Embed Size (px)

Citation preview

1 of 46 January 7, 2017

QF206 Week 1

Quantitative Trading Strategies

Introduction

© Christopher Ting

2 of 46 January 7, 2017

QF206 Week 1

What is Quantitative Trading?

Also known as algorithmic trading

Trading based on buy-or-sell signals generated by algorithms, which are implemented on computer systems for automated executions

Algorithmic signals are highly data driven.

Macroeconomic news: non-farm payroll, FOMC policy etc.

Fundamentals: revenue, cash flow, earnings-per-share etc.

Technical: Moving averages, stochastic indicator, etc.

High-frequency: state of the limit-order book

Algorithmic executions are highly technology driven.

© Christopher Ting

3 of 46 January 7, 2017

QF206 Week 1

The Gist of Quantitative Trading

As long as you can represent relevant information into bits and bytes that the computer system can operate on by the algorithms, it can be regarded as a part of quantitative trading.

Technical analysis

Fundamentals

News

© Christopher Ting

4 of 46 January 7, 2017

QF206 Week 1

In a Nutshell

Algorithmic trading refers to procedural trading rules or strategies

From technical analysis to complex neural network strategies.

Trading horizon can be intraday (high frequency) or longer

Based on trading signals toOpen a position

Close a position, either to take profit or stop loss

© Christopher Ting

5 of 46 January 7, 2017

QF206 Week 1

Institutional Algorithmic Trading (1)

Algorithmic trading (also called automated trading, black box trading and robo-trading) is used to break up large orders into smaller orders to

reduce execution risk

preserve anonymity,

minimize the price impact of a trade.

Hidden portions of large institutional orders are sometimes referred to as dark liquidity pools.

Orders are often partially revealed, in which case they are called iceberg or hidden-size orders.

© Christopher Ting

6 of 46 January 7, 2017

QF206 Week 1

Institutional Algorithmic Trading (2)

The use of programs and computers to generate and execute orders in

markets with electronic access.

Orders come from institutional investors, hedge funds and trading desks.

Institutional clients need to trade large amounts of stocks. These

amounts are often larger than what the market can absorb without

impacting the price.

The main objective of institutional algo trading is not necessarily to

maximize profits but rather to control execution costs and market risk.

The demand for a large amount of liquidity will typically affect the cost

of the trade in a negative fashion (slippage).

Large orders need to be split into smaller orders, to be executed

electronically over the course of minutes, hours and days.

© Christopher Ting

7 of 46 January 7, 2017

QF206 Week 1

Institutional Algo Strategies

Algorithmic trading results from mathematical models that analyze quotes and trades, identify liquidity opportunities, and use the information to make intelligent trading decisions so as to

Trade at or better than the average price over a day (e.g. VWAP, volume weighted average price)

Execute optimally so as to have minimal price impact.

Trade more at market opens and closes when volume is high, and less during slower periods such as around lunch.

Exploit arbitrage opportunities or price spreads between correlated securities.

© Christopher Ting

8 of 46 January 7, 2017

QF206 Week 1

Algo Trading in General

Algorithmic trading is also used in a more general

sense to include “Alpha Models” used to make

trading decisions to generate trading profits or

control risk.

Thus, more generally, algorithmic trading can be

defined as trading based on the use of computer

programs and sophisticated trading analytics to

execute orders according to pre-defined strategies.

© Christopher Ting

9 of 46 January 7, 2017

QF206 Week 1

Who Can Be a Retail Quant Trader?

It is true that most institutional quant traders have advanced degrees in mathematics, science, and engineering.

But trading is deceptively simple: Buy low sell high

Sell high buy low

The crux of the matter is to consistently achieve profitability (after costs, taxes, etc.) quarter after quarter.

If you have taken a few courses in math, statistics, and programming, you are probably as qualified as anyone to tackle some of the basic statistical arbitrage strategies.

© Christopher Ting

10 of 46 January 7, 2017

QF206 Week 1

Who Cannot Be a Retail Quant Trader?

No savings to take care of family commitments

Need immediate profits to sustain daily living

No discipline

Crave for adrenalin pumps

Exuberate over-confidence bordering hubris in character

Hope, delay, and then cut losses in despair

Blame others for losses

Addicted to trading!

No emotional intelligence

Extreme greed: too much risk

Extreme fear: too risk averse

No capacity to conduct independent research

© Christopher Ting

11 of 46 January 7, 2017

QF206 Week 1

Major Asset Classes

Tradable Instruments

© Christopher Ting

12 of 46 January 7, 2017

QF206 Week 1

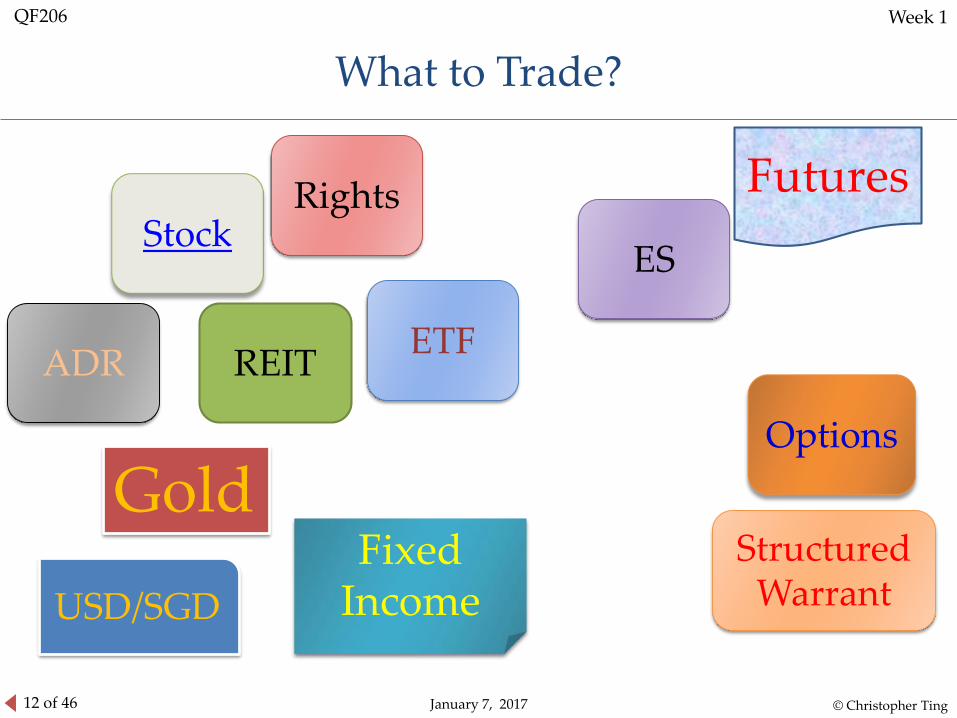

What to Trade?

