Embed Size (px)

Citation preview

Q1 2012

Q1 2012 1

To get back,

Agenda

Q1 highlights

Online classifieds

Media houses

Income statement and Financials

Schibsted Sverige

Outlook

2

Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

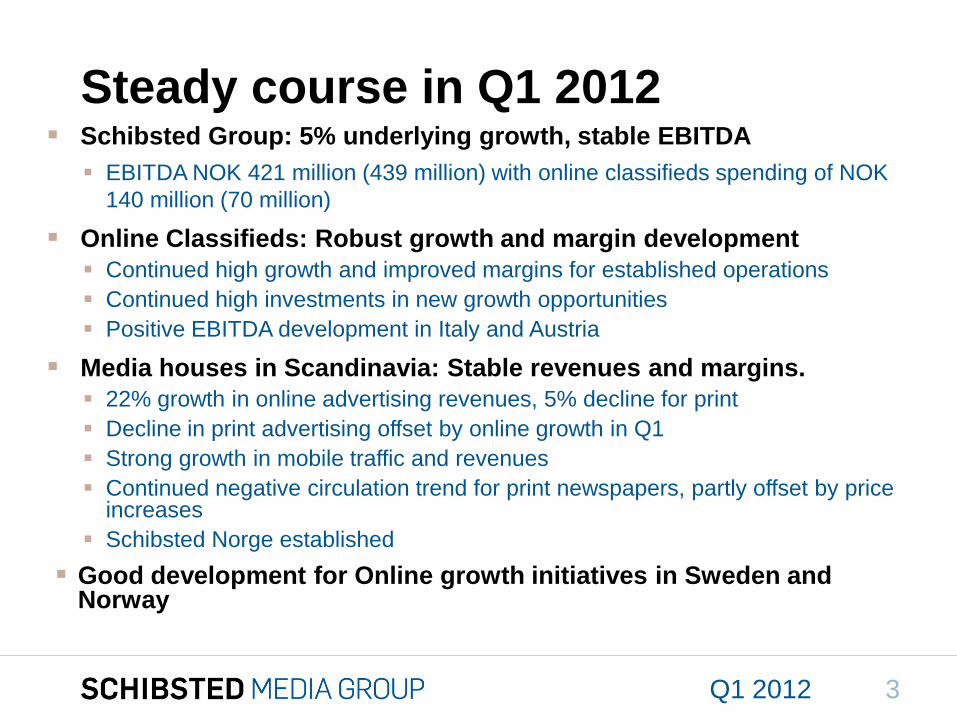

Schibsted Group: 5% underlying growth, stable EBITDA

EBITDA NOK 421 million (439 million) with online classifieds spending of NOK

140 million (70 million)

Online Classifieds: Robust growth and margin development

Continued high growth and improved margins for established operations

Continued high investments in new growth opportunities

Positive EBITDA development in Italy and Austria

Media houses in Scandinavia: Stable revenues and margins.

22% growth in online advertising revenues, 5% decline for print

Decline in print advertising offset by online growth in Q1

Strong growth in mobile traffic and revenues

Continued negative circulation trend for print newspapers, partly offset by price increases

Schibsted Norge established

Good development for Online growth initiatives in Sweden and Norway

Steady course in Q1 2012

Q1 2012 3

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

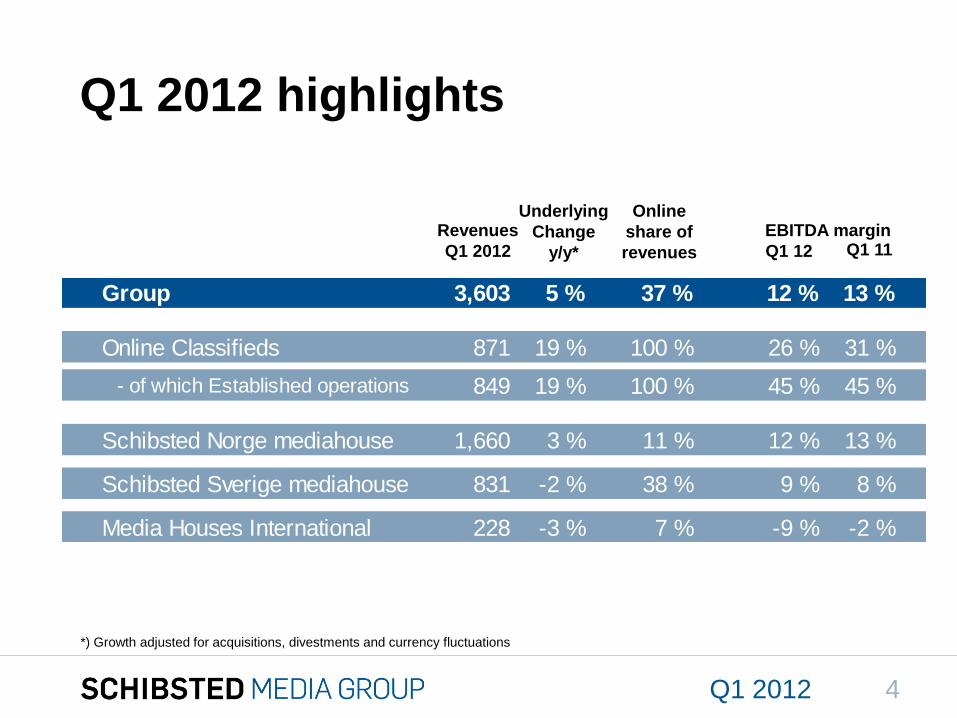

Q1 2012 highlights

Revenues

Q1 2012

EBITDA margin

Q1 12 Q1 11

Underlying

Change

y/y*

*) Growth adjusted for acquisitions, divestments and currency fluctuations

Q1 2012

Online

share of

revenues

Group 3,603 5 % 37 % 12 % 13 %

Online Classifieds 871 19 % 100 % 26 % 31 %

- of which Established operations 849 19 % 100 % 45 % 45 %

Schibsted Norge mediahouse 1,660 3 % 11 % 12 % 13 %

Schibsted Sverige mediahouse 831 -2 % 38 % 9 % 8 %

Media Houses International 228 -3 % 7 % -9 % -2 %

4

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

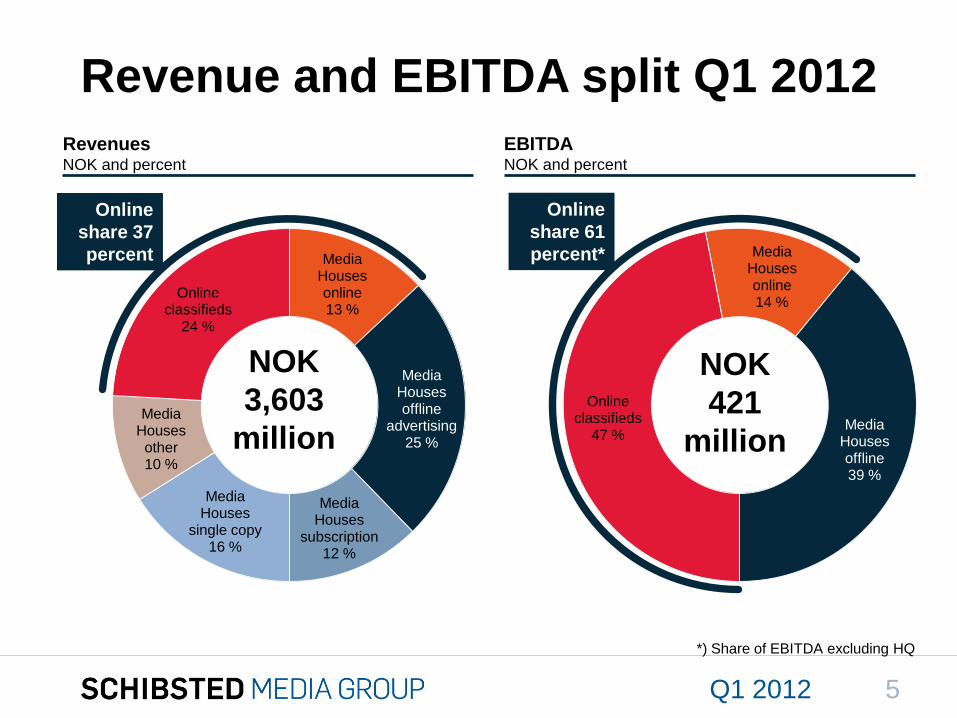

Media Houses online13 %

Media Houses offline

advertising25 %

Media Houses

subscription12 %

Media Houses

single copy16 %

Media Houses other10 %

Online classifieds

24 %

Online classifieds

47 %

Media Houses online14 %

Media Houses offline39 %

Revenue and EBITDA split Q1 2012

*) Share of EBITDA excluding HQ

Online

share 61

percent*

Online

share 37

percent

RevenuesNOK and percent

EBITDANOK and percent

NOK

3,603

million

NOK

421

million

Q1 2012 5

To get back,

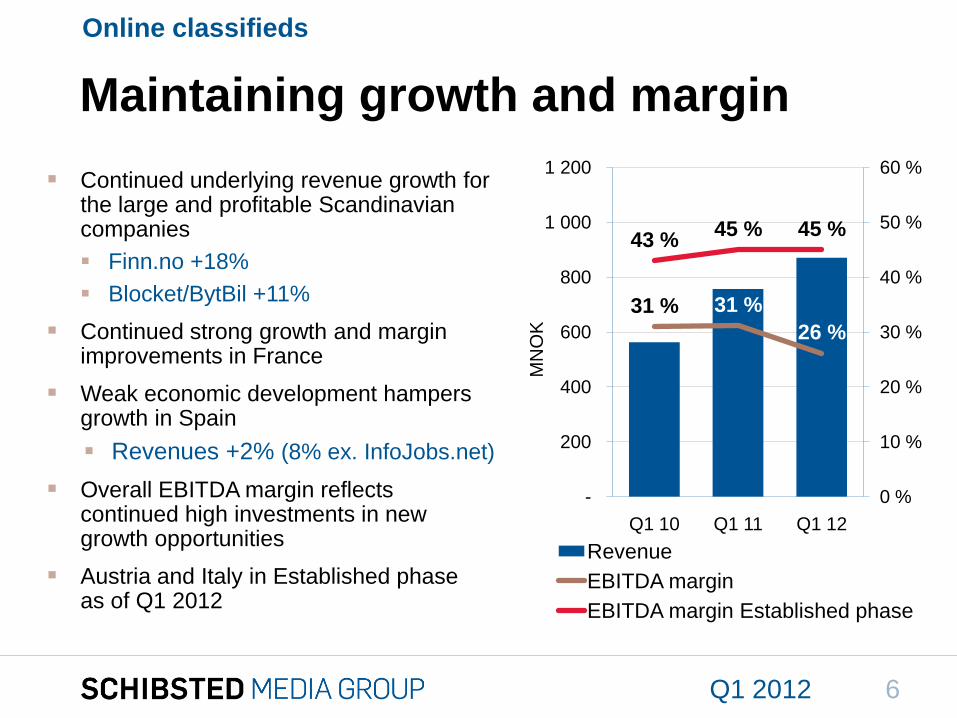

Maintaining growth and margin

Continued underlying revenue growth for the large and profitable Scandinavian companies

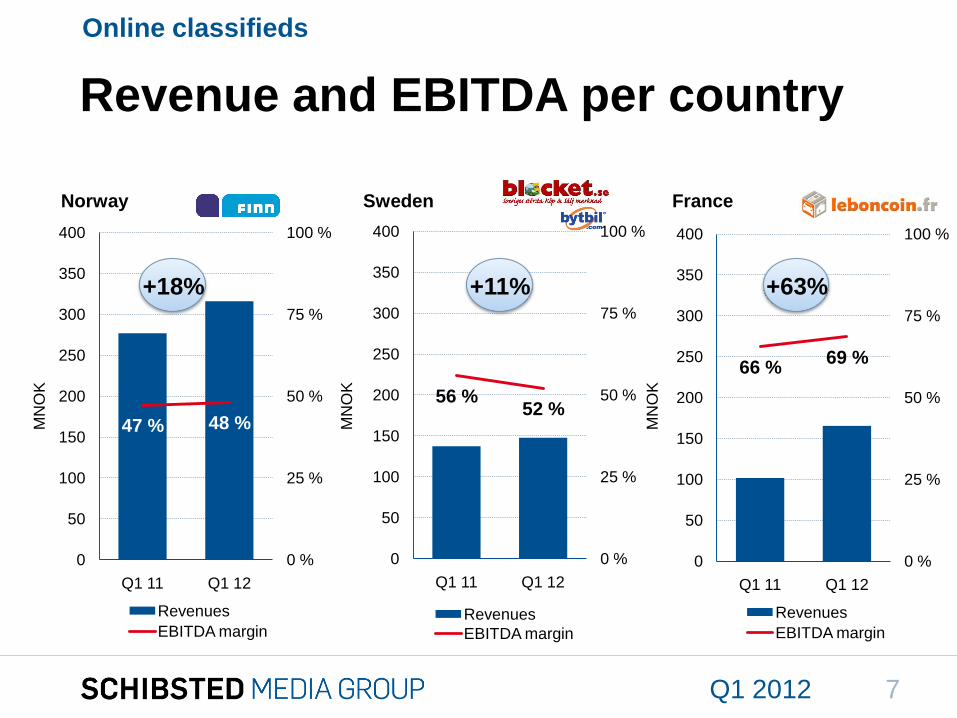

Finn.no +18%

Blocket/BytBil +11%

Continued strong growth and margin improvements in France

Weak economic development hampers growth in Spain

Revenues +2% (8% ex. InfoJobs.net)

Overall EBITDA margin reflects continued high investments in new growth opportunities

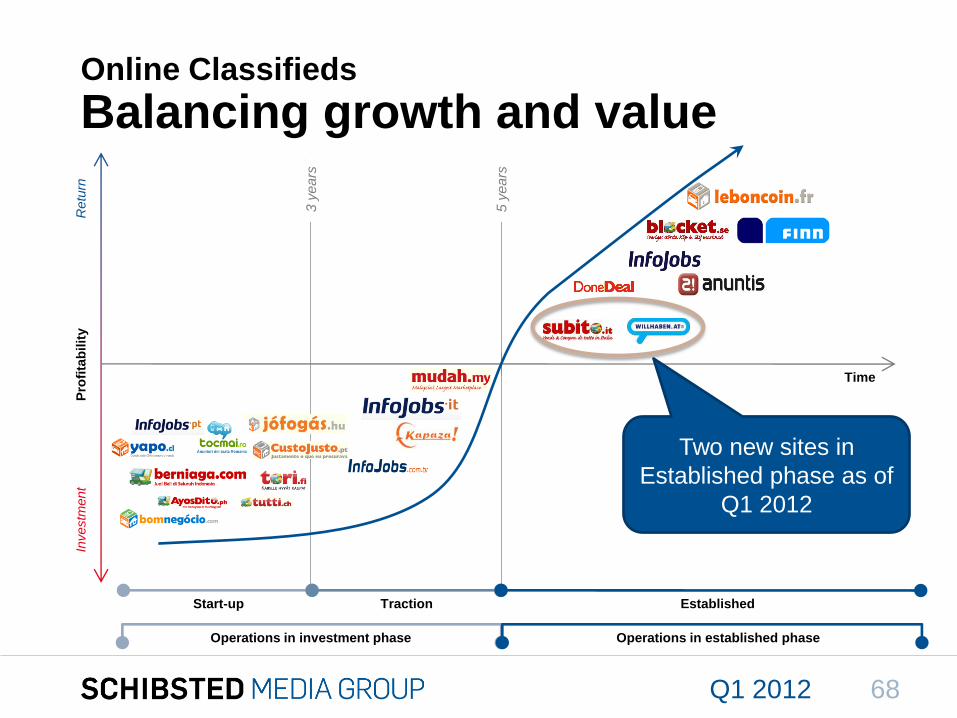

Austria and Italy in Established phase as of Q1 2012

Online classifieds

Q1 2012

MN

OK

31 % 31 %

26 %

43 %45 % 45 %

0 %

10 %

20 %

30 %

40 %

50 %

60 %

-

200

400

600

800

1 000

1 200

Q1 10 Q1 11 Q1 12

Revenue

EBITDA margin

EBITDA margin Established phase

6

To get back,

47 % 48 %

0 %

25 %

50 %

75 %

100 %

0

50

100

150

200

250

300

350

400

Q1 11 Q1 12

Revenues

EBITDA margin

56 %52 %

0 %

25 %

50 %

75 %

100 %

0

50

100

150

200

250

300

350

400

Q1 11 Q1 12

Revenues

EBITDA margin

66 %69 %

0 %

25 %

50 %

75 %

100 %

0

50

100

150

200

250

300

350

400

Q1 11 Q1 12

Revenues

EBITDA margin

Revenue and EBITDA per country

Online classifiedsM

NO

K

MN

OK

MN

OK

Norway Sweden France

Q1 2012

+18% +11% +63%

7

To get back,

Focus on product development and price optimization

Q1 2012

Online classifieds

8

To get back,

BRANDS CATEGORIES FINANCIALS Q1’12

ALL VERTICALSRevenues: 316

Margin: 47%

CARS + GENERALRevenues: 147

Margin: 52%

CARS + GENERAL

JOBS, GENERAL,

REAL ESTATE,

CARS

CARS + GENERAL

Revenues: 386

Margin: 39%

JOBS, GENERAL,

REAL ESTATE,

CARS

CARS + GENERAL

Online classifieds

Established European footprint combined with growth opportunitiesHighly profitable #1 positions

