Embed Size (px)

Citation preview

BscB(IM) 6. Semester

Author: Ida Fosso Jacobsen Supervisor: Sudarshan Kumar Pillalamarri

A Financial and Strategic Analysis of

Norwegian Air Shuttle ASA

Department of Business Studies

Aarhus School of Business

03.05.2010

Abstract

The purpose of this thesis is to analyse Norwegian Air Shuttle ASA, and their economic

performance with help from both a financial and a strategic analysis. Norwegian will be

benchmarked against their largest competitors in the Norwegian and European market, being

SAS Scandinavian Airlines and Cimber Sterling, in order to conclude on how Norwegian

really is performing. The thesis will be based on public available information such as annual

reports in period 2005-2009, and newspaper articles.

Norwegian is the largest low cost airline company in Scandinavia, and the fourth largest in

Europe. They are operating to 85 destinations and 27 countries within Europe, Dubai and

Marrakech. From 2008 to 2009, Norwegian had a growth of 18% in passenger number which

caused an increase of 17.4% in their revenues. This is investigated further in the financial

analysis where Norwegian`s income statement, balance sheet, cash flow statement and key

ratio calculations are being analysed with the purpose of examining their economic

performance and to see if Norwegian has any liquidity problems. The fact that Norwegian in

November 2009 issued shares giving them about 250 million in new capital, and the major

investor HBK Holding (the owner is Norwegian`s CEO) sold some of their shares in the same

period, caused concerns around their financial situation. Especially, since Norwegian is

scheduled to receive 70 newly purchased and leased airplanes during 2008-2014. This is a

step towards them meeting their goal to further decrease their unit costs that will enable them

to continue to offer low prices, and still generate a profit. Both ROIC and Asset Turnover

show that Norwegian could be more effective in utilizing its assets, and the liquidity analysis

shows that Norwegian have problems paying both their current and non-current obligations,

taxes and interest rates.

The strategic analysis focuses on external factors that influence the airline industry such as oil

price and exchange rate. Both of these factors have fluctuated significantly over the last years,

not in a beneficial way. A higher oil price increases unit costs, as fuel is one of the major costs

in the budget, whereas a stronger dollar would not benefit as most of the suppliers trade in this

currency. It is also focused on the fierce competition within the airline industry, which is why

having as low unit costs as possible is important in order to be able to generate a profit.

Based on the financial and strategic analysis it can be concluded that Norwegian is a better

investment possibility than their major competitors SAS and Cimber Sterling.

Table of contents

1

1: Introduction.............................................................................................................................5

1.1: Problem statement................................................................................................................5

1.2: Limitations...........................................................................................................................6

1.3: Structure...............................................................................................................................6

1.4 About Norwegian Air Shuttle ASA......................................................................................7

2: Financial Statement Analysis..................................................................................................8

2.1: The European Airline Market..............................................................................................9

2.2: Income statement...............................................................................................................12

2.2.1: Operating Profit (EBIT)..........................................................................................13

2.2.2: Profitability.............................................................................................................15

2.2.3: Conclusion on the income statement......................................................................17

2.3: Balance sheet.....................................................................................................................18

2.3.1: General overview of the balance sheet...................................................................18

2.3.2: Net working capital.................................................................................................20

2.3.3: Liquidity analysis....................................................................................................21

2.3.4: The Share................................................................................................................23

2.3.4: Conclusion on the balance sheet.............................................................................24

2.4: Cash Flow Statement ........................................................................................................25

2.4.1: Cash Flow from operating activities.......................................................................25

2.4.2: Cash Flow from investing activities.......................................................................26

2.4.3: Cash Flow from financial activities........................................................................27

2.4.4: Change in cash........................................................................................................27

2.4.5: Cash flow ratios......................................................................................................28

2.4.6: Conclusion on the cash flow statement..................................................................30

2.5: Conclusion on the Financial Statement Analysis..............................................................31

3: Strategic Analysis.................................................................................................................32

3.1: PESTEL analysis...............................................................................................................32

3.1.1: Political Aspects.....................................................................................................33

3.1.2: Economical Aspects................................................................................................33

3.1.3: Socio-cultural Factors.............................................................................................34

3.1.4: Technological Factors.............................................................................................34

3.1.5: Environmental Aspects...........................................................................................34

3.1.6: Legal Aspects..........................................................................................................35

2

3.1.7: Summary of the PESTEL analysis..........................................................................36

3.2 Porters 5 forces...........................................................................................................36

3.2.1: The threat of potential new entrants......................................................................37

3.2.2: The bargaining power of suppliers........................................................................37

3.2.3: The bargaining power of buyers.............................................................................38

3.2.4: The threat of substitutes..................................................................................38

3.2.5: The extent of competitive rivalry...........................................................................39

3.2.6: Summary of Porters 5 forces analysis...................................................................39

3.3: Conclusion on the strategic analysis – SWOT analysis.....................................................40

3.3.1: Strengths.................................................................................................................40

3.3.2: Weaknesses.............................................................................................................41

3.3.3: Opportunities..........................................................................................................41

3.3.4: Threats....................................................................................................................42

4: Conclusion on the Strategic and Financial Analysis of Norwegian.....................................43

5: Bibliography....................................................................................................................45

6: Appendix7

Appendix 1: Norwegian`s route network

Appendix 2: Norwegian`s revenue: domestic and international

Appendix 3: Norwegians fleet 2009-2014

Appendix 4: Overview oil price in period 2005-2009

Appendix 5: Overview exchange rate USD/NOK in period 2005-2009

Appendix 6: Overview of the share development for Norwegian in period 2005-2009

Appendix 7: Norwegian Air Shuttle ASA corporate structure

Appendix 8: Cimber Sterling corporate structure

Appendix 9: Scandinavian Airline Group corporate structure 2009

Appendix 10: Norwegian: Income Statement 2005-2009

Appendix 11: Norwegian: Balance Sheet

Appendix 12: Norwegian: Cash Flow Statement

Appendix 13: Norwegian: Traffic Figures

Appendix 14: Norwegian: Calculations

Appendix 15: Norwegian: Share

Appendix 16: Norwegian: Key ratios

Appendix 17: SAS: Income statement 2005-200957

3

Appendix 18: SAS: Balance Sheet

Appendix 19: SAS: Cash Flow Statement

Appendix 20: SAS: Traffic numbers

Appendix 21: SAS: Calculations

Appendix 22: SAS: Cash Flow ratios

Appendix 23: SAS: Share

Appendix 24: Cimber Sterling: Income Statement 2004/2005-2008/2009

Appendix 25: Cimber Sterling: Balance Sheet

Appendix 26: Cimber Sterling: Cash Flow Statement

Appendix 27: Cimber Sterling: Calculations

Appendix 28: Cimber Sterling: Key ratios

1: Introduction

4

The financial crisis has hit the air traffic industry hard. The International Air Traffic

Association write in their report that 2009 has been the worst year for the industry since the

second world war, with a decline in overall passenger demand of 3.5%. This will lead to a

total loss of 11 billion US Dollars for the industry (IATA, 2010).

However, the market can see a clear change in buying behaviour where people tend to be

more cost oriented. Low cost companies such as Norwegian Air Shuttle ASA, from now

referred to as Norwegian, are experiencing growth and an increase in market share compared

to companies such as SAS, known for having higher prices, which are having huge economic

problems. This can clearly be seen in Norway where SAS has lost a substantial part of their

domestic market share to Norwegian over the last years.

In November 2009, Norwegian`s board decided to issue up to 1 620 000 new shares, which

will give them around NOK 250 million kroner in new capital. At the same time, HBK

Holding AS, the major investor in Norwegian, announced that they are selling 970 000 shares

in the company. Norwegian`s CEO, Bjørn Kjos which also is the main owner of HBK

Holding AS, says that this is done because the company wants to strengthen their equity and

be prepared for new growth possibilities in the future1.

1.1: Problem statement

The purpose of this thesis is to look at the economic performance of Norwegian Air Shuttle

ASA and external factors that might influence the air shuttle industry. Norwegian and the

board’s decision on issuing new shares will be the focus of this report, to see if the company

have liquidity problems. When a company is issuing new shares and insiders within

Norwegian are selling shares at the same time, it can make potential investors nervous and be

a sign that something significant is about to happen.

This will be investigated with help from these questions:

- Analyse the financial situation for Norwegian Air Shuttle ASA by looking at the

income statement, balance sheet and the cash flow statement in years 2005-2009.

