Embed Size (px)

Citation preview

The RAFI™ Multi-Factor

Index

Chris Brightman, CFAChief Investment Officer

Research Affiliates, LLC

2

RAFI Multi-Factor Index Series

RAFI Multi-Factor is a smart beta equity strategy that offers diversified factor

exposures through allocations to value, low volatility, quality, momentum, and size.

» Theoretically and empirically robust single-factor strategies

» Diversified factor exposures designed for a smoother ride, offered through a rules-based, transparent index construct

» Potential for added returns through a thoughtful dynamic weighting process

3

Index Global DevelopedDeveloped

Ex US

United

States

Emerging

Markets

RAFI Dynamic Multi-Factor Index

RAFI Multi-Factor Index

RAFI Value Factor Index

RAFI Low Volatility Factor Index

RAFI Quality Factor Index

RAFI Size Factor Index

RA Momentum Factor Index

» No Size Factor Index in Emerging Markets because it is not investable.

» Global Multi-Factor Indices utilize the RAFI Size Factor Developed Index as the size component.

» Momentum is not offered as a stand-alone index product because

» Transparent index construct is not optimal for momentum strategies, and

» Implementation costs as a stand-alone strategy are high. Works well, however, as part of an investment process.

Available Indices

4

A Natural Extension of Our Research

The RAFI™

Fundamental

Index™ Approach

“FundamentalIndexation”

Arnott, Hsu, Moore

Financial Analysts Journal

March 2005

“An Overwrought Orthodoxy”

Arnott

Institutional Investor

December 2006

“Institutionalizing Courage”

Arnott

May 2012

Smart Beta

Strategies and

Factor Exposures

“A Survey of Alternative Equity Index Strategies”

Chow, Hsu, Kalesnik, Little

Financial Analysts Journal

September 2011

“The Surprising Alphafrom Malkiel’s Monkey…”

Arnott, Hsu, Kalesnik, Tindall

Journal of Portfolio Mgmt.

August 2013

Robustness of

Factors

“Finding Smart Beta in the Factor Zoo”

Hsu, Kalesnik

July 2014

“Will Your Factor Deliver?...”

Beck, Hsu, Kalesnik, Kostka

Financial Analysts Journal

September 2016

The Effects of

Valuations on

Smart Beta

“How Can ‘Smart Beta’ Go Horribly Wrong?”

Arnott, Beck, Kalesnik, West

February 2016

“To Win with ‘Smart Beta’ Ask If the Price Is Right”

Arnott, Beck, Kalesnik

June 2016

“Timing ‘Smart Beta’ Strategies? Of Course! Buy Low, Sell High!”

Arnott, Beck, Kalesnik

September 2016

5

Based on the RAFI Fundamental Index Approach

Book Value

Dividends+

Buybacks

Cash Flow

DeleveredSales

» Results in a systematic rebalancing approach with:

› A history of outperformance, based on sound investing principles

› Broad economic representation

› Low turnover, fees, and implementation costs, and high capacity

» Selects and weights securities by fundamental measures of firm size.

6

Starting Universe

• Start with six regions: US, Japan, UK, Europe ex UK, Other Developed, Emerging Markets

• Top 86% by cumulative fundamental weight constitutes large-company portfolios

• 86–98% by cumulative fundamental weight constitutes small-company portfolios

• Bottom 2% excluded due to illiquidity

Assign Factor Scores

• Assign factor scores for the magnitude of each stock’s exposure to value, low volatility, quality, and momentum

Form Individual Factor Indices

• RAFI Value Factor Index

• RAFI Low Volatility Factor Index

• RAFI Quality Factor Index

• RA Momentum Factor Index

• RAFI Size Factor Index (combines the four factor strategies within small company)

Weight Factor Indices by RAFI weight (exception: Momentum)

Implement Trading Controls to Minimize Turnover

• Turnover Control

• Momentum Filtering

RAFI Multi-Factor Index RAFI Dynamic Multi-Factor Index

• Equally weights combination of five factors (except for EM which excludes size)

• Rebalances factor strategies back to equal weight on a quarterly basis

• Uses reversal and momentum measures to allocate to each factor

• Adjusts dynamic allocations quarterly

Investment Process

7

RAFI Factor Index Strategies

8

0.0

0.1

0.2

0.3

0.4

0.5

0.6

Bo

ok-t

o-P

rice

Earn

ing

s-to

-Pri

ce

Cash

flo

w-t

o-P

rice

Div

iden

ds-

to-P

rice

Lo

w B

eta

Lo

w V

ola

tility

-2 t

o -

12 M

on

ths

-2 t

o -

6 M

on

ths

-1 t

o -

12 M

on

ths

Gro

ss P

rofi

tab

ilit

y

Retu

rn o

n E

qu

ity

Gro

ss M

arg

ins

Bo

ok L

evera

ge

50%

Sm

all, 50%

Big

75%

Sm

all, 25%

Big

25%

Sm

all, 75%

Big

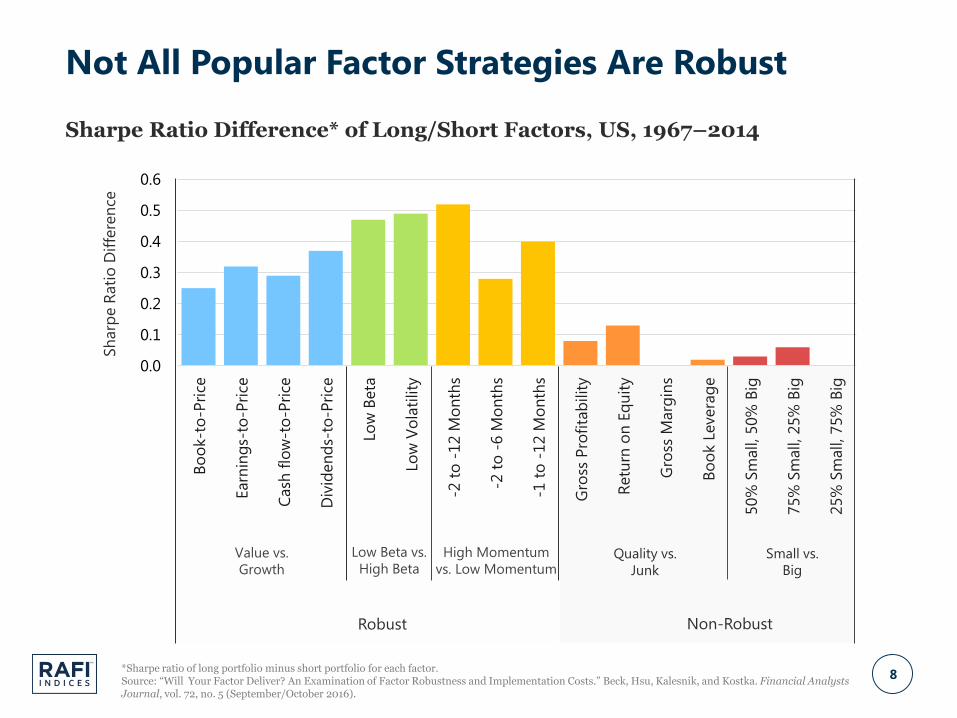

Not All Popular Factor Strategies Are Robust

Sharpe Ratio Difference* of Long/Short Factors, US, 1967–2014

Value vs.

Growth

Low Beta vs.

High Beta

High Momentum

vs. Low MomentumQuality vs.

Junk

Small vs.

Big

Robust Non-Robust

Sh

arp

e R

ati

o D

iffe

ren

ce

*Sharpe ratio of long portfolio minus short portfolio for each factor.Source: “Will Your Factor Deliver? An Examination of Factor Robustness and Implementation Costs.” Beck, Hsu, Kalesnik, and Kostka. Financial Analysts Journal, vol. 72, no. 5 (September/October 2016).

9

RAFI Value Factor Index

» A concentrated value strategy that selects securities by their ratio of fundamentals to capitalization weight

» Selects companies with a large economic footprint relative to their market capitalization

Book Value

Dividends+

Buybacks

Cash Flow

DeleveredSales

Cap-Weight

vs.