NOTE: Revenue figures in MNOK Operations in Established phase Operations in Investment phase

Q1 2012 9

To get back,

Operations in investment phasedeveloping according to plan

Update on Brazil ventures

Job site InfoJobs.br has narrowed the gap to #1

Blocket copy Bomnegocio.com growing well,

according to plan

Approaching #1 positions

in several European

markets

Mudah.my has

strengthened its #1

position, and is increasing

monetization

Q1 2012 10

To get back,

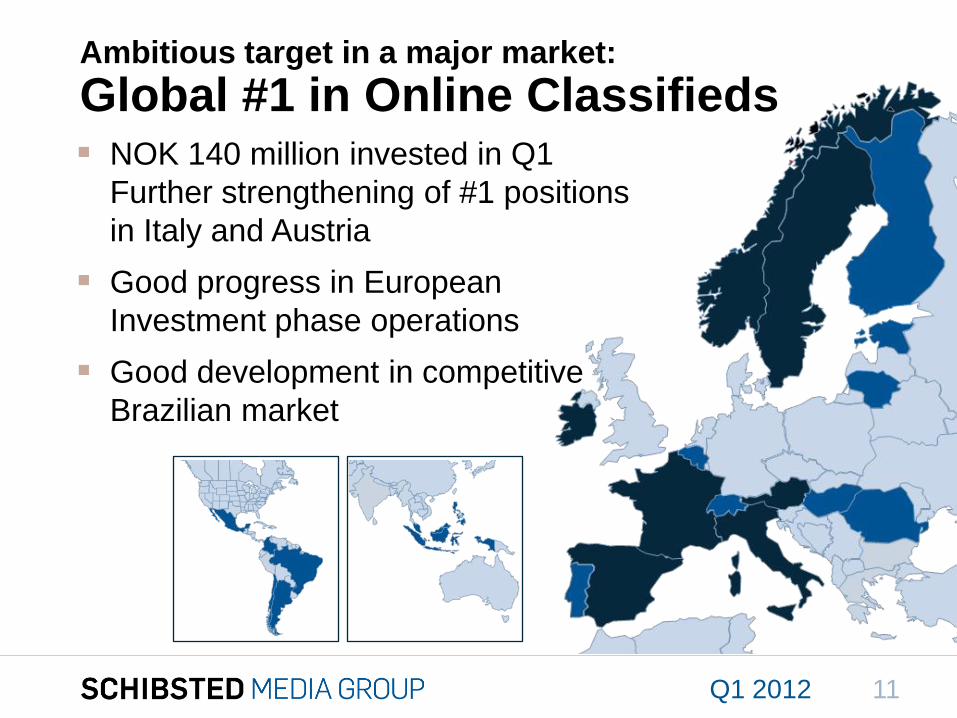

Ambitious target in a major market:

Global #1 in Online Classifieds

Q1 2012

NOK 140 million invested in Q1

Further strengthening of #1 positions

in Italy and Austria

Good progress in European

Investment phase operations

Good development in competitive

Brazilian market

11

Media houses

Q1 2012 12

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

Online news18 %

Online growth

8 %

Offline74 %

NOK

2,491

million

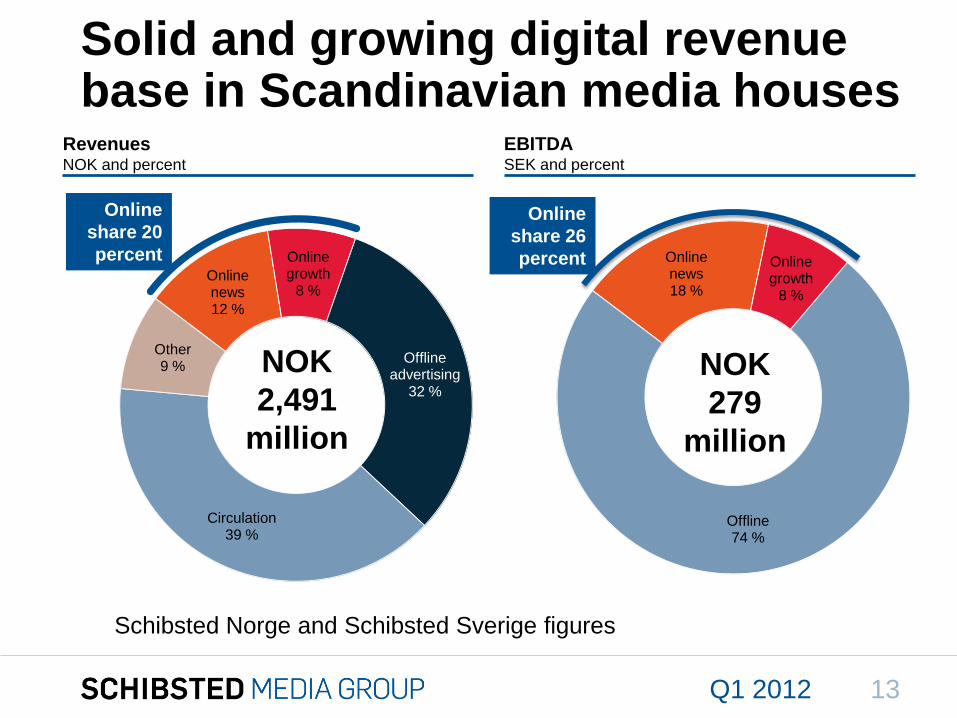

Solid and growing digital revenue base in Scandinavian media houses

RevenuesNOK and percent

EBITDASEK and percent

NOK

279

million

Q1 2012

Online

share 26

percent

Online

share 20

percentOnline news12 %

Online growth

8 %

Offline advertising

32 %

Circulation39 %

Other9 %

Schibsted Norge and Schibsted Sverige figures

13

To get back,

13 % 12 %

0 %

10 %

20 %

30 %

40 %

0

500

1000

1500

2000

Q1 11 Q1 12

Mill

ion

NO

K

Revenues EBITDA margin

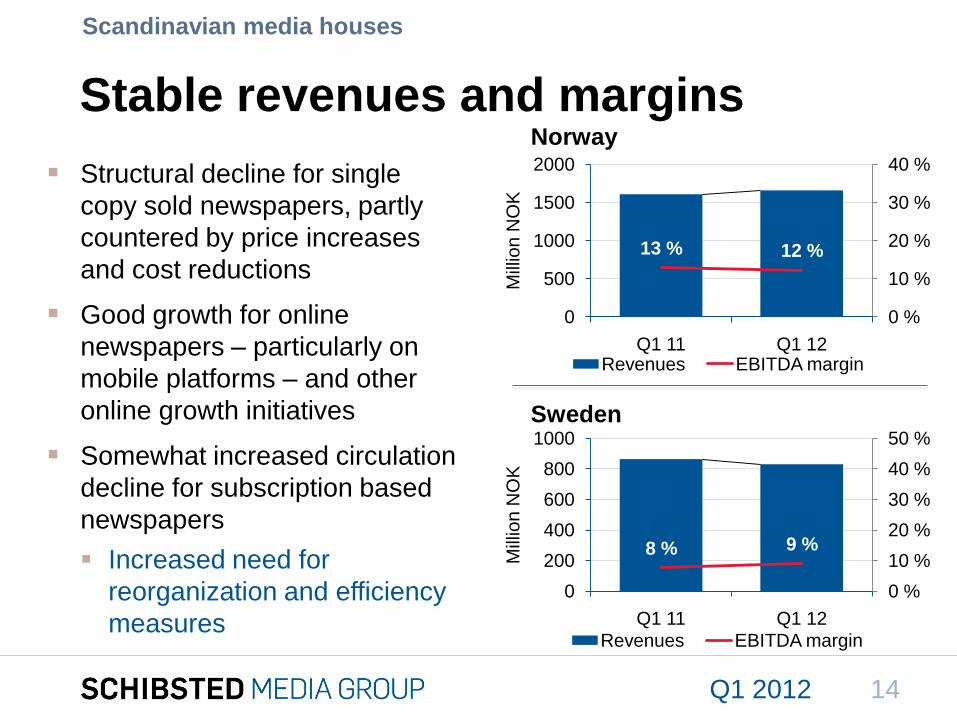

Stable revenues and margins

Structural decline for single

copy sold newspapers, partly

countered by price increases

and cost reductions

Good growth for online

newspapers – particularly on

mobile platforms – and other

online growth initiatives

Somewhat increased circulation

decline for subscription based

newspapers

Increased need for

reorganization and efficiency

measures

Q1 2012

Norway

Sweden

8 % 9 %

0 %

10 %

20 %

30 %

40 %

50 %

0

200

400

600

800

1000

Q1 11 Q1 12

Mill

ion

NO

K

Revenues EBITDA margin

14

Scandinavian media houses

To get back,

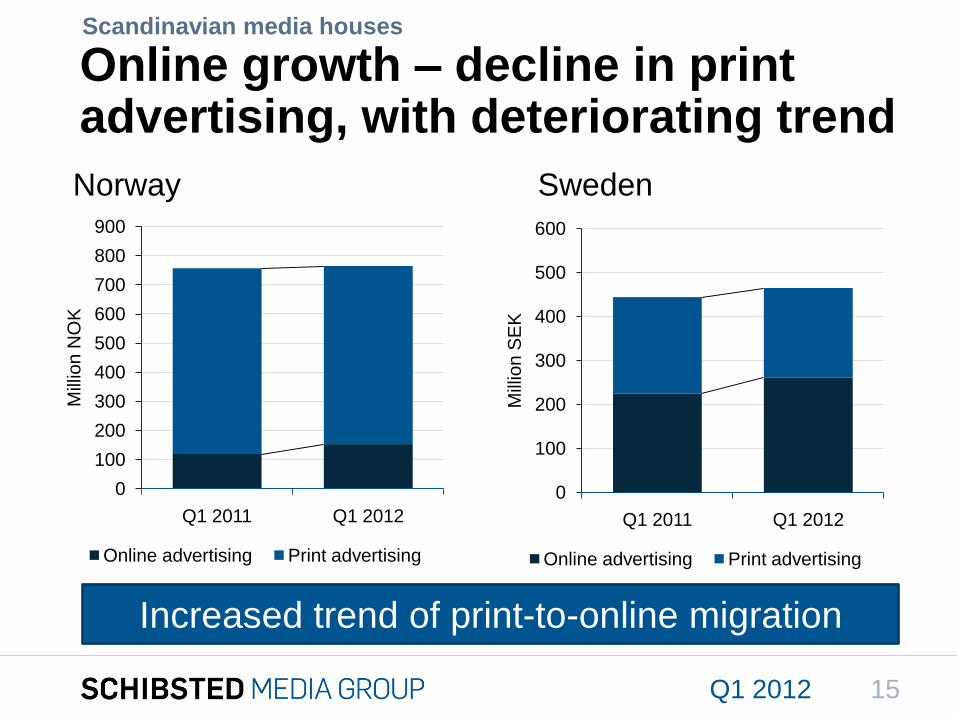

Online growth – decline in print advertising, with deteriorating trend

Q1 2012

Scandinavian media houses

SwedenNorway

Increased trend of print-to-online migration

0

100

200

300

400

500

600

700

800

900

Q1 2011 Q1 2012

Mill

ion

NO

K

Online advertising Print advertising

0

100

200

300

400

500

600

Q1 2011 Q1 2012M

illio

n S

EK

Online advertising Print advertising

15

To get back,

Subscription based newspapers Stable revenue and margins

Q1 2012

Aftenposten

Bergens

TidendeStavanger

Aftenblad FædrelandsvennenSvenska

Dagbladet

EBITDA figures excluding associated companies.

Norway Sweden

7 %

13 % 13 % 13 % 13 % 13 %

4 %

14 % 14 %

3 % 3 %

-2 %

8 % 8 % 7 %

-10 %

0 %

10 %

20 %

30 %

40 %

50 %

60 %

-100

0

100

200

300

400

500

600

Q110 Q111 Q112 Q110 Q111 Q112 Q110 Q111 Q112 Q110 Q111 Q112 Q110 Q111 Q112

MN

OK

Revenue EBITDA-margin (right hand scale)

16

Scandinavian media houses

To get back,

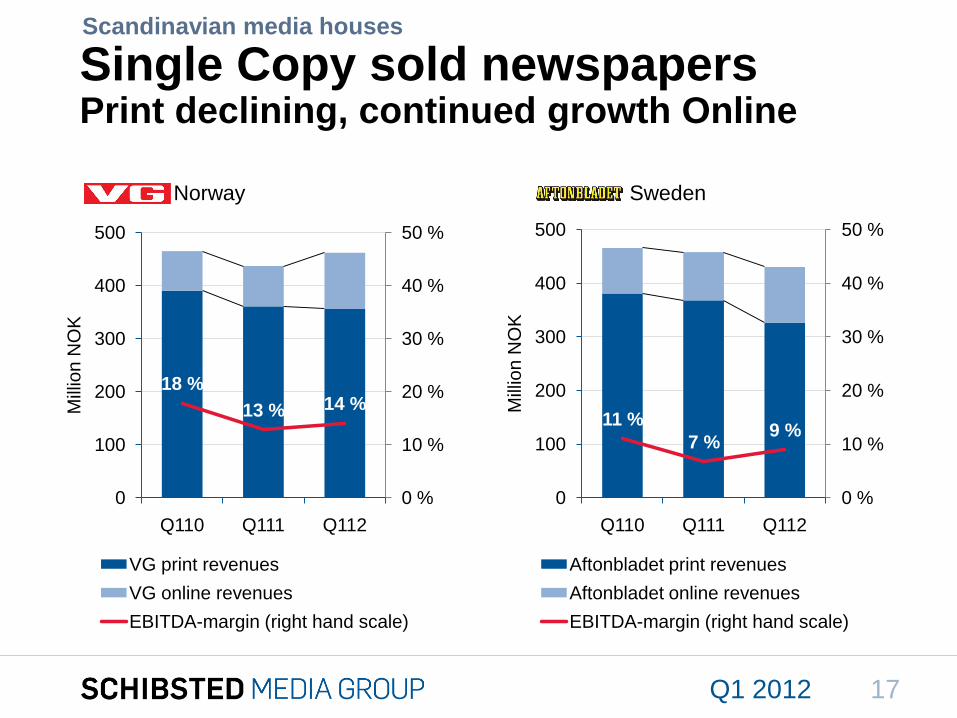

Single Copy sold newspapersPrint declining, continued growth Online

Q1 2012

Norway Sweden

11 %

7 %9 %

0 %

10 %

20 %

30 %

40 %

50 %

0

100

200

300

400

500

Q110 Q111 Q112M

illio

n N

OK

Aftonbladet print revenues

Aftonbladet online revenues

EBITDA-margin (right hand scale)

18 %

13 % 14 %

0 %

10 %

20 %

30 %

40 %

50 %

0

100

200

300

400

500

Q110 Q111 Q112

Mill

ion

NO

K

VG print revenues

VG online revenues

EBITDA-margin (right hand scale)

17

Scandinavian media houses

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

New Online Growth Media

Building high-margin businesses, leveraging strong market positions

Media Houses Online Classifieds

Online

Growth

Media

Q1 2012 18

To get back,

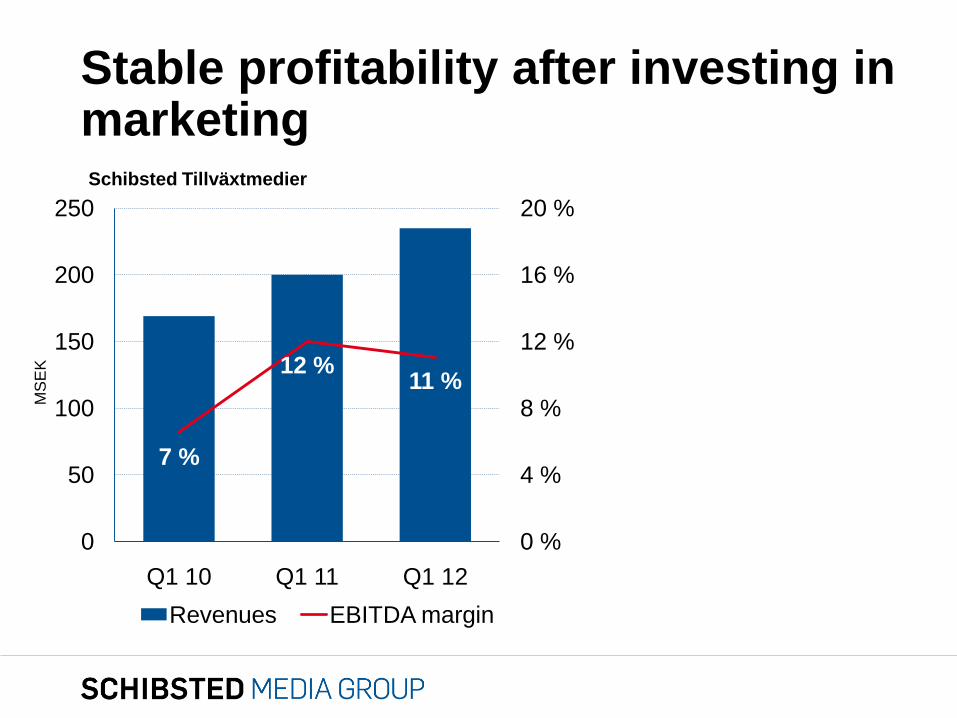

Stable profitability after investing in marketing

Top-line growth of 18%

Strong development for Lendo, Prisjakt.se, Kundkraftand other consumer services sites

