Embed Size (px)

Citation preview

QUARTER 1 2018 LEGISL ATIVE UPDATE

Legislative update

2

GUIDING YOU THROUGH THE LATEST CHANGES

Our legislative update helps you make the most of changes to pensions law and regulation. Guiding you through the latest changes, we aim to give you confidence that your scheme will continue to meet your needs and deliver

value for money and a good outcome for your employees.

Legislative update

3

Q1 2018

01

0203

040506

EMPLOYER-FUNDED Page 4 PENSION ADVICE

SALARY SACRIFICE Page 5

PENSIONS ADVICE Page 6 ALLOWANCE

AUTOMATIC Page 7 ENROLMENT REVIEW

NATIONAL Page 9 INSURANCE REFORMS DELAYED

AUTOMATIC Page 10 ENROLMENT STEP UP

PENSIONS Page 11 DASHBOARD AND NEW SINGLE GUIDANCE BODY

DEFINED BENEFIT Page 12 PENSIONS TRANSFER ADVICE

GOVERNMENT UPDATE REGULATORY UPDATE

An enhancement to the previous £150 tax-exempt limit on employer-funded advice for employees has been implemented, following recommendation by the Financial Advice Market Review (FAMR).

The exemption covers the first £500 of pensions advice provided to an employee – including former and prospective employees – in a particular tax year. Advice can cover a person’s pension arrangements as well as the general financial and taxation issues relating to those funds. The measure reflects the government’s desire to make financial advice more accessible, enabling pension holders to make informed choices about their pension savings.

The employer can pay the adviser or employee benefits consultant for their advice directly, or an employee can be reimbursed for advice they’ve funded without the payment being treated as a benefit in kind.

The income tax and national insurance exemption applies where the advice is made available generally, or to specific employees of qualifying age, or on the grounds of ill-health.

Full details of the conditions are available here.

Government update

4

01

EMPLOYER-FUNDED PENSION ADVICE

£150 £500

The tax-free allowance for employer-funded pension advice has increased from £150 p/a to £500 p/a.

It’s also possible for an employer to include pensions advice as an option in a flexible benefits package, or offer it via salary sacrifice without it being treated as a benefit in kind under the recently introduced ‘optional remuneration arrangement’ rules.

Effective from 6 April 2017, earnings sacrificed by employees in return for a non-cash benefit will generally be taxed. Transitional provisions applying to most salary sacrifice arrangements in place before 6 April 2017 come to an end on 5 April 2018, although some remain in place until 5 April 2021. See our Quarter 1 2017 update for more details.

Significantly, the provision of pensions advice as well as employer-funded pension contributions are among a small number of exempt benefits.

Using salary sacrifice in this way will mean that an employee can effectively fund the advice themselves and still receive the tax and national insurance benefits. Income that is subject to tax and national insurance can be exchanged for employer-funded advice which will be free of both.

As with all salary sacrifice, this will require an amendment to the employees’ contractual terms to take effect. See our guide to salary sacrifice for more details.

Government update

5

SAL ARY SACRIFICE (SAL ARY EXCHANGE)

IMPORTANT TO KNOW

Tax rules around salary sacrifice arrangements are changing, but pension

advice and employer-funded pension contributions will be unaffected.

6

Government update

This is a separate allowance that permits individuals to take up to £500 from their defined contribution pension pots to fund holistic retirement advice – subject to their provider

offering the facility. The allowance can be taken on up to three separate occasions – with only one payment of up to £500 permitted in any given tax year. Advice must be taken from a regulated financial adviser and payment for the advice is made directly from the fund to the adviser without the deduction of any tax. Scottish Widows has introduced this facility.

In theory, it would be possible to use the pensions advice allowance and employer arranged advice together.

Some pension schemes will now allow individuals to pay for advice directly

from their pension pots, tax free.