Stock

ETF

ES

Structured Warrant

ADR

Rights

REIT

Futures

Options

Fixed Income

Gold

USD/SGD

© Christopher Ting

13 of 46 January 7, 2017

QF206 Week 1

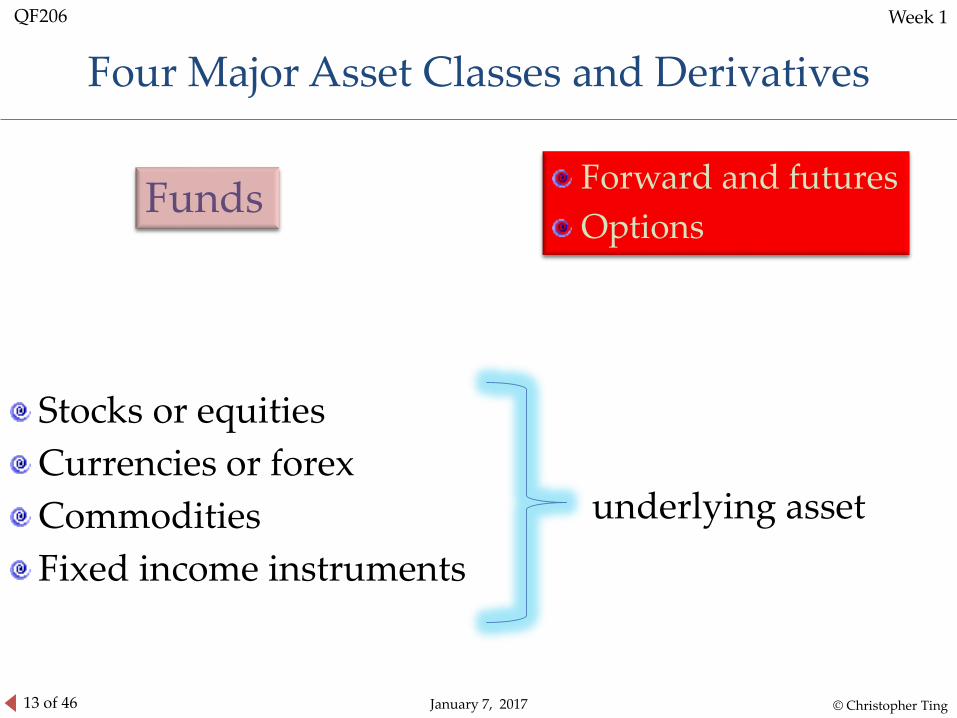

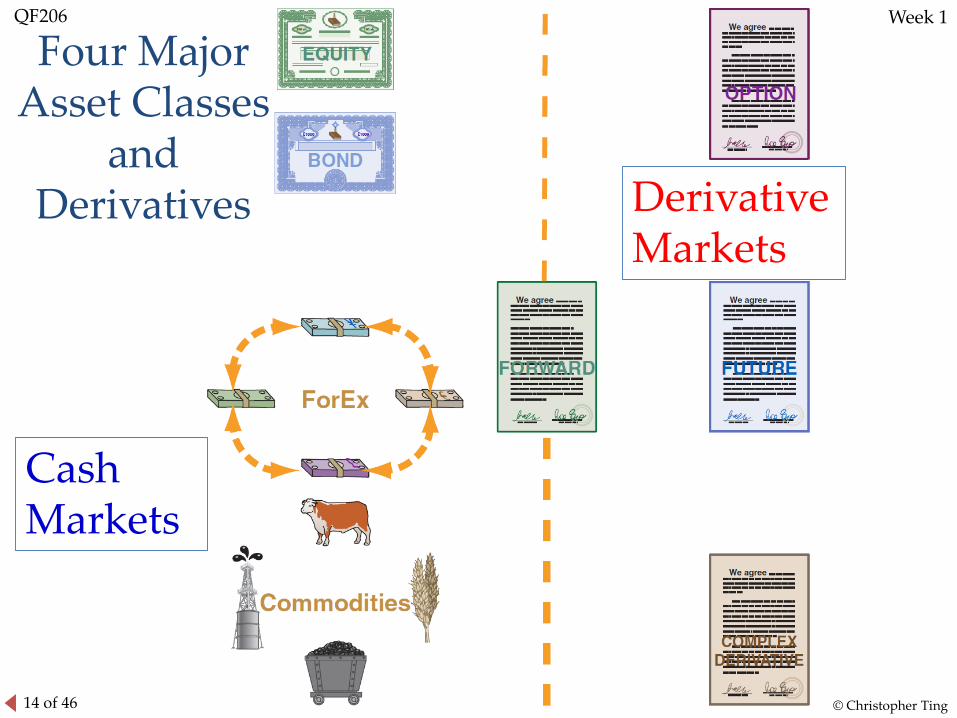

Four Major Asset Classes and Derivatives

Stocks or equities

Currencies or forex

Commodities

Fixed income instruments

Forward and futures

Options

underlying asset

Funds

© Christopher Ting

14 of 46 January 7, 2017

QF206 Week 1

© Christopher Ting

Four Major Asset Classes

and Derivatives

Cash Markets

Derivative Markets

15 of 46 January 7, 2017

QF206 Week 1

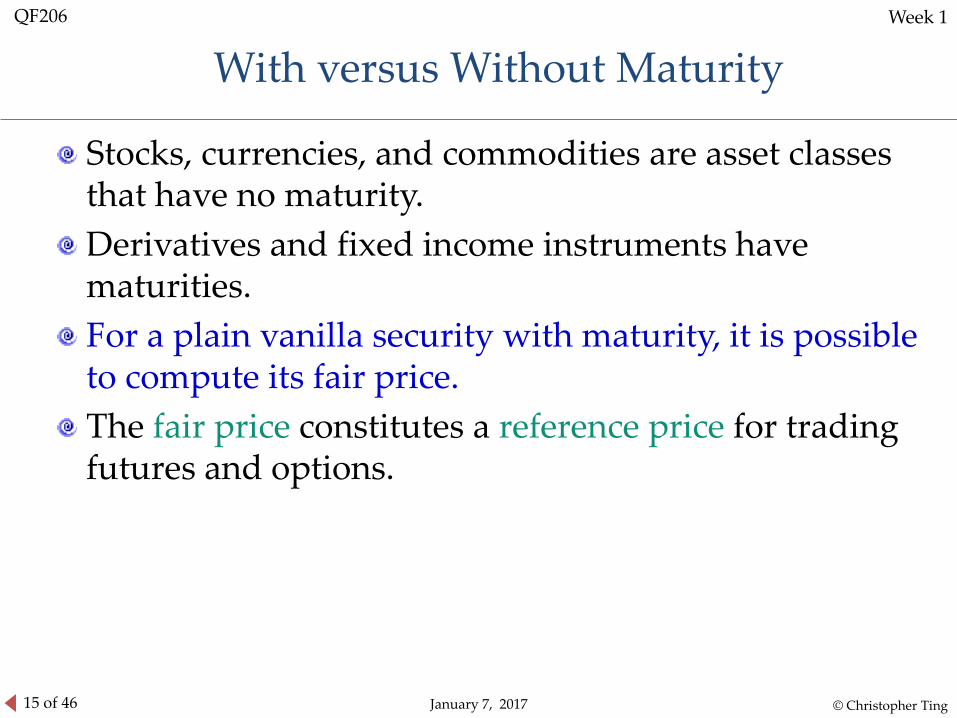

With versus Without Maturity

Stocks, currencies, and commodities are asset classes that have no maturity.

