Embed Size (px)

Citation preview

INSIDELetterfrMarketSectorUAboutCSelected

CHILD

5/23/20CHILDSpWorldEm5/2/201CHILDSaWashing4/27/20CHILDSarecapital4/25/20CHILDSpAllianceWashing4/20/20CHILDSasaletoD3/29/12CHILDShIT/ProfeSummiti3/13/12CHILDSaExecutiv2/20/12CHILDSaLasVega1/6/12CHILDSaonthesaGlobalEm12/30/1CHILDSaGrouponTailwindCHILDSA10GlenlaSuite375Atlanta,GPhone:6Fax:800www.chil

ETHISISSUEromJimUpdateUpdatesCHILDSdTransactions

SNewsandE

012planstoattendthmploymentConfe

12attendstheHROCgton,D.C.

012advisesUtopia,InlizationwithFTV

012presentsattheTeLargeFirmForumgton,D.C.

012advisesAggressoeloitteConsulting

2hostsits3rdAnnuessionalServices&inBoston,MA

2–3/16/12attendstheStaffinveForuminLasV

2–2/24/12attendsHIMSScoas,NV

advisesFahrenhealeofitsITStaffinmploymentSolut

11advisesCumberlanitsrecapitalizatdCapital

AdvisoryPartneakeParkway5,SouthTowerGA30328678.735.3191.717.4912ldsadvisorypartne

Quarte

1231113

Events

he2012CIETTerence

Conferencein

nc.onitsCapital

echServemin

r,LLConitsgLLP

ual&Outsourcing

ngIndustryegas,NV

onferencein

eitTechnologyngBusinesstotions

andConsultingionwith

ers

ers.com

erlyBusi

Letterfrom

TheChangi

WehadourMarch 29thattended thexecutivesinvestorsin

Ourkeynotein the midspreviousdeinternetPC.and social mWorkdaycosuccessatth

Our“HotTospotsintheIT is beinghealthrecorconcept ofoffering remattractive aproviders.

The“Privatofraisingcainvestorsevminority/grmonthwithproviderof

Atourconflegal,HR,diisusuallygoIT),spurredinthemigra

Ourpassionbeacategorallofyouwgoforit!

I hope 201conference

JimChi

inessSer

mJim

ingWorldof

rthirdannualh. It was ourheSummit;50from the larnterestedinth

espeaker,Mast of anotherecade,weexp.Today,wearmedia. Lastonsultingcateheenterprise

opics”paneldeservicesunivdriven by gordsystems,caproviding ITmote infrastruas the revenu

eEquity”panapitalforyourvaluatepotenrowthequityh FTV Capital“BigData”con

ference,wealsigitalagenciesoodforservicdbyM&Aactiationtotheclo

natCHILDSisryleaderdriv

whoarerunnin

12 has startedandwehopet

ilds

rvices&

IT/Professio

lCHILDSIT/Pr first time in0%wereownger professiohespace.

lcolmFrankostep to an e

perienceda shreseeingyetamonth we soegory,toDeloilevelandreal

discussedhealversebesidestovernment inausingasignifas a utility isucture and apue base is re

elwasveryenrcompanythtialinvestmeninvestments. making a grnsulting.

sodiscussedtsandmanagemesfirms.Wheivity(asinfinoud),best‐in‐c

stoadvisecatesfocus,intenngcompaniest

d off great fotoseeyounex

&Techno

onalServices

ProfessionalSn Boston andners/executiveonal services/

ofCognizant,pentirely newhift in technoanothershifttold a companyitte.Thisdeallyservesasa

lthcareITandtheSaaSconsncentives (andficantuptickis finally cominpplication hosecurring and

ntertaining,wroughtheprivnts.ThepaneEchoing thisrowth equity

thefavorablementconsultietherthatchanancialserviceclassfirmsare

tegory‐leadingnsityandultimtoclearlydefi

or you. Thanxtyear!

ologyUp

ervices&Outthe turnout wesofmid‐mar/BPO firms a

presentedave“S curve” inlogyplatformtoanewplatfy called Aggralconfirmstheapreviewofw

dmanagedsersultingmarketd eventually pindemandforng to lifewitsting and supthere is a r

withthepanelivateequitymelalsodiscusss trend,weclinvestment in

economictrengsegments.angeisregulates)orsimplyefindingways

gservicesandmatelyleadstoineyourcateg

nks again for

date

tsourcingSumwas great. Arket servicesand 20% wer

erycompellingtechnology p

ms from thenformfocusedoressor, the leaepotentialofwhatistocome

rvicesassomtmentionedapenalties) torconsultinginhmanaged sepport. Theserelatively high

istsdebatingtmarketsandhosedthegrowinosedasecondnto Utopia, a

endsinthefinThebottomltoryinnatureanevolutionstogrowwith

dtechnologyfohighvalue.Igory(nomatte

all of you w

mmitinBostonAbout 150 peofirms,30%wre private eq

gcasethatweplatforms. InetworkPC tooncloud,mobading firm intheSaaSmode.

meofthebrighabove.Healthcinstall electronthissector.ervices providmodels are vh cost to sw

theprosandcowprivateeqngtrendtowad transactioncategory‐lead

nance/accountineisthatchae(asinhealthcoftechnologyhthechange.

