Embed Size (px)

Citation preview

G

T

Peter Iro

Peter Mc

E: inf

A

Issued Sha

Cash Ba

ABN

Geoff Dono

Jacques Ba

Thomas Hill

onside ‐ No

cIntyre ‐ No

168 S

Western A

T: +6

fo@zamanc

ASX Code: Z

res: 43,660

alance: $3.1

34 124 782

Direc

ohue ‐ Chair

adenhorst ‐

l ‐ Exec Dire

on‐Exec Dire

on‐Exec Dire

Head O

Stirling High

Nedla

Australian 6

1 (8) 9423 5

cominerals.

ZAM

0,000

12M

2 038

ctors

man

‐ MD

ector

ector

ector

ffice

hway

ands

6009

5925

com

Z

q

H

D

e

S

O

l

i

a

D

F

Qufor the

Zamanco Mi

quarterly rep

HIGHLIGHTS

Options Aindicated

Options Aproductio

mangane

Geophysithe end o

Tenders ithe propo

Directors

Current c

Subsequewere con

by a direc

During the Q

exploration p

Study for the

Over the co

level of act

including geo

aim of delin

December q

Feasibility St

uartere perioinerals Limit

port for the p

S

Analysis for

d strong pote

Analysis ind

on of hig

ese and man

ical surveys

of the quarte

invited for t

osed Serenje

s exercised 8

cash on hand

ent to the

nverted to O

ctor), raising

Quarter, the

program as w

e proposed S

oming quarte

tivity and n

ophysics and

neating suff

quarter, the

tudy for the

rly Acod endited (ASX: ZA

period ended

proposed Se

ential econo

icated that o

h and me

ganese meta

for five prio

er;

the key aspe

e Ferromang

8.45m listed

d of A$3.12m

Quarter, a

Ordinary Zam

g A$4.18m, b

Company fo

well as the c

Serenje Ferro

ers, the Com

newsflow re

d follow‐up d

ficient resou

e focus is e

proposed Se

ctiviting 30 SAM; “Compa

d 30 Septem

erenje Ferro

mic returns;

optimal plan

edium carb

al;

ority explora

ects of the B

ganese Proje

Zamanco op

m and no deb

further 20.8

manco share

before costs.

ocused on p

commencem

omanganese

mpany plans

elated to S

drilling are un

urces to jus

expected to

renje Ferrom

ies ReSeptemany”) is plea

mber 2012.

omanganese

;

nt configura

bon ferrom

ation targets

Bankable Fe

ect;

ptions raising

bt;

89m listed

es (including

.

preparations

ment of the B

e Project in Z

s to significa

Serenje. Exp

nderway and

stify the pr

shift towa

manganese P

Page 1

eportmber 20

sed to pres

Project in Z

tion will allo

manganese,

s commence

easibility Stu

g A$1.69m;

Zamanco o

g 1.25m exe

for the upc

Bankable Fea

ambia.

antly increa

ploration act

d planned w

roject. Durin

ards the Ba

Project.

t 012 ent its

Zambia

ow for

silica

ed post

udy for

options

ercised

coming

sibility

se the

tivities

ith the

ng the

nkable

Quarterly Activities Report period ending 30 September 2012

Page 2

ZAMBIAN MANGANESE PROJECTS

Tenements

Zamanco has expanded its portfolio of tenements during the September Quarter through entering into a JV agreement and successfully completing a due diligence on the Evaristo Kampumba tenement (14340‐HQ‐SPP).

This expands Zamanco’s portfolio of tenements to eight (8) covering an area of approximately 2,700km2 as indicated below in Figure 1.

The Epimax Kabwe Small Scale Mining License (7713‐HQ‐SML) due diligence outcome is expected to be completed within the next quarter.

Figure 1: Zamanco’s tenements in Zambia.

Quarterly Activities Report period ending 30 September 2012

Page 3

ZAMBIA EXPLORATION

The commencement of detailed exploration on the Company’s JV tenements was delayed due to the moratorium over the transfer of tenements in Zambia. Whilst the moratorium has now been lifted, the process of tenement transfers is still working through the backlog of applications.

The Company has restructured its JV agreements to allow for access to the exploration properties during the tenement transfer process. As a result of this, the Company is in the process of significantly increasing its exploration program over its priority exploration projects.