10

RAFI Low Volatility Factor Index

» A concentrated low-volatility strategy that selects securities using a systematic risk measure

» Volatility includes both diversifiable and non-diversifiable risk.

» Beta only captures risk associated with the global equity market.

Diversifiable RiskGlobal Beta

Industry Beta

CountryBeta

Systematic Risk

Total Variance

Diversifiable risk is the unexplained variance from a three-factor regression model against a global index, industry index, and country index specific to that stock.

11

RAFI Quality Factor Index

» A concentrated quality strategy that uses the combination of high profitability and low investment to select quality stocks

Profitability Low Investment*

Operating Profitability Asset Growth

Return on Equity Book Growth

Return on Assets

*No Empire Building

12

Improving the Quality Factor

» If quality is not robust, why incorporate as a factor?

US results are for the period 1967–2015; International results are for the period 1987–2015. Results are for large-cap stocks for each region or definition.Source: Research Affiliates, LLC, based on data from CRSP/Compustat and Worldscope/Datastream.

» Quality factors based on profitability are negatively correlated with value.

» Combining profitability and investment is more robust.

Note: Sharpe ratio differences for all strategies except Japan are statistically significant at the 95% confidence level.

0.530.49

0.53

0.06

0.51

0.22 0.210.17

0.09

0.23

-0.20

0.00

0.20

0.40

0.60

0.80

United

States

United

Kingdom

Europe

ex UK

Japan Global

Sharpe Ratios of Quality Vs. Junk

Quality Junk

13

RAFI Size Factor Index

» Equally weighted allocation to four factors—value, low volatility, quality, and momentum—within the small universe

US results are for the period 1967–2014; International results are for the period 1987–2014. Source: “Will Your Factor Deliver? An Examination of Factor Robustness and Implementation Costs.” Beck, Hsu, Kalesnik, and Kostka. Financial Analysts Journal, vol. 72, no. 5 (September/October 2016).

0.50

0.69

0.43

0.61

0.240.19

0.39

-0.05

-0.20

0.00

0.20

0.40

0.60

0.80

Value vs.

Growth

Low Beta vs.

High Beta

Quality vs.

Junk

Winners vs.

Losers

Sharpe Ratios of Factor Portfolios Within Small-Cap Stocks, US

0.58

0.70

0.51

0.66

0.14

0.260.23

-0.15-0.20

0.00

0.20

0.40

0.60

0.80

Value vs.

Growth

Low Beta vs.

High Beta

Quality vs.

Junk

Winners vs.

Losers

Sharpe Ratios of Factor Portfolios within Small-Cap Stocks, Global

Note: Sharpe ratio differences for all factors except Quality in the US are statistically significant at the 95% confidence level.

0.58

0.70

0.51

0.66

0.14

0.260.23

-0.15-0.20

0.00

0.20

0.40

0.60

0.80

Value vs.

Growth

Low Beta vs.

High Beta

Quality vs.

Junk

Winners vs.

Losers

Sharpe Ratios of Factor Portfolios - Global

Long Portfolio Short Portfolio

14

Momentum Factor Index

» Uses multiple measures of momentum as a diversifying component in the RAFI Multi-Factor strategy

Measure Definition Benefit

Standard

Momentum

Past 12-month return excluding

most recent month

Widely known, well-vetted

measure of momentum1

Idiosyncratic

Momentum

Beta-adjusted standard

momentumLess prone to momentum crashes2

Fresh

Momentum

Standard momentum relative to

previous year

Less likely to pick momentum

stocks trading at high valuations3

1. “Returns to Buying Winners and Selling Losers: Implication for Stock Market Efficiency.” Jegadeesh and Titman, Journal of Finance, vol. 48, no. 1, (March 1993).

2. “Idiosyncratic Momentum: US and International Evidence.” Chaves, Journal of Investing, vol. 25, no. 2 (Summer 2016).3. “Fresh Momentum.” Chen, Kadan, and Kose (October 2009).

15

Value Low Volatility Quality Momentum

Characteristics 𝑅𝐴𝐹𝐼

𝐶𝐴𝑃Systematic Risk Profitability

» Oper. Profitability

» ROE

» ROA

Investment

» Asset Growth

» Book Growth

» Momentum

» Idiosyncratic-

Momentum

» Fresh

Momentum

SelectionSelect top ¼ cumulative fundamental weights by

characteristics.Select top ½.

WeightingRAFI Fundamental Index Approach: Delevered Sales,

Cash Flow, Dividends + Buybacks, and Book ValueMarket Cap

Rebalancing Quarterly Staggered Rebalance (25% each quarter) Quarterly

» Size Factor: Average of four factors (value, low volatility, quality, and

momentum) built within small universe and rebalanced quarterly

RAFI Factor Index Construction

1616

Reduced Turnover through

Thoughtful Design Characteristics

17

» Turnover Control: At each quarterly rebalance, replace 10% of current holdings in existing portfolio (20% for momentum).

» Remove securities with the least attractive characteristics.

» Rebalance entire portfolio to current target weights.

» Momentum Filtering

» Rank securities in rebalanced portfolio by standard momentum.

» Top 25% of portfolio ranked by momentum: Do not sell.

» Bottom 25% of portfolio ranked by momentum: Do not buy.

Turnover Control & Momentum Filtering

18

Example – RAFI Value Factor US Index

CharacteristicsWithout Turnover Control &

Momentum Trade FilteringWith Turnover Control

With Turnover Control &

Momentum Trade Filtering

Annual One-Way Turnover 36.9% 26.0% 20.0%

Estimated Transaction Costs 19bps 11bps 9bps

Po

rtfo

lio

Weig

ht

High

Low

Turnover Control

Valu

e S

ign

al

1. Rank existing

portfolio by value

signal (RAFI/Cap).

2. Replace bottom 10%

of portfolio with new

constituents.

Momentum Filtering

Po

rtfo

lio

Weig

ht

High

Low

Mo

men

tum

Sig

nal

Bottom

25%

Don’t

Buy

Top 25%

Don’t

Sell

1. With new names added,

rank Value Factor Index

by momentum.

2. Do not sell high-

momentum stocks while

they’re soaring.

3. Do not buy low-

momentum stocks while

they’re in free fall.

4. Rebalance the middle

50% back to

fundamental weights.

Top 90%

Don’t

Remove

Source: Research Affiliates, LLC, using data from Worldscope, and Datastream. Turnover and transaction costs are estimated for the period 5/1987– 9/2016. Estimated transaction costs assume $5B in AUM.The index data published herein are simulated. Please see important disclosure information at end.

1919

Dynamic Allocation

20

Valuation Cycle for Value Factor

Source: Research Affiliates, LLC, using data from CRSP and Compustat, 1968–2016. Value vs. growth portfolios are constructed using a long/short portfolio of four valuation metrics: book/price, earnings/price, dividend/price, and cash flow/price.

0.13

0.25

0.50

1.00

2.00

0.25

0.50

1.00

2.00

4.00

1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

Relative

Valuation

Value

vs.

Growth

Relative

Performance

Value

vs.

Growth

Value Performance Relative Valuation

A

A

B

B

C

C

D

D

E

E

Nifty Fifty

Biotech Bubble

Tech

Bubble

Global

Financial

Crisis

Value vs. Growth, US, 1968–2016

21

Return Due to Change in Valuation

Source: Research Affiliates, LLC, using data from CRSP and Compustat, 1968–2016. Value vs. growth portfolios are constructed using a long/short portfolio of four valuation metrics: book/price, earnings/price, dividend/price, and cash flow/price.

0.25

0.5

1

2

4

8

16

0.5

1

2

4

8

1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

Rela

tive

Valu

ati

on

, M

om

en

tum

Rela

tive

Perf

orm

an

ce, M

om

en

tum

Up vs. Down, Momentum, US, 1968-2016

Momentum Performance Relative Valuation

0.25

0.5

1

2

4

8

16

0.5

1

2

4

1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

Rela

tive

Valu

ati

on

, Sm

all C

ap

Rela

tive

Perf

orm

an

ce, Sm

all C

ap

Small Cap vs. Large Cap, US, 1968-2016

Small Cap Performance Relative Valuation

0.125

0.25

0.5

1

2

4

8

16

0.5

1

2

4

8

1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

Rela

tive

Valu

ati

on

, Lo

w B

eta

Rela

tive

Perf

orm

an

ce, Lo

w B

eta

Low Beta vs. High Beta, US, 1968-2016

Low Beta Performance Relative Valuation

1

2

4

0.5

1

2

1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

Rela

tive

Valu

ati

on

, P

rofi

tab

ilit

y

Rela

tive

Perf

orm

an

ce, P

rofi

tab

ilit

y

Profitable vs. Unprofitable, US, 1968-2016

Profitability Performance Relative Valuation

22

» Dynamic Indicators

» Long-term reversal: five-year return excluding past one-year return.

