Embed Size (px)

Citation preview

Email Question Answer

And

Analysis of China Real Estate Market

Kaifeng Xia

Columbia University

May 1st, 2015 - May 3rd, 2015

Kiafeng Xia 1 / 14

Contents

Part I: Question Answer ................................................................................................... 2

Summarize the recent policy adjustment of sales tax for secondary home owners: .... 2

How it will impact the transaction vol and prices in both the primary and secondary

markets ......................................................................................................................... 2

Any quantitative measure of the impact from the adjustments .................................... 3

Who will benefit the most and why? ........................................................................... 3

Whether you think it will help to boost the overall housing market in China. ............ 4

Part II: Analysis of China Real Estate Market .............................................................. 5

Conclusion ................................................................................................................... 5

Overall .......................................................................................................................... 5

Long-term Analysis ...................................................................................................... 6

Short-term Analysis ..................................................................................................... 9

Part III: Quantitative Model .......................................................................................... 10

Part IV: Some Problems .................................................................................................. 11

Problematic Data Source ............................................................................................ 11

Suggested Classification of Cities ............................................................................. 11

Kiafeng Xia 2 / 14

Part I: Question Answer

Summarize the recent policy adjustment of sales tax for secondary home owners:

1) Regarding Secondary House Sales Tax: Non-ordinary residence owner who sells the

property purchased in less than 2 years shall be collected sales tax at full price. Non-

ordinary residence owner who sells the property purchased more than 5 years ago and

ordinary residence owner who sell the property purchased in less than 2 years shall be

collected sales tax against the difference between purchasing price and selling price.

Ordinary residence owner who sells the property purchased more than 5 years ago shall

be full sales tax exempted.

2) Regarding Second Home Minimum Down Payment: Minimum down payment for

purchasing second home has reduced to 40% from 60%-70%

How it will impact the transaction vol and prices in both the primary and secondary

markets

I think it would help the transaction volume and prices going up but not very significantly.

Superficially, the policy adjustments in secondary market are not supposed to impact the

primary market much, but they actually do. I think the adjustments are in favor of buyers

who already owned a home but would like to improve their living condition. That is, the

demand of improvement. Also, the adjustments would help develop the secondary market

in China in a long-term, which is currently relatively small. This is good for society wealth

distribution, if no speculative activities are involved. In conclusion, at present, the

government hope to heat up the overall real estate market through every supportive policy,

regardless they are focused on primary market or on secondary market.

Kiafeng Xia 3 / 14

Any quantitative measure of the impact from the adjustments

The only data source I am able to access now is National Bureau of Statistics of China. The

data there for April has not been available to me yet, so the quantitative measure of impact

from these adjustments on March 30 has not been clear. However, other adjustments issued

by the government last year have shown some impacts quantitatively. According to news

last year, some markets in large cities have responded to the policy adjustments.

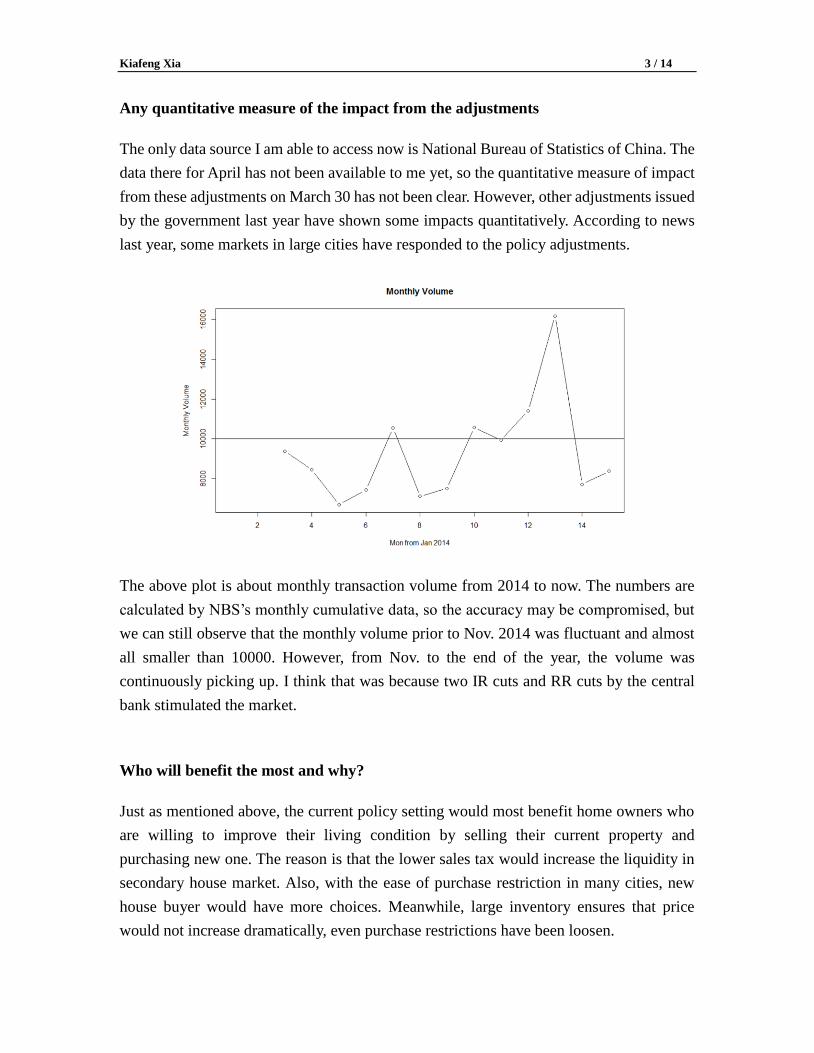

The above plot is about monthly transaction volume from 2014 to now. The numbers are

