Embed Size (px)

Citation preview

Provisions, Contingent

Liabilities and Contingent Assets

http://www.cc.cec/budg/

2

Overview of session

1. Scope of application

2. Key concepts

3. Recognition

4. Measurement

5. Disclosures

6. Specific implications / Next steps

7. Questions

Provisions, Contingent

Liabilities and Contingent Assets1. Scope of application

4

Scope

• Covers accounting for all provisions and contingencies, excluding:

– Social benefits provided by an entity for which it does not receive

consideration that is approximately equal to the value of goods or

services provided

– Provisions resulting from financial instruments carried out at fair

value

– Provisions arising in relation to income taxes

– Employee benefits (except those that arise as a result of a

restructuring)

– Provisions covered by another IPSAS

Provisions, Contingent

Liabilities and Contingent Assets

2. Key concepts

6

Legal and constructive obligations• Legal obligation = an obligation that derives from:

– A contract (through its explicit or implicit terms); or

– Legislation; or

– Other operation of law

• Constructive obligation = an obligation that derives from an entity’s action

where:

– By an established pattern of past practice, published policies or sufficiently

specific current statement, the entity has indicated to other parties that it will

accept certain responsibilities; and

– As a result, the entity has created a valid expectation on the part of those other

parties that it will discharge its responsibilities.

7

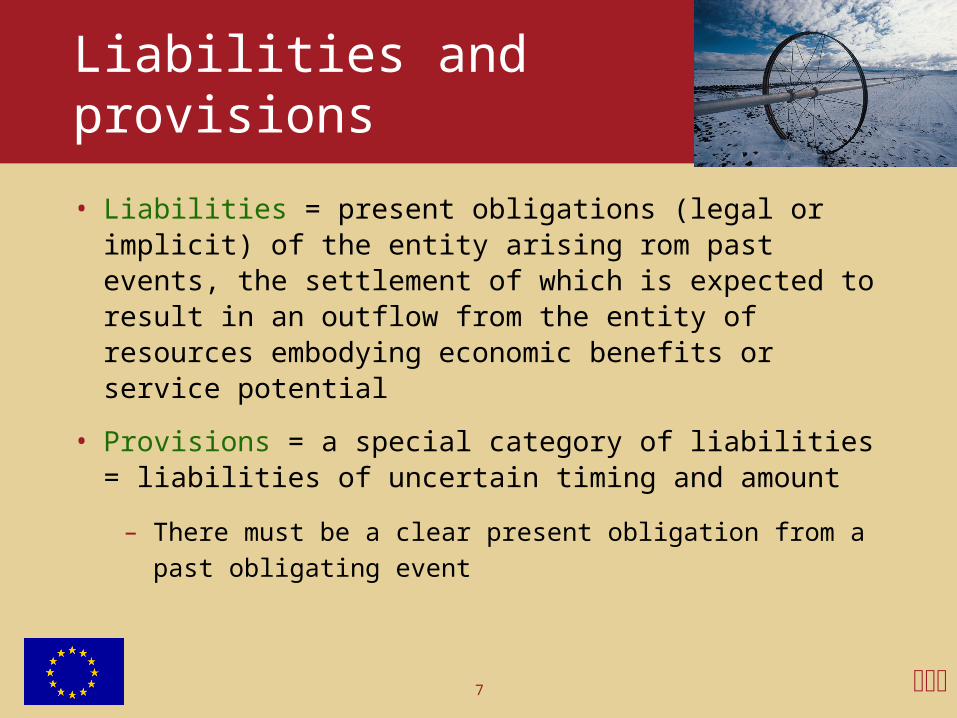

Liabilities and provisions

• Liabilities = present obligations (legal or implicit) of the entity arising rom past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits or service potential

• Provisions = a special category of liabilities = liabilities of uncertain timing and amount

