Embed Size (px)

Citation preview

Journal of MMIJ Vol.127 (2011) No.9

1.Elements of Rare Earth and Classification

The periodic table of the elements, shown in Table 1,

highlights 17 elements comprising Scanndium, Yttrium and 15

elements known as “lanthanoids”1). The elements are lined up

according to the atomic number displayed horizontally and the

same type of electrons in the outermost shell vertically. The

electron number and type of each element gives the physical and

chemical properties2). It can be said that these elements called

“rare earth elements” are similar to each other in some physical

and chemical characters because the outermost electrons are the

same1).

Although there is no defined classification in rare earth,

Table 2 shows common classifications of two methods. One

is to classify into two categories and the other is into three

categories. Solubility of potassium sulfate double salt into water

is used in the case of three categories, e.g. not to solve; light rare

earth, difficult to solve; middle rare earth, easy to solve; heavy

rare earth3).

2.Minerals and Deposits

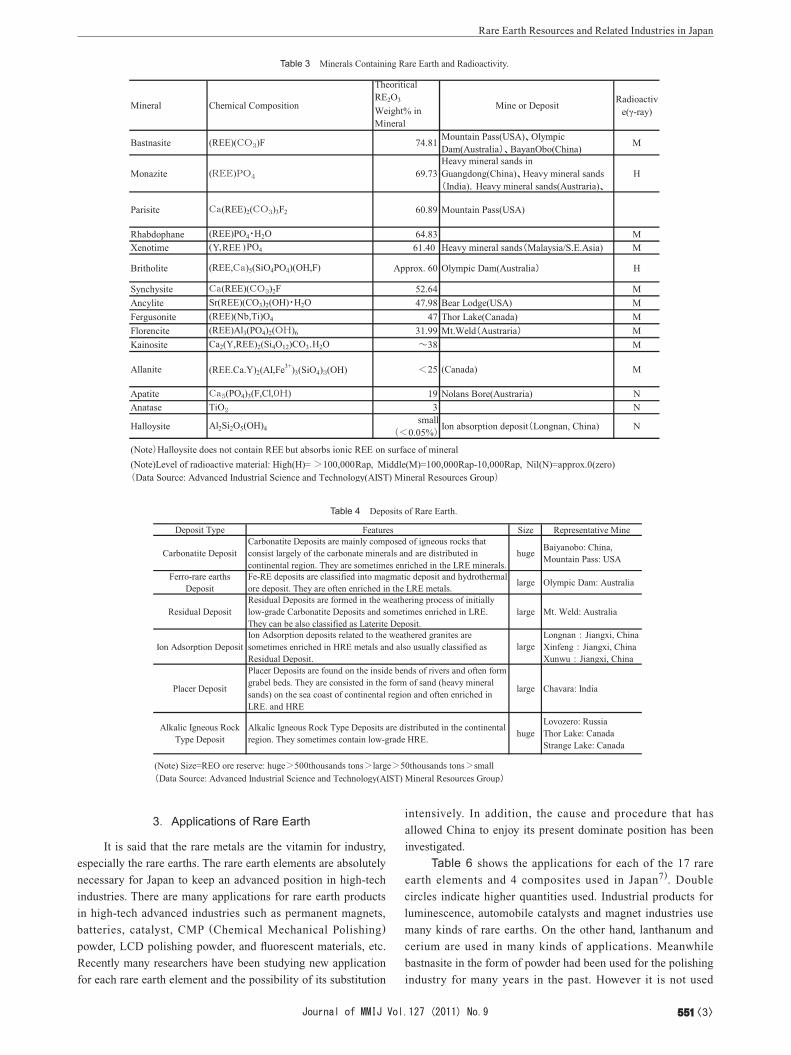

A theoretical percentage of rare earth contained and radio

active level, γ -ray, in main minerals are shown in Table 3. The

minerals of higher radioactive level are monazite and britholite.

There is no defined classification in rare earth deposits.

Table 4 shows comprehensive deposit types at present. Ion

adsorption deposits are actually one of the residual deposits.

However it is separated this time because ion adsorption

deposits consist of clay of halloysite and/or kaolinite to which

surface ionic rare earth elements are adhered3).

It is common that minerals include rare earth elements as

ones of the composition in its crystal, but ion adsorption type

is completely different from these common minerals deposits.