PENSIONS ADVICE ALLOWANCE

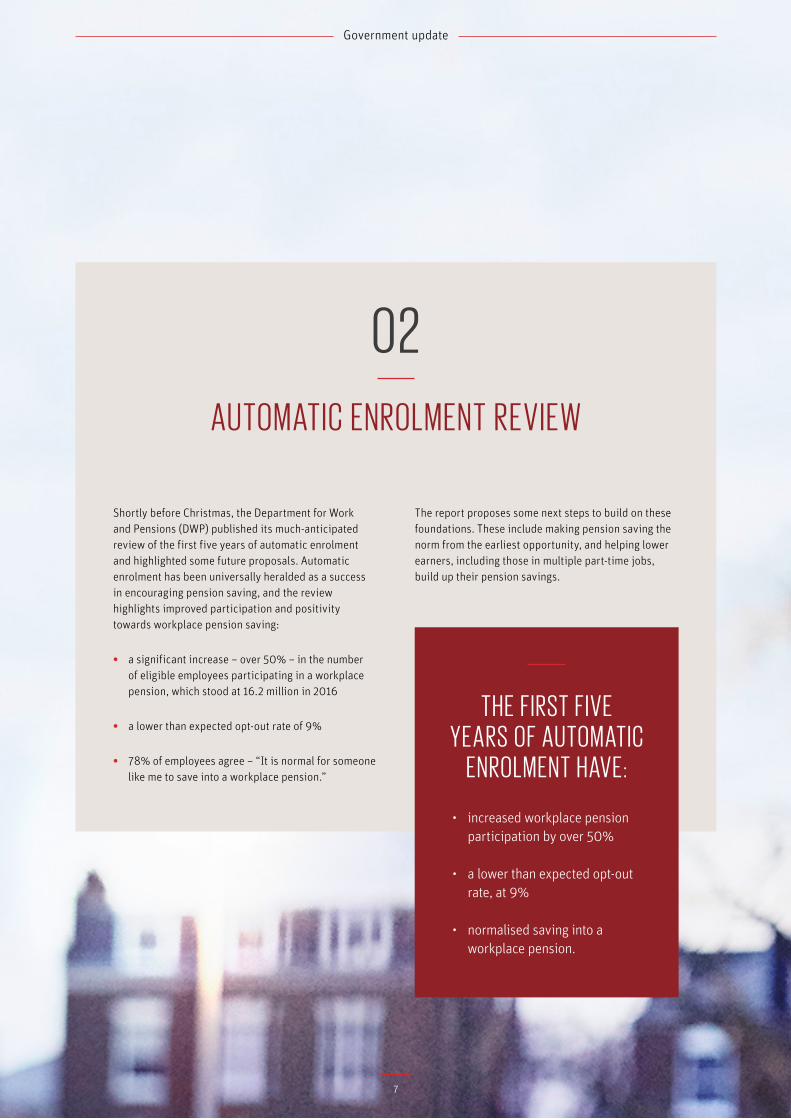

Shortly before Christmas, the Department for Work and Pensions (DWP) published its much-anticipated review of the first five years of automatic enrolment and highlighted some future proposals. Automatic enrolment has been universally heralded as a success in encouraging pension saving, and the review highlights improved participation and positivity towards workplace pension saving:

• a significant increase – over 50% – in the number of eligible employees participating in a workplace pension, which stood at 16.2 million in 2016

• a lower than expected opt-out rate of 9%

• 78% of employees agree – “It is normal for someone like me to save into a workplace pension.”

The report proposes some next steps to build on these foundations. These include making pension saving the norm from the earliest opportunity, and helping lower earners, including those in multiple part-time jobs, build up their pension savings.

Government update

7

02

AUTOMATIC ENROLMENT REVIEW

THE FIRST FIVE YEARS OF AUTOMATIC

ENROLMENT HAVE:

• increased workplace pension participation by over 50%

• a lower than expected opt-out rate, at 9%

• normalised saving into a workplace pension.

Key proposals include:

• lowering the age threshold at which employees become eligible for automatic enrolment from 22 to 18

• removing the lower level of qualifying earnings so that contributions are always calculated from the first pound of an employee’s earnings

• retaining the earnings trigger at £10,000 for 2018/2019, though this is reviewed on an annual basis.

DWP wants to see the first two changes come into effect from the mid-2020s. While this timeframe may be seen as too slow by some, it makes sense to wait until after the forthcoming increases in contributions have bedded in.

There’s no word yet on any further rise to the minimum level of contributions beyond the second phased increase due in April 2019 – it will be important to assess consumer reaction to this. It’s widely acknowledged that saving 8% a year into a pension won’t provide a sufficient pension for most people. However, identifying an adequate threshold for pension saving and how this is made up will require careful consideration if the recent momentum in positive engagement with workplace pension saving is to continue.