– There must be a clear present obligation from a past obligating

event

8

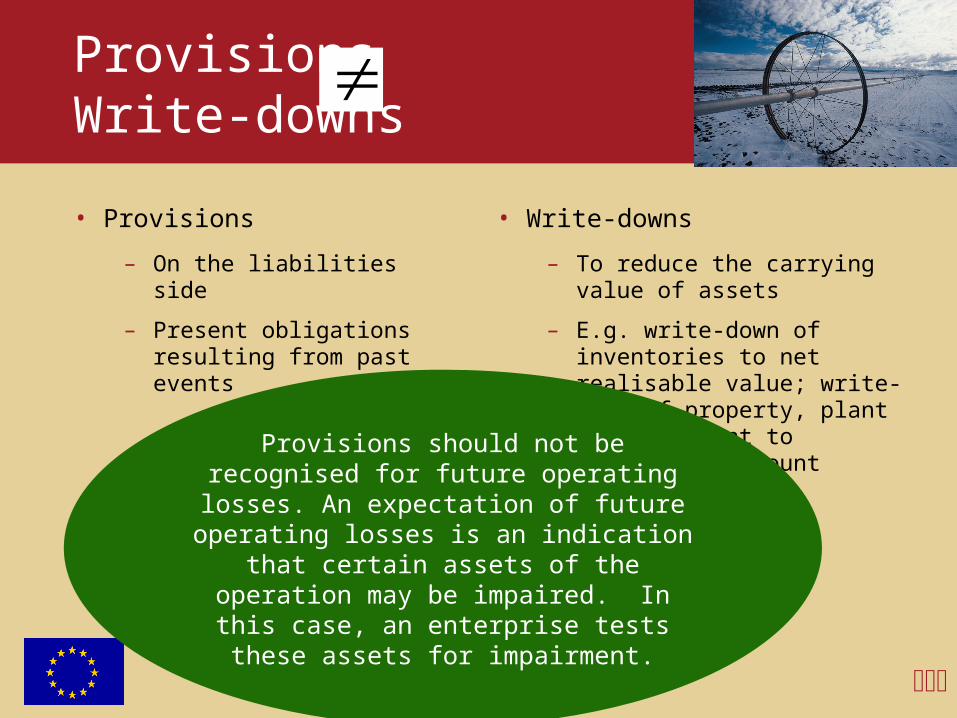

Provisions Write-downs

• Provisions

– On the liabilities side

– Present obligations resulting from past events

• Write-downs

– To reduce the carrying value of assets

– E.g. write-down of inventories to net realisable value; write-down of property, plant and equipment to recoverable amount

Provisions should not be recognised for future operating losses. An expectation of future

operating losses is an indication that certain assets of the operation may be impaired. In

this case, an enterprise tests these assets for impairment.

9

Contingent liabilities and contingent assets

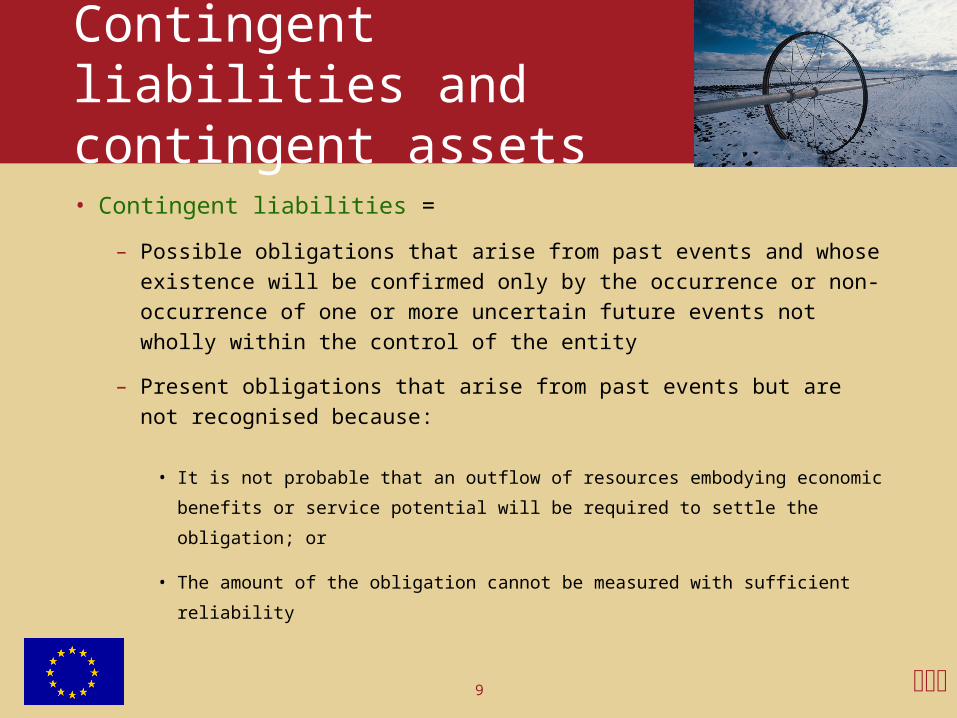

• Contingent liabilities =

– Possible obligations that arise from past events and whose

existence will be confirmed only by the occurrence or non-

occurrence of one or more uncertain future events not wholly

within the control of the entity

– Present obligations that arise from past events but are not

recognised because:

