Embed Size (px)

Citation preview

Real Estate Default Symposium

Clearing Title

© 2012 Default Attorney Group

www.defaultattorneygroup.org

Title Insurance The Title Commitment Clearing Title Title Claims Other Title Issues

Condo and HOA AssociationsMobile Home Basics

What We’ll Cover Today

Title Insurance

What is it? Owner’s Policy

Insurance for the fee owner Lender’s Policy

Insurance for the lender Why is it necessary? How do we use it?

Type of Search/When do you use?

Title Report/Ownership & Encumbrance

Report

Foreclosure Report

Title Insurance Commitment

The Title Commitment: Basic Sections

Schedule A

Fee Simple Owner

Property Description

Schedule B -Requirements

Schedule B - Exceptions

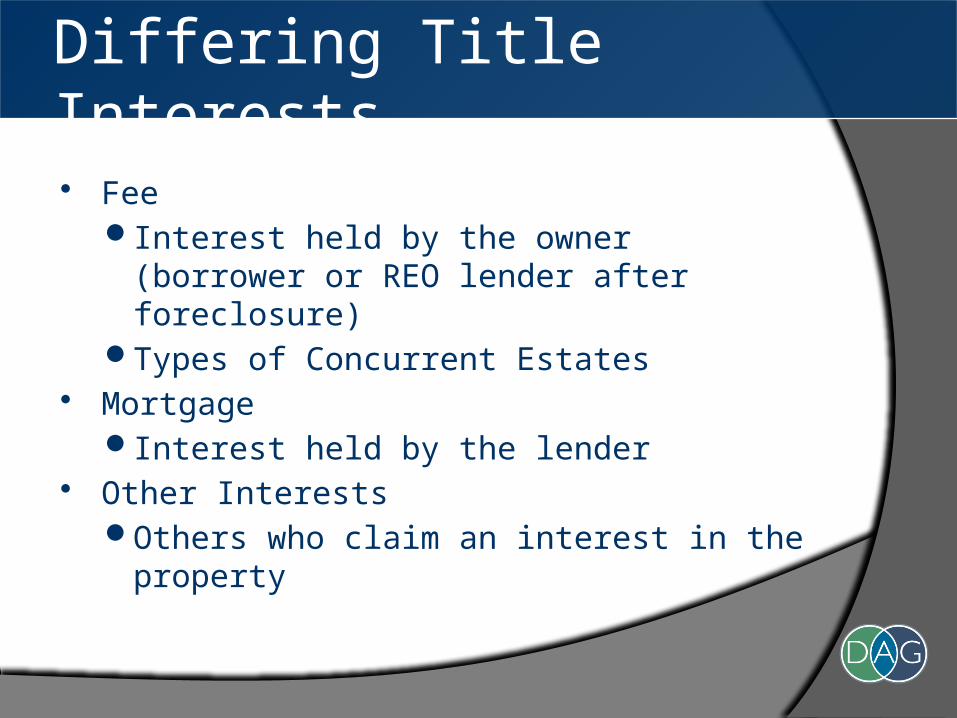

Differing Title Interests

Fee Interest held by the owner (borrower or REO

lender after foreclosure)Types of Concurrent Estates

MortgageInterest held by the lender

Other InterestsOthers who claim an interest in the property

Fee Interests

Types of EstatesJoint TenancyTenancy in CommonTenancy by the EntiretiesLife Estate

Correctness of Descriptions Proper Recording

Office Public Records

Mortgage Interests

Recording Acknowledgement Completeness Assignment Priority Subordinate vs. Superior

Other Interests

Judgments Construction/Mechanic’s Liens Tax Liens Superior Liens vs Subordinate Liens