- Calculate and analyse key ratios to look at the economic performance of Norwegian.

- Which external factors are affecting Norwegian?

1.2: Limitations

1 Andersen, Tor Øyvind; Brander, Anna Sandvig: http://e24.no/boers-og-finans/article3359145.ece

5

The thesis will only focus on the European air shuttle market, which is the market where

Norwegian mainly is operating. The thesis will compare Norwegian against their two largest

competitors in the Scandinavian and European market, Cimber Sterling ASA and

Scandinavian Airlines AS (SAS). It is important to be aware of that SAS is not a low cost

airline company, but are included as this is Norwegian`s biggest competitor in the

Scandinavian market.

All the information about Norwegian, SAS and Cimber Sterling has been collected from their

annual reports in years 2005-2009, and for Norwegian interim report 2009 as their annual

report for 2009 not yet has been published. Information is also collected from Norwegian

newspaper articles, since there has been no contact with the companies. No information has

been collected after April 5, 2010. In the financial analysis SAS`s numbers are in billions,

while Norwegian and Cimber Sterling`s numbers are in million.

1.3: Structure

Section 2: Financial Statement Analysis

In the economic part of the thesis, numbers from the annual report over the five past years

(2005–2009) and interim reports (2008-2009) will be used. First the income statement,

balance sheet and the cash flow will be analysed to see if there are any large changes that we

should be concerned about. Further on the most relevant key ratios for the paper will be

calculated and used when analysing Norwegian`s performance and liquid situation. Even

though the accounts look good, they may in some cases show a misleading picture of the

actual situation, and therefore analysing key ratios are important as it gives a more accurate

analysis and gives a clearer picture of the actual situation. Therefore measuring the

profitability and liquid situation of Norwegian and its competitors will be the focus in this

paper. In the profitability analysis, the DuPont method will be used to measure ratios as ROIC

and ROE. Liquidity analysis is in focus in this thesis, as it looks at if a company is able to pay

its short term debt.

A comparison between Norwegian and Cimber Sterling and SAS will be created by using key

ratios, because then we can see how Norwegian is performing compared to their competitors.

Section 3: Strategic Analysis

6

The thesis will continue with a strategic analysis of the external factors influencing

Norwegian. Methods as the PESTEL analysis and Porter`s 5 Forces will be used to look at the

environment surrounding the organisation. The PESTEL analysis will be created as a list of

the political, economical, socio-cultural, technological, environmental and legal aspects of the

environment the companies are in. Porter`s 5 forces will be used to look at the competitive

environment surrounding Norwegian. The internal part of the strategic analysis is excluded as

there has been no personal contact with Norwegian, but instead strengths and weaknesses are

being included in the SWOT analysis.

1.4: About Norwegian Air Shuttle ASA

Norwegian Air Shuttle ASA was established January 22, 1993 as a company supposed to

continue “Busy Bee of Norway AS” air traffic on the west coast of Norway in cooperation

with Braathens S.A.F.E. In 2002, Norwegian decided to expand and to establish themselves as

a strong player in the domestic air travel industry within Norway, dominated at that time by

Scandinavian Airlines (SAS). Norway is an attractive market due to the large geographical

distances, and the routes between Oslo-Trondheim and Oslo-Bergen is on the list of busiest

routes within Europe. Norwegian decided to establish themselves as a low cost carrier and

started operating on the four busiest routes from Oslo to Trondheim, Bergen, Stavanger and

Tromsø with leased Boeing 737 300 airplanes. The beginning of 2000 was affected by a

recession and travellers were therefore interested in the increased competition and the lower

prices offered by Norwegian2.

Norwegian are following a low cost strategy, where they seek to offer their broad target group

of customers the lowest possible price. This is said to be their competitive advantage. Their

business idea turned out to be successful and had the perfect timing during the financial hard

times, and only after a few months their market share was between 10%-15%. In 2003 they

were listed on the Oslo Stock Exchange, and have since then expanded with both new

domestic and international routes, operating out of new places such as Warsaw in Poland,

Stockholm in Sweden and Copenhagen in Denmark. The company has also used their brand

name to start up other companies as can be seen from their corporate structure (appendix 7).

Bank Norwegian is an internet bank they own 20% of, and Call Norwegian AS that offers

cheap phone and broadband subscriptions, is 100% owned.

2 http://www.norwegian.com/about-norwegian/facts/history/

7

In 2007 they entered into an agreement with Boeing to purchase and lease total of 70 (48

owned, 22 leased) new aircrafts of type 737 800 aircraft in the period 2008 to 2014 (Appendix

3). The new planes will fit into their new strategy of a lower cost base since the new airplanes

have lower maintenance costs and fuel consumption. The plan is to deliver back the leased

airplanes when the rest of the new fleet are delivered by 2014.

Today (April 2010) Norwegian is the biggest low cost airline company in Scandinavia and the

fourth largest in Europe. Their business idea is to give everyone the possibility to travel by air

which is why they follow the low ticket prices strategy. Their goal is to establish themselves

as the preferred supplier of air travelling in selected markets (Annual report 2008; p8).

Norwegian is constantly opening new routes and by end 2009 they has 238 routes to 93

destinations across Europe, North Africa (Marrakech) and Middle East (Dubai) (Appendix 1)

with total of 10.8 million passengers in 2009, a growth of 18% from previous year.

2: Financial Statements Analysis

When analysing financial statements, historical data from the last five years are included to

get an overview of a company’s economical performance. The purpose of this is to discover

the financial value drivers that give the company economic value, and calculating key ratios

will help us find these factors. It is important to get an overview of the statements and to

calculate key ratios, because in some situations a company can make financial statements look

better than the actual situation is (Sørensen; 2009).

Financial statements are divided into income statement, balance sheet and cash flow statement

and they all give us economic information from different aspects. Calculating financial ratios

is important in order to measure the performance of a company, either how productive or how

profitable it is and their liquidity situation. Key ratios are however useless, if not

benchmarked to either a company’s performance over several years, the overall industry, or

another company within the same industry. Such data can create a useful insight of the

company’s performance and find strengths, opportunities, threats and weaknesses. Norwegian

will be compared against two of their biggest competitors, SAS and Cimber Sterling, where

numbers from past five years are used. There are many ratios that can be used to analyse a

company’s performance, and I have chosen to calculate ratios important to this company that

will explain the economic situation and answer the problem statement (Møller 1991).

8

In this thesis years 2005 to 2009 will be analysed and then key ratios will be calculated.

However, in the key ratio analysis only years between 2007 and 2009 will be analysed as this

is concluded to give sufficiently accurate result. Norwegians Annual report 2009 has not yet

been published, therefore analyses of the balance sheet and cash flow statement is not done

for this year, which also affects some of the key ratios. The financial reports for Norwegian

and SAS are following IRFS, but only accounting years from 2006/2007 are IFRS for Cimber

Sterling and therefore previous years will not be analysed.

Consolidated financial statements are a common statement for the parent company and all its

subsidiaries, and are being used in this analysis because it can be seen that all the subsidiaries

within the group are more or less related to the same activities (Appendix 7, 8, 9). However

we have to be aware of that the consolidated statement often gives higher productivity for

each company and that its performance might look better than the actual situation (Schack

2002: p 245).

2.1: The European Airline Market

As stated earlier; the thesis will focus on the European airline market. This broad market

includes both business and pleasure travellers in order to identify as many strategic options as

possible (Lynch 2006: p 81).

Norwegian has had a huge increase in both passengers and revenue over the last years,

carrying close to 11 million passengers in 2009. This increase of 18% from 2008 is related to

the increase in market share in both the Norwegian domestic market and the low cost routes to

the most popular destinations in Europe. The Norwegian market is duopoly, with Norwegian

and SAS as the only operators and their market share development over the last years can be

seen in figure 1. Norwegian has increased their market share in all years, while SAS has

experienced a decrease in market share through the same period. Cimber Sterling`s traffic

numbers is not analysed.

9

Figure 1: Market share development for SAS and Norwegian from 1. tertial innland og utland:

http://www.avinor.no/avinor/trafikk/20_Reisevaner

Figure 2 shows the market share development for airline travel from Norway to destinations

abroad in year 2005 and 2009. The same development as in figure 1 can be seen here. In 2005

SAS was clearly the largest operator followed by Norwegian and KLM. A change can be seen

in 2009 as Norwegian has increased their market share whereas both SAS and KLM

decreased theirs. This indicates that in the recession, low cost airline companies were choosed

over the more traditional airline companies.