• It is not probable that an outflow of resources embodying economic

benefits or service potential will be required to settle the obligation; or

• The amount of the obligation cannot be measured with sufficient reliability

10

Contingent liabilities and contingent assets

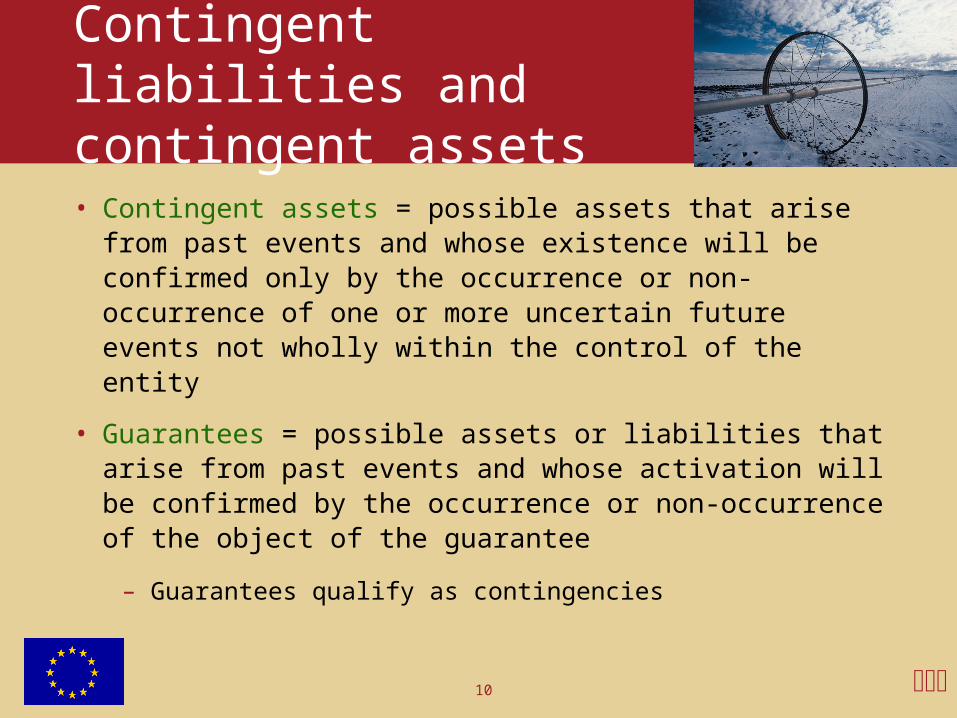

• Contingent assets = possible assets that arise from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity

• Guarantees = possible assets or liabilities that arise from past events and whose activation will be confirmed by the occurrence or non-occurrence of the object of the guarantee