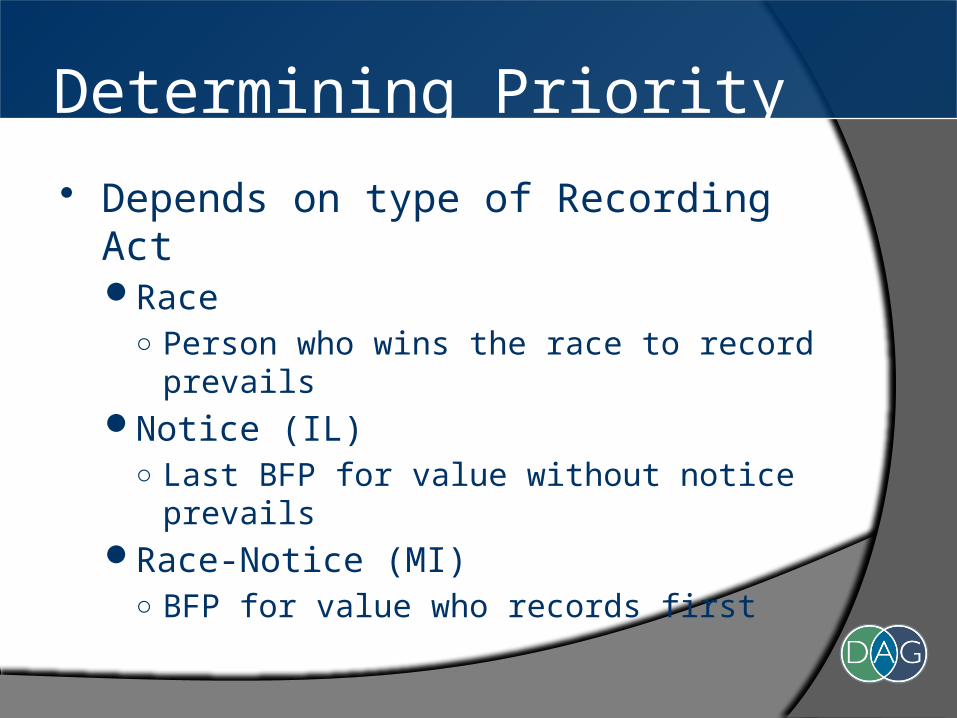

Determining Priority

Depends on type of Recording ActRace

○ Person who wins the race to record prevailsNotice (IL)

○ Last BFP for value without notice prevailsRace-Notice (MI)