2005

NorwegianSASKLMRyanairLufthansaOther

2009

NorwegianSASKLMRyanairLufthansaOther

Figure 2: Market share from airline travel between Norway and destinations abroad. Numbers are from:

http://www.avinor.no/avinor/trafikk/20_Reisevaner

In order to understand Norwegian and how they are operating compared to their competitors,

their cost base it is important to look at (Appendix 13, 20). Norwegian`s numbers of airplanes

and routes have increased over the years, as have capacity/production (Available Seat

Kilometre (ASK)). An overview of Norwegian`s and SAS` unit costs and yield can be seen in

10

figure 3. Norwegian`s yield (income per passenger kilometre) for 2009 has been decreasing

compared to 2008 to 0.60, even though there has been a growth in passengers. This is caused

by the increase in fuel cost, increasing distances and massive cuts in ticket prices. SAS on the

other hand has had a stable yield at 1.22 in period 2007-2008.

Remaining successful in the highly competitive industry is all about having as low unit costs

per seat per kilometre as possible3. Unit costs are affected by external events as fuel price,

distribution costs, airport charges and internal costs as staff costs, type of airlines used and

destinations (Doganis; 2002 p 103). Norwegian`s unit costs have decreased 13% from its peak

in 2008 at 0.56 to 0.49 in 2009. The decrease in units cost has been due to the decrease in fuel

price and exchange rate in dollars and euro since 2008. Ryanair, a company Norwegian does

not see as a major competitor as they have flights to remote airports, has unit costs at 0.29.

Norwegian is expecting their unit costs to continue to decrease to a level below 0.40, when

they are replacing their fleet with all new and more environmentally friendly aircraft that will

yield higher capacity and lower pollution.

2007 2008 20090

0.2

0.4

0.6

0.8

1

1.2

1.4

Norwegian unit costsNorwegian yieldSAS unit costsSAS yield

Figure3: Overview of unit costs and yield for Norwegian and SAS from Annual Report 2007-2009

Figure 3 shows that Norwegian is a low cost based airline company compared to their

competitor SAS, which has both higher unit costs and yield. SAS has historically been one of

the companies with the highest unit costs, but has been forced to decrease its unit costs when

the low cost airlines were established to keep up with the competition and generate a profit.

SAS has tried to compete by offering lower prices, however, this strategy failed as SAS has a

higher cost base, and Norwegian replied by decreasing their prices even more. Therefore SAS

3 Kaspersen, Line: http://www.dn.no/forsiden/naringsliv/article1836896.ece

11

is focusing on a different strategy offering faster check in, free coffee/tea, newspapers, bonus

card and advantages from their membership in Star Alliance for their customers (SAS Annual

Report).

2005 2006 2007 2008 2009 -

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

NorwegianSASCimber Sterling

Figure 4: Own creation from Annual Reports for Norwegian, SAS and Cimber Sterling in period 2005-2009.

The overview of the three companies’ revenues in period 2005-2009 (Figure 4) shows that

SAS clearly has the highest revenues of Norwegian and Cimber Sterling. However, their

revenues have been decreasing in the period compared to both Cimber Sterling`s and

Norwegian`s which has had large growth in last five years. This again indicates that low cost

companies such as Norwegian and Cimber Sterling have increased their revenues in the

recession, while the traditional airline companies with higher cost bases such as SAS have had

problems. The explanations behind this development will be analysed further in the income

statement.

2.2: Income statement

The income statement reports how shareholders` equity has increased or decreased as a result

of operating and financial activities for a specific accounting period. Operating activities are a

company’s primary activities that create value to a company, while financial activities are

activities not directly related to the area of business (Pennan: 2001, p 32). Norwegian`s

operating revenues are all included in the income statement being ticket sales, other passenger

related revenues, and other revenues (table 1).

12

2.2.1: Operating Profit (EBIT)

The equation operating profit, also called earnings before interest and tax (EBIT), is a result

of revenues minus expenses:

Operating profit=Revenues−expences

Operating profit is analysed more closely in order to get a more accurate overview of where

Norwegian`s revenues and expenses come from.

2009 2008 2007 2006 2005Ticket revenue 6 389 406 5 641 533 3 956 000 2 879 400 1 931 663 Other passenger related revenue 788 655 463 609 212 000 62 000 40 583 Other revenue 131 129 121 271 58 202 Total operating revenues 7 309 189 6 226 413 4 226 202 2 941 400 1 972 246 Operational expences 4 318 731 4 892 727 3 171 818 2 368 636 1 504 338 Payroll 1 303 299 1 076 068 622 189 412 940 298 223 Depreciation, amortization and impairment 148 882 129 611 74 044 51 070 29 316 Other operating expences + leasing 966 411 318 094 224 200 139 264 111 091 Other losses/gains 147 767 Total operating expences 6 737 323 6 564 267 4 092 251 2 971 910 1 942 968 Operating profit (EBIT) 571 866 (337 854) 133 951 (30 510) 29 278 Profit (loss) after tax 446 251 3 944 84 580 -21 997 27 980

Table 1: Summary of income statement Norwegian; Annual reports 2005 – 2008, Interim report 2009 Q4.

Norwegian`s revenues have had a steady increase over the years mostly connected to the

growth in passengers. In appendix 2, an overview of how their revenues are divided between

domestic and international travels can be seen. In 2009 revenues coming from domestic

travels increased 26% since 2008, compared to 12% within the same period on international

travels. The income statement to Norwegian are dividing their total operating revenues into

ticket revenues, other passenger related revenues and other revenues as it is related to fees and

third party products. Total operating expenses has also had an increase over the years. Other

operating expenses + leasing costs and depreciation are both increasing due to prepayments

and purchase of new airplanes and also the increased oil price. The growth in production

(ASK) and the acquisition of Norwegian Air Shuttle Sweden AS in 2007 are said to be the

main reasons for the increase in both expenses and revenues.

Norwegian has had a varied operating profit (EBIT) over the years, leading to negative results

in both 2006 and 2008 where expenses are exceeding revenues. These years are also giving

loss (2006) and extremely low profit (2008), which can be explained by the sudden increase

in production (ASK) and passenger traffic and therefore the need to utilize 19 airplanes the

13

last quarter compared to 14 normally. Profit after tax has never been better for Norwegian

than in 2009. The huge increase from 2008 is mainly due to the increase in production and

market share in the Norwegian and the European market.

SAS 2009 2008 2007 2006 2005Total operating revenues 44 992 53 052 50 671 60 924 62 688 Total operating expences 48 074 53 817 49 378 59 651 61 315 Operating profit SEK -3 082 -765 1 293 1 273 1 373 Profit (loss) after tax -2 947 -6 321 636 4 740 255 Cimber Sterling 2008/2009 2007/2008 2006/2007Total operating revenues 1 297 757 1 193 046 970 791 Total operating expences 1 299 476 1 119 503 917 197 Operating profit DKK -1 719 73 543 53 594 Profit (loss) after tax -58 925 56 007 25 845

Table 2: Summary of income statement: SAS Annual report 2005-2009; Cimber Sterling Annual report 2008/2009

SAS as a traditional airline company has had a decreasing development in both revenues and

expenses which lead to a negative operating profit and loss after tax in years 2008 and 2009.

Reasons behind this negative development are the decreasing ASK (production), as a result of

the increased competition and loss of market share. Because of the negative results, SAS is

dependent on new capital to survive. Therefore they managed to convince their owners in

2009 (government in Norway, Sweden, Denmark) to give new capital of 6 billion SEK, but

this didn’t help the company that again are in financial trouble. The group has again asked

their owners for SEK 5 billion in new capital. The owners will oblige, but in return are

expecting a stronger financial position next year with SAS cutting their costs drastically4.

Cimber Sterling as a low cost company has had an increase in both their revenues and

expenses over the years. In 2008/2009 expenses are exceeding revenues which cause a

negative operating profit of DKK -1 719 million and a loss after tax. This is explained by

Cimber Sterling Group AS taking over the bankrupted airline company Sterling Airlines AS

in this accounting period. In this connection the group expanded as a step towards them being

a bigger and more dominating actor in the European airline market. Investments in new

planes, new staff and marketing of the company are expenses that dominated this year. Loss

after tax this year is also explained from an increase in financial expenses, caused by the

increased exchange rate USD/DKK on their loans.

