Embed Size (px)

Citation preview

7 May 2020

Chief Executive Officer

Steve Binnie

Sappi Limited

Q2 FY20 financial results delivering on

strategy

2020

Vision2020

intentionalevolution

next phase

growth

1

Forward-looking statements and Regulation G

2

Forward-looking statementsCertain statements in this release that are neither reported financial results nor other historical information, are forward-looking statements, including but not limited to statements that are predictions ofor indicate future earnings, savings, synergies, events, trends, plans or objectives. The words “believe”, “anticipate”, “expect”, “intend”, “estimate”, “plan”, “assume”, “positioned”, “will”, “may”, “should”,“risk” and other similar expressions, which are predictions of or indicate future events and future trends and which do not relate to historical matters, identify forward-looking statements. In addition, thisdocument includes forward-looking statements relating to our potential exposure to various types of market risks, such as interest rate risk, foreign exchange rate risk and commodity price risk. Youshould not rely on forward-looking statements because they involve known and unknown risks, uncertainties and other factors which are in some cases beyond our control and may cause our actualresults, performance or achievements to differ materially from anticipated future results, performance or achievements expressed or implied by such forward-looking statements (and from past results,performance or achievements). Certain factors that may cause such differences include but are not limited to:

The highly cyclical nature of the pulp and paper industry (and the factors that contribute to such cyclicality, such as levels of demand, production capacity, production, input costs including rawmaterial, energy and employee costs, and pricing)

The impact on our business of adverse changes in global economic conditions The Covid-19 pandemic Unanticipated production disruptions (including as a result of planned or unexpected power outages) Changes in environmental, tax and other laws and regulations Adverse changes in the markets for our products The emergence of new technologies and changes in consumer trends including increased preferences for digital media Consequences of our leverage, including as a result of adverse changes in credit markets that affect our ability to raise capital when needed Adverse changes in the political situation and economy in the countries in which we operate or the effect of governmental efforts to address present or future economic or social problems The impact of restructurings, investments, acquisitions, dispositions and other strategic initiatives (including related financing), any delays, unexpected costs or other problems experienced in

connection with dispositions or with integrating acquisitions or implementing restructurings or other strategic initiatives, and achieving expected savings and synergies, and Currency fluctuations.

We undertake no obligation to publicly update or revise any of these forward-looking statements, whether to reflect new information or future events or circumstances or otherwise.

Regulation G disclosureCertain non-GAAP financial information is contained in this presentation that management believe may be useful in comparing the company’s operating results from period to period. Reconciliation's ofcertain of the non-GAAP measures to the corresponding GAAP measures can be found in the quarterly results booklet for the relevant period. These booklets are available on our website:https://www.sappi.com/quarterly-reports.

Highlights – Q2 FY20

3

EBITDA* $131mDown 30% Y-o-Y

Net debt/EBITDA 3.1X**

EPS* 4 US cents

o Historically low DP prices and reduced volumes significantly impacting profitability

o Packaging and specialities segment continued to grow volumes and profitability

o Significant market share gains in graphics paper business

o Matane integration on track – included in DP segment

o Strong liquidity with cash on hand US$268 million and US$642 million from undrawn committed RCF

• Refer to the supplementary information in this presentation for a reconciliation of EBITDA to reported operating profit and page 25 in our Q2 FY20 financial results booklet (available on www.sappi.com) for a definition of special items.

** Adjusted covenant leverage ratio

Excluding special items*

0

40

80

120

160

200

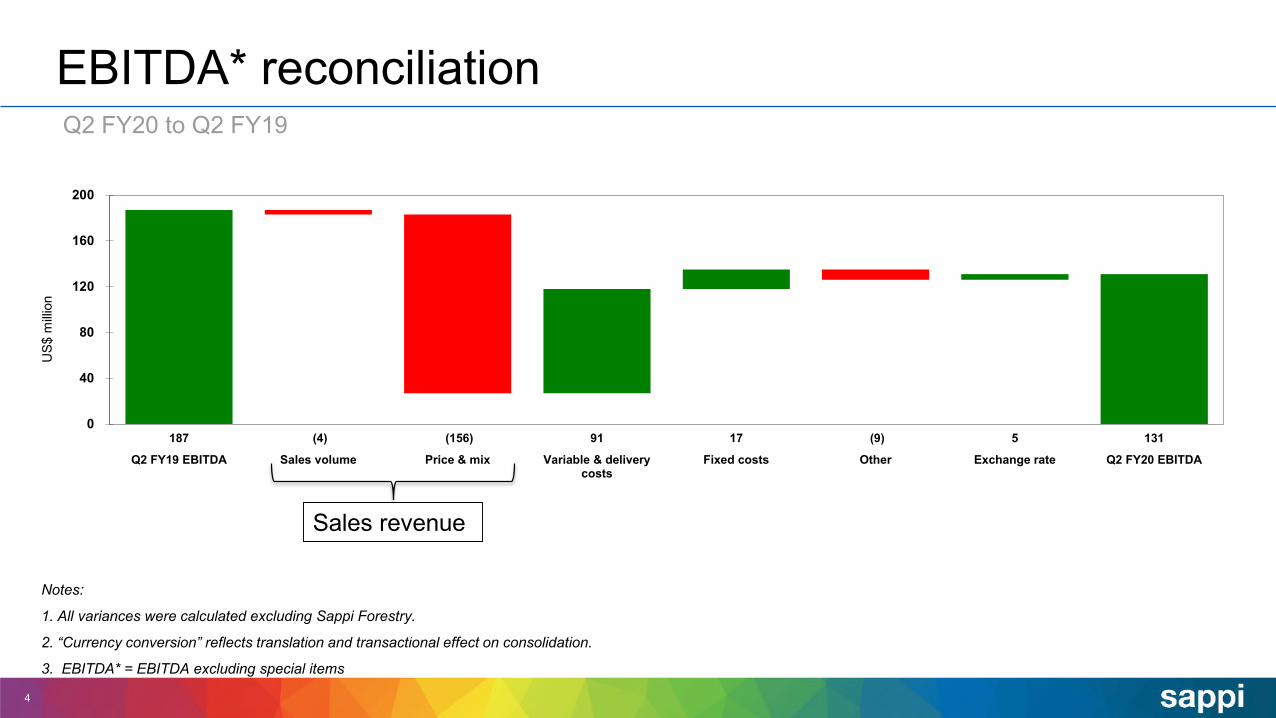

187 (4) (156) 91 17 (9) 5 131

Q2 FY19 EBITDA Sales volume Price & mix Variable & deliverycosts

Fixed costs Other Exchange rate Q2 FY20 EBITDA

EBITDA* reconciliation

4

Q2 FY20 to Q2 FY19

US$

milli

on

Notes:

1. All variances were calculated excluding Sappi Forestry.

2. “Currency conversion” reflects translation and transactional effect on consolidation.

3. EBITDA* = EBITDA excluding special items

Sales revenue

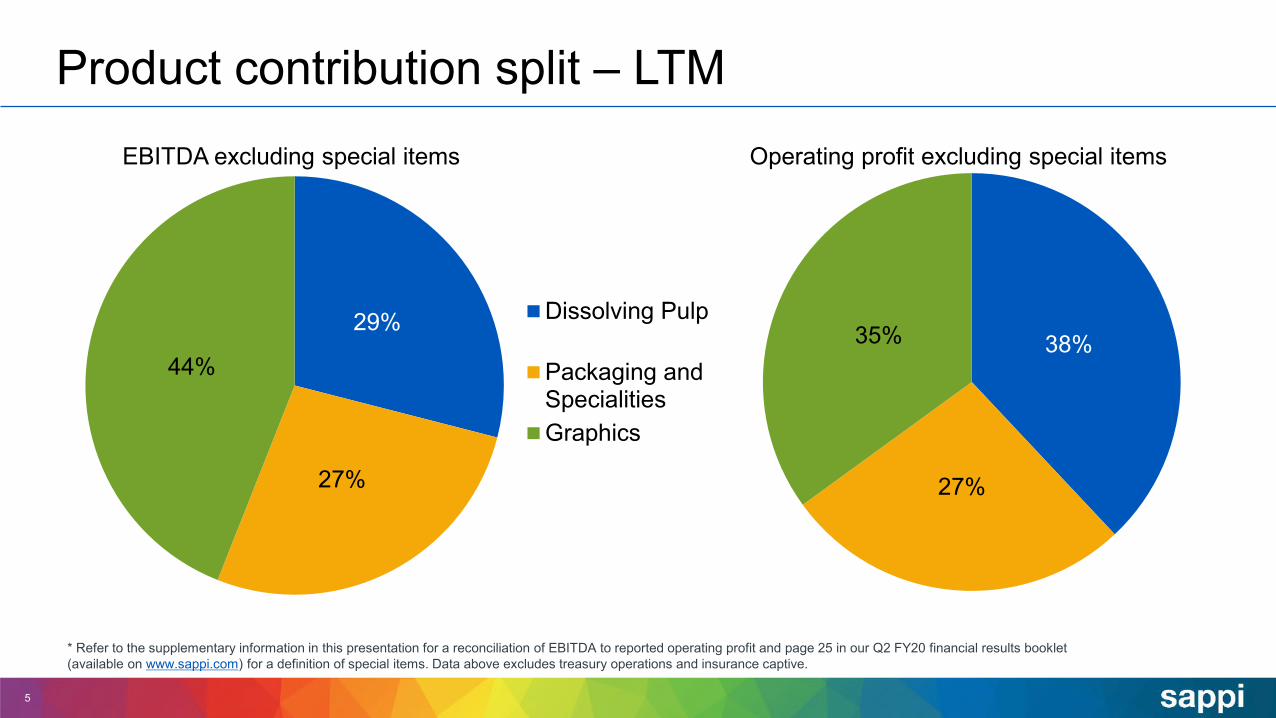

Product contribution split – LTM

5

* Refer to the supplementary information in this presentation for a reconciliation of EBITDA to reported operating profit and page 25 in our Q2 FY20 financial results booklet (available on www.sappi.com) for a definition of special items. Data above excludes treasury operations and insurance captive.

