Embed Size (px)

Citation preview

MLC: HOW TO SOLVE IT

?Questions by Topic and Di�culty Level

Fall, 2017

YUFENG GUO

MLC: How To Solve It

Fall 2017

Yufeng Guo

c© 2017 Yufeng GuoAll rights reserved.

No part of this publication may be reproduced, stored in a retrieval system, ortransmitted in any form or by any means, electronic, mechanical, photocopying,recording, scanning, or otherwise, except as permitted under Section 107 or 108of the 1976 United States Copyright Act, without the prior written permissionof the author.

Limit of Liability/Disclaimer of Warranty. While the publisher and the authorhave used their best efforts in preparing this book, they make no representa-tions or warranties with respect to the accuracy or completeness of the contentsof this book. They make no expressed or implied warranties of any kind andassume no responsibility for errors or omissions. Neither the publisher nor theauthor shall be liable for any loss of profit or any other commercial damages,including but not limited to special, incidental, consequential, or other dam-ages in connection with or arising out of the use of information or programscontained in this book.

10 9 8 7 6 5 4 3 2

Second edition: May 2017

Printed in the United States of America

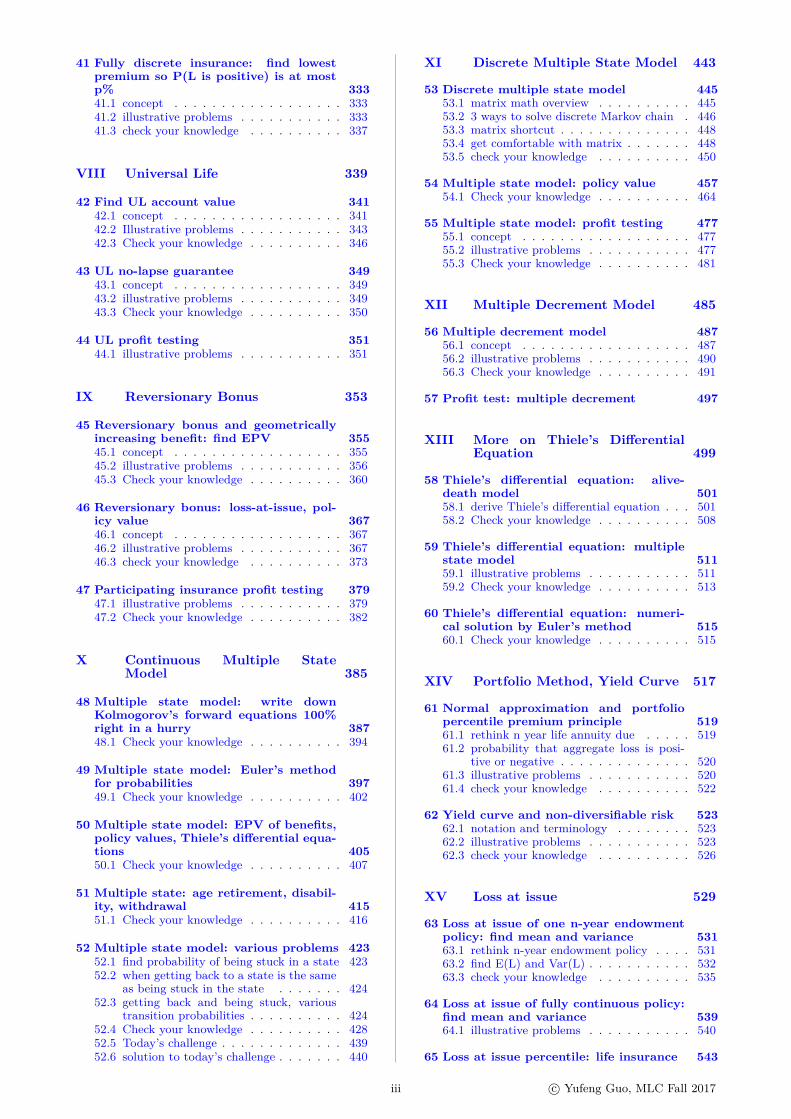

Contents

Contents i

Preface vwhy written answer questions are hard . . . . vintuition vs. rigor . . . . . . . . . . . . . . . . vidon’t second guess what SOA will test you . viihow to prepare for written answer questions . viihow this book can help you . . . . . . . . . . viiiMy story . . . . . . . . . . . . . . . . . . . . viiihow to pass MLC or any actuary exam . . . . viiiknow your stuff . . . . . . . . . . . . . . . . . ixa simple procedure beats the best mind . . . ixacknowledgement . . . . . . . . . . . . . . . . ixoutlook of actuary profession . . . . . . . . . ixFAQ . . . . . . . . . . . . . . . . . . . . . . . xerrata . . . . . . . . . . . . . . . . . . . . . . x

I PRELIMINARY 1

1 Advanced basics 31.1 increasing or decreasing function . . . . 31.2 calculus . . . . . . . . . . . . . . . . . . 41.3 integral . . . . . . . . . . . . . . . . . . 41.4 geometric progression . . . . . . . . . . 41.5 conditional probability, conditional ex-

pectation . . . . . . . . . . . . . . . . . 51.6 basic annuities . . . . . . . . . . . . . . 61.7 arithmetically increasing annuities . . . 61.8 geometrically increasing annuities . . . . 71.9 common probability distributions . . . . 81.10 integral shortcuts . . . . . . . . . . . . . 81.11 Second Fundamental Theorem of Calcu-

lus: FTC 2 . . . . . . . . . . . . . . . . 10

2 Calculator shortcuts 112.1 find mean and variance of a discrete ran-

dom variable . . . . . . . . . . . . . . . 112.2 use a bigger unit . . . . . . . . . . . . . 132.3 find DPP: discounted payback period . . 152.4 find IRR . . . . . . . . . . . . . . . . . . 152.5 pension salary: how to avoid off-by-1 error 15

3 Total probability, mean, variance: dis-crete or continuous 17

4 normal approximation, continuity cor-rection 21

II Single Life: quickly get up tospeed 25

5 APV, life table, death rate 275.1 FM annuity vs. MLC annuity, what’s

the difference? . . . . . . . . . . . . . . 275.2 EPV of n-year term insurance . . . . . 295.3 continuous life annuity and continuous

term insurance . . . . . . . . . . . . . . 305.4 check your knowledge . . . . . . . . . . 31

6 Life annuity, life insurance: EPV recur-sive formulas 35

6.1 concept . . . . . . . . . . . . . . . . . . 356.2 whole life annuity and whole life insurance 366.3 Check your knowledge . . . . . . . . . . 37

7 Select and ultimate table vs. ultimatetable 397.1 concept . . . . . . . . . . . . . . . . . . 397.2 Check your knowledge . . . . . . . . . . 41

III Single Life: build intuition andrigor 45

8 Survival model 478.1 two time-till-death random variables . . 478.2 connection: two time-till-death random

variables . . . . . . . . . . . . . . . . . . 478.3 determine whether survival function is

legitimate . . . . . . . . . . . . . . . . . 488.4 probability density function . . . . . . . 488.5 special death rate symbol revisited . . . 498.6 curtate future lifetime . . . . . . . . . . 498.7 find moments: continuous and curtate

future life time . . . . . . . . . . . . . . 508.8 find moments of min function . . . . . . 518.9 term expectation of life: e and e with a

circle . . . . . . . . . . . . . . . . . . . . 538.10 relationship: term expectation of life

and EPV of annuity . . . . . . . . . . . 538.11 relationship: e and e with a circle . . . . 538.12 UDD . . . . . . . . . . . . . . . . . . . . 538.13 check your knowledge . . . . . . . . . . 54

9 force of mortality 599.1 build intuition . . . . . . . . . . . . . . . 599.2 rigorously define force of mortality . . . 599.3 force of mortality must satisfy two con-

ditions . . . . . . . . . . . . . . . . . . . 619.4 transformation . . . . . . . . . . . . . . 629.5 Check your knowledge . . . . . . . . . . 63

10 Common survival laws 7310.1 constant force of mortality . . . . . . . 7310.2 constant force of mortality between

birthdays . . . . . . . . . . . . . . . . . 7310.3 constant probability density throughout 7310.4 constant probability between birthdays 7310.5 De Moivre’s law . . . . . . . . . . . . . . 7310.6 Gompertz law . . . . . . . . . . . . . . . 7310.7 Makeham’s law . . . . . . . . . . . . . . 7410.8 Check your knowledge . . . . . . . . . . 74

11 Rigorously define life insurance products 7711.1 Insurances Payable at the Moment of

Death . . . . . . . . . . . . . . . . . . . 7711.2 TYPES OF INSURANCE . . . . . . . . 7811.3 Insurances Payable at the End of the

Year of Death . . . . . . . . . . . . . . . 8411.4 Relationships between Insurances

Payable at the Moment of death andthe End of the Year of Death . . . . . . 87

11.5 Formula Summary . . . . . . . . . . . . 8811.6 Check your knowledge . . . . . . . . . . 89

12 Life annuity policy types: rigorously de-fined 10712.1 term life annuity due . . . . . . . . . . . 10712.2 term life annuity immediate . . . . . . . 10812.3 link between term life annuity due and

term endowment . . . . . . . . . . . . . 10912.4 term continuous life annuity . . . . . . . 11012.5 continuous whole life annuity . . . . . . 11112.6 accumulation with interest and survivor-

ship . . . . . . . . . . . . . . . . . . . . 11212.7 Check your knowledge . . . . . . . . . . 112

i

13 Variable insurance 121

14 m-thly, UDD, W2, W3, W3*, claim ac-celeration 12514.1 m-thly n-year term life insurance . . . . 12514.2 EPV: m-thly term insurance under UDD 12714.3 UDD: claim acceleration approach . . . 12814.4 EPV: m-thly n-year annuity due under

UDD . . . . . . . . . . . . . . . . . . . . 13014.5 check your knowledge . . . . . . . . . . 13214.6 Euler-Maclaurin formula . . . . . . . . . 13314.7 Woolhouse’s formula . . . . . . . . . . . 13514.8 EPV of m-thly whole life annuity due:

alpha and beta under UDD . . . . . . . 13614.9 Check your knowledge . . . . . . . . . . 139

15 double punch: m-thly and fractionalage: as in AMLCR Example 7.10 14515.1 Check your knowledge . . . . . . . . . . 146

16 Calculate change 149

IV Multiple Lives and Joint Lives 151

17 Joint life: basics 15317.1 concept . . . . . . . . . . . . . . . . . . 15317.2 illustrative problems . . . . . . . . . . . 15617.3 check your knowledge . . . . . . . . . . 161

18 Joint life annuity including reversionaryannuity 16718.1 concept . . . . . . . . . . . . . . . . . . 16718.2 illustrative problems . . . . . . . . . . . 16718.3 check your knowledge . . . . . . . . . . 168

19 Common shock 17119.1 concept . . . . . . . . . . . . . . . . . . 17119.2 illustrative problems . . . . . . . . . . . 171

20 Joint lives: double integrals 17520.1 concept . . . . . . . . . . . . . . . . . . 17520.2 illustrative problems . . . . . . . . . . . 17520.3 Check your knowledge . . . . . . . . . . 182