Increased marketing efforts in Q1 reduced margins

Stable development for Hitta.se

New market place for mobile phones and subscriptions established

Schibsted Tillväxtmedier

MS

EK

Q1 2012

7 %

12 % 11 %

0 %

5 %

10 %

15 %

20 %

0

50

100

150

200

250

Q1 10 Q1 11 Q1 12

Revenues EBITDA margin

19

Scandinavian media houses

Financials

Q1 2012 20

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

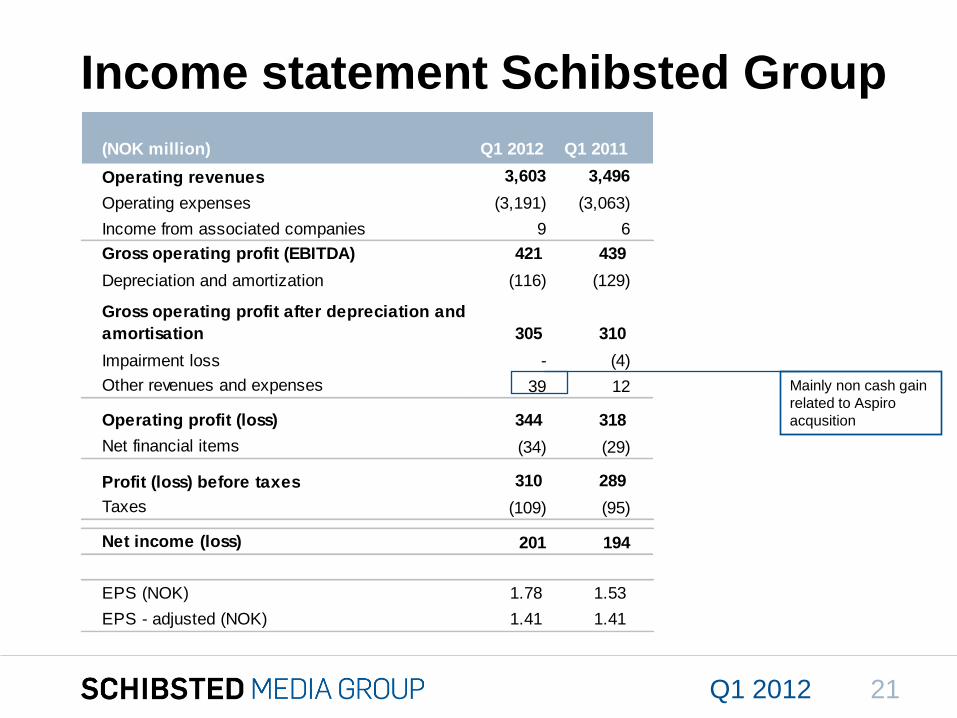

Income statement Schibsted Group

Q1 2012

Mainly non cash gain

related to Aspiro

acqusition

(NOK million) Q1 2012 Q1 2011

Operating revenues 3,603 3,496

Operating expenses (3,191) (3,063)

Income from associated companies 9 6

Gross operating profit (EBITDA) 421 439

Depreciation and amortization (116) (129)

Gross operating profit after depreciation and

amortisation 305 310

Impairment loss - (4)

Other revenues and expenses 39 12

Operating profit (loss) 344 318

Net financial items (34) (29)

Profit (loss) before taxes 310 289

Taxes (109) (95)

Net income (loss) 201 194

EPS (NOK) 1.78 1.53

EPS - adjusted (NOK) 1.41 1.41

21

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

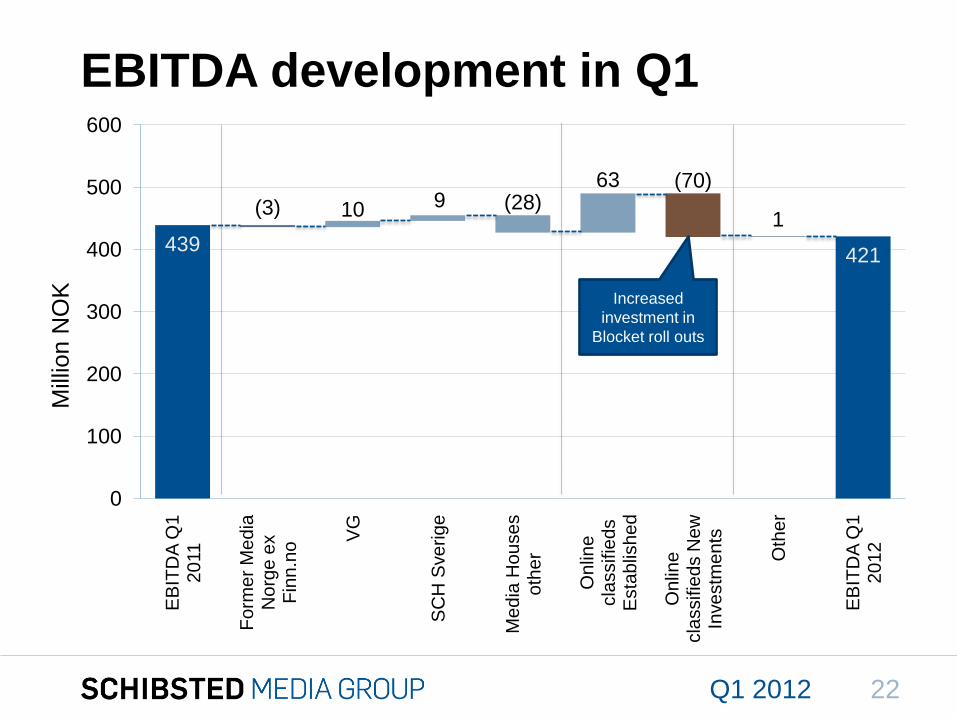

439421

(3) 10 9 (28)63 (70)

1

0

100

200

300

400

500

600

EB

ITD

A Q

1

20

11

Form

er

Media

N

org

e e

x

Fin

n.n

o

VG

SC

H S

ve

rig

e

Me

dia

Ho

use

s

oth

er

On

line

cla

ssifie

ds

Esta

blis

he

d

Onlin

e

cla

ssifie

ds N

ew

In

ve

stm

en

ts

Oth

er

EB

ITD

A Q

1

2012

EBITDA development in Q1M

illio

n N

OK Increased

investment in

Blocket roll outs

Q1 2012 22

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

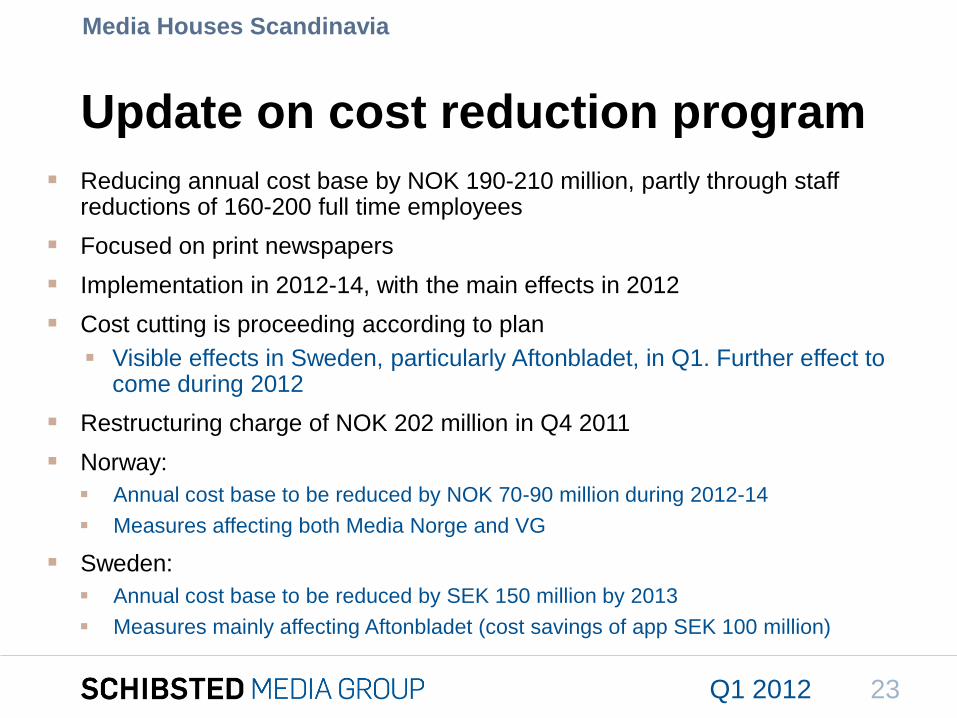

Reducing annual cost base by NOK 190-210 million, partly through staff reductions of 160-200 full time employees

Focused on print newspapers

Implementation in 2012-14, with the main effects in 2012

Cost cutting is proceeding according to plan

Visible effects in Sweden, particularly Aftonbladet, in Q1. Further effect to come during 2012

Restructuring charge of NOK 202 million in Q4 2011

Norway:

Annual cost base to be reduced by NOK 70-90 million during 2012-14

Measures affecting both Media Norge and VG

Sweden:

Annual cost base to be reduced by SEK 150 million by 2013

Measures mainly affecting Aftonbladet (cost savings of app SEK 100 million)

Update on cost reduction program

Media Houses Scandinavia

Q1 2012 23

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

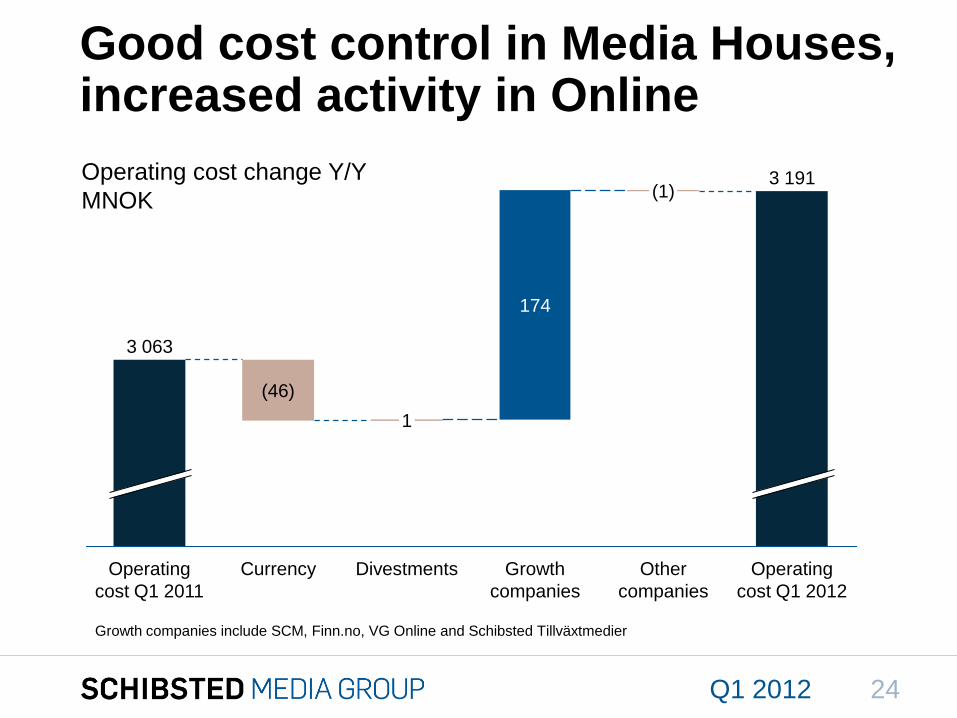

Q1 2012

Good cost control in Media Houses, increased activity in Online

Growth

companies

Operating

cost Q1 2012

(1)3 191

Other

companies

1

Currency

174

Divestments

(46)

Operating

cost Q1 2011

3 063

Operating cost change Y/Y

MNOK

Growth companies include SCM, Finn.no, VG Online and Schibsted Tillväxtmedier

24

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

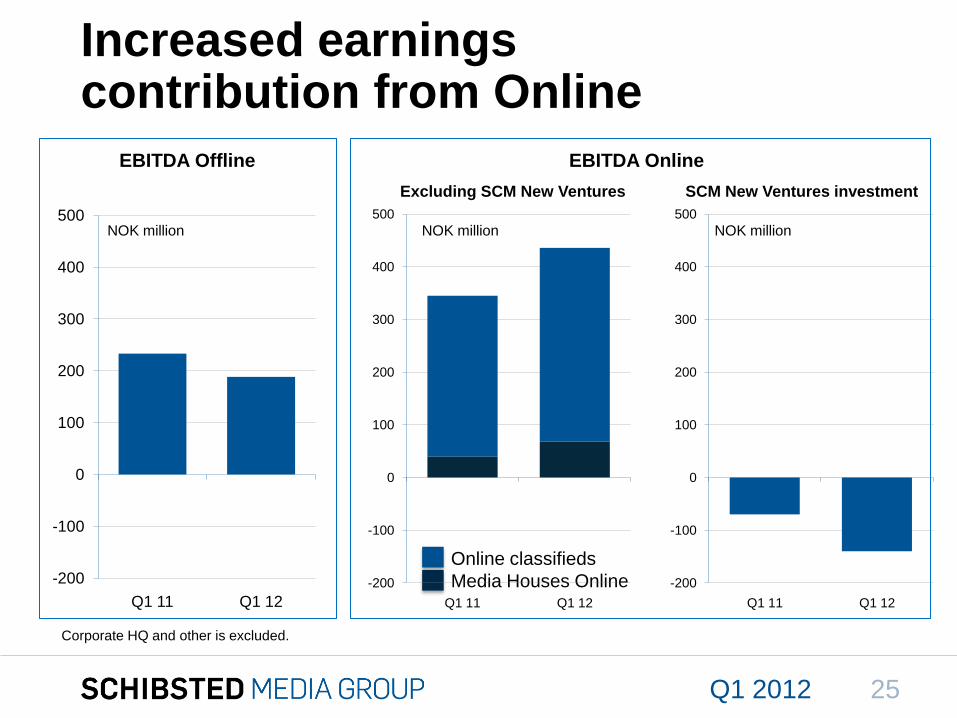

Increased earnings contribution from Online

EBITDA Offline EBITDA Online

Excluding SCM New Ventures SCM New Ventures investment

Q1 2012

Corporate HQ and other is excluded.

Online classifieds

Media Houses Online

NOK million NOK million NOK million

25

-200

-100

0

100

200

300

400

500

Q1 11 Q1 12

-200

-100

0

100

200

300

400

500

Q1 11 Q1 12

-200

-100

0

100

200

300

400

500

Q1 11 Q1 12

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

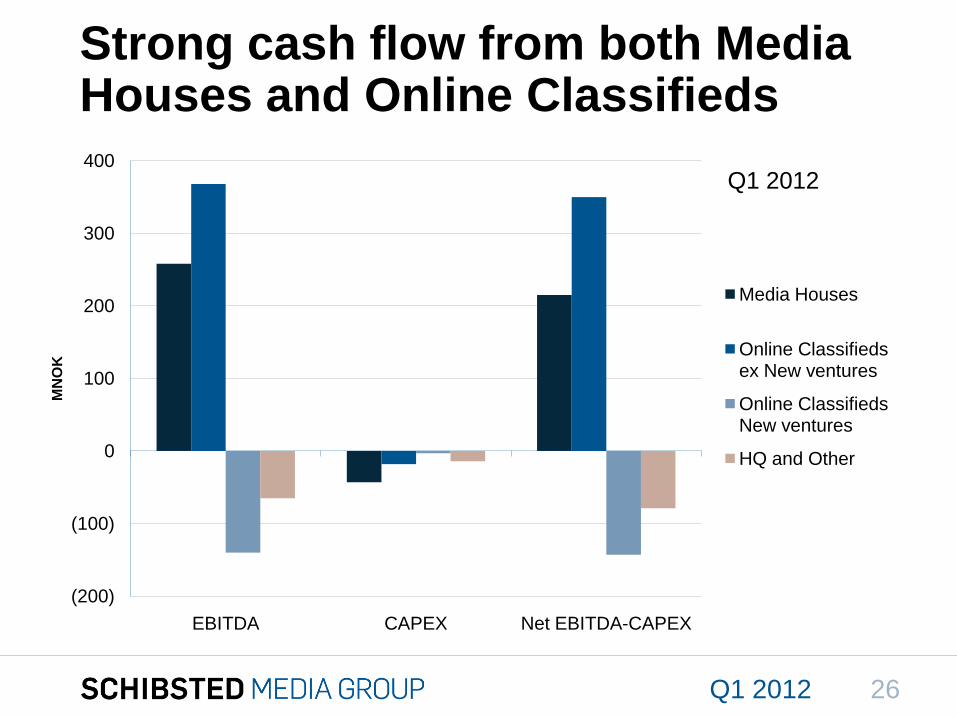

(200)

(100)

