deal. Assuming it proceeds, the transaction will combine the number two orthopedics player by revenue (Zimmer) with the fourth-ranked firm to create a new entity with revenues of nearly US$8 billion. Importantly, the deal promises to position Zimmer as a leader in the musculoskeletal sector, with particular depth in knee and hip implants. Biomet’s sports medicine products, meantime, will give Zimmer additional depth in the trauma market, an area where Johnson & Johnson currently dominates because of its 2011 megadeal with Synthes.

The Zimmer/Biomet transaction is expected to trigger even more deal-making in the orthopedic space, as smaller firms seek scale to remain competitive. Moreover, we may see similar deals to deepen product offerings in other therapeutic areas — especially those with an abundance of competitors. Indeed, as we were writing Pulse, news broke that Danaher was to acquire Nobel Biocare Holding for US$2.2 billion to create the leading dental-focused medtech based on sales of consumables and equipment.

In some cases, the push to add product scope may turn buyers into sellers. As we have witnessed in the pharma business, or with Johnson & Johnson’s divestiture of its Ortho-Clinical Diagnostics division, larger companies may realign their portfolios to create fewer business units with competitive scale. (See “Seeking scale” on page 57.)

Creating scope in multiple disease areasIf the Zimmer/Biomet and Danaher/Nobel Biocare mergers are motivated by deepening product scope, Medtronic/Covidien takes the argument to a new level. In essence, executives championing that megamerger argue that depth in one particular disease area is no longer sufficient. To change conversations with hospital purchasers, especially as vendor consolidation continues, medtech developers must have breadth across multiple disease areas. Call it the über-scope approach.

It’s too soon to say whether the Medtronic/Covidien transaction will have a positive impact on the ways in which the combined entity brokers contracts with hospital purchasers, or whether scale at this level is required to achieve greater leverage with health care buyers. That said, there is no doubt that Medtronic/Covidien has already altered the conversation about the role of medtech M&A in creating entities that can survive in today’s tougher health care climate.

As we note on page 68, the US$42.9 billion merger joins two leading medtech companies to create a new entity that will rival Johnson & Johnson’s medtech division in annual sales. Medtronic and Covidien offer complementary product portfolios: Medtronic supplies a range of devices for the cardiology, neurology

and diabetes markets, while Covidien specializes in hospital supplies. Together, the combined entity will be one of the leading medtech distributers in six of the top 10 hospital purchasing categories, according to Medtronic.

“The addition of Covidien broadens our footprint,” Medtronic Chairman and CEO Omar Ishrak told an interviewer after the announcement of the merger. “The value proposition of Covidien’s technology is primarily to deliver hospital efficiency, while Medtronic’s chronic disease therapies deliver value in post-acute settings. When these two are combined, in a world in which integrated health franchises will be more common, we become a very attractive partner — we can deliver value in the hospital, in a measurable fashion, and value that is realized outside the hospital.”

In an era when health care buyers are inundated with must-dos, it may well be that the scale of a Medtronic/Covidien makes such entities more attractive suppliers during contract negotiations. Indeed, the emergence of a new initiative in the US, SharedClarity, which is sponsored by the payer UnitedHealth Group in conjunction with multiple provider groups, underscores why medtech executives see scaling their businesses as an important strategic priority.

The dearth of comparative data has long vexed medtech customers who argue the rate and volume of the research hasn’t kept pace with the introduction of new products. SharedClarity was created at least partially to rectify that situation, as well as to deliberately correlate existing research with value claims. As SharedClarity’s President, Mark West, explains on page 18, the company recruits physicians from its member hospitals to review the published literature and

Perspectives

16 EY | Pulse of the industry

establish which technologies provide better health outcomes. SharedClarity then takes the process one step further: its sourcing group also negotiates purchasing agreements with product manufacturers based on the evidence amassed. In March 2014, SharedClarity announced the results of its first review and awarded contracts for drug-eluting and bare metal stents.