○ BFP for value who records first prevails

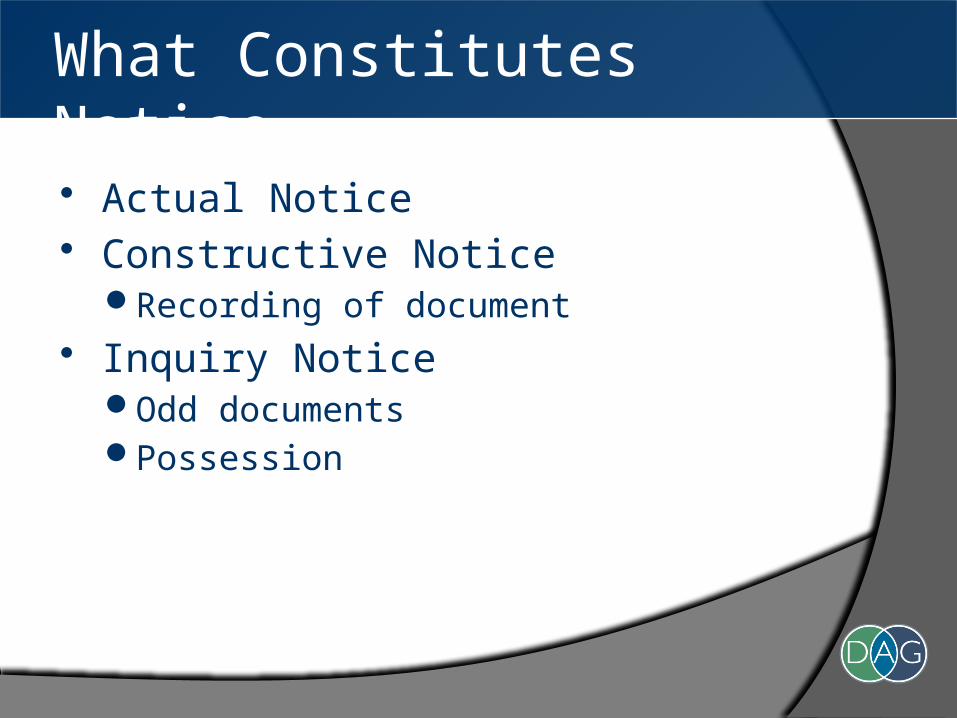

What Constitutes Notice Actual Notice Constructive Notice

Recording of document Inquiry Notice

Odd documentsPossession

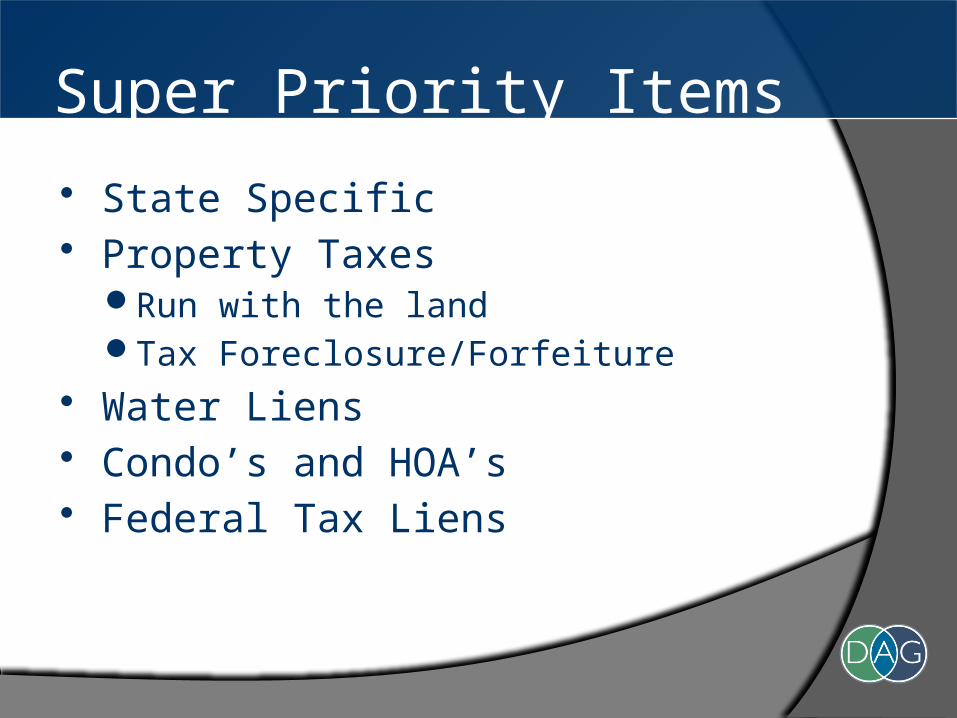

Super Priority Items State Specific Property Taxes

Run with the landTax Foreclosure/Forfeiture

Water Liens Condo’s and HOA’s Federal Tax Liens

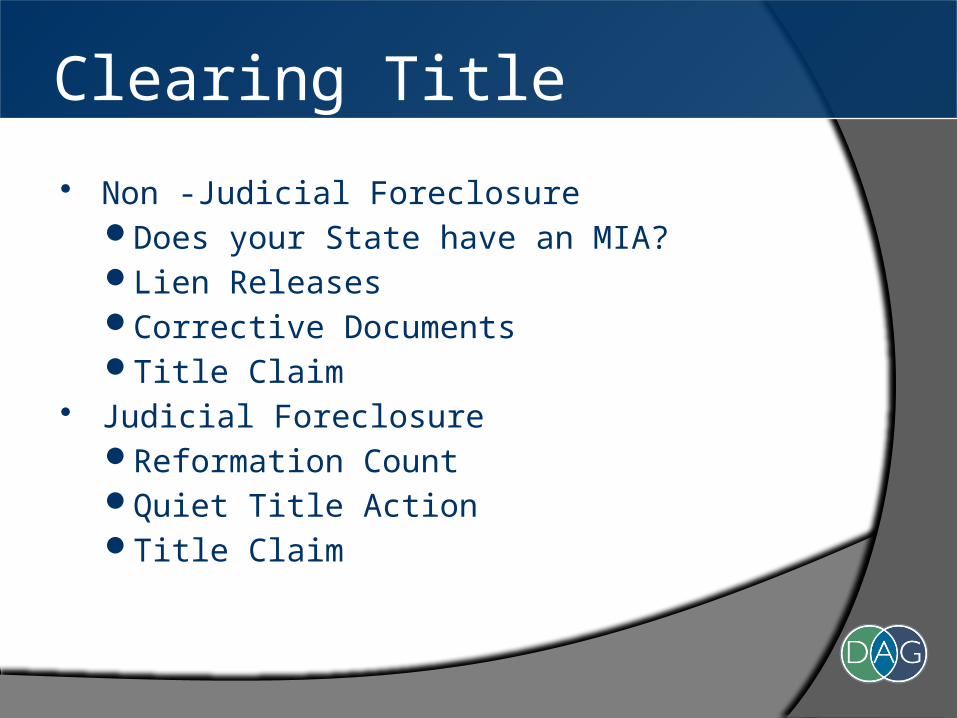

Clearing Title

Non -Judicial ForeclosureDoes your State have an MIA?Lien ReleasesCorrective DocumentsTitle Claim

