Embed Size (px)

Citation preview

E U R O P E A N U R O L O G Y 6 3 ( 2 0 1 3 ) e 5 3 – e 5 6

ava i lable at www.sciencedirect .com

journal homepage: www.europeanurology.com

Letter to the Editor

Re: Christian Bolenz, Stephen J. Freedland, Brent K.

Hollenbeck, et al. Costs of Radical Prostatectomy for

Prostate Cancer: A Systematic Review. Eur Urol. In press.

http://dx.doi.org/10.1016/j.eururo.2012.08.059

Justification of eventually higher costs is one of the main

arguments against robot-assisted surgery. Bolenz and

colleagues presented a systematic review comparing costs

of all types of radical prostatectomy (RP) [1], followed by an

editorial comment by Stewart et al. [2]. Bolenz et al.

concluded that new technology, such as robot-assisted RP

(RALP), results in added costs for the procedure and that

cost-effectiveness of new technologies should be assessed

before widespread adoption [1]. Stewart et al. stated that

even open retropubic RP (RRP) has become ‘‘minimally

invasive’’ and thus the advantages of RALP have diminished

[2]. Considering the restricted financial resources of many

health care systems, the golden years of robotic surgery may

soon be ending [2]. Because I cannot completely support

these arguments, I am writing this letter to the editor.

1. Presentation and discussion of cost factors

Based on the current literature Bolenz et al. [1] had to focus on

11 studies for qualitative synthesis. However, I would expect

a more detailed survey of factors in such cost analyses. What

are direct and indirect costs? What represents mean

procedure costs and total costs? What are cost centres?

Which cost categories have to be included? How should all of

these costs be evaluated? What impact will costs have on the

different health care systems in the United States and

Europe? Which method might be the ideal form of analysis?

What can we learn from history?

2. Definition of costs and cost calculation

Manufacturers use cost calculation (costing) to determine a

price that can be completely attributed to the production of

specific goods or services. Direct costs refer to materials,

labour, and expenses related to the production of a product.

Other costs, such as those for personnel, are more difficult to

assign to a specific product and therefore are considered

indirect costs (Table 1) [3]. Janitors, maintenance workers,

DOI of original article: http://dx.doi.org/10.1016/j.eururo.2012.08.059.

0302-2838/$ – see back matter # 2012 European Association of Urology. Phttp://dx.doi.org/10.1016/j.eururo.2012.12.024

supply room supervisors, sales people, secretaries, and

marketing staff support the manufacturing process but do

not directly affect production. Apart from these definitions,

the term overhead cost is used. These costs include rent or

notes paid on the property, the purchase and depreciation

expense of equipment, utility costs, and any labour costs

that cannot be allocated to a specific product, job, or service.

Running costs are defined as the amount spent to operate an

organisation, including salaries, utilities, and rent.

For adequate costing, it is necessary to determine cost

centres in the company to which direct and/or indirect costs

can be allocated. In hospitals, cost centres usually include

different services involved in pre-, peri- and postoperative

care of the patient, such as theatre, anaesthesia, normal

ward, intensive care unit, laboratory/transfusion, and

cardiology (Table 1). The Institute for the Hospital

Remuneration System (InEK) uses 11 cost centres for yearly

calculation of the German-Diagnosis Related Groups system

[3]. Furthermore, InEK determines eight different cost

categories as being involved during treatment, such as

salaries of doctors, nurses, and administration and costs for

supplies, medication, and implants [4]. Based on this

structure, a modular cost analysis is feasible [5,6] (Table 2).

In the articles reviewed by Bolenz et al. [1], cost centres

and cost categories are mixed up. Tomaszewski et al. [7]

compared RRP and RALP with variables such as cardiology,

imaging, laboratory tests, nursing, and surgery representing

cost centres and clinical administration, operating room

(OR) supply, and pharmacy as cost categories. Anderson

et al. [8] compared RRP and LRP with cost centres

(laboratory/pathology, radiology, room and board, operat-

ing room) as well as cost categories (surgical supplies,

professional fees, transfusion, pharmacy).

3. Simplification of cost analysis

A more rough-and-ready approach to cost analysis is to

allocate indirect costs based on each cost centre percentage

share of direct costs. This approach is commonly taken

for assigning costs of the hospital’s administration and

occasionally overhead costs [3]. When comparing different

operative procedures for the same indications, cost calcula-

tion could be simplified because cost centres (eg, dialysis

unit, radiology, cardiology, pathology) and some cost

ublished by Elsevier B.V. All rights reserved.