firms.AspirinIwouldchalleerhowsmall)

who attended

1Q20

nonoplewereuity

earethetheilitythedel’s

htestcareonicThedersverywitch

consuityardslastding

ting,angecarey(as

ngtoengeand

our

012

Page|2

CHILDSCHILDS

Note:TheOutsourc

Busine1Q201Techno

Source:C

60

65

70

75

80

85

90

95

100

105

110

May

SAdvisoryPaSBusinessSer

eCHILDSBusinesscing(BPO),Huma

B

ssServices&12comparedtologyisprovin

CHILDSdatabasea

y‐11 Jun‐11

Businrtners(“CHILrvices&Techn

sServices&TechnnCapitalManage

BusinessSe

TechnologyMto520transacngtobehealth

andCapitalIQ

1 Jul‐11

CHILDS

nessServDS”)tracksalnologyIndexs

nologyIndexismaement(HCM),Mar

ervices&Te

M&Avolumewctionsnotedinhyandhaspos

Aug‐11 Sep

SQuarte

vices&Tlistofpubliclyslightlyunder

adeupofselectpurketing&Informa

echnology

wasupin1Qvn4Q2011andsitivemoment

p‐11 Oct‐11

S&P50

erlyUpda

Technolytradedcomprperformedth

ubliccompaniesinationServicesand

M&ADeals

s.4Qandyeard581in1Q20tum.

1 Nov‐11

00 CHILD

ate:1Q2

ogyMarpaniesinourcheS&P500Ind

nthefollowingsedFacilitiesService

sbyQuarte

r‐over‐year.W011.TheM&A

Dec‐11 Jan

DSIndex

2012

rketUpdcoresectors.Idexbutisbegi

ectors:IT/Professies.Indexdataasof

er(2004–

We’venotedaAmarketforB

n‐12 Feb‐12

dateInthefirstquainningtoreco

ionalServicesandofMay15,2012.

1Q2012)

atotalof609tBusinessServi

2 Mar‐12

arterof2012,over.

dBusinessProcess

transactionsinces&

Apr‐12 May

the

s

n

y‐12

Page|3

CHILDSQuarterlyUpdate:1Q2012

SectorUpdate:IT/ProfessionalServicesandBPO

IT/ProfessionalServicesComparablePublicCompanyAnalysis

PublicCompanyStockPerformanceIn the last ninemonths, themajorityof theIT/Professional services indices generallyunderperformed the S&P. The twoexceptions are the mid‐market consultingservices segmentand themanagedservicessegment, which are outperforming themarket.

Mid‐MarketConsulting FederalITServices

TheaverageLTMEBITDAmultipleis8.8x,whichislowerthanlastquarter’smultipleof9.5x.

TheaverageLTMEBITDAmultipleis5.5xthisquarter,lowerthanlastquarter’smultipleof6.2x.

ManagedServices VARs/SystemIntegrators

The average LTM EBITDA multiple has decreased to 13.3xfrom13.6xinthefourthquarterof2011.

The average LTM EBITDA multiple is 5.9x, unchanged fromlastquarter.

*Excludedfromaveragecalculations.LTM=LastTwelveMonths.DataobtainedfromCapitalIQ.StockpricesasofMay15,2012

40

50

60

70

80

90

100

110

120

May‐11 Jun‐11 Jul‐11 Aug‐11 Sep‐11 Oct‐11 Nov‐11 Dec‐11 Jan‐12 Feb‐12 Mar‐12 Apr‐12 May‐12

Mid‐MarketConsultingServices FederalITServices ManagedServices VARs/SystemIntegrators S&P500Index