calculated by NBS’s monthly cumulative data, so the accuracy may be compromised, but

we can still observe that the monthly volume prior to Nov. 2014 was fluctuant and almost

all smaller than 10000. However, from Nov. to the end of the year, the volume was

continuously picking up. I think that was because two IR cuts and RR cuts by the central

bank stimulated the market.

Who will benefit the most and why?

Just as mentioned above, the current policy setting would most benefit home owners who

are willing to improve their living condition by selling their current property and

purchasing new one. The reason is that the lower sales tax would increase the liquidity in

secondary house market. Also, with the ease of purchase restriction in many cities, new

house buyer would have more choices. Meanwhile, large inventory ensures that price

would not increase dramatically, even purchase restrictions have been loosen.

Kiafeng Xia 4 / 14

Whether you think it will help to boost the overall housing market in China.

It cannot be denied that such ease adjustments would somehow help to boost the overall

housing market. However, I doubt the effect of these adjustments, because

1) The secondary house market is relatively small in China. Chinese home buyers are

more willing to buy new residence. Therefore, I think adjustments in secondary market

only play an assistant role.

2) The recent drop in housing market mainly results from large inventory. Secondary

market stimulation may show the impact in a long term as the improvement demand

grows slow.

3) Loosening policy setting may be only expedient, since speculative activities may come

back to the market after purchase restriction was removed for some time, which may

recall the restrictions.

4) The reduction of minimum requirement for down payment was just changing it to a

moderate level. 40% is not very encouraging.

However, to a long-term extent, I think the real estate market in China would recover and

increase stable until the population structure is largely changed in the future. Because the

need is there, no policy or administrative measures could permanently beat the supply-

demand relationship.

Kiafeng Xia 5 / 14

Part II: Analysis of China Real Estate Market

This report mainly analyzes the China real estate market from beginning of 2014 to March,

2015, and secondary house market after policy adjustments.

Conclusion

1) In the long term, China real estate market would develop differentially depending on

regions and cities. Such fragmented development has started showing. The scale of the

market would stay large but fragmented development would cause uneven distribution

of the total. Also, in the future, large real estate companies would have more

opportunities while small ones would have more risks.

2) In the short term, the 2015 real estate market would gradually recover. The volume

would increase mildly and price may not increase significantly in light of large

inventory awaiting. The recovery rate depends on specific situation of each city.

The above 2 opinions are partially referred to monthly data from National Bureau of