» Short-term momentum: one-year return minus past one-month return.

» Rebalance Dynamic Allocation Quarterly

» Start with equal-weight anchor.

» Allocate toward factors that have underperformed over the past five years, but have outperformed over the past one year.

» Dynamic allocation limited to ±15% of equal-weight anchor.

Dynamic Factor Allocation

23

Factor Valuations Today – United States

Source: Research Affiliates, LLC, using data from CRSP and Compustat, 1967–2016. The index data published herein are simulated. Please see important disclosure information at end.

Valuations Relative to History (3/31/2017)

0.25

0.50

1.00

2.00

RAFI Dynamic

Multi-Factor

US Index

RAFI Value

Factor US

Index

RAFI Low

Volatility Factor

US Index

RAFI Quality

Factor US

Index

RA Momentum

Factor US

Index

RAFI Size

Factor US

Index

Ag

gre

gate

Valu

ati

on

Rati

o v

s. C

ap

-Weig

ht

10th to 90th Percentile Median Valuation Current Valuation

24

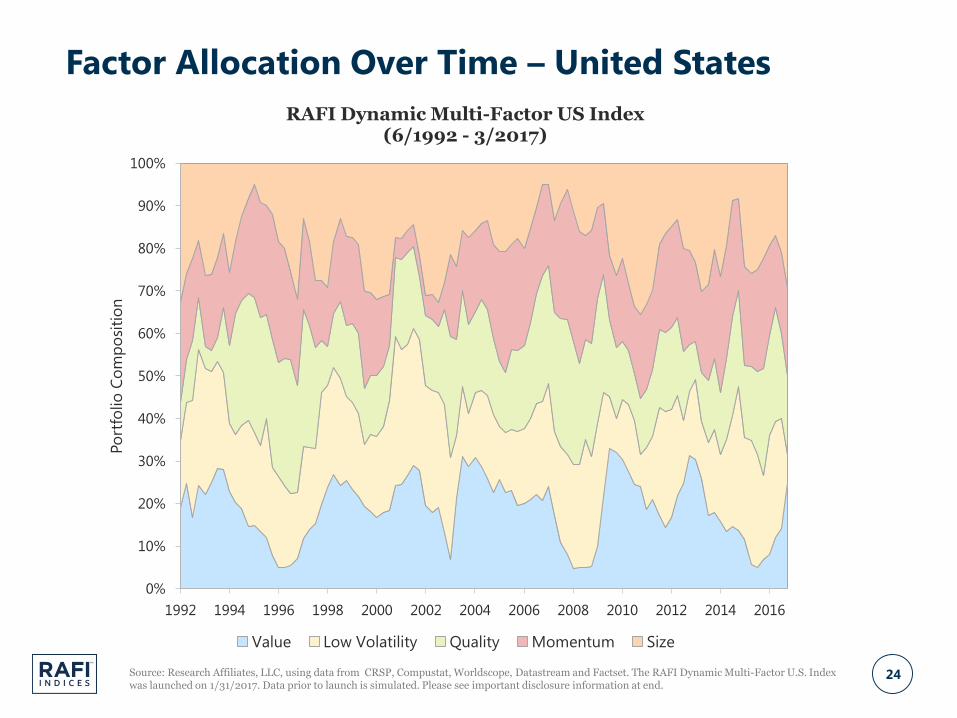

Factor Allocation Over Time – United States

Source: Research Affiliates, LLC, using data from CRSP, Compustat, Worldscope, Datastream and Factset. The RAFI Dynamic Multi-Factor U.S. Index was launched on 1/31/2017. Data prior to launch is simulated. Please see important disclosure information at end.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Po

rtfo

lio

Co

mp

osi

tio

nRAFI Dynamic Multi-Factor US Index

(6/1992 - 3/2017)

Value Low Volatility Quality Momentum Size

25

Performance and Characteristics

Source: Research Affiliates, LLC, using data from Solactive, CRSP, Compustat, Worldscope, and Datastream. The RAFI Multi-Factor U.S. indices were launched on 1/31/2017. Data prior to launch is simulated. One-way turnover data is for the period 1993 – 2016. Capacity and transaction cost estimates are as of 12/31/2016.

Results – United States

Factor Regression

United States

6/1992–3/2017

Annualized

Return

Annualized

Volatility

Sharpe

Ratio

Tracking

Error

Information

Ratio

One-Way

Turnover

Capacity

$B

Cost at

$5B

RAFI Dynamic Multi-Factor US Index 12.4% 12.7% 0.77 4.4% 0.64 50.9% 18.8 0.13%

RAFI Multi-Factor US Index 12.0% 12.7% 0.74 4.2% 0.59 38.0% 29.8 0.08%

Russell 3000 Index 9.5% 14.5% 0.48

RAFI Value Factor US Index 13.0% 15.1% 0.69 7.8% 0.44 18.3% 30.5 0.08%

RAFI Low Volatility Factor US Index 11.1% 11.2% 0.76 9.0% 0.17 15.0% 46.3 0.05%

RAFI Quality Factor US Index 11.9% 12.3% 0.76 5.9% 0.39 19.2% 36.2 0.07%

RA Momentum Factor US Index 12.0% 14.0% 0.67 4.6% 0.52 90.2% 4.0 0.62%

RAFI US Index 11.5% 14.9% 0.60 5.1% 0.39 11.8% 192.3 0.01%

Russell 1000 Index 9.6% 14.4% 0.49

RAFI Size Factor US Index 12.6% 16.4% 0.61 5.4% 0.55 53.3% 3.7 0.67%

Russell 2000 Index 9.6% 18.7% 0.38

United States

6/1992–3/2017

Alpha

(Annual)

Beta

(Mkt-Rf)

Size

(SMB)

Value

(HML)

Profitability

(RMW)

Investment

(CMA)

Momentum

(WML)

Low Beta

(BAB)

RAFI Dynamic Multi-Factor US Index 0.6% 0.93 0.13 0.03 0.06 0.19 0.05 0.13

RAFI Multi-Factor US Index 0.3% 0.93 0.13 0.04 0.08 0.17 0.02 0.14

RAFI Value Factor US Index 0.2% 0.99 0.18 0.20 0.10 0.39 -0.09 0.17

RAFI Low Volatility Factor US Index 0.2% 0.74 0.03 0.04 0.03 0.18 -0.08 0.40

RAFI Quality Factor US Index 0.6% 0.90 -0.03 -0.07 0.20 0.33 -0.06 0.14

RA Momentum Factor US Index 0.8% 1.00 -0.06 0.04 0.06 -0.03 0.21 -0.03

RAFI Size Factor US Index 0.5% 0.99 0.58 -0.02 0.06 0.00 0.09 0.08

RAFI US Index 0.1% 0.97 0.00 0.17 0.08 0.24 -0.09 0.10

26

Performance and Characteristics

Source: Research Affiliates, LLC, using data from Solactive, CRSP, Compustat, Worldscope, and Datastream. The RAFI Multi-Factor Developed Indices were launched on 3/31/2017. Data prior to launch is simulated. One-way turnover data is for the period 1993 –2016. Capacity and transaction cost estimates are as of 12/31/2016.