Table 1 – Overview of the nomenclature used in recent studies analysing the costs of radical prostatectomy

Term Description

Direct costs Direct costs refer to material, labour, and expenses related to the production of a product or procedure

Indirect costs Costs such as depreciation or administrative expenses that are more difficult to assign to a specific product or operation

Overhead costs Costs including the rent or notes paid on the property; the purchase and depreciation expense of equipment; utility costs; and any

labour costs that cannot be allocated to a specific product, job, or service

Running costs Amount regularly spent to operate an organisation, used for things such as salaries, utilities, and rent

Total costs Sum of direct and indirect costs (eg, hospital costs)

Cost centres Centres of activity in the hospital to which direct and/or indirect costs can be allocated, including areas involved in pre-, peri- and

postoperative care, such as ward, intensive care unit, theatre, anaesthesia, laboratory/pathology, radiology, cardiology, and other

medical services

Cost categories Discrimination of costs involved during treatment, such as salaries of doctors, nurses, and administration and costs for supplies,

medication, and implants

Table 2 – Modular cost calculation based on InEK data [5] in euros: (a) G23A (appendectomy); (b) F10Z (exchange of pacemaker aggregate)

(a)

Cost centre Physician Nurses Technicians Supply Infrastructure Total

Ward 208.3 497.0 49.5 67.0 291.4 1.1113.3

ICU 1.2 2.9 0.3 0.8 1.5 6.5

Theatre 106.1 – 138.8 106.5 94.0 445.4

Anaesthesia 111.0 – 89.0 34.6 31.6 266.3

Cardiology 0.2 – 0.2 0.0 0.2 0.6

Gastroenterology 0.5 – 0.7 0.1 0.5 1.9

Radiology 3.7 – 4.6 2.1 3.8 14.1

Laboratory 5.4 – 22.0 16.2 6.7 51.3

Others 12.4 0.9 13.9 3.7 10.5 41.4

Basic costs* – – – – 262.4 262.4

Total 448.8 500.6 319.0 229.9 704.7 2.203.3

(b)

Cost centre Physician Nurses Technicians Supply Infrastructure Total

Ward 136.2 331.7 32.8 143.5 294.7 937.9

ICU 38.0 82.5 3.1 39.0 31.5 197.7

Theatre 199.2 – 134.3 8.999.6 226.3 9.559.5

Anaesthesia 151.4 – 107.9 74.5 89.8 423.5

Cardiology 61.4 – 75.6 3.899.5 93.1 4.129.6

Gastroentero–logy 0.2 – 0.2 0.1 0.2 0.7

Radiology 15.3 – 23.5 10.4 28.6 77.8

Laboratory 7.1 – 22.0 16.2 6.7 51.3

Others 12.4 0.9 41.3 41.9 22.4 112.7

Basic costs* – – – – 85.9 85.9

Total 636.5 416.7 474.2 13.278.9 908.3 15.714.5

ICU = intensive care unit.* Overhead costs.

E U R O P E A N U R O L O G Y 6 3 ( 2 0 1 3 ) e 5 3 – e 5 6e54

categories (eg, professional fees, nonmedical infrastructure)

are identical and thus can be taken out of the calculation.

Costing should focus only on relevant cost centres

(eg, normal ward, intensive care unit, theatre, anaesthesia)

and cost categories (eg, salaries, supply, and medical

infrastructure), calculating all relevant parameters, such

as OR time plus preparation, anaesthesia time, analgesics/

transfusion, and surgical supplies (Table 3).

Some of these parameters have to be evaluated carefully;

for example, when comparing RALP with other alternatives, it

has to be taken into account that the surgeon does not have to

scrub and thus is not involved in patient preparation.

Moreover, there has to be a strict definition of relevant

times (eg, anaesthesia time equals hands-on to hands-off;

preparation equals scrubbing of bedside OR team with

parallel preparation of the robot plus skin disinfection). Every

institutional calculation should be based on evaluated

clinical data, including analgesics, transfusion rate, epidural

catheter, and stratification of patients with and without

pelvic lymph node dissection. These calculations were

incomplete in the articles reviewed by Bolenz et al. [1].

Such parameters are useful as data sources for computer

models taking averages and ranges of costs [8]. However,

this analysis assumes that there is a linear correlation

between costs and parameters such as OR time or hospital

stay. This does not reflect clinical reality: In case of 10-h OR

occupancy, there is a quantum leap in cost benefit, when

anaesthesia time can be reduced to allow performance of

three cases instead of two with same personal resources

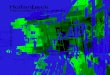

(ie, 200 min; Table 4). The experience of high-volume centres

has proven that this might be feasible (Fig. 1), and Rebuck

et al. [9] demonstrate further options for reducing times and

Table 3 – Relevant cost centres and categories for cost comparison of radical prostatectomy with indicating parameters

Cost centre Physician Nurses Technicians Supply Infrastructure

Ward Hospital stay Hospital stay – Transfusion

Analgesics

NR

ICU Invasiveness* Invasiveness* – Transfusion

Analgesics

NR

Theatre OR time plus preparation time – OR time plus preparation time OR set

Instruments

Sterile cover

Maintenance

Da Vinci cost**

Anaesthesia Anaesthesia time

(hands on to hands off)

– Anaesthesia time

(hands on to hands off)

NR NR

ICU = intensive care unit; OR = operating room; NR = not relevant.* Depending on clinical pathways.** Depending on health care system.

