Embed Size (px)

Citation preview

Rajasthan Identity Card & Government Benefits Delivery Scheme

(Bhamasha)

jktLFkku igpku i= rFkk jktdh; lsokvksa ds ykHk ds izHkkoh forj.k dh ;kstuk

¼Hkkek’kkg½

Electronic Benefit Transfer Financial Inclusion Women Empowerment State Resident Data Hub Family Identification Resident Identity Card

Scheme Components

Who was Bhamasha ?

The word Bhamasha has been taken from the remarkable character in the Indian History who was an intelligent man, a philanthropist, a warrior and most important a Jain Shrawak.

He belonged to Oswal Vaishya community. He was advisor to Maharana Pratap. Bhamasha fought massive wars against Moguls, looted their treasures, donated all his wealth for Mewar and consistently helped Maharana Pratap as his advisor.

He was an example of the spirit of love for his motherland.

(1547 - 1600 )

What is Financial Inclusion ?

Financial inclusion or inclusive financing is thedelivery of financial services at affordable costs tosections of disadvantaged and low-income segmentsof society.

Financial Inclusion, broadly defined, refers touniversal access to a wide range of financial servicesat a reasonable cost.

The availability of banking and payment services tothe entire population without discrimination is theprime objective of financial inclusion public policy.

Financial inclusion broadens the resource base of thefinancial system by developing a culture of savingsamong large segment of rural population and plays itsown role in the process of economic development.Further, by bringing low income groups within theperimeter of formal banking sector; financial inclusionprotects their financial wealth and other resourcesin exigent circumstances.Financial inclusion also mitigates the exploitation ofvulnerable sections by the usurious money lendersby facilitating easy access to formal credit.

Why Financial Inclusion ?

RBI on Financial Inclusion

The term "financial inclusion" has gained importance since the early2000s, a result of findings about financial exclusion and its directcorrelation to poverty.

In India, RBI has initiated several measures to achieve greaterfinancial inclusion, such as facilitating no-frills accounts and Generalcredit cards for small deposits and credit. Some of these steps are:

Opening of no-frills accounts (a/c with nil or min. Balance) Relaxation on know-your-customer (KYC) norms Engaging Business Correspondents (BCs) (Jan 2006 and Sept.2010 to

address last mile problem) Use of Technology (use ICT to provide services through BC model where account

can be operated using biometrics)

Adoption of EBT(transfer social benefits electronically into the bank account of beneficiary)

Simplified branch Authorization (general approval to open braches in tier III to tier VI cities)

Opening of branches in unbanked rural centres (25% of branches to be opened in the year to be allocated to unbanked rural centres)

Indicators on Financial Inclusion

As per census 2011, only 58.7% of households are availing banking servicesin the country. However, as compared with previous census 2001, availing ofbanking services increased significantly largely on account of increase inbanking services in rural areas.

Extent of Financial Inclusion - Banking Service

The CRISIL Inclusix indicate that there is an overall improvement in the financial inclusion in India :

Extent of Financial Inclusion - CRISIL

The Reserve Bank of India (RBI) set up the Khan Commission in 2004 to look into financial inclusion and the recommendations of the commission were incorporated into the mid-term review of the policy (2005–06).

In India, financial inclusion first featured in 2005, when it was introduced by K.C. Chakraborthy, the chairman of Indian Bank. Mangalam became the first village in India where all households were provided banking facilities. Norms were relaxed for people intending to open accounts with annual deposits of less than Rs. 50,000.

In January 2006, the Reserve Bank permitted commercial banks to make use of the services of non-governmental organizations (NGOs/SHGs), micro-finance institutions, and other civil society organizations as intermediaries for providing financial and banking services. These intermediaries could be used as business facilitators or business correspondents by commercial banks.

RBI on Financial Inclusion

In Sept.2010, RBI - as part of its Financial Inclusion mandate, announced to permit banks to engage CSC Operators/VLEs as Business Correspondents

Sustainability issues with Bank’s BC model led to using CSCnetwork across the country to act as BCs.