Results – Developed

Factor Regression

Developed

6/1992-3/2017

Annualized

Return

Annualized

Volatility

Sharpe

Ratio

Tracking

Error

Information

Ratio

One-Way

Turnover

Capacity

$B

Cost at

$5B

RAFI Dynamic Multi-Factor Dev Index 10.6% 13.1% 0.61 3.8% 0.75 52.8% 26.6 0.09%

RAFI Multi-Factor Dev Index 10.5% 13.1% 0.60 3.7% 0.76 41.1% 35.7 0.07%

RAFI Value Factor Dev Index 12.2% 14.9% 0.64 5.8% 0.77 24.3% 26.0 0.10%

RAFI Low Volatility Factor Dev Index 10.7% 11.2% 0.73 6.9% 0.43 20.0% 43.9 0.06%

RAFI Quality Factor Dev Index 10.6% 12.6% 0.63 4.3% 0.67 22.1% 44.6 0.06%

RA Momentum Factor Dev Index 9.2% 14.0% 0.48 3.9% 0.39 94.8% 6.3 0.40%

RAFI Size Factor Dev Index 10.7% 15.3% 0.53 6.6% 0.45 56.3% 3.6 0.69%

RAFI Developed Index 9.9% 14.2% 0.52 3.6% 0.62 12.3% 227.3 0.01%

MSCI World Index 7.7% 14.5% 0.35

Developed

6/1992–3/2017

Alpha

(Annual)

Beta

(Mkt-Rf)

Size

(SMB)

Value

(HML)

Profitability

(RMW)

Investment

(CMA)

Momentum

(WML)

Low Beta

(BAB)

RAFI Dynamic Multi-Factor Dev Index 0.2% 0.95 0.16 0.08 0.13 0.07 0.08 0.08

RAFI Multi-Factor Dev Index 0.2% 0.95 0.16 0.08 0.15 0.06 0.04 0.09

RAFI Value Factor Dev Index 1.0% 1.03 0.29 0.29 0.25 0.15 -0.06 -0.01

RAFI Low Volatility Factor Dev Index 1.4% 0.76 0.03 0.00 -0.06 0.11 -0.07 0.38

RAFI Quality Factor Dev Index 0.5% 0.92 0.03 0.02 0.31 0.14 -0.03 0.10

RA Momentum Factor Dev Index -0.8% 0.99 -0.10 0.06 0.10 -0.03 0.22 0.00

RAFI Size Factor Dev Index 0.3% 1.01 0.66 0.03 0.15 -0.03 0.09 0.01

RAFI Developed Index 0.5% 0.98 0.01 0.25 0.06 0.08 -0.07 0.01

27

Performance and Characteristics

Source: Research Affiliates, LLC, using data from Solactive, CRSP, Compustat, Worldscope, and Datastream. The RAFI Multi-Factor Developed ex-U.S. indices were launched on 1/31/2017. Data prior to launch is simulated. One-way turnover data is for the period 1993 – 2016. Capacity and transaction cost estimates are as of 12/31/2016.

Results – Developed ex-US

Factor Regression

Developed ex US

6/1992–3/2017

Annualized

Return

Annualized

Volatility

Sharpe

Ratio

Tracking

Error

Information

Ratio

One-Way

Turnover

Capacity

$B

Cost at

$5B

RAFI Dynamic Multi-Factor DxUS Index 9.5% 14.6% 0.47 3.9% 0.86 53.1% 11.6 0.22%

RAFI Multi-Factor DxUS Index 9.4% 14.7% 0.47 3.8% 0.87 41.9% 15.2 0.16%

RAFI Value Factor DxUS Index 11.0% 16.5% 0.51 5.6% 0.87 26.0% 9.5 0.26%

RAFI Low Volatility Factor DxUS Index 9.8% 12.7% 0.57 6.7% 0.55 22.0% 20.2 0.12%

RAFI Quality Factor DxUS Index 9.5% 14.5% 0.48 4.1% 0.83 22.6% 20.5 0.12%

RA Momentum Factor DxUS Index 8.4% 15.2% 0.38 4.2% 0.56 97.1% 2.8 0.91%

RAFI Size Factor DxUS Index 9.1% 16.3% 0.40 6.5% 0.46 55.7% 1.7 1.44%

RAFI Developed ex US Index 8.5% 16.0% 0.37 3.3% 0.72 12.8% 178.6 0.01%

MSCI World ex US Index 6.1% 16.2% 0.22

Developed ex US

6/1992–3/2017

Alpha

(Annual)

Beta

(Mkt-Rf)

Size

(SMB)

Value

(HML)

Profitability

(RMW)

Investment

(CMA)

Momentum

(WML)

Low Beta

(BAB)

RAFI Dynamic Multi-Factor DxUS Index 0.6% 0.97 0.12 0.12 0.08 0.02 0.10 0.06

RAFI Multi-Factor DxUS Index 0.7% 0.97 0.12 0.15 0.10 0.00 0.06 0.06

RAFI Value Factor DxUS Index 1.3% 0.97 0.16 0.41 0.23 0.11 0.00 -0.08

RAFI Low Volatility Factor DxUS Index 1.3% 0.96 0.04 0.08 -0.04 0.04 -0.06 0.36

RAFI Quality Factor DxUS Index 1.0% 0.96 0.02 0.11 0.21 0.02 0.01 0.09

RA Momentum Factor DxUS Index -0.1% 0.94 -0.10 0.10 -0.04 -0.06 0.26 -0.03

RAFI Size Factor DxUS Index 0.9% 1.00 0.62 0.03 0.13 -0.05 0.07 0.01

RAFI Developed ex US Index 0.9% 0.96 0.00 0.26 0.05 0.01 -0.05 -0.03

28

Performance and Characteristics

Source: Research Affiliates, LLC, using data from Solactive, CRSP, Compustat, Worldscope, and Datastream. The RAFI Multi-Factor Global indices were launched on 3/31/2017. Data prior to launch is simulated. One-way turnover data is for the period 1993 – 2016. Capacity and transaction cost estimates are as of 12/31/2016.

Results – Global

Factor Regression

Global

6/2007-3/2017

Annualized

Return

Annualized

Volatility

Sharpe

Ratio

Tracking

Error

Information

Ratio

One-Way

Turnover

Capacity

$B

Cost at

$5B

RAFI Dynamic Multi-Factor Global Index 5.5% 16.2% 0.30 2.5% 0.64 56.4% 27.8 0.09%

RAFI Multi-Factor Global Index 5.4% 16.3% 0.30 2.1% 0.74 43.0% 36.8 0.07%

RAFI Value Factor Global Index 5.6% 18.6% 0.27 4.2% 0.43 26.8% 22.3 0.11%

RAFI Low Volatility Factor Global Index 6.1% 13.1% 0.42 6.3% 0.35 20.8% 36.2 0.07%

RAFI Quality Factor Global Index 6.3% 15.9% 0.36 2.7% 0.92 24.0% 41.0 0.06%

RA Momentum Factor Global Index 4.1% 16.4% 0.22 3.6% 0.06 93.9% 6.5 0.38%

RAFI Size Factor Developed Index 5.3% 18.4% 0.26 4.6% 0.32 58.6% 3.6 0.69%

RAFI Global Index 4.5% 17.6% 0.22 2.6% 0.23 11.7% 108.7 0.02%

MSCI All Country World Index 3.9% 17.1% 0.19

Global

6/2007–3/2017

Alpha

(Annual)

Beta

(Mkt-Rf)

Size

(SMB)

Value

(HML)

Profitability

(RMW)

Investment

(CMA)

Momentum

(WML)

Low Beta

(BAB)

RAFI Dynamic Multi-Factor Global Index -0.1% 0.98 0.05 -0.01 0.12 0.22 0.09 0.02

RAFI Multi-Factor Global Index -0.1% 0.98 0.06 -0.02 0.15 0.20 0.05 0.02

RAFI Value Factor Global Index 0.8% 1.06 0.23 0.10 0.15 0.38 0.01 -0.22

RAFI Low Volatility Global Index -0.8% 0.78 -0.10 -0.07 0.02 0.29 -0.13 0.50

RAFI Quality Factor Global Index 0.2% 0.98 -0.06 -0.07 0.33 0.23 0.01 0.00

RA Momentum Factor Global Index -1.0% 1.01 -0.10 0.02 0.14 0.01 0.23 -0.01

RAFi Size Factor Developed Index 1.2% 1.03 0.43 -0.13 -0.08 0.15 0.13 -0.12

RAFI Global Index 0.1% 1.00 -0.07 0.20 0.03 0.20 -0.06 -0.05

29

Performance and Characteristics

Source: Research Affiliates, LLC, using data from Solactive, CRSP, Compustat, Worldscope, and Datastream. The RAFI Multi-Factor Emerging Market indices were launched on 1/31/2017. Data prior to launch is simulated. One-way turnover data is for the period 1993 – 2016. Capacity and transaction cost estimates are as of 12/31/2016.