CompanyName StockPrice%of52WkHigh

LTMRevenue

LTMEBITDA

AdvisoryBoardCo. $94.14 95.7% 4.1x * 26.7x *

CIBER,Inc. $3.87 60.9% 0.3x 14.5x

CRAInternationalInc. $20.01 67.1% 0.5x 5.1x

EdgewaterTechnologyInc. $3.86 86.2% 0.4x 4.5x

ExponentInc. $47.42 89.0% 2.1x 9.3x

FTIConsulting,Inc. $31.34 69.6% 1.2x 7.2x

HuronConsultingGroupInc. $32.48 79.5% 1.5x 8.7x

MattersightCorporation $7.85 82.6% 3.8x * NM

NavigantConsultingInc. $12.84 87.8% 1.2x 8.1x

PerficientInc. $12.39 95.7% 1.5x 12.4x

ResourcesConnectionInc. $12.27 84.7% 0.7x 9.2x

SapientCorp. $10.57 65.0% 1.2x 9.9x

TheHackettGroup,Inc. $5.53 84.0% 1.0x 9.6x

TowersWatson&Co. $65.08 95.5% 1.2x 6.8x

Average 81.7% 1.1x 8.8x

EnterpriseValue/

CompanyName StockPrice%of52Wk

HighLTM

RevenueLTM

EBITDA

CACIInternationalInc. $45.95 69.1% 0.5x 4.9x

DynamicsResearchCorp. $6.24 39.3% 0.5x 4.6x

ICFInternationalInc. $22.80 78.0% 0.7x 7.3x

ManTechInternationalCorporation $23.38 50.5% 0.3x 3.3x

NCI,Inc. $4.30 17.7% 0.2x 3.8x

SAIC,Inc. $11.00 62.5% 0.4x 9.1x

OfficialPaymentsHoldings,Inc. $4.71 83.7% 0.3x NM

TylerTechnologies,Inc. $37.06 89.1% 3.6x * 20.2x *

Average 61.2% 0.4x 5.5x

EnterpriseValue/

CompanyName StockPrice%of52WkHigh

LTMRevenue

LTMEBITDA

CenturyLink,Inc. $38.63 88.8% 2.5x 6.0x

Equinix,Inc. $163.06 94.6% 5.9x 14.2x

InternapNetworkServicesCorp. $7.21 87.4% 1.8x 10.5x

LimelightNetworks,Inc. $2.64 44.7% 0.8x 116.0x *

RackspaceHosting,Inc. $52.91 87.4% 6.5x 22.4x

Average 80.6% 3.5x 13.3x

EnterpriseValue/

CompanyName StockPrice%of52Wk

HighLTM

RevenueLTM

EBITDA

AtosS.A. $57.11 91.2% 0.7x 6.5x

BlackBoxCorp. $22.07 66.3% 0.5x 5.6x

CapGeminiS.A. $35.94 68.5% 0.4x 4.6x

DatalinkCorp. $10.77 93.7% 0.4x 8.0x

ePlusInc. $30.42 89.0% 0.3x 5.3x

LogicaPLC $1.06 46.1% 0.4x 5.2x

Average 75.8% 0.4x 5.9x

EnterpriseValue/

Page|4

CHILDSQuarterlyUpdate:1Q2012

BPOComparablePublicCompanyAnalysis

PublicCompanyStockPerformanceIn the lastninemonths, theMajorBPOandMid‐Market BPO segments have generallyunderperformed the S&P 500, but havebeguntoshowsomeimprovementinrecentweeks.

MajorBPO Mid‐MarketBPO

TheaverageLTMEBITDAmultipleis9.4xthisquarter,downfromlastquarter’smultipleof10.0x.

The average LTM EBITDA multiple is 8.6x this quarter, adecreasefromlastquarter’smultipleof10.0x.

Teleservices

TheaverageLTMEBITDAmultiplehasdecreasedto4.0xfrom4.3xinthefourthquarterof2011.

*Excludedfromaveragecalculations.LTM=LastTwelveMonths.DataobtainedfromCapitalIQ.StockpricesasofMay15,2012

40

50

60

70

80

90

100

110

120

May‐11 Jun‐11 Jul‐11 Aug‐11 Sep‐11 Oct‐11 Nov‐11 Dec‐11 Jan‐12 Feb‐12 Mar‐12 Apr‐12 May‐12