Derivatives and fixed income instruments have maturities.

For a plain vanilla security with maturity, it is possible to compute its fair price.

The fair price constitutes a reference price for trading futures and options.

© Christopher Ting

16 of 46 January 7, 2017

QF206 Week 1

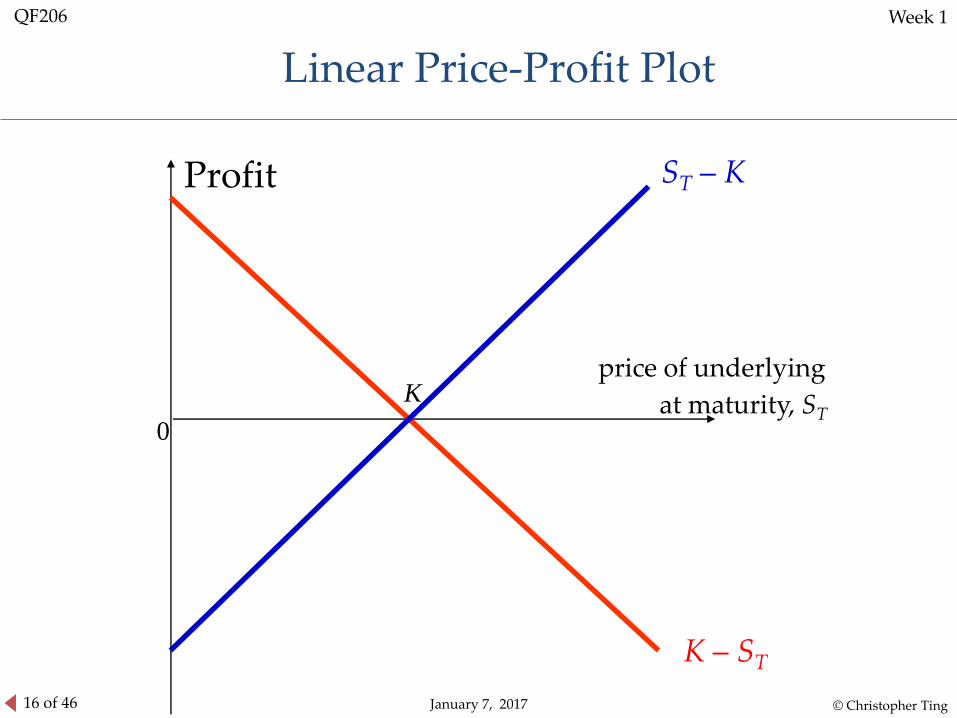

Linear Price-Profit Plot

Profit

price of underlying

at maturity, STK

0

ST – K

K – ST

© Christopher Ting

17 of 46 January 7, 2017

QF206 Week 1

© Christopher Ting

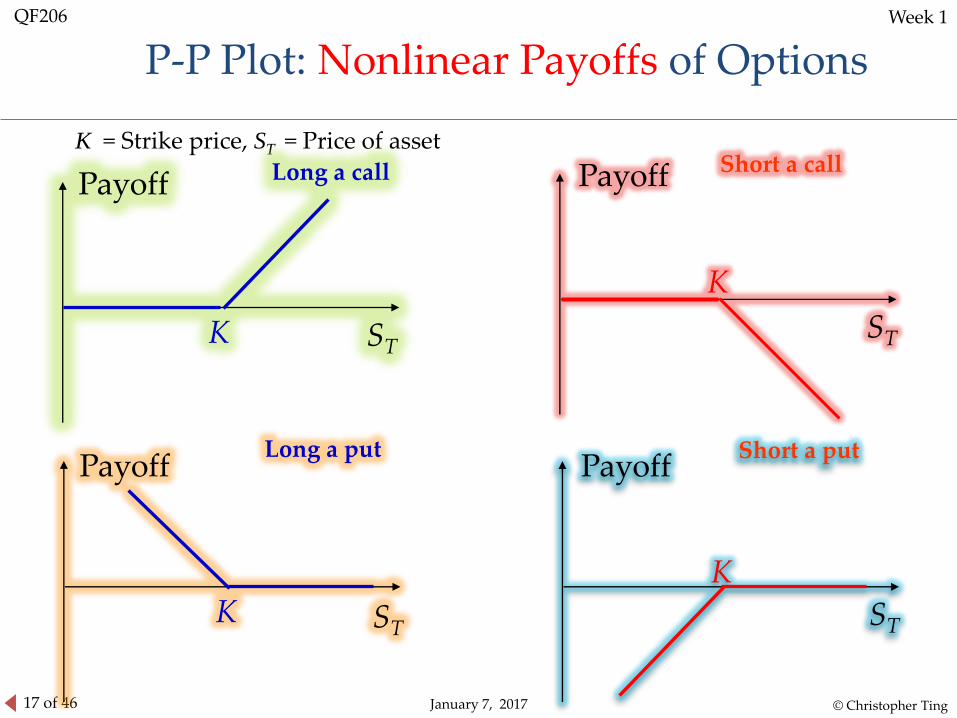

P-P Plot: Nonlinear Payoffs of Options

K = Strike price, ST = Price of asset

Payoff

STK

Long a call Payoff

ST

K

Short a call

Payoff

ST

K

Short a putPayoff

STK

Long a put

18 of 46 January 7, 2017

QF206 Week 1

© Christopher Ting

19 of 46 January 7, 2017

QF206 Week 1

© Christopher Ting

20 of 46 January 7, 2017

QF206 Week 1

© Christopher Ting

21 of 46 January 7, 2017

QF206 Week 1

© Christopher Ting

22 of 46 January 7, 2017

QF206 Week 1

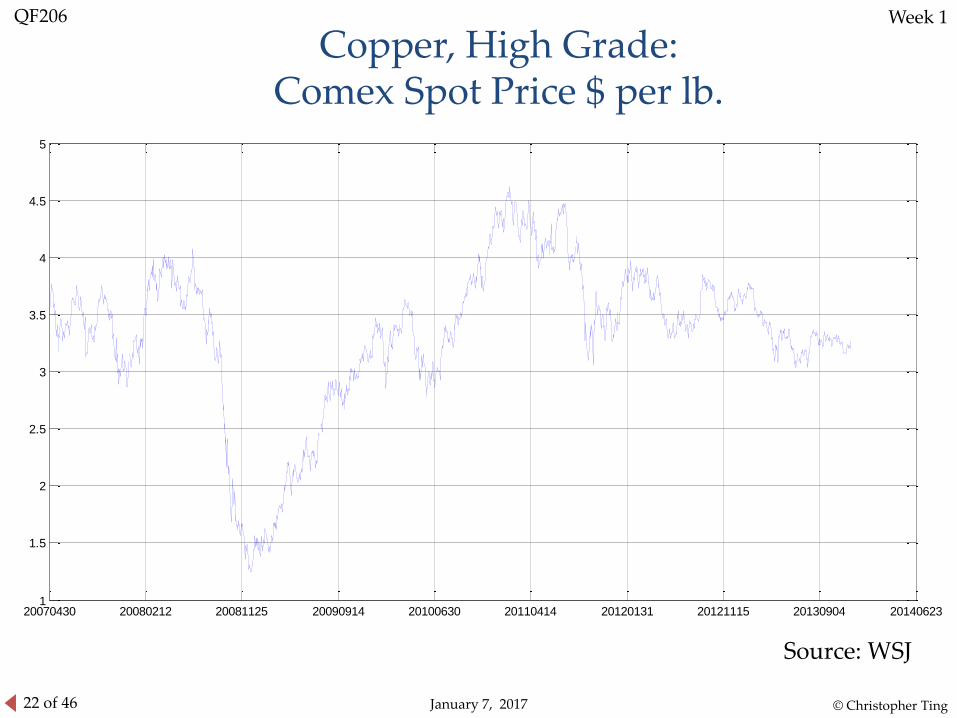

20070430 20080212 20081125 20090914 20100630 20110414 20120131 20121115 20130904 201406231

1.5

2

2.5

3

3.5

4

4.5

5

Copper, High Grade: Comex Spot Price $ per lb.

