-

7/29/2019 Randall Wray - Fiscal Cliff

1/39

Fiscal Cliffs, Debt Limits, and

Unsustainable Deficits: Can the US

ReallyRun Out of Dollars?

L . RANDALL WRAY, LEVY INST ITUTE & UMKC

W RAY R@ UM KC. E DU

W W W . L E V Y . O RG

WWW.ECONOMONITOR.COM/LRWRAY/

mailto:[email protected]://www.levy.org/http://www.levy.org/mailto:[email protected]

-

7/29/2019 Randall Wray - Fiscal Cliff

2/39

Fiscal Constraints

President Obama: Government is running out of money!

Economists: Unsustainable debt path!

70% of Americans say progress on Deficit needed this year

Chinese might stop lending to us!

Zimbabwe and Weimar hyperinflation!

Burden our grandkids!

Look at Euroland!

Sovereign debt crisis

Default risk

Bond vigilantes

-

7/29/2019 Randall Wray - Fiscal Cliff

3/39

But Is that True?

It aint what you dont know that gets youinto trouble. Its what

you know for sure

that just aint so. Mark Twain

First lets look at the data

-

7/29/2019 Randall Wray - Fiscal Cliff

4/39

Debt Limits, Fiscal Cliff,Sequestration

Debt limit imposed century ago

2011 Budget Control Act created FiscalCliff to hit Jan 1,

2013

postponed until March; compromise increasedpayroll tax

Sequestration: $1.2 trillion in cuts

$600B domestic (Air Traffic, Headstart)

$600B military

Reduce GDP 1% directly, and multiplier

-

7/29/2019 Randall Wray - Fiscal Cliff

5/39

Is there evidence of run-away,Weimar/Zimbabwe Deficit

Spending?

Is debt at historic high?

Is govt spending out of control?

Have we hocked ourselves to China?Does debt burden our

grandkids?

Will Entitlements bankrupt ourgrandkids?

-

7/29/2019 Randall Wray - Fiscal Cliff

6/39

-

7/29/2019 Randall Wray - Fiscal Cliff

7/39

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

2005-I

2005-II

2005-III

2005-IV

2006-I

2006-II

2006-III

2006-IV

2007-I

2007-II

2007-III

2007-IV

2008-I

2008-II

2008-III

2008-IV

2009-I

2009-II

2009-III

2009-IV

2010-I

2010-II

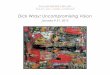

Federal Government Receipts and Expenditures(QoQ Change)

Source: Bureau of Economic Analysis and Authors'

Calculations

Tax Receipts

TransferPayments

ConsumptionExpenditures

-

7/29/2019 Randall Wray - Fiscal Cliff

8/39

-

7/29/2019 Randall Wray - Fiscal Cliff

9/39

-

7/29/2019 Randall Wray - Fiscal Cliff

10/39

-

7/29/2019 Randall Wray - Fiscal Cliff

11/39

Foregin Holdings of US Treasuries

(% of total he ld by Foreign Countries)

0

10

20

30

40

50

60

70

80

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Brazil

Taiw an

Hong Kong

Caribbean Banking

CentersOil Exporters

Germany

UK

China

Japan

Source: US Department of Treasury, November 2009 figures

Note: For some years the holdings of the selected countries have

been insignificant, so they are included in the category

-

7/29/2019 Randall Wray - Fiscal Cliff

12/39

Treasury Security Holdings (% of Total Oustanding)

0

10

20

30

40

50

60

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

Q3

2010

Q1

%

-2

-1

0

1

2

3

4

5

6

7Held by Rest of

the World

Foreign Official

Holdings

Foreign Private

Holdings

Financial SectorHoldings

Current Account

Balance (Sign

Reversed)*

Source: US Flow of Funds Accounts (f or Treasury Holdings) and

Bureau of Economic Analysis (for Current Account data)

*Current account data is as of the end of 2009; treasury

holdings data is as of 2009 Q3

-

7/29/2019 Randall Wray - Fiscal Cliff

13/39

But What About the Long Run?

Budget deficit already falling as taxrevenues recover

Some claim the problem is not with thecurrent situation, but

with entitlements

We face chronic Budget Deficits and risingDebt for decades

Infinite Horizon forecasts: Tens of trillions ofdollars of

unfunded commitments

-

7/29/2019 Randall Wray - Fiscal Cliff

14/39

Remember Clinton andGoldilocks?