A geophysical survey including ground magnetics, ground gravity, resistivity and conductivity commenced in October on five of the Company’s JV projects. The ground magnetics survey will take the longest to complete, with 43 days estimated to complete the 428 line km of survey. It is expected that this work will be completed by the end of November 2012. The ground gravity, resistivity and conductivity surveys will be completed in parallel with the ground magnetics survey.

Whist there are outcrops and trenching data available for the five priority exploration projects, the geophysical surveys will be used to better map the manganiferous ore zones prior to drilling. Manganese mineralisation in the project areas usually occurs as tabular bodies, however it is known to pinch and swell along strike as well as to have differing down dip extensions. This program is designed to assist the Company in targeting the resource drilling program, expected to commence before the end of 2012.

Quarterly Activities Report period ending 30 September 2012

Page 4

Evaristo Kampumba (14340‐HQ‐SPP)

An initial report on the Evaristo Kampumba (14340‐HQ‐SPP) tenement was received with promising grades of manganese ranging from 32% Mn to 51%Mn. This tenement will form part of the five priority projects.

A short field investigation of license 14340‐HQ‐SPP near Kapiri Mposhi, Zambia was conducted by Minrom Consulting in September 2012 (Figure 2). Mineralisation encountered in the license is situated in a large open pit which has been mined previously by artisanal miners.

Figure 2: Map indicating the field tracks and waypoint investigated by Minrom Consulting within license 14340‐HQ‐SPP.

Quarterly Activities Report period ending 30 September 2012

Page 5

Four grab samples were collected, two in situ samples from the manganese bearing vein, one from the iron rich piles left after manganese had been removed and one selectively taken from all the best manganese nodules found around the pit (Figure 3).

Figure 3: Examples of braunnite type in situ manganese (top) and more iron rich psilomelane and braunnite type manganese (bottom) removed from the Kampumba license 14340‐HQ‐SPP.

The deposit represents a vein type manganese deposit with manganese mineralisation being concentrated by localised trap sites such as faults. The latter stated lends the deposit a type 2 characteristic namely that it has been enriched by secondary structures such as faults along which enrichment conduits may have formed.

Quarterly Activities Report period ending 30 September 2012

Page 6

Figure 4: Portion of the manganese vein showing high grade manganese (visual inspection) in the form of braunnite.

Results from the grab samples clearly shows that the manganese veins contain zones which are more iron rich and more manganese rich. The richest portion of manganese is from the zones in the vein where braunnite mineralisation was observed.

Table 1: Provisional table showing the sample descriptions and corresponding waypoints.

Sample ID Waypoint Description Type of sample

Mn % Fe% SiO2 %

S 4101 Ks1 In situ sample from

manganese rich portion of the vein

Grab sample 50.95 7.90 0.96

S 4102 Ks2 In situ sample selected in

friable part of vein across the whole of the vein

Grab sample 31.91 29.41 2.23

S 4103 Ks3 Grab sample of more Fe rich

portion of vein Grab sample 15.93 50.63 0.15

S 4104 Ks4

Selective sample of higher quality (upon visual

inspection) manganese nodules around the open pit

Grab sample 46.77 10.51 1.47

Quarterly Activities Report period ending 30 September 2012

Page 7

Scoping work by Zamanco has outlined the trace of a possible zone of manganese mineralisation in and adjacent to license 14340‐HQ‐SPP (Figure 5). A trend of manganese mineralisation is clearly visible as extending from east to west. The identification of possible zones of further trenching and channel sampling could be identified using geophysical exploration concentrated along this trend.

Figure 5: Map showing the proposed trend of a larger manganese vein in the Kampumba area. Geophysical exploration should be focussed around this area.

The sampled manganese at the Kampumba pit is of high quality, and warrants further investigation in order to elucidate if there is any extension of the manganese vein from the Kampumba pit area. Localised geophysical exploration will be employed around the Kampumba open pit as there clearly is a potential for extension of the manganese reef.

OPTIONS ANALYSIS

Pyrocon, in conjunction with EPS, an associated company was commissioned by Zamanco to investigate different process routes for the downstream processing of manganese ore in Zambia. As the Company has already investigated various limiting factors such as power, haulage and sea transport, the study was based upon the premise of the production of 60,000tpa of high carbon ferromanganese and 12,000tpa of manganese metal.