Statistics of the PRC and reports from China Index Academy

Overall

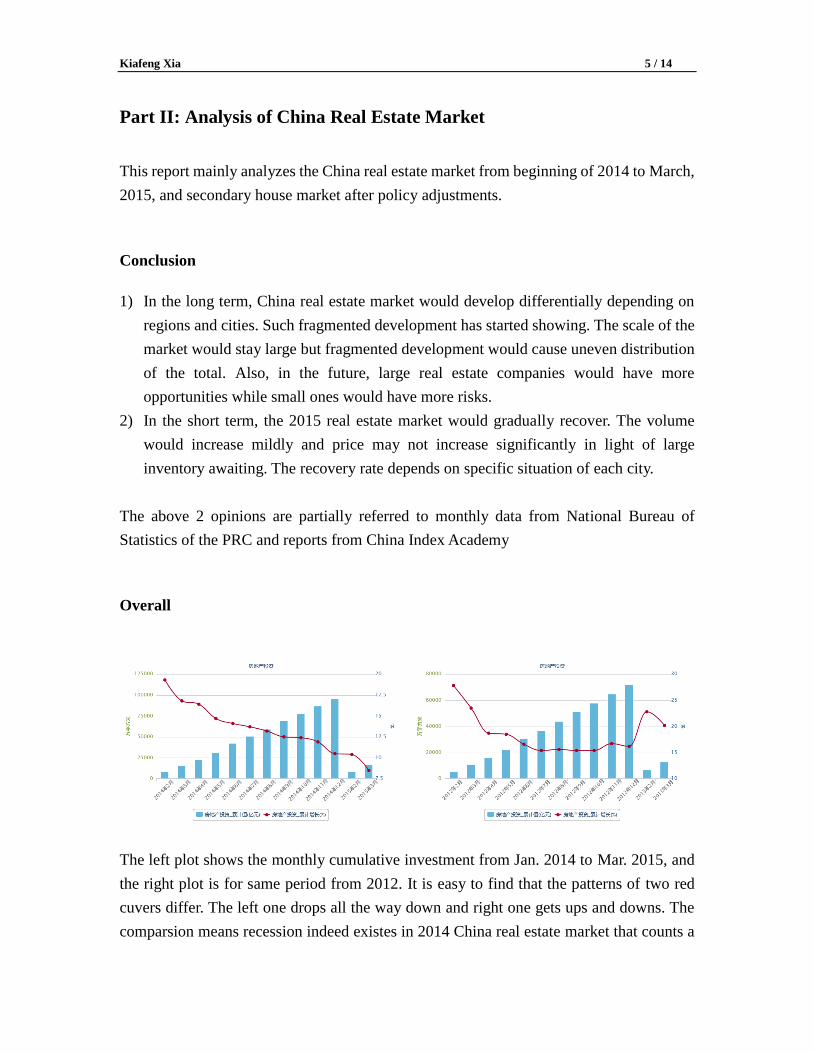

The left plot shows the monthly cumulative investment from Jan. 2014 to Mar. 2015, and

the right plot is for same period from 2012. It is easy to find that the patterns of two red

cuvers differ. The left one drops all the way down and right one gets ups and downs. The

comparsion means recession indeed existes in 2014 China real estate market that counts a

Kiafeng Xia 6 / 14

large portion of the China overall economy. Therefore, its bad performance directly brought

the government relaxing sales tax on March 30, 2015, along with more easy financail

supports issued before, in order to maintain the development of overall economy.

In my opinion, the recession in the market is a consequence of the existance of bubble in

the market. The cause of recession is primarily due to large inventoy levels in many cities.

Deveplors’ expectation was too optimistic on the market, so they built too many houses.

They had such expectation because the speculative activies were prevailing in the past,

which pushed the price skyrocketing. To squeeze out the speculative activies, many cities

implemented purchase restriction couple years ago, which resulted the nowaday redundent

inventory. Impacted by the recession, many small realtors are living hard.

Long-term Analysis

In long term, the gross real estate market would be huge. This judgment comes from 1)

China has a large population base, 2) job opportunities would bring movement of

population, 3) cities are developing and expanding.

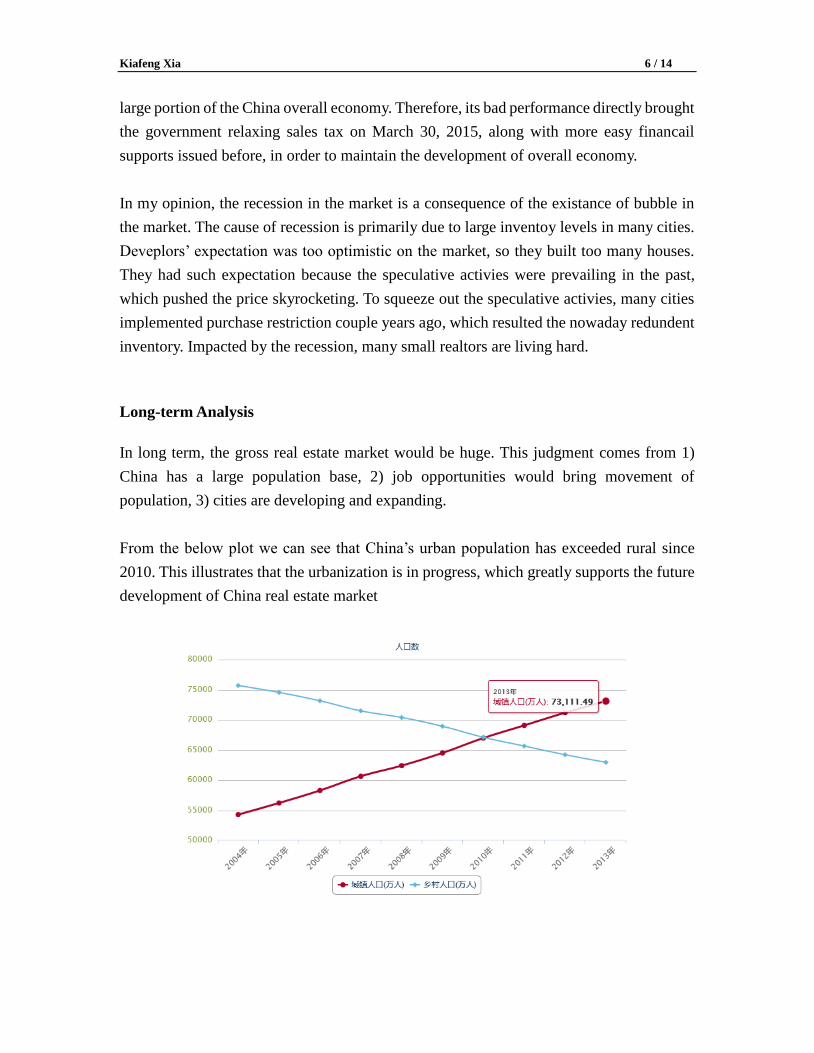

From the below plot we can see that China’s urban population has exceeded rural since

2010. This illustrates that the urbanization is in progress, which greatly supports the future

development of China real estate market

Kiafeng Xia 7 / 14

Real estate market as a market cannot stand away from general market principle, which is

supply-demand relationship. Therefore, as long as the demand force is strong, the overall