0

100

200

300

400

EBITDA CAPEX Net EBITDA-CAPEX

MN

OK

Media Houses

Online Classifieds ex New ventures

Online Classifieds New ventures

HQ and Other

Strong cash flow from both Media Houses and Online Classifieds

Q1 2012

Q1 2012 26

To get back,

-

500

1 000

1 500

2 000

2 500

3 000

3 500

< 1 yr < 2 yrs

< 3 yrs

< 4 yrs

< 5 yrs

> 5 yrs

Other interest-bearing debt Bonds and CP's

Drawn bankfacilities Undrawn bankfacilities

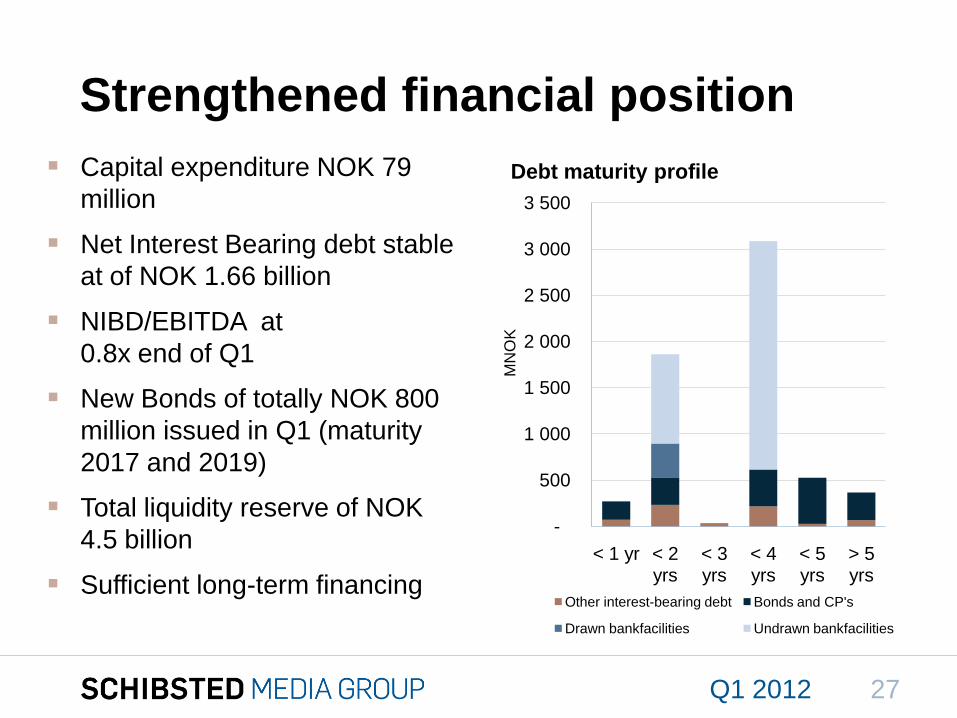

Strengthened financial position

Capital expenditure NOK 79

million

Net Interest Bearing debt stable

at of NOK 1.66 billion

NIBD/EBITDA at

0.8x end of Q1

New Bonds of totally NOK 800

million issued in Q1 (maturity

2017 and 2019)

Total liquidity reserve of NOK

4.5 billion

Sufficient long-term financing

Q1 2012

Debt maturity profile

MN

OK

27

To get back,

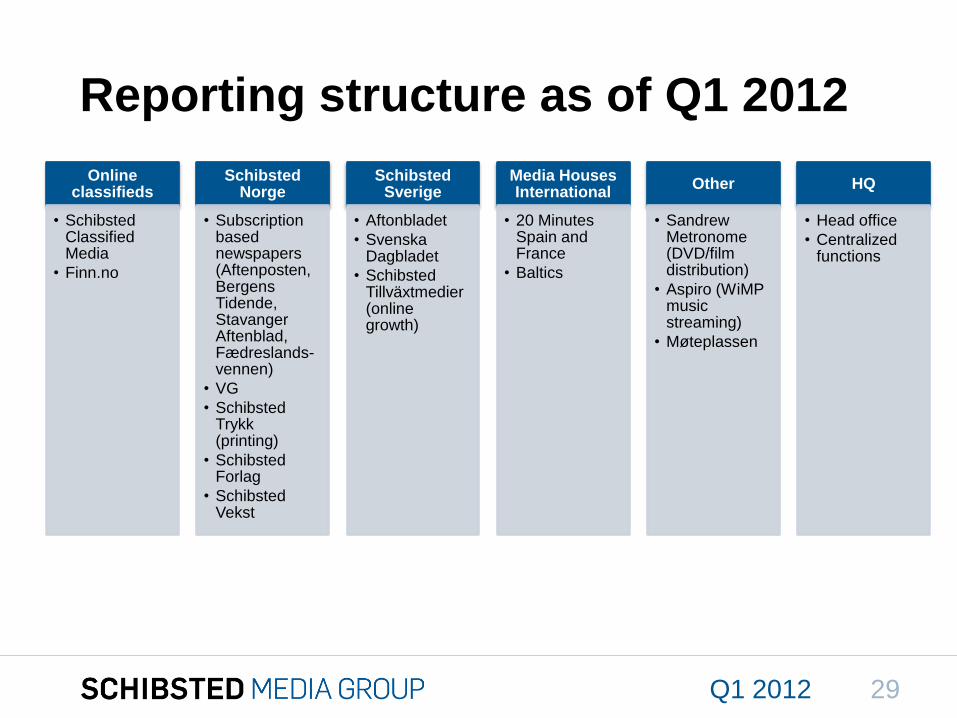

New Business segments as of Q1 2012

Background: Alignment to our operating- and management structure

Schibsted Norge established, combining all Norwegian media house

activities

Hitta.se is now seen more as an integrated part of media Houses.

Directories not a part of our international expansion strategy

Main changes in operating segments:

Media Houses Scandinavia split in two:

Schibsted Norge and Schibsted Sverige

Hitta.se moved from Online classifieds to Schibsted Sverige

Aspiro reported in “Other” segment

Centralized functions, previously part of Media Houses Scandinavia,

are now part of “Headquarters”

Q1 2012 28

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

Q1 2012

Reporting structure as of Q1 2012

Online classifieds

• Schibsted Classified Media

• Finn.no

Schibsted Norge

• Subscriptionbasednewspapers(Aftenposten, Bergens Tidende, Stavanger Aftenblad, Fædreslands-vennen)

• VG

• Schibsted Trykk (printing)

• Schibsted Forlag

• Schibsted Vekst

Schibsted Sverige

• Aftonbladet

• SvenskaDagbladet

• Schibsted Tillväxtmedier (online growth)

Media Houses International

• 20 MinutesSpain and France

• Baltics

Other

• SandrewMetronome(DVD/film distribution)

• Aspiro (WiMPmusicstreaming)

• Møteplassen

HQ

• Head office

• Centralizedfunctions

29

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

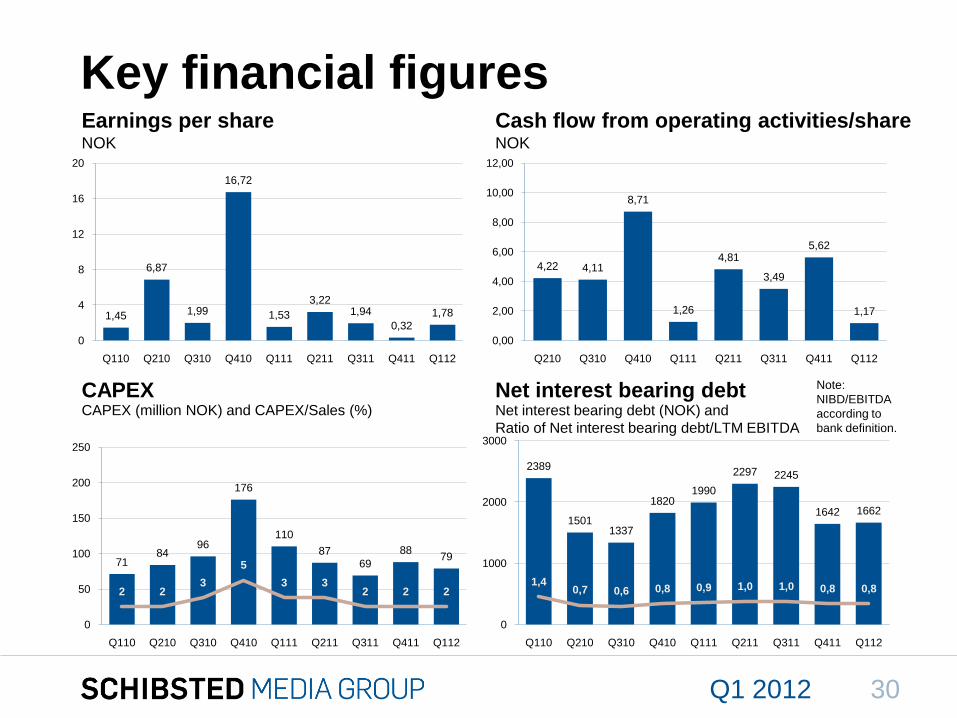

Key financial figuresEarnings per share Cash flow from operating activities/share

CAPEX Net interest bearing debt

NOK NOK

CAPEX (million NOK) and CAPEX/Sales (%) Net interest bearing debt (NOK) and

Ratio of Net interest bearing debt/LTM EBITDA

Note:

NIBD/EBITDA

according to

bank definition.

Q1 2012

1,45

6,87

1,99

16,72

1,53

3,221,94

0,32

1,78

0

4

8

12

16

20

Q110 Q210 Q310 Q410 Q111 Q211 Q311 Q411 Q112

4,22 4,11

8,71

1,26

4,81

3,49

5,62

1,17

0,00

2,00

4,00

6,00

8,00

10,00

12,00

Q210 Q310 Q410 Q111 Q211 Q311 Q411 Q112

2389

15011337

18201990

2297 2245

1642 1662

1,40,7 0,6 0,8 0,9 1,0 1,0 0,8 0,8

0

1000

2000

3000

Q110 Q210 Q310 Q410 Q111 Q211 Q311 Q411 Q112

7184

96

176

110

8769

8879

2 23

5

3 32 2 2

0

50

100

150

200

250

Q110 Q210 Q310 Q410 Q111 Q211 Q311 Q411 Q112

30

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

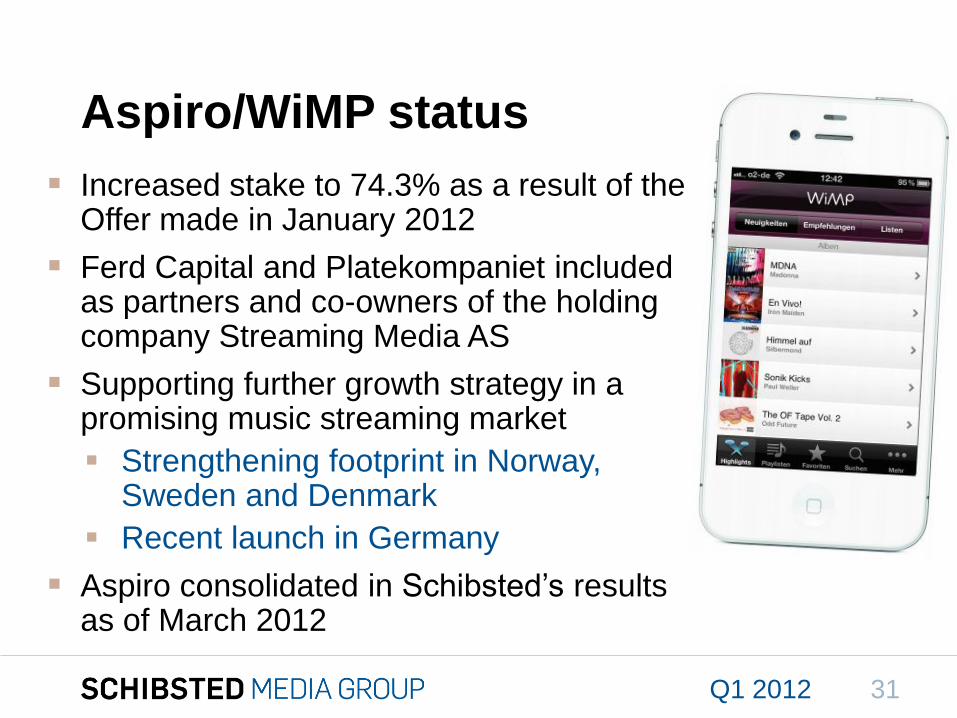

Increased stake to 74.3% as a result of the Offer made in January 2012

Ferd Capital and Platekompaniet included as partners and co-owners of the holding company Streaming Media AS

