Embed Size (px)

Citation preview

Quarterly Report June 2013

29 July 2013

ABOUT ALTONA

Altona Mining Limited (ASX: AOH) is

an international base metals producer

with a focus on copper.

The Company has two main assets:

The Outokumpu Project in south-east

Finland comprises an underground

decline mine and processing plant.

Production commenced in 2012 and

averages 8,000tpa of copper,

8,400ozpa of gold and 1,600tpa of

zinc.

The Roseby Copper Project near Mt

Isa in Queensland has a resource

containing 1.52Mt of copper and

0.38Moz of gold. A Definitive

Feasibility Study has been completed

for a 7Mtpa open pit copper-gold mine

and concentrator at Little Eva.

Shares on issue: 528,992,704

Options on issue: 1,365,000

Share rights on issue: 9,677,749

Cash on hand: A$26.1M

Market capitalisation

at 16.5 cents per share A$87M

Altona Mining Limited

ACN: 090 468 018

Ground Floor, 1 Altona Street

West Perth

Western Australia 6005

T: +61 8 9485 2929

ASX: AOH

Frankfurt: A2O

Oslo: ALTM

Outokumpu Meets Production Guidance in First Full Year

JUNE QUARTER PRODUCTION

Copper in concentrates 1,809 tonnes

Gold in concentrates 1,822 ounces

C1 cash cost US$2.23/lb of payable copper

Production - The June quarter copper production for the

Outokumpu Project was lower than the previous quarter due

to lower ore volumes and the planned stoping sequence in

lower grade ore.

Guidance increased - Annual production guidance for

FY2014 has been increased to 7,600-8,400 tonnes of

copper, 8,000-9,000 ounces of gold at a C1 cash cost of

US$1.70-1.85 per pound. The first full year of production

exceeded initial guidance and met subsequently upgraded

guidance.

C1 Cash costs - C1 cash cost of US$2.23 per pound of

payable copper was above the FY2013 average of US$1.69

per pound. Lower gold credits and production volumes

contributed to the performance. Costs are expected to return

to lower levels next quarter.

Cashflow from operations - Operating cashflow was A$3.0

million after capital expenditure.

Cash on hand - A$26.1 million plus receivables from

concentrate sales of A$5.0 million at 30 June 2013. Cash is

up ~15% from the March quarter of A$22.6 million.

Outokumpu drilling - A number of high grade intercepts

have been returned from the Wallaby-Wombat gap area and

are expected to add to resources and reserves:

13.4 metres at 4.7% copper, 0.8g/t gold

14.8 metres at 4.0% copper, 1.2g/t gold

11.3 metres at 4.6% copper, 0.9g/t gold

11.0 metres at 16.1g/t (gold uncut)

Roseby partnering - Discussions with various parties to

either sell, partner or finance the Little Eva project have yet

to deliver an offer acceptable to Altona. The Company has

reduced activities at Roseby whilst the process continues.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

2.

Recent aerial shot of the Luikonlahti mill site. It shows the tailings dam (A) at top centre, the cobalt-nickel

concentrate storage dam to the left (B) and old pits at C.

The Luikonlahti mill buildings showing the workshop at A, the old shaft and secondary crusher at B, the mill hall at C and concentrate storage sheds at D. The former talc processing facilities are at E and the cobalt-nickel concentrate storage dam at F.

A

B

C

A

B

C

D

E

F

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

3.

Safety, Environment and People

Safety

performance

continues to

improve

Safety performance at Outokumpu in the June quarter saw modest improvement. Up

to the middle of June the operation had achieved 255 days without a lost time incident

(“LTI”) prior to an incident involving a trainee’s ankle injury at the mill. The year to

date lost time injury frequency rate and medically treated injury frequency rate per one

million man hours continue to trend downwards and are now 9 and 21 respectively.

Altona continues to be unsatisfied with the number of incidents which leaves us short

of our aim to be equal to, or better than, the best of our Finnish peers in safety

performance. There will be a renewed focus on our safety culture after the Finnish

summer break.

The Company now has 110 employees and 105 contractors in Finland and 15

employees in Australia.

There were no reportable environmental incidents during the quarter.

Commentary on Markets and Outlook for FY2014

Outokumpu

Project has

outperformed

initial

production and

grade

expectations

The Outokumpu Project is a quality de-risked and profitable operation. The mine will

underpin the Company’s earnings for many years to come. The first full year of

production exceeded initial guidance and met subsequently updated guidance. In

general, the achieved production grade has outperformed expectations whilst ore and

concentrate production volumes have met or exceeded estimates.

Altona has reviewed its activities in light of the recent fall in metal prices. Early stage

exploration activities at Roseby have been reduced and a focus placed on cost and

capital management. Our aim is to maximise our cash position. Remaining financially

strong in current market conditions is both prudent and more likely to bring

opportunity.

Production Guidance and Outlook for FY2014

This year the Company will focus on:

1. Updating the mine plan to incorporate recent high grade drilling, current metal

prices and new mining strategies.

2. Completing major infrastructure projects at Outokumpu; main access decline and

Cobalt-Nickel concentrate storage facility.

3. Optimising costs and production at Outokumpu.

4. Evaluating the potential for longer mine life or expanded production at

Outokumpu.

Higher

production

guidance for

FY2014, the

first year of full

production

Production guidance for FY2014 has been raised from that given for FY2013 and is

expected to be slightly below life of mine reserve grade but at design throughput rate

of 550,000 tonnes per annum. Grades are scheduled to improve in subsequent years.

The guidance is tabulated on the next page. It should be noted that there is upside

risk to these forecasts from the potential to include in the mine plan recently

discovered higher grades in the Wallaby-Wombat gap.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

4.

Guidance

increased for

FY2014

Production Guidance and Assumptions Adopted for 2013/2014

Ore tonnes 525,000-570,000 tonnes

Copper grade 1.45-1.60%

Gold grade 0.60-0.70g/t

Copper metal in concentrate 7,600-8,400 tonnes

Gold in concentrate 8,000-9,000 ounces

Zinc metal in concentrate 1,600-1,700 tonnes

C1 cash costs per pound payable copper (after credits) US$1.70-1.85/lb copper

Copper price assumption US$3.15/lb

Gold price assumption US$1,250/ounce

Zinc price assumption US$0.85/lb

Euro:USD exchange rate 1.32

All capital expenditure is currently under review for opportunities to defer or delay

expenditure. Guidance for sustaining and other capital expenditure is €14-16 million.