Table 4 – Relevant data for direct cost parameters of robot-assisted radical prostatectomy

Cost parameter Average (range) Difference vs RRP Benchmark Comment

Anaesthesia time, min 322 (168–589) No data 200 min Significant benefit only if benchmark is reached

Preparation 24 (7–92) 20 min

OR time 256 (140–386) 112 140 min

Turnover 43 (21–111) 40 min

Supply, $

Instruments 2852 (1243–11 275) 1800–2315 1500 Cost reduction by use of only three different instruments

Cover of robot 1884 s 1568 s Indirect costs* not included

Hospital stay, d

USA 1 (1–2) 1 NR Depending on health care system

Germany 7 (6–12) 2 ($500/d) Waiting list required

35% less

Transfusion costs, $ 15 (0–37) 80–390 NR Varying results for RRP

ICU costs, $ 414 700 NR Depending on clinical pathways

Rehabilitation period, d 11 38 10 (186 s/d) Only one study

RRP = retropubic radical prostatectomy; OR = operating room; NR = not relevant; ICU = intensive care unit.

Indirect costs (puchase and maintenance) per da Vinci procedure: 3.456 s ($2698–5893).

E U R O P E A N U R O L O G Y 6 3 ( 2 0 1 3 ) e 5 3 – e 5 6 e55

direct costs of RALP. However, reduction of hospital stay can

only be beneficial if the bed is filled immediately with

another patient.

Finally, calculations of purchase costs depend on the

health care system. In Germany, there is a dual health care

reimbursement system: Cost-intensive devices (eg, com-

puted tomography [CT], magnetic resonance imaging [MRI],

radiotherapy unit, cardiology unit, ultrasound device,

surgical robots) are financed by the state and/or the

community, whereas running costs are covered by health

[(Fig._1)TD$FIG]Fig. 1 – Console times of a single surgeon (J.R.) during his first 257 cases.After 50 cases, the benchmark of 80 min could be reached.

care insurance. Accordingly, urology competes with other

faculties. In our institution, the department of radiology

received two CT and two MRI units without any need for

additional fundraising, whereas the da Vinci system

required a substantial amount of extrainstitutional funding.

I am not aware of any study showing the superiority of MRI

over CT such that related investments are associated with

any cost reduction.

4. Cost benefit of robot-assisted radical

prostatectomy

Introduction of RALP is associated with significant costs for

purchase, maintenance, and supply. This is aggravated by the

manufacturer monopoly, similar to the history of extracor-

poreal shock wave lithotripsy (ESWL) [10]: Only reduction of

dialysis rate was able to prove the financial benefit of ESWL,

whereas significantly shorter hospital stay and even earlier

rehabilitation were not able to compensate for investment

and running costs (Table 5). This fact did not stop worldwide

distribution of lithotripters, dividing urologic departments

into first- and second-class services at the time.

RALP provides advantages apart from less invasiveness,

reduction of analgesics, and almost complete elimination of

transfusion rates. These advantages include earlier rehabil-

itation and reduction of long-term side effects (ie, stricture

Table 5 – Cost-efficiency calculation

Cost parameter Costs/year, DM Costs/ESWL, DM Comment

Investment costs

4 400 000 DM

880 000 1955 5-yr subscription, 450 cases/yr

Personnel 325 000 722 Less personnel for ESWL vs OR

Maintenance 159 000 355 –

Supply

Electrodes – 900

–

Hospital stay, 6d vs 14d – 1512 210 DM/d

Rehabilitation, 11d vs 25d – 585 55% of patients work

Dialysis costs – 4560 Possibility to avoid dialysis by ESWL = 0.0045

Total – 2725 Benefit per ESWL

DM = Deutsche Mark; ESWL = extracorporeal shockwave lithotripsy; OR = operating room.

Modified from Miller et al. [10].

E U R O P E A N U R O L O G Y 6 3 ( 2 0 1 3 ) e 5 3 – e 5 6e56

rate). Again, these benefits do not completely compensate

for the costs, but there is no return: The train has already left

the station, as we experienced with the introduction of

ESWL. In the modern world, medicine represents a market,

with the hospitals competing for patients.