The Indian government and the Reserve Bank of India (RBI)have been very proactive in promoting ‘Financial Inclusion’ andamong various initiatives, the ‘Business Correspondent Model’is being seen as a new and innovative way to serve theunbanked, by allowing banks to reach the underserved throughexternal agents

RBI on Financial Inclusion

The Scheme

13

Vision..

To expand existing electronic infrastructure

backbone for providing cash as well as non-cash

benefits to all ordinary residents of the state at

their door steps using biometrically secured

process and providing multi-purpose identity card

and also reforming governance & delivery

systems in the process.

Objective

To reform and Institutionalise direct benefit delivery mechanism of government programmes To transfer all cash benefits directly to the bank account of the beneficiaries

of the state. To provide all non-cash benefits directly into the hands of the beneficiaries

of the state using single data set and aadhaar enabled biometricauthentication.

To issue Rajasthan Identity and Multi-purpose card to all ordinaryresident of the State for facilitating their identification & access toservices.

To bring about complete financial inclusion in the State by makingbanking service available near the doorsteps of the residents of thestate through banks / post office / business correspondents (CSCs etc.)empowering especially women.

To provide effective check on the leakage of direct benefit transfer tobeneficiaries;

To financially empower women;

Aadhaar Identification Data (KYR) – Includes - Name, Date of birth, Gender, Address,

and biometric imprints. Proof of Identity. Proof of Address.

Basic Demographic Data (KYR+) – Will include - marital status, income, religion,

category, occupation, educational qualification Family Identity Socio-economic Status

Scheme Specific Data – Scheme specific parameters To be maintained by Departments concerned

Database of Ordinary Resident

Name

Address

Gender

Date of birth1 person1 number

4 demographics + 3 biometrics = 1 unique Aadhaar number

Photo

Both

iris

10 finger-

prints

Aadhaar Identification Data(KYR)

Basic Demographic Data (KYR+)

The key usage of State resident KYR data is for : ‘Seeding’ of departmental databases with

Aadhaar number ‘Cleaning’ of departmental databases (Format

standardisation, duplicate removal, incorrect information etc.)

Legitimate Resident data accessible to States’ applications

Ability to better manage the fund disbursement and social welfare / financial inclusion schemes

State Resident Data Hub

UID CIDR

KYR and KYR+ dataat State Data Center

Dept. of Food & Civil Supplies

Election Department

Rural Development Department

Department of Social Welfare

CIDR Verification of KYR Data

State Resident Data Hub

Scheme Specific Data

Aadhaar Data(KYR) andBasic Demographic Data under the bhamasha scheme (KYR+)

State Resident Data Hub

Any change to KYR data needs to be first done at CIDR. SRDH data should be maintained up-to-date with CIDR so that the services of SRDH are reliable for the State Departments using the data.

To collect and create single data set for all ordinaryresidents of the State in 3 layers – Aadhaar data Basic Demographic data including grouping of

individuals into Family Scheme Specific Data (to be maintained by department)

Organizing individual data in family data

Every ordinary resident who is 21 years and above candeclare himself/herself as head of the family. It will beencouraged for families to declare women heads offamily;

20

Collection of Individual & Family Data

Empowerment/Benefits to Families/Individuals

Every ordinary resident will be able to have anAadhaar number and household/family identificationnumber;

Will be able to access & receive benefits under all thebeneficiary schemes through a single BhamashahPlatform. Family Benefits would be deposited in bankaccount of women;

Every ordinary resident will be able to have amultipurpose identity card and Bank account linkedwith core banking facility at their doorsteps;

22

On completion of enrolment process, everyIndividual shall be issued a Multi-purpose cumIdentity card

Following information shall be on the card alongwithhis photo :

Aadhaar Number, Household number, Name ofcardholder, Date of issue of Card, Validity of Card,Bank Account detail, Category, Gender, Date ofBirth, Religion and Address.