– Guarantees qualify as contingencies

Provisions, Contingent

Liabilities and Contingent Assets

3. Recognition

12

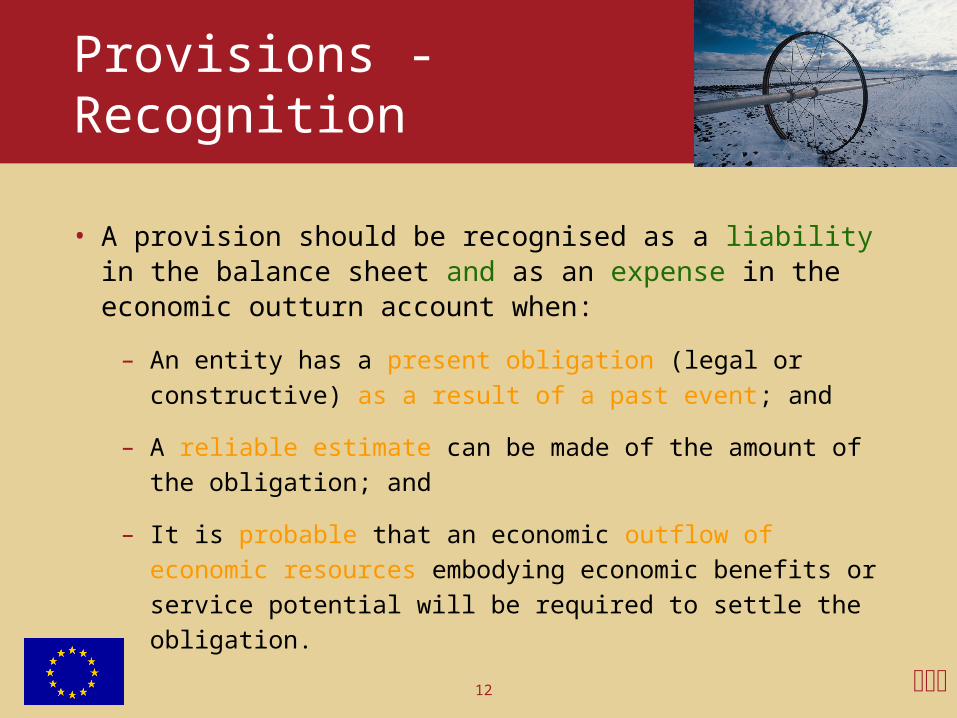

Provisions - Recognition

• A provision should be recognised as a liability in the balance sheet and as an expense in the economic outturn account when:

– An entity has a present obligation (legal or constructive) as a

result of a past event; and

– A reliable estimate can be made of the amount of the obligation;

and

– It is probable that an economic outflow of economic resources

embodying economic benefits or service potential will be required

to settle the obligation.

13

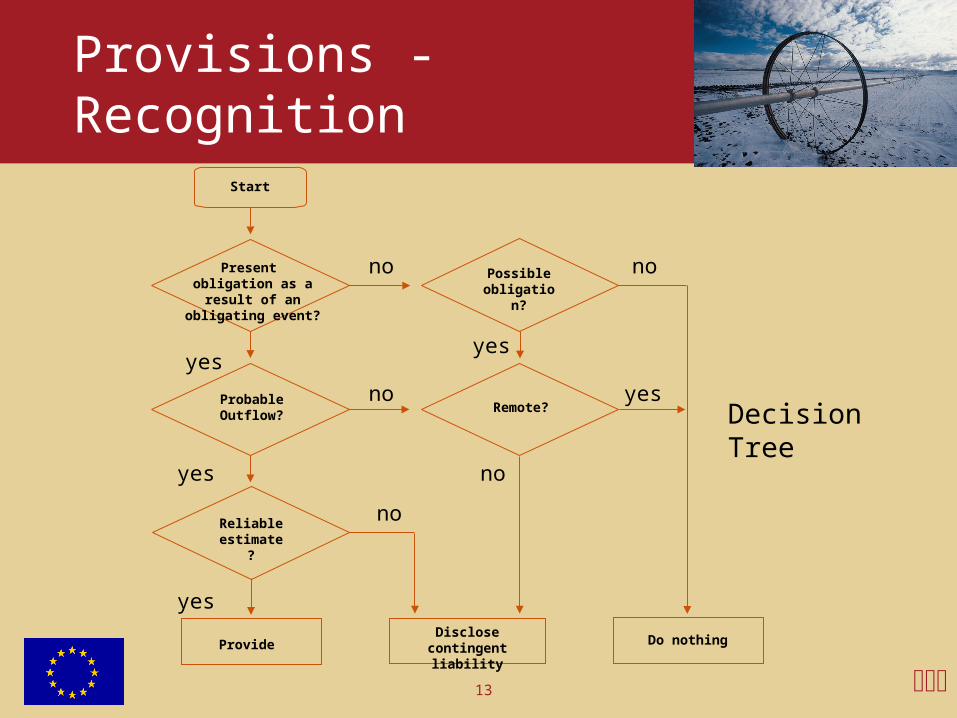

Provisions - Recognition

Decision Tree

Present obligation as a result of an

obligating event?

Probable Outflow?

Reliableestimate?

Possible obligation?

Remote?