The ion adsorption deposit contents only 0.05-0.2% of rare

earth which is too small comparing to other minerals as above in

Table 3. But it is very easy to separate rare earth elements from

such clay4, 5). In such ion adsorption mines ammonium sulfate

solution is sprinkled from the top of the ore body and gathered

at the foot.

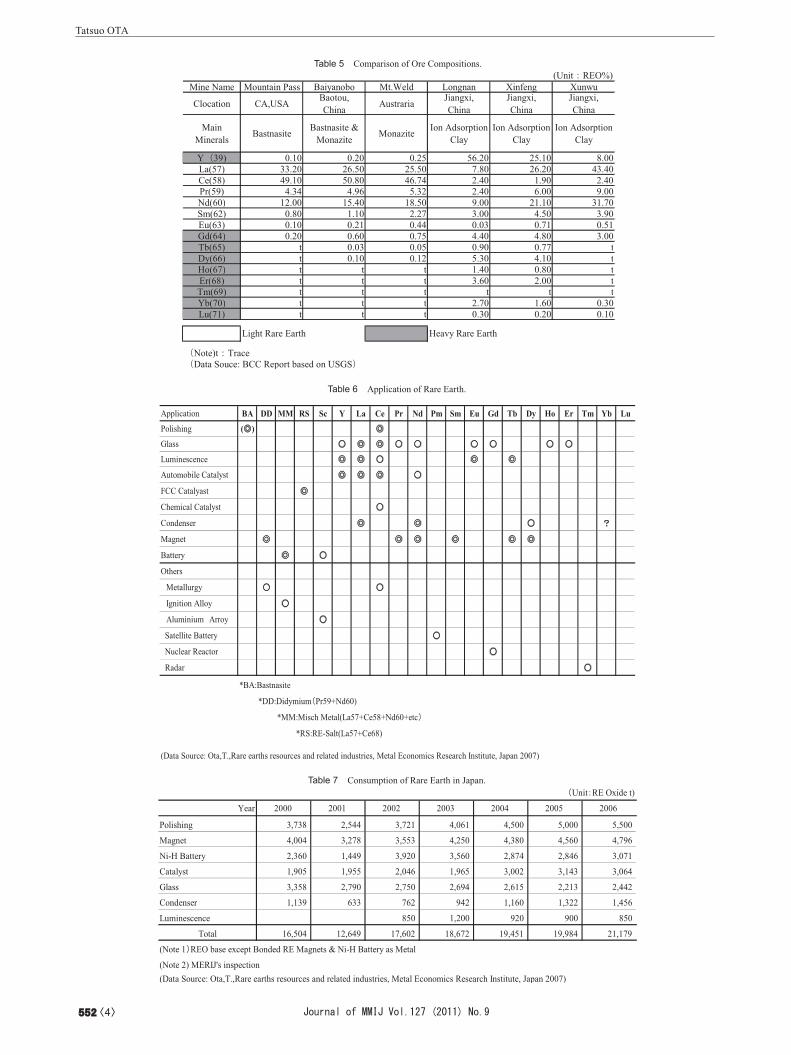

Table 5 shows typical specifications of representative rare

earth mines of the world, all of these mines except China have

ceased or are under development6). There are many types of ion

adsorption clays in details of which are enriched in heavy REE (Rare Earth Elements), light REE or both.

by Tatsuo OTA1

Rare Earth Resources and Related Industries in Japan*

Journal of MMIJ Vol.127 p.549 − 557 (2011)

©2011 The Mining and Materials Processing Institute of Japan

High-tech industries require rare earths which consists of 17 elements. There are many applications for rare earth elements. Having analyzed the United States Geological Survey’s data, the world reserves of rare earths cover more than eight hundred years’ consumption based on total mine production of 130,000 tons in 2010. However, worldwide customers have recently suffered rising major prices and limited quantities in procurement. This is attributed to the Chinese policy of trying to control the production and export, despite the consumption increasing year by year in the world as well as in Japan. China employs a hard policy in rare earth based on their dominate market share at present, which is referred to as “Chinese historical strategy”. This policy was not carried out until recently, although they recognized it in 1992. In those days it was actually meaningless because many other suppliers besides China existed. This policy was based upon the fact that they have a 97% dominant share in the production of rare earth concentrates. They can supply this natural resource to all countries of the world.

Considering this situation and the commodities’ life cycle, it is clear that new sources other than from China should be developed, as a “China plus one” strategy. The heavy rare earths, such as Dysprosium, Terbium and the middle rare earth Europium are absolutely required for Japanese to maintain a high level of advanced technology.