Supporting further growth strategy in a promising music streaming market

Strengthening footprint in Norway, Sweden and Denmark

Recent launch in Germany

Aspiro consolidated in Schibsted’s results as of March 2012

Q1 2012

Aspiro/WiMP status

31

To get back,

Exposure to Spain Online classifieds

Revenues full year 2011: EUR 95 million

EBITDA full year 2011 : EUR 30 million

Intangible assets*: year end 2011: EUR 387.4 million

20 Minutes

Revenues full year 2011: EUR 22.3 million

EBITDA full year 2011: EUR -3.6 million

Intangible assets: year end 2011: EUR 0.6 million

Financial development unsatisfactory in 20 Minutes

Different measures are being studied

Q1 2012 32

*) Includes Italian assets

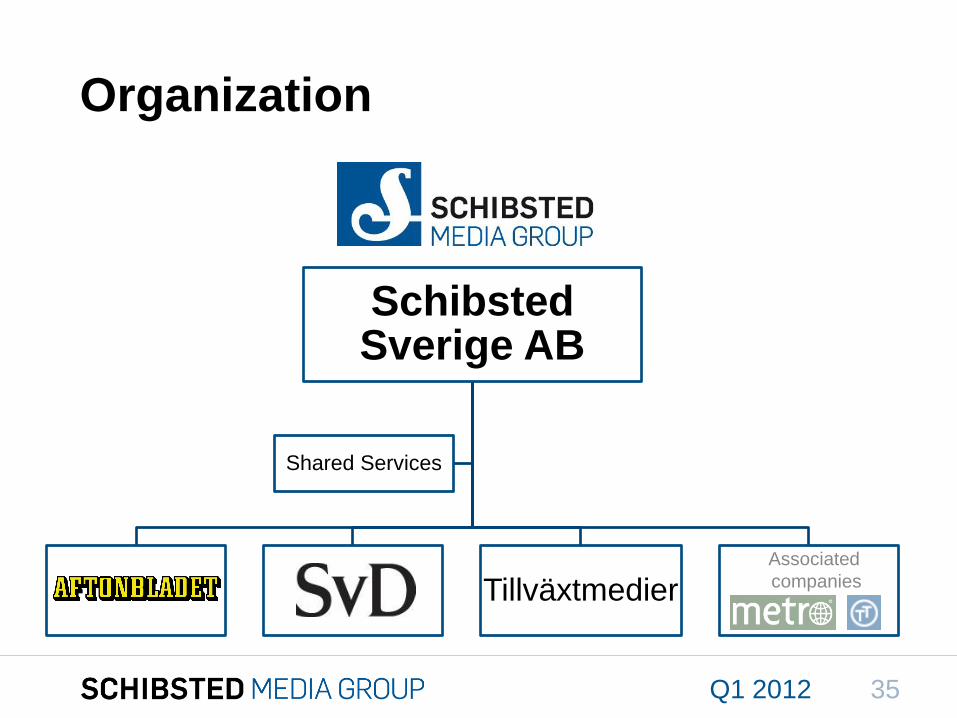

Schibsted Sverige

Q1 2012 33

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

Welcome to Schibsted Sverige

34Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

Schibsted Sverige AB

Tillväxtmedier

Shared Services

Organization

Associated

companies

35Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

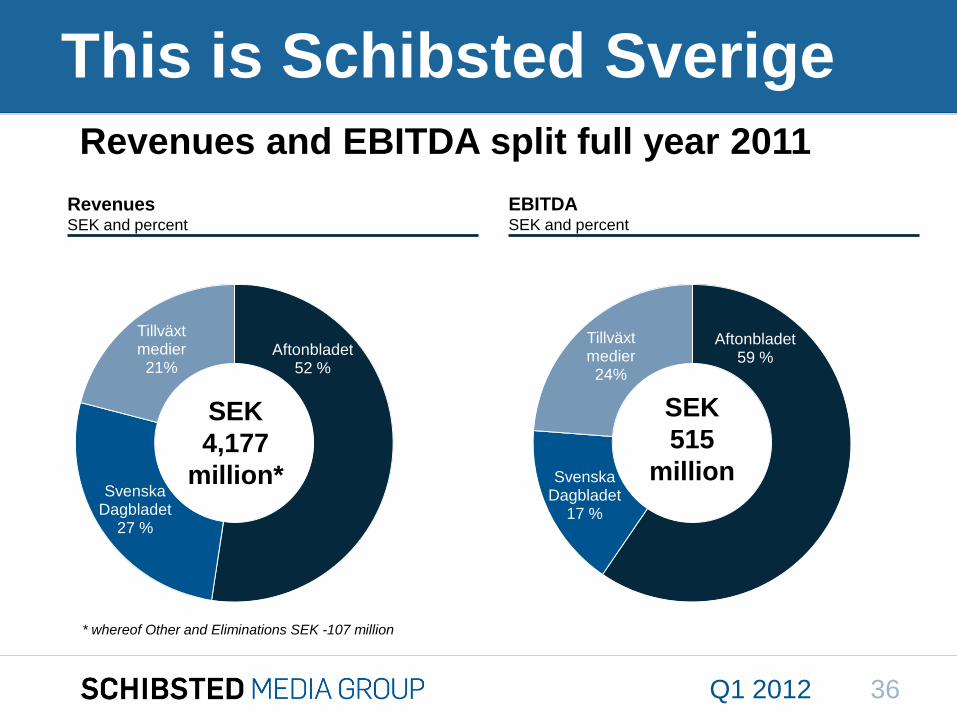

Revenues and EBITDA split full year 2011

Aftonbladet52 %

Svenska Dagbladet

27 %

Tillväxtmedier21%

SEK

4,177

million*

Aftonbladet59 %

Svenska Dagbladet

17 %

Tillväxtmedier24%

SEK

515

million

RevenuesSEK and percent

EBITDASEK and percent

* whereof Other and Eliminations SEK -107 million

This is Schibsted Sverige

36Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

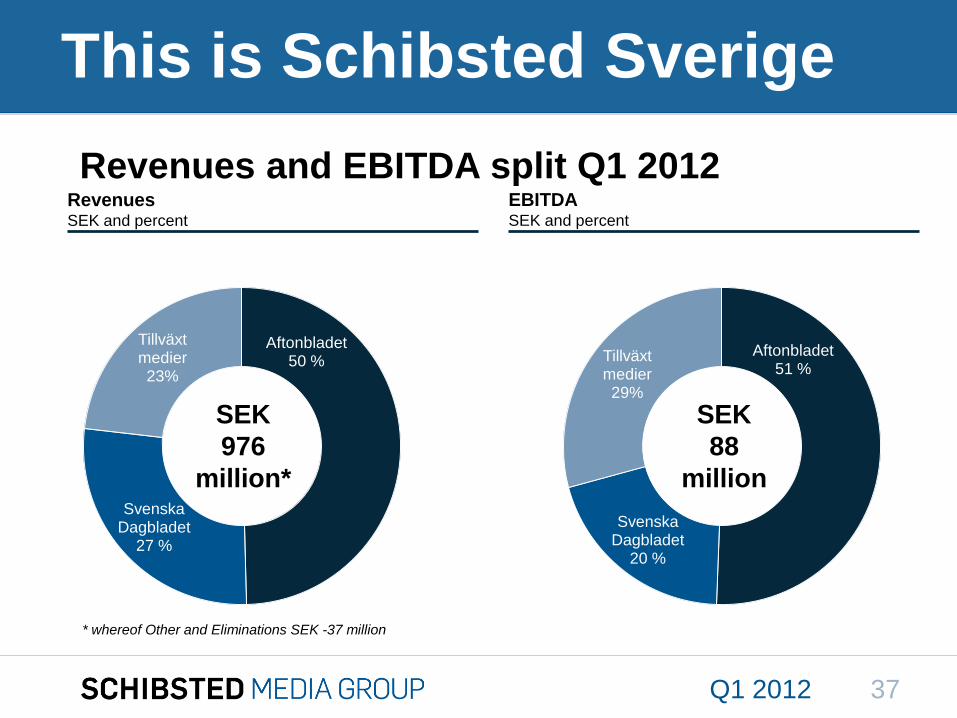

Aftonbladet50 %

Svenska Dagbladet

27 %

Tillväxtmedier23%

SEK

976

million*

Aftonbladet51 %

Svenska Dagbladet

20 %

Tillväxtmedier29%

SEK

88

million

Revenues and EBITDA split Q1 2012RevenuesSEK and percent

EBITDASEK and percent

* whereof Other and Eliminations SEK -37 million

This is Schibsted Sverige

37Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

Every week

38

Strong digital position

Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

39Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

40Q1 2012

To get back,

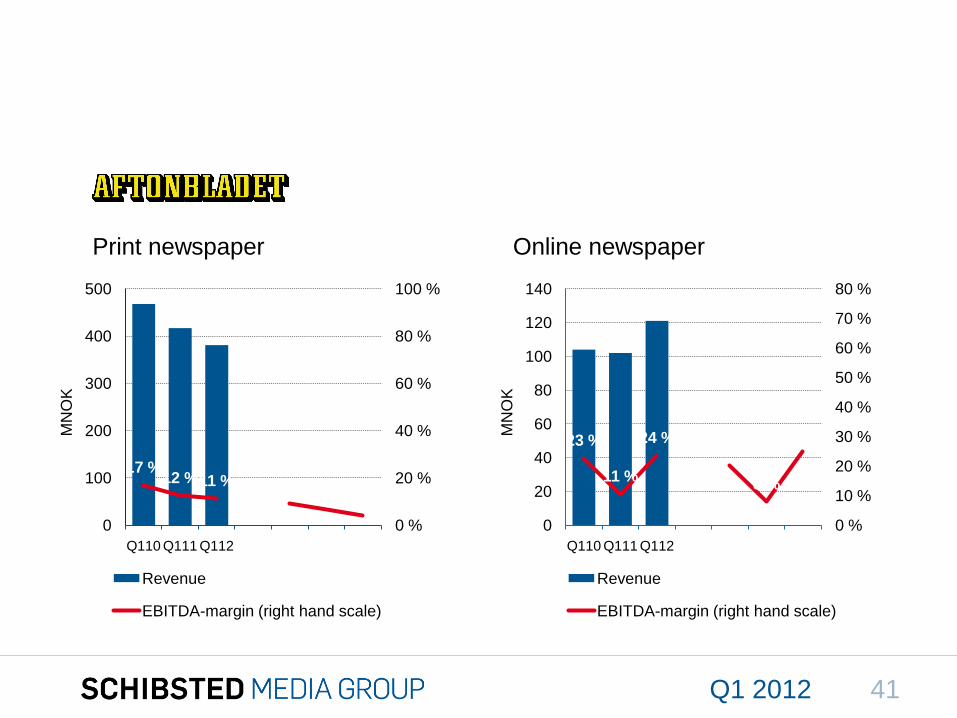

17 %12 %11 % 9 % 6 % 4 %

0 %

20 %

40 %

60 %

80 %

100 %

0

100

200

300

400

500

Q110 Q111 Q112

MN

OK

Revenue

EBITDA-margin (right hand scale)

23 %

11 %

24 %20 %

8 %

25 %

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

0

20

40

60

80

100

120

140

Q110 Q111 Q112

MN

OK

Revenue

EBITDA-margin (right hand scale)