Results – Emerging Markets

Emerging Markets

6/2007–3/2017

Annualized

Return

Annualized

Volatility

Sharpe

Ratio

Tracking

Error

Information

Ratio

One-Way

Turnover

Capacity

$B

Cost at

$5B

RAFI Dynamic Multi-Factor EM Index 4.7% 23.0% 0.18 3.9% 0.68 53.0% 3.0 0.83%

RAFI Multi-Factor EM Index 4.8% 23.1% 0.18 3.8% 0.70 45.3% 3.8 0.65%

RAFI Value Factor EM Index 6.2% 26.4% 0.22 8.6% 0.48 21.4% 4.8 0.52%

RAFI Low Volatility EM Index 6.1% 19.1% 0.29 8.4% 0.47 22.2% 5.8 0.43%

RAFI Quality Factor EM Index 4.1% 23.6% 0.15 5.2% 0.38 22.4% 5.7 0.44%

RA Momentum Factor EM Index 3.4% 23.3% 0.12 5.3% 0.23 95.2% 0.8 3.17%

RAFI Emerging Markets Index 4.1% 24.6% 0.15 4.8% 0.42 16.2% 34.2 0.07%

MSCI Emerging Markets Index 2.1% 23.6% 0.07

Factor Regression

Emerging Markets

6/2007–3/2017

Alpha

(Annual)

Beta

(Mkt-Rf)

Size

(SMB)

Value

(HML)

Profitability

(RMW)

Investment

(CMA)

Momentum

(WML)

Low Beta

(BAB)

RAFI Dynamic Multi-Factor EM Index -0.3% 0.99 -0.07 0.10 0.06 0.24 0.10 -0.04

RAFI Multi-Factor EM Index -0.3% 0.99 -0.06 0.12 0.07 0.21 0.09 -0.04

RAFI Value Factor EM Index -0.2% 0.98 0.16 0.46 0.25 0.32 0.00 -0.23

RAFI Low Volatility EM Index 2.5% 0.80 -0.08 -0.07 -0.19 0.32 0.02 -0.02

RAFI Quality Factor EM Index -0.6% 1.01 -0.32 -0.02 0.17 0.33 -0.04 -0.04

RA Momentum Factor EM Index -1.8% 1.05 -0.08 0.02 0.01 0.14 0.33 0.03

RAFI Emerging Markets Index -1.1% 1.00 -0.13 0.34 0.10 0.27 -0.13 -0.06

30

» Uses robust single-factor strategies.

» Diversifies allocations to individual factors:

» Balanced factor exposures

» Low tracking error/high information ratio

» Ability to weather sharp or prolonged downturns of any single

factor

» Systematic approach spares investors from performance chasing.

Summary

31

Appendix

32

3/31/2017# of

SecuritiesP/E P/B P/S P/CF

Dividend

Yield

Weighted Avg.

Mkt. Cap ($B)

RAFI Dynamic Multi-Factor Global Index 3522 17.5 1.9 0.9 8.2 2.6% 54.7

RAFI Multi-Factor Global Index 3626 17.5 1.9 1.0 8.3 2.6% 56.1

RAFI Value Factor Global Index 827 13.9 1.2 0.5 5.6 2.5% 32.5

RAFI Low Volatility Factor Global Index 985 18.0 2.2 1.2 9.3 2.8% 68.7

RAFI Quality Factor Global Index 805 18.0 2.7 1.2 9.1 2.9% 70.8

RA Momentum Factor Global Index 1105 18.4 2.0 1.4 8.8 2.5% 86.5

RAFI Global Index 2594 16.4 1.5 1.0 7.1 2.8% 83.8

RAFI Dynamic Multi-Factor Developed Index 3052 18.7 2.0 1.0 9.0 2.6% 57.7

RAFI Multi-Factor Developed Index 3134 18.7 2.0 1.0 9.1 2.6% 59.0

RAFI Value Factor Developed Index 653 15.6 1.3 0.5 6.2 2.5% 35.5

RAFI Low Volatility Factor Developed Index 648 19.2 2.5 1.2 10.4 2.9% 78.0

RAFI Quality Factor Developed Index 579 19.3 3.0 1.2 9.7 2.8% 77.9

RA Momentum Factor Developed Index 847 19.9 2.1 1.5 10.4 2.5% 90.0

RAFI Size Factor Developed Index 1981 19.2 2.1 1.1 10.2 2.1% 4.5

RAFI Developed Index 1766 17.7 1.6 1.0 7.9 2.8% 89.8

RAFI Dynamic Multi-Factor Dev. ex US Index 2147 17.6 1.6 0.9 8.0 2.9% 32.8

RAFI Multi-Factor Developed ex US Index 2152 17.3 1.5 0.8 7.8 2.9% 32.1

RAFI Value Factor Developed ex US Index 312 14.0 0.8 0.4 4.9 2.7% 26.4

RAFI Low Volatility Factor Dev. ex US Index 461 17.7 1.8 1.0 8.8 3.2% 34.3

RAFI Quality Factor Developed ex US Index 361 18.1 2.2 1.1 8.8 3.1% 41.9

RA Momentum Factor Developed ex US Index 582 19.1 1.7 1.2 9.1 3.0% 48.8

RAFI Size Factor Developed ex US Index 1225 16.8 1.6 0.9 9.6 2.6% 3.7

RAFI Developed ex US Index 1238 16.5 1.3 0.8 6.6 3.3% 48.6

Global

Developed

Developed ex US

Source: Research Affiliates, LLC, using data from Solactive and Factset.

Characteristics

33

3/31/2017# of

SecuritiesP/E P/B P/S P/CF

Dividend

Yield

Weighted Avg.

Mkt. Cap ($B)

RAFI Dynamic Multi-Factor US Index 947 20.1 2.8 1.3 10.8 2.4% 92.8

RAFI Multi-Factor US Index 947 20.0 2.7 1.2 10.4 2.4% 90.2

RAFI Value Factor US Index 112 16.7 1.6 0.7 7.0 2.6% 63.2

RAFI Low Volatility Factor US Index 113 18.8 3.6 1.2 11.2 2.7% 113.6

RAFI Quality Factor US Index 123 19.7 5.8 2.1 13.0 2.5% 142.4

RA Momentum Factor US Index 228 22.9 3.2 2.2 13.0 2.2% 131.6

RAFI Size Factor US Index 549 22.0 2.3 1.1 10.4 2.0% 5.4

RAFI US Index 528 19.1 2.3 1.4 10.0 2.3% 134.6

RAFI Dynamic Multi-Factor EM Index 574 11.5 1.1 0.7 4.7 2.8% 29.3

RAFI Multi-Factor EM Index 574 11.6 1.1 0.7 4.9 2.8% 32.3

RAFI Value Factor EM Index 145 8.7 0.7 0.4 3.3 3.2% 13.7

RAFI Low Volatility EM Index 266 9.8 1.0 0.7 5.4 3.8% 12.4

RAFI Quality Factor EM Index 207 10.7 1.3 1.2 5.7 3.9% 26.9

RA Momentum Factor EM Index 252 14.6 1.8 1.2 5.8 2.2% 68.4

RAFI Emerging Markets Index 828 10.9 1.1 0.8 4.2 2.9% 41.8

United States

Emerging Markets

Source: Research Affiliates, LLC, using data from Solactive and Factset.

Characteristics (cont.)

34Source: Research Affiliates, LLC, using data from CRSP, Compustat, Worldscope, Datastream and Factset. The RAFI Dynamic Multi-Factor Global Index was launched on 3/31/2017. Data prior to launch is simulated. Please see important disclosure information at end.