C1 cash cost

guidance of

US$1.70-

US$1.85 per

pound

C1 cash costs are expected to be similar to or slightly above this year at US$1.70-

US$1.85 per pound. This is in the context of a lower planned head grade, lower

credits due to lower forecast gold prices, forecast stronger Euro and higher treatment

charges/refining charges (“TC/RC”). As the head grade improves, the C1 cash cost

will reduce.

Outokumpu Operations

The fourth

quarter of

production

closes a

satisfying first

full financial

year as a

producer

Outokumpu Project Production Statistics

This

Quarter

Year to

Date

Ore mined Tonnes 129,740 544,249

Copper (%) 1.38 1.63

Gold (g/t) 0.54 0.61

Zinc (%) 0.58 0.58

Ore milled Tonnes 135,000 542,704

Copper (%) 1.46 1.61

Gold (g/t) 0.57 0.64

Zinc (%) 0.59 0.64

Recovery Copper (%) 91.5 91.1

Gold (%) 73.3 73.2

Zinc (%) 48.4 43.4

Contained metal in concentrates Copper (tonnes) 1,809 7,955

Gold (ounces) 1,821 8,192

Zinc (tonnes) 382 1,508

Sales

Copper concentrate delivered Tonnes 8,428 36,892

Contained metal Copper (tonnes) 1,813 8,012

Gold (ounces) 1,822 8,299

Zinc concentrate delivered Tonnes 829 3,353

Contained metal Zinc (tonnes) 410 1,523

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

5.

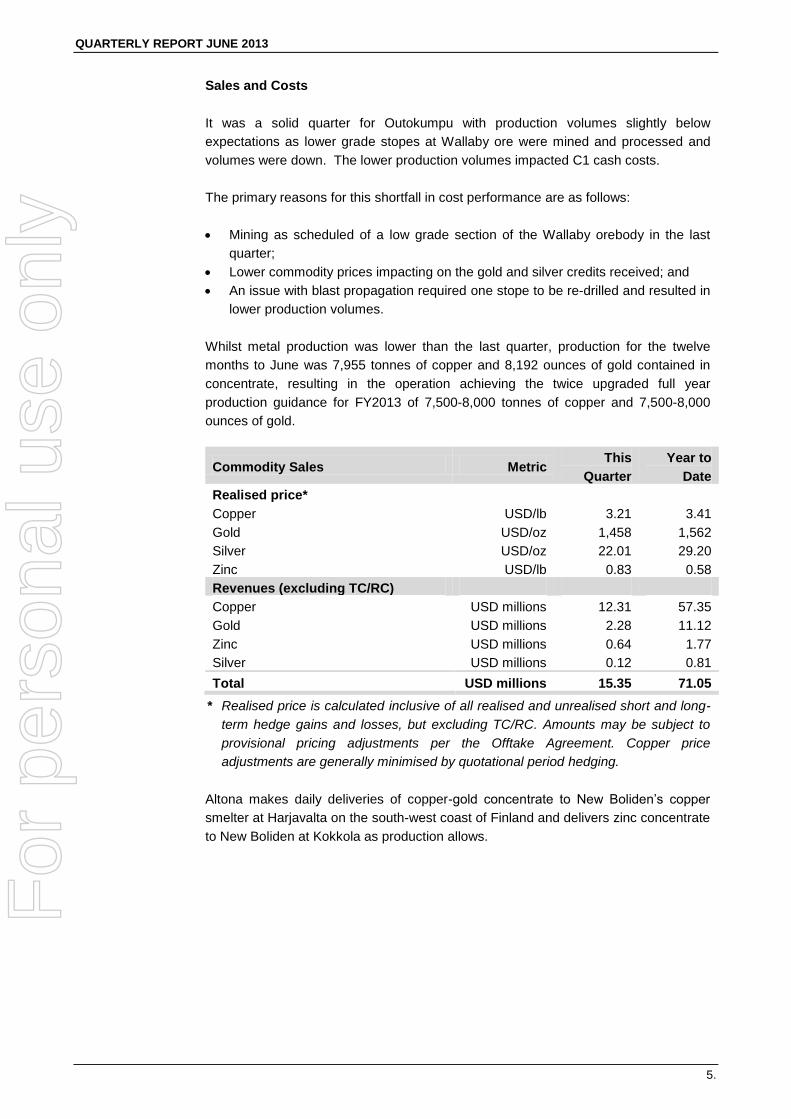

Sales and Costs

It was a solid quarter for Outokumpu with production volumes slightly below

expectations as lower grade stopes at Wallaby ore were mined and processed and

volumes were down. The lower production volumes impacted C1 cash costs.

The primary reasons for this shortfall in cost performance are as follows:

Mining as scheduled of a low grade section of the Wallaby orebody in the last

quarter;

Lower commodity prices impacting on the gold and silver credits received; and

An issue with blast propagation required one stope to be re-drilled and resulted in

lower production volumes.

Whilst metal production was lower than the last quarter, production for the twelve

months to June was 7,955 tonnes of copper and 8,192 ounces of gold contained in

concentrate, resulting in the operation achieving the twice upgraded full year

production guidance for FY2013 of 7,500-8,000 tonnes of copper and 7,500-8,000

ounces of gold.

Commodity Sales Metric

This

Quarter

Year to

Date

Realised price*

Copper USD/lb 3.21 3.41

Gold USD/oz 1,458 1,562

Silver USD/oz 22.01 29.20

Zinc USD/lb 0.83 0.58

Revenues (excluding TC/RC)

Copper USD millions 12.31 57.35

Gold USD millions 2.28 11.12

Zinc USD millions 0.64 1.77

Silver USD millions 0.12 0.81

Total USD millions 15.35 71.05

* Realised price is calculated inclusive of all realised and unrealised short and long-

term hedge gains and losses, but excluding TC/RC. Amounts may be subject to

provisional pricing adjustments per the Offtake Agreement. Copper price

adjustments are generally minimised by quotational period hedging.

Altona makes daily deliveries of copper-gold concentrate to New Boliden’s copper

smelter at Harjavalta on the south-west coast of Finland and delivers zinc concentrate

to New Boliden at Kokkola as production allows.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

6.

Cash costs

reflect lower

grades and

volumes

Quarterly Production of Metal in Concentrate and Cash Cost by Quarter

*C1 cash cost calculated per Brook Hunt methodology. The cash cost data during the

commissioning period (Q1, Q2 2012) is not meaningful.

Cost performance for the full year, including 3 months where production was still

ramping up to design, was pleasing. Year to date costs of US$1.69 per pound fall just

outside the upgraded guidance range of US$1.40-1.60 per pound.