1996: US Federal Govt begins to runsurpluses; continued for 2.5

years

Clinton projects surpluses for next 15 years All Govt debt will

be retired

But: Private debt explodes and then

recession restores deficits. Why: The Meaning of Zero:

0=Private Bal + Govt Bal + Foreign Bal

-

7/29/2019 Randall Wray - Fiscal Cliff

15/39

-

7/29/2019 Randall Wray - Fiscal Cliff

16/39

PRIVATE SECTOR BALANCE + GOVERNMENT BALANCE = CURRENT ACCOUNT

BALANCE

Accounting Identity of Financial Balances

INTERNAL FINANCIAL BALANCE EXTERNAL FINANCIAL BALANCE

THE CONCEPTUAL FRAMEWORK

-

7/29/2019 Randall Wray - Fiscal Cliff

17/39

-

7/29/2019 Randall Wray - Fiscal Cliff

18/39

Purported Unsustainability ofGovernment Deficits and Debt

Sustainability issues Relation between interest rates and

economic growth:

If r>g growth of debt

Growth of Debt Bond Vigilantes push up r

accelerating the rise of debt ratios

Excessive Deficit-to-GDP and Debt-to-GDP ratios:inflation and

ultimately insolvency

So: We must show:

a) why govt doesnt face insolvency, and

b) why deficits dont raise interest rates

-

7/29/2019 Randall Wray - Fiscal Cliff

19/39

St. Louis Fed

"As the sole manufacturer of dollars, whose debt is

denominated in dollars, the U.S. government can never

become insolvent, i.e., unable to pay its bills. In this

sense,

the government is not dependent on credit markets to remain

operational. Moreover, there will always be a market for

U.S.government debt at home because the U.S. government has

the only means of creating risk-free dollar-denominated

assets.

Government can NEVER run out of Dollars; It can NEVER be

forced to default; It can NEVER be forced to miss a payment;

It

is NEVER subject to whims ofbond vigilantes.

-

7/29/2019 Randall Wray - Fiscal Cliff

20/39

-

7/29/2019 Randall Wray - Fiscal Cliff

21/39

Myths, Superstition, Old-Time Religion

"I think there is an element of truth in the superst i t ion

that thebudget must be balanced at al l t imes. Once it is

debunked

[that] takes away one of the bulwarks that every society

must

have against expenditure out of control. There must be

discipline

in the allocation of resources or you will have anarchistic

chaos

and inefficiency. And one of the functions ofold fashion ed

relig ion was to scare people by somet imes what might be

regarded as my ths into behaving in a way that the long -run

civi l ized l i fe requires.(Samuelson)

Necessity of balancing the budget is a myth, a superstition,

theequivalent of that old-time religion.

So what is the truth? If economics is to rise above

superstition, weneed to know.

-

7/29/2019 Randall Wray - Fiscal Cliff

22/39

How Government Spends its OwnCurrency: Keystrokes

Spending credits

Government credits banks reserves; bank creditsaccount of

recipient

Taxes debits

Government debits banks reserves; bank debitsaccount of

taxpayer

Deficits net credits

Government net credits banks reserves; bank netcredits account

of recipient

-

7/29/2019 Randall Wray - Fiscal Cliff

23/39

Money as Scorekeeping

-

7/29/2019 Randall Wray - Fiscal Cliff

24/39

Bond Sales by Government: Why the Bond VigilantesCannot Dictate

Terms

Deficit spending net credits reserves Creates Net Financial

Wealth in nongovt sector

Excess Reserves bid overnight rate down

To Feds support rate (fed funds rate)

Bonds: Interest earning alternative (IRMA)

Part of Monetary Policy, whether new issues or openmarket

sales

Changes form of Net Financial Wealth (longer maturity)

(NB: Surpluses net debitsOMP or Redemptions)

-

7/29/2019 Randall Wray - Fiscal Cliff

25/39

Self-imposed constraints

Budgeting, debt limits

Operational constraints:

Treasury writes checks on accounts at CB

CB prohibited from buying Treasury Debt new issues

Use of Special Depositories

Use of Tax and Loan accts

-

7/29/2019 Randall Wray - Fiscal Cliff

26/39

Central Bank Policy

Consensus: central banks always operate on overnight

interest rate

Accommodates Demand for Reserves

Convertible vs. non-convertible currencies

Convertible: can lose control of interest rate (Greece)

Nonconvertible: controls overnight rate (Japan)

-

7/29/2019 Randall Wray - Fiscal Cliff

27/39

Sovereign Currency: Summary

Deficit spending creates private financial wealth Note that CB

operations do not; it buys government bonds or

lends against collateral (helicopter drop is fiscal policy)