21 3 lives 18921.1 concept . . . . . . . . . . . . . . . . . . 189

V Policy Value 191

22 Loss-at-issue random variable, equiva-lence principle, net premium, gross pre-mium 19322.1 equivalence premium principle . . . . . . 19322.2 exam change: now vs. pre 2014 . . . . . 19322.3 percent-of-premium expense, per policy

expense, per 1000 insurance expense . . 19422.4 Check your knowledge . . . . . . . . . . 198

23 Find policy value: gross, net, expense 20923.1 concept . . . . . . . . . . . . . . . . . . 21023.2 policy value as a group savings account

value per policy in force . . . . . . . . . 21223.3 how to solve it . . . . . . . . . . . . . . 21423.4 Check your knowledge . . . . . . . . . . 219

24 Policy value: miscellaneous topics 22924.1 purpose of reserve . . . . . . . . . . . . 22924.2 policy gain each year: endowment vs.

term . . . . . . . . . . . . . . . . . . . . 22924.3 policy value immediately after anniversary23424.4 N identical policies . . . . . . . . . . . . 23524.5 prove retrospective policy value equal to

prospective policy value . . . . . . . . . 23624.6 policy value of m-thly . . . . . . . . . . 236

24.7 policy value evaluation date is neither abenefit or premium dates . . . . . . . . 237

24.8 policy value interpolation . . . . . . . . 23824.9 derive and use policy value recursive for-

mula . . . . . . . . . . . . . . . . . . . . 238

25 Policy value: various topics 24125.1 special formulas . . . . . . . . . . . . . . 24125.2 level expenses at the beginning of the

year for all years . . . . . . . . . . . . . 24125.3 death benefit depends on previous policy

value . . . . . . . . . . . . . . . . . . . . 24225.4 constant DSAR . . . . . . . . . . . . . . 24325.5 constant DSAR at least for some years . 244

26 Policy alteration 24726.1 concept . . . . . . . . . . . . . . . . . . 24726.2 illustrative problems . . . . . . . . . . . 24726.3 Check your knowledge . . . . . . . . . . 248

27 Full preliminary term reserve 25127.1 check your knowledge . . . . . . . . . . 253

28 Return of premium policies 25728.1 concept . . . . . . . . . . . . . . . . . . 25728.2 Check your knowledge . . . . . . . . . . 260

29 ROP: single premium 265

30 Profit test 26730.1 concept . . . . . . . . . . . . . . . . . . 26730.2 illustrative problems . . . . . . . . . . . 26830.3 Check your knowledge . . . . . . . . . . 269

31 Zeroized reserve 27531.1 illustrative problems . . . . . . . . . . . 27531.2 Check your knowledge . . . . . . . . . . 276

32 Profit by source 27732.1 concept . . . . . . . . . . . . . . . . . . 27732.2 illustrative problems . . . . . . . . . . . 27732.3 Check your knowledge . . . . . . . . . . 281

33 DSAR: death strain at risk 28533.1 illustrative problems . . . . . . . . . . . 285

34 Gross premium: adjust expense inflation 287

VI All about percentiles 291

35 percentile, median, quantile 29335.1 definitions . . . . . . . . . . . . . . . . . 29335.2 percentile of big 3 distributions: uni-

form, exponential, normal . . . . . . . . 29535.3 two rules about percentile . . . . . . . . 295

36 find n-th percentile of Tx and Kx underIllustrative Life Table 29736.1 how to solve it . . . . . . . . . . . . . . 29736.2 check your knowledge . . . . . . . . . . 300

37 Graph Y and Z 305

38 Probability Y, Z less than 313

39 Find percentile: Y and Z 31939.1 core concept . . . . . . . . . . . . . . . . 31939.2 illustrative problems . . . . . . . . . . . 31939.3 check your knowledge . . . . . . . . . . 323

VII lowest premium to achieve goals 327

40 Fully continuous insurance: find lowestpremium so P(L is positive) is at mostp% 329

41 Fully discrete insurance: find lowestpremium so P(L is positive) is at mostp% 33341.1 concept . . . . . . . . . . . . . . . . . . 33341.2 illustrative problems . . . . . . . . . . . 33341.3 check your knowledge . . . . . . . . . . 337

VIII Universal Life 339

42 Find UL account value 34142.1 concept . . . . . . . . . . . . . . . . . . 34142.2 Illustrative problems . . . . . . . . . . . 34342.3 Check your knowledge . . . . . . . . . . 346

43 UL no-lapse guarantee 34943.1 concept . . . . . . . . . . . . . . . . . . 34943.2 illustrative problems . . . . . . . . . . . 34943.3 Check your knowledge . . . . . . . . . . 350

44 UL profit testing 35144.1 illustrative problems . . . . . . . . . . . 351

IX Reversionary Bonus 353

45 Reversionary bonus and geometricallyincreasing benefit: find EPV 35545.1 concept . . . . . . . . . . . . . . . . . . 35545.2 illustrative problems . . . . . . . . . . . 35645.3 Check your knowledge . . . . . . . . . . 360

46 Reversionary bonus: loss-at-issue, pol-icy value 36746.1 concept . . . . . . . . . . . . . . . . . . 36746.2 illustrative problems . . . . . . . . . . . 36746.3 check your knowledge . . . . . . . . . . 373

47 Participating insurance profit testing 37947.1 illustrative problems . . . . . . . . . . . 37947.2 Check your knowledge . . . . . . . . . . 382

X Continuous Multiple StateModel 385

48 Multiple state model: write downKolmogorov’s forward equations 100%right in a hurry 38748.1 Check your knowledge . . . . . . . . . . 394

49 Multiple state model: Euler’s methodfor probabilities 39749.1 Check your knowledge . . . . . . . . . . 402

50 Multiple state model: EPV of benefits,policy values, Thiele’s differential equa-tions 40550.1 Check your knowledge . . . . . . . . . . 407

51 Multiple state: age retirement, disabil-ity, withdrawal 41551.1 Check your knowledge . . . . . . . . . . 416

52 Multiple state model: various problems 42352.1 find probability of being stuck in a state 42352.2 when getting back to a state is the same

as being stuck in the state . . . . . . . 42452.3 getting back and being stuck, various

transition probabilities . . . . . . . . . . 42452.4 Check your knowledge . . . . . . . . . . 42852.5 Today’s challenge . . . . . . . . . . . . . 43952.6 solution to today’s challenge . . . . . . . 440

XI Discrete Multiple State Model 443

53 Discrete multiple state model 44553.1 matrix math overview . . . . . . . . . . 44553.2 3 ways to solve discrete Markov chain . 44653.3 matrix shortcut . . . . . . . . . . . . . . 44853.4 get comfortable with matrix . . . . . . . 44853.5 check your knowledge . . . . . . . . . . 450

54 Multiple state model: policy value 45754.1 Check your knowledge . . . . . . . . . . 464

55 Multiple state model: profit testing 47755.1 concept . . . . . . . . . . . . . . . . . . 47755.2 illustrative problems . . . . . . . . . . . 47755.3 Check your knowledge . . . . . . . . . . 481

XII Multiple Decrement Model 485

56 Multiple decrement model 48756.1 concept . . . . . . . . . . . . . . . . . . 48756.2 illustrative problems . . . . . . . . . . . 49056.3 Check your knowledge . . . . . . . . . . 491

57 Profit test: multiple decrement 497

XIII More on Thiele’s DifferentialEquation 499

58 Thiele’s differential equation: alive-death model 50158.1 derive Thiele’s differential equation . . . 50158.2 Check your knowledge . . . . . . . . . . 508

59 Thiele’s differential equation: multiplestate model 51159.1 illustrative problems . . . . . . . . . . . 51159.2 Check your knowledge . . . . . . . . . . 513

60 Thiele’s differential equation: numeri-cal solution by Euler’s method 51560.1 Check your knowledge . . . . . . . . . . 515

XIV Portfolio Method, Yield Curve 517

61 Normal approximation and portfoliopercentile premium principle 51961.1 rethink n year life annuity due . . . . . 51961.2 probability that aggregate loss is posi-

tive or negative . . . . . . . . . . . . . . 52061.3 illustrative problems . . . . . . . . . . . 52061.4 check your knowledge . . . . . . . . . . 522

62 Yield curve and non-diversifiable risk 52362.1 notation and terminology . . . . . . . . 52362.2 illustrative problems . . . . . . . . . . . 52362.3 check your knowledge . . . . . . . . . . 526

XV Loss at issue 529

63 Loss at issue of one n-year endowmentpolicy: find mean and variance 53163.1 rethink n-year endowment policy . . . . 53163.2 find E(L) and Var(L) . . . . . . . . . . . 53263.3 check your knowledge . . . . . . . . . . 535

64 Loss at issue of fully continuous policy:find mean and variance 53964.1 illustrative problems . . . . . . . . . . . 540

65 Loss at issue percentile: life insurance 543

iii c© Yufeng Guo, MLC Fall 2017

66 loss at issue percentile: fully continuous 553

67 Loss at issue percentile: life annuity 557

XVI Pension Mathematics 561

68 Pension math: accrued liability andnormal cost 56368.1 actuarial cost methods . . . . . . . . . . 56368.2 PUC, TUC, AL, NC . . . . . . . . . . . 56368.3 accrued benefit recursive formula . . . . 56468.4 illustrative problems . . . . . . . . . . . 56468.5 Check your knowledge . . . . . . . . . . 570

69 Rate of salary, salary scale, and salary 57769.1 concept . . . . . . . . . . . . . . . . . . 57769.2 illustrative problems . . . . . . . . . . . 577

69.3 Check your knowledge . . . . . . . . . . 578

70 Replacement ratio, DC contribution 58570.1 illustrative problems . . . . . . . . . . . 58570.2 Check your knowledge . . . . . . . . . . 586

71 Multiple retirement ages, service table,benefit reduction 59571.1 illustrative problems . . . . . . . . . . . 59571.2 Check your knowledge . . . . . . . . . . 600

72 EPV of accrued pension withdrawalbenefit, COLA 60972.1 illustrative problems . . . . . . . . . . . 60972.2 Check your knowledge . . . . . . . . . . 611

73 Actuarial liability, normal cost: multi-ple members 617

Preface

In the pre-2014 MLC exams, all questions were multiple choice. Developing intuition was paramount and developingrigor was thrown out of the window. You never needed to memorize how to precisely define a symbol or rigorouslyprove a formula; intuition was all you needed to pass a multiple choice exam. Now tables were turned and writtenanswer questions count for 60% of the MLC exam points. To pass MLC, you need to build intuition and, moreimportantly, rigor as rigor is far more difficult to build than intuition.

Intuition alone is not enough to pass MLC

When SOA added written answer questions to MLC in 2014, it was a paradigm shift. Gone were the days whenan exam candidate just needed to understand the essence of actuarial concepts without having to worry about how torigorously define anything. Unfortunately, many students still study for the MLC the old ways. This is how a typicalstudent, Jones, studies for in MLC:

• Jones’ focus is on understanding concepts intuitively without any concern on how to define anything rigorously.

• Jones spends most of his study time on perfecting multiple choice questions.

– It’s easy for Jones to find tons of old SOA or CAS multiple choice questions to hone his skill– Multiple choices are fun because Jones can use the power of elimination, not to mention there are loads of

shortcuts for him to use (such as constant force of mortality shortcuts in Ax and ax).