Multi-Purpose Card

Statistics

S.No.

Particulars Population as per 2011

census

Projected population for 2014

1. Population – Male 3,55,50,997 3,74,72,3652. Population - Female 3,29,97,440 3,47,80,800

Total 6,85,48,437 7,22,53,165

State’s Current Population

S.No.

Particulars Population as per 2011

census

Projected population for 2014

1. Population – Rural 5,15,00,352 5,42,83,7092. Population - Urban 1,70,48,085 1,79,69,456

Total 6,85,48,437 7,22,53,165

Students (As per 2011 census)

S.No. Particulars Population1. Population – Child ( 0 - 6 yrs) 1,06,49,504

S.No. Particulars Population(in Lacs)

1. Primary School Students 91.622. Upper Primary School Students 37.393. Secondary/Sr. Secondary Students 56.574. Graduation 5.46

Total 191.04

Beneficiaries under various Programme

S.No.

Particulars Population(in Lacs)

1. Ration Cards 167.78 2. Vehicle Registration 1003. Domestic Electric Connection 604. NAREGA Job Cards 99.47

5. Indira Awas Yojana Houses Constructed (2012-13)

0.83

6. Jan Shree Bima Yojana 26.227. Indira Gandhi Rastriya Widow Pension Yojana 1.38. National Health Insurance Scheme 7.33 9. Rajasthan Social Security Scheme beneficiary

(State and Centre sponsored schemes)56.87

Rajasthan Social Security Scheme Beneficiary

S.No.

Particulars Population(in Lacs)

State Sponsored :1. State Widow Pension Scheme 6,43,4312. State Disability Pension Scheme 3,33,2663. State Old Age Pension Scheme 37,61,645Centre Sponsored :4. Indira Gandhi Old Age Pension Scheme 8,07,9855. Indira Gandhi National Welfare Pension

Scheme1,17,945

6. Indira Gandhi National Disability Pension Scheme

22,852

Total 56,87,124

Scholarships

S.No. Particulars Population(in Lacs)

1. ScholarshipsSC Post Matric 2.41ST Post Matric 2.50OBC Post Matric 1.40Minority Post Matric 0.24Total 6.55

Implementation Strategy

Implementation and Management of Scheme

District Collector will head implementation in thedistrict. He would act as District Bhamashah Manager(DBM) for implementation of the Bhamashah schemein the district.

District Level Statistical Officer (Deputy Director /Assistant Director) would be District BhamashahOfficer and shall be responsible for effectiveimplementation of the scheme in the district.

Block Level Statistical Officer would be BlockBhamashah Officer and would ensure effectiveimplementation of the scheme in its block.

Implementation and Management of Scheme

District level and Block level BhamashahOfficers shall work under the aegis of PlanningDepartment and shall carry out following works: Management of Enrolment of residents and

continuous updation of Data. Ensure quality of enrolment under the scheme Co-ordinate between various stakeholders of the

scheme viz. departmental offices, banks, bankingcorrespondants, emitra/CSC, enrolment agenciesetc.

Resolve problems encountered in the scheme withintheir jurisdiction

RajComp Info Service Ltd. shall be State LevelScheme Implementation Agency for the BhamashahScheme. Scope of work of RISL would be as follows :

To select Enrolment Agencies; To manage and store central database of ordinary

residents of the state and to ensure its security inthe State Data Center;

Management of Bhamashah Application; Preparation and distribution of Resident Cards.

State Level Scheme Implementation Agency

To develop application software for use by enrolment agencies forEnrolment of individuals

To prepare Aadhaar database and store in SDC To link various departmental data with Aadhaar data To collect basic demographic data about ordinary residents

through enrolment agencies To facilitate two level verification of data collected during enrolment To regularly update the integrated database To provide technical assistance to all stakeholders for data

management and storage To provide training to various stakeholders under the scheme To provide Multi-purpose cards to all individuals after completion of

enrolment process

SIA – Data Management & Storage

To develop algorithm for linking Aadhaar data withother departmental data

To develop algorithm for linking Aadhaar data withother departmental Scheme Specific Data

To capture and manage all transactions related withdisbursement of benefits to individuals underBhamashah Scheme

To link individual Aadhaar and bank detail withPayment Gateway developed by National PaymentAuthority so that the benefits could be transferred tothe right beneficiary.