4 Sparre, Martin Riber; Kaspersen, Line: http://www.dn.no/forsiden/borsMarked/article1834613.ece

14

2.2.2: Profitability

When measuring profitability ratios we will look at if the company are earning enough in

order to generate a satisfying profit (Penman: 2001, p 366). When analysing Norwegian, the

profitability key ratios will be based on Return on Equity (ROE). This is done because it can

be further decompounded into financial leverage and Return on Invested Capital (ROIC) in

the DuPont analysis.

Assets

Turnover

ROIC Profit

MarginROE Financial

Leverage

Figure 5: Three step DuPont decomposition from Sørensen: 2009: p.255, adjusted by me

The DuPont model (figure 5) is used in this thesis because it is a good approach to use when

determining factors influencing Norwegians profitability. It decomposes Return on Equity

(ROE) in two components being ROIC and financial leverage, where ROIC are further being

decomposed into assets turnover and profit margin. The ratios except profit margin will need

numbers from the balance sheet (assets and equity), but are included in the DuPont analysis as

it is explaining how effective and profitable a company is. Financial leverage is a ratio that

analyses to which degree net operating assets are financed by net financial obligations or

equity, and therefore this ratio will be calculated and analysed in the liquidity analysis

(Pennan 2001: p 354) (Sørensen 2009: p 255).

Key ratio 2009 2008 2007 2006 2005ROE (%) 35,7 % 0,6 % 22,0 % -10,9 % 19,8 %Return on Invested Capital (ROIC) 12,3 % 0,2 % 4,6 % -2,6 % 0,07Profit Margin (%) 6,1 % 0,1 % 2,0 % -0,7 % 1,4 %EBIT Margin (%) 7,8 % -5,4 % 3,2 % -1,0 % 1,5 %Asset Turnover 1,46 1,96 1,81 2,77 2,92

Table 3: Key financial ratios Norwegian: calculations with guidelines from “Den Danske Finansanalytikerforening” (The Danish Society of Investment Professionals)

15

Return on Equity (ROE) is the first ratio to investigate in the profitability analysis. It is used

to see what profit shareholders can expect compared to other investments possibilities e.g. the

interest rate you get in the bank (around 3% - 4%). Norwegian`s ROE have been changing

over the last years, with a close to zero result in 2008 which reflects the same development as

profit/loss for the specific year. However, in the other years ROE has been high, including

2009 where it is 35.7%, giving a good payoff compared to other investments possibilities.

Even though Norwegian`s expected return in most of the accounted years is good,

shareholders need to consider the risk of losses as the airline industry are highly competitive

and therefore also risky. Normally, industries that are risky give a higher ROE, and it is

therefore important to take risk in consideration, as the money could be placed in a bank at a

interest rate that is more or less stable.

Return on Invested Capital (ROIC) measures how operational efficient a company is using its

available assets, excluding how the company is financed. This is why ROIC is such a good

ratio for comparing companies that might have different structures. ROIC are in 2008 0.2%,

and in 2009 12.3% which is a good development for the company. ROE are automatically

affected by ROIC, and therefore the bad ROIC in 2008 can explain the bad ROE the same

year. We should therefore take a deeper look at ROIC to see what could be the reason for

these negative ratios, which is why ROIC are further decomposed into profit margin and

assets turnover.

Profit margin explains how much of the revenue that creates profit and how much that are left

to cover tax, interest e.g. The table shows that Norwegian`s profit margin are at a level of

0.1% in 2008 and 6.1% in 2009. In 2008, Norwegian has had a low profit after tax that can

explain the low profit margin. Assets turnover is an activity ratio that explains how efficient

the company utilizes its assets to produce revenue; how operationally efficient the company

is. If this ratio is high, it could mean that the company is managing to use its assets efficiently

to generate sales and profits. Norwegian does not have the highest ratios and the fact that they

are decreasing over the years indicates that Norwegian is not that operationally efficient.

Since operating profit were analysed in the first part of the income statement, EBIT margin is

included in the ratio analysis. It is a good ratio to use when comparing companies within the

same industry to see how effective they are and how much they have grown over the years.

As EBIT margin is comparing revenues and expenses, this ratio is negative in 2008 as

16

expenses exceeded revenues this year. In the other years it looks good and the ratio is

increasing, which shows that they have grown over the years.

SAS 2009 2008 2007 2006 2005ROE -29,4 % -48,9 % 3,8 % 33,3 % 2,1 %ROIC -7,0 % -15,2 % 1,3 % 9,6 % 0,5 %Profit Margin -6,6 % -11,9 % 1,3 % 7,8 % 0,4 %EBIT Margin -6,9 % -1,4 % 2,6 % 2,1 % 2,2 %Asset Turnover 1,06 1,22 1,04 1,19 1,08Cimber Sterling 2008/2009 2007/2008 2006/2007ROE -32,5 % 27,7 % 12,7 %ROIC -0,05 % 0,05 % 0,03 %Profit Margin -4,5 % 4,7 % 2,7 %EBIT Margin -0,1 % 6,2 % 5,5 %Asset Turnover 1,19 1,14 1,11

Table 4: Key ratios SAS and Cimber Sterling

Norwegian`s profitability key ratios are compared against SAS` and Cimber Sterling` to see

how well they are performing and how efficient they are. Both SAS and Cimber Sterling has

the same development as their ROE, ROIC, profit margin and EBIT margin are all negative

over the last year. This is not a positive development and it can be concluded that they are not

profitable or using its available assets as efficient, because they have not created any profit

over the last years. A potential investor will need to consider the risk as an investment has not

lead to any payoff in 2009.

2.2.3: Conclusion on the income statement

Despite the competitive market and the economic recession, Norwegian experienced 2009 as

one of their best years with a continued growth in revenues (17.4%), EBIT and profit after

tax. The growth is related to the increased in ticket sales, which was expected as the company

has continued to increase their market share both domestically within Norway and in the rest

of Europe. Due to investments in a new fleet, their expenses also increased over the last years.

The profitability analysis was made on the background of the DuPont analysis where ROE

where decomposed into ROIC as was further decomposed into profit margin and assets

turnover. Many of the key ratios for Norwegian are in 2008 low due to the decrease in profit

after tax this year. However, the ratios in 2009 are good. Return on Equity (ROE) is at a high

level in 2009, meaning that shareholders can expect higher return than from other investments

possibilities. Because of the fluctuating numbers through the years, this has to be seen in

connection with the high level of risk there is to invest in a competitive market like the airline

industry. ROIC and asset turnover analyses show how efficient Norwegian is using its assets

17

to create revenue. ROIC are at a low level but show an increasing tendency compared to

previous years, whereas asset turnover is at a decreasingly low level, indicating that there are

room for improvement. Profit margin is increasing and at a high level in 2009, meaning that a

large amount of the revenue creates profit, and that there are some left to cover tax and

interest rates.

SAS and Cimber Sterling have negative ratios in ROE, ROIC, profit margin and EBIT margin

in 2009. This indicates that Norwegian has better efficiency and profitability ratios than their

competitors, being better at utilize its assets and create profit. However, further analysis with

liquidity ratios is necessary in order to come up with a final conclusion.

2.3: Balance Sheet

The balance sheet is listing a company`s assets, equity and liabilities in a given period of time,

and are used when investigating a company’s liquidity and financial leverage. Assets are

investments expected to generate future profit, equity are the claims by the owners and

liabilities are claims to the payoff from the assets by claimants other than owners. Both the

assets and liabilities are divided into current and non-current, where current are

generating/pay cash within a year and non-current are long term obligations (Pennan 2001: p

28). To sum up, the balance sheet is an overview of the company’s investments and claims on

return of these investments, and as the equation states: shareholders equity equals the

difference between assets and liabilities:

Equity=Assets−Liabilities

The focus of this report will be on the balance sheet and the cash flow statements financial

ratios as it is measuring liquidity, as the purpose of this thesis is to analyse Norwegian and

their financial situation.

2.3.1: General overview of the balance sheet

2009 2008 2007 2006 2005Assets 5 021 964 3 178 884 2 331 097 1 061 944 675 822 Liabilities 3 420 254 2 281 515 1 822 824 801 217 534 236 Equity 1 601 710 897 368 508 273 260 727 141 586

Table 5: Balance sheet for Norwegian; Source: Annual Report 2005-2008, Interim report Q4 2009.