• It was only one month before the actual exam when he tried a newly released MLC exam under the exam condition.He scored well in the multiple choice part of the exam, but he did poorly in written answer questions. To his surprise,Jones discovered that written answer questions were the real enemy, but it was too late to turn the tide.

• The final exam day arrived. Though none of the constant force of mortality shortcuts he memorized were testedin the exam, he aced the multiple choice section nonetheless. However, he failed miserably in the written answerpart. SOA seemed to know exactly where to poke Jones’ weakness.

• Jones failed and now is restudying for MLC.

why written answer questions are hard

Suppose you need to answer two sets of questions, one set is multiple choice and the other written answer.

Example 0.0.1

3

4 x

What is the value of x?(A)3 (B)4 (C)5 (D)6 (E)7

Example 0.0.2

3

4 x

(a) (3 points) Derive the Pythagorean theorem fromthe first principle. In addition, show that x = 5.

(b) (4 points) Aliens captured the earth and threat-ened to annihilate the human race unless theywere convinced that humans made at least oneimportant discovery. You were sent by yourfollow earthmen to convince aliens that thePythagorean theorem was a vital discovery. Ex-plain why Pythagorean theorem is an importantdiscovery.

v

Example 0.0.3

For a fully discrete whole life insurance of 100,000 on(50), you are given:

(i) The gross premium is calculated under the equiv-alence principle.

(ii) Expenses, payable at the beginning of the year,are:

% of Premium Per PolicyFirst Year 40% 25Renewal 5% 10

(iii) Claim cost: 100 per death.

(iv) Mortality: Illustrative Life Table.

(v) i = 0.06

Calculate the expense premium for this policy.(A)120 (B)170 (C)220 (D)270 (E)320

Calculate the expense premium policy value at theend of Policy Year 10.(A)− 600 (B)− 200 (C)200 (D)600 (E)1, 000

Example 0.0.4

For a fully discrete whole life insurance of 100,000 on(50), you are given:

(i) The gross premium is calculated under the equiv-alence principle.

(ii) Expenses, payable at the beginning of the year,are:

% of Premium Per PolicyFirst Year 40% 25Renewal 5% 10

(iii) Claim cost: 100 per death.

(iv) Mortality: Illustrative Life Table.

(v) i = 0.06

(a) (2 points) Define the expense premium.

(b) (3 points) Show that the prospective expense pre-mium policy value at the end of Policy Year 10 is−600 to the nearest of 10. Explain why the ex-pense premium policy value at the end of PolicyYear 10 is negative.

(c) (2 points) Prove that the retrospective expensepremium policy value and the prospective ex-pense premium policy value at the end of PolicyYear 10 are equal.

The cognitive skill required to solve a written answer question is significantly higher than what is required to solve amultiple choice question.

intuition vs. rigor

Let’s use the concept of the force of mortality and explore the difference between intuitive thinking and rigorous thinking.

What’s the force of mortality? Well, it’s kind of like the force of interest. The force of interest is aninstantaneous rate of increase of your money in a savings account. The force of mortality is an instanta-neous rate of increase of what? Yes, an instantaneous rate of increase of the number of survivors `x or aninstantaneous rate of increase of the survival function.

But wait! There’s a catch. While money grows over time, the survival function decreases over time –people die over time. So we need to add a negative sign to prevent the force of mortality from becomingnegative. No body likes negative numbers. All I need to do is to translate the force of interest formula

A(t) = A(0) exp

(∫ t

0δ(s)ds

).

into the force of mortality formula:

tpx = 0px exp

(−∫ t

0µx(s)ds

)

I got it! What else? Wait! The next formula is like a definition. I shall memorize it.

µx(t) = − d

dtln tpx

That’s about it. I definitely don’t want to clog my head with useless proofs or fancy jargons invented byscholars who live in the cloud. Next, why don’t I solve a bunch of (multiple choice) problems to cement myunderstanding?

Here’s a rigorous approach to the force of mortality:

Let T0 represent the future lifetime of a newborn. Let Tx represent the future lifetime of life aged x. The forceof mortality at age x is represented by µx. We define µx as:

µx = limdx→0+

1dxPr[T0 ≤ x+ dx | T0 > x]

However, Pr[Tx ≤ t] = Pr[T0 ≤ x+ t | T0 > x]

⇒ µx = limdx→0+

1dxPr[Tx ≤ dx]

Let Sx = P (Tx > t) represent the survival function of Tx. The above equation can be rewritten as:

µx = limdx→0+

1dx

(1− Sx(dx)

). . .

While intuitive thinking has served you well in P and FM, it’s no longer sufficient for passing MLC. SOA wants toencourage the next generation of actuaries to be articulate, precise, and resourceful in their professions who can handleanything thrown at them. It doesn’t want to send a bunch of smart calculators to the ASA and FSA destinations.

don’t second guess what SOA will test you

While multiple choice questions tend to be more predictable over time, for written answer questions the sky is the limit.SOA can ask you to do anything, from defining a rudimentary concept such as tpx, to explaining an obscure idea ofzeroized reserves, to the dreaded work of deriving Thiele’s differential equation. To bring this idea home, let’s look atthe following example:

Example 0.0.5

(MLC Fall 2015 Q5) ( 10 points ) Dana buys a Type B universal life contract of 100,000. You are given:

(i)

Policy Year k AnnualPremium

Annual Costof Insurance

Rate Per1000

Percent ofPremiumCharge

AnnualExpenseCharge

SurrenderCharge

1 1000 —— 60% —— ——2 P2 2 10% 10 2003 P3 3 10% 10 100

k ≥ 4 Pk k 5% 10 0

(ii) The credit interest rate is ic = 0.06

(iii) Dana’s account value at the end of year 1 is 165.

(iv) Except as indicated, there are no deaths or surrenders.

(a) (2 points) Show that if P2 were 1000, Dana’s account value at the end of year 2 would be 920 to the nearest 10.You should calculate the account value to the nearest 1.

(b) (2 points) Dana’s account value at the end of year 3 can be expressed as aP2 + bP3 + c. Calculate a, b, and c.

(c) (4 points) In year 2, Dana pays a premium of 1000 with probability 0.6, or 200 with probability 0.4.If he paid 1000 in year 2, then in year 3 he will pay either 1000 with probability 0.6, or 200 with probability 0.4.If he paid 200 in year 2, then in year 3 he will pay either 1000 with probability 0.2, or 200 with probability 0.8.

(i) Calculate the expected death benefit payable at the end of year 3, if Dana dies then.(ii) Calculate the expected surrender benefit payable at the end of year 3, if Dana surrenders the contract then.

(d) (2 points) Dana’s identical twin, Mark, buys a contract identical to Dana’s. If Mark pays 1000 every year, Mark’saccount value at the end of year 10 will be 5114.Mark will pay premiums of 1000 in 9 of the first 10 years. Mark will pay no premium in one year, with the yearof no premium equally likely to be year 3 or year 10.Calculate Mark’s expected surrender value at the end of year 10.

The setup of this question, especially Part (b), (c), and (d), is simply the work of a genius. You have a better chanceof getting struck by lightning than guessing that SOA will test your UL account value this way. To score this problem,you just have to know the UL account value inside out. Now memorized shortcut can save you.

how to prepare for written answer questions

First, from Day One, say goodbye to the pure intuition based learning and embrace rigor in your study. Learn how todefine and derive. Build a new habit of showing your work so a random grader can follow your steps.

Next, embrace the pain of studying for MLC. There’s no shortcut to learning policy values, profit testing, or anyother major concept in MLC. You just have to spend a lot of time learning major concepts and solving problems.

vii c© Yufeng Guo, MLC Fall 2017

how this book can help you

Imagine that you are to play a chess with a devil. If you win at least 6 out of 10 games, you move on with your life.Otherwise, your life comes to screeching halt and you go to your basement to relearn chess and prepare for anothermatch. How can you beat the devil?

The only thing I can think of is to become a well-rounded chess player. Play a lot of games and experience a lot offighting scenarios so you can adapt to change.

In this book, I throw you into a wide range of problems, some written answer and others multiple choice stylequestions. The goal is to help you build both intuition and rigor necessary for passing MLC.

Before writing this book, I went through the SOA syllabus and the AMLCR textbook and identified the majorconcepts you need to learn to score well in both the written answer questions and the multiple choice questions for theexam. I then wrap these concepts in a series of problems.

In each chapter, I’ll teach you how to solve one major type of written answer or multiple choice questions. If you canmaster the problems in my book, you’ll have gained a sophisticated understanding of the core concepts and should beable to tackle most problems SOA throws at you, whether the questions are multiple choice or written answer ones.

My story

I came to U.S. from China when I was in my late twenties. I started my first corporate job in U.S. in the IT departmentof a large insurance company. After working there for about 2 years, I was ready to switch my career. If you have everworked in a large IT department or any large department of a large company, you’ll find that there are thousands ofpeople just like you who go to the same building in the morning around the same time you go to the building and wholeave the same building in the afternoon around the same time you leave the building. The company’s giant parking lotswere filled with thousands of cars, one of which was my second hand red Toyota Camry. The building is nice. Coworkersare nice. But I felt like a drop of water in the ocean.

I was floating around not sure how to make use of my life. Then one day I heard the actuary profession. I heardthat if you were an actuary, you were among the elite group because there weren’t enough actuaries to go around. Iwas interested. I decided to study for P. By that time, I hadn’t touched calculus for 13 years. Fortunately, it took mejust a couple of months to relearn calculus. I took P and got a 9. I was overjoyed. I applied for a job in the actuarydepartment and became an actuary.

When I became an entry level actuary, I was in my early 30’s, about 8 years older than most of my peers, who got theactuary job straight from college. To quickly pass actuary exams, I used a bold strategy: reverse engineering. This isnot for the faint of the heart. Think twice before you try it. It works like this. Before I took an exam, say MLC, I useda company printer and printed out all the released MLC exam papers and the official solution papers. There was a stackof paper on my desk. From the stack, I pulled out the most recent exam paper, looked up the SOA solutions, looked upthe subject from the textbook, and studied the subject. Then I moved to the next exam paper. I call this just-in-timestudy, similar to the just-in-time inventory method used in Toyota and many other auto manufacturing plants aroundthe world.

It typically took me two to three months to master all the released papers. When the final exam day came, I walkedinto the exam room. You know what I saw? Sure there were surprise problems, but most exam problems were just likethe problems tested before. I was able to solve those similar problems pretty much 100% right. I just passed anotherexam.

However, since written answer questions were added in 2014 and there aren’t many released written answer questionsto master. My old strategy may not work any more.

how to pass MLC or any actuary exam

Based on my experience of studying for actuary exams, I firmly believe that to pass an actuary exam you need to do 2things: (1) you have to understand the core concepts, and (2) you have to be able to quickly solve the types of problemsSOA likes to test.

Building a coherent body of knowledge of the subject matter is the most critical and the most time-consuming partof studying for an actuary exam. If you walk into the exam room muddleheaded or with scanty knowledge of basictheories, none of the tips or tricks you learned from an exam prep book would save you. Any chess master will tell youthat there are no shortcuts in learning chess. You just have to know your stuff!