Government update

8

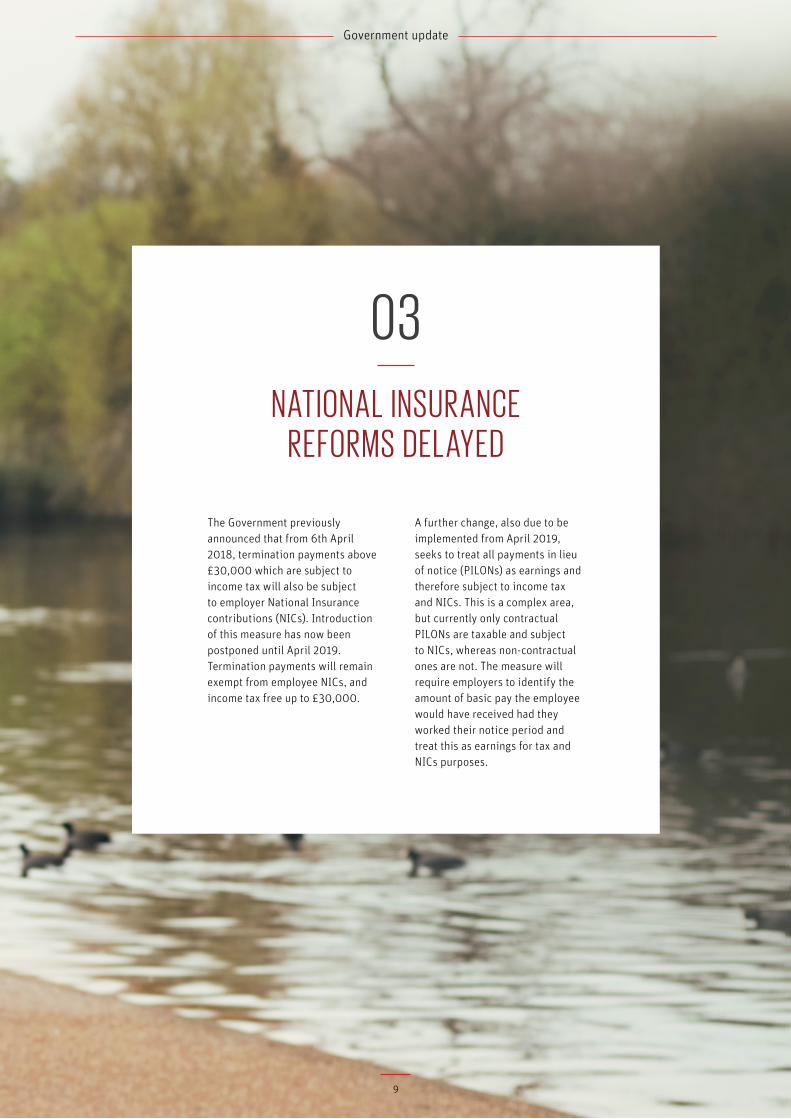

The Government previously announced that from 6th April 2018, termination payments above £30,000 which are subject to income tax will also be subject to employer National Insurance contributions (NICs). Introduction of this measure has now been postponed until April 2019. Termination payments will remain exempt from employee NICs, and income tax free up to £30,000.

A further change, also due to be implemented from April 2019, seeks to treat all payments in lieu of notice (PILONs) as earnings and therefore subject to income tax and NICs. This is a complex area, but currently only contractual PILONs are taxable and subject to NICs, whereas non-contractual ones are not. The measure will require employers to identify the amount of basic pay the employee would have received had they worked their notice period and treat this as earnings for tax and NICs purposes.

Government update

9

03

NATIONAL INSUR ANCE REFORMS DEL AYED

This is also an ideal opportunity to further promote the benefits of pension saving to improve awareness and engagement amongst the workforce.

Employers may well look for support from advisers and providers in this respect and Scottish Widows has developed a range of employee engagement

material – please ask your usual Scottish Widows contact for more details.

04

AUTOMATIC ENROLMENT STEP UP

5% Minimum total pension

contributions from 6 April 2018.

8% Minimum total pension

contributions from 6 April 2019.

Regulatory Update

10

As we approach the first ‘step up’ in minimum contributions that takes place in April 2018, it’s important for employers to remind members of the increase. We have produced a summary of the revised contribution levels, which also includes some frequently asked questions to help employers to

respond to enquiries from employees.

The DWP announced towards the end of 2017 it would be taking over ownership of the project to deliver the Pensions Dashboard – an initiative due to launch in 2019 enabling pension savers to view details of all of their retirement savings in one place. It says people have an average of 11 different jobs during their lifetime which can make keeping track of pension benefits difficult.

Aiming to cover the state pension, defined benefit (or ‘final salary’) and defined contribution (or ‘money purchase’) pensions, it would provide savers with current valuations and scheme contact details. The Minister of Pensions, Guy Opperman, is due to provide a progress report to Parliament at the end of March 2018.

DWP is also responsible for establishing a new single Public Financial Guidance Body – scheduled to launch in October 2018 – replacing the Money Advice Service, Pensions Advisory Service, and DWP’s ‘Pension Wise’. The aim is to remove duplication and make it easier for consumers to find the education, support and guidance they require in their retirement planning.

Regulatory update

11

05

PENSIONS DASHBOARD AND NEW SINGLE GUIDANCE BODY

THE AVER AGE WOR KER HAS 11 JOBS OVER THEIR L IFETIMEThe DWP aims to launch the Pensions Dashboard in 2019 to help workers find and keep track of their pension benefits.

The Financial Conduct Authority (FCA) is considering responses to its consultation in relation to defined benefit transfers and is due to publish

its findings in Quarter 1.

Interim findings based on a sample of cases revealed that customer outcomes were improved in nearly half of the cases, an acknowledgement that defined benefit transfers can be appropriate for some individuals in

certain circumstances.

Regulatory update

12

06

DEFINED BENEFIT PENSIONS TR ANSFER ADVICE

Scottish Widows Limited. Registered in England and Wales No. 3196171. Registered office in the United Kingdom at 25 Gresham Street, London EC2V 7HN. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Financial Services Register number 181655.

27404 02/18

HELPING YOU MAKE THE MOST OF CHANGE