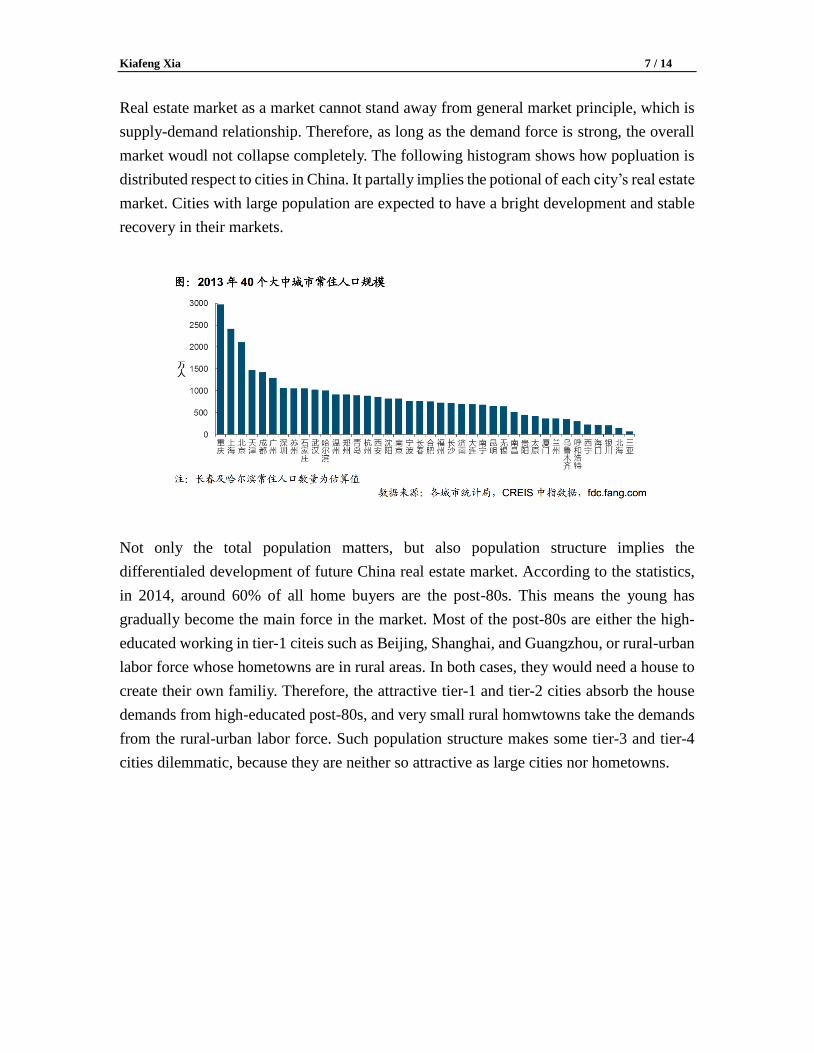

market woudl not collapse completely. The following histogram shows how popluation is

distributed respect to cities in China. It partally implies the potional of each city’s real estate

market. Cities with large population are expected to have a bright development and stable

recovery in their markets.

Not only the total population matters, but also population structure implies the

differentialed development of future China real estate market. According to the statistics,

in 2014, around 60% of all home buyers are the post-80s. This means the young has

gradually become the main force in the market. Most of the post-80s are either the high-

educated working in tier-1 citeis such as Beijing, Shanghai, and Guangzhou, or rural-urban

labor force whose hometowns are in rural areas. In both cases, they would need a house to

create their own familiy. Therefore, the attractive tier-1 and tier-2 cities absorb the house

demands from high-educated post-80s, and very small rural homwtowns take the demands

from the rural-urban labor force. Such population structure makes some tier-3 and tier-4

cities dilemmatic, because they are neither so attractive as large cities nor hometowns.