However, knowing the subject well doesn’t guarantee passing the exam or earning a high grade any more than goodtechnical skills guarantee a job offer. It’s a sad reality that often those who know how to play the interview game get thejob. When you take actuary exams, your knowledge is measured by your ability to solve the SOA style questions. Topass MLC, you’ll need to immerse yourself in the types of problems SOA likes to test or you’ll be one of those “theorysmart, exam poor” people.

One key part of studying the SOA exam papers is to identify commonly tested problem types and learn how to solvethem quickly. For example, finding the UL account value is tested in virtually every exam. Your first round of effort isto understand what is UL, what is Type A and Type B, what is COI, what is corridor, and how the UL account valuebuilds up over time. After you understand these basic concepts, you face a choice about how to find the Type A ULaccount value. Should you solve two linear equations on AVt and COIt or should you memorize the formulas for AVtand COIt to avoid having to solve two equations in the exam? You might try both approaches and see which methodsuits you. You might find that there’s no clear winner and that you want to learn both. However, before taking theexam, you must have a tried-and-true procedure for calculating the Type A UL account value. You don’t want to walkinto exam empty handed without a proven method in your head.

Here’s the final point. It’s not absolutely necessary, but it helps. Most people’s performance will downgrade in theheat of the exam. To be safe, strive to learn at least a little bit more than the minimal knowledge required to pass MLC.When I was studying an old exam paper, I often asked myself “How can I make this problem harder?” If I saw a subjectthat was in the syllabus but that was not tested in the past, I often forced myself to learn at least a little bit aboutit. Even if the subject didn’t show up in the test, knowing that I was not a complete idiot on the subject reduced myanxiety.

know your stuff

Google Maps are handy especially when you go to a new place, but I hope you know how to get to your work or schoolwhen you left your phone at home or there’s no internet connection. Over the years, I have developed many alternativeroutes for my daily commute. If route A is closed, I know what an alternative route to go. I know which road tendsto be jammed by school buses, which road is more likely to have accidents, which alley is slippery when it snows. Thisknowledge serves me well. Just the other day, while I was driving to work, the road I took had a car accident. Whilemost drivers were stuck in the traffic, I knew the exact small neighborhood that I needed to turn to bypass the trafficjam.

In virtually every career you choose, there’s no substitute for learning the basics for doing the job. To study for MLC,you just have to learn the fundamentals: the force of mortality, the multiple state model, profit testing, to name a few.

When I was a college student in China, one day I found a great shortcut for learning English. I’m sure many of youhave attempted, at some point in your life, to be very good at a foreign language that is fundamentally differentfrom your native language. A foreign language is like a bottomless pit. No matter how much effort you put intoit, you almost always end up going nowhere. You are good enough to say “How are you?” but never be able tounderstand a movie. You are so angry with yourself and with the foreign language.

Anyway, one day I had a great revelation. If I could spend a year memorizing an English dictionary, I wouldmaster the English language once for all! The first few weeks were great. I felt my vocabulary grew exponentiallyat least for the words that started with the letter A. However, two months later my balloon of hope was punctured.I couldn’t move beyond the letter A. And I forgot most of the words I learned. I went back to square one.

man’s never-ending quest for shortcuts

There are shortcuts for solving some problems in MLC (such as constant force of mortality shortcuts). However,there’s no shortcut for building a coherent body of knowledge for life contingency theories. You just have to learnone concept at a time. You just have to cycle through the major MLC concepts several times to achieve sophisticatedunderstanding.

Most of you reading this book should plan to spend at least 3 months to study for MLC. Learning takes time. Thatsaid, if you are a high achiever or you got a 5 last time and are re-taking MLC, 2 months might be enough.

a simple procedure beats the best mind

I remember a story I learned from a computer programming book. The story goes like this. A town in the Midwesthas two coffee shops, A and B. If you visit Shop A, sometimes you can get coffee right away but other times they runout of coffee and you have to wait a little while. Shop B, on the other hand, always has coffee ready for a customerwho just walks in. Both shops are in the same town and their workers have roughly the same skills. How does Shop Boutsmart Shop A? In turns out that Shop B has a simple procedure. If you work in Shop B, from Day One you learnthis rule: when existing coffee in a container reaches a certain low level, stop whatever you are doing and immediatelystart brewing new coffee. This procedure makes all the difference.

A procedure in programming is called an algorithm. When studying for an actuary exam, you’ll need to buildalgorithms for commonly tested problems to avoid having to reinvent the wheel in the heat of the exam. When the bigexam day comes, most of the problem types in the exam should be familiar to you and your job is just to recall pre-builtalgorithms. Don’t purposely put yourself on the spot without an algorithm for finding the Type A UL account value.You have only several minutes per exam problem and in the heat of the exam it’s really hard to invent a solution to anunseen problem type.

acknowledgement

First, I want to thank two actuaries, Nathan Hardiman and Robin Cunningham, for their generosity. They gave metheir Arch manual for the then Course 3 or Exam M practically free. Years ago they wrote a really good study manualcalled Arch for the then MLC. You might not know that of all the exams for ASA, MLC changes most frequently. Forexample, if you dig through old Course 3 exam papers, you’ll find the famous problem of “Lucky Tom finds coins at thePoisson rate of ... per hour.” The Poisson distribution or Poisson process was a hot topic dreaded by many. To yourrelief, SOA dropped the Poisson process from the syllabus. Anyway, Nathan and Robin have their full time corporateactuarial jobs and couldn’t keep up with frequent changes in the exam syllabus. Instead of withdrawing their Arch bookfrom the market and letting their brain child die, they decided to give the Arch manual to another author. Since I wrotemany study manuals, they gave me the book.

The Arch manual was a turning point for me technically. After downloading their manuscript from my email, I foundout that Arch was written in LATEX, not in Word. That was the first time I saw LATEX code. At at time, I was lookingfor a solution to a long standing problem of Word crashing on me. Arch was a god sent. From Arch, I learned LATEXand switched from Word to LATEX for my future books.

In addition, I want to thank the many LATEX contributors for their wonderful packages. Without LATEX or many ofits special packages, this book isn’t possible.

Finally, I think you, dear reader, for reading the thoughts and reasoning I came up with after my actuarial day job.I hope you find this book useful. If you end up using this book, I thank you for the opportunity of being part of yourjourney into the actuarial dream land.

outlook of actuary profession

According to the U.S. Bureau of Labor Statistics, employment of actuaries is projected to grow 18% from 2014 to 2024,much faster than the average for all occupations. What are you waiting for? Study for MLC today!

ix c© Yufeng Guo, MLC Fall 2017

FAQ

Does this book cover the entire syllabus?Yes. The entire syllabus is covered.

Is this book sufficient for passing MLC?No author can guarantee that if you read his book you will surely pass MLC. That said, if you can master thisbook and master the SOA exam papers, you have built a solid foundation for passing MLC.

What companion book do you recommend to use along side with this book?I recommend that you can use this book together with the AMLCR textbook and the SOA exam papers.

errata

Sample chapters and the errata for this book can be found at http://deeperunderstandingfastercalc.com/mlc-solver.php

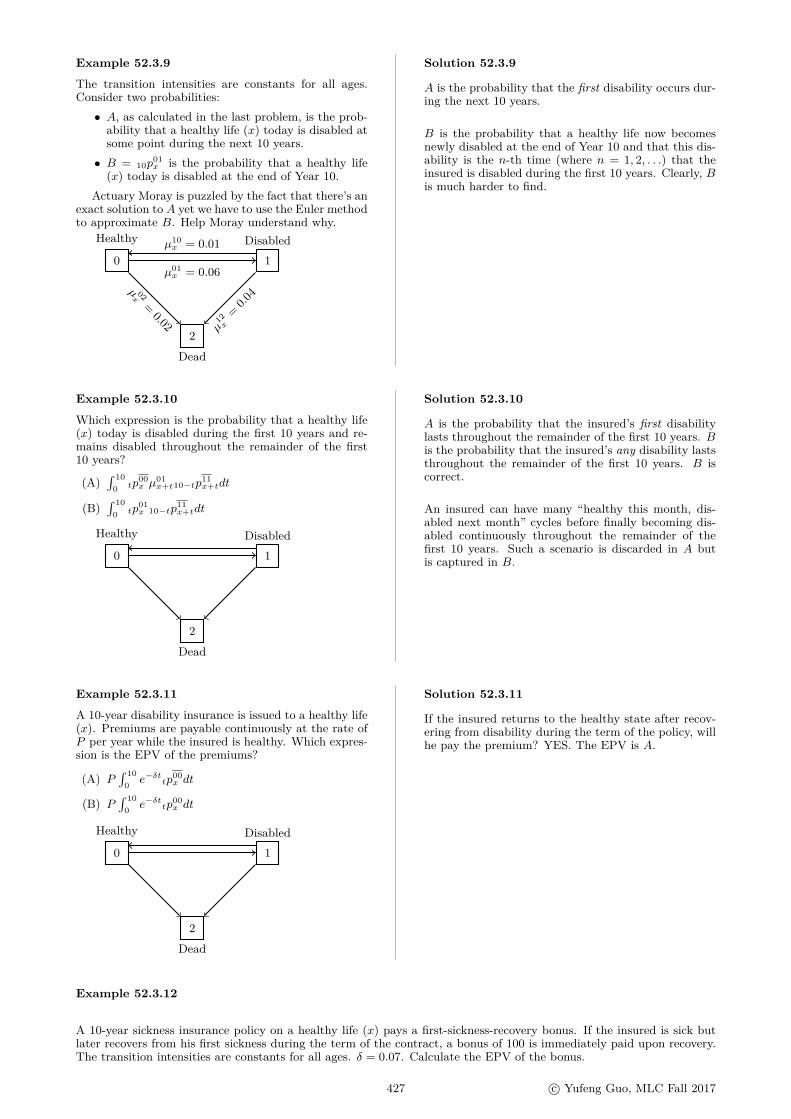

Chapter 48

Multiple state model: write down Kolmogorov’s forwardequations 100% right in a hurry

One major pain point that many exam candidates have is to correctly write down the Kolmogorov’s forward equationsin the heat of the exam. A minor pain point is to write down the associated boundary conditions for the Kolmogorov’sforward equations. Today we’re going to put an end to these struggles. After reading this chapter, you’ll be able towrite down the Kolmogorov’s forward equations and the boundary conditions 100% correct in a hurry.

Example 48.0.1

A combined disability and critical illness policy is issued to a healthy life age x. Write down the Kolmogorov’s forwardequations and the boundary conditions for

(a) tp00x

(b) tp01x

(c) tp02x

(d) tp03x

Healthy Sick

Dead Critically ill

0 1

2 3

µ01x+t

µ10x+t

µ02x+t

µ13x+t

µ32x+t

µ12x+tµ03

x+t

Solution 48.0.1

(a) Write down the Kolmogorov’s forward equation for tp00x .

Step 1. For each node j where j = 0, 1, 2, 3, change the name of the node from j to 0j.

Healthy Sick

Dead Critically ill

00 01

02 03

µ01x+t

µ10x+t

µ02x+t

µ13x+t

µ32x+t

µ12x+tµ03

x+t

We interpret each node as follows: at t = 0, the universe has 1 healthyperson (ancestor) and no one else. This person’s offsprings fill the uni-verse. The population of this universe is always one at any time. Un-fortunately, the offspring population isn’t growing, unlike Abraham’schildren. At t, we count the people in the universe.