Cost Performance

This

Quarter

(US$M)

This

Quarter

(US$/lb)

Year

to Date

(US$/lb)

Mining costs 5.64 1.46 1.16

Ore trucking costs 0.84 0.22 0.21

Site processing costs 3.12 0.81 0.68

TC/RC and transport 1.46 0.37 0.34

Other cash costs 0.47 0.12 0.12

Net gold, silver and zinc credits * (2.90) (0.75) (0.82)

C1 Cash cost per pound payable copper 2.23 1.69

Capital expenditure 4.00 1.04 1.06

Financing costs 0.40 0.10 0.08

Total Expenditure (capital and operating) 13.03 3.37 2.83

Note: No royalties are payable in Finland.

* Based on invoiced prices, and excluding hedge settlements (subject to finalisation

of provisional pricing).

Mining

Ore production was below expectations whereas the copper grade of 1.38% was

above the 1.26% planned.

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

2.5

-

500

1,000

1,500

2,000

2,500

3,000

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013

Copper (tonnes) Gold (ounces)

C1 cost (USD/lb)* YTD C1 cost (USD/lb)*

Left Scale: Right Scale:

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

7.

Some six stopes were completed and filled during the quarter and three new stopes

were open at the end of the period. Reconciliation of mine production to reserve

models and of mine to mill at 99.9% is excellent.

Some 1,132 metres of decline and level development was completed in the quarter

and mine development is now down to 500 metres below surface (400 level).

Capital expenditure for the quarter consisted of approximately US$3.7 million of

decline, level and fresh air shaft development plus US$0.1 million of miscellaneous,

discretionary items.

Targeting mine

developed to

650 metres

deep by end of

FY2014

During FY2014, it is anticipated that the mine will develop from its current depth of

500 metres below surface to 650 metres below surface with the commencement of

mining in the lower Wallaby zone. The current mine plan has the decline reaching its

final depth of 800 metres in 2015. It is expected that mining will persist to greater

depths. The programme of drilling to test for extensions to the mine will commence in

September.

Figure 1: North-south longitudinal section (looking west) of the Kylylahti mine

showing the mine plan, drill drive and zone targeted for additional

resources.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

8.

A new life of mine plan is nearing completion which will incorporate a change in

mining method within the deeper Wombat zone from longitudinal longhole open

stoping to transverse open stoping. This allows for better management of any risk

from regional stress fields deeper in the mine and permits a higher conversion of

resource to reserve. It is expected that a new Reserve estimate will be available in

late August.

Resource Development and Exploration

Drilling depth

extensions to

commence in

September

The lower Wombat Zone is open at depth with the deepest drillhole (OKU-927J)

intersecting 72 metres at 1.8% copper of typical Outokumpu style of mineralisation.

Altona expects to commence drill testing for possible extensions of the Kylylahti mine

at depth in September.

Extensions to

Resources

delineated in

the Wallaby-

Wombat gap

About 6,670 metres of underground definition drilling was completed during the

quarter mostly at the lower levels of the Wallaby orebody in the gap between Wallaby

and the lower Wombat zone.

The Kylylahti deposit comprises two zones, an upper zone termed Wallaby and a

lower zone named Wombat. The gap between these two zones was ill-defined in

surface drilling and has been subject to intensive drilling from underground in the past

few months.

The upper Wallaby zone has been found to be thicker, extend deeper and is

significantly higher grade than the grade of the resource model (1.6-1.8% copper).

The lower Wombat zone has been extended 10-30 metres higher and now overlaps

with the Wallaby zone. Grades are similar to the previous resource model but

thicknesses are much greater.

A gold rich zone has been defined in the hanging wall of the Wallaby zone and

includes some high grades.

Best intersections using a 0.4% copper cut-off are:

11 metres at 4.6% copper in KU-263

11 metres at 3.1% copper in KU-331

15 metres at 4.0% copper in KU-337

7 metres at 4.8% copper in KU-336

11 metres at 16g/t gold (uncut) in KU-182

The drilling is continuing and will be incorporated into a Resource update and the

mine plan.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

9.

New drilling is

in close

proximity to

existing mine

development

and high grade

mineralisation

could be added

to the FY2014

mine plan

The diagram below highlights the extensions and upgrades to the prior resource

model on section 6972 810mN in the gap zone. The drilling demonstrates that the

gap is in fact an overlap due to structural offset of the ore zone.

An update to both Resources and Reserves at 30 June 2013 will be provided in late

August / early September. It is likely that there will be multiple mining zones, both

copper and gold on a number of levels in the gap zone. Current decline development

is adjacent to this zone but level development is yet to expose this ore.

Figure 2: Cross section 6972 810mN showing overlap of upper Wallaby zone with

lower Wombat zone.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

10.

Processing

The Luikonlahti processing plant operated at a rate controlled by ore availability and

delivered a high level of recovery this quarter.

Recoveries

meeting or

exceeding

expectations

Copper recovery of 91.5% for the quarter and copper-gold concentrate grades were

in line with design. Zinc concentrate grade of 49.7% and zinc recovery of 48.4% are

below design of 50% zinc grade and zinc recovery of 50% but have improved from

the previous quarter and are the focus of ongoing optimisation.

Copper concentrates were delivered to our customer in Finland, New Boliden without

incident or penalty.

Securing a low

risk option for

disposal of

sulphide waste

has brought

forward capital

expenditure

The commencement of construction of a new cobalt-nickel concentrate storage dam

this financial year is required to ensure capacity is available in early 2015 when the

current dam will likely be filled. Overall expenditure in FY2014 on this dam and on the

tailings dam is estimated at €3-4 million. Commencement of construction of the new

dam concurrently with scheduled lifts on the existing dam will minimise the risk of

interruption to production. It should be noted that there is considerable value in the

cobalt and nickel metal stored in these dams, metal which remains available for

potential exploitation at a later date.

A suitable location for the new dam has been identified and land acquisition and

permitting activities have commenced. Engineering and cost estimates for stage 1 of

the new dam are nearing completion and land clearance activities have commenced.

It was intended to complete a detailed study on expanding mill capacity from 550,000

tonnes per annum to 800,000 tonnes per annum in 2013. The approximate capital

cost of an expansion was estimated in scoping studies at €7 million and the

expansion was tentatively planned for mid-2014 upon completion of deep drilling to

identify additional ore reserves. The study and the potential expansion have been

deferred and timing will be reviewed in early 2014.

A permit to allow processing above the permitted rate of 550,000 tonnes per annum is

in the regulatory approval process. The permit was expected to be available in late

2013, but amendments to the regulatory environment have changed this estimate to

early 2014.