The scope requirement was to investigate the economics of producing HC FeMn as well as looking at the various other alloys that can be produced from HC FeMn. These included medium carbon FeMn (MC FeMn), low carbon ferromanganese (LC FeMn) and SiMn. The scope included the determination of the various plant requirements for these various options as well as the amounts of consumables required for each option.

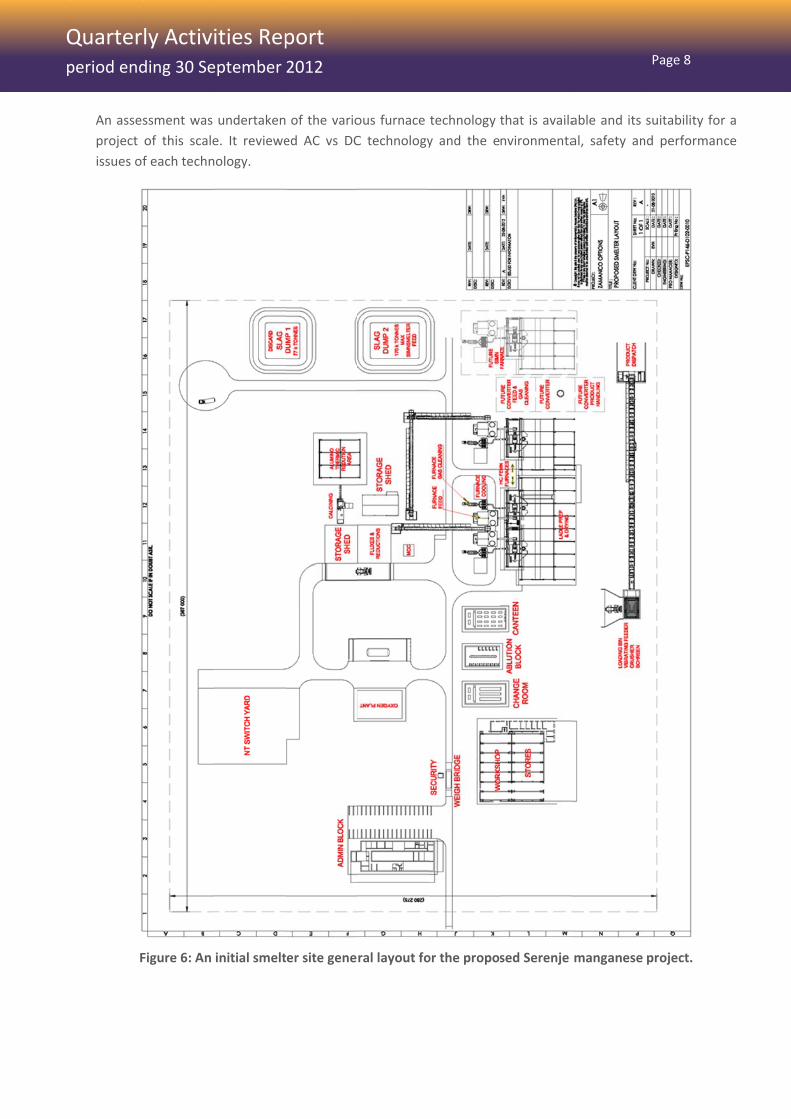

QpQuarterperiod end

An assesproject issues of

F

ly Actividing 30 Se

ssment was of this scalef each techn

Figure 6: An

ities Repeptember

undertakene. It revieweology.

initial smelt

port 2012

of the varioed AC vs DC

er site gene

ous furnace C technology

ral layout fo

technology y and the e

or the propos

that is availanvironmenta

sed Serenje

able and its al, safety an

manganese

Page 8

suitability fond performa

project.

or a nce

Quarterly Activities Report period ending 30 September 2012

Page 9

Study Results

The intention of the option study was to evaluate several process routes in order to determine which are more favourable. These high level selection criteria will be used to generate the scope for further studies or to define the constraints for product selection as part of a Bankable Feasibility Study. The option study has identified several areas where additional work is required to ensure that project and operational risk is mitigated. The most important is complete ore characterisation including beneficiation, calcining (if required) and smelting tests.