MajorBPO Mid‐MarketBPO Teleservices S&P500Index

CompanyName StockPrice%of52WkHigh

LTMRevenue

LTMEBITDA

Accentureplc $58.93 89.4% 1.2x 7.5x

CGIGroup,Inc. $20.74 85.8% 1.5x 8.1x

CognizantTechnologySolutionsCo $61.20 78.5% 2.5x 12.2x

ComputerSciencesCorporation $26.37 58.7% 0.4x 17.7x

ConvergysCorporation $13.30 93.5% 0.5x 2.3x

EPIQSystems,Inc. $11.12 72.7% 2.3x 9.5x

GenpactLtd. $16.46 90.6% 2.1x 11.7x

InfosysLtd. $44.82 79.8% 3.3x 10.4x

IronMountainInc. $30.20 84.4% 2.8x 9.1x

ITCLtd. $4.29 91.3% 7.9x * 23.7x *

PitneyBowesInc. $13.45 54.1% 1.2x 6.0x

TataConsultancyServicesLimited $22.79 94.7% 4.8x 16.2x

UnisysCorporation $18.03 63.5% 0.2x 1.7x

WiproLtd. $7.52 89.3% 2.5x 12.9x

XeroxCorp. $7.40 68.3% 0.8x 5.6x

Average 79.6% 1.9x 9.4x

EnterpriseValue/

CompanyName StockPrice%of52Wk

HighLTM

RevenueLTM

EBITDA

AdityaBirlaNuvoLimited $15.01 78.5% 0.9x 3.7x

HCLTechnologiesLtd. $9.09 93.4% 1.7x 10.8x

HexawareTechnologiesLimited $2.23 89.6% 2.0x 9.7x

iGATECorporation $17.92 89.7% 2.0x 9.4x

MphasisLimited $7.33 80.7% 1.2x 6.6x

PatniComputerSystemsLimited $9.62 99.3% 1.4x 8.8x

SatyamComputerServicesLimited $1.28 73.4% 1.0x 6.2x

Syntel,Inc. $58.56 92.2% 3.2x * 10.7x

TechMahindraLimited $11.85 79.9% 1.7x 7.7x

VanceInfoTechnologiesInc. $10.49 37.2% 1.1x 12.6x

Average 81.4% 1.4x 8.6x

EnterpriseValue/

CompanyName StockPrice%of52WkHigh

LTMRevenue

LTMEBITDA

ConvergysCorporation $13.30 93.5% 0.5x 2.3x

StarTek,Inc. $2.63 49.7% 0.1x NM

SykesEnterprises,Incorporated $16.24 71.6% 0.5x 4.3x

TeleTechHoldingsInc. $14.87 66.4% 0.6x 5.3x

Average 70.3% 0.4x 4.0x

EnterpriseValue/

Page|5

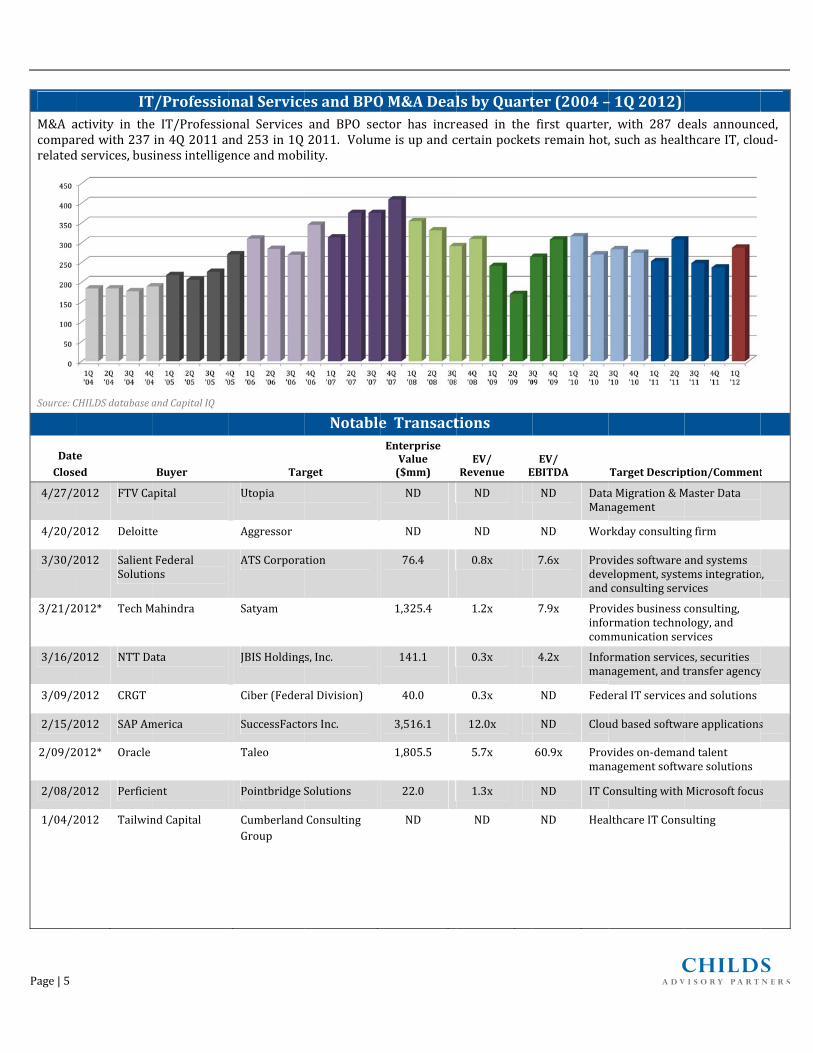

M&A acomparrelated

Source:C

DatClose

4/27/2

4/20/2

3/30/2

3/21/2

3/16/2

3/09/2

2/15/2

2/09/2

2/08/2

1/04/2

*Annou

ITactivity in theredwith237dservices,bus

CHILDSdatabasea

teed

2012 FTVCa

2012 Deloitt

2012 SalientSolutio

012* TechM

2012 NTTDa

2012 CRGT

2012 SAPAm

012* Oracle

2012 Perficie

2012 Tailwin

uncedDate

T/Professioe IT/Professioin4Q2011ainessintellige

andCapitalIQ

Buyer

apital

te

tFederalons

Mahindra

ata

merica

ent

ndCapital

CHILDS

onalServiceonal Servicesnd253in1Qenceandmobi

Tar

Utopia

Aggressor

ATSCorpora

Satyam

JBISHolding

Ciber(Feder

SuccessFacto

Taleo

Pointbridge

CumberlandGroup

SQuarte

esandBPOand BPO sec2011.Volumility.

Notable

rget

ation

s,Inc.

ralDivision)

orsInc.