Expansion

remains under

consideration

A study of the potential to expand production and de-bottleneck the plant is

underway. However, activity has been slowed due to delays in the permitting process

and that the results of resource extension drilling will not be available until late 2013.

Little Eva Project

Little Eva has

mining and

environmental

permits in

place and a

completed DFS

A Definitive Feasibility Study (“DFS”) on the 100% owned Little Eva Copper-Gold

Project, 90 kilometres north-east of Mt Isa in Queensland, Australia was completed in

May 2012. The Project is 11 kilometres north of MMG’s $1.2 billion Dugald River zinc

mine. The Dugald River project is now under construction.

The fully permitted Little Eva Project is part of Altona’s larger Roseby Project and

represents the first stage of the development of the large resource inventory at

Roseby.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

11.

Partnering

process

proceeding

slowly

The process to sell, partner or finance the Little Eva project attracted considerable

initial interest. However, against a background of challenging debt and equity

markets and poor sentiment, no proposal likely to add value for shareholders has

emerged. Altona is continuing discussions with a number of parties.

Roseby is a strategic asset. The Little Eva mine is a fully permitted development

opportunity for a 40,000 tonne per annum copper mine which retains considerable

upside.

In the meanwhile, a number of initiatives have been launched to reduce costs and

realise value from efforts taken to date. These include:

Reduction of early stage exploration activity at Roseby.

Closure of the Cloncurry exploration office, and the reduction in exploration staff.

Technical work will focus on updating and optimising all resource and reserve

models following 2 years of intense drilling activity.

There is no compulsion on Altona to act quickly on realising value from the Roseby

asset and value will remain the principal driver in our commercial discussions with

potential partners, acquirers and financiers.

Roseby Exploration

A major

regional

exploration

RAB

programme

was completed

A major regional reconnaissance drilling programme of 6,223 metre Rotary Air Blast

(“RAB”) drilling for 1,012 shallow holes was completed at Roseby. The programme

was designed to test high value exploration targets which have potential to deliver

additional copper sulphide ore feed to Little Eva. Results are shown on Figures 3, 4

and 5.

The Companion/Brolga target is 30 kilometres south of Little Eva and is a 7 kilometre

long north-south trending zone of small artisanal historic copper workings,

outcropping oxide copper mineralisation (with rare visible gold) and high grade rock

chip samples ranging up to 10-26% copper and 25g/t gold in value. Prior drilling is

very sparse (only 4 holes) returning intersections up to 7.5 metres at 0.9% copper.

Shallow RAB drilling at 25 or 50 metre spacing along 400-800 metre line spacing

returned numerous anomalies results up to 1.16% copper. Maximum single sample

copper assay highlights include:

3 metres at 1.16 % (CPB041)

3 metres at 0.96 % (CPB040)

3 metres at 0.61 % (CPB051)

The Green Hill target is a possible continuation of the mineralised trends which hosts

the Bedford deposit and Turkey Creek prospect. The target is marked by numerous

artisanal historic workings, rock chips and soil anomalies coincident with magnetic

and/or radiometric anomalies.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

12.

Shallow RAB drilling at 25 or 50 metre spacing along 400 metre line spacing defined

several copper anomalies 50-75 metres wide on a number of lines. Maximum single

sample copper assay highlights include:

2 metres at 0.97 % (GHB171)

1 metres at 0.73 % (GHB017)

3 metres at 0.60 % (GHB169)

3 metres at 0.59 % (GHB170)

Whilst a number of targets for follow up have been generated, no immediate drilling is

planned for the balance of this field season.

Corporate

Cash

Strong cash

balance with

A$31.8 million

in cash,

receivables

and stocks

The Company has A$26.09 million in cash, receivables from concentrate sales of

A$5.00 million and inventories of A$0.75 million. A$2.10 million is also held in cash

as security for environmental performance. The cash balance has increased from the

prior quarter. Cash movements for the quarter are tabulated below.

Quarterly Cashflow (June quarter) A$ (millions)

Opening cash 22.59

Proceeds from concentrate sales 21.99

Outokumpu operating costs (12.11)

Sustaining capital expenditure * (6.67)

Other capital expenditure (0.17)

Debt service (0.46)

Roseby activities (1.31)

Overheads/Corporate (1.46)

Interest received and other ** 3.69

Closing cash position 26.09

* Sustaining capital includes mine decline development and tailings dam costs etc.

** Other includes exchange rate adjustments.

Please note an Appendix 5B disclosure as required by ASX for exploration entities is

enclosed. The forecast cash expenditure for the next quarter required in that form

excludes all revenues and does not reflect net cash outflow.

Debt

The Company has debt of US$20.4 million with Credit Suisse. Principal repayments

commence in March 2014. The loan will be fully paid by 30 June 2016. The

Company also has €1.8 million of finance lease for mining equipment.

Hedging

The Company has copper, gold and zinc hedging denominated in Euros. Deliveries

into the hedge book this quarter were 540 tonnes of copper at €5,575 per tonne, 873

ounces of gold at €1,190 per ounce and 201 tonnes of zinc at €1,475 per tonne.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

13.

The schedule of outstanding metal deliveries is given below.

Year ended

30 June

Copper

(t)

Copper

(€/t)

Gold

(oz)

Gold

(€/oz)

Zinc

(t)

Zinc

(€/t)

2014 2,832 5,656 5,000 1,191 795 1,479

2015 2,946 5,656 5,004 1,191 804 1,479

2016 3,264 5,656 5,003 1,191 809 1,479

Total 9,042 14,999 2,408

Hedge book

has positive

value of €7.8

million

At the time of writing, the copper price was €5,310 per tonne and the gold price €978

per ounce.

The mark to market value of the hedge book at 30 June 2013 is €7.8 million.

The Company also undertakes short-dated (3 months) hedging to secure revenue for

the period (Quotational Period) between the receipt of the provisional invoice for

concentrate sales and the final pricing. Realised and unrealised gains and losses on

Quotational Period hedging have been included in the realised prices per commodity

shown in page 5. Altona has recorded a gain of US$1.33 million on these hedges for

the quarter.