In order to produce any other ferromanganese alloy products it is necessary to first install a HC FeMn smelter. The design intent is for three small furnaces to be constructed followed by adding a converter section for the production of MC FeMn as well as an additional small smelter for the production of SiMn. Initial start‐up will produce a HC FeMn product allowing other products to follow in the next phases of the project.

The converter route producing a medium carbon ferromanganese (MC FeMn) product shows the most favourable operating cost value addition. This however must be weighed against the initial capital investment of a converter and associated peripherals to be determined.

The furnace design can be optimised so that it is possible to produce both HC FeMn and SiMn from the same furnaces, which allows flexibility in the final product depending on market requirements.

The following process routes were investigated:

1. High Carbon Ferromanganese (HC FeMn)

a. The first option includes the use of a HG ore and addition of iron scrap to supplement the shortage of iron units. Iron units can alternatively be supplemented by iron ore.

Figure 1a: HC FeMn production from HG ore and scrap iron.

Quarterly Activities Report period ending 30 September 2012

Page 10

b. The second option includes the use of HG ore together with an iron rich LG ore to eliminate the use of iron scrap additions.

2. Medium/Low Carbon Ferromanganese (MC/LC FeMn)

a. The first option is to install a converter and to convert HC FeMn to MC and/or LC FeMn by oxygen blowing.

Figure 2a: MC FeMn or LC FeMn production with a converter

b. The second option is to utilise SiMn and the mixing of a lime ore melt in a ladling process called the Perrin process.

3. Silicomanganese (SiMn)

a. This option utilises the HC FeMn slag with HG ore addition to produce SiMn.

4. Manganese (Mn)

a. Metallic manganese production by aluminothermic reduction is a licenced process under third party scope.

For the production of HC FeMn, the study found that it would require 121‐141ktpa of ore to produce 60ktpa of HC FeMn, depending if option 1a or 1b was implemented.

For the proposed subsequent conversion of HC FeMn to MC/LC FeMn, the study showed that the 60ktpa of HC FeMn could be converted into 56ktpa of MC FeMn or 52ktpa of LC FeMn. This was shown by the authors to be quite important as although it would result in 7% less product per annum, the MC FeMn price is significantly higher than that for HC FeMn (currently 60% higher), which would outweigh the loss of volume. The study indicated that a converter would be required to produce MC FeMn and that further work was required to determine the cost‐benefit analysis of the additional capital required.

Quarterly Activities Report period ending 30 September 2012

Page 11

For the production of SiMn, it was indicated that it would be possible to produce SiMn using the same furnaces as the HC FeMn whilst utilising the slag from HC FeMn as the ore feed. Pyrocon estimated that 9.5ktpa of SiMn could be produced from the waste slag product and the addition of 4,200tpa of high grade manganese ore. It is estimated that the value of the production of SiMn was comparable to the value of the production of HC FeMn.

BANKABLE FEASIBILITY STUDY

Zamanco’s management, in association with its consultants, have been investigating and assessing the processing plant requirements for the Serenje Manganese Project for over a year. At each stage of the process, the proposed configuration has been calibrated against the available power, water and resource availability to determine a project that is economically robust and able to be built using these constraints.

The Bankable Feasibility Study (“BFS”) involves the assessment of a number of variables from the objective of minimising risk and maximising project value. During the BFS, several alternative production scenarios will be assessed on the basis of meeting these objectives.

Work to be completed as part of the BFS includes:

Resource Drilling and Estimation – Geophysical surveys are about to commence on five priority exploration projects in Zambia with the aim of firming up resource drilling targets. Drilling is expected to start before the end of 2012 with a resource estimate to be completed based on these results.

Mining Studies – Whilst the mining studies require a resource block model as a starting point, the mining study will look at the mining equipment and personnel requirements for an open pit mining operation and beneficiation plant for the production of approximately 200,000t of ore per annum.

Haulage Studies – This study will look at the haulage requirements from the mine to the proposed smelter site at Serenje, as well as haulage requirements to and from Serenje to Beira or Dar es Salaam. It is currently anticipated that 200,000t of ore will be hauled to Serenje and ~72,000t of product will be trucked to port each year.