Kiafeng Xia 8 / 14

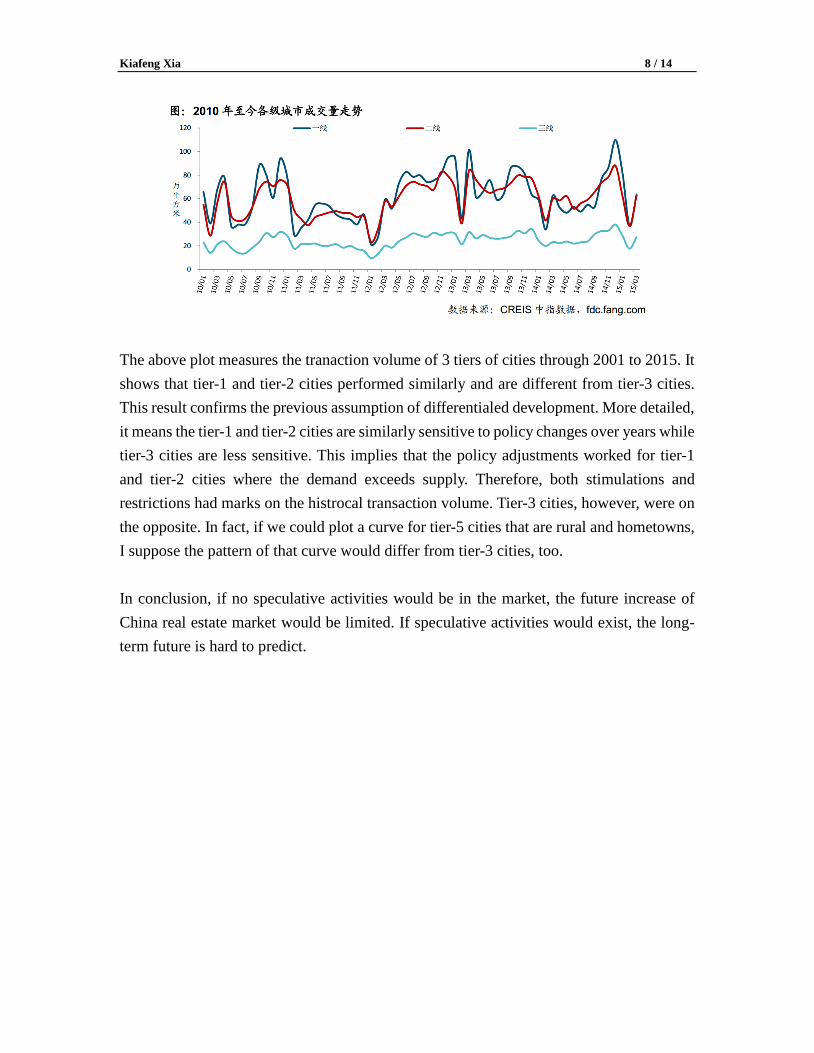

The above plot measures the tranaction volume of 3 tiers of cities through 2001 to 2015. It

shows that tier-1 and tier-2 cities performed similarly and are different from tier-3 cities.

This result confirms the previous assumption of differentialed development. More detailed,

it means the tier-1 and tier-2 cities are similarly sensitive to policy changes over years while

tier-3 cities are less sensitive. This implies that the policy adjustments worked for tier-1

and tier-2 cities where the demand exceeds supply. Therefore, both stimulations and

restrictions had marks on the histrocal transaction volume. Tier-3 cities, however, were on

the opposite. In fact, if we could plot a curve for tier-5 cities that are rural and hometowns,

I suppose the pattern of that curve would differ from tier-3 cities, too.

In conclusion, if no speculative activities would be in the market, the future increase of

China real estate market would be limited. If speculative activities would exist, the long-

term future is hard to predict.

Kiafeng Xia 9 / 14

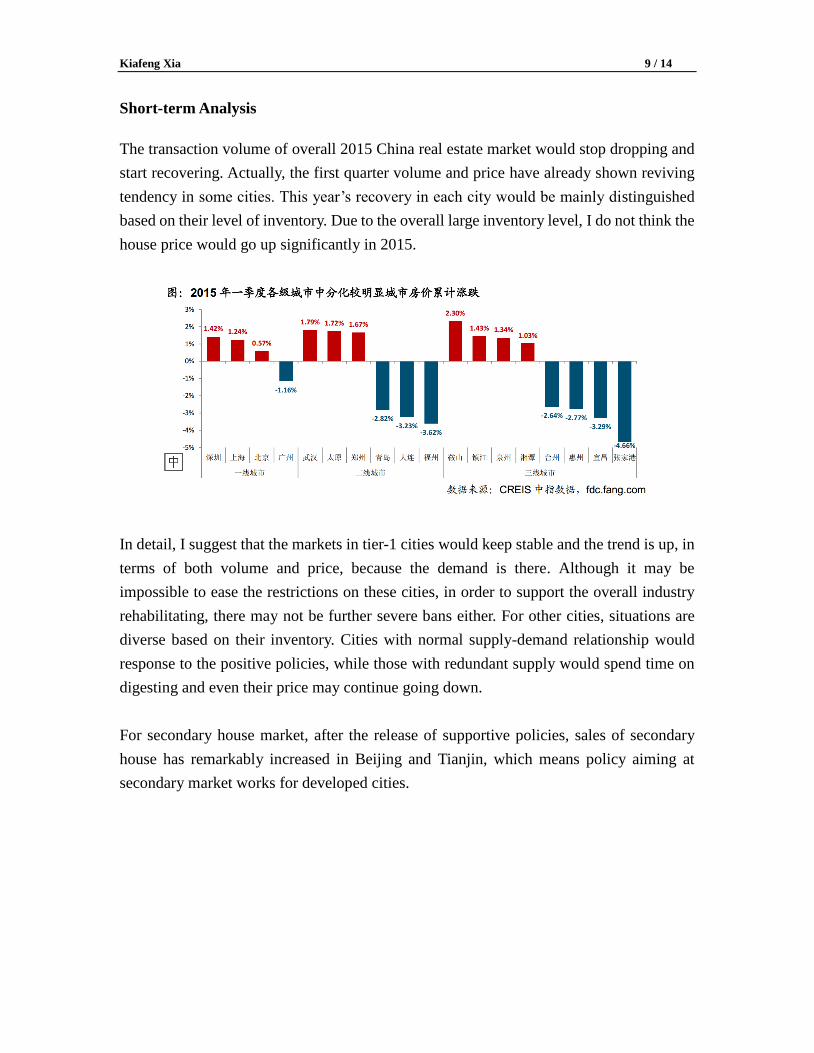

Short-term Analysis

The transaction volume of overall 2015 China real estate market would stop dropping and

start recovering. Actually, the first quarter volume and price have already shown reviving

tendency in some cities. This year’s recovery in each city would be mainly distinguished

based on their level of inventory. Due to the overall large inventory level, I do not think the

house price would go up significantly in 2015.