Share Price Activity on ASX

Quarter open 0.22¢

High 0.22¢

Low 0.13¢

Quarter close 0.14¢

Average daily volume 448,257

Competent Persons Statement

The information in this report that relates to Exploration Targets, Exploration Results,

Mineral Resources or Ore Reserves is based on information compiled by Dr Alistair

Cowden BSc (Hons), PhD, MAusIMM, MAIG, Mr Jarmo Vesanto MSc, MAusIMM, Mr

Jani Impola, MSc, MAusIMM and Mr Jari Juurela MSc, MAusIMM. Dr Cowden, Mr

Vesanto, Mr Impola and Mr Juurela are full time employees of the Company and have

sufficient experience which is relevant to the style of mineralisation and type of

deposit under consideration and to the activity being undertaking to qualify as a

Competent Person as defined in the 2012 Edition of the ‘Australasian Code for

Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Dr Cowden,

Mr Vesanto, Mr Impola and Mr Juurela consent to the inclusion in the report of the

matters based on their information in the form and context in which it appears.

Please direct

enquiries to:

Alistair Cowden James Harris

Managing Director Professional Public Relations

Tel: +61 8 9485 2929 Tel: +61 8 9388 0944

[email protected] [email protected]

Jochen Staiger

Swiss Resource Capital AG - Germany

Tel: +41 71 354 8501

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

14.

Figure 3: Location of RAB drilling completed this quarter at the Roseby Project.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

15.

Figure 4: Results of RAB drilling at the Companion and Brolga areas.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

16.

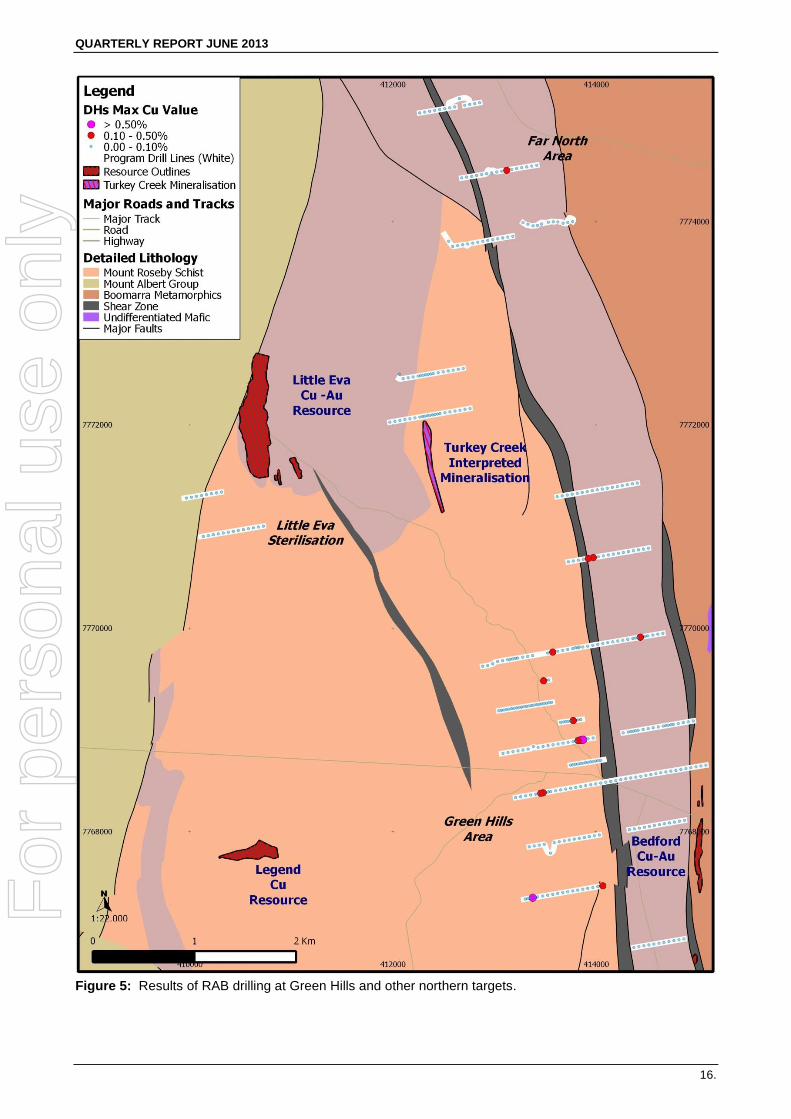

Figure 5: Results of RAB drilling at Green Hills and other northern targets.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

17.

Table 1: Resource Estimates for the Roseby Project

DEPOSIT

TOTAL CONTAINED

MEASURED INDICATED INFERRED METAL

Tonnes Grade Copper Gold Tonnes Grade Tonne Grade Tonnes Grade

million Cu Au

tonnes ounces million Cu Au

million Cu Au

million Cu Au

% g/t % g/t % g/t % g/t

Copper-Gold Deposits

Little Eva 100.3 0.54 0.09 538,000 271,000 36.3 0.63 0.08 41.4 0.48 0.08 22.6 0.49 0.11

Ivy Ann 7.5 0.57 0.07 43,000 17,000 5.4 0.60 0.08 2.1 0.49 0.06

Lady Clayre 14.0 0.56 0.20 78,000 85,000 3.6 0.60 0.24 10.4 0.54 0.18

Bedford 1.7 0.99 0.20 17,000 11,000 1.3 1.04 0.21 0.4 0.83 0.16

Sub-total 123.4 0.55 0.10 675,000 384,000 36.3 0.63 0.08 51.7 0.52 0.09 35.5 0.51 0.13

Copper Only Deposits

Blackard 76.4 0.62 475,000 27.0 0.68 6.6 0.60 42.7 0.59

Scanlan 22.2 0.65 143,000 18.4 0.65 3.8 0.60

Longamundi 10.4 0.66 69,000 10.4 0.66

Legend 17.4 0.54 94,000 17.4 0.54

Great Southern 6.0 0.61 37,000 6.0 0.61

Caroline 3.6 0.53 19,000 3.6 0.53

Charlie Brown 0.7 0.40 3,000 0.7 0.40

Sub-total 136.7 0.61 840,000 27.0 0.68 25.0 0.64 84.7 0.59

TOTAL 260.1 0.58 0.05 1,515,000 384,000 63.2 0.65 0.05 76.7 0.55 0.06 120.1 0.56 0.04

See ASX release of 26 July 2011, 19 December 2011, 23 April 2012, 3 July 2012 and 22 August 2012 for full details of resource estimation methodology and

attributions. It is Altona’s view that the estimates for Little Eva, Bedford, Ivy Ann, Lady Clayre, Legend and Blackard deposits have full Table 1 disclosure

and whilst disclosed prior to the adoption of JORC 2012 comply with that edition of the Code. The remainder of the deposits are compliant with JORC 2004.

Note: All figures may not sum exactly due to rounding.

Little Eva is reported above a 0.2% copper lower cut-off grade, all other deposits are above 0.3% copper lower cut-off grade.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

18.