Source: WSJ

© Christopher Ting

23 of 46 January 7, 2017

QF206 Week 1

© Christopher Ting

24 of 46 January 7, 2017

QF206 Week 1

Observations

© Christopher Ting

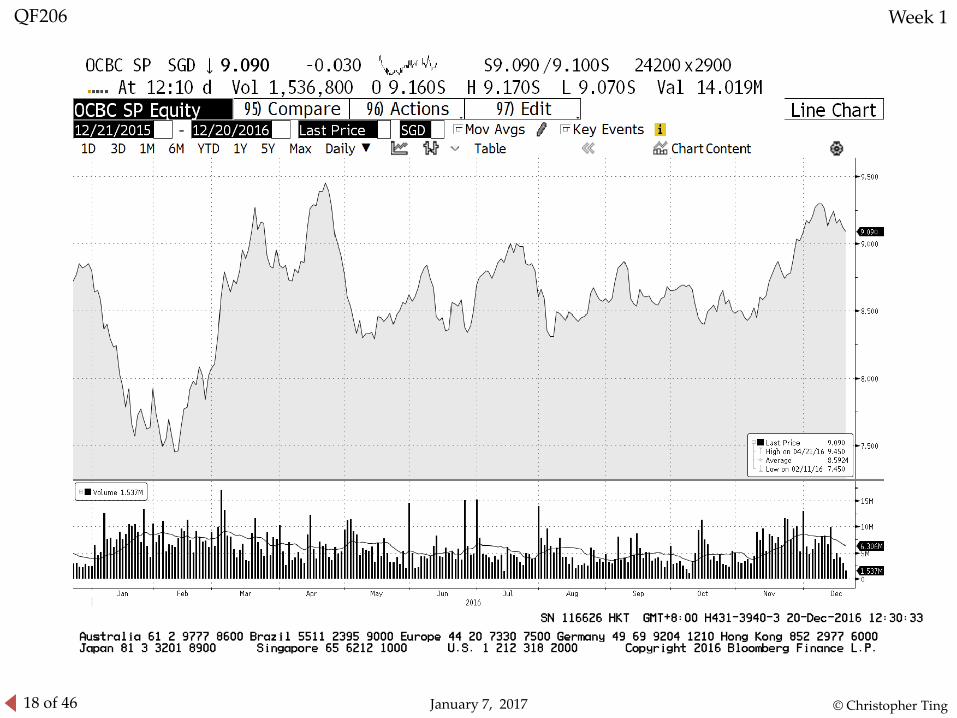

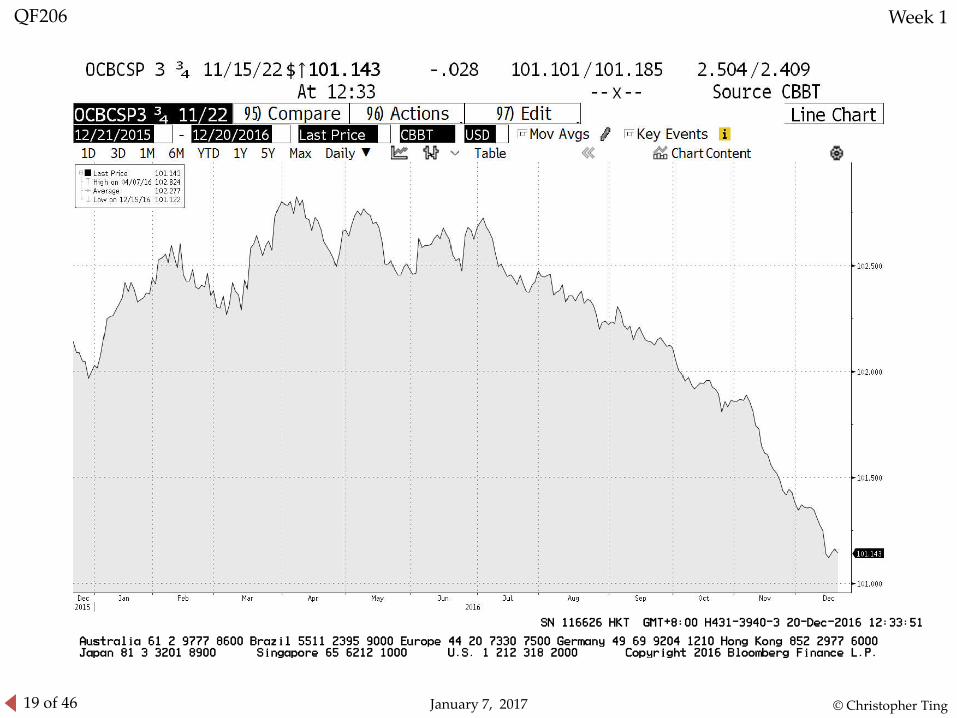

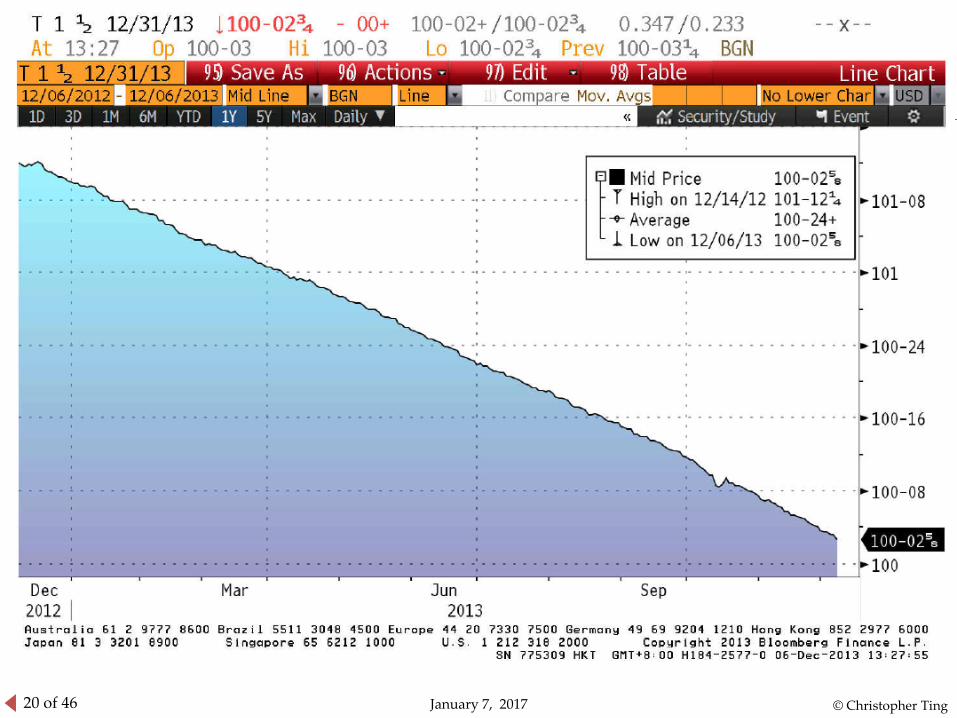

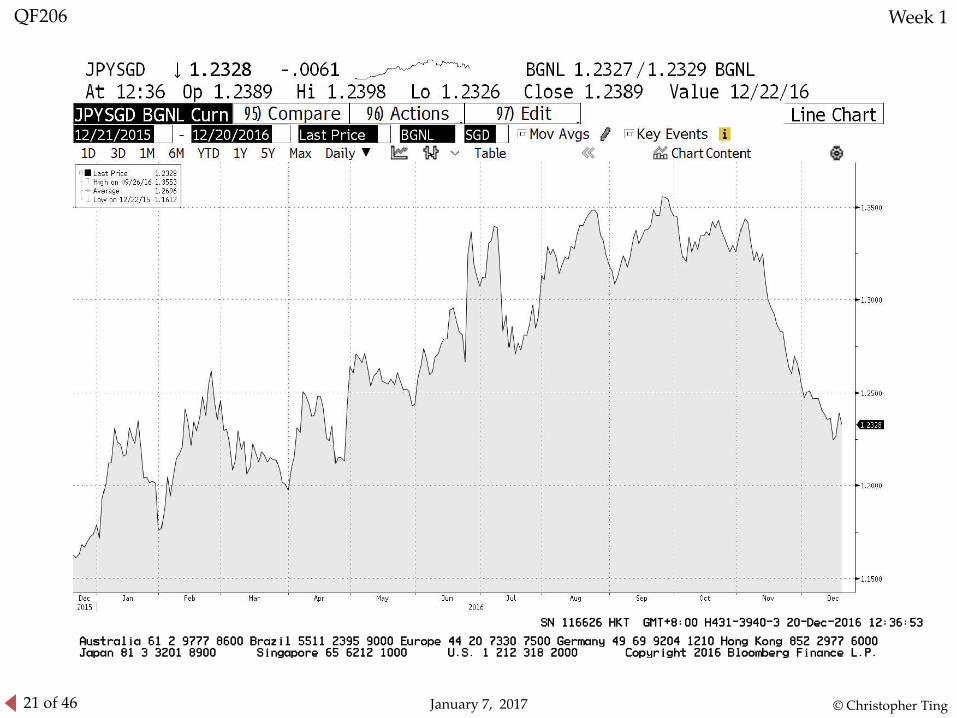

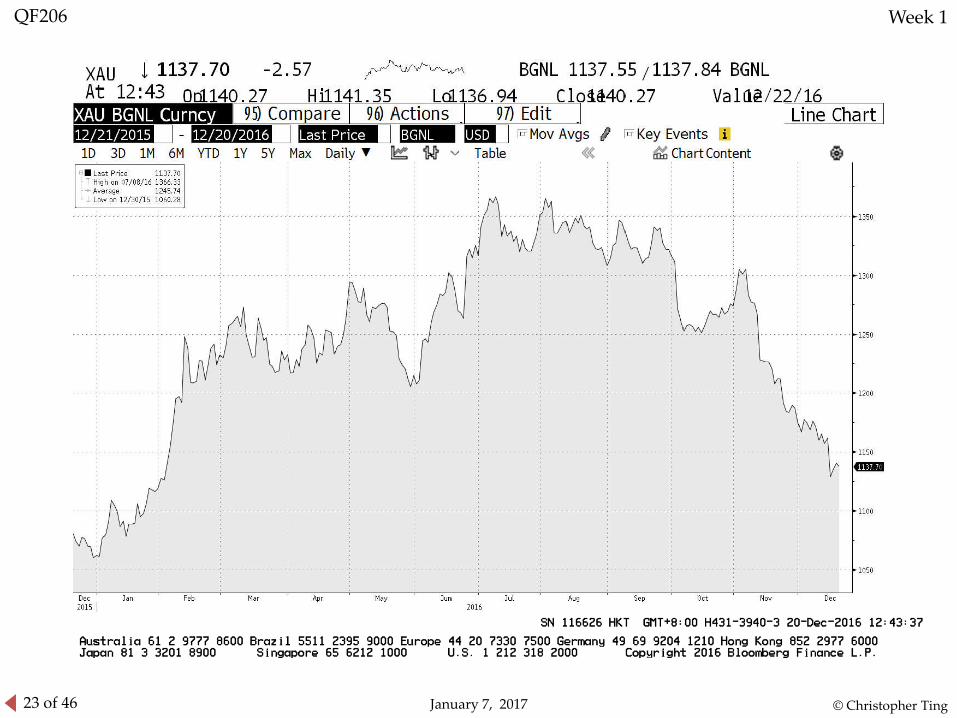

Every asset class has its own price dynamics.

In fact, at the market microstructure level,

every tradable product exhibits a different market behavior

just like no two people are 100% alike, even for “twins”

Example: Nikkei futures

So, which product to trade?

25 of 46 January 7, 2017

QF206 Week 1

Cash Market versus Derivative Market

Cash index

Singapore MSCI Index

Nikkei 225 Index

Spot rates

EUR/USD

GBP/USD

Futures contracts

SIMSCI futures contracts

Nikkei futures

Futures contracts

EUR-USD

USD-JPY

© Christopher Ting

26 of 46 January 7, 2017

QF206 Week 1

When to Trade?