29%

27%

44%

Dissolving Pulp

Packaging andSpecialitiesGraphics

38%

27%

35%

EBITDA excluding special items Operating profit excluding special items

6

Segment volume & EBITDA* margin

0.0%2.0%4.0%6.0%8.0%10.0%12.0%

600700800900

1,0001,1001,200

Graphics volume Graphics margin

0.0%

5.0%

10.0%

15.0%

20.0%

100

150

200

250

300

350

Pack/Spec volume Pack/Spec margin

0%

10%

20%

30%

40%

100150200250300350400

DP volume EBITDA margin

EBITDA* = EBITDA excluding special items

Maturity profile*Fiscal years

7

268

8723 43 45

455

113

25

526

25

246

347

65 85

0

100

200

300

400

500

600

2020 2021 2022 2023 2024 2025 2026 2027 2032

US$

milli

on

Cash Short-term SPH term debt Securitisation SSA

EUR450m bondEUR350m bond

US$221m bond

*Graph excludes US$97 million in IFRS16 leases – Average maturity of 4 years

Capex

8

0

100

200

300

400

500

600

2016 2017 2018 2019 2020E

US$

milli

on

Maintenance Efficiency and expansion

9

Segmental overview

Sappi Europe

10

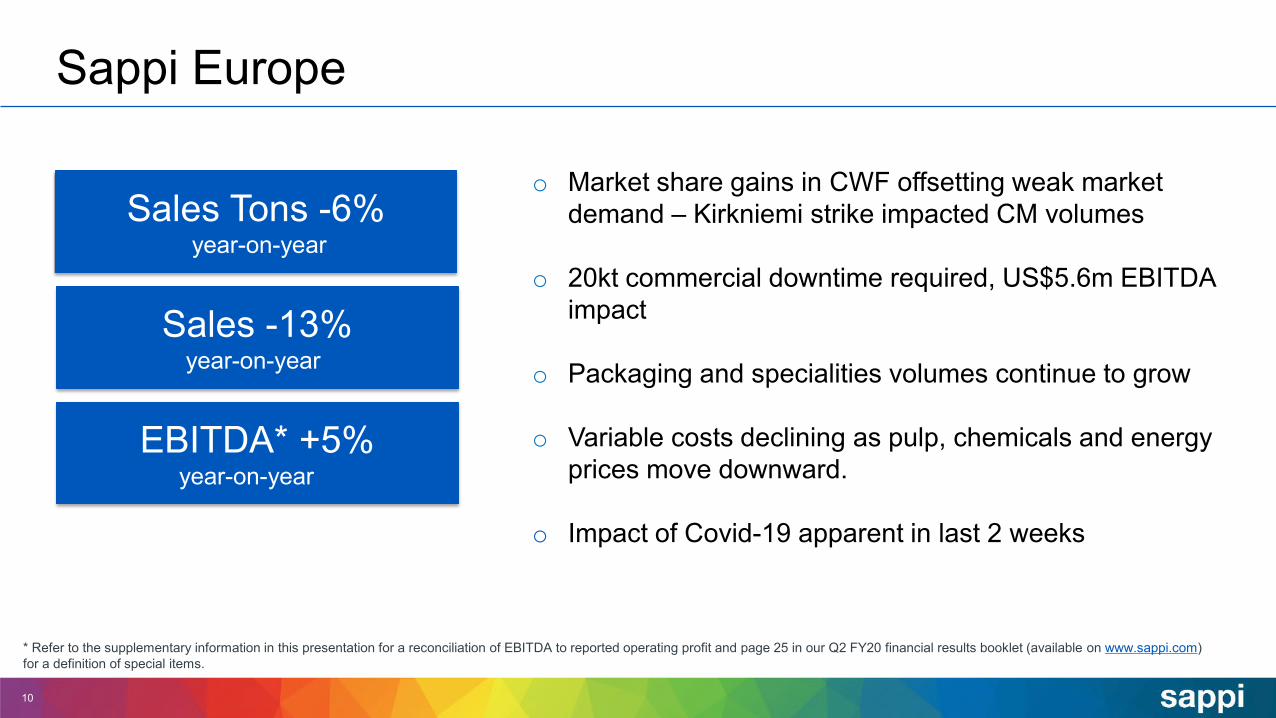

Sales Tons -6%year-on-year

Sales -13%year-on-year

EBITDA* +5%year-on-year

* Refer to the supplementary information in this presentation for a reconciliation of EBITDA to reported operating profit and page 25 in our Q2 FY20 financial results booklet (available on www.sappi.com) for a definition of special items.

o Market share gains in CWF offsetting weak market demand – Kirkniemi strike impacted CM volumes

o 20kt commercial downtime required, US$5.6m EBITDA impact

o Packaging and specialities volumes continue to grow

o Variable costs declining as pulp, chemicals and energy prices move downward.

o Impact of Covid-19 apparent in last 2 weeks

Sappi North America

11

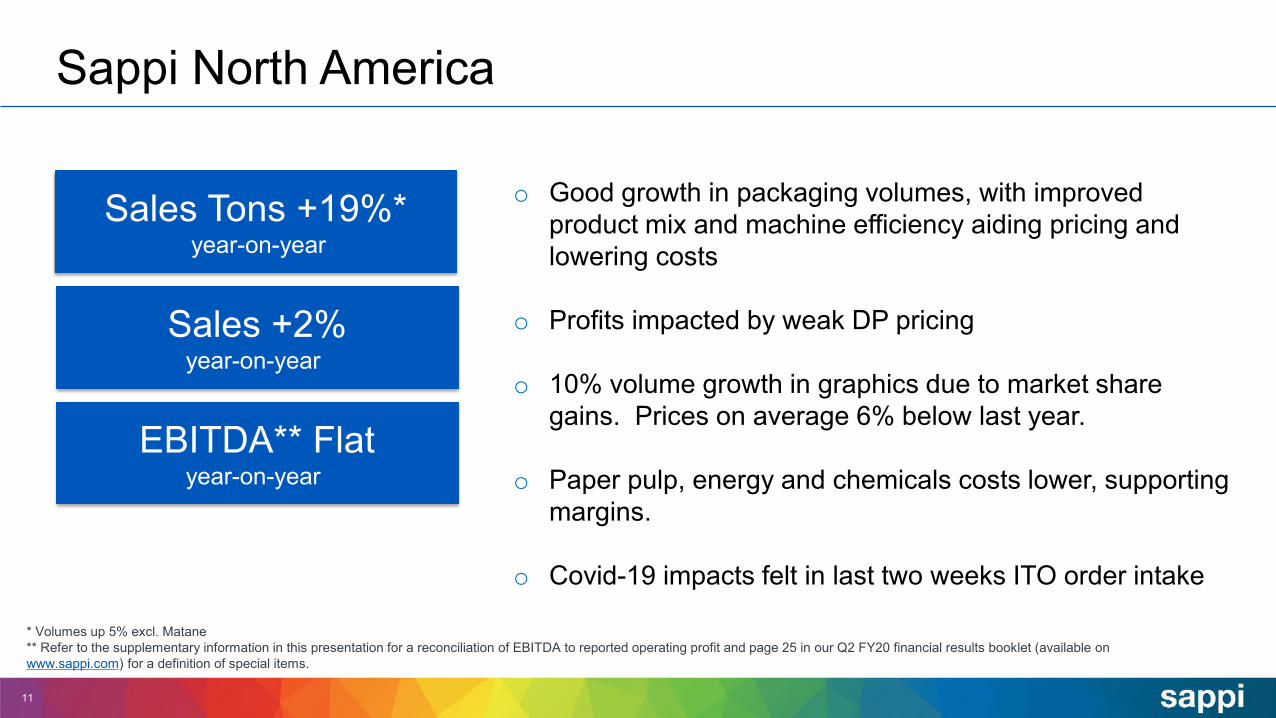

Sales Tons +19%*year-on-year

Sales +2%year-on-year

EBITDA** Flatyear-on-year

* Volumes up 5% excl. Matane** Refer to the supplementary information in this presentation for a reconciliation of EBITDA to reported operating profit and page 25 in our Q2 FY20 financial results booklet (available on www.sappi.com) for a definition of special items.

o Good growth in packaging volumes, with improved product mix and machine efficiency aiding pricing and lowering costs

o Profits impacted by weak DP pricing

o 10% volume growth in graphics due to market share gains. Prices on average 6% below last year.

o Paper pulp, energy and chemicals costs lower, supporting margins.

o Covid-19 impacts felt in last two weeks ITO order intake

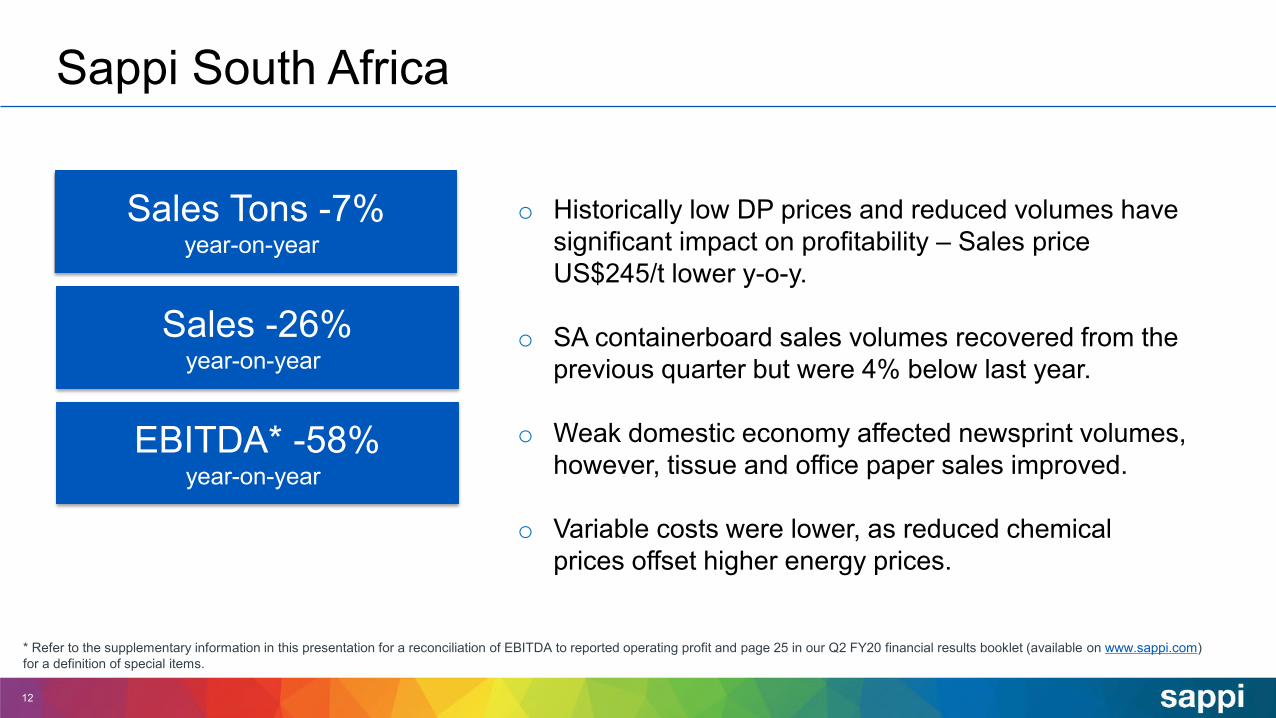

Sappi South Africa

12

Sales Tons -7%year-on-year

Sales -26%year-on-year

EBITDA* -58%year-on-year

* Refer to the supplementary information in this presentation for a reconciliation of EBITDA to reported operating profit and page 25 in our Q2 FY20 financial results booklet (available on www.sappi.com) for a definition of special items.

o Historically low DP prices and reduced volumes have significant impact on profitability – Sales price US$245/t lower y-o-y.

o SA containerboard sales volumes recovered from the previous quarter but were 4% below last year.

o Weak domestic economy affected newsprint volumes, however, tissue and office paper sales improved.

o Variable costs were lower, as reduced chemical prices offset higher energy prices.