Table 2: Kylylahti Resource Estimate - December 2012

Tonnes

(m)

Cu

(%)

Au

(g/t)

Zn

(%)

Co

(%)

Ni

(%)

Measured 1.2 1.50 0.71 0.60 0.27 0.20

Indicated 6.4 1.22 0.69 0.55 0.23 0.21

Inferred 0.3 0.97 0.57 0.70 0.24 0.18

TOTAL 7.9 1.25 0.69 0.56 0.23 0.20

Metal Tonnes

99,050 175,750oz 44,250 18,550 16,200

See ASX release dated 9 April 2013 for JORC 2012 Compliance.

Table 3: Kylylahti Ore Reserves, December 2012

Tonnes

(m)

Cu

(%)

Au

(g/t)

Zn

(%)

Co

(%)

Ni

(%)

Probable Ore Reserves 3.6 1.69 0.66 0.67 0.26 0.14

Metal Tonnes

60,500 76,100oz 24,000 9,400 5,000

See ASX release dated 9 April 2013 for JORC 2012 Compliance.

Table 4: Outokumpu Resources, December 2012

Deposit Classification Tonnes

(m)

Cu

(%)

Au

g/t

Zn

(%)

Co

(%)

Ni

(%)

Kylylahti

Measured 1.19 1.50 0.71 0.60 0.27 0.20

Indicated 6.40 1.22 0.69 0.55 0.23 0.21

Inferred 0.31 0.97 0.57 0.70 0.24 0.18

Total 7.91 1.25 0.69 0.56 0.23 0.20

Saramäki Inferred 3.40 0.71 - 0.63 0.09 0.05

Vuonos Inferred 0.76 1.76 - 1.33 0.14 -

Hautalampi

Measured 1.03 0.47 - 0.06 0.13 0.47

Indicated 1.23 0.30 - 0.07 0.11 0.42

Inferred 0.90 0.30 - 0.10 0.10 0.40

Total 3.16 0.36 - 0.07 0.11 0.43

Riihilahti Indicated 0.14 1.69 - - 0.04 0.16

Valkeisenranta Indicated 1.54 0.29 - - 0.03 0.71

Särkiniemi Indicated 0.10 0.35 - - 0.05 0.70

Sarkalahti Inferred 0.19 0.33 - - - 1.02

TOTAL 17.20 0.90 0.32 0.45 0.15 0.26

See Vulcan ASX Release of 16 November 2009 for JORC 2004 compliance for deposits other than Kylylahti.

This release can be found on the Finland Resource and Reserve Estimates page of Altona’s website.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

19.

APPENDIX 5B

Mining Exploration entity quarterly report Name of entity

ALTONA MINING LIMITED

ABN Quarter ended (“current quarter”)

35 090 468 018 30 June 2013

Consolidated statement of cash flows

Cash flows related to operating activities

Current Quarter (3 months) A$’000

Year to Date (12 months)

$A’000

1.1 Receipts from product sales and related debtors 21,990 77,194

1.2 Payments for (a) exploration and evaluation (1,314) (5,999)

(b) development (net of grant received) * (5,187) (18,148)

(c) production (12,109) (40,898)

(d) administration (1,457) (7,072)

1.3 Dividends received - -

1.4 Interest and other items of a similar nature received 215 712

1.5 Interest and other costs of finance paid (460) (1,260)

1.6 Income taxes rebate - -

1.7 Other** 1,320 1,103

Net Operating Cash Flows 2,998 5,632

Cash flows related to investing activities

1.8 Payment for purchases of: (a) prospects - -

(b) equity investments - -

(c) other fixed assets (1,650) (7,692)

1.9 Proceeds from sale of: (a) prospects - -

(b) equity investments - -

(c) other fixed assets - -

1.10 Loans to other entities - -

1.11 Loans repaid by other entities - -

1.12 Other - -

Net investing cash flows (1,650) (7,692)

1.13 Total operating and investing cash flows (carried forward) 1,348 (2,060)

* Mine development expenditure have be re-classified to this category for the year-to-date following clarification from the ASX.

** Proceeds from sale of assets, Quotational Period hedges and bonds and security deposits

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

20.

Cash flows related to financing activities

1.14 Proceeds from issues of shares (net of costs) - -

1.15 Proceeds from sale of forfeited shares - -

1.16 Proceeds from borrowings - -

1.17 Repayment of borrowings - -

1.18 Dividends paid - -

1.19 Other - -

Net financing cash flows - -

Net increase (decrease) in cash held 1,348 (2,060)

1.20 Cash at beginning of quarter/year 22,587 26,711

1.21 Exchange rate adjustments to 1.20 2,158 1,442

1.22 Cash at end of quarter 26,093 26,093

Payments to directors of the entity and associates of the directors Payments to related entities of the entity and associates of the related entities

Current quarter

$A’000

1.23 Aggregate amount of payments to the parties included in item 1.2

336

1.24 Aggregate amount of loans to the parties included in item 1.10

-

1.25 Explanation necessary for an understanding of the transactions

Payment of directors’ fees, salaries and superannuation to the directors during the quarter.

Non-cash financing and investing activities 2.1 Details of financing and investing transactions which have had a material effect on consolidated

assets and liabilities but did not involve cash flows

N/A

2.2 Details of outlays made by other entities to establish or increase their share in projects in which the

reporting entity has an interest

N/A

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

21.

Financing facilities available Add notes as necessary for an understanding of the position.

Amount available $A’000

Amount used $A’000

3.1 Loan facilities(*) - 22,359

3.2 Credit standby arrangements - -

(*) The Credit Suisse debt facility of US$20 million has been fully drawn down. Estimated cash outflows for next quarter (excluding any proceeds from concentrate sales and other income)

$A’000

4.1 Evaluation/Exploration (1,236)

4.2 Development (4,560)

4.3 Production (12,287)

4.4 Administration (2,181)

Total (20,264)

Reconciliation of Cash

Reconciliation of cash at the end of the quarter (as shown in the consolidated statement of cash flows) to the related items in the accounts is as follows.

Current quarter $A’000

Previous quarter $A’000

5.1 Cash on hand and at bank 18,534 11,567

5.2 Deposits at call 7,559 11,020

5.3 Bank overdraft - -

5.4 Other (provide details) - -

Total: cash at end of quarter (item 1.22) 26,093 22,587

Changes in interests in mining tenements

6.0 See attached Schedule A. For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

22.