• In the node name 0j, 0 is the ancestor’s name; j is the offspring’sname.

• tp00x is the (expected) number of the healthy people at t.

• tp01x is the (expected) number of the sick people at t.

• tp02x is the (expected) number of the dead people at t.

• tp03x is the (expected) number of the critically ill people at t.

• The total population at t is tp00x + tp

01x + tp

02x + tp

03x = 1.

Step 2. From all the nodes, isolate the nodes that point to the node 00. The insureds in these nodes can flow into thenode 00, causing d

dttp

00x to increase.

387

Healthy Sick

00 01

µ10x+t

positive forces of d

dttp

00x : tp

01x µ

10x+t

Step 3. From all the nodes, isolate the nodes that are pointed to by the node 00. The insureds in the node 00 canflow into these nodes, causing d

dttp

00x to decrease.

Healthy Sick

Dead Critically ill

00 01

02 03

µ01x+t

µ02x+t

µ03x+t

negative forces of d

dttp

00x : −tp00

x

(µ01x+t + µ02

x+t + µ03x+t)

Step 4: Combine the positive and the negative forces and you’ll get the Kolmogorov’s forward equation.

Healthy Sick

Dead Critically ill

0 1

2 3

µ01x+t

µ10x+t

µ02x+t

µ13x+t

µ32x+t

µ12x+tµ03

x+t

d

dttp

00x = tp

01x µ

10x+t − tp

00x

(µ01x+t + µ02

x+t + µ03x+t)

The boundary condition is either the beginning condition or the ending condition. Since at time zero, the insured ishealthy, the boundary conditions are

0p00x = 1, 0p

01x = 0p

02x = 0p

03x = 0

(b) Write down the Kolmogorov’s forward equation for tp01x . Isolate the positive forces (the nodes that can flow into

the node 01):

Healthy Sick

00 01

µ01x+t

positive forces of d

dttp

01x : tp

00x µ

01x+t

Isolate the negative forces (the nodes that the node 01 can flow into):

Healthy Sick

Dead Critically ill

00 01

02 03

µ10x+t

µ12x+t µ13

x+t

negative forces of d

dttp

01x : −tp01

x

(µ10x+t + µ12

x+t + µ13x+t)

Combine the positive and the negative forces:

Healthy Sick

Dead Critically ill

0 1

2 3

µ01x+t

µ10x+t

µ02x+t

µ13x+t

µ32x+t

µ12x+tµ03

x+t

d

dttp

01x = tp

00x µ

01x+t − tp

01x

(µ10x+t + µ12

x+t + µ13x+t)

boundary condition: 0p00x = 1, 0p

01x = 0p

02x = 0p

03x = 0

(c) Write down the Kolmogorov’s forward equation for tp02x . Isolate all the nodes that can flow into the node 02:

Healthy Sick

Dead Critically ill

00 01

02 03

µ02x+t

µ32x+t

µ12x+t

positive forces: d

dttp

02x : tp

00x µ

02x+t + tp

01x µ

12x+t + tp

03x µ

32x+t

There are no negative forces that will pull the insured away from the 02 node. The population in the node 02 can onlyincrease.

d

dttp

02x = tp

00x µ

02x+t + tp

01x µ

12x+t + tp

03x µ

32x+t

boundary condition: 0p00x = 1, 0p

01x = 0p

02x = 0p

03x = 0

(d) Write down the Kolmogorov’s forward equation for tp03x .

389 c© Yufeng Guo, MLC Fall 2017

Healthy Sick

Critically ill

00 01

03

µ13x+t

µ03x+t

positive forces: d

dttp

03x : tp

00x µ

03x+t + tp

01x µ

13x+t

Dead Critically ill

02 03µ32x+t

negative forces: d

dttp

03x : −tp03

x µ32x+t

⇒ d

dttp

03x = tp

00x µ

03x+t + tp

01x µ

13x+t − tp

03x µ

32x+t

boundary condition: 0p00x = 1, 0p

01x = 0p

02x = 0p

03x = 0

Example 48.0.2

(Same model as before but repeated for convenience) A combined disability and critical illness policy is issued to ahealthy life age x. Write down the Kolmogorov’s forward equations for

(a) tp10x

(b) tp11x

(c) tp12x

(d) tp13x

Healthy Sick

Dead Critically ill

0 1

2 3

µ01x+t

µ10x+t

µ02x+t

µ13x+t

µ32x+t

µ12x+tµ03

x+t

Solution 48.0.2

The process is the same as that in the previous problem. First, we relabel each node as 1j.

Healthy Sick

Dead Critically ill

10 11

12 13

µ01x+t

µ10x+t

µ02x+t

µ13x+t

µ32x+t

µ12x+tµ03

x+t

We interpret each node as follows: at some point before t, the universehas only 1 sick person (ancestor). This person’s children fill the universe.At t, we count the people in the universe.

• In the node name 1j, 1 is the ancestor’s name; j is the offspring’sname.

• tp10x is the (expected) number of the healthy people at t.

• tp11x is the (expected) number of the sick people at t.

• tp12x is the (expected) number of the dead people at t.

• tp13x is the (expected) number of the critically ill people at t.

• The total population at t is tp10x + tp

11x + tp

12x + tp

13x = 1.

(a)

Healthy Sick

10 11

µ10x+t

positive forces: d

dttp

10x : tp

11x µ

10x+t

Healthy Sick

Dead Critically ill

10 11

12 13

µ01x+t

µ02x+t

µ03x+t

negative forces: d

dttp

10x : −tp10

x

(µ01x+t + µ02

x+t + µ03x+t)

⇒ d

dttp

10x = tp

11x µ

10x+t − tp

10x

(µ01x+t + µ02

x+t + µ03x+t)

(b)

Healthy Sick

10 11

µ01x+t positive forces: d

dttp

11x : tp

10x µ

01x+t

Healthy Sick

Dead Critically ill

10 11

12 13

µ10x+t

µ13x+t

µ12x+t

negative forces: d

dttp

11x : −tp11

x

(µ10x+t + µ12

x+t + µ13x+t)

⇒ d

dttp

11x = tp

10x µ

01x+t − tp

11x

(µ10x+t + µ12

x+t + µ13x+t)

(c) There are only positive forces for the node 12:

Healthy Sick

Dead Critically ill

10 11

12 13

µ02x+t

µ32x+t

µ12x+t

d

dttp

12x = tp

10x µ

02x+t + tp

11x µ

12x+t + tp

13x µ

32x+t

391 c© Yufeng Guo, MLC Fall 2017

(d)

Healthy Sick

Critically ill

10 11

13

µ13x+t

µ03x+t

positive forces: d

dttp

13x : tp

10x µ

03x+t + tp

11x µ

13x+t

Dead Critically ill

12 13µ32x+t

negative forces: d

dttp

13x : −tp13

x µ32x+t

⇒ d

dttp

13x = tp

10x µ

03x+t + tp

11x µ

13x+t − tp

13x µ

32x+t

Example 48.0.3

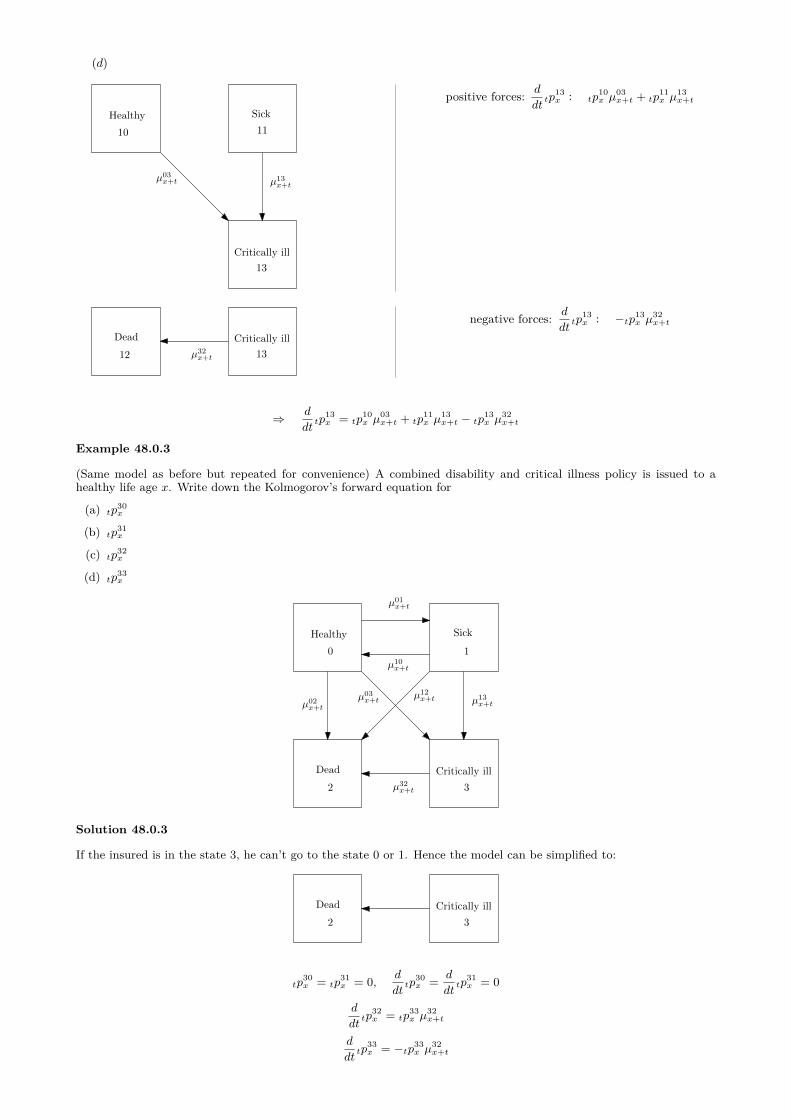

(Same model as before but repeated for convenience) A combined disability and critical illness policy is issued to ahealthy life age x. Write down the Kolmogorov’s forward equation for

(a) tp30x

(b) tp31x

(c) tp32x

(d) tp33x

Healthy Sick

Dead Critically ill

0 1

2 3

µ01x+t

µ10x+t

µ02x+t

µ13x+t

µ32x+t

µ12x+tµ03

x+t

Solution 48.0.3

If the insured is in the state 3, he can’t go to the state 0 or 1. Hence the model can be simplified to:

Dead Critically ill

2 3

tp30x = tp

31x = 0, d

dttp

30x = d

dttp

31x = 0

d

dttp

32x = tp

33x µ

32x+t

d

dttp

33x = −tp33

x µ32x+t

Example 48.0.4

(Same model as before but repeated for convenience) A combined disability and critical illness policy is issued to ahealthy life age x. Write down the Kolmogorov’s forward equations for

(a) tp20x

(b) tp21x

(c) tp22x

(d) tp23x

Healthy Sick

Dead Critically ill

0 1

2 3

µ01x+t

µ10x+t

µ02x+t

µ13x+t

µ32x+t

µ12x+tµ03

x+t

Solution 48.0.4

If the insured is currently in the state 2, he’ll be stuck in the state 2 and can’t go to the state 0, 1 or 3. The model canbe simplified to:

Dead

2

tp20x = tp

21x = tp

23x = 0, tp

22x = 1

⇒ d

dttp

20x = d

dttp

21x = d

dttp

22x = d

dttp

23x = 0

Example 48.0.5

(Same model as before but repeated for convenience) A combined disability and critical illness policy is issued to ahealthy life age x. The insured is currently in the state 0. Explain why

d

dttp

00x + d

dttp

01x + d

dttp

02x + d

dttp

03x = 0

Healthy Sick

Dead Critically ill

0 1

2 3

µ01x+t

µ10x+t

µ02x+t

µ13x+t

µ32x+t

µ12x+tµ03

x+t

Solution 48.0.5

Since the total population is always one, the total change of the population is always zero. Similarly,

d

dttp

10x + d

dttp

11x + d

dttp

12x + d

dttp

13x = 0

d

dttp

20x + d

dttp

21x + d

dttp

22x + d

dttp

23x = 0

d

dttp

30x + d

dttp

31x + d

dttp

32x + d

dttp

33x = 0

393 c© Yufeng Guo, MLC Fall 2017

48.1 Check your knowledge

Homework 48.1.1

Write down the formula for d

dttp

01x .