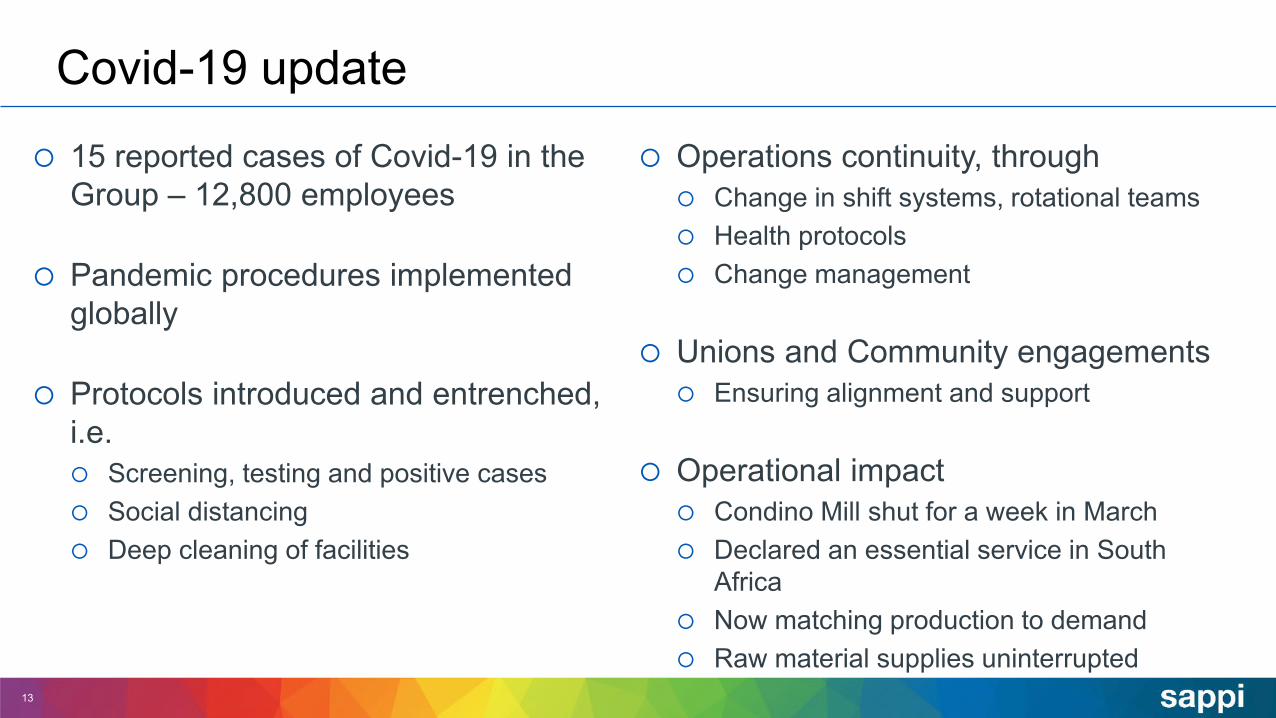

Covid-19 update

13

15 reported cases of Covid-19 in the Group – 12,800 employees

Pandemic procedures implemented globally

Protocols introduced and entrenched, i.e. Screening, testing and positive cases Social distancing Deep cleaning of facilities

Operations continuity, through Change in shift systems, rotational teams Health protocols Change management

Unions and Community engagements Ensuring alignment and support

Operational impact Condino Mill shut for a week in March Declared an essential service in South

Africa Now matching production to demand Raw material supplies uninterrupted

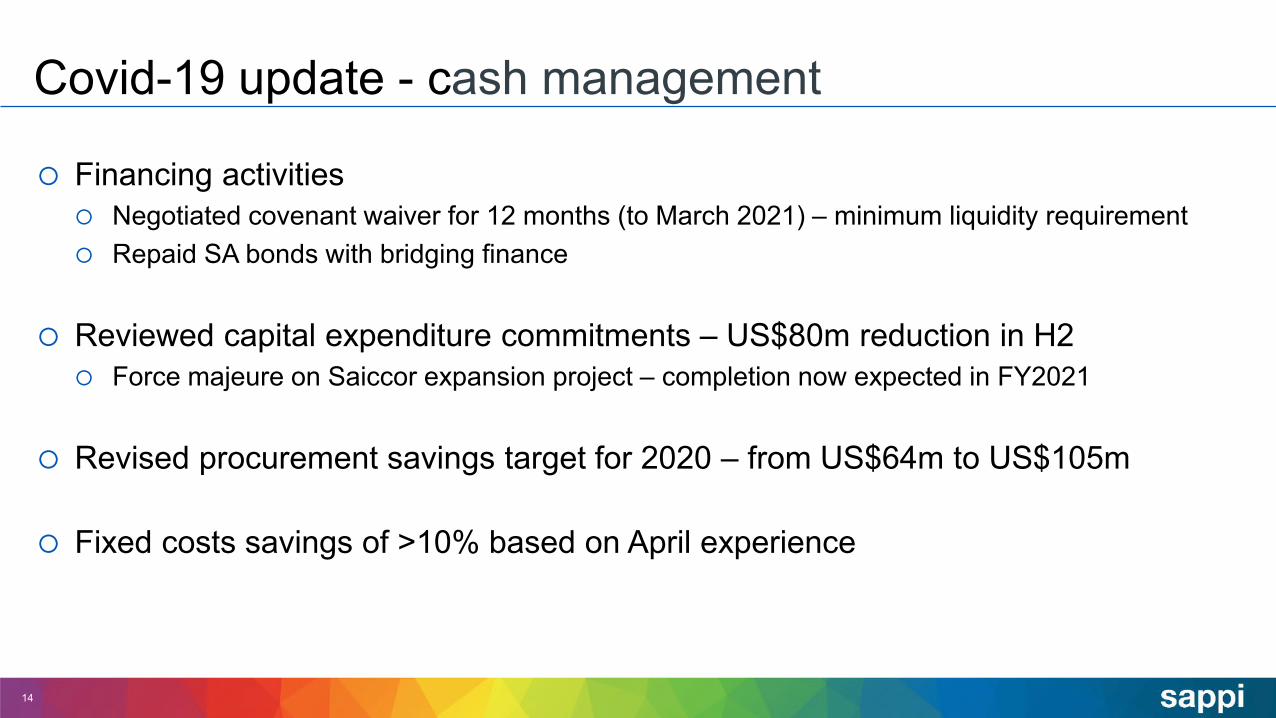

Covid-19 update - cash management

Financing activities Negotiated covenant waiver for 12 months (to March 2021) – minimum liquidity requirement Repaid SA bonds with bridging finance

Reviewed capital expenditure commitments – US$80m reduction in H2 Force majeure on Saiccor expansion project – completion now expected in FY2021

Revised procurement savings target for 2020 – from US$64m to US$105m

Fixed costs savings of >10% based on April experience

14

Covid-19 update - cash management

Working capital management Restricting stock build Resisting delays in receivables – Overdues remain constant with prior quarters

Applying for government assistance where criteria is met Differs by region, mostly from May onwards

Short-interval control Daily cash monitoring and weekly cash flow forecasts Invoice and order intake monitoring

15

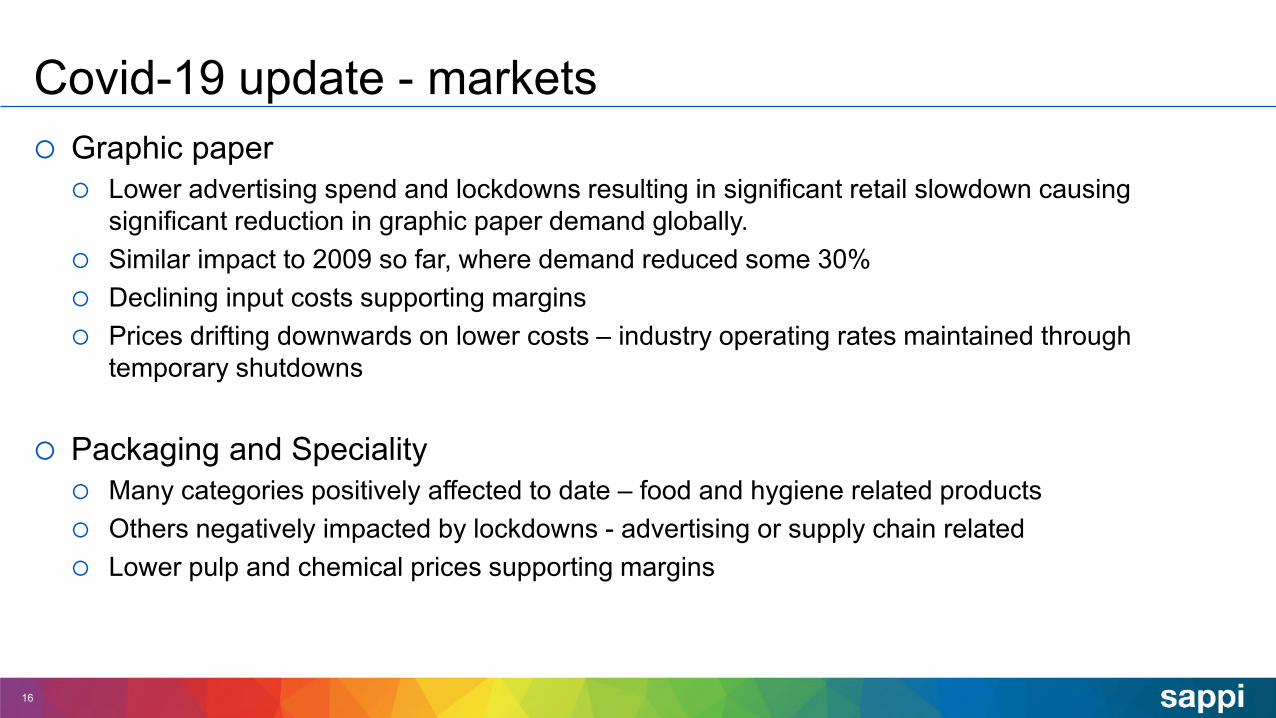

Covid-19 update - markets Graphic paper Lower advertising spend and lockdowns resulting in significant retail slowdown causing

significant reduction in graphic paper demand globally. Similar impact to 2009 so far, where demand reduced some 30% Declining input costs supporting margins Prices drifting downwards on lower costs – industry operating rates maintained through

temporary shutdowns

Packaging and Speciality Many categories positively affected to date – food and hygiene related products Others negatively impacted by lockdowns - advertising or supply chain related Lower pulp and chemical prices supporting margins

16

Covid-19 update - markets

Dissolving Pulp Retail lockdowns in many geographies have impacted entire textile supply chain

Growth in E-commerce/online sales not enough to offset impact on brick and mortar stores Initial signs in China point to a slow recovery post lock-down

DP demand down approximately 35%, similar to 2009, though duration then was short-lived. Exchange rate movements lowering costs for many producers, DP price trending lower in line

with VSF pricing. VSF production impacted by lockdowns in some regions – excess capacity remains an issue

with lower demand. BCTMP sales holding up well, and pricing has improved over the last few months

17

18

US retail sales March 2020 - 8.7% MoM by category

-50.5%

-27.1% -26.8% -26.5%-23.3%

-19.7%-15.1%

1.3% 3.1% 4.3%

26.9%

-60%

-45%

-30%

-15%

0%

15%

30% Retail sales % +(-) change in March , month over month

Average retail sales -8.7%

The coronavirus pandemic triggered steep drops in several areas of March retail sales

Source: US Commerce Department

19

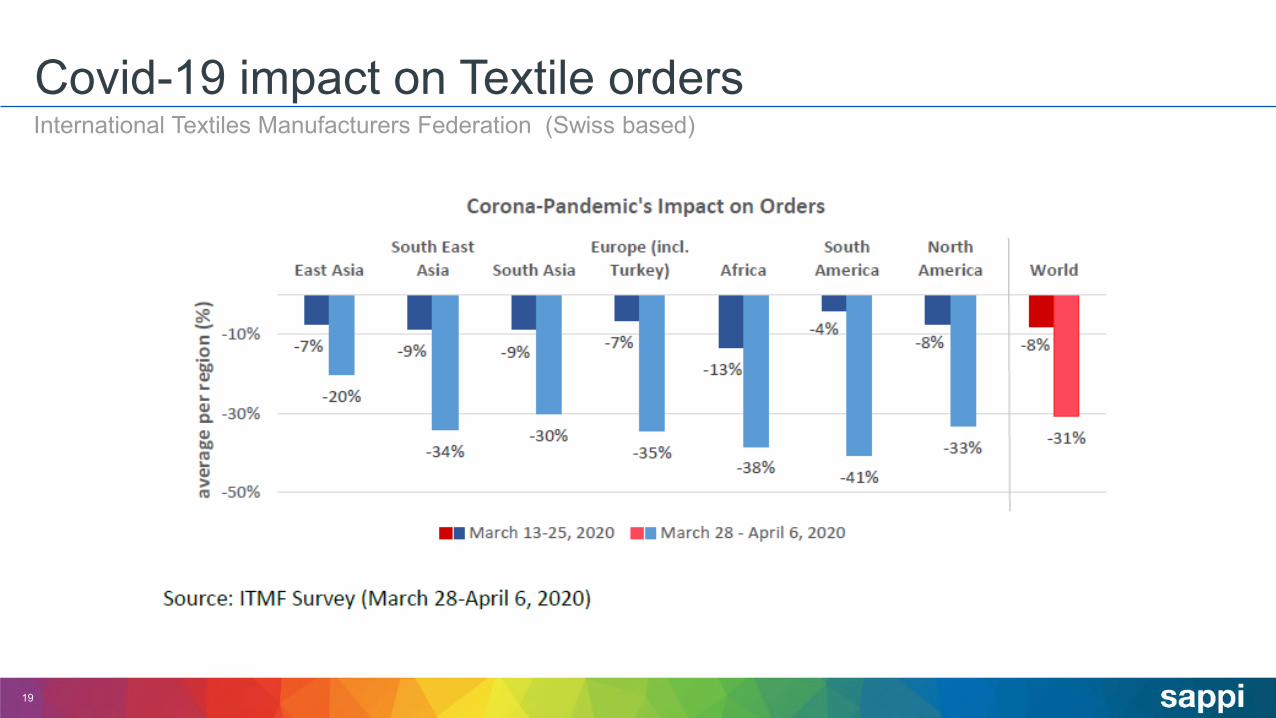

Covid-19 impact on Textile ordersInternational Textiles Manufacturers Federation (Swiss based)