In detail, I suggest that the markets in tier-1 cities would keep stable and the trend is up, in

terms of both volume and price, because the demand is there. Although it may be

impossible to ease the restrictions on these cities, in order to support the overall industry

rehabilitating, there may not be further severe bans either. For other cities, situations are

diverse based on their inventory. Cities with normal supply-demand relationship would

response to the positive policies, while those with redundant supply would spend time on

digesting and even their price may continue going down.

For secondary house market, after the release of supportive policies, sales of secondary

house has remarkably increased in Beijing and Tianjin, which means policy aiming at

secondary market works for developed cities.

Kiafeng Xia 10 / 14

Part III: Quantitative Model

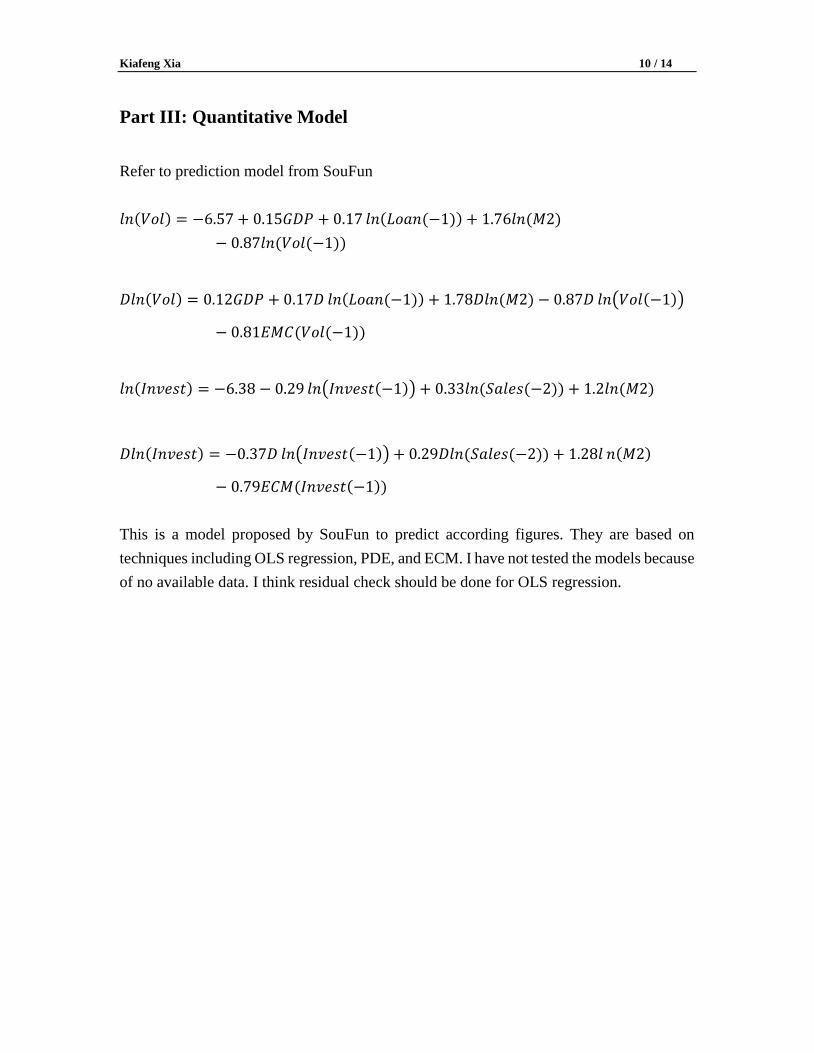

Refer to prediction model from SouFun

𝑙𝑛(𝑉𝑜𝑙) = −6.57 + 0.15𝐺𝐷𝑃 + 0.17 𝑙𝑛(𝐿𝑜𝑎𝑛(−1)) + 1.76𝑙𝑛(𝑀2)

− 0.87𝑙𝑛(𝑉𝑜𝑙(−1))

𝐷𝑙𝑛(𝑉𝑜𝑙) = 0.12𝐺𝐷𝑃 + 0.17𝐷 𝑙𝑛(𝐿𝑜𝑎𝑛(−1)) + 1.78𝐷𝑙𝑛(𝑀2) − 0.87𝐷 𝑙𝑛(𝑉𝑜𝑙(−1))

− 0.81𝐸𝑀𝐶(𝑉𝑜𝑙(−1))

𝑙𝑛(𝐼𝑛𝑣𝑒𝑠𝑡) = −6.38 − 0.29 𝑙𝑛(𝐼𝑛𝑣𝑒𝑠𝑡(−1)) + 0.33𝑙𝑛(𝑆𝑎𝑙𝑒𝑠(−2)) + 1.2𝑙𝑛(𝑀2)

𝐷𝑙𝑛(𝐼𝑛𝑣𝑒𝑠𝑡) = −0.37𝐷 𝑙𝑛(𝐼𝑛𝑣𝑒𝑠𝑡(−1)) + 0.29𝐷𝑙𝑛(𝑆𝑎𝑙𝑒𝑠(−2)) + 1.28𝑙 𝑛(𝑀2)

− 0.79𝐸𝐶𝑀(𝐼𝑛𝑣𝑒𝑠𝑡(−1))

This is a model proposed by SouFun to predict according figures. They are based on

techniques including OLS regression, PDE, and ECM. I have not tested the models because

of no available data. I think residual check should be done for OLS regression.