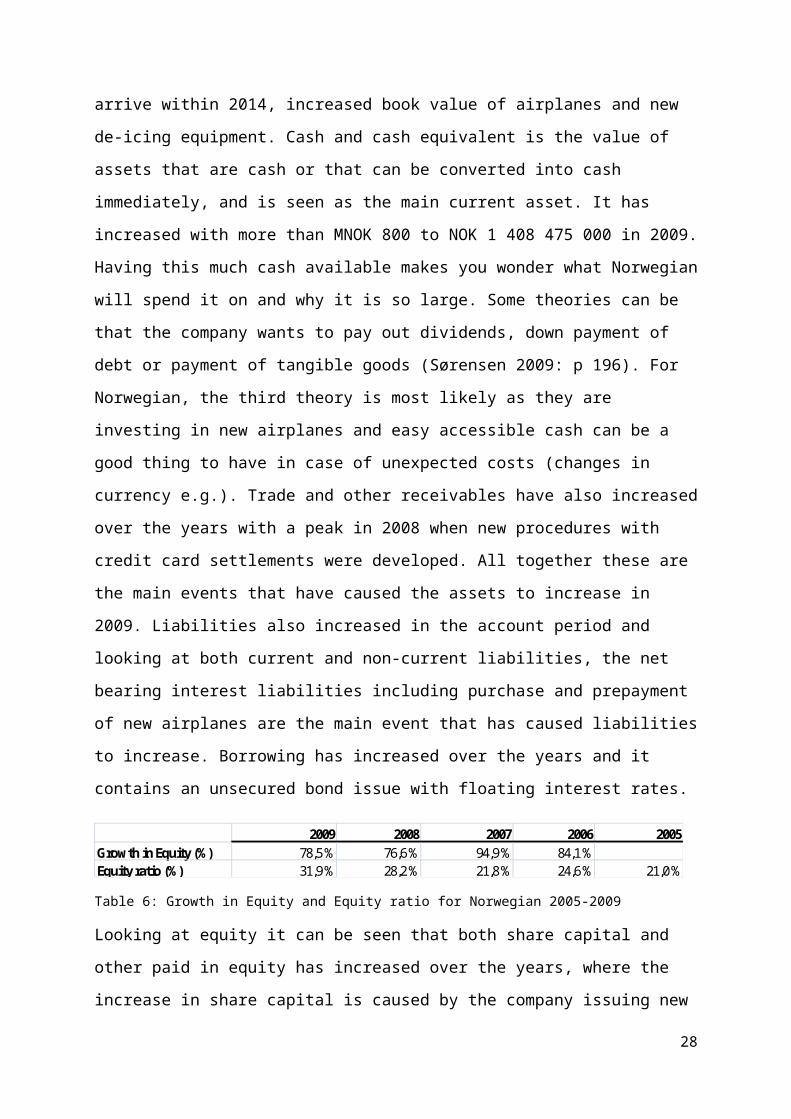

Norwegian`s assets, liabilities and equity have increased rapidly over the years (appendix 11).

In 2009 non-current assets accounted for 52% of total assets and were characterized with the

arrival and prepayments of the new airplanes that will arrive within 2014, increased book

18

value of airplanes and new de-icing equipment. Cash and cash equivalent is the value of

assets that are cash or that can be converted into cash immediately, and is seen as the main

current asset. It has increased with more than MNOK 800 to NOK 1 408 475 000 in 2009.

Having this much cash available makes you wonder what Norwegian will spend it on and why

it is so large. Some theories can be that the company wants to pay out dividends, down

payment of debt or payment of tangible goods (Sørensen 2009: p 196). For Norwegian, the

third theory is most likely as they are investing in new airplanes and easy accessible cash can

be a good thing to have in case of unexpected costs (changes in currency e.g.). Trade and

other receivables have also increased over the years with a peak in 2008 when new procedures

with credit card settlements were developed. All together these are the main events that have

caused the assets to increase in 2009. Liabilities also increased in the account period and

looking at both current and non-current liabilities, the net bearing interest liabilities including

purchase and prepayment of new airplanes are the main event that has caused liabilities to

increase. Borrowing has increased over the years and it contains an unsecured bond issue with

floating interest rates.

2009 2008 2007 2006 2005Growth in Equity (%) 78,5 % 76,6 % 94,9 % 84,1 %Equity ratio (%) 31,9 % 28,2 % 21,8 % 24,6 % 21,0 %

Table 6: Growth in Equity and Equity ratio for Norwegian 2005-2009

Looking at equity it can be seen that both share capital and other paid in equity has increased

over the years, where the increase in share capital is caused by the company issuing new

shares. The growth in equity of 78.5% between 2008 and 2009 and the increasing equity ratio

are seen as a positive thing for a company, but when the cash is coming from issuing new

shares it could indicate that the company is experiencing liquidity problems. To reject this

theory Norwegian stated in a press release that the reason behind the issuing of new shares is

to strengthen their equity, secure their strong market position and to prepare the company for

continued growth possibilities. The CEO Bjørn Kjos says that now that they are becoming

more international due to the expansion over the last years, they want to attract new investors

to invest in the company5.

It is also important to say that Norwegian has not yet paid dividends. They have a rule that

this will not be done before the financial situation is more stable and they have an equity ratio

above an appropriate level (Annual report 2008: p 19). SAS have not paid out dividends in

5 Andersen, Tor Øyvind; Brander, Anna Sandvig: http://e24.no/boers-og-finans/article3359145.ece

19

period 2005-2009, and state that this will not be done before their financial situation is at a

more stable level. Cimber Sterling did pay out dividends in year 2007/2008.

SAS 2009 2008 2007 2006 2005Assets 42 495 43 364 48 770 51 164 58 016 Liabilities 31 106 34 682 31 621 34 776 45 935 Equity 11 389 8 682 17 149 16 388 12 081 Cimber Sterling 2008/2009 2007/2008 2006/2007Assets 1 090 212 1 045 645 874 780 Liabilities 927 834 845 212 671 810 Equity 162 378 200 433 202 970

Table 7: Balance sheet overview: SAS and Cimber Sterling

SAS has had a decrease in assets over the last years and decrease in liabilities except from an

increase in 2008. Equity has varied over the years but is increasing again after a decrease in

2008. The decrease in assets is mainly due to a decrease in intangible assets (goodwill)

because of the sale of Air Baltic 4th quarter of 2008. The decrease in liabilities is caused by

purchase of new airplanes and income received from the sale of Air Baltic. The increase in

equity is caused by issuing new shares and it is important to mention that the company

received SEK 6 billion to cover their massive loss in 2008 (page 14). SAS`s cash and cash

equivalent is also looked at to see if they have had the same development as Norwegian. Cash

available is also large in SAS, but has a decreasing tendency compared to previous years.

As for Cimber Sterling, it can be seen that they have had the same progress as Norwegian

with an increase in both assets and liabilities. However, their equity has decreased over the

last three years. The increase in assets and liabilities is caused by them purchasing Sterling

Airlines in 2008/2009. Cimber Sterling`s cash and cash equivalent has been decreasing from

its peak in 2006/2007 to a more stable level in 2008/2009. Therefore it can be concluded that

looking at SAS and Cimber Sterling, there is nothing in the overall industry that can explain

the reason behind Norwegian having as much cash available.

2.3.2: Net working capital

Net working capital is calculated as current assets – current liabilities and tells us if the

company is able to pay its current liabilities with current assets. It is therefore important not to

include financial items that are not involved in generating sales (Pennan 2001: p 359). Cash

and cash equivalents are included in the calculation as the majority are cash in bank and short

term deposits with maturity of three months or less being easy accessible (Annual report

2008: note 24, p. 61).

20

A positive net work capital indicates that the company are not having any current liquidity

problems. Norwegian net work capital has been positive in all years except from 2008 and

2009 (appendix 14). This indicates that Norwegian has not had any problems paying their

short term debt in earlier years, except over the last two years. However, it is important to

notice that if it wasn’t for the large and increasing cash and cash equivalent the net working

capital would have been negative in the other years as well. Looking at 2008 and 2009, net

working capital is negative and it seems that Norwegian in this year had problems paying

their short term liabilities with their short term assets. It could also just be an indicator

towards that Norwegian this year invested heavily and had a huge growth. Therefore further

investigation with liquidity analysis will be necessary in order to see how serious their

problems are.

2.3.3 Liquidity analysis

Norwegian`s liquid situation will be investigated with background from the balance sheet. It

is important to measure liquidity ratios to see a Norwegian’s ability to meet current

obligations with assets that can be quickly converted into cash. This because liquidity tells us

about a company’s ability to repay non-current debt, and financial leverage tells us the

relative size of financial assets.