Pyrometallurgical Studies – Following on from the Option Analysis, this study will look in detail at the requirements for the production of high carbon ferromanganese, medium carbon ferromanganese and/or silica manganese. The study will assess the alternatives of staging the development of the various smelters versus the construction of the plant in one go.

Environmental, Permitting and Social Studies – The environmental and social aspects of the study will commence for the Serenje component of the project, with the studies relating to the mine areas to commence once the mining studies are underway. These studies will look at the environmental impact of the proposed activities, ways of minimising disturbance as well as ways to increase the social participation rate for stakeholders in the vicinity of the project.

Economics and Optimal Financing Strategies – It is expected that the BFS will result in at least two different development strategies based on either the construction of the project in one go or as a staged approach with subsequent components financed out of cashflow. In conjunction with project and equity financiers, the Company will assess the route that maximises the benefits and minimises risks for the Zamanco shareholders.

It is expected that the BFS will take ~7 months to complete with a deliverable report expected by end of Q2 2013.

Quarterly Activities Report period ending 30 September 2012

Page 12

CORPORATE

During the Quarter, the Company issued 8,510,000 Ordinary shares, upon conversion by Directors of listed Zamanco options, raising A$1.69m.

Subsequent to the Quarter, a further 20,890,000 Ordinary shares were issued following the conversion of listed Zamanco options that expired on 30 September 2012. This included the exercise of 1.25m options held by a director. The conversion of the A$0.20 options, which was underwritten by Taylor Collison and BBY Limited, raised A$4,178,000 (before costs).

Following the conversion of the options, the Company has 64,550,000 Ordinary shares on issue.

Cash Position

As at 30 September 2012, the Company had A$3.12m in cash and equivalents.

NEXT QUARTER

Following the completion of the initial exploration program on the Zambian JV tenements, the Company plans to significantly increase activities in the December quarter including:

Complete geophysical survey over priority targets; Mobilise and commence diamond/RC drilling after completion and interpretation of geophysical survey over priority targets;

Completion of the signing of Exploration and Mining Access agreements as well as registration of securities over tenement areas;

Commencement of the BFS for the proposed Serenje Ferromanganese Project. Actively pursue the increase of Zamanco’s tenement portfolio through tenements that are currently under investigation.

Should you require further information please contact:

Geoff Donohue Jacques Badenhorst Chairman Managing Director Ph: +61 8 9423 5925 Ph: + 27 82 780 8443 Certain information in this announcement refers to the intentions of Zamanco Minerals Limited, but these are not intended to be forecasts, forward looking statements, or statements about future matters for the purposes of the Corporations Act or any other applicable law. The occurrence of events in the future are subject to risks, uncertainties and other factors that may cause Zamanco Minerals Limited’s actual results, performance or achievements to differ from those referred to in this announcement. Competent Person Statement The information in this report that relates to Exploration Results including exploration data and geological interpretations within Zambia is based on information compiled by Mr Oscar van Antwerpen, a member of Minrom Consulting, a mineral resource management company based in South Africa. Mr van Antwerpen is a member in goodstanding of the Geological Society of South Africa which is a “Recognised Overseas Professional Organisation” (ROPO). A ROPO is an accredited organisation to which Competent Persons must belong for the purpose of preparing reports on Exploration Results, Mineral Resources and Ore Reserves for submission to the ASX. Mr van Antwerpen has sufficient experience, which is relevant to the style of mineralisation and type of deposits under consideration and to the activity being undertaken to qualify as a Competent Person as defined in the 2004 Edition of The JORC Code. Mr van Antwerpen consents to the inclusion in the report of the matters based on the information in the form and context in which it appears.

The Exploration Targets in this report have been developed based on surface and trenching exploration only at this stage. The potential quantity and grade is conceptual in nature. There has been insufficient exploration to define a Mineral Resource and that it is uncertain if further exploration will result in the determination of a Mineral Resource.

Appendix 5B Mining exploration entity quarterly report

+ See chapter 19 for defined terms. 01/06/2010 Appendix 5B Page 1

Rule 5.3

Appendix 5B

Mining exploration entity quarterly report Introduced 1/7/96. Origin: Appendix 8. Amended 1/7/97, 1/7/98, 30/9/2001, 01/06/10.