CB Lends; Treasury Spends

Doesnt matter whether bonds must be sold firstso long asCB

accommodates reserve demand

Doesnt matter whether CB prohibited from buying new

issuesroundabout through banks

Doesnt matter whether Treasury must have money in itsacct at CB

to spendCB and banks cooperate

-

7/29/2019 Randall Wray - Fiscal Cliff

28/39

Principles of Functional Finance(Abba Lerner)

i. Government shouldspend more if there isunemployment

ii. Government shouldsupply more money (reserves) ifinterest

rates are too high

NB: Budgetary outcome, Debt outcome should never be

primary consideration

-

7/29/2019 Randall Wray - Fiscal Cliff

29/39

Friedman or Keynes?

Let us suppose that one day a helicopter flies over this

community and drops an additional $1000 in bills fromthe sky,

which is, of course, hastily collected bymembers of the community

Milton Friedman, Optimal

Quantity of Money If the Treasury were to fill old bottles with

bank notes,

bury them at suitable depths in disused coal mines

and leave it to private enterprise on tried principles of

laissez faire to dig the notes up again there need beno more

unemployment and the real income of the

country would then become a good deal greater than it

actually is. JM Keynes, The General Theory

-

7/29/2019 Randall Wray - Fiscal Cliff

30/39

Friedman or Keynes?

Martin Wolfe, FT: In the present exceptional

circumstances, when expanding private credit andspending is so

hard, if not downright dangerous, thecase for using the states

power to create credit and

money in support of public spending is strong.

Adair Turner: Japan should have done some outrightmonetary

financing over the last 20 years, and if it haddone so would now

have a higher nominal grossdomestic product, some combination of a

higher pricelevel and a higher real output level, and a lower debt

togross domestic product ratio.

-

7/29/2019 Randall Wray - Fiscal Cliff

31/39

Japan: a scary precedent?

Japan: rapid growth in 1980s, with highestbudget deficits in

developed world

Massive real estate boom in late 1980s

Govt Budget moved to surplus Economy collapsed; 20 years of

recession, deflation, falling real estate

prices Relies on zero interest rates and massive

XR (QE)

-

7/29/2019 Randall Wray - Fiscal Cliff

32/39

-

7/29/2019 Randall Wray - Fiscal Cliff

33/39

-

7/29/2019 Randall Wray - Fiscal Cliff

34/39

-

7/29/2019 Randall Wray - Fiscal Cliff

35/39

EURO: Non-Sovereign Currency

Member states gave up own sovereign currencies

Adopted a foreign currency, the Euro

Much like a USA state: a user of the currency, not issuer

Constrained in its spending: tax revenue, bond sales,

willingness of ECB to lend

Problem: no fiscal equivalent to Uncle Sam in Washington

-

7/29/2019 Randall Wray - Fiscal Cliff

36/39

Euro is the Problem

By adopting the euro sovereign nations have turnedinto something

like U.S. states.

Unlike U.S. states euro governments have to fundpensions and

healthcare

Euro governments had to deal with banking problems

in the U.S. the Fed did the bailing out.

U.S. States Debt/GDP Ratios

(Average 1997-2008)

Alaska 15.7 Montana 12.2

Connecticut 12.1 New Hampshire 13.0

Hawaii 12.2 New York 10.5

Maine 11.0 Rhode Island 16.9

Massachusetts 16.5 Vermont 12.6

-

7/29/2019 Randall Wray - Fiscal Cliff

37/39

Conclusions

Currency-issuing Government spends bycrediting bank accts, taxes

by debiting

Can always afford to spend more

Issues: inflation, exchange rate effects, interest

rateeffects

Sovereign currency gives more policy space

No default risk

Can control interest rates

Can use policy to achieve full employment

-

7/29/2019 Randall Wray - Fiscal Cliff

38/39

What I did and did NOT say

I did say: Sovereign Government faces no financial

constraints;

cannot become insolvent in its own nonconvertible currency

But it can only buy what is for sale

I did NOT say that Government ought to buy everything for

sale

Size of Government is a political decision with economic

effects

I did NOT say that deficits cannot be inflationary:

Deficits that are too big can cause inflation I did NOT say that

deficits cannot affect exchange rates:

Sovereign Governments let currency float; float means

currency can go up and down

-

7/29/2019 Randall Wray - Fiscal Cliff

39/39

Thank you

L. Randall Wray

Professor of Economics, UMKCSenior Scholar, Levy Economics

[email protected]/LRWRAY/

http://www.levy.org/http://www.levy.org/