Financial leverage (Debt to equity) 2,14 2,54 3,59 3,07 3,77 Current ratio 0,92 0,95 1,04 1,01 1,07Quick ratio 0,90 0,93 1,01 0,98 0,99Solvency 46,8 % 39,3 % 27,9 % 32,5 % 26,5 %

Table 8: Norwegian: Liquidity ratios

Quick ratio looks at the company’s ability to repay current liabilities with current assets in the

short term perspective, and therefore inventory is excluded in the calculation because it will

take a longer period of time to convert this into cash. The quick ratio is only in year 2007

above its optimal level at 1, but it is close to the optimal level in the other years. The concern

is that the ratio has had a decreasing tendency since 2007. Current ratio measure Norwegian’s

ability to cover current liabilities with current assets, looking at it from a longer perspective

that the quick ratio, and therefore inventory are included. The current ratios optimal level is

around 2, and it can be seen that the ratio has not been at a satisfactory level in any of the

years and there is a decreasing tendency. Because of the decreasing tendency in both quick

and current ratio it can be said that Norwegian is experiencing payment problems in the short

and longer run. They should focus on the decreasing tendency that can indicate them having

21

problems creating liquidity. The solvency ratio measures a company`s ability to meet its long

term commitments. Norwegian has had a high and increasing solvency ratio above 20%, over

the last three years indicating that they are a financially healthy company, and that there are

no sign of them failing its obligations. Because of the high degree of debt and the fact that

solvency it is calculated with equity, it does take the cash from the current share issue in

consideration. Therefore it is important to notice that this liquidity ratios might not give the

right picture of the actual situation, and it is therefore important to look at it in relation to the

cash flow ratios in the next chapter (Schack 2002: p 72).

Financial leverage ratios measures to which extent net operating assets are financed by net

financial obligations or by equity (Pennan 2001: p 339). For Norwegian, debt to equity ratio is

analysed because it measures how much of the company is leveraged in debt. If this number is

high, it could mean that the company rely on debt as a source of financing, which is the case

for Norwegian. Debt to equity ratio has been at a level above 2 in the last years, however,

there is a decreasing tendency which is good as Norwegian then rely on debt as a source of

financing in a decreasing way.

SAS 2009 2008 2007 2006 2005Quick ratio 0,67 0,93 1,04 1,12 0,92 Current ratio 0,71 0,89 1,09 1,18 0,97 Financial leverage (Debt to Equity) 2,73 3,99 1,84 2,12 3,80 Cimber Sterling 2008/2009 2007/2008 2006/2007Quick ratio 0,42 0,47 0,73 Current ratio 0,60 0,63 0,88 Financial leverage (Debt to Equity) 5,71 4,22 3,31

Table 9: Liquidity ratios for SAS and Cimber Sterling

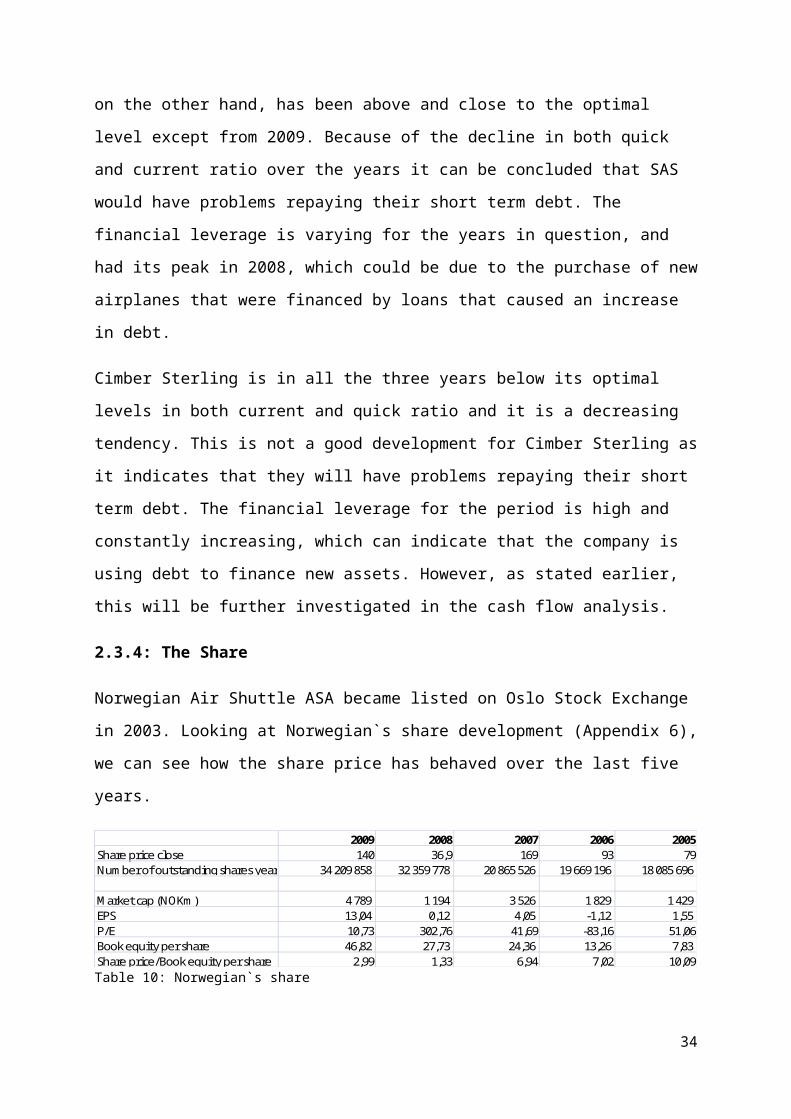

SAS has had a decrease in their current and quick ratio from 2006. The current ratio is below

the optimal level in all years, and it could be concluded that in the longer run it will be hard

for the company to repay their debt. The quick ratio, on the other hand, has been above and

close to the optimal level except from 2009. Because of the decline in both quick and current

ratio over the years it can be concluded that SAS would have problems repaying their short

term debt. The financial leverage is varying for the years in question, and had its peak in

2008, which could be due to the purchase of new airplanes that were financed by loans that

caused an increase in debt.

Cimber Sterling is in all the three years below its optimal levels in both current and quick

ratio and it is a decreasing tendency. This is not a good development for Cimber Sterling as it

22

indicates that they will have problems repaying their short term debt. The financial leverage

for the period is high and constantly increasing, which can indicate that the company is using

debt to finance new assets. However, as stated earlier, this will be further investigated in the

cash flow analysis.

2.3.4: The Share

Norwegian Air Shuttle ASA became listed on Oslo Stock Exchange in 2003. Looking at

Norwegian`s share development (Appendix 6), we can see how the share price has behaved

over the last five years.

2009 2008 2007 2006 2005Share price close 140 36,9 169 93 79Number of outstanding shares year end 34 209 858 32 359 778 20 865 526 19 669 196 18 085 696

Market cap (NOKm) 4 789 1 194 3 526 1 829 1 429 EPS 13,04 0,12 4,05 -1,12 1,55 P/E 10,73 302,76 41,69 -83,16 51,06Book equity per share 46,82 27,73 24,36 13,26 7,83 Share price/Book equity per share 2,99 1,33 6,94 7,02 10,09

Table 10: Norwegian`s share

The share price has increased over the years except from 2008 where it was historically low,

however, it ended 2009 at 140 kroner. The number of outstanding shares has also increased

over the accounting years caused by issuing of new shares in order to strengthen their strong

position in the market and letting new investors be a part of their expansion process6. Market

cap measures the market value for the company’s outstanding shares; the value of the

company. It shows that Norwegian`s market cap has been increasing except from a decrease

in 2008 expected after the historically low share price.

In 2009 earnings per share (ESP) generates profit after tax at 13.04 kroner per share, which is

good compared to previous years. This ratio is useful when comparing companies as you

should always invest in a company that gives as high EPS as possible. Looking at earnings per

share for SAS (appendix 23) shows that Norwegian will be the preferred investment as SAS

generates loss after tax at -1.19 kroner per share.