SIA-Management of Bhamashah Scheme Platform

State level Scheme Implementing agencyshall select field level enrolment agencies forthe work of enrolment of ordinary residents atfield level. For ensuring enrolment : Camps would be organised. Permanent enrolment stations shall be opened at

Bharat Nirman Seva Kendra for a period of oneyear.

E-Mitra centers (C.S.C.s) would be used forcontinuous updation.

Field Agency for Enrolment (EA)

Resident with Aadhaar Number : Resident with aadhaar identification number shall

be provided with enrolment form with pre-populated data already available with State.

The resident would be required to fill the emptyfields in the form.

The details provided by resident would be fed inthe software.

The form shall also contain detail of groupingindividuals into families.

Enrolment Process

Resident without Aadhaar Number : If individual does not have aadhaar number,

facility for aadhaar registration would be availablein the enrolment camps.

Photographs & biometric detail would be capturedfor such individuals.

Provision for correction of data would also beavailable in the enrolment camps.

Enrolment Process

Enrolment Activities

Ongoing Activities

Verification procedures

Demographic & biometric

data capture

Data transfer to

CIDR

CIDR

Rejections identified

Biometric De-duplication

UID Assignment

Data Updation

Biometric Authentication

Letter Printing & Delivery

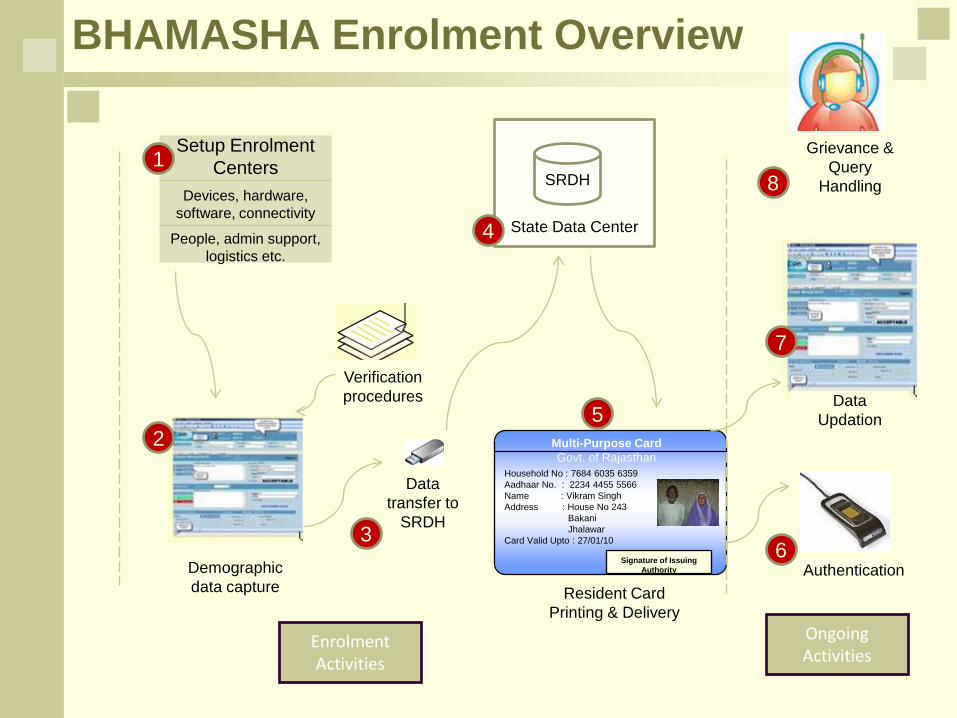

Setup Enrolment Centers

Devices, hardware, software, connectivity

People, admin support, logistics etc.