Big news like non-farm payroll will cause short-term wild swing

When market opens and closes, short-term swings tend to happen

Ever heard of quadruple witching?

“Sell in May and go away,” is it true?

End-of-year tends to be more quiet.

The keywords are, Seasonality, Episodes

© Christopher Ting

27 of 46 January 7, 2017

QF206 Week 1

Where to Trade?

Regulated exchanges

Dark pools

Self-regulatory

Brokered market

Over-the-counter (OTC) market

© Christopher Ting

28 of 46 January 7, 2017

QF206 Week 1

Controversies

Controversy 1: It is a zero-sum game.

Controversy 2: Market is “efficient” in impounding information into prices.

Controversy 3: Big (HFT) player has an “unfair” advantage.

Controversy 4: MARKET is a gigantic Casino.

Money And Return Keep Everybody Trading

© Christopher Ting

29 of 46 January 7, 2017

QF206 Week 1

Why Trade?

In the face of these controversies, why trade?

To invest

To divest

To rebalance the portfolio

To conduct market timing

To encourage entrepreneurship, capital market is needed.

But have we been brainwashed by capitalism?

To hedge against price fluctuation

To manage risks

To make a living!?

Scalping

Market making

© Christopher Ting

30 of 46 January 7, 2017

QF206 Week 1

How to Trade?

This course is mainly about how to trade, and also how not to trade.

Trading strategies, plans, discipline, realistic expectations, common sense are needed

© Christopher Ting

31 of 46 January 7, 2017

QF206 Week 1

© Christopher Ting

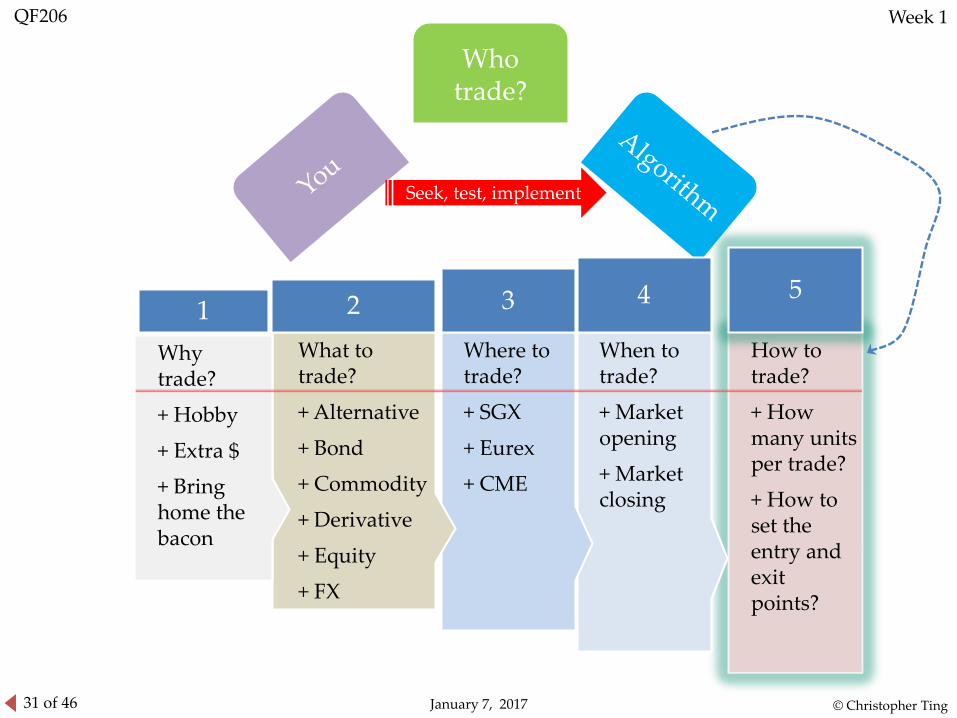

Who trade?

How to trade?

+ How many units per trade?

+ How to set the entry and exit points?

5

When to trade?

+ Market opening

+ Market closing

4

Where to trade?

+ SGX

+ Eurex

+ CME

3

What to trade?

+ Alternative

+ Bond

+ Commodity

+ Derivative

+ Equity

+ FX

2

Why trade?

+ Hobby

+ Extra $

+ Bring home the bacon

1

Seek, test, implement

32 of 46 January 7, 2017

QF206 Week 1

Trading versus Investment

© Christopher Ting

33 of 46 January 7, 2017

QF206 Week 1

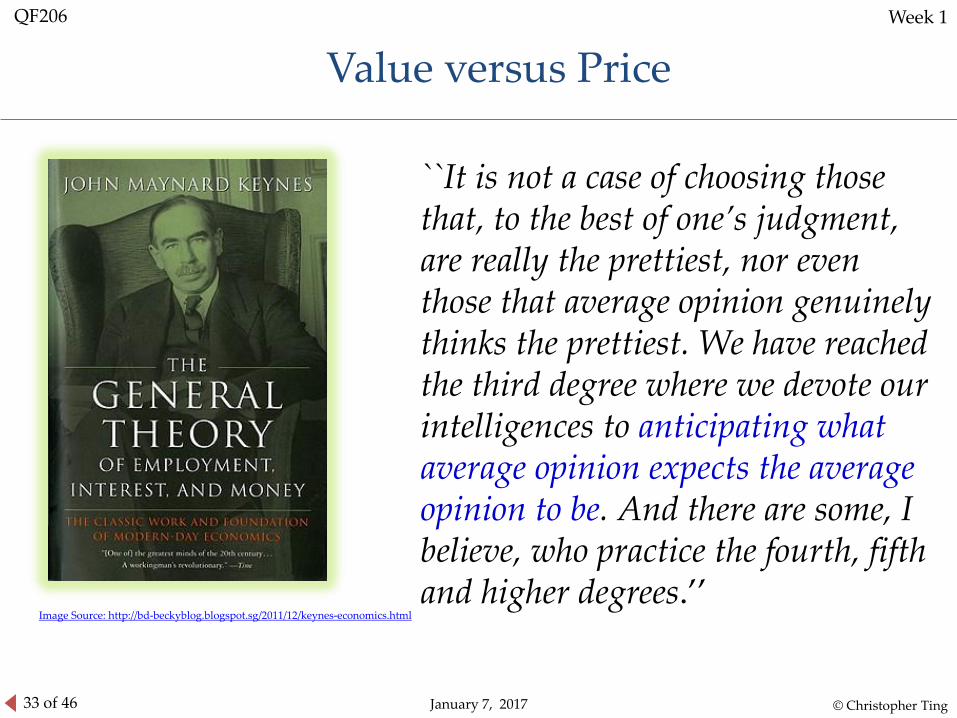

Value versus Price

``It is not a case of choosing those that, to the best of one’s judgment, are really the prettiest, nor even those that average opinion genuinely thinks the prettiest. We have reached the third degree where we devote our intelligences to anticipating what average opinion expects the average opinion to be. And there are some, I believe, who practice the fourth, fifth and higher degrees.’’