Solutions

Consulting

erlyUpda

OM&ADealctor has incremeisupandc

eTransactEnterpriseValue($mm)

ND

ND

76.4

1,325.4

141.1

40.0

3,516.1

1,805.5

22.0

ND

ate:1Q2

lsbyQuarteased in thecertainpocket

tions

EV/Revenue E

ND

ND

0.8x

1.2x

0.3x

0.3x

12.0x

5.7x

1.3x

ND

2012

ter(2004–first quartertsremainhot,

EV/EBITDA

ND DataMan

ND Wor

7.6x Provdeveand

7.9x Provinfocom

4.2x Infoman

ND Fede

ND Clou

60.9x Provman

ND ITC

ND Hea

–1Q2012)r, with 287 d,suchasheal

TargetDescrip

aMigration&Mnagement

rkdayconsultin

videssoftwareelopment,systeconsultingserv

videsbusinesscrmationtechno

mmunicationser

ormationservicenagement,andt

eralITservices

udbasedsoftwa

videson‐demannagementsoftw

Consultingwith

althcareITCons

eals announcthcareIT,clou

ption/Comment

MasterData

ngfirm

andsystemsemsintegrationvices

consulting,ology,andrvices

es,securitiestransferagency

sandsolutions

areapplications

ndtalentwaresolutions

Microsoftfocus

sulting

ced,ud‐

t

n,

y

s

s

Page|6

Merge

CHILDSIT/Prodeals. OnAssa9.2xvTheHetransacthe “otHROan

M&Aacquarter

Source:C

DateClose

3/26/2

3/20/2

3/19/2

3/9/20

2/1/20

1/3/20

rsandAcqui

S recordedfessional ServThemost sigignmenttoacvaluationmul

ealthcaresegmctionoccurrinther” categoryndPEO/RPO.

ctivityremainrwithtwelve

CHILDSdatabasea

eed2012 CEPInc

2012 OnAssi

2012 inVenti

012 CRGTIn

012 CTPartn

012 Adecco

SectorsitionsbySeg

27 HCM trvices segmengnificant transcquireApexSytiple.

ment isstill slng inQ1. Theywhich includ

nedflatat27t(or55.6%)of

andCapitalIQ

Buyerc.

ignment

vHealth

nc.

ners

CHILDS

Update:gment

ransactionsnt being the msactionwas thystems,a$60

low in termsere remains sdes search, te

HCMM&

transactionsinftheM&Adea

TargFortuneIndu

ApexSystem

KforceClinicResearchDiv

CIBER,Inc.,FDivision

J‐M.BeigbedSearch

VSNInc.

SQuarte

:Human

in 1Q 2012most active wheannouncem0.0millionde

ofM&A,withsignificant inteechnical/engin

&ADealsby

n1Q.Internatalsinvolvingin

Notabl

get

E

ustriesInc.

ms

calvision

Federal

er‐CEO

erlyUpda

nCapital

2 withwith 11mentbyealwith

honly2erest inneering,

yQuarter(2

tionalcompannternationalta

eTransactEnterpriseValue($mm) R20.5

600.0

50.0

40.0

44.3

117.6

ate:1Q2

Manage

1Q201

2004–1Q

nieswereextrargetsandnea

tions

EV/Revenue

EEB

0.3x N

0.9x 9

0.5x N

0.3x N

ND N

ND N

2012

ement(H

12StaffingM&A

2012)

remelyactiveiarly50.0%inv

EV/ITDA TaND PEOof

outsou

9.2x Informservice

ND Clinicaresour

ND ITstafgovern

ND Leaderservice

ND ProvidJapan

HCM)

ADealVolume

intheM&Amvolvingintern

argetDescriptfferinghumanrurcingservices

mationTechnoloes

altrialtemporarcesolutions

ffingsolutionstnment

rshiprecruitmees

derofHumanRe

bySegment

arketthisnationalbuyer

tion/Commentresources

ogystaffing

ryandpermane

tofederal

entandconsulti

esourceservice

rs.

t

ent

ing

esin

Page|7

CHILDSQuarterlyUpdate:1Q2012

HCMComparablePublicCompanyAnalysis

PublicCompanyStockPerformanceOf the HCM segments we track,commercial/multi‐line and healthcare haveconsistentlyperformedtheweakest.IT/professionalstaffingunderperformedtheS&P500formostof2011buthassincerecoveredsignificantly.Over the past year, HRO has significantlytradedinlinewiththeS&P.

Commercial&Multi‐LineStaffing IT&ProfessionalStaffing

The average LTM EBITDA multiple this quarter has stayedconstantat6.7x.

TheaverageLTMEBITDAmultiple is9.8xthisquarterwhichisupfrom9.2xinthefourthquarterof2011.

ExecutiveSearch HealthcareStaffing

The average LTM EBITDA multiple decreased to 4.2x thisquarter,from5.8xinthefourthquarterof2011.

TheaverageLTMEBITDAmultiplehasdecreasedto8.2xfrom9.7xinthefourthquarter.

HROutsourcing HRTechnology

TheaverageLTMEBITDAmultipleis10.1xthisquarterwhichisupfrom8.8xinthefourthquarterof2011.

TheaverageLTMEBITDAmultipleis32.6xthisquarter,downfrom35.9xlastquarter.