Judicial ForeclosureReformation CountQuiet Title ActionTitle Claim

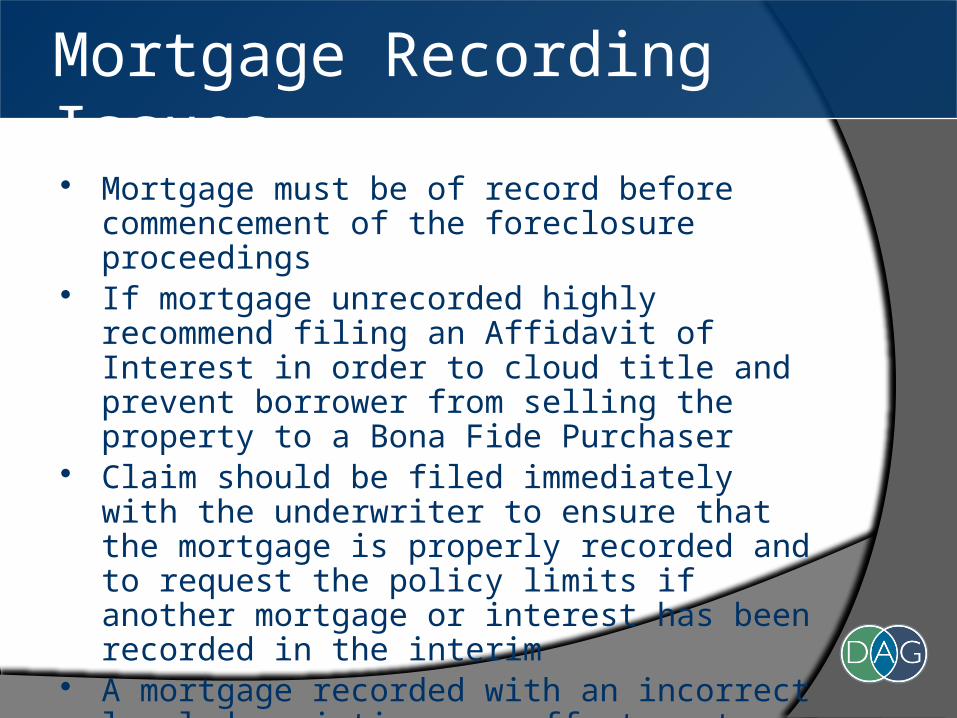

Mortgage Recording Issues Mortgage must be of record before commencement of

the foreclosure proceedings If mortgage unrecorded highly recommend filing an

Affidavit of Interest in order to cloud title and prevent borrower from selling the property to a Bona Fide Purchaser

Claim should be filed immediately with the underwriter to ensure that the mortgage is properly recorded and to request the policy limits if another mortgage or interest has been recorded in the interim

A mortgage recorded with an incorrect legal description can affect mortgage priority

Mutual Indemnity Agreement (MIA) State Specific

An agreement between most title underwriters where issues predating the recording of the mortgage to be foreclosed will be removed as exceptions from the foreclosure title commitment if a clean title policy has been issued

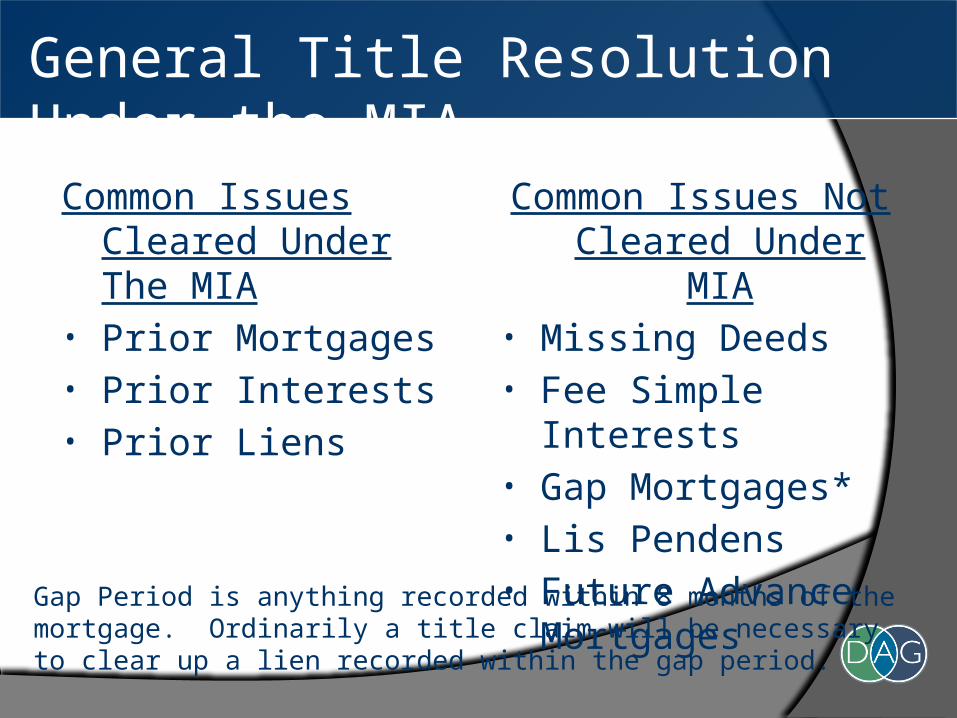

General Title Resolution Under the MIA

Common Issues Cleared Under The MIA

• Prior Mortgages• Prior Interests• Prior Liens

Common Issues Not Cleared Under MIA

• Missing Deeds• Fee Simple Interests• Gap Mortgages*• Lis Pendens• Future Advance