Name of entity

Zamanco Minerals Limited

ABN Quarter ended (“current quarter”)

54 093 278 436 30 September 2012

Consolidated statement of cash flows

Cash flows related to operating activities

Current quarter $A’000

Year to date (3 months) $A’000

1.1 Receipts from product sales and related debtors ‐ ‐

1.2 Payments for (a) exploration & evaluation (b) development (c) production (d) administration

(345) ‐ ‐

(95)

(345)‐‐

(95) 1.3 Dividends received ‐ ‐1.4 Interest and other items of a similar nature

received 16 16

1.5 Interest and other costs of finance paid ‐ ‐1.6 Income taxes paid ‐ ‐1.7 Other (GST) 6 6

Net Operating Cash Flows

(418) (418)

Cash flows related to investing activities

1.8 Payment for purchases of: (a) prospects (b) equity investments (c) other fixed assets

‐ ‐ ‐

‐‐‐

1.9 Proceeds from sale of: (a) prospects (b) equity investments (c) other fixed assets

‐ ‐ ‐

‐‐‐

1.10 Loans to other entities ‐ ‐1.11 Loans repaid by other entities ‐ ‐1.12 Other (provide details if material) ‐ ‐

Net investing cash flows ‐ ‐

1.13 Total operating and investing cash flows (carried forward) (418) (418)

Appendix 5B Mining exploration entity quarterly report

+ See chapter 19 for defined terms. Appendix 5B Page 2 01/06/2010

1.13 Total operating and investing cash flows (brought forward) (418) (418)

Cash flows related to financing activities

1.14 Proceeds from issues of shares, options, etc. (net of costs) 1,702 1,702

1.15 Proceeds from sale of forfeited shares ‐ ‐1.16 Proceeds from borrowings ‐ ‐1.17 Repayment of borrowings ‐ ‐1.18 Dividends paid ‐ ‐1.19 Other (provide details if material) ‐ ‐ Net financing cash flows 1,702 1,702

Net increase (decrease) in cash held

1,284 1,284

1.20 Cash at beginning of quarter/year to date 1,832 1,8321.21 Exchange rate adjustments to item 1.20

1.22 Cash at end of quarter 3,116 3,116

Payments to directors of the entity and associates of the directors Payments to related entities of the entity and associates of the related entities

Current quarter $A'000

1.23

Aggregate amount of payments to the parties included in item 1.2 112

1.24

Aggregate amount of loans to the parties included in item 1.10 ‐

1.25

Explanation necessary for an understanding of the transactions

• payment of consulting fees

Non-cash financing and investing activities 2.1 Details of financing and investing transactions which have had a material effect on consolidated