Price-Earnings (P/E) indicates a firm’s possibility to grow earnings. If this ratio is high it

means that the future earnings are expected to be higher than current earnings, but it is

important to be aware that P/E can be high because current year’s earnings have been low, as

in the case of Norwegian which has experienced lower earnings in previous years. When

6 Andersen, Tor Øyvind; Brander, Anna Sandvig: http://e24.no/boers-og-finans/article3359145.ece

23

analysing P/E we also needs to consider risk, as a high risk on future earnings will give lower

P/E (Pennan 2001: p 527). Book equity per share assesses the minimum value of a company`s

equity in a current situation as it does not look into the future. The ratio is good and it has

been increasing over the five years, and it can be seen that the book value is not above the

market value in any of the years. Share price divided by book equity per share is calculated to

see what the market is expecting. For Norwegian, all the ratios are above 1 and it can be

concluded that the market expects ROE to exceed the owners` expected return on investment

and give value to the owners.

2.3.5: Conclusion on the balance sheet

The balance sheet tells us about a company’s assets, liabilities and equity, and is used to

analyse the liquidity situation within a company with help of key ratio analysis. Norwegian`s

balance sheet, assets and equity have all been increasing over the years. The main events

causing this increase are purchase and prepayments of new airplanes, an increase in cash and

cash equivalents, and issuing of new shares. Cash and cash equivalents that is easy accessible

cash has had a huge growth over the last years. This must be them preparing for their new

investments as such a tendency cannot be seen from either SAS`s or Cimber Sterling`s

balance sheet. Norwegian`s net working capital is positive in all years except 2008 and 2009,

indicates that they have not had problems paying their current debt, except from the last two

years.

The financial ratio analysis from the balance sheet concludes that there are signs of liquidity

problems both current and non-current. This because the quick ratio is close to, but below its

optimal level, and the current ratio is far below its optimal level. However, they should be

concerned as the decreasing ratios could indicate that Norwegian has problems creating

liquidity. The financial leverage is high but showing a decreasing tendency, which indicates

that the company is at a decreasing level relying on debt as a source of financing. Their

solvency ratio, that includes equity, is at a good level indicating that they are a financial

healthy company. However, this needs to be investigated closer in the cash flow analysis.

Norwegian are performing better compared to SAS`s and Cimber Sterling`s by looking at the

key ratios. The quick and current ratio analysis concluded that SAS would have problems

repaying their debt in the short and longer run. As their debt to equity ratio is higher than

Norwegian`s, meaning that they are depending on debt as a source of financing at a higher

degree than Norwegian. Cimber Sterling has current and quick ratios far from to its optimal

24

level, and the debt to equity ratio is high and increasing, indicating that they are relying on

debt as a source of financing at an increasing level.

2.4: Cash Flow statement

The cash flow statement connects the income statement with the balance sheet and explains

how the company has used and received cash over the account period. It is important to pay

increased attention towards the cash flow statements, as it focuses on cash available for

operations and investments and will help to understand how well companies can handle new

investments or potential losses. Analysing key ratios from the cash flow statement will

continue the liquidity analysis from the balance sheet, and we will get a more accurate

overview of the situation in Norwegian (appendix 12).

The Cash flow statement is divided into three groups being cash flow from operating

activities, cash flow from investing activities and cash flow from financial activities. By

adding these activities together we will see if there has been a decrease or increase in the

company’s cash flow in the accounting period (Pennan 2001: p 35):

Cash ¿operations+cash¿ investment+cash¿ financing=change∈cash

Norwegian 2009 2008 2007 2006 2005Net cash flow from operating activities 884 404 -385 551 457 932 75 562 95 356 Net cash flow from investing activities -1 269 894 -253 475 -532 619 -245 257 -38 368 Net cash flow from financial activities 1 188 162 686 644 306 425 139 864 -14 601 Change in cash 800 938 52 466 229 713 -29 839 42 387 SAS Net cash flow from operating activities -3 414 -2 651 2 866 2 102 1 507 Net cash flow from investing activities -2 611 -2 913 -213 7 485 1 001 Net cash flow from financial activities 4 284 2 480 -4 492 -7 438 -2 457 Change in cash -1 741 -3 084 -1 839 2 149 51 Cimber Sterling 2008/2009 2007/2008 2006/2007Net cash flow from operating activities 154 329 115 539 64 529 Net cash flow from investing activities -94 666 -250 139 -23 142 Net cash flow from financial activities -57 195 110 850 -41 627 Change in cash 2 468 -23 750 -240

Table 10: Norwegian, SAS and Cimber Sterling cash flow statement 2005-2009

2.4.1: Cash flow from operating activities

Net cash flow from operating activities is cash generated from selling products and net cash

used, useful to study as it gives a better overview than earnings from the income statement. A

company that have positive earnings and positive cash flow from operating activities indicates

that they will be able to pay its debt. Looking at Norwegian`s cash flow from operating

activities it can be seen that they had positive values in all years except 2008, which means

25

that they were generating less cash than they used this year. In 2009 they generated MNOK

884 404, mostly due to an increase in operating revenues and a reduction in accounts

receivable. This was a huge increase after the decrease in 2008 due to the huge loss in net

profit after tax and the changes in net working capital.

Changes in working capital needs to be looked at closer, and will be analysed with use of

2008 numbers. Working capital was also investigated in the balance sheet (p.20) as current

assets minus current liabilities. It is also included in the cash flow statement because

companies normally increase or decrease their current assets or current liabilities in the

accounting period. It can be seen that there has been an increase in inventory, accounts

receivable and payable, meaning that the company has spent more money on purchasing

assets this year. Therefore the amounts need to be subtracted from the operating profit. The

same happens with the change in assets, liabilities and air traffic settlements, but since there

has been a decrease since last year, this number is added to operating profit.

Looking at SAS cash flow statement, it can be seen that cash flow from operating activities

has been decreasing since 2007. A major part of this is due to negative net income before tax

of -2 947 billions and large restructuring costs. Net cash flow from operating activities has

also increased for Cimber Sterling, meaning that they are generating more cash than they are

using, even though they delivered a loss after tax of DKK -58 925 million.

2.4.2: Cash flow from investing activities

Net cash flow from investing activities is cash spent on purchasing new assets less cash

received from selling assets. Norwegian`s investment activities have been negative over the

past five years, but in 2008 their investment activities decreased. The reason behind this

decrease was due to a gain from a sale of a USD currency hedge contract, and not because

they were spending less on new investments. As shown in the cash flow statement both

payments of inventory and tangible goods increased this period, as the investments of the first

10 Boeing airplanes have partially been financed by Pre-Delivery-Payment7 (purchase of new

airplanes). Between 2008 - 2009 we can see a huge increase in cash flow from investing

activities that again can be explained by payment of two new airplanes from Boeing and

prepayments of the rest of the airplanes. The purchase of the new airplanes is an investment

Norwegian regards as urgent to keep up with the strong competition within the industry as the

new airplanes will help the company to decrease their cost base.

7 Aircraft manufactures often require customers to make down payments before aircrafts are delivered.

26

Looking at SAS and Cimber Sterling, their cash flow from investing activities has also been

negative through the last three years. The decrease in investing activities from 2008 to 2009

for SAS are explained by prepayments and purchase of new airplanes and that the company at

the same time received payment for the sale of Air Baltic and sold and leased backs some of

their airplanes. Cimber Sterling has had a decrease in investing activities from last year

despite their purchase of Sterling AS.

2.4.3: Cash flow from financial activities

Net cash flow from financial activities is cash transactions that are claimants from equity and

debt. For Norwegian it can be seen that financing activities in all years are positive and that

there has been an increase over the five years. Their debt has also been increasing over the

years and since there has been almost no repayment of debt the financial activities consists of

issuing new shares and proceeds from long term debt. Especially the increase between 2009

and 2008 can be explained by issuing of new shares which caused their equity ratio to

increase. It also shows that in 2009 they issued MNOK 400 unsecured bonds with a maturity

date in 2012. In this connection they bought back MNOK 137 in bond issue with maturity

date 2010.

Compared to their competitors, SAS`s cash flow from financial activities has increased in

2009. This is explained by a decline in net borrowings which was financed by issuing new

shares. Cimber Sterling has negative values in financial activities in 2008/2009 due to

repayment of debt. In 2007/2008 they took a loan and at the same time paid MDKK 45 080 in

dividends which therefore explains the positive financial activities for this year.

2.4.4: Change in cash

The change in cash and cash equivalents are the operating, investing and financing activities

added together, but we also need to take the foreign exchange effect on cash in consideration.

The change in foreign exchange rate needs to be considered as Norwegian is an international

company where most of their cash comes from American dollars (USD) and Euro (EUR).

Change in cash will indicate the health for a company and the more cash available, the better.