*Excludedfromaveragecalculations.LTM=LastTwelveMonths.DataobtainedfromCapitalIQ.StockpriceasofMay15,2012

0

20

40

60

80

100

120

140

May‐11 Jun‐11 Jul‐11 Aug‐11 Sep‐11 Oct‐11 Nov‐11 Dec‐11 Jan‐12 Feb‐12 Mar‐12 Apr‐12 May‐12

C/ML IT/Prof Search HC HRO HRTech S&P500Index

CompanyName StockPrice%of52Wk

HighLTM

RevenueLTM

EBITDAAdeccoS.A. $40.95 64.3% 0.3x 7.3xKellyServices,Inc. $13.26 68.7% 0.1x 5.1xManpowerGroup $37.61 58.8% 0.1x 4.8xRandstadHoldingNV $29.40 63.4% 0.3x 8.5xTrueBlue,Inc. $16.32 89.6% 0.4x 7.7x

Average 68.9% 0.3x 6.7x

EnterpriseValue/CompanyName StockPrice

%of52WkHigh

LTMRevenue

LTMEBITDA

AnalystsInternationalCorp. $3.80 52.1% 0.2x 3.7xCDICorp. $17.96 96.5% 0.3x 7.8xComputerTaskGroupInc. $13.00 83.7% 0.6x 10.3xKforceInc. $13.84 89.9% 0.4x 23.0xMastechHoldings,Inc. $5.80 92.7% 0.2x 5.2xOnAssignmentInc. $16.23 83.8% 1.1x 11.3xRCMTechnologiesInc. $5.79 98.5% 0.3x 5.4xRobertHalfInternationalInc. $28.98 89.7% 1.0x 11.6xAverage 85.8% 0.5x 9.8x

EnterpriseValue/

CompanyName StockPrice%of52Wk

HighLTM

RevenueLTM

EBITDACTPartners $6.28 45.2% 0.4x NMHeidrick&StrugglesInternationalInc. $17.73 64.3% 0.5x 4.8xKorn/FerryInternational $13.97 58.3% 0.5x 3.7xAverage 55.9% 0.4x 4.2x

EnterpriseValue/

CompanyName StockPrice%of52Wk

HighLTM

RevenueLTM

EBITDAAMNHealthcareServicesInc. $6.52 74.5% 0.5x 8.5xCrossCountryHealthcare,Inc. $4.04 50.5% 0.3x 7.9xTeamStaff,Inc. $1.33 40.7% 0.2x NMAverage 55.2% 0.4x 8.2x

EnterpriseValue/

CompanyName StockPrice%of52Wk

HighLTM

RevenueLTM

EBITDAAutomaticDataProcessing,Inc. $53.11 93.0% 2.3x 10.3xBarrettBusinessServicesInc. $20.51 96.5% 0.4x 23.5xCapitaPLC $10.34 83.3% 2.0x 10.9xInsperity,Inc. $26.08 80.8% 0.2x 4.8xPaychex,Inc. $30.06 91.8% 4.7x 11.1xTowersWatson&Co. $65.08 95.5% 1.2x 6.8xXchangingPLC $1.70 92.0% 0.4x 3.4xAverage 90.4% 1.6x 10.1x

EnterpriseValue/

CompanyName StockPrice%of52Wk

HighLTM

RevenueLTM

EBITDA51jobInc. $49.26 70.6% 5.3x 14.7xConcurTechnologies,Inc. $62.17 95.0% 8.1x 61.8xDiceHoldings,Inc. $10.38 67.5% 3.3x 8.2xMonsterWorldwide,Inc. $8.69 56.3% 1.0x 7.0xSabaSoftware,Inc. $8.77 66.9% 2.0x NMTheUltimateSoftwareGroup,Inc. $76.93 92.7% 7.0x 71.3xAverage 74.8% 4.5x 32.6x

EnterpriseValue/

Page|8

Wenotthefirs

Source:C

DatClos

3/16/2

3/12/2

2/28/2

2/28/2

Ma

tedatotalof1stquarterofla

CHILDSdatabasea

teed

2012 PlayPh

2012 Ebiqui

2012 St.Ive

2012 PeppeGroup

Sector

arketing&

131transactioastyear.

andCapitalIQ

Buyer

hone,Inc.

ityplc

s

rs&Rogers

CHILDS

Update

&Informatio

onsinthefirs

Ta

SocialHou

FLEHoldin

InciteMarPlanningL

Iknowtion

SQuarte

–Marke

onServices

stquarterof2

Notabl

arget

ur

ngs

rketingLimited

n

erlyUpda

eting&I

sM&ADea

2012,compare

eTransactEnterpriseValue($mm)

51.5

7.8

14.6

5.8

ate:1Q2

nformat

lsbyQuart

edto97trans

tions

EV/Revenue

ND

1.3

2.2x

ND

2012

tionServ

ter(2004–

sactionsin4Q

EV/EBITDA

ND Ps

ND Pip

10.3x Pc

ND Pms

vices

–1Q2012)

Q2011and12

TargetDescri

Providesmobileservices

Providesmediancludingsummperformanceda

Providesmarkeconsultingservi

Providesinformmarketingandaservices

20transaction

iption/Comme

esocialmarketi

auditservices,marizingata

etresearchandices

mation‐basedanalyticconsult

nsin

ent

ing

ting

Page|9

CHILDSQuarterlyUpdate:1Q2012

MarketingandInformationServicesComparablePublicCompanyAnalysis

PublicCompanyStockPerformancePrint/fulfillmentcontinuestounderperformcompared to other segments of the sectorand the S&P. Information services is theonly segment currently outperforming theS&P.

Marketing&Analytics InformationServices

TheaverageLTMEBITDAmultipleisdownfrom7.0xlastquarterto6.5xthisquarter.