assets and liabilities but did not involve cash flows N/A

2.2 Details of outlays made by other entities to establish or increase their share in projects in which the

reporting entity has an interest N/A

Appendix 5B Mining exploration entity quarterly report

+ See chapter 19 for defined terms. 01/06/2010 Appendix 5B Page 3

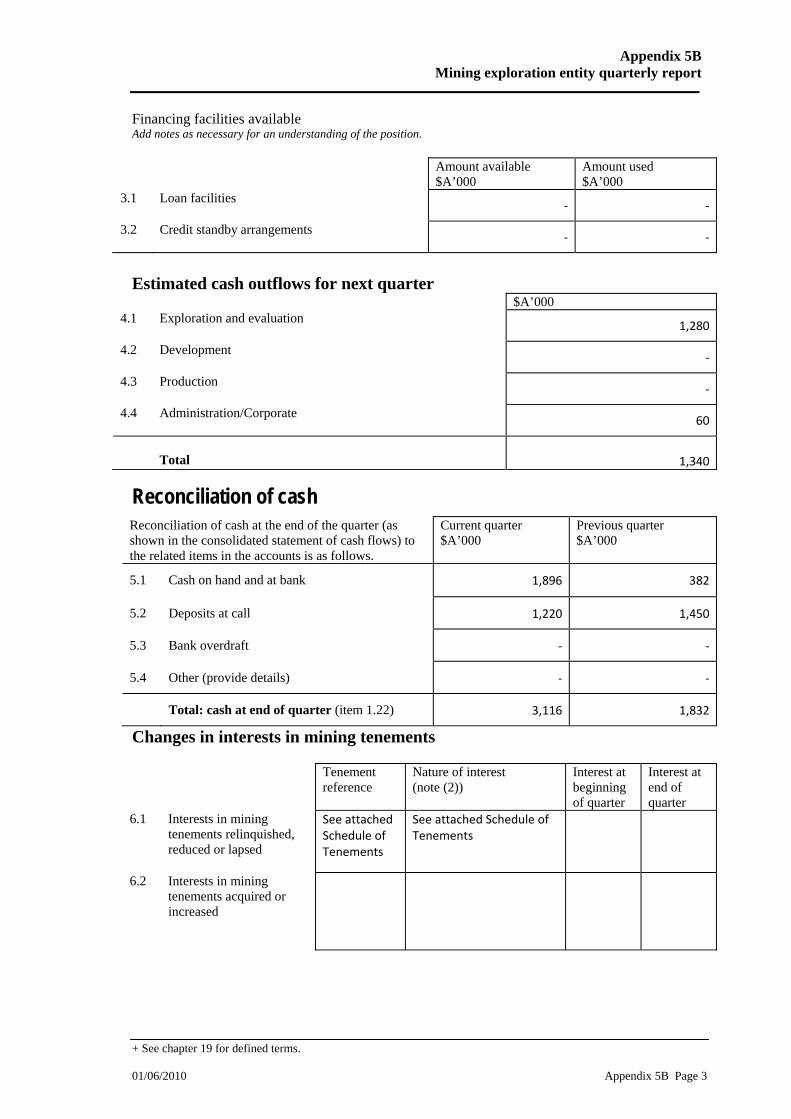

Financing facilities available Add notes as necessary for an understanding of the position.

Amount available $A’000

Amount used $A’000

3.1 Loan facilities ‐ ‐

3.2 Credit standby arrangements ‐ ‐

Estimated cash outflows for next quarter

$A’000 4.1 Exploration and evaluation

1,280

4.2 Development ‐

4.3 Production ‐

4.4 Administration/Corporate 60

Total 1,340

Reconciliation of cash Reconciliation of cash at the end of the quarter (as shown in the consolidated statement of cash flows) to the related items in the accounts is as follows.

Current quarter $A’000

Previous quarter $A’000

5.1 Cash on hand and at bank 1,896 382

5.2 Deposits at call 1,220 1,450

5.3 Bank overdraft ‐ ‐

5.4 Other (provide details) ‐ ‐

Total: cash at end of quarter (item 1.22) 3,116 1,832

Changes in interests in mining tenements Tenement

reference Nature of interest (note (2))

Interest at beginning of quarter

Interest at end of quarter

6.1 Interests in mining tenements relinquished, reduced or lapsed

See attachedSchedule of Tenements

See attached Schedule ofTenements

6.2 Interests in mining tenements acquired or increased

Appendix 5B Mining exploration entity quarterly report

+ See chapter 19 for defined terms. Appendix 5B Page 4 01/06/2010

Issued and quoted securities at end of current quarter Description includes rate of interest and any redemption or conversion rights together with prices and dates. Total number Number quoted Issue price per

security (see note 3) (cents)

Amount paid up per security (see note 3) (cents)

7.1 Preference +securities (description)

7.2 Changes during quarter (a) Increases through issues (b) Decreases through returns of capital, buy-backs, redemptions

7.3 +Ordinary securities 43,660,000 43,660,000 Fully paid

7.4 Changes during quarter (a) Increases through issues (b) Decreases through returns of capital, buy-backs

8,510,000

8,510,000

Fully Paid

7.5 +Convertible debt securities (description)

7.6 Changes during quarter (a) Increases through issues (b) Decreases through securities matured, converted

7.7 Options (description and conversion factor)

20,890,0001,000,000

20,890,000‐

Exercise price $0.20 $0.25

Expiry date30 September 2012

30 June 2013 7.8 Issued during

quarter

7.9 Exercised during quarter 8,510,000 8,510,000 $0.20 30 September 2012

7.10 Expired during quarter

7.11 Debentures (totals only)

7.12 Unsecured notes (totals only)

Appendix 5B Mining exploration entity quarterly report

+ See chapter 19 for defined terms. 01/06/2010 Appendix 5B Page 5

Compliance statement 1 This statement has been prepared under accounting policies which comply with

accounting standards as defined in the Corporations Act or other standards acceptable to ASX (see note 4).