Issued and quoted securities at end of current quarter

Total number Number quoted

Issue price per security

Amount paid up per security

7.1 Preference securities (description)

- - - -

7.2 Changes during quarter

- - - -

7.3 Ordinary securities

528,992,704 528,992,704 - -

7.4 Changes during quarter - Issued

55,000 55,000 - -

7.5 Converting debt Securities (description and conversion factor)

- - - -

7.6 Changes during quarter

- - - -

7.7 Options (description and conversion factor)

365,000 1,000,000

9,677,749^

- -

Exercise Price

$1.50 $0.44

-

Expires

30 June 2013 18 November 2013

(various)

7.8 Issued during quarter

- - - -

7.9 Exercised during quarter

55,000^ - - -

7.10 Expired during quarter

60,000^ - -

-

7.11 Debentures (totals only)

- - - -

7.12 Unsecured notes (totals only)

- - - -

^ Share rights issued pursuant to approved Employee Share Scheme. These Share Rights form part of the Long Term

Incentive Scheme in compliance with Altona’s Remuneration Policy. The Share Rights have various expiry dates and performance hurdles.

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

23.

Compliance statement

1. This statement has been prepared under accounting policies which comply with accounting standards

as defined in the Corporations Law or other standards acceptable to ASX.

2. This statement does give a true and fair view of the matters disclosed.

Sign here: Date: 29 July 2013

Company Secretary

Print Name: Eric Hughes

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

24.

SCHEDULE A

FINNISH MINING TENEMENTS

Interests in mining tenements relinquished, reduced or lapsed during the quarter.

Three eight-year (original five-year and additional three-year) Kylylahti Copper’s claims with mining register

numbers 7976/1-3 will expire in July 2013. A combined three year extension application, Kokonvaara was

submitted to cover all three expiring claims. The combined area of the claims was reduced to meet the new

Mining Act requirements.

Interests in mining tenements acquired or increased during the quarter

Five new claims were granted for Kylylahti Copper Oy. Kokka 2-6 claims cover the historic Outokumpu style

Kokka deposit and surrounds. Claims cover a total area of 330 hectares.

A three-year extension to the Vaara claim was granted for Kuhmo Metals Oy.

An application for a 32.5ha expansion to the Luikonlahti auxiliary area was submitted during the quarter. The

area is planned to cover the cobalt-nickel concentrate storage facility.

A new 511 hectares claim application (Perttilahti South) was submitted. The extensive claim area is

designed to cover the area between existing Perttilahti-Kokonvaara claim extensions and lake Viinijärvi SE of

Perttilahti.

Interests in mining tenements at end of the quarter

OUTOKUMPU AREA Mining Licenses

Number Name Holder

3593/1a Kylylahti Kylylahti Copper Oy

3593/1b Kylylahti Kylylahti Copper Oy

3593/1c Kylylahti ML extension Kylylahti Copper Oy

3593/2a Kylylahti 2 Kylylahti Copper Oy 348/1a, 563/1a, 98/13b, 257/1a Hautalampi Vulcan Hautalampi Oy

7975 Riihilahti Kylylahti Copper Oy 553/1a,2a,4a,6a-11a Luikonlahti1-2,4,6-11 Kylylahti Copper Oy

1281/1a-2a Petkel I+ II Kylylahti Copper Oy

2061/1a Petkellahti Kylylahti Copper Oy 553/1a,2a,4a,6a-11a Luikonlahti auxiliary areas Kylylahti Copper Oy 553/1a,2a,4a,6a-11a Luikonlahti auxiliary areas Expansion Kylylahti Copper Oy

Claims Number Name Holder

7799/2 Kylylahti 2 Kylylahti Copper Oy

7799/3 Kylylahti 3 Kylylahti Copper Oy

7799/4 Kylylahti 4 Kylylahti Copper Oy

7914/1 Saramäki 1 Kylylahti Copper Oy

7906/1 Perttilahti 1 Kylylahti Copper Oy

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

25.

7906/2 Perttilahti 2 Kylylahti Copper Oy

7906/3 Vuonos 1 Kylylahti Copper Oy

7906/4 Vuonos 2 Kylylahti Copper Oy

7906/5 Vuonos 3 Kylylahti Copper Oy

8393/1 Polvikoski 1 Kylylahti Copper Oy

8393/2 Polvikoski 2 Kylylahti Copper Oy

8393/3 Kylylahti 6 Kylylahti Copper Oy

8394/1 Saramäki 2 Kylylahti Copper Oy

8525/1 Sukkula 1 Kylylahti Copper Oy

8525/2 Sukkula 2 Kylylahti Copper Oy

7976/1 Kokonvaara Kylylahti Copper Oy

7976/2 Perttilahti1 Kylylahti Copper Oy

7976/3 Perttilahti2 Kylylahti Copper Oy

8623/1 Sivakkavaara 2a Kylylahti Copper Oy

8623/2 Sivakkavaara 2b Kylylahti Copper Oy

8623/3 Sivakkavaara 3 Kylylahti Copper Oy

8974/1 Kokka 2 Kylylahti Copper Oy

8974/2 Kokka 3 Kylylahti Copper Oy

8974/3 Kokka 4 Kylylahti Copper Oy

8974/4 Kokka 5 Kylylahti Copper Oy

9106/1 Kokka 6 Kylylahti Copper Oy

Perttilahti South Kylylahti Copper Oy

Reservations Number Name Holder

VA2011:0001 Ala-Penikka Kylylahti Copper Oy

VA2012:0188 Miihkali Kylylahti Copper Oy

VA2012:0189 Saramäki-South Kylylahti Copper Oy

KUHMO JOINT VENTURE

Mining Licenses Number Name Holder

7014 Hietaharju Kuhmo Metals Oy

7922 Peura-aho Kuhmo Metals Oy

Claims Number Name Holder

Saarikylä belt

ML2012:0047 Vaara Kuhmo Metals Oy

8049/1 Kotisuo Kuhmo Metals Oy

8049/2 Kauniinlampi Kuhmo Metals Oy

8049/3 Hoikkalampi Kuhmo Metals Oy

8049/4 Rytys Kuhmo Metals Oy

8049/5 Vaara North Kuhmo Metals Oy

8396/1 Hoikka Kuhmo Metals Oy

8618/1 Hakovaara Kuhmo Metals Oy

8602/1 Vaara West Kuhmo Metals Oy

Kiannanniemi

7922/1 Peura-aho Kuhmo Metals Oy

8033/3 Peura-aho North Kuhmo Metals Oy

8033/1 Peura-aho East Kuhmo Metals Oy

8033/2 Peura-aho NE Kuhmo Metals Oy

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

26.