Apart from offering benefits to purchasers, the SharedClarity model presents opportunities for medtech companies. The first is the most obvious — a stable channel to the market. The second advantage is validation by an independent third party. The final advantage is the goodwill that results from cooperatively participating in the negotiation process. Presumably, a company the size of a combined

Medtronic/Covidien is better positioned to negotiate those purchasing agreements because its economies of scale mean it can be more disciplined about its own costs, thereby passing along price savings to customers like SharedClarity while still maintaining reasonable margins.

Success in one purchasing negotiation is likely to breed further success, not simply with the original buyer but with other purchasing organizations. Thus, medtechs that have participated, and won contracts, with groups like SharedClarity develop relationships as trusted partners, setting the stage for further positive negotiations.

For medtech companies, achieving this trust is no small matter. Customers are increasingly demanding more data before they commit to a purchase — and are not necessarily getting it. “I’ve been asking

about clinical outcomes and impact on the patient with every new technology I’ve assessed,” says Georgia Regents’ Rawson. “For the most part, vendors have not had the answers to those questions.”

4. Take costs out of the health care system

Recognizing that commoditization is a fait accompli in certain disease areas, medtechs could also go on the offensive, devising products or technologies that provide better value because they remove costs from the system. There are two ways to achieve this. First, companies can reduce their costs of production, for instance by engineering a simpler, lower-tech device or by manufacturing the product more cheaply, and passing the savings on to the customer.

Perspectives

Customers are increasingly demanding more data before

they commit to a purchase — and are not necessarily getting it.

17Medical technology report 2014

Guest article

The concept stemmed from business reviews carried out by UnitedHealthcare — the largest commercial payer in the US — and Dignity Health. The theme of medical devices kept coming up, in particular the lack of independent knowledge of how these products perform, and their affordability. I was head of supply chain at the Cleveland Clinic and was asked to develop some business models, one of which is SharedClarity. Over the last four years, we have taken the concept to business plan, to investment, to operations, and now we are achieving results.

The business model is two-fold. One side of it is understanding how medical devices perform, and the other is collaborative contracting within our own membership, which now includes Baylor Scott & White Health, Advocate Health Care and McLaren Health Care, as well as UnitedHealthcare and Dignity.

On the clinical side, we have identified 30 product families on which to focus — high-cost, high-technology, high-clinical-impact products, such as pacemakers, defibrillators, stents, knees, hips and urological slings. Together, these 30 product families account for about US$35 billion a year in the US market. We assign those products a clinical review team, and we go through a structured clinical product review for each. We also tap into Optum, which is owned by UnitedHealth, for comparative effectiveness work. We believe that if you really want to understand how a product performs, you have to follow the patient, and you have to have data that go from

diagnosis to procedure to after-care. What differentiates us is that we have the data that follow that longitudinal activity.

We recently completed the clinical review and contracting process for our first three products — drug-eluting stents, bare metal stents and peripheral stents — a process that took six months. Clinical review teams first look at existing research on the product. They survey specialists who use the product to get input on product attributes and performance. Then we see if there’s consensus on how the products perform. If there isn’t, we ask: why not? What information and data are lacking? What holes in our clinical knowledge base do we need to fill? This could lead us to more surveys, more reviews of existing research or a customized study.

Once the clinical review team has done its work, we go to a collaborative contracting process on behalf of our members. Here, our strategy is simple: first, we take the output from the clinical review teams and their findings. Second, our members commit to purchasing a significant portion of their volume off SharedClarity contracts. And third, we use the findings of our clinical review team to help us to rationalize the number of products that we use.

The clinical review and contracting process went very well for our first three products. Every one of our members achieved double-digit cost savings on the contracts — it was the type of quantum leap of improved affordability that we were hoping for.

Our credibility with device manufacturers is based on the fact that the physicians are engaged not only in the process of evaluating the product, but also in its implementation. We don’t charge administration fees, and we are not structured like a group purchasing organization. And we have a committed model. When our supplier for drug-eluting stents signed the contract, they notified us it was the largest committed contract in the United States that they remember signing.

Something I didn’t expect is that we are a change management company, too. We are changing the processes and culture — administrative and physician engagement, joint decision-making — within our health system members and the medical device community.