The most important things for proceeding with such development projects are education and training because these projects require manpower, technology, and capital. It is easy to collect money at present if the project is attractive. This technology is maintained by manpower which requires high quality education, training and experience.KEY WORDS: Rare Earth, Magnet, Battery, Low Emission Vehicle, China

549 〈1〉

*Received 17 April, 2009; accepted for publication 29 June, 20111. Automotive-Related Business Unit, Mitsubishi Corporation, 6-1, Marunouchi 2-Chome, Chiyoda-ku, Tokyo Postal Code: 100-8086, JAPAN[For Correspondence] Tel: [81]-3-3210-3536, Fax: [81]-3-3210-6006,

E-mail: [email protected]

Journal of MMIJ Vol.127 (2011) No.9

Tatsuo OTA

550 〈2〉

(Note) Upper:atomic number, Middle:symbol of element, Lower; name of element

Table 1 Periodic Table of the Elements.

Table 2 Classification of Rare Earth Elements.

Journal of MMIJ Vol.127 (2011) No.9

Rare Earth Resources and Related Industries in Japan

3.Applications of Rare Earth

It is said that the rare metals are the vitamin for industry,

especially the rare earths. The rare earth elements are absolutely

necessary for Japan to keep an advanced position in high-tech

industries. There are many applications for rare earth products

in high-tech advanced industries such as permanent magnets,

batteries, catalyst, CMP (Chemical Mechanical Polishing)

powder, LCD polishing powder, and fluorescent materials, etc.

Recently many researchers have been studying new application

for each rare earth element and the possibility of its substitution

intensively. In addition, the cause and procedure that has

allowed China to enjoy its present dominate position has been

investigated.

Table 6 shows the applications for each of the 17 rare

earth elements and 4 composites used in Japan7). Double

circles indicate higher quantities used. Industrial products for

luminescence, automobile catalysts and magnet industries use

many kinds of rare earths. On the other hand, lanthanum and

cerium are used in many kinds of applications. Meanwhile

bastnasite in the form of powder had been used for the polishing

industry for many years in the past. However it is not used

551 〈3〉

Table 3 Minerals Containing Rare Earth and Radioactivity.

Table 4 Deposits of Rare Earth.

Journal of MMIJ Vol.127 (2011) No.9

Tatsuo OTA

552 〈4〉

Table 5 Comparison of Ore Compositions.

Table 7 Consumption of Rare Earth in Japan.

Table 6 Application of Rare Earth.

Journal of MMIJ Vol.127 (2011) No.9

Rare Earth Resources and Related Industries in Japan

553 〈5〉

Table 8 Demand Quantity of Rare Earth in Japan.

Table 9 Production of Rare Earth Magnet in Japan.

at present because of radioactivity concerns. The radioactive

character of rare earth minerals is one of the biggest problems in

the development of new mines.

4.Consumption in Japan

Continuous official data for rare earths is very limited

in Japan at present, especially relating consumption. Table 7

shows results calculated with some formulas for each

application7, 8). However this data does not include nickel-

metal hydride (Ni-MH) rechargeable batteries for hybrid electric

vehicles. The rough consumption quantity of rare earth in the

form of mischmetal (MM) was approximately 600mt or more

in 2006, which should be added to these figures. There are two

reasons why Ni-MH rechargeable batteries does not include the

quantity of hybrid electric vehicles. One is that movements have

been in recent years, and the other is that this area is proprietary

information for automobile and battery manufacturers. Major

high-tech industries consuming many kinds of rare earths

in Japan include rechargeable batteries, rare earth magnets,

low emission vehicles, panel and color televisions. The most

important representative members are for magnets and batteries.

Japan Society New Metals internally works up some interesting

statistics about this kind of rare earth demand in Japan from

1995 onwards that shows Table 8.

Table 9 shows the production data for rare earth magnets

in Japan9,10). The quantity of sintered rare earth magnets has

been increasing until now, although some of their factories have

been transferred overseas. The unit price of magnets of both

kinds declined until 2005.

Table 10 shows the battery production data in Japan11).