Maintaina healthybalancesheet

Rationalisedeclining

businesses

Accelerate growth in

higher margin growth

segments

Achievecost

advantages

Improveoperational

and machineefficiencies

Maximiseprocurement

benefits Optimisebusiness

processes

Continuouslybalance

paper supplyand demandin all regions

Wherepossible

convert papermachines tohigher marginbusinesses

Optimiseworkingcapital

Strongcash

generationSmart

financing

Expandpaper

packaginggrades

Enhancespecialised celluloseportfolio

Extractvalue from our

biorefinerystream

Our group strategy

20

At Sappi we do business with integrity and courage; making smart decisions which we execute with speed.Our values are underpinned by an unrelenting focus on and commitment to safety.

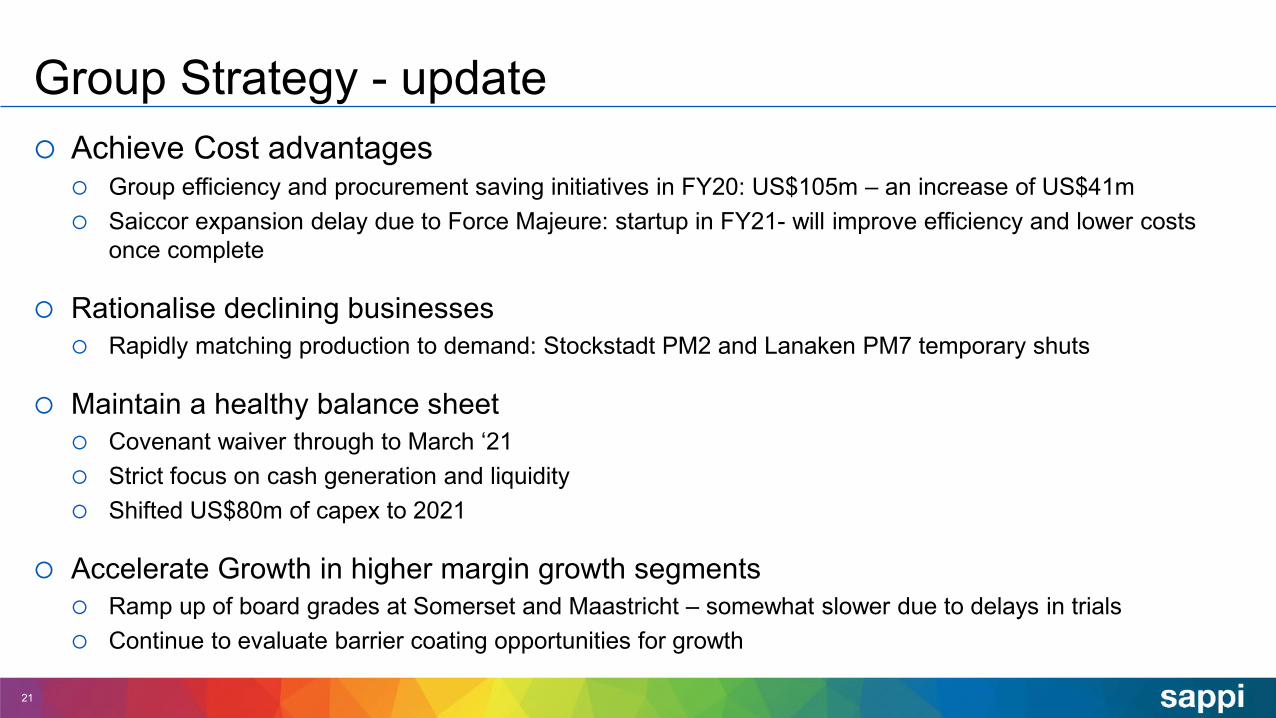

Group Strategy - update Achieve Cost advantages

Group efficiency and procurement saving initiatives in FY20: US$105m – an increase of US$41m Saiccor expansion delay due to Force Majeure: startup in FY21- will improve efficiency and lower costs

once complete

Rationalise declining businesses Rapidly matching production to demand: Stockstadt PM2 and Lanaken PM7 temporary shuts

Maintain a healthy balance sheet Covenant waiver through to March ‘21 Strict focus on cash generation and liquidity Shifted US$80m of capex to 2021

Accelerate Growth in higher margin growth segments Ramp up of board grades at Somerset and Maastricht – somewhat slower due to delays in trials Continue to evaluate barrier coating opportunities for growth

21

DP and Graphic paper demand expected to be significantly impacted

Focus on liquidity and cash flow – various cost savings measures implemented, excess production

curtailed, non-essential capital expenditure delayed and optimisation of working capital.

Packaging and specialities segment continues to grow and recent conversions will continue to

ramp up. Citrus outlook encouraging which will positively impact SA containerboard sales.

Saiccor expansion project completion likely only in FY2021 due to force majeure declaration.

Annual maintenance shuts shifted as late as possible and capital expenditure for remainder of

2020 expected to be US$200 million.

22

Outlook

Thank you

23

24

Supplementary information

Excluding special items*

25

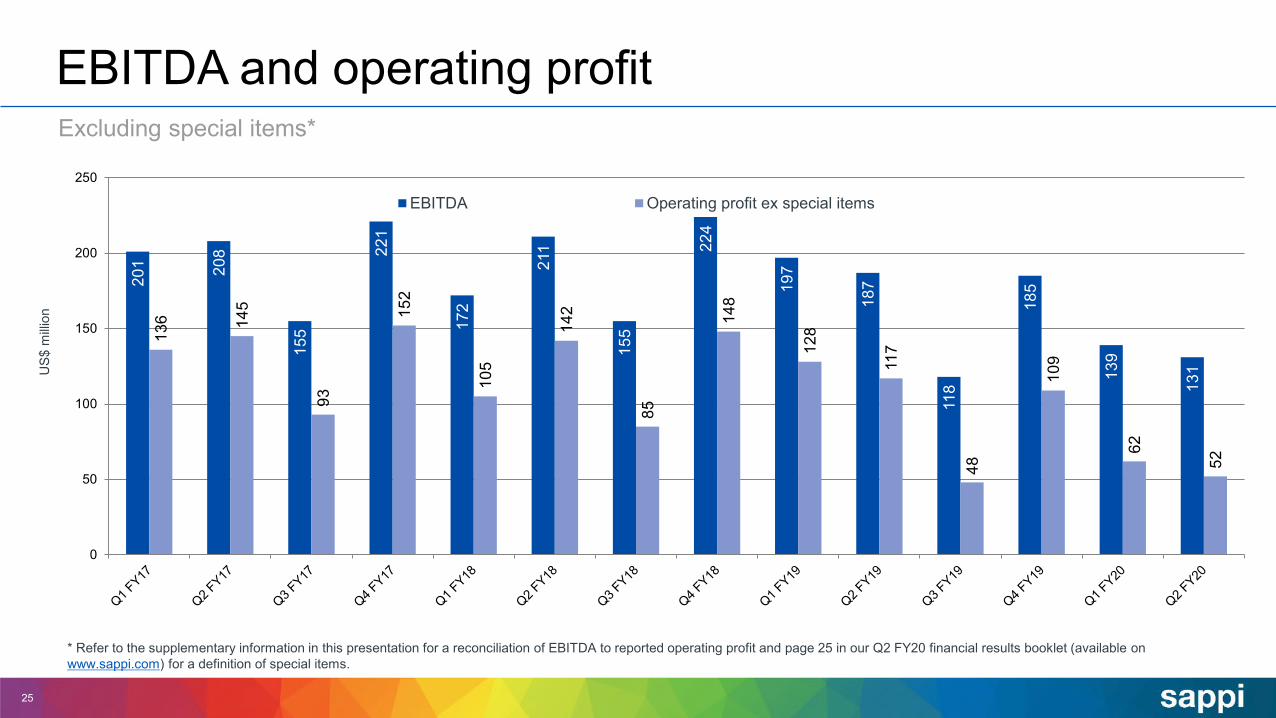

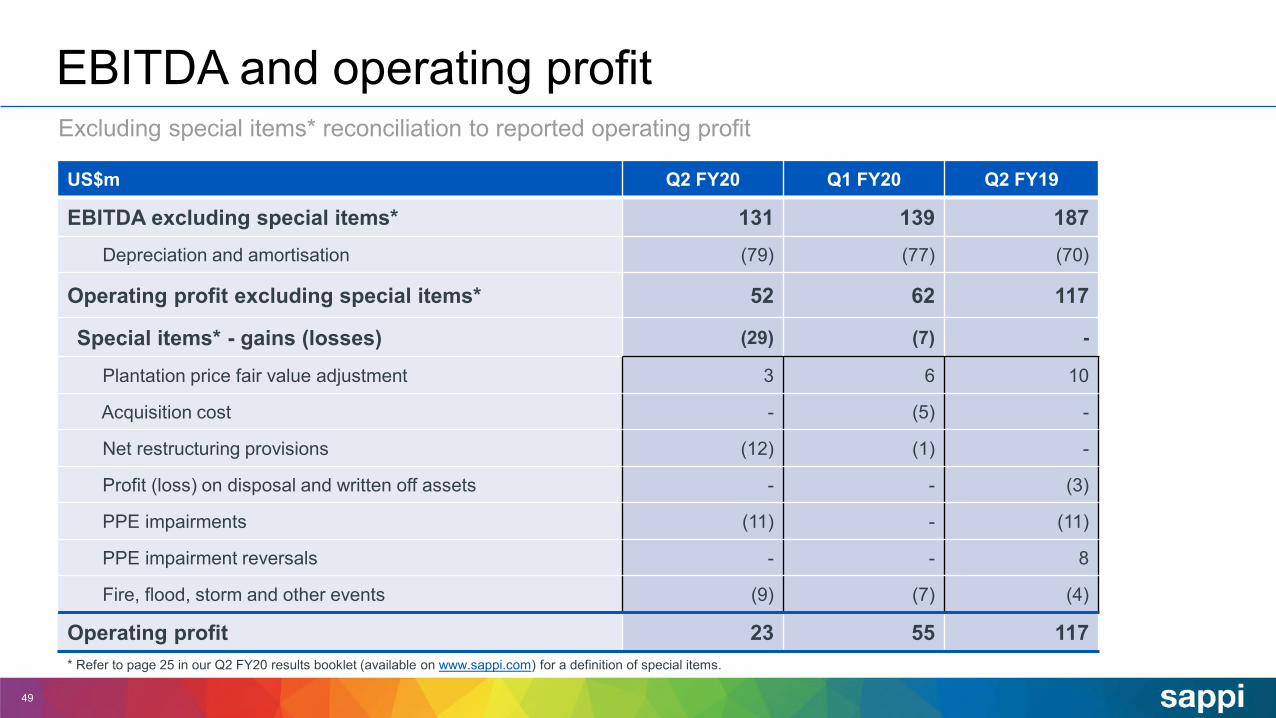

EBITDA and operating profit

* Refer to the supplementary information in this presentation for a reconciliation of EBITDA to reported operating profit and page 25 in our Q2 FY20 financial results booklet (available on www.sappi.com) for a definition of special items.