Start

ProvideDisclose contingent

liabilityDo nothing

yesno

no

nono

yes

yes

yesyes

no

14

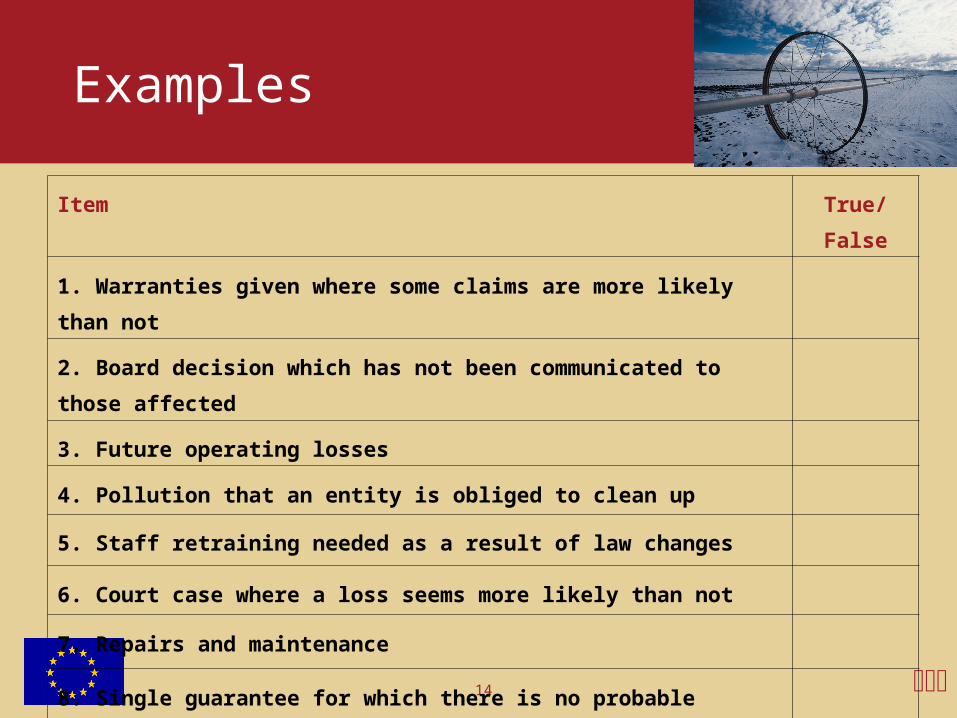

Examples

Item True/False

1. Warranties given where some claims are more likely than not

2. Board decision which has not been communicated to those affected

3. Future operating losses

4. Pollution that an entity is obliged to clean up

5. Staff retraining needed as a result of law changes

6. Court case where a loss seems more likely than not

7. Repairs and maintenance

8. Single guarantee for which there is no probable outflow of economic

benefits

15

Specific application of recognition criteria

• Restructuring provisions

– Programme which materially changes scope of business

– Following two conditions need to be met to be recorded as

provision

Detailed plan identifying key features of programme and its

implementation must exist at balance sheet date

Must be valid expectation that business will undergo restructuring

– Can only include direct expenses associated with restructuring

programme; cannot relate to ongoing operation of business

16

Specific application of recognition criteria

• Onerous contracts

– Unavoidable costs of meeting obligation greater than economic

benefits expected to be received

– Should include all indirect benefits that are derived from the

contract

– A provision should be made for the present obligation net of

recoveries – the unavoidable costs reflect the least net cost of

exiting from the contract, which is the lower of:

• The cost of fulfilling it; and

• Any compensation or penalties arising from failure to fulfil it.

Provisions, Contingent

Liabilities and Contingent Assets

4. Measurement

18

Measurement

• Best estimate at balance sheet date of amount needed to settle obligation

• If range is predicted with all the same likelihood of occurrence, mid point must be selected

• Large population of items – expected value measurement

• Anticipated cash flows must be discounted at risk free rate where changing value of money over time is material:

- Carrying value of liability increases by imputed interest in each period; recognised as interest expense in income statement

19

Measurement – Worked example

• A government medical laboratory provides diagnostic scanners with a one-year guarantee for parts and labour.

• Experience indicates that 70% of the diagnostic scanners will not be the subject of warranty claims, 25% will have minor defects and 5% will require replacement or major work. 100,000 units were provided in the current year. Major repair or replacing the unit costs approximately 25. Minor repairs cost 5 each.