Suppliers are in the process of trying to figure out the model of the future, and who they should partner with. Their relationship with physicians has changed. They realize that payers play an important new role, and they are working out how to engage with them. That is one reason why we have built a process that engages not only the payers but the providers, and creates an easy entry for them that way. They have been very receptive to what we’re doing, and we see ourselves as their future partners.

Our growth opportunities are global. UnitedHealthcare bought Amil [Brazil’s largest insurer and hospital operator]. This represents a fascinating opportunity — Amil is using some products that aren’t approved for the US. It’s good to gain some intelligence on those products, and to have an opportunity to do global contracts for medical devices. I think we’ll see more globalization of products, and the more options and competition we have, the better it is for patients.

Collaborative contracting Mark West

President, SharedClarity

The advent of SharedClarity is a very clear indication of the push that we’ve seen for some time now toward outcomes and value within health systems.

Perspectives

18 EY | Pulse of the industry

The second way is predicated on taking costs out of the system. In this scenario, how the actual medical technology is priced isn’t the main focus; what matters most is whether the product results in credible cost offsets that reduce the total cost of care.

This is the bar Johnson & Johnson’s Ethicon division is hoping to clear with Sedasys, its computer-assisted anesthetic delivery system for colon cancer and upper gastrointestinal screenings. Given the sophisticated automation underpinning Sedasys, the instrument can be used to deliver the anesthetic propofol in the absence of an anesthesiologist. (The gastroenterologist conducting the exam would oversee the drug’s delivery.) Johnson & Johnson estimates this will allow health care groups to cut colon cancer screening costs significantly, from an estimated US$600-US$2,000 to around US$150. Uptake of Sedasys, which launched in early 2014, has been modest, in part because Ethicon has deliberately chosen to make sure physicians are properly trained in how and when the device should be used before rolling it out more broadly.

Creating a new device like Sedasys requires companies assume significant manufacturing, engineering and R&D costs — it took over a decade to develop the instrument. But medtechs can also either refine their engineering processes to create simpler products that can be sold more cheaply, or shift manufacturing to markets where labor costs are lower. In fact, such cost-saving strategies are already in evidence in India and China, where both domestic and multinational medtechs are devising lower-cost, affordable products to treat the new and rapidly growing middle class in each country. (See “Sea change in China’s medtech industry” on page 20.) “The fact that the Chinese Government wants to

create a socialized health care system for 1.5 billion people is the largest opportunity in the world for medtech firms,” says Rob ten Hoedt of Eucomed and Medtronic.

As companies redesign and adapt their portfolios to develop products for emerging markets, they may take advantage of this “reverse product flow” to build no-frills, lower-cost products for use in developed markets. That’s what Smith & Nephew is doing via Syncera, an orthopedics-focused pilot that reduces the need for on-site technicians and other services associated with two key hip and knee replacement products. As a result of these changes, Smith & Nephew believes it can reduce implant costs by as much as 50%. The company first introduced the Syncera pilot in emerging markets; in August 2014, it launched a similar experiment in the US.

At the time of the US launch, CEO Olivier Bohuon told investors that the ultimate idea behind Syncera was to maintain margins by reducing prices on its orthopedic products in tandem with less intensive marketing, a process that was expected to play out over at least a year. So far, health care buyers are responding positively to the experiment: Bohuon noted that several customers were poised to sign multi-year Syncera contracts, despite its relative newness. “If you take a hospital that has 700 implants a year, over the three-year contract this hospital will enjoy net cash flow benefit of well over US$4 million,” he said.

The shape of things to comeIn an effort to stave off commoditization, companies must also rethink their branding strategies. They will need to move beyond product-specific branding

to developing messages that emphasize their customer-centricity, reliability and partnering capabilities. In essence, this beyond-the-product style of branding is a natural evolutionary step in an environment where the differences between individual products are perceived to be small or non-existent.

Moving forward, it will be interesting to see how — or if — medtechs will position themselves as brand builders. In other words, can the medtechs, via their products and services, help providers achieve top-quality care metrics that allow these care teams to attract more patients and build share in their own respective markets? By directly empowering care providers, medtechs that enhance the bottom lines of their customers give those buyers a very compelling reason to be loyal to specific medtech brands.