201 20

8

155

221

172

211

155

224

197

187

118

185

139

131

136 14

5

93

152

105

142

85

148

128

117

48

109

62

52

0

50

100

150

200

250

US$

milli

on

EBITDA Operating profit ex special items

26

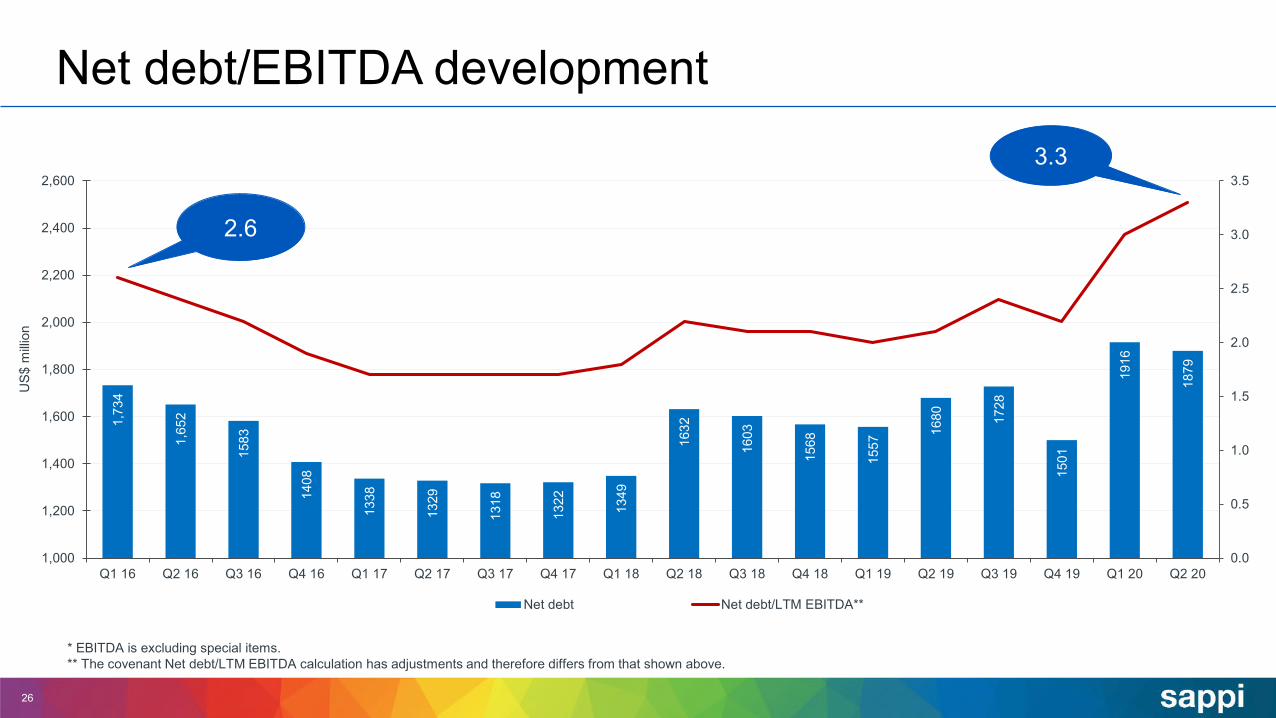

Net debt/EBITDA development

* EBITDA is excluding special items.** The covenant Net debt/LTM EBITDA calculation has adjustments and therefore differs from that shown above.

1,73

4

1,65

2

1583

1408

1338

1329

1318

1322 1349

1632

1603

1568

1557

1680 17

28

1501

1916

1879

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18 Q4 18 Q1 19 Q2 19 Q3 19 Q4 19 Q1 20 Q2 20

US$

milli

on

Net debt Net debt/LTM EBITDA**

3.3

2.6

Global packaging and speciality production sitesSappi Somerset (USA)Sappi Alfeld (Germany) Sappi Tugela (South Africa)Sappi Stockstadt (Germany) Sappi Condino (Italy)

Label Papers, Paperboard, Flexible Packaging

Flexible Packaging, Label, Paperboard, Containerboard , Silicone Base Papers,

Functional Papers

ContainerboardLabel Papers, Flexible Packaging, Containerboard

Flexible Packaging, Silicone Base Papers, Dye Sublimation Paper

Sappi Cloquet (USA)Sappi Maastricht (Netherlands) Sappi Ngodwana (South Africa)Sappi Lanaken (Belgium) Rockwell Dundee (Scotland)

Label Papers ContainerboardPaperboard Functional Papers Functional Papers andFlexible Packaging

Sappi Ehingen (Germany)

Containerboard Flexible Packaging, Label Papers, Inkjet Papers, Dye Sublimation Papers

Sappi Carmignano (Italy)

27

Accelerategrowth in

higher margingrowth

segments

Extractvalue from our

biorefinerystream

Enhancespecialisedcelluloseportfolio

Expandpaper

packaginggrades

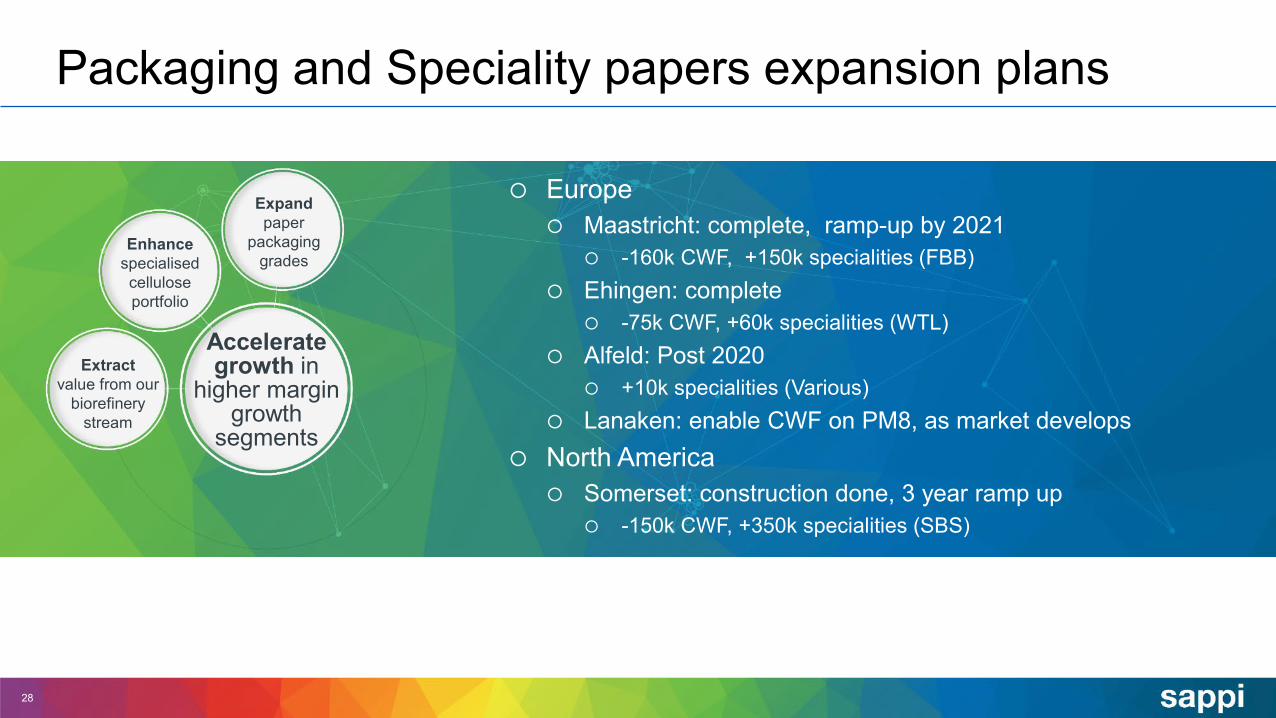

Packaging and Speciality papers expansion plans

28

Europe Maastricht: complete, ramp-up by 2021

-160k CWF, +150k specialities (FBB) Ehingen: complete

-75k CWF, +60k specialities (WTL) Alfeld: Post 2020

+10k specialities (Various) Lanaken: enable CWF on PM8, as market develops

North America Somerset: construction done, 3 year ramp up

-150k CWF, +350k specialities (SBS)

29

Product Groups and ProductsEU Packaging

and Specialities

Sappi North America packaging offering

30

C1S PaperPaperboard (SBS)

Label Paper Bag PaperFolding Carton

LithoLamination

Food service Board

Proto C1S, Spectro C1S

Proto Litho LusterFSBLusterPlate

Bristols

LusterCote LusterPrintSpectro (C1S & C2S)

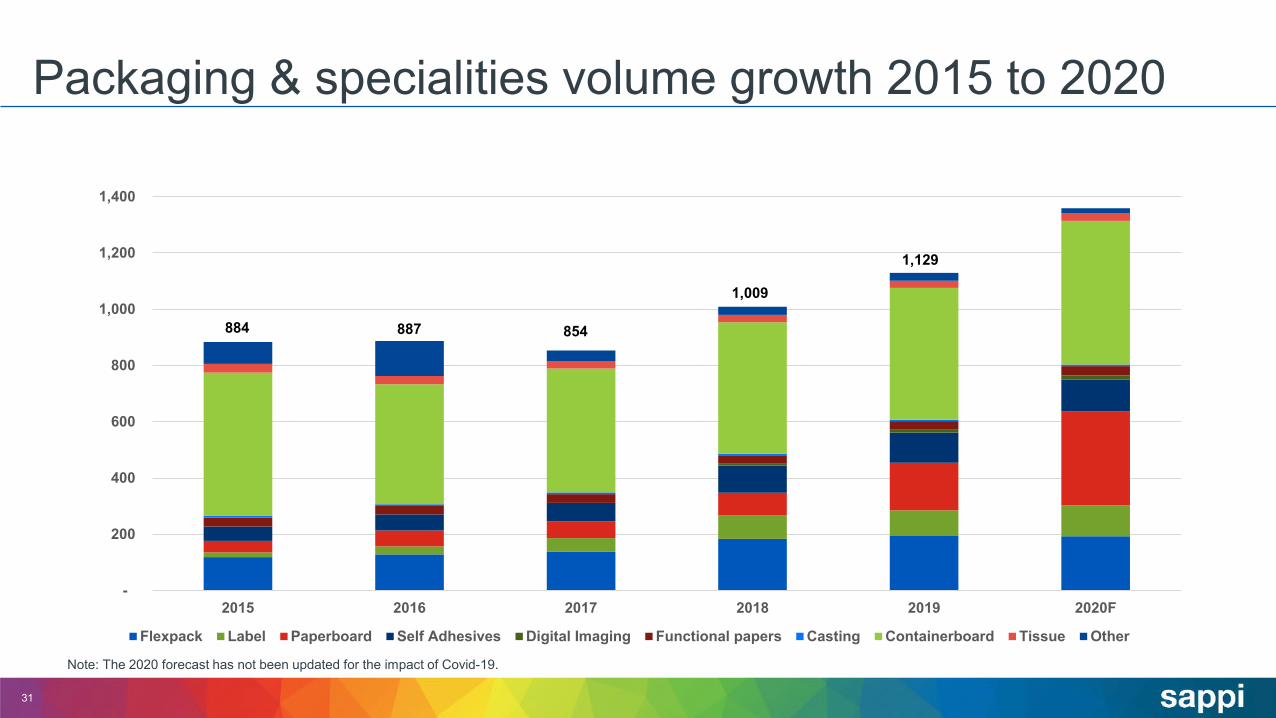

Packaging & specialities volume growth 2015 to 2020

31

-

200

400

600

800

1,000

1,200

1,400

2015 2016 2017 2018 2019 2020F

Flexpack Label Paperboard Self Adhesives Digital Imaging Functional papers Casting Containerboard Tissue Other

884 887 854

1,009

1,129

Note: The 2020 forecast has not been updated for the impact of Covid-19.