MortgagesGap Period is anything recorded within 8 months of the mortgage. Ordinarily a title claim will be necessary to clear up a lien recorded within the gap period.

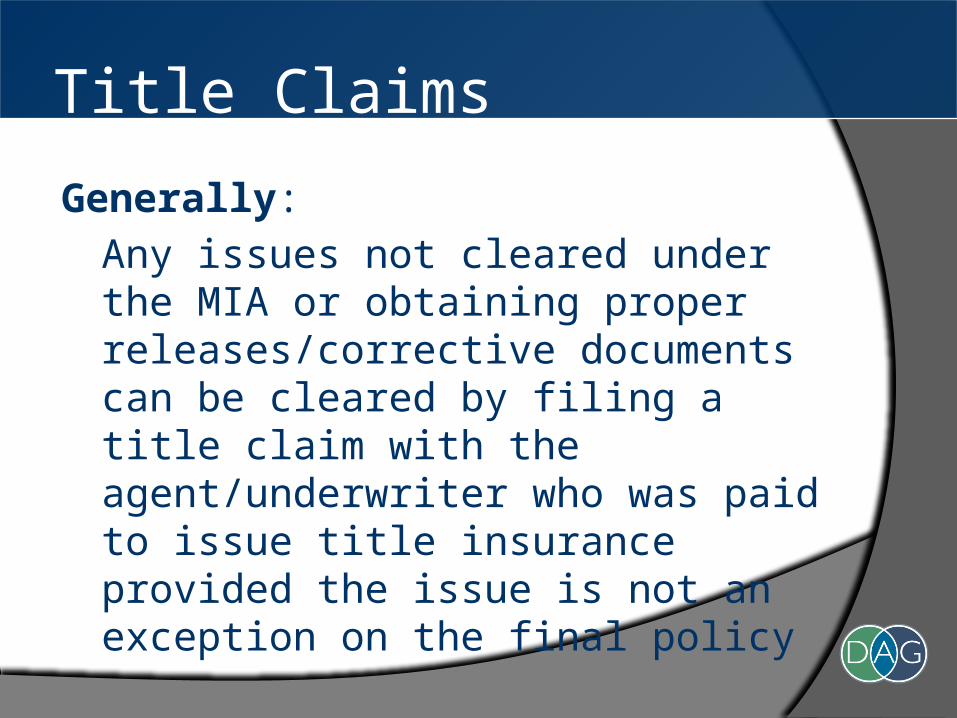

Title Claims

Generally: Any issues not cleared under the MIA or obtaining proper releases/corrective documents can be cleared by filing a title claim with the agent/underwriter who was paid to issue title insurance provided the issue is not an exception on the final policy