When it comes to charting a new course to differentiation, medtech companies have a range of options to consider, and a growing number of peers to emulate. Whatever strategies for differentiating differently companies ultimately adopt, they need to give themselves time to assess and analyze not just the nature of changing purchasing habits in their core markets, but the implications of those changes for their products.

The strategies we have set out here offer a good starting point for medtech companies as they consider the next steps they should take to grow their markets. If their products already demonstrate superior outcomes, for example, there is less pressure to embark on strategies that increase scope, whether that is through additional products or services. Note that superior outcomes alone may no longer be enough to sway buyers — especially if the innovation does not also fulfil a purchaser’s key objective to take costs out of the system.

Perspectives

19Medical technology report 2014

Case study

A sea change is occurring in China’s medtech industry. Since 2008, the Chinese market for medical devices has nearly doubled in size, and at US$16.1 billion is now second only to the US. Double-digit growth rates for medtech sales have put China at the forefront of multinational medtech companies’ strategies. But their enthusiasm comes with a note of caution: an evolving regulatory environment and government policies aimed at boosting the domestic industry mean that the path to market — already complicated — is not likely to become simpler. Meanwhile, many Chinese medtech companies have stepped up their investment in innovation, with an eye on the global market.

High-end in vitro diagnostics specialist Mindray Medical International, for instance, invests around 10% of its

revenues in R&D. Time Medical Systems, meantime, is a pioneer in the development of high-temperature superconducting (HTS) coil technology for use in clinical MRI scanners, while MicroPort is developing its own drug-eluting stents.

These companies, and a growing number of others, offer stiff competition for multinational companies’ products in China — and not just in terms of product sales. They are actively seeking M&A opportunities, both at home and internationally, in order to boost the quality of their product lines. In June 2013, Mindray acquired California company Zonare Medical Systems, an ultrasound technology specialist in the high-end radiology segment with sales teams in the US, Canada, Scandinavia and Germany. In the same month, MicroPort Scientific acquired OrthoRecon, the hip

and knee implant business of Tennessee-based Wright Medical Group, and announced that it would base its global orthopedic business in Tennessee.

Dr. Olaf Schermeier, Chief Officer for Global R&D at Fresenius Medical Care, understands the potential risks to his business model. “We are one of the largest renal care product providers in China, but competition will certainly come,” he says. “We should never underestimate local [Chinese] engineers.”

But equally, the skills learned by multinational companies in developing low-cost products for the Chinese market — and the agility they have had to maintain in keeping up with policy changes — will also add value in their home markets, where health reform and commoditization are now facts of life.

Sea change in China’s medtech industry

20 EY | Pulse of the industry

Perspectives

20 EY | Pulse of the industry

Why medtech should embrace commoditization

Rob ten HoedtChairman, Eucomed Executive Vice President & President EMEA & Canada, Medtronic

Guest article Perspectives

Western Europe currently spends €110 billion on health care. It has become clear that growth in health care spending cannot continue to outpace the growth of gross national product. If we don’t find a way to provide care in a completely innovative way, fewer people will have access to adequate care.

The drive to value in health care is behind the commoditization of medtech. And while only a small portion of spending currently goes to medical devices, the medtech industry will soon have a major role to play in care delivery if the drive to value transforms care in the way it should. There is massive potential in remote patient management, using smart IT and decision-making platforms to allow patients to live a healthy life at home. There are opportunities in data management and analysis to improve the consistency and quality of care. There are opportunities to incorporate robotics and nanotechnology. We can now deliver technologies and drug-device combinations at very small levels to precisely the places they are needed. A healthy environment for medtech is crucial for these developments.

We need to provide technologies that have clear health benefits, but we also have to prove that they have clear economic benefits. There is growing awareness that medical technology can offer value across the health system, but health care systems themselves have difficulty dealing with that. A product may be shown to decrease the cost of care after a patient is discharged, but it

may not be accepted because it slightly increases the cost of care in the hospital.