Print newspaper Online newspaper

41Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

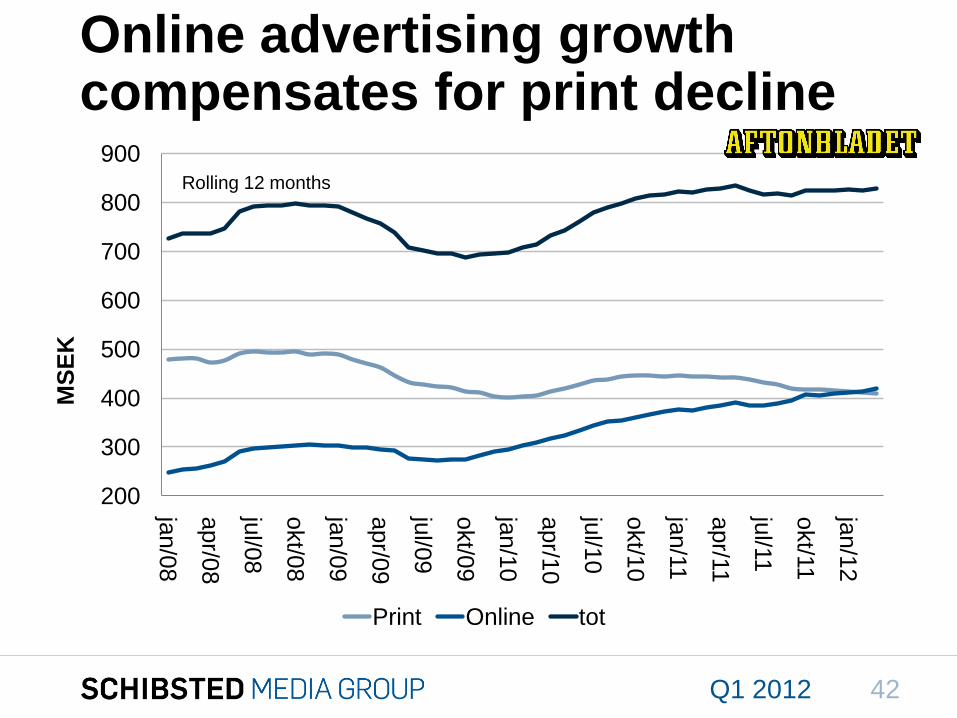

Online advertising growth compensates for print decline

200

300

400

500

600

700

800

900

jan/0

8

apr/0

8

jul/0

8

okt/0

8

jan/0

9

apr/0

9

jul/0

9

okt/0

9

jan/1

0

apr/1

0

jul/1

0

okt/1

0

jan/1

1

apr/1

1

jul/1

1

okt/1

1

jan/1

2

MS

EK

Print Online tot

Rolling 12 months

42Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

User payment

in AftonbladetToday around

150,000

customers

43Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

Schibsted Tillväxtmedier

44Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

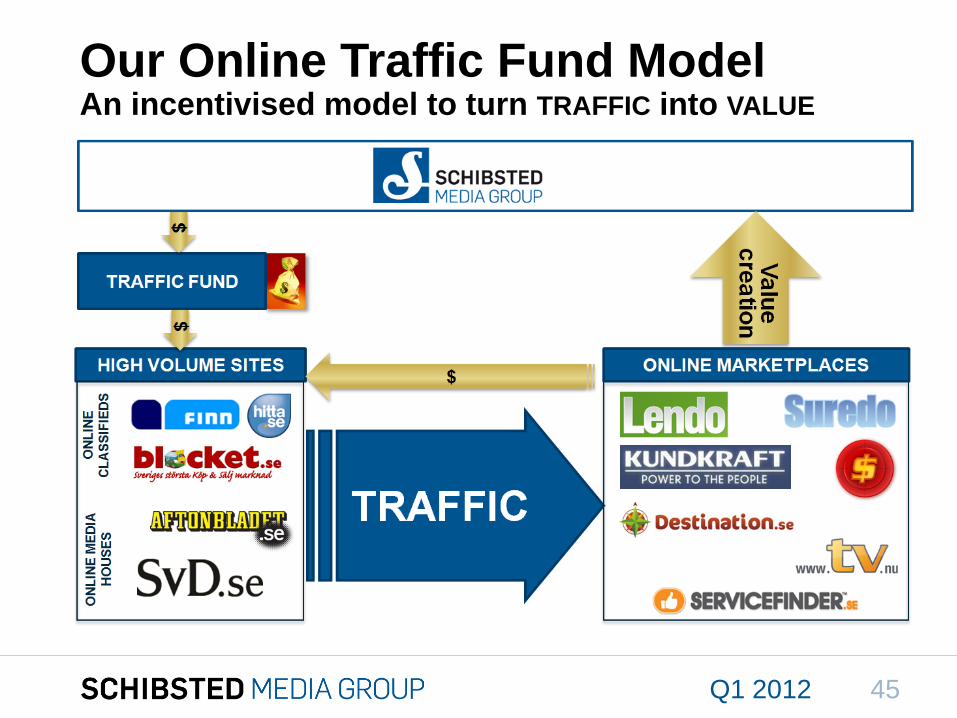

Our Online Traffic Fund ModelAn incentivised model to turn TRAFFIC into VALUE

45Q1 2012

To get back,

Stable profitability after investing in marketingSchibsted Tillväxtmedier

MS

EK

7 %

12 %11 %

0 %

4 %

8 %

12 %

16 %

20 %

0

50

100

150

200

250

Q1 10 Q1 11 Q1 12

Revenues EBITDA margin

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

Personal finance: Market places for private economy

Banks

Insurance companies

Suppliers of electricity

Telcos

Service providers

Cost efficient

customer

acquisition

Better

decisions

47Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

Product overview

Purchase club with yearly

negotiation

Loan intermediation

Electricity price comparison

Insurance advise

Mobile telephony

2009

2009

2011

2011

2012

48Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

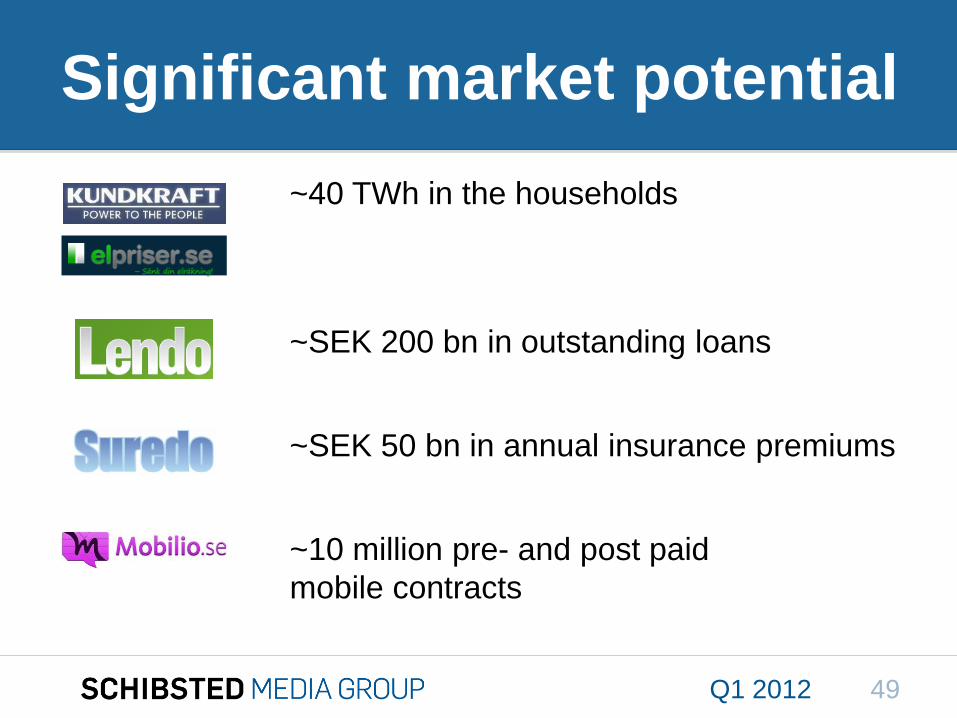

Significant market potential

~40 TWh in the households

~SEK 200 bn in outstanding loans

~SEK 50 bn in annual insurance premiums

~10 million pre- and post paid

mobile contracts

49Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

Focus on growth in 2012

80% revenue growth in Q1 12 vs Q1 11

Significant increase in market- and product investments

Good profit margin despite being in a growth phase

Collaborations within and without Schibsted Media Group

Active search for new investments

50Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

51Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

Interaction between Blocket.se and Tillväxtmedier

52Q1 2012

Outlook

Q1 2012 53

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

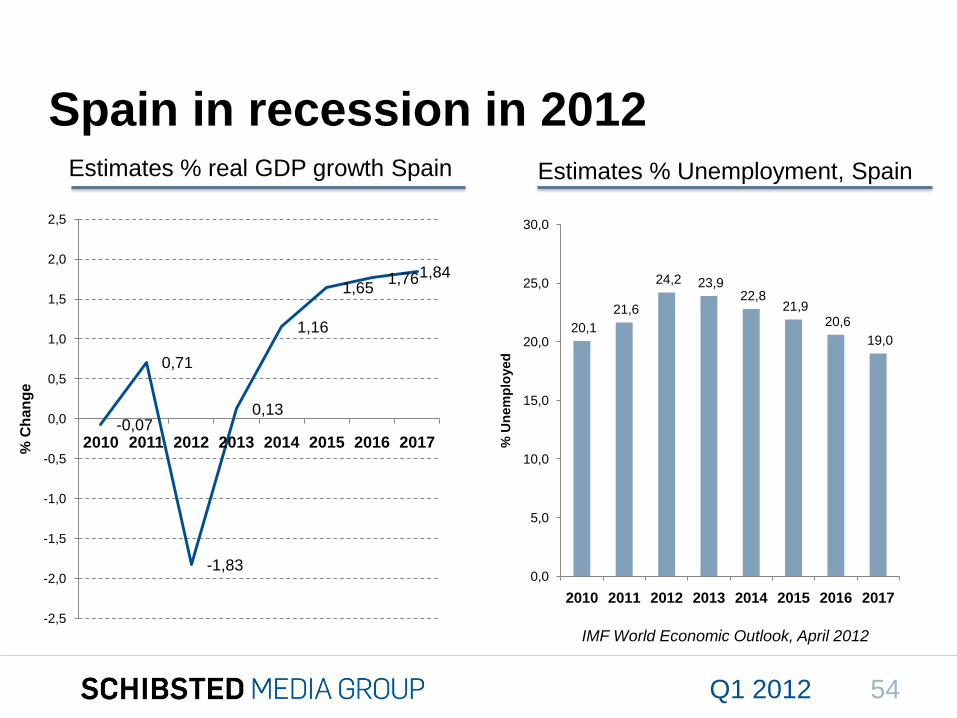

Spain in recession in 2012

-0,07

0,71

-1,83

0,13

1,16

1,65 1,76 1,84

-2,5

-2,0

-1,5

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

2010 2011 2012 2013 2014 2015 2016 2017% C

han

ge

20,1

21,6

24,2 23,9 22,8

21,9 20,6

19,0

0,0

5,0

10,0

15,0

20,0

25,0

30,0

2010 2011 2012 2013 2014 2015 2016 2017

% U

nem

plo

yed

Estimates % real GDP growth Spain Estimates % Unemployment, Spain

IMF World Economic Outlook, April 2012

Q1 2012 54

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

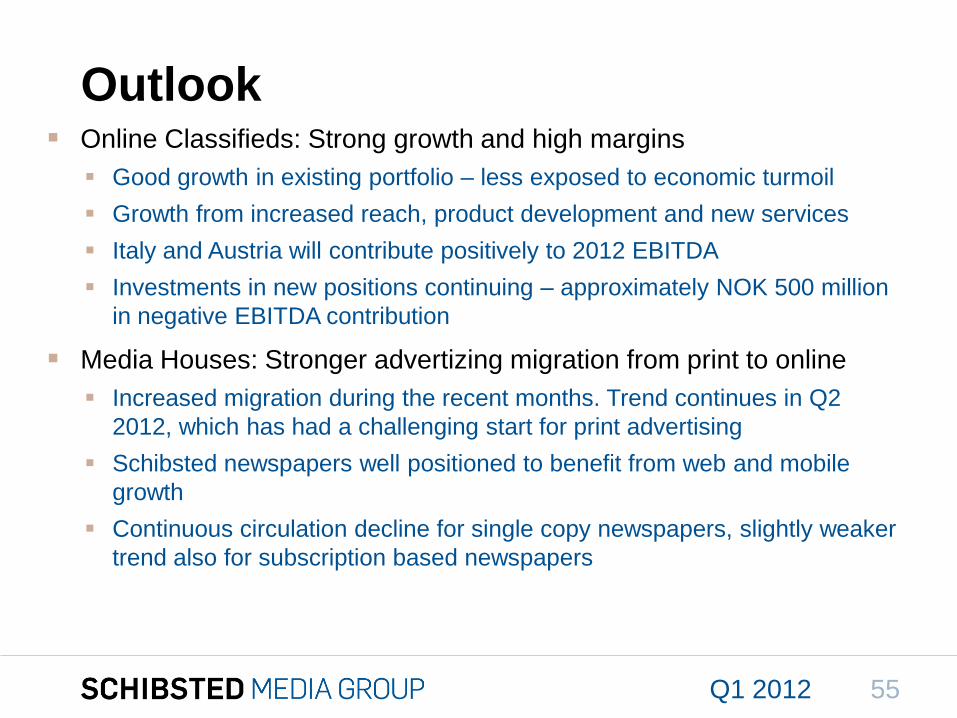

Online Classifieds: Strong growth and high margins

Good growth in existing portfolio – less exposed to economic turmoil

Growth from increased reach, product development and new services

Italy and Austria will contribute positively to 2012 EBITDA

Investments in new positions continuing – approximately NOK 500 million

in negative EBITDA contribution

Media Houses: Stronger advertizing migration from print to online

Increased migration during the recent months. Trend continues in Q2

2012, which has had a challenging start for print advertising

Schibsted newspapers well positioned to benefit from web and mobile

growth

Continuous circulation decline for single copy newspapers, slightly weaker

trend also for subscription based newspapers

Outlook

Q1 2012 55

Q&A

56Q1 2012

57Q1 2012

AppendicesSpreadsheet containing detailed Q1 2012 and Historical and analytical

Information can be downloaded from www.schibsted.com/ir

58Q1 2012

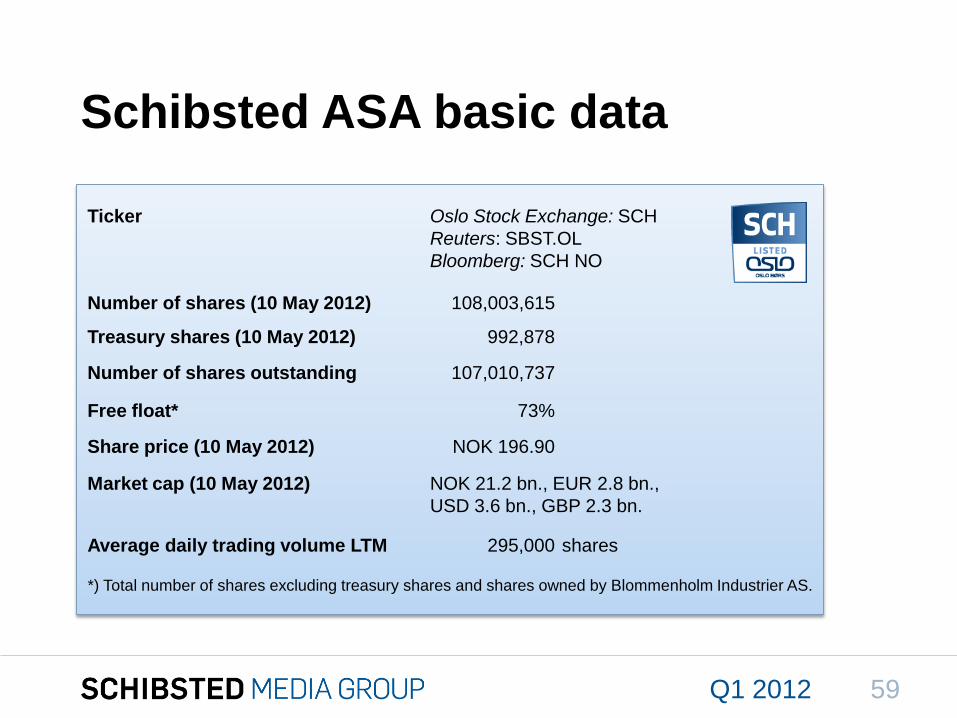

Schibsted ASA basic data

Ticker Oslo Stock Exchange: SCH

Reuters: SBST.OL

Bloomberg: SCH NO

Number of shares (10 May 2012) 108,003,615

Treasury shares (10 May 2012) 992,878

Number of shares outstanding 107,010,737

Free float* 73%

Share price (10 May 2012) NOK 196.90

Market cap (10 May 2012) NOK 21.2 bn., EUR 2.8 bn.,

USD 3.6 bn., GBP 2.3 bn.

Average daily trading volume LTM 295,000 shares

*) Total number of shares excluding treasury shares and shares owned by Blommenholm Industrier AS.

59Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

2005 Acquisition of Hitta.se

2005 Launch of Sesam and acquisition of Internettkatalogen

2006 Schibsted International Classifieds & Search – launch

of Willhaben.at and LeBoncoin.fr

2006 Acquisition of selected assets of Trader Classified

Media (International Classifieds Acquired)

2006 Divestment of ownership in TV 2

2006 Divestment of ownership TV4

2007 Media Norge approved by Schibsted’s general meeting

2009 Rolv Erik Ryssdal new CEO

2009 Media Norge established

2009 Increased ownership in Finn.no and InfoJobs.net

2009 Non core activities Metronome, Retriever, Basefarm,

Teleadress divested

2010 Increased ownership in Leboncoin.fr from 50% to

100%

2011 Merger with Media Norge.

2011 The Blocket-copy Bomnegocio.com launched in Brazil

2012 Schibsted Norge AS established

1839 Chr. Schibsted Forlag (publishing house)

founded

1860 Christiania Adresseblad launched in Oslo –

renamed Aftenposten in 1861

1966 Takeover of VG

1989 Reorganisation from a private family company to

a limited company

1992 Listing at the Oslo Stock Exchange with a

growth strategy declaration

1992 First TV and film investments

1995 First New Media/Internet investments

1995 First investments in Kanal 2 in Estonia

1996 Acquisition of Aftonbladet

1998 Acquisition of Svenska Dagbladet

1998 Investment in Eesti Meedia Group

1999 Launch of the free newspaper concept 20

Minutes

2000 Launch of Finn

2003 Acquisition of Blocket

Historical development

See also: http://www.schibsted.com/en/About-Schibsted/History/

60Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

61Q1 2012

Top 20 shareholders

Data as of 31 March 2012. Updated information at: www.schibsted.com/en/ir/Share/Shareholders/

Rank Name Holding Share

1 Blommenholm Industrier AS 28 188 589 26,1 %

2 Folketrygdfondet 7 547 470 7,0 %

3 JPMorgan Chase Bank, Nordea Treaty Account * 7 246 424 6,7 %

4 Goldman Sachs & Co - Equity * 4 669 336 4,3 %

5 NWT Media AS 4 545 815 4,2 %

6 Bank Of New York Mellon * 4 461 341 4,1 %

7 State Street Bank And Trust Co. * 1 991 162 1,8 %

8 State Street Bank And Trust Co. * 1 935 390 1,8 %

9 JPMorgan Chase Bank * 1 666 359 1,5 % % of foreign shareholders** 52,2 %

10 Clearstream Banking S.A. * 1 349 085 1,2 % Number of shareholders 5 119

11 Citibank NA London Branch * 1 157 687 1,1 % Number of shares 108 003 615

12 SHB Institutional Sales Stockholm, C/O Handelsbanken Asset Mgn 1 150 168 1,1 % Shares ow ned by Schibsted 992 878

13 Skandinaviska Enskilda Banken * 1 035 634 1,0 %

14 Schibsted ASA 992 878 0,9 % Largest countries of ownership

15 BNP Paribas Secs Services Paris * 928 000 0,9 % Norw ay** 48,8 %

16 Odin Norge 877 171 0,8 % USA 16,6 %

17 Fid. Funds-Eu. Blue Chip FND/Sicav 764 240 0,7 % United Kingdom 14,6 %

18 The Northern Trust Co. * 716 514 0,7 % Sw eden** 7,0 %

19 Montague Place Custody Services * 713 835 0,7 % Luxembourg 4,3 %

20 Statoil Pensjon 651 076 0,6 % France 2,3 %

Source: VPS

*) Nominee accounts

**) NWT Media AS is counted for as a Sw edish shareholder.

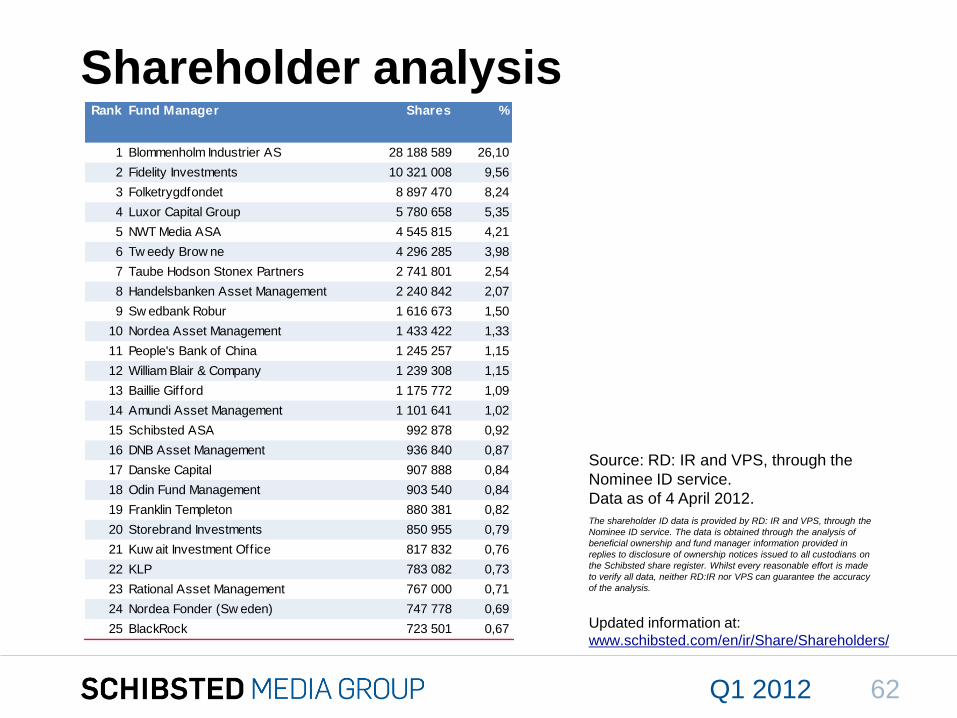

Shareholder analysis

The shareholder ID data is provided by RD: IR and VPS, through the

Nominee ID service. The data is obtained through the analysis of

beneficial ownership and fund manager information provided in

replies to disclosure of ownership notices issued to all custodians on

the Schibsted share register. Whilst every reasonable effort is made

to verify all data, neither RD:IR nor VPS can guarantee the accuracy

of the analysis.

Source: RD: IR and VPS, through the

Nominee ID service.

Data as of 4 April 2012.

Updated information at:

www.schibsted.com/en/ir/Share/Shareholders/

62Q1 2012

Rank Fund Manager Shares

1 Blommenholm Industrier AS 28 188 589 26,10

2 Fidelity Investments 10 321 008 9,56

3 Folketrygdfondet 8 897 470 8,24

4 Luxor Capital Group 5 780 658 5,35

5 NWT Media ASA 4 545 815 4,21

6 Tw eedy Brow ne 4 296 285 3,98

7 Taube Hodson Stonex Partners 2 741 801 2,54

8 Handelsbanken Asset Management 2 240 842 2,07

9 Sw edbank Robur 1 616 673 1,50

10 Nordea Asset Management 1 433 422 1,33

11 People's Bank of China 1 245 257 1,15

12 William Blair & Company 1 239 308 1,15

13 Baillie Gifford 1 175 772 1,09

14 Amundi Asset Management 1 101 641 1,02

15 Schibsted ASA 992 878 0,92

16 DNB Asset Management 936 840 0,87

17 Danske Capital 907 888 0,84

18 Odin Fund Management 903 540 0,84

19 Franklin Templeton 880 381 0,82

20 Storebrand Investments 850 955 0,79

21 Kuw ait Investment Office 817 832 0,76

22 KLP 783 082 0,73

23 Rational Asset Management 767 000 0,71

24 Nordea Fonder (Sw eden) 747 778 0,69

25 BlackRock 723 501 0,67

%

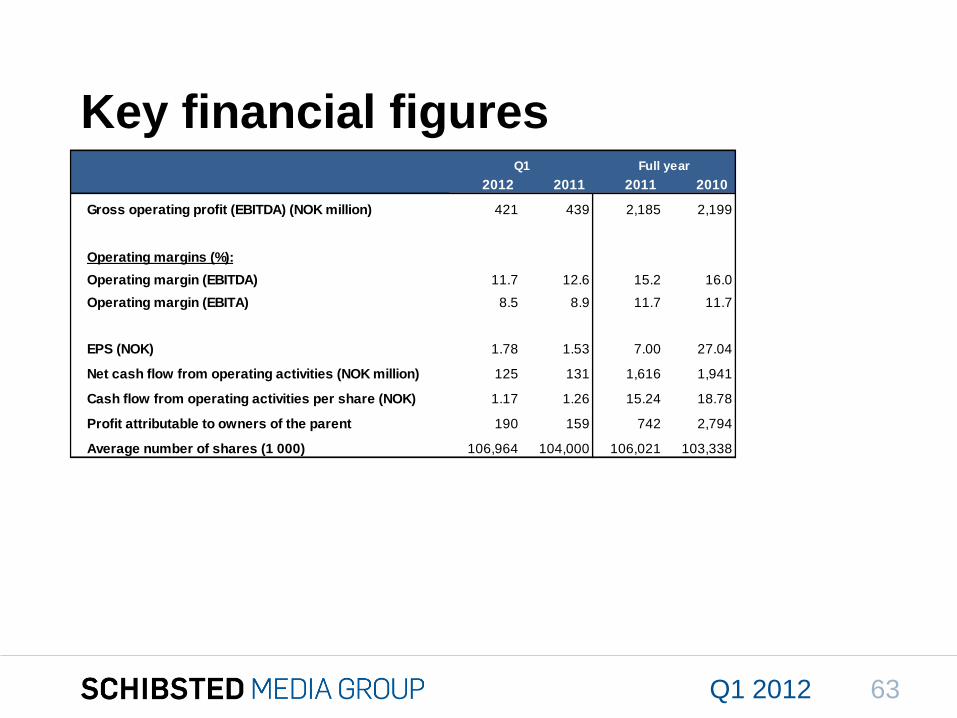

Key financial figures

2012 2011 2011 2010

Gross operating profit (EBITDA) (NOK million) 421 439 2,185 2,199

Operating margins (%):

Operating margin (EBITDA) 11.7 12.6 15.2 16.0

Operating margin (EBITA) 8.5 8.9 11.7 11.7

EPS (NOK) 1.78 1.53 7.00 27.04

Net cash flow from operating activities (NOK million) 125 131 1,616 1,941

Cash flow from operating activities per share (NOK) 1.17 1.26 15.24 18.78

Profit attributable to owners of the parent 190 159 742 2,794

Average number of shares (1 000) 106,964 104,000 106,021 103,338

Full yearQ1

Q1 2012 63

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

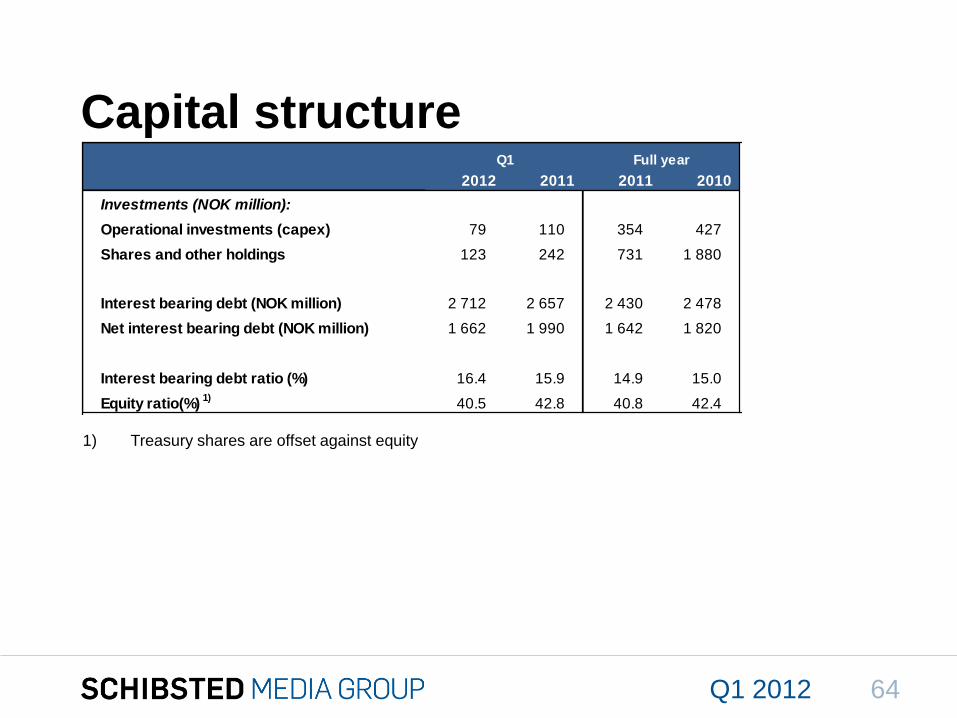

Capital structure

2012 2011 2011 2010

Investments (NOK million):