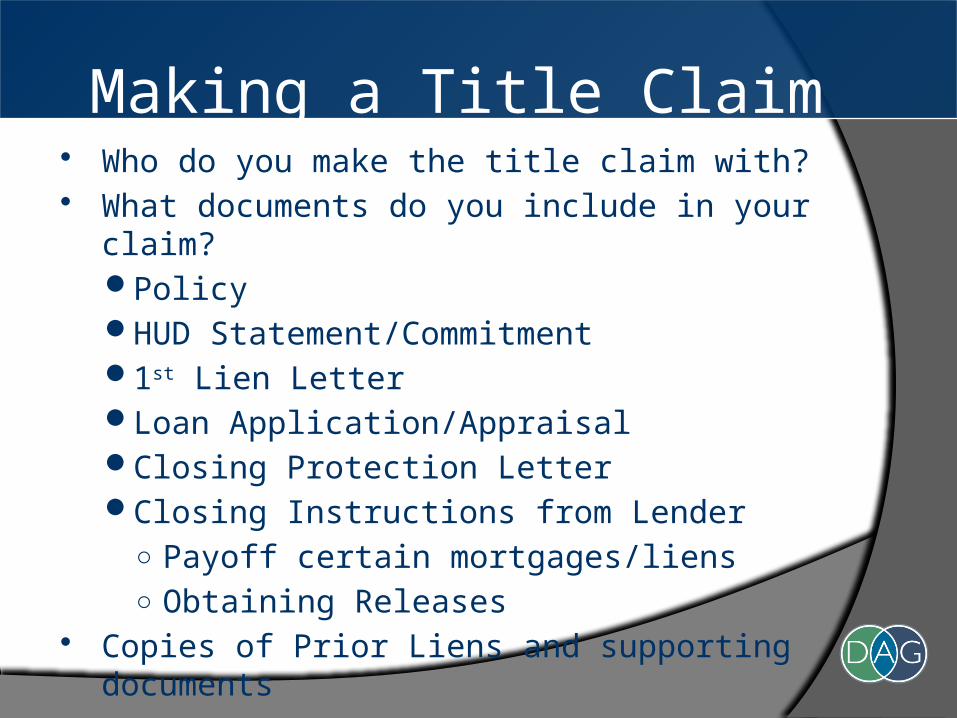

Making a Title Claim Who do you make the title claim with? What documents do you include in your claim?

PolicyHUD Statement/Commitment1st Lien LetterLoan Application/AppraisalClosing Protection LetterClosing Instructions from Lender