Clearly, debate and discussion need to happen between the medtech industry and health care providers to make sure that we are all focused on the total cost of care. As an industry, we can’t expect care providers to simply pay for the technology and then figure out themselves where the benefits will fall. If we are convinced of the benefits of our technologies, we may have to guarantee those benefits up front with a risk-sharing agreement. That will dramatically change our traditional business model, but it will also open up a much larger portion of the market and improve patients’ access to therapies.

We’re an engineering-driven industry, and that spirit needs to stay alive. If you only take economic values into account, you will never end up with something truly innovative. But the moment that technologies are created, all companies — whether they are small, medium or large medtech firms — need to initiate discussions about value.

If we in medtech are to genuinely improve delivery of care, we need to move beyond the transactional model and take more responsibility for patient outcomes. We should get paid when the desired outcome is achieved. The device is only part of the total solution for the patient. In diabetes, for example, patients may need an insulin pump, insulin, exercise and a healthy diet in order to get well. We need to do more than just supply the insulin pump. We need to become more active

in the delivery of care so that we can guarantee that those other activities are done properly and the maximum benefit of our technology is realized. Not only do we need to collect and share data, but we must also find ways to ensure that the appropriate care is delivered.

We can only achieve this if there is complete trust in what we do, among policy makers, payers, providers and patients. It is important for Eucomed to work with the European Commission to make sure that regulations for medtech optimize the quality of the technologies that come to market, but don’t stifle innovation, which would be equally devastating for patients.

As people start to pay more out of their own pockets for health care, they will demand more in return, at higher quality. Although we believe that patients should have a bigger say, medtech industry business models are predominantly focused on care providers, payers and regulators. One of our objectives at Eucomed is to create a dialog with patients so that we can build relationships, understand patients’ expectations and understand the language that we as an industry should start to use to communicate with patients.

Commoditization is a natural trend in any technology-based industry. But the medtech industry should not regard it as a threat. I would rather ask: How will medtech benefit from the opportunities this trend is creating?

We need to provide technologies that have clear health benefits, but we

also have to prove that they have clear economic benefits.

21Medical technology report 2014

Taking a new approach

José E. AlmeidaChairman, AdvaMed

Chairman, President and Chief Executive Officer, Covidien

Guest articlePerspectives

While innovating to save and improve lives will always be a central focus, economic pressures on providers, payers and other stakeholders are increasing, and the medical technology industry must find ways to reach beyond its core strengths of developing next-generation treatments and cures if it is to continue thriving.

Change has been rapid and sweeping. The Patient Protection and Affordable Care Act, growing pressures of cost containment, provider consolidation and other market forces are working to fundamentally alter the landscape. Changing incentives are prompting payers and providers to explore new payment mechanisms such as accountable care organizations, bundling and pay-for-performance that place a premium on delivering high-quality patient care with greater efficiency and lower costs. No less important, today’s patients — armed with the latest online intelligence and demanding the best modern care has to offer — are taking a more proactive role in their health care decision-making.

To meet these many challenges, medical technology companies need to take a new approach. Other than working to secure positive coverage policies, our industry has not traditionally engaged deeply with payers. Yet, we are uniquely positioned to partner with both payers and health care systems to redesign care, eliminate waste and improve patient outcomes. I believe our industry has both the ability and

foresight to leverage its strengths in new ways to partner with payers and provide value in a wider sense.

At Covidien, for example, we are piloting several new approaches to help health care systems meet the challenges of today’s highly dynamic health care environment.

One is our Project CARES (Covidien Analytics to Reduce Episode Spend) pilot program, which leverages the analytics expertise of our medical affairs team to help hospitals better understand why health care providers spend different amounts of money to care for patients with the same disease. Most hospitals do not have the data analysis infrastructure and specialized capabilities to identify and address this cost variation or the reasons behind it. By providing detailed analysis of a hospital’s end-to-end cost of care, Project CARES helps institutions identify opportunities to capture value through improving episode performance; benchmark how they are performing relative to their peers; and pinpoint areas with the largest potential for improvement.