Investment ina robot has resulted intheeconomic survival

of urologic departments in Germany, leading to a significant

increase in prostate cancer and establishing waiting lists for

RALP. Evidently, reduction of OR time is the most challenging

aspect of the actual situation: Only if a centre is able to

performthreeRALPprocedures inonetheatremighttherebea

chance to meet the benchmark (Table 4).

5. The future of robot-assisted radical

prostatectomy

The monopoly of RALP creates a dilemma; however, we

have experience with such a situation. We should not stop

using this extremely helpful technology in our daily surgical

practice only because of an unfavourable cost–benefit

analysis. On a large scale, RALP can be cost-efficient for a

hospital by attracting patients, specializing surgeons, and

ideally establishing waiting lists as a basis for economics. In

our centre, introduction of the da Vinci device resulted in an

increase in our overall costs per case from 500 s to 550 s (ie,

compared to 840 s for the cardiology department). We

observed a 10% increase in patients after 2 yr, and our

budget was adjusted accordingly. Actually, there is no

reason for us not to use state-of-the-art technology to

perform RP.

But what will the future be? A restriction of new

technology due to restricted finances? I do not believe this!

As with ESWL [11], several robotic devices will come on the

market and result in a significant price reduction. Changing

stone distribution actually favours endourology for various

indications (eg, ureteral calculi). Accordingly, we may see a

renaissance in simpler techniques, such as laparoscopy, but

with significantly improved instruments and ergonomics

[12]. Open surgery, however, will not survive as the first-

line option for RP.

Conflicts of interest: The author has nothing to disclose.

References

[1] Bolenz C, Freedland SJ, Hollenbeck BK, et al. Costs of radical pros-

tatectomy for prostate cancer: a systematic review. Eur Urol.

In press. http://dx.doi.org/10.1016/j.eururo.2012.08.059.

[2] Stewart SB, Reed SD, Moul JW. Will the future of health care lead to

the end of the robotic golden years? Eur Urol. In press. http://

dx.doi.org/10.1016/j.eururo.2012.10.019.

[3] Shepard DS, Hodgkin D, Anthony Y. Analysis of hospital costs:

a manual for managers. World Health Organization Web site.

whqlibdoc.who.int/publications/2000/9241545283.pdf.

[4] Calculation handbook (Kalkulationshandbuch v.3.0) of the Institute

for the Hospital Remuneration System, the autonomy for the German

Refined–Diagnosis Related Groups [in German]. Institut fur das

Entgeltsystem im Krankenhaus Web site. http://www.g-drg.de/cms/

Kalkulation2/DRG-Fallpauschalen_17b_KHG/Kalkulationshand buch.

[5] Plucker W, Wolkinger F. Personalbestimmung nach DRG. Arzt und

Krankenhaus 2007;81:9–12.

[6] Rassweiler J. Wie zuverlassig sind die InEK-Daten fur die Personal-

bedarfsermittlung. Arzt und Krankenhaus 2007;81:333–7.

[7] Tomaszewski JJ, Matchett JC, Davies BJ, Jackman SV, Hrebinko RL,

Nelson JB. Comparative hospital cost-analysis of open and robotic-

assisted radical prostatectomy. Urology 2012;80:126–9.

[8] Anderson JK, Murdock A, Cadeddu JA, Lotan Y. Cost comparison of

laparoscopic versus radical retropubic prostatectomy. Urology 2005;

66:557–60.

[9] Rebuck DA, Zhao LC, Helfland BT, et al. Simple modifications in

operating room processes to reduce the times and costs associated

with robot-assisted laparoscopic radical prostatectomy. J Endourol

2011;25:955–60.

[10] Miller K, Fuchs G, Rassweiler J, Eisenberger F. Financial analysis,

personal planning and organizational requirements for the instal-

lation of a kidney lithotripter in a urologic department. Eur Urol

1984;10:217–21.

[11] Rassweiler JJ, Knoll T, Kohrmann KU, et al. Shock wave technology

and application: an update. Eur Urol 2011;59:784–96.

[12] Rassweiler JJ, Goezen AS, Jalal AA, et al. A new platform improving

the ergonomics of laparoscopic surgery: initial clinical evaluation

of the prototype. Eur Urol 2012;61:226–9.

[TD$FIRSTNAME]Jens [TD$FIRSTNAME.E] [TD$SURNAME]Rassweiler

Klinikum Heilbronn, Department of Urology, Am Gesundbrunnen 20,

Heilbronn, 74078, Germany

E-mail address: [email protected].

December 17, 2012

Published online on December 31, 2012

![Meet Madison Webb from The 3rd Woman by Jonathan Freedland [EXTRACT]](https://img.pdfslide.net/doc/110x75/577c988b1a28ab163a8b6a25/meet-madison-webb-from-the-3rd-woman-by-jonathan-freedland-extract.jpg)