Operational investments (capex) 79 110 354 427

Shares and other holdings 123 242 731 1 880

Interest bearing debt (NOK million) 2 712 2 657 2 430 2 478

Net interest bearing debt (NOK million) 1 662 1 990 1 642 1 820

Interest bearing debt ratio (%) 16.4 15.9 14.9 15.0

Equity ratio(%) 1)

40.5 42.8 40.8 42.4

Full yearQ1

1) Treasury shares are offset against equity

Q1 2012 64

To get back,

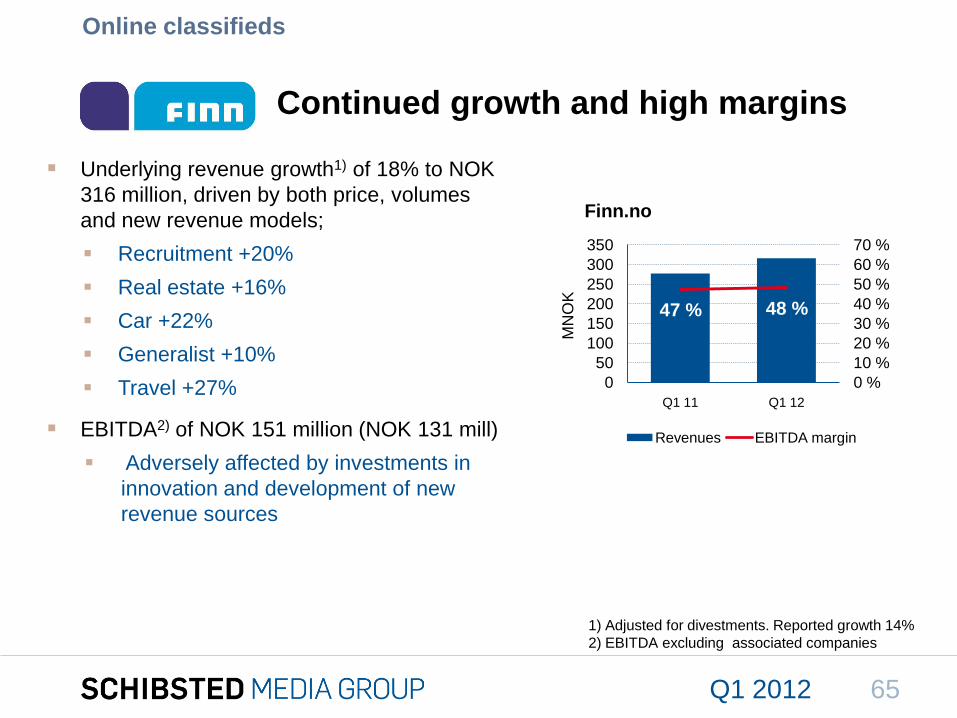

Continued growth and high margins

Underlying revenue growth1) of 18% to NOK

316 million, driven by both price, volumes

and new revenue models;

Recruitment +20%

Real estate +16%

Car +22%

Generalist +10%

Travel +27%

EBITDA2) of NOK 151 million (NOK 131 mill)

Adversely affected by investments in

innovation and development of new

revenue sources

Online classifieds

1) Adjusted for divestments. Reported growth 14%

2) EBITDA excluding associated companies

Finn.no

MN

OK

65Q1 2012

47 % 48 %

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

0

50

100

150

200

250

300

350

Q1 11 Q1 12

Revenues EBITDA margin

To get back,

Good growth and high margins

Underlying revenue growth1) of 11% to SEK

173 million, driven by both price, volumes

and new products

EBITDA of SEK 90 million (SEK 90 mill)

Investments in real estate and recruitment

verticals and discontinuation of group

internal license fees affect EBITDA margin

adversely

New products launched in Q3 2011 with

positive early response from the market

Online classifieds

1) Adjusted for discontinuation of Group internal revenues. Reported

growth was 7%.

Blocket.se/Bytbil.com

MS

EK

66Q1 2012

56 % 52 %

0 %

20 %

40 %

60 %

80 %

100 %

0

50

100

150

200

Q1 11 Q1 12

Revenues EBITDA margin

To get back,

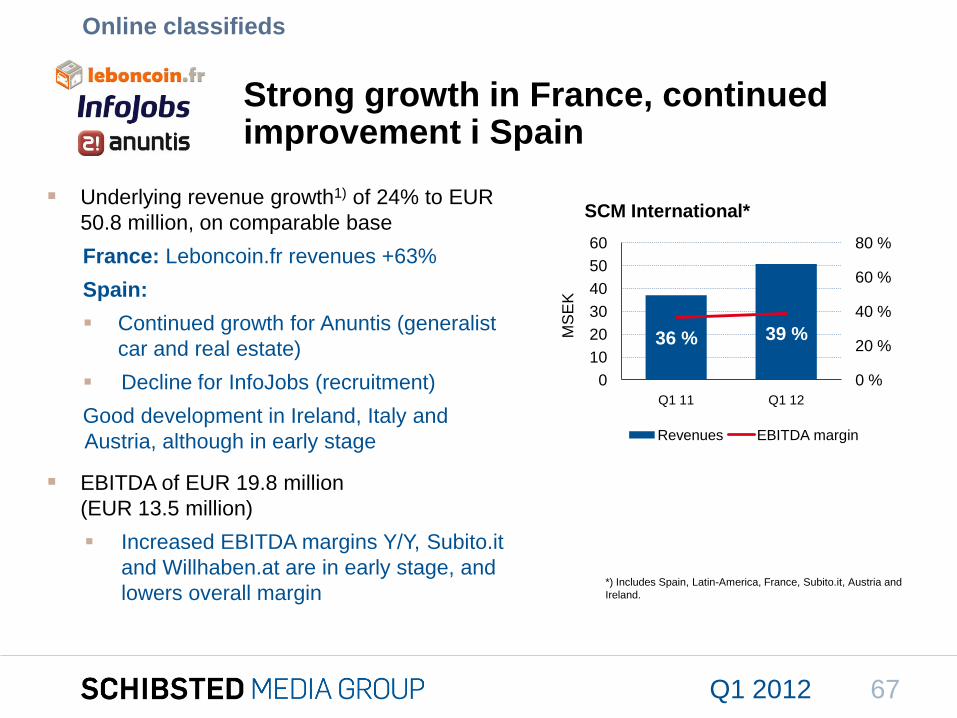

Strong growth in France, continuedimprovement i Spain

Underlying revenue growth1) of 24% to EUR

50.8 million, on comparable base

France: Leboncoin.fr revenues +63%

Spain:

Continued growth for Anuntis (generalist

car and real estate)

Decline for InfoJobs (recruitment)

Good development in Ireland, Italy and

Austria, although in early stage

EBITDA of EUR 19.8 million

(EUR 13.5 million)

Increased EBITDA margins Y/Y, Subito.it

and Willhaben.at are in early stage, and

lowers overall margin

Online classifieds

SCM International*

MS

EK

*) Includes Spain, Latin-America, France, Subito.it, Austria and

Ireland.

67Q1 2012

36 % 39 %

0 %

20 %

40 %

60 %

80 %

0

10

20

30

40

50

60

Q1 11 Q1 12

Revenues EBITDA margin

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

3 y

ea

rs

5 y

ea

rs

Online Classifieds

Balancing growth and valueP

rofi

tab

ilit

yIn

vestm

ent

Retu

rn

Start-up Traction Established

Time

Operations in established phaseOperations in investment phase

68Q1 2012

Two new sites in

Established phase as of

Q1 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

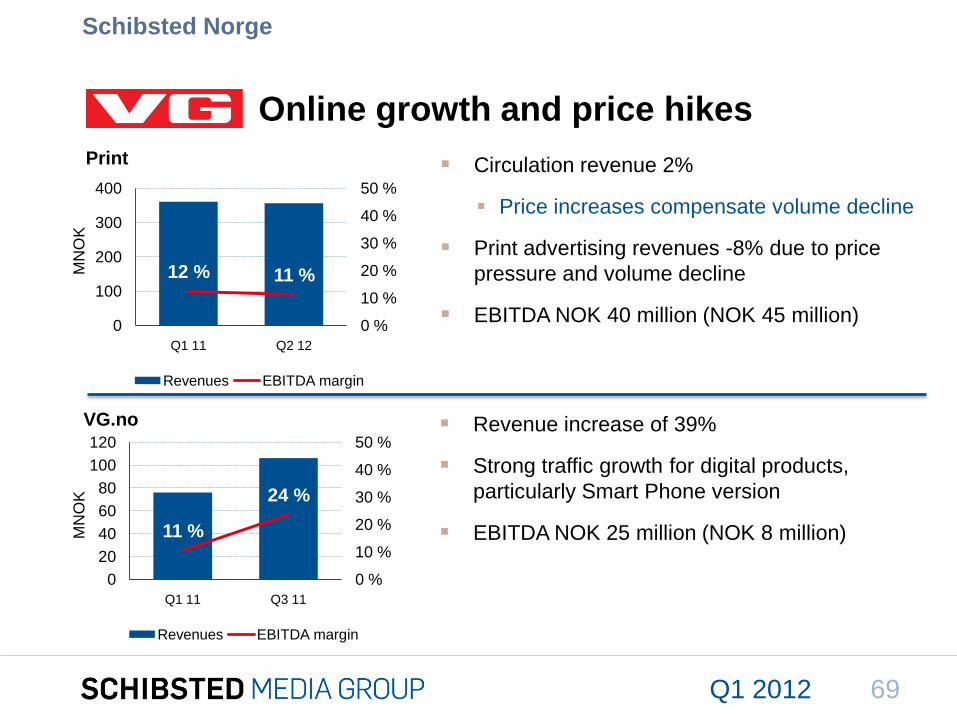

Circulation revenue 2%

Price increases compensate volume decline

Print advertising revenues -8% due to price

pressure and volume decline

EBITDA NOK 40 million (NOK 45 million)

Online growth and price hikes

Schibsted Norge

VG.no

MN

OK

MN

OK

Revenue increase of 39%

Strong traffic growth for digital products,

particularly Smart Phone version

EBITDA NOK 25 million (NOK 8 million)

69Q1 2012

11 %

24 %

0 %

10 %

20 %

30 %

40 %

50 %

0

20

40

60

80

100

120

Q1 11 Q3 11

Revenues EBITDA margin

12 % 11 %

0 %

10 %

20 %

30 %

40 %

50 %

0

100

200

300

400

Q1 11 Q2 12

Revenues EBITDA margin

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

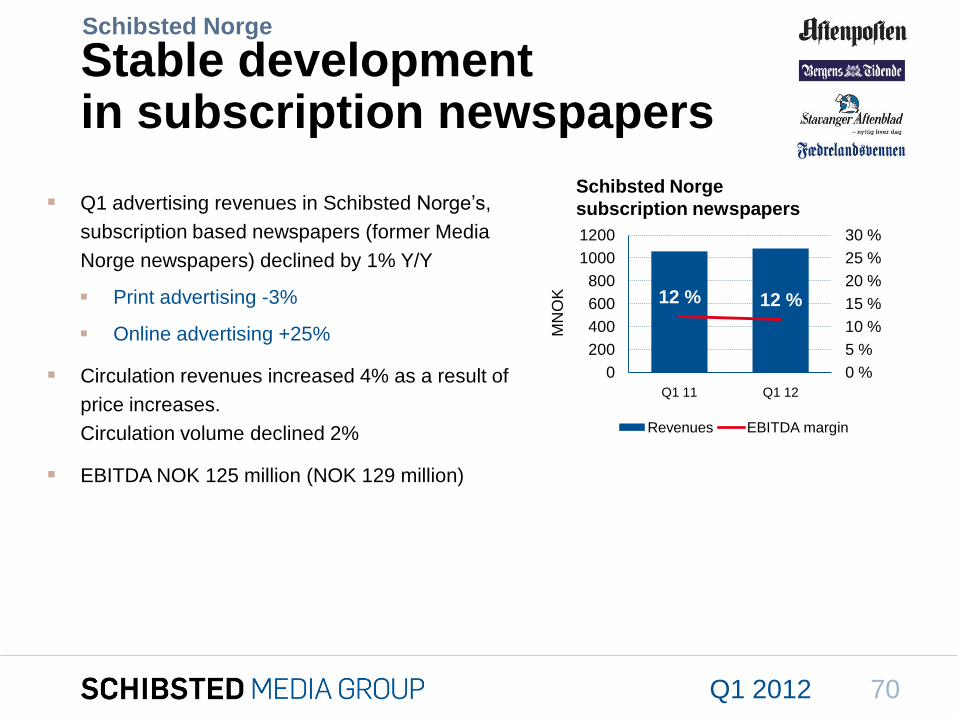

Q1 advertising revenues in Schibsted Norge’s,

subscription based newspapers (former Media

Norge newspapers) declined by 1% Y/Y

Print advertising -3%

Online advertising +25%

Circulation revenues increased 4% as a result of

price increases.

Circulation volume declined 2%

EBITDA NOK 125 million (NOK 129 million)

Stable development in subscription newspapers

Schibsted Norge

Schibsted Norge

subscription newspapers

MN

OK

70Q1 2012

12 % 12 %

0 %

5 %

10 %

15 %

20 %

25 %

30 %

0

200

400

600

800

1000

1200

Q1 11 Q1 12

Revenues EBITDA margin

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

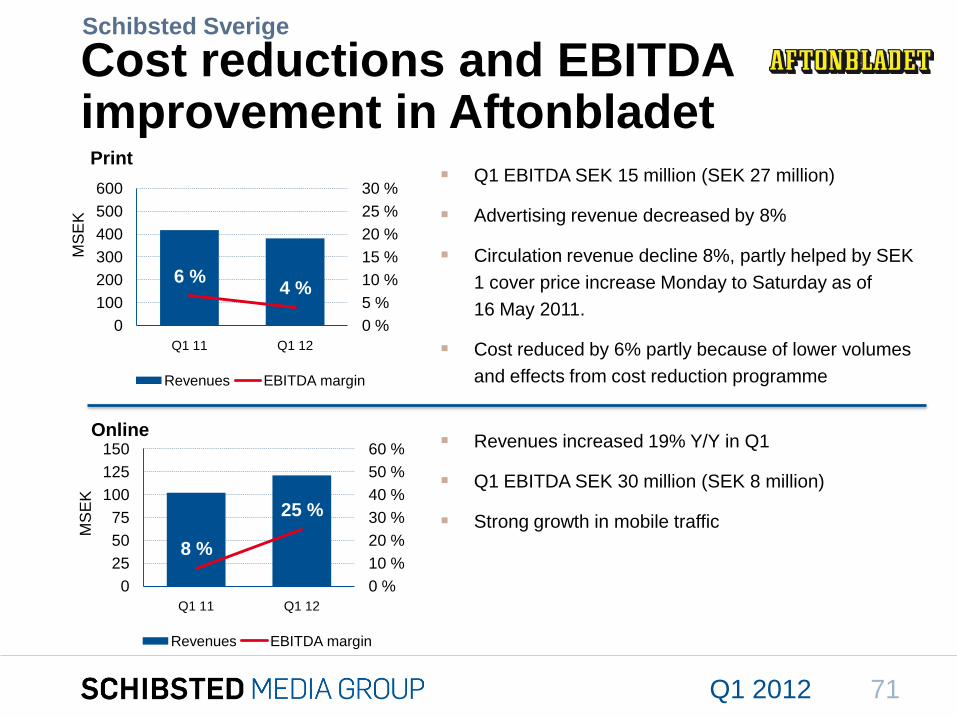

Q1 EBITDA SEK 15 million (SEK 27 million)

Advertising revenue decreased by 8%

Circulation revenue decline 8%, partly helped by SEK

1 cover price increase Monday to Saturday as of

16 May 2011.

Cost reduced by 6% partly because of lower volumes

and effects from cost reduction programme

Cost reductions and EBITDA improvement in Aftonbladet

Schibsted Sverige

Online Revenues increased 19% Y/Y in Q1

Q1 EBITDA SEK 30 million (SEK 8 million)