20

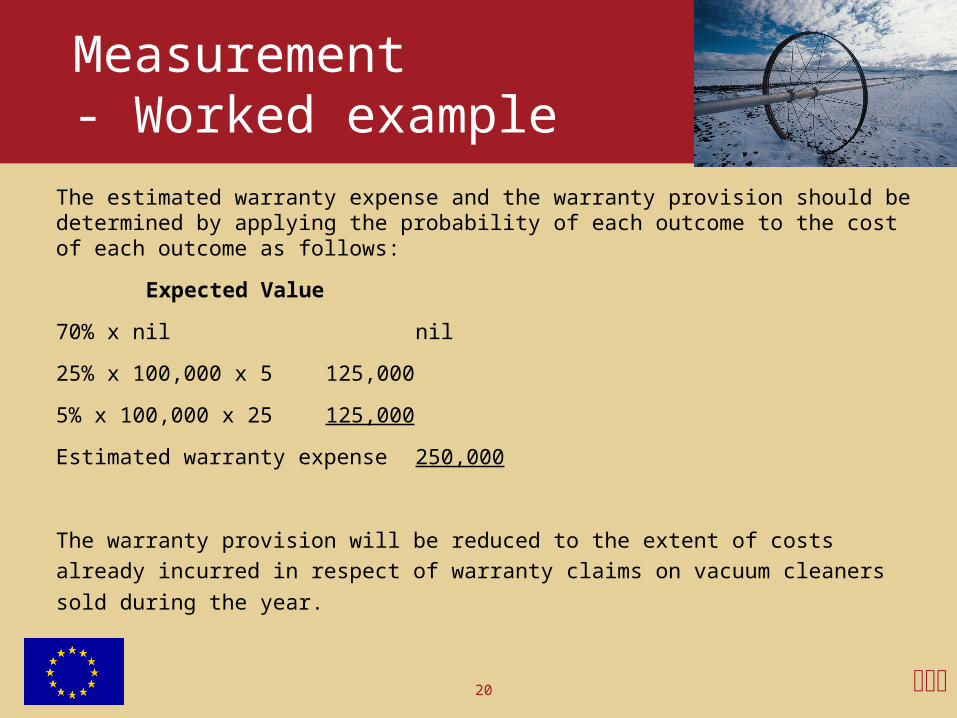

Measurement- Worked example

The estimated warranty expense and the warranty provision should be determined by applying the probability of each outcome to the cost of each outcome as follows:

Expected Value

70% x nil nil

25% x 100,000 x 5 125,000

5% x 100,000 x 25 125,000

Estimated warranty expense 250,000

The warranty provision will be reduced to the extent of costs already incurred in

respect of warranty claims on vacuum cleaners sold during the year.

21

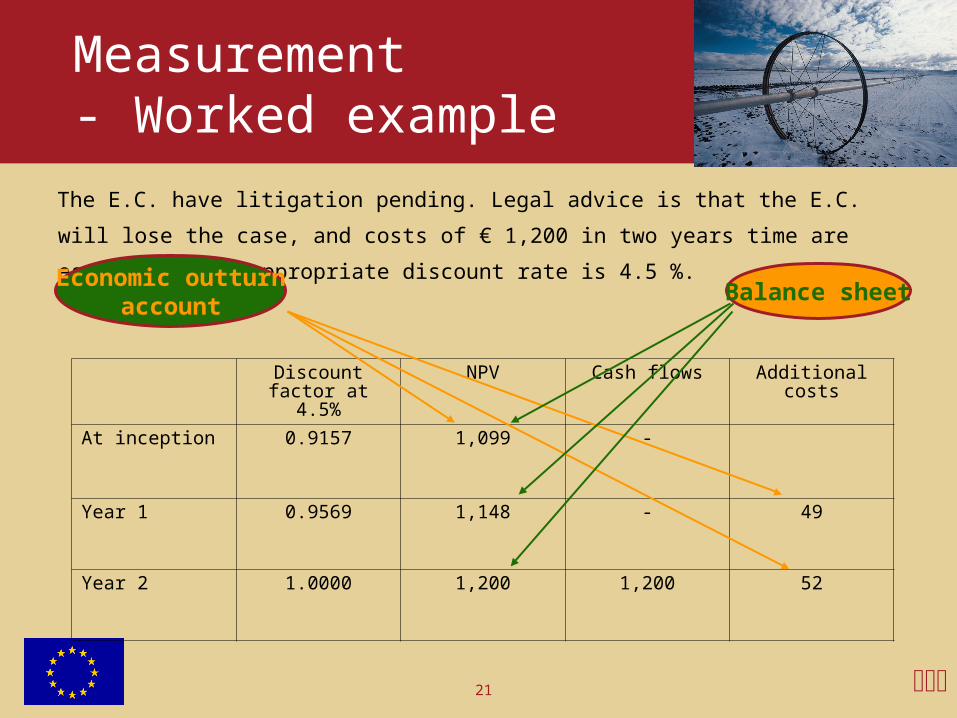

Measurement- Worked example

The E.C. have litigation pending. Legal advice is that the E.C. will lose the case, and costs

of € 1,200 in two years time are estimated. The appropriate discount rate is 4.5 %.