1

2

3

4

5

6

7

8

AADHAAR Enrolment Overview

Grievance & Query

Handling

Multi-Purpose Card Govt. of Rajasthan

Enrolment Activities

Ongoing Activities

Verification procedures

Demographic data capture

Data transfer to

SRDH

State Data Center

SRDH

Data Updation

AuthenticationResident Card

Printing & Delivery

Setup Enrolment Centers

Devices, hardware, software, connectivity

People, admin support, logistics etc.

1

2

3

4

5

6

7

8

BHAMASHA Enrolment Overview

Grievance & Query

Handling

Household No : 7684 6035 6359Aadhaar No. : 2234 4455 5566Name : Vikram SinghAddress : House No 243

BakaniJhalawar

Card Valid Upto : 27/01/10

Signature of Issuing Authority

Proposed Rate Payable to Enrolment Agency

S.No Particulars Proposed Rate

For ordinary residents whose Aadhaar Enrolment has not been done :

1. Rate payable for Aadhaar Enrolment (Rs.28/-)To be Finalized2. Rate payable for collection of basic demographic

data about ordinary residents (To be finalized)

For ordinary residents whose Aadhaar Enrolment has been done :1. Rate payable for collection of basic demographic

data about ordinary residentsTo be Finalized

S.No

Particulars Expected Number (in Lacs)

Rate(in Rs.)

Amount(Rs. in Lacs)

Non-recurring Cost :1. Aadhaar Enrolment 150 28/- 4,2002. Bhamashah Enrolment 600 15/- 9,0003. Cost of Application Software NA NA 2504. Digital Signatures 1.0 600/- 6005. State Resident Data Hub NA NA 10006. Resident Identity Card including

distribution600 25/- 15000

7. Logistics/Training/I.E.C. NA NA 5508. Stationary NA NA 3309. Contingency NA NA 270

Total 31,200

Estimated Cost of Implementation of Scheme

Estimated Cost of Implementation of Scheme

S.No

Particulars Expected Number (in Lacs)

Rate(in Rs.)

Amount(Rs. in Lacs)

Recurring Cost (required for three years) :1. Cost of running Point of Service

(For 10000 kiosks @ Rs. 3000/- per kiosk per month)

0.10 3000/-Per month

per POS

10800

2. Reissue of Identity Card(Population - 722 – 685 = 37)

50 25/- 1250

3. Misc. Expenditure NA 10,00,000/- 330Total 12380Grand Total 43580

First Verification : By Gram Sevaks/ Patwari / authorised officer of

local bodies on the basis of documents providedby the ordinary residents.

Second Verification : By Tehsildar /Nayab Tehsildar /Block

Development Officer after Public Disclosure as is done as in case of Jamabandhi Verification.

Verification of Enrolled Data

Updation of Enrolment Details

Updation would be required to be undertaken onregular basis.

CSC/emitra kiosks would be authorized for updation ofdetail of the residents on chargeable basis.

Updation would be required under followingcircumstances:

- Addition on acquiring age of five years- Marriage of girls – change of family/address- New Family on attaining age of 21 years/Marriage - Deletion in case of death

Bank Account

All ordinary residents above age of 18 years would bemotivated to open a bank account linked with corebanking facility.

Residents who already have a bank account (withcore banking facility) would be able link the sameaccount under the scheme.

Residents below the age of 18 years may open theirown account or link their name to an account withsome major in the family/ head of family.

All banks/post offices would be free to provide servicein any of the districts of the state.

MOU/Agreement would be entered with a few bankswho would like to partner by increasing their B.C.network.

Minimum one point of service would be created by Government in each Gram Panchayat.

Both cash as well as non-cash services would be provided through these point of services. Enrolment of residents (Aadhaar as well as Bhamasha) G2C & B2C Service (being provided by CSC Kiosks) Banking Service (to be provided by BC) Grievance Filing (Rajasthan Sampark Center)

Available facilities would be leveraged for the purpose.