Factor Allocation Over Time – Global

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Po

rtfo

lio

Co

mp

osi

tio

nRAFI Dynamic Multi-Factor Global Index

(4/2007 - 3/2017)

Value Low Volatility Quality Momentum Size

35

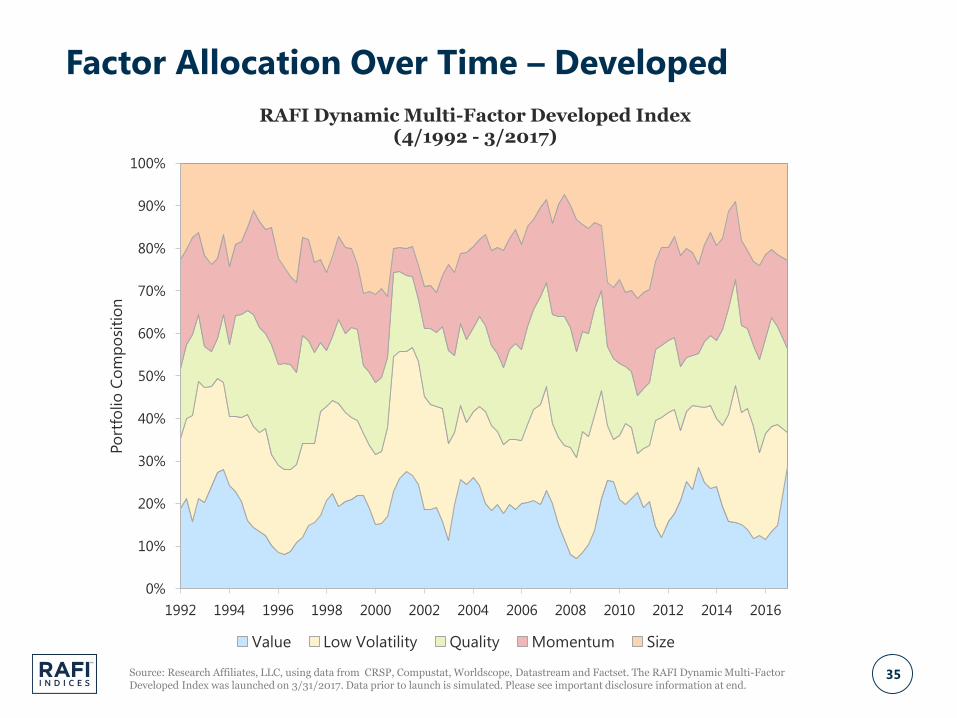

Factor Allocation Over Time – Developed

Source: Research Affiliates, LLC, using data from CRSP, Compustat, Worldscope, Datastream and Factset. The RAFI Dynamic Multi-Factor Developed Index was launched on 3/31/2017. Data prior to launch is simulated. Please see important disclosure information at end.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Po

rtfo

lio

Co

mp

osi

tio

nRAFI Dynamic Multi-Factor Developed Index

(4/1992 - 3/2017)

Value Low Volatility Quality Momentum Size

36

Factor Allocation Over Time – Developed ex US

Source: Research Affiliates, LLC, using data from CRSP, Compustat, Worldscope, Datastream and Factset. The RAFI Dynamic Multi-Factor Developed ex US Index was launched on 1/31/2017. Data prior to launch is simulated. Please see important disclosure information at end.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Po

rtfo

lio

Co

mp

osi

tio

nRAFI Dynamic Multi-Factor Developed ex US Index

(6/1992 - 3/2017)

Value Low Volatility Quality Momentum Size

37Source: Research Affiliates, LLC, using data from CRSP, Compustat, Worldscope, Datastream and Factset. The RAFI Dynamic Multi-Factor Emerging Markets Index was launched on 1/31/2017. Data prior to launch is simulated. Please see important disclosure information at end.

Factor Allocation Over Time – Emerging Markets

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Po

rtfo

lio

Co

mp

osi

tio

nRAFI Dynamic Multi-Factor Emerging Markets Index

(6/2007 - 3/2017)

Value Low Volatility Quality Momentum

38

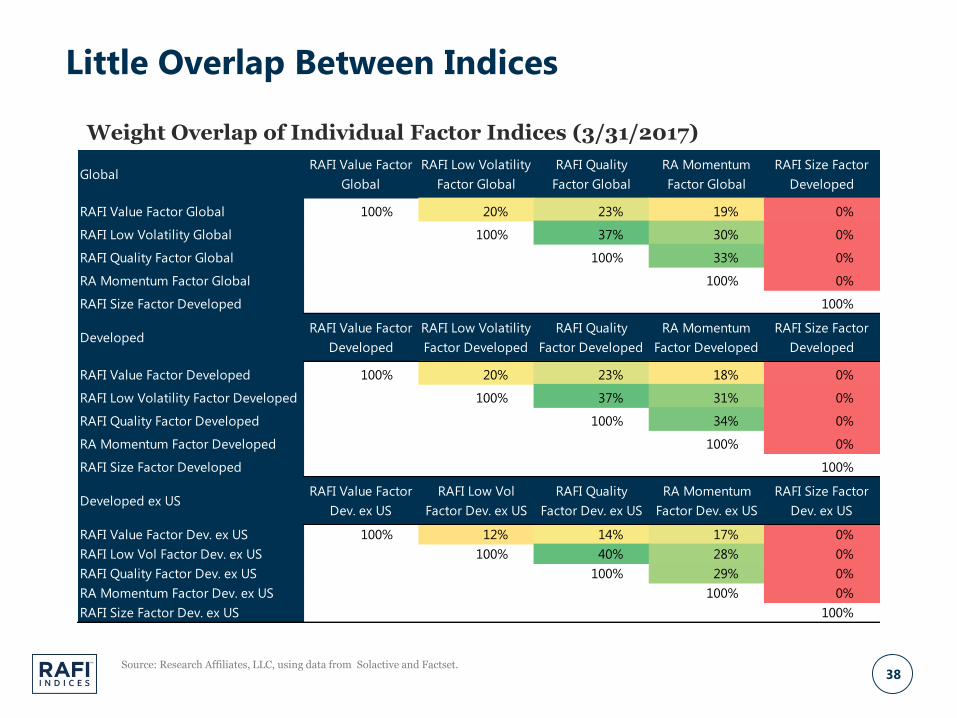

GlobalRAFI Value Factor

Global

RAFI Low Volatility

Factor Global

RAFI Quality

Factor Global

RA Momentum

Factor Global

RAFI Size Factor

Developed

RAFI Value Factor Global 100% 20% 23% 19% 0%

RAFI Low Volatility Global 100% 37% 30% 0%

RAFI Quality Factor Global 100% 33% 0%

RA Momentum Factor Global 100% 0%

RAFI Size Factor Developed 100%

DevelopedRAFI Value Factor

Developed

RAFI Low Volatility

Factor Developed

RAFI Quality

Factor Developed

RA Momentum

Factor Developed

RAFI Size Factor

Developed

RAFI Value Factor Developed 100% 20% 23% 18% 0%

RAFI Low Volatility Factor Developed 100% 37% 31% 0%

RAFI Quality Factor Developed 100% 34% 0%

RA Momentum Factor Developed 100% 0%

RAFI Size Factor Developed 100%

Developed ex USRAFI Value Factor

Dev. ex US

RAFI Low Vol

Factor Dev. ex US

RAFI Quality

Factor Dev. ex US

RA Momentum

Factor Dev. ex US

RAFI Size Factor

Dev. ex US

RAFI Value Factor Dev. ex US 100% 12% 14% 17% 0%

RAFI Low Vol Factor Dev. ex US 100% 40% 28% 0%

RAFI Quality Factor Dev. ex US 100% 29% 0%

RA Momentum Factor Dev. ex US 100% 0%

RAFI Size Factor Dev. ex US 100%

Source: Research Affiliates, LLC, using data from Solactive and Factset.

Weight Overlap of Individual Factor Indices (3/31/2017)

Little Overlap Between Indices

39

United StatesRAFI Value Factor

US

RAFI Low Volatility

Factor US

RAFI Quality

Factor US

RA Momentum

Factor US

RAFI Size Factor

US

RAFI Value Factor US 100% 17% 13% 13% 0%

RAFI Low Volatility Factor US 100% 43% 33% 0%

RAFI Quality Factor US 100% 31% 0%

RA Momentum Factor US 100% 0%

RAFI Size Factor US 100%

Emerging MarketsRAFI Value Factor

EM

RAFI Low Volatility

Factor EM

RAFI Quality

Factor EM

RA Momentum

Factor EM

RAFI Value Factor EM 100% 18% 21% 13%

RAFI Low Volatility Factor EM 100% 29% 15%

RAFI Quality Factor EM 100% 28%

RA Momentum Factor EM 100%

Source: Research Affiliates, LLC, using data from Solactive and Factset.