TheaverageLTMEBITDAmultipleis8.7xthisquarter,whichisdownfrom9.3xinthefourthquarterof2011.

Print/Fulfillment HealthcareStaffingTheaverageLTMEBITDAmultipledecreasedto6.6x,whichisdownfrom7.8xinthefourthquarterof2011.

LTM=LastTwelveMonths.DataobtainedfromCapitalIQ.StockpriceasofMay15,2012

50

60

70

80

90

100

110

120

May‐11 Jun‐11 Jul‐11 Aug‐11 Sep‐11 Oct‐11 Nov‐11 Dec‐11 Jan‐12 Feb‐12 Mar‐12 Apr‐12 May‐12

Marketing&Analytics InformationServices Print/Fulfillment S&P500Index

CompanyName StockPrice%of52WkHigh

LTMRevenue

LTMEBITDA

AcxiomCorporation $13.46 90.2% 1.0x 4.6x

Harte‐HanksInc. $8.56 83.6% 0.7x 6.7x

Havas $5.18 90.4% 1.1x 7.2x

TheInterpublicGroupofCompanies,Inc. $11.28 87.4% 0.8x 6.5x

MDCHoldingsInc. $28.40 93.4% 1.6x NM

OmnicomGroupInc. $50.45 96.7% 1.2x 7.6x

PublicisGroupeSA $47.95 86.8% 1.1x 6.3x

Average 89.8% 1.1x 6.5x

EnterpriseValue/

CompanyName StockPrice%of52WkHigh

LTMRevenue

LTMEBITDA

AllianceDataSystemsCorporation $126.27 96.6% 3.8x 12.9x

DigitalRiverInc. $15.21 44.5% 0.5x 3.7x

Dun&BradstreetCorp. $67.87 78.4% 2.3x 7.6x

EquifaxInc. $46.23 97.9% 3.2x 9.8x

IntersectionsInc. $12.62 54.9% 0.6x 4.2x

NationalResearchCorp. $50.25 96.7% 4.3x 13.7x

Average 78.2% 2.4x 8.7x

EnterpriseValue/

CompanyName StockPrice%of52WkHigh

LTMRevenue

LTMEBITDA

CenveoInc. $1.83 27.7% 0.7x 6.5x

InnotracCorp. $1.34 69.4% 0.2x 5.8x

PFSwebInc. $3.64 64.0% 0.2x 9.4x

ValassisCommunicationsInc. $20.75 64.9% 0.6x 4.9x

Average 56.5% 0.4x 6.6x

EnterpriseValue/

Page|10

Wenot

Source:C

DatClos

3/23/

3/08/

3/07/

1/23/

The Funderp

*Exclude

60

70

80

90

100

110

120

May‐11 Ju

tedatotalof1

CHILDSdatabase

teed

/2012 LDCLt

/2012 Heckm

/2012 Solidiu

/2012 Forge

Facil

Facilities anperformedthe

dfromaverageca

un‐11 Jul‐11 Aug‐11

Facilitie

Facil

164transactio

eandCapitalIQ

Buyer

td.

mannCorporatio

umOy

GroupLimited

itiesServices

nd SecuritieseS&P500this

alculations.LTM

Sep‐11 Oct‐11 Nov‐11

esServicesIndex Securities

CHILDS

Sector

litiesServic

onsthisquarte

T

AirlineSeLimited

on ThermoF

OutotecO

CTECPty

sStockIndex

s Servicesquarter.

=LastTwelveMo

Dec‐11 Jan‐12 Feb‐12

Services S&P500Index

SQuarte

rUpdate

cesM&AD

er,upfrom15

Notabl

Target

ervices

Fluids

Oy

Ltd.

x

stock indice

nths.Dataobtain

Mar‐12 Apr‐12 May‐1

erlyUpda

–Facilit

ealsbyQua

9transaction

eTransactEnterpriseValue($mm)

47.6

227.5

118.9

16.5

F

es

Theacomp

nedfromCapitalI

12

Comp

ABMI

EMCO

Fluor

G4Spl

Garda

Johnso

MitieG

Nation

PikeE

Rento

Securi

Avera

ate:1Q2

tiesServ

arter(2004

sin4Q2011a

tions

EV/Revenue EB

0.5x

ND

1.1x 1

ND

FacilitiesSer

averageLTMEparedto7.3xi

IQ.Stockpriceas

anyName

IndustriesInc.

RGroupInc.

Corporation

lc

aWorldSecurityCo

onControlsInc.