Point of Service

S.No.

Particulars Point of Service

Services being provided

1. Emitra Kiosks in Urban Area 1350 50 G2C services2. CSC Kiosks in Rural Area 5800 50 G2C services3. Bharat Nirman Seva Kendra

(IT Kendra)9177 Banking as well as

G2C services would be provided

4. Number of branches of banks in Rajasthan

4737 Banking services

5. Number of post offices in RajasthanRural

Urban9661666

Postal service &Banking service

6. Primary Agriculture Co-operative Societies (PACS)

5799 Banking service

7. Business Correspondants 2500 Banking services

Point of Service

DepositRemittance

Balance enquiryWithdrawal

Inclusive banking

Business Correspondents Micro-ATM Aadhaar authentication

Aadhaar enabled micropayments for inclusive banking

Aadhaar enabled micro-ATM – Sample Receipt

4. Authenticate

2. AADHAAR number, money transfer instruction, biometrics

Resident

BC with Micro-ATM

Ram’s bank account

BC’s bank account

Interoperable Switch

1. Withdrawal request

3. Forward to switch

6. Debit

7. Credit

8. Inform: Call / SMS

9. Cash

UIDAI

5. Authorize

• Any bank• Any channel • Any where

Inclusive Technology for Financial access

Aadhaar Data

Aadhaar ++ Data

Beneficiary Database of Govt.Department-1

Beneficiary Database of Corporation-n

Beneficiary Database of Govt.Department-2

Application Layer for Convergence of Aadhaar data with database of different departments

Adm..Deptt-1 on e-Grass Adm..Deptt-nAdm..Deptt-2 on e-

Grass

Application Layer to Capture transaction detail of benefit transferred to beneficiary

Bank

IFMS

Citizen

Bank

Citizen

Scheme Architecture

Roles of Stakeholders

Roles & Responsibilities of Stakeholder

Administrative Department

DOIT&C(State Registrar-UID)

District Collector

Govt. of India

Field Agency-DE&S

Government

RISL

DE&S

SIA

• LSPs• Bank• DE&S• Service Providers like ISP etc.

Policy Making Execution / implementation Framework

Kiosk 1

Kiosk 2

Kioskn

Technical - Application S/W- Infrastructure

Financial - Management- Cash handling- Audit

Logistical – Human ResourceCommunicationInfra Setup

(Civil, car, furniture etc.)Procurement / Selection

Management of- Human- Application- Documents- Money

Legal

HUBPoint of Service

Aggregation

Finalization of this Scheme regarding implementation of RBI guidelines in the State

Finalization of Commission to be paid to Banks for providing banking service in rural areas

Co-ordination with various stakeholders Arbitration for Dispute resolution between various

stakeholders Finalization of social schemes to be covered under

Bhamashah Scheme Providing place for establishment of Point of Service

in the premises of Bharat Nirman Seva Kendra

Government

District Level Statistical Officer (Deputy Director / Assistant Director) would be District Bhamashah Officer and shall be responsible for effective implementation of the scheme in the district.

Block Level Statistical Officer would be Block Bhamashah Officer and would ensure effective implementation of the scheme in its block

Overall Management of enrolment of residents and continuous updation of enrolment data

Ensure proper verification of data so as to ensure quality of enrolment data

Co-ordinate between various stakeholders of the scheme viz. departmental offices, banks, banking correspondents, emitra/CSC, enrolment agencies etc

Resolve problems encountered in the scheme within their jurisdiction

Department of Economics & Statistics

SIA - RISL

RajComp Info Service Ltd. shall be State LevelScheme Implementation Agency for the BhamashahScheme. Scope of work of RISL would be as follows :

To select Enrolment Agencies; To manage and store central database of ordinary

residents of the state and to ensure its security inthe State Data Center;

Management of Bhamashah Application; Preparation and distribution of Resident Cards.