Rare earth are used in Ni-MH rechargeable batteries. The

production of Ni-MH batteries had increased until 2000, but

afterward it decreased year by year until 2005. This was caused

by the transfer of factories from Japan to overseas, especially

China, in 2000. Lithium-ion rechargeable batteries were first

introduced into the market in 1995 and achieved the highest

market share in 2002. Ni-Cd battery was decreasing year by

year because of pollution problem associated with disposal.

The figures of Ni-MH batteries do not include that for

hybrid electric vehicles, or low emission vehicles because no

exact data exists. It is said that 7-8kg of this hydrogen storage

metal alloy is used in one hybrid electric vehicle. Its MM

content is 30% and equal to 2kg per car. The production of

such hybrid electric vehicles in 2006 was about 333,000 mostly

produced in Japan. That implies about 666 tons of MM was

consumed by Japanese manufacturers.

Table 10 Production of Rechargeable Battery in Japan.

Table 11 Rare Earth Import in Japan.

Journal of MMIJ Vol.127 (2011) No.9

Tatsuo OTA

5.Import in Japan

China enjoys a 97% share of the world production of

concentrate separated products, which means that the export

quantity from China is almost equal to the total import quantity

of the other countries. Export share from China to Japan is

approximately 1/3 of the total exported from China recently.

The import quantity of each year is listed in Table 1112). Import

quantity increased rapidly in 2006. For example 41,955 tons

was more than 30% compared to 31,107 tons in 2005. It was

supposed to be additional purchase for extra stock, considering

Chinese policy of control of export quantity with export quota (license) and export tax after withdrawal of Value Added Tax

rebate. Import quantity in 2007 was a little bit smaller than

the previous year. It also indicates that a huge import quantity

in 2006 included extra stockpile. But the imported quantity in

2009 was decreased rapidly because of the effects of subprime

mortgage crisis, Lehman shock, on September 15th in 2008

previous year, which showed recovery in 2010.

The share of Chinese materials in Japan had been

increasing year by year until 2008, except in 2001 when the raw

materials market of rare earth was affected by the collapse of the

IT bubble in 2000.

6.Price Trend in Japan

The price had been stable until 2004, but its trend

was changed to upward in 2005. In 2006 this trend became

f irmer and the prices have been rising rapidly, especially

after the imposition of export tax at 10%, which began in

November 2006. Export tax should be paid by exporter (China)

theoretically because it is the domestic law in China. However,

the additional charge was born by the importer, such as Japan,

by putting extra on the usual selling price. Customers in Japan

could not reject this requirement by suppliers as there is no

replacing of China as a supplier. Table 12 shows the rising trend

in prices 13). Neodymium (Nd), terbium (Tb) and dysprosium (Dy) are used by high quality magnet industries, especially

NdFeB alloy magnets, of which each element combines over

20% Nd, 2-6% Dy, 3-5% B and the balance of Fe. In addition

a very small quantity of Dy is replaced by Tb in order to get

greater magnetic effect. The prices of Dy and Tb are very high

because their production quantity is very limited and because

their content in ores is low.

It was a world wide trend that most commodity prices

had been falling since their peak in summer, 2008. Rare earth

prices were no exception, especially after subprime mortgage

crisis and recession in the United States, although the prices of

heavy rare earths have been relatively stable. However the prices

have been increasing since 2nd half in 2010 because of Chinese

policy of limited export quota.