Weight Overlap of Individual Factor Indices (3/31/2017)

Little Overlap Between Indices (cont.)

40

Global (6/2007–3/2017)RAFI Value Factor

Global

RAFI Low Volatility

Factor Global

RAFI Quality Factor

Global

RA Momentum

Factor Global

RAFI Size Factor

Developed

RAFI Value Factor Global 1.00 -0.28 -0.06 -0.27 0.46

RAFI Low Volatility Factor Global 1.00 0.54 0.31 -0.23

RAFI Quality Factor Global 1.00 0.56 -0.10

RA Momentum Factor Global 1.00 0.08

RAFI Size Factor Developed 1.00

Developed (6/1992–3/2017)RAFI Value Factor

Developed

RAFI Low Volatility

Factor Developed

RAFI Quality Factor

Developed

RA Momentum

Factor Developed

RAFI Size Factor

Developed

RAFI Value Factor Developed 1.00 0.49 0.53 0.00 0.47

RAFI Low Volatility Factor Developed 1.00 0.76 0.25 0.22

RAFI Quality Factor Developed 1.00 0.28 0.21

RA Momentum Factor Developed 1.00 0.33

RAFI Size Factor Developed 1.00

Developed ex US (6/1992–3/2017)RAFI Value Factor

Dev ex US

RAFI Low Vol

Factor Dev ex US

RAFI Quality Factor

Dev ex US

RA Momentum

Factor Dev ex US

RAFI Size Factor

Dev ex US

RAFI Value Factor Dev ex-US 1.00 0.38 0.49 0.15 0.51

RAFI Low Volatility Factor Dev ex-US 1.00 0.74 0.41 0.37

RAFI Quality Factor Dev ex-US 1.00 0.54 0.39

RA Momentum Factor Dev ex-US 1.00 0.28

RAFI Size Factor Dev ex-US 1.00

Source: Research Affiliates, LLC, using data from Factset, Solactive, Worldscope and Datastream. Correlation of excess returns is relative to the following benchmarks: MSCI All Country World for Global, MSCI World for Developed, MSCI World ex-US for Developed ex-US. The launch date for all Developed ex-US indices is 1/31/2017. The launch date for all Global and Developed Indices is 3/31/2017. Performance prior to launch is simulated. Please see important disclosure information at end.

Correlation of Excess Returns

Low Correlation of Excess Returns

41

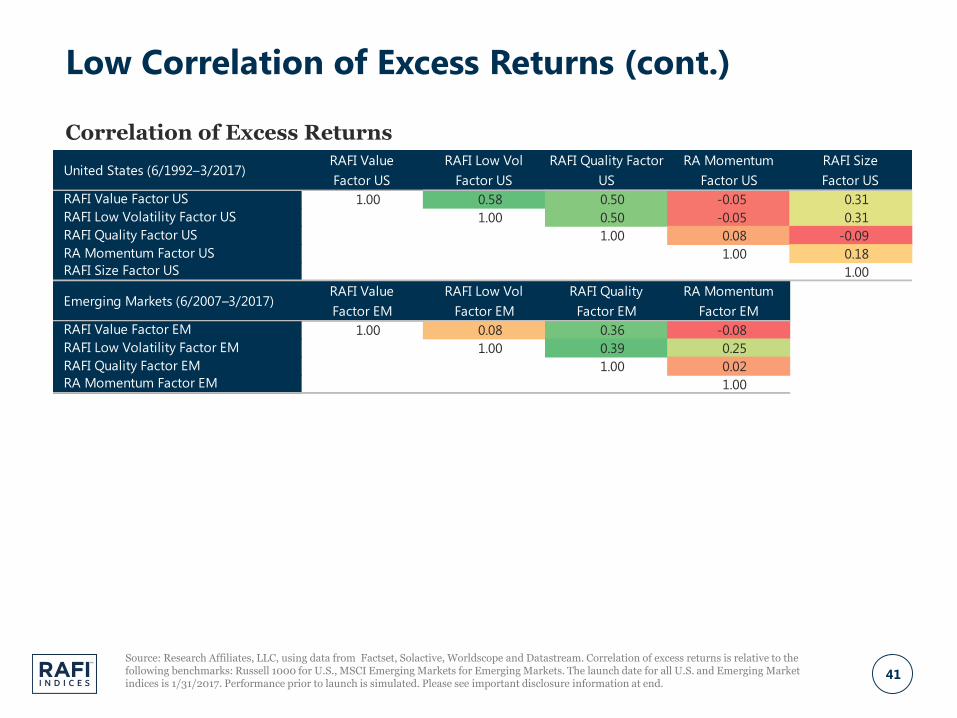

United States (6/1992–3/2017)RAFI Value

Factor US

RAFI Low Vol

Factor US

RAFI Quality Factor

US

RA Momentum

Factor US

RAFI Size

Factor US

RAFI Value Factor US 1.00 0.58 0.50 -0.05 0.31

RAFI Low Volatility Factor US 1.00 0.50 -0.05 0.31

RAFI Quality Factor US 1.00 0.08 -0.09

RA Momentum Factor US 1.00 0.18

RAFI Size Factor US 1.00

Emerging Markets (6/2007–3/2017)RAFI Value

Factor EM

RAFI Low Vol

Factor EM

RAFI Quality

Factor EM

RA Momentum

Factor EM

RAFI Value Factor EM 1.00 0.08 0.36 -0.08

RAFI Low Volatility Factor EM 1.00 0.39 0.25

RAFI Quality Factor EM 1.00 0.02

RA Momentum Factor EM 1.00

Source: Research Affiliates, LLC, using data from Factset, Solactive, Worldscope and Datastream. Correlation of excess returns is relative to the following benchmarks: Russell 1000 for U.S., MSCI Emerging Markets for Emerging Markets. The launch date for all U.S. and Emerging Market indices is 1/31/2017. Performance prior to launch is simulated. Please see important disclosure information at end.

Correlation of Excess Returns

Low Correlation of Excess Returns (cont.)