Groupplc

nalSecurityGroup

ElectricCorporation

kilInitialplc

itasAB

age

2012

vices

4–1Q201

anddownfrom

EV/BITDA T

ND Proviairlin

ND Recycservi

10.9x Provitechnminin

ND Proviconstmain

rvicesCompa

EBITDAmultiin4Q2011.

ofMay15,2012

StockPrice W

$22.75

$27.95

$51.68

$4.41

or $7.43

$31.38

$4.53

In $8.62

n $7.57

$1.31

$7.26

2)

m186in1Q2

TargetDescript

idessupportseneindustryclingandwastecesidesprocesssonologies,andsengandmetalluridessustainabletruction,operatntenancesolutio

arableCompa

plewas7.1xt

%of52WkHigh

LTRev

92.4% 0

90.4% 0

74.3% 0

93.4% 0

66.2% 0

73.1% 0

94.5% 0

68.7% 0

76.4% 0

81.4% 0

76.6% 0

80.7% 0

E

2011.

tion/Comment

ervicestothe

emanagement

lutions,ervicesforthergicalindustrieeengineering,tions,andons

anyAnalysis

thisquarter

TMvenue

LTMEBITDA

.3x 8.2x

.3x 5.7x

.3x 6.0x

.8x 8.5x

.7x 6.7x

.7x 8.8x

.6x 8.6x

.5x NM

.6x 5.9x

.9x 5.5x

.4x 6.9x

.6x 7.1x

EnterpriseValue/

s

A

/

Page|11

CHILDSQuarterlyUpdate:1Q2012

AboutCHILDSAdvisoryPartnersCHILDSAdvisoryPartnersprovidesexceptionalinvestmentbankingservicestohigh‐performingbusinessservicesandtechnologycompanies in the middle market. Our combination of sector focus, proven processes and entrepreneurial edge set us apart.Collectively,ourseniorbankershaveexecutedover350M&Aandfinancingtransactions.CHILDS,amemberofFINRAandSIPC,isaregisteredbroker‐dealer.

OurServicesSell‐sideAdvisory:Whenyoudesiretosellormergeyourbusiness,wehelpyouprepare,positionandexecutetheprocesswithconfidentialityandspeedtoobtainmaximumresults.

Buyouts&Recapitalizations:We know the private equity groups interested in the sector and can help you prepare for duediligenceandtransactionsuccess.

Buy‐side Advisory: CHILDS can help you source deals, qualify them and negotiate them. Our sourcing “engine”, marketknowledgeandexperienceincreativedealstructureswillensurethatyouseeasmanydealsaspossibleandhavetheabilitytogetthemdone.

Debt/EquityCapitalRaises: Weadvisecompaniesseekingequityordebtcapital forgrowth, recapitalizationor restructuring.CHILDScanhelpyounegotiatewithyourexisting lenderstoreneworrestructuredebtfacilities. Ifneeded,wecantap intoourmanybankingrelationshipstosolicitandnegotiatetermsheetswithotherpotentiallendersaswell.

Financial&StrategicAdvisory:Weprovideanobjectiveanddisciplinedmethodologytohelpyourteamdevelopawinningplanfor short‐term performance and long‐term value creation. Whether it’s a Value Creation Road Map, Strategic AlternativesAssessment,EmployeeStockOwnershipPlan,orFairnessOpinion,weprovideinsighttotheoptionsavailableforcompanyownerstomaximizevalueandliquidity.

SectorFocus–BusinessServices&Technology

IT/ProfessionalServices

HumanCapitalManagement

BusinessProcessOutsourcing FacilityServices

Marketing&InfoServices

Consulting

ManagedServices

Federal

Tech‐enabledbusinessservices

Software

Staffing

HumanResourceOutsourcing

VendorManagementServices/ManagedServiceProvider

RecruitmentProcessOutsourcing

ProfessionalEmploymentOrganization

HCMTechnology

Collections/Receivables

LegalProcessOutsourcing

Teleservices

KnowledgeProcessOutsourcing

RevenueCycleManagement

FacilitiesManagement

Security

Building&Janitorial

Engineering&Maintenance

EquipmentRental

Logistics

Advertising&Media

DigitalAgencies

DataAnalytics

DirectMarketing

Print/Fulfillment

Page|12

Wecom

mpletedthefo

JimChildsManagingDirecPhone:(770)5Email:jchilds@

DavePhillipsDirectorBusinessServicPhone:(904)2Email:dphillips

ollowingtrans

ctor00‐3611

@childsap.com

ces92‐[email protected]

CHILDS

actionsrecen

SQuarte

Rec

tly:

Contac

CooperMilManagingDBusinessSePhone:(770Email:cmill

JimmySecrDirectorTechnologyPhone:(770Email:jsecr

erlyUpda

centActivit

ctInformat

llsDirectorervices0)500‐[email protected]

retarski

y&ProfessionalS0)500‐3619retarski@childsap

ate:1Q2

ty

tion

Services

p.com

2012

DoDiTePhEm

AlVicBuPrPhEm

onHolbrookirectorechnology&Profehone:(949)276‐8mail:dholbrook@

lanBuglercePresidentusinessServicesrivateEquityCoorhone:(678)735‐5mail:abugler@ch

rdinator5320ildsap.com

Page|13

CHILDS

Sele

SQuarte

ctedCHI

erlyUpda

ILDSTra

ate:1Q2

ansactio

2012

ons

![Zoe Childs, Andrew Childs, Pauline Childs, Heather Lee ... · 644 childs v.desormeaux [2006] 1 S.C.R. Social hosts of parties where alcohol is served do not owe a duty of care to](https://img.pdfslide.net/doc/110x75/5e6b7c893e44c3792553cacc/zoe-childs-andrew-childs-pauline-childs-heather-lee-644-childs-vdesormeaux.jpg)