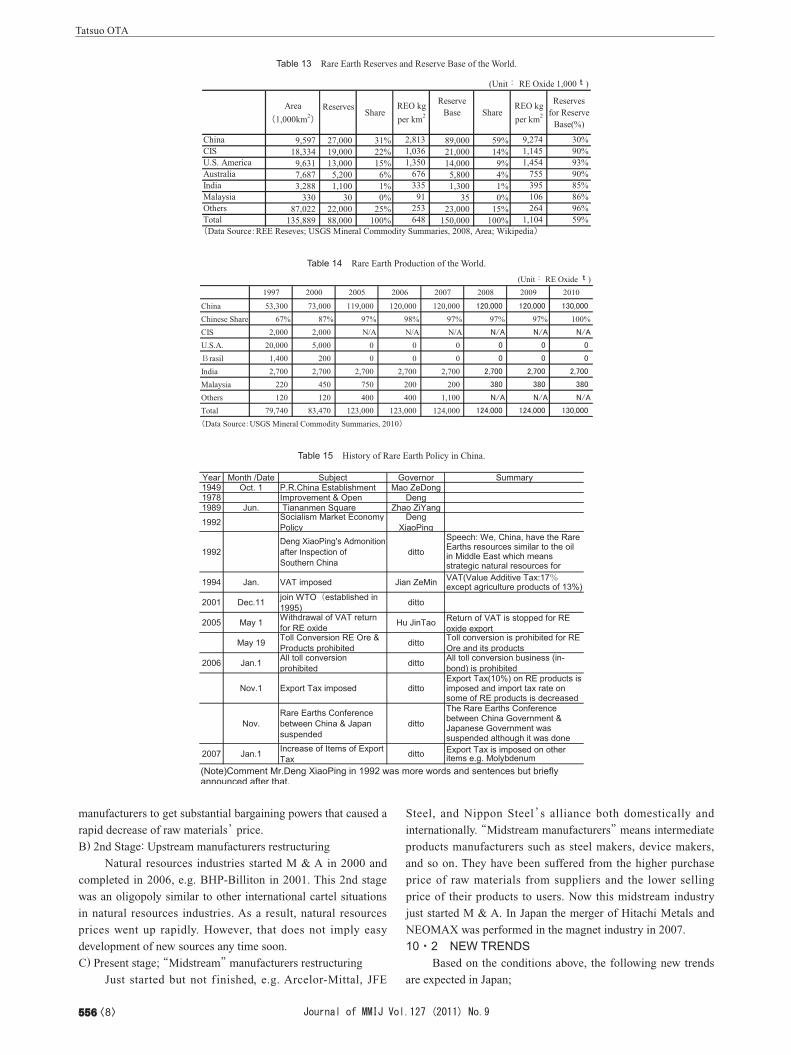

7.Reserves and Reserve Basis of The World

Table 13 shows the rare earth reserves and the reserve

base of the world14), to which area data is added. China’s

reserves’ percentage for reserve base is only 30% but the

percentage of the other countries is approximately 90%.

Therefore there remains potential deposits exist in China. Chinese

quantity of unit area on reserves and reserve base are also larger

than the other countries. This means the deposit density of rare

earth in China is high as well as total reserve volume.

8.Mine Production of The World

The Chinese mine production share in past was lower

than present, e.g. 67% in 1997, though this 67% was still too

large in the world production. The Chinese share had been

increasing year by year as shown in Table 1414, 15). Mines and

plants in India ceased production of heavy mineral sands, and

also stopped the concentration and extraction plants. They were

to be reorganized for reconstruction. This scheme has reached

the final stage and the production will be restarted in 201116).

Considering the USGS presentation of Indian production

quantity of 2,700t p.a., the USGS does not seem to pay any

attention as the production quantity is so small. Anyway China

makes a monopoly of the production at present.

9.History of Rare Earth in China

A brief History of rare earth policy in China is reviewed in

Table 15. In 1978 Mr. Deng XiaoPing, the then PM of China,

changed the planned economy to one of reform and openness.

In 1992, after he inspected the southern China, he noted the

following; “We, China, have the rare earth resources similar to

the oil in Middle East as strategic natural resources.”17) As of

May 1st of 2002, all the foreign investment was prohibited in

the rare earth upstream industry. It means that any investment

in mines by foreigners in China was completely prohibited and

foreigners’ exclusive investment in the rare earth extraction

industry was prohibited too. In addition, the rebate of the Value

Added Tax on rare earth oxide export was stopped as of May

1st 2005. Toll conversion of rare earth ore and its products

was prohibited as of May 19th 2005. A shocking policy was

announced a few days before Nov. 1st 2006. The policy was that

export tax of 10% should be imposed on rare earth products and

it started Nov. 1st but the import tax rate on some high quality

rare earth products was decreased. This export tax has now

increased 15%-25%18).

“The 18th Rare Earth Conference between China & Japan”

was planned to be held in Japan in 2006 or 2007. However it

was abandoned due to China’s intentions. This conference had

been held once a year since 1988, and was resumed in April

2009 in Tokyo. The agenda included engineering and technical

matters in addition to the previous supply and demand ones.

This may assist with a new relation between China and Japan.

10.Discussion and Conclusions

The following are some factors to be considered for the

reasons why the present tight situation exists in rare earth as

a natural resource, as well as in the associated intermediate

products.

10・1 BACKGROUNDA) 1st Stage: Downstream manufacturers restructuring

Automobile industries started M & A in 1980’s and

completed in 1990’s. This movement allowed downstream

554 〈6〉

Journal of MMIJ Vol.127 (2011) No.9

Rare Earth Resources and Related Industries in Japan

Table 12 Trend of Price of Rare Earth Metals in Japan.