Image Source: http://bd-beckyblog.blogspot.sg/2011/12/keynes-economics.html

© Christopher Ting

34 of 46 January 7, 2017

QF206 Week 1

Experiment

Pick a number between 1 to 12 you think is the month of birth of instructor’s son.

Pick a number between 1 to 12 you think the majority will pick.

© Christopher Ting

35 of 46 January 7, 2017

QF206 Week 1

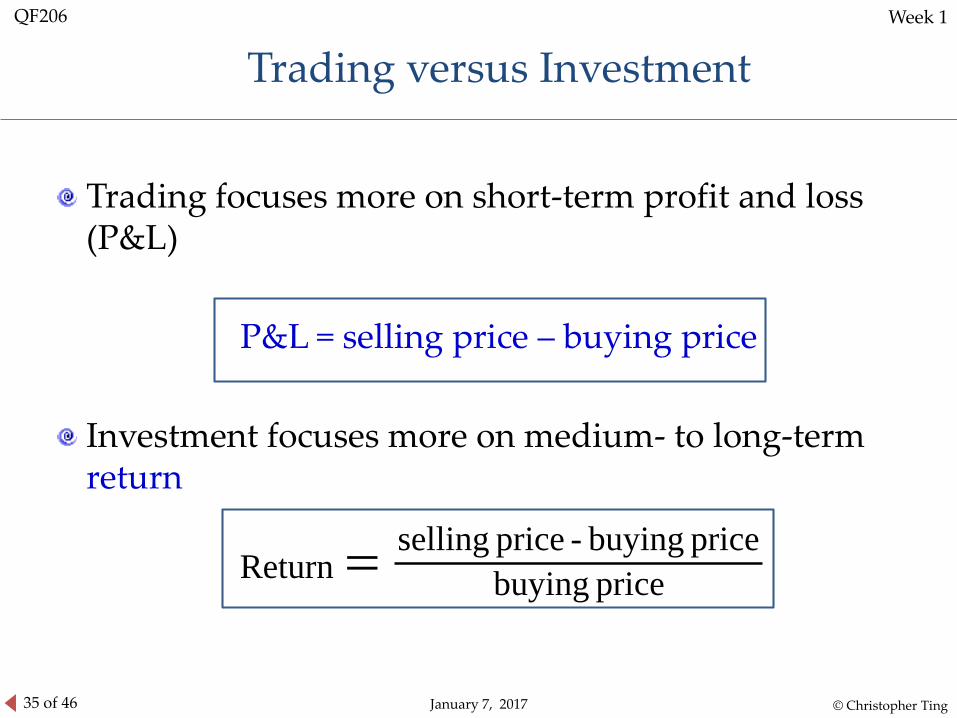

Trading focuses more on short-term profit and loss (P&L)

P&L = selling price – buying price

Investment focuses more on medium- to long-term return

Trading versus Investment

price buying

price buying - price sellingReturn

© Christopher Ting

36 of 46 January 7, 2017

QF206 Week 1

A Numerical Illustration

Suppose you sold 3 contracts of SIMSCI futures @ 366.00 and closed your position within the same day @ 365.50.

The P&L would be, per contract, 366.00 – 365.50 = 0.50 index point, which is 10 ticks.

For SIMSCI futures, each index point is S$100.

Therefore, the total profit before costs is

3 × 0.50 × S$100 = S$150.

Suppose your equity, the fund deposited at your broker, is $30,000. The return on equity (ROE) of this trade is 0.5%.

© Christopher Ting

37 of 46 January 7, 2017

QF206 Week 1

© Christopher Ting

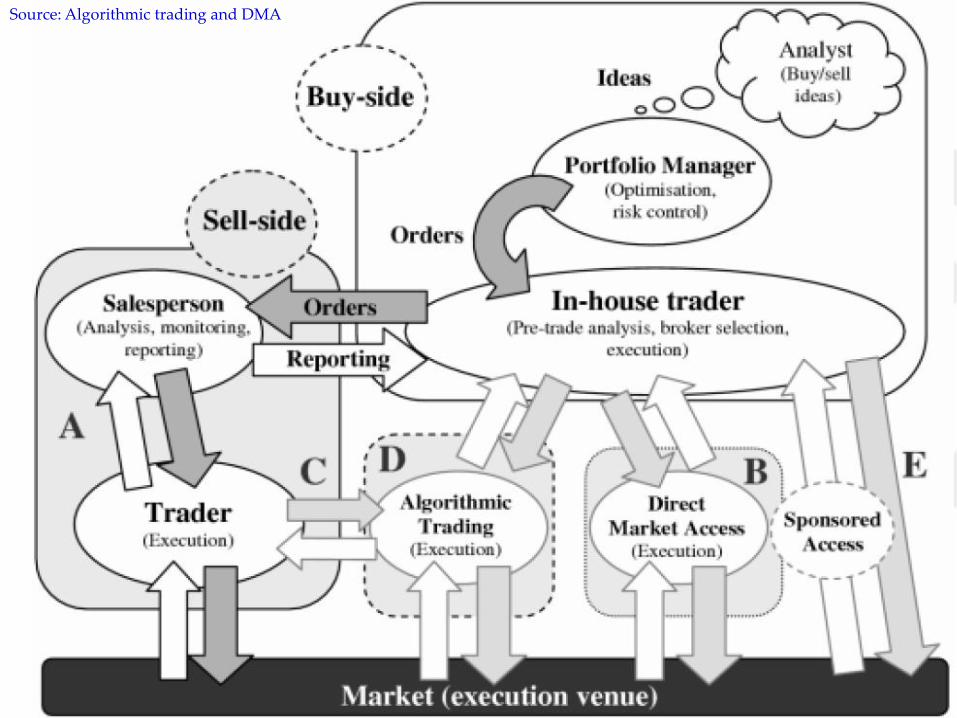

Source: Algorithmic trading and DMA

38 of 46 January 7, 2017

QF206 Week 1

Major Types of Buy-side Stock Investors

Institutional investors Mutual fund

Passive exchange trade fund (ETF)