Kiafeng Xia 11 / 14

Part IV: Some Problems

Problematic Data Source

1) The data source may be the most problematic issue during the research. The data from

National Bureau of Statistics of PRC is terrible. They are too insufficient and in an

unusable form mostly. Therefore, I could not either make my own quantitative

prediction or even test the model from SouFun. It seems that China Index Academy has

a database that provides relatively feasible data, but I do not have access to it. In fact,

the problem of data source has always been a problem when doing China-related

research.

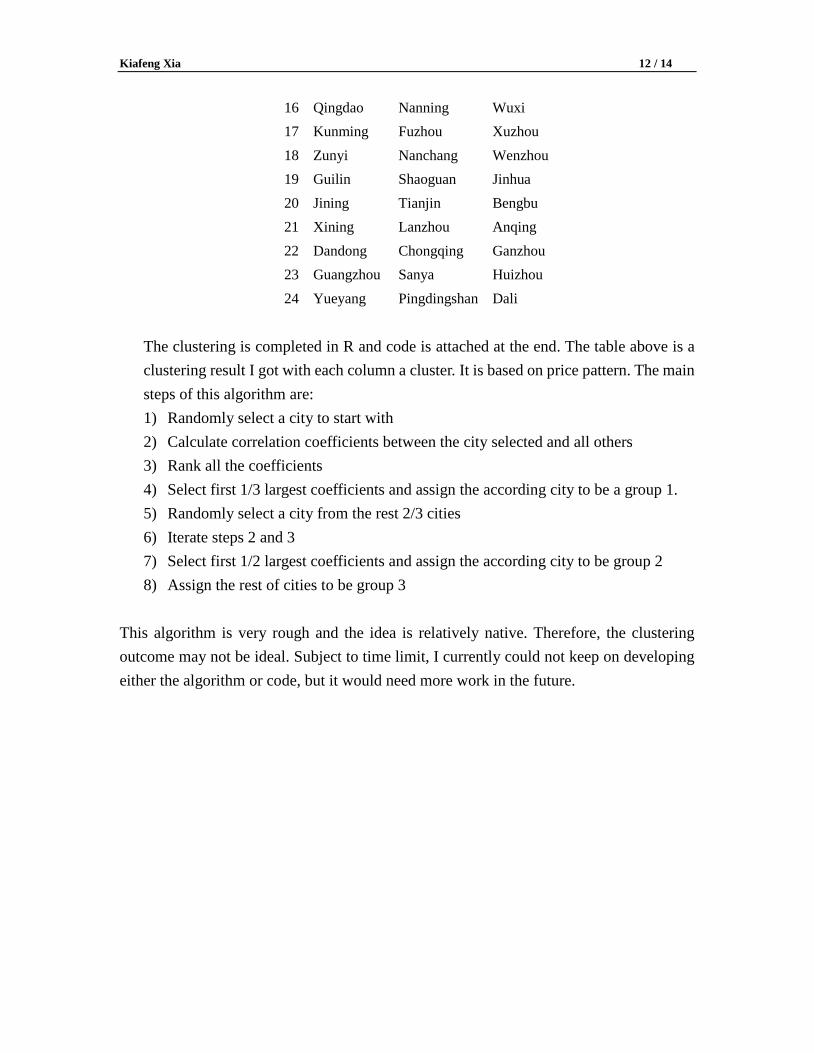

Suggested Classification of Cities

2) I think the current classification of cities based on tiers is not so reasonable. Instead, I

think cities with similar historical price pattern or volume pattern should be classified

as a group. This is a cluster problem, and I proposed an algorithm for this clustering

based on last year’s price index. The data I used was 70 large and medium sized cities

index from NBS.