For Norwegian the net change in cash and cash equivalents is positive and has been increasing

over the last three years, indicating that the company is doing well and is generating enough

cash for future investments and growth.

27

The large increase in operating and financial activities in 2009 is the main reason why

Norwegian is having this much cash available that can be used in e.g. new investments. This

can be a sign of Norwegian being a stable and solvent company, but further investigations are

needed with help from the cash flow ratios, because if it wasn’t for the share issue, the change

in cash might not have given us this situation.

2.4.5: Cash flow ratios

Cash flow ratios measure a company’s ability to meet financial and operational commitments

and also consider the risk involved. The financial analysis of key ratios from the cash flow

statement will be used to continue the liquidity analysis from the balance sheet as it gives a

more accurate picture of Norwegian`s liquidity situation than the current and quick ratios. The

cash flow can also help managers to better understand problem areas within the company and

plan to be more efficient (The power of Cash Flow ratios: 1998).

Operating cash flow 0,4 -0,2 0,4 0,1 0,2Cash current debt coverage 0,4 -0,2 0,4 0,1 0,2Cash interest coverage 40,1 -5,5 -5,7 -146,2Total debt 0,26 -0,17 0,25 0,09 0,18

Table 11: Cash Flow ratios for Norwegian

Operating cash flow measures a company’s ability to generate cash to pay short term debt

(within a year). A company should have a ratio above 1, because then a company is

generating enough cash to pay its current commitments, and at the same time they have

margin in case of further growth in operating cash flow etc. If the ratio is below its optimal

level, a company most likely needs external help to pay its current liabilities, and the threat of

bankruptcy increases. This is the case of Norwegian which in all years has had ratios close to

zero, and in 2008 negative. This indicates that Norwegian has had problems financing their

short term debt during this period, and that the company therefore has been and still are

depending on external help in order to pay their short term debt. Cash current debt coverage

measures the same as operating cash flow but takes dividend into consideration. Since

Norwegian will not pay out dividends unless their equity ratio is more stable, cash current

debt coverage equals operating cash flow.

Funds flow coverage measures if a company can pay “unavoidable” costs as interest rates and

taxes. The purpose of this analysis is see how pressured the company is and if they can bear

new investments and further growth. Funds flow coverage is not calculated for Norwegian as

28

they repayment of debt is not to be seen in the overview of financial activities since 2004.

However, it will be calculated for both SAS and Cimber Sterling.

Cash interest coverage measures if a company is able to pay interests on its debt. This ratio is

very actual, especially in these days as some companies are borrowing more than they can

afford. As it can be seen Norwegian has had negative ratios in previous years except 2008

where the ratio are positive and above an optimal level of 1, and that year the company would

not have had problems paying interests on their debt this year.

Total debt measures the company’s ability to cover future debt obligations, and it indicates

how long it will take to repay debt, assuming that all cash flow from operating activities goes

to repay debt. A low ratio indicates that a company may have problems to repay debt in the

future, which can be seen as Norwegian`s ratios are zero in most of the year, and negative in

2008. This confirms findings from the balance sheet indicating that the company will have

problems repaying debt in the future.

2009 2008 2007 2006 2005Operating cash flow (OCF) -0,19 -0,16 0,14 0,12 0,07Cash current debt coverage (CDC) -0,19 -0,16 0,14 0,12 0,07Funds flow coverage (FFC) -0,34 0,17 0,50 0,32 -5,35Cash interest coverage(CIC) 5,05 3,81 -1,49 -0,39 0,13Total debt -0,11 -0,08 0,09 0,06 0,03

Table 12: Cash Flow ratios for SAS

Financial key ratios from the cash flow statement are also calculated for SAS and Cimber

Sterling to see how Norwegian is performing compared to their competitors. SAS`s operating

cash flow and the cash current debt coverage are the same as SAS do not pay out dividends.

The ratios are negative and close to zero in all five years meaning that SAS have problems

generating cash to pay the short term debt themselves. Funds flow coverage is positive during

the period except for 2009, meaning that this year SAS was not able to pay their unavoidable

costs as taxes. Cash interest coverage is constantly growing and is at a level of 5.05 in 2009,

indicating that SAS is able to pay interest on their debt. Their ability to pay tax and dividends

is not favourable, however, they are able to pay interest on their debt.

Operating cash flow (OCF) 0,33 0,30 0,22Cash current debt coverage (CDC) 0,33 0,19 0,22Funds flow coverage (FFC) 1,84 -0,64 2,56Cash interest coverage(CIC) -4,26 -2,88 -2,40Total debt 0,17 0,14 0,10

Table 13: Cash Flow ratios for Cimber Sterling

29

The overview of Cimber Sterling shows that their operating cash flow and cash current debt

coverage are both below the optimal level of 1. In 2007/2008 the company decided to pay out

DKK 45 080 million in dividends, which is why cash current debt coverage is decreasing this

year. This ratio indicates that the company itself will have problems generating cash to pay

their short term debt. The funds flow coverage is good in 2006/2007 and 2008/2009,

indicating that the company can pay costs as taxes and dividends. They are not able to pay

interest on their debt seen from cash interest coverage that is negative in all years.

2.4.6: Conclusion on the Cash Flow statement

The cash flow statement is an overview of what the company has used and received in cash

during the years. From Norwegian`s cash flow statement, it can be seen that the company has

had positive values in investing activities in all years except 2008, when they spent more cash

than they generated. This can also be seen from investing activities that have negative values

in each year, meaning that Norwegian spent more cash on purchase of assets than they

received from assets sold. The cash flow statement is therefore strongly affected by

prepayments and purchase of new airplanes which were in Norwegians focus especially in

2008 and 2009. In the problem statement it is stated that the company’s liquid situation in

relation to their issuing of shares need to be investigated. The financial activities show that

issuing new shares is the main activity which causes the company to end up with positive

values in financial activities over the last four years. A positive increase in change in cash

indicates that they are generating enough cash for future investments and growth.

The analysis of liquidity ratios from the balance sheet has been continued to measure

Norwegians ability to generate cash to pay back short term debt and to pay interest. Based on

the balance sheet, we concluded that Norwegian have liquidity problems paying their short

term and future debt. In the cash flow analysis, operating cash flow concluded that Norwegian

has had and will continue on have problems generating enough cash to pay their short term

debt, which is not good as the company then rely on external help and the risk of bankruptcy

increases. However, it needs to be remembered that this ratio does not take the issuing of

share in account. Total debt ratio indicates that they will have problems in the future repaying

their debt, but the cash interest coverage concludes that Norwegian has been able to pay

interest on its debt over the last two years with good margin.

However, looking at Norwegian`s performance compared to SAS and Cimber Sterling, it does

not look bad as their ratios are better than the competitors. Their competitors have liquidity

30

problems evidenced by the same ratio calculations. Both companies’ ratios are fluctuating a

lot. Overall, SAS will have problems generating cash to pay both current and non-current debt

and to pay unavoidable costs, but they should be able to pay interest on their debt. Cimber

Sterling on the other hand, is able to generate cash to repay short term debt and pay

unavoidable costs, but not able to pay interest rates on their debt.

2.5: Conclusion on the financial statement analysis

Despite the economic recession and the fact that 2009 has been the hardest year for the airline

industry since the Second World War, Norwegian delivered their best result historically. Their

revenues had a growth of 17.4% between 2008 to 2009 (appendix 16), which is good

compared to the overall market which saw a passenger decrease of 3%, and their biggest

competitors SAS and Cimber Sterling ended 2009 with a loss after tax. The growth in profit

after tax for Norwegian over the years is due to larger market shares both domestically, in

Europe, and with the decrease of unit costs. It is important for a low cost airline company like

Norwegian to have as low unit costs as possible, which enables them to offer low ticket prices

and still generate a profit. Therefore they are constantly finding new ways to decrease their

unit costs even more, and over the last years they have purchased new airplanes that will

increase their capacity and decrease fuel consumption and again decrease unit costs further.

The research question has been to look at Norwegian`s liquidity situation in connection to the

issuing of shares. This will be investigated in the key ratio analysis.

The prepayments and purchase of new airplanes has affected all the financial statements over

the last two years. From the balance sheet it can be seen that both assets and liabilities have

increased after prepayments, purchase and arrival of new airplanes, and equity increasing

after issuing shares. The cash flow statement reflects the same development as operating

activities are positive, meaning that Norwegian generated more cash than expenses mostly

due to an increased profit in 2009. Invested activities had a huge increase from 2008 to 2009,