32

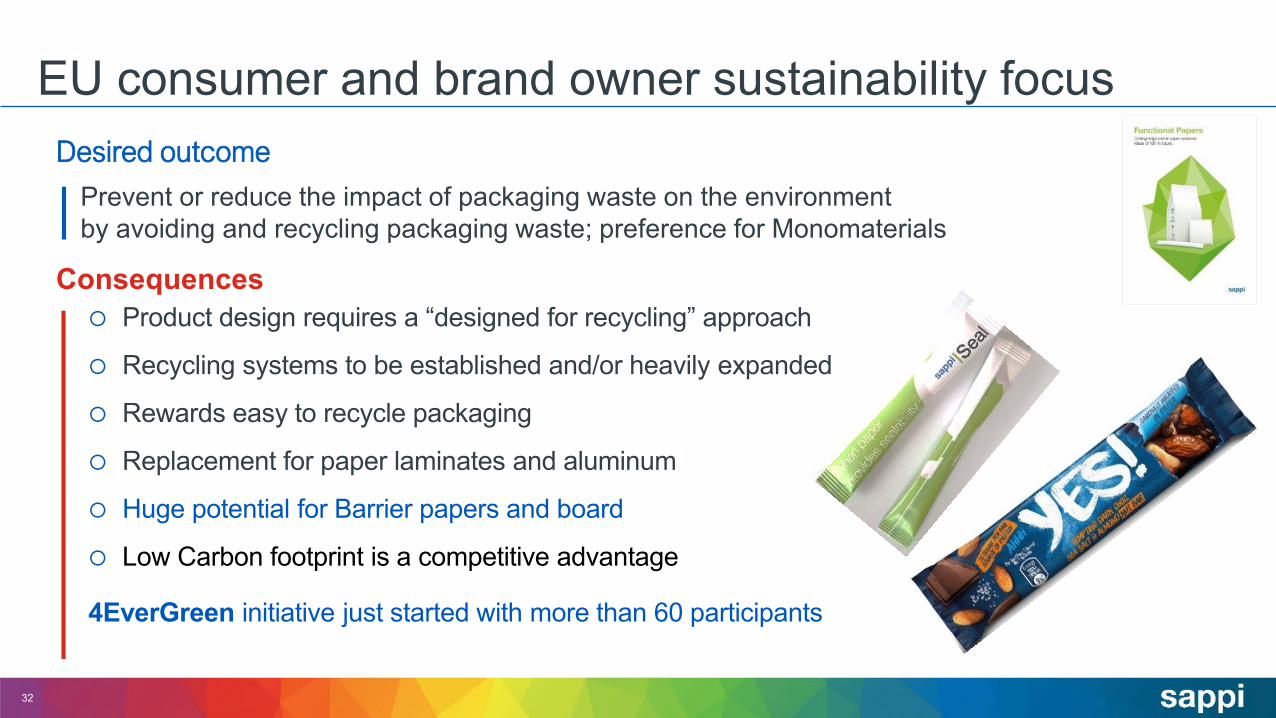

EU consumer and brand owner sustainability focusDesired outcome

Prevent or reduce the impact of packaging waste on the environment by avoiding and recycling packaging waste; preference for Monomaterials

Consequences Product design requires a “designed for recycling” approach

Recycling systems to be established and/or heavily expanded

Rewards easy to recycle packaging

Replacement for paper laminates and aluminum

Huge potential for Barrier papers and board

Low Carbon footprint is a competitive advantage

4EverGreen initiative just started with more than 60 participants

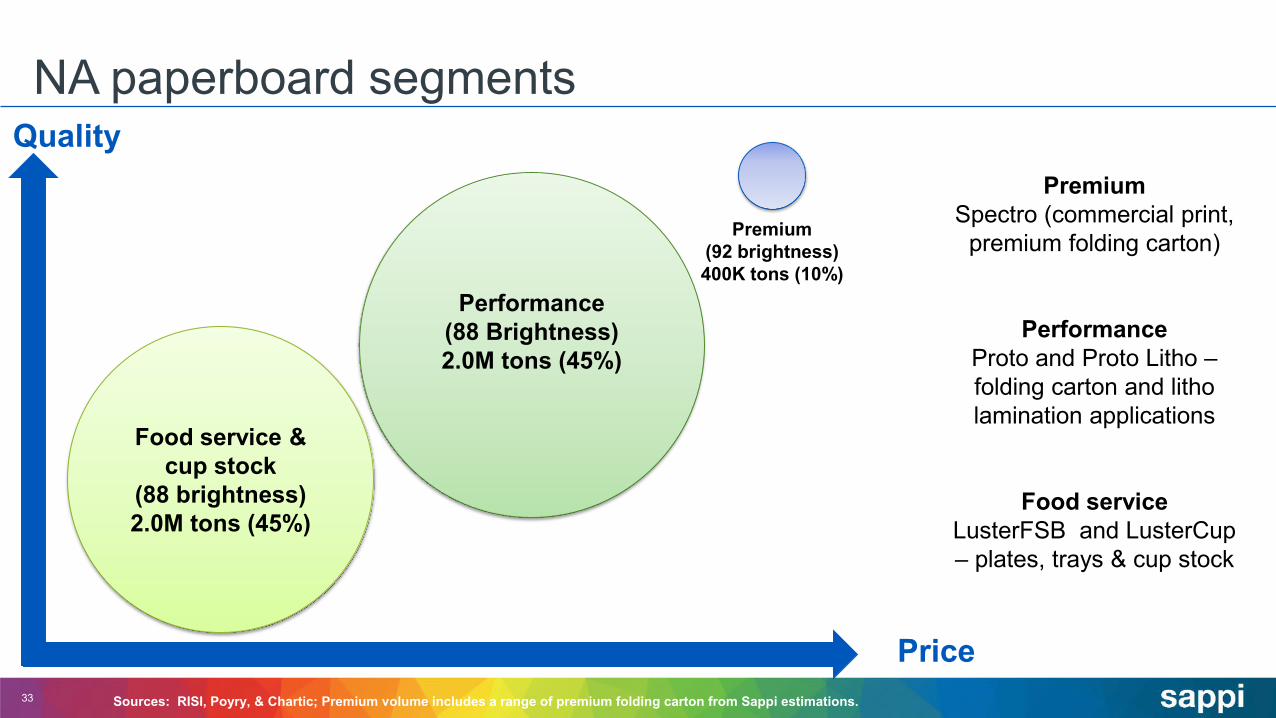

NA paperboard segments

33

PremiumSpectro (commercial print,

premium folding carton)

PerformanceProto and Proto Litho –folding carton and litho lamination applications

Food serviceLusterFSB and LusterCup – plates, trays & cup stock

Sources: RISI, Poyry, & Chartic; Premium volume includes a range of premium folding carton from Sappi estimations.

Performance (88 Brightness)2.0M tons (45%)

Premium (92 brightness)400K tons (10%)

Food service & cup stock

(88 brightness)2.0M tons (45%)

Price

Quality

SA total containerboard market – local market share

34

966

992

967

1,00

0 1,01

2

44%

36% 37% 37% 37%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

940

950

960

970

980

990

1,000

1,010

1,020

FY15 FY16 FY17 FY18 FY19

Market Size (kton) Sappi Market share

Sappi

MondiMpact

Corruseal

New Era

NeopakOther+Import

Market Split Includes Cape Kraft and Enstra

The above market size includes virgin and recycled containerboard

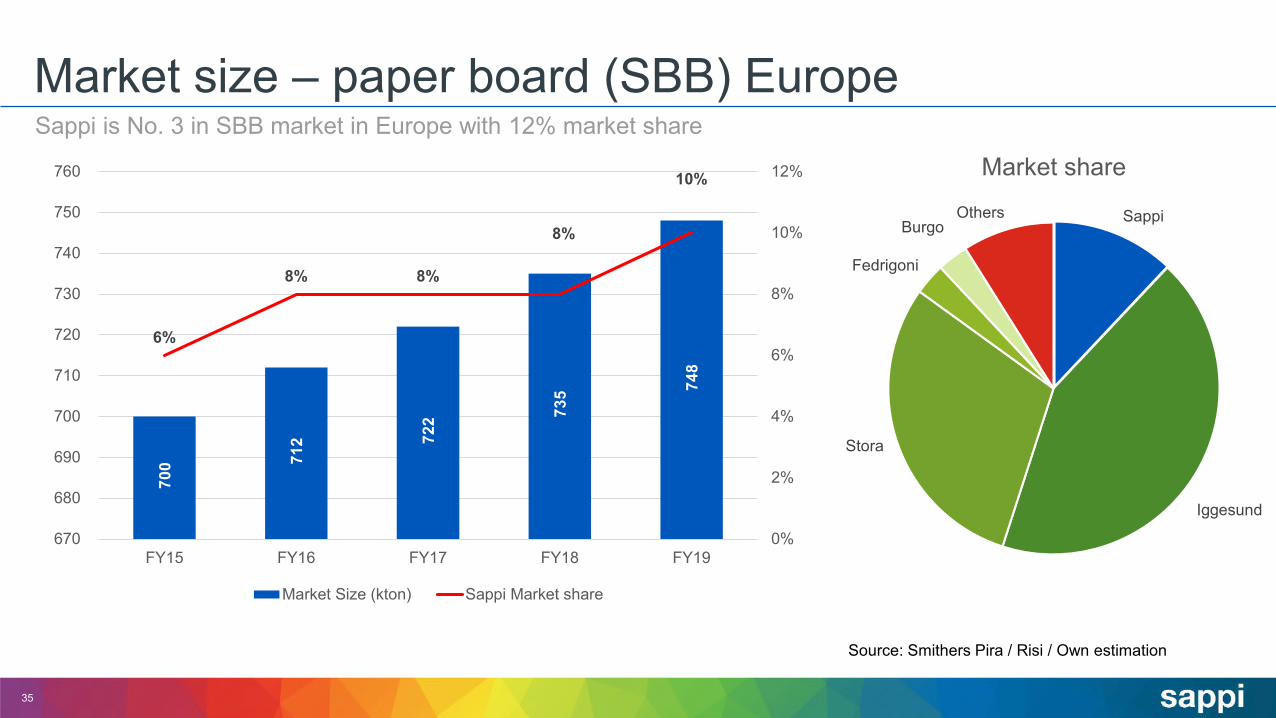

Market size – paper board (SBB) EuropeSappi is No. 3 in SBB market in Europe with 12% market share

35

700 71

2 722 73

5 748

6%

8% 8%

8%

10%

0%

2%

4%

6%

8%

10%

12%

670

680

690

700

710

720

730

740

750

760

FY15 FY16 FY17 FY18 FY19

Market Size (kton) Sappi Market share

Sappi

Iggesund

Stora

Fedrigoni

BurgoOthers

Market share

Source: Smithers Pira / Risi / Own estimation

Market size – flexible packaging EuropeSappi is the market leader in flexible packaging in Europe