Covidien is also looking at ways to help identify unnecessary variation in resource utilization. For example, in a pilot program conducted with Fairview Health Services in Minneapolis, we were able to develop appropriate standards and best practices for utilization of our products. Through this program, we have been able to help Fairview save a projected US$100,000

to US$200,000 per year through a shared-savings arrangement whereby our sales reps for select product areas serve as utilization managers. Under this program, payment for our offerings is based on appropriate utilization, not just on the amount sold.

These approaches recognize the shifting challenges facing providers today, and the results are positive for all parties. For such partnerships to work, however, all stakeholders must be willing to look beyond their traditional roles and experiment with new ways of collaborating. In addition to finding new ways to use the information we get from our day-to-day interaction with providers, there is an opportunity for medical technology players to create value by helping patients make better-informed care decisions. Covidien is partnering with United Healthcare on a pilot initiative to help patients in our workforce better understand the advantages of minimally invasive surgical approaches. We aim to see if this information incents patients to choose providers who have proven results in these approaches, which often have better outcomes at lower costs.

These programs and others that are beginning to emerge are just a start, but they show what might be possible. The challenge ahead will be to think of innovation in a way that looks beyond the next breakthrough product to additional ways that medical technology companies can partner with all stakeholders — patients, physicians, health care systems and payers — to develop solutions that will enhance care while benefiting the overall health care system.

Innovation has long been a hallmark of the medical technology industry. The groundbreaking products created by entrepreneurial device and diagnostics companies have led to remarkable improvements in patient outcomes over the last several decades. Fueled by research and development budgets that are more than twice the average for other US industries, the device industry continues to frequently bring new and improved iterations of products to market.

22 EY | Pulse of the industry

Strength, resilience and energyJohn J. Greisch

President and Chief Executive Officer, Hill-Rom

In the Belgium contest, Tim Howard made a World Cup record-setting 16 saves. His performance, gritty determination and commitment to the game — and to his team — made for great drama. Howard has a reputation for playing through pain; his resilience, strength and energy serve as a metaphor for what it will take for medical technology companies to succeed in the future.

The environment for medical technology companies continues to be challenging. The uneasy global economy and volatile health care market mean our customers face unprecedented pressure.

In our more mature markets, hospitals everywhere are looking for ways to reduce costs. More than ever before, hospitals are being thoughtful about the level of service they want to provide, deciding what is essential and what isn’t; they are looking for what truly will make a difference in outcomes, and discarding what will be merely incremental. In developing markets, the circumstances are different, but governments and payers are asking the same question: How can they deliver optimal care to the most people for the least cost?

To be successful in the coming years, the medical technology industry must be laser-focused and bring the strength, resilience and energy Tim Howard embodies to the health care arena. In particular, we must:

Retain strong focus on what’s best for patients and caregivers. Intense business and regulatory pressures can sometimes divert our attentions from

the premier reason we exist — to improve the lives of patients and caregivers through our innovative technologies. If we keep our focus where it should be, the associated metrics on cost, quality (including patient engagement and patient satisfaction) and outcomes are likely to be more easily addressed. For example, numerous studies show that encouraging patient mobility not only helps improve patient outcomes, but also has a positive effect on a hospital’s bottom line. At Hill-Rom, we’ve designed a progressive mobility program to help make it easier for hospitals to get ICU patients moving as quickly as possible. The program is built on the most recent clinical evidence, checked by national thought leaders, and provides the practical tools necessary to improve patient mobility.

Empathize with the customer. The reimbursement landscape has changed fundamentally. Hospitals and clinicians everywhere resonate with the mantra of “doing more with less.” In more developed markets, the payment incentive structure emphasizes quality, access and choice — but generally not volume. This paradigm shift is taking place where the difference between “victory and defeat” is a margin of 2% or less, so workflow efficiency is a key area of strategic focus. Today, more than ever, medtech partners will distinguish themselves by fully appreciating, articulating and responding to their customers’ needs. One big need: reducing hospital-acquired infections, which in the US are estimated to cost up to US$45 billion annually. To help hospitals, Hill-Rom has created a software program using locating technology to help