Pension fund

Sovereign wealth fund

Hedge fund

Insurance company

Bank

Corporate nominee

Retail Start-up investor

Family business

Household/individual

© Christopher Ting

39 of 46 January 7, 2017

QF206 Week 1

© Christopher Ting

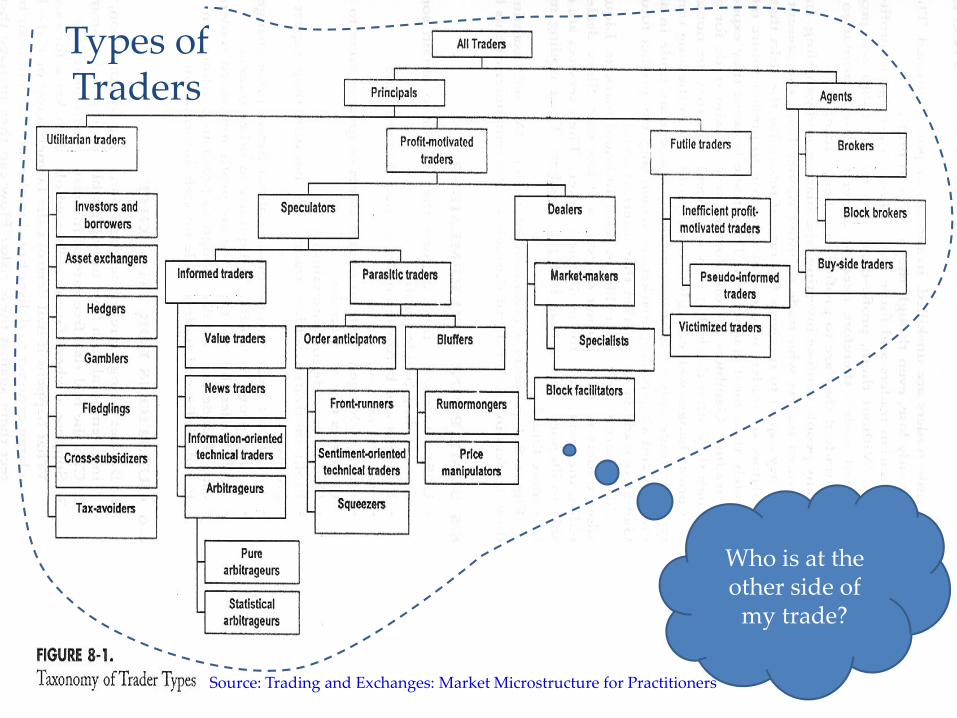

Types of Traders

Who is at the other side of

my trade?

Source: Trading and Exchanges: Market Microstructure for Practitioners

40 of 46 January 7, 2017

QF206 Week 1

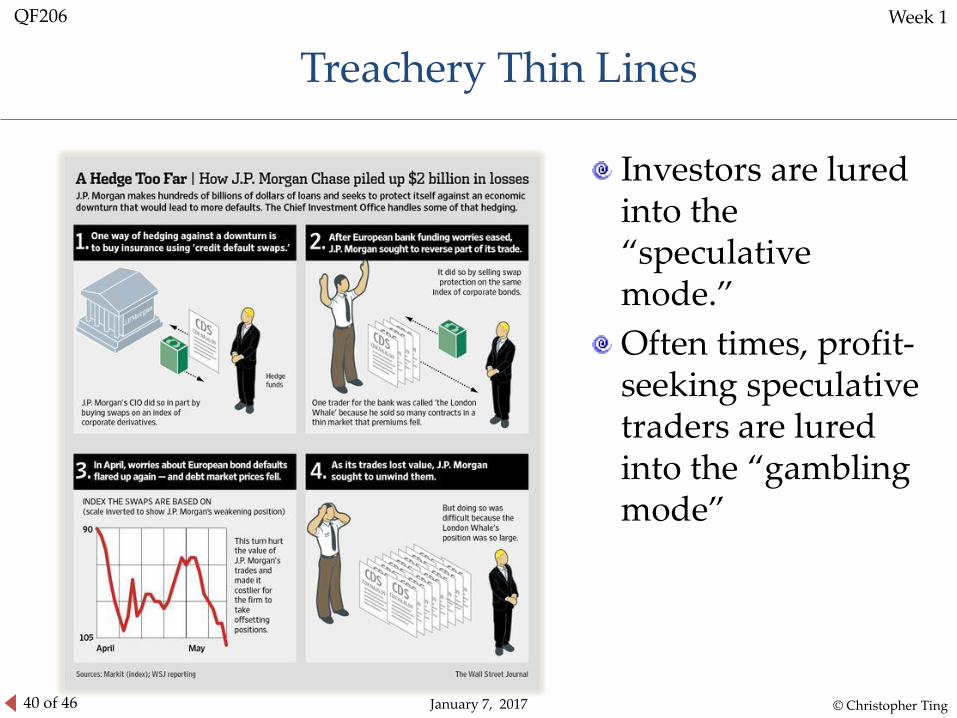

Treachery Thin Lines

Investors are lured into the “speculative mode.”

Often times, profit-seeking speculative traders are lured into the “gambling mode”

© Christopher Ting

41 of 46 January 7, 2017

QF206 Week 1

Market Making

Dealers constantly buy and sell in the market. Post quotes and stand ready to trade, and thereby provide

immediacy and liquidity to the market.

Market makers need capital to finance their inventories. The capital available to them thus limits their ability to offer liquidity.

Because market making is very risky, investors generally do not like to invest in market-making operations.

Market-making firms that have significant external financing typically have excellent risk-management systems that prevent their dealers from generating large losses.

© Christopher Ting

42 of 46 January 7, 2017

QF206 Week 1

Scalping

Dealers often are known by other names. At futures exchanges, dealers are often called scalpers, day traders, locals, or market makers. At many stock exchanges and options exchanges, they are known as designated market makers instead.

Scalpers are dealers who buy and sell for their own account. They try not to hold large positions for more than a few minutes. They are continuously acquiring and unwinding their positions.

© Christopher Ting

43 of 46 January 7, 2017

QF206 Week 1

Trading Strategy 1: Scalping

Intra-day indicators as buy/sell signal from charts

Market making

Picking up nickels in front of a steamroller

http://www.westminster-consulting.com/Files/Blog/Images/steam_roller3.png

© Christopher Ting

44 of 46 January 7, 2017

QF206 Week 1

Portfolio Rebalancing

As time goes on, a portfolio's current asset allocation will drift away from an investor's original target asset allocation. If left unadjusted, the portfolio will either become too risky, or too conservative.

The goal of rebalancing is to move the current asset allocation back in line to the originally planned asset allocation.

In portfolio rebalancing, investors need to trade large quantity, and a liquid market is beneficial.

© Christopher Ting

45 of 46 January 7, 2017

QF206 Week 1

Market Timing

The act of attempting to predict the future direction of the market, typically through the use of technical indicators or economic data.

The practice of switching among mutual fund asset classes in an attempt to profit from the changes in their market outlook. Example: Allocate more into bond market if equity risk increases

Many hedge funds and active mutual funds are trying to beat the market. But on average, their performances are dismal, as academicians would want you to think.

© Christopher Ting

46 of 46 January 7, 2017

QF206 Week 1

Takeaways

Algorithmic/Quantitative trading is about using data, machine learning (Artificial Intelligence), and automation to trade.

Seek and test algo trading strategies using the art and science of statistics to determine what, where, when, and how to trade.

Every listed tradable is unique.

Trading is not about you and other market participants. Remember Keynes’ beauty contest metaphor.

Scalpers provides liquidity.

© Christopher Ting