555 〈7〉

Journal of MMIJ Vol.127 (2011) No.9

Tatsuo OTA

manufacturers to get substantial bargaining powers that caused a

rapid decrease of raw materials’ price.

B) 2nd Stage: Upstream manufacturers restructuring

Natural resources industries started M & A in 2000 and

completed in 2006, e.g. BHP-Billiton in 2001. This 2nd stage

was an oligopoly similar to other international cartel situations

in natural resources industries. As a result, natural resources

prices went up rapidly. However, that does not imply easy

development of new sources any time soon.

C) Present stage; “Midstream” manufacturers restructuring

Just started but not f inished, e.g. Arcelor-Mittal, JFE

Steel, and Nippon Steel’s alliance both domestically and

internationally. “Midstream manufacturers” means intermediate

products manufacturers such as steel makers, device makers,

and so on. They have been suffered from the higher purchase

price of raw materials from suppliers and the lower selling

price of their products to users. Now this midstream industry

just started M & A. In Japan the merger of Hitachi Metals and

NEOMAX was performed in the magnet industry in 2007.

10・2 NEW TRENDSBased on the conditions above, the following new trends

are expected in Japan;

Table 13 Rare Earth Reserves and Reserve Base of the World.

Table 14 Rare Earth Production of the World.

Table 15 History of Rare Earth Policy in China.

556 〈8〉

Journal of MMIJ Vol.127 (2011) No.9

Rare Earth Resources and Related Industries in Japan

A) Collaboration of Japanese government and private

organization has been executed more rapidly and deeply, e.g.

3-R, Substitute R&D and new mine development. As to mine

development, the National Institute of Advanced Industrial

Science and Technology (AIST) is now researching new deposits

of rare earth which does not include radioactive material,

e.g. apatite deposit containing heavy rare earth. Ferrous rich

manganese ore deposits also containing heavy rare earth

without radio-active materials19). Recently AIST agreed with

the Council for Geoscience of South Africa to develop a ferrous

rich manganese ore deposit in South Africa.

B) Technology of decreasing consumption quantity of Dy

and Tb, which is essential for the NdFeB alloy magnets, is

now under development by Shin-Etsu Chemical Co., Ltd.20),

Intermetallics Co., Ltd. and Osaka University for example. The

development seems to have already succeeded in the laboratory

of Shin-Etsu Chemical Co., Ltd. Shin-Etsu has now started a

study of its commercial application.

C) New applications are developed in biology and medical

areas, although the volume is not so large, e.g. MRI probe21),

scission and manipulation of DNA22).

10・3 FUTURE PROBLEMSA) Detailed statistical data of RE in Japan;

Exact data of rare earth is very difficult compared to other

items. For example China uses 23 HS codes for trading, but only

7 codes in Japan23).

B) Judgment of commodity life;

Only 16 years have passed since lithium ion rechargeable

batteries were introduced into the market. MRI, for example,

rare earth magnets was expected to expand at f irst stage but

uses superconductors at present. As to polishing, cerium oxide

took over from hematite for use in glass polishing in 1963. After

that the new float method of glass making did not use cerium.

High quality glass production followed the float method, which

required cerium usage again. Following that, a new pressed

glass method was developed and consumption of cerium was

decreased24). At present cerium is required for polishing of flat

panel, LCD, PDP and Chemical Mechanical Polishing (CMP), as

such the required quantity in semiconductor industry is large25).

C) How to proceed and manage new projects;

Projects require money, manpower and technology. Money

is suff icient at present, but manpower and technology are

lacking in upstream treatment of rare earths at present. This is

due to the rare earth market being depressed for a long period

of time. Manpower requires high quality education, training and

experience. Additionally, a project manager requires “passion”

for accomplishing a big great achievement.