Strong growth in mobile traffic

MS

EK

MS

EK

71Q1 2012

6 %4 %

0 %

5 %

10 %

15 %

20 %

25 %

30 %

0

100

200

300

400

500

600

Q1 11 Q1 12

Revenues EBITDA margin

8 %

25 %

0 %

10 %

20 %

30 %

40 %

50 %

60 %

0

25

50

75

100

125

150

Q1 11 Q1 12

Revenues EBITDA margin

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

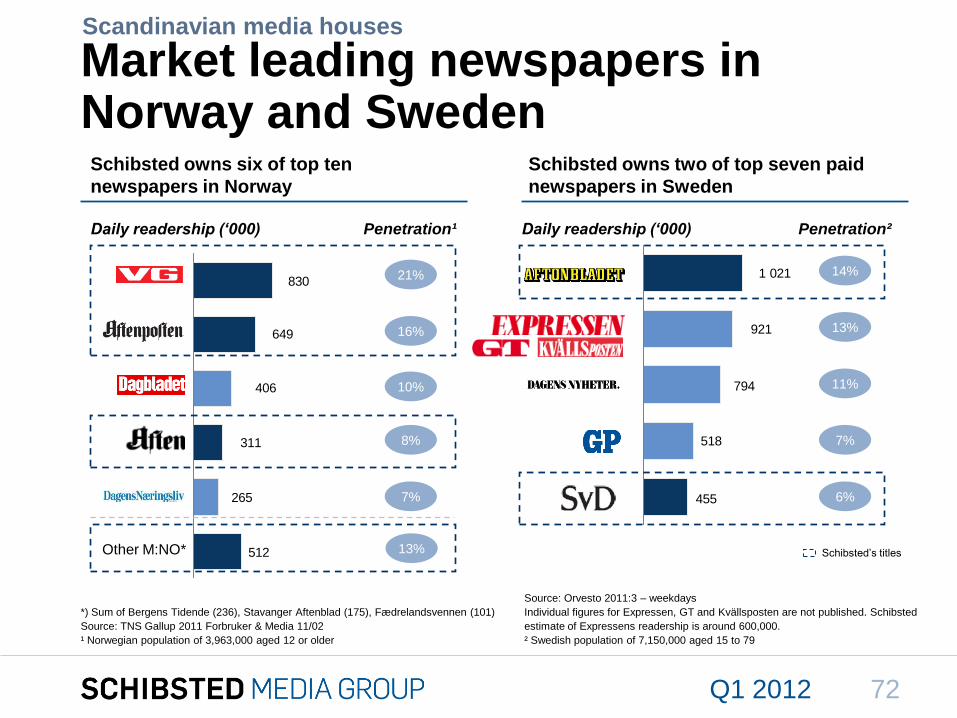

Market leading newspapers in Norway and Sweden

455

518

794

921

1 021830

649

406

311

265

512

Schibsted owns six of top ten

newspapers in Norway

Daily readership (‘000) Penetration¹ Daily readership (‘000) Penetration²

Source: Orvesto 2011:3 – weekdays

Individual figures for Expressen, GT and Kvällsposten are not published. Schibsted

estimate of Expressens readership is around 600,000.

² Swedish population of 7,150,000 aged 15 to 79

Schibsted owns two of top seven paid

newspapers in Sweden

Schibsted’s titles

21%

16%

10%

8%

7%

14%

13%

11%

7%

6%

Other M:NO* 13%

72Q1 2012

*) Sum of Bergens Tidende (236), Stavanger Aftenblad (175), Fædrelandsvennen (101)

Source: TNS Gallup 2011 Forbruker & Media 11/02

¹ Norwegian population of 3,963,000 aged 12 or older

Scandinavian media houses

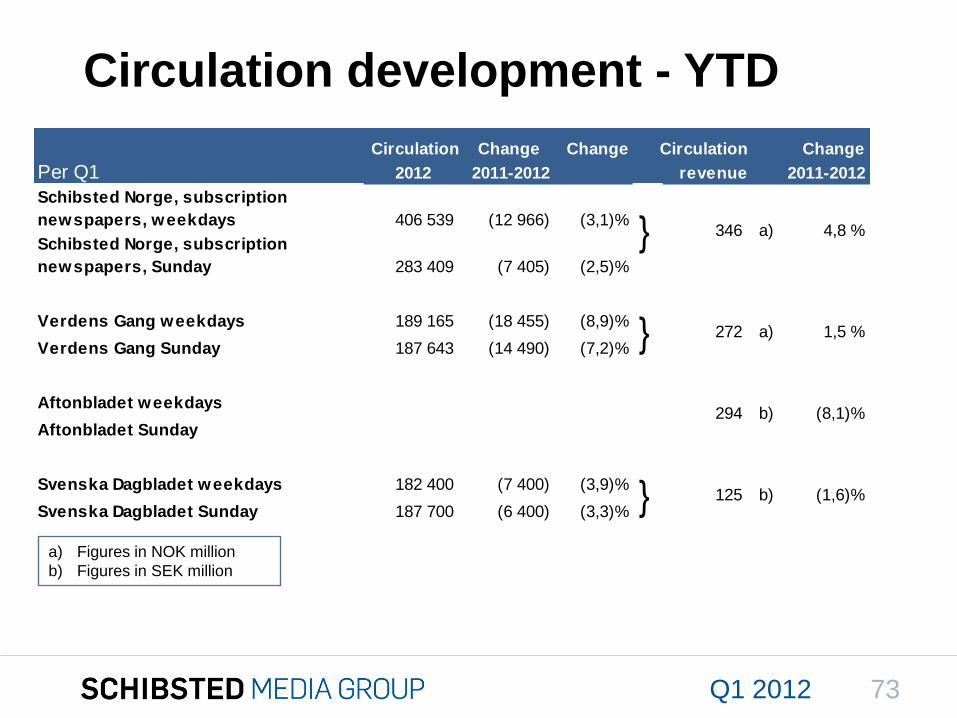

Circulation development - YTD

Circulation Change Change Circulation Change

Per Q1 2012 2011-2012 revenue 2011-2012

Schibsted Norge, subscription

newspapers, weekdays 406 539 (12 966) (3,1)%

Schibsted Norge, subscription

newspapers, Sunday 283 409 (7 405) (2,5)%

Verdens Gang weekdays 189 165 (18 455) (8,9)%

Verdens Gang Sunday 187 643 (14 490) (7,2)%

Aftonbladet weekdays

Aftonbladet Sunday

Svenska Dagbladet weekdays 182 400 (7 400) (3,9)%

Svenska Dagbladet Sunday 187 700 (6 400) (3,3)% } 125 b) (1,6)%

}

} 272

294

1,5 %

a) 4,8 %

(8,1)%

a)

b)

346

a) Figures in NOK million

b) Figures in SEK million

Q1 2012 73

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

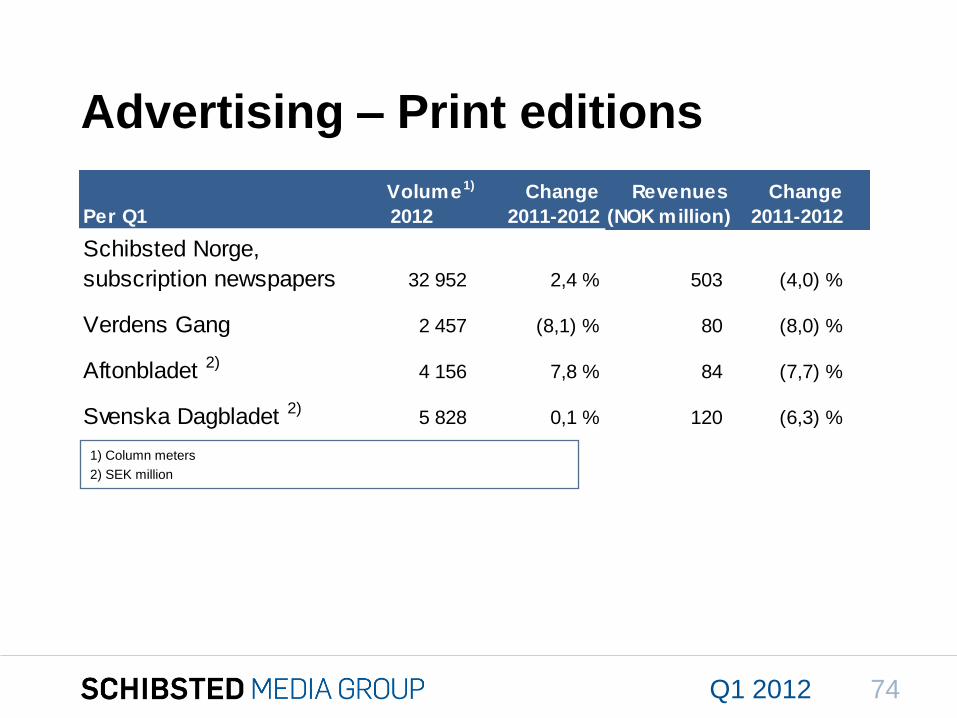

Advertising – Print editions

1) Column meters

2) SEK million

Volume1) Change Revenues Change

Per Q1 2012 2011-2012 (NOK million) 2011-2012

Schibsted Norge,

subscription newspapers 32 952 2,4 % 503 (4,0) %

Verdens Gang 2 457 (8,1) % 80 (8,0) %

Aftonbladet 2)4 156 7,8 % 84 (7,7) %

Svenska Dagbladet 2)5 828 0,1 % 120 (6,3) %

Q1 2012 74

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

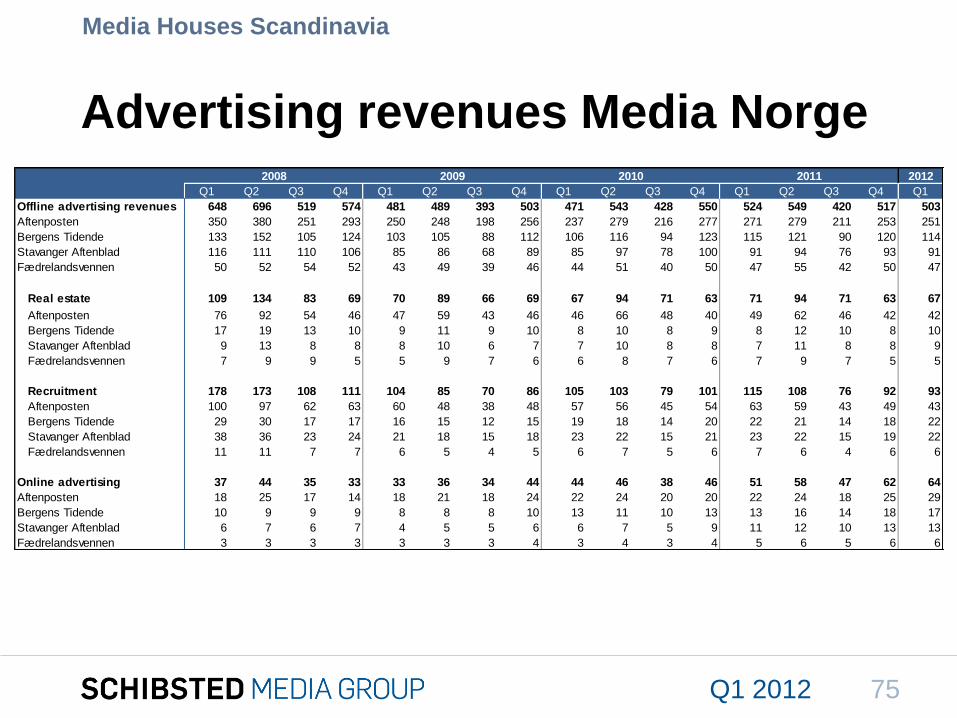

Advertising revenues Media Norge

Media Houses Scandinavia

75Q1 2012

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Offline advertising revenues 648 696 519 574 481 489 393 503 471 543 428 550 524 549 420 517 503

Aftenposten 350 380 251 293 250 248 198 256 237 279 216 277 271 279 211 253 251

Bergens Tidende 133 152 105 124 103 105 88 112 106 116 94 123 115 121 90 120 114

Stavanger Aftenblad 116 111 110 106 85 86 68 89 85 97 78 100 91 94 76 93 91

Fædrelandsvennen 50 52 54 52 43 49 39 46 44 51 40 50 47 55 42 50 47

Real estate 109 134 83 69 70 89 66 69 67 94 71 63 71 94 71 63 67

Aftenposten 76 92 54 46 47 59 43 46 46 66 48 40 49 62 46 42 42

Bergens Tidende 17 19 13 10 9 11 9 10 8 10 8 9 8 12 10 8 10

Stavanger Aftenblad 9 13 8 8 8 10 6 7 7 10 8 8 7 11 8 8 9

Fædrelandsvennen 7 9 9 5 5 9 7 6 6 8 7 6 7 9 7 5 5

Recruitment 178 173 108 111 104 85 70 86 105 103 79 101 115 108 76 92 93

Aftenposten 100 97 62 63 60 48 38 48 57 56 45 54 63 59 43 49 43

Bergens Tidende 29 30 17 17 16 15 12 15 19 18 14 20 22 21 14 18 22

Stavanger Aftenblad 38 36 23 24 21 18 15 18 23 22 15 21 23 22 15 19 22

Fædrelandsvennen 11 11 7 7 6 5 4 5 6 7 5 6 7 6 4 6 6

Online advertising 37 44 35 33 33 36 34 44 44 46 38 46 51 58 47 62 64

Aftenposten 18 25 17 14 18 21 18 24 22 24 20 20 22 24 18 25 29

Bergens Tidende 10 9 9 9 8 8 8 10 13 11 10 13 13 16 14 18 17

Stavanger Aftenblad 6 7 6 7 4 5 5 6 6 7 5 9 11 12 10 13 13

Fædrelandsvennen 3 3 3 3 3 3 3 4 3 4 3 4 5 6 5 6 6

2008 2009 2010 2011 2012

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

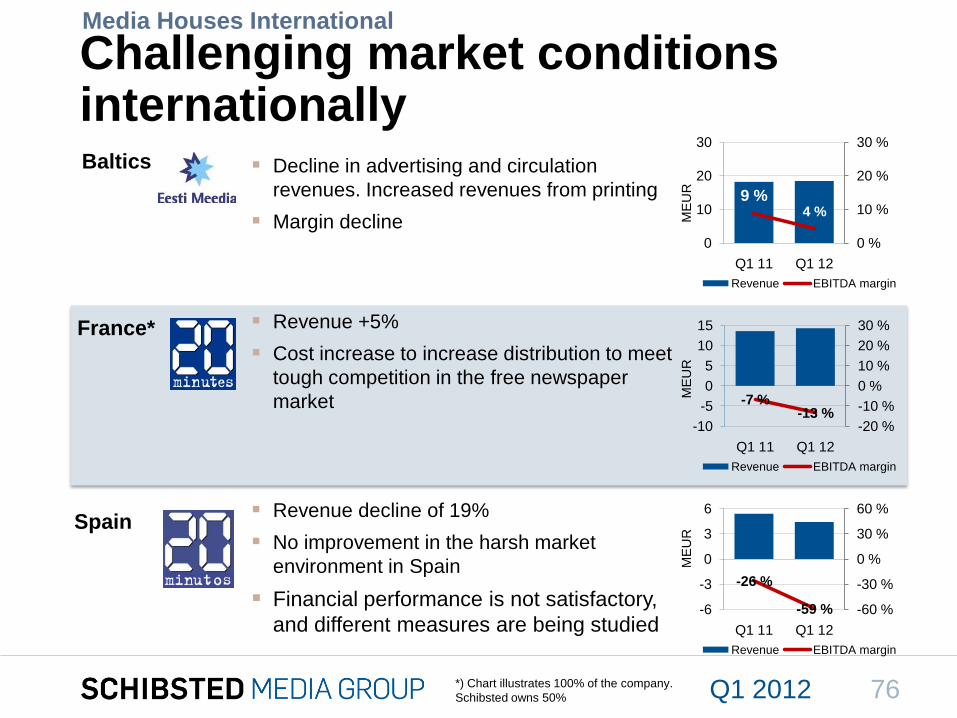

Challenging market conditions internationallyBaltics

France*

Spain

Decline in advertising and circulation

revenues. Increased revenues from printing

Margin decline

Revenue +5%

Cost increase to increase distribution to meet

tough competition in the free newspaper

market

Revenue decline of 19%

No improvement in the harsh market

environment in Spain

Financial performance is not satisfactory,

and different measures are being studied

Media Houses International

*) Chart illustrates 100% of the company.

Schibsted owns 50%M

EU

RM

EU

RM

EU

R76Q1 2012

-26 %

-59 % -60 %

-30 %

0 %

30 %

60 %

-6

-3

0

3

6

Q1 11 Q1 12

Revenue EBITDA margin

-7 %-13 %

-20 %

-10 %

0 %

10 %

20 %

30 %

-10

-5

0

5

10

15

Q1 11 Q1 12

Revenue EBITDA margin

9 %4 %

0 %

10 %

20 %

30 %

0

10

20

30

Q1 11 Q1 12

Revenue EBITDA margin

To get back,

Turn off ’CLASSIFICED’ via

2. Deactivate by clicking off the

Visit Schibsted’s homepages

www.schibsted.com/ir

Jo Christian Steigedal, VP Investor Relations

Tel: +47 2310 6600

Investor information

Schibsted ASA

Apotekergaten 10, P.O. Box 490 Sentrum, NO-0105 Oslo

Tel: +47 23 10 66 00. Fax: +47 23 10 66 01. E-mail:

www.schibsted.com

77Q1 2012

78Q1 2012