36

1,45

5 1,48

3 1,51

2 1,53

4 1,55

7

8%9% 9%

12%13%

0%

2%

4%

6%

8%

10%

12%

14%

1,400

1,420

1,440

1,460

1,480

1,500

1,520

1,540

1,560

1,580

FY15 FY16 FY17 FY18 FY19

Market Size (kton) Sappi Market share

Sappi

Billerud

Mondi

Ahlstrom

Others

Market share

Source: Smithers Pira / Risi / Own estimation

Capacity Limit reached

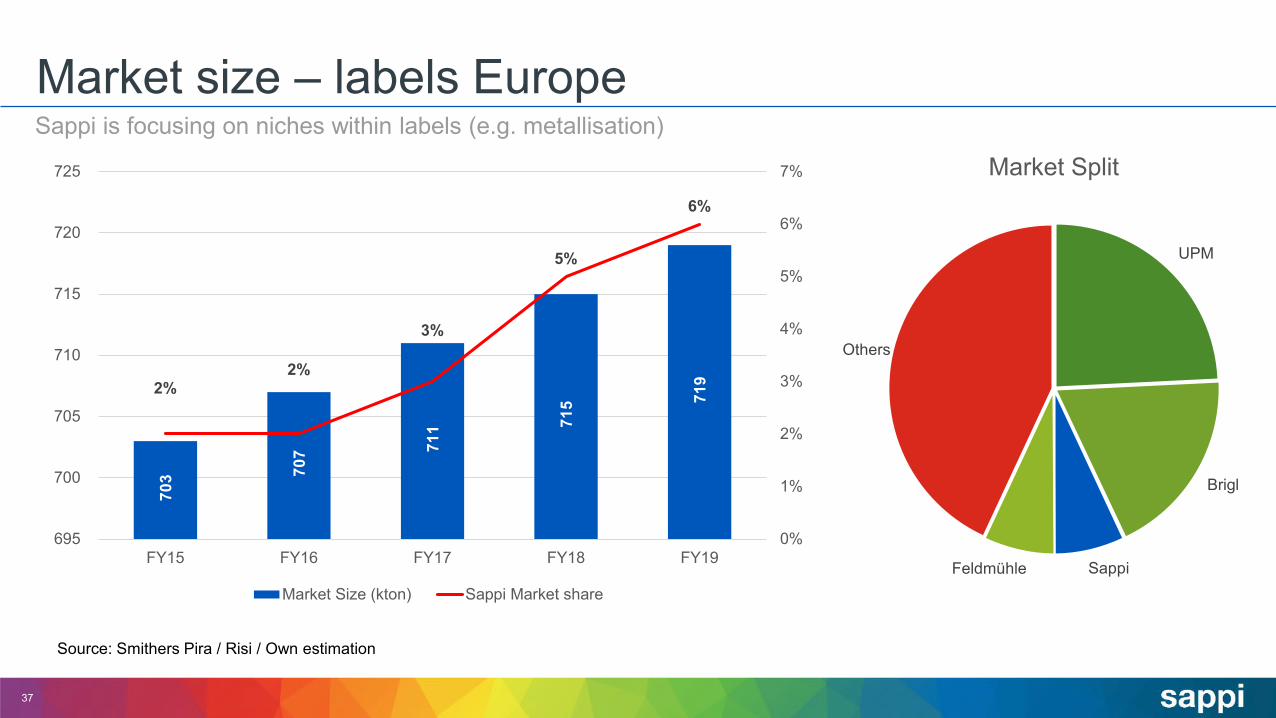

Market size – labels EuropeSappi is focusing on niches within labels (e.g. metallisation)

37

703 70

7 711 71

5 719 2%

2%

3%

5%

6%

0%

1%

2%

3%

4%

5%

6%

7%

695

700

705

710

715

720

725

FY15 FY16 FY17 FY18 FY19

Market Size (kton) Sappi Market share

UPM

Brigl

SappiFeldmühle

Others

Market Split

Source: Smithers Pira / Risi / Own estimation

Market size – self-adhesive EuropeSappi is No. 3 in Europe after UPM and Ahlstrom

38

491 50

2 512 52

2 533

10%11%

13%

18%

20%

0%

5%

10%

15%

20%

25%

470

480

490

500

510

520

530

540

FY15 FY16 FY17 FY18 FY19

Market Size (kton) Sappi Market share

UPM

Ahlstrom

Sappi

Delfort

Others

Market split

Source: Smithers Pira / Risi / Own estimation

Capacity limit reached

Market size – digital solutions EuropeSappi is market leader in dye sublimation in Europe

39

35 40

45 50

58

17%

25%

0

0.05

0.1

0.15

0.2

0.25

0.3

-

10

20

30

40

50

60

70

FY15 FY16 FY17 FY18 FY19

Market Size (kton) Sappi Market share

Sappi

Neenah

F. Schoeller

Beaver

Hansol

Others

Market split

Sappi Neenah F. SchoellerBeaver Hansol Others

Source: Smithers Pira / Pöyry / Risi / Own estimation

40

Sappi Europe

* Sales less operating profit excluding special items divided by tons sold.** Refer to the supplementary information in this presentation for a reconciliation of EBITDA to reported operating profit and page 25 in our Q2 FY20 financial results booklet (available on www.sappi.com) for a definition of special items.

Q2 FY20 Q1 FY20 Q2 FY19

Tons sold (‘000) 793 795 842

Sales (EURm) 606 619 675

Price/Ton (EUR) 764 779 802

Cost/Ton* (EUR) 733 737 773

Operating profit excluding special items**(EURm) 25 33 24

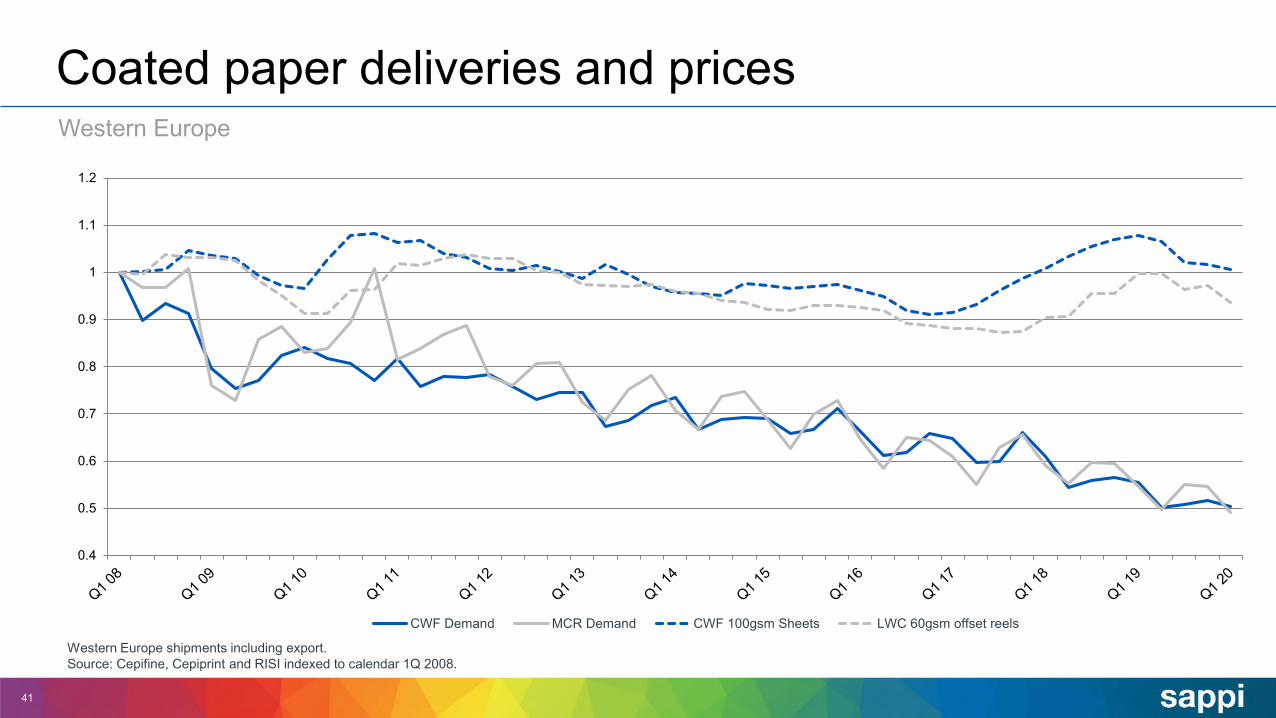

Western Europe

41

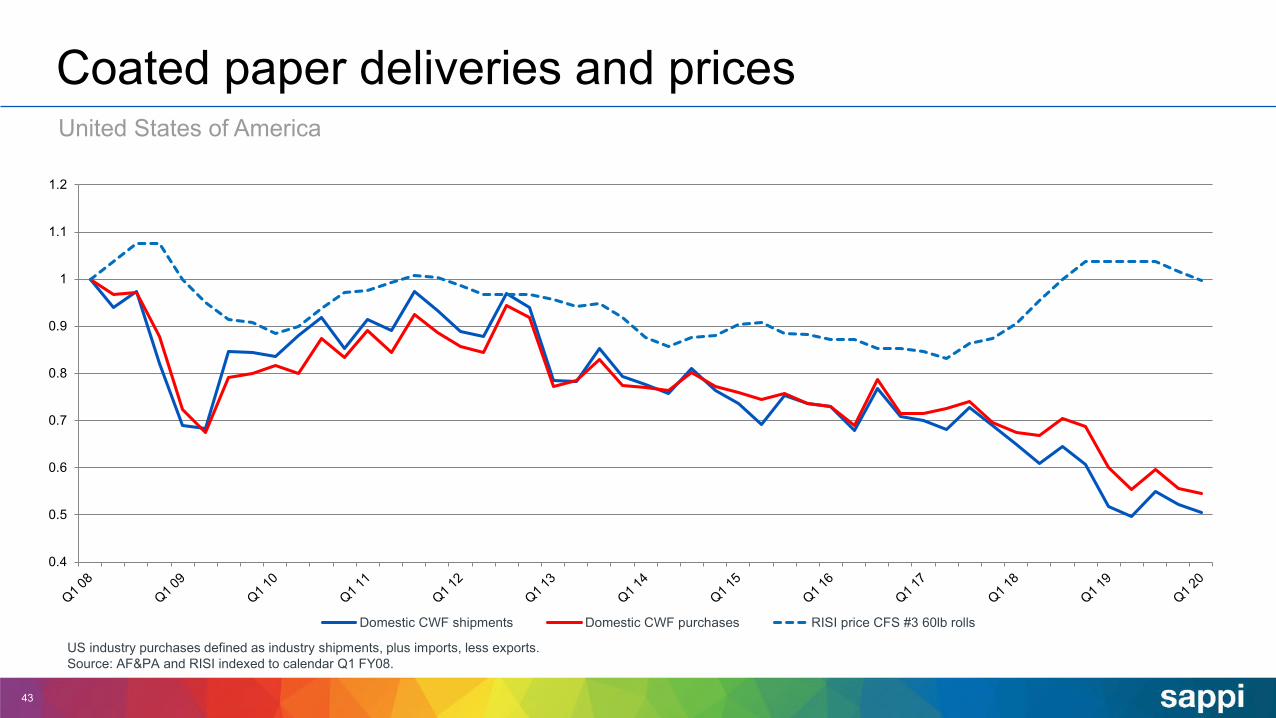

Coated paper deliveries and prices

Western Europe shipments including export.Source: Cepifine, Cepiprint and RISI indexed to calendar 1Q 2008.