Healthy Sick

Dead

0 1

2

µ10x

µ01x

µ 02x µ12x

Homework Solution 48.1.1

Difficultyd

dttp

01x = tp

00x µ

01x+t − tp

01x (µ10

x+t + µ12x+t)

Homework 48.1.2

Write down the formula for d

dttp

00x .

Healthy Sick

Dead

0 1

2

µ10x

µ01x

µ 02x µ12x

Homework Solution 48.1.2

Difficulty

d

dttp

00x = tp

01x µ

10x+t − tp

00x (µ01

x+t + µ02x+t)

Homework 48.1.3

Write down the formula for d

dttp

22x .

Healthy Sick

Dead

0 1

2

µ10x

µ01x

µ 02x µ12x

Homework Solution 48.1.3

Difficultyd

dttp

22x = 0

Homework 48.1.4

Write down the formula for d

dttp

10x , d

dttp

12x , d

dttp

02x .

Healthy Sick

Dead

0 1

2

µ10x

µ01x

µ 02x µ12x

Homework Solution 48.1.4

Difficulty

d

dttp

10x = tp

11x µ

10x+t − tp

10x (µ01

x+t + µ02x+t)

d

dttp

12x = tp

11x µ

12x+t + tp

10x µ

02x+t

d

dttp

02x = tp

00x µ

02x+t + tp

01x µ

12x+t

Homework 48.1.5

Use the Kolmogorov’s forward equation to derive the formula:

tp00x = exp

(−∫ t

0(µ01x+s + µ02

x+s)ds

)

Healthy Sick

Dead

0 1

2

µ10x

µ01x

µ 02x µ12x

Homework Solution 48.1.5

Difficulty

d

dttp

00x = tp

01x µ

10x+t − tp

00x (µ01

x+t + µ02x+t)

Since we want the insured to be continuously in the state 0, set tp01x = 0:

⇒ d

dttp

00x = −tp00

x (µ01x+t + µ02

x+t)

1tp00x

d

dttp

00x = d

dtln tp00

x = −(µ01x+t + µ02

x+t)

Integrate both sides:

tp00x = C exp

(−∫ t

0(µ01x+s + µ02

x+s)ds

)where C is a constant.

0p00x = 1, ⇒ C = 1

tp00x = exp

(−∫ t

0(µ01x+s + µ02

x+s)ds

)

395 c© Yufeng Guo, MLC Fall 2017

Chapter 49

Multiple state model: Euler’s method for probabilities

Example 49.0.1

A combined disability and critical illness policy is issued to a healthy life age x. Let h = 1/12 (e.g. one month timestep). Use the Euler’s method and estimate the following probabilities:

(a) hp00x

(b) hp01x

(c) hp02x

(d) hp03x

Healthy Sick

Dead Critically ill

0 1

2 3

µ01x+t = 0.004

µ10x+t = 0.0008

µ02x+t = 0.0005(1 + t) µ13

x+t = 0.0006

µ32x+t

µ12x+tµ03

x+t

µ03x+t = 0.0004

µ12x+t = µ02

x+t = 0.0005(1 + t)

µ32x+t = 2µ02

x+t = 0.001(1 + t)

Solution 49.0.1

The boundary conditions are:0p

00x = 1, 0p

01x = 0p

02x = 0p

03x = 0

(a)d

dttp

00x = tp

01x µ

10x+t − tp

00x

(µ01x+t + µ02

x+t + µ03x+t)

⇒(d

dttp

00x

)t=0

= 0p01x µ

10x+0 − 0p

00x

(µ01x+0 + µ02

x+0 + µ03x+0)

= 0µ10x+0 − 1

(µ01x+0 + µ02

x+0 + µ03x+0)

= 0− 1(0.004 + 0.0005(1 + 0) + 0.0004

)= −0.0049

hp00x ≈ 0p

00x + h

(d

dttp

00x

)t=0

= 1 + 112 × (−0.0049) = 0.99959167

(b)

d

dttp

01x = tp

00x µ

01x+t − tp

01x

(µ10x+t + µ12

x+t + µ13x+t)

(d

dttp

01x

)t=0

= 0p00x µ

01x+0 − 0p

01x

(µ10x+0 + µ12

x+0 + µ13x+0)

= µ01x+0 = 0.004

hp01x ≈ 0p

01x + h

(d

dttp

01x

)t=0

= 0 + 112 × 0.004 = 0.00033333

(c)

397

d

dttp

02x = tp

00x µ

02x+t + tp

01x µ

12x+t + tp

03x µ

32x+t(

d

dttp

02x

)t=0

= 0p00x µ

02x+0 + 0p

01x µ

12x+0 + 0p

03x µ

32x+0

= µ02x+0 = 0.0005(1 + 0) = 0.0005

hp03x ≈ 0p

03x + h

(d

dttp

03x

)t=0

= 0 + 112 × 0.0005 = 0.00004167

(d)

d

dttp

03x = tp

00x µ

03x+t + tp

01x µ

13x+t − tp

03x µ

32x+t(

d

dttp

03x

)t=0

= 0p00x µ

03x+0 + 0p

01x µ

13x+0 − 0p

03x µ

32x+0

= µ03x+0 = 0.0004

hp03x ≈ 0p

03x + h

(d

dttp

03x

)t=0

= 0 + 112 × 0.0004 = 0.00003333

Check: 0.99959167 + 0.00033333 + 0.00004167 + 0.00003333 = 1 OK

Example 49.0.2

(Same model as before but repeated for convenience) A combined disability and critical illness policy is issued to ahealthy life age x. Let h = 1/12 (e.g. one month time step). Use the Euler’s method and estimate the followingprobabilities:

(a) 2hp00x

(b) 2hp01x

(c) 2hp02x

(d) 2hp03x

Healthy Sick

Dead Critically ill

0 1

2 3

µ01x+t = 0.004

µ10x+t = 0.0008

µ02x+t = 0.0005(1 + t) µ13

x+t = 0.0006

µ32x+t

µ12x+tµ03

x+t

µ03x+t = 0.0004

µ12x+t = µ02

x+t = 0.0005(1 + t)

µ32x+t = 2µ02

x+t = 0.001(1 + t)

You are given: hp00x = 0.99959167, hp01

x = 0.00033333, hp02x = 0.00004167, and hp

03x = 0.00003333

Solution 49.0.2

(a)d

dttp

00x = tp

01x µ

10x+t − tp

00x

(µ01x+t + µ02

x+t + µ03x+t)

⇒(d

dttp

00x

)t=h

= hp01x µ

10x+h − hp

00x

(µ01x+h + µ02

x+h + µ03x+h)

= 0.00033333× 0.0008− 0.99959167(0.004 + 0.0005(1 + 1/12) + 0.0004

)= −0.00493938

2hp00x ≈ hp

00x + h

(d

dttp

00x

)t=h

= 0.99959167 + 112 × (−0.00493938) = 0.99918006

(b)

d

dttp

01x = tp

00x µ

01x+t − tp

01x

(µ10x+t + µ12

x+t + µ13x+t)

(d

dttp

01x

)t=h

= hp00x µ

01x+h − hp

01x

(µ10x+h + µ12

x+h + µ13x+h)

= 0.99959167× 0.004− 0.00033333(0.0008 + 0.0005(1 + 1/12) + 0.0006

)= 0.00399772

2hp01x ≈ hp

01x + h

(d

dttp

01x

)t=h

= 0.00033333 + 112 × (0.00399772) = 0.000666473

(c)

d

dttp

02x = tp

00x µ

02x+t + tp

01x µ

12x+t + tp

03x µ

32x+t(

d

dttp

02x

)t=h

= hp00x µ

02x+h + hp

01x µ

12x+h + hp

03x µ

32x+h

= 0.99959167× 0.0005(1 + 1/12) + 0.00033333× 0.0005(1 + 1/12) + 0.00003333× 0.001(1 + 1/12)

= 0.00054166

2hp02x ≈ hp

02x + h

(d

dttp

02x

)t=h

= 0.00004167 + 112 × 0.00054166 = 0.00008700

(d)

d

dttp

03x = tp

00x µ

03x+t + tp

01x µ

13x+t − tp

03x µ

32x+t(

d

dttp

03x

)t=h

= hp00x µ

03x+h + hp

01x µ

13x+h − hp

03x µ

32x+h

= 0.99959167× 0.0004 + 0.00033333× 0.0006− 0.00003333× 0.001(1 + 1/12)

= 0.00040000

2hp03x ≈ hp

03x + h

(d

dttp

03x

)t=h

= 0.00003333 + 112 × 0.00040000 = 0.00006663

Check: 0.99918006 + 0.000666473 + 0.00008700 + 0.00006663 = 1.0000002 ≈ 1 OK

Example 49.0.3

(Same model as before but repeated for convenience) A combined disability and critical illness policy is issued to a healthylife age x. Let h = 1/12 (e.g. one month time step). Write down the formulas for each of the following probabilitiesunder the Euler’s method. Numerical calculations are not expected.