○ Payoff certain mortgages/liens○ Obtaining Releases

Copies of Prior Liens and supporting documents

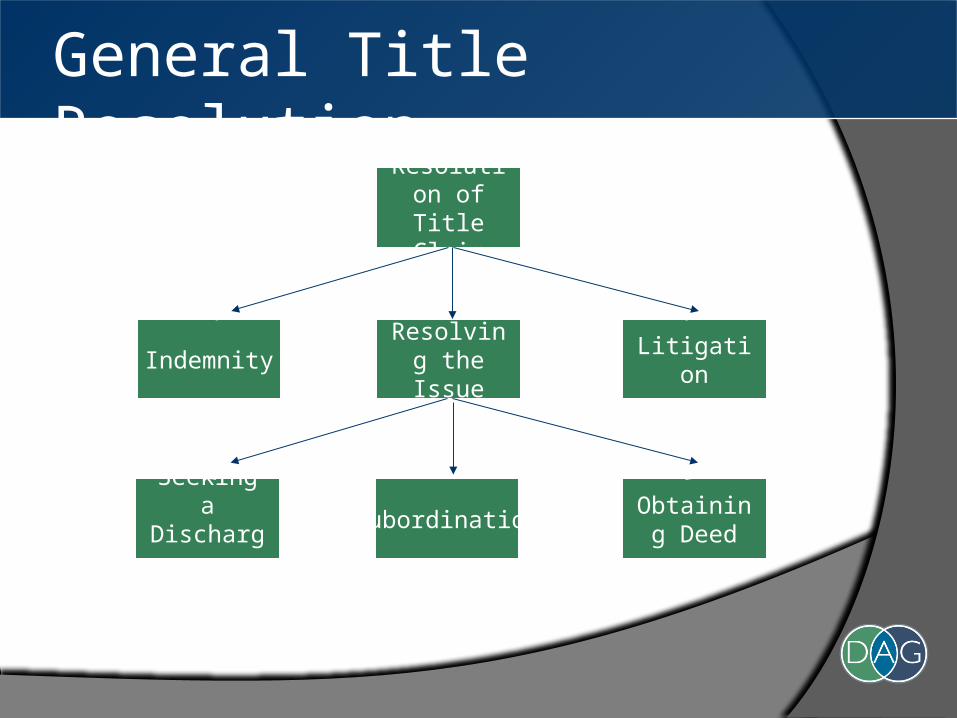

General Title ResolutionResolution

of Title Claim

Seeking a Discharge

Obtaining Deed

IndemnityResolving the Issue

Litigation

Subordination

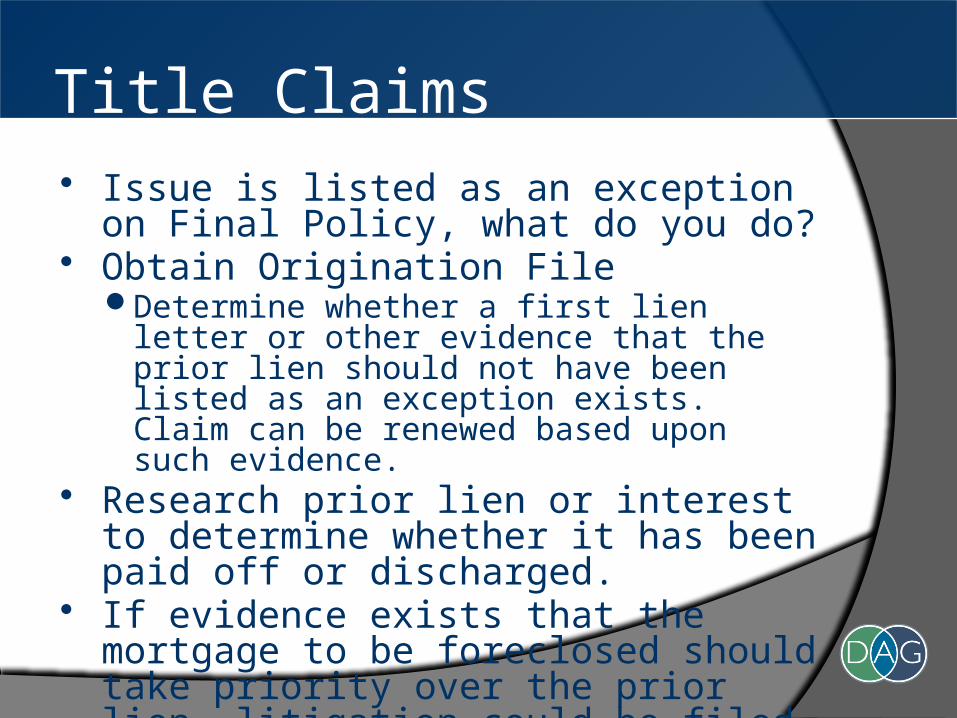

Title Claims Issue is listed as an exception on Final Policy,

what do you do? Obtain Origination File

Determine whether a first lien letter or other evidence that the prior lien should not have been listed as an exception exists. Claim can be renewed based upon such evidence.

Research prior lien or interest to determine whether it has been paid off or discharged.

If evidence exists that the mortgage to be foreclosed should take priority over the prior lien, litigation could be filed to establish priority.

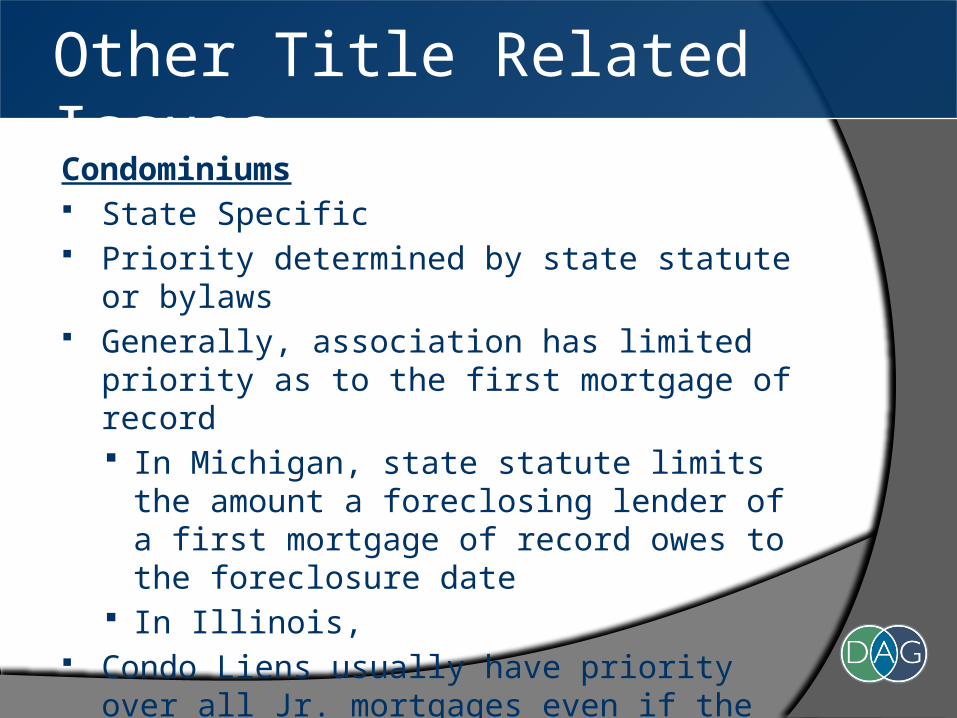

Other Title Related IssuesCondominiums State Specific Priority determined by state statute or bylaws Generally, association has limited priority as to the first