42

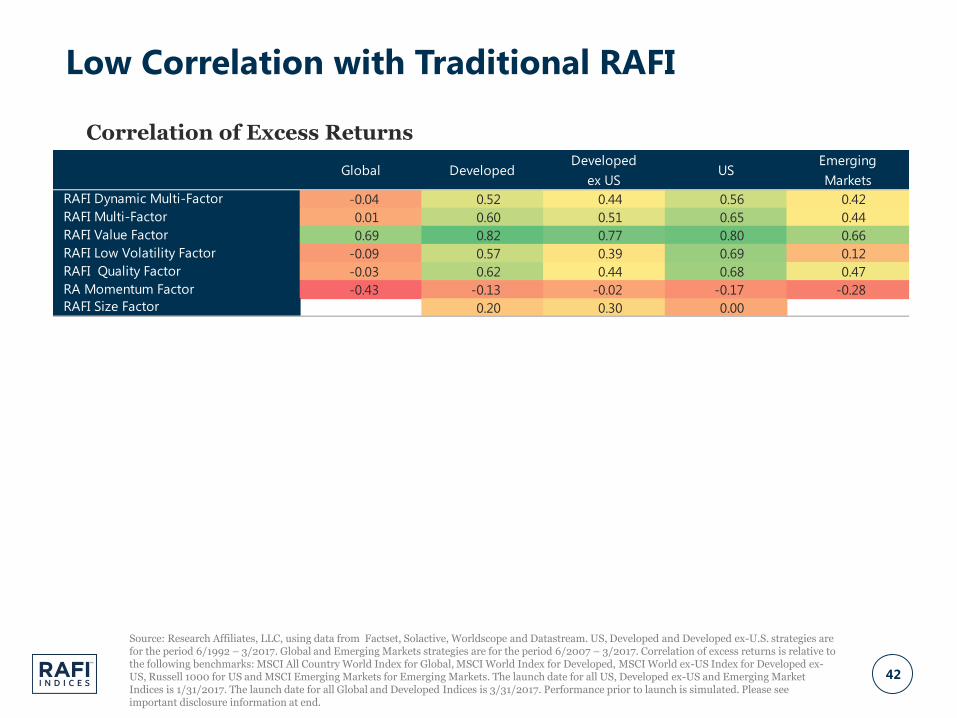

Global DevelopedDeveloped

ex USUS

Emerging

Markets

RAFI Dynamic Multi-Factor -0.04 0.52 0.44 0.56 0.42

RAFI Multi-Factor 0.01 0.60 0.51 0.65 0.44

RAFI Value Factor 0.69 0.82 0.77 0.80 0.66

RAFI Low Volatility Factor -0.09 0.57 0.39 0.69 0.12

RAFI Quality Factor -0.03 0.62 0.44 0.68 0.47

RA Momentum Factor -0.43 -0.13 -0.02 -0.17 -0.28

RAFI Size Factor 0.20 0.30 0.00

Source: Research Affiliates, LLC, using data from Factset, Solactive, Worldscope and Datastream. US, Developed and Developed ex-U.S. strategies are for the period 6/1992 – 3/2017. Global and Emerging Markets strategies are for the period 6/2007 – 3/2017. Correlation of excess returns is relative to the following benchmarks: MSCI All Country World Index for Global, MSCI World Index for Developed, MSCI World ex-US Index for Developed ex-US, Russell 1000 for US and MSCI Emerging Markets for Emerging Markets. The launch date for all US, Developed ex-US and Emerging Market Indices is 1/31/2017. The launch date for all Global and Developed Indices is 3/31/2017. Performance prior to launch is simulated. Please see important disclosure information at end.

Correlation of Excess Returns

Low Correlation with Traditional RAFI

43

www.rafi.com

Thank You

44

By accepting this document you agree to keep its contents confidential. You also agree not to

disclose the contents of this document to third parties (including potential co-investors) without

the prior written permission of RAFI Indices, LLC (including its related entities).

The material contained in this document is for information purposes only. This material is not

intended as an offer or solicitation for the purchase or sale of any security or financial instrument,

nor is it advice or a recommendation to enter into any transaction. Any offer to sell or a

solicitation of an offer to buy or sell shall be made solely by the legally permitted entity

registered or licensed with the applicable regulator(s) and only to qualified investors through a

regulatory registration statement or subject to an applicable exemption and disclosure document

such as a private placement memorandum for pooled investment vehicles, or investment

management agreement for separately managed accounts. The information contained herein

should not be construed as financial or investment advice on any subject matter. RAFI Indices,

LLC and its related entities do not warrant the accuracy of the information provided herein, either

expressed or implied, for any particular purpose.

The index data published herein may be simulated and in such instances, no allowance has been

made for trading costs, management fees, or other costs, are not indicative of any specific

investment, are unmanaged and cannot be invested in directly. Past performance, including

simulated performance, is no guarantee of future performance and actual index results may

differ. Any information and data pertaining to an index contained in this document relate only to

the index itself and not to any asset management product based on the index.

Investors should be aware of the risks associated with data sources and quantitative processes

used in the creation of the index related data. Errors may exist in data acquired from third party

vendors, the construction of indices, and in coding related to the index construction process.

While RAFI Indices, LLC and its related entities take steps to identify data and process errors so as

to minimize the potential impact of such errors on index performance, they cannot guarantee

that such errors will not occur.

Frank Russell Company is the source and owner of the Russell index data contained or reflected

in this material and copyrights related thereto. Frank Russell Company and Research Affiliates,

LLC have entered into a strategic alliance with respect to the Russell RAFI Indexes. The Russell

RAFI Indexes are calculated by Russell in conjunction with Research Affiliates LLC. All intellectual

property rights in the Russell RAFI Indexes (the “Index”) vest in Russell and RA. Neither Russell

nor RA or their licensors accept any liability for any errors or omissions in the Index and / or

Index ratings or underlying data. No further distribution of Russell Data is permitted without

Russell’s express written consent. Russell® is a trademark of Frank Russell Company. Research

Affiliates, LLC is the owner of the trademarks, service marks, patents and copyrights related to the

Fundamental Index and the Fundamental Index methodology. The presentation may contain

confidential information and unauthorized use, disclosure, copying, dissemination, or

redistribution is strictly prohibited. This is a presentation of Research Affiliates, LLC. Frank Russell

Company is not responsible for the formatting or configuration of this material or for any

inaccuracy in Research Affiliates’ presentation thereof.

Copyright MSCI. All Rights Reserved. Without prior written permission of MSCI, this information

and any other MSCI intellectual property may only be used for your internal use, may not be

reproduced or redisseminated in any form and may not be used to create any financial

instruments or products or any indices. This information is provided on an “as is” basis, and the

user of this information assumes the entire risk of any use made of this information. Neither

MSCI nor any third party involved in or related to the computing or compiling of the data makes

any express or implied warranties, representations or guarantees concerning the MSCI index-

related data, and in no event will MSCI or any third party have any liability for any direct, indirect,

special, punitive, consequential or any other damages (including lost profits) relating to any use

of this information.

The trademarks Fundamental Index™, RAFI™, Research Affiliates Equity™, RAE™, and the Research

Affiliates™ trademark and corporate name and all related logos are the exclusive intellectual

property of Research Affiliates, LLC and in some cases are registered trademarks in the U.S. and

other countries. The RAFI trademark is used under license by RAFI Indices, LLC. The RAFI Indices,

LLC corporate name and all related logos are the exclusive intellectual property of RAFI Indices,

LLC.

Various features of the Fundamental Index™ methodology, including an accounting data-based

non-capitalization data processing system and method for creating and weighting an index of

securities, are protected by various patents, and patent-pending intellectual property of Research

Affiliates, LLC. (See all applicable US Patents, Patent Publications, Patent Pending intellectual

property and protected trademarks located at https://www.researchaffiliates.com/en_us/about-

us/legal.html#d, which are fully incorporated herein.) Any use of these trademarks, logos,

patented or patent pending methodologies without the prior written permission of Research

Affiliates, LLC, is expressly prohibited. Research Affiliates, LLC, reserves the right to take any and

all necessary action to preserve all of its rights, title, and interest in and to these marks, patents or

pending patents.

RAFI Indices, LLC is a wholly owned subsidiary of Research Affiliates Global Holdings, LLC and

does not offer or provide investment advice or offer or sell any securities, commodities or

derivative instruments or products. Any such business may only be conducted through registered

or licensed entities and individuals permitted to do so within the respective jurisdiction and only

in conjunction with the legally required disclosure documents and subject to the all legally

required regulatory filings.

RAFI Indices, LLC, its affiliates, agents, and each of their respective officers, directors, employees,

agents, representatives and licensors (collectively “RI”) shall not be liable to any third party for

any loss or damage, direct, indirect or consequential, arising from or related to (i) any inaccuracy

or incompleteness in, errors or omissions in the enclosed information (the “Presentation

Material”) or (ii) any decision made or action taken by any third party in reliance upon the

Presentation Material. RI does not make any warranties, express or implied, to anyone regarding

the Presentation Material, including, without limitation, any warranties with respect to the

timeliness, sequence, accuracy, completeness, currentness, merchantability, quality or fitness for a

particular purpose or any warranties as to the results to be obtained by any third-party in

connection with the use of the Presentation Material. RI shall not be liable to anyone for loss of

business revenues, lost profits or any indirect, consequential, special or similar damages

whatsoever, whether in contract, tort or otherwise, even if advised of the possibility of such

damages.

© 2017 RAFI Indices, LLC. All rights reserved. Duplication or dissemination prohibited without

prior written permission.

Important Information

![Duo Multi-Factor Authentication (MFA) · Multi-Factor Authentication (MFA) Documentation: FAQs [1] Duo Multi-Factor Authentication (MFA): Frequently Asked Questions (FAQs) What is](https://img.pdfslide.net/doc/110x75/5b65cd517f8b9a6e1f8c5f4e/duo-multi-factor-authentication-mfa-multi-factor-authentication-mfa-documentation.jpg)