(a) nhp00x

(b) nhp01x

(c) nhp02x

(d) nhp03x

Healthy Sick

Dead Critically ill

0 1

2 3

µ01x+t = 0.004

µ10x+t = 0.0008

µ02x+t = 0.0005(1 + t) µ13

x+t = 0.0006

µ32x+t

µ12x+tµ03

x+t

µ03x+t = 0.0004

µ12x+t = µ02

x+t = 0.0005(1 + t)

µ32x+t = 2µ02

x+t = 0.001(1 + t)

Solution 49.0.3

399 c© Yufeng Guo, MLC Fall 2017

(a)d

dttp

00x = tp

01x µ

10x+t − tp

00x

(µ01x+t + µ02

x+t + µ03x+t)

⇒(d

dttp

00x

)t=(n−1)h

= (n−1)hp01x µ

10x+(n−1)h − (n−1)hp

00x

(µ01x+(n−1)h + µ02

x+(n−1)h + µ03x+(n−1)h

)nhp

00x ≈ (n−1)hp

00x + h

(d

dttp

00x

)t=(n−1)h

(b)

d

dttp

01x = tp

00x µ

01x+t − tp

01x

(µ10x+t + µ12

x+t + µ13x+t)

(d

dttp

01x

)t=(n−1)h

= (n−1)hp00x µ

01x+(n−1)h − (n−1)hp

01x

(µ10x+(n−1)h + µ12

x+(n−1)h + µ13x+(n−1)h

)nhp

01x ≈ (n−1)hp

01x + h

(d

dttp

01x

)t=(n−1)h

(c)

d

dttp

02x = tp

00x µ

02x+t + tp

01x µ

12x+t + tp

03x µ

32x+t(

d

dttp

02x

)t=(n−1)h

= (n−1)hp00x µ

02x+(n−1)h + (n−1)hp

01x µ

12x+(n−1)h + (n−1)hp

03x µ

32x+(n−1)h

nhp02x ≈ (n−1)hp

02x + h

(d

dttp

02x

)t=(n−1)h

(d)

d

dttp

03x = tp

00x µ

03x+t + tp

01x µ

13x+t − tp

03x µ

32x+t(

d

dttp

03x

)t=(n−1)h

= (n−1)hp00x µ

03x+(n−1)h + (n−1)hp

01x µ

13x+(n−1)h − (n−1)hp

03x µ

32x+(n−1)h

nhp03x ≈ (n−1)hp

03x + h

(d

dttp

03x

)t=(n−1)h

Example 49.0.4

(Same model as before but repeated for convenience) A combined disability and critical illness policy is issued to ahealthy life age x. Let h = 1/12 (e.g. one month time step). Use the Euler’s method and estimate the followingprobabilities:

(a) hp10x

(b) hp11x

(c) hp12x

(d) hp13x

Healthy Sick

Dead Critically ill

0 1

2 3

µ01x+t = 0.004

µ10x+t = 0.0008

µ02x+t = 0.0005(1 + t) µ13

x+t = 0.0006

µ32x+t

µ12x+tµ03

x+t

µ03x+t = 0.0004

µ12x+t = µ02

x+t = 0.0005(1 + t)

µ32x+t = 2µ02

x+t = 0.001(1 + t)

Solution 49.0.4

It may strike you as absurd to calculate these probabilities given that at time zero (e.g. contract initiation) the insuredis in the state 0. However, we can still compile these probabilities by arbitrarily assuming that the insured is in the state1 at time zero. The boundary conditions for these probabilities are:

0p11x = 1, 0p

10x = 0p

12x = 0p

13x = 0

(a)d

dttp

10x = tp

11x µ

10x+t − tp

10x

(µ01x+t + µ02

x+t + µ03x+t)

⇒(d

dttp

10x

)t=0

= 0p11x µ

10x+0 − 0p

10x

(µ01x+0 + µ02

x+0 + µ03x+0)

= 1× µ10x+0 − 0

(µ01x+0 + µ02

x+0 + µ03x+0)

= µ10x+0 = 0.0008

hp01x ≈ 0p

01x + h

(d

dttp

01x

)t=0

= 0 + 112 × 0.0008 = 0.00006667

(b)

d

dttp

11x = tp

10x µ

01x+t − tp

11x

(µ10x+t + µ12

x+t + µ13x+t)

(d

dttp

11x

)t=0

= 0p10x µ

01x+0 − 0p

11x

(µ10x+0 + µ12

x+0 + µ13x+0)

= −(µ10x+0 + µ12

x+0 + µ13x+0)

= −(0.0008 + 0.0005(1 + 0) + 0.0006

)= −0.00190000

hp11x ≈ 0p

11x + h

(d

dttp

11x

)t=0

= 1 + 112 × (−0.00190000) = 0.99984167

(c)

d

dttp

12x = tp

10x µ

02x+t + tp

11x µ

12x+t + tp

13x µ

32x+t(

d

dttp

12x

)t=0

= 0p10x µ

02x+0 + 0p

11x µ

12x+0 + 0p

13x µ

32x+0

= µ12x+0 = 0.0005(1 + 0) = 0.0005

hp12x ≈ 0p

12x + h

(d

dttp

12x

)t=0

= 0 + 112 × 0.0005 = 0.00004167

(d)

d

dttp

13x = tp

10x µ

03x+t + tp

11x µ

13x+t − tp

13x µ

32x+t(

d

dttp

13x

)t=0

= 0p10x µ

03x+0 + 0p

11x µ

13x+0 − 0p

13x µ

32x+0

= µ13x+0 = 0.0006

hp13x ≈ 0p

13x + h

(d

dttp

13x

)t=0

= 0 + 112 × 0.0006 = 0.00005

Check: 0.00006667 + 0.99984167 + 0.00004167 + 0.00005 = 1 OK

401 c© Yufeng Guo, MLC Fall 2017

49.1 Check your knowledge

Homework 49.1.1

You are given the following model (AMLCR textbook Example 8.5):

• µ01x = a1 + b1 exp(c1x), µ10

x = 0.1µ01x , µ02

x = a2 + b2 exp(c2x), µ12x = µ02

x

• a1 = 0.0004, b1 = 3.4674× 10−6, c1 = 0.138155

• a2 = 0.0005, b2 = 7.5858× 10−5, c2 = 0.087498

Healthy Sick

Dead

0 1

2

µ10x

µ01x

µ 02x µ12x

Let h = 1/12 and x = 60.

(a) Briefly explain why it’s difficult or impossible to find an exact formula for hp00x .

(b) Briefly explain why the Euler’s method works.

(c) Calculate hp00x

(d) Calculate hp01x

(e) Calculate hp02x

(f) Calculate 2hp00x

(g) Calculate 2hp01x

(h) Calculate 2hp02x

Homework Solution 49.1.1

Difficulty(a) To find tp

00x , tp01

x , and tp02x , we need to solve 3 differential equations with the help of the boundary conditions:

d

dttp

00x = tp

01x µ

10x+t − tp

00x (µ01

x+t + µ02x+t)

d

dttp

01x = tp

00x µ

01x+t − tp

01x (µ10

x+t + µ12x+t)

d

dttp

02x = tp

00x µ

02x+t + tp

01x µ

02x+t

boundary conditions: tp00x = 1, tp

01x = tp

02x = 0

To understand the difficulty of solving these equations, notice that in the first equation, the term tp00x appears on

both sides. In addition, the righthand side has a term tp01x .

Like most other differential equations, these equation generally don’t have exact solutions except under some simpli-fying assumptions. However, we can use numerical methods to approximate solutions to differential equations. Thereare many methods to approximate solutions to a differential equation. One of the oldest and easiest but probably theleast efficient method was devised by Euler and is called the Euler method.

(b) This is the essence of the Euler method. Suppose we need to find the value of an unknown function f(x) at x = b.We know the function’s initial value f(a). We also know the slope of f(x) at any point. Then we can divide [a, b] inton subintervals each of length h = (b− a)/n and successively use the tangent line approximation to find f(b).

f(a+ h) ≈ f(a) + hf ′(a)

f(a+ 2h) ≈ f(a+ h) + hf ′(a+ h). . .

f(b) ≈ f(b− h) + hf ′(b− h)The above method uses the forward recursion. The forward recursion works when you know the initial condition such

as 0p00x = 1. However, in some cases we know only the ending condition. For example, for any insurance contract, at

contract expiration, the policy value is always zero. From the ending zero policy value, we can use the Euler’s methodto find the beginning policy values. Here’s the math for the backwards recursion.

f ′(b) ≈ f(b)− f(b− h)h

f(b− h) ≈ f(b)− f ′(b)h

f(b− 2h) ≈ f(b− h)− f ′(b− h)h. . .

(c)

hp00x ≈ 0p

00x + h

[tp

01x µ

10x+t − tp

00x (µ01

x+t + µ02x+t)

]t=0

= 0p00x + h

[0p

01x µ

10x − 0p

00x (µ01

x + µ02x )]

0p00x = 1, 0p

01x = 0

µ01x + µ02

x = a1 + b1 exp(c1x) + a2 + b2 exp(c2x)

= 0.0004 + 3.4674× 10−6e0.138155(60) + 0.0005 + 7.5858× 10−5e0.087498(60) = 0.029158122

⇒ hp00x ≈ 1− 1

12(µ01x + µ02

x ) = 1− 0.02915812212 = 0.997570

(d)

d

dttp

01x = tp

00x µ

01x+t − tp

01x (µ10

x+t + µ12x+t)

⇒ hp01x ≈ 0p

01x + h

[0p

00x µ

01x − 0p

01x (µ10

x + µ12x )]

= hµ01x

= 0.0004 + 3.4674× 10−6e0.138155(60)

12 = 0.001184

(e)d

dttp

02x = tp

00x µ

02x+t + tp

01x µ

12x+t

hp02x ≈ 0p

02x + h

[0p

00x µ

02x + 0p

01x µ

12x

]= hµ02

x

= 0.01495424112 = 0.001246

Alternatively,hp

02x = 1− (hp00

x + hp01x ) = 1− (0.997570 + 0.001184) = 0.001246

(f)

2hp00x ≈ hp

00x + h

[hp

01x µ

10x+h − hp

00x (µ01

x+h + µ02x+h)

]= 0.997570 + 0.001184× 0.001436372− 0.997570(0.014363722 + 0.01506002)

12 = 0.995124

(g)

2hp01x ≈ hp

01x + h

[hp

00x µ

01x+h − hp

01x (µ10

x+h + µ12x+h)

]= 0.001184 + 0.997570× 0.014363722− 0.001184(0.001436372 + 0.01506002)

12 = 0.002376

(h)

2hp02x ≈ hp

02x + h

[hp

00x µ

02x+h + hp

01x µ

12x+h

]= 0.001246 + 0.997570× 0.014363722 + 0.001184× 0.01506002

12 = 0.002500

Alternatively,2hp

02x = 1− (2hp

00x + 2hp

01x ) = 1− (0.995124 + 0.002376) = 0.002500

By the way, the Euler method does not require you to divide the interval [a, b] into subintervals of an equal length.However, equal length subintervals are often chosen for the ease of implementation.