8033/5 Peura-aho SW Kuhmo Metals Oy

8033/4 Peura-aho South Kuhmo Metals Oy

8618/3 Myllyaho 1 Kuhmo Metals Oy

8618/4 Myllyaho 2 Kuhmo Metals Oy

8745/1 Hietaharju North Kuhmo Metals Oy

Huutoniemi

8476/1 Huutoniemi 1 Kuhmo Metals Oy

8476/2 Huutoniemi 2 Kuhmo Metals Oy

8476/3 Huutoniemi 3 Kuhmo Metals Oy

8476/4 Huutoniemi 4 Kuhmo Metals Oy

Moisiovaara

8047/4 Luokkivaara Kuhmo Metals Oy

8055/1 Luokkipuro Kuhmo Metals Oy

8055/2 Hyyrylainen Kuhmo Metals Oy

8049/7 Sika-aho Kuhmo Metals Oy

8049/8 Paatola Kuhmo Metals Oy

8049/9 Likosuo Kuhmo Metals Oy

8049/10 Karsikkosuo Kuhmo Metals Oy

8049/11 Lehdonmaa Kuhmo Metals Oy

8049/12 Harju Kuhmo Metals Oy

8049/13 Yhteisenaho Kuhmo Metals Oy

8049/14 Selkajarvi Kuhmo Metals Oy

8049/15 Kaartilanvaara Kuhmo Metals Oy

8049/16 Kaivolampi Kuhmo Metals Oy

8049/17 Paatolaislampi Kuhmo Metals Oy

8233/1 Kinnula Kuhmo Metals Oy

8233/2 Kupusenkangas Kuhmo Metals Oy

8242/6 Metsälä Kuhmo Metals Oy

8242/4 Viima-aho Kuhmo Metals Oy

8242/5 Rinneaho Kuhmo Metals Oy

8242/3 Kemppaanlehto Kuhmo Metals Oy

8956/2 Lehdonmaa South Kuhmo Metals Oy

Arola - Harma North

7923/1 Arola Kuhmo Metals Oy

8047/1 Arola South Kuhmo Metals Oy

8047/2 Palovaara South Kuhmo Metals Oy

8047/3 Tiikkaja-aho Kuhmo Metals Oy

8043/1 Kelosuo South Kuhmo Metals Oy

8049/18 Karhujarvi Kuhmo Metals Oy

8049/19 Palovaara Kuhmo Metals Oy

8049/20 Putkisuo Kuhmo Metals Oy

8049/21 Kelosuo Kuhmo Metals Oy

8049/22 Pitkaaho Kuhmo Metals Oy

8242/2 Antinaho Kuhmo Metals Oy

8242/1 Nyberginlehto Kuhmo Metals Oy

8500/1 Korkea-aho 2 Kuhmo Metals Oy

8500/2 Korkea-aho 3 Kuhmo Metals Oy

8762/1 Naurissuo Kuhmo Metals Oy

9412/1 Tiikkaja-aho 2 Kuhmo Metals Oy

8955/1 Kelosuo East Kuhmo Metals Oy

8955/2 Kirnulampi Kuhmo Metals Oy

Kuhmo Area

8055/3 Siivikkovaara Kuhmo Metals Oy

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

27.

8055/4 Niemenkyla Kuhmo Metals Oy

8049/24 Riihilampi Kuhmo Metals Oy

KOTALAHTI AREA NICKEL

Mining Licenses Number Name Holder

6977/1a Särkiniemi Vulcan Kotalahti Oy

7739 Valkeisenranta Vulcan Kotalahti Oy

AUSTRALIAN MINING TENEMENTS Interests in mining tenements relinquished, reduced or lapsed during the quarter A letter of surrender was sent together with Deep Yellow Limited to fully surrender EPM14367-Spider. Interests in mining tenements acquired or increased during the quarter No mining tenements (e.g. EPMs) were acquired during the quarter. Renewal applications for nine (9) greater Roseby Project EPMs and one (1) Queensland Regional Project EPMs are currently being processed by the Queensland DNRM. Correspondence was received from the Queensland DNRM during the June Quarter approving the renewal application for EPM12529-Cabbage Tree. The area under granted EPMs within Queensland presently totals 1,494.0km

2.

Interests in mining tenements at end of the quarter QUEENSLAND – ROSEBY PROJECT Mining Leases (ML)

Number Name Holder

90162 Scanlan Altona Mining Ltd / Roseby Copper Pty Ltd 90163 Longamundi Altona Mining Ltd / Roseby Copper Pty Ltd 90164 Blackard Altona Mining Ltd / Roseby Copper Pty Ltd 90165 Little Eva Altona Mining Ltd / Roseby Copper Pty Ltd 90166 Village Altona Mining Ltd / Roseby Copper Pty Ltd

Exploration Permit for Minerals (EPM)

Number Name Holder

8059 Cameron River Altona Mining Ltd 8506 Mt Roseby Altona Mining Ltd / Roseby Copper Pty Ltd 9056 Pinnacle Altona Mining Ltd / Roseby Copper Pty Ltd 10266 Highway Altona Mining Ltd / Roseby Copper Pty Ltd 10833 Cameron Altona Mining Ltd / Roseby Copper Pty Ltd 11004 Ogorilla Altona Mining Ltd / Roseby Copper Pty Ltd 11611 Gulliver Altona Mining Ltd / Roseby Copper Pty Ltd 12121 Gulliver East Altona Mining Ltd / Roseby Copper Pty Ltd 12492 Queen Sally Altona Mining Ltd / Roseby Copper Pty Ltd 12493 Quamby Altona Mining Ltd / Roseby Copper Pty Ltd 12529 Cabbage Tree Altona Mining Ltd / Roseby Copper Pty Ltd 13249 Lilliput Altona Mining Ltd / Roseby Copper Pty Ltd 14363 Bannockburn Altona Mining Ltd 14365 Corella Altona Mining Ltd 14535 Roseby Infill Altona Mining Ltd / Roseby Copper Pty Ltd 14556 Coolullah Altona Mining Ltd 14822 River Gum Altona Mining Ltd 18784 Roseby East Roseby Copper Pty Ltd 18983 Coolullah North Roseby Copper Pty Ltd

For

per

sona

l use

onl

y

QUARTERLY REPORT JUNE 2013

28.

QUEENSLAND – REGIONAL PROJECTS Exploration Permit for Minerals (EPM)

Number Name Holder

9611 Happy Valley Altona Mining Ltd 14367 Spider Altona Mining Ltd (49%) / Deep Yellow Limited (51%) 14370 Malakoff Altona Mining Ltd 14371 Mt. Angelay Altona Mining Ltd

For

per

sona

l use

onl

y