0.4

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

CWF Demand MCR Demand CWF 100gsm Sheets LWC 60gsm offset reels

42

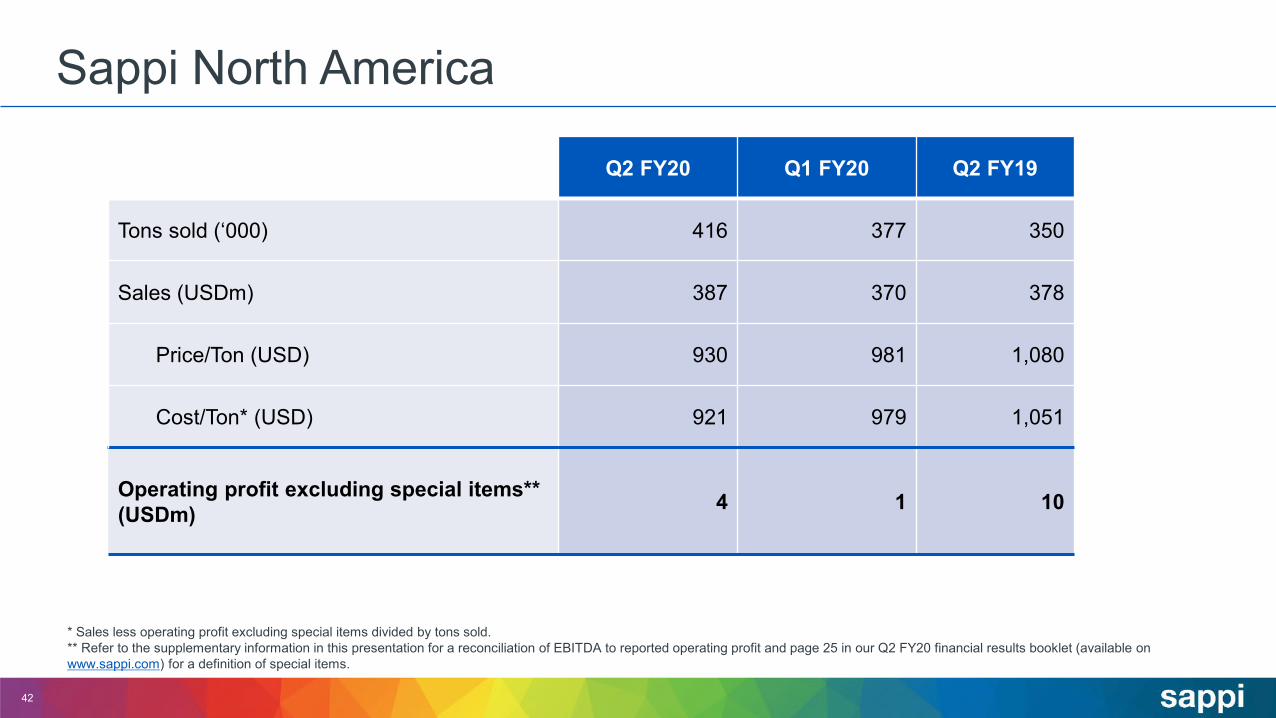

Sappi North America

* Sales less operating profit excluding special items divided by tons sold.** Refer to the supplementary information in this presentation for a reconciliation of EBITDA to reported operating profit and page 25 in our Q2 FY20 financial results booklet (available on www.sappi.com) for a definition of special items.

Q2 FY20 Q1 FY20 Q2 FY19

Tons sold (‘000) 416 377 350

Sales (USDm) 387 370 378

Price/Ton (USD) 930 981 1,080

Cost/Ton* (USD) 921 979 1,051

Operating profit excluding special items**(USDm) 4 1 10

United States of America

43

Coated paper deliveries and prices

US industry purchases defined as industry shipments, plus imports, less exports.Source: AF&PA and RISI indexed to calendar Q1 FY08.

0.4

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

Domestic CWF shipments Domestic CWF purchases RISI price CFS #3 60lb rolls

44

Sappi South Africa

* Sales less operating profit excluding special items divided by tons sold.** Refer to the supplementary information in this presentation for a reconciliation of EBITDA to reported operating profit and page 25 in our Q2 FY20 financial results booklet (available on www.sappi.com) for a definition of special items.

Q2 FY20 Q1 FY19 Q2 FY19

Tons sold (‘000) 389 338 418

Sales (ZARm) 3,979 3,549 4,982

Price/Ton (ZAR) 10,229 10,500 11,919

Cost/Ton* (ZAR) 9,404 9,541 9,237

Operating profit excluding special items**(ZARm) 321 324 1,121

45

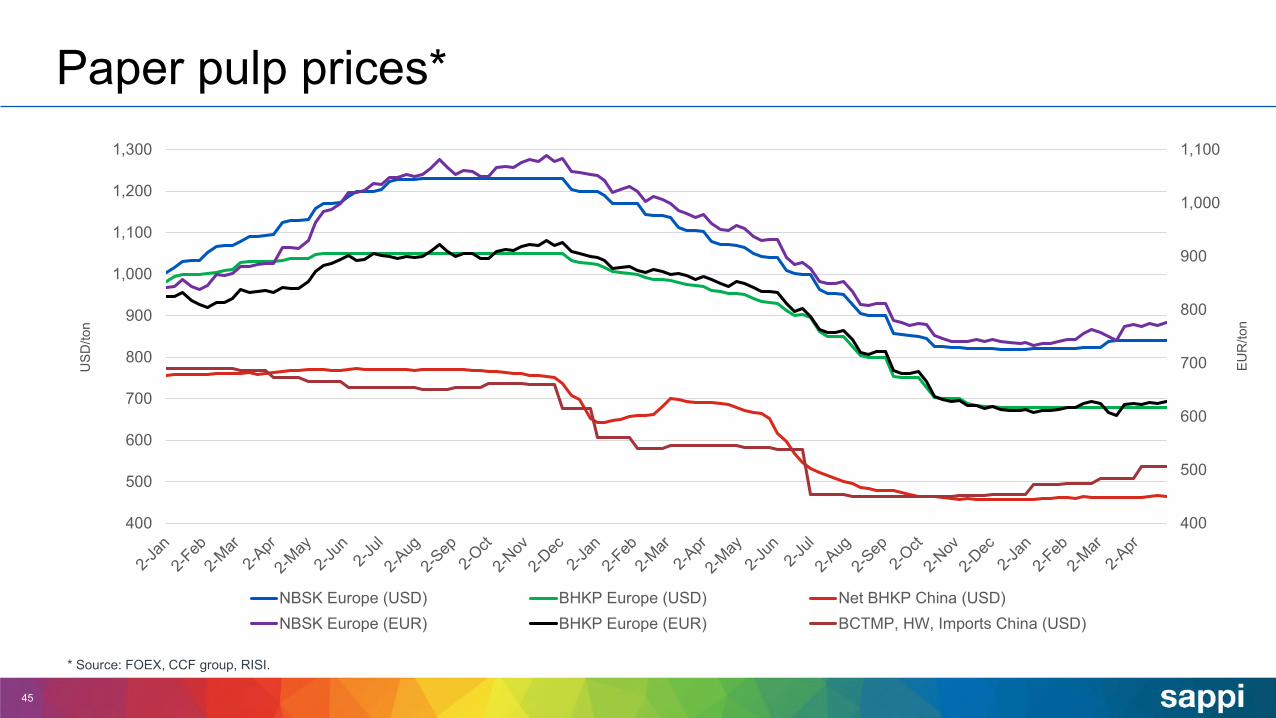

Paper pulp prices*

* Source: FOEX, CCF group, RISI.

EUR

/ton

400

500

600

700

800

900

1,000

1,100

400

500

600

700

800

900

1,000

1,100

1,200

1,300

NBSK Europe (USD) BHKP Europe (USD) Net BHKP China (USD)NBSK Europe (EUR) BHKP Europe (EUR) BCTMP, HW, Imports China (USD)

USD

/ton

46

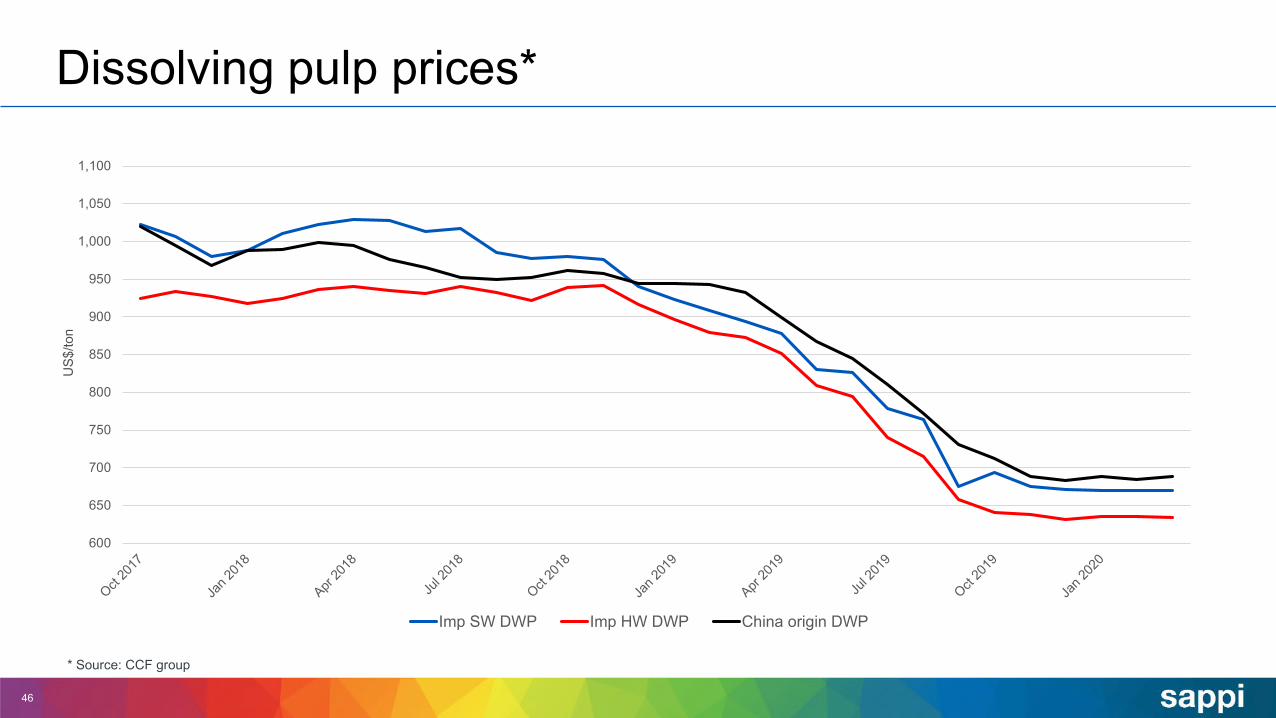

Dissolving pulp prices*

* Source: CCF group

600

650

700

750

800

850

900

950

1,000

1,050

1,100

Imp SW DWP Imp HW DWP China origin DWP

US$

/ton

47

Textile fibre prices*

* Source: CCF group

US$

/ton

0

500

1,000

1,500

2,000

2,500

3,000

Cotton 328 Cotton "A" Index PSF 1.4 D VSF 1.2 D VSF 1.5 D

Cash flow

48

US$m Q2 FY20 Q1 FY20 Q2 FY19

Cash generated from operations 116 136 182Movement in working capital (14) (76) (80)

Net finance costs paid (18) (35) (21)

Finance income received 1 2 1

Taxation (paid) refund (11) (32) (43)

Dividend paid - - (92)

Cash generated from operating activities 74 (5) (53)

Cash utilised in investing activities (74) (273) (95)Capital expenditure (70) (112) (95)

Proceeds on disposal of assets - - 1

Acquisition of subsidiary - (158) -

Other non-current asset movements (4) (3) (1)

Net cash generated (utilised) - (278) (148)

Excluding special items* reconciliation to reported operating profit

49

EBITDA and operating profit

* Refer to page 25 in our Q2 FY20 results booklet (available on www.sappi.com) for a definition of special items.

US$m Q2 FY20 Q1 FY20 Q2 FY19

EBITDA excluding special items* 131 139 187Depreciation and amortisation (79) (77) (70)

Operating profit excluding special items* 52 62 117

Special items* - gains (losses) (29) (7) -

Plantation price fair value adjustment 3 6 10

Acquisition cost - (5) -

Net restructuring provisions (12) (1) -

Profit (loss) on disposal and written off assets - - (3)

PPE impairments (11) - (11)

PPE impairment reversals - - 8

Fire, flood, storm and other events (9) (7) (4)

Operating profit 23 55 117

Thank you

50