Cluster 1 Cluster 2 Cluster 3

1 Yueyang Pingdingshan Shijiazhuang

2 Zhanjiang Shenyang Nanjing

3 Xian Quanzhou Hangzhou

4 Dalian Changsha Ningbo

5 Yinchuan Yichang Hefei

6 Huhehaote Baotou Xiamen

7 Yantai Xiangyang Jinan

8 Nanchong Luzhou Zhengzhou

9 Guiyang Chengdu Wuhan

10 Changchun Luoyang Shenzhen

11 Beijing Shanghai Haikou

12 Haerbin Yangzhou Tangshan

13 Wulumuqi Jiujiang Qinhangdao

14 Beihai Taiyuan Jinzhou

15 Mudanjiang Changde Jilin

Kiafeng Xia 12 / 14

16 Qingdao Nanning Wuxi

17 Kunming Fuzhou Xuzhou

18 Zunyi Nanchang Wenzhou

19 Guilin Shaoguan Jinhua

20 Jining Tianjin Bengbu

21 Xining Lanzhou Anqing

22 Dandong Chongqing Ganzhou

23 Guangzhou Sanya Huizhou

24 Yueyang Pingdingshan Dali

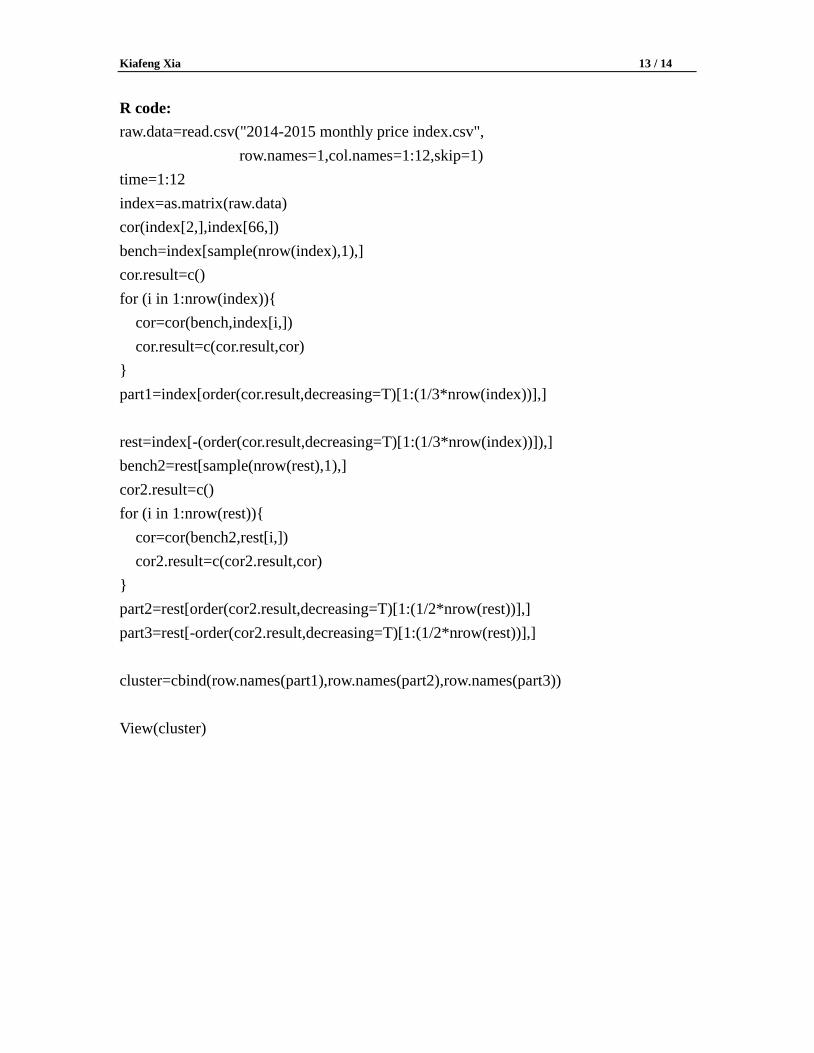

The clustering is completed in R and code is attached at the end. The table above is a

clustering result I got with each column a cluster. It is based on price pattern. The main

steps of this algorithm are:

1) Randomly select a city to start with

2) Calculate correlation coefficients between the city selected and all others

3) Rank all the coefficients

4) Select first 1/3 largest coefficients and assign the according city to be a group 1.

5) Randomly select a city from the rest 2/3 cities

6) Iterate steps 2 and 3

7) Select first 1/2 largest coefficients and assign the according city to be group 2

8) Assign the rest of cities to be group 3

This algorithm is very rough and the idea is relatively native. Therefore, the clustering

outcome may not be ideal. Subject to time limit, I currently could not keep on developing

either the algorithm or code, but it would need more work in the future.

Kiafeng Xia 13 / 14

R code:

raw.data=read.csv("2014-2015 monthly price index.csv",

row.names=1,col.names=1:12,skip=1)

time=1:12

index=as.matrix(raw.data)

cor(index[2,],index[66,])

bench=index[sample(nrow(index),1),]

cor.result=c()

for (i in 1:nrow(index)){

cor=cor(bench,index[i,])

cor.result=c(cor.result,cor)

}

part1=index[order(cor.result,decreasing=T)[1:(1/3*nrow(index))],]

rest=index[-(order(cor.result,decreasing=T)[1:(1/3*nrow(index))]),]

bench2=rest[sample(nrow(rest),1),]

cor2.result=c()

for (i in 1:nrow(rest)){

cor=cor(bench2,rest[i,])

cor2.result=c(cor2.result,cor)

}

part2=rest[order(cor2.result,decreasing=T)[1:(1/2*nrow(rest))],]

part3=rest[-order(cor2.result,decreasing=T)[1:(1/2*nrow(rest))],]

cluster=cbind(row.names(part1),row.names(part2),row.names(part3))

View(cluster)