2 This statement does /does not* (delete one) give a true and fair view of the matters

disclosed.

Sign here: ............................................................ Date: 31 October 2012

(Director/Company secretary) Print name: PETER R IRONSIDE Notes 1 The quarterly report provides a basis for informing the market how the entity’s

activities have been financed for the past quarter and the effect on its cash position. An entity wanting to disclose additional information is encouraged to do so, in a note or notes attached to this report.

2 The “Nature of interest” (items 6.1 and 6.2) includes options in respect of interests in

mining tenements acquired, exercised or lapsed during the reporting period. If the entity is involved in a joint venture agreement and there are conditions precedent which will change its percentage interest in a mining tenement, it should disclose the change of percentage interest and conditions precedent in the list required for items 6.1 and 6.2.

3 Issued and quoted securities The issue price and amount paid up is not required in

items 7.1 and 7.3 for fully paid securities. 4 The definitions in, and provisions of, AASB 1022: Accounting for Extractive

Industries and AASB 1026: Statement of Cash Flows apply to this report. 5 Accounting Standards ASX will accept, for example, the use of International

Accounting Standards for foreign entities. If the standards used do not address a topic, the Australian standard on that topic (if any) must be complied with.

== == == == ==

Appendix 5B Mining exploration entity quarterly report

+ See chapter 19 for defined terms. Appendix 5B Page 6 01/06/2010

Zamanco Minerals Limited ABN 34 124 782 038

Notes to and forming part of Appendix 5B

Mining exploration entity quarterly report as at 30 September 2012 Note 1 – Mining Tenement Schedule

ZAMBIAN TENEMENTS

1. Mkushi

Tenement Registered Holder or Applicant % Interest held 15836‐HQ‐SPP transfer to Zamanfour pending Jack Stuart Zamanfour Minerals Ltd ‐ 49%

Jack Stuart – 51% 17585‐HQ‐LPL application pending Zamanfour Minerals Ltd Zamanfour Minerals Ltd ‐ 49%

Jack Stuart – 51%

2. Mansa

Tenement Registered Holder or Applicant % Interest held 15817‐HQ‐LPL transfer to Zamantwo pending Jack Stuart Zamantwo Minerals Ltd ‐ 49%

Jack Stuart – 51%

3. Milenge

Tenement Registered Holder or Applicant % Interest held 12897‐HQ‐LPL transfer to Zamanone pending Albert Malama Zamanone Mining Ltd ‐ 80%

Albert Malama – 20% 17584‐HQ‐LPL application pending Zamanone Mining Ltd Zamanone Mining Ltd ‐ 80%

Albert Malama – 20%

4. Evaristo Kampumba

Tenement Registered Holder or Applicant % Interest held 14340‐HQ‐SPP transfer to Zamanthree pending Evaristo Mutambo Zamanthree Minerals Ltd ‐ 49%

Evaristo Mutambo – 51%

5. Serenje/Milenge – (Subject to due diligence)

Tenement Registered Holder or Applicant % Interest held 14553‐HQ‐LPL Edith Lukwesa 100%

6. Chinsali – (Subject to due diligence)

Tenement Registered Holder or Applicant % Interest held 13487‐HQ‐SPP Sunday Sinyangwe 100%

Appendix 5B Mining exploration entity quarterly report

+ See chapter 19 for defined terms. 01/06/2010 Appendix 5B Page 7

7. EML Kabwe – (Subject to due diligence)

Tenement Registered Holder or Applicant % Interest held 7713‐HQ‐SML Epimax Mining Ltd 100%

8. EML Mansa ‐ (Subject to due diligence)

Tenement Registered Holder or Applicant % Interest held 14369‐HQ‐LPL Epimax Mining Ltd 100% WEST AUSTRALIAN TENEMENTS

9. Yundamindera Joint Venture – Crest Minerals earning 51%

Tenement Registered Holder or Applicant % Interest held E39/1110 BrilliantGold Pty Ltd

APG Resources Pty Ltd 70% 30%