mortgage of record In Michigan, state statute limits the amount a

foreclosing lender of a first mortgage of record owes to the foreclosure date

In Illinois, Condo Liens usually have priority over all Jr. mortgages

even if the Jr. mortgage is recorded first

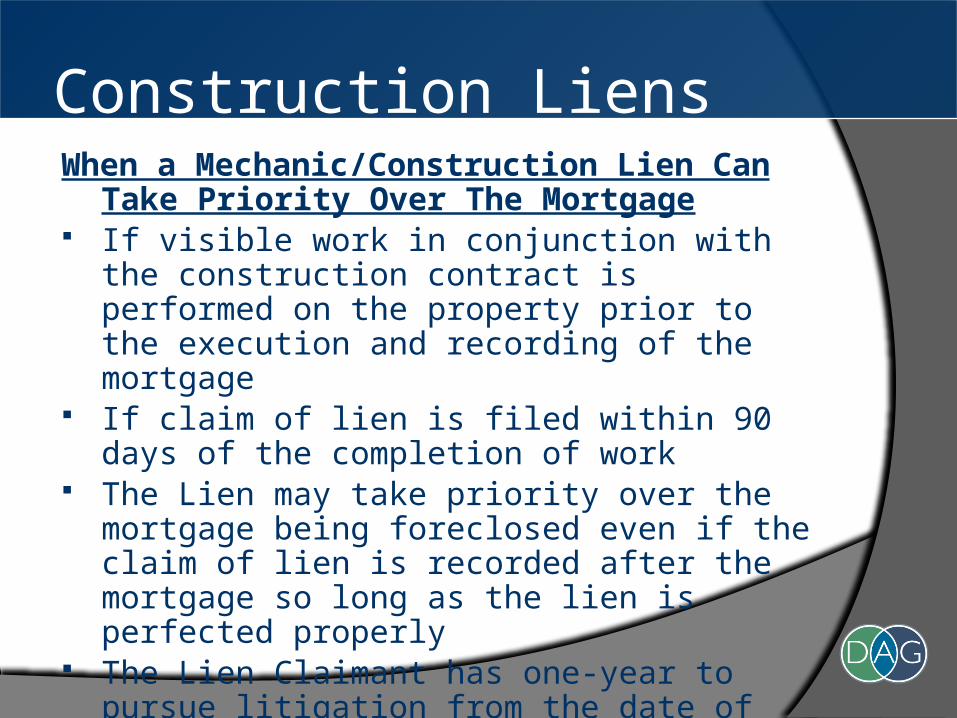

Construction LiensWhen a Mechanic/Construction Lien Can Take

Priority Over The Mortgage If visible work in conjunction with the construction

contract is performed on the property prior to the execution and recording of the mortgage

If claim of lien is filed within 90 days of the completion of work

The Lien may take priority over the mortgage being foreclosed even if the claim of lien is recorded after the mortgage so long as the lien is perfected properly

The Lien Claimant has one-year to pursue litigation from the date of the recording of the lien

Specific Title Related IssuesTitle Claims Regarding Construction Liens In the event that a construction lien has been

properly perfected and has the potential to establish priority over the insured mortgage a title claim should be made

The Closing Agent should ensure that any potential liens for on going construction are subordinated to the mortgage

Obtain Affidavit at closing from the borrowers stating that there are no construction projects recently completed or on going for which a claim of lien could be filed

Mobile Home Basics A Manufactured Home is treated like a motor

vehicle

Therefore, a vehicle “certificate of title” is issued….it is considered personal property

Note: Be careful to distinguish a mobile or manufactured home from a modular home!

Discovering a Mobile Home County Tax Assessment Deed Language/description Loan Appraisal ALTA 7 Title Policy

To Convert to Real Property

Most States Require 4 Things: Proper Physical Attachment Real Property Taxation by County County Land Records DMV Retirement

Must achieve both “physical” attachment and “legal” conversion

Proper Attachment

Varies by State: No Wheels No Axles Secured to Foundation

County Tax Office

The mobile home has to be taxed as part of the real property and be valued as part of the land

County Land Records Most states require that you record something in

the land records to indicate the ‘intent’Affidavit of AffixtureDeclaration of Intent to Affix (DOI)Statement of Ownership and Location

Some states/counties require that the DOA be approved by a building inspection to confirm the “physical” requirements

DMV Requirements

States vary here:1. Create title first….in order to ‘cancel’

2. If never created…simply ‘retire’’

- Some states require submission of deeds, DOI’s, etc to show proof of ‘affixation’

© 2012 Default Attorney Group www.defaultattorneygroup.org

Thank you for your time.

Questions?

![Vagrant for PHP - PHP UserGroup Berlin...$ vagrant up [default] Importing base box 'precise64'... [default] Matching MAC address for NAT networking... [default] Clearing any previously](https://img.pdfslide.net/doc/110x75/5ededbb7ad6a402d666a36d5/vagrant-for-php-php-usergroup-berlin-vagrant-up-default-importing-base.jpg)