Provide Technical Solution necessary for delivery of online, real time banking services, customer authentication and monitoring and management of POSs/Kiosks

Ensure linkage of CSCs with local bank branches Train the SCAs and VLEs to deliver banking and

financial services Finalization of commission payable to BC/BC agent Timely payment of commission to SCAs to ensure

sustainable service delivery via Point of service Provide technical support for successful delivery of

services. Coordinate in procuring microATM for VLEs

Bank

Depute permanent team at district enrolment stations i.e. at Bharat Nirman Seva Kendra.

Ensure enrolment of all ordinary residents of the State

Extend full support to District Administration during enrollment process

Extend following services to the residents – Aadhaar Enrolment , e-KYC, e-Aadhaar, Bhamashah

Enrolment and updation of data etc.

Enrolment Agencies

Ensure VLEs are ready to become the POS/Kiosks for delivery of banking services

Ensure availability of adequate infrastructure at CSCs including power backup and connectivity

Manage and monitor VLEs activity, providing first level support for timely service delivery

Mobilize and sensitize the local community to access banking and financial services via CSCs

Coordination with banks to ensure smooth implementation

Reconciliation of transactional detail Share commission paid by bank with VLEs

LSP/SCA as Business Correspondent

Adhere to the eligibility criteria and apply to become bank’s POS

Ensure availability of the required infrastructure at the CSC

Procure biometric device from banks in the form of softloan

Undergo training to deliver banking and financial services to citizens

Create and maintain independent settlement account to enable banking and financial transactions with bank

Ensure timely service delivery and adherence to the banking norms

VLEs / Kiosks as BC agent

Expectation

Expectation from Banks in the Scheme

Open more and more aadhaar enabled bank accounts so that the user is not required to visit branches for undertaking banking transaction.

Banks to enhance their reach by enrolling more and more Business Correspondants for providing services at door steps of citizen.

Enter MOU with CSC kiosks to act as Business Correspondants for providing banking services using microATMs.

Expectation from LSPs in the Scheme

LSPs to enter MOU with Banks to act as Business Correspondants for providing banking services using microATMs. This would provide additional source of revenue for CSC kiosk. Rate for per transaction to be fixed.

Business Correspondants of various banks to enter MOU with LSPs for opening of CSC kiosks. This would provide additional source of revenue for these business correspondants.

Expectation from EAs in the Scheme

Enrolment agencies to enroll more and more residents under the scheme both for Aadhaar registration and Basic demographic detail collection and

grouping into families.

To facilitate mobile camps as per requirement of District Administration.

Time Lines

S.No. Particulars Timeline1. Backend preparation of Two Layers of Data by

merging various departmental data viz. (AadhaarData & Basic Demographic Data alongwith family grouping )

June 2014

2. Bhamashah Application for field level enrolment

June 2014

3. Establishment of Point of Service July – Nov. 2014

4. Collection of field level data by Enrolment agencies alongwith aadhaar seeding of citizen data

July – Nov. 2014

5. Bhamashah Application for DBT June 20146. Go Live for Pilot Testing Dec. 2014

Thank You

S.No. Particulars Number of Branches1. State Bank of India 11512. Nationalized Bank 18863. Regional Rural Bank 11004. Private Sector Banks 5945. Foreign Banks 6

Total 4737Total Deposits with Banks 151983 crores

Number of Branches of Banks in Rajasthan

Back

![Fully, (Almost) Tightly Secure IBE and Dual System Groups · In an Identity-Based Encryption (IBE) scheme [27], encryption requires only the identity of the recipient (e.g. an email](https://img.pdfslide.net/doc/110x75/5f7cc08e86529b18fb013f73/fully-almost-tightly-secure-ibe-and-dual-system-groups-in-an-identity-based-encryption.jpg)

![Identity: n v identity (-ies p) [identity]](https://img.pdfslide.net/doc/110x75/61c6ea26100dbe3ec3259821/identity-n-v-identity-ies-p-identity.jpg)