403 c© Yufeng Guo, MLC Fall 2017

Homework 49.1.2

You are given the following model:

Healthy Sick

Dead

0 1

2

µ10x = 0.02

µ01x = 0.04µ 02x

=0.01(1 +

t) µ12x

=0.0

2(1+t)

Set h = 0.1. For n = 1, 2, 3, calculate the followingprobabilities:

(a) nhp00x , nhp01

x , and nhp02x

(b) nhp10x , nhp11

x , and nhp12x

(c) nhp20x , nhp22

x , and nhp22x

Difficulty

t µ01x+t µ02

x+t µ10x+t µ12

x+t0 0.04 0.010 0.02 0.020h 0.04 0.011 0.02 0.0222h 0.04 0.012 0.02 0.024

t

(d

dttp

00x

)t

(d

dttp

01x

)t

(d

dttp

02x

)t

(d

dttp

10x

)t

(d

dttp

11x

)t

(d

dttp

12x

)t

0 −0.05000000 0.04000000 0.01000000 0.02000000 −0.04000000 0.02000000h −0.05066500 0.03963200 0.01103300 0.01981800 −0.04175200 0.021934002h −0.05131728 0.03924696 0.01207032 0.01962944 −0.04348102 0.02385158

t tp00x tp

01x tp

02x tp

10x tp

11x tp

02x

0 1.0000000 0.0000000 0.0000000 0.0000000 1.0000000 0.0000000h 0.9950000 0.0040000 0.0010000 0.0020000 0.9960000 0.00200002h 0.9899335 0.0079632 0.0021033 0.0039818 0.9918248 0.00419343h 0.9848018 0.0118879 0.0033103 0.0059447 0.9874767 0.0065786

tp20x = tp

21x = 0, tp

22x = 1

Homework 49.1.3

The transition intensities are constants for all ages.Healthy Disabled

Dead

0 1

2

µ10x = 0.01

µ01x = 0.06

µ 02x=

0.02 µ12x

=0.0

4

Set h = 112 . For n = 1, 2, 3, calculate the following

probabilities:

(a) nhp00x , nhp01

x , and nhp02x

(b) nhp10x , nhp11

x , and nhp12x

Difficulty

Homework Solution 49.1.2

µ01x+t µ02

x+t µ10x+t µ12

x+t0.06 0.02 0.01 0.04

t

(d

dttp

00x

)t

(d

dttp

01x

)t

(d

dttp

02x

)t

(d

dttp

10x

)t

(d

dttp

11x

)t

(d

dttp

12x

)t

0 −0.08000000 0.06000000 0.02000000 0.01000000 −0.05000000 0.04000000h −0.07941667 0.05935000 0.02006667 0.00989167 −0.04974167 0.039850002h −0.07883776 0.05870563 0.02013214 0.00978427 −0.04948495 0.03970068

t tp00x tp

01x tp

02x tp

10x tp

11x tp

02x

0 1.0000000 0.0000000 0.0000000 0.0000000 1.0000000 0.0000000h 0.9933333 0.0050000 0.0016667 0.0008333 0.9958333 0.00333332h 0.9867153 0.0099458 0.0033389 0.0016576 0.9916882 0.00665423h 0.9801455 0.0148380 0.0050166 0.0024730 0.9875644 0.0099626

Chapter 50

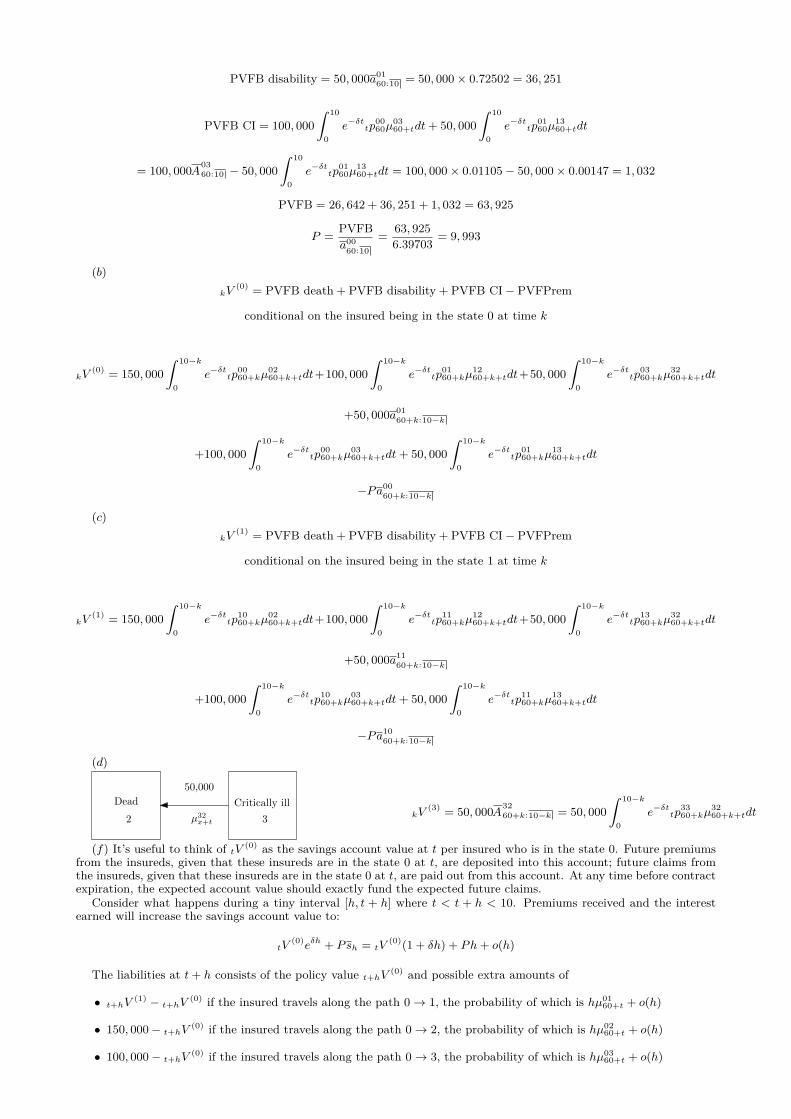

Multiple state model: EPV of benefits, policy values,Thiele’s differential equations

Example 50.0.1

An insurer issues a combined 5-year disability income and death benefit policy to a healthy life aged 65. You are given:

• µ01x = a1 + b1 exp(c1x), µ10

x = 0.1µ01x , µ02

x = a2 + b2 exp(c2x), µ12x = µ02

x

• a1 = 0.0004, b1 = 3× 10−6, c1 = 0.15

• a2 = 0.0005, b2 = 8× 10−5, c2 = 0.02

• δ = 0.06

• The premium is payable continuously at the rate of P per year while the insured is healthy.

• A benefit of $50,000 per year is payable continuously while the insured is disabled.

• A death benefit of $100,000 is payable immediately upon death.

Healthy Disabled

Dead

0 1

2

µ10x

µ01x

µ 02x µ12x

(a) Write down the formula for the EPV of the premiums

(b) Write down the formula for the EPV of the disability benefit

(c) Write down the formula for the EPV of the death benefit

(d) Calculate P . Selective actuarial values:

• a0065:5 = 3.684

•∫ 5

0 e−δt

tp0065µ

0265+tdt = 0.0579

•∫ 5

0 e−δt

tp0165µ

1265+tdt = 0.0102

• a0165:5 = 0.6008

(e) Instead of paying $50,000 while the insured disabled, the policy pays $20,000 immediately upon disability. Writedown the formula for the EPV of the disability benefit.

Solution 50.0.1

(a) Pa0065:5 =

∫ 5

0tp

0065e−δtdt

(b) 50, 000a0165:5 = 50, 000

∫ 5

0tp

0165e−δtdt

(c) 100, 000A0265:5 = 100, 000

∫ 5

0e−δt

(tp

0065µ

0265+t + tp

0165µ

1265+t

)dt

(d) P =50, 000a01

65:5 + 100, 000A0265:5

a0065:5

= 50, 000× 0.6008 + 100, 000(0.0579 + 0.0102)3.684 = 10, 003

(e) 20, 000A0165:5 = 20, 000

∫ 5

0e−δttp

0065µ

0165+tdt

405

Example 50.0.2

(Same model as that in the previous problem but the benefit structure is different) An insurer issues a combined 5-yeardisability and death benefit insurance policy to a healthy life aged 65. You are given:

• µ01x = a1 + b1 exp(c1x), µ10

x = 0.1µ01x , µ02

x = a2 + b2 exp(c2x), µ12x = µ02

x

• a1 = 0.0004, b1 = 3× 10−6, c1 = 0.15

• a2 = 0.0005, b2 = 8× 10−5, c2 = 0.02

• i = 0.06

• A monthly premium P is payable in advance conditional on the life being healthy at the premium date.

• A benefit of $50,000 per year is payable monthly in arrears while the life is disabled.

• A death benefit of $100,000 is payable immediately upon death.

Healthy Disabled

Dead

0 1

2

µ10x

µ01x

µ 02x µ12x

(a) Write down the formula for the EPV of the premiums.

(b) Of the two values a(12)0065:5 and a00

65:5 , which one is bigger? Justify your answer.

(c) Write down the formula for the EPV of the disability benefit

(d) Write down the formula for the EPV of the death benefit.

(e) Write down the formula for P .

Solution 50.0.2

(a) 12P a(12)0065:5 = P

(1 + 1/12p

0065v

1/12 + 2/12p0065v

2/12 + 3/12p0065v

3/12 + . . .+ 5−1/12p0065v

5−1/12)

(b) a(12)0065:5 > a00

65:5

More premium will be paid up front under a(12)0065:5 , similar to the fact that a00

65:5 > a0065:5 .

(c) 50, 000a(12)0165:5 = 50, 000× 1

12

(1/12p

0165v

1/12 + 2/12p0165v

2/12 + 3/12p0165v

3/12 + . . .+ 5p0165v

5)

(d) 100, 000A0265:5 = 100, 000

∫ 5

0e−δt

(tp

0065µ

0265+t + tp

0165µ

1265+t

)dt

(e) P =50, 000a(12)01

65:5 + 100, 000A0265:5

12a(12)0065:5

50.1 Check your knowledge

Homework 50.1.1

An insurer issues a combined 10-year disability and death benefit policy to a healthy life aged 50. You are given:

Healthy Disabled

Dead

0 1

2

µ10x+t

µ01x+t

µ 02x+t µ

12x+t

(a) The product pays a continuous disability benefit at the rate of 50,000 per year while the insured is disabled, andpays a death benefit of 100,000 at the moment of death.

(b) Gross premium is payable continuously at the rate of P per year while the insured is healthy

(c) Premium expense is 2% of the gross premium. There are no other expenses.

(d) δ = 0.05

(e) µ01x+t = 0.02, µ10

x+t = 0.01, µ02x+t = 0.01 + 0.005t, µ12

x+t = 0.02 + 0.01t

Selective actuarial values where x = 50 and n = 10:

k A01x+k:n−k A

02x+k:n−k A

12x+k:n−k a00

x+k:n−k a01x+k:n−k a10

x+k:n−k a11x+k:n−k

0 0.12856 0.23701 0.37223 6.49636 0.50610 0.26205 6.146855 0.07652 0.19262 0.32982 3.84198 0.16607 0.08384 3.61567

(a) Calculate P .

(b) Actuary Mark decided to invent a new symbolAi→j→rx:n to represent the APV of the benefit 1 payable immediately

up on (x) moving from the state j to the state r during the first n years given that the insured is in the state i attime zero. Calculate the sum of A0→0→2

55:5 and A0→1→255:5 for this policy.

(c) Actuary Katie is a computation wizard and can calculate anything including a0250+k:10−k and a12

50+k:10−k where0 ≤ k ≤ 10. Define these two symbols and explain whether it ever makes sense for her to calculate these two valuesfor this policy.

(d) This is how Actuary Jeff explains the difference between a0250:10 and a12

50:10 : Both symbols represent the APV ofthe benefit 1 payable continuously while the insured is dead, with payments ceasing after first 10 years. However,a02

50:10 is the APV of such benefits where the insured is healthy at death. In contrast, a1250:10 is the APV of such

benefits where the insured is disabled at death. Is Jeff’s explanation correct?

(e) Define the symbol A0250+k:10−k .

(f) Calculate the gross premium policy value 5V(0).

(g) Calculate the gross premium policy value 5V(1).