Discount factor at 4.5%

NPV Cash flows Additional costs

At inception 0.9157 1,099 -

Year 1 0.9569 1,148 - 49

Year 2 1.0000 1,200 1,200 52

Economic outturnaccount

Balance sheet

22

Other issues

• Reimbursement:

– To be recognised when, and only when, it is virtually certain that

reimbursement will be received if the entity settles the obligation

– The reimbursement should be treated as a separate asset

– In the economic outturn account, the expenses relating to a

provision may be presented net of the amount recognised for the

reimbursement

• Use of provision:

– A provision should be used only for expenditures for which the

provision was originally recognised.

Provisions, Contingent

Liabilities and Contingent Assets

5. Disclosures

24

Disclosures - Provisions

• Key disclosures required:

– Accounting policies for each major type of provision (for example, warranties)

– Movements in provisions during the period

– Descriptions of contingent liabilities and contingent assets

25

Disclosures - Guarantees• Guarantees for pre-financing received for procurement and for

grants

• Performance guarantees:

– “Regular” performance guarantees: disclose

– “Specific” guarantees related to performance guarantees: do not

disclose but consider as they are automatically activated and are

in essence a liability towards the contractor

• Guarantees given or received by the DG ECFIN for borrowings and loans

• Guarantees received by the DG BUDG when fines are disputed

Provisions, Contingent

Liabilities and Contingent Assets 6. Specific implications /

Next steps

27

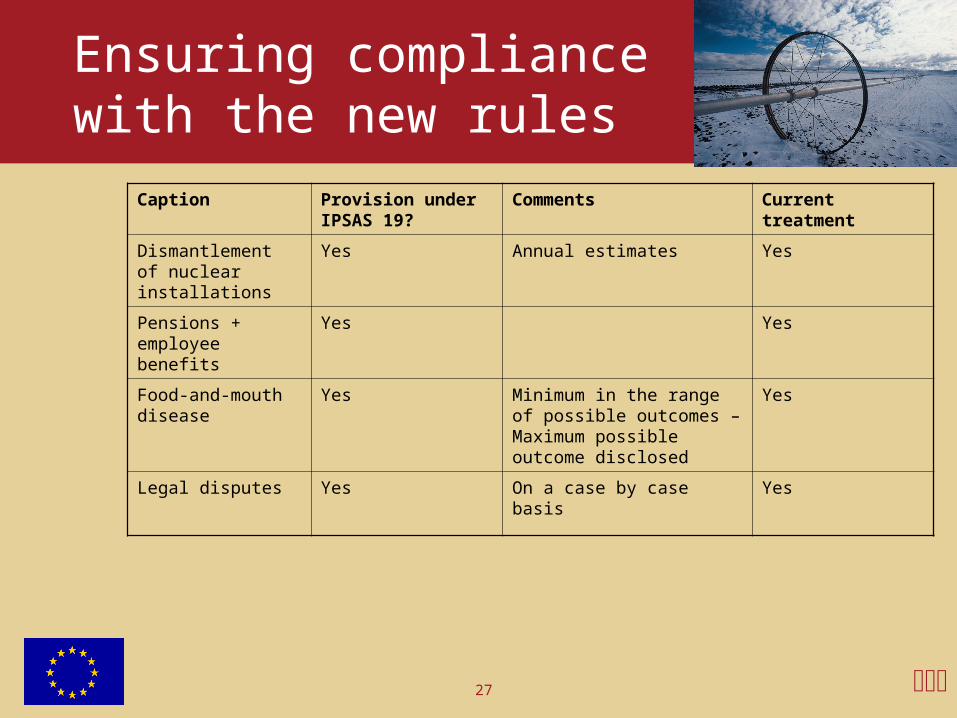

Ensuring compliance with the new rules

Caption Provision under IPSAS 19?

Comments Current treatment

Dismantlement of nuclear installations

Yes Annual estimates Yes

Pensions + employee benefits

Yes Yes

Food-and-mouth disease

Yes Minimum in the range of possible outcomes – Maximum possible outcome disclosed

Yes

Legal disputes Yes On a case by case basis Yes

Provisions, Contingent Assets

and Contingent Liabilities7. Questions

http://www.cc.cec/budg/