References

1) T. Masui: 14th Rare earth Summer School, (2006), 1-10. 2) K. Tamao, H. Sakurai and H. Fukuyama: Shyukihyo, (Newton, Tokyo, 2007), pp.30-37. 3) S. Ishihara and H. Murakami: Chishitsu News, 609(2005), 4-18. 4) S. Ishihara and H. Murakami: Chishitsu News, 624(2006), 10-29. 5) A. Shibayama, Y. Tanamachi and S. Nakamura: Journal of MMIJ,123 (2007), 552-554. 6) C. Sinton: Study of the rare earth resources and markets for the Mt. Weld, (BCC Research,

2006). 7) T. Ota: Rare earth resources and related industries (in Japanese), (Metal Economics

Research Institute of Japan, 2007). 8) T. Urai: Chugoku rare earth sanngyono gennjoto doko oyobi nihon rare earth sangyoeno

eikyo (in Japanese), (Metal Economics Research Institute of Japan, 2005). 9) Japan Electronics & Information Technology Industries Association: Statistics, (2010).10) N. Ishigaki and H. Yamamoto: Magnetics Japan, 3(2008), 525-538.11) Ministry of Economy, Trade and Industry: Statistics, (1995, 1996, 1997, 1998, 1999, 2000,

2001, 2002, 2003, 2004, 2005, 2006, 2007, 2008, 2009, 2010).12) Ministry of Finance: Statistics, (2000, 2001, 2002, 2003, 2004, 2005, 2006, 2007, 2008,

2009, 2010).13) Arum Publishing Co.: Industrial Rare Metals, (2005, 2006, 2007, 2008, 2009).14) USGS (United States Geological Survey): Mineral Commodity Summaries, (2008),

pp.134-135.15) USGS(United States Geological Survey): Mineral Commodity Summaries, (1999, 2000,

2001, 2002, 2003, 2004, 2005, 2006, 2007, 2008, 2009, 2010).16) Arum Publishing Co.: Rare Metal News, 2355 (2008), 8.17) Inner Mongolia Science and Technology Agency High-tech Industrial Zone Web-site: “We,

China, have the rare earth resources similar to the oil in Middle East” (in Chinese), (2008), pp.1-2.

18) Research in China: China Rare earth Industry Report, (2008), pp.10-12.19) Advanced Industrial Science and Technology: News, Press Release, (2007).20) T. Minowa: Kinzoku, 77 (2007), 592-592.21) M. Y. Katayama: Rare Earths, 50 (2007), 42-43.22) J. Sumaoka, T. Hirano and M. Komiyama: Rare Earths, 50 (2007), 104-105.23) T. Ota: BM news, 40 (2008), 29-33.24) Japan Society of New Metals: Rare Earths, (1988), pp.96-102.25) Gin-ya Adachi: An Overview of Functions and Applications of Rare Earths, (Shiemu

Shuppan, Tokyo2006), pp.271-279.

557 〈9〉

これらのことや商品のライフサイクルを勘案すると「チャイナ プ

ラス ワン」として中国以外の新しいソースの開発が必要なことは言

うまでもない。特にレアアース元素の中でも重希土ではジスプロシ

ウム,テルビウムと中希土ではユウロピウムが重要である。

プロジェクトは人,もの,金とよく言われるが,それらプロジェ

クトを推進するにあたり最も必要なことは教育である。現在資金

はそのプロジェクトが良ければ直ぐに集めることが出来る。技術

は人によって支えられているものであり,その人には高度な教育

が欠かせない。

レアアース資源と日本の産業 *

太 田 辰 夫 1

ハイテク産業に欠かせないレアアースは 17 元素からなっており

多くの用途がある。米国地質調査所のデータによればレアアース

は 2010 年の鉱石生産量である 130,000 トン ( レアアース酸化物換

算 ) で割れば 800 年以上の充分な埋蔵量があることとなる。しか

しながら最近世界のレアアース顧客はその価格上昇と原料手当て

に苦しんで来た。これは年々日本と同様に世界で消費量が増加し

ているにもかかわらず,生産と輸出を管理しようとする中国の政

策に起因している。中国は現在の支配的なシェアーを基に「中国

の歴史的戦略」とも呼ばれる強固な政策を取って来た。この戦略

は 1992 年に中国では認識はされたものの最近まで発動されなかっ

た。その理由は当時は中国以外の他供給者がいて発動しても無意

味であったからである。しかしこの政策は今や世界精鉱生産量の

97%と言う支配的な中国のシェアーと中国が世界の全ての国にレ

アアース資源を供給出来ることに基き効果的に運営されている。

*2009 年 4 月 17 日受付 2011 年 6 月 29 日受理

1. 正会員 三菱商事 ( 株 ) 自動車関連ユニット 部長代理

キーワード: レアアース,希土類,磁石,電池,低公害車,

中国